Embed Size (px)

Citation preview

The Biggest FX Problem (That No One Talks About)Multi-Currency Accounting, FX & ERPs

This ebook will reveal the most common types of accounting errors, breakdowns in accounting controls, system configuration issues and process deficiencies that lead to unnecessary FX gain/loss.

Background & Purpose 3

The Data Dilemma: Getting to the Source of FX Accounting Volatility 4

The Challenge of Defining Exposures 5

Recording the Transaction 6

Revaluation under FAS 52 & IAS 21 Framework 8

Recording and Remeasuring Multicurrency Accounting Data 9

Diagnosing Accounting Volatility: Symptoms, Questions

& the Self-Assessment10

Key Questions to Ask 11

Assessing Your Organization’s Foreign Currency Exposure Management

Situation12

Foreign Currency Exposure Management: An Enterprise Issue 13

The FX Exposure Management Process Owner: Starting Where the Buck Stops 14

About the Author 15

TABLE OF CONTENTS

We hear time and time again that Treasurers and Controllers alike “don’t know what they don’t know” about their foreign currency exposure data.

All too often, the first symptom of a problem shows up as a material misstatement of FX gain/loss with serious consequences. Usually, this is a result of what FiREapps has coined as: “accounting volatility.”

We use this term to describe the phenomenon of systemic, recurring inaccuracies that exist in most multi-currency accounting systems, that obscure the true magnitude of a company’s foreign currency exposure in ways that make the problem difficult to detect.

In many cases, accounting volatility is reflected in the delta between hedging actions and actual FX gain/loss resulting from the underlying exposure.

Accounting Volatility

Page 11 | Four quick questions to diagnose accounting volatility

�2�2

In this ebook, FiREapps will highlight a critical issue facing Treasury departments and cover shortcomings in the way companies today account for multi-currency transactions and manage the resulting foreign currency exposures.

Time and again, our analysis of foreign currency exposure management processes within hundreds of companies uncovers a ticking time bomb that could (and eventually does) have material impact on a company’s financial performance and its ability to accurately reflect FX gain/loss within their financial statements in accordance with GAAP/IAS. Frequently, this time bomb is an undetected exposure hidden within the ERP or accounting system that is masked by a variety of data integrity issues. Without adequate visibility into the source data they receive from the Controller’s organization, Treasury can do little more than cope with/or try to manage around the problem. As a result, their decisions, even when based on sound strategies, are ineffective and even potentially counter-productive.

All too often, this time bomb is detected once it’s too late. The problem ultimately surfaces in the FX gain/loss line of the income statement and the CFO is faced with foreign currency exposures that have serious economic and compliance consequences.

Getting to the heart of the matter and preventing a disaster begins with a close examination of the accounting systems,

controls and related processes that undermine the accuracy and completeness of their foreign currency exposure data. The first section of this white paper will deal specifically with the issue of accounting volatility— a result of pervasive, self-reinforcing inaccuracies that exist in most accounting systems with regard to foreign currency— that obscures the true magnitude of a company’s exposure in ways that make the problem difficult to detect.

An examination of the people and processes that contribute to foreign currency exposure identification often reveals uncoordinated activities and the lack of a true process owner who has the oversight and authority to adequately manage and drive actions throughout the entire process. In the second part of this ebook, we’ll discuss why foreign currency exposure management goes beyond Treasury or the Controller’s organization and is ultimately an enterprise issue. Companies that approach foreign currency exposure management from an enterprise perspective, assigning the proper ownership, authority and resources to the process, can focus their attention and energies on strategic, value-based decision making that will protect and enhance the value of the firm. The third part of this ebook will discuss how companies can begin to transform their foreign currency management practices into enterprise-level, institutionalized processes.

Accounting Volatility: Systemic, recurring inaccuracies that exist in most multi-currency accounting systems, that obscure the true magnitude of a company’s foreign currency exposure in ways that make the problem difficult to detect. In many cases, accounting volatility is reflected in the delta between hedging actions and actual FX gain/loss resulting from the underlying exposure.

BACKGROUND & PURPOSE

�3

In every case we have witnessed, the question isn’t if companies are misstating FX gains/losses, but whether the impact is material.

The Data Dilemma: Getting to the Source of FXRelated Accounting Volatility

�4

In most companies, the Treasury organization is accountable for managing foreign currency exposure and the related FX gain/loss. While Treasury often maintains control over the process of selecting hedging instruments and internal risk management tactics, their ability to mitigate the effects of FX volatility depends on accurate and complete exposure data. If the data is inaccurate or incomplete, companies may execute risk mitigating actions within policy but still sustain significant FX gain/loss volatility.

The real problem with foreign currency exposure data integrity issues is that they are extremely difficult to detect until a major problem has surfaced.

In our experience, we frequently find off-setting errors and omissions that distort foreign currency data, falsely masking the true exposure in ways that make it difficult to isolate an anomaly and determine the source of an error. We’ve come to refer to this phenomenon as accounting volatility, a pervasive, self-reinforcing sequence of data integrity issues that become increasingly complex and intractable over time.

Treasury is a customer of the accounting organization when it comes to foreign currency exposure data. Assuming that a multi-currency accounting system is in place for the enterprise, valid foreign currency exposure data is dependent upon two key premises:

1. Multi-currency transactions have been properly recorded in the transaction currency.

2. Accounts that are required to be revalued in accordance with FAS 52 / IAS 21 are being revalued on a periodic basis.

Accounting volatility can result if multi-currency accounting entries have not been recorded appropriately, or if the revaluation process is not properly identifying accounts that should be revalued. The result in either case is a misstatement of the foreign currency gain/loss in the income statement for the enterprise. Either foreign currency gain/loss remains embedded within the monetary asset and liability accounts in the balance sheet, or it has been improperly recognized prematurely in the income statement.

In the following section of this ebook, we will discuss these issues and provide questions that CFOs and Treasurers can ask of their Controller to determine the future likelihood, and historical magnitude, of accounting volatility within their organization.

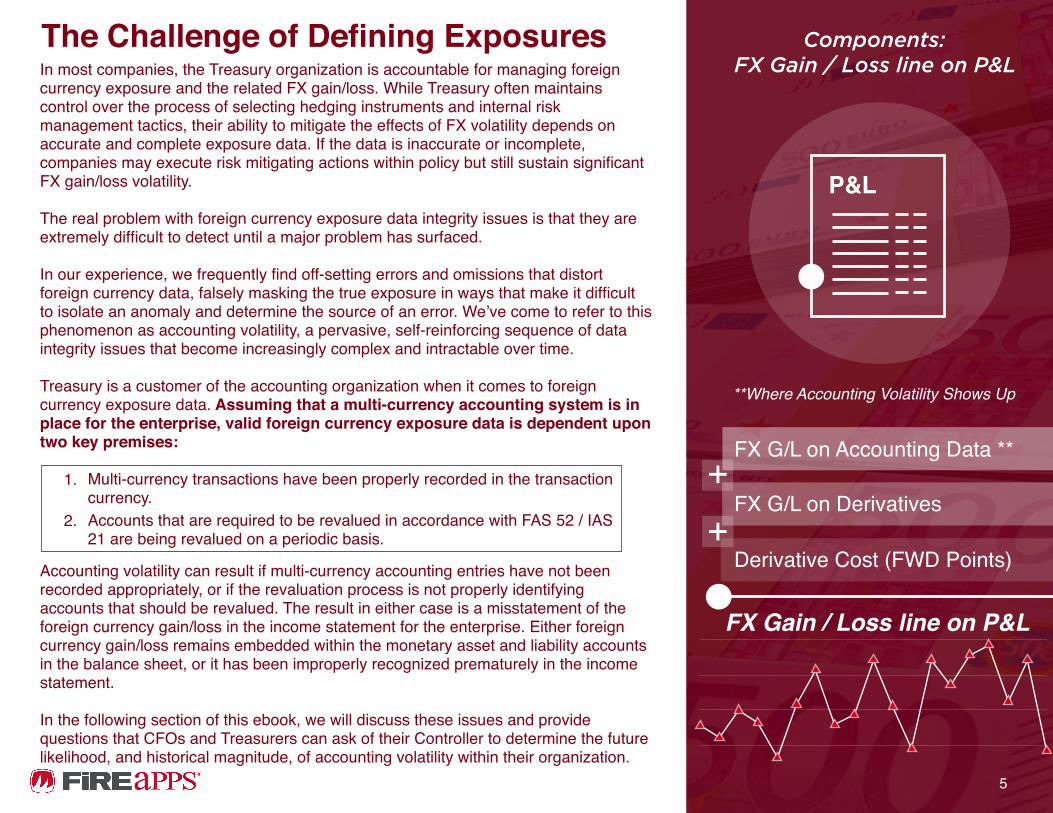

The Challenge of Defining Exposures

�5

P&L

Components: FX Gain / Loss line on P&L

FX G/L on Accounting Data **

FX G/L on Derivatives

Derivative Cost (FWD Points)

FX Gain / Loss line on P&L

**Where Accounting Volatility Shows Up

++

�5

U

One difficult to detect issue that has serious impact on foreign currency exposure management is the entry of the foreign currency transaction in the functional currency instead of the transaction currency. As a result, the exposure is not detectable and cannot be managed by Treasury. In addition, the foreign currency gain/loss associated with this transaction exposure is not realized incrementally with the process of account revaluation. Rather, it is

realized all at once, when the transaction is cleared or settled.Another prevalent issue is the clearing and reconciliation of multi-currency account balances in functional currency instead of transaction currency. This results in invalid transaction currency balances and mismatched relationships between the transaction currency and functional currency within the accounting system. Because revaluation processes are based upon transaction currency balances, invalid transaction currency balances can lead to invalid unrealized

FX gain/loss calculations and posted results when revaluation occurs during period-end processing. These accounting issues are evidence of a process breakdown usually attributed to employee training in the area of transaction entry. Detecting these issues requires a disciplined analytic review of the monthly foreign currency FX gain/loss for entities within the enterprise, given the foreign currency exposure relationships within the entities and changes in foreign currency rates during the month.

1. Under certain conditions, the revaluation processes may be run multiple times with uncoordinated results, effectively reapplying FX adjustments.

2. Revaluation criteria are usually managed through the use of variants (i.e. predefined parameter definitions) that are static, requiring constant manual updates to reflect current accounts and entity relationships; these updates are often overlooked

3. In situations where the Controller organization is decentralized, account setup and changes in entity relationships contribute to uncoordinated revaluation criteria and the potential to either:1. Revalue some accounts2. Revalue accounts multiple times3. Revalue accounts that should not be revalued

SAPORACLE

Specific FX-related configuration, administration and maintenance issues in most major ERP systems add to the complexity and potential for problems with multi-currency accounting.

Recording the Transaction

1. Oracle does not define a functional currency at the company level. It is defined for a set of books.

2. The ability to support multiple functional currencies for a company is often overlooked or misconfigured.

3. Revaluation rules apply only in the context of a company in a set of books. If a company transacts in multiple sets of books, multiple rules may be required for the same accounts and/or currencies – this is often overlooked or misunderstood.

4. Revaluation processing looks at functional currency of the set of books, not the company. A non-functional transaction in a set of books with the same currency will be ignored for revaluation.

�6

Intercompany MismatchesIntercompany transactions have a significant impact on the nature, level, and complexity of a company’s foreign currency exposure. Generally, intercompany transactions are recorded in one of the functional currencies of the entities that comprise the intercompany relationship. As a rule, the intercompany account balances recorded in the two entities that comprise an intercompany relationship should net to zero on a currency-by-currency basis.

Despite this, one common source of accounting volatility is mismatched intercompany balances, where one entity has recorded an intercompany payable or receivable, while the other has either neglected to record the corresponding transaction, or has recorded it inaccurately. This too is a symptom of a multi-faceted process breakdown, one in the recording of the transaction and another associated with the reconciliation process.

Intercompany transactions that take place in a currency other than the functional currency of either entity in the intercompany relationship create additional exposure for the enterprise and further complicate the FX exposure management process. As described in the table at the bottom, when a third currency enters this relationship, each entity has an exposure to the transaction. There are two ways to resolve this issue and eliminate the exposure. One way is to execute two currency conversions: one entity purchases the currency, and the other entity sells the currency. Alternately, a process must be developed to convert the third currency balance into one of the entity's functional currencies based upon a pre-determined rate convention, followed by a single currency conversion to settle the balance.

In many cases, creating an intercompany transaction in a third currency is not an acceptable business practice. Unfortunately, due to the complexity around intercompany balances, lack of visibility in transaction currency across multiple systems, multi-department responsibilities, and inadequate tools and reporting infrastructure, this departure from acceptable business practice often goes undetected.

Intercompany Transaction in Functional Currency:Multinational Company Acc#100 (USD)

Foreign Subsidiary Acc# 200 (Euro)

Accounts Payable Accounts Receivable

Account 100 I/C 12000 USD ($1M) Payable to Acc#200

Account 200 I/C 12000 USD $1M Received from Acc#100

[Exposure: none] [Exposure: $1M USD]

Intercompany Transaction in A Third Currency:Multinational Company Acc#100 (USD)

Foreign Subsidiary Acc# 200 (Euro)

Accounts Payable Accounts Receivable

Acc 100 I/C 12000 (100M JPY) (Japanese Yen) to Acc 200

Acc 200 I/C 12000 100M JPY Japanese Yen from Acc 100

[Exposure: (100M JPY)] [Exposure: 100M JPY]

�7

As detailed previously, accounting and process issues related to transaction data quality may not be the only source of accounting volatility. In many cases, problems related to monetary asset and liability account revaluation in accordance with FAS 52 / IAS 21 guidelines contribute to unreliable FX gain/loss statements.

In our work with clients in setting up end-to-end processes for identifying foreign currency exposure, we routinely uncover, and help customers to resolve, issues related to revaluation validity that hamper their ability to properly reflect the impact of currency revaluation on their financial statements. We commonly encounter inaccurate results from improper revaluation of accounts across the enterprise. We typically find a combination of accounts that are being revalued properly, accounts that should be revalued but are not, and finally, accounts that are being revalued, but shouldn’t be. In most cases, companies are unaware of the problem.

In either scenario, the underlying root causes of these inconsistencies can be grounded in the following factors:

1. Treasury has no visibility to this account in their exposure management process

- Thus, they cannot mitigate risk with regard to the underlying currency exposure

2. There is no unrealized FX gain/loss being recorded on a monthly basis- The total FX gain/loss that exists within the account is sitting in the balance sheet, waiting

to be realized all at once when transaction(s) making up the account balances are cleared

and/or adjusted

System Configuration & Administration Issues: Revaluation Under FAS 52 / IAS 21 Framework

1. Treasury takes risk mitigating actions for these inaccurate balances (in the accounts) as part

of the exposure management process- An associated FX gain/loss in addition to

currency conversions, hedge valuations/settlements and the inherent cost (bank fees, forward points, and/or option premiums) associated with currency hedge transactions are recorded for the account

2. The effects of the risk mitigating currency actions have been realized with

no off-setting amounts that would have resulted from an underlying exposure

-The company will eventually discover that the account should not have been revalued and records the adjustment to reverse the recorded unrealized FX gain/loss

Scenario #1An account that should be revalued is not being revalued

Scenario #2Accounts that should not be remeasured are identified for remeasurement

**See next page for variables affecting both factors

Accounts for RevaluationX✓✓

XX

✓X

Accounts not for Revaluation✓✓✓

✓✓

✓✓

�8

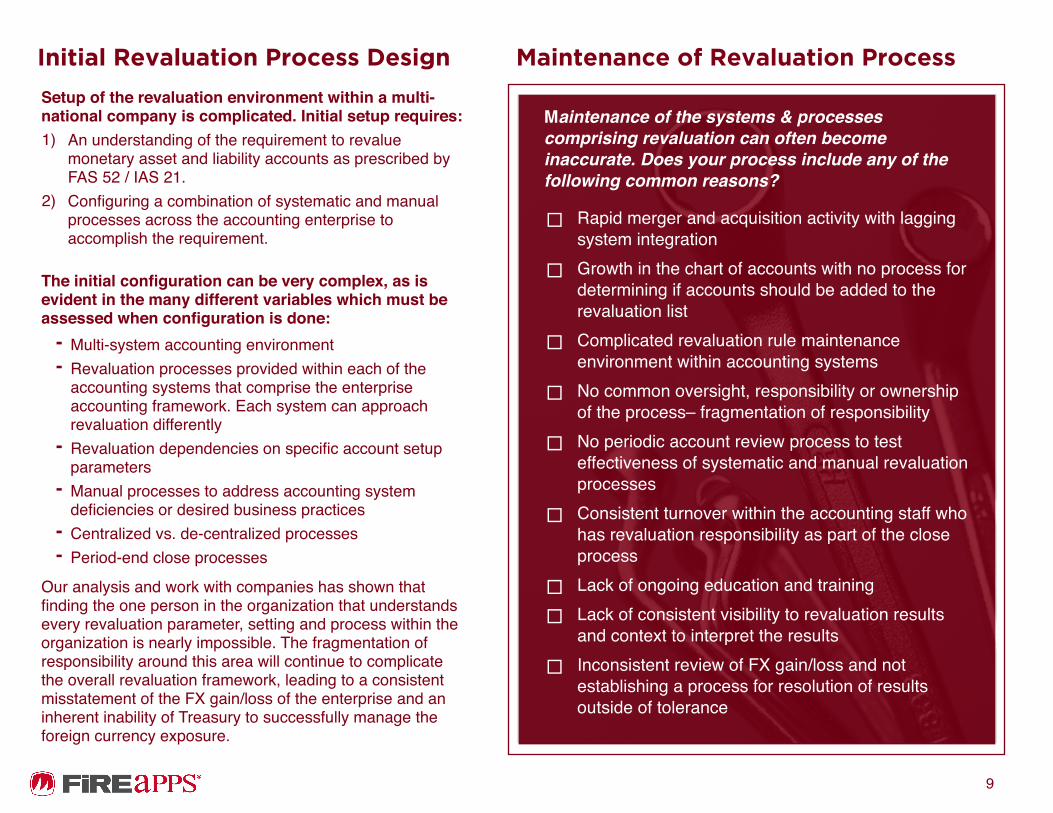

1. Initial setup of the revaluation environment within a multi-national company is complicated.

2. Maintenance of the systems and processes comprising revaluation become inaccurate over time.

**You may encounter compliance issues as a result of this scenario

Setup of the revaluation environment within a multi-national company is complicated. Initial setup requires: 1) An understanding of the requirement to revalue

monetary asset and liability accounts as prescribed by FAS 52 / IAS 21.

2) Configuring a combination of systematic and manual processes across the accounting enterprise to accomplish the requirement.

The initial configuration can be very complex, as is evident in the many different variables which must be assessed when configuration is done:

- Multi-system accounting environment- Revaluation processes provided within each of the

accounting systems that comprise the enterprise accounting framework. Each system can approach revaluation differently

- Revaluation dependencies on specific account setup parameters

- Manual processes to address accounting system deficiencies or desired business practices

- Centralized vs. de-centralized processes- Period-end close processes

Our analysis and work with companies has shown that finding the one person in the organization that understands every revaluation parameter, setting and process within the organization is nearly impossible. The fragmentation of responsibility around this area will continue to complicate the overall revaluation framework, leading to a consistent misstatement of the FX gain/loss of the enterprise and an inherent inability of Treasury to successfully manage the foreign currency exposure.

Maintenance of the systems & processes comprising revaluation can often become inaccurate. Does your process include any of the following common reasons?

□ Rapid merger and acquisition activity with lagging system integration

□ Growth in the chart of accounts with no process for determining if accounts should be added to the revaluation list

□ Complicated revaluation rule maintenance environment within accounting systems

□ No common oversight, responsibility or ownership of the process– fragmentation of responsibility

□ No periodic account review process to test effectiveness of systematic and manual revaluation processes

□ Consistent turnover within the accounting staff who has revaluation responsibility as part of the close process

□ Lack of ongoing education and training

□ Lack of consistent visibility to revaluation results and context to interpret the results

□ Inconsistent review of FX gain/loss and not establishing a process for resolution of results outside of tolerance

Initial Revaluation Process Design Maintenance of Revaluation Process

�9

Diagnosing Accounting Volatility: Symptoms, Questions & the Self-Assessment

�11

So far, we have discussed common foreign currency exposure data integrity issues, the role of ERP and accounting systems administered by IT and/or the Controller’s organization, and accounting and organizational issues that contribute to the problem of accounting volatility. Next, we’ll consider the symptoms of these problems in the form of key questions that CFOs or Treasurers can pose to their Controller to indicate the degree of accounting volatility that exists within their organization.

How confident is your Controller that multi-currency transactions are being recorded properly, including initial entry and clearing of the transactions?If multi-currency transactions are not being recorded or cleared properly, they can create unexpected fx gain/loss volatility. As discussed previously, if a regional accounting manager records a multi-currency invoice in the local currency of the entity instead of the transaction currency, the Treasurer will have no visibility to the exposure. When the payment is cleared, the gain/loss on the transaction will unexpectedly impact the income statement.

When was the last time the Controller reviewed enterprise-wide revaluation to determine if the system(s) configuration and related processes produced a result that complied with FAS 52 / IAS 21?In the vast majority of companies we have worked with, we have uncovered multiple ERP/accounting system setup/configuration problems and process issues which not only raise compliance concerns, but also create embedded FX gain/loss volatility that is very difficult to detect and manage.

How confident is accounting that intercompany transactions are being reconciled on a timely basis and are in balance?We commonly witness intercompany transactions that demonstrate the significant balance discrepancies discussed previously. Intercompany issues we often encounter that can cloud foreign currency exposures include:- Intercompany transactions where only one side of the transaction is recorded in the G/L - Intercompany transactions that do not have matching balances- Intercompany transactions that are not posted in the same transaction currency- Intercompany transactions that are recorded in a third currency (functional currency of entity)

Does the Controller perform foreign currency gain/loss analysis on a regular, monthly basis and maintain a proactive process for the resolution of exceptions?If yes, how often do they encounter unexpected results, and what is the process for investigation and resolution? If no, how do they verify that the gain/loss on currency exposures is as expected and within the corporate tolerance?

1

2

3

4

Upon addressing these key questions, you should be able to assess your company’s ability to quantify and manage foreign currency exposures.

Using the FX Exposure Management Capability Model on the next page, you can determine your company’s current capabilities and define concrete goals to improve your ability to quantify and manage foreign currency exposure.

Assessing Your Organization’s Foreign Currency Exposure Management Situation

Take the Self-Assessment On the Next Page

Outcomes Consistent, material, unexplained FX gain/loss

Occasional, material unexplained FX gain/loss

Periodic, immaterial unexplained FX gain/loss

Explainable FX gain/loss within risk tolerance

Controlled FX gain/loss

Each row of checkboxes below corresponds to the category on its left. For each row, select one checkbox that is most applicable.. When completed, look at each column individually. The one with the most items checked will be an indicator of your company’s ability to manage foreign currency exposure. Take special note of the items checked towards the left of the page— these are key opportunities for improvement.

Multicurrency Accounting (MCA)

Systems & Revaluation

Processes

▢ Incorrect MCA configuration or no MCA functionality ▢ Incorrect MCA configuration ▢ Some issues with MCA

configuration ▢ Minimal issues with MCA configuration ▢ Properly configured and

maintained MCA system

▢Incorrect revaluation configurations and lack of effective controls

▢Incorrect revaluation configurations and lack of effective controls

▢ Periodic issues with revaluation and configuration process ▢

Minimal issues with revaluation and configuration process

▢ Proper revaluation controls and testing processes

Multicurrency Accounting

Transaction & Processes

Controls

▢Intercompany transactions (I/C) not in balance and not reconciled

▢Intercompany transactions (I/C) not in balance and not reconciled

▢ I/C transactions are in balance and reconciled ▢ I/C transactions are in

balance and reconciled ▢I/C transaction balance and effective process in place for settlement

▢Lack of MC translation controls contributing to embedded FX G/L

▢Lack of MC transaction controls contributing to embedded FX G/L

▢ Lack of MC transaction controls contributing to embed FX G/L ▢ Basic controls for MC

transactions in place ▢Proper controls in place for MC transactions, period testing of controls

Exposure Definition and

Analytics

▢ Manual, spreadsheet based ▢ Manual, spreadsheet based ▢ Manual spreadsheet based ▢ Automated exposure data gathering and analytics ▢ Automated exposure data

gathering and analytics

▢ No FX gain/loss analytics and exception management ▢

Limited FX gain/loss analytics, no exception management ▢ Performs FX gain/loss analysis,

no exception management ▢Performs FX gain/loss analysis, no exception management

▢Monthly FX gain/loss analysis with effective exception management

▢ Unable to effectively quantify FX exposures ▢ Limited ability to effectively

quantify FX exposures ▢ Limited ability to effectively quantify FX exposures ▢ Automated exposure

calculation ▢ Automated expsoure calculation

▢ Lack of visibility into exposure root causes ▢ Limited visibility into exposure

root causes ▢ Limited visibility into exposure root causes ▢ In-depth visibility and

understanding of exposures ▢ In-depth visibility and understanding of exposures

Exposure Management

Decision Making

▢ Decentralized and uncoordinated ▢ Decentralized and

uncoordinated ▢ Decentralized and uncoordinated ▢ Centralized decision making

and transaction execution ▢ Centralized decision making and transaction execution

▢ Process latency resulting in increased market risk ▢ Process latency resulting in

increased market risk ▢ Process latency resulting in increased market risk ▢ Minimal process latency ▢ Minimal process latency

▢Frequent hedging mistakes resulting in under-hedged/ over-hedged exposures

▢Periodic hedging mistakes resulting in under-hedged/ over-hedged exposures

▢Occasional hedging mistakes resulting in under-hedged/ over-hedged exposures

▢Efficient and cost-effective use of derivatives for hedging

▢ Efficient and cost-effective use of derivatives for hedging

▢ Reactive decision making ▢ Reactive decision making ▢ Reactive decision making ▢ Proactive decision making ▢ Proactive decision making

FX Rate Conversions

▢ No strategy for recording FX transactions ▢ No strategy for recording FX

transactions ▢ Increasing awareness of impact of FX rate conventions ▢ Strategy in place for FX rate

conventions ▢ Established rate conventions for recording transactions

Risk Management Framework and

Policy

▢ No formal policy definition, Treasury working in isolation ▢

Basic FX risk management policy ▢ Comprehensive FX risk

management policy ▢ Comprehensive FX risk management policy ▢ Enterprise risk management

policy and risk tolerances

▢ No process benchmarks or metrics ▢ No process benchmarks or

metrics ▢ No process benchmarks or metrics ▢ Minimal benchmarks or

metrics ▢ Established benchmarks and metrics

▢ No formal role coordination with other departments ▢ Limited coordination with

other departments ▢ Limited coordination with other departments ▢ Cross-functional

coordination & collaboration ▢ Cross-functional coordination and collaboration

Which best describes the outcome of your current currency program?

1 2 3 4 5

Using the FX Exposure Management Capability Model below, you can determine your company’s current capabilities and define a concrete checklist of goals to improve your ability to quantify and manage foreign currency exposure.?

�12

Foreign Currency Exposure Management: An Enterprise Issue

In almost every conversation we conduct with CFOs, Controllers and Treasurers, a common theme emerges: an overall lack of cross-functional coordination and collaboration within their company with regard to activities that impact FX exposure quantification and measurement. While Treasury may be regarded as the process owner, in reality, they maintain control of, and have authority over, only one piece of the puzzle. Different functional groups within an organization contribute to foreign currency exposures and their management process. The FX gain/loss line on the corporate income statement is the ultimate product of these efforts. Responsibility and accountability for that number resides with the Chief Financial Officer. As such, it is the CFO who assumes responsibility and accountability for the process, and must ensure coordination among the contributing functional groups to ensure that this result is both accurate and acceptable within company policies. The only way to ensure the kind of cross-functional coordination required to properly manage the foreign currency exposure management process is to elevate awareness and priority of the issue throughout the enterprise.

Acknowledging foreign currency exposure as an enterprise risk means assigning the proper level of oversight, accountability and resources to the entire management process. At a strategic level, the FX business process owner must have the strategic responsibility for addressing and maintaining currency risk management decisions, processes and policies. The FX business process owner must be able to coordinate tactical activities across multiple disciplines, and communicate effectively with finance, accounting, tax and operations representatives from around the globe. Ultimately, they’re the stakeholder with visibility into the foreign currency exposures and management process, from data to exposure, across the enterprise.

The FX Exposure Management Process Owner: Starting Where the Buck Stops

Additional Resources

Savvy corporates are adopting a roundtable approach to currency risk management. Currency has become an issue outside the halls of treasury. Modern currency aware organizations understand that currency impacts many areas of the company, and all of those areas are represented at the company’s currency roundtable. Everyone at the currency roundtable has access to accurate, complete, and timely exposure data, as well as the analytics to understand how those exposures impact their functional area – and, conversely, how decisions they make affect currency exposures and the company’s overall financial performance.

For more detail on the currency roundtable approach, check out the following blog post:

Currency Impacts Every Function of the Organization – So Who’s at Your Currency Roundtable?

Blog

Currency surprises impact in obvious (and not-so-obvious) ways. When a company’s revenue is regularly eroded by currency surprises, it has less cash available for productive activity. That loss has ripple effects, including credit rating downgrades that raise the firm’s cost of capital and debt covenant breaches that limit its access to liquidity. Both reduce available cash and limit the firm’s ability to deliver maximum profit to shareholders.

For more detail on the deeper-seated impacts of currency surprises, check out the following AFP Exchange article:

Below the Surface: FX impacts on revenue are just the tip of the iceberg

Blog

Recommended Next Steps CFOs, Treasurers and Controllers can turn to FiREapps to provide an unparalleled ability to access accurate and complete exposure data, on demand. Our platform is backed by a team of experts who continually support the currency risk management processes at some of the largest companies in the world. Put simply, companies who have identified FX related accounting or exposure management issues can rely on FiREapps to provide a solution to remediate any sources of accounting volatility and inaccuracy. In many cases, companies choose to leverage FiREapps industry leading software platform to measure, monitor and manage their currency risk management programs on an ongoing basis.

To learn more, contact FiREapps by phone at +1 866-928-FIRE (3473) or via e-mail at [email protected].

About FiREapps FiREapps helps treasury and finance professionals understand and manage currency impact to financial results. Companies ranging from Accenture to Yahoo use FiREapps analytics to monitor & manage the impact of currency on their business. Established in 2005 as a division of Rim-Tec (Risk Management Technologies), FiREapps developed the first solution to automate foreign exchange exposure management for multinational companies, delivering unparalleled expertise and driving measurable results.

To this day, FiREapps is focused on helping companies quantify their foreign exchange exposure and cost-effectively insulate their organization from the uncertainty of currency volatility. Whether we’re working with a Fortune 50 organization or a growing U.S. company poised to go global, we take the same approach to understanding our customer’s foreign exchange policies, processes and objectives. By providing an assessment of the effectiveness of a customer’s current practices, we can then prescribe specific solutions to meet their goals. In most cases, our recommendations are supported by FiREapps currency risk management platform. A cloud based software suite that customers can deploy to cost-effectively manage their own foreign exchange exposure management processes. FiREapps relies on these same technologies to streamline our FX exposure management design, implementation and support services.

About the Author Corey Edens co-founded Rim-Tec, Inc. in 2000, (FiREapps is a division of Rim-Tec) acting as the company’s Chief Financial/Solution Officer. Prior to Rim-Tec’s inception, he was the President of Valcon Distributing Ltd., Inc. Before Valcon, Edens served as the Controller and Director of Operations for the Microsoft Network. He has also worked as Controller and CFO in the real estate and computer industries and has several years of auditing experience at Deloitte Haskins and Sells. Edens is a Certified Public Accountant and holds a B.S. degree with high honors in accounting from the University of Montana.

Wolfgang Koester is the CEO and co-founder of FiREapps. He has over 30 years of extensive experience in developing and implementing currency risk management programs for Fortune 2000 companies and governments. Prior to forming FiREapps, he served as President of GFTA Trendanalysen Inc., a quantitative currency management company. He has been named as one of the “100 Most Influential People in Finance” by Treasury & Risk and is a member of Global Finance’s “Who’s Who in Foreign Exchange.” Koester holds a Bachelor of Science degree from Arizona State University and a Master’s degree in International Management from The Garvin School of International Management. He is a board member of ACI International and The Financial Markets Association.