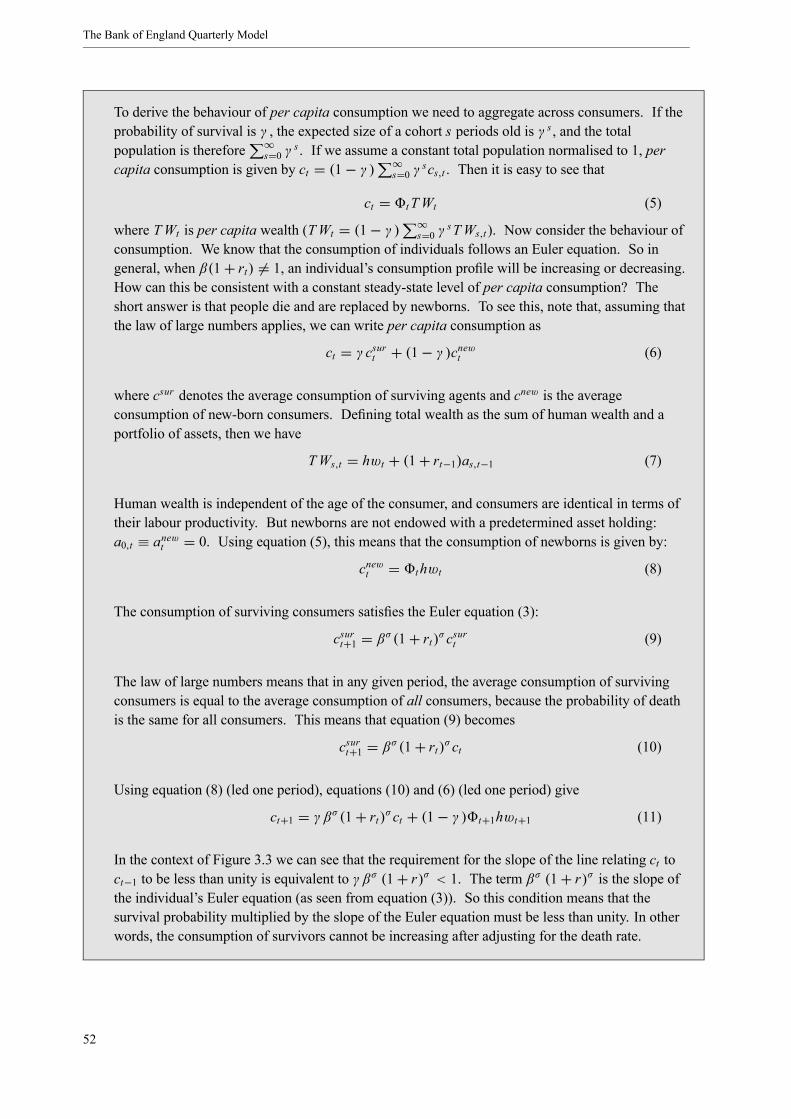

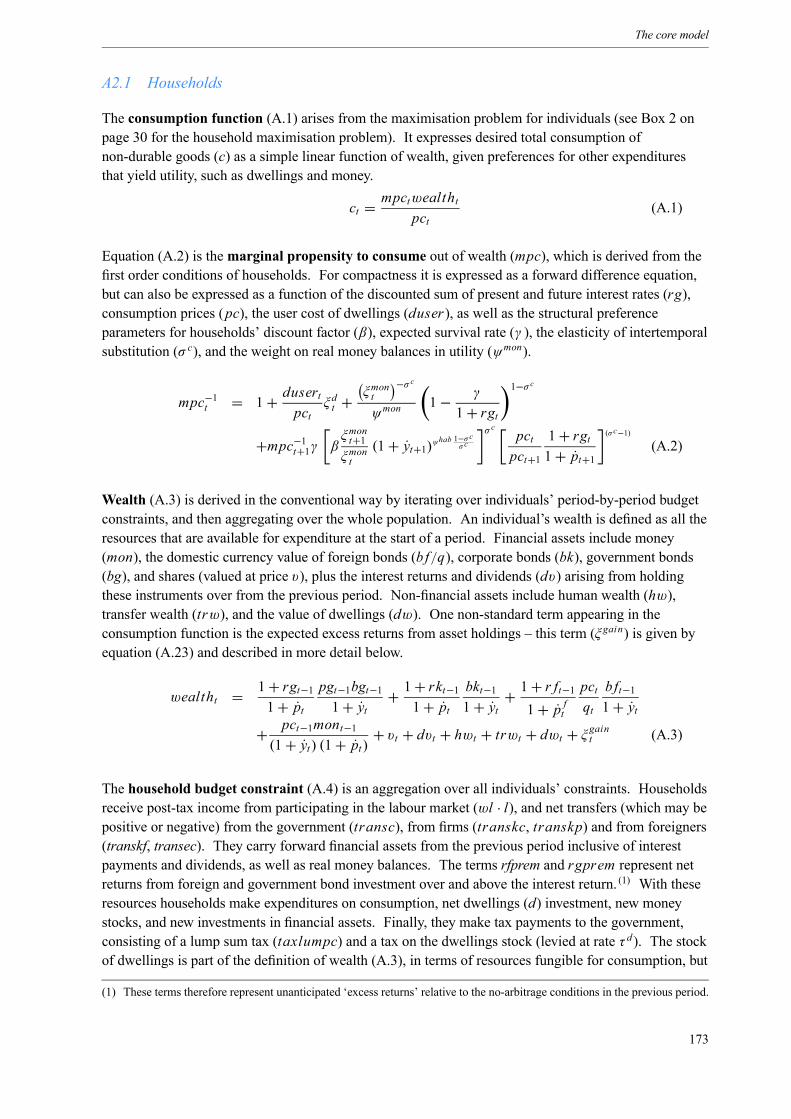

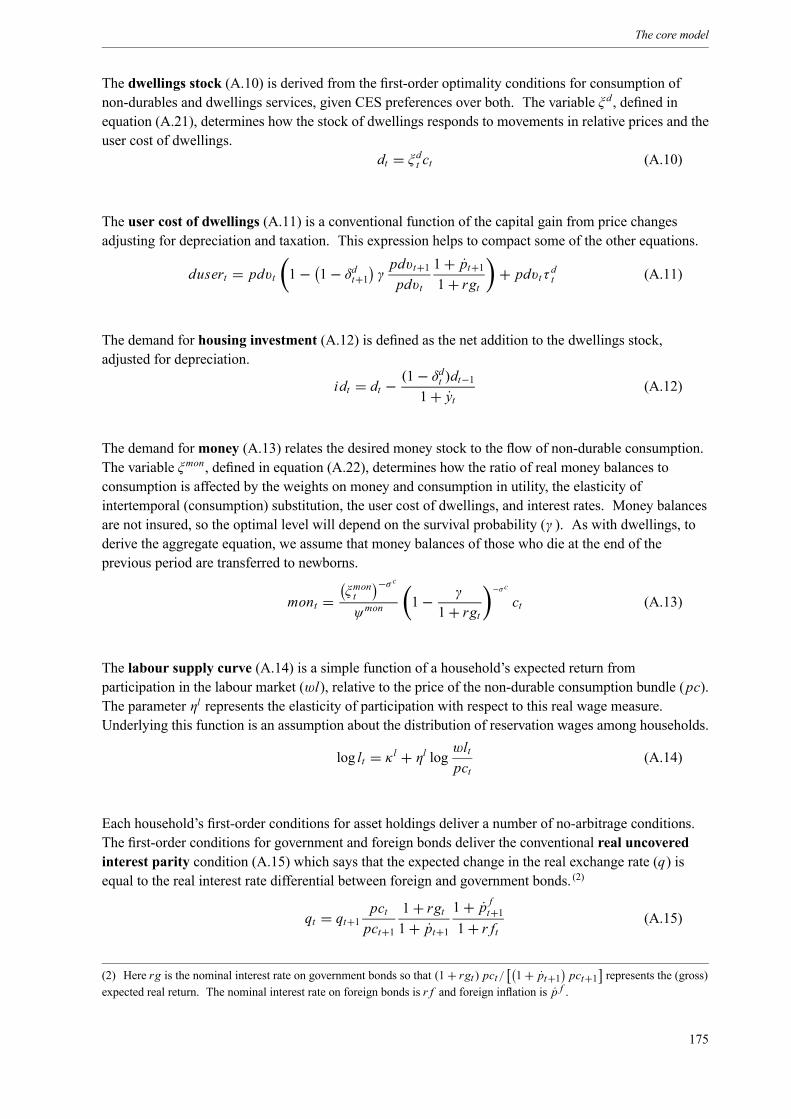

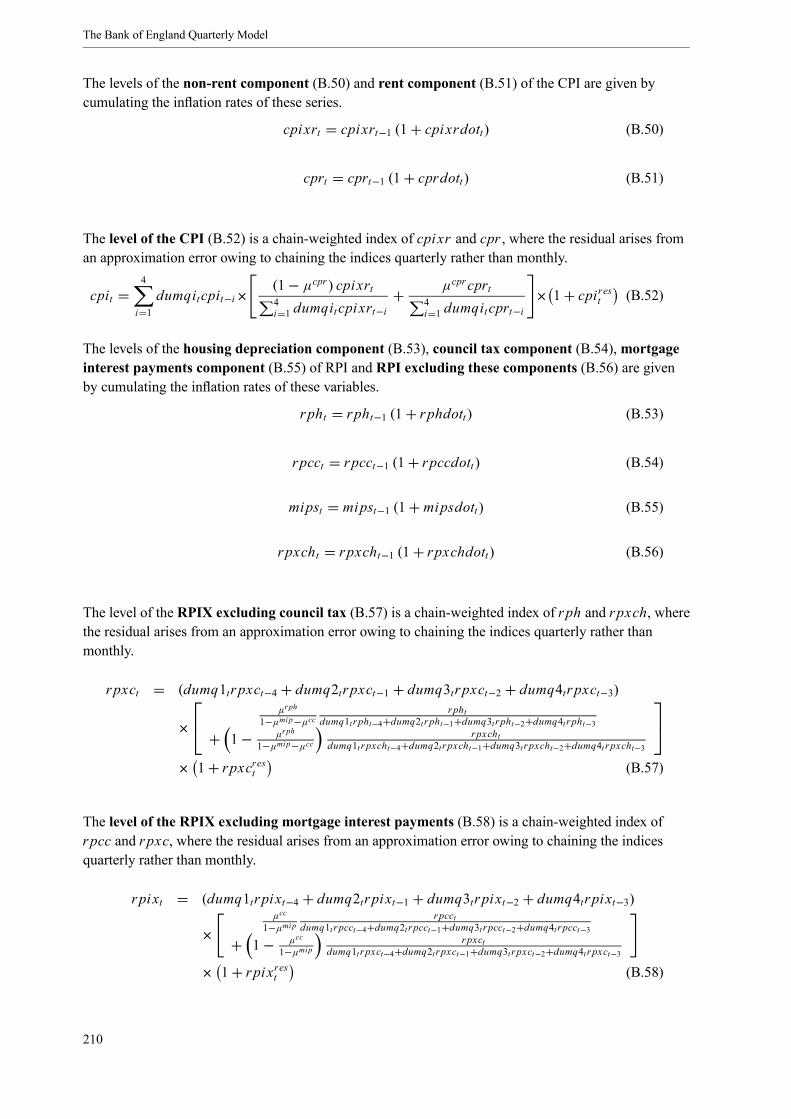

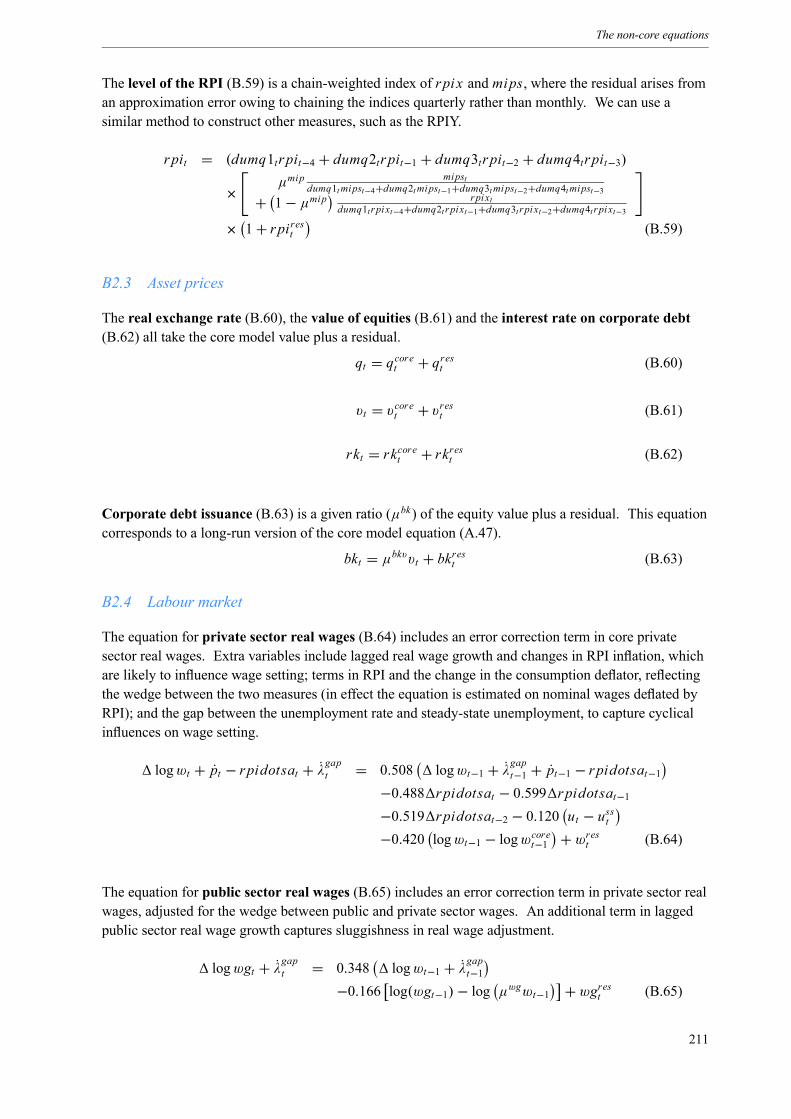

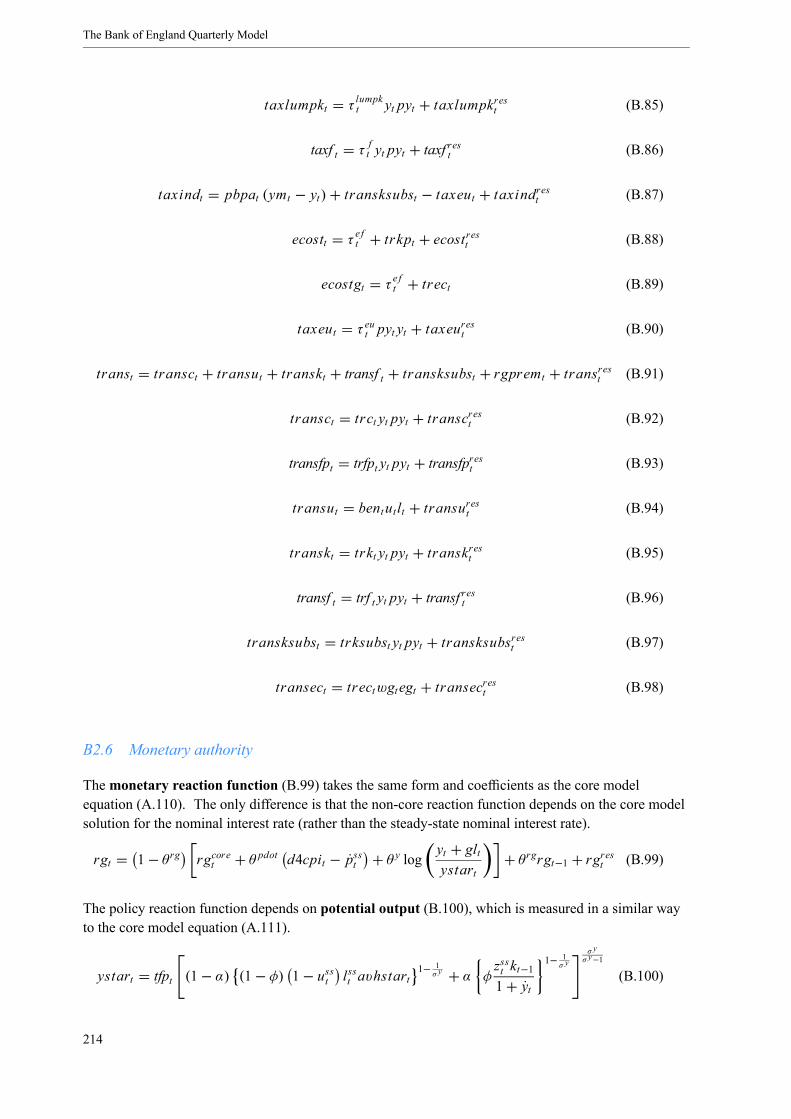

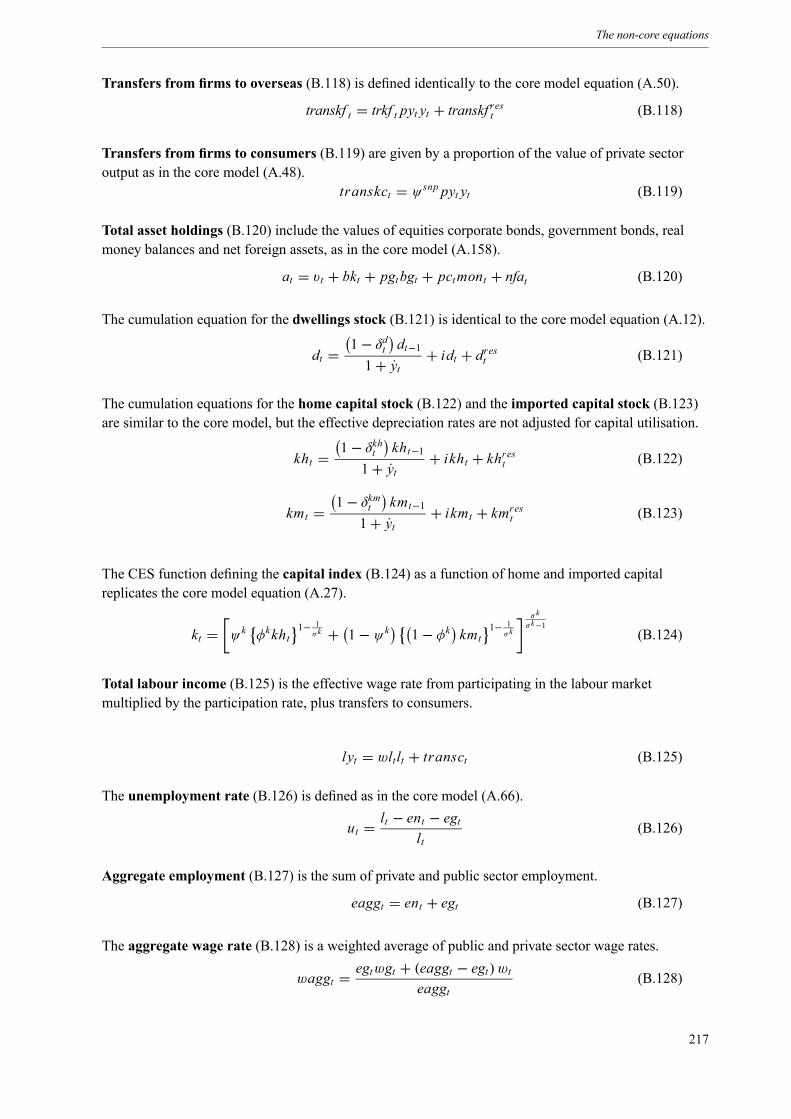

Embed Size (px)

Citation preview

The Bank of England Quarterly Model

Richard Harrison, Kalin Nikolov, Meghan Quinn, Gareth Ramsay,Alasdair Scott and Ryland Thomas

Further copies of this publication are available, at £10 plus p&p, from:

Publications GroupTelephone: 020 7601 4030email: [email protected]

The Bank of England’s website is at www.bankofengland.co.uk

A pdf file of this book and an ASCII file containing the model equations are available at:www.bankofengland.co.uk/publications/beqm/

Bank of England, Threadneedle Street, London, EC2R 8AH

c Bank of England 2005

ISBN 1 85730 153 6

Contents

Foreword 1

Acknowlegements 3

1 Introduction and overview 5

1.1 The role of models and forecasts at the Bank of England 5

1.2 An overview of BEQM 6

1.3 Some key technical features of BEQM 8

1.4 The structure of this book 9

1.5 Summary 10

2 Project motivation and model design 11

2.1 Motivations and challenges 11

2.2 The design of BEQM 12

2.3 A comparison with other models 15

2.4 Summary 18

3 The core theory 23

3.1 Overview 23

3.2 Characterisation of the agents 26

3.3 Characterisation of the markets 38

3.4 The nominal side of the economy and monetary transmission 44

3.5 Long-run growth 49

3.6 Summary 50

4 The core/non-core hybrid approach 61

4.1 Functional forms 62

4.2 Making the hybrid system work 63

4.3 Summary 67

5 Implementing and solving the model 69

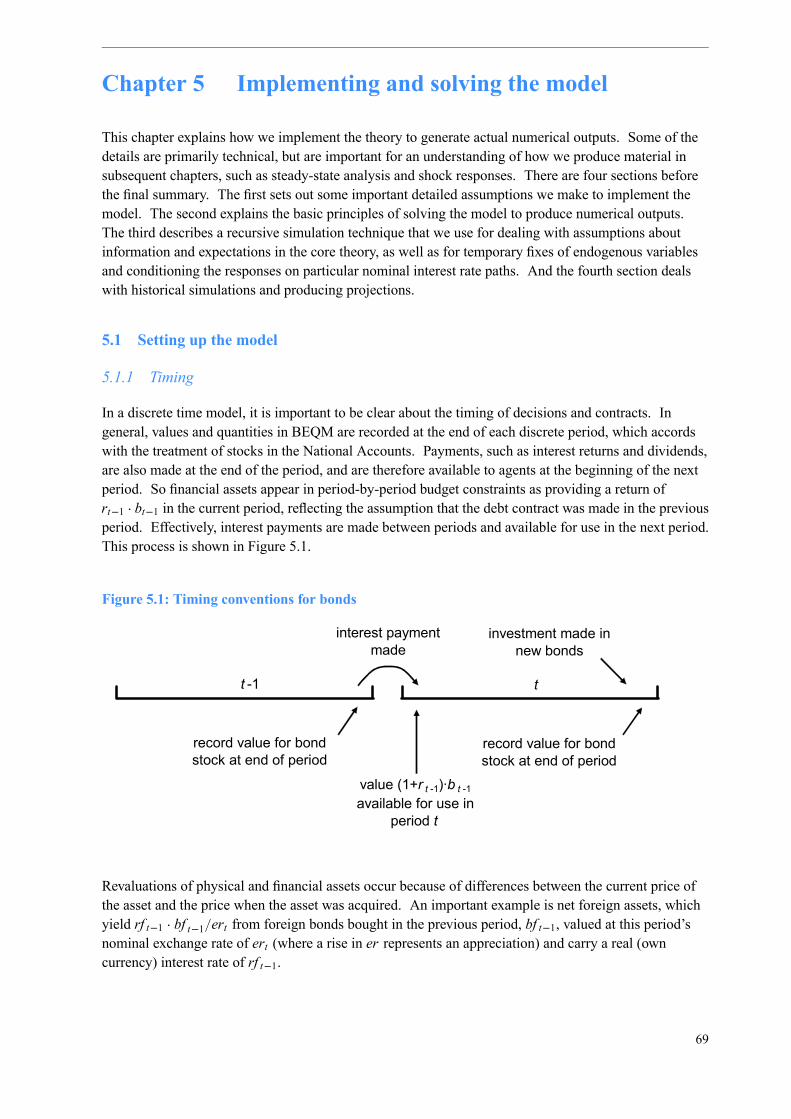

5.1 Setting up the model 69

5.2 Solving the model 74

5.3 Recursive simulations 75

5.4 Applications 79

5.5 Summary 83

i

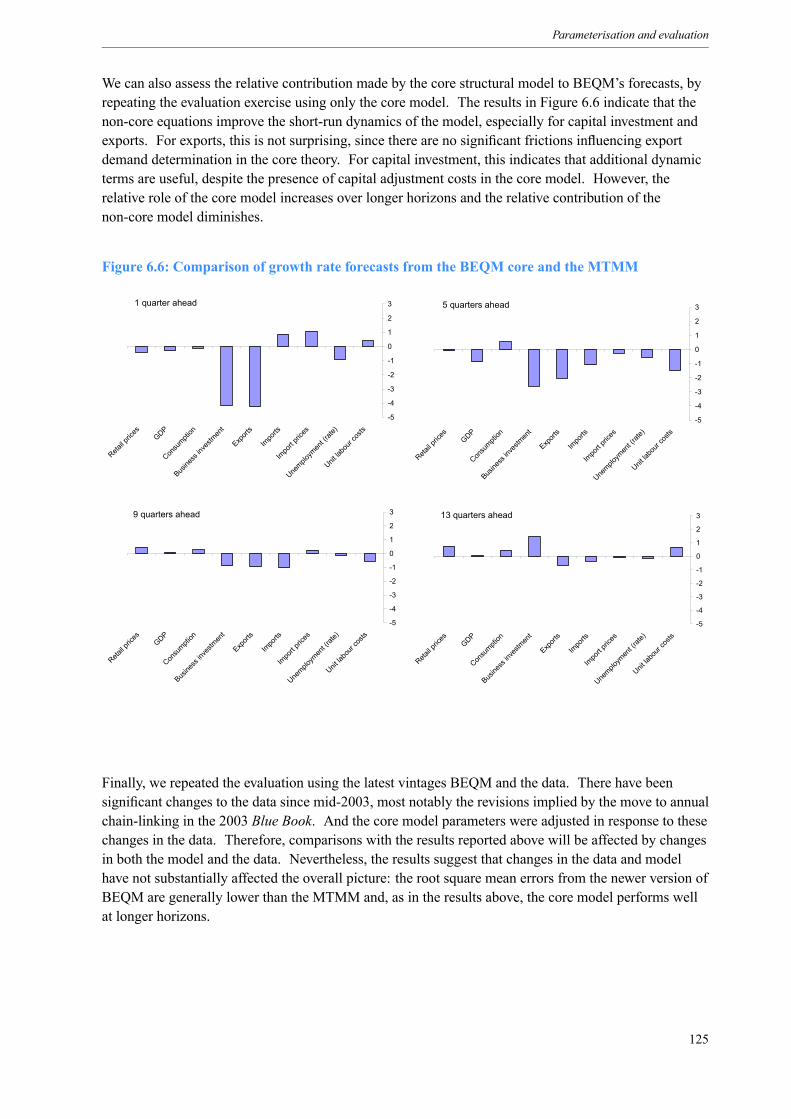

6 Parameterisation and evaluation 85

6.1 Issues in parameterising the core model 85

6.2 The model-consistent database 86

6.3 Parameterising the structural core model 97

6.4 Parameterising the non-core equations 113

6.5 An evaluation of the model’s forecast performance 121

6.6 Summary 126

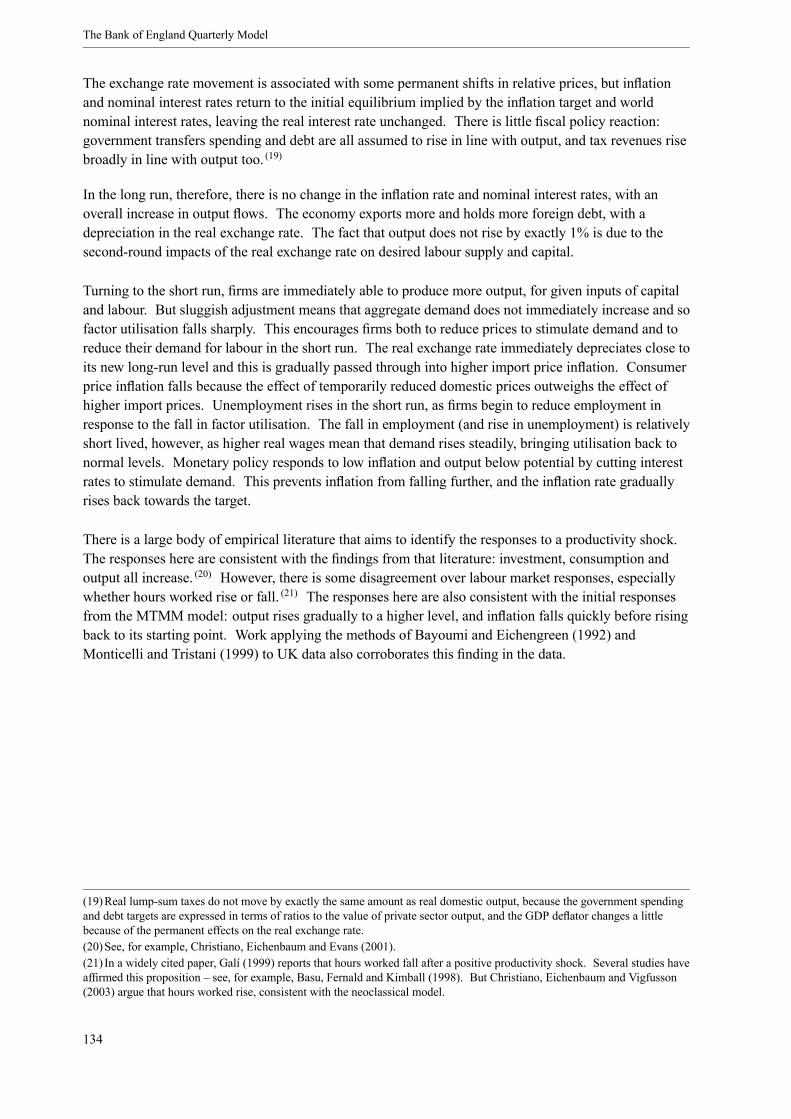

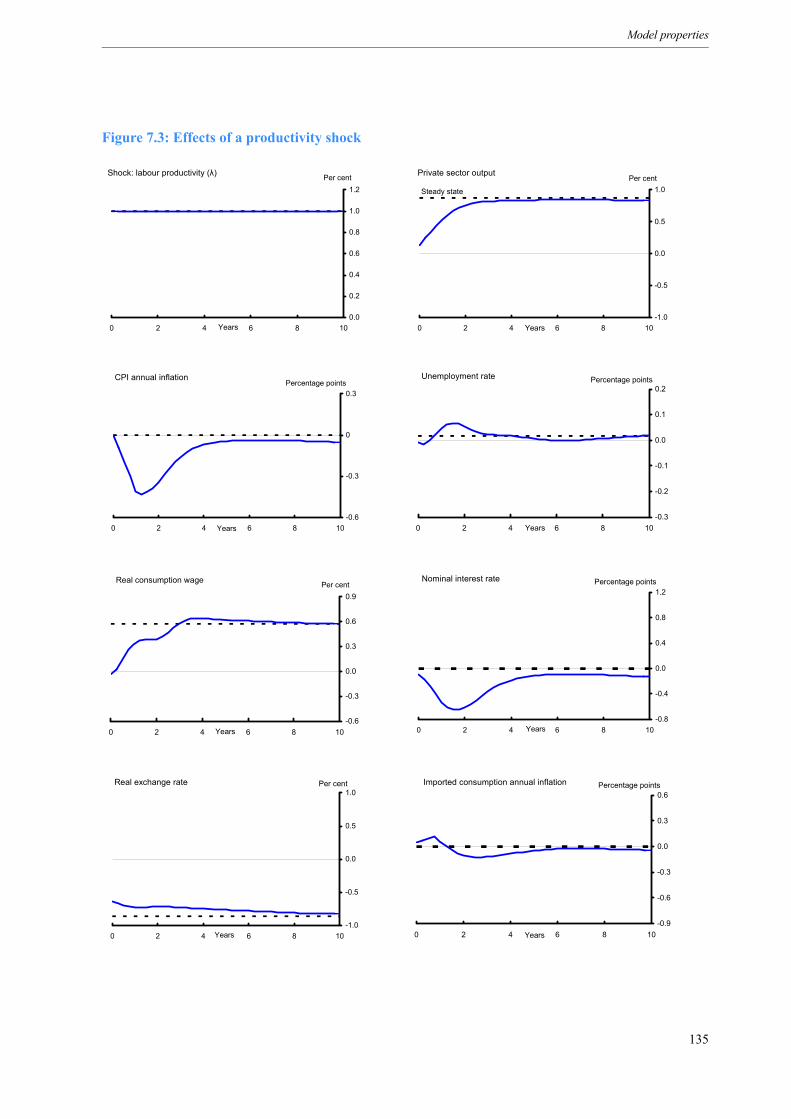

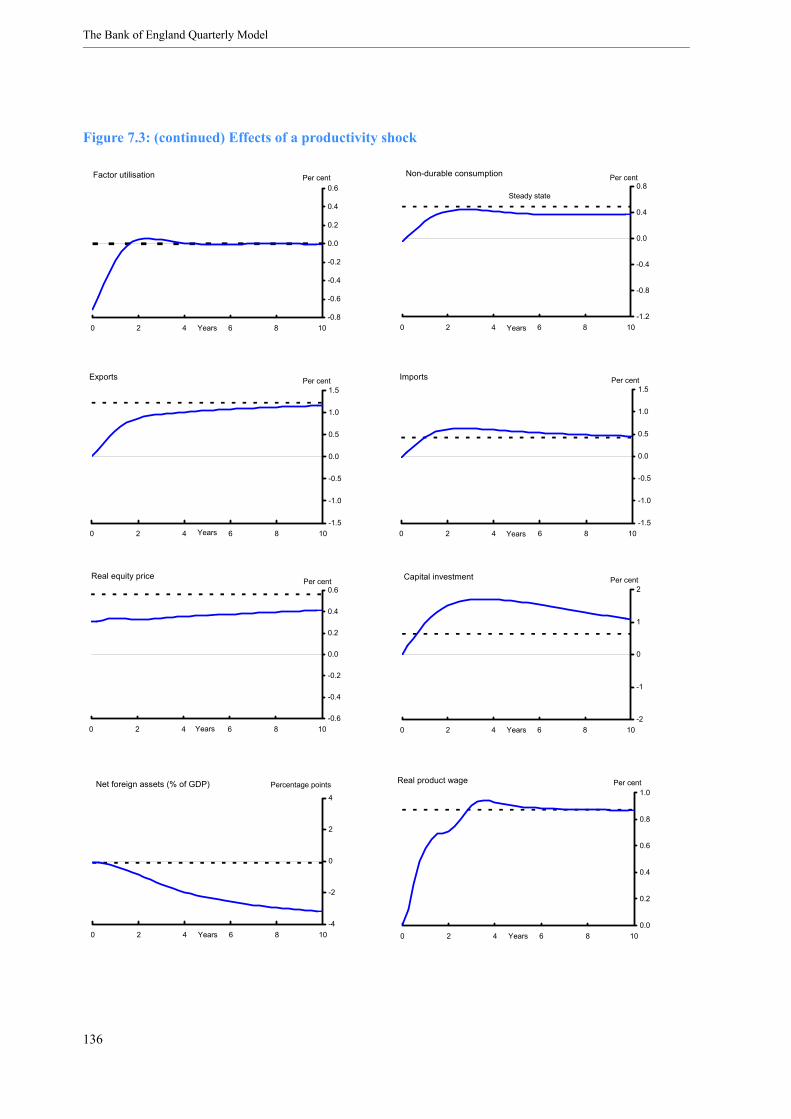

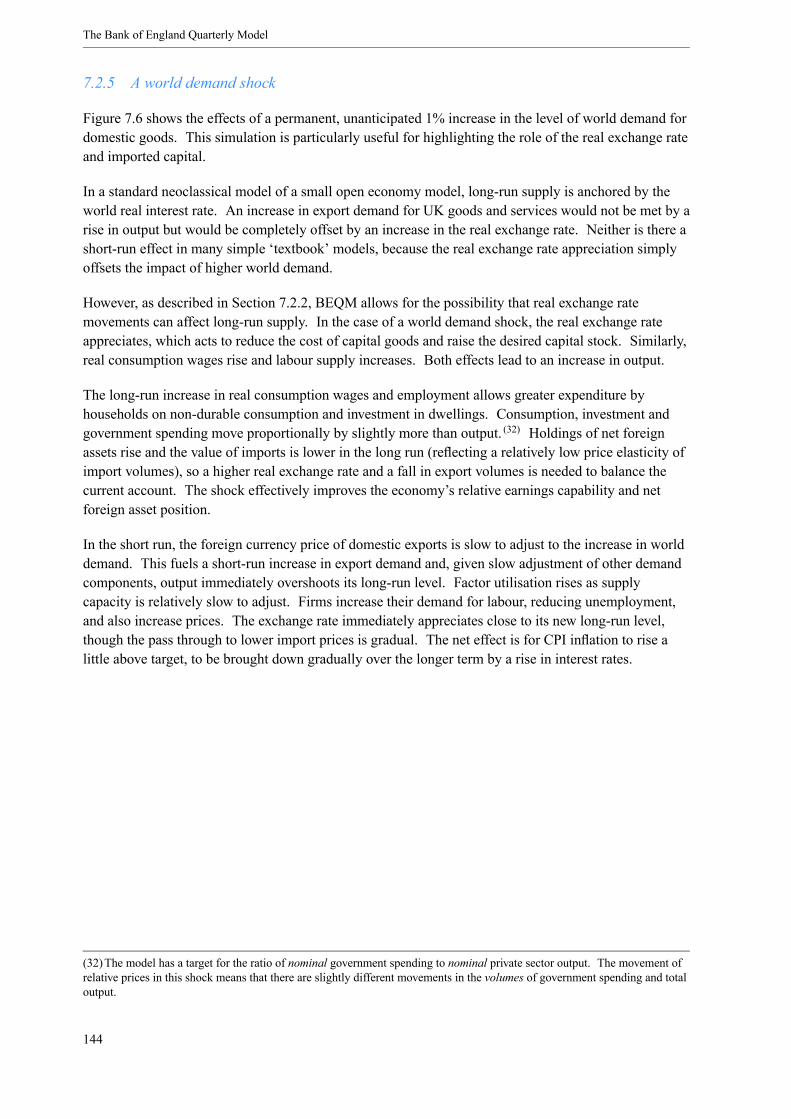

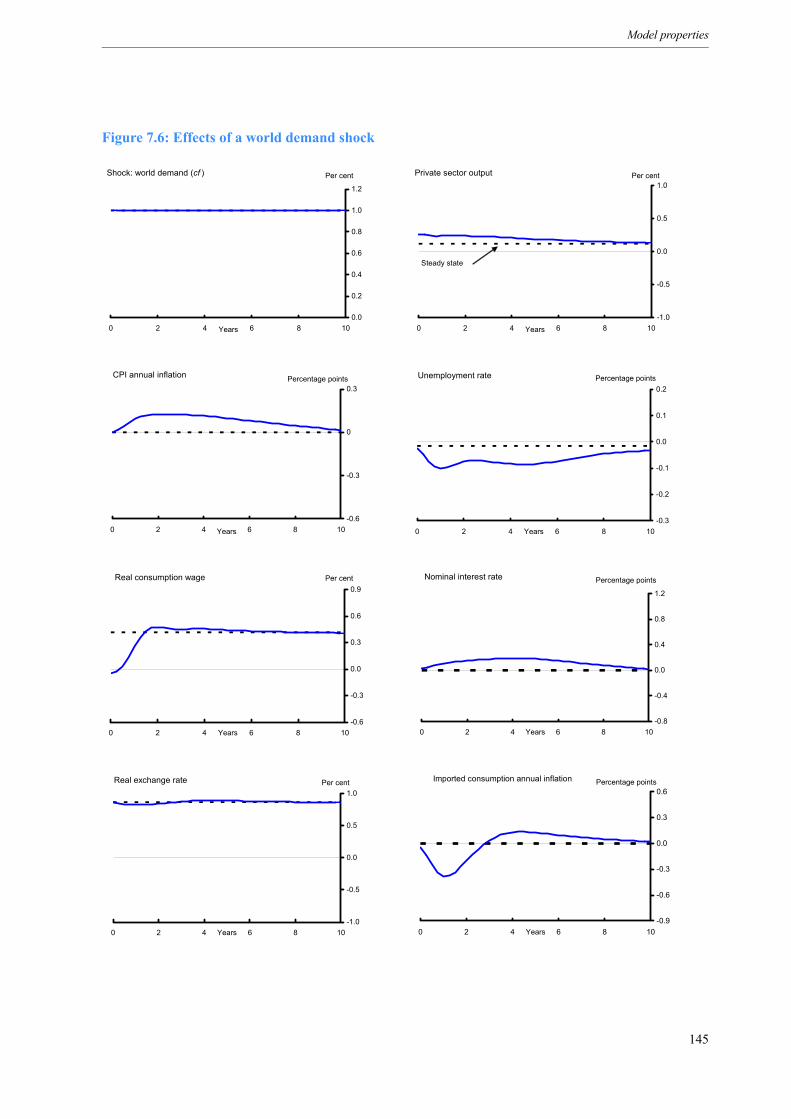

7 Model properties 127

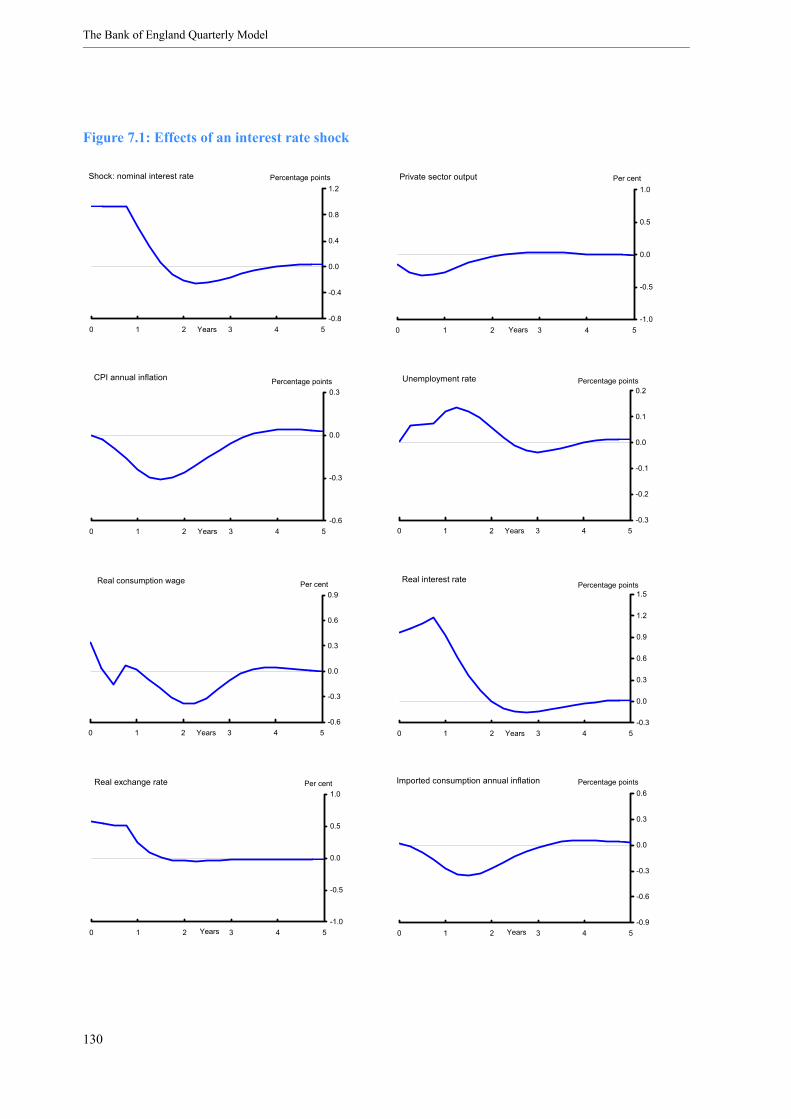

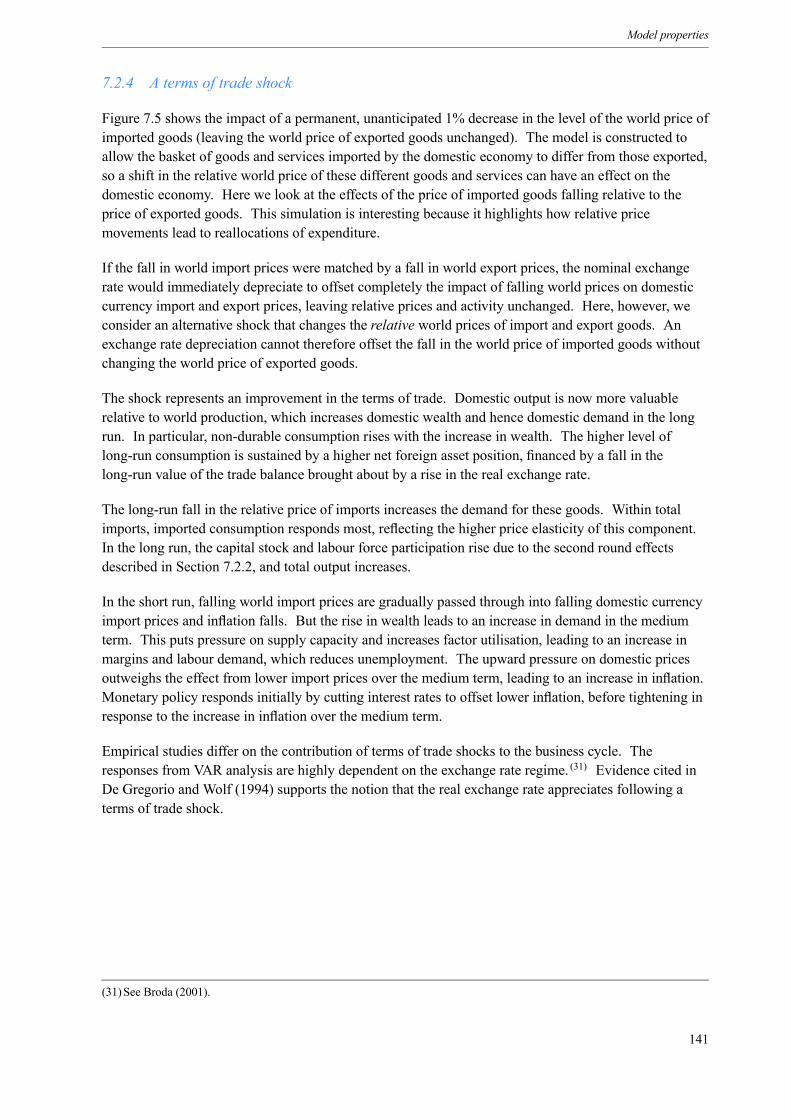

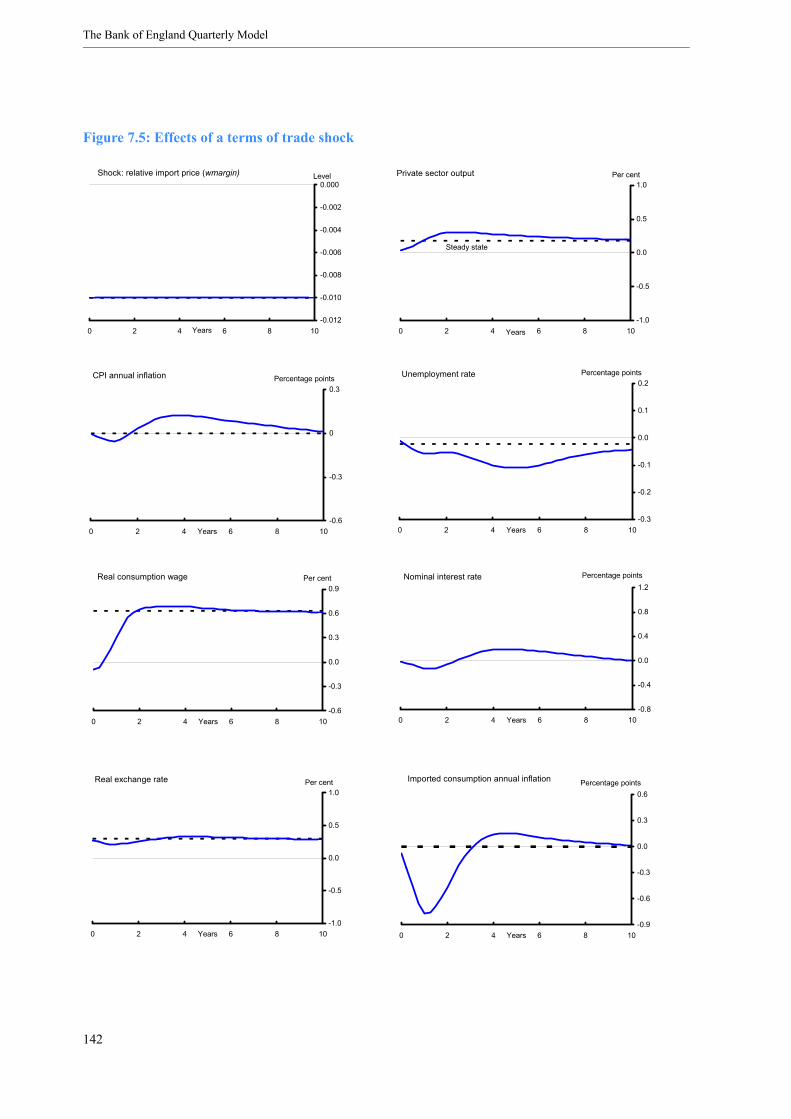

7.1 Interpreting the responses 127

7.2 Shock responses 128

7.3 Summary 150

8 Final remarks 151

References 153

Appendices

A The core model 165

A.1 Mnemonics 165

A.2 Core model equations 172

B The non-core equations 197

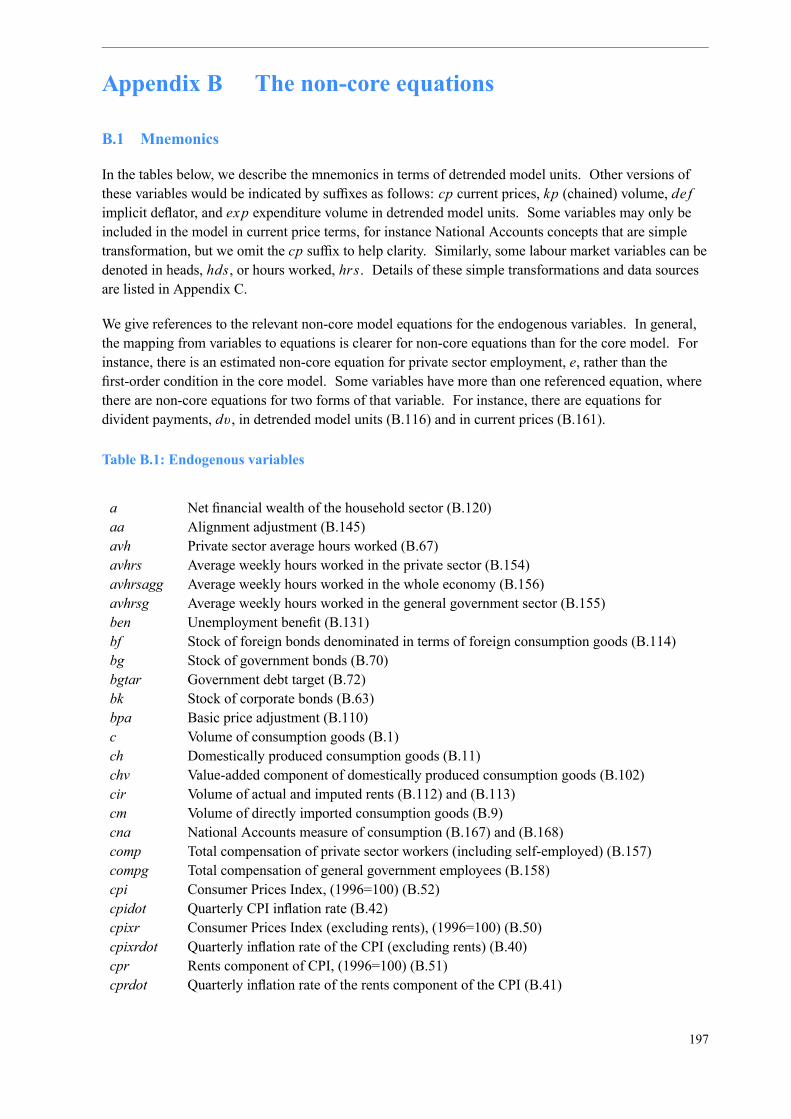

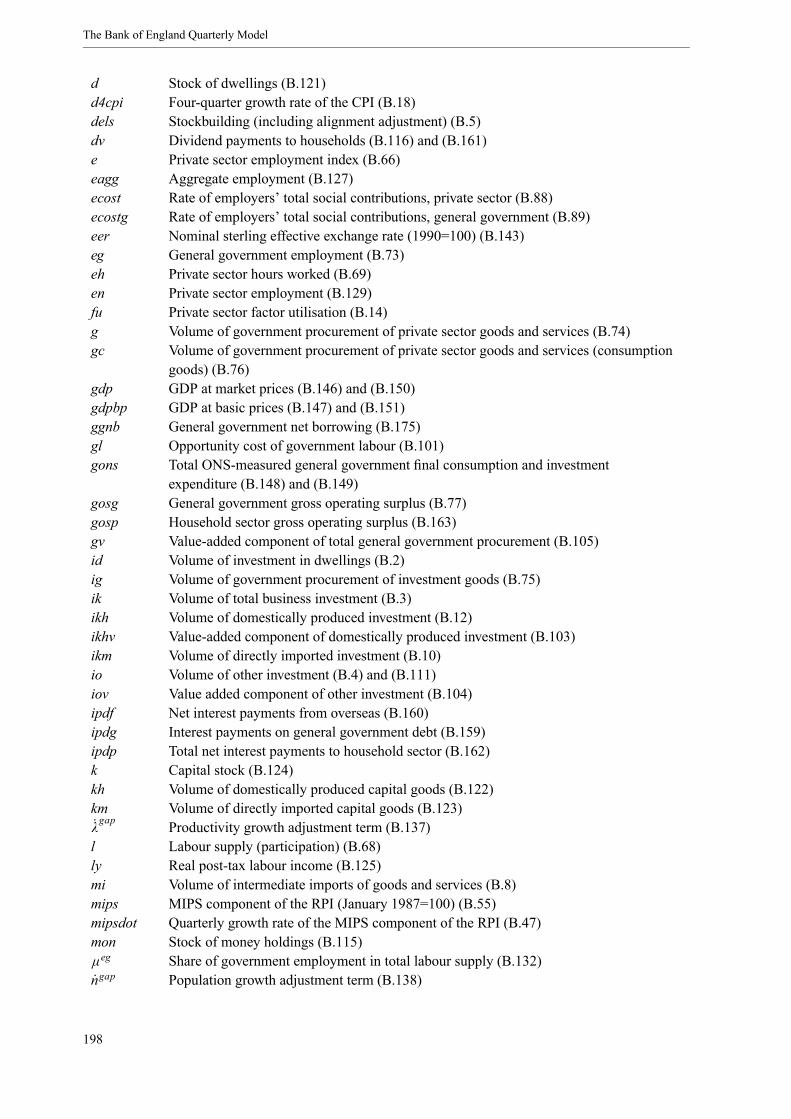

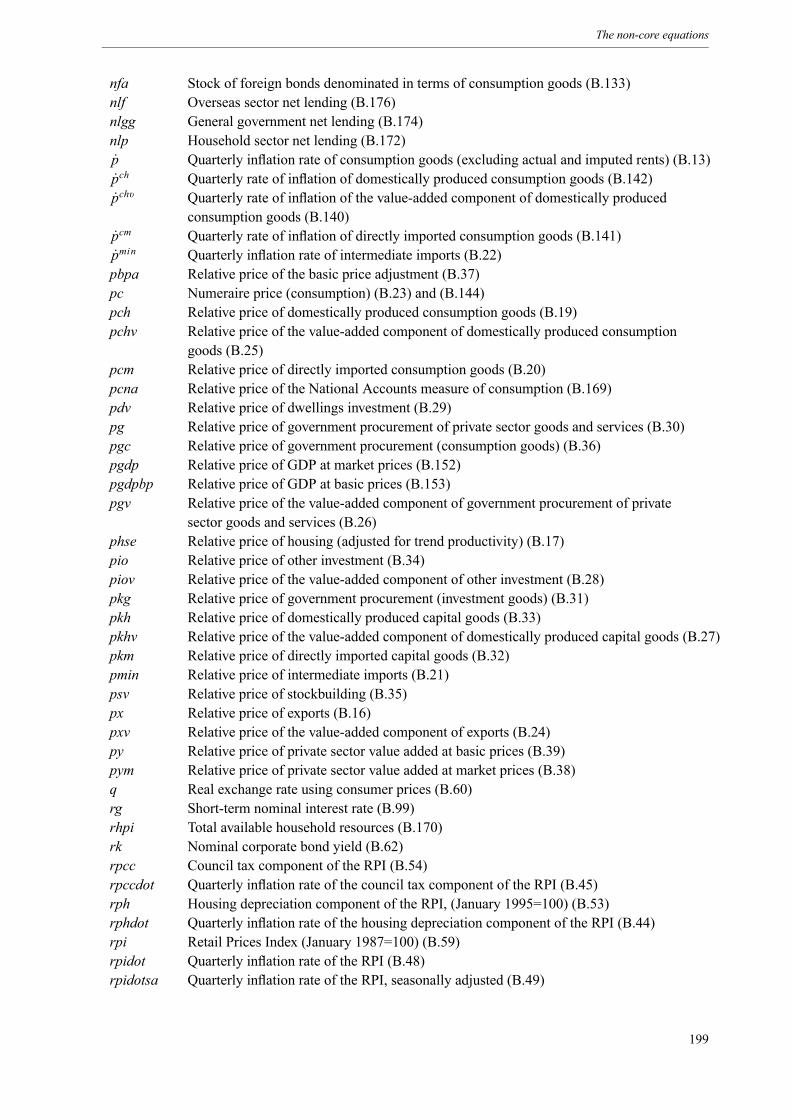

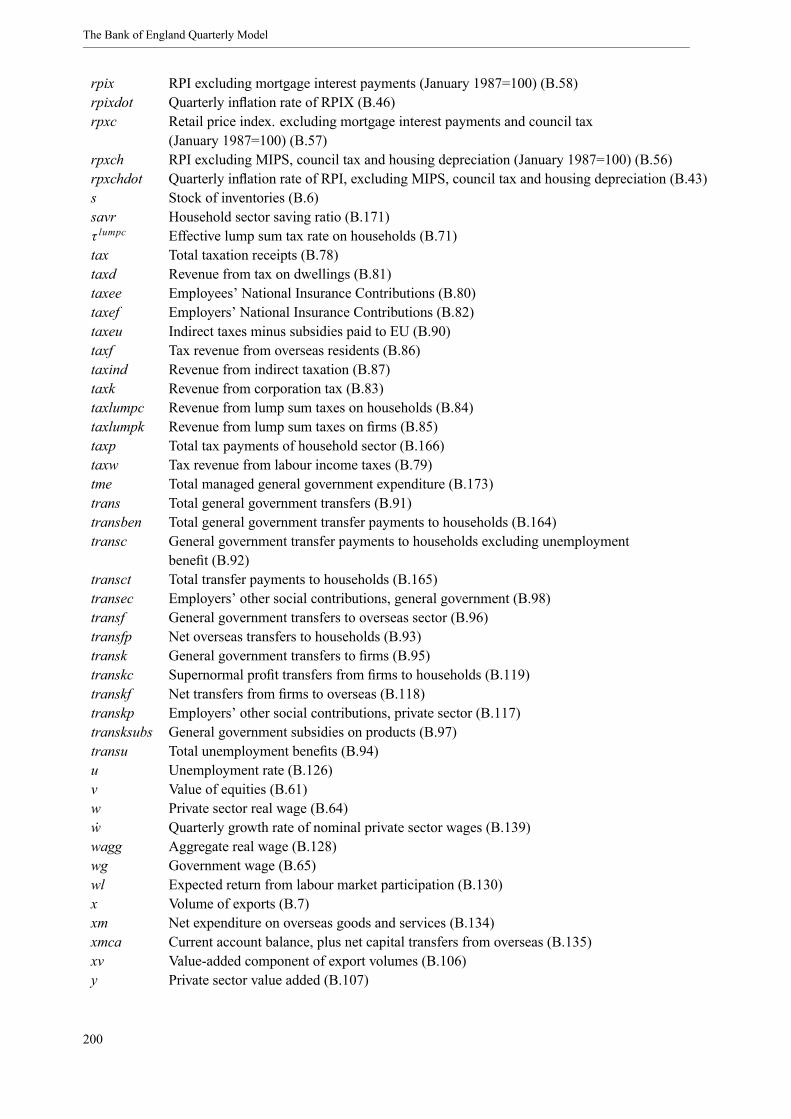

B.1 Mnemonics 197

B.2 Non-core equations 203

C Data transformations and sources 225

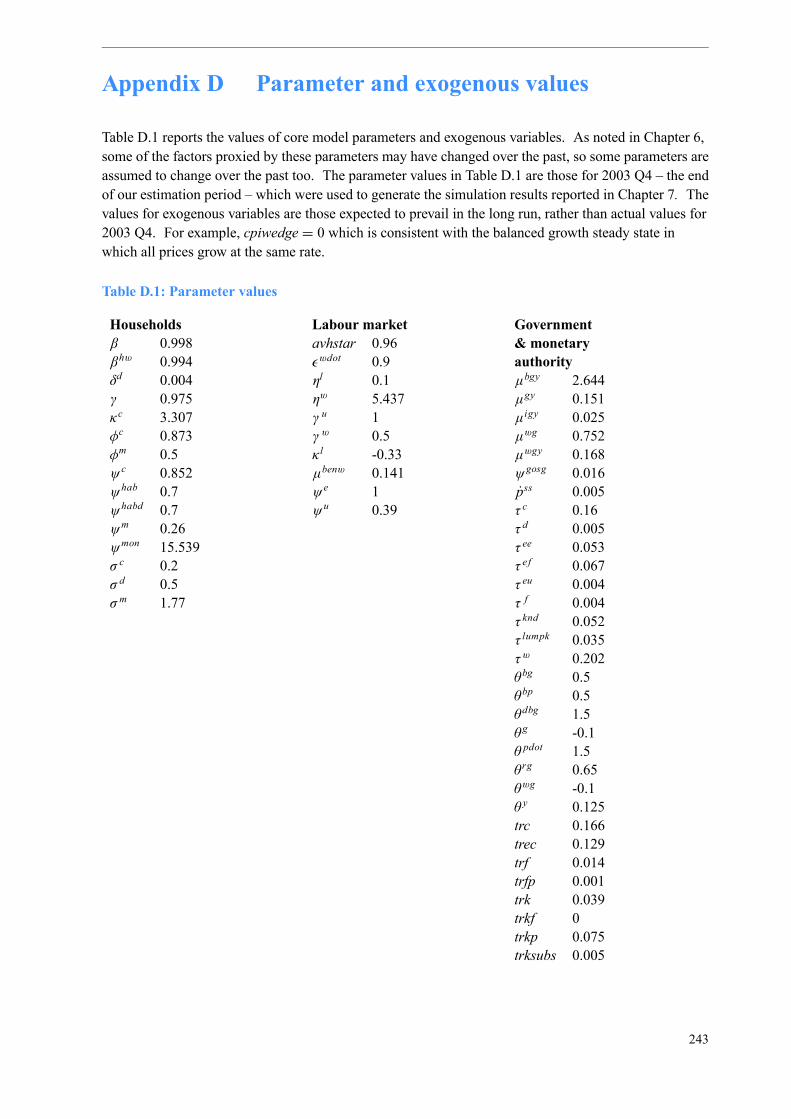

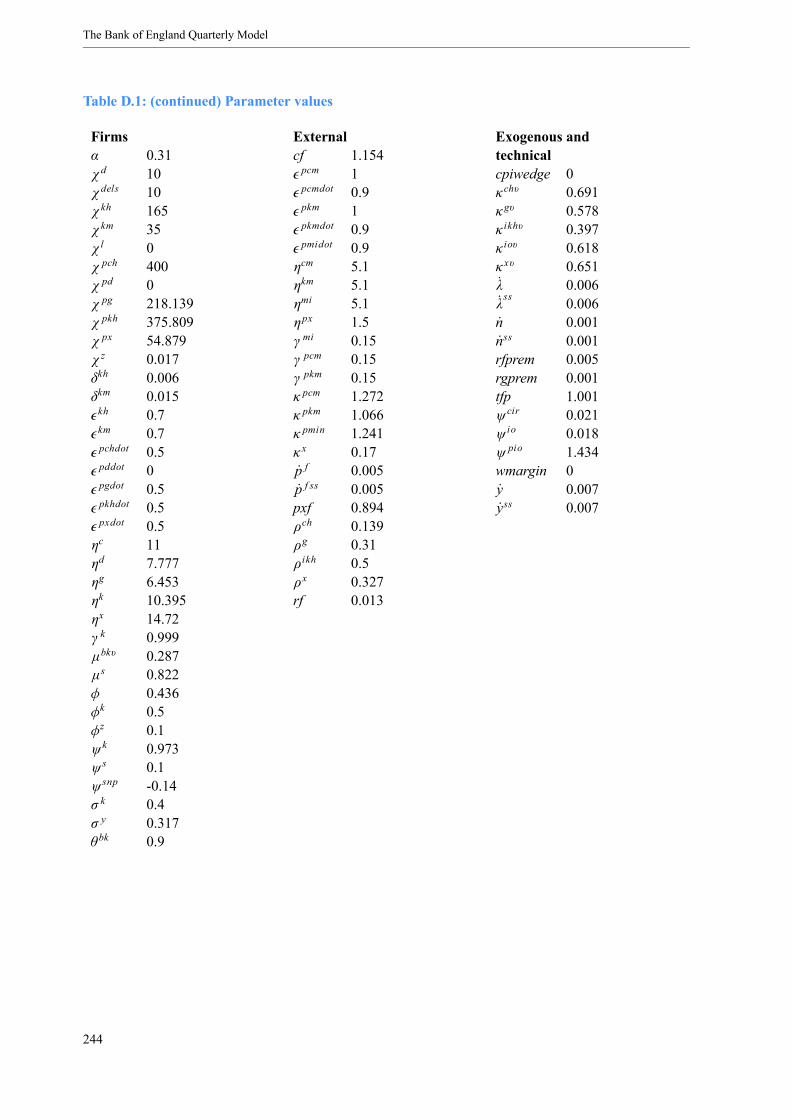

D Parameter and exogenous values 243

ii

List of figures

2.1 The trade-off between theory and data 12

2.2 A stylised forecast sequence 15

3.1 Key agents in the model macroeconomy 24

3.2 Key flows and assets 25

3.3 Consumption equilibrium in the steady state 27

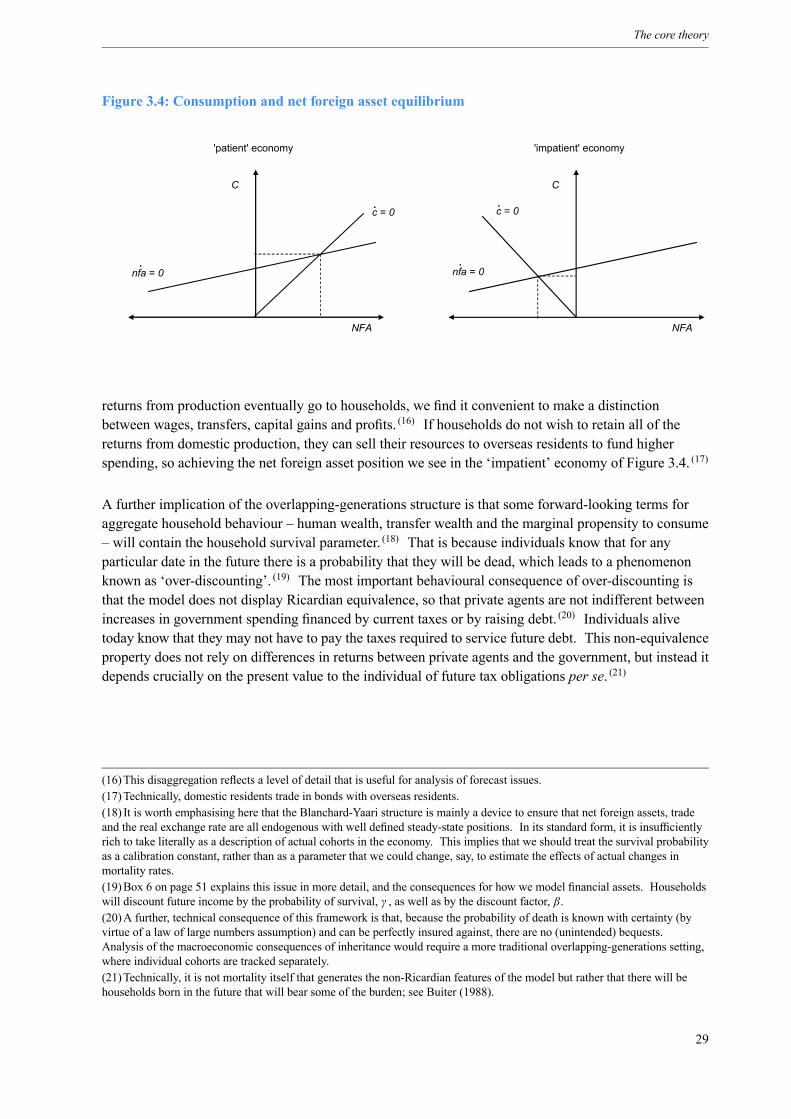

3.4 Consumption and net foreign asset equilibrium 29

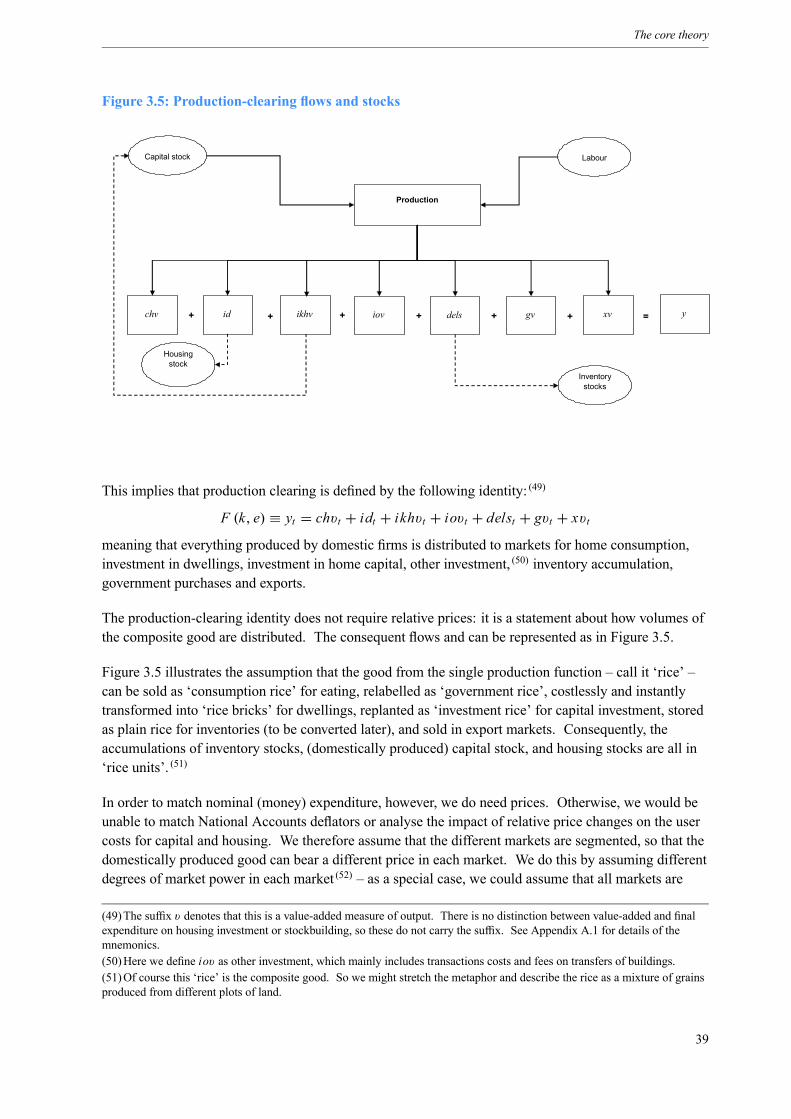

3.5 Production-clearing flows and stocks 39

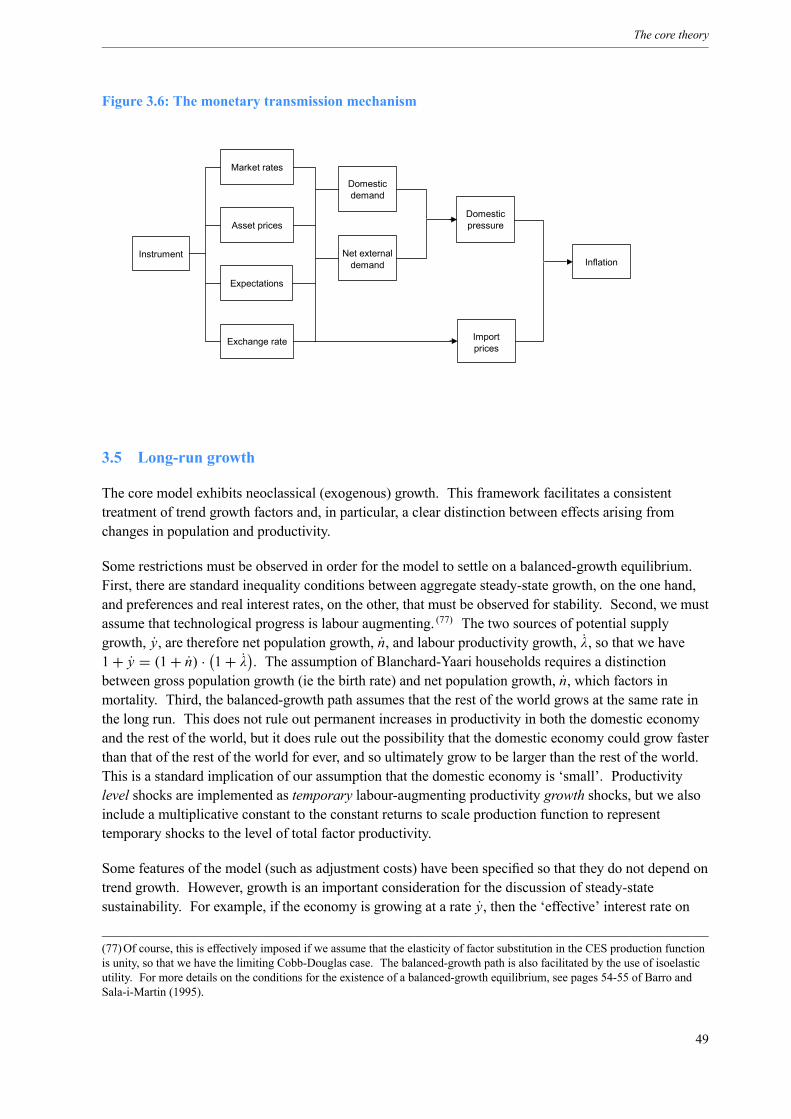

3.6 The monetary transmission mechanism 49

5.1 Timing conventions for bonds 69

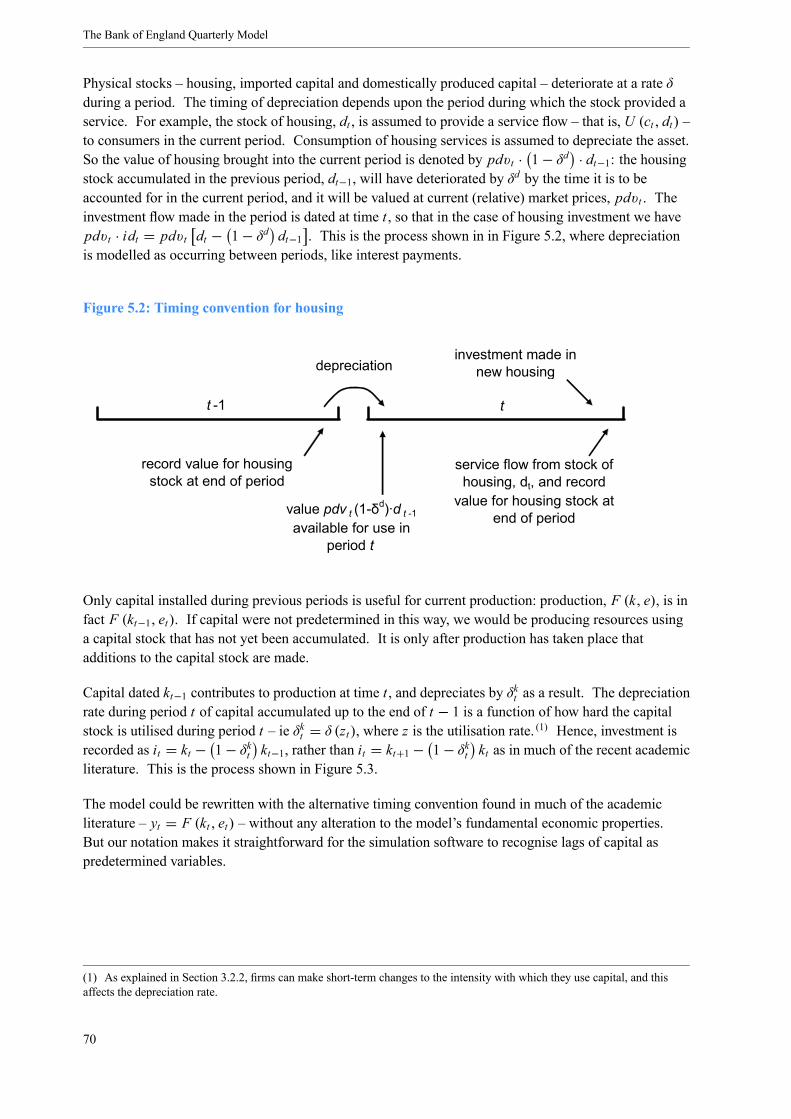

5.2 Timing convention for housing 70

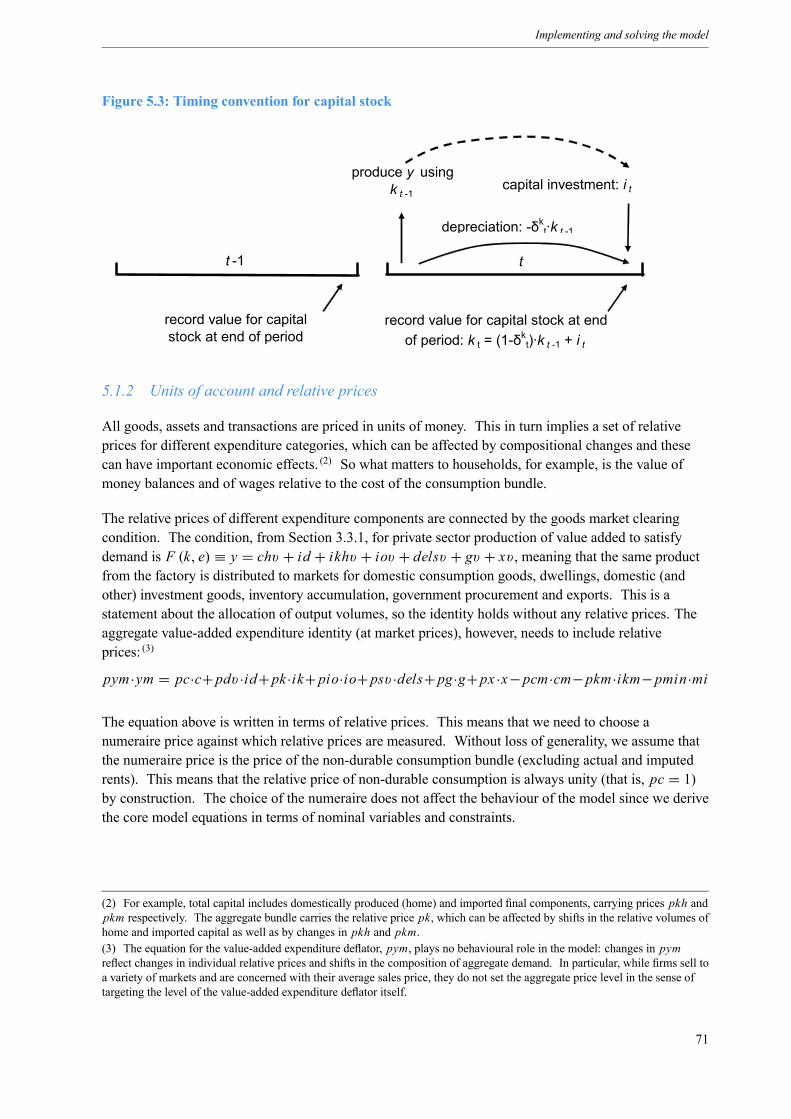

5.3 Timing convention for capital stock 71

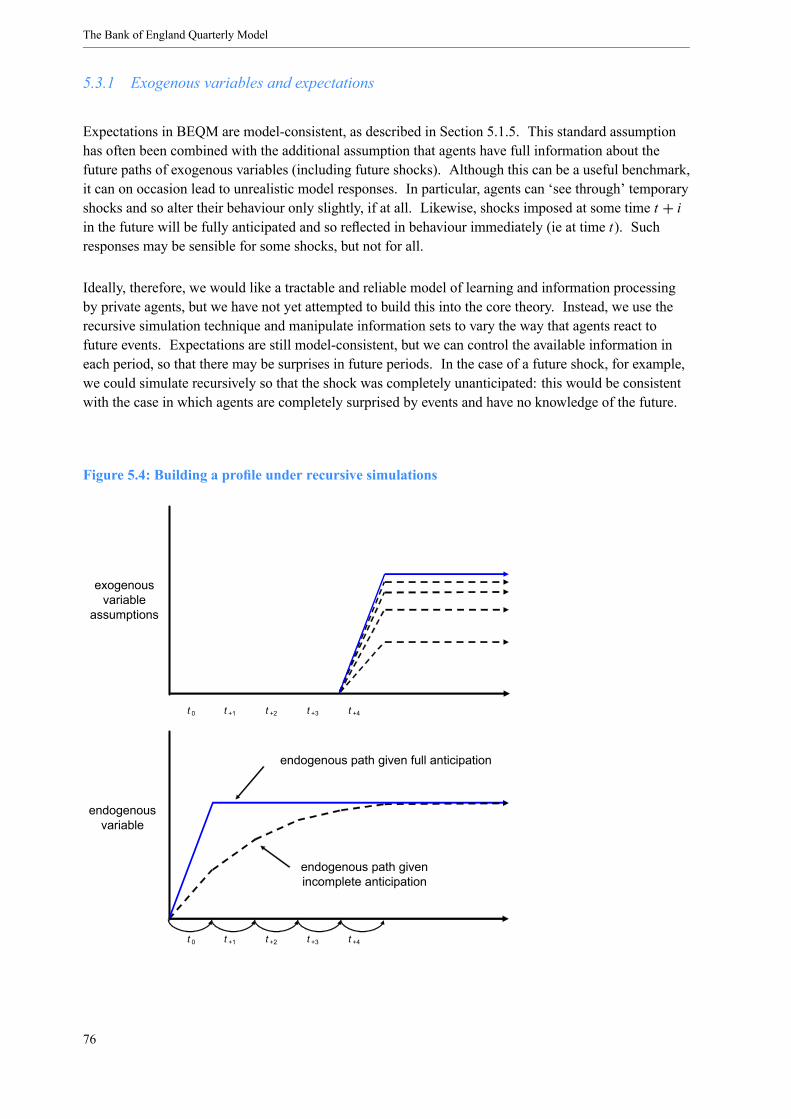

5.4 Building a profile under recursive simulations 76

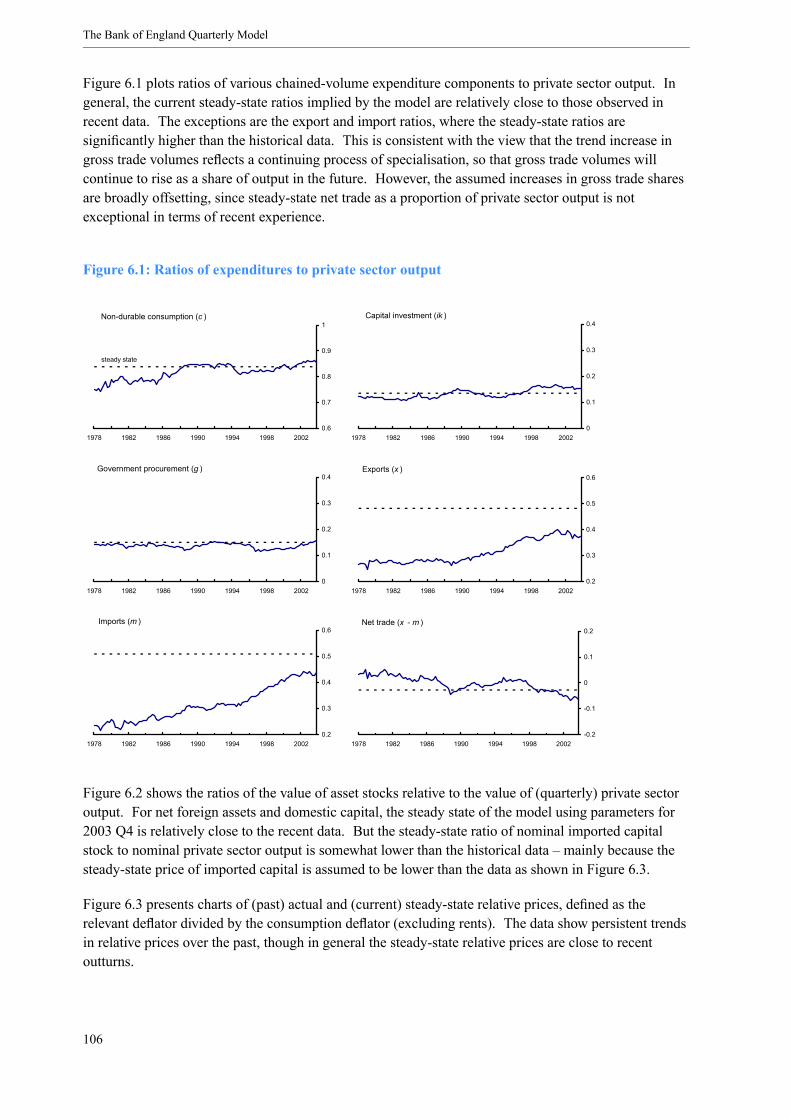

6.1 Ratios of expenditures to private sector output 106

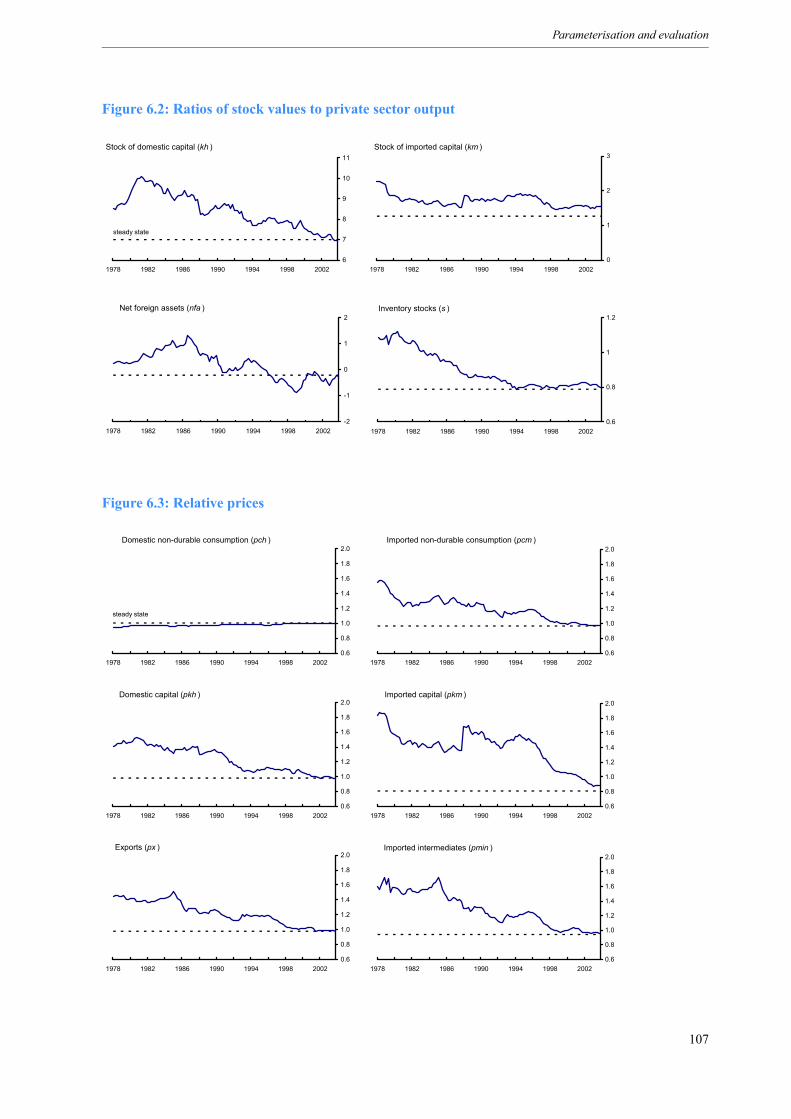

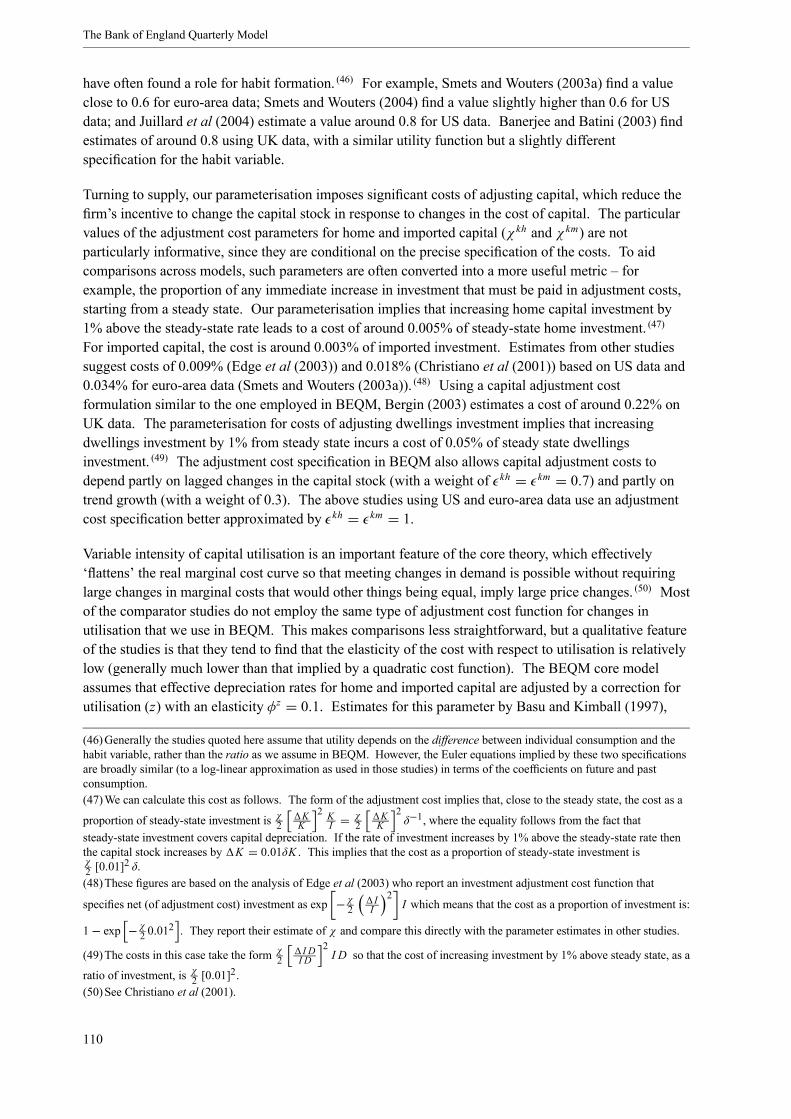

6.2 Ratios of stock values to private sector output 107

6.3 Relative prices 107

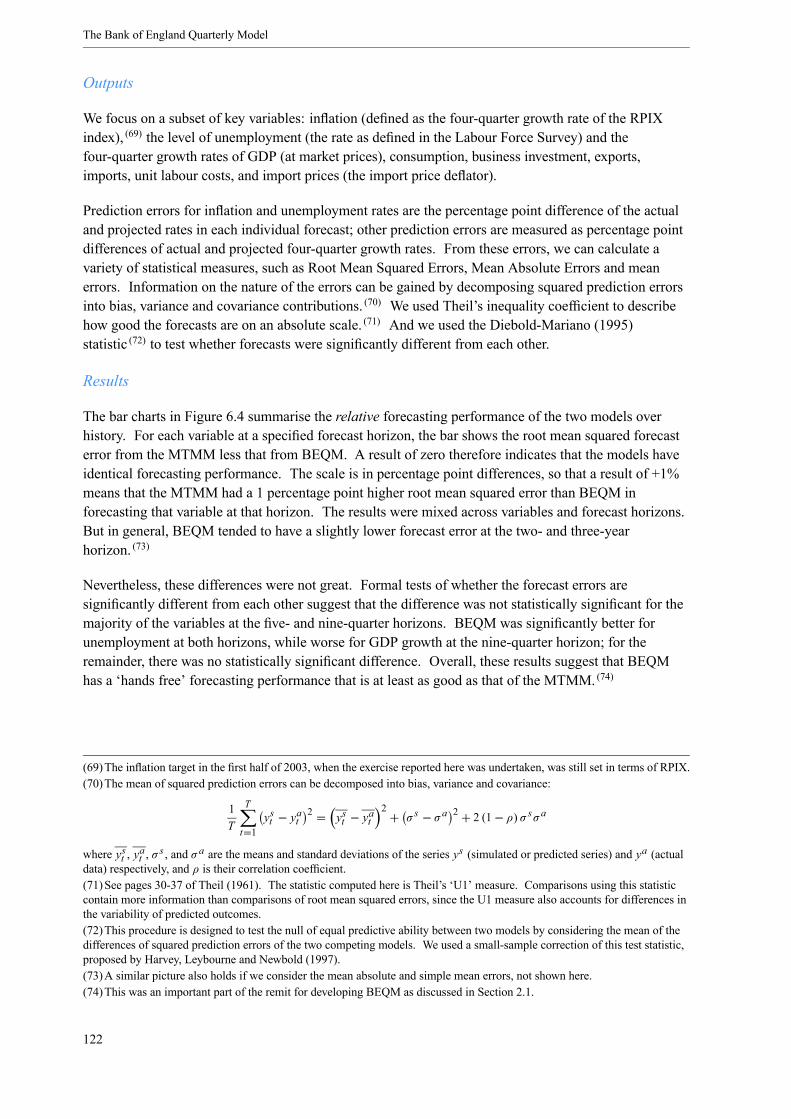

6.4 Comparison of growth rate forecasts from BEQM and the MTMM 123

6.5 Theil inequality coefficients 124

6.6 Comparison of growth rate forecasts from the BEQM core and the MTMM 125

7.1 Effects of an interest rate shock 130

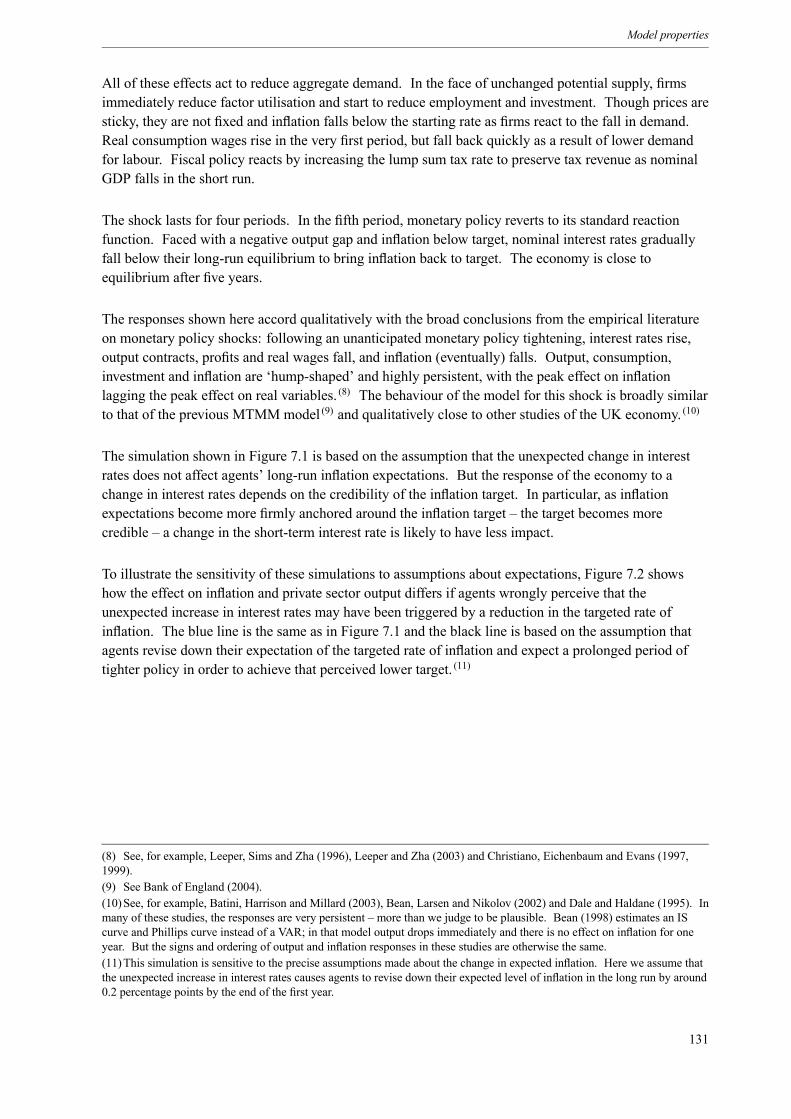

7.2 How expectations can affect shock responses 132

7.3 Effects of a productivity shock 135

7.4 Effects of a government spending shock 139

7.5 Effects of a terms of trade shock 142

7.6 Effects of a world demand shock 145

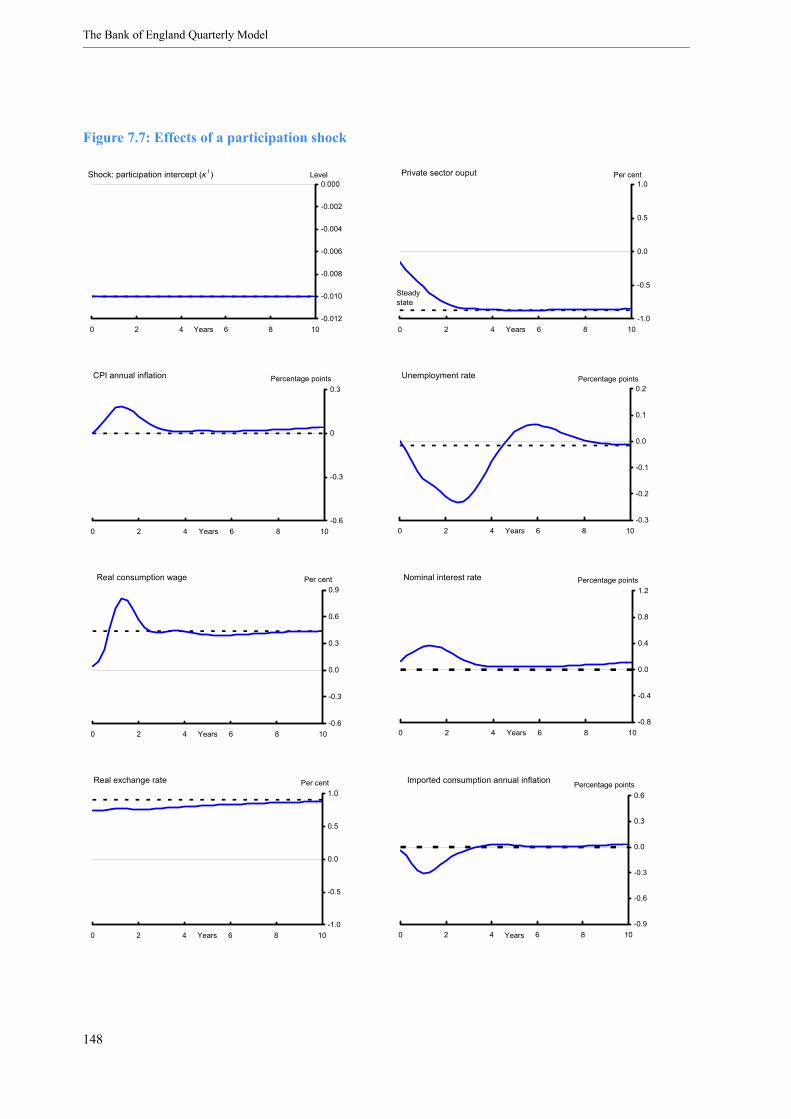

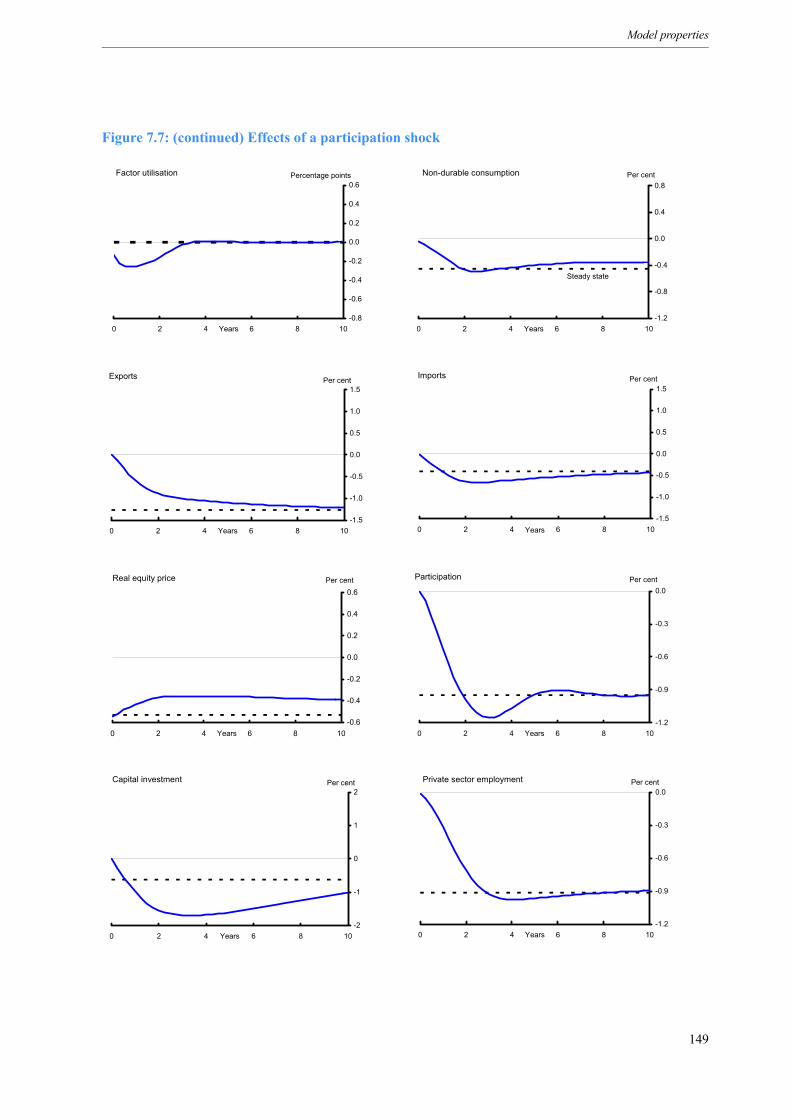

7.7 Effects of a participation shock 148

iii

List of tables

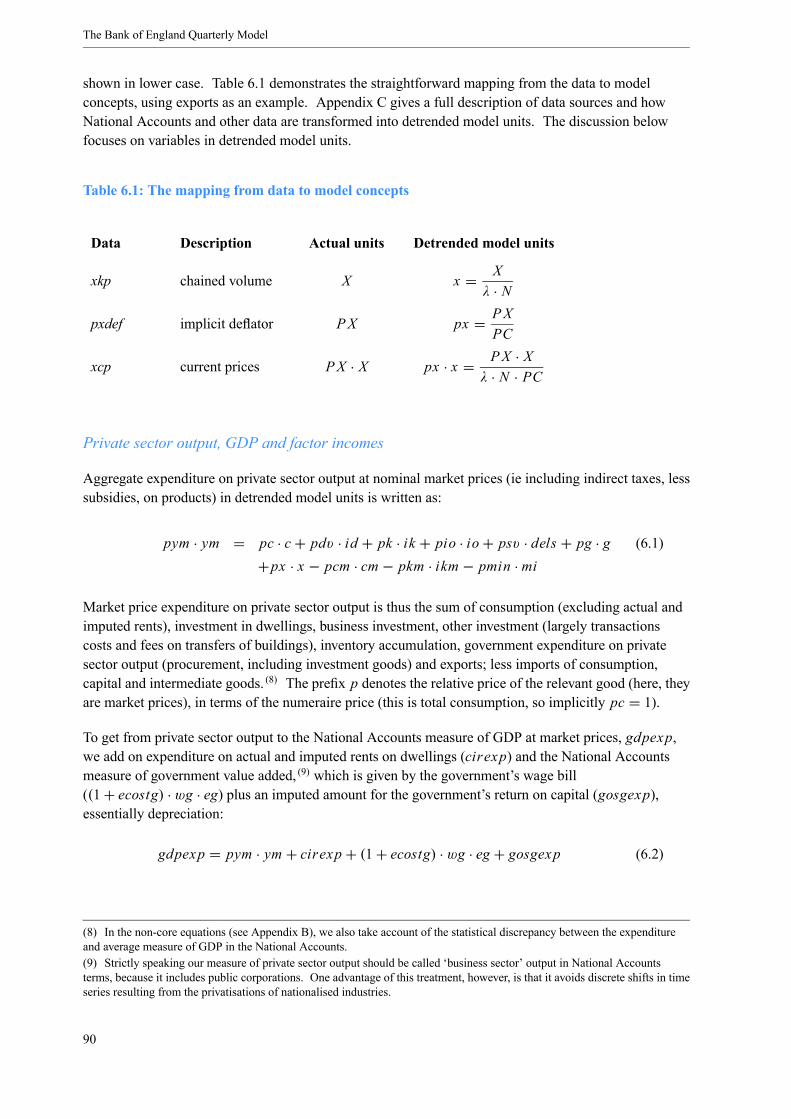

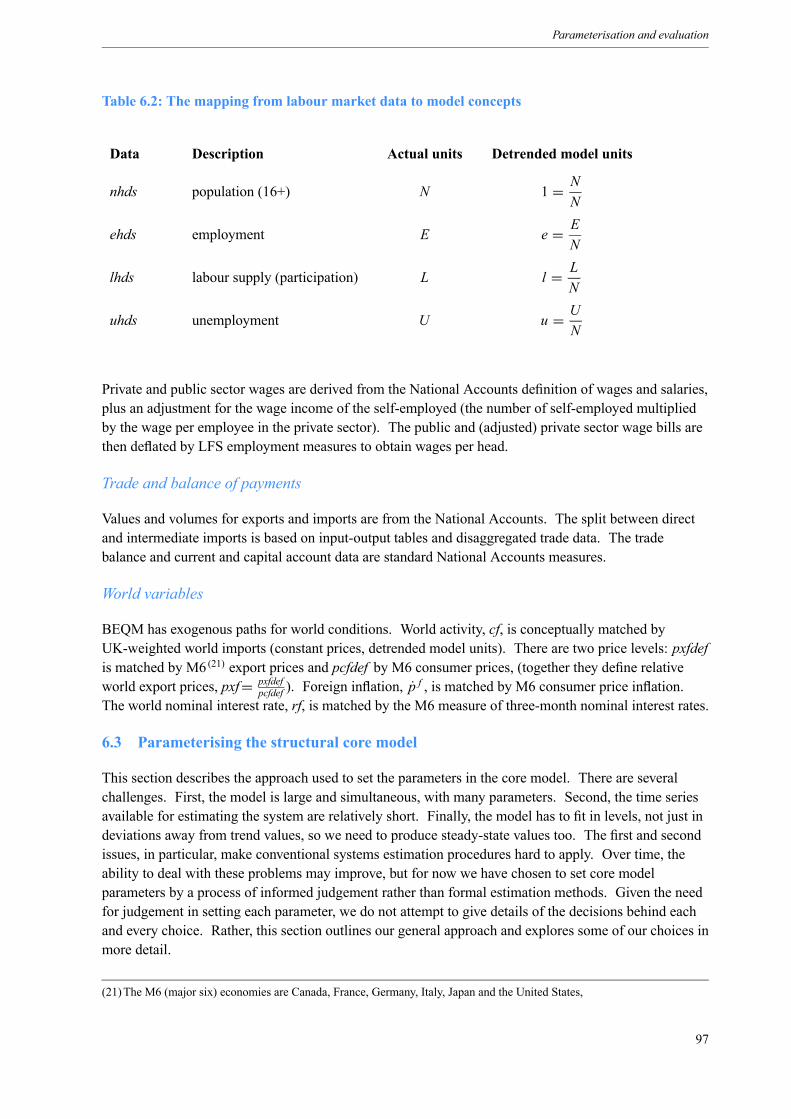

6.1 The mapping from data to model concepts 90

6.2 The mapping from labour market data to model concepts 97

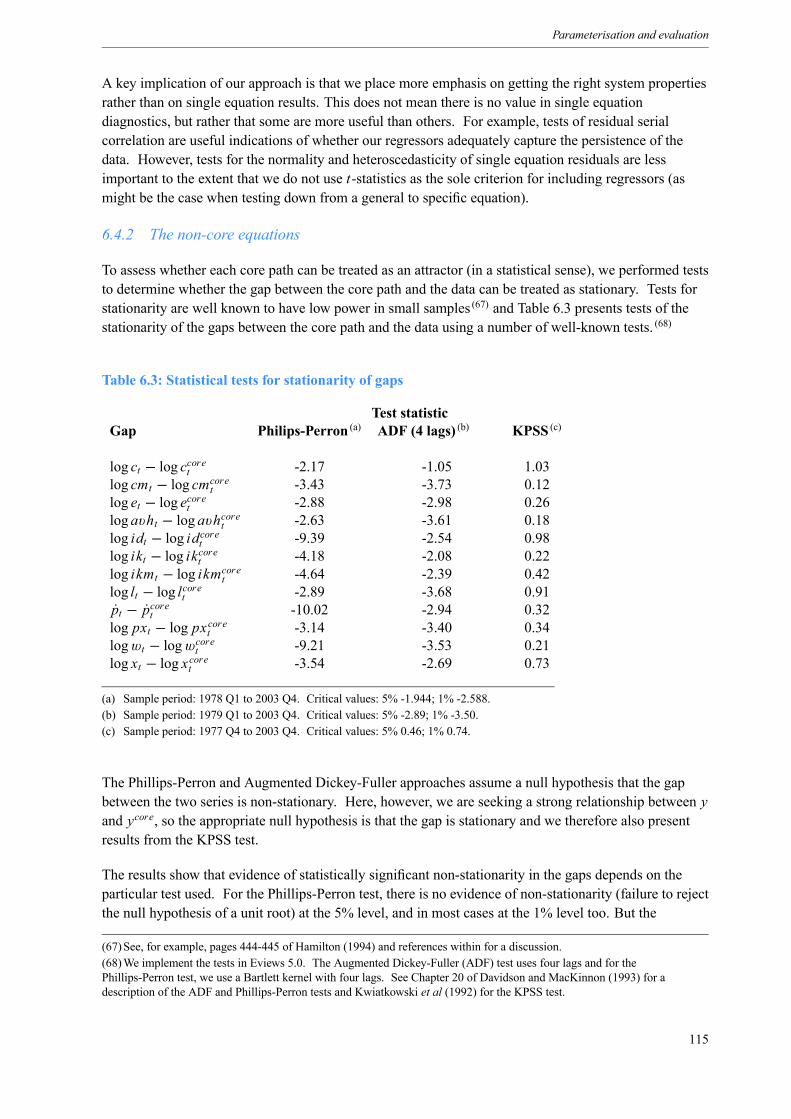

6.3 Statistical tests for stationarity of gaps 115

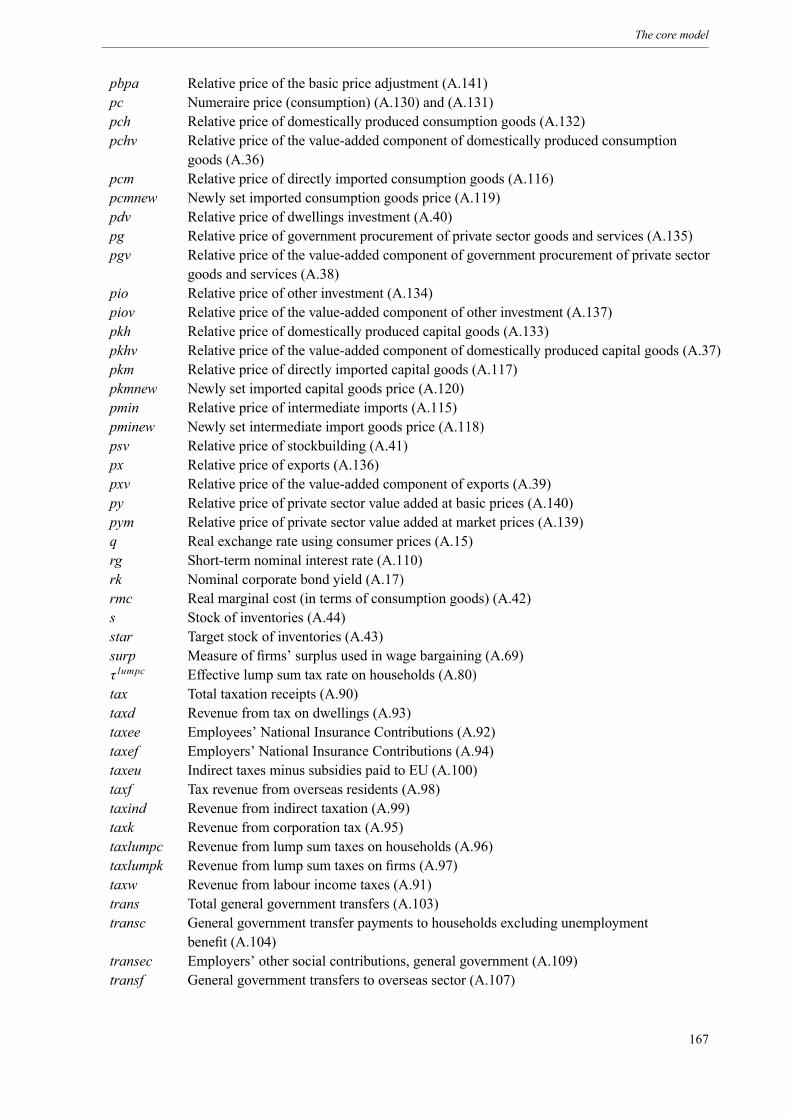

A.1 Endogenous variables 165

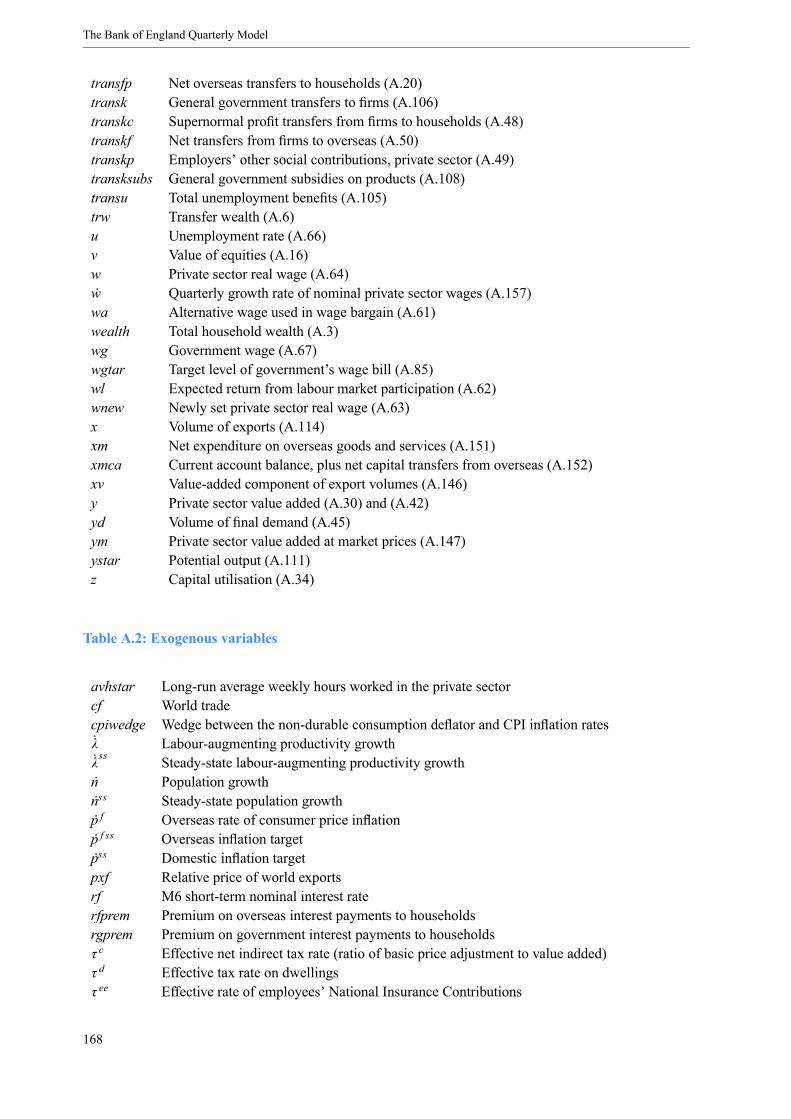

A.2 Exogenous variables 168

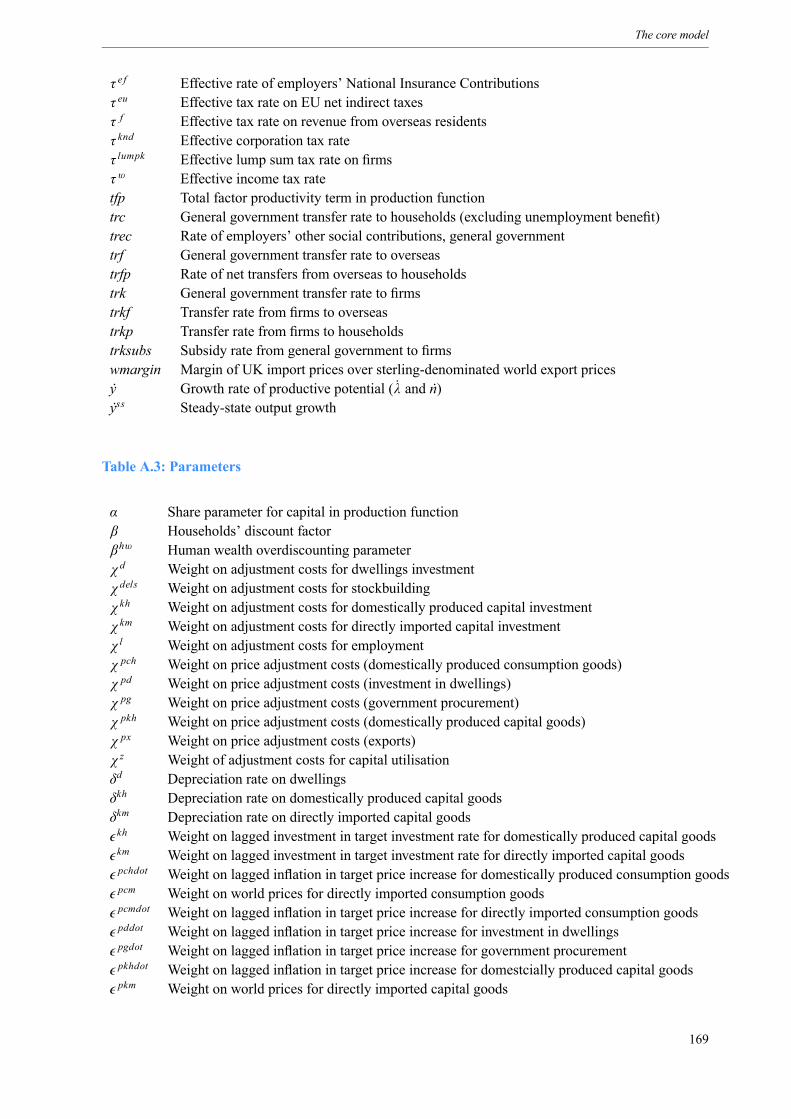

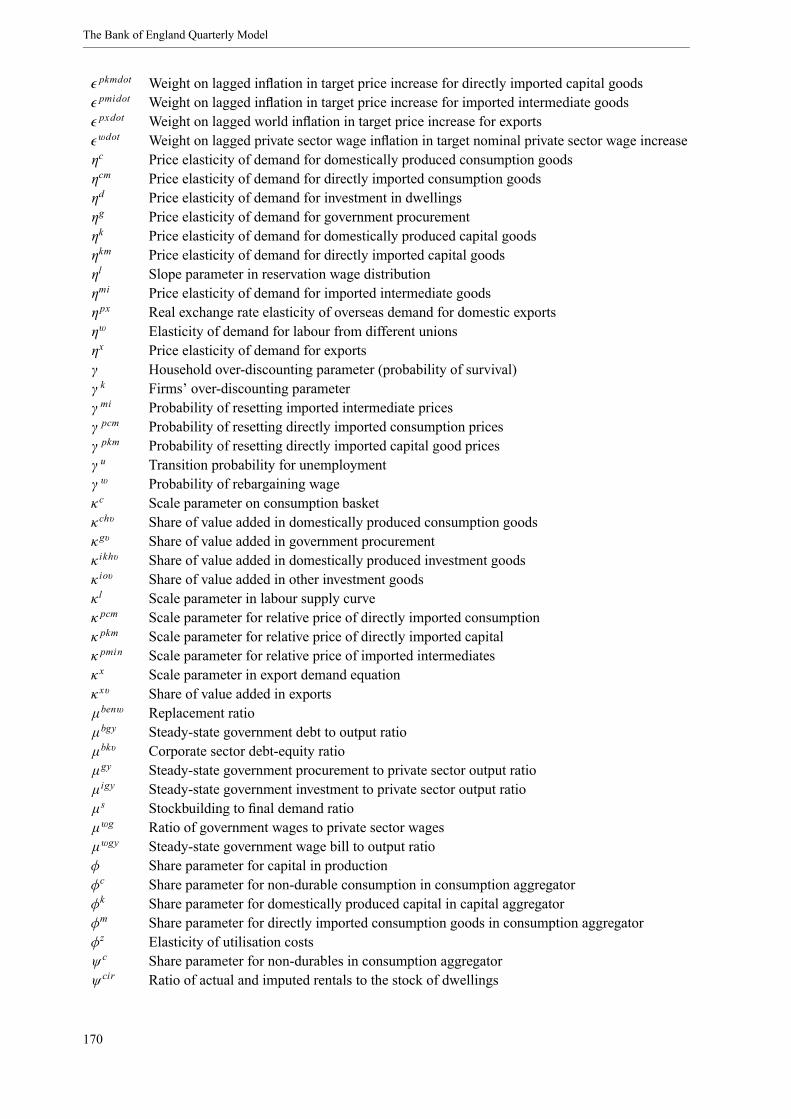

A.3 Parameters 169

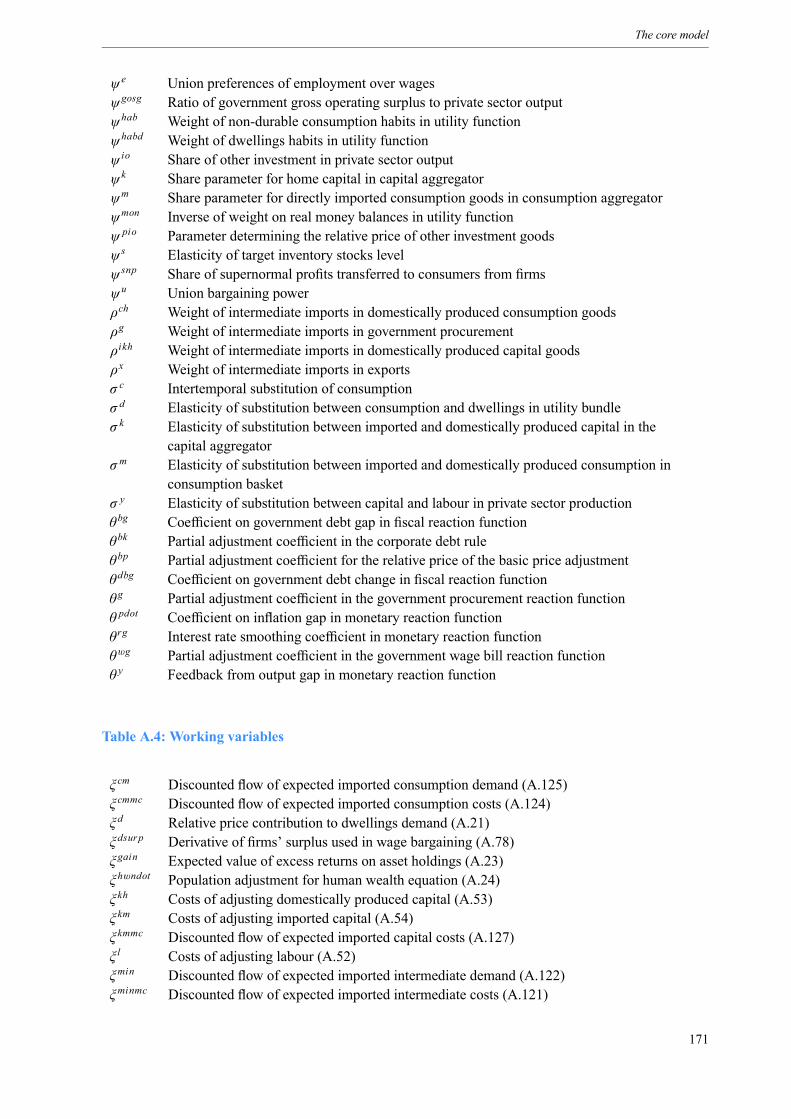

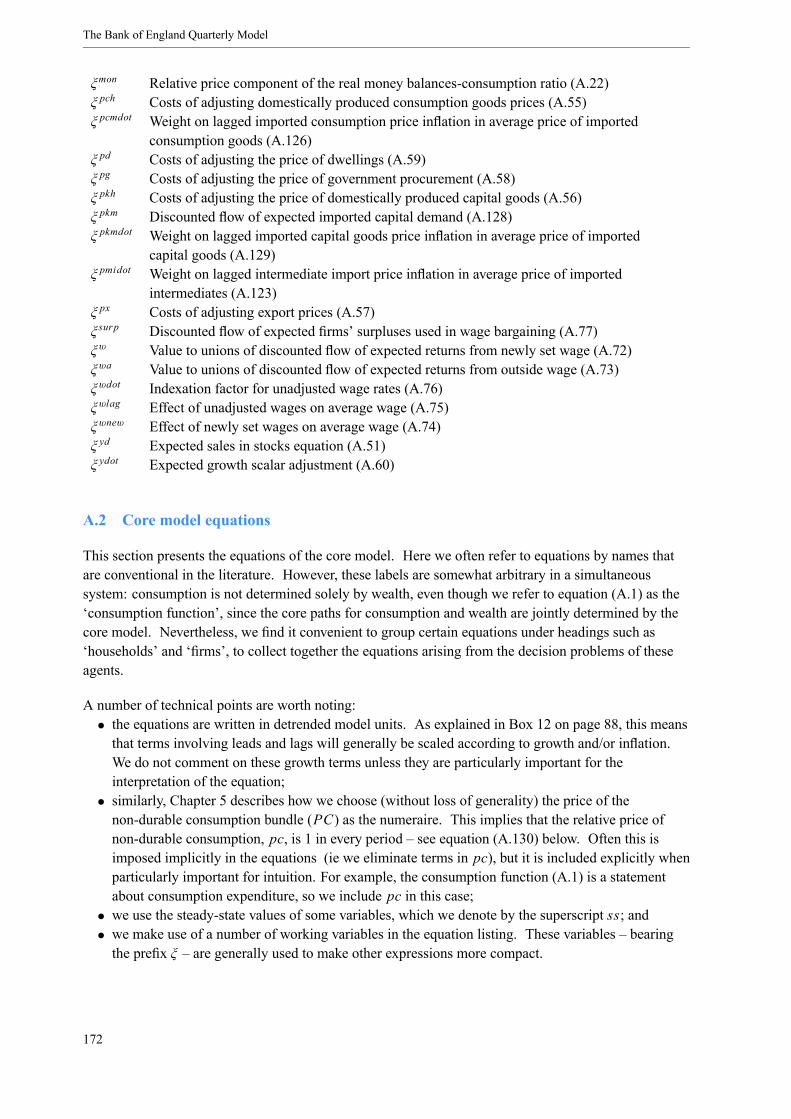

A.4 Working variables 171

B.1 Endogenous variables 197

B.2 Exogenous variables 201

B.3 Parameters 202

C.1 Data sources and transformations for BEQM 225

D.1 Parameter values 243

v

List of technical boxes

1 Some recent developments towards hybrid structural models 19

2 The consumer’s maximisation problem 30

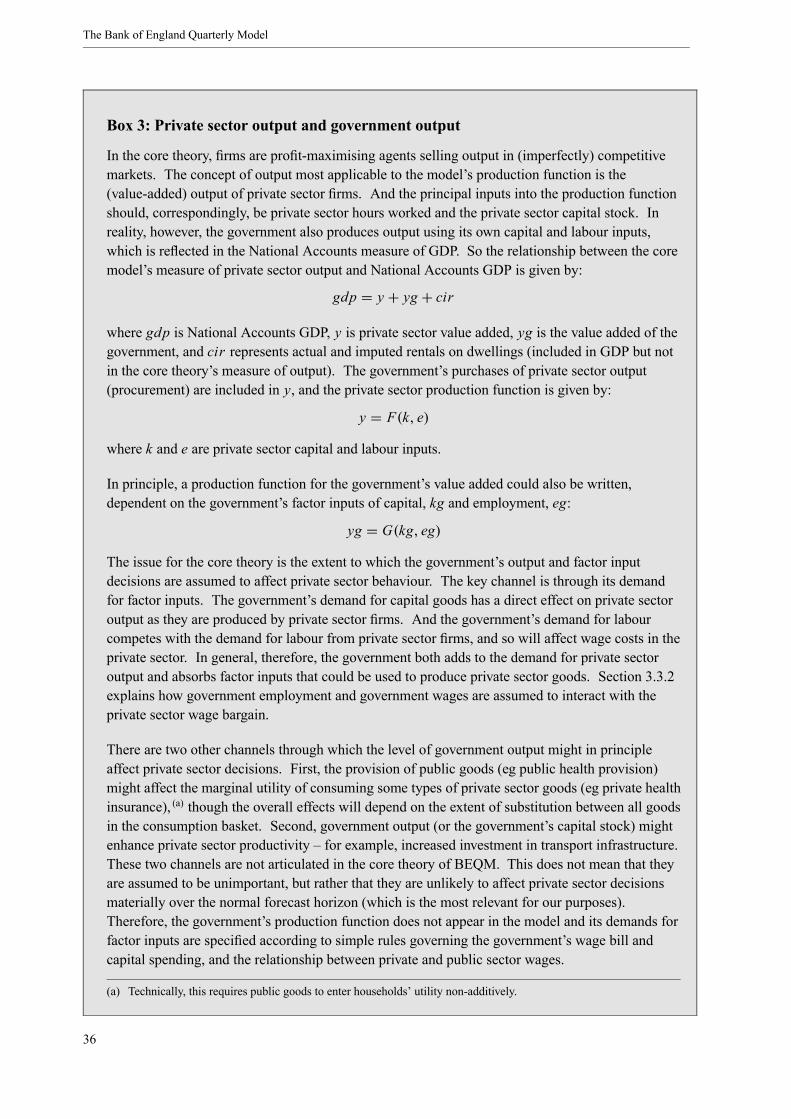

3 Private sector output and government output 36

4 Over-discounting and insurance against mortality 42

5 The determination of inflation 46

6 How does the Blanchard-Yaari model make consumption stationary? 51

7 The firm’s maximisation problem 54

8 The union bargaining problem 58

9 The hybrid approach applied to the Ramsey model 64

10 The exogenous variables model 78

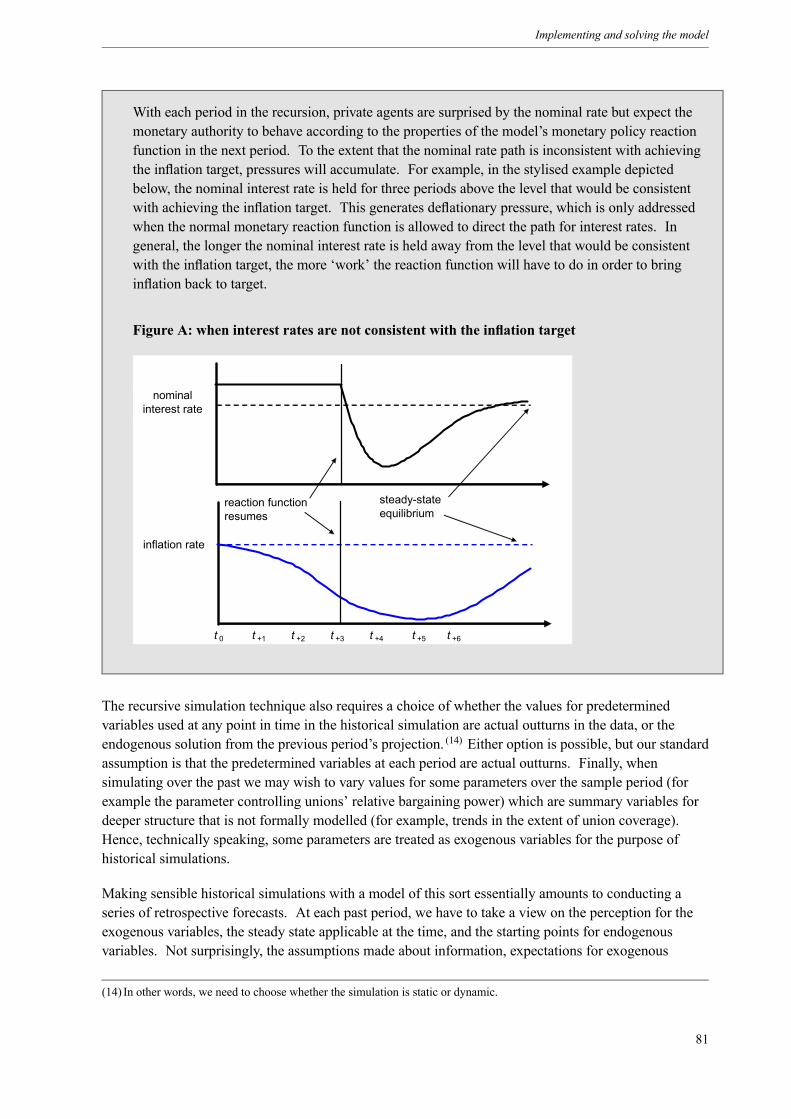

11 Conditioning nominal interest rate paths 80

12 Detrending and model units 88

13 The sensitivity of the steady state to changes in parameter values 103

vii

Foreword

This book contains details of the Bank of England’s new quarterly model which is used to help theMonetary Policy Committee produce its economic projections. The book builds on the previous bookson the Bank’s use of economic models.

The new quarterly model is a valuable addition to the Bank’s ‘suite of models’. It does not represent asignificant shift in the Committee’s view of how the economy functions or of the transmissionmechanism of monetary policy. Rather its value lies in the fact that its more consistent and clearlyarticulated economic structure better captures the MPC’s vision of how the economy functions and soprovides the Committee with a more useful and flexible tool to aid its deliberations. The project todevelop a new quarterly model has been an important initiative and I am grateful to all the Bank staffwho contributed to its success. The Bank has an outstanding group of economists and they are theunsung heroes and heroines of the success of the United Kingdom’s new monetary framework.

But all economic models, however good, represent simplifications of reality and, as such, no singlemodel can possibly address the many and varied issues that matter for economic policy. Thisrecognition is central to the Bank’s use of economic models and its approach to economic forecasting.The Bank relies on a plurality of models to help inform the Committee’s projections. And these modelsare used as tools to help the Committee reach the economic judgements that play a critical role inshaping its projections, rather than simply to generate mechanical forecasts. Economic forecasting isultimately a matter of judgement.

The economy is constantly changing and so too will the quarterly model and the other models used bythe Bank. The model described in this book is part of an evolving process and the Bank will continue todevote resources to both reaping the benefits from the advances this new model brings and developing itfurther.

Mervyn King, Governor of the Bank of EnglandJanuary 2005

1

Acknowledgements

The authors would like to thank Mark Allan, Pedro Alvarez-Lois, Charles Bean, Andy Blake, FabioCanova, Spencer Dale, Rebecca Driver, Karen Dury, Philip Evans, Guillermo Felices, GeorgeKapetanios, Hashmat Khan, Lavan Mahadeva, Stephen Millard, Andrew Moniz, Adrian Pagan, LauraPiscitelli, Simon Price, James Proudman, Peter Sinclair, Jan Vlieghe, Peter Westaway, SimonWren-Lewis and Tony Yates for comments on drafts of this material, and Andrew Holder for his work aseditor.

We would also like to thank our successors as forecasters and model users – in particular, James Bell,Alex Brazier, Michael Grady, and Iain de Weymarn – for their work during the transition to the newmodel.

The views expressed in this book are those of the authors and should not be thought to represent those ofthe Monetary Policy Committee.

3

Chapter 1 Introduction and overview

The Bank of England has developed a new macroeconomic model for use in preparing the MonetaryPolicy Committee’s quarterly economic projections. The new Bank of England Quarterly Model(BEQM) was used to an increasing extent during 2003 and is the main tool in the suite of modelsemployed by the staff and the Monetary Policy Committee (MPC) in the construction of the projectionscontained in the quarterly Inflation Report.

This book explains the motivation for BEQM and the economic and modelling approaches underlying it;it also includes a full technical account of the model and its quantitative properties. This chapter (1)

describes the role of models at the Bank of England in helping to produce the MPC’s quarterlyprojections, explains the motivation for the new model, and provides an overview of BEQM and themodelling approaches underlying it. It also includes a guide to the remaining chapters, which describeBEQM in greater detail.

1.1 The role of models and forecasts at the Bank of England

The Bank of England is mandated by the Chancellor of the Exchequer to aim at an inflation target – atthe time of writing, a 2% annual inflation rate of the Consumer Prices Index (CPI) – and uses a veryshort-term nominal interest rate as its instrument to pursue this target. Because of the lags betweenchanges to interest rates and the associated effects on inflation, setting monetary policy is inherently aforward-looking exercise. Hence the quarterly Inflation Report, in addition to assessing the current stateof the economy, contains projections for output growth and inflation for up to three years out, based onassumptions of both constant and market-based interest rates. These projections represent theCommittee’s best judgement of both the most likely central outcome and the range of possiblealternative outcomes around that central case. A key element of the analysis contained in the InflationReport is to consider the major risks and uncertainties surrounding the central projection, rather than tofocus simply on the central point predictions for GDP growth and inflation.

The Bank uses numerous economic models to help produce these projections. (2) No model can doeverything – all models are imperfect, precisely because they are simplifications of reality. And eachprojection is a judgement of the MPC rather than a mechanical output from any model. Nonetheless theBank has found, like many other policy institutions, that, when producing its economic projections, it ishelpful to use a macroeconomic model as the primary organisational framework to process the variousjudgements and assumptions made by the Committee. This is the role now played by BEQM.

The forecast process at the Bank involves a high degree of interaction between the Bank’s staff and themembers of the Monetary Policy Committee. In particular, a key element of the forecast process is forCommittee members to assess the extent to which different economic judgements and assumptionsconcerning the major issues affecting the economy could influence their view of future prospects. Thisprocess is critical to understanding the nature of the risks and uncertainties surrounding the centralprojection. In order to be able to carry out this sort of analysis, the main forecast model ideally needs arelatively explicit economic structure that identifies the key behavioural parameters and channels withinthe economy.

(1) This chapter is based on the article on the new model that was published in the Summer 2004 Quarterly Bulletin, see Bankof England (2004).(2) The Bank’s use of economic models is discussed in more detail in Chapter 1 of Bank of England (1999a).

5

The Bank of England Quarterly Model

The importance of having a model suitable for analysing the implications of different economicjudgements and assumptions is not new. This role was also central to the design of the previous macromodel used by the Bank, the Medium-Term Macro Model (MTMM). (3) Indeed, the basic economicstructure of BEQM is very similar to that of the MTMM. The aim of BEQM is not to incorporate adifferent view of how the economy works or of the role of monetary policy. Rather, the decision todevelop a new model reflected the view that recent advances in both economic understanding and,importantly, in computational power meant that it was possible to improve upon the articulation of theeconomic structure within the MTMM. As Pagan (2003) noted in his report on modelling andforecasting at the Bank of England, the MTMM was no longer ‘state of the art’. In particular, Paganconcluded that ‘It seems highly likely that [a new model] could achieve the same empirical coherence[as the MTMM] with a stronger theoretical perspective’. In doing so, this would provide the Committeewith a more flexible and coherent framework to aid its economic deliberations. That, in short, is whatthe new model tries to achieve through a clearer articulation of the underlying structure of the economyand a more explicit identification of the role expectations play.

1.2 An overview of BEQM

BEQM describes the behaviour of the UK economy at a relatively aggregated level that is closely relatedto the incomes and expenditures recorded in the UK National Accounts. To do this, the model containsformal descriptions of the behaviour of private domestic agents, policymakers and the rest of the world,and their interactions in markets for capital and financial assets, goods, and labour.

Households consume imported and domestically produced goods. When deciding on their current levelof consumption, and hence their level of saving or borrowing, households are assumed to want to keeptheir lifetime consumption as smooth as possible. To do this, households can borrow and save using arange of financial assets, including domestic equities, corporate debt, government debt, money, andforeign assets. In addition, in the short run, households’ levels of consumption can be influenced by avariety of other factors, such as short-term fluctuations in their income and their level of confidenceabout the future.

Firms seek to maximise profits by hiring labour and buying capital in order to produce output. Firms andworkers bargain over wages and, given the outcome, firms are assumed to choose the labour they wish toemploy so that the costs of any extra workers are compensated for by the higher revenues they generate.Similarly, firms’ desired level of capital is determined by the cost of capital and the return to extrainvestment. The output that firms produce is sold in markets for domestic consumption, investment andgovernment procurement, as well as in housing and export markets. Firms are assumed to face varyingdegrees of competition in these markets, which implies that firms may receive a different profit marginfrom the sale of their goods in each market. The composition of total sales will therefore affect revenueand profits, so that relative demand conditions will matter as well as overall demand conditions. Firmsface competition from importers for consumption and investment goods, and have to price their productsin export markets so as to achieve maximum profits. In addition, various short-run factors can influencefirms’ behaviour, such as the short-run prospects for demand affecting the speed with which they invest.

The government buys output from domestic firms and labour from households, financed by raising taxesand selling debt, in addition to a small amount of revenue that accrues from seigniorage. Total revenuealso has to be sufficient to pay the cost of servicing the existing level of government debt and anygovernment transfers. For long-run solvency, the fiscal authority may at some stage have to adjust apolicy instrument – such as a tax rate – to ensure that the fiscal budget constraint is met. A variety of

(3) The Medium-Term Macro Model is described in more detail in Bank of England (2000).

6

Introduction and overview

fiscal policy ‘rules’ can be considered. In general, these rules assume that any required fiscal adjustmentoccurs only gradually.

The monetary policy maker has the job of anchoring the nominal side of the economy. The nominaltarget could, in principle, be specified in terms of any nominal aggregate, such as the nominal exchangerate, the growth rate of nominal output, or the growth rate of the money stock. The default assumptionis that the central bank targets an annual inflation rate of the CPI of 2%, using the short nominal interestrate as its instrument. An assumption about the policy rule used by the central bank – the monetarypolicy reaction function – is required for inflation to be anchored in the long run. The structure allows avariety of different reaction functions to be incorporated.

BEQM assumes that UK capital markets are ‘small’, in the sense that the demand for and supply offinancial assets in the United Kingdom do not affect the level of interest rates prevailing in the rest of theworld. Since all claims on domestic firms’ assets and government debt must ultimately be held either bydomestic households or the rest of the world, it follows that the United Kingdom’s net foreign assetposition is determined jointly by the decisions of firms and the government about how many financialliabilities to issue and by domestic households about how many of these assets to hold. The rest of theworld affects these decisions through assumptions about the level of foreign real interest rates and worlddemand.

These decisions also have implications for the United Kingdom’s trade balance. Suppose, for example,UK households were assumed to want to hold only some of the domestic financial assets on offer, suchthat the United Kingdom maintained a net debt with the rest of the world. This would imply that, in thelong run, the United Kingdom would need to have a trade surplus sufficient to meet the costs ofservicing this debt. The equilibrium real exchange rate moves so as to ensure that exports and importsachieve this long-run balance. This story is further complicated by the assumption that UK producershave some market power in the prices they set in world markets, so the long-run trade balance will, ingeneral, depend on assumptions made about conditions in both financial and goods markets.

The main channels through which changes in monetary policy are transmitted to the rest of the economyare similar to those previously described by the Monetary Policy Committee. (4) The fact that prices andnominal wages move only slowly means that the central bank, by changing the nominal interest rate, hasthe ability to influence real interest rates. Lower real rates tend to encourage consumers to spend morenow. Lower real rates also encourage investment and spending on housing by lowering financing costs,and they make it less costly to hold inventories. The combined effect is to push up domestic demand. Tomeet that demand, firms will demand more of the factors used in the production of goods and services,namely capital and labour. This in turn is likely to increase the costs of these factors of production.

The fact that the UK economy is a small open economy adds an important channel through whichmonetary policy operates. In particular, a lower domestic real interest rate may tend to encourage adepreciation in the real exchange rate. This will lead to both a direct price effect – the prices of importedgoods will rise – and a number of possible indirect (or ‘second-round’) effects, reflecting both anypass-through from higher import prices onto domestic prices and costs, and the impact of any change incompetitiveness associated with the change in the real exchange rate on the United Kingdom’s tradebalance.

The impact of changes in aggregate demand on prices and inflation will depend on the way in whichagents – households, firms, policymakers and the rest of the world – interact with each other. Other

(4) See Bank of England (1999b).

7

The Bank of England Quarterly Model

things being equal, increased demand for workers leads to higher wage costs, which firms will typicallyattempt to pass on to some degree in the form of higher prices. Similarly, increases in world prices or anexchange rate depreciation create pressure on import prices. And increased demand for domesticallyproduced goods will also create incentives for firms to raise prices.

Inflationary pressures reflect the degree of imbalance between the level of demand and the capacity offirms to meet that demand. The level of demand and potential supply will depend on both the currentstance of monetary policy and the stance expected in the future. Likewise, firms’ responses to thesepressures on capacity will depend on the extent to which they are likely to persist, and hence on theexpected stance of monetary policy in the future. The importance of future expectations in determiningcurrent inflationary pressures underlines the central importance of monetary policy anchoring privatesector expectations of the long-term inflation rate.

1.3 Some key technical features of BEQM

The improved economic structure of BEQM is reflected in a number of specific features. First, it has awell defined steady state. This means that, in the long run, all variables in the model settle on paths thatare growing consistently with each other in a sustainable equilibrium. This aids analysis of economicissues, since an understanding of the medium term requires an understanding not just of short-run forces,but also of where the economy is heading to in the long run. For example, a stable steady-state solutionwould not be compatible with a situation in which household debt was increasing without bound.

In characterising this steady state, careful attention has been paid to ‘stock-flow’ and ‘flow-flow’accounting. This is designed to ensure that all economic flows within the economy are accounted for –all income is spent or saved, for example – and that all expenditures have implications for physical andfinancial stocks. This again aids the understanding of medium-term issues. For example, stock-flowconsistency implies that monetary policy cannot stimulate consumption indefinitely, since this wouldimply an erosion of households’ net wealth, which they could not ignore forever.

Another important feature of the new model is that it contains more explicit forward-lookingrepresentations of agents’ expectations about the future. These include expectations about future labourincome, aggregate demand, the exchange rate, and so on. Models with fully forward-looking agents cansometimes exhibit unrealistic dynamic properties; in particular, if households and firms are assumed tohave perfect foresight, they might adjust their behaviour immediately in response to future anticipatedevents. But in reality the economy does not ‘jump’ about in this fashion. That partly reflects the factthat it is often costly for households and firms to change their behaviour very rapidly. In addition, firmsand households do not have perfect foresight. Instead, they have to form expectations on the basis oflimited information. BEQM incorporates both of these features. In particular, it is structured in such away that assumptions about the speed of adjustment and the amount of information available to agentscan be changed in order to help the Committee to assess how these assumptions could affect the futurepath of the economy.

These features are not new: some or all of them are present in many other models currently used bypolicy institutions, such as the Bank of Canada’s Quarterly Projection Model, the FRB/US model at theUS Federal Reserve Board of Governors, and the Reserve Bank of New Zealand’s FPS model. Indeed,these features were often an explicit aim of pioneering work on macro modelling in the United Kingdomover the past 25 years, such as the Liverpool model, the London Business School model, the COMPACTmodel, and various models at the Cambridge Economic Policy Group and the National Institute ofEconomic and Social Research. The implementation in BEQM may differ in technical details, reflecting

8

Introduction and overview

decisions made on how to satisfy the particular demands of forecasting at the Bank, but the basic ideasand motivations are the same.

1.4 The structure of this book

This book explains the factors which led the Bank to develop a new model and the way it went aboutdoing this. In doing so, it provides a thorough technical description of the new model, including detailsof its theory, construction and use. The main text of the chapters is written with the intention of avoidingheavily technical expositions. In some parts, where there are issues that may need more detailedexplanation, use is made of boxes, which can be read or passed by as the reader chooses. Technicaldetails are contained in appendices. The following provides a guide to the remaining chapters.

Chapter 2 contains a fuller discussion of the particular requirements made upon forecasting models atthe Bank of England and how that is reflected in the design of BEQM. The aim of the project was thatthe new model should provide a richer, more explicit, theoretical structure, while matching the data atleast as well as the previous macro model. It would also need to be flexible and reliable under differentforecasting assumptions and conventions. This led us to the concept of building the model with twoparts – a layer that provides the theoretical core of the model, and a layer of extra dynamics designed, inpart, to facilitate judgemental adjustments. The idea of adding ad hoc or ‘data-driven’ dynamics totheoretical structure is not a new one, but the implementation has many variations. The chaptertherefore includes comparisons with alternative modelling approaches and some other macro models.

Chapter 3 discusses the core theory. The individual building blocks of the theoretical core are largelyconventional, as seen in Section 1.2. However, a key focus in the development of BEQM was ensuringthat the model works consistently as a system, with close attention paid to the constraints and linkagesbetween agents.

Chapter 4 follows with an account of the ad hoc dynamics. These equations take the paths from the coretheory and combine them, if needed, with extra persistence and variables that proxy for effects missingin the core theory. These effects might be missing because we choose not to attempt to model them in afully structural way: the additional structure to do so consistently would make the model much morecomplicated and potentially difficult to run. Additionally, there are some effects that seem empiricallyrobust, but are very difficult to model formally.

Chapter 5 provides technical details of how we solve the model. A key issue here is the treatment ofexpectations, and in particular how to deal with cases in which agents do not fully anticipate futureevents. We address this issue by the use of so-called ‘recursive simulations’ that potentially limit theamount of information available to agents from period to period.

Chapter 6 discusses the parameterisation of the model. The main problem that we face is that the modelis large, in order to be able to handle typical forecast issues with sufficient richness. And in order totreat the theoretical building blocks in the model consistently, the model is highly simultaneous – inother words, one agent’s actions will generally depend on all other agents’ actions at the same time. Themodel is therefore too large to confront using conventional econometric techniques for estimatingsimultaneous systems. This issue is not new and confronts all builders of large macro models. Ourapproach is to separate out parameterisation from evaluation. That is, we select parameter values basedon a range of evidence, and then evaluate the whole system against a number of different criteria. Themodel is parameterised to achieve a plausible long-run relation to observed values for key ratios, and toachieve dynamic properties that are at least as good as those of the previous model, by usingeconometric evidence and priors about the transmission of shocks. We find the theoretical core does

9

The Bank of England Quarterly Model

well at tracking broad movements and does quite well at forecasting at longer horizons (two and threeyears) over history. But some variables track better than others, and we find econometric evidence thatthe model’s fit is improved by the inclusion in the non-core equations of proxies for short-run effectssuch as credit constraints, house price effects, confidence and accelerator effects.

Chapter 7 shows how all of the preceding elements come together in terms of model properties. Shockresponses are a useful way of illustrating the overall model properties, and we present several, includingdemand, supply and policy shocks.

Finally, Chapter 8 concludes with some remarks on future uses and directions for the model.

A number of appendices set out supporting detail to the discussion in these chapters. Appendix A setsout the core model equations and mnemonics, with comments on the economic rationale for theequations. Appendix B presents similar detail for the non-core equations. Appendix C details datatransformations and sources and Appendix D sets out parameter values.

1.5 Summary

The Bank of England has developed a new macroeconometric model for use in preparing the MPC’squarterly economic projections. This model uses recent advances in economic understanding andcomputational power to develop and improve upon existing models used at the Bank. The new modeldoes not represent a change in the Committee’s view of how the economy works or of the role ofmonetary policy. Indeed, the sensitivity of output and inflation to temporary changes in interest rates isbroadly similar to that in existing models used at the Bank. However, the model does provide theCommittee with a more flexible and coherent framework to aid its economic deliberations.

10

Chapter 2 Project motivation and model design

This chapter describes some of the thinking behind the new model. Section 2.1 sets out the project’smotivation, and how the requirements for the new model relate to the problem of achieving boththeoretical and empirical consistency, but in a way that is suitable for practical forecasting. This leads toa description of the design of the new model (Section 2.2). Section 2.3 compares BEQM with someother macroeconomic models, before a summary in Section 2.4.

2.1 Motivations and challenges

The main motivation for developing the new model was to improve theoretical consistency and clarity.In particular, one of the key benefits of a formal model is that it can remind us of important implicationsthat are not immediately apparent. The importance attached to understanding the ‘economics’ of theforecast, and to exploring the various risks and uncertainties surrounding the central projection, points tothe need for a clear and explicit economic structure.

If the forecast were simply a mechanical process – that is, the production of a single, ‘best’ prediction,without alteration or imposition of judgement – then the comparative advantage would lie withatheoretic models such as large-dimensional common factor models. (1) Instead, the MPC wants tounderstand what is driving the economy. This focuses attention on forces at work in the economy –asking what economic shocks are affecting the economy, how will they work their way through theeconomy, and what implications do they have for monetary policy. A central problem here is that thereare often several possible explanations for observed inflation. For example, a fall in inflation could bethe result of an increase in productive potential; a fall in wage growth; an increase in domesticcompetition; pass-through of lower world prices; or an exchange rate appreciation.

Without theoretical consistency and clarity, a model would lack the structure and linkages needed todiscriminate between these different hypotheses. The model should be consistent at a general level withthe MPC’s view of how the economy works (especially the monetary transmission mechanism).Moreover, to be used as a forecasting device, the model should produce realistic responses, whichimplies that it has to be matched to the data. At the same time, the final, published forecast is aconditional projection, based on policymakers’ judgements about risks, influenced by other models andinformation. This, in turn, implies that theoretical strictness should not preclude the ability to apply awide range of judgement to the model’s ‘naive’ projections.

To summarise, the project had three clear challenges:

• to incorporate theory that is rich enough to be able to analyse a wide range of economic issues,while remaining tractable, internally consistent, coherent and easily understood;

• to make this theoretically tight model match the data at least as well as the previous model; and• to make the model reliable and efficient under different forecasting assumptions, and amenable tothe imposition of judgemental adjustments and conditioning paths.

(1) Indeed, the Bank maintains a number of such models for comparison with the conditional forecast.

11

The Bank of England Quarterly Model

2.2 The design of BEQM

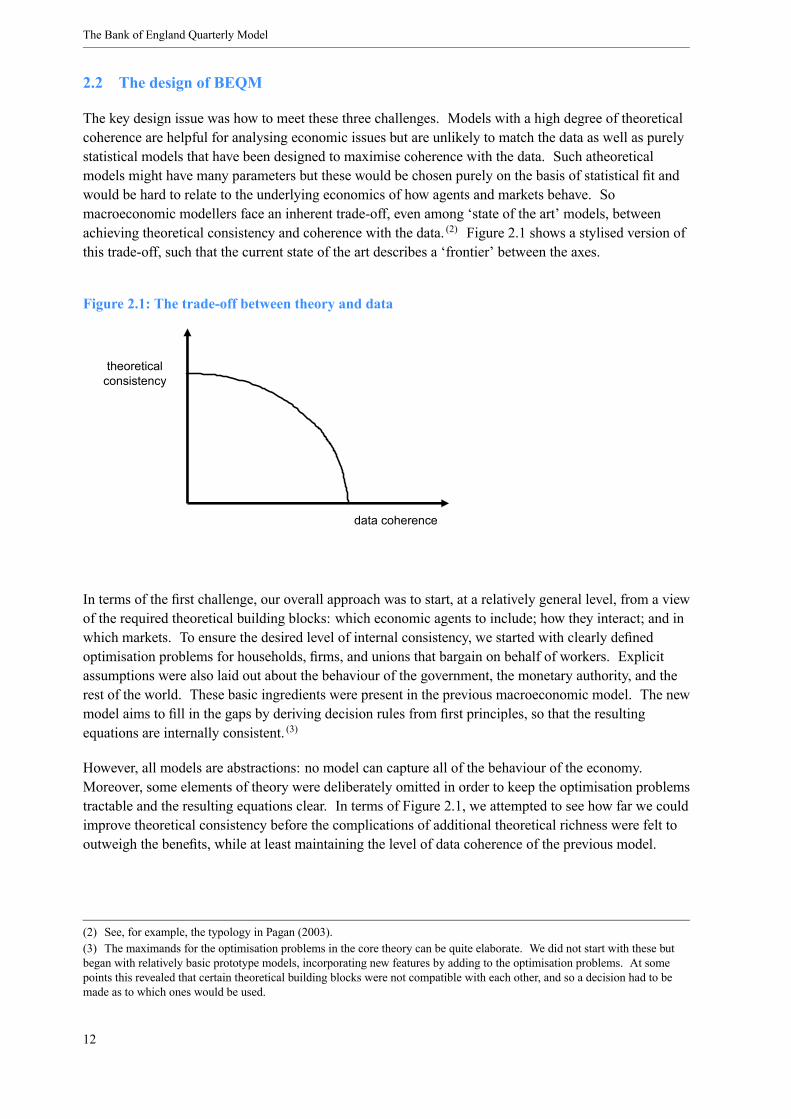

The key design issue was how to meet these three challenges. Models with a high degree of theoreticalcoherence are helpful for analysing economic issues but are unlikely to match the data as well as purelystatistical models that have been designed to maximise coherence with the data. Such atheoreticalmodels might have many parameters but these would be chosen purely on the basis of statistical fit andwould be hard to relate to the underlying economics of how agents and markets behave. Somacroeconomic modellers face an inherent trade-off, even among ‘state of the art’ models, betweenachieving theoretical consistency and coherence with the data. (2) Figure 2.1 shows a stylised version ofthis trade-off, such that the current state of the art describes a ‘frontier’ between the axes.

Figure 2.1: The trade-off between theory and data

theoretical consistency

data coherence

In terms of the first challenge, our overall approach was to start, at a relatively general level, from a viewof the required theoretical building blocks: which economic agents to include; how they interact; and inwhich markets. To ensure the desired level of internal consistency, we started with clearly definedoptimisation problems for households, firms, and unions that bargain on behalf of workers. Explicitassumptions were also laid out about the behaviour of the government, the monetary authority, and therest of the world. These basic ingredients were present in the previous macroeconomic model. The newmodel aims to fill in the gaps by deriving decision rules from first principles, so that the resultingequations are internally consistent. (3)

However, all models are abstractions: no model can capture all of the behaviour of the economy.Moreover, some elements of theory were deliberately omitted in order to keep the optimisation problemstractable and the resulting equations clear. In terms of Figure 2.1, we attempted to see how far we couldimprove theoretical consistency before the complications of additional theoretical richness were felt tooutweigh the benefits, while at least maintaining the level of data coherence of the previous model.

(2) See, for example, the typology in Pagan (2003).(3) The maximands for the optimisation problems in the core theory can be quite elaborate. We did not start with these butbegan with relatively basic prototype models, incorporating new features by adding to the optimisation problems. At somepoints this revealed that certain theoretical building blocks were not compatible with each other, and so a decision had to bemade as to which ones would be used.

12

Project motivation and model design

The sort of tightly specified structural model that this process delivers is a useful device for thinkingabout the transmission of shocks and policy, and the identification of different economic stories.However, such a model would probably have some difficulty in matching the data fully, because it wouldalways be missing some potentially important economic elements. Typically, in much of the academicliterature over the past 25 years, models have been designed to answer a specific question and cantherefore be focused on specific issues. In our case, however, the model is intended to be used as ageneral-purpose vehicle for policy analysis and forecasting, and we cannot neatly restrict the range ofeconomic issues that the model will face. Moreover, the ultimate users – policymakers on the MPC –must have confidence that the model is able to match general features of the UK economy and itsresponse to shocks, even if some of this behaviour is difficult to model structurally.

One approach to matching movements in the data, commonly used for macroeconomic models, is totreat the theory as a guide to the economic variables that appear in econometric regressions. (4) If a strictapproach is taken to deriving a reduced-form equation from theory, then the equation parameters will becombinations of the deep parameters from the structural decision rules. If cross-equation restrictionswere not strictly enforced, the linkages implicit in the original specifications would be weakened. Thiswould be problematic for our purposes, because so many of the forecast issues and risks revolve aroundcompeting structural stories, and we need to be able to trace their different effects through the model.These are not just variations in exogenous effects, such as assumptions for future world trade, but also inhow the economy responds to those effects. (5)

An alternative approach could be to retain the structural specifications derived from the optimisationproblems and to add extra, ad hoc components. But it is not clear where to place ad hoc elements in amicro-founded simultaneous system. Indeed, experiments along these lines confirmed that it would beeasy to create a system that generated unpredictable results and that might not even solve. To reap fullbenefit from a structural system, any additional elements should be worked through consistently fromthe original optimisation problem, which could risk making the model large and intractable.

To secure the benefits of the new model, our approach was to build the model in two distinct parts: atheoretical ‘core’ model, and ‘non-core’ equations that include additional variables and dynamics notmodelled formally in the core. When used together, these two parts form the full model that is the actualplatform used for producing forecast paths and allows the direct application of judgement.

The theoretical core is a structural model, containing a set of decision rules derived from first principlesand an associated set of consistency conditions, such as accounting constraints and stock-flow identities.It could be thought of as a dynamic general equilibrium model in which adjustment costs and otherfrictions are modelled explicitly. The decision rules are dynamic and are derived from the assumptionsthat agents act to maximise forward-looking objective functions according to dynamic constraints. (6) Itdescribes how we would expect changes in exogenous forces to work their way through the modeleconomy. A change to a given structural parameter would usually feed into many different decisionrules and would therefore affect how the system responds to shocks. The paths from this core model aretreated as starting points for the final forecast paths.

(4) See, for example, the programme laid out in Fair (1993) and (1994).(5) For example, the responses of the economy if goods markets were more or less competitive are well defined whereparameters for demand elasticities are identified throughout the system. But with reduced forms, the answer is often buried inthe constants and (quasi-) elasticities of the system. An expert user could make use of intercept adjustments, but this wouldtake some skill and time, which is not ideal when a large number of economic issues and uncertainties must be processedquickly.(6) For example, consumers are assumed to maximise expected lifetime utility subject to the constraint that their assets evolveaccording to a period-by-period budget constraint.

13

The Bank of England Quarterly Model

The full forecast model supplements the paths from the theoretical core with a statistical model of thediscrepancy between historical outturns and the paths generated by the core model. We supplement thecore theory for two reasons. First we might allow for different dynamics, such as more persistence thanthe theory implies. Second, we might allow for influences from variables that proxy for missing effects,such as credit channel effects and confidence effects through the business cycle. The only restriction onthe structure of ad hoc non-core equations is that the projected path for a given variable should alwaysconverge to the long-run equilibrium imposed by the core theory. This forecasting model is strictlyautoregressive, so that judgement (7) can be used to modify paths in a predictable way, which would bemore difficult within the structural core model. This is an important feature, allowing us to impose theCommittee’s judgements, using off-model information.

Actual forecast paths are thus combinations of three types of information:

• theoretical insight from the structural core model;• data-driven evidence on historical correlations of endogenous variables with other factors,especially those that are not formally accounted for in the structural core; and

• a direct application of judgement, informed by other models and staff expertise.

A key forecast question is how much weight these different contributions should carry in deriving thefinal forecast path.

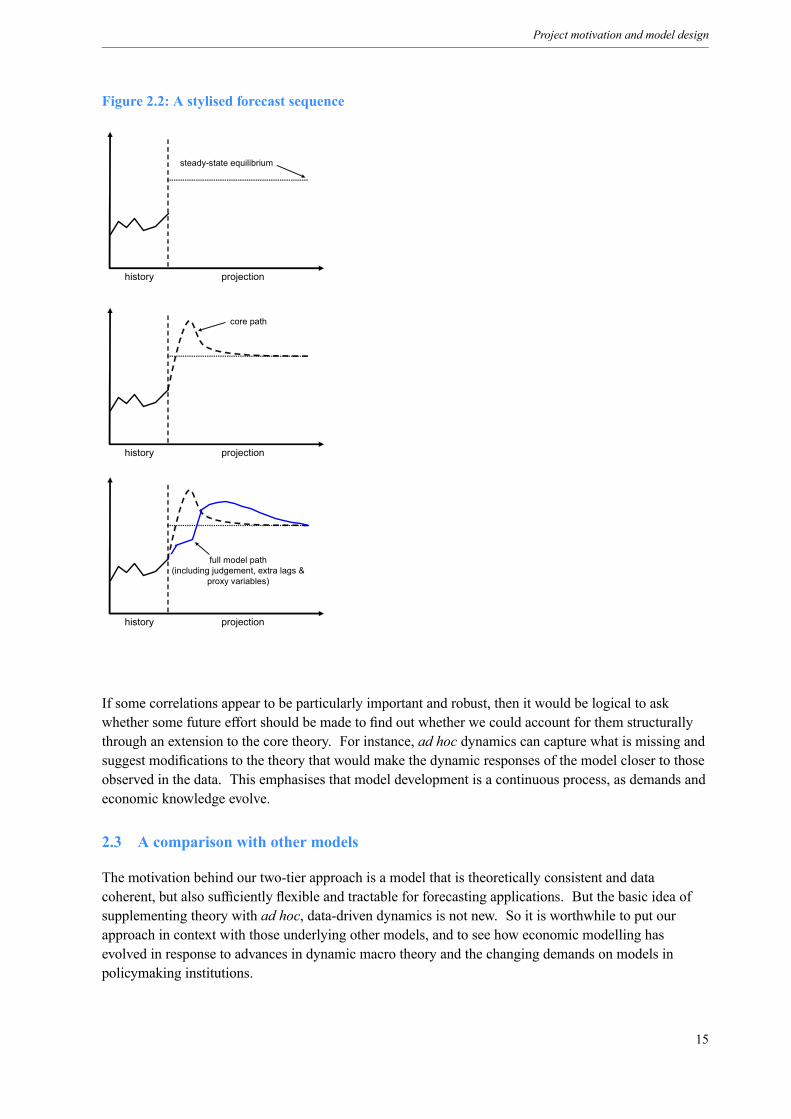

The profile for a given endogenous variable is built up from the core model and supplemented in the fullmodel by additional variables, dynamics or judgement, as illustrated in the stylised sequence below andin Figure 2.2: (8)

• given values for the exogenous variables, a steady-state version of the core model determines asustainable long-run equilibrium value;

• the core model indicates a path that converges from the current starting point to the long-run levelthat is consistent with the decision rules and constraints in the core theory; and

• in the full model, the path might have additional lags or proxy variables added, or judgementapplied. (9)

While this process allows a relatively free modification of the original path for a given endogenousvariable, the system still preserves accounting identities and stock-flow relations, so there are no ‘freelunches’ allowed by the application of judgement (the details of the application of this approach arediscussed in Chapter 4).

(7) These ‘addfactors’ are additional exogenous elements on the right-hand sides of equations. They are set to zero in the longrun, but can take various values to affect the path of a left-hand side variable. For example, suppose we have a system of theform:

y1t = a1 · y1t−1 + e1ty2t = a2 · y1t + e2t

A ‘type 1’ fix on y2t would be where we use e2t to achieve a desired path for y2t . For a ‘type 2’ fix, we would use e1t to affecty1t and therefore y2t .(8) For simplicity, the illustration is as if stationary and abstracts from trend growth.(9) This representation is very stylised; in practice, judgement might be applied to the long run (for instance, by changing coremodel parameters) as well as the short run.

14

Project motivation and model design

Figure 2.2: A stylised forecast sequence

history projection

history projection

steady-state equilibrium

core path

history projection

full model path(including judgement, extra lags &

proxy variables)

If some correlations appear to be particularly important and robust, then it would be logical to askwhether some future effort should be made to find out whether we could account for them structurallythrough an extension to the core theory. For instance, ad hoc dynamics can capture what is missing andsuggest modifications to the theory that would make the dynamic responses of the model closer to thoseobserved in the data. This emphasises that model development is a continuous process, as demands andeconomic knowledge evolve.

2.3 A comparison with other models

The motivation behind our two-tier approach is a model that is theoretically consistent and datacoherent, but also sufficiently flexible and tractable for forecasting applications. But the basic idea ofsupplementing theory with ad hoc, data-driven dynamics is not new. So it is worthwhile to put ourapproach in context with those underlying other models, and to see how economic modelling hasevolved in response to advances in dynamic macro theory and the changing demands on models inpolicymaking institutions.

15

The Bank of England Quarterly Model

There has been a long UK tradition associated with cointegration-based econometrics, which has beenvery influential in macromodelling. This approach uses theory to posit the existence of long-runrelations, which would be incorporated into the model if validated on statistical grounds. Examples ofthis approach include Hall and Henry (1987) and, to some extent, the Bank of England’s earlier MTMMmodel, which in broad terms is a large, restricted Vector Error-Correction Model (VECM). Thisapproach puts less emphasis on some aspects of theory, insofar as short-run dynamics are largely ‘datadriven’, and long-run relations implied by theory have to be confirmed by empirical work. For example,the modeller would not insist that the model has a balanced-growth equilibrium, but instead would testwhether the cointegrating relation implied by this was present in the data. (10) Similarly, the existence offorward-looking expectations and susceptibility to the Lucas critique are hypotheses to be tested. (11)

In the 1980s, a generation of UK macro models emerged that attempted to respond to the Lucas critiquedirectly with the use of rational expectations econometrics. (12), (13) These models typically placed astrong emphasis on consistency conditions such as stock-flow relations. (14) A typical approach wouldbe to take an equilibrium condition derived under the assumption of rational expectations and estimatethe parameters using some form of instrumental variables. For example, a consumption function mightbe used as the starting point for a regression of current consumption on leads of consumption, lags, andwealth terms. A good example of such an approach is the NIDEM model produced by the NationalInstitute of Economic and Social Research. (15) Such an approach effectively allows the model-builder totest directly the coherence of the theoretical relation against the data. The equations are nonetheless stillreduced form, with cross-equation restrictions enforced to varying degrees. (16) Because of this, some adhoc measures would be necessary if some technical features, such as a long-run balanced-growthsolution, were required. (17), (18)

In terms of models actively used by policy institutions to support forecasts and policy analysis, there hasbeen a steady shift towards models that place greater emphasis on theoretical consistency. (19), (20) Forexample, the Bank of Canada shifted from the RDXF model to the QPM in the early 1990s, and theBoard of Governors of the Federal Reserve moved from the MPS to the FRB/US model. The QPMmodel placed more weight on theoretically plausible parameter values than on direct econometric

(10)See Doornik and Hendry (1994) for an example of this approach.(11)See, for example, Favero and Hendry (1992).(12)An outstanding early example was the work on the Liverpool model (Minford (1980)). Subsequent work included that atthe National Institute for Economic and Social Research (Hall and Henry (1985) and (1987)), the LBS model (Budd et al(1984) and Dinenis et al (1989)), the City University CUBS model, and, more recently, COMPACT (Darby et al (1999)). SeeWallis and Whitley (1991) for a commentary.(13)Wallis (1980) was an early investigation of the consequences of rational expectations for macroeconometric specifications.(14)The importance of consistency conditions was emphasised in pioneering work on optimal control in forward-lookingmodels – see, for example, Holly and Zarrop (1983) and Holly (1986).(15)This has several vintages; see Wren-Lewis (1989) for an example.(16) In this sense, these models can be interpreted as overidentified VARs; typical identifying assumptions that would bemaintained are homogeneity restrictions.(17)For example, in the case of the NIESR model referred to here, a stable net foreign asset position was ensured byconfiguring the fiscal rule so that the government effectively took the role of ensuring an economy-wide savings equilibrium.(18)Extensive comparisons of UK macro models have been conducted, especially by the ESRC Macroeconomic ModellingBureau from 1983 to 1999. See Andrews et al (1984), (1985), (1986); Fisher et al (1987), (1989), (1990); and Church et al(1991), (1993), (1995), (1997), (2000).(19)This was facilitated by advances in solution algorithms that made simulations with large-scale non-linear models withmodel-consistent expectations feasible; see, for example, Fisher, Holly and Hughes-Hallett (1986).(20)Some, however, would regard existing macroeconometric forecasting models as well within the possible frontier, payingless attention to issues of simultaneity and cross-equation restrictions than would have been the case in macroeconomic modelsof the 1960s; see Sims (2002). Indeed, the Liverpool model of the late 1970s was theoretically very strict by today’s standards.

16

Project motivation and model design

estimates. (21) It uses a calibrated theoretical model to pin down a set of steady-state attractors forerror-correcting relationships. (22) Dynamics are driven by assuming, on a partial equilibrium basis, thatthere are adjustment costs between current and long-run target levels for a variable. (23)

In the FRB/US model, theory is used to inform long-run relationships, and some of these are forwardlooking, such as human wealth. (24) Dynamics are assumed to be driven by generalised adjustment costs,and the existence of higher orders of adjustment costs introduces a role for forward expectations. (25)

The full model is a mixture of structural relations implied by a partial equilibrium treatment of theory(such as the decision rule for aggregate consumption) and some reduced-form relations (such as thetrade block, which employs error-correcting relationships.)

A similar transition was made by the International Monetary Fund (IMF) with the shift to the Mark IIIvintage of the MULTIMOD multi-country model. Since MULTIMOD was intended to be used more asa simulation model rather than a direct forecasting tool, several of the changes which were implementedin the Mark III version arose from the need to enrich its theoretical structure, so that it could deal withnew macroeconomic issues such as current account imbalances. (26) As with the QPM, a steady-statemodel enforced necessary terminal conditions. (27)

Other central banks have followed with variations of their own. In 1997, the Reserve Bank of NewZealand moved away from spreadsheet-based forecasting to a formal model, FPS, that drew on theexperience with QPM. (28) That model can be viewed as a forward-looking IS/LM system with adisaggregated IS curve. The difference between ad hoc calibrated dynamics and ‘equilibrium’ dynamicsfor real variables defines an output gap, which drives the nominal side through a Phillips curve. Work atthe Bank of Japan has pursued and extended this approach, (29) and a variant of the QPM model has beenused by the Sveriges Riksbank in the form of the RIKSMOD model.

Recent work at several institutions indicates that this process may go several steps further. Projects atthe Board of Governors of the Federal Reserve and the Bank of Canada are now under way to exploremodels with theory-based dynamics as well as long-run properties. Work on the GEM model at the IMFand the EDGE and AINO models at Bank of Finland can also be seen in this way.

In the case of BEQM, the model is split into two tiers – the structural model is kept intact, with noattempt to introduce ad hoc components directly; forecast paths are constructed as a weighted average ofpaths from the structural model and paths driven by statistically robust correlations, together withapplication of policymakers’ judgements. This approach reflects the nature of the forecast process at theBank of England. As much as possible, an attempt is made to understand the forces at work on themacroeconomy in terms of fundamental economic drivers and constraints, which are articulated in the

(21)For example, Coletti et al (1996) comment that ‘there had been a systematic tendency towards over-fitting equations andtoo little attention to capturing the underlying economics. It was concluded that the model should focus on capturing thefundamental economics necessary to describe how the macro economy functions, and, in particular, how policy works’ (page14).(22)See Black et al (1994).(23)See Coletti et al (1996).(24)See Brayton and Tinsley (1996).(25)See Kozicki and Tinsley (1999).(26)See Laxton et al (1998).(27)This was to compute the terminal conditions for the forward-looking variables in the model. It also enabled users to relaxthe assumption of earlier vintages that current accounts have to balance in the long run, which enabled better investigation ofsustainability issues.(28)See Black et al (1997) and Hunt et al (2000).(29)See Fujiwara et al (2004).

17

The Bank of England Quarterly Model

core model. But our understanding of the macroeconomy is imperfect, so it is logical to ask whethersome weight should be given to correlations that are robust in the data but might be difficult to explain ormodel in a fully structural way. Other, more specialised models can provide insight on specific issues orvariables, as can sectoral expertise available within the Bank. These suggest instances when judgementcan usefully be applied.

2.4 Summary

This chapter discusses some of the factors behind the design of BEQM. The main motivation fordeveloping a new model was to improve theoretical consistency and clarity. A number of specificrequirements stem from its role in helping to produce the MPC’s quarterly economic forecast and inanalysing the economic issues underlying the forecasts, together with associated risks and uncertainties.This meant that we want a model that is rich enough to be able to analyse a wide range of economicissues; that can match the observed data; and that is reliable and robust under the pressures of a real-timeforecasting round – including the ability to impose judgement and conditioning paths.

Our approach was to build a model with two distinct parts. We start with a tightly specified theoreticalcore model, containing dynamic decision rules derived from the solution of dynamic optimisationproblems. We supplement this with non-core equations that include additional lags and variables tomatch dynamics that are not modelled formally in the core. These equations also allow the impositionof judgement based on ‘off-model’ information. The final forecast path can be thought of as acombination of theoretical insight from the structural core model; additional variables and dynamicsfrom the non-core; and direct application of judgement.

Finally, we put BEQM into historical context by discussing advances in macroeconomic model buildingover the past 25 years. Over time, greater emphasis has been placed on theoretical consistency, andadvances in computing power have allowed more complex models to be employed.

18

Project motivation and model design

Box 1: Some recent developments towards hybrid structural models

Substantial effort in recent years has been directed towards ‘hybrid’ models, which preserverelatively strong, theoretically derived identification structures but nonetheless fit the dataaccording to some well defined statistical metric. Some of this work can be thought of as comingfrom a relatively atheoretic perspective, such as the Vector Auto Regression (VAR) literature; otherwork takes theoretically tight models, such as from the Dynamic Stochastic General Equilibrium(DSGE) literature, as a starting point, and asks what has to be done to make such models fit thedata. The attempt at convergence is logical, because both approaches yield a compactautoregressive form that can be assessed against the data.

In the VAR literature more and more use has been made of long-run (and even short-run)identifying restrictions; for example, Leeper and Zha (2001) aimed to produce a VAR model that is‘useful’ for monetary policy analysis. A small number of papers have attempted to exploit thedata-matching properties of VARs together with the story-telling advantages of structural models.McKibbin, Pagan and Robertson (1998), for example, start with a VAR to produce a hybrid modelthat retains the very short-run properties of the VAR, but is designed to match some of the featuresof a calibrated structural model. There is now a substantial literature that assesses DSGE modelsagainst their corresponding VARs. (a)

In a conventional DSGE approach, first-order approximations to the decision rules derived fromdynamic optimisation problems are evaluated at a deterministic steady state. The useful ‘trick’ ofthe DSGE approach that makes the solution of these models tractable is to assume that theexogenous variables follow a simple autoregressive process. Given this assumption, the rationalexpectations of future variables can be derived as functions of current states of the world, leadingto a backward-looking representation of the dynamic solution to the model. The generic statespace representation of these models will have the form

st = Ast−1 + But (1)yt = Cst (2)

where s is a vector of states of the world, u is a vector of shocks and y is a vector of endogenousvariables. A, B, and C are conformable matrices, where the elements are combinations ofstructural parameters. Usually y will be larger-dimensioned than s: given knowledge about theevolution of a relatively limited number of states of the world (eg capital stock, previous levels ofconsumption), we make inferences about a wide range of variables (such as output, wage rates,employment, and asset prices).

In its state-space form, the model can be run recursively against the historical data and predictionerrors can be extracted from the difference between predicted and actual y. Notionally at least,these errors could be used to evaluate a likelihood function. A problem arises when applying thisto the canonical Ramsey mode, which has a single stochastic process (technology), in that thecovariance matrix is singular. But if we augment the range of extrinsic dynamics so that there is astochastic process for each endogenous variable, then exact maximum likelihood is possible.

(a) See, for example, Canova, Finn, and Pagan (1994).

19

The Bank of England Quarterly Model

Hence, in recent years we have seen papers (eg Hansen (1985)) in which parameters that wouldpreviously have been held fixed are allowed to vary over time. For example, instead of aconventional household maximisation problem with fixed time preference and utility weights onconsumption (c) and leisure (the proportion of available time not spent working, 1− h):

max Et∞

i=0β i {log ct+i + A log (1− ht+i )}

we could now specify the problem as

max Et∞

i=0ϕt+i {log ct+i + At log (1− ht+i )}

ϕ t+i = (1− ρϕ)ϕ + ρϕϕ t+i−1 + εϕt+i 0 ≤ ρϕ < 1At+i = (1− ρ A) A + ρ AAt+i−1 + εAt+i 0 ≤ ρA < 1

Other extensions include capital-specific and labour-specific effectiveness processes, time-varyinginvestment efficiency, and policy shocks. One would add shock processes to the optimisationproblem until there is a stochastic process for each endogenous variable. Then estimation ofparameters is possible using the Kalman filter to extract prediction errors to be assessed using thelikelihood function. A recent example of adding shock processes to the optimisation problem canbe found in Smets and Wouters (2003a) A potential disadvantage with this type of model is thatits projections are driven by a large set of unobservable shocks, some of which might be regardedas arbitrary and difficult to interpret.

A Bayesian rather than classical approach to this problem can also be taken. One implementationis to use the recursive state-space form of the theoretical model to generate artificial data. Theparameters of the system can then be estimated using a pseudo-sample that combines actual withartificial data. The higher the proportion of artificial data used in the pseudo-sample, the higherthe weight on theoretical priors. Bayesian ‘shrinkage’ procedures can be used to determine theoptimal weight on theory and data. For example, Ingram and Whiteman (1994) showed that usingpriors and cross-equation restrictions from a Real Business Cycle (RBC) model allowed for aconsiderable improvement in the performance of a VAR, compared with the unrestricted VARform and a VAR using the Minnesota (random walk) prior. Recent implementations include DelNegro and Schorfheide (2004).

In different contexts, it is conventional to refer to (2) as a measurement equation, reflecting theassumption that the linear transforms of state values in Cs will only be imperfect approximationsto observed data in y. For example, we do not observe ‘output’ or ‘marginal product of labour’directly, but have constructed measures such as ‘private sector value added at current prices’ and‘unit labour costs’.

Sargent (1989) exploited this structure to deal with issues about data mismeasurement. In hisschema, we would have (1) as before, but (2) would be augmented to include error terms:

yt = Cst + etet = Det−1 + ξ t

20

Project motivation and model design

As the error terms are assumed to represent measurement error, they are orthogonal: D and cov(et)are assumed to be diagonal. However, Ireland (2004) suggests that we interpret the errors as adhoc processes to make up for the misspecification of the model in fitting the data to y, by allowingD and cov(et) to have non-zero off-diagonal elements. In this case, the errors are not orthogonaland will be correlated with the elements in s in almost all cases. In other words, the theoreticalmodel embodied in the relations (1) and (2) is assumed to be wrong, and so the question, in thespirit of Watson (1993), is what needs to be done in e in order to match the data in y.

While much progress has been made in terms of numerical methods, these sorts of techniques haveonly been applied to relatively compact systems where the interpretation of the correspondingreduced-form VAR representation is relatively straightforward. It is not yet clear how the addedunobservable extrinsic dynamics in these models should be interpreted in terms of the demands ofa forecast process and the need to understand the underlying economic drivers of the forecast.Nonetheless, this literature holds some promise in terms of reconciling demands for theoreticalconsistency with coherence with the data.

21

Chapter 3 The core theory

This chapter summarises the core theory, describing the main building blocks, with attention to theinteractions between agents and the key assumptions. An overview of the core theory (Section 3.1) isfollowed in Section 3.2 by discussion of the objectives and constraints of the key agents: households,firms, the government, the monetary authority and the rest of the world. Section 3.3 describes how theseagents interact in markets for goods, labour and capital. This is followed in Section 3.4 by an account ofthe nominal side, including money market equilibrium and the price level, nominal wages and prices,inflation, and the monetary transmission mechanism. Section 3.5 deals with real trend growth, followedby a summary of the chapter in Section 3.6.

3.1 Overview

We can think of the core theory as an organising framework for analysing the economy. It should helpus tease apart competing explanations of what we observe in the data, by reminding us of the differentimplications of each story. To do this, the theory in the core model needs to be sufficiently rich andgeneral to handle a wide range of issues, while at the same time being compact enough to be tractable,reliable and clear. In order to secure the level of internal consistency that we want from the core model,we take an optimisation-based approach that begins with clear statements about how the key agents actin the face of constraints.

To this end, we wanted the theory to describe an economy where:

• households receive wage income and transfers from both firms and the government, and returnsfrom assets, while paying for a bundle of domestically produced and imported consumption goods,making investments in housing and financial assets (shares, bonds and money) and paying taxes tothe government;

• domestic firms receive income from selling final goods in domestic and overseas markets, whilepaying taxes and (potentially) receiving transfers from the government, paying for factor inputs ofdomestically sourced capital goods, imported capital goods, and labour. They finance this activitythrough the issue of equity and debt, and accumulating and decumulating inventories;

• the government generates revenue from taxes, new debt issuance and seigniorage, while purchasinggoods and services from firms and labour services from households, and servicing existing debt;

• the monetary authority sets a short-term nominal interest rate in order to achieve an inflation targetand, consequently, provides nominal stability; and

• the rest of the world provides capital, goods and services demanded by the domestic economy, andis a potential market for domestic production.

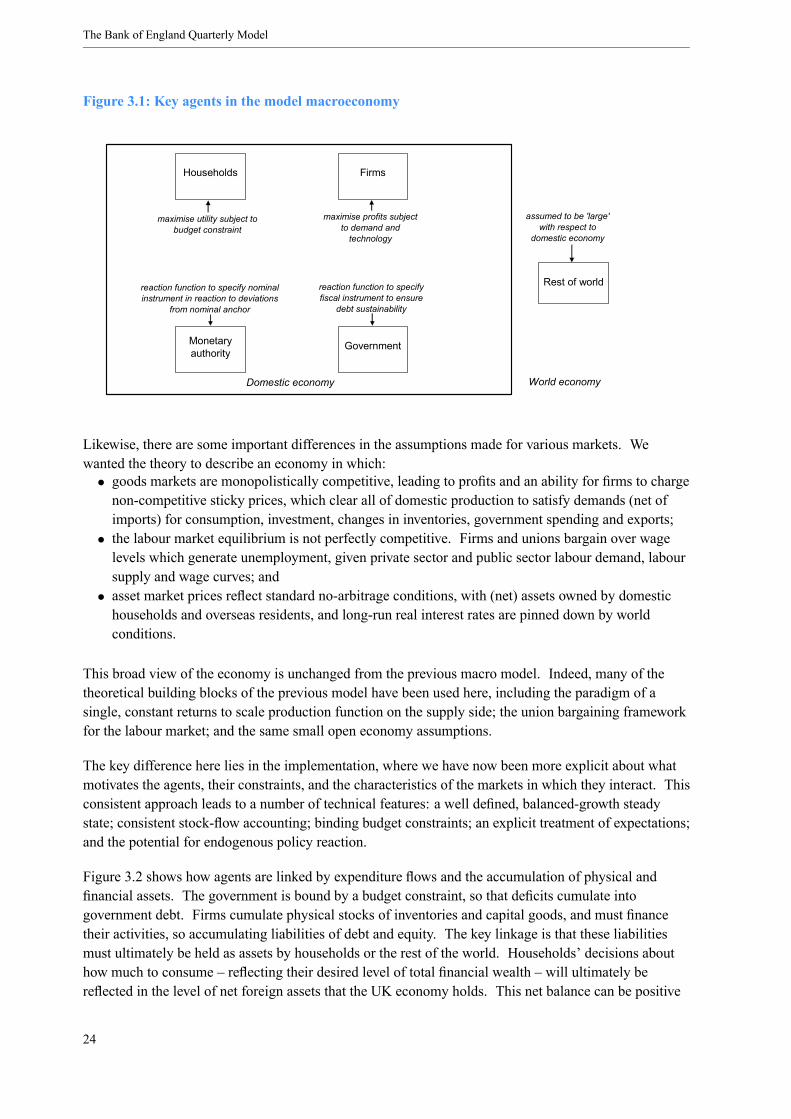

The core theory contains explicit decision rules and constraints that specify how these key agentsinteract with each other in markets for capital, financial assets, goods and labour. The treatment of theagents differs quite substantially: decision rules for households and firms arise out of explicitoptimisation problems, while the rest of the world is exogenous. The monetary authority and thegovernment are given simple reaction functions that specify policy targets and an endogenousinstrument. This description of the core model economy is illustrated in Figure 3.1.

23

The Bank of England Quarterly Model

Figure 3.1: Key agents in the model macroeconomy

Households Firms

GovernmentMonetary authority

Domestic economy World economy

maximise utility subject to budget constraint

maximise profits subject to demand and

technology

reaction function to specify nominal instrument in reaction to deviations

from nominal anchor

reaction function to specify fiscal instrument to ensure

debt sustainability

Rest of world

assumed to be 'large' with respect to

domestic economy

Likewise, there are some important differences in the assumptions made for various markets. Wewanted the theory to describe an economy in which:• goods markets are monopolistically competitive, leading to profits and an ability for firms to chargenon-competitive sticky prices, which clear all of domestic production to satisfy demands (net ofimports) for consumption, investment, changes in inventories, government spending and exports;

• the labour market equilibrium is not perfectly competitive. Firms and unions bargain over wagelevels which generate unemployment, given private sector and public sector labour demand, laboursupply and wage curves; and

• asset market prices reflect standard no-arbitrage conditions, with (net) assets owned by domestichouseholds and overseas residents, and long-run real interest rates are pinned down by worldconditions.

This broad view of the economy is unchanged from the previous macro model. Indeed, many of thetheoretical building blocks of the previous model have been used here, including the paradigm of asingle, constant returns to scale production function on the supply side; the union bargaining frameworkfor the labour market; and the same small open economy assumptions.

The key difference here lies in the implementation, where we have now been more explicit about whatmotivates the agents, their constraints, and the characteristics of the markets in which they interact. Thisconsistent approach leads to a number of technical features: a well defined, balanced-growth steadystate; consistent stock-flow accounting; binding budget constraints; an explicit treatment of expectations;and the potential for endogenous policy reaction.

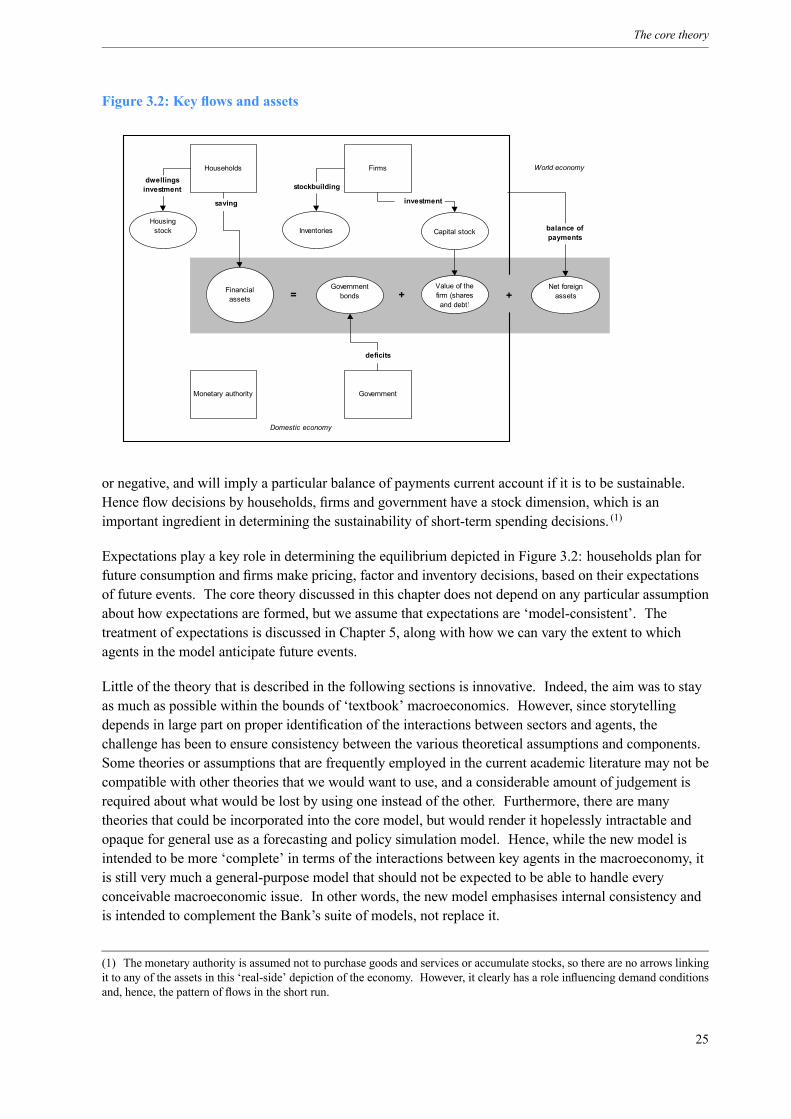

Figure 3.2 shows how agents are linked by expenditure flows and the accumulation of physical andfinancial assets. The government is bound by a budget constraint, so that deficits cumulate intogovernment debt. Firms cumulate physical stocks of inventories and capital goods, and must financetheir activities, so accumulating liabilities of debt and equity. The key linkage is that these liabilitiesmust ultimately be held as assets by households or the rest of the world. Households’ decisions abouthow much to consume – reflecting their desired level of total financial wealth – will ultimately bereflected in the level of net foreign assets that the UK economy holds. This net balance can be positive

24

The core theory

Figure 3.2: Key flows and assets

Households Firms

GovernmentMonetary authority

Financial assets

Government bonds

Value of the firm (shares and debt)

Housing stock Capital stock

Net foreign assets+

saving

deficits

investment

Domestic economy

World economy

balance of payments

Inventories

= +

dwellings investment stockbuilding

or negative, and will imply a particular balance of payments current account if it is to be sustainable.Hence flow decisions by households, firms and government have a stock dimension, which is animportant ingredient in determining the sustainability of short-term spending decisions. (1)

Expectations play a key role in determining the equilibrium depicted in Figure 3.2: households plan forfuture consumption and firms make pricing, factor and inventory decisions, based on their expectationsof future events. The core theory discussed in this chapter does not depend on any particular assumptionabout how expectations are formed, but we assume that expectations are ‘model-consistent’. Thetreatment of expectations is discussed in Chapter 5, along with how we can vary the extent to whichagents in the model anticipate future events.

Little of the theory that is described in the following sections is innovative. Indeed, the aim was to stayas much as possible within the bounds of ‘textbook’ macroeconomics. However, since storytellingdepends in large part on proper identification of the interactions between sectors and agents, thechallenge has been to ensure consistency between the various theoretical assumptions and components.Some theories or assumptions that are frequently employed in the current academic literature may not becompatible with other theories that we would want to use, and a considerable amount of judgement isrequired about what would be lost by using one instead of the other. Furthermore, there are manytheories that could be incorporated into the core model, but would render it hopelessly intractable andopaque for general use as a forecasting and policy simulation model. Hence, while the new model isintended to be more ‘complete’ in terms of the interactions between key agents in the macroeconomy, itis still very much a general-purpose model that should not be expected to be able to handle everyconceivable macroeconomic issue. In other words, the new model emphasises internal consistency andis intended to complement the Bank’s suite of models, not replace it.

(1) The monetary authority is assumed not to purchase goods and services or accumulate stocks, so there are no arrows linkingit to any of the assets in this ‘real-side’ depiction of the economy. However, it clearly has a role influencing demand conditionsand, hence, the pattern of flows in the short run.

25

The Bank of England Quarterly Model

3.2 Characterisation of the agents

3.2.1 Households

Households are important because their choice of a desired level of financial assets, given the supply ofdomestic assets, determines the long-run equilibrium for sustainable consumption, net foreign assets andthe trade balance. A key issue for the theory of the household is how this equilibrium is determined.We also want the household theory to account for the demand for real money balances, the demand forhousing, and the split of consumption between domestically produced and imported goods. Further, wewant some control over the short-run dynamic convergence to long-run equilibrium for these demands.Our approach starts with a standard utility-maximisation problem, but instead of dealing with a singlerepresentative agent, we aggregate individual decision rules to derive total demands for consumption,housing and money.

We consider first the optimisation problem for individuals: they aim to maximise lifetime utility subjectto their expected lifetime resources. The first source of utility is consumption of domestically producedand imported non-durable goods, and services from housing (which we treat as a very durable good).Individuals also gain utility from holding real money balances, which in this context can be thought of asan implicit requirement for cash for transactions. (2) Individuals also form habits and value leisuretime. (3) To keep the model as simple as possible, we abstract from public finance issues that might berelevant for a fiscal authority, so public goods do not enter utility and government consumption andinvestment do not benefit households directly. (4) Turning to income, households rent their labour tofirms or the government and receive wages in return (see Section 3.3.2). Households are also assumedto receive certain transfers directly from firms (such as corporate pension contributions), as well astransfers from the government (such as government benefits). To smooth consumption, households canborrow and save using a range of financial assets, including government securities, corporate bonds,shares and foreign bonds. (5)

A commonly used assumption is that of a representative agent who lives for ever, which would implythat the level of net foreign assets is not pinned down to a particular long-run equilibrium level. (6) Ourassumption that the domestic economy is small in relation to international capital markets implies that aninfinitely lived domestic agent would be able to borrow an infinite amount and pay it off in the indefinitefuture. If such domestic agents were ‘impatient’ relative to the rest of the world, domestic householdswould accumulate an infinite amount of net foreign debt; if domestic agents were more ‘patient’ than therest of the world, the domestic economy would acquire all the assets from the rest of world. (7) Thiswould violate the assumption that the domestic economy is small in relation to international capitalmarkets and is incompatible with our basic requirement that the interaction of agents in the modeldetermines a long-run sustainable equilibrium for consumption, net foreign assets and trade.

(2) Money is assumed to provide services that mitigate transactions frictions. Real money balances enter the utility functionadditively.(3) Technically, this is not implemented in the same way as conventional direct leisure in lifetime utility, and does not affectthe marginal propensity to consume. ‘Unions’ are assumed to bargain on behalf of workers – see Section 3.3.2.(4) As long as public goods enter utility additively, they would not affect consumption decisions in any case.(5) See Box 2 on page 30 for the consumer’s maximisation problem.(6) This model does have growth – see Section 3.5 – so that in what follows ‘consumption’ refers to the consumption-outputratio.(7) That is, if β (1+ r) > 1, where β is the individual’s discount factor and r a real return on assets, then consumption willsteadily grow and foreign assets will fall. Conversely, if β (1+ r) < 1 then consumption will steadily fall and foreign assetswill rise. See Chapter 3 of Barro and Sala-i-Martin (1995).

26

The core theory

There are several modifications to the infinitely lived representative agent model that renderconsumption stationary. (8) However, these methods typically imply that one of consumption, netforeign assets or the current account has to return to a predetermined value, rather than each reactingendogenously to shocks, as we would like. In addition, they usually require that the household rate oftime preference equals a constant foreign real interest rate, which is an unattractive feature in our casebecause movements in foreign real interest rates can be a key forecast issue. Further, these modelstypically preclude discussions of ‘pure’ wealth effects, which would further restrict the ability of themodel to analyse forecast issues. (9)

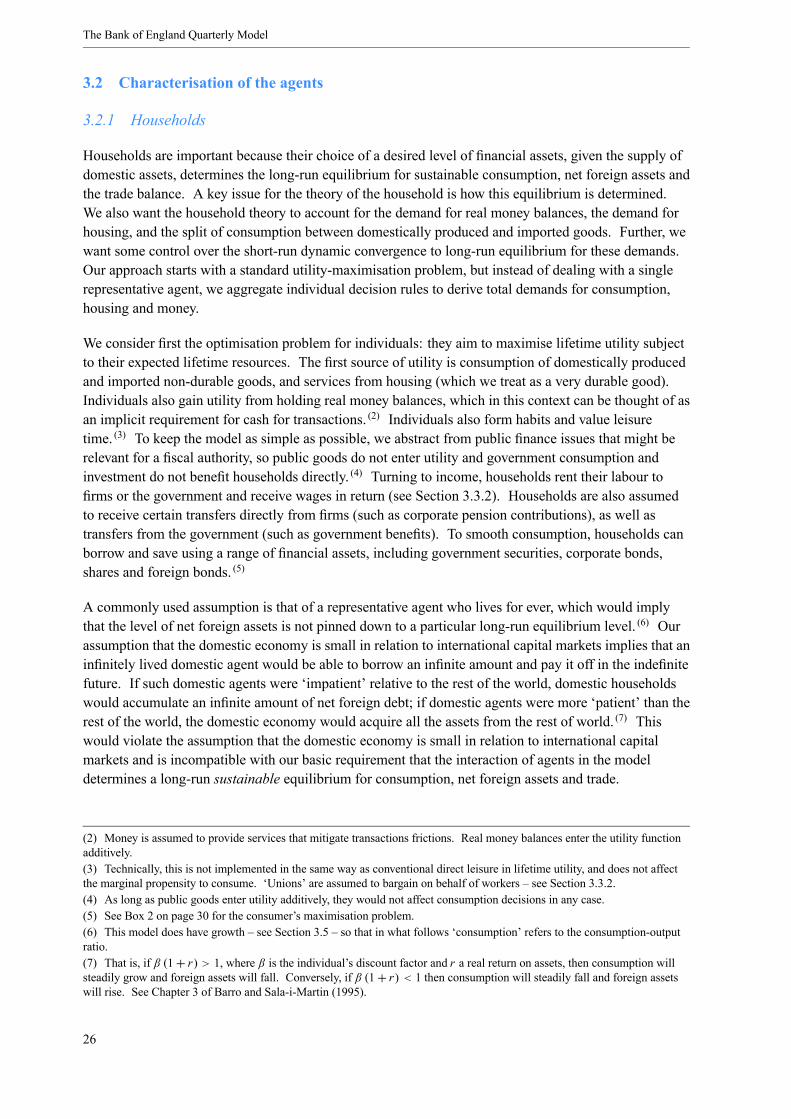

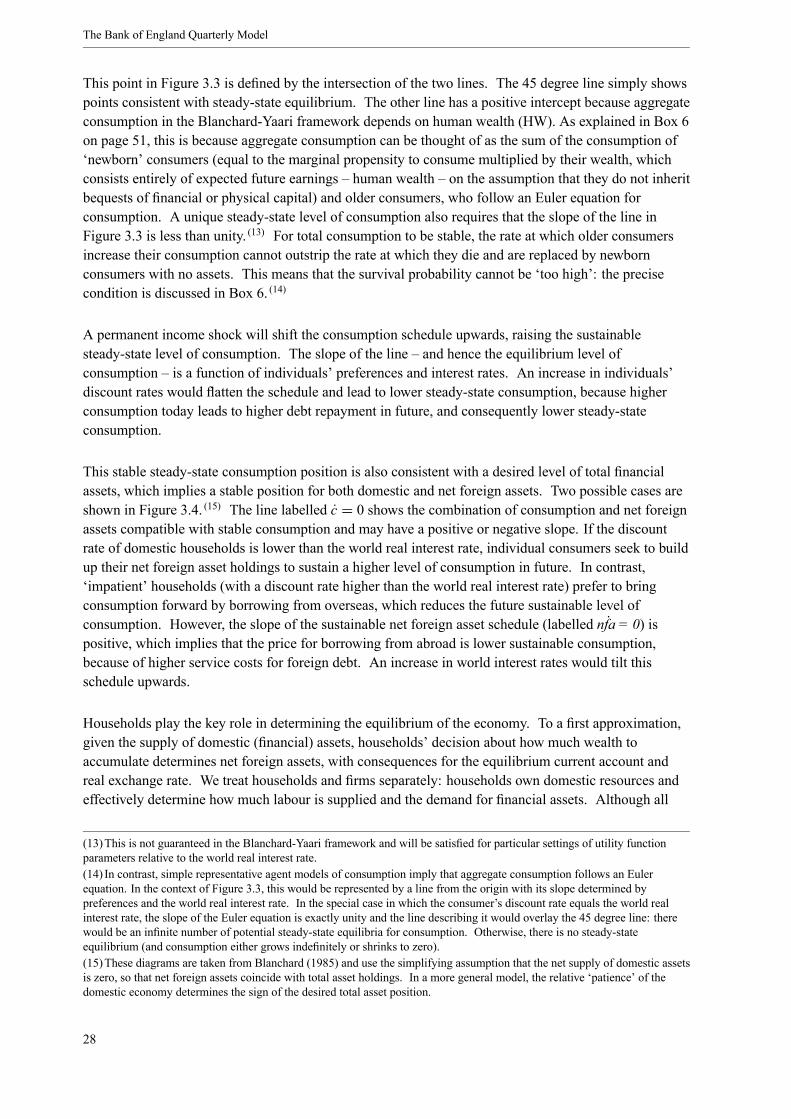

Instead, we ensure that consumption is stationary by assuming that households do not live for ever. Inparticular, following Blanchard and Yaari, (10) we assume that individual households face a constantprobability of survival from period to period, with new households being born to replace those that havedied. As with a representative agent model, they aim to maximise expected utility, subject to aperiod-by-period budget constraint with a standard transversality condition imposed. (11) This leads tointertemporal conditions for individuals (such as the consumption Euler condition) that are the same asin the infinitely lived representative agent case. Aggregate consumption, however, is stationary. Theintuitive reason is that, because individuals do not expect to live forever, households in aggregate areprevented from borrowing or saving unlimited amounts. When we aggregate over the entire population,the aggregate economy settles on a constant ratio of consumption to income in the long run. (Box 6 onpage 51 explains this formally in a simplified model.) This can be represented in Figure 3.3, (12) wherethe long-run consumption level (abstracting from growth) is defined by the point where ct = ct−1 = c∗.

Figure 3.3: Consumption equilibrium in the steady state

c t

c *c t = f (ct -1,HW t )

c * c t-1

45°