Embed Size (px)

Citation preview

The Accounting Cycle

1.) Transactions occur in the normal course of business. We record them in our records with a JOURNAL ENTRY (called “Journalizing”).

(Equivalent of entering a row on transaction worksheet)

2.) Journal entries are then “transferred” to the GENERAL LEDGER (called “Posting”).

(Equivalent of putting dollar amount in a column on the transaction worksheet)

3.) A trial balance may be prepared. It shows the balance (amount and whether debit or credit) of each account. A trial balance is NOT the same as a “Balance Sheet”, which is a formal financial statement.

The Process

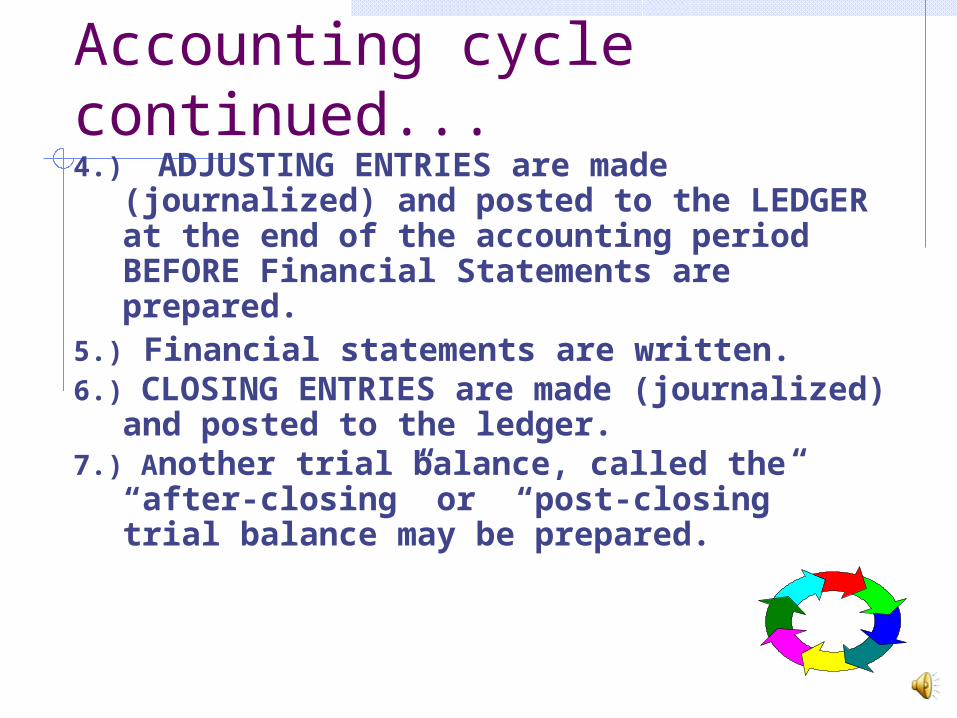

Accounting cycle continued...4.) ADJUSTING ENTRIES are made

(journalized) and posted to the LEDGER at the end of the accounting period BEFORE Financial Statements are prepared.

5.) Financial statements are written.6.) CLOSING ENTRIES are made

(journalized) and posted to the ledger. 7.) Another trial balance, called the “after-

closing” or “post-closing” trial balance may be prepared.

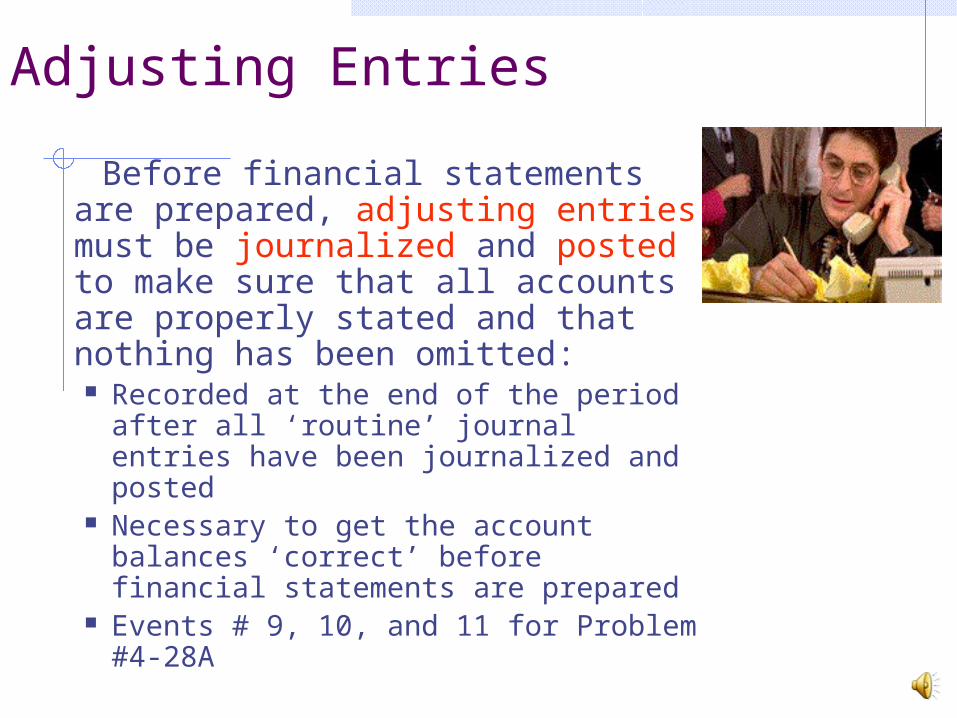

Adjusting Entries

Before financial statements are prepared, adjusting entries must be journalized and posted to make sure that all accounts are properly stated and that nothing has been omitted: Recorded at the end of the period

after all ‘routine’ journal entries have been journalized and posted

Necessary to get the account balances ‘correct’ before financial statements are prepared

Events # 9, 10, and 11 for Problem #4-28A

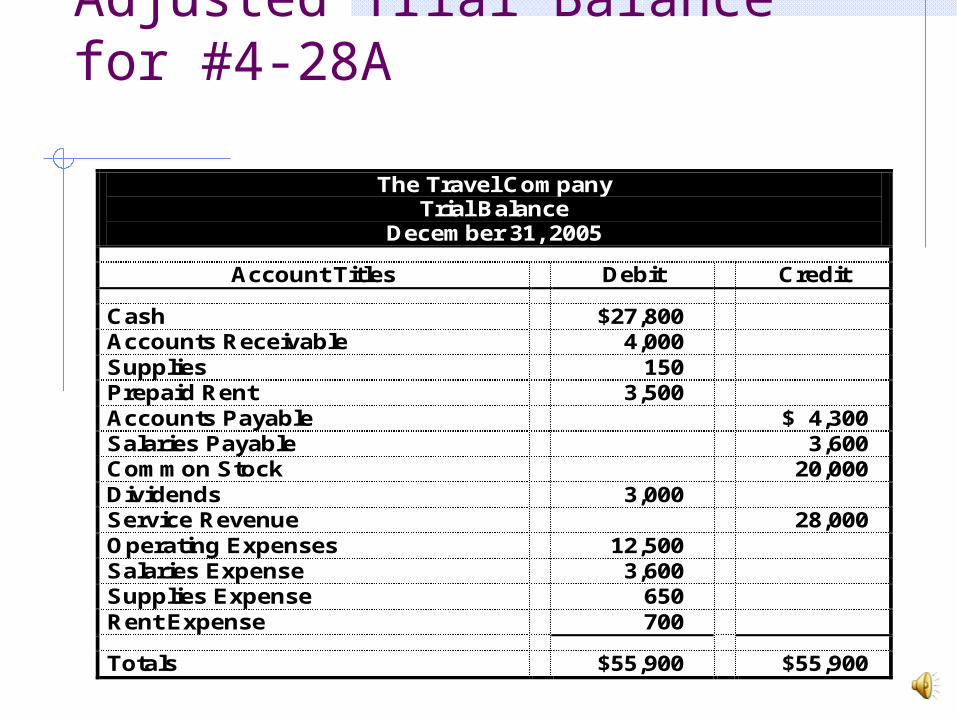

Trial Balance for Prob. 4-28A

The Slide for The Travel Company (Prob. 4-28A) is an “Adjusted Trial Balance”—it reflects the account balances after the three adjusting entries (#9, 10, & 11) have been journalized and posted to the ledger accounts.

(This file is among the files I provided to you)

Adjusted Trial Balance for #4-28A

The Travel Company Trial Balance

December 31, 2005

Account Titles Debit Credit

Cash $27,800 Accounts Receivable 4,000 Supplies 150 Prepaid Rent 3,500 Accounts Payable $ 4,300 Salaries Payable 3,600 Common Stock 20,000 Dividends 3,000 Service Revenue 28,000 Operating Expenses 12,500 Salaries Expense 3,600 Supplies Expense 650 Rent Expense 700

Totals $55,900 $55,900

LEDGER ACCOUNT BALANCES after the adjusting entries, but before the closing entries, are the dollar amounts that go on the financial statements.

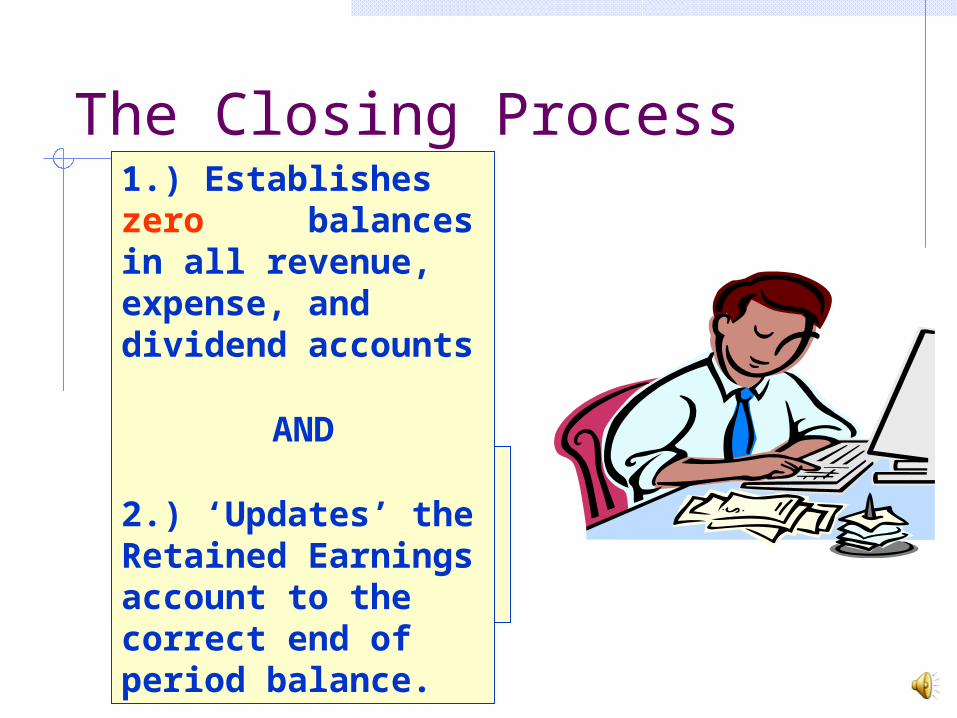

The Closing Process

Let’s look at the closing entries for

Collins Consultants.

1.) Establishes zero balances in all revenue, expense, and dividend accounts

AND

2.) ‘Updates’ the Retained Earnings account to the correct end of period balance.

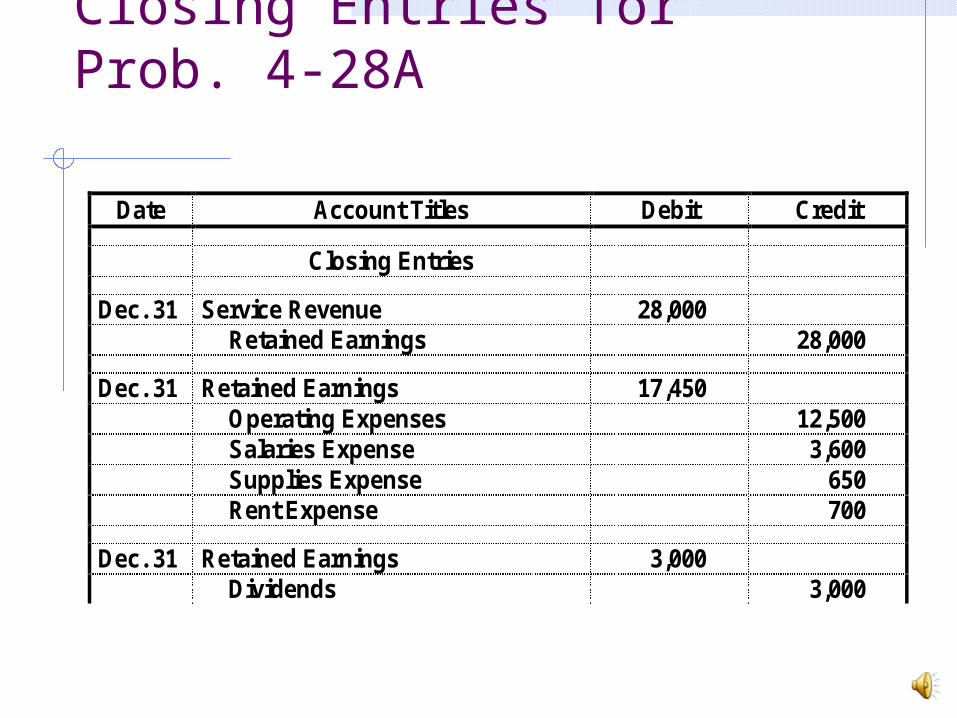

Closing Entries for Prob. 4-28A

Follow the three step approach for closing entries for the Class problem:

1) Close out (get to zero balance) the revenue accounts

2) Close out (get to zero balance) the expense accounts

3) Close out (get to zero balance) the dividends account

Review the ‘after-closing’ trial balance: Which accounts are missing? Which account has a different dollar

balance?

Closing Entries for Prob. 4-28A

Date Account Titles Debit Credit

Closing Entries

Dec. 31 Service Revenue 28,000 Retained Earnings 28,000

Dec. 31 Retained Earnings 17,450 Operating Expenses 12,500 Salaries Expense 3,600 Supplies Expense 650 Rent Expense 700

Dec. 31 Retained Earnings 3,000 Dividends 3,000

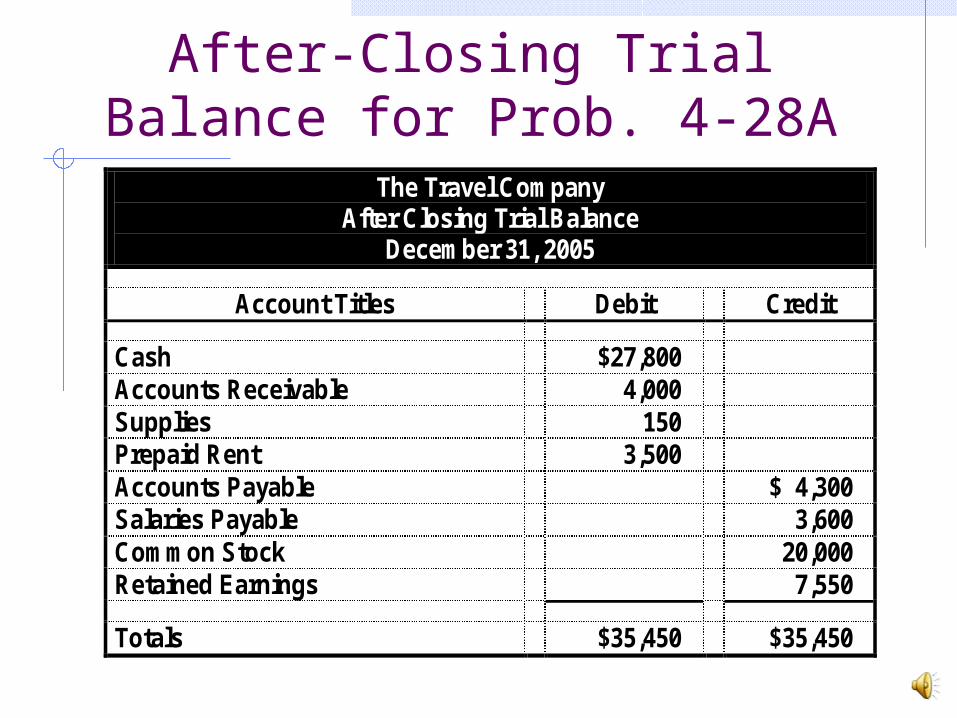

After-Closing Trial Balance for Prob. 4-28A

The Travel Company After Closing Trial Balance

December 31, 2005

Account Titles Debit Credit

Cash $27,800 Accounts Receivable 4,000 Supplies 150 Prepaid Rent 3,500 Accounts Payable $ 4,300 Salaries Payable 3,600 Common Stock 20,000 Retained Earnings 7,550

Totals $35,450 $35,450

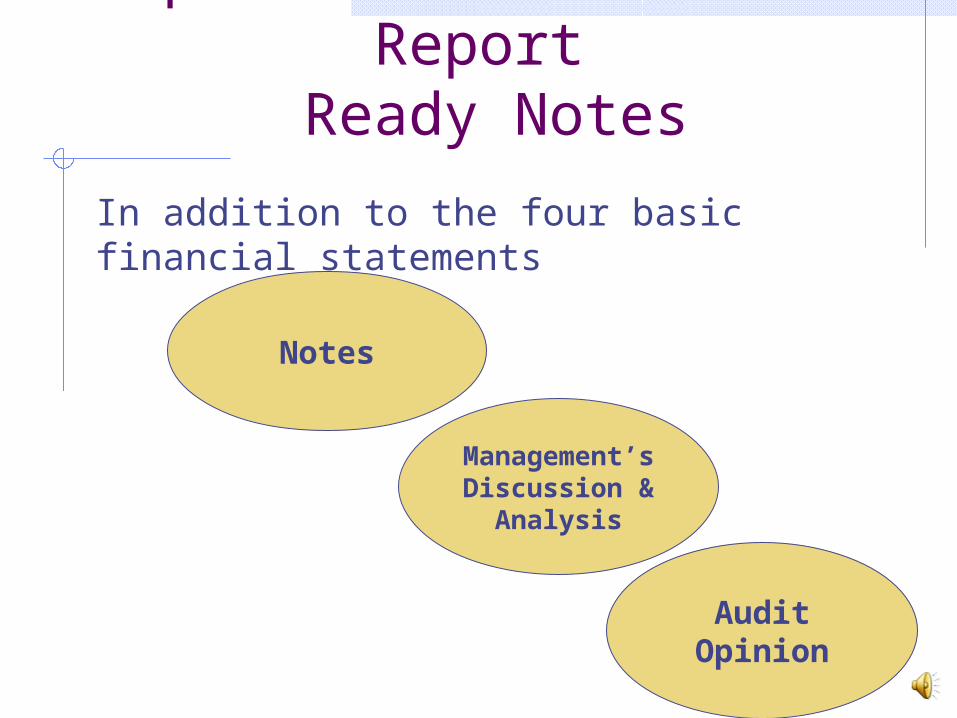

Components of the Annual Report

Ready Notes

Notes

Management’s Discussion & Analysis

Audit Opinion

In addition to the four basic financial statements

Class Assignment Questions

Questions 1, 13, 15-17 (Page 181 in textbook)

Chapter 4

The End