Embed Size (px)

Citation preview

The Big Picture

Source Multi-Asset Portfolio 2015

This first edition of The Big Picture distils our views about a wide range of

assets into the Source Multi-Asset Portfolio (SMAP). The US economy is

strong enough to keep the Fed on a tightening path but the global bias is

towards easing. Sovereign bonds are caught in the middle: equities, real

estate, high yield and emerging market debt provide better alternatives.

Non-US assets must fight against the strengthening dollar.

Key conclusions

• Equities, real estate and high yield corporate debt offer the best risk-adjusted

returns over one and five year horizons (see Figure 1). Overweight.

• Cash, government bonds and investment grade corporate debt promise

low/negative returns. Underweight (favour short duration).

• EM debt is the one exception. Overweight.

• Commodities have no role for now. Zero weight.

• US assets are helped by the expected appreciation of the dollar, with

Overweight positions in US equities, high yield debt and real estate.

Must-have assets

• Chinese equities – expected 15-20% annualised return over five years.

• Japanese equities – expected double digit returns over five years (in USD).

• European real estate (currency hedged) – double digit returns in 2015.

• US high yield –- the best of a bad fixed income bunch (5%-10% ann. returns).

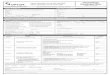

Figure 1 – Projected 5-year returns for global assets and neutral portfolio

Returns are annualised in USD. Risk adjusted returns are projected returns divided by historical 5yr

standard deviations. See appendices for methodology.

Source: Source Research

Date

4 December 2014

Paul Jackson

Head of Research

London

András Vig

Research Associate

London

Source U.S.

For further information on

Source in the U.S. please

contact:

1-844-3SOURCE

1-844-376-8723

www.sourceETF.com

Data as of 25/11/14

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-1%

0%

1%

2%

3%

4%

5%

6%

7%Returns Risk-Adjusted (RHS)

December 2014 Straight from the Source 2

Multi-asset research

The Big Picture

Table of Contents

Summary and conclusions 3

Source Multi-Asset Portfolio 4

Getting it vaguely right 5

Which assets? 5

Better to be vaguely right than exactly wrong 6

What is neutral? 6

Source Multi-Asset Portfolio 8

Economic and policy outlook 8

Valuations 9

Market forecasts 10

Expected returns 10

Optimised allocations 11

Allocations within asset classes 12

Currency hedging 13

Global Asset Classes 14

Cash 14

Government Bonds 15

Corporate Bonds 16

Corporate High Yield Bonds 17

Equities 18

Real Estate 19

Commodities 20

Appendices 21

Consensus economic forecasts 21

Asset class yields versus history 22

Expected returns 23

Methodology 24

Disclaimers 25

December 2014 Straight from the Source 3

Multi-asset research The Big Picture

Summary and conclusions

Six years on from the global financial crisis and “may

you live in interesting times” is starting to sound like a

curse. Unfortunately, the returns we expect over the

next five years are far from interesting (see Figure 2).

Interest rates are close to zero in many developed

countries and bond yields are at or close to record lows.

Finding income remains a challenge and capital losses

are likely when rates start to rise. Unfortunately, the

most important central bank (the US Federal Reserve)

seems primed to start raising rates during 2015, as are

those of Australia, Canada and the UK.

However, the global economy remains fragile, with

growth likely to be less than 3% in 2015. A number of

important countries either have low growth (Eurozone,

Japan and India) or are decelerating toward recession

(Brazil, China and Russia). Hence, there are plenty of

central banks currently easing (BOJ, ECB, and PBOC)

or who are likely to do so (in Brazil, India and Russia).

This will limit the extent to which global bond yields rise

– yields may be low but capital losses will be limited.

The most interesting areas will be high yield corporate

debt (especially in the US) and emerging market

sovereign debt. In all likelihood, the divergence of

central bank policies will continue to support the US

dollar, which makes it difficult to justify holding low-

yielding assets outside the US.

Better returns will be available on equity-like assets

(equities, real estate, high yield and EM debt) and that

is where the Source Multi-Asset Portfolio is focused

(see Figure 2, with full detail overleaf in Figure 3).

Despite the anticipated tightening by the Fed, and

already stretched valuations, we suspect the S&P 500

will continue to advance during 2015, with a year-end

target of 2400 (due to strong profit growth and a touch

of multiple expansion as money continues to flow from

overseas). Returns will flatten out thereafter.

Japanese equities are expected to produce the

strongest returns (Nikkei 225 reaching 21,500 by the

end of 2015), though some of those returns will be lost

in currency translation. Non-UK European equities will

produce double digit returns over the next five years, in

our view, but the support offered by the ECB in the near

term will not match that coming from the BOJ.

Real estate returns are expected to match those of

equities but higher volatility counts against it.

Commodities are expected to continue on a downward

path as the super-cycle deflates and, for the moment,

we cannot justify having them in the portfolio.

As already mentioned, the dollar is likely to continue in

the ascendant and many of our decisions reflect a

preference for US assets. As a result, we are

overweight the US dollar (and EM currencies by the

way), while being underweight the yen and the euro.

Here are the key assumptions underpinning our views

(and therefore the key risks):

• No global recession (helped by weak oil).

• PBOC, ECB and BOJ continue easing.

• Fed eventually tightens, boosting the dollar.

• Major government bond markets do not crash.

• US equity multiples continue to expand.

Figure 2 – Total returns and Source Multi-Asset Portfolio*

Expected Total Returns (USD) Neutral Policy Source Multi- Position

1-year 5-year Portfolio Range Asset Portfolio vs Neutral

Cash -4.3% 1.0% 5% 0-10% 3% Underweight

Government Bonds -4.0% -0.4% 30% 10-50% 18% Underweight

Corporate IG -0.8% 0.4% 10% 0-20% 5% Underweight

Corporate HY 6.2% 3.8% 5% 0-10% 10% Overweight

Equities 14.6% 5.7% 45% 20-70% 60% Overweight

Real Estate 8.6% 6.1% 3% 0-6% 4% Overweight

Commodities -5.8% 0.9% 2% 0-4% 0% Underweight

*This is a simulated portfolio.

Source: Source Research

December 2014 Straight from the Source 4

Multi-asset research The Big Picture

Source Multi-Asset Portfolio*

Figure 3 – Source Multi-Asset Portfolio (04/12/14)

*This is a simulated portfolio.

Source: Source Research

Neutral Policy Range Allocation Position vs Neutral

Cash 5% 0-10% 3% -2

USD 2% 2% 0

EUR 1% 0% -5

GBP 1% 1% 0

JPY 1% 0% -5

Bonds 45% 10-80% 33% -2

Government 30% 10-50% 18% -3

US 10% 10% 0

Europe ex-UK (Eurozone) 8% 4% -3

UK 2% 0% -5

Japan 8% 0% -5

Emerging Markets 2% 4% 5

Corporate IG 10% 0-20% 5% -3

US Dollar 5% 4% -1

Euro 3% 0% -5

Sterling 1% 1% 0

Japanese Yen 1% 0% -5

Corporate HY 5% 0-10% 10% 5

US Dollar 4% 8% 5

Euro 1% 2% 5

Equities 45% 20-70% 60% 3

US 25% 34% 2

Europe ex-UK 7% 9% 1

UK 4% 5% 1

Japan 4% 6% 3

Emerging Markets 5% 6% 1

Real Estate 3% 0-6% 4% 2

US 1% 2% 5

Europe 1% 1% 0

UK 0.5% 0% -3

Japan 0.5% 1% 3

Emerging Markets 0% 0% 0

Commodities 2% 0-4% 0% -5

Energy 1% 0% -5

Industrial Metals 0.3% 0% -2

Precious Metals 0.3% 0% -2

Agriculture 0.3% 0% -2

Total 100% 100%

Currency Exposure

USD 49% 60% 1

EUR 21% 16% -1

GBP 8.5% 7% -1

JPY 14.5% 7% -3

EM 7% 10% 2

Total 100% 100%

December 2014 Straight from the Source 5

Multi-asset research

The Big Picture

Getting it vaguely right

Introduction

The Big Picture is how we will communicate our views

about a broad range of asset classes and geographies.

Macro in orientation, we need to constrain our asset

allocation choices to a limited number of key decisions

(“it is better to be vaguely right than exactly wrong”).

This is the subject matter of this introductory document

– setting the asset allocation framework.

Having decided which asset categories are investible

and worthy of inclusion in a multi-asset portfolio, we

need to consider which decisions really matter. For

instance, the size of government bond markets and

their low correlation with other asset groups makes the

allocation to this asset category one of the most

important decisions (see Figure 4). On the other hand,

equities, high yield corporate debt and real estate are

highly correlated and can in some ways be grouped into

one unit. As a final example, emerging market equities

are highly correlated with other equity markets, whereas

emerging market sovereign debt has not historically

been highly correlated with developed world sovereign

markets (in fact it was more highly correlated to

developed equity markets).

Figure 4 – Average cross-asset correlations*

*Based on data since 2001, as shown in Figure 5

Source: Datastream and Source Research

This framework allows us to structure a model portfolio

and to develop some notion of a neutral stance (though

every investor will have their own benchmark). We then

develop our view of potential future returns, based on

valuations and fundamentals, and use them to develop

a risk adjusted set of preferences. Many of the factors

we consider are long term in orientation (up to five

years) but we construct our model portfolio with a 12

month view (hopefully long enough to avoid chasing

recent trends and short enough to be relevant).

The bottom line is our set of preferences:

Overweight: Equities, HY & EM debt, real estate

Underweight: Cash, sovereigns, IG debt, commodities

Favoured currency: US dollar

Which assets do we consider?

The main considerations when selecting potential

assets for the Source Model Portfolio are:

• Investibility – the asset class has to be easily

accessible to a wide range of investors (either

directly or via funds).

• Size – it has to be large enough to be of interest to

large, as well as small, investors.

• Liquidity – there has to be enough to ensure that

asset allocation switches can easily be executed.

With the above in mind, we have chosen to include the

following assets:

• Equities – fits all of the above criteria and a staple

part of most investor portfolios.

• Bonds – same as for equities. Categories include

government debt, investment grade and high yield

corporate debt and emerging market debt.

• Real Estate – most real estate is not accessible to

the average investor but REITs are a suitable

vehicle. It is reasonable to ask whether REITs

behave more like real estate or equity markets but

we believe that over the long term they reflect the

returns on their underlying real estate investments

(see Are REITs Real Estate? for a review of the

relevant literature and some interesting statistical

evidence from the Swiss Finance Institute in support

of this supposition).

• Commodities – a difficult asset class to access

directly but fund alternatives exist. Not obviously a

staple part of any portfolio but can play a role from

time to time.

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

December 2014 Straight from the Source 6

Multi-asset research The Big Picture

• Cash – apart from the need to fund day to day

activity (transaction motive), cash is also needed for

precautionary (safety buffer) and speculative

(bargain hunting) purposes.

Obvious omissions from the above list are:

• Alternative investments – usually taken to be hedge

funds and private equity. As these are essentially

different ways to gain access to the asset categories

outlined above, we have decided to simplify matters

by avoiding them.

• Foreign exchange – FX exposure is implicit in most

of the regional allocations within the various asset

classes. The returns on cash, in particular, are very

similar to pure FX outcomes. We do, however,

allow currency hedging on a selective basis.

Better to be vaguely right than exactly wrong

Just as we do not want to go down to the level of

choosing the equity or debt of individual companies, as

the effort outweighs the potential gains (in our view), we

need to decide which decisions are worth taking and

which are not (the fewer we can get away with the

better).

Figure 5 – Global asset correlations since 2001*

*Based on monthly total returns in local currency.

Source: MSCI, BAML, Datastream and Source Research

An obvious answer is to group assets together that

share high correlations. Starting with 43 individual

assets (global and regional indices for equities,

sovereigns, corporates, real estate, cash, currencies

and product indices for commodities) and looking at

different time periods (since 2001) in both local

currency and USD , the conclusions are:

• There is a high degree of correlation within each

asset group. This gives the unsurprising result that

we can group together regional equity indices into

one global bloc and so on for each asset class.

• The one major exception to the above point is

emerging market debt, which behaves more like

developed equity markets than developed sovereign

markets. This is especially true when we are using

local currency returns.

• The asset groups with the lowest correlations to the

rest are cash and government bonds. This is true

over different time periods and in both local

currency and USD versions. Figure 5 is a clear

example, using returns in local currency since 2001.

From that perspective, the decisions about these

two groups are the most important to be made.

• The one asset group that has a decent correlation

with government bonds is investment grade

corporate debt.

• Via its reasonable correlation with high yield

corporate debt, investment grade is a stepping

stone from government debt to a clear grouping of

three equity-like assets: equities, corporate high

yield debt and real estate (REITs).

• Commodities are on the fringes of this latter group.

There are of course richer conclusions to be drawn the

further we delve into the individual asset classes but as

first suggested by logician Carveth Read: “it is better to

be vaguely right than exactly wrong”. Hence we treat

those more detailed decisions as secondary.

What is neutral?

Every investor has their own idea of what constitutes a

neutral or benchmark allocation to the various asset

classes, based on their own situation and preferences.

By definition, we cannot match your circumstances but

we need to have some notion of neutral around which

to express our views.

EquitiesGov

Bonds

Corp

Bonds -

IG

Corp

Bonds -

HY

Commo-

dities

Real

EstateCash

Equities - -0.36 0.18 0.72 0.44 0.76 -0.18

Gov

Bonds-0.36 - 0.60 -0.15 -0.25 -0.12 0.05

Corp

Bonds -

IG

0.18 0.60 - 0.55 0.14 0.43 -0.15

Corp

Bonds -

HY

0.72 -0.15 0.55 - 0.40 0.75 -0.21

Commo-

dities0.44 -0.25 0.14 0.40 - 0.36 -0.04

Real

Estate0.76 -0.12 0.43 0.75 0.36 - -0.14

Cash -0.18 0.05 -0.15 -0.21 -0.04 -0.14 -

December 2014 Straight from the Source 7

Multi-asset research The Big Picture

One obvious solution is to use the market

capitalisations of the assets we intend to use (as a

representation of what the portfolio would look like if we

had the good fortune to be able to buy everything that

exists). Figure 6 shows our best attempt at doing this,

based on commonly used indices. Bearing in mind that

different data providers and indices give different

answers, this is not a definitive answer: simply the one

that makes the most sense to us.

Figure 6 – Market Capitalisation of Global Assets

Market Cap ($bn) Weighting

Equities 36,891 47%

Gov. Bonds 24,642 32%

Corp IG 8,609 11%

Corp HY 2,121 3%

Real Estate 1,624 2%

Commodities 500 1%

Cash* 3,719 5%

Total 78,106

*Note: the market cap for cash is simply set to make it 5% of the total.

Source: MSCI, BAML, Datastream, Reuters and Source Research

Having said that, there are some asset classes for

which no sensible market capitalisation exist which

necessitated some educated guesses on our part:

• Real estate means different things to different

people. Savills estimate the global market cap to be

$180trn (around five times the size of global equity

markets as measured by MSCI). However much of

that is residential and not investible (Savills reckons

investible commercial real estate amounts to

$20trn). Most investors do not have the wherewithal

to make direct investments, making REITs the easy

choice. According to Reuters, the global market cap

invested in REITs is $1.6trn.

• Commodities are even trickier. Viewed in terms of

annual production or inventory levels, the numbers

are enormous but the amount actually invested in

commodities is quite small (if difficult to identify).

Commodity ETPs add up to just over $100bn, while

the assets managed in this category by hedge funds

is reckoned by BarclayHedge to be around $300bn.

Allowing for the possibility of other funds and direct

investments suggests that around $500bn is

invested in this asset category.

• Cash is not as easy as it sounds. We think of it as

short term deposits and prefer to include short term

government paper in the bonds section. If we are

looking at broad monetary aggregates, the global

stock is likely to exceed GDP and is probably in the

hundreds of trillions of dollars (depending upon

which monetary aggregate we use). However, like

commodities, cash has many more uses than simply

acting as an investment and it is hard to think of it in

terms of market capitalisation. In reality, most

investors limit their cash holdings to no more than

10% and we do likewise (with an arbitrary neutral

weighting of 5%).

December 2014 Straight from the Source 8

Multi-asset research The Big Picture

Source Multi-Asset Portfolio

The decisions about portfolio weightings are made in

four steps:

• Estimation of expected returns, based on

fundamentals and valuations.

• Allocation to global asset categories (using

optimisation techniques to avoid obvious errors).

• Fine tuning of allocations within each asset group

(by region, style etc.).

• Decisions about currency hedging.

Economic and policy outlook

Given the above discussion of correlations across asset

classes and the conclusion that choices about

weightings to cash and government bonds are the most

important decisions we can make, it is only natural to

place a lot of emphasis on cyclical and policy

considerations.

Figure 7 – Top ten economies’ share of Global GDP*

% Cumulative %

United States 19% 19%

Euro Area 15% 34%

China 11% 45%

Japan 6% 50%

United Kingdom 3% 53%

Brazil 3% 56%

Russia 2% 58%

India 2% 60%

Canada 2% 62%

Australia 2% 64%

*2013 data. Source: IMF and Source Research

Around 50% of global GDP is accounted for by the US,

Eurozone, China and Japan, with the next six largest

economies accounting for a further 14% (see Figure 7).

Limiting our focus to those ten economies should allow

a near comprehensive view of the global economy,

without wasting valuable time.

One common influence for the economies under

consideration is the recent decline in the price of oil and

energy in general. Though evidence is mixed about the

effect of a fall in oil prices, when due to rising supply (as

we think it is right now) it should provide a boost to

growth, depress inflation and allow central banks to

remain accommodative for longer. In our view, the

recent $30-$40 decline in the price of oil, if it proves

permanent, will boost the GDP of non-oil exporting

nations by 0.3%-0.6% over two years (see Ample

Sufficiency).

Figure 8 – Real GDP growth vs 20y average

Source: IMF and Source Research

Though not enormous, this will be of particular help in

countries/regions struggling for growth, such as the

Eurozone. It will be accompanied by lower inflation

(perhaps as much as 0.2%-0.3% over two years). We

view this as a positive (higher real incomes, less

pressure on central banks to tighten, lower bond yields)

rather than a “deflation” negative.

Figure 8 shows that most of the 10 largest economies

are currently in the lower half of their 20 year growth

range. However, with the exceptions of Brazil, China

and Russia, they are in the recovery/acceleration

phase. Figure 9 shows this in stylistic fashion

(consensus economic forecasts are shown in Appendix

1).

This is not great news from a growth perspective (the

consensus world GDP forecast for 2014 is only 2.5%,

according to Bloomberg) but it suggests most central

banks will remain supportive. With G10 inflation

expected to be below 1.5% during 2014 (Bloomberg

consensus) it is unlikely tightening would be on the

agenda were it not for the extreme policy settings

currently in place in many countries.

-15

-10

-5

0

5

10

15

Min Max

2014 Growth 20y Average

December 2014 Straight from the Source 9

Multi-asset research

The Big Picture

Figure 9 – The economic roller coaster

Source: Source Research

Any tightening that does occur (especially in the US,

UK, Australia and Canada), will likely start during mid-

2015 at the earliest and will be gentle in the first

instance (the recent decline in oil prices can only help in

that regard). Even better, it will be balanced by

loosening in China, Japan and the Eurozone (and

eventually India and Brazil). Those worried about Fed

tightening should also bear in mind that financial market

reactions have historically not been as bad as

commonly supposed (see Who’s afraid of the big, bad

Fed?).

Economic and policy divergence over the coming years

has a number of implications:

• First, the dollar is likely to remain in the ascendant

against major currencies.

• Second, any negative effects stemming from Fed

tightening (see Who’s afraid of the big, bad Fed?),

will be less acutely felt in non-US markets and may

even be ignored. Bonds are most under threat in the

US, the question elsewhere being whether local

policy easing will be sufficient to offset the upward

pull on yields coming from the US.

• It is hard to identify any economy sufficiently

advanced in its cycle to fear the negative effects on

cyclical assets that occur when tightening brings on

recession.

• It is too early to move back into cyclical commodities

(industrial metals, energy).

Valuations

No valuation metric exists that covers all asset classes,

certainly nothing that would include commodities. The

closest we can get to a common measure is yield.

Figure 10 shows the yield on a range of global assets,

within their (varying) historical ranges. A glance reveals

the following:

• The yields on virtually all assets are below historical

averages (except for Japanese equities and EM

assets in general, as revealed in Appendix 2).

• Those on cash and bonds are nearly as low as they

have ever been (with the exception of EM bonds).

December 2014 Straight from the Source 10

Multi-asset research The Big Picture

• Equities and real estate offer higher yields than

government and investment grade corporate bonds.

• The highest yields of all are available on high yield

debt (and EM sovereigns).

With government bond yields so low, it is hard to

imagine strong returns from here. For instance,

Eurozone 10yr yields are around 0.8%. Even if they fall

to 0.5%, the capital gain would be only 3% and, of

course, the ongoing income stream is minimal. Short of

believing global recession is imminent, it is hard to

make the case for government bonds, especially as US

yields are expected to rise.

Figure 10 – Global yields vs historical averages

Source: BAML, FTSE, Datastream and Source Research

Investment grade corporate yields are also close to

historical lows, as are the spreads versus government

benchmarks. High yield looks interesting from a pure

yield perspective, unless recession is imminent, though

spreads versus benchmarks are compressed.

Market forecasts

Before moving onto expected returns, it is worth

outlining the forecasts for a range of key market

variables that underpin those projections. Figure 11

shows our one and five year forecasts for important

central bank rates, as well as for bond, currency, equity

and commodity markets. Again, with the wish to be

vaguely right rather than exactly wrong, the point is to

show broad directions and magnitudes rather than be

precisely correct. The notable features are:

• Rising central bank rates and bond yields in the UK

and US and eventually elsewhere.

• Dollar appreciation against most currencies.

• Strengthening equity markets (see China).

• Weak commodity markets in the short term but

cyclical groups recovering over the medium term.

Figure 11 – Market forecasts*

Current Forecast

(25/11/14) 1-year 5-year

Central Bank Rates

US 0.25 0.50 3.00

Eurozone 0.05 0.05 1.50

China 5.60 5.00 5.00

Japan 0.07 0.10 1.00

UK 0.50 0.75 3.50

10yr Bond Yields

US 2.26 2.70 4.00

Eurozone 0.75 0.75 2.50

China 3.79 3.50 3.50

Japan 0.45 0.40 2.30

UK 2.01 2.50 4.30

Exchange Rates/US$

EUR/USD 1.25 1.15 1.10

USD/CNY 6.14 6.15 6.20

USD/JPY 117.98 125.00 100.00

GBP/USD 1.57 1.50 1.50

Equity Indices

S&P 500 2067 2400 2300

Euro Stoxx 50 3226 3500 4500

FTSE A50 7902 8900 16000

Nikkei 225 17408 21500 24500

FTSE 100 6731 7100 7650

Commodities

Oil (Brent) 78 70 80

Gold 1199 1100 900

Copper 6653 6000 8000

*See Appendix 4 for methodology.

Source: Datastream and Source Research

Expected returns

The above market forecasts are derived from the same

process that generates expected returns but there is not

an exact mapping. For example: the expected returns

on bonds are based on indices with mixed maturities

(average maturity 5yrs-7yrs), rather than on a 10 year

bond; the commodity returns are based on broad

commodity groups (energy and industrial metals, for

instance) rather than on specific products (Brent and

copper, say); the expected returns include income

flows; the USD versions of expected returns allow for

projected currency movements.

Our projections for expected returns are shown in

Appendix 3 and summarised in Figure 12. For each

0

5

10

15

20

25

Cash GovBonds

CorpBonds

Corp HY Equities RealEstate

December 2014 Straight from the Source 11

Multi-asset research The Big Picture

asset category Appendix 3 shows historical annualised

total returns in USD (both for the last 10 years and over

the full history available). We also show how current

yields compare to historical norms, which helps to

formulate forecasts of where those yields will go in the

future (of course, there is no yield for commodities).

Figure 12 – Projected total returns on global assets

and neutral portfolio (USD, annualised)*

*See appendices 3 & 4.

Source: Source Research

The projected capital gains/losses are derived from

those yield forecasts (except of course for commodities)

and are added to current yields (plus growth in the case

of equities and real estate) to generate total returns in

local currency (in the case of cash there are no capital

gains/losses and we assume a straight line move in

rates to generate the income stream over the forecast

horizons). In the case of commodities, the returns are a

reflection of our views about price developments (based

on real prices and cyclical considerations).

Finally, the local currency total returns are adjusted by

our currency forecasts to generate returns in USD.

Those currency forecasts are derived from a mix of

factors including valuations (real exchange rates) and

fundamentals (central bank policies, say).

Not surprisingly, given the reduced level of bond yields

and the expected tightening by the Fed, the total returns

on sovereign bonds are low/negative. Those on

corporate bonds, especially high yield, are better. Cash

returns are minimal at this stage, though we expect

them to increase over a five year time horizon.

On the assumption we are not heading for global

recession, and given the more attractive yields they

offer, we expect better returns from both equities and

real estate, over both a one year and a five year time

frame. The one year returns are so high because we

assume ongoing compression of yields in most

markets, under the influence of central bank asset

purchases and flows out of fixed income assets.

There is a non-negligible risk that the commodities

super cycle is over and that we are in the middle of a

long run deflation of raw material prices. If this is the

case, prices will continue trending downward for some

time. However, this does not mean the cycle is dead

and it is possible that Fed tightening will be associated

with strong performance by cyclical commodities

(energy and industrial metals) as has been the case

historically. Also, the recent easing by the PBOC, if

continued, could be a catalyst for recovery in raw

material markets.

Optimised allocations

We prefer to keep the focus on the fundamentals of

investment returns rather than on the technical features

of optimisation processes and have therefore chosen to

stick with the most basic process as developed by

Harry Markowitz.

Having developed the expected returns outlined above,

we then need to combine them with a covariance

matrix. Rather than forecasting every part of the

covariance matrix, we are relying on history to provide a

guide. In truth, the correlations between major asset

classes do not vary enormously from one five year

period to another, though they can change dramatically

during short periods (such as the 2007-09 crisis). For

the purposes of the current exercise, we assume that

the covariance matrix of the last five years acts as a

reasonable template for the coming period.

Combining the expected returns derived above with the

information from the recent covariance matrix allows us

to develop optimised portfolios. We look at the

optimisation in two ways: maximising the Sharpe Ratio

and maximising return subject to volatility being no

higher than for the benchmark portfolio. The results are

shown in Figure 13, which is the basis of the Source

Multi-Asset Portfolio.

It is noticeable that equities and high yield corporate

debt are given above neutral allocations no matter

-10%

-5%

0%

5%

10%

15%

1-year

5-year

December 2014 Straight from the Source 12

Multi-asset research The Big Picture

which optimisation approach is used (Sharpe Ratio or

Maximised Return, 1yr or 5yr projected returns). This is

reflected in the Source Multi-Asset Portfolio.

Real estate, on the other hand, is penalised within the

optimisation because of its higher volatility.

Nevertheless, we choose to give it an Overweight

allocation to gain more diversification across the

“equity-like” assets.

Government bonds are underweighted in virtually all

cases, especially when using one year returns and we

stick with this idea in the Source Multi-Asset Portfolio.

Investment grade corporate debt is the closest

substitute for sovereign debt but unfortunately the

optimisation results are of little help, running from a

zero allocation when five year returns are used to

neutral/overweight positions when using one year

returns (the predicted one year returns on cash and

sovereigns are so poor that IG is used as the next best

thing to reduce volatility). We go with an underweight

but non-zero allocation and suggest short duration.

The results for cash are in some way similar to those of

IG debt (though reversed) and we choose to maintain a

non-zero underweight allocation (to allow future

flexibility more than anything else).

Commodities are zero-weighted under all optimisation

scenarios (as a result of our bearish price views) and

we stick with that in the Source Multi-Asset Portfolio.

Allocations within asset classes

As mentioned above, the correlations across regions

within each asset category are so high that intra-asset

class decisions are very much of second order

importance versus inter-asset class allocations.

Nevertheless, whether for fundamental, valuation or

currency reasons it is useful to have the freedom to

impact predicted returns by choosing individual regional

weights (Appendix 4 gives detailed expected return

information).

The major considerations in this respect are:

• The contrast in central bank policies between the

US and UK on the one hand (tightening over the

next year) and China, the Eurozone and Japan on

the other (central banks loosening). Asset prices

are more likely to find support from policy makers

outside the Anglo-Saxon world. Also, USD is likely

to continue on the upside.

• The flipside is that growth is stronger where central

banks are tightening (US and UK), which provides

some offset to higher rates. However, a weak JPY

and EUR should provide future support to their

respective economies.

• The rich valuation of US equities, certainly when

compared to those in the Eurozone and Japan.

• The likely rebound at some stage over the next year

in cyclical commodities (industrial metals and

energy). They are typically weak in the run-up to

Fed rate hikes but strengthen when the Fed is

tightening.

Figure 13 – Optimised allocations for global assets

Using 1y Return Using 5y Return

Neutral Portfolio

Policy Range

Sharpe Ratio

Max Return

Sharpe Ratio

Max Return

Source Multi-Asset Portfolio

Cash 5% 0-10% 0% 0% 6% 10% 3%

Government Bonds 30% 10-50% 10% 24% 10% 32% 18%

Corporate IG 10% 0-20% 10% 20% 0% 0% 5%

Corporate HY 5% 0-10% 10% 10% 10% 10% 10%

Equities 45% 20-70% 70% 46% 70% 48% 60%

Real Estate 2% 0-6% 0% 0% 4% 0% 4%

Commodities 3% 0-4% 0% 0% 0% 0% 0%

“Sharpe Ratio” shows the results of maximising the Sharpe Ratio. “Max Return” maximises returns while not exceeding the volatility of the Neutral

Portfolio. This is a simulated portfolio.

Source: Source Research

December 2014 Straight from the Source 13

Multi-asset research

The Big Picture

Given that we are not forecasting global recession, we

view bonds as more of a danger than an opportunity at

this stage (except for high yield). As can be seen in

Appendix 2, the obvious exceptions are emerging

markets, where yields are relatively high and where

some important countries are showing recessionary

conditions (China, Brazil, Russia, for instance) and US

high yield, where yields are above 6% and the

economic cycle remains supportive (high yield tends to

be a strong performer in the run up to Fed tightening –

see the aforementioned Who’s afraid of the big, bad

Fed?). Within sovereign debt markets, the only above

neutral allocation is to emerging markets.

Among equities and real estate, the most comfortable

yields versus historical norms are generally to be had

outside the US but dividend growth remains a support

for the US, as does anticipated dollar strength. We are

overweight all equity markets but if your time horizon is

five years rather than one we would suggest a focus on

non-US markets. Within real estate, we have a

preference for US and Japanese markets and see little

scope for UK yields to decline much further (and are

Underweight there).

Figure 14 – Current real* price vs history (Std. dev)

*Deflated by US CPI. Source: GSCI, Datastream and Source Research

Not a lot can be said about commodity market

valuations as no satisfactory metric exists. Perhaps the

best that can be done is to compare real prices with

historical norms (by real we mean adjusted by US CPI).

Figure 14 shows for S&P GSCI groups how todays real

prices compare to the average of the last 40 years.

With the exception of Agriculture, prices appear to be

above historical norms, suggesting downside risk

unless there have genuinely been changes in the

structure of commodity markets over the last decade or

so. Given that commodities tend not to perform well in

the run up to Fed tightening, there seems scant reason

to have commodity exposure at this stage.

Currency hedging

There have historically been at least two good reasons

to adopt a cautious approach to currency hedging: first,

it is notoriously difficult to forecast exchange rates and,

second, hedging can sometimes be very costly.

While it remains difficult to forecast currency markets,

the convergence of major interest rates around zero

has virtually eliminated the cost of hedging, so we

should be more open to hedging than usual. This is

even more so when the case for buying an asset is

predicated upon weakness of its associated currency,

which is particularly the case with Japanese equities

and to a lesser extent for those of the Eurozone.

Figure 15 – Real exchange rates (deviation from

historical norm)

Source: OECD, Datastream and Source Research

In general, when a currency is expected to make

sustained gains (as is currently the case for the US

dollar), the case for holding assets in that currency

(either directly or via currency hedges) is all the greater.

If we were buying Japanese or Eurozone equities in

isolation, we would want to hedge the currency

exposure into USD. However, through our broad

investment choices, we are already underweight the

yen and the euro and do not wish to accentuate those

positions by currency hedging. Also, the yen is now

extremely cheap in real terms (see Figure 15).

-1.0

-0.5

0.0

0.5

1.0

1.5

-25

-20

-15

-10

-5

0

5

10

CHF EUR GBP USD JPY

Current/Average since 1980 (%)

December 2014 Straight from the Source 14

0

2

4

6

8

10

12

14

16

18

1694 1734 1774 1814 1854 1894 1934 1974 2014

Bank of England Base Lending Rate

Cash (Underweight)

We suggest allocating 3% of the portfolio to cash

instruments, which is underweight compared to the 5%

neutral position. Expected returns are weak due to

abnormally low central bank rates and are negative in

many cases when translated into USD (we expect dollar

appreciation). On that basis the weighting should be

zero but a positive balance is maintained for speculative

purposes (awaiting opportunities).

Our projections take account of the expected

divergence of central bank policies between the Anglo-

Saxon world on the one hand and the Eurozone, Japan

and China on the other. We expect rates to rise in the

US and UK, as tightening starts within the next 12

months. As a result, cash returns should climb, albeit

from very low levels.

Figure 16 – FED target rate

Source: Datastream and Source Research

As shown by Figures 16 and 17, rates are well below

historical norms, suggesting plenty of scope for rate

hikes once economic conditions normalise.

By contrast, the ECB, the BOJ and the PBOC have

recently announced further easing, thus rates should

remain at their current levels near the zero-bound in the

two developed economies. The PBOC is famously

difficult to read, but we expect accommodative policy

measures to continue in 2015.

Figure 17 – Bank of England target rate

Source: Global Financial Data

Looking further out (5 years), we see rates returning to

near-normal, mid-cycle levels in Anglo-Saxon

economies. In our view, they will start rising in the rest

of the developed world, too, though remaining at

historically low levels.

Figure 18 – Projected returns (annualised) Figure 19 – Rates vs. History

LIBOR Rates Return USD Return

Now In 1y In 5y 1y 5y 1y 5y

USD 0.1% 0.5% 3.0% 0.3% 1.4% 0.3% 1.4%

EUR 0.0% 0.1% 1.5% 0.1% 0.6% -7.8% -1.9%

GBP 0.5% 0.8% 3.5% 0.6% 1.8% -3.9% 0.8%

JPY 0.0% 0.1% 1.0% 0.1% 0.4% -5.5% 3.8%

Source: Datastream and Source Research

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

USD EUR GBP JPY

Now

Average

-5

0

5

10

15

20

54 59 64 69 74 79 84 89 94 99 04 09 14

FED Policy Rate

Synthetic Policy Rate (using Bernanke rule of thumb)

Global Asset Classes

December 2014 Straight from the Source 15

Multi-asset research

Global Asset Classes

Government Bonds (Underweight)

We suggest allocating 18% of the portfolio to

government bonds, which is underweight compared to

the 30% neutral position. As indicated in Figure 22,

expected returns are negative in many cases as bond

yields are expected to follow policy rates higher (see

Figure 20).

Figure 20 – US policy rate vs 10y yields

Source: Datastream

With the ending of QE3 in the US, the next policy step

in the Anglo-Saxon world should be a rise in rates. We

expect this to drive local bond yields higher (UK political

uncertainty will add to pressures there). Short duration

bonds are preferred.

Policy divergence should dampen the global effect of

Fed tightening. The BoJ has already announced a step-

up in QE, while the ECB is widely expected to introduce

further easing measures, perhaps eventually including

sovereign bond purchases. As a result, we expect

yields in those markets to stay at their current levels or

move lower in the coming year.

Despite the rise in US yields, we suspect those in EM

can fall from current relatively generous levels (see

Figure 21), especially with a number of central banks

likely to loosen (in Brazil, China, India and Russia, say).

Figure 21 – Government bond yields vs history

Source: BAML, JPM, Datastream and Source Research

Moving to a five year time horizon, we see a return of

global yields to mid-cycle levels, resulting in negative

expected returns in developed markets (except the UK,

where the higher starting yield helps).

Generous yields render Emerging Markets the only

attractive proposition among sovereign markets (even

allowing for USD appreciation), making them the only

region where we suggest an overweight position.

Figure 22 – Projected returns (annualised) Figure 23 – Yields vs History

Redemption Yields Return USD Return

Now In 1y In 5y 1y 5y 1y 5y

US 1.4% 1.9% 3.7% -1.1% -0.3% -1.1% -0.3%

Eurozone 1.0% 1.0% 2.8% 0.7% -0.7% -7.6% -3.3%

UK 1.9% 2.4% 4.2% -1.0% 0.2% -5.4% -0.8%

Japan 0.4% 0.3% 2.0% 0.9% -1.1% -4.6% 2.2%

EM 5.7% 5.5% 6.0% 6.9% 5.5% 1.6% 4.5%

Source: Datastream and Source Research

0%

2%

4%

6%

8%

10%

US EZ UK JP EM

Now Average

0

2

4

6

8

10

12

14

83 86 89 92 95 98 01 04 07 10 13

US Fed Funds Rate US 10y Yield

0

2

4

6

8

10

12

14

16

18

Global EM US Europe EZ UK Japan

December 2014 Straight from the Source 16

Multi-asset research

Global Asset Classes

Corporate Bonds (Underweight)

We suggest allocating 5% of the portfolio to corporate

investment grade bonds, which is underweight

compared to the 10% neutral position. Though we think

spreads to government bonds can narrow further, this

asset class will not escape forever the bleak outlook on

sovereign debt (Figure 24 shows the strong correlation

between the two asset classes).

Figure 24 – 5y rolling correlations of total returns*

*Global indices. Source: BAML, Datastream and Source Research

As is the case with government bonds, yields on IG

corporate debt are at or close to historical lows (see

Appendix 2). However, spreads versus sovereigns

remain above all-time lows (see Figure 25). We

suspect spreads can narrow over the next 12 months,

leaving corporate yields little changed from current

levels (see Figure 26). Returns will nevertheless be

limited and better options exist in other asset classes.

Taking account of projected currency movements, the

favoured market within this asset class over the next 12

months is the US.

Figure 25 – US corporate bond yields vs history

Source: BAML, Datastream and Source Research

We see even less merit in holding corporate bonds over

a 5-year horizon as we think equivalent returns will be

available on cash. As we expect corporate spreads to

normalise over the medium term, we expect the yield on

corporate IG instruments to rise even faster than that on

benchmark government bonds (in many regions). This

will eradicate much of the advantage given by higher

yields. Returns on yen IG bonds are better than most

because we expect the yen to rebound over the

medium term. In general, short duration bonds are

preferred.

Figure 26 – Projected returns (annualised) Figure 27 – Yields vs History

Redemption Yields Return USD Return

Now In 1y In 5y 1y 5y 1y 5y

US Dollar 3.1% 3.2% 5.1% 2.4% 1.8% 2.4% 1.8%

Euro 1.2% 1.2% 3.5% 1.3% -0.5% -7.1% -3.0%

Sterling 3.5% 3.4% 6.5% 4.3% 1.5% -0.3% 0.6%

Yen 0.3% 0.2% 2.0% 0.8% -1.0% -4.7% 2.3%

Source: Datastream and Source Research

0%

2%

4%

6%

8%

USD EUR GBP JPY

Now Average

0.70

0.75

0.80

0.85

0.90

0.95

1.00

02 03 04 05 06 07 08 09 10 11 12 13 14

Gov-Corp BondCorrelation ofMonthly Returns

0

100

200

300

400

500

600

700

86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

Corp vs Gov Spreads

December 2014 Straight from the Source 17

Multi-asset research

Global Asset Classes

Corporate High Yield Bonds (Overweight)

We suggest allocating 10% of the portfolio to corporate

high yield bonds, which is overweight compared to the

5% neutral position and the maximum allowed in our

model. Yields are high relative to other fixed income

assets and we expect them to fall in the short term,

giving a favourable outlook.

Figure 28 – US GDP vs high yield spreads

Source: BAML, Datastream and Source Research

As Figure 28 shows, spreads are contra-cyclical and

are approaching cyclical lows. We suspect that spreads

can narrow further in the US, as the economy continues

to expand, though we see limited scope for this to

happen in the Eurozone (lower yields and a fragile

economy). Default rates are not currently an issue as

we do not expect recession (see Figure 29).

The cyclical nature of the high yield asset class makes

it more akin to equities than government bonds. Hence,

there should be no surprise that the projected returns

shown in Figure 30 are closer to those expected for

equities than for other fixed income assets.

Figure 29 – US vs Eurozone GDP growth

Source: IMF, Bloomberg and Source Research

Looking further out, we see yields rising with those on

government debt and then some (as spreads move

back to mid-cycle averages). This implies capital losses

but the generous coupons more than make up for that,

especially in the US. In fact, based on our forecasts, US

high yield will outperform US equities over a five year

time horizon (equity valuations are stretched). Keeping

duration short will help minimise capital losses.

Within the high yield space, the US is clearly preferred

to the Eurozone, though both are preferred to other

fixed income alternatives.

Figure 30 – Projected returns (annualised) Figure 31 – Yields vs History

Redemption Yields Return USD Return

Now In 1y In 5y 1y 5y 1y 5y

US Dollar 6.5% 5.9% 9.5% 9.2% 5.0% 9.2% 5.0%

Euro 4.4% 4.4% 9.0% 4.4% 2.3% -4.3% -0.3%

Source: Datastream and Source Research

0%

2%

4%

6%

8%

10%

12%

USD EUR

Now Average

0

400

800

1200

1600

2000

2400-6

-4

-2

0

2

4

6

85 88 91 94 97 00 03 06 09 12

GDP Growth (%, YoY)

HY Bond Yield-Gov Bond Yield Spread (RHS, Inverted)

-10

-5

0

5

10

15

US Eurozone

Average Now 2015F

December 2014 Straight from the Source 18

Multi-asset research

Global Asset Classes

Equities (Overweight)

We suggest allocating 60% of the portfolio to equities,

which is overweight compared to the 45% neutral

position. Valuations are no longer cheap, but remain far

from the extremes of fixed income. At this stage of the

cycle equities tend to outperform. Couple that with

accommodative central banks in the Eurozone, Japan

and China and it becomes difficult to argue against the

asset class.

Figure 32 – Shiller P/E (S&P 500)

Source: Robert Shiller and Source Research

On the basis of decent dividend growth and a slight re-

rating, we think equities will be the strongest-performing

asset class over the next 12 months. Japan and the US

stand out, but for different reasons. The maturing bull

market in the US should support both dividend growth

and valuations, while efforts by the BOJ and the

Japanese government should provide a healthy

environment for Japanese equities (which are also

benefitting from important asset allocation swings at

some domestic funds). UK and emerging market stocks

may lag during 2015 (UK political uncertainty, limited

EM dividend growth).

Figure 33 – Global dividend growth and DY (%)

Source: Datastream and Source Research

Looking over the next five years, we expect equities to

be among the best performing asset classes (only high

yield is expected to do better on a risk adjusted basis).

Figure 33 suggests that valuations are not stretched

globally and that dividend growth is modest (and can

improve).

However, we expect stretched valuations and

decelerating dividends to handicap the US market

(Figure 32), with better returns available in Japan, EM

and the Eurozone (mainly due to an upturn in their

respective economic cycles).

Figure 34 – Projected returns (annualised) Figure 35 – Div. growth assumptions

Dividend Yields Return USD Return

Now In 1y In 5y 1y 5y 1y 5y

US 1.9% 1.8% 2.5% 18.2% 4.5% 18.2% 4.5%

Eur ex-UK 3.0% 2.9% 3.0% 11.8% 10.1% 2.5% 7.2%

UK 3.2% 3.2% 3.8% 8.4% 6.2% 3.6% 5.2%

Japan 1.7% 1.5% 1.6% 26.6% 8.9% 19.7% 12.6%

EM 3.1% 3.0% 3.0% 6.5% 11.0% 1.2% 9.9%

Source: Datastream and Source Research

0

5

10

15

20

25

30

35

40

45

1881 1901 1921 1941 1961 1981 2001

Shiller P/E Average

-25

-20

-15

-10

-5

0

5

10

15

20

25

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

74 77 80 83 86 89 92 95 98 01 04 07 10 13

DY Dividend Growth (YoY, RHS)

0%

2%

4%

6%

8%

10%

12%

US Eur ex-UK

UK JP EM

Year 1 Year 2-5

December 2014 Straight from the Source 19

Multi-asset research

Global Asset Classes

Real Estate (Overweight) We suggest allocating 4% of the portfolio to real estate,

which is overweight compared to the 3% neutral

position. As with equities, we assume decent dividend

growth with some re-rating, providing double-digit

returns on a 12-month forward basis. Nevertheless,

their high correlation with equities and also higher

volatility makes us less keen on REITs in comparison.

Figure 36 – Global REITs vs MSCI World

Source: FTSE, MSCI, Datastream and Source Research

In our view, real estate will have a strong 2015 on the

back of cyclical tailwinds. We keep our dividend growth

estimates slightly below probability-weighted historical

averages and assume a tad of re-rating. This sets real

estate up as the second-best performing asset class if

our estimates are correct.

We expect the UK to lag as it has already had a good

run (and the political outlook is uncertain), but the rest

of the world should see double-digit total returns. Japan

and Europe stand out, where we think near 16% returns

are likely. Valuations seem reasonable and most

markets seem to have turned a corner in Europe, while

the BOJ’s plan to purchase J-REITs should provide a

boost in Japan.

Figure 37 – Historical Dividend Yield Ranges

Source: FTSE, Datastream and Source Research

As we look further ahead, annualised total returns on

REITs seem the most attractive for the next 5-years,

beating all other asset classes. This is despite an

assumed de-rating (except in Europe ex-UK) and

comes with the help of decent dividend growth (5% per

annum). The main reason for not having a bigger

allocation to the asset class is its relatively high

volatility.

Figure 38 – Projected returns (annualised) Figure 39 – Div. growth assumptions

Dividend Yields Return USD Return

Now In 1y In 5y 1y 5y 1y 5y

US 3.6% 3.5% 4.0% 10.6% 5.4% 10.6% 5.4%

Europe 3.6% 3.3% 3.3% 16.1% 8.2% 6.5% 5.4%

UK 3.4% 3.4% 4.0% 6.9% 3.8% 2.2% 2.9%

Japan 1.6% 1.5% 2.0% 15.9% 7.6% 9.6% 11.3%

EM 3.7% 3.6% 4.0% 14.3% 9.6% 8.6% 8.5%

Source: Datastream and Source Research

40

60

80

100

120

140

160

180

05 06 07 08 09 10 11 12 13 14

FTSE EPRA/NAREIT Global

MSCI World

0

2

4

6

8

10

12

14

Global EM US Eur ex-UK

UK Japan

0%

2%

4%

6%

8%

10%

12%

US Europe UK JP EM

Year 1

Year 2-5

December 2014 Straight from the Source 20

Multi-asset research

Global Asset Classes

Commodities (Underweight)

We suggest allocating 0% of the portfolio to

commodities, versus a neutral position of 2%. We

expect further weakness in all the main commodity

groups, except agriculture in the next 12 months. Due

to the lack of comparable valuation measures for

commodities, we base our views on real prices (US

CPI-adjusted) relative to their long-run averages.

Figure 40 – Real Brent oil prices (US CPI adjusted)

Source: Datastream and Source Research

The most important constituent in our chosen

benchmark (GSCI) is energy and within that oil. Despite

a big fall in oil prices year-to-date, we do not see an

imminent rebound. The most recent OPEC meeting

ended with no agreement to cut production as Saudi

Arabia seems intent on driving marginal producers out

of the market (in North America in particular). The

“game of chicken” continues and we do not expect

either of them to blink in the next 12 months.

Figure 41 – Real wheat prices (US CPI adjusted)

Source: USDA, Robert Shiller, Datastream and Source Research

The other major constituent in the index is agriculture.

This non-cyclical group is impacted more by supply

shocks than by slow burning demand developments. It

is well-known that farmers cannot immediately change

their output to reflect changes in price, as many of their

processes are annual. Hence, the price weakness seen

this year due to bumper harvests will no doubt result in

less crops being sown for next year, which will

eventually bring about a recovery in prices (helped by

the prospect of mild El Nino conditions).

On a 5-year view, we forecast modest gains for most

groups, except precious metals – they will be penalised

by the strong dollar and the rise in real bond yields. At

this point, there seems no reason to hold commodities,

though that will change.

Figure 42 – Projected Returns Figure 43 – Real Index vs History

Yields Return USD Return

Now 1y 5y 1y 5y 1y 5y

Energy - - - -9.9% 0.6% -9.9% 0.6%

Ind Metals - - - -9.8% 3.8% -9.8% 3.8%

Prec Metals - - - -8.3% -5.6% -8.3% -5.6%

Agriculture - - - 10.0% 2.0% 10.0% 2.0%

Source: Datastream and Source Research

0

1

2

3

4

5

6

7

NRG Ind M Prec M Ag

Now

Average

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

87 89 91 93 95 97 99 01 03 05 07 09 11 13

Real Oil Real Oil Avg0

20

40

60

80

100

120

140

160

180

200

US Real wheat prices, adjusted by theCPI index (rebased) - All Wheat

November 2014 Straight from the Source 21

Appendix 1: Consensus economic forecasts

Figure 44 – Consensus economic forecasts

GDP Growth (%)

2013 2014 2015 2016

World 2.2 2.5 2.9 3.1

US 2.2 2.2 3.0 2.9

Eurozone -0.4 0.8 1.2 1.5

China 7.7 7.4 7.0 7.0

Japan 1.5 0.9 1.0 0.9

UK 1.7 3.0 2.6 2.3

Brazil 2.5 0.2 1.2 2.2

Russia 1.3 0.3 0.7 1.5

India 4.7 5.3 5.7 6.3

Canada 2.0 2.3 2.5 2.5

Australia 2.3 3.1 2.8 3.2

CPI Change (%)

2013 2014 2015 2016

World 2.5 2.3 2.6 2.8

US 1.5 1.7 1.8 2.2

Eurozone 1.3 0.5 1.0 1.4

China 2.6 2.2 2.5 2.8

Japan 0.4 2.8 1.9 1.9

UK 2.6 1.6 1.9 2.0

Brazil 6.2 6.3 6.3 5.9

Russia 6.8 7.5 7.0 5.5

India 10.9 7.6 6.6 6.5

Canada 0.9 2.0 1.8 2.0

Australia 2.5 2.6 2.5 2.7

Nominal GDP (%)

2013 2014 2015 2016

World 4.7 4.8 5.6 6.0

US 3.7 3.9 4.9 5.2

Eurozone 0.9 1.3 2.2 2.9

China 10.5 9.8 9.7 10.0

Japan 1.9 3.7 2.9 2.8

UK 4.3 4.6 4.5 4.3

Brazil 8.9 6.5 7.6 8.1

Russia 8.2 7.8 7.7 7.1

India 16.2 13.3 12.6 13.1

Canada 3.0 4.3 4.3 4.5

Australia 4.8 5.8 5.4 6.0

Source: Bloomberg, except for India (provided by Oxford Economics)

December 2014 Straight from the Source 22

Multi-asset research

Appendix

Appendix 2: Global valuations vs history

Figure 45 – Global yields vs historical averages

Source: BAML, FTSE, Datastream and Source Research

-5

0

5

10

15

20

25

30

Cash G

lob

al

Cash E

UR

Cash G

BP

Cash U

SD

Cash J

PY

Glo

bal G

ov B

on

ds

EM

Gov B

ond

s

US

Gov B

on

ds

Eu

rope G

ov B

on

ds

EZ

Go

v B

on

ds

UK

Gov B

on

ds

Japan G

ov B

on

ds

Glo

bal C

orp

US

Co

rp

Eu

rope C

orp

UK

Co

rp

Japan C

orp

Glo

bal H

Y

US

HY

Eu

rope

HY

Glo

ba

l E

q

EM

Eq

US

Eq

Eu

rope

Eq

Eu

rope e

x-U

K E

q

UK

Eq

Japan E

q

Glo

bal R

eal E

st

EM

Real E

st

US

Real E

st

Eu

rope e

x-U

K R

eal E

st

UK

Real E

st

Japan R

ea

l E

st

Average Now

December 2014 Straight from the Source 23

Multi-asset research

Appendix

Appendix 3: Expected returns

Figure 46 – Expected Returns

Historical Projected

Total Return (USD) Yield Yield Capital Return Total Return Total Return (USD)

10y Overall Now Average 1y 5y 1y 5y 1y 5y 1y 5y

Cash 1.0% 3.4% 0.1% 1.7% 0.3% 2.0% 0.0% 0.0% 0.3% 1.1% -4.3% 1.0%

USD 1.9% 2.0% 0.1% 1.8% 0.5% 3.0% 0.0% 0.0% 0.3% 1.4% 0.3% 1.4%

EUR 1.0% 4.4% 0.0% 1.9% 0.1% 1.5% 0.0% 0.0% 0.1% 0.6% -7.8% -1.9%

GBP 0.5% 3.6% 0.5% 2.9% 0.8% 3.5% 0.0% 0.0% 0.6% 1.8% -3.9% 0.8%

JPY -1.3% -0.1% 0.0% 0.2% 0.1% 1.0% 0.0% 0.0% 0.1% 0.4% -5.5% 3.8%

Gov. bonds 3.4% 7.2% 1.1% 4.5% 1.4% 3.1% -2.3% -2.6% -1.1% -0.6% -4.0% -0.4%

US 4.4% 7.7% 1.4% 5.0% 1.9% 3.7% -2.7% -2.8% -1.1% -0.3% -1.1% -0.3%

Eurozone 4.3% 8.4% 1.0% 5.1% 1.0% 2.8% -0.3% -2.4% 0.7% -0.7% -7.6% -3.3%

UK 3.9% 8.8% 1.9% 6.2% 2.4% 4.2% -3.0% -2.8% -1.0% 0.2% -5.4% -0.8%

Japan 0.6% 6.0% 0.4% 2.3% 0.3% 2.0% 0.5% -2.1% 0.9% -1.1% -4.6% 2.2%

EM 8.1% 9.6% 5.7% 8.7% 5.5% 6.0% 1.1% -0.3% 6.9% 5.5% 1.6% 4.5%

Corp bonds 4.7% 6.0% 2.6% 4.7% 2.6% 4.7% 0.2% -2.2% 2.8% 1.2% -0.8% 0.4%

US Dollar 5.6% 8.1% 3.1% 7.0% 3.2% 5.1% -0.8% -2.1% 2.4% 1.8% 2.4% 1.8%

Euro 3.9% 5.1% 1.2% 4.3% 1.2% 3.5% 0.1% -2.5% 1.3% -0.5% -7.1% -3.0%

Sterling 4.1% 6.9% 3.5% 6.0% 3.4% 6.5% 0.8% -3.0% 4.3% 1.5% -0.3% 0.6%

Japanese Yen -0.1% 1.5% 0.3% 0.9% 0.2% 2.0% 0.5% -1.9% 0.8% -1.0% -4.7% 2.3%

High yield 8.1% 7.1% 6.4% 9.8% 5.5% 9.4% 3.7% -2.4% 10.1% 4.8% 6.2% 3.8%

US Dollar 7.9% 8.7% 6.5% 10.6% 5.9% 9.5% 2.7% -2.4% 9.2% 5.0% 9.2% 5.0%

Euro 7.6% 6.8% 4.4% 10.1% 4.4% 9.0% -0.1% -3.8% 4.4% 2.3% -4.3% -0.3%

Equities 7.2% 9.7% 2.4% 2.8% 2.3% 2.9% 13.1% 3.1% 15.7% 5.7% 14.6% 5.7%

US 8.2% 10.2% 1.9% 3.0% 1.8% 2.5% 16.1% 2.4% 18.2% 4.5% 18.2% 4.5%

Europe ex-UK 6.4% 10.4% 3.0% 3.1% 2.9% 3.0% 8.6% 6.9% 11.8% 10.1% 2.5% 7.2%

UK 5.3% 10.3% 3.2% 4.2% 3.2% 3.8% 5.0% 2.7% 8.4% 6.2% 3.6% 5.2%

Japan 3.2% 9.3% 1.7% 1.4% 1.5% 1.6% 24.7% 7.3% 26.6% 8.9% 19.7% 12.6%

EM 10.0% 11.8% 3.1% 2.4% 3.0% 3.0% 3.3% 7.8% 6.5% 11.0% 1.2% 9.9%

Real Estate* 7.0% 7.0% 3.4% 3.6% 3.3% 3.8% 8.4% 2.8% 12.0% 6.4% 8.6% 6.1%

US 8.3% 13.0% 3.6% 4.7% 3.5% 4.0% 6.8% 1.6% 10.6% 5.4% 10.6% 5.4%

Europe 7.3% 6.6% 3.6% 4.6% 3.3% 3.3% 12.3% 4.7% 16.1% 8.2% 6.5% 5.4%

UK 5.1% 5.1% 3.4% 4.2% 3.4% 4.0% 3.4% 0.1% 6.9% 3.8% 2.2% 2.9%

Japan 8.3% 1.3% 1.6% 1.8% 1.5% 2.0% 14.1% 5.9% 15.9% 7.6% 9.6% 11.3%

EM 15.0% 15.0% 3.7% 2.9% 3.6% 4.0% 10.3% 5.6% 14.3% 9.6% 8.6% 8.5%

Commodities -3.9% 8.6% - - - - -5.8% 0.9% -5.8% 0.9% -5.8% 0.9%

Energy -6.4% 7.0% - - - - -9.9% 0.6% -9.9% 0.6% -9.9% 0.6%

Ind. Metals 4.9% 7.1% - - - - -9.8% 3.8% -9.8% 3.8% -9.8% 3.8%

Prec. Metals 9.1% 6.7% - - - - -8.3% -5.6% -8.3% -5.6% -8.3% -5.6%

Agriculture -0.2% 3.8% - - - - 10.0% 2.0% 10.0% 2.0% 10.0% 2.0%

Source: BAML, MSCI, FTSE, GSCI, Datastream and Source Research

Notes: Less than 10y history for Real Estate

See Methodology in Appendix 4

December 2014 Straight from the Source 24

Multi-asset research

Appendix

Appendix 4: Source Multi-Asset Portfolio Methodology

Portfolio construction process

The Source Multi-Asset Portfolio is a simulated and not a real portfolio. We use optimisation processes to guide our

allocations around “neutral” and within prescribed policy ranges based on our estimations of expected returns and using

historical covariance information. This guides the allocation to global asset groups (equities, government bonds etc),

which is the most important level of decisions. We then allocate across regions within each asset group. Currency

hedging can be used. We use long term inputs but the portfolio is constructed with a 12 month time horizon.

Which asset classes?

We look for investibility, size and liquidity. With that in mind, we have chosen to include: equities, bonds (government,

corporate investment grade and corporate high yield), REITs to represent real estate, commodities and cash (all across a

range of geographies). We use cross-asset correlations to determine which decisions are the most important.

Neutral allocations and policy ranges

We use market capitalisation in USD for major benchmark indices to calculate neutral allocations. For commodities, we

use industry estimates for total ETP market cap + assets under management in hedge funds + direct investments. We

use an arbitrary 5% for cash as its use as an investment instrument is limited. We impose diversification by using policy

ranges for each asset category (the range is usually symmetric around neutral).

Expected returns

The process for estimating expected returns is based upon yield (except commodities, of course). After analysing how

yields vary with the economic cycle, and where they are situated within historical ranges, we forecast the direction and

amplitude of moves over the next one and five years. Cash returns are calculated assuming a straight-line move in short

term rates towards our targets (with, of course, no capital gain or loss). Bond returns assume a straight-line progression

in yields, with capital gains/losses predicated upon constant maturity (effectively supposing constant turnover to achieve

that). Forecasts of corporate and high yield spreads are based upon our view of the economic cycle. Coupon payments

are added to give total returns. Equity and REIT returns are based on dividend growth assumptions, using probability-

weighted historical rates and adjusting them as appropriate. We calculate total returns by applying those growth

assumptions and adding the forecast dividend yield. No such metrics exist for commodities; therefore we base our

projections on US CPI-adjusted real prices relative to their long-term averages and views on the economic cycle.

Optimising the portfolio

Using a covariance matrix based on monthly USD total returns for the last 5 years, we run two optimisation processes:

maximising the Sharpe Ratio and maximising returns with volatility no greater than that of the neutral portfolio. We repeat

this process for both 1-year and 5-year expected returns and adjust the suggested allocation to diversify further if

necessary. The optimiser is based on the Markowitz model.

Currency hedging

We adopt a cautious approach when it comes to currency hedging as currency movements are notoriously difficult to

accurately predict and sometimes hedging can be costly. Also, some of our asset allocation choices are based on

currency forecasts. We use an amalgam of central bank rate forecasts, policy expectations and real exchange rates

relative to their historical averages to predict the direction and amplitude of currency moves.

December 2014 Straight from the Source 25

Multi-asset research

Appendix

Important information

Investors in Source products should note that the value of your investment may go down as well as up. As a

result you may not get back the amount of capital you invest.

This document is for discussion purposes only, and without limitation this document does not constitute an offer or a

recommendation to enter into any transaction. The calculations and charts set out herein are indicative only, make

certain assumptions and no guarantee is given that future performance or results will reflect the information herein. Past

performance is not a guarantee of future performance. Performance may be volatile, and an investor could lose all or a

substantial portion of his or her investment. When making an investment decision, you should rely solely on the final

documentation and any prospectus relating to the transaction and not this information document. Investment strategies

involve numerous risks.

The directors of Source UK Services Limited, Source Investment Management Limited, Fund Source (US) LLC and

Source Exchange Traded Investments LLC (collectively and separately “Source”) do not guarantee the accuracy and/or

the completeness of any data included herein and Source shall have no liability for any errors, omissions, or interruptions

herein. Source makes no warranty, express or implied, as to the information described herein. All data and performance

shown is historical unless otherwise indicated. Investors should consult their own business, tax, legal and accounting

advisors with respect to this proposed transaction and they should refrain from entering into a transaction unless they

have fully understood the associated risks and have independently determined that the transaction is appropriate for

them. In no way should Source be deemed to be holding itself out as a financial adviser or a fiduciary of the recipient

hereof and this document is not intended to be "investment research" as defined in the Handbook of the UK Financial

Conduct Authority; nor is it intended to be “research” as defined in relevant U.S. securities laws and rules.

This communication is only intended for and will be only distributed to persons resident in jurisdictions where such

distribution or availability would not be contrary to local laws or regulations.

© 2014 Source UK Services Limited, 110 Cannon Street, London EC4N 6EU, UK.

Distributed by Fund Source (US) LLC.