Embed Size (px)

Citation preview

iTHE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

(NBAA)THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS

TANZANIA

THE ACCOUNTANCY PROFESSIONAL SYLLABUS

Executive DirectorNational Board of Accountants and Auditors (NBAA)

National Audit Office “Audit House” 8th Floor, 4 Ukaguzi Road, P.O. Box 1271,

41104, Tambukareli,Tel: +255 26 2963318-9

Email: [email protected]: www.nbaa.go.tz

JUNE 2019

ii THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

1THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

1.0 INTRODUCTIONThis Handbook has been prepared to provide guidance to trainers and candidates preparing for the Board’s examinationsin the Professional Examination Scheme leading to the Certified Public Accountant (CPA) qualification. The handbookshould be read in conjunction with the NBAA Examination and Training Bylaws.

The handbook shows the examination structure and subject relationship/progression as one moves from the lower to the final level. Details concerning candidacy registration, exemption requests, examination entry and training requirements are provided to enable a prospective candidate to easily follow the requirements when applying for candidacy registration and/or requesting for exemption.

For candidates transferring from the phased out syllabus to the new syllabus, a detailed conversion scheme has been provided to guide the candidate on what papers he/she would be eligible to attempt. The handbook further prescribes the syllabus to be followed in preparation for the examinations. Under each subject area the following items are indicated:

Contact Hours: It is the expected duration that a candidate should spend in direct contact with a tutor or lecturer to sufficiently cover the subject matter.

Subject Descriptions: This provides an overview of the subject matter on what this subject entails to cover.

Aims and Objectives: These broadly show the aims and objectives of the subject matter.

Pre-requisite subject: this shows the lower subject which determines the understanding of the corresponding higher level subject

Learning Outcomes: These are the expected outputs in the course of learning showing the knowledge and skills that are expected to be imparted to candidates on completion of the course.

2 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Teaching and Learning Strategies: These are the expected inputs in the course of learning

Contents: These show descriptions of areas to be covered in the subject matter.

Time Allocation: It provides guidance on the number of hours to be spent in covering a topic in the subject area.

References: This provides the recommended reading material to be used in the course of learning where main reading is the study guide that has been prepared carefully to cover the whole syllabus for each subject area.

2.0 ABOUT NBAAThe National Board of Accountants and Auditors (NBAA) was established in 1972 by authority of the Auditors and Accountants (Registration) Act No.33 as amended by Act No. 2 of 1995, to among other things, promote and provide opportunities and facilities for the study of, and training in accountancy, auditing and allied subjects. In executing such responsibilities, the Board conducts accountancy examinations twice in a year.

3.0 THE EXAMINATIONSThe Board administers a two tier examination scheme in the following categories(i) Accounting Technician examination scheme(ii) Professional examination scheme

These examinations are conducted semi-annually during the months of May and November each year. There are also mid-session examinations which are held in February and August involving three subjects A5 Business Law, B4 Public Finance & Taxation I and C4 Public Finance & Taxation II.

The Accounting Technician examination scheme consists of two levels covering the following subjects:

3THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

ACCOUNTING TECHNICIAN LEVEL I

Code Subject Name

T01 Bookkeeping and AccountsT02 Elements of Business Mathematics and StatisticsT03 Introduction to Information and Communication TechnologyT04 Business Communication Skills

ACCOUNTING TECHNICIAN LEVEL II

T05 Principles of Accounting and AuditingT06 Principles of Cost Accounting and ProcurementT07 Elements of Commercial Knowledge and TaxationT08 Accounting for Public Sector and Cooperatives

The Professional Examination Scheme consists of three levels as follows

Code Subject Name

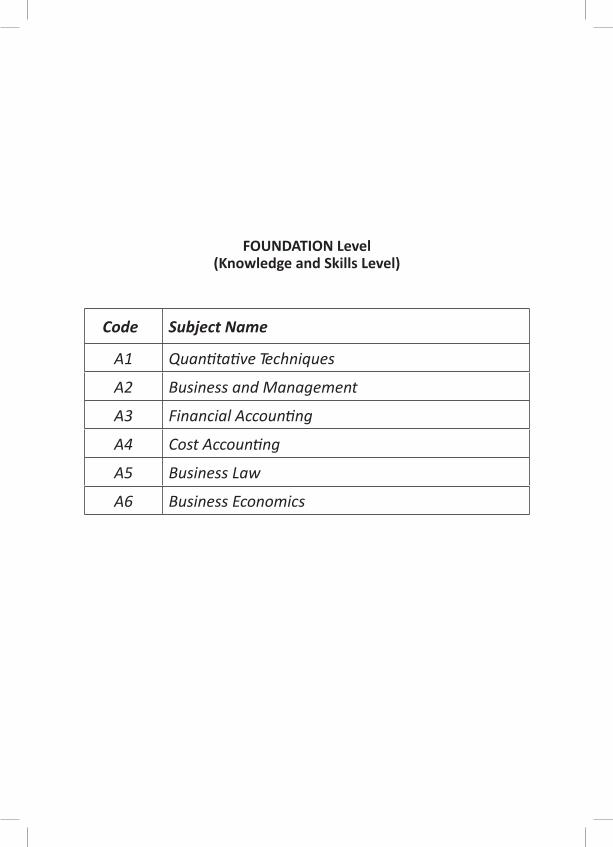

FOUNDATION Level (Knowledge and Skills Level)

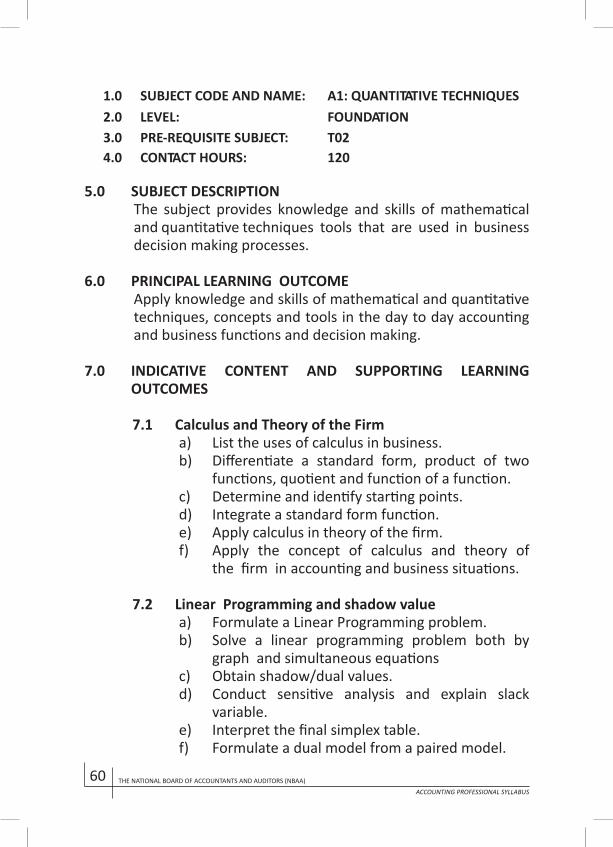

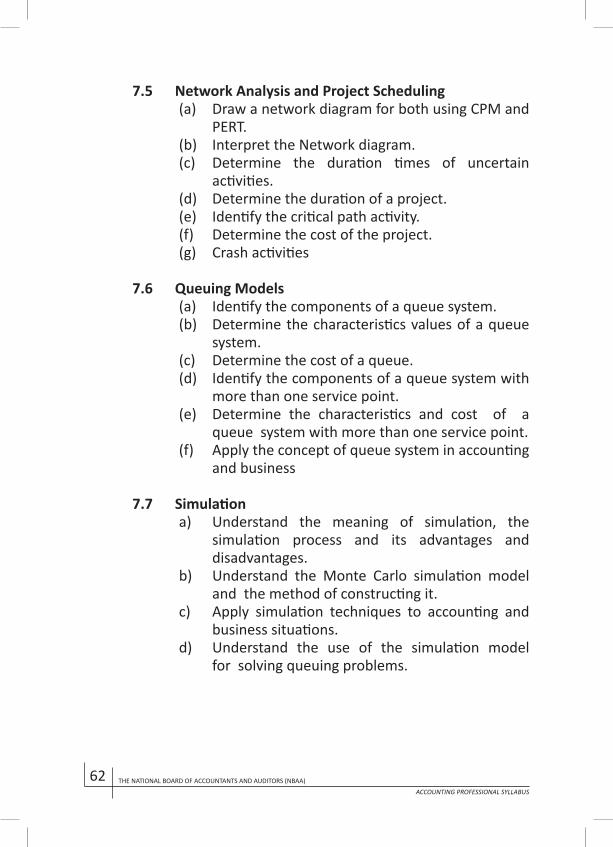

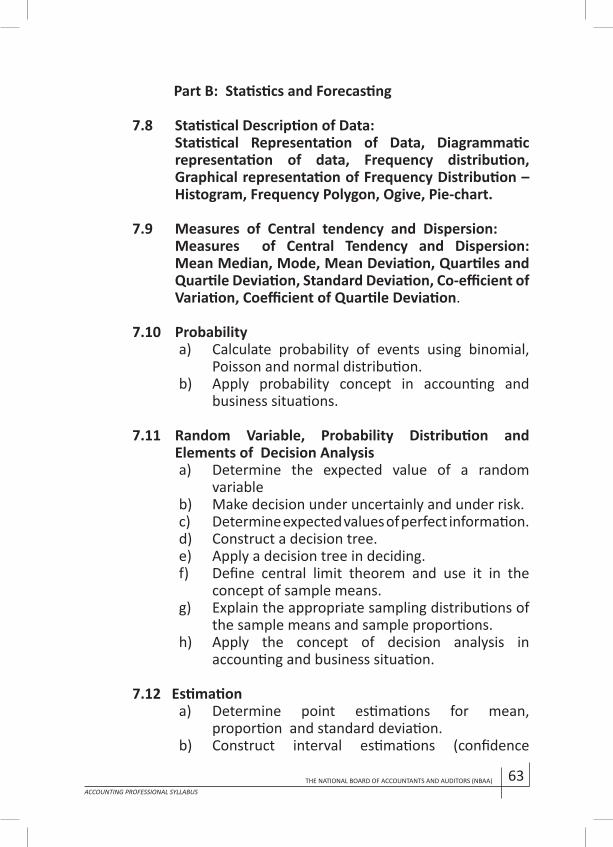

A1 Quantitative TechniquesA2 Business and ManagementA3 Financial AccountingA4 Cost AccountingA5 Business LawA6 Business Economics

4 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

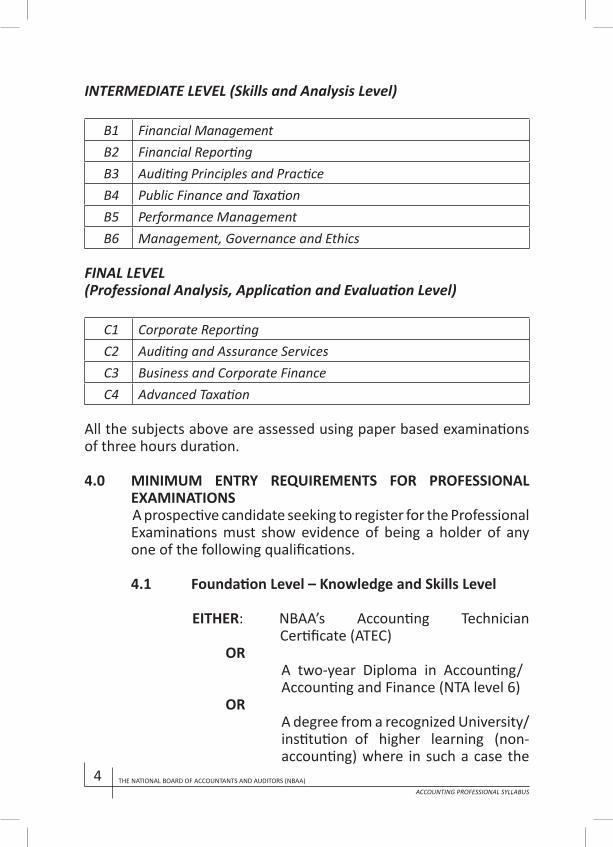

INTERMEDIATE LEVEL (Skills and Analysis Level)

B1 Financial ManagementB2 Financial Reporting B3 Auditing Principles and PracticeB4 Public Finance and Taxation B5 Performance ManagementB6 Management, Governance and Ethics

FINAL LEVEL(Professional Analysis, Application and Evaluation Level)

C1 Corporate ReportingC2 Auditing and Assurance ServicesC3 Business and Corporate FinanceC4 Advanced Taxation

All the subjects above are assessed using paper based examinations of three hours duration.

4.0 MINIMUM ENTRY REQUIREMENTS FOR PROFESSIONAL EXAMINATIONSA prospective candidate seeking to register for the Professional Examinations must show evidence of being a holder of any one of the following qualifications.

4.1 Foundation Level – Knowledge and Skills Level

EITHER: NBAA’s Accounting Technician Certificate (ATEC)

ORA two-year Diploma in Accounting/Accounting and Finance (NTA level 6)

ORA degree from a recognized University/institution of higher learning (non-accounting) where in such a case the

5THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

exemptions to be granted shall be considered on subject to subject basis depending on candidate’s specialty.

4.2 Intermediate Level - Skills and AnalysisEITHER NBAA’s Foundation Level Statement

of Success Letter as per the conversion scheme indicated from page 17

OR A bachelor degree majoring in Accounting/Accounting and Finance from a recognized University/Institution of Higher Learning.

4.3 Final Level – Professional Analysis, Application and Evaluation)NBAA Intermediate Level Statement of Success letter as per conversion scheme indicated from page 17

4.4 Qualifications Obtained Outside Tanzania:Holders of qualifications obtained outside the country who wish to pursue the accountancy profession in Tanzania are required to submit together with their application request, transcripts and detailed syllabus of the programme undertaken for consideration. In whatever case, the institution must be an accredited institution by an approved regulatory body in the country where it has been obtained.

The applicants shall further be required to get a confirmation of such recognition from either Tanzania Commission for Universities (TCU) or National Council for Technical Education (NACTE) as the case may be.

5.0 RECOGNITION OF QUALIFICATIONS FOR PURPOSES OF EXEMPTIONA qualification shall be eligible for an exemption only if that exemption is claimed within five years after being obtained. Any qualification obtained within or outside the country

6 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

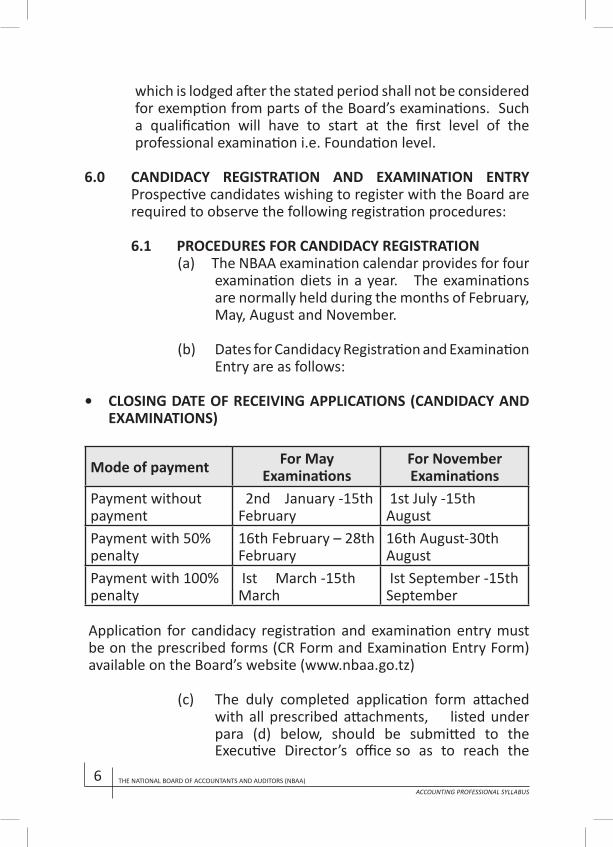

which is lodged after the stated period shall not be considered for exemption from parts of the Board’s examinations. Such a qualification will have to start at the first level of the professional examination i.e. Foundation level.

6.0 CANDIDACY REGISTRATION AND EXAMINATION ENTRY Prospective candidates wishing to register with the Board are required to observe the following registration procedures:

6.1 PROCEDURES FOR CANDIDACY REGISTRATION(a) The NBAA examination calendar provides for four

examination diets in a year. The examinations are normally held during the months of February, May, August and November.

(b) Dates for Candidacy Registration and Examination Entry are as follows:

• CLOSING DATE OF RECEIVING APPLICATIONS (CANDIDACY AND EXAMINATIONS)

Mode of payment For May Examinations

For November Examinations

Payment without payment

2nd January -15th February

1st July -15th August

Payment with 50% penalty

16th February – 28th February

16th August-30th August

Payment with 100% penalty

Ist March -15th March

Ist September -15th September

Application for candidacy registration and examination entry must be on the prescribed forms (CR Form and Examination Entry Form) available on the Board’s website (www.nbaa.go.tz)

(c) The duly completed application form attached with all prescribed attachments, listed under para (d) below, should be submitted to the Executive Director’s office so as to reach the

7THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

office on or before the last date January or July as the case may be. An application for candidacy registration received after the closing date shall be liable for penalty fee as indicated item 6.1 (b).

(d) The duly filled Candidacy Registration should be submitted with the following attachments:(i) Three recently taken identical passport

size photographs taken on white background (showing a full face with two ears of the applicant) and signed by the applicant at the back.

(ii) Photocopies of all certificates relevant to the application, authenticated by a Magistrate, Notary Public or by the Executive Director of the Board.

(iii) Applicable Registration and/or Exemption and Subscription Fee.

(iv) A duly filled Identity Request Form, the form which comes along with the candidacy registration form when downloading the form.

(e) As evidence of registration as a candidate, the Board shall issue an “Identity Card” to every registered candidate. The Identity Card bears the candidate’s registration number (CR. No.), the number which will be the permanent examination reference number for purposes of all communication with the NBAA.

The identify card shall be required for admission requirements to the examination hall. It is important, therefore, for a candidate to preserve it securely and produce it when needed during the examinations.

8 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

(d) No change of names by the prospective candidate shall allowed at the time of registration. Prospective candidates shall use the names appearing on the certificates which qualified the prospective candidate for admission

6.2 EXAMINATION ENTRY PROCEDURES(a) Applications to write the examinations must

be made on the prescribed form which is downloadable from the Board’s website. An applicant must, prior to application to examination entry, must be a registered candidate i.e. has already filled and submitted to the Board the Candidacy Registration form.

(b) Applications for May examinations are acceptable up to the 15th of February, and applications for November examinations are acceptable up to the 15th of August.

(c) A candidate shall be admitted to sit for the Board’s examinations at any one of its levels subject to the regulations applicable to that examination, provided that:(i) The candidate possesses the qualifications

prescribed as the minimum necessary to sit that particular level of examination.

(ii) The application is made on the prescribed form, the form which is downloadable from the Board’s website.

The duly filled form is returned on or before the prescribed closing date and is accompanied by appropriate examination entry fees.

Late applications are liable for penalty fee as indicated in the examination entry form

9THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

(iii) The candidate has met the minimum training requirements provided by approved Tuition Provider, and the examination entry form has been endorsed by the tuition provider certifying that the candidate is ready to sit for the examinations.

(d) The candidate must indicate in the examination entry form, an examination centre preferred to take the examinations. The Centres currently approved by the Board are indicated at the back of an entry form. Examinations are conducted in as many centres in the country as the Board may determine from time to time.

(e) Change of examination centre shall be allowed if lodged in writing at least one month before the date the examination is to commence. Late requests for change of center shall not be entertained.

(f) The candidate once accepted to take the examinations shall later receive an Examination Admission letter, containing the examination time table specifying the centre at which the candidate shall write the examination. Detailed instructions to examination candidates shall be enclosed and should be read carefully. The Admission Docket shall be posted to the candidate at least two weeks before the date of the examination. Candidates residing in Dar es Salaam shall be informed when to come and collect their letters of admission in person at the Board’s offices.

(g) An examination candidate will be allowed to enter in the examination room on production of an examination admission letter and NBAA Identity Card.

10 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

6.3 ORDER OF TAKING EXAMINATIONS AND EXAMINATIONS COMPLETION PERIODA registered candidate is required to observe thisrequirement while applying to sit for any level of theBoard’s examinations to take advantage of the optionsavailable.

Professional Examinations:

6.3.1 Foundation Level (Knowledge and Skills)A candidate is at liberty to choose the number of papers to attempt in this level and shall be allowed to retain a pass obtained in any subject attempted on scoring a pass grade.

A candidate applying to sit for the Foundation level examinations shall be required to pass all the papers in that level before being allowed to move to the next level. In some cases a candidate may be allowed to sit for both Foundation and Intermediate Levels provided that the subjects should not exceed five.

6.3.2 Duration of retaining passed papers:A candidate shall be given a maximum of three years to complete the passed papers in that level, failure of which the passes of the previously passed papers shall be withdrawn and a candidate shall have to re-sit all the papers in that level.

6.3.3 Maximum Time Limit to Complete the Foundation LevelA candidate shall be given a maximum of six years to complete the Foundation level before being automatically deregistered.

6.3.4 Intermediate Level (Skills and Analysis)A candidate is at liberty to choose the number of papers to attempt in this level and shall be allowed to retain a pass obtained in any subject attempted on scoring a pass grade.

11THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

A candidate applying to sit for the Intermediate level examinations shall be required to pass all the papers in that level before being allowed to move to the next level.

6.3.5 Duration of retaining passed papers:A candidate shall be given a maximum of three years to complete the passed papers in that level, failure of which the passes of the previously passed papers shall be withdrawn and a candidate shall have to re-sit all the papers in that level.

6.3.6 Maximum Time Limit to Complete the Intermediate LevelA candidate shall be given a maximum of six years to complete the Intermediate level before being automatically deregistered.

6.3.7 Final Level (Professional Analysis, Application and Evaluation)A candidate applying to sit for the Final level examinations shall be required to pass all the papers in that level to qualify as a CPA (T).

A candidate is at liberty to choose the number of papers to attempt in this level and shall be allowed to retain a pass obtained in any subject attempted on scoring a pass grade.

6.3.8 Duration of retaining passed papers:A candidate shall be given a maximum of three years to complete the papers in that level, failure of which the passes of the previously passed papers shall be withdrawn and a candidate shall have to re-sit all the papers in that level.

6.3.9 Maximum Time Limit to Complete the Final LevelA candidate shall be given a maximum of six years to complete the Final level before being automatically deregistered.

12 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

6.4 EXAMINATION POSTPONEMENT

6.4.1 Postponement within Acceptable datesA candidate wishing to withdraw from an examination, may do so in writing and is required to lodge the application to reach the Board on or before 15th February – for the May examinations and 15th August for the November examination. In such cases, full fee shall be carried forward to the immediate next examination session. A candidate shall, however, be required to fill a fresh examination entry form and submit it before the normal closing date of receiving the application to examination entry.

6.4.2 Postponement after the acceptable dates Application to postpone the examinations received after the acceptable dates i.e. after 15th February for May examinations and 15th August shall not be entertained. In such situations, a candidate shall be required to pay afresh all the applicable fees.

6.4.3 Postponement due to Ill-health (medically unfit)6.4.3.1 A candidate falling sick during the

examination week may lodge an application to postpone from an examination in writing. The application should be supported by a valid medical report from the registered practitioner to substantiate the claim.

6.4.3.2 Treatment sheets, prescriptions, sick sheets for purposes of validating a postponement claim shall not be considered for this purpose.

6.4.3.3 A candidate whose application for postponement has been accepted by the Board, shall be required to fill a fresh examination entry form applying for the examination the next coming session and

13THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

lodge it on or before the closing date of receiving the applications.

Half of the fees paid may be carried forward to the next examination session upon application.

6.5 REQUESTS FOR EXEMPTION(a) Applicants seeking exemptions in parts of the

Board’s examinations shall indicate such requests in the Candidacy Registration and Exemption form by filling an appropriate section of the form.

(b) Applications for exemptions should to be finalized before one sits for the subject(s) in an examination level in which exemption is sought and the application for exemption should be lodged at least two months before the closing date of the examination session to allow sufficient time for the application to be verified and assessed.

(c) An applicant shall be required to submit detailed syllabus and transcripts for the programme(s) undertaken showing the subject content details for the subject(s) in which exemption is sought for assessment.

In cases where the institutional program has already been assessed by the Board and exemption to the program granted (this applies to the accounting programmes offered by the institutions of higher learning within the country) then the syllabus need not be attached.

(d) An application for exemption shall not be considered if an applicant has already attempted any subject in that level.

(e) The Board shall consider an applicant’s request for exemption upon being satisfied that the

14 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

coverage of the subject(s) being requested for exemption adequately covers at least 80% of the NBAA syllabus.

(f) In all instances, it is important to show proof that the University or institution awarding that qualification is an accredited institution. Such a proof can be obtained from Tanzania Commission for Universities (TCU) or National Council for Technical Education (NACTE) as the case may be.

(g) The application for exemption shall have to be finalized before attempting an examination level for which exemption is sought.

(h) The exemption sought by an applicant shall be considered on a subject to subject basis upon receipt of adequate evidence of the content of the subjects in which exemption is sought.

(i) No exemption shall be granted at the Intermediate (Skills and Analysis Level) and at the Final Levels (Professional Analysis, Application and Evaluation Level) of the Board’s examinations.

(j) NBAA’s candidates transferring from the phased out examination scheme to the new examination scheme shall enjoy exemptions on the previously passed papers as shall be spelt out in the conversion scheme.

7.0 FEES An applicant wishing to register and sit for the Board’s

examinations shall be required to pay appropriate fees upon submission of the candidacy registration and/or examination entry form.

15THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

7.1 Major Types of FeesThere are four major types of fees payable by theapplicant to the Board:

(i) The first type of fee is a Candidacy Registration Fee which is payable upon submission of a duly completed Candidacy Registration Form. As evidence of registration, a student shall be given a Candidacy Registration Number (CR. No.) and an identity card bearing that number.

(ii) The second type of fee is a Student’s Annual Subscription Fee (SASF) which is payable, by those applicants who are registering with the Board for the first time, upon registration, and thereafter every January of each year. For those who have already registered themselves as candidates, the fee is payable every year in the month of January. This fee shall to be paid annually by every candidate as long as he/she is registered as a candidate with the Board and wishes to remain in the register of candidates. The fee ceases to be payable when one completes the CPA programme in full or ceases to be registered as a candidate with the Board.

(iii) The third type of fee is an Exemption Fee. This fee shall be payable by those applicants

who by virtue of their prior learning, seek exemptions on parts of the Board’s examinations. This fee shall be submitted along with the application for candidacy registration or once the amount payable has been determined.

(iv) The fourth type of fee is the Examination Fee. This fee shall be payable upon submission of

duly filled Examination Entry Form applying for an examination in an examination level.

16 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

7.2 Other types of fees that may be payable depending on the candidate’s status may include:(i) Penalty Fee A candidate who submits an application for

candidacy registration and/or examination entry after the closing date of receiving such applications shall be liable for a penalty fee charge which shall be paid along with other applicable fees.

(ii) Transcript fee Transcript fee shall be charged to a candidate

who lodges a request for preparation of transcript. A candidate who applies for a transcript shall also be required to submit two colored identical pass port size photographs.

(iii) Loss/renewal of ID fee A candidate who has lost his/her identity or

wants to renew the ID card upon expiry shall be charged such a fee. The candidate shall be required to submit two colored identical pass port size photographs and must fill an ID request form.

(iv) Search fee A candidate who requests for an information

which requires for searching of such information shall be required to pay for search fee. Such information may include previous performance records, receipts for payments done to the Board etc.

(v) Duplicate certificate fee A candidate who request for a copy of his/her

certificate shall be required to pay the required fee and submit a police report on loss of such document and copy of public announcement notification.

17THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

(vi) Appeal fee and late lodgment of appeal fee A candidate who wishes to appeal against

examination results or any penalty imposed shall be required to pay for the service accompanied with a lodgment of appeal form. Similarly, a candidate who lodges an appeal after the stipulated period shall be charged late lodgment of appeal fee.

(vii) Application processing fee Candidate who submits an application for

candidacy/examination shall be required to pay fee for the respective form

The rates for the above fees shall be determined by the Governing Board from time to time.

7.3 Mode of Payment of the fees:Payments of fees/charges shall be made throughNBAA Account as shall be determined by the Boardand indicated in the relevant form(s).

The original-pay-in slip shall have to be submitted to the Board for receipting. The slip has to be attached together with the relevant form(s) supporting that payment.

8.0 TRAINING OPPORTUNITIESAlthough the Board does not directly involve itself in training of candidates preparing to sit for its examinations, it collaborates with training institutions both public and private to ensure that quality training is offered to candidates preparing for theexaminations.

Training opportunities is available on either part-time or full time basis as detailed hereunder:

18 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

8.1 Part-time Courses:Candidates aspiring to sit for the Board’s examinationsmust undertake rigorous training offered by the registered tuition providers before sitting for the examinations. The tuition providers conduct training in different modes depending on the varied choices ofthe learners. The training can be either done during the evening and/or on weekends or on day time where candidates in employment may request for full day release from their employers

The part-time courses have proved to be useful as they provide platforms to exchange knowledge, ask questions and solve problems in group work.

8.2 Full time Courses:Full-time courses provide structured training schemesresulting into award of certificates, diplomas/higher diplomas or degrees on successful completion of the programme. The institutions which run such programmes follow an approved syllabi which is recognized by the Board and which may result into exemptions on parts of the Board’s examinations.

All in all upon completion of such programmes aspiring candidates must seek registration with the Board as candidates and attend review classes offered by the registered tuition providers before sitting for the examinations.

8.3 Study Aids:The Board in an endeavour to assist candidates preparing for its examination provides the following:

8.3.1 A specialized reference library:The Board maintained a specialized library which is stocked with relevant reading materials. The library is at the Mhasibu House Complex. All

19THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

registered candidates who are up-to-date with their subscriptions are allowed to use the library throughout the year without additional cost. The learning materials stocked at the library provide additional readings to candidates over and above what is in the specialized learning materials developed specifically for each subject areas examined by the Board.

8.3.2 Learning Materials:The Board has developed specialized learning materials for each subject area which are designed in a manner that candidates can easily grasp and acquire the appropriate knowledge in the area to be examined. The readily available end of chapter questions also help the candidate to build a solid foundation in answering examination questions.

8.3.3 Other facilities and learning resources provided by the Board include:a. Questions and Suggested Solutions of previous

examinationsb. Detailed Examiners’ and Performance Reportc. The Accountant Magazine d. A bookshop which sells most of the required

reading materials

9.0 DECLARATION OF RESULTSResults of the examination shall be communicated to every candidate as soon as possible, once the results have been approved and declared by the Governing Board.

Candidates shall be informed of their examination results through individual letters dispatched to each candidate but the general results shall be displayed on the NBAA Public Notice Board and on the website.

20 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

The result letters to each candidate shall show the performance in each paper by using the following codes:

A = Distinction = 80 – 100%B = Credit = 60 – 79%C = Pass = 40 – 59%F = Fail = 0 – 39%

X = Did not attempt (Absent)E = ExemptedQ = Disqualified

Candidates shall not be informed of the numerical grades scored in any paper.

10.0 Minimum Pass Mark:The Board shall determine the minimum pass mark to itsexaminations. The current pass mark for the Professionalexaminations is be 40%.

11.0 NBAA AWARDSThe Certified Public Accountant (CPA) CertificateA candidate who has successfully completed the Final level examinations shall be awarded a Certificate of Completion of the Certified Public Accountant [CPA(T)].

A candidate who has successfully completed a module in a stage, shall be issued with a statement of certificate for that module.

12.0 TRANSITIONAL ARRANGEMENTS

12.1 Candidates transferring from phased out syllabus to the new syllabusThe Board has in place a system of accommodating candidates transferring from old/phase out syllabus to the new syllabus. A Conversion Scheme has been prepared to take account of candidates who have

21THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

completed a level/module or those who have been referred in one or two subjects in the phased out syllabus (May 2008 – May 2014 syllabus) transferring to the new syllabus.

The following categories of candidates’ examination status have been considered in the Conversion Scheme

12.1.1 Candidates who passed a level/module Candidates who had passed a level/module, now transferring to the new syllabus shall be required to sit for the new subjects that have not been covered in the phased out syllabus.

12.1.2 Candidates with Referral Status: Candidates who had referral status,

now transferring to new syllabus shall be considered on paper to paper basis for all the papers that had not been covered under the new syllabus.

The candidates, however shall be required to observe the progression rule.

12.1.3 Candidates whose referral status was revoked/ withdrawn under the phased out examination Candidate with that status now transferring to the new syllabus shall be considered on all the papers that had been revoked plus the all other papers that had not been covered under the new syllabus.

12.1.4 Candidates who had fail status Candidates who had failed a level/module

now transferring to the new syllabus, shall be considered on the basis of current examination status he/she holds.

22 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

12.2 Institutional Qualifications considered for exemption from parts of the Board’s examinationsIn recognition of prior learning, the Board accredits institutional programmes offered by the accountancy training institutions in the country and grants exemption to those institutions which meet the minimum exemption requirements as follows:

12.2.1 Three years’ degree in Accounting specialty/NTA level 8/Advanced Diploma in Accounting Graduates of Bachelor of Accounting/ Bachelor of Accounting and Finance/ Bachelor of Business Administration – Accounting Option or NTA Level 8 accounting program from recognized institutions that had been accredited by the Board shall start at the Intermediate Level (Skills and Analysis Level)

12.2.2 Two year Diploma in Accounting/NTA level 6 Accounting Programs

Holders of Diploma in Accounting/Diploma in Business Administration – Accounting option/NTA Level 6 – Accounting programs from the recognized institutions that had been accredited by the Board shall start at Foundation Level (Knowledge and Skills Level)

12.2.3 Holders of Certificate in Accounting/NTA level 4 with accounting specialty

Holders of Certificate in Accounting/NTA level 4 specializing in Accounting from recognized institutions that had been accredited by the Board shall start at ATEC II examinations.

23THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

12.2.4 Holders of Non Accounting Qualifications from accredited institutions

12.2.4.1 Non-Accounting Degrees Holders of non-accounting degree qualifications from the accredited institutions shall be considered for exemption on subject to subject basis depending of the area of specialty of the qualification obtained; for example a holder of a degree in Business law from an accredited institution shall be considered for exemption in the Foundation Level on that paper only, while a holder of degree in Statistics shall be considered for exemption on that paper at the Foundation level.

No exemption shall be considered at the Intermediate or Final Level of the Board’s examinations.

12.2.4.2 Holders of non-accounting diplomas/certificates Holders of non-accounting diplomas/certificates shall be considered for exemption on the area of specialty at the ATEC II/I level.

12.2.4.3 Holders of Postgraduate Qualifications Holders of post graduate qualifications

shall not be considered for exemption apart from the undergraduate qualification obtained which shall be considered for exemption on area of specialty.

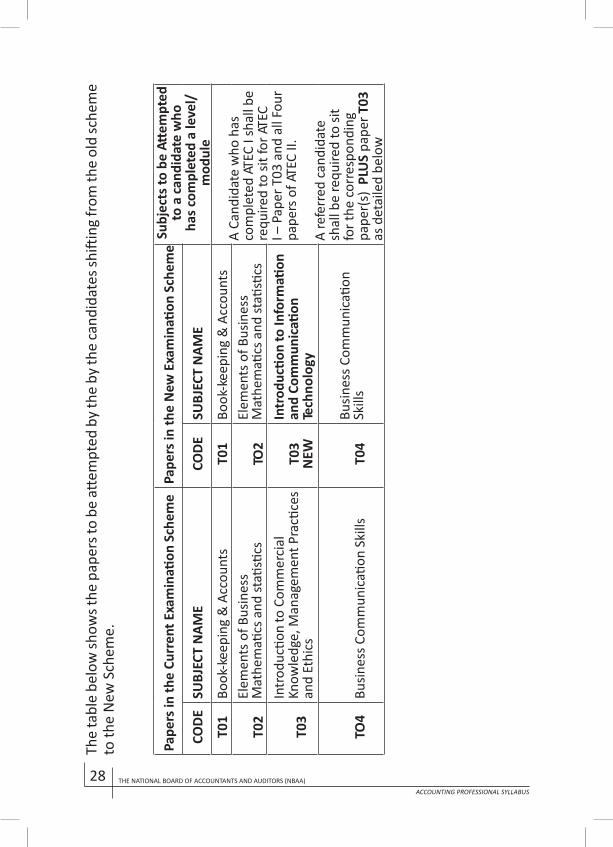

The table below sets forth the conversion scheme to be applied in determining new entry point to candidates who sat under the current examination scheme and syllabus.

24 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

13. Conversion Scheme:The conversion scheme shows how candidates under the existing syllabus will be transferred to the new examinationscheme and syllabus.The conversion scheme aims at ensuring that candidates under the current examination scheme are fairly placed in the new syllabus by considering the papers that have already been passed so that they can get an exemption (a credit) on them.Such consideration has only been made to those candidates who have either gained a pass in a level/module or have been referred in one or two paper(s) as the case may be.Candidates who have not earned a referral status or passed i.e. failed candidates in a level/module will have to sit for the corresponding papers under the new examination scheme.

13.1 Accounting Technician Examinations

13.1.1. Accounting Technician Level ICandidates who have successful completed ATEC I of the existing syllabus shall be required to sit for T03: Introduction to Information and Communication Technology in ATEC I. This is a new subject introduced in this level.

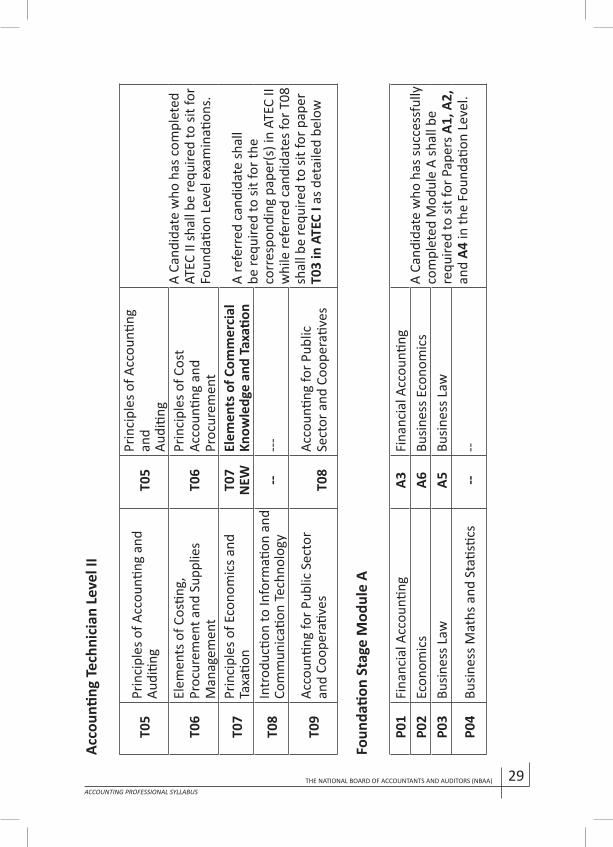

13.1.2 Accounting Technician Level IICandidates who have successful completed ATEC II shall proceed to Foundation Level examinations.

13.1.3 Referred Candidates in ATEC I or ATEC IICandidates who have been referred in one or two papers in the Accounting Technician Level I or Level II of the existing syllabus shall be required to sit for the corresponding/new papers in either level as detailed in the Conversion Scheme Table below.

25THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

13.2 Professional Level Examinations

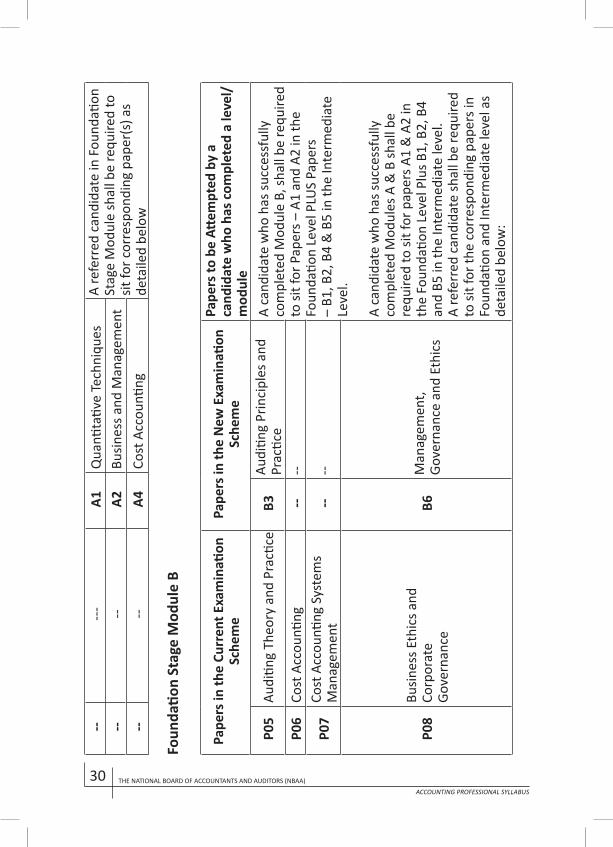

13.2.1 Foundation Stage Module ACandidates who have successful completed Module A of the existing syllabus shall be required to sit for papers:A1 Quantitative Techniques,A2 Business and Management andA4 Cost Accounting in the Foundation Level

13.2.2 Foundation Stage Module BCandidates who have successful completed Module B of the existing syllabus shall be required to sit for papers:A1 Quantitative Techniques andA2 Business and Management in the

Foundation level examinations.

13.2.3 Referred Candidates in Foundation StageCandidates who have been referred in one or two papers in the Foundation Stage examinations of the existing syllabus shall be required to sit for the corresponding/new papers in either level as detailed in the Conversion Scheme Table below.

13.2.4 Intermediate Stage Module CCandidates who have successful completed Intermediate Stage -Module C of the existing syllabus shall be required to sit for paper(s):A2 Business and Management in the

Foundation Level andB1 Financial Management, B4 Public Finance & Taxation I andB5 Performance Management in the

Intermediate Level.

26 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

13.2.5 Intermediate Stage Module D Examinations:Candidates who have successful completed the Intermediate Stage Module D of the existing syllabus shall be required to sit for papers:B4 Public Finance & Taxation I and B5 Performance Management papers of the

Intermediate Level.

13.2.6 Referred Candidates in the Intermediate Stage examinations Candidates who have been referred in one paper in the Intermediate Stage examinations of the existing syllabus shall be required to sit for the corresponding/new paper in either level as detailed in the Conversion Scheme Table below.

13.2.7 Final Stage Module E examinationsCandidates who have successful completed Final Level - Module E examinations shall be required to sit for paper(s):B5 Performance Management in the

Intermediate level andC1 Corporate Reporting and C2 Audit and Assurance in the Final level.

13.2.8 Final Stage Module E & FCandidates who have successfully completed Modules E and F of the existing syllabus shall be eligible for the Certificate of Completion of the CPA (T) programme.

13.2.9 Candidates who failed Module ECandidates who failed Module E from 2010 shall be required to sit for five subjects in order to qualify for CPA(T) as follows: B5 Performance Management and all four subject in the Final Level.

27THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

13.2.10 Referred Candidates in the Final Stage Examinations Candidates who have been referred in one paper in the Final Stage examinations of the existing syllabus shall be required to sit for the corresponding/new paper in either level as detailed in the Conversion Scheme Table below

13.3 Transitional Arrangements:During the transition period, candidates shall be allowed to sit for papers across the levels as long as:(i) the paper(s) in the lower level are also taken at

the same sitting(ii) the maximum papers taken does not exceed five(iii) the progression rule allows the candidate to sit

for those papers.

EXAMINATION STRUCTURE AND CONVERSION SCHEMETo assist candidates who transfer from the old examination scheme to the revised examination scheme, a conversion scheme has been worked out (simplified) to show where these candidates fit in the new scheme.

28 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

The

tabl

e be

low

show

s the

pap

ers t

o be

atte

mpt

ed b

y th

e by

the

cand

idat

es sh

iftin

g fr

om th

e ol

d sc

hem

e to

the

New

Sch

eme.

Pape

rs in

the

Curr

ent E

xam

inati

on S

chem

ePa

pers

in th

e N

ew E

xam

inati

on S

chem

eSu

bjec

ts to

be

Attem

pted

to

a c

andi

date

who

ha

s com

plet

ed a

leve

l/m

odul

eCO

DESU

BJEC

T N

AME

CODE

SUBJ

ECT

NAM

E

T01

Book

-kee

ping

& A

ccou

nts

T01

Book

-kee

ping

& A

ccou

nts

A Ca

ndid

ate

who

has

co

mpl

eted

ATE

C I s

hall

be

requ

ired

to si

t for

ATE

C I –

Pap

er T

03 a

nd a

ll Fo

ur

pape

rs o

f ATE

C II.

A re

ferr

ed ca

ndid

ate

shal

l be

requ

ired

to si

t fo

r the

corr

espo

ndin

g pa

per(

s) P

LUS

pape

r T03

as

det

aile

d be

low

T02

Elem

ents

of B

usin

ess

Mat

hem

atics

and

stati

stics

TO2

Elem

ents

of B

usin

ess

Mat

hem

atics

and

stati

stics

T03

Intr

oduc

tion

to C

omm

erci

al

Know

ledg

e, M

anag

emen

t Pra

ctice

s an

d Et

hics

T03

NEW

Intr

oduc

tion

to In

form

ation

an

d Co

mm

unic

ation

Te

chno

logy

TO4

Busin

ess C

omm

unic

ation

Ski

llsT0

4Bu

sines

s Com

mun

icati

onSk

ills

29THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Acco

untin

g Te

chni

cian

Lev

el II

T05

Prin

cipl

es o

f Acc

ounti

ng a

ndAu

ditin

gT0

5Pr

inci

ples

of A

ccou

nting

an

dAu

ditin

gA

Cand

idat

e w

ho h

as c

ompl

eted

AT

EC II

shal

l be

requ

ired

to si

t for

Fo

unda

tion

Leve

l exa

min

ation

s.

A re

ferr

ed c

andi

date

shal

l be

requ

ired

to si

t for

the

corr

espo

ndin

g pa

per(

s) in

ATE

C II

whi

le re

ferr

ed c

andi

date

s for

T08

sh

all b

e re

quire

d to

sit f

or p

aper

T0

3 in

ATE

C I a

s det

aile

d be

low

T06

Elem

ents

of C

ostin

g,

Proc

urem

ent a

nd S

uppl

ies

Man

agem

ent

T06

Prin

cipl

es o

f Cos

t Ac

coun

ting

and

Proc

urem

ent

T07

Prin

cipl

es o

f Eco

nom

ics a

ndTa

xatio

nT0

7N

EWEl

emen

ts o

f Com

mer

cial

Know

ledg

e an

d Ta

xatio

n

T08

Intr

oduc

tion

to In

form

ation

and

Com

mun

icati

on Te

chno

logy

-----

T09

Acco

untin

g fo

r Pub

lic S

ecto

r an

d Co

oper

ative

sT0

8Ac

coun

ting

for P

ublic

Se

ctor

and

Coo

pera

tives

Foun

datio

n St

age

Mod

ule

A

P01

Fina

ncia

l Acc

ounti

ngA3

Fina

ncia

l Acc

ounti

ngA

Cand

idat

e w

ho h

as su

cces

sful

ly

com

plet

ed M

odul

e A

shal

l be

requ

ired

to si

t for

Pap

ers A

1, A

2,

and

A4 in

the

Foun

datio

n Le

vel.

P02

Econ

omic

sA6

Busin

ess E

cono

mic

sP0

3Bu

sines

s Law

A5Bu

sines

s Law

P04

Busin

ess M

aths

and

Sta

tistic

s--

--

30 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

-----

A1Q

uanti

tativ

e Te

chni

ques

A re

ferr

ed c

andi

date

in F

ound

ation

St

age

Mod

ule

shal

l be

requ

ired

to

sit fo

r cor

resp

ondi

ng p

aper

(s) a

s de

taile

d be

low

----

A2Bu

sines

s and

Man

agem

ent

----

A4Co

st A

ccou

nting

Foun

datio

n St

age

Mod

ule

B

Pape

rs in

the

Curr

ent E

xam

inati

onSc

hem

ePa

pers

in th

e N

ew E

xam

inati

onSc

hem

e

Pape

rs to

be

Attem

pted

by

a ca

ndid

ate

who

has

com

plet

ed a

leve

l/m

odul

e

P05

Audi

ting

Theo

ry a

nd P

racti

ceB3

Audi

ting

Prin

cipl

es a

ndPr

actic

eA

cand

idat

e w

ho h

as su

cces

sful

ly

com

plet

ed M

odul

e B,

shal

l be

requ

ired

to si

t for

Pap

ers –

A1

and

A2 in

the

Foun

datio

n Le

vel P

LUS

Pape

rs–

B1, B

2, B

4 &

B5

in th

e In

term

edia

teLe

vel.

A ca

ndid

ate

who

has

succ

essf

ully

co

mpl

eted

Mod

ules

A &

B sh

all b

e re

quire

d to

sit f

or p

aper

s A1

& A

2 in

th

e Fo

unda

tion

Leve

l Plu

s B1,

B2,

B4

and

B5 in

the

Inte

rmed

iate

leve

l.A

refe

rred

can

dida

te sh

all b

e re

quire

d to

sit f

or th

e co

rres

pond

ing

pape

rs in

Fo

unda

tion

and

Inte

rmed

iate

leve

l as

deta

iled

belo

w:

P06

Cost

Acc

ounti

ng--

--

P07

Cost

Acc

ounti

ng S

yste

ms

Man

agem

ent

----

P08

Busin

ess E

thic

s and

Co

rpor

ate

Gove

rnan

ceB6

Man

agem

ent,

Gove

rnan

ce a

nd E

thic

s

31THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Inte

rmed

iate

Sta

ge M

odul

e C

P09

Fina

ncia

l Rep

ortin

g I

B2Fi

nanc

ial R

epor

ting

A ca

ndid

ate,

who

has

succ

essf

ully

co

mpl

eted

Mod

ule

C, sh

all b

e re

quire

d to

sit f

or P

aper

A2

in th

e Fo

unda

tion

Leve

l Plu

s pap

ers B

1,

B4 a

nd B

5 in

the

Inte

rmed

iate

Le

vel.

A re

ferr

ed c

andi

date

shal

l be

requ

ired

to si

t for

the

corr

espo

ndin

g pa

pers

as s

how

n be

low

.

P.10

Rese

arch

, Con

sulta

ncy

and

Repo

rting

----

P.11

Qua

ntita

tive

Tech

niqu

es fo

rDe

cisio

n M

akin

gA1

Qua

ntita

tive

Tech

niqu

es(F

ound

ation

Lev

el)

32 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Inte

rmed

iate

Sta

ge M

odul

e D

P12

Man

agem

ent P

rinci

ples

and

Prac

tices

A2Bu

sines

s and

Man

agem

ent

(in F

ound

ation

Lev

el)

A ca

ndid

ate,

who

has

su

cces

sful

ly c

ompl

eted

Mod

ule

D, sh

all b

e re

quire

d to

sit f

or

Pape

rs B

4 &

B5.

A ca

ndid

ate

who

has

succ

essf

ully

co

mpl

eted

Mod

ules

C &

D sh

all

be re

quire

d to

sit f

or p

aper

s B4

and

B5 in

the

Inte

rmed

iate

Lev

el

Refe

rred

can

dida

tes s

hall

be

requ

ired

to si

t for

cor

resp

ondi

ng

pape

rs in

Fou

ndati

on a

nd

Inte

rmed

iate

leve

lsas

det

aile

d be

low

:

P13

Corp

orat

e Fi

nanc

eB1

Fina

ncia

l Man

agem

ent

P14

Entr

epre

neur

ship

----

-----

B4Pu

blic

Fin

ance

& T

axati

on

-----

B5Pe

rfor

man

ce M

anag

emen

t

33THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Fina

l Sta

ge M

odul

e E

Pape

rs in

the

Curr

ent E

xam

inati

onSc

hem

eCo

rres

pond

ing

Pape

rs in

the

New

Exam

inati

on S

chem

ePa

pers

to b

e Att

empt

ed b

y a

cand

idat

e w

ho h

as c

ompl

eted

a

leve

l/m

odul

eCO

DESU

BJEC

T N

AME

CODE

SUBJ

ECT

NAM

E

P15

Fina

ncia

l Rep

ortin

g II

C1Co

rpor

ate

Repo

rting

A ca

ndid

ate,

who

has

succ

essf

ully

co

mpl

eted

Mod

ule

E, sh

all b

e re

quire

d to

sit f

or P

aper

s – B

5 in

the

Inte

rmed

iate

Lev

el, C

1 an

d C2

in th

e Fi

nal L

evel

.

A re

ferr

ed c

andi

date

in M

odul

e E

shal

l be

requ

ired

to si

t for

cor

resp

ondi

ng

pape

rs A

s det

aile

d be

low

:

P16

Inte

rnati

onal

Fin

ance

C3Bu

sines

s and

Cor

pora

teFi

nanc

e

P17

Publ

ic F

inan

ce a

nd T

axati

onC4

Adva

nced

Tax

ation

Fina

l Sta

ge M

odul

e F

P18

Audi

ting

and

Assu

ranc

eSe

rvic

esC2

Audi

t and

Ass

uran

ceSe

rvic

esA

cand

idat

e w

ho h

as su

cces

sful

ly

com

plet

ed M

odul

e E

& F

shal

l be

elig

ible

for C

ertifi

cate

of C

ompl

etion

of

CPA

(T)

A re

ferr

ed c

andi

date

shal

l be

requ

ired

to si

t for

the

corr

espo

ndin

gpa

per(

s) a

s det

aile

d be

low

:

P19

Man

agem

ent A

ccou

nting

&

Con

trol

B5Pe

rfor

man

ce M

anag

emen

t–

in th

e In

term

edia

te L

evel

P20

Cont

empo

rary

Issu

es in

Acco

untin

gC1

Corp

orat

e Re

porti

ng

34 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

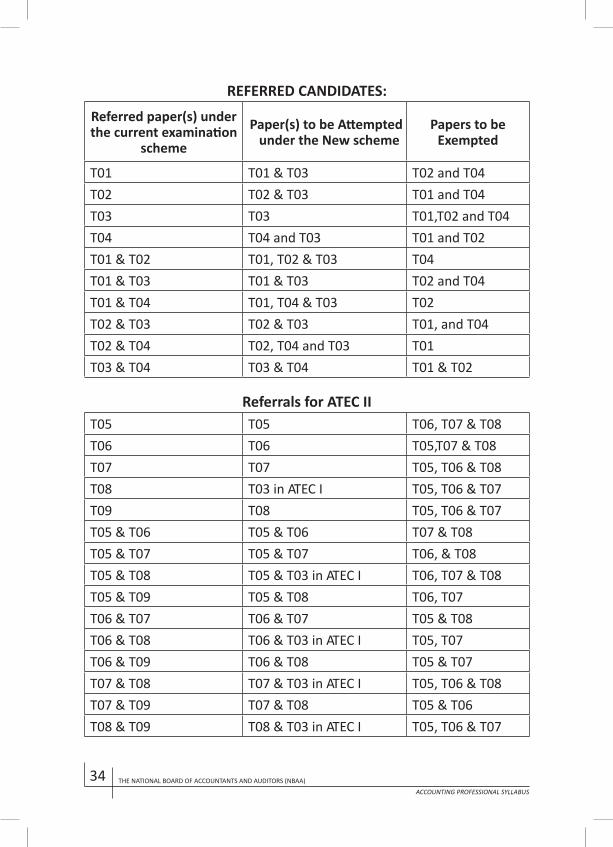

REFERRED CANDIDATES:Referred paper(s) under the current examination

scheme

Paper(s) to be Attempted under the New scheme

Papers to beExempted

T01 T01 & T03 T02 and T04T02 T02 & T03 T01 and T04T03 T03 T01,T02 and T04T04 T04 and T03 T01 and T02T01 & T02 T01, T02 & T03 T04T01 & T03 T01 & T03 T02 and T04T01 & T04 T01, T04 & T03 T02T02 & T03 T02 & T03 T01, and T04T02 & T04 T02, T04 and T03 T01T03 & T04 T03 & T04 T01 & T02

Referrals for ATEC IIT05 T05 T06, T07 & T08T06 T06 T05,T07 & T08T07 T07 T05, T06 & T08T08 T03 in ATEC I T05, T06 & T07T09 T08 T05, T06 & T07T05 & T06 T05 & T06 T07 & T08T05 & T07 T05 & T07 T06, & T08T05 & T08 T05 & T03 in ATEC I T06, T07 & T08T05 & T09 T05 & T08 T06, T07T06 & T07 T06 & T07 T05 & T08T06 & T08 T06 & T03 in ATEC I T05, T07T06 & T09 T06 & T08 T05 & T07T07 & T08 T07 & T03 in ATEC I T05, T06 & T08T07 & T09 T07 & T08 T05 & T06T08 & T09 T08 & T03 in ATEC I T05, T06 & T07

35THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

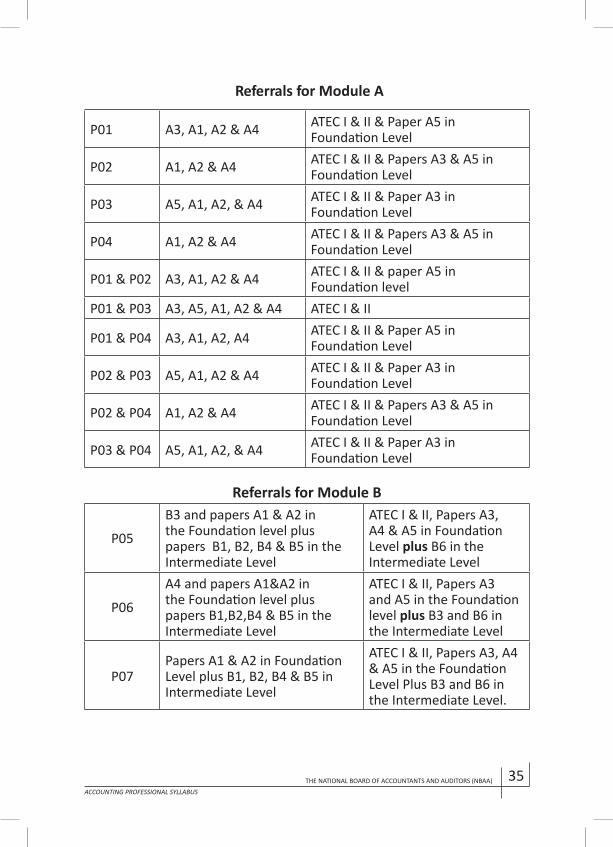

Referrals for Module A

P01 A3, A1, A2 & A4 ATEC I & II & Paper A5 inFoundation Level

P02 A1, A2 & A4 ATEC I & II & Papers A3 & A5 in Foundation Level

P03 A5, A1, A2, & A4 ATEC I & II & Paper A3 inFoundation Level

P04 A1, A2 & A4 ATEC I & II & Papers A3 & A5 in Foundation Level

P01 & P02 A3, A1, A2 & A4 ATEC I & II & paper A5 inFoundation level

P01 & P03 A3, A5, A1, A2 & A4 ATEC I & II

P01 & P04 A3, A1, A2, A4 ATEC I & II & Paper A5 inFoundation Level

P02 & P03 A5, A1, A2 & A4 ATEC I & II & Paper A3 inFoundation Level

P02 & P04 A1, A2 & A4 ATEC I & II & Papers A3 & A5 in Foundation Level

P03 & P04 A5, A1, A2, & A4 ATEC I & II & Paper A3 inFoundation Level

Referrals for Module B

P05

B3 and papers A1 & A2 in the Foundation level plus papers B1, B2, B4 & B5 in the Intermediate Level

ATEC I & II, Papers A3, A4 & A5 in Foundation Level plus B6 in the Intermediate Level

P06

A4 and papers A1&A2 in the Foundation level plus papers B1,B2,B4 & B5 in the Intermediate Level

ATEC I & II, Papers A3and A5 in the Foundationlevel plus B3 and B6 inthe Intermediate Level

P07Papers A1 & A2 in Foundation Level plus B1, B2, B4 & B5 in Intermediate Level

ATEC I & II, Papers A3, A4& A5 in the FoundationLevel Plus B3 and B6 inthe Intermediate Level.

36 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

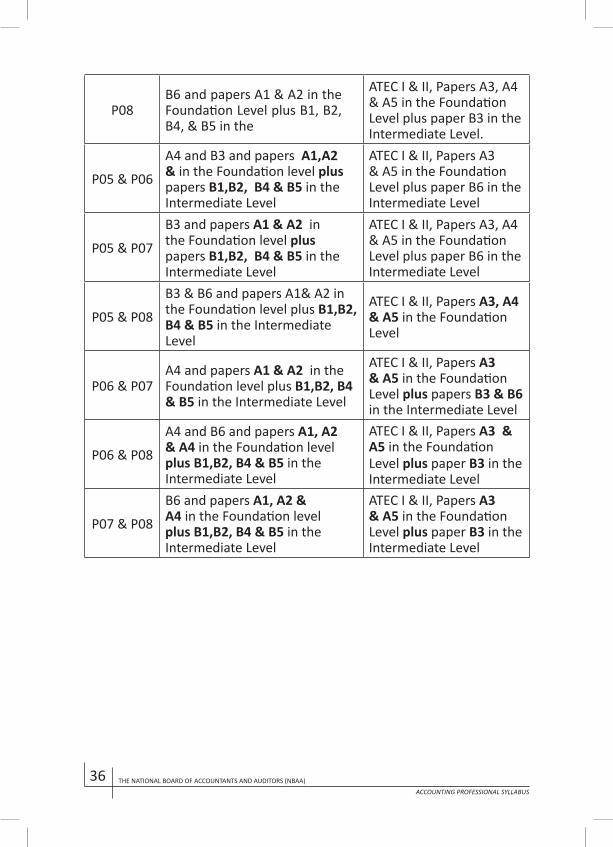

P08B6 and papers A1 & A2 in the Foundation Level plus B1, B2, B4, & B5 in the

ATEC I & II, Papers A3, A4& A5 in the FoundationLevel plus paper B3 in theIntermediate Level.

P05 & P06

A4 and B3 and papers A1,A2& in the Foundation level pluspapers B1,B2, B4 & B5 in theIntermediate Level

ATEC I & II, Papers A3& A5 in the FoundationLevel plus paper B6 in theIntermediate Level

P05 & P07

B3 and papers A1 & A2 in the Foundation level plus papers B1,B2, B4 & B5 in the Intermediate Level

ATEC I & II, Papers A3, A4& A5 in the FoundationLevel plus paper B6 in theIntermediate Level

P05 & P08

B3 & B6 and papers A1& A2 in the Foundation level plus B1,B2, B4 & B5 in the Intermediate Level

ATEC I & II, Papers A3, A4& A5 in the FoundationLevel

P06 & P07A4 and papers A1 & A2 in theFoundation level plus B1,B2, B4& B5 in the Intermediate Level

ATEC I & II, Papers A3& A5 in the FoundationLevel plus papers B3 & B6in the Intermediate Level

P06 & P08

A4 and B6 and papers A1, A2& A4 in the Foundation levelplus B1,B2, B4 & B5 in theIntermediate Level

ATEC I & II, Papers A3 & A5 in the FoundationLevel plus paper B3 in theIntermediate Level

P07 & P08

B6 and papers A1, A2 &A4 in the Foundation levelplus B1,B2, B4 & B5 in theIntermediate Level

ATEC I & II, Papers A3& A5 in the FoundationLevel plus paper B3 in theIntermediate Level

37THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

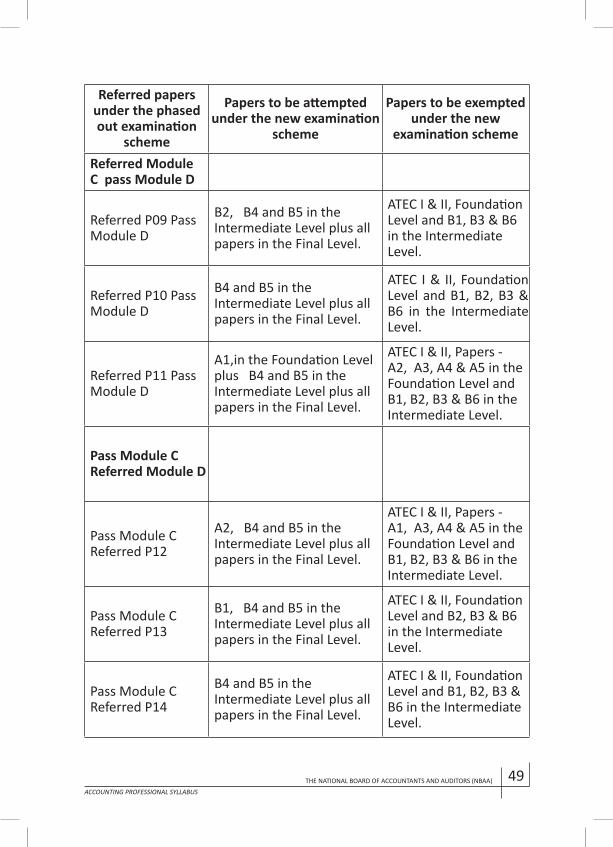

Referrals for Module C

P09Papers – A2 in the Foundation Level plus B1, B2, B4 & B5 in the Intermediate level

ATEC I & II, Papers – A1, A3, A4 & A5 in the Foundation level plus B3 and B6 in the Intermediate level

P10Papers – A2 in the Foundation level plus B1, B4 & B5 in the Intermediate level

ATEC I & II, Papers – A1, A3, A4 & A5 in the Foundation level plus B2, B3 and B6 in the Intermediate level.

P11Papers – A1 & A2 in the Foundation level plus B1, B4 & B5 in the Intermediate level

ATEC I & II, Papers – A3,A4 & A5 in the Foundationlevel plus B2, B3 and B6 inthe Intermediate level.

Referrals for Module D

P12Papers – A2 in Foundation Level plus B4 & B5 in the Intermediate Level

ATEC I & II, Papers – A1,A3, A4 & A5 in the Foundation Level plus B1, B2, B3 & B6 in the Intermediate Level

P13 Papers – B1, B4 & B5 in theIntermediate Level

ATEC I & II, Foundation Level plus B2, B3, & B6 in the Intermediate Level.

P14 Papers – B4 & B5 in theIntermediate Level

ATEC I & II, Foundation Level plus B1, B2, B3, & B6 in the Intermediate Level.

38 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referrals for Module EReferred Papers under the current Exam- ination Scheme

Paper(s) to be Attempted under the New Scheme

Papers to be Exemptedunder the New Scheme

P15C1 and papers – B5 in the Intermediate level plus C2 in the Final Level

ATEC I & II, Foundation Level, Intermediate Level Papers – B1, B2, B3, B4 & B6 plus Papers- C3 & C4 in the Final Level.

P16C3 and papers – B5 in the Intermediate level plus C1 & C2 in the Final Level

ATEC I & II, Foundation Level, Intermediate Level Papers – B1, B2, B3, B4 & B6 plus Paper – C4 in the Final Level.

P17C4 and papers – B5 in the Intermediate level plus C1, C2 & C4 in the Final Level

ATEC I & II, Foundation Level, Intermediate Level Papers – B1, B2, B3, B4 & B6 plus Papers – C3 in the Final Level.

Referrals in Module F

P18 Paper C2 in the Final Level

ATEC I & II, FoundationLevel, Intermediate Level& Papers – C1, C3 & C4 inthe Final Level.

P19 Papers – B5 in the Intermediate level

ATEC I & II, Foundation Level, Intermediate Level Papers – B1, B2, B3, B4 & B6 plus Papers – C1, C2, C3 & C4 in the Final Level.

P20 Paper C1 in the Final Level

ATEC I & II, FoundationLevel, Intermediate Level& Papers – C2, C3 & C4 inthe Final Level.

39THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

CONVERSION SCHEME TOCANDIDATES WITH INTERMODULE REFERRAL STATUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

Referred in Module A and Module B the following papers:

P01 & P05

A1,A2,A3, in Foundation level and B1, B2, B3,B4,and B5 in the Intermediate Level plus all papers in the Final Level

ATEC I & II, Papers - A4& A5 in the FoundationLevel and B6 in theIntermediate Level.

P01 & P06

A1, A2,A3 and A4 in theFoundation Level andB1, B2, B4, and B5 in theIntermediate Level plus allpapers in the Final Level

ATEC I & II, Papers - A5 in the Foundation Level and B3 & B6 in the Intermediate Level.

P01 & P07

A1, A2, A3 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level

ATEC I & II, Papers - A5 in the Foundation Level and B3 & B6 in the Intermediate Level.

P01 & P08

A1, A2 and A3 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A4& A5 in the FoundationLevel and B3 in theIntermediate Level.

P02 & P05

A1, and A2 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B6 in the Intermediate Level.

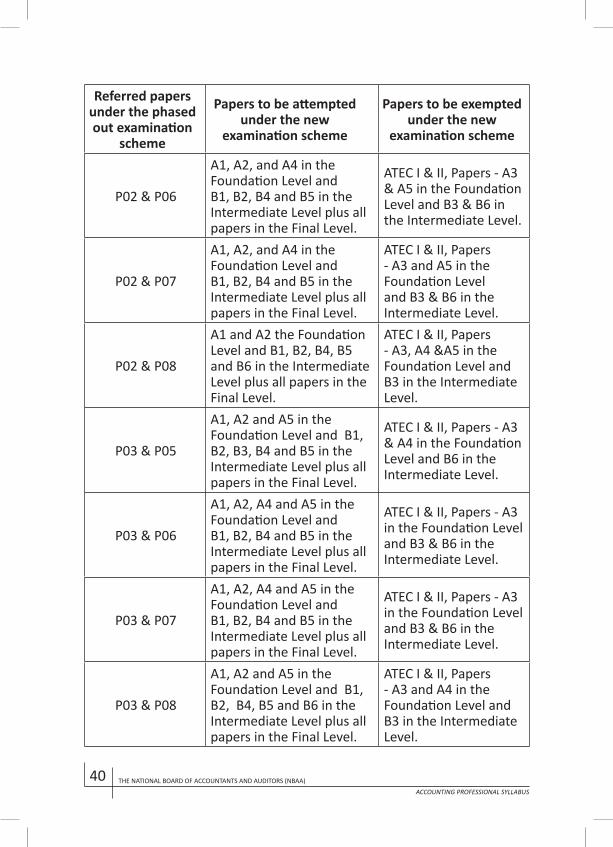

40 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

P02 & P06

A1, A2, and A4 in the Foundation Level and B1, B2, B4 and B5 in theIntermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

P02 & P07

A1, A2, and A4 in the Foundation Level and B1, B2, B4 and B5 in theIntermediate Level plus all papers in the Final Level.

ATEC I & II, Papers- A3 and A5 in theFoundation Leveland B3 & B6 in theIntermediate Level.

P02 & P08

A1 and A2 the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers- A3, A4 &A5 in theFoundation Level andB3 in the IntermediateLevel.

P03 & P05

A1, A2 and A5 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A4 in the FoundationLevel and B6 in theIntermediate Level.

P03 & P06

A1, A2, A4 and A5 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3 in the Foundation Level and B3 & B6 in the Intermediate Level.

P03 & P07

A1, A2, A4 and A5 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3 in the Foundation Level and B3 & B6 in the Intermediate Level.

P03 & P08

A1, A2 and A5 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers- A3 and A4 in theFoundation Level andB3 in the IntermediateLevel.

41THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

P04 & P05

A1 and A2 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B6 in the Intermediate Level.

P04 & P06

A1, A2 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

P04 & P07

A1, A2 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

P04 & P08

A1 and A2 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B3 in the Intermediate Level.

P01, P05 & P06

A1, A2, A3 and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A5 in the Foundation Level and B6 in the Intermediate Level.

P01, P05 & P07

A1, A2, A3 and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A5 in the Foundation Level and B6 in the Intermediate Level.

P01, P05 & P08

A1, A2 and A3 in the Foundation Level and B1, B2, B3, B4, B5 & B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A4& A5 in the FoundationLevel.

42 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

P01, P06 & P07

A1, A2, A3 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A5 in the Foundation Level and B3 & B6 in the Intermediate Level.

P01, P06 & P08

A1, A2, A3 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A5 in the Foundation Level and B3 in the Intermediate Level.

P01, P07 & P08

A1, A2, A3 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A5 in the Foundation Level and B3 in the Intermediate Level.

P02, P05 & P06

A1, A2 and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B6 in theIntermediate Level.

P02, P05 & P07

A1, A2, and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B6 in theIntermediate Level.

P02, P05 & P08

A1 and A2 in the Foundation Level and B1, B2, B3, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level.

43THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

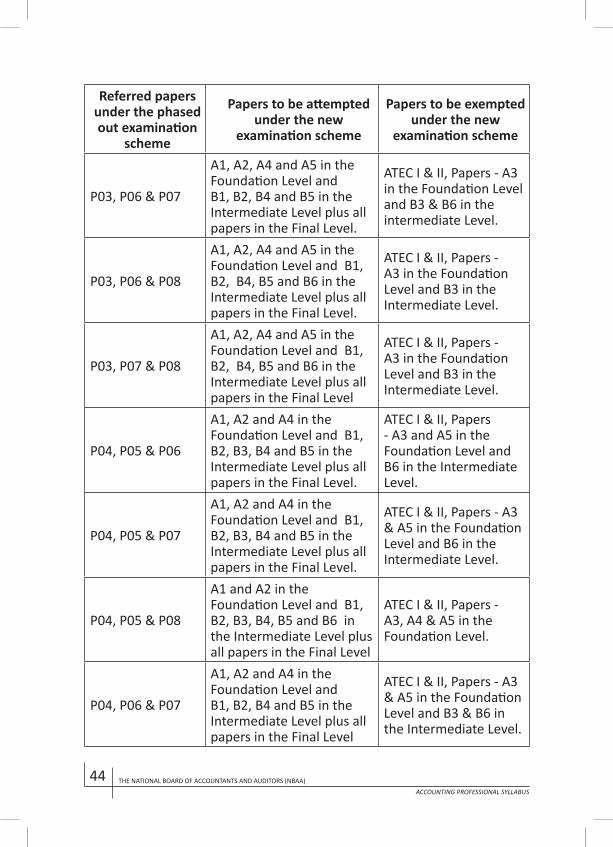

P02, P06 & P07

A1, A2 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

P02, P06 & P08

A1, A2 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 in theIntermediate Level.

P02, P07 & P08

A1, A2 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 in theIntermediate Level.

P03, P05 & P06

A1, A2, A4 and A5 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3 in the Foundation Level and B6 in the Intermediate Level.

P03, P05 & P07

A1, A2, A4 and A5 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3 in the Foundation Level and B6 in the Intermediate Level.

P03, P05 & P08

A1, A2 and A5 in the Foundation Level and B1, B2, B3, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A4 in the FoundationLevel.

44 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

P03, P06 & P07

A1, A2, A4 and A5 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3 in the Foundation Level and B3 & B6 in the intermediate Level.

P03, P06 & P08

A1, A2, A4 and A5 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3 in the Foundation Level and B3 in the Intermediate Level.

P03, P07 & P08

A1, A2, A4 and A5 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level

ATEC I & II, Papers - A3 in the Foundation Level and B3 in the Intermediate Level.

P04, P05 & P06

A1, A2 and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers- A3 and A5 in theFoundation Level andB6 in the IntermediateLevel.

P04, P05 & P07

A1, A2 and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B6 in theIntermediate Level.

P04, P05 & P08

A1 and A2 in the Foundation Level and B1, B2, B3, B4, B5 and B6 inthe Intermediate Level plus all papers in the Final Level

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level.

P04, P06 & P07

A1, A2 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

45THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

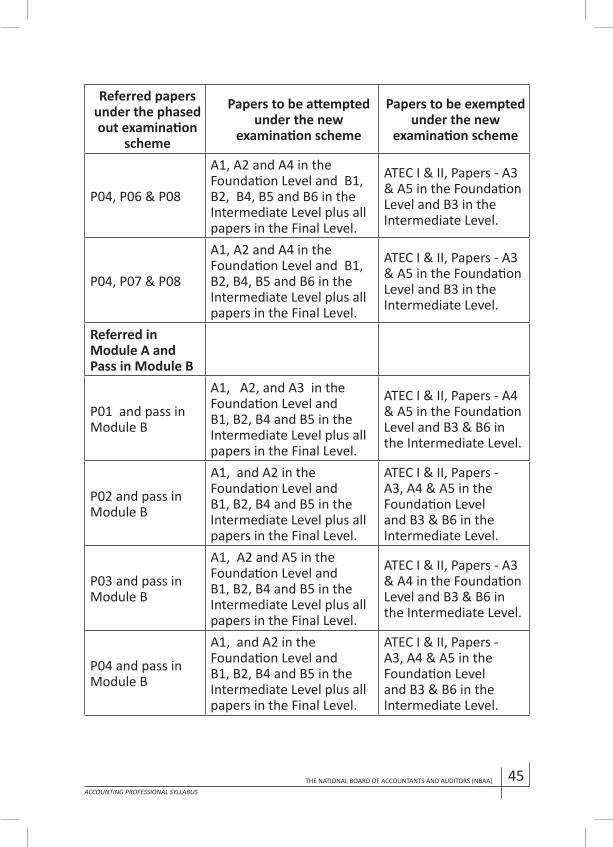

P04, P06 & P08

A1, A2 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 in theIntermediate Level.

P04, P07 & P08

A1, A2 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 in theIntermediate Level.

Referred in Module A and Pass in Module B

P01 and pass inModule B

A1, A2, and A3 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A4& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

P02 and pass inModule B

A1, and A2 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B3 & B6 in the Intermediate Level.

P03 and pass inModule B

A1, A2 and A5 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3& A4 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

P04 and pass inModule B

A1, and A2 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B3 & B6 in the Intermediate Level.

46 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

Pass in Module A and Referred in Module B

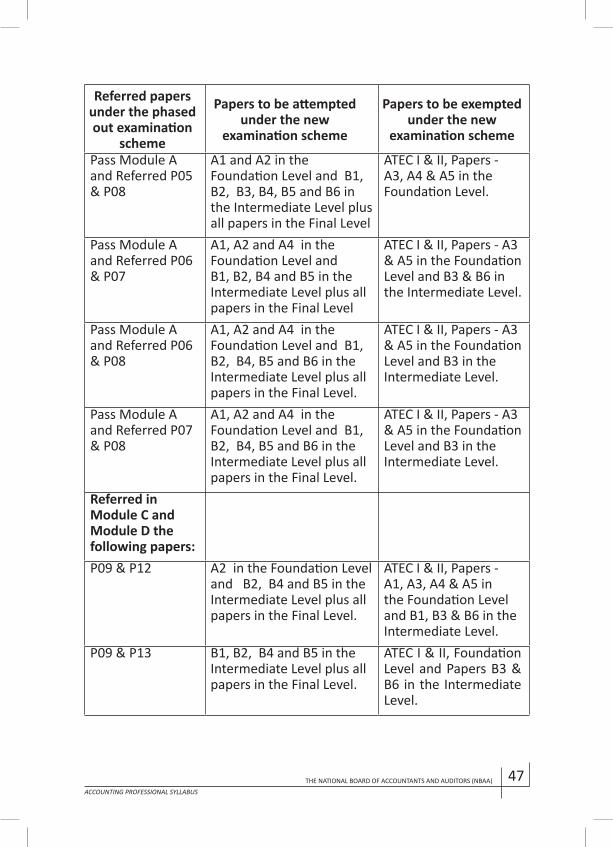

Pass Module Aand Referred P05

A1, and A2 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B6 in the Intermediate Level.

Pass Module Aand Referred P06

A1, A2 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

Pass Module Aand Referred P07

A1, A2 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

Pass Module Aand Referred P08

A1 and A2 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B3 in the Intermediate Level.

Pass Module Aand Referred P05& P06

A1, A2 and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B6 in theIntermediate Level.

Pass Module Aand Referred P05& P07

A1, A2 and A4 in the Foundation Level and B1, B2, B3, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B6 in theIntermediate Level.

47THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

Pass Module Aand Referred P05& P08

A1 and A2 in the Foundation Level and B1, B2, B3, B4, B5 and B6 inthe Intermediate Level plus all papers in the Final Level

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level.

Pass Module Aand Referred P06& P07

A1, A2 and A4 in theFoundation Level andB1, B2, B4 and B5 in theIntermediate Level plus allpapers in the Final Level

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 & B6 inthe Intermediate Level.

Pass Module Aand Referred P06& P08

A1, A2 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 in theIntermediate Level.

Pass Module Aand Referred P07& P08

A1, A2 and A4 in the Foundation Level and B1, B2, B4, B5 and B6 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3& A5 in the FoundationLevel and B3 in theIntermediate Level.

Referred in Module C and Module D the following papers:P09 & P12 A2 in the Foundation Level

and B2, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A1, A3, A4 & A5 in the Foundation Leveland B1, B3 & B6 in theIntermediate Level.

P09 & P13 B1, B2, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Foundation Level and Papers B3 & B6 in the Intermediate Level.

48 THE NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS (NBAA)ACCOUNTING PROFESSIONAL SYLLABUS

Referred papers under the phased out examination

scheme

Papers to be attempted under the new

examination scheme

Papers to be exempted under the new

examination scheme

P09 & P14B2, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Foundation Level and B1, B3 & B6 in the Intermediate Level.

P10 & P12

A2 in the Foundation Level and B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers -A1, A3, A4 & A5 in theFoundation Level andB1, B2, B3 & B6 in theIntermediate Level.

P10 & P13B1, B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, FoundationLevel and B2, B3 & B6in the IntermediateLevel.

P10 & P14B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Foundation Level and B1, B2, B3 & B6 in the Intermediate Level.

P11 & P12

A1 and A2 in the Foundation Level and B4 and B5 in the Intermediate Level plus all papers in the Final Level.

ATEC I & II, Papers - A3, A4 & A5 in the Foundation Level and B1, B2, B3 & B6 in the Intermediate Level.

P11 & P13

A1 in the Foundation Level and B1, B4 and B5 in the Intermediate Level plus all papers in the Final Level.