Embed Size (px)

Citation preview

The Association between Management Earnings Forecast Errors and Accruals

Guojin Gong Department of Accounting Smeal College of Business

Pennsylvania State University [email protected]

Laura Yue Li

Department of Accountancy College of Business

University of Illinois at Urbana-Champaign [email protected]

Hong Xie

Lubin School of Accounting Whitman School of Management

Syracuse University [email protected]

April 2008

We would like to thank Leslie Hodder (FARS discussant), Xiaoling Chen, Dan Givoly, Steven Huddart, Bin Ke, Andrew Leone, James McKeown, Mort Pincus, Yong Yu, Theodore Sougiannis, Raghu Venugopalan, and workshop participants at the 2008 Financial Accounting and Reporting Section (FARS) Annual Meeting, Kansas University, Pennsylvania State University, University of Illinois at Urbana-Champaign, and Syracuse University for helpful comments.

The Association between Management Earnings Forecast Errors and Accruals

ABSTRACT

We investigate the association between the errors in management forecasts of next year’s earnings and current year’s accruals. We propose that managers’ assessment about their firms’ business prospects is necessarily imperfect given the uncertainty in the operating environment. When managers’ imperfect business assessment manifests in both accrual generation and earnings forecasts, managers likely display greater optimism (pessimism) in forecasting earnings when accruals are relatively high (low). Consistent with our proposition, we find a positive association between management earnings forecast errors and accruals, and this positive association is stronger for firms operating in a highly uncertain business environment and for industries exhibiting strong co-variation between accruals and employee growth. Supplementary analysis reveals that the presence of management earnings forecasts does not significantly reduce accrual mispricing. Overall, our results support the view that voluntarily disclosed information may contain errors that are predictable based on mandatorily reported information, which potentially limits the efficacy of voluntary disclosure in assisting investors to better understand mandatorily reported information.

Keywords: voluntary disclosure; management earnings forecasts; mandatory disclosure;

accruals. Data Availability: Data used in this study are available from sources indicated in the paper.

1

I. INTRODUCTION

Mandatory and voluntary disclosures represent two important channels by which

managers communicate information to outside shareholders.1 While a considerable literature has

shown that both corporate disclosures contain value-relevant information and significantly

influence security prices (see Kothari (2001) and Healy and Palepu (2001) for literature reviews),

the question of whether voluntarily disclosed information contains errors that can be predicted

based on mandatorily reported information is largely unexplored in the extant research. A formal

investigation of this issue can further our understanding of the informational value of voluntary

disclosure which has important implications for investors and standard setters.

In this paper we examine the association between the errors in management forecasts of

next year’s earnings and current year’s accruals. We are interested in accruals and management

earnings forecasts because both accrual creation and earnings forecasts involve a high degree of

managerial subjectivity. We propose that, under an uncertain operating environment, managers’

knowledge about their firms’ business prospects is necessarily imperfect, which results in

unintentional errors in managers’ assessment of future firm performance. When managers have

flexibility to convey their imperfect business assessment through both accruals and earnings

forecasts, these two information disclosures likely contain common errors. Therefore, we expect

managers to display greater optimism (pessimism) in forecasting earnings when accruals are

relatively high (low).2

1 The U.S. Securities and Exchange Commission (SEC) mandates a variety of corporate filings that provide information on firms’ financial performance, governance structure, compensation practice, and major corporate transactions. Managers also voluntarily provide the capital market with additional relevant disclosures through forecasts of key accounting numbers (such as earnings, cash flows and sales), press releases, conference calls, internet sites, and other communication channels. 2 See Section II for further discussions of our conjecture.

2

Our proposition that managers’ imperfect foresight manifests in both voluntary and

mandatory disclosures is in line with recent studies showing that managers’ personal beliefs

affect multiple dimensions of corporate decisions. Malmendier and Tate (2005, 2008) show that

CEOs who overestimate the future returns of their firms (measured by a failure to divest

company-specific risk on their personal accounts) tend to undertake excessive capital

investments or pursuit unnecessary acquisitions when they have abundant internal funds at their

disposal. Ben-David et al. (2007) further document that CFO overconfidence (measured as mis-

calibrated beliefs based on a survey) induces distortions in a series of corporate decisions,

including investing, external financing and payout decisions. Similar to these studies, our

proposition that managers’ imperfect assessment of business prospects simultaneously affects

both mandatory and voluntary disclosures is consistent with the spillover effect of managerial

judgmental errors from one domain to another.

Using the First Call’s Company Issued Guidance (“CIG”) database, we find a

significantly positive association between management earnings forecast errors (defined as

forecasted earnings minus actual earnings) and accruals. If this positive association indeed stems

from unintentional errors in managers’ assessment of business prospects, we expect to observe a

stronger positive association among firms operating in a more uncertain business environment

where managers’ projection errors are likely to be more substantial. Empirical results confirm

our expectation. We find that the positive relation between management forecast errors and

accruals is stronger for firms having higher sales growth volatility, higher cash flow volatility, or

longer operating cycle.

Even with uncertainty in the operating environment, a positive association between

management forecast errors and accruals may not exist if managers have little flexibility in

3

conveying their business assessment through accruals. The degree to which managers can utilize

accruals to convey their subjective beliefs varies depending on the nature of the business,

industry practice, and available accounting choices allowed by the Generally Accepted

Accounting Principles (GAAP). If the positive association between management forecast errors

and accruals arises as a result of managerial judgmental errors being revealed in both information

disclosures, we expect to find a stronger positive association for firms exhibiting higher co-

variation between accruals and growth-related activities that capture managers’ assessment of

business prospects (e.g., employee growth as proposed by Zhang (2007)). Empirical results show

that for industries in which accruals highly co-vary with employee growth, management forecast

errors exhibit significantly positive relation with accruals. In contrast, for industries in which

accruals show little co-variation with employee growth, the relation between management

forecast errors and accruals is insignificant. These findings lend further support to the

proposition that common errors imbedded in managers’ business assessment manifest in both

accruals and earnings forecasts, which induces a positive relation between management forecast

errors and accruals.

We recognize that the positive relation between management forecast errors and accruals

may also arise from managers’ intentional misrepresentation in both information disclosures for

the purpose of reaping private benefits. To shed some light on this issue, we use managers’

trading direction (i.e., purchase or sale) as indication of their true beliefs concerning future

business prospects. We find that the association between management forecast errors and

accruals is significantly positive when the level of accruals more likely reflects managers’ true

beliefs about future firm performance (such as high/low accruals followed by share

purchases/sales). On the other hand, this association is virtually non-existent when accruals are

4

more likely manipulated to enhance managers’ trading profitability (such as high/low accruals

followed by share sales/purchases). These findings do not support the intentional

misrepresentation view that managers manipulate accruals and earnings forecasts in the same

direction in order to boost trading gains, but are consistent with the notion that both accruals and

earnings forecasts reflect managers’ unintentional errors about firms’ business prospects. One

explanation for these findings is that high litigation risk surrounding insider trading deters

managers from issuing intentionally biased public earnings forecasts which are easily verified ex

post. Nevertheless, managers potentially face a variety of economic incentives (besides insider

trading) when making disclosure decisions. We acknowledge that our study cannot completely

rule out this intentional misrepresentation explanation and additional research is required to fully

discriminate between competing explanations for managers’ accrual-related forecast errors.

This paper extends the literature on the interaction between mandatory and voluntary

disclosures. Prior research has proposed that voluntary disclosure provides useful information

that helps outsiders better understand financial information reported in regulatory filings (e.g.,

Kimbrough 2005; Drake et al. 2007; Louis et al. 2007). However, our results indicate that when

mandatory reporting (such as accruals) and voluntary disclosure (such as management earnings

forecasts) both involve a high degree of managerial subjectivity, mandatory and voluntary

disclosures may display common errors, which potentially undermines the informational value of

voluntary disclosure in facilitating more efficient pricing of mandatorily reported information.

Indeed, our supplementary analysis suggests that the availability of management earnings

forecasts has no significant impact on accrual mispricing.

Our study also provides new evidence for the management earnings forecast literature.

Prior research has proposed various factors (such as information asymmetry, managerial

5

incentives, and managers’ personal traits) that may affect the issuance and properties of

management earnings forecasts (See Hirst et al. (2007) for a recent literature review). We add to

this literature by showing that management earnings forecasts contain predictable errors in

relation to historically reported accruals. Our results caution investors to carefully evaluate

management earnings forecasts in forming their earnings expectations, especially when the firm

operates in a highly uncertain business environment or belongs to an industry where accruals

highly co-vary with growth-related activities.

Furthermore, our findings have important implications for regulators and standard setters.

Before drafting accounting standard changes or proposing disclosure-related policies, regulators

and standard setters need to consider the possibility that mandatory and voluntary disclosures

may display common errors under certain circumstances. Encouraging expanded voluntary

disclosure or greater managerial subjectivity in financial reporting may not necessarily improve a

firm’s information environment if the resulting corporate disclosures simply reflect the common

errors in managers’ assessment of business prospects.

Finally, our study offers complementary evidence to the accrual mispricing literature.

The accrual mispricing literature since Sloan (1996) has not reached a consensus regarding

whether the accrual-based hedge portfolio returns reflect market mispricing of accruals or

compensation for higher risk associated with extreme accruals. 3 Our findings indicate that

managers, similar to financial analysts (Bradshaw et al. 2001), 4 make more optimistic

3 Prior research on accrual mispricing mostly concurs that the accrual-based hedge portfolio returns reflect investors’ inefficient processing of accruals information (e.g., Sloan 1996; Bradshaw et al. 2001; Collins et al. 2003; Fairfield et al. 2003). Recently, a few studies propose rational explanations for the accrual-based hedge portfolio returns (e.g. Khan 2007; Ng 2005; Wu et al. 2007). Furthermore, Kraft et al. (2006) identify a few research design flaws that exist in prior accrual mispricing studies. 4 Bradshaw et al. (2001) find a positive association between analyst earnings forecast errors (defined as analyst consensus forecasts minus actual earnings) and accruals. They interpret this finding as analysts failing to efficiently assess the future earnings implications of accruals in forming earnings expectations, which supports the mispricing interpretation of the accrual-based hedge portfolio returns.

6

(pessimistic) earnings forecasts following periods of high (low) accruals. Given management

earnings forecasts significantly affect market earnings expectations (e.g., Ajinkya and Gift 1984;

Waymire 1984; Pownall and Waymire 1989), we thus provide additional corroborating evidence,

in a similar spirit to Bradshaw et al. (2001), that the accrual anomaly is at least partly driven by

market participants’ failure to correctly assess the future earnings implications of accruals.

The remainder of the paper is organized as follows. In the next section we review related

literature. Section III develops our hypotheses. Section IV describes the sample selection process

and the empirical regression model used to test the relation between management earnings

forecast errors and accruals. Section V presents and discusses empirical results. Section VI

provides supplementary analysis concerning the impact of management earnings forecasts on

accrual mispricing. The study concludes in Section VII.

II. RELATED LITERATURE

Prior Literature on Management Earnings Forecast Errors

Prior studies have proposed various incentive-related factors that may motivate managers

to bias their earnings forecasts for the purpose of inflating market earnings expectations (Frost

1997; Koch 1999; Rogers and Buskirk 2006), deterring industry entrants (Newman and Sansing

1993); facilitating equity issuance (Frankel et al. 1995; Lang and Lundholm 2000), improving

trading profitability (Aboody and Kasznik 2000; Noe 1999; Rogers and Stocken 2005), or

reducing expected legal costs (Skinner 1994, 1997; Baginski et al. 2002; Rogers and Stocken

2005). Asides from managerial incentives, McNichols (1989) finds that management earnings

forecasts contain predictable errors in relation to historical stock returns, suggesting that

managers fail to efficiently incorporate information contained in past stock prices in their

7

earnings forecasts. Despite these studies, little research has examined the relation between

management earnings forecast errors and mandatorily reported accounting information.

Prior Literature on the Relation between Mandatory and Voluntary Disclosures

Prior studies examining the relation between mandatory and voluntary disclosures are

motivated primarily from the discretionary nature of voluntary disclosure. Analytically, Einhorn

(2005) demonstrates that various features of mandatory reporting (such as the level of discretion

in mandatory reporting and the information quality of mandatory disclosure) affect managers’

propensity to provide voluntary disclosure. Empirically, it is well documented that volatile

earnings tend to reduce the frequency of management earnings forecasts (e.g., Waymire 1985;

Cox 1985; Imhoff 1978). More recently, Francis et al. (2008) find that firms exhibiting good

earnings quality provide a larger quantity of voluntary disclosures in annual reports and 10Ks

than firms exhibiting poor earnings quality.

Several other studies use market-based measures of mandatory reporting properties to

examine the relation between mandatory and voluntary disclosures. Lennox and Park (2006) find

that historical earnings response coefficient is positively associated with management’s issuance

of earnings forecasts. However, Lang and Lundholm (1993) find a negative association between

the earnings-return correlation and AIMR disclosure ratings, and Tasker (1998) also documents a

negative association between her proxy for financial statement informativeness and the

occurrence of conference calls.

Overall, this line of research has mostly focused on the occurrence or the quantity of

voluntary disclosure and its relation with mandatory reporting properties. In this paper we extend

prior research by examining the error in voluntarily disclosed forward-looking information (i.e.,

8

management earnings forecast errors) and its relation with a key aspect of mandatory reporting,

accruals.5

III. HYPOTHESIS DEVELOPMENT

Relation between Management Earnings Forecast Errors and Accruals

We propose that mandatory and voluntary disclosures likely contain common errors

resulting from managers’ imperfect assessment of business prospects being reflected in both

disclosures. A firm’s operating environment is replete with uncertainty due to changing business

conditions (such as unpredictable shifts in market demand and competitor strategies). This

implies that managers’ knowledge of their firms’ business environment is necessarily imperfect.

Managers’ imperfect knowledge unavoidably generates errors in managers’ assessment of firms’

business prospects. In addition, uncertainty in operating environment may induce or exacerbate

managers’ cognitive biases in processing information (e.g., Hirshleifer 2001; Zhang 2006),

which also lead to errors in managers’ assessment of business prospects. When managers

communicate their biased business assessment through both voluntary and mandatory disclosures,

these two information disclosures likely contain common errors.

To empirically test this conjecture, we examine whether the errors in management

forecasts of next year’s earnings (defined as forecasted earnings minus actual earnings) are

positively related to current year’s accruals. We focus on management earnings forecasts instead

of other forms of voluntary disclosure because, in addition to reflecting managers’ projections

5 A related paper by Kasznik (1999) examines the relation between management earnings forecasts and discretionary accruals. He predicts and finds that legal costs and reputation concerns motivate managers to inflate accruals in order to minimize optimistic forecast errors. The key difference between our study and Kasznik (1999) is that we focus on current accruals and their relation with management forecasts of future earnings, while Kasnik (1999) focuses on future accruals reported after management earnings forecasts.

9

about future firm performance, these forecasts are quantitative and ex post verifiable.6 We

choose to examine accruals because reporting accruals involves substantial managerial

projections about firms’ business prospects. Since forecasting earnings and reporting accruals

both involve a high degree of managerial subjectivity, errors imbedded in managers’ business

assessment likely manifest in both management earnings forecasts and accruals. For instance,

when managers are optimistic (pessimistic) about the firm’s future market demand, they tend to

over- (under-) stock inventory, thus creating high (low) level of accruals through increases in

inventory.7 At the same time, management earnings forecasts would display similar optimism

(pessimism) reflecting managers’ personal beliefs about future firm performance. Therefore, we

hypothesize that management earnings forecasts contain greater optimistic (pessimistic) errors

when accruals are relatively high (low), or a positive relation between management earnings

forecast errors and accruals.8

H1: There is a positive association between management earnings forecast errors and accruals.

Impacts of Uncertainty in Operating Environment and Accruals-Growth Co-variation

A positive association between management forecast errors and accruals (as proposed

above) will exist as long as the following two conditions hold. First, there is uncertainty in the

operating environment such that managers unavoidably commit errors in assessing their firms’

business prospects. Second, managers have flexibility to convey their subjective assessment

6 In contrast, other types of voluntary disclosures are not necessarily followed by confirmatory reports for verification (such as projections of market trend) or do not reveal forward-looking information (such as disclosures of historical customer satisfaction). 7 Similarly, when managers are optimistic (pessimistic) about the collectibility of existing accounts receivable, they tend to under- (over-) estimate receivable allowances, thus creating high (low) level of accruals through increases in accounts receivable. 8 Besides reflecting managers’ personal assessment about firms’ business prospects, accruals are also influenced by firms’ underlying economics. In subsequent empirical tests, we control for various firm characteristics (such as operating performance and growth) to account for firms’ underlying economics that may affect accruals.

10

about firms’ business prospects through both accruals and earnings forecasts. The cross-sectional

variations in environmental uncertainty and in managerial reporting flexibility, thus, have

predictable implications to our proposition.

Greater uncertainty in operating environment naturally results in greater errors in

managers’ assessment of firms’ business prospects. Greater uncertainty also leaves more room

for psychological biases (Hirshleifer 2001). Hence, under a more uncertain operating

environment, management earnings forecasts and accruals are likely affected to a greater extent

by common errors in managers’ business assessment. We therefore expect to observe a stronger

positive association between management forecast errors and accruals when there is greater

uncertainty in firms’ operating environment.

H2: The positive association between management earnings forecast errors and accruals is stronger for firms operating in a more uncertain business environment.

Even with uncertainty in the operating environment, a positive association between

management forecast errors and accruals may not exist unless managers are allowed to convey

their biased assessment through both disclosure channels. While management earnings forecasts

largely reflect managers’ personal beliefs regarding future firm performance, reported accruals

may not. The degree to which accruals convey managers’ subjective assessment varies with the

nature of the business, industry practice, and available accounting choices allowed by GAAP.

For example, managers in retail industries may increase inventory purchases to convey their

expectations of improving future market demand. However, such a strategy would not be

applicable to service industries or firms with no inventories. When managers have limited

flexibility in communicating their projections through accruals, the errors imbedded in

11

management earnings forecasts may not appear in accruals, thus weakening the positive

association between management forecast errors and accruals.

We use the co-variation between accruals and managers’ growth-related activities to

measure managerial flexibility in using accruals to convey their subjective assessment.9 The

premise is that growth-related activities capture managers’ assessment of their firms’ business

prospects. If managers have plenty of flexibility to convey their business assessment through

accruals, we would observe high co-variation between accruals and growth-related activities. We

therefore hypothesize that firms exhibiting high co-variation between accruals and growth-

related activities have a stronger positive association between management forecast errors and

accruals.

H3: The positive association between management earnings forecast errors and accrualsis stronger for firms exhibiting high co-variation between accruals and growth-related activities.

An Alternative Explanation – Intentional Misrepresentation of Information Disclosures

We have proposed that unintentional errors in managers’ assessment of future business

prospects result in a positive association between management forecast errors and accruals.

However, we recognize that this positive association could also arise from managers’ intentional

misrepresentation of multiple information disclosures for the purpose of reaping private benefits.

Such intentional misrepresentation is costly to managers due to potential legal actions from

shareholders (e.g., Skinner 1994, 1997; Francis et al. 1994) and loss of reputation (e.g., Williams

1996; Hutton and Stocken 2007). Nevertheless, the expanded safe-harbor provisions in the

Private Securities Litigation Reform Act of 1995 alleviate the legal concern associated with

9 See Section 4 for the measurement of the co-variation between accruals and managers’ growth-related activities.

12

forward-looking disclosures, which potentially increases managers’ propensity for intentional

misrepresentation.

Managers have various incentives to bias their earnings forecasts and reported accruals.

For instance, managers may manipulate accruals downwards prior to share repurchases or stock

option grants to boost potential gains from repurchased stocks or awarded stock options (Gong et

al. 2008; Baker et al. 2003), and these firms may also provide pessimistic earnings forecasts prior

to these events (Brockman et al. 2008; Aboody and Kasznik 2000). Alternatively, external

financing activities may motivate managers to inflate accruals (Teoh et al. 1998a, 1998b) and

knowingly introduce optimistic biases to voluntary disclosures (Lang and Lundholm 2000),

although empirical evidence is still mixed concerning these conjectures (Ball and Shivakumar

2007; Shivakumar 2000; Frankel et al. 1995). 10 It is worth noting that prior studies only

separately examine managers’ manipulation of accruals versus management earnings forecasts.

Whether managers simultaneously utilize both information disclosures to reap private benefits

remains an empirical issue.

Rather than providing a comprehensive examination of various managerial incentives,

which is beyond the scope of our study, we choose to examine insider trading to distinguish the

intentional misrepresentation explanation from the unintentional mis-assessment view. Insider

trading (executed subsequent to management earnings forecasts) has potential to reflect

managers’ assessment of business prospects and at the same time, possibly reveal their

10 Teoh et al. (1998a, 1998b) show that firms inflate earnings prior to initial public offerings (IPOs) and seasoned public offerings (SEOs), but Ball and Shivakumar (2007) conclude that the average IPO firm does not inflate earnings prior to the IPO. In addition, Shivakumar (2000) proposes that the documented earnings inflation prior to SEOs results from managers’ rational response to anticipated investor reactions at offering announcements rather than the intention to deceive investors. Regarding voluntary disclosure, Frankel et al. (1995) find that external financing activities (including both equity and bond issuances) do not lead to more optimistically biased management earnings forecasts. However, Lang and Lundhom (2000) document that firms that substantially increase their disclosure activities prior to SEOs experience price increases prior to the offering, suggesting that SEO firms increase voluntary disclosures to “hype the stock.”

13

manipulative incentives. Specifically, we rely on the trading direction to infer managers’ true

beliefs about future firm performance, with share purchases indicating favorable outlooks and

share sales implying future performance declines.11 We then identify cases where accruals likely

reflect managers’ true beliefs concerning future firm performance (such as high/low accruals

followed by share purchases/sales), and cases where accruals are likely manipulated to boost

managers’ trading gains (such as high/low accruals followed by share sales/purchases). Our

purpose is to examine whether the positive association between management forecast errors and

accruals is attributable to unintentional mis-assessment (likely captured by the former case) or

intentional manipulation (likely captured by the latter case) being manifested in both accruals

and management earnings forecasts.

If it is the unintentional mis-assessment that drives the positive association between

management forecast errors and accruals, we expect this positive association to be stronger for

firms with accruals reflecting managers’ true beliefs about future firm performance than firms

where accruals are likely manipulated to enhance managers’ trading profitability. In other words,

we expect a stronger positive association between management forecast errors and accruals when

managers purchase (sell) shares following periods of high (low) accruals.

H4a: Under the unintentional error explanation, the positive association between management earnings forecast errors and accruals is stronger for firms where managers purchase (sell) shares following periods of high (low) accruals than firms where managers sell (purchase) shares following periods of high (low) accruals.

Alternative, if intentional misrepresentation underlies the positive association between

management forecast errors and accruals, we expect this positive association to be stronger when

11 Although non-information-based liquidity trading may add noises to our tests, it unlikely biases our inferences towards a particular direction.

14

accruals primarily serve to boost managers’ trading gains as opposed to revealing managers’

personal business assessment. In other words, we expect a stronger positive association between

management forecast errors and accruals when managers sell (purchase) shares following

periods of high (low) accruals.

H4b: Under the intentional misrepresentation explanation, the positive association between management earnings forecast errors and accruals is stronger for firms where managers sell (purchase) shares following periods of high (low) accruals than firms where managers purchase (sell) shares following periods of high (low) accruals.

IV. SAMPLE SELECTION AND RESEARCH DESIGN

Sample Selection

We collect management earnings forecasts for fiscal years 1996-2006 from the First

Call’s Company Issued Guidance (“CIG”) database. The sample period starts in 1996 because

the passage of the Private Securities Litigation Reform Act of 1995 expanded the safe-harbor

protection to firms issuing forward-looking information and thus changed firms’ legal

environment. We only include point and range forecasts because forecast errors are less clearly

defined for other forms of forecasts (such as open-ended and qualitative). To assure that

managers have knowledge of accruals when issuing next year’s earnings forecasts, for each firm-

year, we retain the first management earnings forecasts issued at or after current year (year t)

earnings announcement. To avoid confounding effects of year t+1 quarterly earnings, we

exclude management earnings forecasts issued at or after year t+1 first quarter earnings

announcement.12 We also exclude firms with insufficient data on the Compustat and CRSP to

12 Accruals information is fully disclosed in annual reports and may not be available at earnings announcements to outsiders, although an increasing percentage of firms voluntarily disclose balance sheet information (which can be used to infer accruals information) at earnings announcements (e.g., Louis et al. 2007). We assume that managers possess full knowledge of year t accruals by year t earnings announcement. Since a large proportion of management

15

measure accruals and related firm characteristics. The sample selection procedure, summarized

in Panel A of Table 1, yield a final sample of 1,648 firms with 4,443 firm-year observations. We

present the time-series distribution of the sample in Panel B of Table 1. As shown, the number of

forecasting firms increases over the sample period, consistent with an increasing propensity for

managers to provide earnings guidance.13

Research Design

To test our hypotheses, we regress management earnings forecast errors on accruals and

previously identified determinants of management forecast errors, using the ordinary least

squares (OLS) regression with standard errors adjusted for heteroscedasticity and firm-level

clustering (firm subscripts are suppressed):14

1

12111098

7165432

101

)(

)(

+

+

+

+++

++++++

++++++

+=

∑∑ tiiii

tttt

ttttt

Rttt

YearDummymmyIndustryDuBMNANALYSTSMVLnRETURNLITIGATION

TRADEXFINIndConAltmanZESURPROA

orWCACCWCACCMFE

εγλ

βββββ

ββββββ

βα

(1)

Where:

MFEt+1 = The first management forecast of year t+1 earnings per share (adjusted for stock splits and dividends) issued at or after year t earnings announcement but before year t+1 first quarter earnings announcement minus year t+1 actual earnings per share, scaled by the closing share price at the end of year t;

WCACCt

( RtWCACC )

= Working capital accruals (Decile Ranks of working capital accruals scaled to range from 0 to 1), measured as – [Increase in accounts

forecasts for year t+1 earnings are issued with year t earnings announcements (87% for our sample), this measurement window (from year t earnings announcement to year t+1 first quarter earnings announcement) allows us to collect a reasonable sample of management earnings forecasts without being confounded by year t+1 quarterly earnings realizations. Our results are qualitatively similar if we measure management forecast errors based on the first management earnings forecasts issued during the second quarter of year t+1. 13 The increasing trend in the number of forecasting firms may also reflect more comprehensive coverage by First Call since 1998 (Anilowski et al. 2007). 14 Specifically, we use SURVEYREG procedure and CLUSTER statement in SAS to account for the potential firm-level serial-correlation when estimating the coefficients and standard errors.

16

receivable (Compustat annual data item #302) + Increase in inventory (#303) + Decrease in accounts payable (#304) + Decrease in income tax payable (#305) + Net change in other accrued liabilities (#307)] / lagged total assets (#6);

ROAt = Return-on-assets, measured as earnings before extraordinary items (#123) divided by lagged total assets (#6);

ESURPt = Earnings surprise, measured as actual earnings for year t minus the most recent analyst consensus (median) forecast prior to year t earnings announcement (if the firm has no analyst following, we use earnings change), scaled by the closing share price at the end of year t;

AltmanZt = Altman’s Z score (Altman 1968), computed as [1.2 × working capital (#4 – #5) / total assets – 1.4 × retained earnings (#36) / total assets + 3.3 × operating income (#178) / total assets + 0.6 × market value of equity (#25×#199) / total liabilities (#181) + sales (#12) / total assets];

IndCont = Industry Concentration, measured as the Herfindahl index calculated as the sum of the squares of the market shares of the firms’ sales within each four-digit SIC industry;

XFINt+1 = External financing, measured as net equity financing plus net debt financing scaled by lagged total assets (#6), where net equity financing equals cash proceeds from the sale of common and preferred stock (#108) minus cash payments for the purchase of common and preferred stock (#115) minus cash payments for dividends (#127), and net debt issuance equals cash proceeds from the issuance of long-term debt (#111) minus cash payments for long-term debt reductions (#114) minus the net changes in current debt (#301);

TRADE = Net sales (in thousands of shares) from open market transactions or stock option transactions (i.e., option grants or option exercises) by the top five executives during the one-month period following management earnings forecasts (per Thomson Financial Insider Trading database);

LITIGATIONt = Equals one for litigious industries including Bio-technology (SIC 2833 to 2836), Computer Hardware (SIC 3570 to 3577), Electronics (SIC 3600 to 3674), Retailing (SIC 5200 to 5961), and Computer Software (SIC 7371 to 7379), and zero otherwise;

RETURNt = Buy-and-hold 12-month market-adjusted stock returns for year t; Ln(MVt) = Natural logarithm of market value of equity (MV), where MV equals

year-end stock price (#25) multiplied by common shares outstanding (#199), in millions of dollars;

NANALYSTS = Number of individual analyst’s forecasts in the most recent consensus analyst forecast prior to management earnings forecasts (per First Call);

BMt = Book-to-market ratio, measured as book value of equity (#60) divided by market value of equity (MV);

Industry Dummy = Fama-French 12 industry dummies; and Year Dummy = Year dummies.

17

Our primary interest is the coefficient on working capital accruals (i.e., β1). We focus on

working capital accruals because, relative to total accruals, they largely reflect managerial

estimation and projection about near-term earnings (e.g., stock inventory in anticipation of

improving market demand for the next year) as opposed to long-term earnings growth (e.g.,

increase plant investments to expand production capacity in anticipation of sustained future

growth). Thus, future earnings implications of working capital accruals are better aligned with

the forecasting horizon of management one-year-ahead earnings forecasts. Based on Hypothesis

1 (H1) which predicts a positive relation between management forecast errors and accruals, we

expect the coefficient β1 to be significantly positive.

We control for various factors that may affect management earnings forecast errors and

potentially confound the association between management forecast errors and accruals. First,

prior research suggest that managers of poorly performing firms or financially distressed firms

have greater incentives to provide optimistic earnings forecasts to support market earnings

expectations (e.g., Frost 1997; Koch 1999; Rogers and Stocken 2005; Rogers and Buskirk 2006).

Firms’ operating performance also directly affects the level of accruals through the accrual

accounting system. We thus include return-on-assets (ROA), prior year’s earnings surprises

(ESURP), and Altman’s Z-score (AltmanZ) to control for the potential impacts of firm

performance and distress risk on managers’ forecast errors and accruals.

Second, industry competition may motivate managers to hide firm profitability possibly

via pessimistic earnings forecasts (Newman and Sansing 1993). We thus include industry

concentration ratio (IndCon) to control for this effect. Third, we control for external financing

(XFIN) in the regression since external financing has been proposed as an important factor that

may induce managerial optimism in forecasting earnings (e.g., Frankel et al. 1995; Lang and

18

Lundholm 2000) as well as earnings inflation through income-increasing abnormal accruals (e.g.,

Teoh et al. 1998a, 1998b), although empirical findings concerning these conjectures are still

mixed.15 Fourth, incentives to maximize potential gains from trading the firm’s securities may

induce managers to issue biased earnings forecasts (Aboody and Kasznik 2000; Rogers and

Stocken 2005). We thus control for insider trading (TRADE) in the regression. Fifth, we include

a dummy variable identifying litigious industries (LITIGATION) since the litigation environment

affects managers’ incentives to intentionally bias voluntarily disclosed information (e.g., Skinner

1994, 1997; Baginski et al. 2002; Rogers and Stocken 2005). Sixth, McNichols (1989) finds a

significantly negative relation between management forecast errors and past stock returns,

arguing that management earnings forecast do not fully reflect information contained in

historical stock prices. We thus control for past stock returns (RETURN) in the regression.

We add several additional control variables relating to the general information

environment that may affect the cost-benefit tradeoff of issuing biased or inaccurate management

earnings forecasts. We control for firm size (MV) and analyst coverage (NANALYSTS) since

larger firms and firms followed by a larger number of analysts generally face greater public

scrutiny and thus have greater incentives to avoid excessive errors in management earnings

forecasts (e.g., Baginski et al. 2002). We also control for firm growth (BM) since high growth

firms’ valuation largely hinges on expected future cash flows (rather than the value of assets in

place), which intensifies the market demand and public scrutiny for forward-looking information

disclosures. In this case, managers may have incentives to forecast optimistically to “hype the

stock”, but also expose themselves to heightened litigation risks and loss of reputation. Rogers

and Stocken (2005) find an insignificant relationship between management forecast errors and

15 See footnote 9 for a discussion of the mixed empirical evidence.

19

firm growth. Finally, we add industry dummies and year dummies to control for fixed industry

and time effects. To mitigate the influences of outliers and errors in the data, we winsorize the

top and bottom one-percentiles of the regression variables (except IndCon, LITIGATION, and

NANALYSTS).

V. EMPIRICAL RESULTS Descriptive Statistics

Panel A of Table 2 outlines the descriptive statistics for our sample of 4,443 firm-years.

Consistent with prior studies showing optimistic biases in management earnings forecasts issued

early-in-the-year (e.g., Choi and Ziebart 2004), we find that the average management forecast

errors (MFEt+1) is significantly positive at 0.006. As also shown in the table, the average

working capital accruals (WCACC) and total accruals (TACC) are 0.014 and -0.059 respectively.

As expected, our sample contains large firms with average (median) market capitalization (MV)

of $5,241 million ($1,082 million).

Panel B of Table 2 contains pair-wise correlations between management forecast errors,

accruals, and other regression variables included in equation (1). We find that management

forecast errors are positively correlated with working capital accruals (Pearson correlation =

0.129) and total accruals (Pearson correlation = 0.092), suggesting that managers who issue more

optimistic (pessimistic) forecasts of next year’s earnings tend to report relatively high (low)

accruals. In addition, the correlations between working capital accruals and other regression

variables are mostly modest (correlations are mostly less than 0.1 in magnitude), suggesting that

multicolinearity concern unlikely affects our empirical inferences.

20

Univariate Analysis on the Relation between Management Forecast Errors and Accruals

Table 3 presents the mean and median of management forecast errors (MFEt+1) across

deciles of working capital accruals (WCACCt) portfolios. As shown, the mean (median) value of

MFEt+1 increases from 0.001 (-0.002) for the lowest WCACCt decile to 0.015 (0.003) for the

highest WCACCt decile. The difference in the mean (median) MFEt+1 between the highest and

lowest WCACCt deciles is statistically significant at less than 1% (1%) level based on a two-tail

t-test (z-test). To put these numbers into perspective, with a price-to-earnings ratio of 12 (the

sample median), the average management forecast errors in the lowest and highest WCACC

deciles amount to 1.2% and 18% of reported earnings, respectively. The positive relation

between MFEt+1 and WCACCt is also transparent as illustrated in Figure 1.

As a robustness check, we also examine the mean and median of MFEt+1 across deciles

of total accruals (TACCt). We measure total accruals as income before extraordinary items (#123)

minus operating cash flows (#308 – #124) deflated by lagged total assets (#6). Our findings are

also reported in Table 3. Similar to the results based on WCACCt, the mean and median MFEt+1

increase with the level of TACCt. In summary, the univariate results in Table 3 provide initial

evidence that managers reporting relatively high (low) accruals tend to issue more (less)

optimistically biased forecasts of next year’s earnings.

Multivariate Analysis on the Relation between Management Forecast Errors and Accruals

Table 4 presents the multivariate regression results from estimating equation (1). As

shown, the coefficient on WCACC is significantly positive (Coefficient = 0.084, t-stat = 4.44),

consistent with earlier univariate findings that management forecasts are relatively more

optimistic (pessimistic) following periods of high (low) accruals. The effect of WCACC on

21

management forecast errors is not only statistically significant, but also economically significant.

With a price-to-earnings ratio of 12 (the sample median), a 1% increase in working capital

accruals (as a percentage of total assets) would increase the errors in management forecasts by

about 0.84% of reported earnings (i.e., 12×0.070×1% = 0.84%). Results also show that this

positive coefficient remains highly significant when we measure WCACC using scaled decile

rankings (Coefficient = 0.011, t-stat = 3.85).16

As a robustness check, we again examine the relation between management forecast

errors and total accruals after controlling for other factors that also affect management forecast

errors. As reported under the last two columns of Table 4, the coefficient on TACC is

significantly positive (Coefficient = 0.046, t-statistics = 5.31) and so is the coefficient on TACCR

(Coefficient = 0.008, t-statistics = 4.35). Overall, results reported in Table 4 provide strong

evidence that management earnings forecasts are positively related to both working capital

accruals and total accruals, supporting Hypothesis 1 (H1).

Turning to control variables, we find a significantly positive coefficient on operating

performance (ROA), suggesting that managers appear to over-extrapolate past performance in

forecasting future earnings.17 We also observe that management earnings forecasts are more

optimistic when past earnings surprises (ESURP) are more negative, consistent with recent

16 In untabulate results, we find that management earnings forecast errors exhibit significantly positive relations with each major component of working capital accruals (including changes in receivable, changes in inventory, changes in accounts payable and other working capital accruals). 17 Our observed positive relation between management earnings forecast errors and accruals may be confounded by managers’ over-extrapolation of realized performance in forecasting earnings because high (low) accruals may result from superior (poor) economic performance and a neutral application of accounting rules, rather than managers’ proactive choices that aim to convey their personal assessment about the firm’s business prospects. To further ensure that our results are not driven by managers’ extrapolation of past economic performance, we identify cases where accruals are least likely driven by concurrent firm performance. Specifically, we select firms ranked in the top (bottom) quintile of WCACC but ranked in the bottom (top) quintile of ROA, and re-estimate equation (1) for these firms. Untabulated results show a significantly positive coefficient on WCACCR (Coefficient = 0.022, t-stat = 2.23), suggesting that over-extrapolation of past performance unlikely fully explain the positive association between management forecast errors and accruals.

22

evidence that managers bundle negative earnings surprises with optimistic earnings forecasts to

support market earnings expectations (Rogers and Buskirk 2006). In addition, we document a

significantly positive coefficient on LITIGATION, suggesting that managers in litigious

industries on average display greater optimism in forecasting earnings.18 We also find that past

stock returns are negatively related with management forecast errors, consistent with

McNichols’s (1989) finding that stock prices reflect information beyond that in management

earnings forecasts. Finally, larger firms and high growth firms tend to forecast more

conservatively in our sample.19

Influence of Uncertainty in Operating Environment on the Relation between Management Forecast Errors and Accruals

We propose that managerial mis-assessment of business prospects introduce common

errors in accruals and earnings forecasts, thus inducing a positive relation between management

forecast errors and accruals. Suppose this managerial mis-assessment explanation holds,

Hypothesis 2 (H2) predicts that the positive relation between management forecast errors and

accruals is stronger for firms operating in an uncertain business environment than firms

operating in a stable business environment.

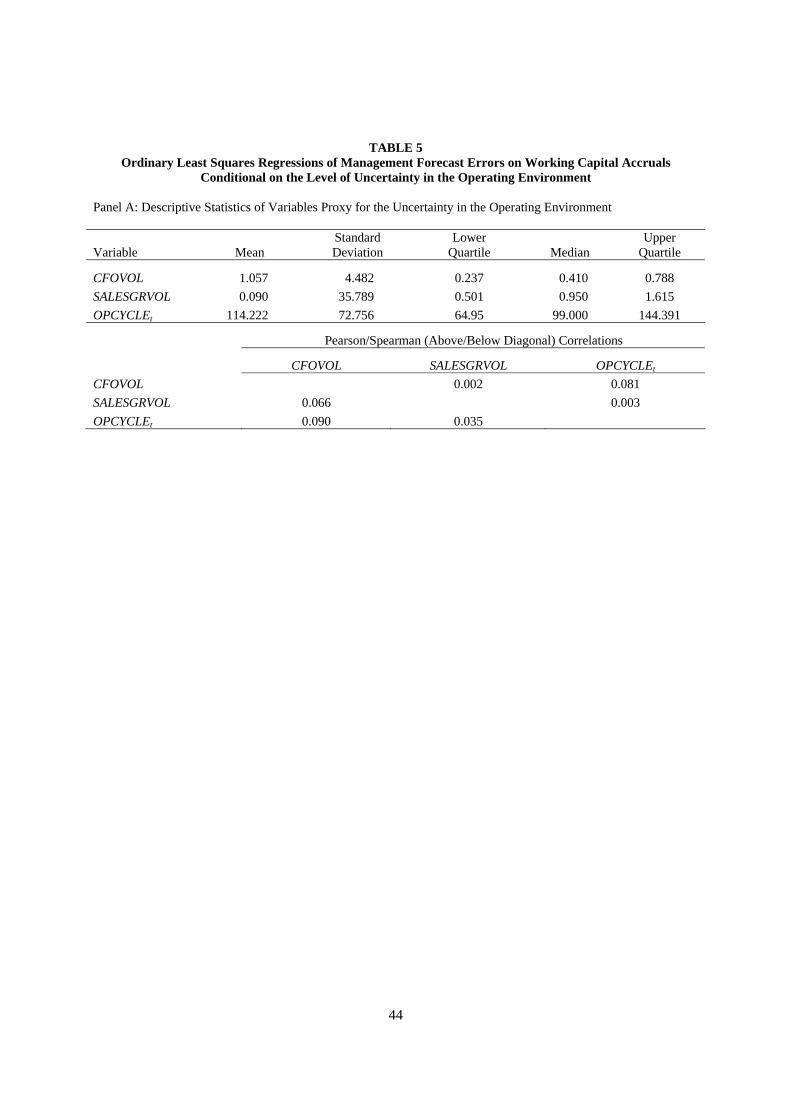

We measure the uncertainty in operating environment based on three alternative proxies:

(1) cash flow volatility (CFOVOL), defined as standard deviation of operating cash flows

(divided by lagged total assets) over the prior five years scaled by the magnitude of average

18 This finding seems inconsistent with the deterrence effect of litigation on optimistic forecasts. One possibility is that litigation concern is more relevant for management forecasts issued shortly before the earnings announcement (see Soffer et al. 2000), but we focus on management forecasts issued early in the year. 19 Kasznik (1999) suggests that managers use positive discretionary accruals to manage reported earnings upward to minimize optimistic errors in management earnings forecasts. We thus include year t+1’s discretionary accruals (based on cross-sectional Modified Jones’ Model) to re-estimate equation (1). Similar as Rogers and Stocken (2005), we find an insignificant coefficient on next year’s discretionary accruals (untabulated). The coefficient on working capital accruals remains significantly positive.

23

operating cash flows (divided by lagged total assets) over the same period; (2) sales growth

volatility (SALESGRVOL), defined as standard deviation of sales growth over the prior five years

scaled by the average sales growth over the same period, and (3) operating cycle (OPCYCLE),

defined as average accounts receivable divided by sales plus average inventory divided by cost

of goods sold then multiplied by 365. These proxies are intended to capture multiple aspects of

environmental uncertainty. In particular, volatility in operating cash flows potentially originates

from unstable market conditions that affect the firms’ cash flow generating abilities; sales growth

volatility largely reflects temporal fluctuations in customer demand; and the length of operating

cycle depends on the firm’s production function and business model Collectively, these measures

parsimoniously capture the inherent uncertainty in measuring accruals and forecasting earnings.

As shown in Panel A of Table 5, the correlations among these measures are fairly low, consistent

with the idea that these variables reflect different dimensions of environmental uncertainty.

Panel B of Table 5 reports OLS regression results for equation (1) across subsamples of

firms ranked in the top, middle and bottom thirds of each environmental uncertainty proxy. For

firms ranked in the bottom third of CFOVOL, the coefficient on WCACCR is significantly

positive (Coefficient = 0.006, t-stat = 2.48). Moving to the subsample ranked in the top third of

CFOVOL, the magnitude of the coefficient on WCACCR is more than doubled (Coefficient =

0.013, t-stat = 3.46). The coefficient difference between the top and bottom subsamples is

statistically significant at less than 1% level based on a two-tail F-test. Similarly, we find that the

coefficient on WCACCR is significantly more positive for firms ranked in the top third of

SALESGRVOL or OPCYCLE than firms ranked in the bottom third of SALESGRVOL or

OPCYCLE.

24

As a sensitive check, we also examine how the positive relation between management

forecast errors and total accruals varies with the level of environment uncertainty. In untabulated

results, we find that the positive relation between management forecast errors and totals accruals

is significantly stronger for subsample firms ranked in the top third of CFOVOL, SALESGRVOL

or OPCYCLE, respectively, than their bottom-third counterparts. These results are consistent

with the conjecture that managers who cope with a highly uncertain operating environment likely

make greater errors in assessing the firm’s business prospects, thus strengthening the positive

relation between management forecast errors and accruals.

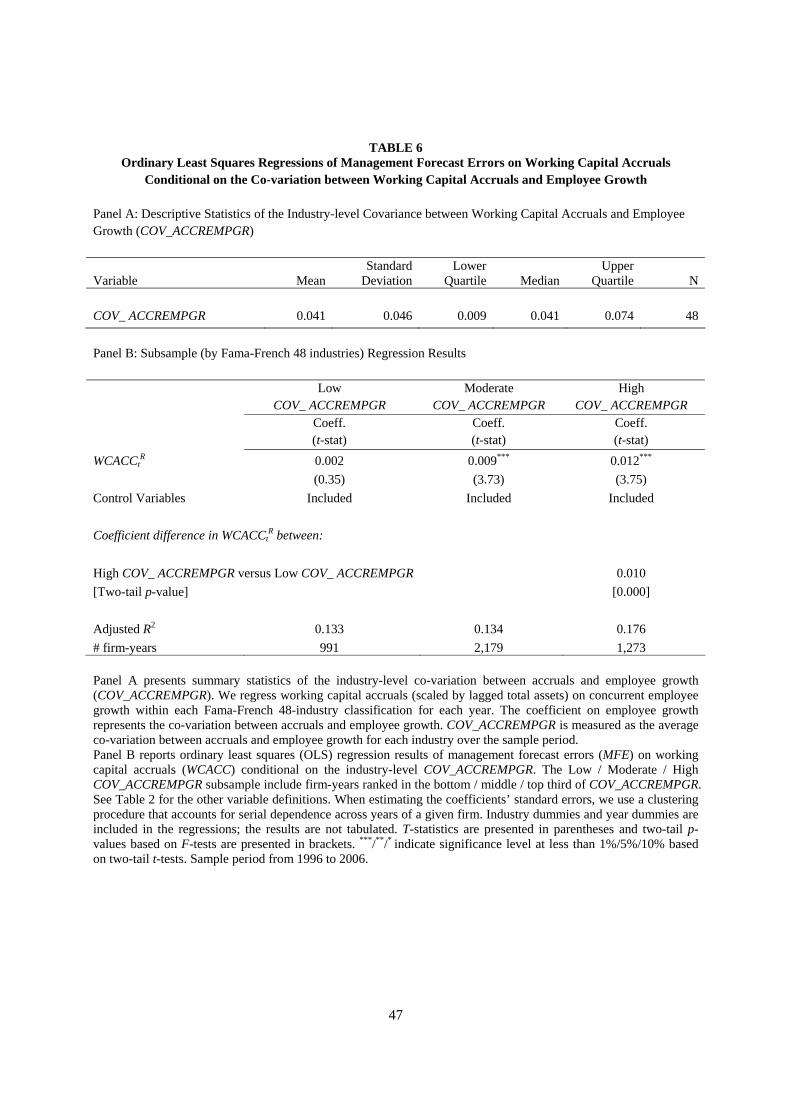

Influence of Accrual-Growth Co-variation on the Relation between Management Forecast Errors and Accruals

Suppose managerial mis-assessment of business prospects contribute to the positive

relation between management forecast errors and accruals, Hypothesis 3 (H3) predicts that this

positive relation is stronger when accruals highly co-vary with growth-related activities that

reflect managerial projections about firms’ future prospects.

We use growth in the number of employees to capture managers’ projections about firm’s

business prospects (Zhang 2007). Employee growth reflects managers’ growth expectations as

revealed through human capital investment decisions and is free of any biases in the firm’s

financial reporting system.20 Similar as Zhang (2007), we categorize industries based on the co-

variation of accruals with growth in the number of employees. Specifically, for each year, we

regress working capital accruals (scaled by lagged total assets) on concurrent employee growth

within each Fama-French 48-industry classification. The coefficient on employee growth

20 Zhang (2007) argues that growth in the number of employees is a better measure for firm growth than conventional growth measures based on financial information (such as market-to-book, growth in cash sales, growth in total assets, etc.) because employee growth is a non-accounting-based variable and, therefore, is free of any measurement error or discretionary choices inherent in the accounting system.

25

represents the extent to which accruals co-vary with concurrent employment decisions. We then

rank industries based on the average co-variation between accruals and employee growth over

our sample period (COV_ACCREMPGR). As expected, retailers, wholesalers, and manufacturers

tend to have high co-variation between accruals and employee growth. For example, the top five

industries with the highest COV_ACCREMPGR include Tobacco Products, Wholesale,

Chemicals, Machinery and Fabricated Products. On the other extreme, service and agriculture

production industries often have low accrual-growth co-variation. In particular, Trading, Coal,

Entertainment, Insurance and Agriculture are among the industries exhibiting the lowest co-

variation between accruals and employee growth.

Panel A of Table 6 provides summary statistics for COV_ACCREMPGR. As shown, the

inter-industry variation in this variable is large, ranging from 0.009 in the lower quartile to 0.074

in the upper quartile. Panel B of Table 6 reports OLS regression results for equation (1) across

industries ranked in the top, middle, and bottom thirds of COV_ACCREMPGR. Results show

that the relation between management forecast errors and working capital accruals is

insignificant for industries exhibiting the lowest co-variations between working capital accruals

and employee growth (Coefficient = 0.002, t-stat = 0.35). In contrast, for industries in which

working capital accruals co-vary strongly with employee growth, the coefficient on WCACCR is

significantly positive (Coefficient = 0.012, t-stat = 3.75). The coefficient difference between

these two subsamples is statistically significant at less than 1% level based on a two-tail F-test.

We similarly construct the accrual-employee growth co-variation based on total accruals

(COV_TACCREMPGR). In untabulated results, we find that the association between

management forecast errors and totals accruals is statistically insignificant for industries ranked

among the bottom third of COV_TACCREMPGR, whereas this association is significantly

26

positive for industries ranked in the top third of COV_TACCREMPGR. These results further

support the conjecture that managerial mis-assessment of business prospects, which manifests in

both accruals and management earnings forecasts, contributes to the positive relation between

management forecast errors and accruals.

Intentional Misrepresentation as an Alternative Explanation

While we have proposed that the positive association between management forecast

errors and accruals is caused by managers’ unintentional errors in assessing firms’ future

prospects, this positive association could also arise from managers’ intentional misrepresentation

of their earnings forecasts and accruals. That is, managers may intentionally bias their earnings

forecasts upward (downward) when reported accruals are relatively high (low), even though they

fully understand that high (low) accruals are likely followed by poorer (better) performance than

forecasted.

To distinguish between these two explanations, we examine the implications of insider

trading on the association between management forecast errors and accruals. We measure insider

trading based on net acquisition/disposition of stocks and options by the top five executives

(CEO, Chairman, CFO, COO, and Vice President) during the one-month period following the

management forecasts. Under the unintentional mis-assessment explanation, Hypotheses 4a (H4a)

predicts that the positive association between management earnings forecast errors and accruals

is stronger when managers purchase (sell) shares following periods of high (low) accruals. Under

the alternative intentional misrepresentation explanation, Hypotheses 4b (H4b) predicts that the

positive association between management earnings forecast errors and accruals is stronger when

managers sell (purchase) shares following periods of high (low) accruals. We thus form two

27

subsamples of firms to test these hypotheses. Sample A consists of firm-years ranked in the top

(bottom) quintile of WCACC and with managers’ share purchases (sales) subsequent to

management forecasts. Sample B includes firm-years ranked in the top (bottom) quintile of

WCACC and with managers’ share sales (purchases) following management forecasts. We

expect Sample A to represent cases where the level of accruals more likely reflects managers’

personal beliefs about future firm performance, and Sample B to identify cases where accruals

are more likely manipulated to boost managers’ trading profitability.

Table 7 reports OLS regression results for equation (1) for Sample A and Sample B. As

shown, for Sample A where accruals more likely reflect managers’ true beliefs about future firm

performance, the coefficient on WCACCR is significantly positive (Coefficient = 0.013, t-stat =

2.77). In contrast, the coefficient on WCACCR is insignificant (Coefficient = 0.001, t-stat = 0.10)

for Sample B where accruals are more likely manipulated to boost trading gains.

In untabulated sensitivity checks, we find that the relation between management forecast

errors and total accruals is significantly positive when total accruals are likely to reflect

managers’ true beliefs about future firm performance (i.e., top/bottom quintile of TACC followed

by share purchases/sales). In contrast, we no longer observe a significant association between

management forecast errors and total accruals when total accruals are likely manipulated to boost

managers’ trading gains (i.e., top/bottom quintile of TACC followed by share sales/purchases).

These results do not support the conjecture that managerial self-serving incentives lead to

intentional misrepresentation in managers’ multiple information disclosures such as accruals and

earnings forecasts. On the contrary, these results provide strong supporting evidence for the

unintentional explanation that the reflection of managers’ imperfect business assessment in both

disclosures causes the positive relationship.

28

To further corroborate our findings, we examine insider trading activities for firm-years

that drive the positive association between management forecast errors and accruals. Specifically,

we select firm-years ranked in the top (bottom) quintile of WCACC and also issued optimistic

(pessimistic) earnings forecasts. Untabulated results show that when top quintile accruals are

followed by optimistic management forecasts, a majority of managers (54%) purchase, as

opposed to sell, shares. On the other hand, when bottom quintile accruals are followed by

pessimistic management forecasts, a majority of managers (55%) chooses to sell, rather than

purchase, shares. These results again are inconsistent with managers’ intentional

misrepresentation of accruals and earnings forecasts to enhance trading profitability.

VI. SUPPLEMENTARY ANALYSIS: THE INFLUENCE OF MANAGEMENT EARNINGS FORECASTS ON ACCRUAL MISPRICING

Prior literature generally advocates voluntary disclosure as a valuable source of

information that helps reduce mispricing of accounting information (e.g., Drake et al. 2007;

Kimbrough 2005; Louis et al. 2007). However, given management earnings forecasts contain

predictable errors in relation to accruals (as suggested in our findings above), it is ex ante unclear

whether biased management earnings forecasts are able to facilitate more efficient pricing of

accruals information. On one hand, managers’ optimistic (pessimistic) forecasts following

periods of high (low) accruals may exacerbate investors’ over-reaction to accruals. On the other

hand, biased management earnings forecasts may still be able to improve earnings expectations

formed without management forecasts and thus help investors better understand accruals.

Empirically, it is also possible that managers, analysts, and investors all make similar judgmental

errors in projecting the firm’s business prospects, which implies a null effect of management

earnings forecasts on accrual mispricing.

29

We address this issue by testing whether the availability of management earnings

forecasts affects the profitability from an accrual-based trading strategy. Specifically, we

estimate the following model using ordinary least squares (OLS) regression with standard errors

adjusted for heteroscedasticity and firm-level clustering:

165432

1211211

+

+

++++++

×+×++=

ttR

ttRt

Rt

Rt

Rtt

IMRatioEPBETABMMV

MFWCACCNoMFWCACCMFNoMFSARET

εβββββ

ββαα (2)

where SARETt+1 is the buy-and-hold 12-month size-adjusted returns cumulated from the fourth

month after the end of year t and estimated strictly following the recommendation of Kraft et al.

(2006). NOMF (MF) is a dummy variable that equals one (zero) for firm-years having no

management earnings forecasts issued during the year (based on First Call’s population), and

zero (one) for firm-years having at least one management one-year-ahead earnings forecast

issued at or after year t earnings announcement and before year t+1 first quarter earnings

announcement (i.e., the same sample used in earlier analyses). WCACCR, MVR, BMR, and EPR are

decile ranks of WCACC, MV, BM, and EP (earnings-to-price ratio), scaled to range from 0 to1.

BETA is market beta estimated over the 36-month period prior to the end of year t.

Since managers have ample flexibilities to either withhold or provide earnings forecasts,

we control for the endogenous nature of the management forecast issuance decision by including

the Inverse Mill’s Ratio (IMRatio) generated from the following probit regression aiming to

predict the issuance decision of management earnings forecasts.

))(

()1Pr(

1

109876

5143210

+

+

+++

+++++

+++++==

∑∑ tiiii

tttt

ttttt

YearDummymmyIndustryDuBMNANALYSTSMVLnLITIGATIONEARNVOL

RTNVOLAFEERCROAWCACCfMF

εγλ

βββββ

βββββα

(3)

Following Lennox and Park (2006), we include return-on-assets (ROA), earnings

response coefficient (ERC), the magnitude of analyst forecast errors (|AFE|), return volatility

30

(RTNVOL), earnings volatility (EARNVOL), litigious industry dummy (LITIGATION), firm size

(LnMV), analyst following (NANALYSTS), book-to-market ratio (BM), and industry and year

dummies (See Lennox and Park (2006) for details on variable measurement).21 In addition, we

include the magnitude of working capital accruals because more extreme accruals are generally

more difficult to assess by analysts and outside investors (e.g., Sloan 1996; Bradshaw et al.

2001). To reduce information asymmetry, managers therefore may have greater incentive to

provide earnings forecasts when accruals are more extreme.

Panel B of Table 8 reports our findings from estimating equation (2). As shown under the

column Model (2), the coefficients on WCACCR×NoMF and WCACCR×MF are both significantly

negative with similar statistical significance levels (Coefficient = -0.055 and -0.054, t-statistics =

-2.22 and -2.23, respectively). A formal test of the difference in these two coefficients cannot

reject the null of no difference (two-tail p-value = 0.965), suggesting that investors appear to

overreact to working capital accruals to the same extent regardless of whether managers provide

earnings forecasts or not.22 Hence, management earnings forecasts do not appear to help market

participants better assess accruals’ implications for future earnings. Consistent with prior studies,

we also find that future size-adjusted returns are positively related with book-to-market ratio and

market beta and negatively related with firm size (e.g., Fama and French 1992; Basu 1977; Sloan

1996; Desai et al. 2004).

VII. CONCLUSION

21 Lennox and Park (2006) also include analyst forecast revisions of two-period-head earnings. We do not include analyst forecast revisions of two-year-ahead earnings since doing so will substantially reduce our sample size. 22 We also examine the impact of management earnings forecasts on accrual mispricing conditional on the environmental uncertainty or accruals-growth co-variation. Untabulated results show that the differences between the accrual-based hedge portfolio returns are statistically insignificant between firms with relatively stable versus highly uncertain operating environment and across industries exhibiting low versus high co-variation between accruals and employee growth.

31

This paper documents that managers tend to forecast next year’s earnings more

optimistically (pessimistically) when current year’s accruals are relatively high (low), and that

managers’ unintentional mis-assessment of firm’s business prospects likely contributes to the

positive relation between management earnings forecast errors and accruals.

Our findings have important implications for the general investment community and

academic researchers. First, the positive relation between management forecasts errors and

accruals cautions investors to carefully evaluate forward-looking information disclosures from

the management when forming earnings expectations. Second, the empirical evidence implies

that voluntary disclosure may not always facilitate efficient pricing of accounting information

due to the possibility that voluntarily disclosed information may contain predictable errors that

are correlated with reported accounting information. This perspective stands in contrast to the

conclusion in many prior studies that voluntary disclosure provides useful information that helps

outsiders better understand accounting information reported in regulatory filings (e.g.,

Kimbrough 2005; Drake et al. 2007; Louis et al. 2007). Regulators and standard setters should be

aware of the possibility that expanded voluntary disclosure, when containing predictable errors

related to mandatory disclosure, may not facilitate more efficient pricing of mandatorily

disclosed information. Lastly, our findings suggest that future research examining the sources of

market mispricing of accounting information needs to consider corporate insiders’ inefficiency in

assessing business prospects, in addition to outsiders (such as investors’ and analysts’)

inefficiency in information processing.

32

REFERENCES Aboody, D., and R. Kasznik. 2000. CEO stock option awards ad the timing of corporate

voluntary disclosures. Journal of Accounting and Economics 29 (3): 73-100. Ajinkya, B., and M. J. Gift. 1984. Corporate managers' earnings forecasts and symmetrical

adjustments of market expectations. Journal of Accounting Research 22 (2): 425-444. Altman, E. 1968. Financial ratios, discriminant analysis and the prediction of corporate

bankruptcy. The Journal of Finance 23 (4): 589-609. Anilowski, C., M. Feng, and D. Skinner. 2007. Does earnings guidance affect market returns?

The nature and information content of aggregate earnings guidance. Journal of Accounting and Economics 44 (1-2): 36-63.

Baginski, S, E. Conrad, and M. Kimbrough. 2002. The effect of legal environment on voluntary

disclosure: Evidence from management earnings forecasts issued in U.S. and Canadian markets. The Accounting Review 77 (1): 25-50.

Baker, T., Collins, D., Reitenga, A., 2003. Stock option compensation and earnings management

incentives. Journal of Accounting, Auditing and Finance 18: 557-582. Ball, R. and L. Shivakumar, 2007, Earnings quality at initial public offerings: Managerial

opportunism or public-firm conservatism. Journal of Accounting and Economics (forthcoming).

Bamber, L. S., and Y. S. Cheon. 1998. Discretionary management earnings forecast disclosures:

Antecedents and outcomes associated with forecast venue and forecast specificity choices. Journal of Accounting Research 36 (2): 167-190.

Basu, S. 1977. Investment performance of common stocks in relation to their price-earnings

ratios: A test of the efficient market hypothesis. Journal of Finance 32 (3): 663-682. Ben-David, I., J. R. Graham and C.R. Harvey. 2007. Managerial overconfidence and corporate

policies. Working Paper. University of Chicago Bradshaw, M., S. Richardson, and R. Sloan. 2001. Do analysts and auditors use information in

accruals? Journal of Accounting Research 39 (June): 45-74. Choi, J. H., and D. A. Ziebart. 2004. Management earnings forecasts and the market’s reaction to

predicted bias in the forecast. Asia-Pacific Journal of Accounting and Economics 11 (2): 167-192.

Collins, D. W., G. Gong, and P. Hribar. 2003. Investor sophistication and the mispricing of

accruals. Review of Accounting Studies 8 (2-3): 251-276.

33

Comment, R., and G. Jarrell. 1991. The relative signaling power of Dutch-auction and fixed-price self-tender offers and open-market share repurchases. Journal of Finance 46: 1243-1271.

Cox, C. 1985. Further evidence on the representativeness of management earnings forecasts. The

Accounting Review 60 (3): 692-701. Dechow, P. 1994. Accounting earnings and cash flows as measures of firm performance: The

role of accounting accruals. Journal of Accounting and Economics 18 (1): 3-42. Dechow, P., S. Richardson, and R. Sloan. 2006. The persistence and pricing of the cash

component of earnings. Working Paper. University of Michigan. Desai, H., S. Rajgopal, and M. Venkatachalam. 2004. Value-glamour and accruals mispricing:

One anomaly or two? The Accounting Review 79 (2): 355-385. Drake, M. S., J. N. Myers and L. A. Myers. 2007. Disclosure quality and the mispricing of

accruals and cash flow. Working Paper, Texas A&M University. Fama E., and K. French. 1992. The cross-section of expected stock returns. Journal of Finance,

47 (3): 427-465. Fairfield, P., S. Whisenant and T. Yohn. 2003. Accrued earnings and Growth: Implications for

future profitability and market mispricing. The Accounting Review 78 (1): 353-371. Francis J., D. Philbrick, and K. Schipper. 1994. Shareholder litigation and corporate disclosure.

Journal of Accounting Research 32: 137-164. Frankel, R., M. McNichols and G. P. Wilson. 1995. Discretionary disclosure and external

financing. The Accounting Review 70 (1):135-150. Frost, C. 1997. Disclosure policy choices of U.K. firms receiving modified audit reports. Journal

of Accounting and Economics 23 (2): 163-187. Gong, G., H. Louis, and A. Sun. 2008. Earnings management and firm performance following

open-market repurchases. Journal of Finance 63 (2): 947-986. Graham, J., C. R. Harvey, and S. Rajgopal. 2005. The economic implications of corporate

financial reporting. Journal of Accounting and Economics 40: 3-73. Healy, P. M. and K. G. Palepu. 2001. Information asymmetry, corporate disclosure, and the

capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31: 405-440.

Hirshleifer, D. 2001. Investor psychology and asset pricing. Journal of Finance 56, 1533–1596.

34

Hutton, A., and P. Stocken. 2007. Effect of reputation on the credibility of management forecasts. Working Paper, Boston College.

Ikenberry, D., J. Lakonishock, and T. Vermaelen. 1995. Market underreaction to open market

share repurchases. Journal of Financial Economics 39: 181-208. Kasznik, R., and B. Lev. 1995. To warn or not to warn: Management disclosure in the face of an

earnings surprise. The Accounting Review 70 (1): 113-134. Khan, M. 2007. Are accruals mispriced? Evidence from tests of an intertemporal capital asset

pricing model. Journal of Accounting and Economics 45 (1): 55-77. Kimbrough, M. D. 2005. The effect of conference calls on analyst and market underreaction to

earnings announcements. The Accounting Review 80: 189-219. Koch, A. 1999. Financial distress and the credibility of management earnings forecasts. Working

Paper, Carnegie Mellon University. Kothari, S. P. 2001. Capital markets research in accounting. Journal of Accounting and

Economics 31: 105-231. Kraft, A., A. J. Leone, and C. Wasley. 2006. An analysis of the theories and explanations

offered for the mispricing of accruals and accrual components. Journal of Accounting Research 44 (May): 297-339.

Kraft, A., A. J. Leone, and C. Wasley. 2007. Regression-based tests of the market pricing of

accounting numbers: The Mishkin test and ordinary least squares. Journal of Accounting Research, forthcoming.

Lang, M. H., and R. J. Lundholm. 2000. Voluntary disclosure and equity offerings: Reducing

information asymmetry or hyping the stock? Contemporary Accounting Research 17 (4): 623-662.

Lennox, C., and C. Park. 2006. The informativeness of earnings and management’s issuance of

earnings forecasts. Journal of Accounting and Economics 42: 439-458. Louis, H., D. Robinson, and A. Sbaraglia. 2007. An integrated analysis of the association

between accrual disclosure and the abnormal accrual anomaly. Review of Accounting Studies, forthcoming.