Embed Size (px)

DESCRIPTION

Pie Investment Analyst Mike Ross discusses Auckland’s housing market and asks, is the equation sustainable?

Citation preview

The Auckland Property Market

WHERE TO FROM HERE?

Pie Investment Analyst Mike Ross discusses Auckland’s housing market and asks, is the equation sustainable?

4 SLICE OF PIE. JUNE 2016

5 SLICE OF PIE. JUNE 2016

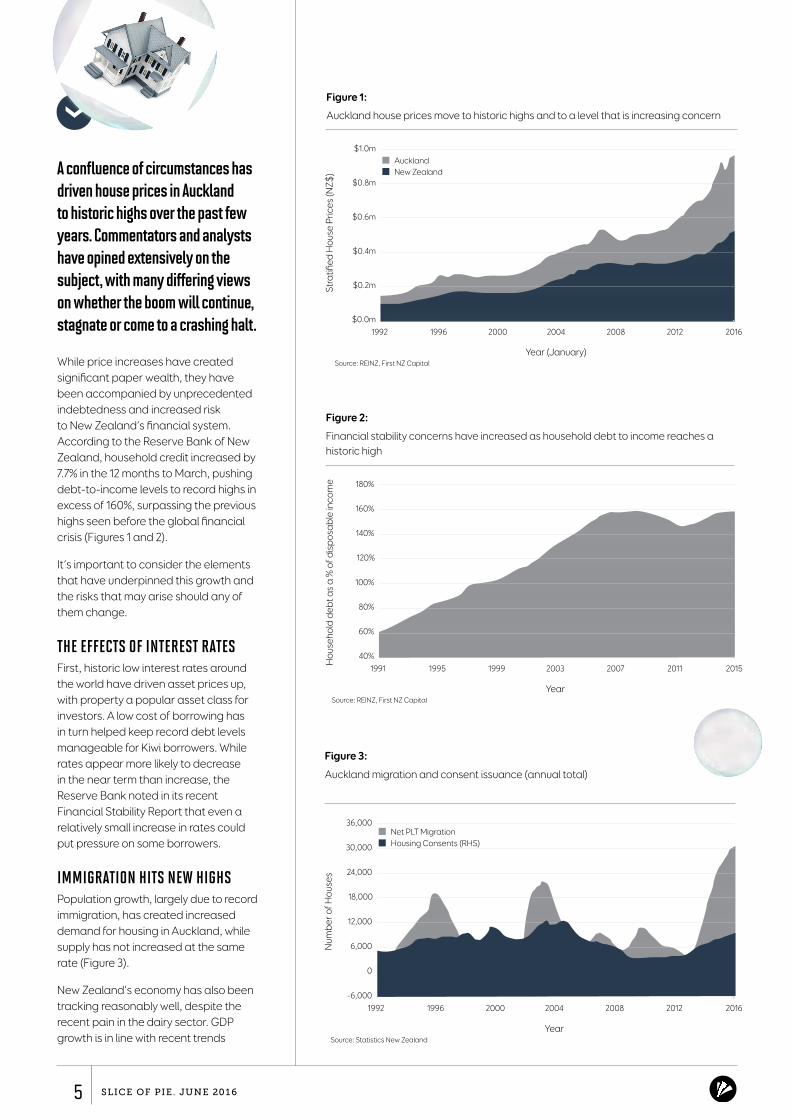

A confluence of circumstances has driven house prices in Auckland to historic highs over the past few years. Commentators and analysts have opined extensively on the subject, with many differing views on whether the boom will continue, stagnate or come to a crashing halt.

While price increases have created significant paper wealth, they have been accompanied by unprecedented indebtedness and increased risk to New Zealand’s financial system. According to the Reserve Bank of New Zealand, household credit increased by 7.7% in the 12 months to March, pushing debt-to-income levels to record highs in excess of 160%, surpassing the previous highs seen before the global financial crisis (Figures 1 and 2).

It’s important to consider the elements that have underpinned this growth and the risks that may arise should any of them change.

THE EFFECTS OF INTEREST RATESFirst, historic low interest rates around the world have driven asset prices up, with property a popular asset class for investors. A low cost of borrowing has in turn helped keep record debt levels manageable for Kiwi borrowers. While rates appear more likely to decrease in the near term than increase, the Reserve Bank noted in its recent Financial Stability Report that even a relatively small increase in rates could put pressure on some borrowers.

IMMIGRATION HITS NEW HIGHSPopulation growth, largely due to record immigration, has created increased demand for housing in Auckland, while supply has not increased at the same rate (Figure 3).

New Zealand’s economy has also been tracking reasonably well, despite the recent pain in the dairy sector. GDP growth is in line with recent trends

Figure 1:

Auckland house prices move to historic highs and to a level that is increasing concern

Source: REINZ, First NZ Capital

$1.0m

$0.8m

$0.6m

$0.4m

$0.2m

$0.0m1992 1996 2000 2004 2008 2012 2016

Stra

tified

Hou

se P

rices

(NZ$

)

AucklandNew Zealand

Year (January)

Figure 2:

Financial stability concerns have increased as household debt to income reaches a historic high

Source: REINZ, First NZ Capital

180%

140%

160%

120%

100%

80%

60%

40%1991 1995 1999 2003 2007 2011 2015

Hou

seho

ld d

ebt a

s a

% o

f dis

posa

ble

inco

me

Year

Figure 3:

Auckland migration and consent issuance (annual total)

Source: Statistics New Zealand

36,000

24,000

30,000

18,000

12,000

6,000

0

-6,0001992 1996 2000 2004 2008 2012 2016

Num

ber o

f Hou

ses

Net PLT MigrationHousing Consents (RHS)

Year

and unemployment has been relatively flat. A strong housing market and the associated paper wealth helps to drive consumer confidence.

Although these pillars are propping up the housing market at present, should one or more start to roll over, then the equation begins to look unsustainable. Most key drivers of the housing boom are cyclical by nature, and so will inevitably reverse.

FEAR OF MISSING OUTMany buyers seem to forget this, rushing to the market for fear of missing out. They feel the market running away from them and the longer they leave it the less affordable it becomes. They’re willing to borrow multiples of their income without giving much thought to the potential downside should the market turn. Many seem to forget that house prices do go down.

One only needs to look back a few years to the Global Financial Crisis. Kiwis were relatively insulated from the fallout of the GFC – the 10% drop in the local housing market paled in comparison to the 30-40% falls seen in the United States and parts of Europe.

While it is true recent falls in the domestic property market have been short in duration and quick to recover, the experience abroad should be the benchmark for risk when assessing our current housing market. With debt-to-income at historic highs and interest rates at historic lows, we are in unchartered territory.

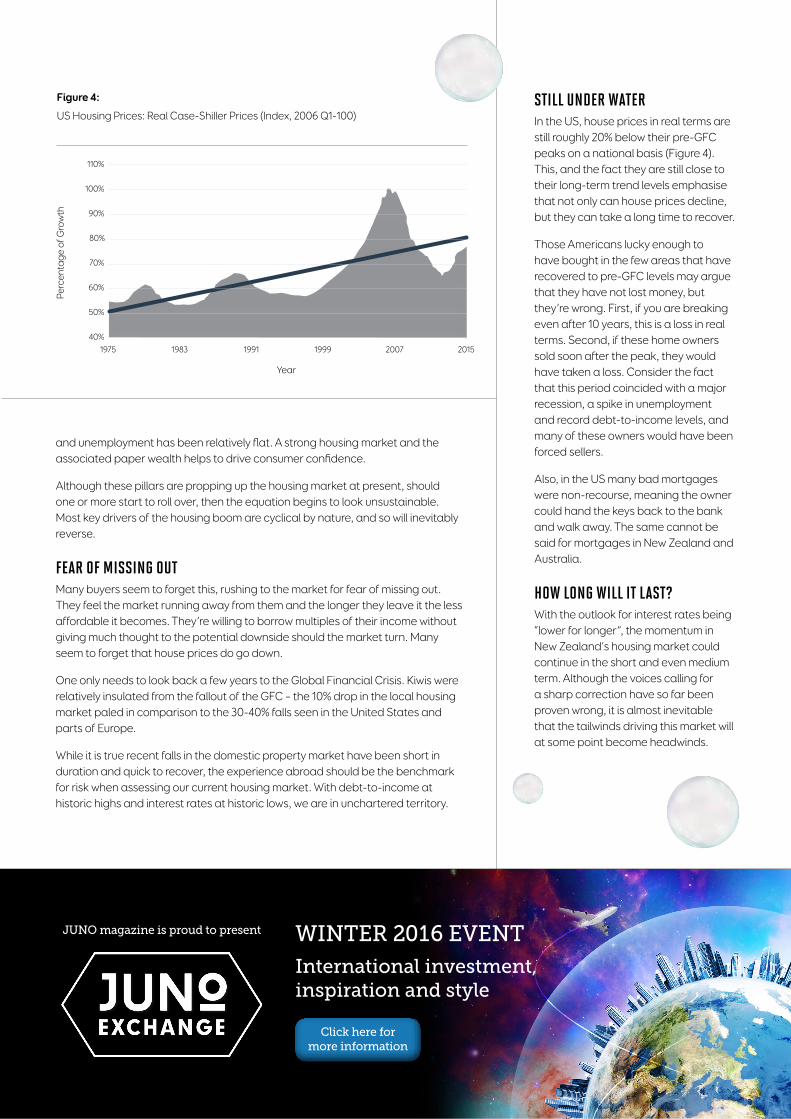

Figure 4:

US Housing Prices: Real Case-Shiller Prices (Index, 2006 Q1-100)

110%

90%

100%

80%

70%

60%

50%

40%1975 1983 1991 1999 2007 2015

Perc

enta

ge o

f Gro

wth

Year

STILL UNDER WATERIn the US, house prices in real terms are still roughly 20% below their pre-GFC peaks on a national basis (Figure 4). This, and the fact they are still close to their long-term trend levels emphasise that not only can house prices decline, but they can take a long time to recover.

Those Americans lucky enough to have bought in the few areas that have recovered to pre-GFC levels may argue that they have not lost money, but they’re wrong. First, if you are breaking even after 10 years, this is a loss in real terms. Second, if these home owners sold soon after the peak, they would have taken a loss. Consider the fact that this period coincided with a major recession, a spike in unemployment and record debt-to-income levels, and many of these owners would have been forced sellers.

Also, in the US many bad mortgages were non-recourse, meaning the owner could hand the keys back to the bank and walk away. The same cannot be said for mortgages in New Zealand and Australia.

HOW LONG WILL IT LAST?With the outlook for interest rates being “lower for longer”, the momentum in New Zealand’s housing market could continue in the short and even medium term. Although the voices calling for a sharp correction have so far been proven wrong, it is almost inevitable that the tailwinds driving this market will at some point become headwinds.

WINTER 2016 EVENT

International investment, inspiration and style

JUNO magazine is proud to present

Click here for more information

![Request for Proposal (RFP) for Property Management · PDF file1 Request for Proposal (RFP) for Property Management System [Hotel Name Here] Owned by: [Owner Name Here] [Date Here]](https://img.pdfslide.us/doc/110x75/5a89b6697f8b9adb648b921c/request-for-proposal-rfp-for-property-management-request-for-proposal-rfp.jpg)

![Property Flyers… · To reset credentials, Click Here To enter property data manually, Click here. If you need to reload a file that you had previously uploaded, Click Here. C] Check](https://img.pdfslide.us/doc/110x75/5f15d6b55cc8315ae701282e/property-flyers-to-reset-credentials-click-here-to-enter-property-data-manually.jpg)

![Request for Proposal (RFP) for Property Management System ... · Property Management System [Hotel Name Here] Owned by: [Owner Name Here] [Date Here] This template is provided for](https://img.pdfslide.us/doc/110x75/605b91aae558a017c53d2e0e/request-for-proposal-rfp-for-property-management-system-property-management.jpg)