Embed Size (px)

Citation preview

The Annuity PuzzleThe Annuity Puzzle

Richard MacMinn

Illinois State University

Presentation at L5

The Fifth International Longevity Risk and Capital Market Solutions Conference

New York, New York

September 25, 2009

LiteratureLiterature Yaari, M. (1965). "Uncertain Lifetime, Life Insurance, and the Theory of the Consumer."

The Review of Economic Studies 32: 137-150. Davidoff, T., J. R. Brown, et al. (2005). "Annuities and Individual Welfare." American

Economic Review 95(5): 1573 - 1590. Warshawsky, M. (1988). "Private Annuity Markets in the United States: 1919-1984."

Journal of Risk and Insurance 55(3): 518-528. Friedman, B. M. and M. J. Warshawsky (1990). "The cost of annuities: implications for

saving behavior and bequests." Quarterly Journal of Economics 105(1): 135-154. Poterba, J. M. (2001). "Annuity Markets and Retirement Security." Fiscal Studies 22: 249-

279. Inkmann, J., P. Lopes, et al. (2007). How deep is the Annuity Market Participation

Puzzle?, Working Paper, presented at CESifo Venice Summer Institute. Purcal, S. and J. Piggott (2008). "Explaining Low Annuity Demand: An Optimal Portfolio

Application to Japan." Journal of Risk and Insurance 75(2): 493-516. Lockwood, L. (2009). Bequest Motives and the Annuity Puzzle. Chicago, University of

Chicago. Sinclair, S. H. and K. A. Smetters (2004). Health Shocks and the Demand for Annuities.

Washington, DC, Congressional Budget Office. Sheshinski, E. (2008). The Economic Theory of Annuities. Princeton, Princeton University

Press. Cannon, E. and I. Tonks (2008). Annuity Markets. Oxford, Oxford University Press.

Tuesday, April 18, 2023 2http://www.macminn.org/

The Classic Economic ParadigmThe Classic Economic Paradigm

Portfolio Model◦Dates now and then◦The consumer/investor selects a portfolio now

of annuities, bonds and life insurance◦The portfolio payoff occurs then◦The investor survives or not to obtain the

portfolio payoff then◦The investor exhibits selfish behavior

Tuesday, April 18, 2023 http://www.macminn.org/ 3

Portfolio ModelPortfolio ModelThe portfolio isThe survival probability isThe annuity, bond and life insurance

prices areThe consumption now and then depend

on the portfolio choices

Tuesday, April 18, 2023 http://www.macminn.org/ 4

, ,a b l 1 q

, ,a b lp p p

Portfolio ModelPortfolio ModelConsumption now and then are

Given a utility function u. Expected utility is

Tuesday, April 18, 2023 http://www.macminn.org/ 5

0 a a b b l lc w p p p

1

0

1a b

qc

q

( ) ,0

, (1 )

a a b b l l

a a b b l l a b

F u w p p p q

u w p p p q

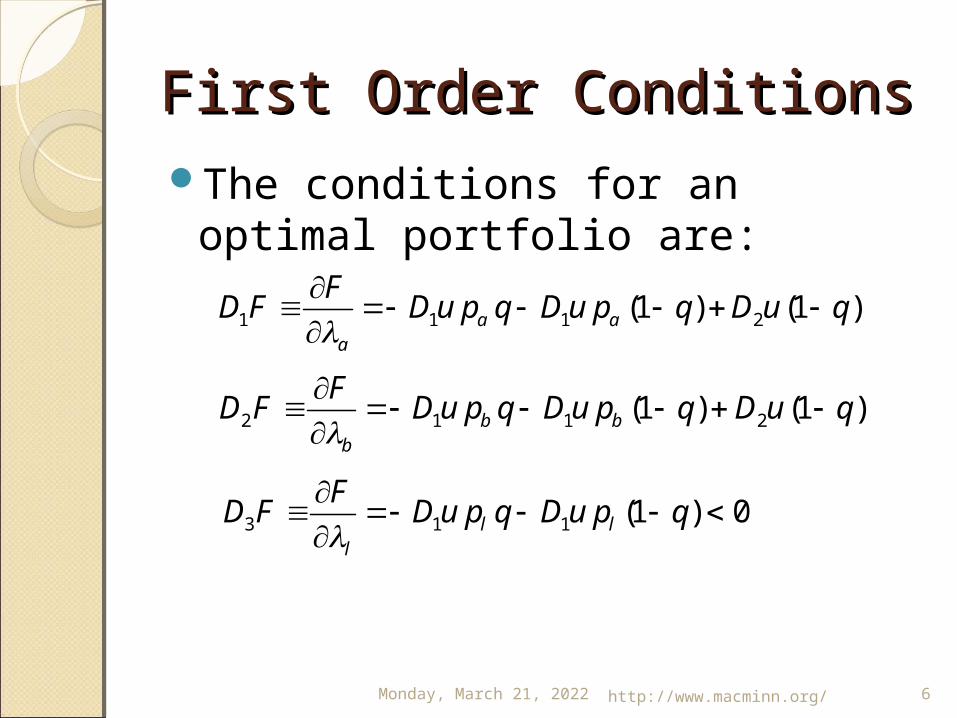

First Order ConditionsFirst Order ConditionsThe conditions for an optimal portfolio

are:

Tuesday, April 18, 2023 http://www.macminn.org/ 6

1 1 1 2(1 ) (1 )a aa

FD F D u p q D u p q D u q

2 1 1 2(1 ) (1 )b bb

FD F D u p q D u p q D u q

3 1 1 (1 ) 0l ll

FD F D u p q D u p q

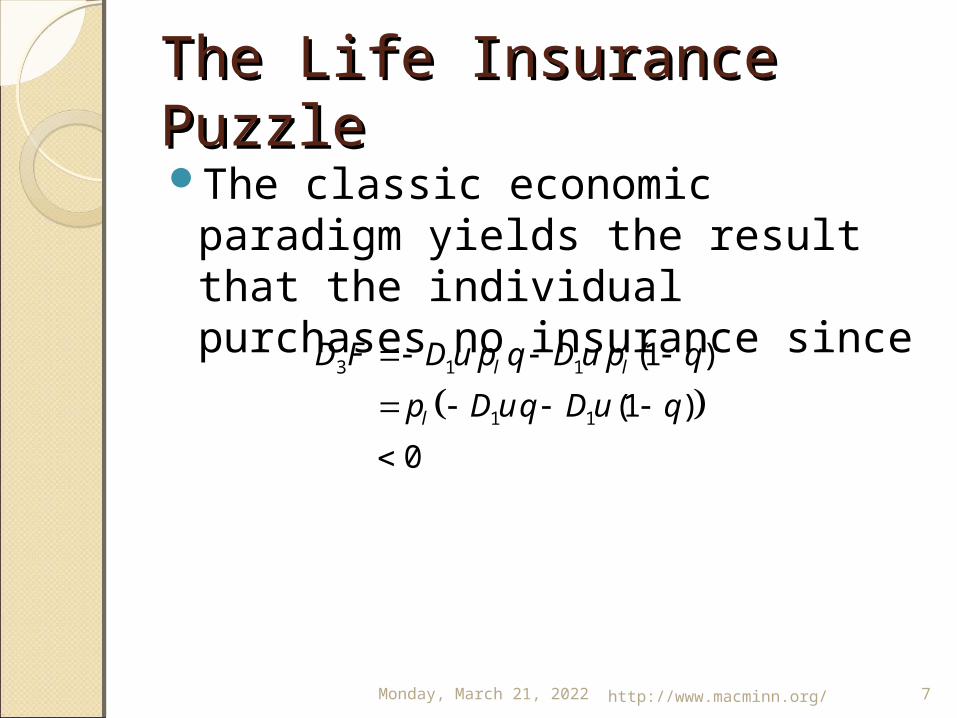

The Life Insurance PuzzleThe Life Insurance PuzzleThe classic economic paradigm yields the

result that the individual purchases no insurance since

Tuesday, April 18, 2023 http://www.macminn.org/ 7

3 1 1

1 1

(1 )

(1 )

0

l l

l

D F D u p q D u p q

p D u q D u q

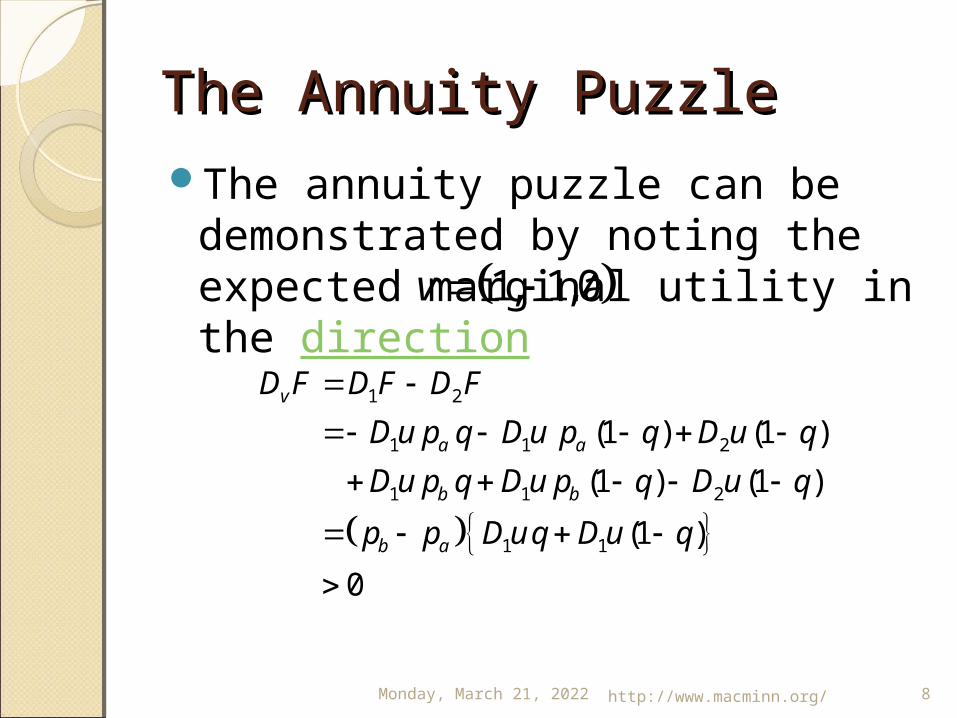

The Annuity PuzzleThe Annuity PuzzleThe annuity puzzle can be demonstrated

by noting the expected marginal utility in the direction

Tuesday, April 18, 2023 http://www.macminn.org/ 8

1, 1,0v

1 2

1 1 2

1 1 2

1 1

(1 ) (1 )

(1 ) (1 )

(1 )

0

v

a a

b b

b a

D F D F D F

D u p q D u p q D u q

D u p q D u p q D u q

p p D u q D u q

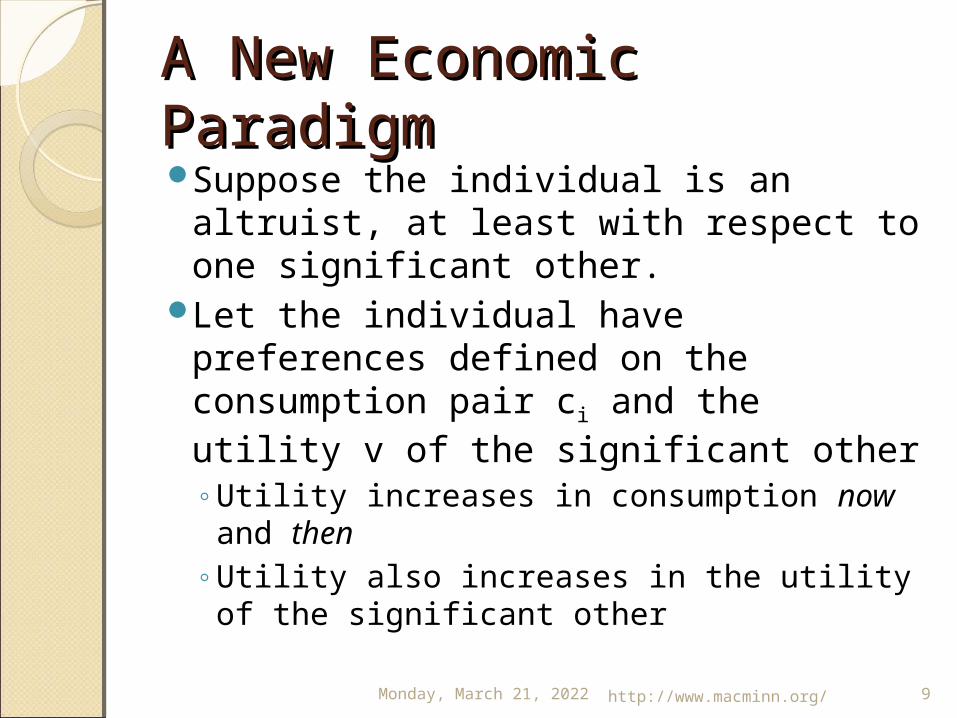

A New Economic ParadigmA New Economic ParadigmSuppose the individual is an altruist, at

least with respect to one significant other.Let the individual have preferences

defined on the consumption pair ci and the utility v of the significant other◦Utility increases in consumption now and then◦Utility also increases in the utility of the

significant other

Tuesday, April 18, 2023 http://www.macminn.org/ 9

Portfolio Theory againPortfolio Theory againConsumption now and then for the

individual and significant other

Tuesday, April 18, 2023 http://www.macminn.org/ 10

1

11

0

(1 ) 11id

ia bil

qc qc

qc q

1

11 11

b lsds

a bsl

qc qc

qc q

0 1i a a b b l lc w p p p

0s a a b b l lc w p p p

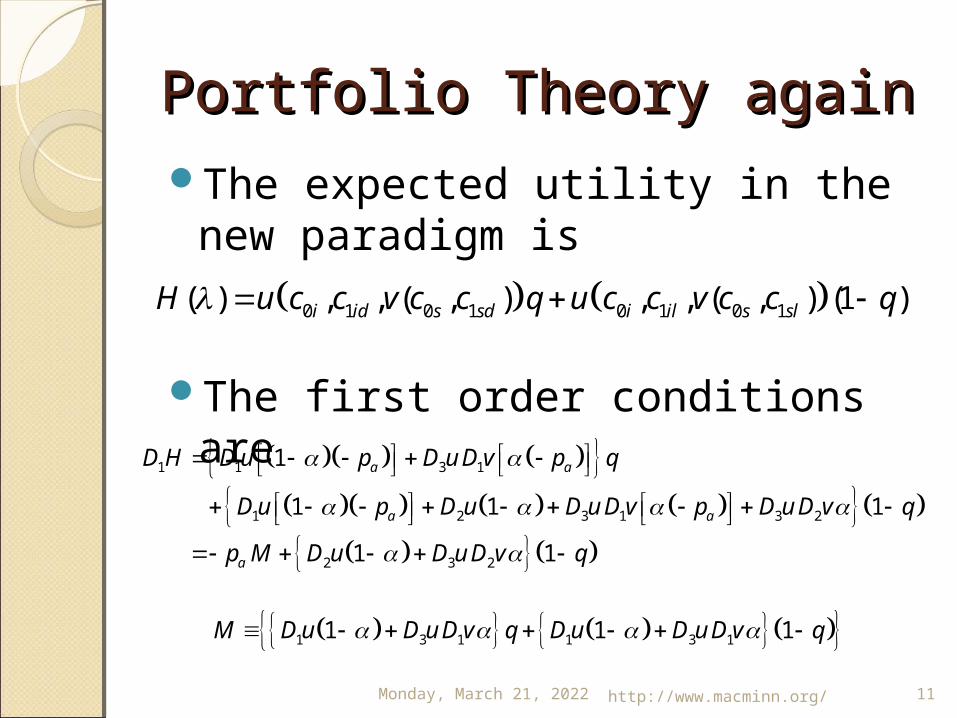

Portfolio Theory againPortfolio Theory againThe expected utility in the new paradigm

is

The first order conditions are

Tuesday, April 18, 2023 http://www.macminn.org/ 11

0 1 0 1 0 1 0 1( ) , , ( , ) , , ( , ) (1 )i id s sd i il s slH u c c v c c q u c c v c c q

1 1 3 1

1 2 3 1 3 2

2 3 2

1

1 1 1

1 1

a a

a a

a

D H D u p D u D v p q

D u p D u D u D v p D u D v q

p M D u D u D v q

1 3 1 1 3 11 1 1M D u D u D v q D u D u D v q

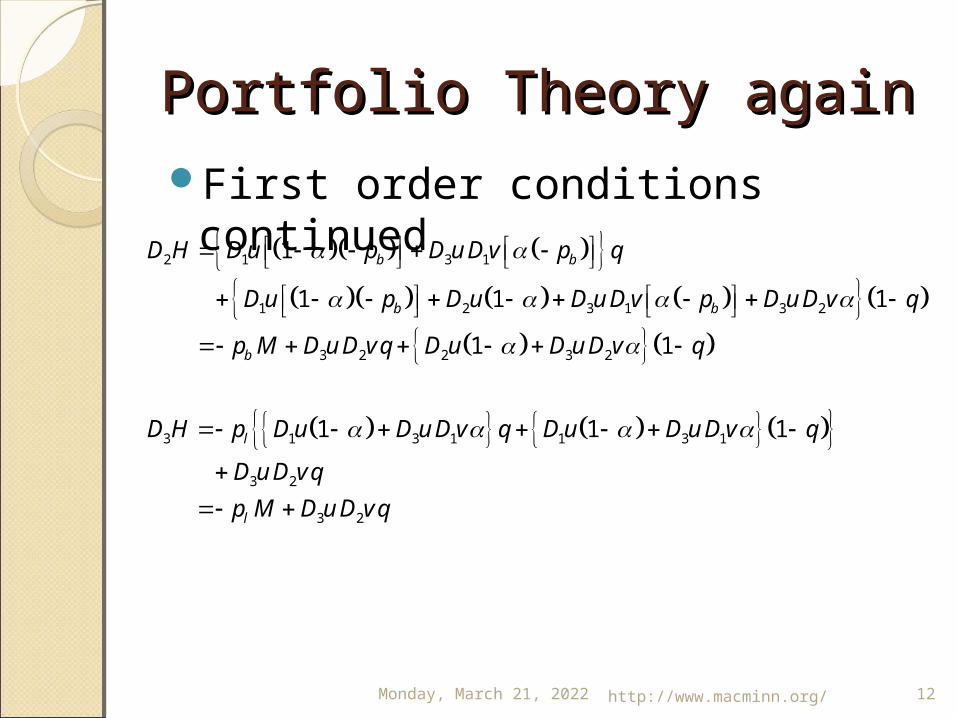

Portfolio Theory againPortfolio Theory againFirst order conditions continued

Tuesday, April 18, 2023 http://www.macminn.org/ 12

2 1 3 1

1 2 3 1 3 2

3 2 2 3 2

1

1 1 1

1 1

b b

b b

b

D H D u p D u D v p q

D u p D u D u D v p D u D v q

p M D u D v q D u D u D v q

3 1 3 1 1 3 1

3 2

3 2

1 1 1l

l

D H p D u D u D v q D u D u D v q

D u D v q

p M D u D v q

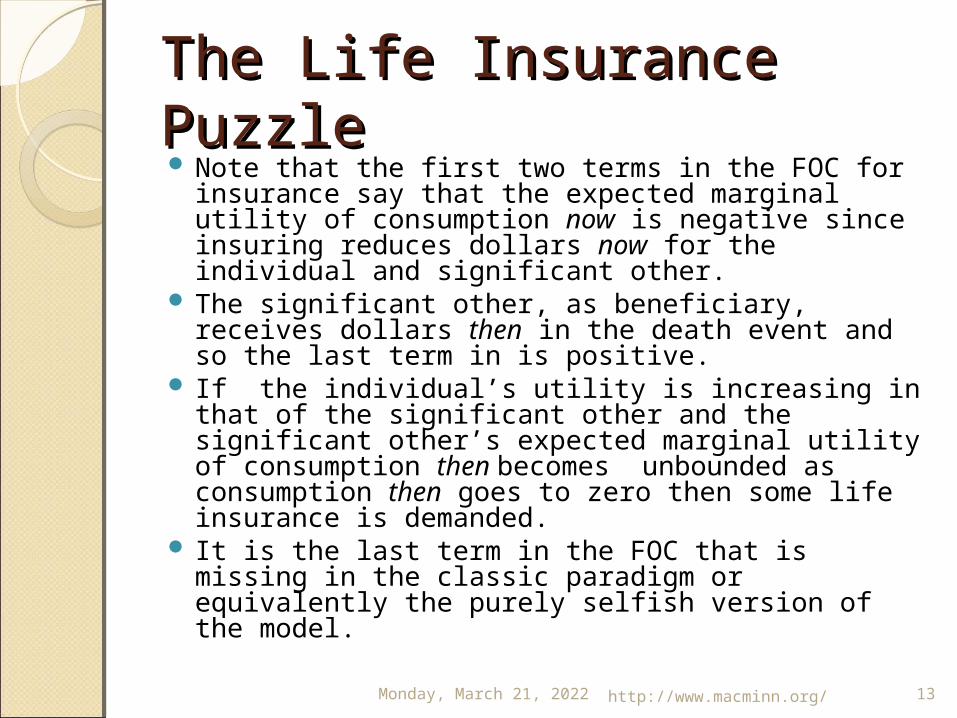

The Life Insurance PuzzleThe Life Insurance Puzzle Note that the first two terms in the FOC for insurance say that

the expected marginal utility of consumption now is negative since insuring reduces dollars now for the individual and significant other.

The significant other, as beneficiary, receives dollars then in the death event and so the last term in is positive.

If the individual’s utility is increasing in that of the significant other and the significant other’s expected marginal utility of consumption then becomes unbounded as consumption then goes to zero then some life insurance is demanded.

It is the last term in the FOC that is missing in the classic paradigm or equivalently the purely selfish version of the model.

Tuesday, April 18, 2023 http://www.macminn.org/ 13

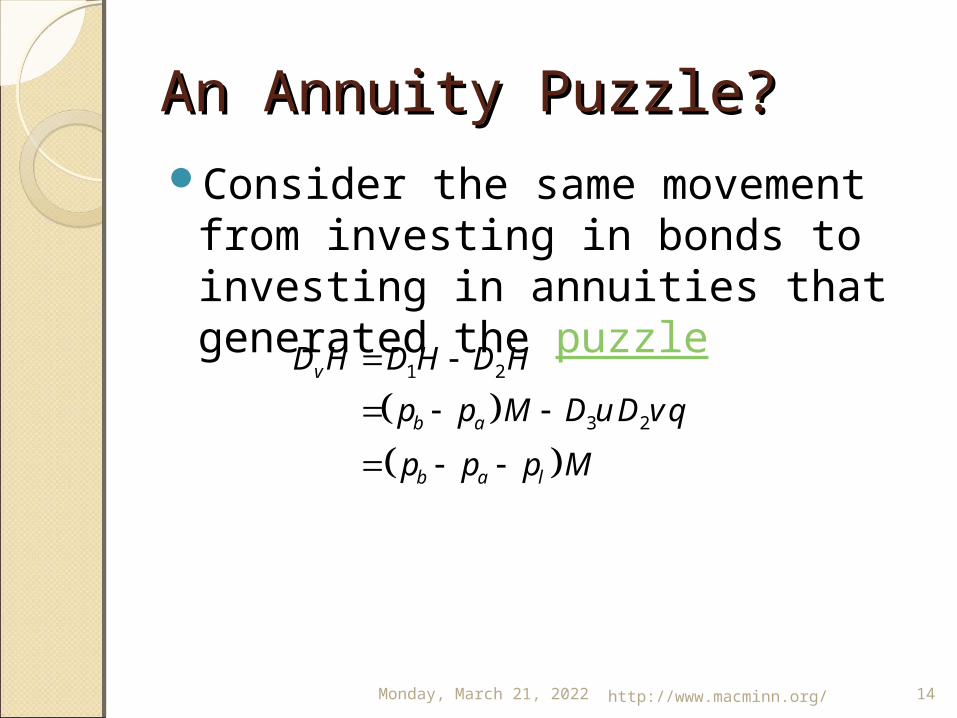

An Annuity Puzzle?An Annuity Puzzle?Consider the same movement from

investing in bonds to investing in annuities that generated the puzzle

Tuesday, April 18, 2023 http://www.macminn.org/ 14

1 2

3 2

v

b a

b a l

D H D H D H

p p M D u D v q

p p p M

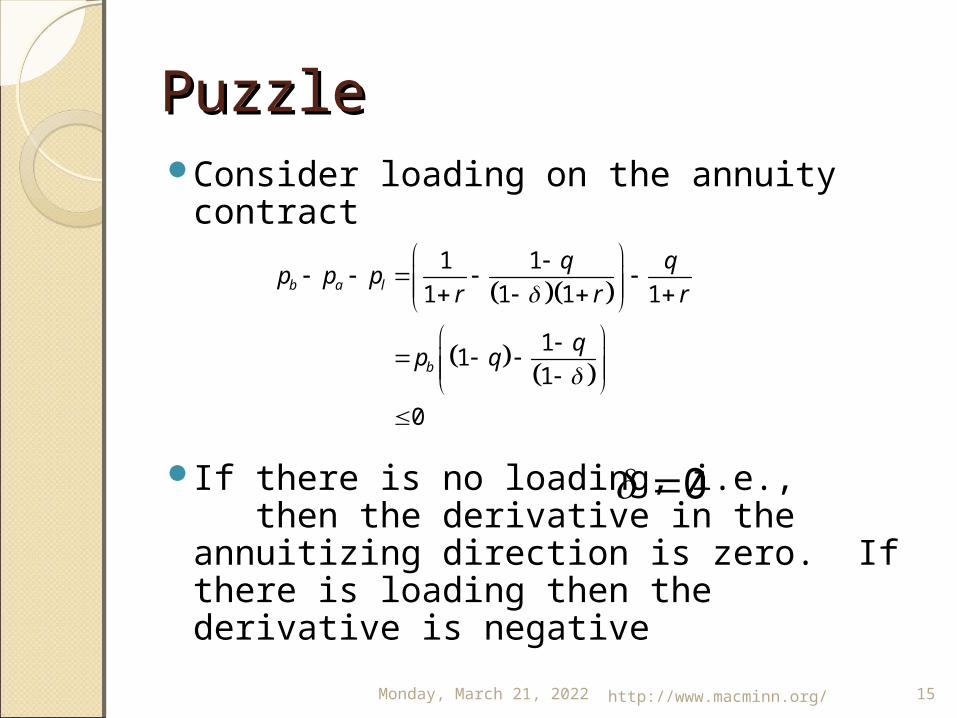

PuzzlePuzzleConsider loading on the annuity contract

If there is no loading, i.e., then the derivative in the annuitizing direction is zero. If there is loading then the derivative is negative

Tuesday, April 18, 2023 http://www.macminn.org/ 15

1 1

1 1 1 1

11

1

0

b a l

b

q qp p p

r r r

qp q

0

Extensions of the New ParadigmExtensions of the New Paradigm

Financial Distress◦Annuity provider◦Insurer

Health Risks

Tuesday, April 18, 2023 http://www.macminn.org/ 16

Financial DistressFinancial DistressConsider the risk of insolvency for the

annuity provider. How does this risk affect the demand for

annuities? If p is the probability of insolvency then p (1

– q) is the probability that the individual survives and has an annuity that does not provide the promised payment.

This changes the individual’s expected utility.

The demand for annuities is weakened even without altruism.

Tuesday, April 18, 2023 http://www.macminn.org/ 17

Health RiskHealth RiskConsider an uninsurable health risk that

necessitates a medical expenditure now.The wealth now becomes

where L represent the expense now that occurs with probability p. Also suppose that the health risk does not affect the mortality rate.

Suppose that the annuity is illiquid.Such a health risk eliminates or reduces

the demand for annuities.

Tuesday, April 18, 2023 http://www.macminn.org/ 18

1

w L pW

w p

Concluding remarksConcluding remarksThe economic paradigm must be changed so

that the demand for life insurance can be rationalized. This analysis does that.

This analysis provides the theoretical foundation for the bequest motive.

There is no annuity puzzle in the new paradigm.

Financial distress may weaken the annuity demand.

A health risk may eliminate the annuity demand.

Tuesday, April 18, 2023 http://www.macminn.org/ 19