Embed Size (px)

Citation preview

Presented by: Jim Amos, Jack Earle, John Hamburger,

Dennis Wieczorek & Philip Zeidman

Monday, February 18th, 2013 DLA Piper LLP (US)

The 22nd Annual

―Elements of Successful Franchising: Working Through

Difficult Economic Times‖

1

Partner | DLA Piper Dennis Wieczorek

2

Philip Zeidman Partner | DLA Piper

3

Jim Amos

4

Chairman | Tasti D Lite and Planet Smoothie

5

Managing Partner | Earle Enterprises Jack Earle

John Hamburger President | Franchise Times Corp.

6

Philip Zeidman, Partner

DLA Piper LLP (US)

7

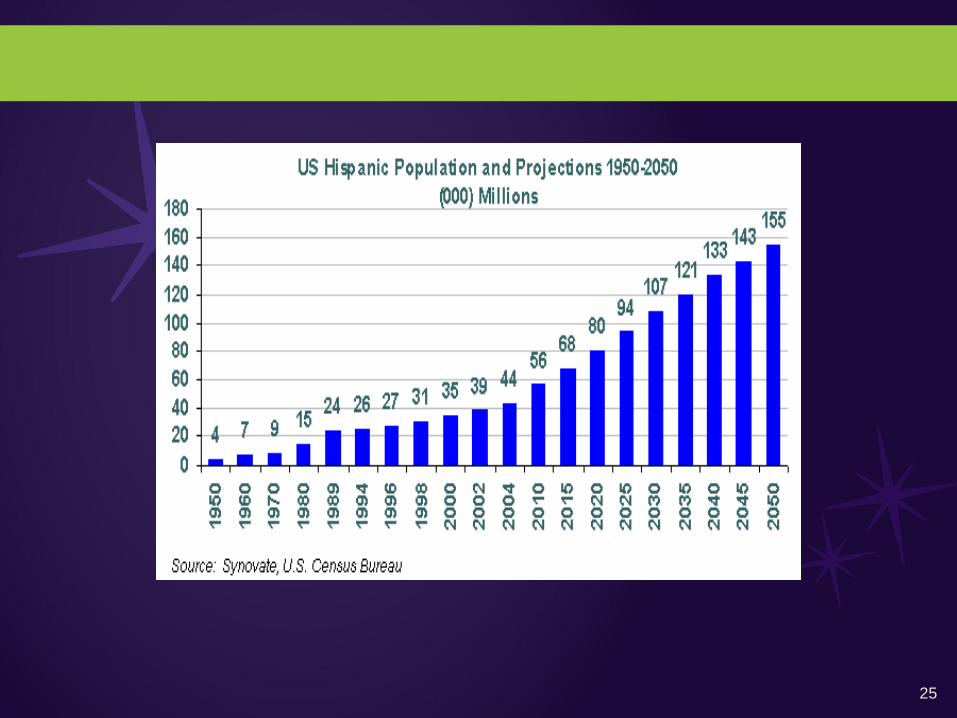

How is Franchising Affected by

the World Around us?

8

FOCUS ON VALUE

9

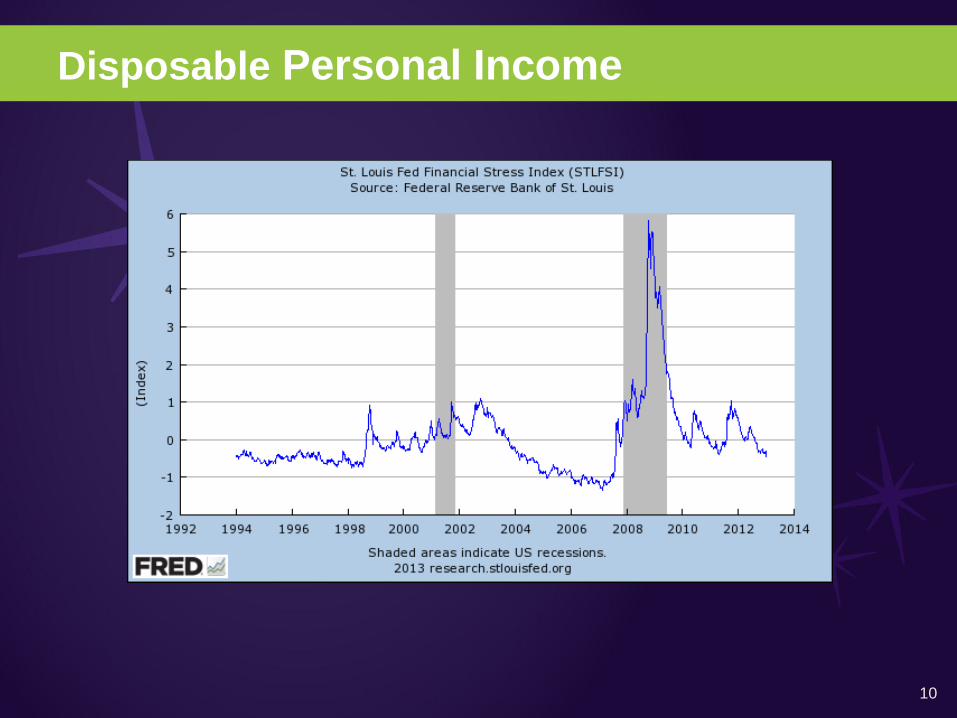

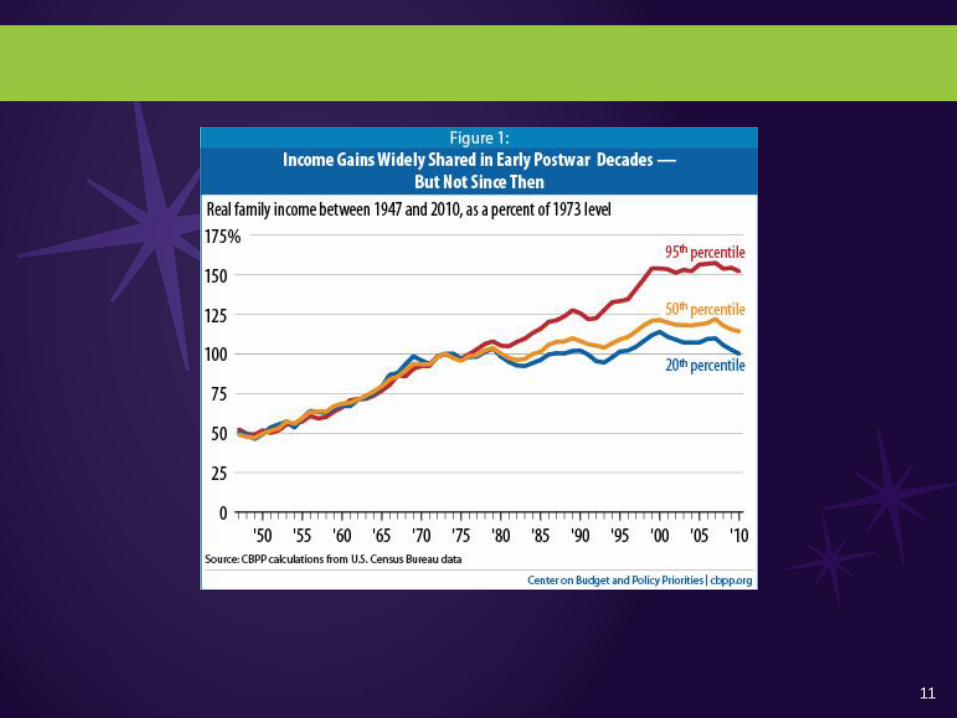

Disposable Personal Income

10

11

Wendy’s, Domino’s ring in new year

with aggressive value plans

12

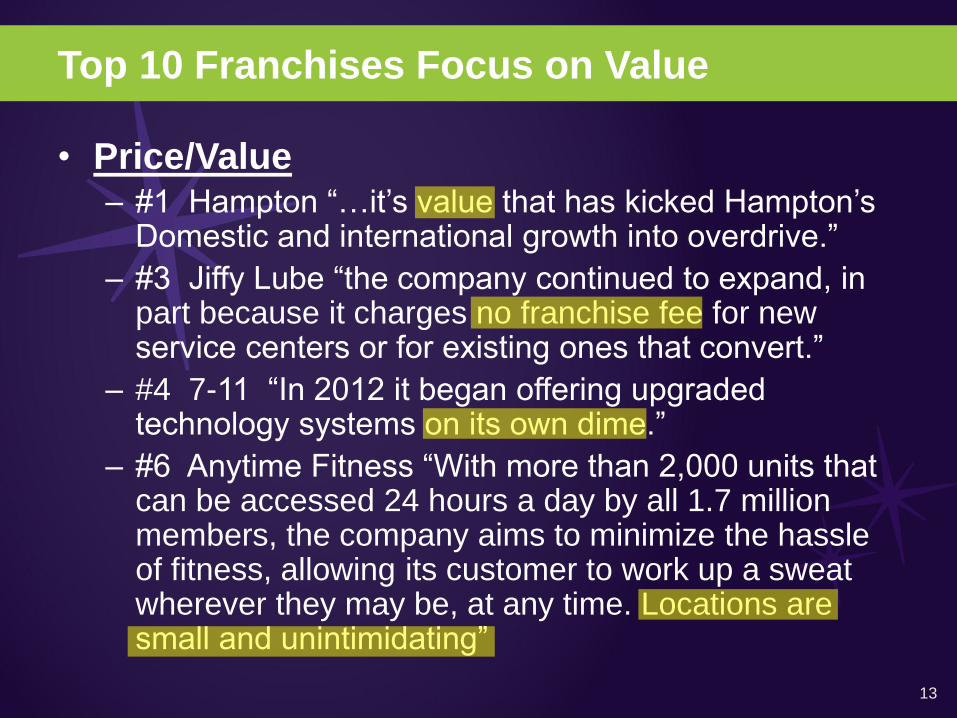

Top 10 Franchises Focus on Value

• Price/Value – #1 Hampton “…it’s value that has kicked Hampton’s

Domestic and international growth into overdrive.”

– #3 Jiffy Lube “the company continued to expand, in part because it charges no franchise fee for new service centers or for existing ones that convert.”

– #4 7-11 “In 2012 it began offering upgraded technology systems on its own dime.”

– #6 Anytime Fitness “With more than 2,000 units that can be accessed 24 hours a day by all 1.7 million members, the company aims to minimize the hassle of fitness, allowing its customer to work up a sweat wherever they may be, at any time. Locations are small and unintimidating”

13

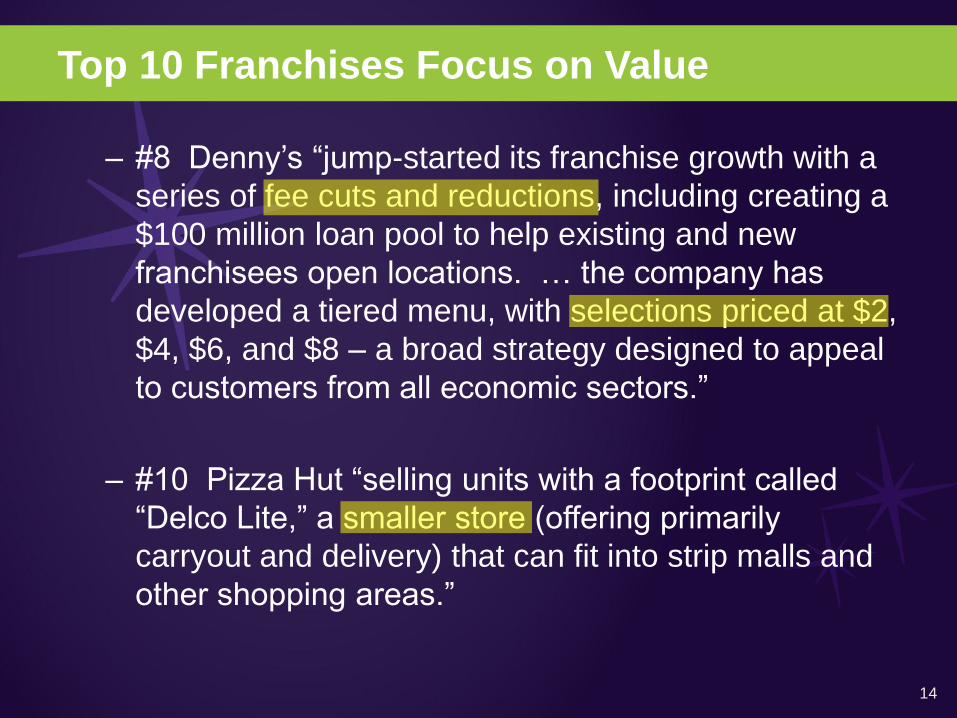

Top 10 Franchises Focus on Value

– #8 Denny’s “jump-started its franchise growth with a

series of fee cuts and reductions, including creating a

$100 million loan pool to help existing and new

franchisees open locations. … the company has

developed a tiered menu, with selections priced at $2,

$4, $6, and $8 – a broad strategy designed to appeal

to customers from all economic sectors.”

– #10 Pizza Hut “selling units with a footprint called

“Delco Lite,” a smaller store (offering primarily

carryout and delivery) that can fit into strip malls and

other shopping areas.”

14

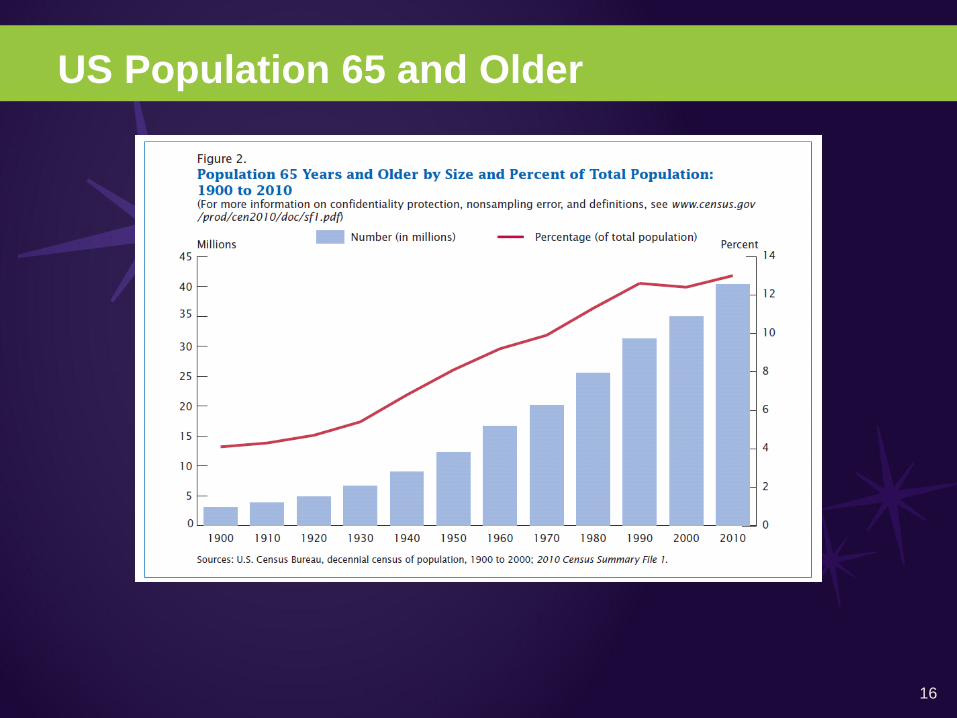

FOCUS ON AGING

15

US Population 65 and Older

16

Aging Population Drives Growth in

Elder Care Franchises

17

FOCUS SHIFTS TO WOMEN

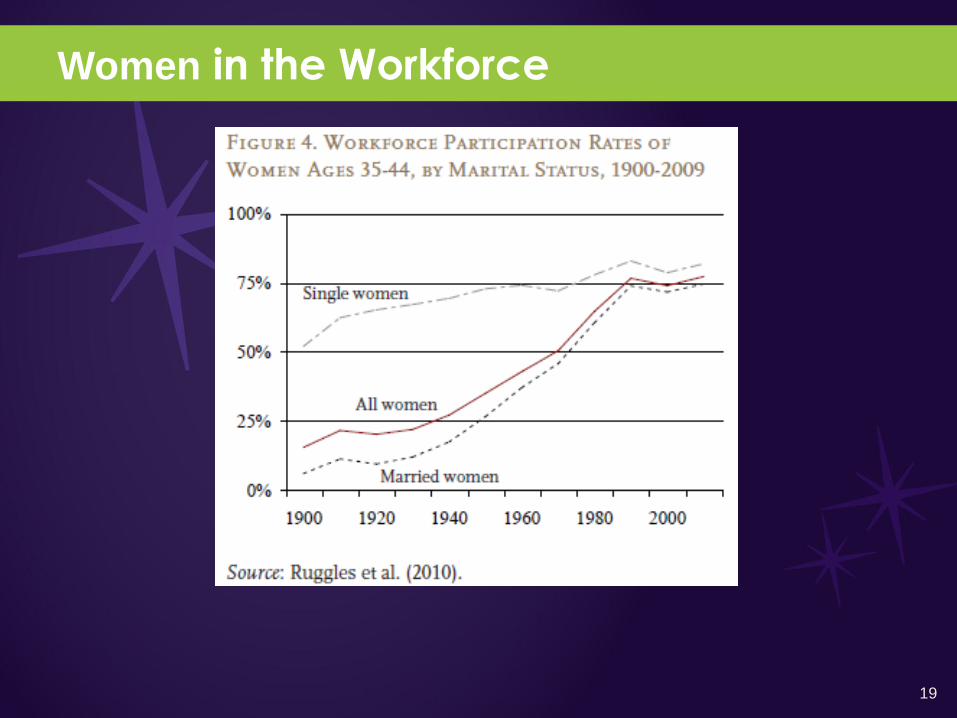

18

Women in the Workforce

19

LIFESTYLE

• FITNESS

• ENVIRONMENTAL

• DIETARY

20

7-Eleven Shifts Focus to

Healthier Food Options

21

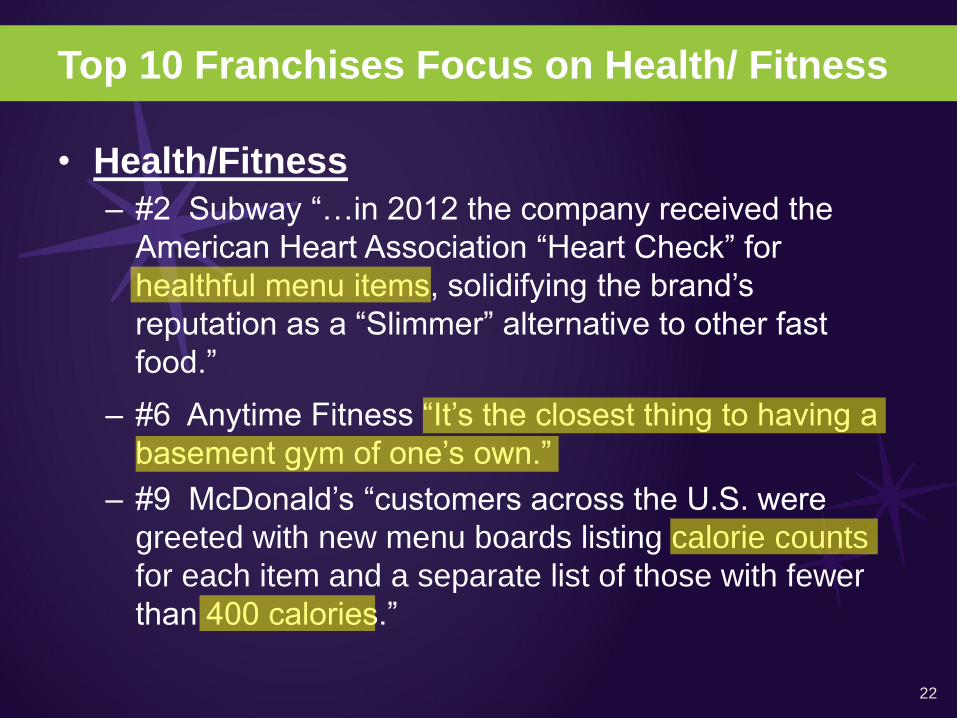

Top 10 Franchises Focus on Health/ Fitness

• Health/Fitness

– #2 Subway “…in 2012 the company received the

American Heart Association “Heart Check” for

healthful menu items, solidifying the brand’s

reputation as a “Slimmer” alternative to other fast

food.”

– #6 Anytime Fitness “It’s the closest thing to having a

basement gym of one’s own.”

– #9 McDonald’s “customers across the U.S. were

greeted with new menu boards listing calorie counts

for each item and a separate list of those with fewer

than 400 calories.”

22

FOCUS ON MINORITIES

23

24

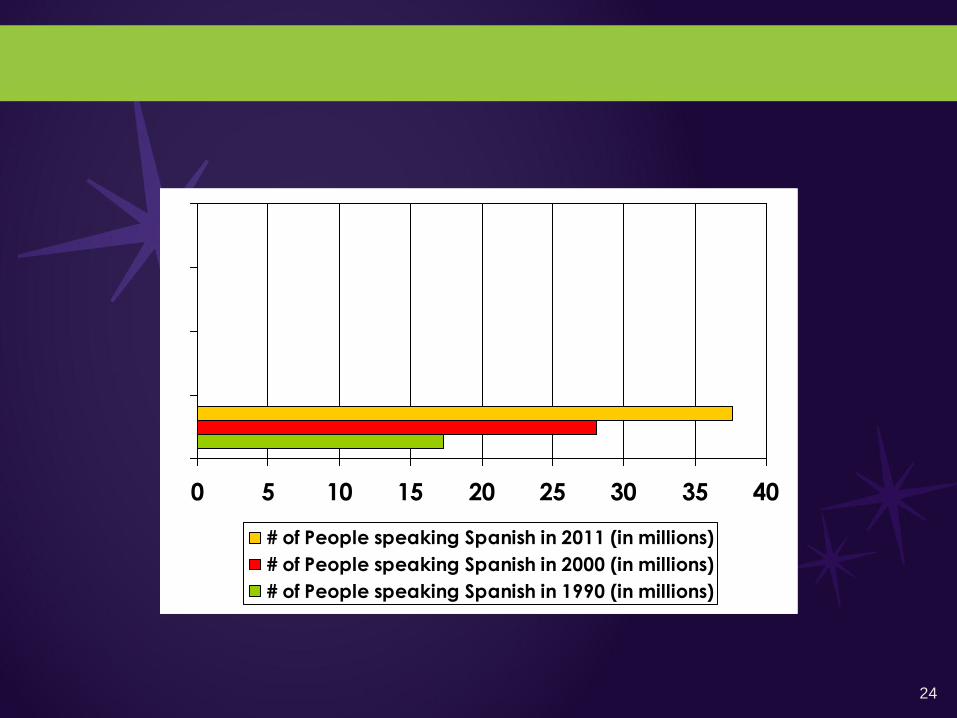

0 5 10 15 20 25 30 35 40

# of People speaking Spanish in 2011 (in millions)

# of People speaking Spanish in 2000 (in millions)

# of People speaking Spanish in 1990 (in millions)

25

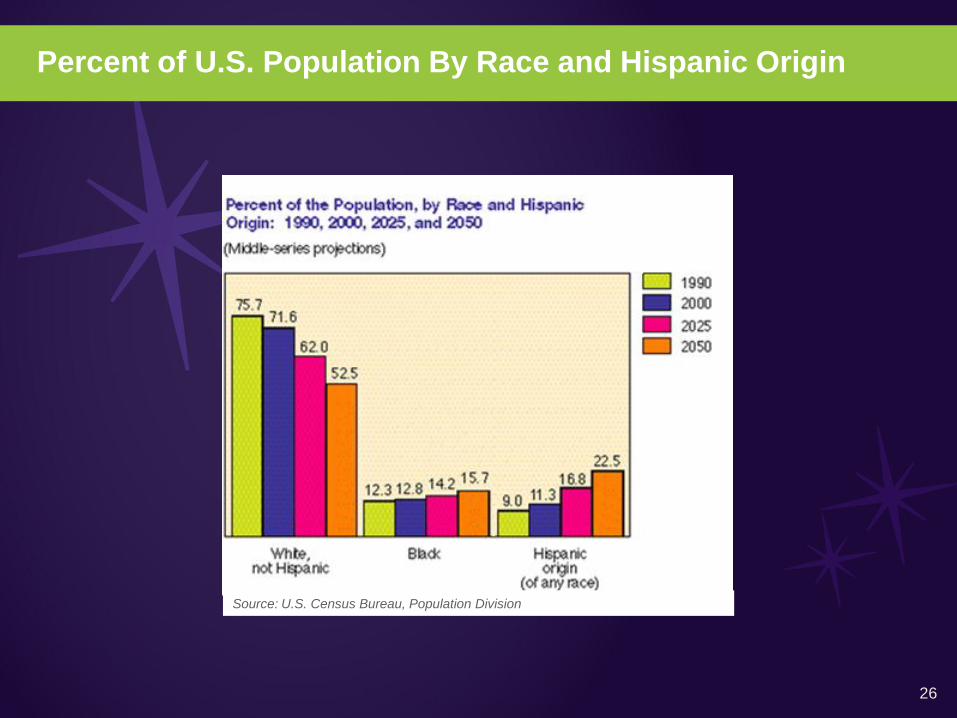

Percent of U.S. Population By Race and Hispanic Origin

26

Source: U.S. Census Bureau, Population Division

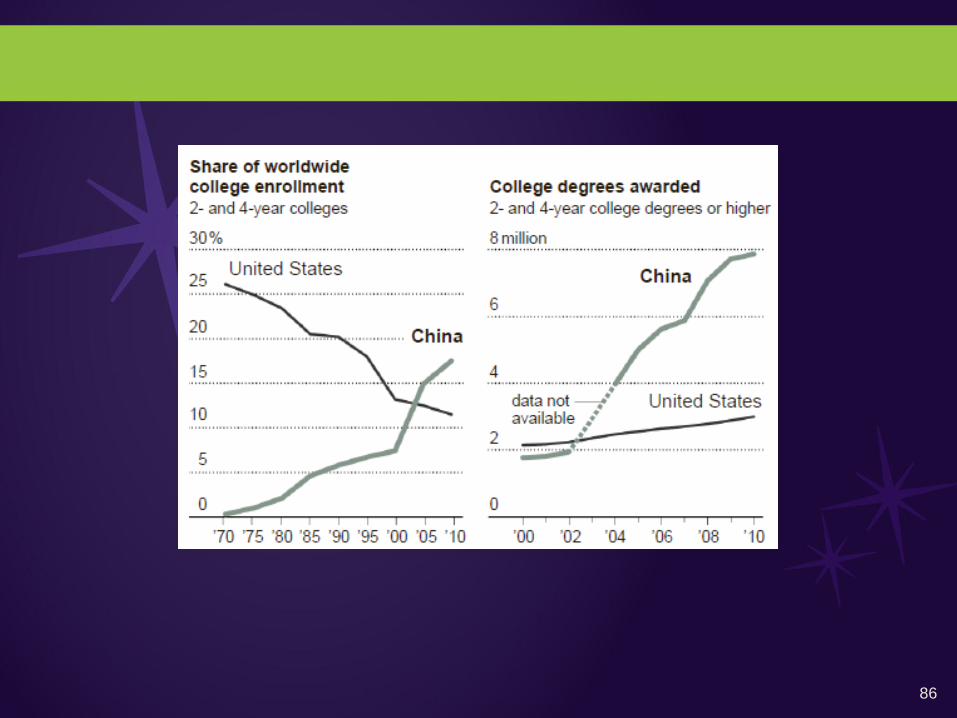

Education

27

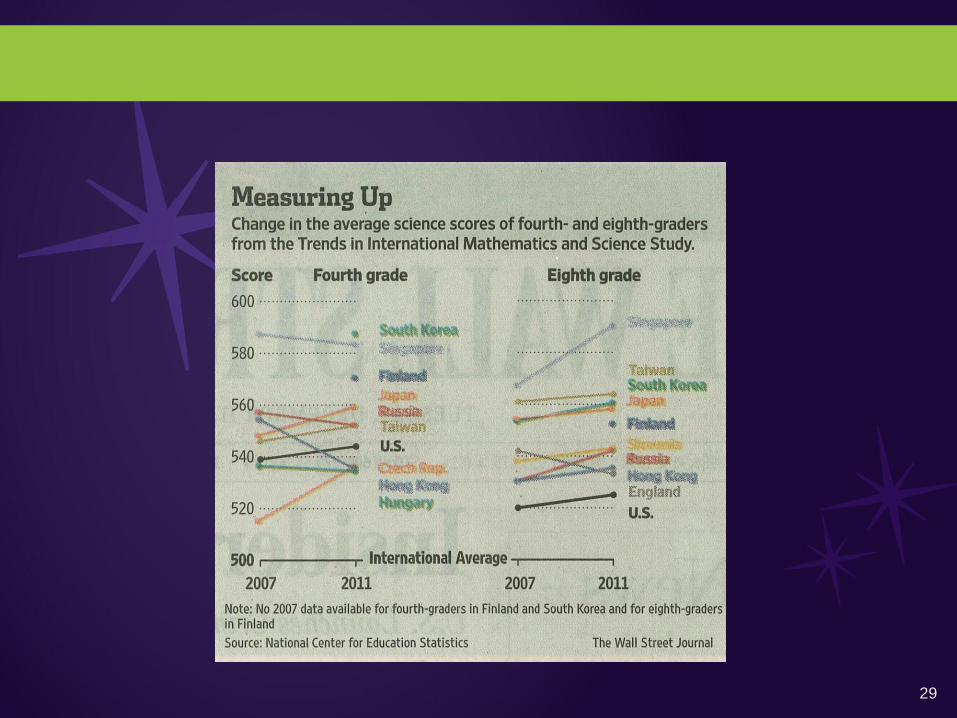

Competitors Still Beat

U.S. in Tests

28

29

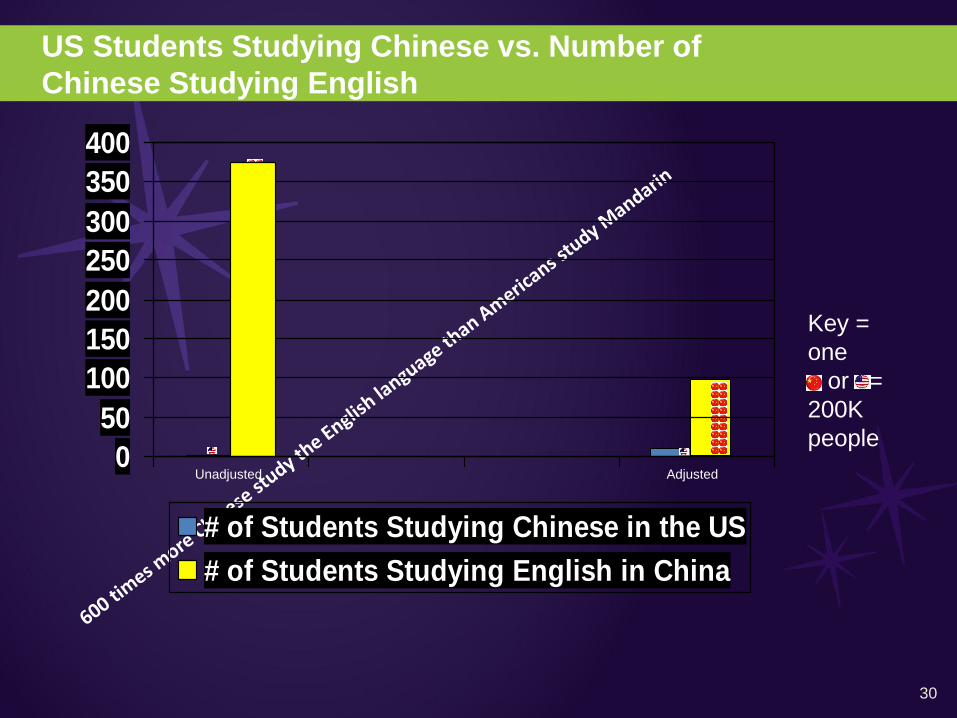

US Students Studying Chinese vs. Number of

Chinese Studying English

Key =

one

or =

200K

people

Unadjusted Adjusted

30

0

50

100

150

200

250

300

350

400

# of Students Studying Chinese in the US

# of Students Studying English in China

Dennis Wieczorek, Partner

DLA Piper LLP (US)

31

WHAT’S HAPPENING RIGHT

NOW? TRENDS

FRANCHISORS ARE FACING

TODAY

32

The Institutionalization of

Franchising

33

Institutionalization of Franchising

• Financial Markets Have a Better Understanding

of Franchising

– Public companies

– Securitization

– Private equity

34

Institutionalization of Franchising

• Private Equity

– Numerous transactions

• Purchase from founder

• Purchase from another P/E firm

– Attractive because

• Predictable revenue stream

• Growth model

• Modest capital needs

35

Institutionalization of Franchising

• Private Equity

– But not all roses

• Prominent bankruptcies

• Restructurings at others

• Many relate to acquisitions before crash in 2008

36

SOCIAL MEDIA

37

Social Media

• Key element of many franchise programs

– Most often to reach customers and create loyalty

(and consumer facing programs are important to

franchise sales)

– But broader uses too: jobs, franchise sales

38

Social Media

• Differences among franchise systems – some love it, some tolerate it, but can’t be ignored

• Need social media policy (ops manual, agreements) – Most common-franchisee can use social

media but subject to some overall franchisor control

– Legal issues • Truth-in-advertising

• Defamation

• Franchise laws

• Endorsements

39

Social Media

• Importance to Franchise Sales

– Robust sites allow interaction with

candidates

– Blogs

– Validation from existing franchisees

(lessens need for phone intrusions)

40

• Who is watching your brand on social media?

– Staff

– Outside service

• Without unifying policies, could create chaos

Social Media

41

The Government

Is Here To Help You

42

Government Intrusion

Employment

– Health care

– Fast union elections (in lieu of card check)

– Wage hour laws – continued litigation

– But recent success in litigation against NLRB

43

Intersection With Employment Law

Can a franchisee be an employee of the franchisor?

• Massachusetts case – minimum wage and other requirements

– IFA working on a statutory change

• Some favorable decisions in other states

• But plaintiffs lawyers are expanding cases to other franchise systems

44

Government Intrusion

Operations

– Menu labeling

– What you can sell – N.Y.C. beverage law

– Where you can locate – local zoning restrictions

45

Government Intrusion

Financial matters

– Credit

• IFA working with SBA to facilitate use of Franchise

Registry

– Taxes

• Only going up and continuing uncertainty

regarding debt and spending

– Federal ethanol policies

46

―Nexus‖ – What Does It Mean?

• KFC v. Iowa – first high court holding that

franchisor has nexus with a state for

income tax purposes

• Income tax different from sales tax

• Nexus exists if trademarks used in state

47

Government Intrusion

Franchising

– Some issues percolating in several states

– IFA fought off CA bill

– New activity in MA and elsewhere

48

The Affordable Care Act

49

Affordable Care Act

• Unless very small (less than 50 employees), it

applies to many franchisors and franchisees

• Setting up additional entities doesn’t help -

attribution rules

50

Affordable Care Act

• Understanding the law

• Determining financial impact

• Retaining employees – dealing with the

competition

• Public relations issues

51

Government Intrusion

• Franchisors and franchisees are on the

same page on almost every issue

• IFA increasingly recognized as the

voice of small business (and all of

franchising)

52

John Hamburger, President

Franchise Times

53

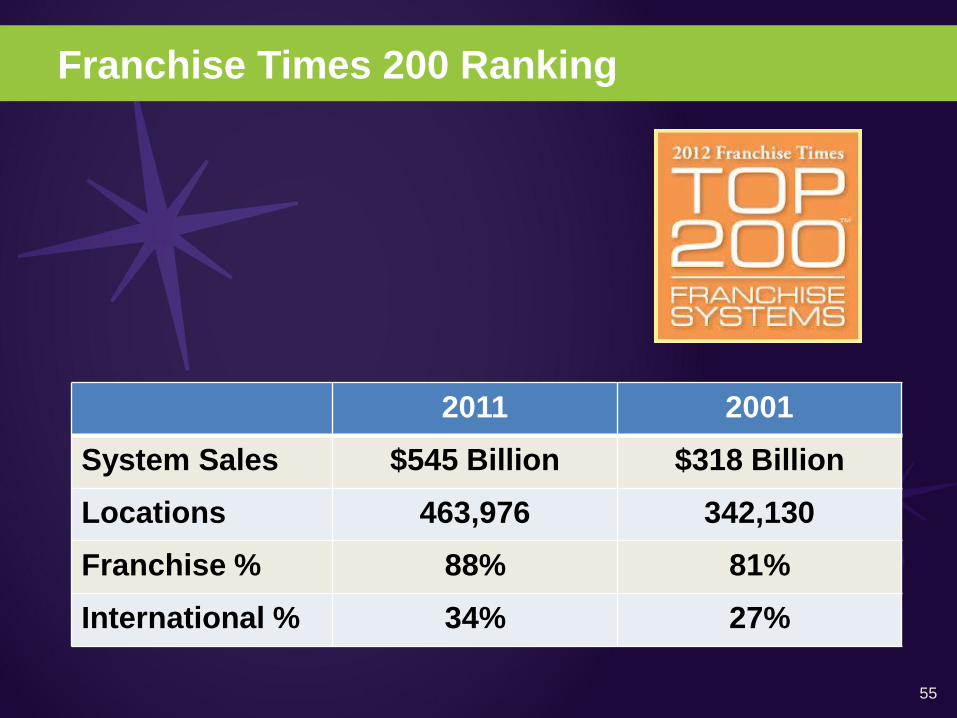

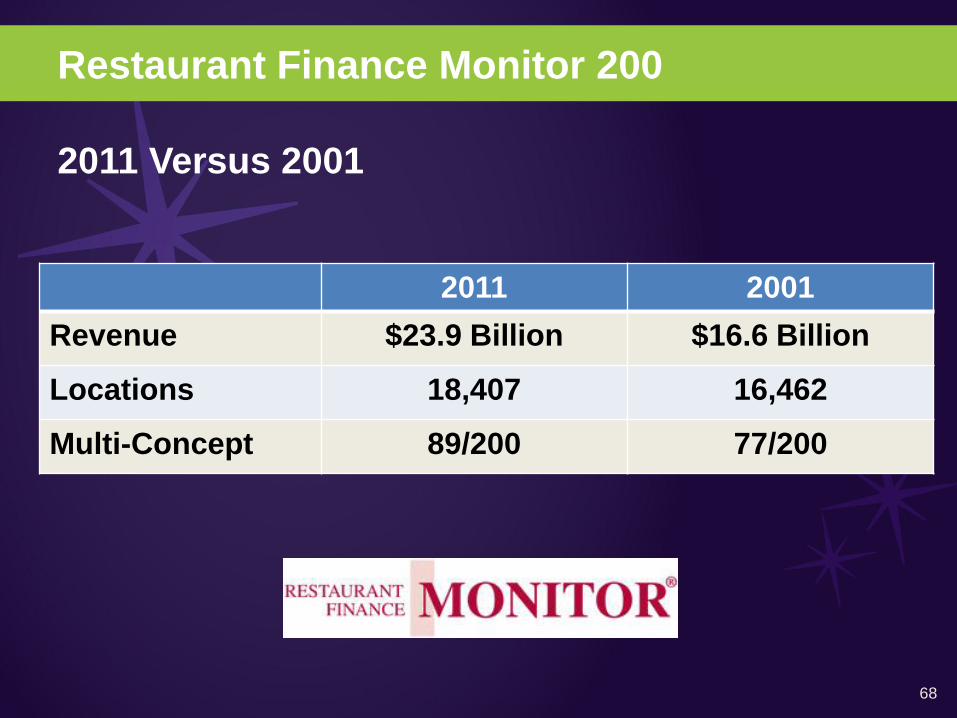

Restaurant Finance Monitor 200

• The Top 200 U.S. Restaurant Franchisees in the

U.S.

• Ranked According to Annual Sales and Number

of Franchised Units

54

Franchise Times 200 Ranking

2011 2001

System Sales $545 Billion $318 Billion

Locations 463,976 342,130

Franchise % 88% 81%

International % 34% 27%

55

The Top 10 Franchises–Revenue

Company Worldwide Sales

McDonald‘s $85.9B

7-Eleven $76.6B

KFC $21.3B

Subway $16.6B

Burger King $15.0B

Pizza Hut $12.6B

Ace Hardware $12.5B

Hertz $11.9B

Circle K $11.8B

Wendy‘s $9.2B

56

The Top 10 Franchises–Locations

Company Worldwide Locations

7-Eleven 43,912

Subway 35,920

McDonald‘s 33,510

KFC 17,401

Pizza Hut 13,747

H&R Block 12,776

Burger King 12,512

Jani-King 11,170

JAN-PRO 10,680

Dunkin‘ Donuts 9,792

57

10-Year Sales Growth

Company Worldwide Sales

7-Eleven $46.9B

McDonald‘s $45.3B

KFC $12.6B

Subway $11.4B

Pizza Hut $5.0B

Tim Horton‘s $4.6B

Hilton Hotels $4.4B

Dunkin‘ Donuts $3.5B

Burger King $3.3B

H&R Block $3.2B

58

10-Year Unit Growth

Company Worldwide Locations

7-Eleven 21,264

Subway 19,961

KFC 5,586

Dunkin‘ Donuts 4,892

McDonald‘s 4,454

Liberty Tax Service 3,522

Domino‘s 2,670

Jani-King 2,648

H&R Block 2,425

Coverall Cleaning 2,168

59

10-Year International Unit Growth

Company International Locations

7-Eleven 21,037

Subway 8,487

KFC 6,205

McDonald‘s 3,493

Domino‘s 2,576

Century 21 2,273

Pizza Hut 1,875

Burger King 1,823

Dunkin‘ Donuts 1,620

Dairy Queen 1,284

60

10-Year Percentage Growth

Company Worldwide Sales

Liberty Tax Service 3335%

Wingstop 1804%

Jimmy John‘s 1796%

Plato‘s Closet 1424%

Cold Stone Creamery 1005%

Buffalo Wild Wings 929%

Panera Bread 646%

Goddard School 575%

McAlister‘s Deli 458%

Tim Horton‘s 430%

61

10-Year Largest Unit Declines

Company Worldwide Locations

Taco Bell -738

Midas -526

Holiday Inn -505

Hardee‘s -419

Schlotzky‘s -322

Jiffy Lube -255

Sir Speedy -238

Play It Again Sports -177

Travelodge -158

Fantastic Sams -135

62

Growth Trends–Sandwiches

Company Worldwide Sales

Jimmy Johns‗s $970M

Einstein Bagels $413M

McAlister‘s Deli $367M

Firehouse Subs $285M

Jersey Mikes $280M

Corner Bakery $261M

63

Growth Trends–Fitness

Company Worldwide Sales

Massage Envy $804M

Planet Fitness $520M

Anytime Fitness $365M

Snap Fitness $334M

64

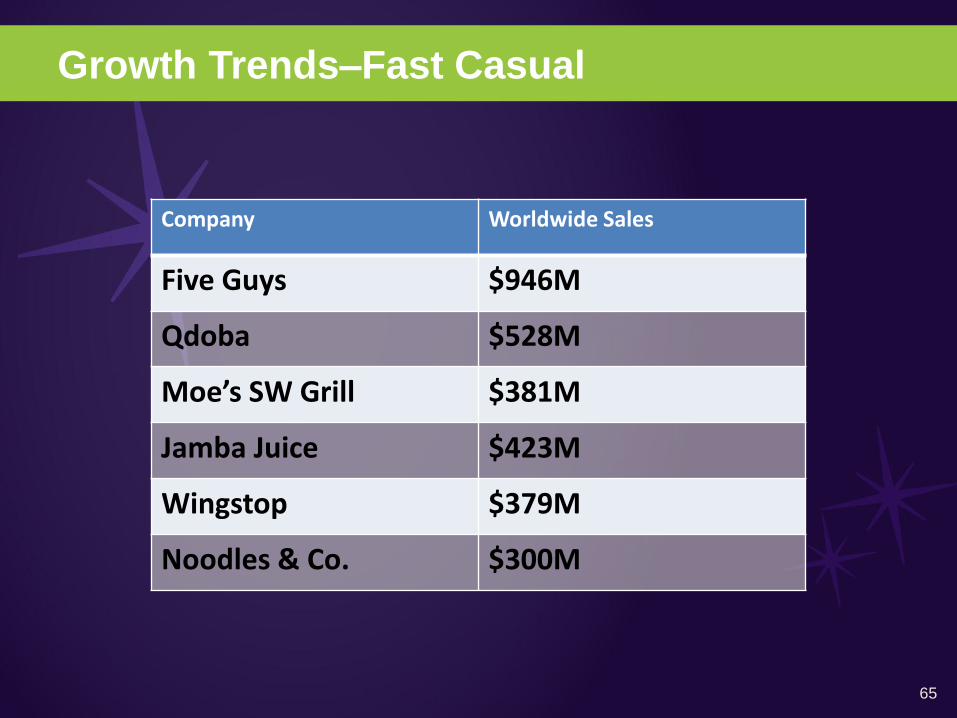

Growth Trends–Fast Casual

Company Worldwide Sales

Five Guys $946M

Qdoba $528M

Moe’s SW Grill $381M

Jamba Juice $423M

Wingstop $379M

Noodles & Co. $300M

65

Franchise Times 200

Franchise Concentration

% Franchised 2011 2001

100% 66/200 61/200

>90% 113/200 103/200

>80% 138/200 122/200

66

Franchise Times 200

International Franchising

2011 2001

Overall 34% 27%

>50% 21/200 16/200

>25% 54/200 47/200

67

Restaurant Finance Monitor 200

2011 Versus 2001

2011 2001

Revenue $23.9 Billion $16.6 Billion

Locations 18,407 16,462

Multi-Concept 89/200 77/200

68

Monitor 200—Largest Franchisees

Company Annual Sales

NPC International $938M Pizza Hut

Apple American $821M Applebee‘s

Bridgeman Foods $518M Chili‘s—Wendy‘s

Covelli $426M Panera

Strategic $405M Burger King

Boddie-Noell $386M Hardees

Carrols $348M Burger King

Harman Mgmt $346M KFC—Taco Bell

Briad Group $327M TGI Fridays—

Wendy‘s

Doherty $303M Applebees—Panera 69

WHAT HAVE WE LEARNED FROM THE MONITOR 200

STUDY?

• Increase in multi-concept franchisees

• Primary concept is a large brand

• Growth is from consolidation, not unit growth

• Lenders, PE firms, lower margins and high

remodeling costs are driving consolidation

• Large franchisees are willing to accept modest

risks with secondary brands

• Top 200 are heavily targeted by franchisors

70

WHAT‘S IN STORE FOR THE FUTURE?

• Franchising is still a growth business

• New ideas come along frequently on trends

• Companies would be wise to focus on

international development

• Franchisees seek strong brands

• Capital migrates to the strong brands

71

THE GROWING

INTERNATIONALIZATION OF

FRANCHISING

72

International Growth

The 200 Top Franchisors now have 34% of Their

Units Outside the U.S.

Courtesy of Franchise Times

73

International Growth

• The Larger the Franchise Network, the Higher

the % Outside the U.S.

Courtesy of Franchise Times

74

International Growth

• But Not Just the Giants. . .

• And Not Just Food Service. . .

• And Not Just Hotels. . .

• Service and Retail. . .

75

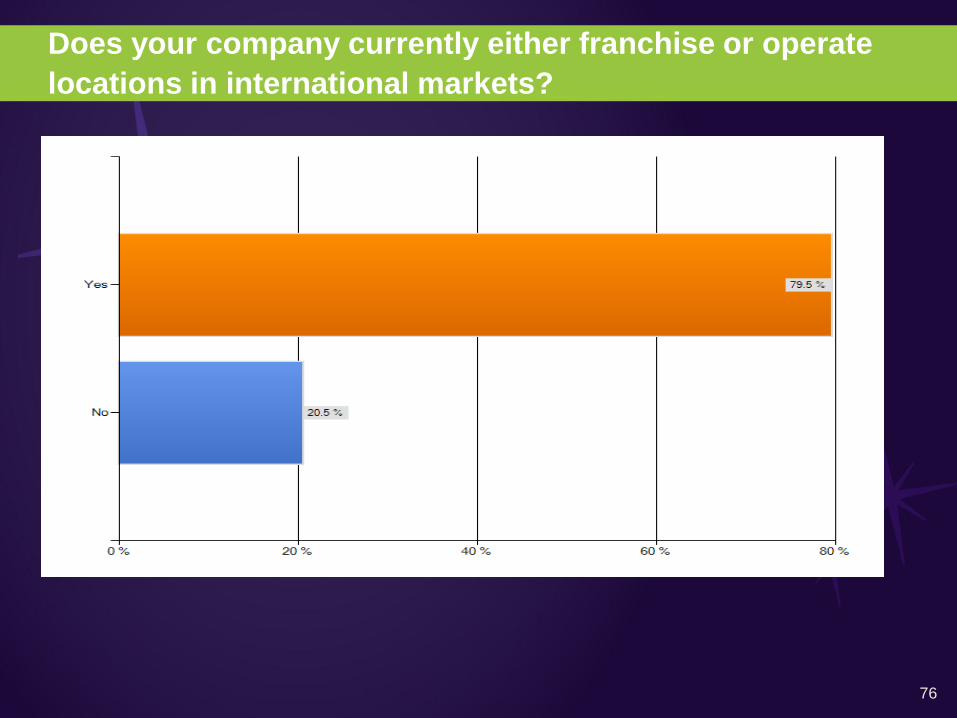

Does your company currently either franchise or operate

locations in international markets?

76

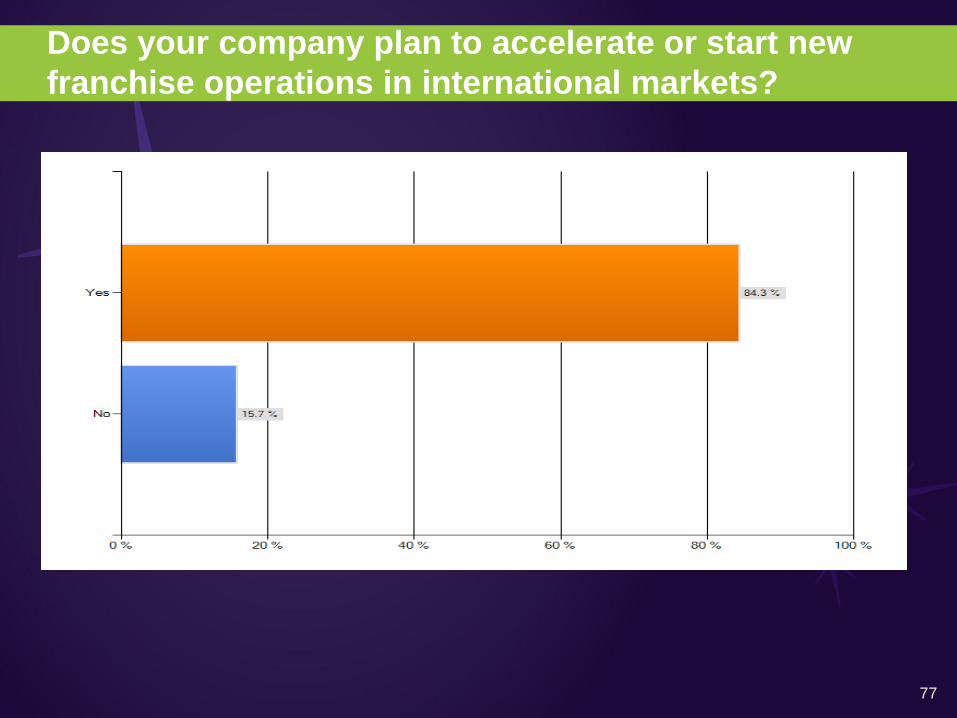

Does your company plan to accelerate or start new

franchise operations in international markets?

77

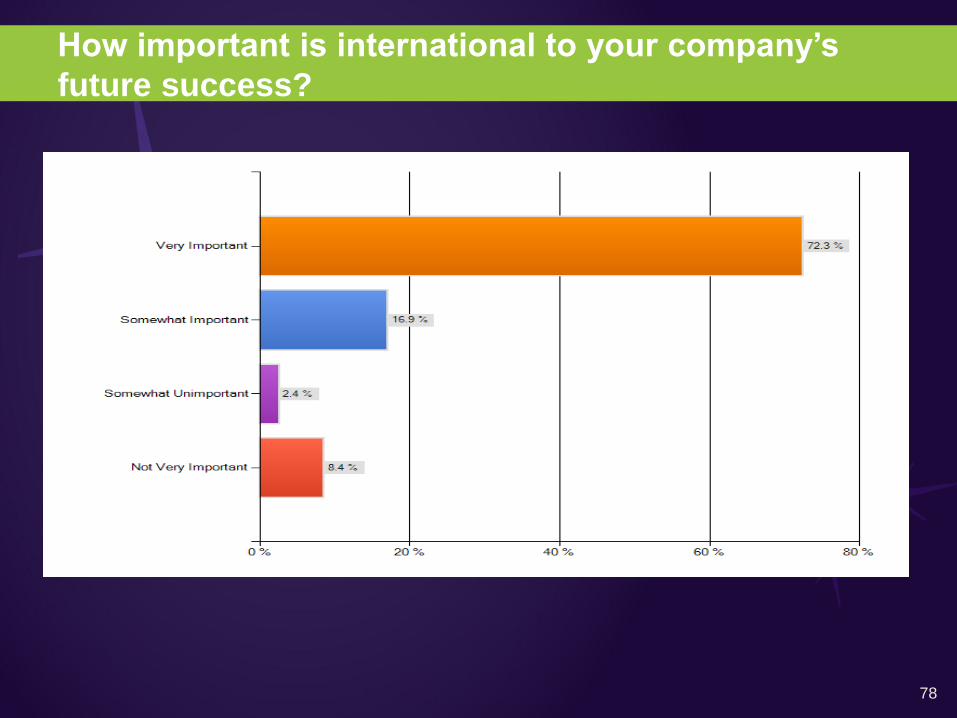

How important is international to your company‘s

future success?

78

WHY IS THIS HAPPENING, AND

WHY IS IT HAPPENING NOW?

79

THE LEGAL ASPECTS OF

INTERNATIONAL FRANCHISING

80

Franchise Laws Around the World:

Beginning of the 1970‘s

Copyright © 2011 DLA Piper. All rights reserved. 81

Franchise Laws Around the World:

Beginning of the 1980‘s

Copyright © 2011 DLA Piper. All rights reserved. 82

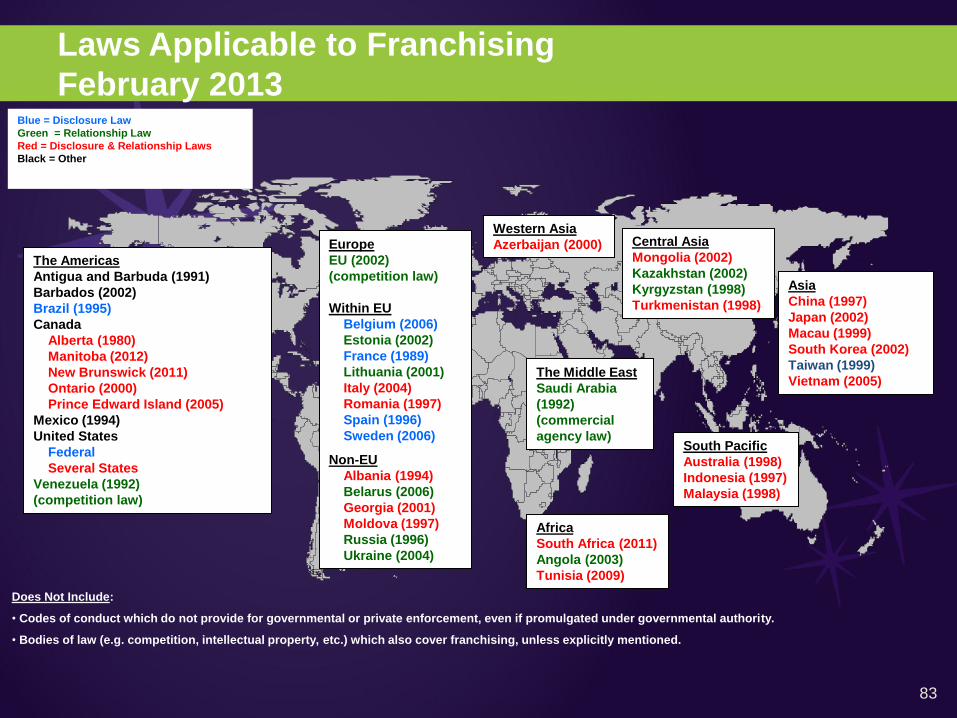

Laws Applicable to Franchising

February 2013

83

Blue = Disclosure Law

Green = Relationship Law

Red = Disclosure & Relationship Laws

Black = Other

The Americas

Antigua and Barbuda (1991)

Barbados (2002)

Brazil (1995)

Canada

Alberta (1980)

Manitoba (2012)

New Brunswick (2011)

Ontario (2000)

Prince Edward Island (2005)

Mexico (1994)

United States

Federal

Several States

Venezuela (1992)

(competition law)

Europe

EU (2002)

(competition law)

Within EU

Belgium (2006)

Estonia (2002)

France (1989)

Lithuania (2001)

Italy (2004)

Romania (1997)

Spain (1996)

Sweden (2006)

Non-EU

Albania (1994)

Belarus (2006)

Georgia (2001)

Moldova (1997)

Russia (1996)

Ukraine (2004)

Central Asia

Mongolia (2002)

Kazakhstan (2002)

Kyrgyzstan (1998)

Turkmenistan (1998)

Asia

China (1997)

Japan (2002)

Macau (1999)

South Korea (2002)

Taiwan (1999)

Vietnam (2005) The Middle East

Saudi Arabia

(1992)

(commercial

agency law) South Pacific

Australia (1998)

Indonesia (1997)

Malaysia (1998)

Does Not Include:

• Codes of conduct which do not provide for governmental or private enforcement, even if promulgated under governmental authority.

• Bodies of law (e.g. competition, intellectual property, etc.) which also cover franchising, unless explicitly mentioned.

Africa

South Africa (2011)

Angola (2003)

Tunisia (2009)

Western Asia

Azerbaijan (2000)

• Implications for U.S. Franchisors

• Upside or downside?

84

Becoming More Like Us?

Improving Markets Abroad

• Spreading affluence, growing middle

class

• …the pluses and minuses

• Growing Competition

– By indigenous Companies

– Coming into the U.S.

– For employees

85

86

87

Moments of Opportunity…Moments of

Peril

88

Programs or rights not included at outset

will prove difficult to initiate later.

89

Establish objective criteria, or

self-executing mechanisms or events that

eliminate need to take confrontational

position with franchisees.

90

Preserve right at renewal to require franchisee to –

– Sign a current franchise agreement

– Upgrade its facility to current standards

– Use appropriate occasions to require franchisee

to update or improve.

91

What if you‘re wrong?

92

WHEN TROUBLES COME…

93

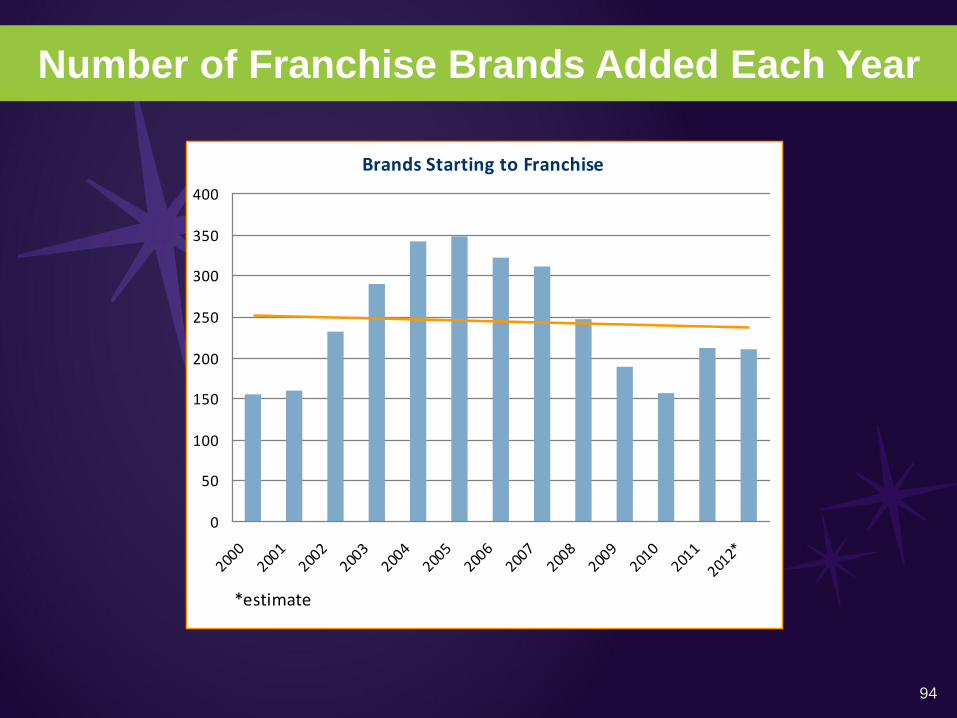

Number of Franchise Brands Added Each Year

94

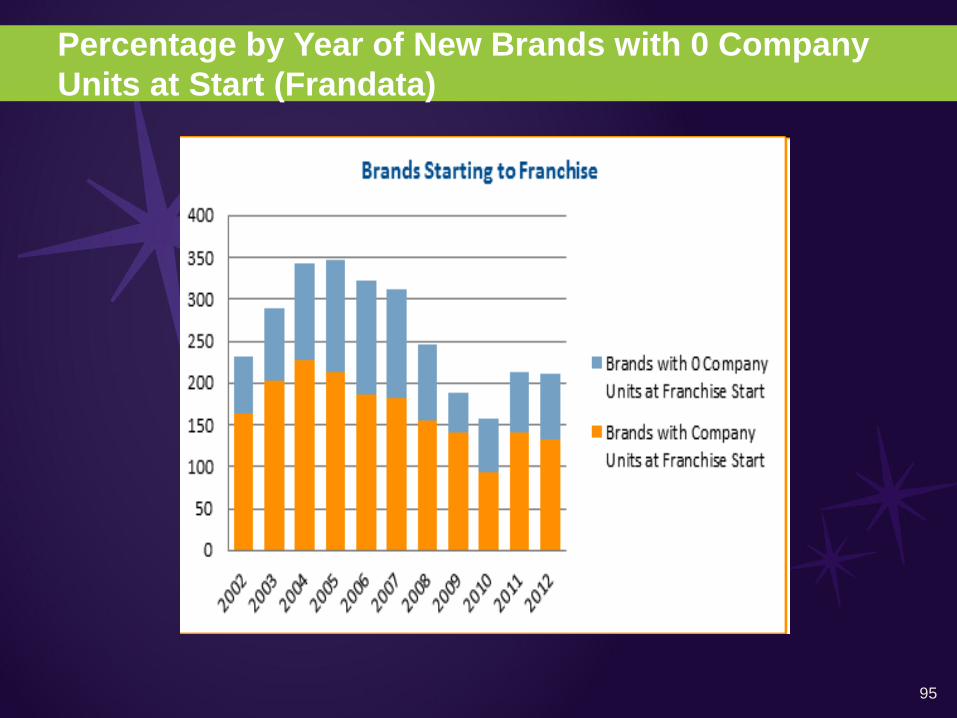

Brands Starting to Franchise

0

50

100

150

200

250

300

350

400

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012*

*estimate

Percentage by Year of New Brands with 0 Company

Units at Start (Frandata)

95

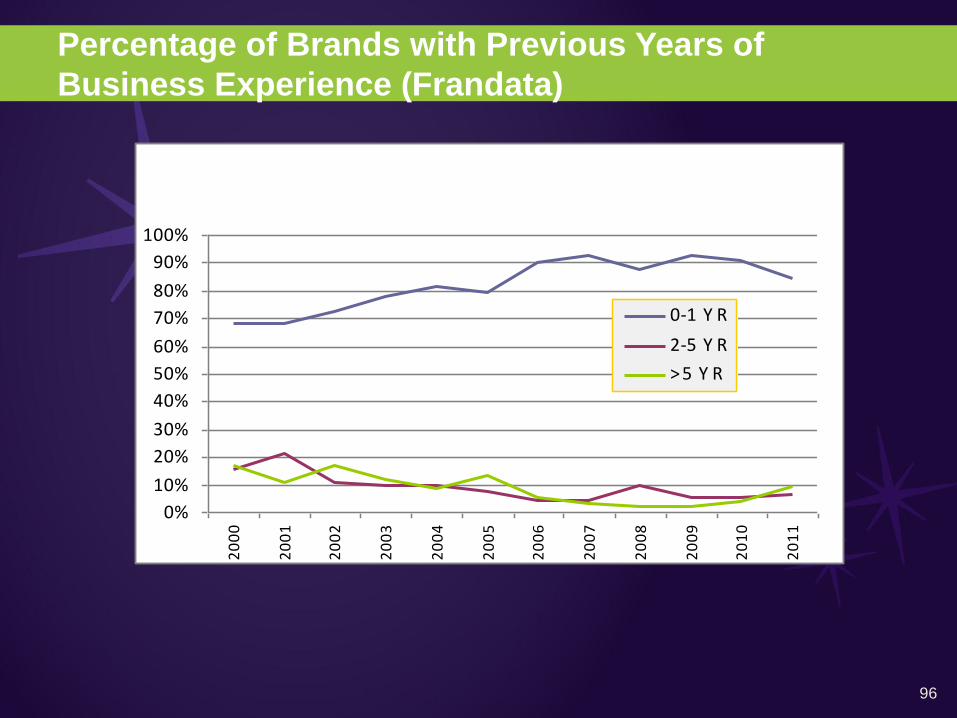

Percentage of Brands with Previous Years of

Business Experience (Frandata)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%2

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

0-1 Y R

2-5 Y R

> 5 Y R

96

“Majority of US Franchises Now Owned

by Multi-Unit Franchisees”

97

Q & A

98

Contact Information

Jim Amos

Email: [email protected]

T: 615-550-3114

Jack Earle

Email: [email protected]

T: 856-797-9870

John M. Hamburger

Email: [email protected]

T: 612-767-3201

Dennis E. Wieczorek

Email: [email protected]

T: 312-368-4087

Philip F. Zeidman

Email: [email protected]

T: 202-799-4272

99

100

DLA Piper LLP (US) gratefully acknowledges

the following:

101