Embed Size (px)

Citation preview

Prepared by Pete Benner for U of M AFSCME

1

THE AFFORDABLE CARE ACTAND UNIVERSITY OF MINNESOTA

EMPLOYEES AND FAMILIES

November 7,2013

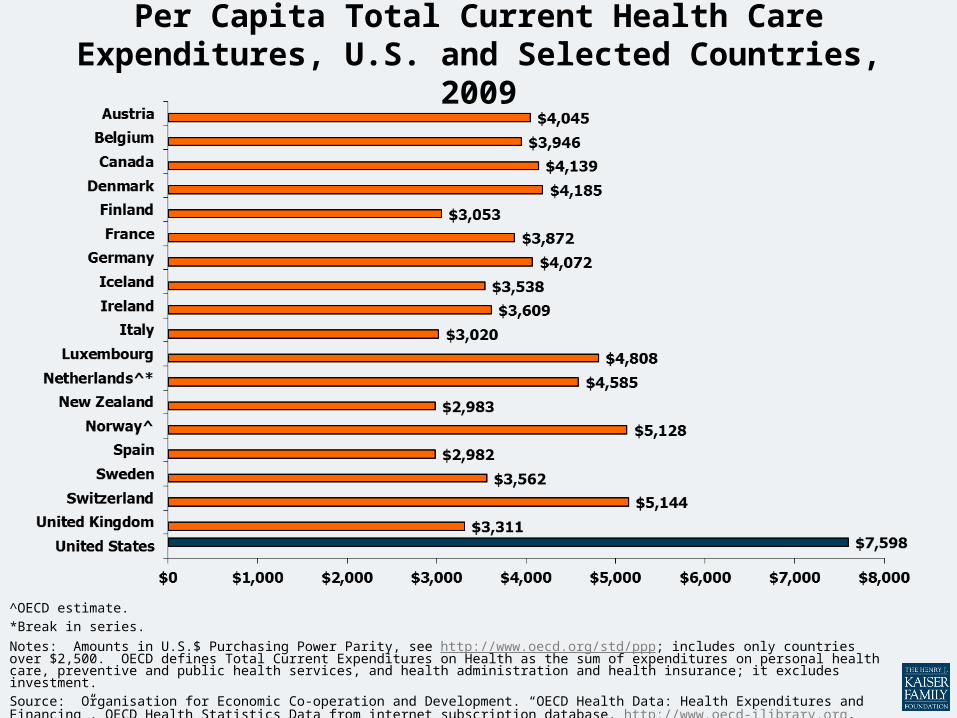

Per Capita Total Current Health Care Expenditures, U.S. and Selected Countries, 2009

^OECD estimate.*Break in series.Notes: Amounts in U.S.$ Purchasing Power Parity, see http://www.oecd.org/std/ppp; includes only countries over $2,500. OECD defines Total Current Expenditures on Health as the sum of expenditures on personal health care, preventive and public health services, and health administration and health insurance; it excludes investment. Source: Organisation for Economic Co-operation and Development. “OECD Health Data: Health Expenditures and Financing”, OECD Health Statistics Data from internet subscription database. http://www.oecd-ilibrary.org, data accessed on 01/10/12.

Prepared by Pete Benner for U of M AFSCME

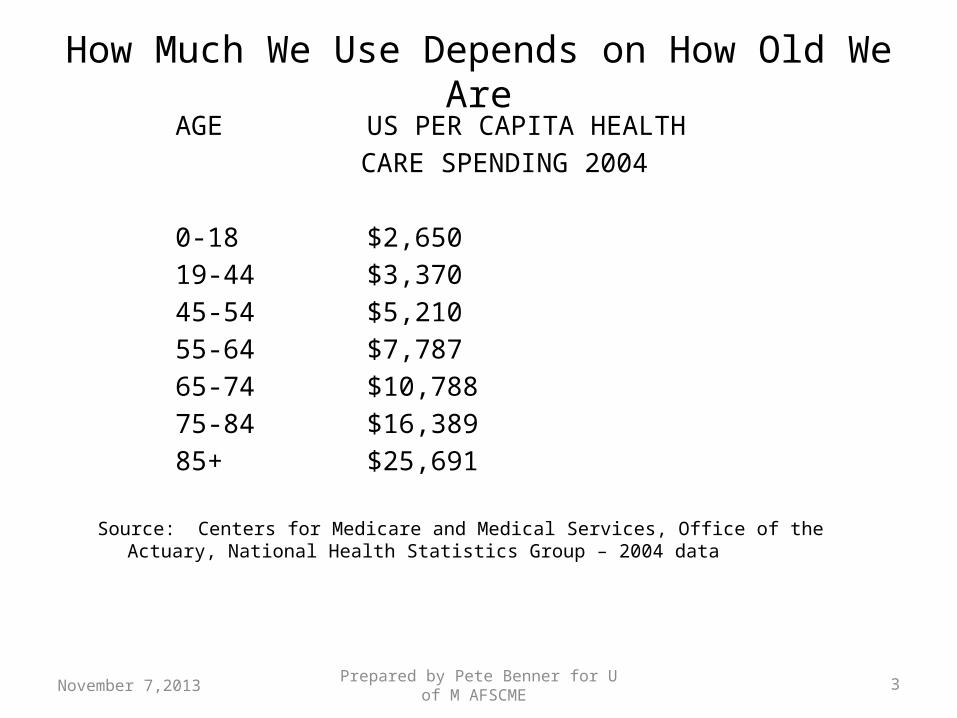

How Much We Use Depends on How Old We AreAGE US PER CAPITA HEALTH

CARE SPENDING 2004

0-18 $2,650 19-44 $3,370 45-54 $5,210 55-64 $7,787 65-74 $10,788 75-84 $16,389

85+ $25,691

Source: Centers for Medicare and Medical Services, Office of the Actuary, National Health Statistics Group – 2004 data

3November 7,2013

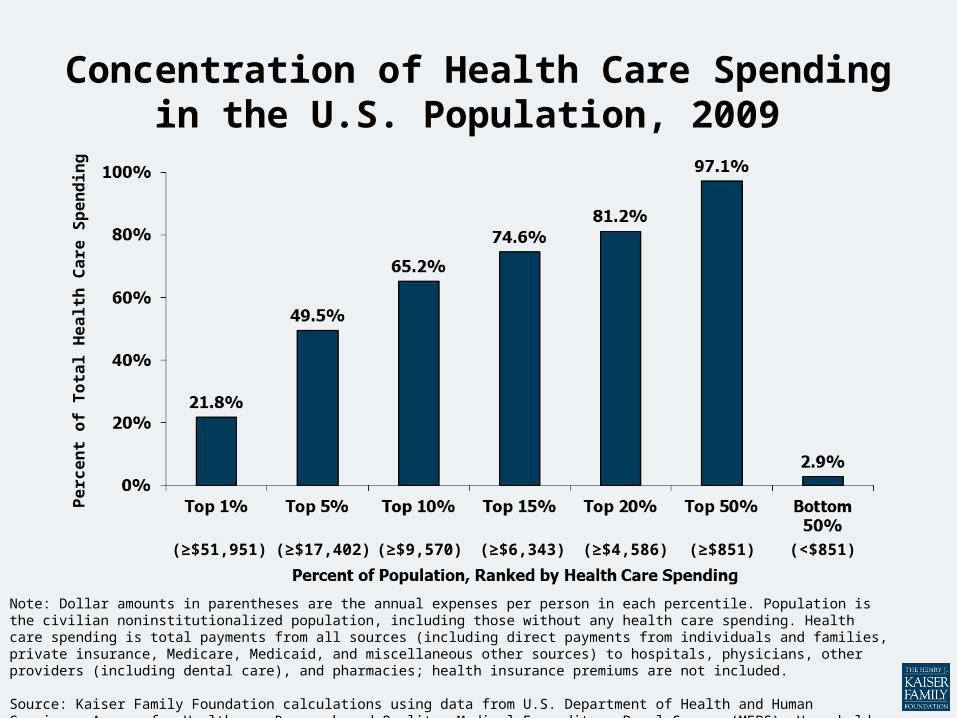

Note: Dollar amounts in parentheses are the annual expenses per person in each percentile. Population is the civilian noninstitutionalized population, including those without any health care spending. Health care spending is total payments from all sources (including direct payments from individuals and families, private insurance, Medicare, Medicaid, and miscellaneous other sources) to hospitals, physicians, other providers (including dental care), and pharmacies; health insurance premiums are not included.

Source: Kaiser Family Foundation calculations using data from U.S. Department of Health and Human Services, Agency for Healthcare Research and Quality, Medical Expenditure Panel Survey (MEPS), Household Component, 2009.

Concentration of Health Care Spending in the U.S. Population, 2009

(≥$51,951)

(≥$17,402)

(≥$9,570) (≥$6,343) (≥$4,586) (≥$851) (<$851)

Perc

en

t of

Tota

l H

ealt

h C

are

Sp

en

din

g

Prepared by Pete Benner for U of M AFSCME

5

It’s the Prices Stupid!• “It is higher health care spending coupled with lower

– not higher – use of health services that adds up to much higher prices in the United States than in any other member nation of the Organization for Economic Cooperation and Development. Aside from a few high-tech services, Americans actually use less health care and rely on fewer health-care resources than do residents of other industrialized countries.” Uwe Reinhardt, New York Times Economix Blog, March 29, 2013

November 7,2013

Prepared by Pete Benner for U of M AFSCME

6

Take Aways

• Healthy need to help pay for the sick• Young need to help pay of the old• Well Off need to help pay for the rest of us• It is not the fault of the patient – which is not

the same as saying patients do not sometimes ask for care which adds no value or might actually hurt them

November 7,2013

Prepared by Pete Benner for U of M AFSCME

7

Affordable Care Act So Far

• Affordable Care Act Passes 2010.• Adult Children to Age 25 – 2011 - regardless of

residence, school attendance, marital status• Guaranteed Issue Kids• Early Retiree Reinsurance Program – help

employers maintain coverage for pre-65 retirees.

November 7,2013

Prepared by Pete Benner for U of M AFSCME

8

ACA So Far

• Health Plan Loss Ratios capped at 80% for individual and small group markets and 85% for large group market.

• Increased Medicare taxes for the 1% - 2013• Closing of the Medicare Rx Donut Hole - 2013

November 7,2013

Prepared by Pete Benner for U of M AFSCME

9

What’s Next?

• Individual Mandate for Adults Starts 2014• Employer Mandate Starts 2015• Medical Assistance Expansion to 138% FPL

starts 2014• Minnesota Health Insurance Exchange Starts

2014• Premium and Out of Pocket Subsidies in

Individual Market Start in 2014

November 7,2013

Prepared by Pete Benner for U of M AFSCME

10

Individual Mandate

• Everyone Must Have Health Insurance Coverage or Pay Penalty

• Insurance must provide “Minimum Essential” Coverage

• 2014 Penalty of $95 or 1% of household income• 2015 Penalty of $325 or 2% of household income• 2016 Penalty of $695 or 2.5% of household income• Medical Assistance, Medicare, VA, TriCare,

Employment based coverage, and individual coverage all meet the requirement for coverage.

November 7,2013

Prepared by Pete Benner for U of M AFSCME

11

Help for Minnesotans• In January, Minnesotans will be covered from

birth to age 65 by a combination of Medical Assistance, MinnesotaCare, and MNsure.

• Some of this will be continuation of existing programs and some will be new programs from the Affordable Care Act.

November 7,2013

Prepared by Pete Benner for U of M AFSCME

12

Minnesota Insurance Marketplace MNsure

• Offer health plans to individuals who want premium or out of pocket subsidies.

• Offer health plans to small employers.• Administer premium and out of pocket subsidies.• Train and Oversee “Navigators” and “In-Person

Assisters”.• Run single seamless enrollment and eligibility

determination system for public programs and for MNsure.

November 7,2013

Prepared by Pete Benner for U of M AFSCME

13

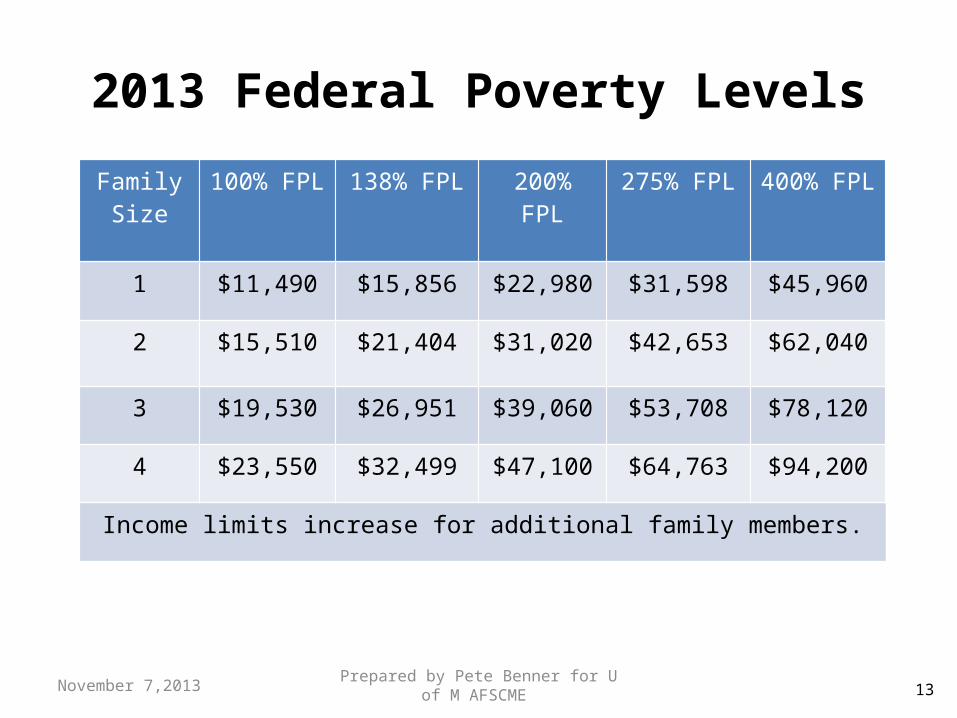

2013 Federal Poverty Levels

FamilySize

100% FPL 138% FPL 200% FPL

275% FPL 400% FPL

1 $11,490 $15,856 $22,980 $31,598 $45,960

2 $15,510 $21,404 $31,020 $42,653 $62,040

3 $19,530 $26,951 $39,060 $53,708 $78,120

4 $23,550 $32,499 $47,100 $64,763 $94,200

Income limits increase for additional family members.

November 7,2013

Prepared by Pete Benner for U of M AFSCME

Modified Adjusted Gross Income

• MAGI is your adjusted gross income from your federal tax form – adding in any non-taxable social security income and any tax-exempt interest – and for eligibility for Medical Assistance taking out scholarships, awards or grants used for educational purposes (plus a couple other things that will not impact many people). Separate rules for American Indians.

14November 7,2013

Prepared by Pete Benner for U of M AFSCME

Who will MNsure serve?• Medical Assistance

– Medical Assistance: kids and pregnant women under 275% FPL – regardless of whether covered or can be covered under employer sponsored insurance

– Medical Assistance: Adults below 138% FPL – regardless of whether covered or can be covered under employer sponsored insurance

– No asset test

– Coverage options determined by Department of Human Services

– Care provided through health plans – no premium, $2.65/month deductible, $3 office copay and Drug copays no more than $3 for MA

– If currently covered by employer, MA may have you stay on your insurance and reimburse premium and out of pocket.

15November 7,2013

Prepared by Pete Benner for U of M AFSCME

Who will MNsure serve?• MinnesotaCare

– MinnesotaCare: Adults between 138% and 200% FPL – but only of they cannot be covered under “affordable” employer sponsored insurance either as an employee or as a dependent

– Full Benefit Set for all adults

– No asset test

– Coverage options determined by Department of Human Services

– Care provided through health plans – premium from $4 to $50/month/adult, $2.65/month deductible, $3 office copay, $3 drug copay and $3.50 ER copay for MinnesotaCare.

– If currently covered by employer, would need to dis-enroll during open enrollment period

16November 7,2013

Prepared by Pete Benner for U of M AFSCME

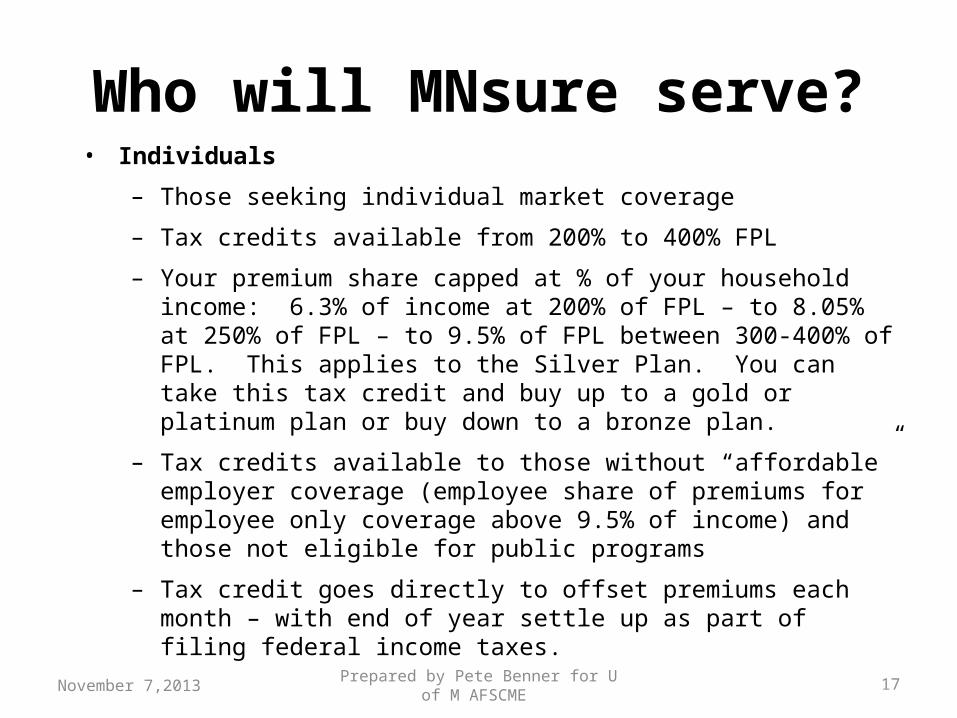

Who will MNsure serve?• Individuals

– Those seeking individual market coverage

– Tax credits available from 200% to 400% FPL

– Your premium share capped at % of your household income: 6.3% of income at 200% of FPL – to 8.05% at 250% of FPL – to 9.5% of FPL between 300-400% of FPL. This applies to the Silver Plan. You can take this tax credit and buy up to a gold or platinum plan or buy down to a bronze plan.

– Tax credits available to those without “affordable” employer coverage (employee share of premiums for employee only coverage above 9.5% of income) and those not eligible for public programs

– Tax credit goes directly to offset premiums each month – with end of year settle up as part of filing federal income taxes.

17November 7,2013

Prepared by Pete Benner for U of M AFSCME

18

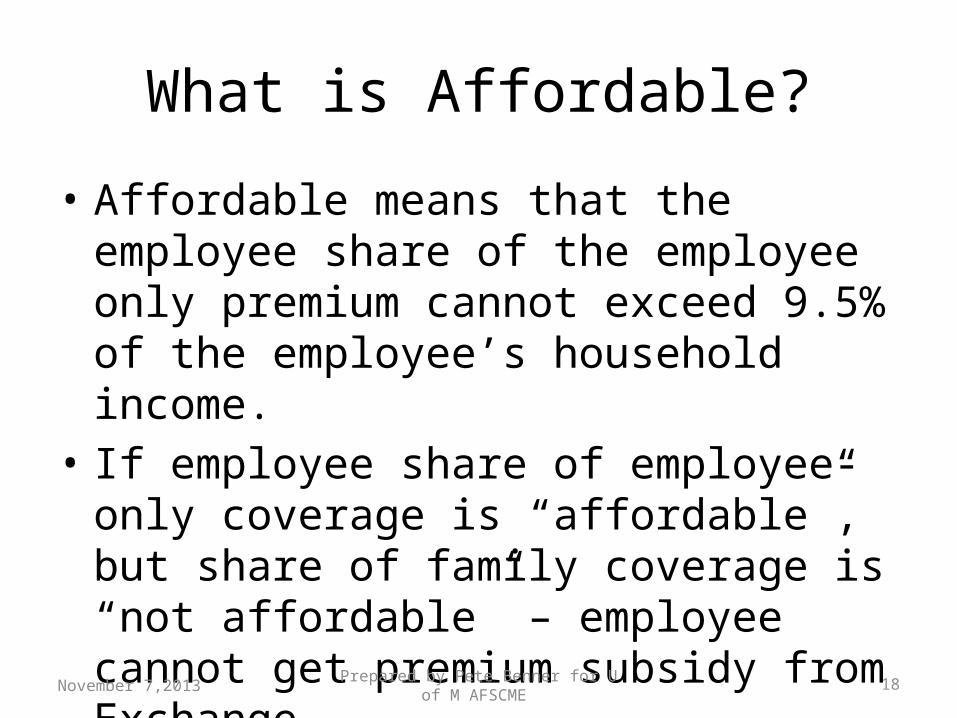

What is Affordable?

• Affordable means that the employee share of the employee only premium cannot exceed 9.5% of the employee’s household income.

• If employee share of employee-only coverage is “affordable”, but share of family coverage is “not affordable” – employee cannot get premium subsidy from Exchange.

November 7,2013

Prepared by Pete Benner for U of M AFSCME

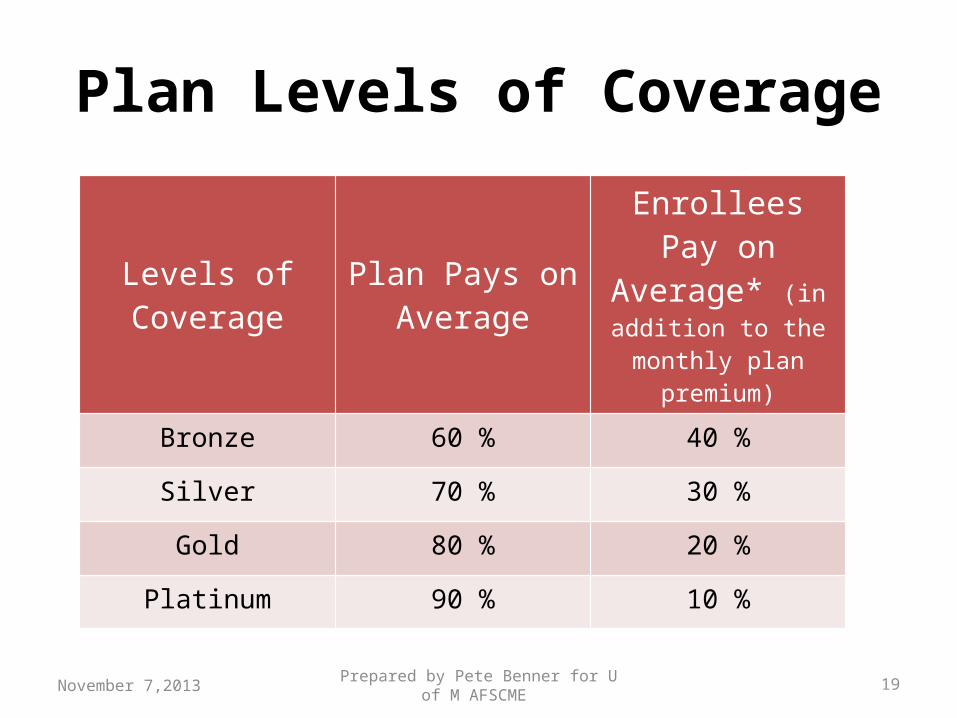

Plan Levels of Coverage

Levels of Coverage

Plan Pays on Average

Enrollees Pay on Average* (in

addition to the monthly plan

premium)

Bronze 60 % 40 %

Silver 70 % 30 %

Gold 80 % 20 %

Platinum 90 % 10 %

19November 7,2013

Prepared by Pete Benner for U of M AFSCME

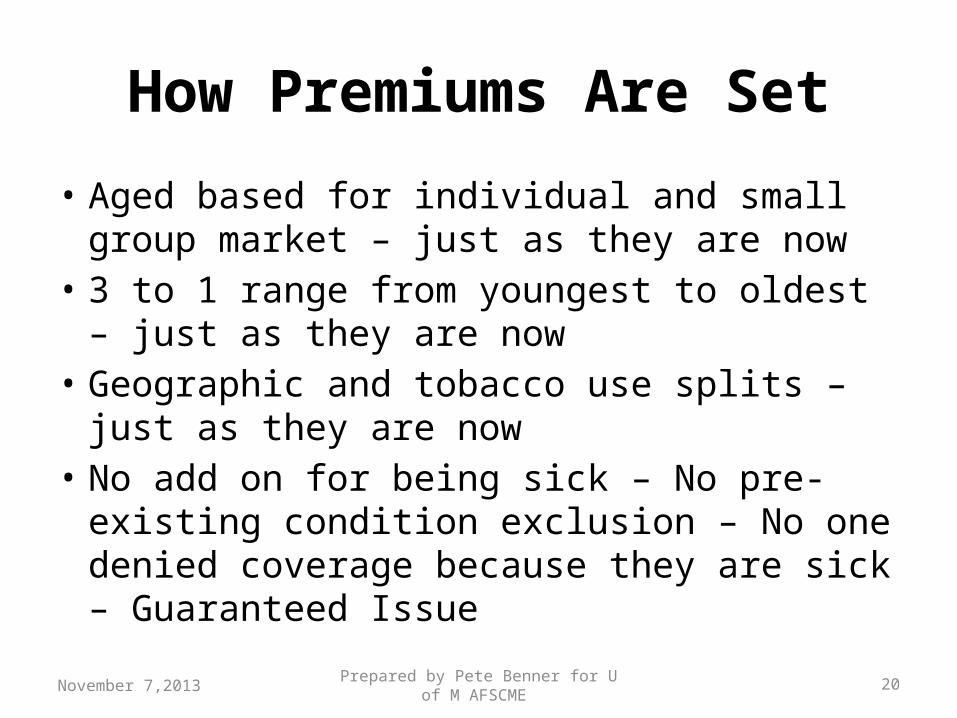

How Premiums Are Set

• Aged based for individual and small group market – just as they are now

• 3 to 1 range from youngest to oldest – just as they are now

• Geographic and tobacco use splits – just as they are now

• No add on for being sick – No pre-existing condition exclusion – No one denied coverage because they are sick – Guaranteed Issue

20November 7,2013

Prepared by Pete Benner for U of M AFSCME

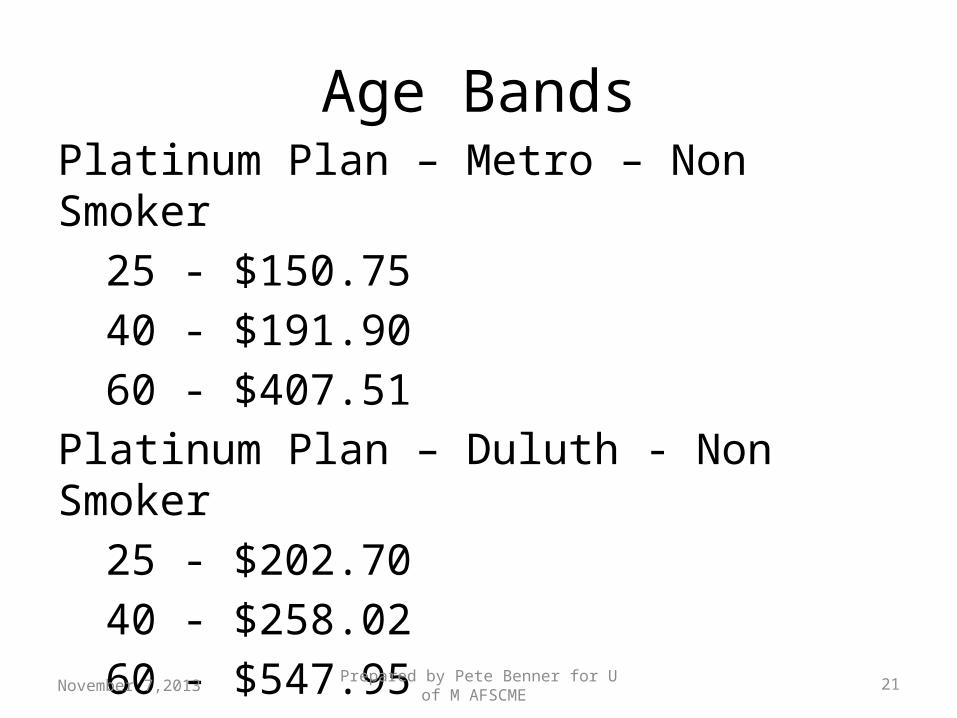

21

Age BandsPlatinum Plan – Metro – Non Smoker

25 - $150.7540 - $191.9060 - $407.51

Platinum Plan – Duluth - Non Smoker25 - $202.7040 - $258.0260 - $547.95

November 7,2013

Prepared by Pete Benner for U of M AFSCME

22

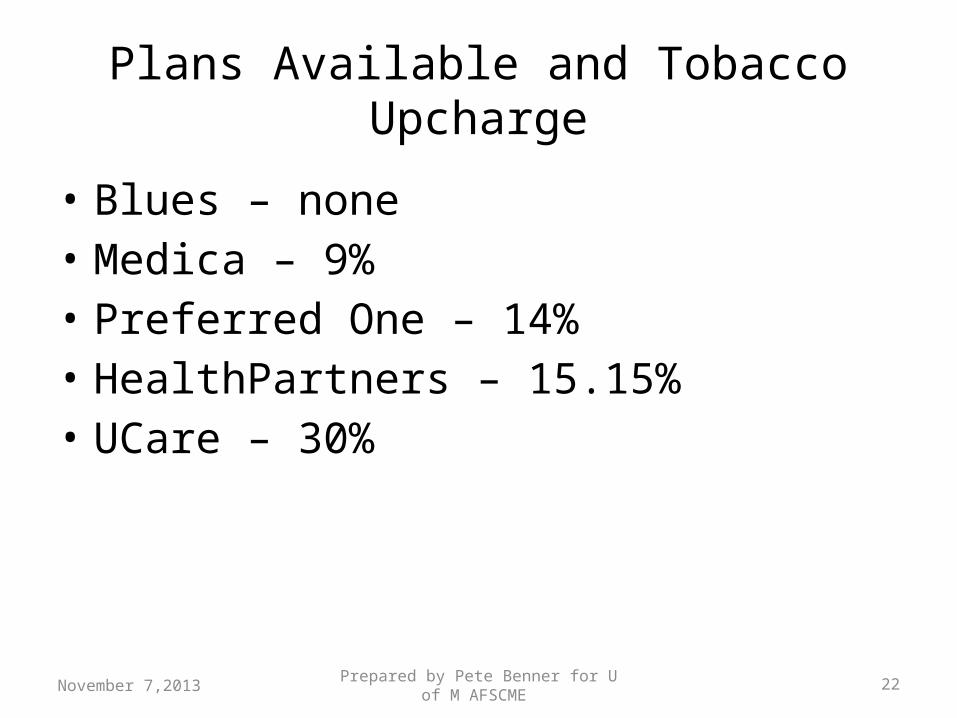

Plans Available and Tobacco Upcharge

• Blues – none• Medica – 9%• Preferred One – 14%• HealthPartners – 15.15%• UCare – 30%

November 7,2013

Prepared by Pete Benner for U of M AFSCME

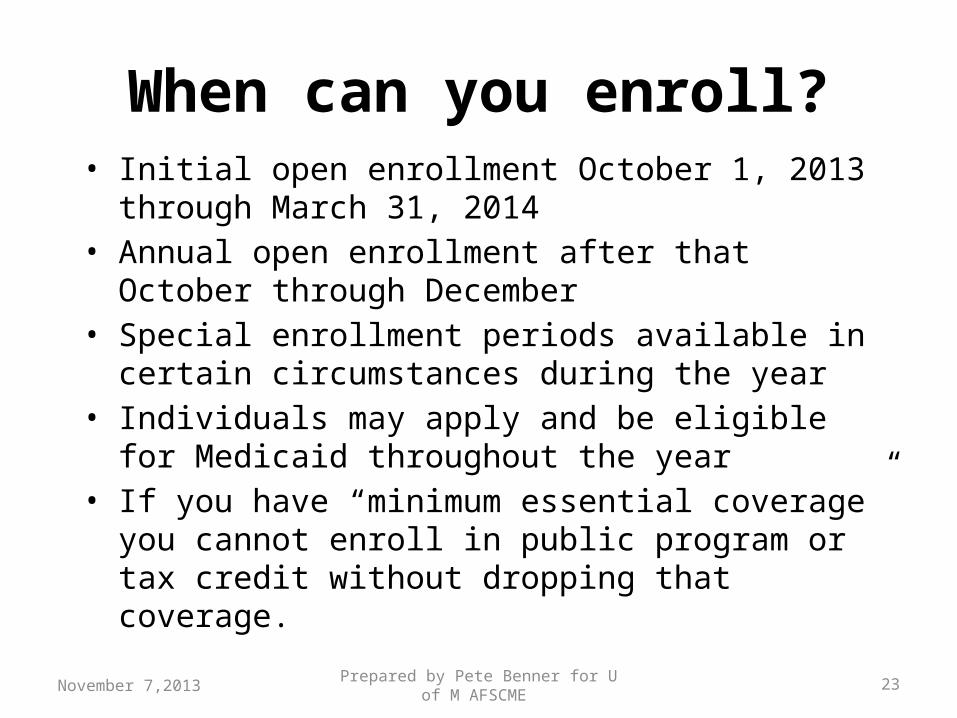

When can you enroll?• Initial open enrollment October 1, 2013 through March 31,

2014• Annual open enrollment after that October through

December • Special enrollment periods available in certain

circumstances during the year• Individuals may apply and be eligible for Medicaid

throughout the year• If you have “minimum essential coverage” you cannot enroll

in public program or tax credit without dropping that coverage.

23November 7,2013

Prepared by Pete Benner for U of M AFSCME

MNsure Assisters

Website

Toll-free call

center

In-Person Assista

nce

Help when you

need it

24November 7,2013

Prepared by Pete Benner for U of M AFSCME

Who Wins?• Kids, Grandkids and Pregnant Women to Medical Assistance• Lowest Income workers to Medical Assistance no matter

what• Workers excluded from employer coverage to MNsure• Workers for whom employee only coverage is not affordable

to MNsure• Workers on unpaid leave or layoff to MNsure. Former

employees to MNsure. • Pre-65 early retirees to MNsure. Public sector retirees with

Health Care Savings Plans through MSRS can use that money to pay MNsure premiums and still get premium tax credit.

25November 7,2013

Prepared by Pete Benner for U of M AFSCME

26

MNSURE

www.mnsure.org

November 7,2013