Embed Size (px)

Citation preview

terveystalo.com #terveystalo

TERVEYSTALO - LEADING THE WAY IN CUSTOMER-CENTRIC PROACTIVE CARE

© Terveystalo

Agenda

• Terveystalo in brief 1 • Terveystalo as an investment 2 • 2018 highlights 3 • Q&A 4

3

© Terveystalo

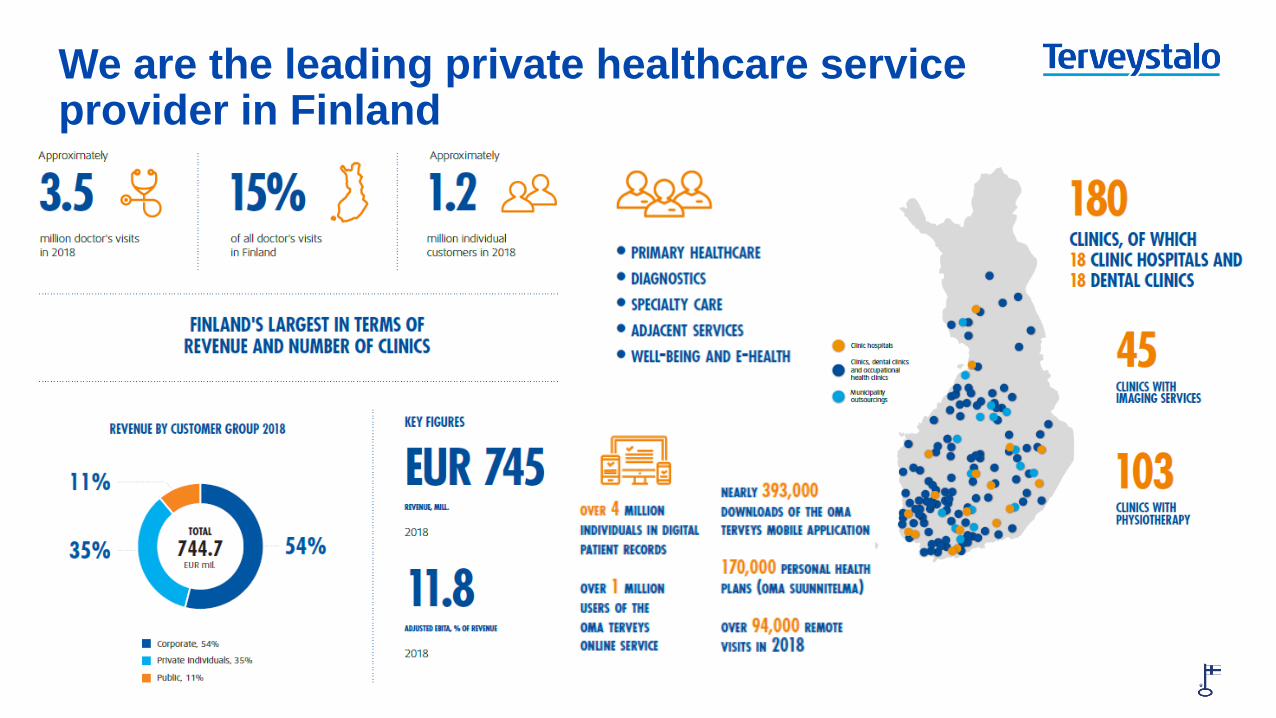

We are the leading private healthcare service provider in Finland

4

© Terveystalo

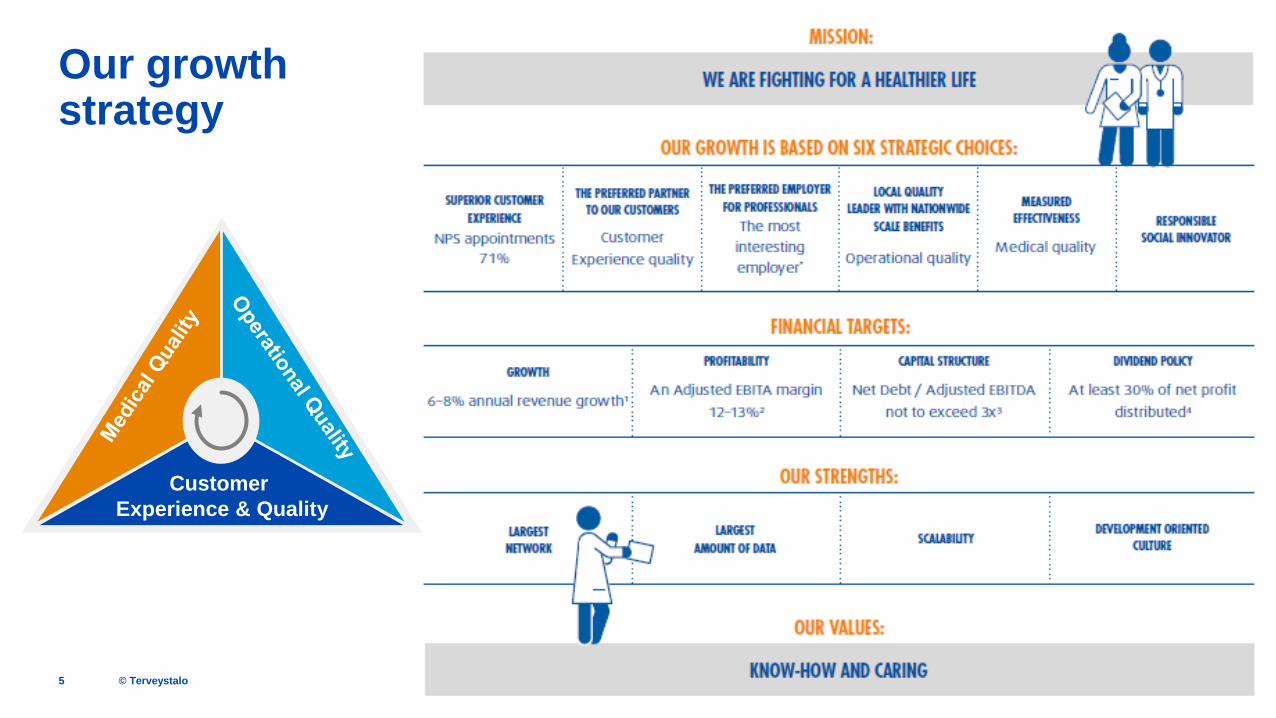

Our growth strategy

5

Customer Experience & Quality

Terveystalo as an investment

Megatrends accelerate structural

market growth

Customized services

for different customer groups enable growth in evolving markets

Competitive advantage from

scale - operational leverage and

optimised use of resources

Opportunities to accelerate

growth through

acquisitions

Corporate culture that attracts healthcare

professionals

© Terveystalo

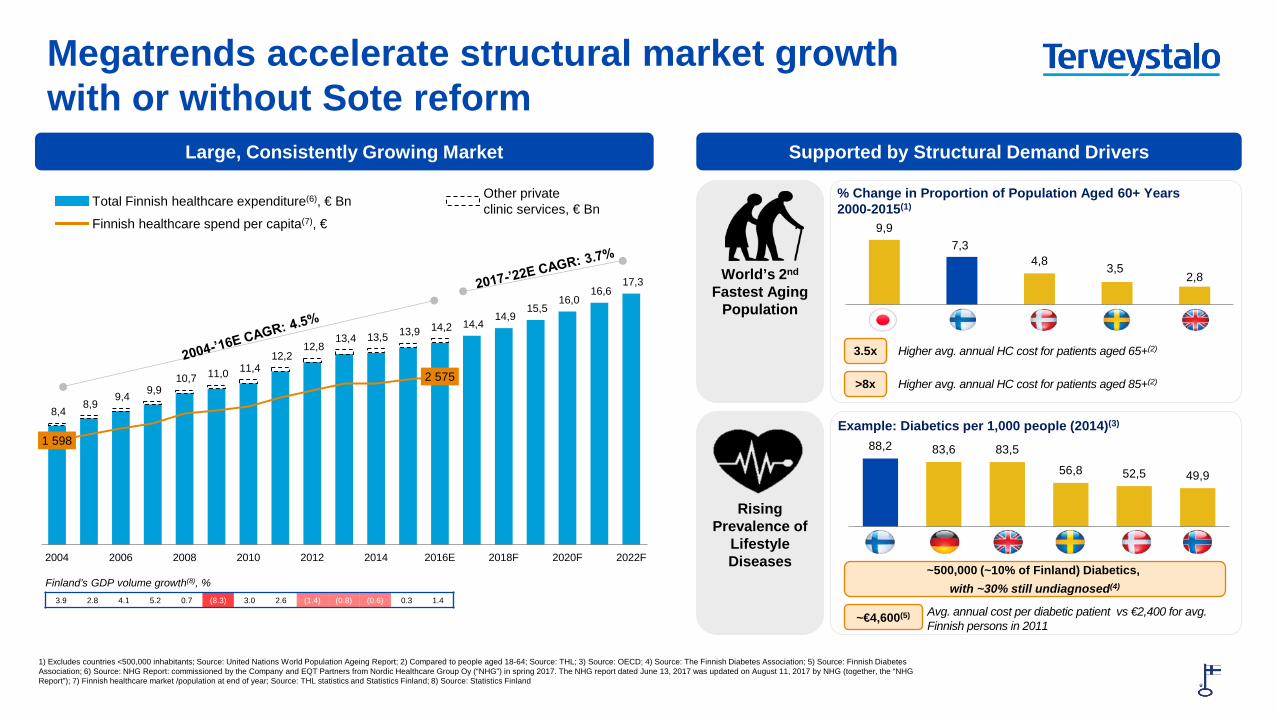

8,4 8,9

9,4 9,9 10,7 11,0 11,4

12,2 12,8

13,4 13,5 13,9 14,2 14,4 14,9

15,5 16,0

16,6 17,3

1 598

2 575

2004 2006 2008 2010 2012 2014 2016E 2018F 2020F 2022F

7

1) Excludes countries <500,000 inhabitants; Source: United Nations World Population Ageing Report; 2) Compared to people aged 18-64; Source: THL; 3) Source: OECD; 4) Source: The Finnish Diabetes Association; 5) Source: Finnish Diabetes Association; 6) Source: NHG Report: commissioned by the Company and EQT Partners from Nordic Healthcare Group Oy (“NHG”) in spring 2017. The NHG report dated June 13, 2017 was updated on August 11, 2017 by NHG (together, the “NHG Report”); 7) Finnish healthcare market /population at end of year; Source: THL statistics and Statistics Finland; 8) Source: Statistics Finland

World’s 2nd Fastest Aging

Population

Rising

Prevalence of Lifestyle Diseases

9,9 7,3

4,8 3,5 2,8

Japan Fin Den Swed UK

% Change in Proportion of Population Aged 60+ Years 2000-2015(1)

3.5x

>8x

Example: Diabetics per 1,000 people (2014)(3)

~500,000 (~10% of Finland) Diabetics, with ~30% still undiagnosed(4)

Avg. annual cost per diabetic patient vs €2,400 for avg. Finnish persons in 2011

~€4,600(5)

88,2 83,6 83,5

56,8 52,5 49,9

Fin Ger UK Swe Den Nor

Higher avg. annual HC cost for patients aged 65+(2)

Higher avg. annual HC cost for patients aged 85+(2)

Megatrends accelerate structural market growth with or without Sote reform

Large, Consistently Growing Market Supported by Structural Demand Drivers

Total Finnish healthcare expenditure(6), € Bn

Finnish healthcare spend per capita(7), €

Finland’s GDP volume growth(8), %

3.9 2.8 4.1 5.2 0.7 (8.3) 3.0 2.6 (1.4) (0.8) (0.6) 0.3 1.4

Other private clinic services, € Bn

© Terveystalo

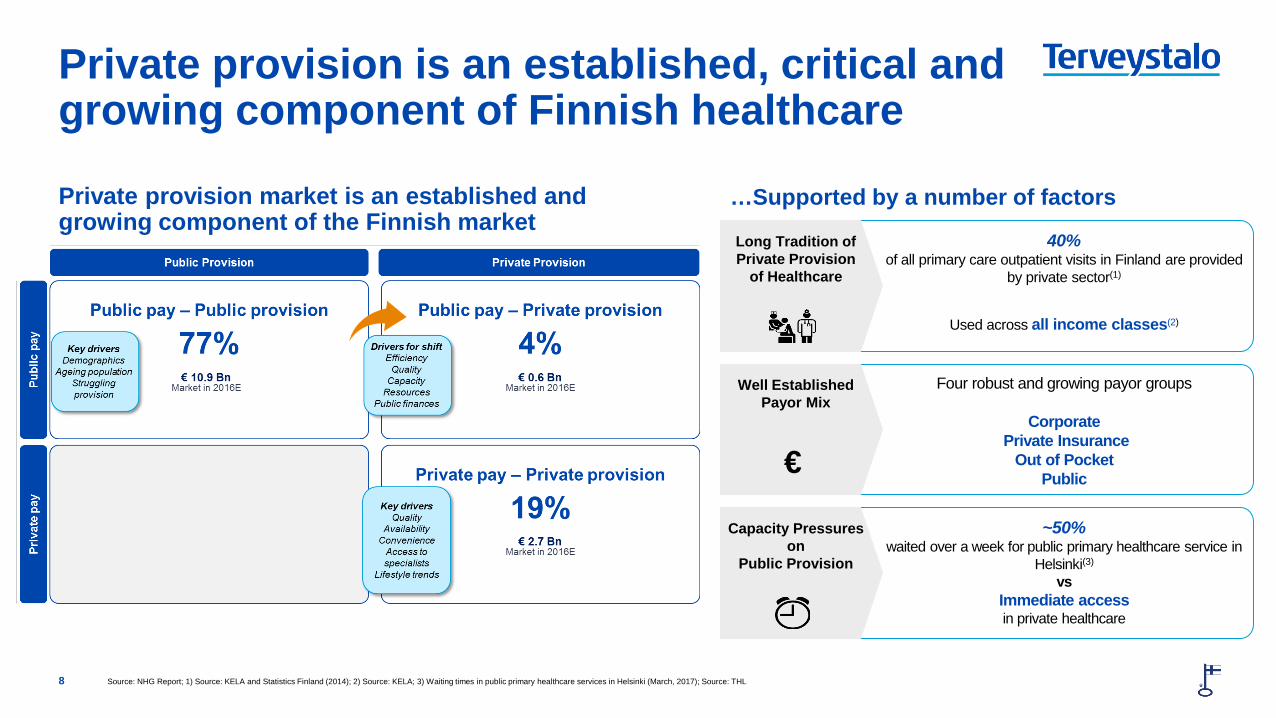

Private provision market is an established and growing component of the Finnish market

…Supported by a number of factors

8

Private provision is an established, critical and growing component of Finnish healthcare

40% of all primary care outpatient visits in Finland are provided

by private sector(1)

Used across all income classes(2)

Long Tradition of Private Provision

of Healthcare

Four robust and growing payor groups

Corporate Private Insurance

Out of Pocket Public

Well Established Payor Mix

~50% waited over a week for public primary healthcare service in

Helsinki(3) vs

Immediate access in private healthcare

Capacity Pressures on

Public Provision

€

Source: NHG Report; 1) Source: KELA and Statistics Finland (2014); 2) Source: KELA; 3) Waiting times in public primary healthcare services in Helsinki (March, 2017); Source: THL

Key trends shaping the market

Polarization of health & exercising habits

Rise of mental wellness

Wellbeing beyond traditional OHC

Value-based corporate wellness programs gaining popularity

11.3.2019 9

Several trends are driving growth in wellbeing services

Source: NHG

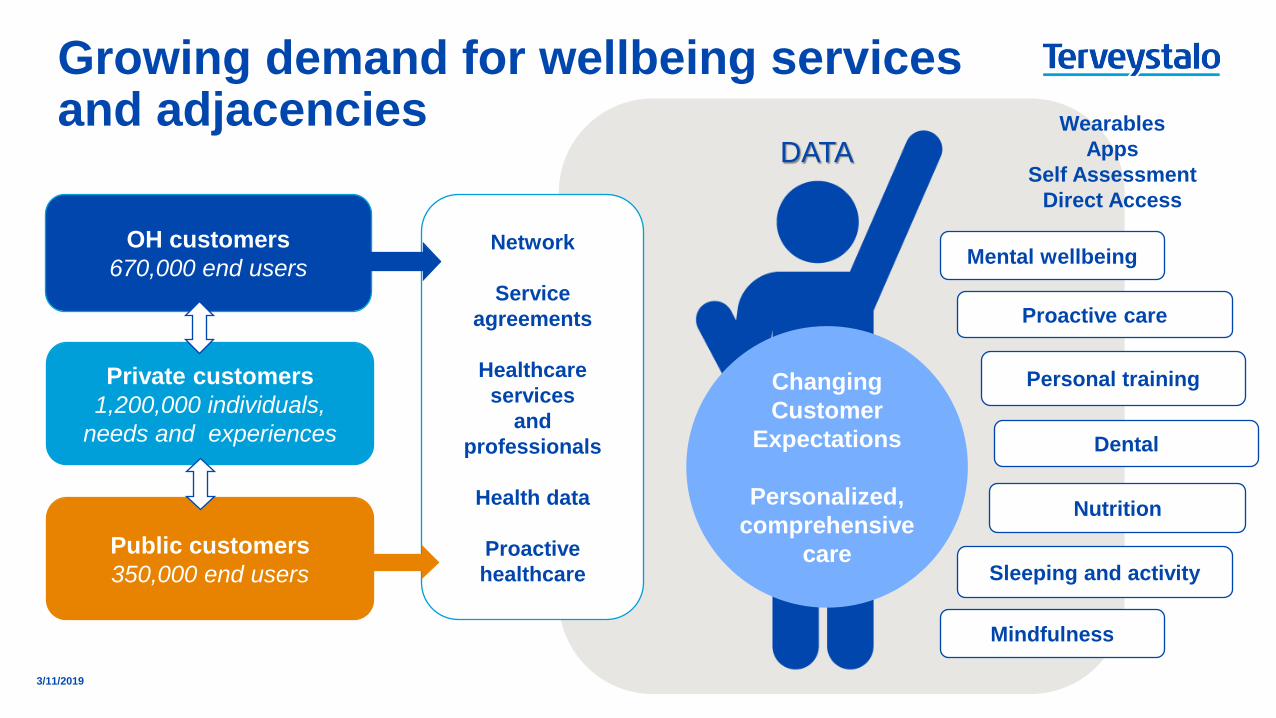

Growing demand for wellbeing services and adjacencies

3/11/2019

OH customers 670,000 end users

Public customers 350,000 end users

Private customers 1,200,000 individuals,

needs and experiences

Network

Service agreements

Healthcare

services and

professionals

Health data

Proactive healthcare

Changing Customer

Expectations

Personalized, comprehensive

care

Dental

Mindfulness

Sleeping and activity

Nutrition

Wearables Apps

Self Assessment Direct Access

Mental wellbeing

Proactive care

Personal training

DATA

© Terveystalo

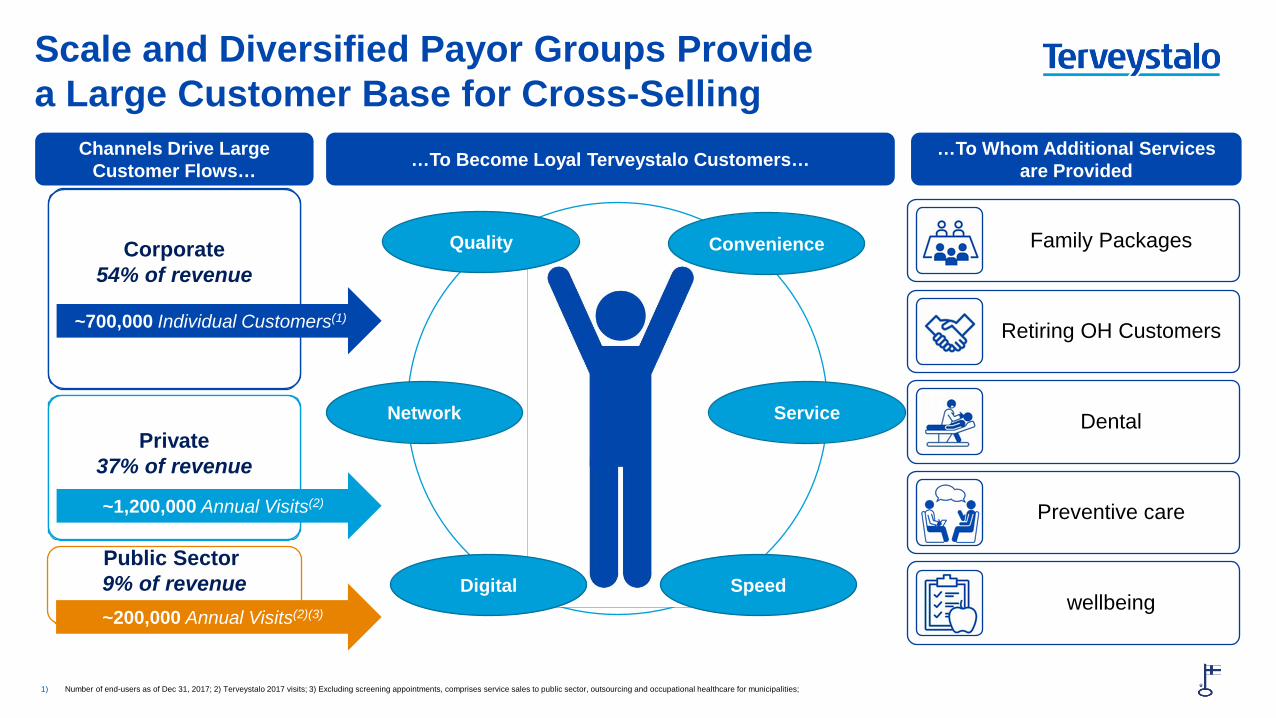

Private 37% of revenue

Public Sector 9% of revenue

Corporate 54% of revenue

Channels Drive Large Customer Flows…

…To Whom Additional Services are Provided …To Become Loyal Terveystalo Customers…

Convenience Quality

Speed Digital

Service Network

~700,000 Individual Customers(1)

~200,000 Annual Visits(2)(3)

~1,200,000 Annual Visits(2)

Family Packages

Retiring OH Customers

Dental

Preventive care

wellbeing

11 1) Number of end-users as of Dec 31, 2017; 2) Terveystalo 2017 visits; 3) Excluding screening appointments, comprises service sales to public sector, outsourcing and occupational healthcare for municipalities;

Scale and Diversified Payor Groups Provide a Large Customer Base for Cross-Selling

© Terveystalo

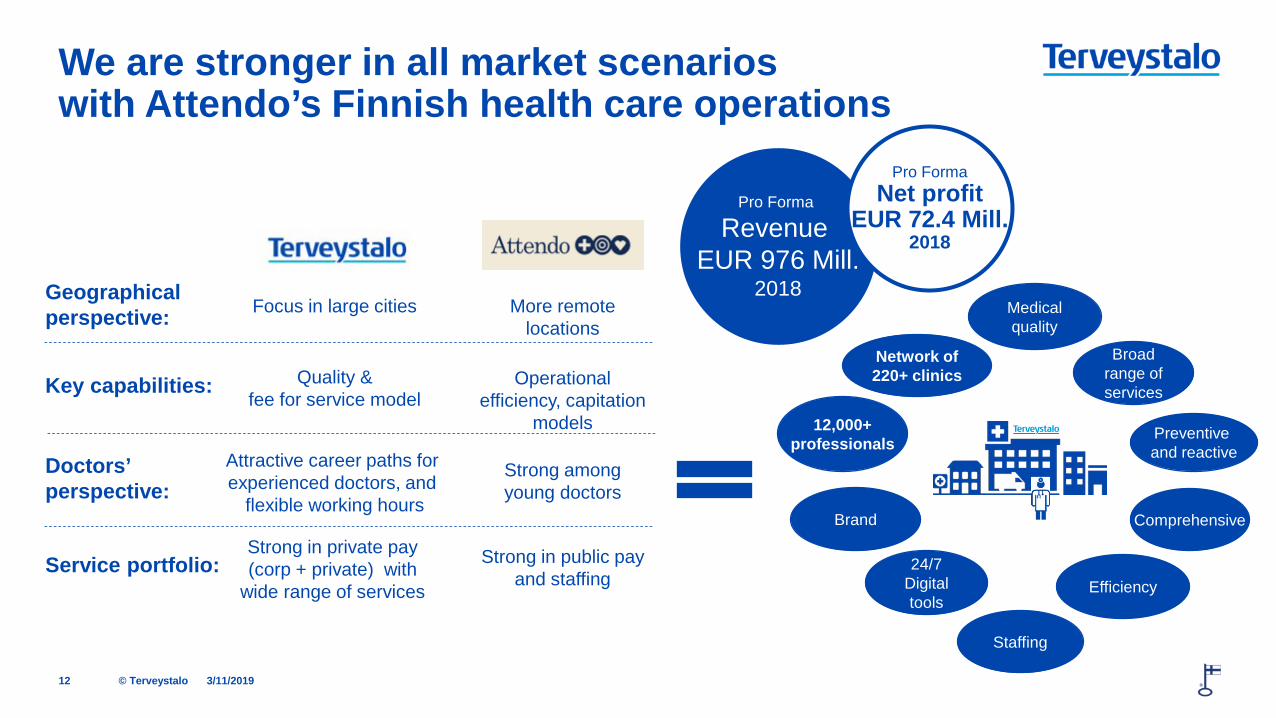

We are stronger in all market scenarios with Attendo’s Finnish health care operations

3/11/2019 12

Geographical perspective:

Key capabilities:

Doctors’ perspective:

Service portfolio:

Focus in large cities More remote locations

Quality & fee for service model

Operational efficiency, capitation

models

Attractive career paths for experienced doctors, and

flexible working hours

Strong among young doctors

Strong in private pay (corp + private) with

wide range of services

Strong in public pay and staffing

Medical quality

Broad range of services

Brand

24/7 Digital tools

Staffing

Efficiency

Preventive and reactive

12,000+ professionals

Comprehensive

Network of 220+ clinics

Pro Forma

Revenue EUR 976 Mill.

2018

Pro Forma Net profit

EUR 72.4 Mill. 2018

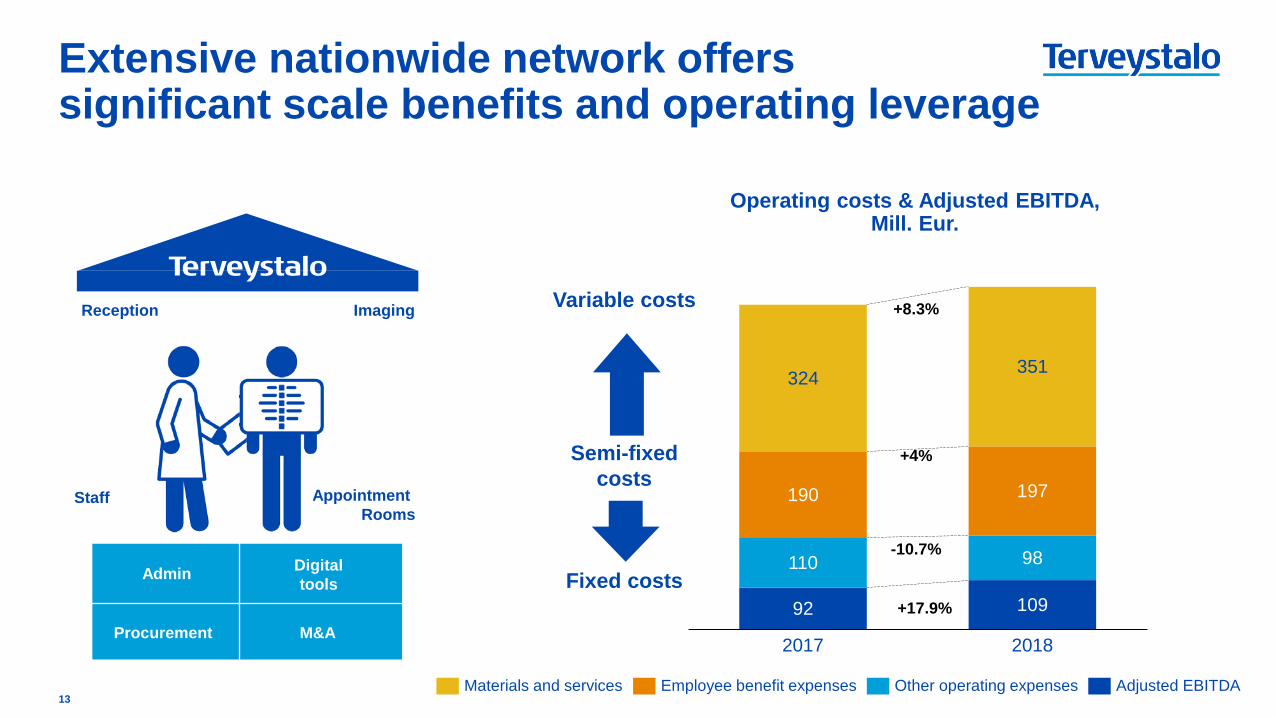

Extensive nationwide network offers significant scale benefits and operating leverage

13

Operating costs & Adjusted EBITDA, Mill. Eur.

Admin

Procurement

Digital tools

M&A

Reception

Staff

Variable costs

Semi-fixed costs

Fixed costs

Appointment Rooms

Imaging

92 109

110 98

190 197

324 351

2018 2017

Materials and services Employee benefit expenses Other operating expenses Adjusted EBITDA

+8.3%

+4%

-10.7%

+17.9%

© Terveystalo

Digitalisation drives superior customer experience, improved medical outcomes and profitability

14

Analysis of Big

Data for Improved Medical Outcomes

Digitalisation for improved cost efficiency

Customer Engagement and Loyalty

Customer Experience & Quality

© Terveystalo

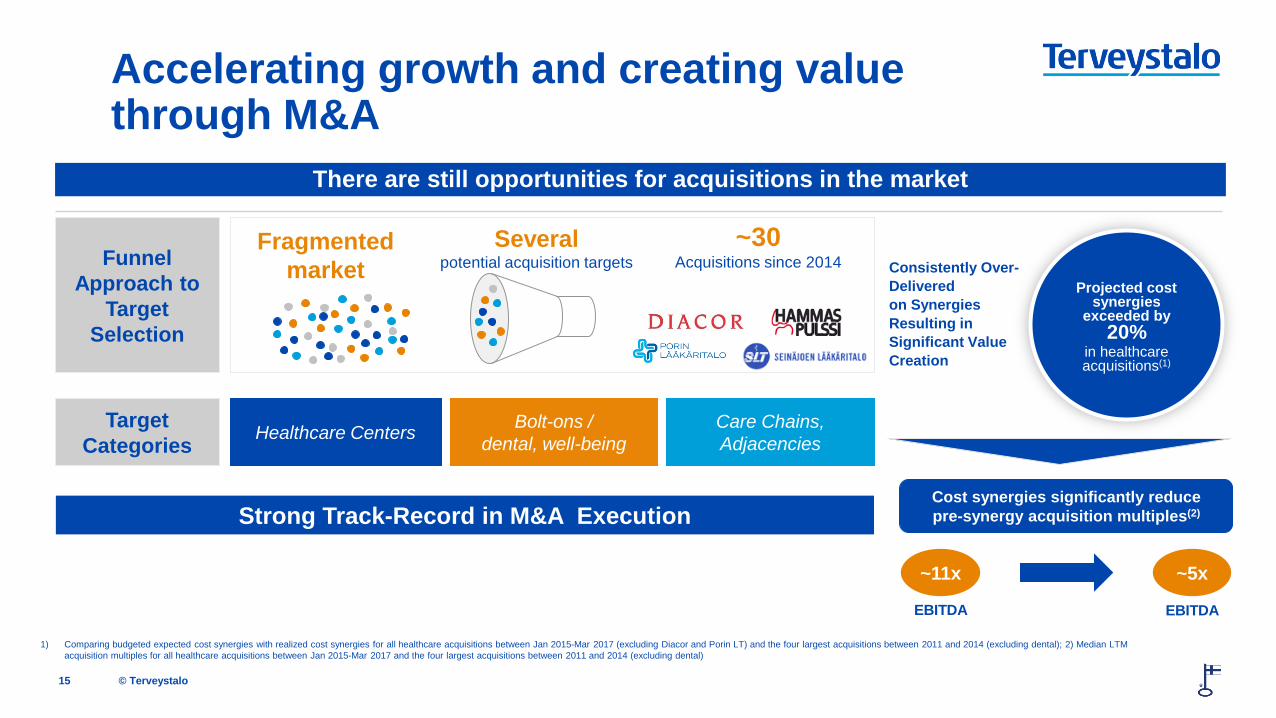

Funnel Approach to

Target Selection

Accelerating growth and creating value through M&A

There are still opportunities for acquisitions in the market

15

Projected cost synergies

exceeded by 20%

in healthcare acquisitions(1)

Target Categories Healthcare Centers Bolt-ons /

dental, well-being Care Chains, Adjacencies

Fragmented

market Several

potential acquisition targets ~30

Acquisitions since 2014

1) Comparing budgeted expected cost synergies with realized cost synergies for all healthcare acquisitions between Jan 2015-Mar 2017 (excluding Diacor and Porin LT) and the four largest acquisitions between 2011 and 2014 (excluding dental); 2) Median LTM acquisition multiples for all healthcare acquisitions between Jan 2015-Mar 2017 and the four largest acquisitions between 2011 and 2014 (excluding dental)

Consistently Over-Delivered on Synergies Resulting in Significant Value Creation

Cost synergies significantly reduce pre-synergy acquisition multiples(2)

~11x ~5x

EBITDA EBITDA

Strong Track-Record in M&A Execution

© Terveystalo

Satisfied customers and professionals

NPS 71 % Appointments

NPS 91 % Hospital services

93 % of employees are satisfied with Terveystalo as a place of work

The most desired employer

© Terveystalo

Integrated Platform with Multiple Avenues for Growth

17

Extensive Network

Large Loyal Customer Base

Customer Oriented Strategy

Preferred Employer

A Frontrunner in Digital Offering

Quality and Brand

Market Growth and Capturing Share

Continued M&A in a Fragmented Market

Aim to Increase Revenue per Customer

• Proven track record of sourcing, integration

and synergy realisation

• Strong structural demand drivers

• Increasing share of private-provision

• Expanding addressable market due to technology

• Loyal customer base with frequent interaction

• Preventive care

• Expanding services to family members

terveystalo.com #terveystalo

2018 HIGHLIGHTS

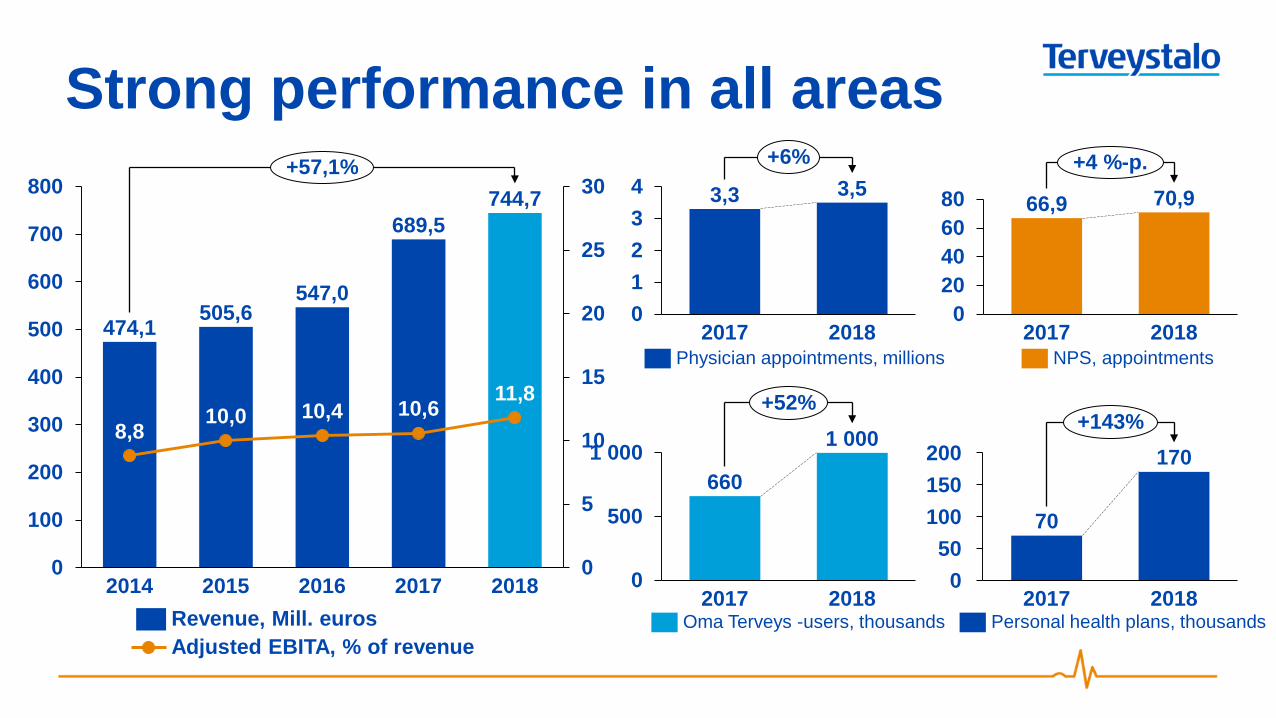

Fifth year of robust growth

Broad scale development across operations

Further investments in digital services

Preventive and well-being services grew at a record pace

Double digit growth in public health care services

474,1 505,6

547,0

689,5 744,7

8,8 10,0 10,4 10,6

11,8

0

5

10

15

20

25

30

0

100

200

300

400

500

600

700

800

2017 2018 2014 2016 2015

+57,1%

Revenue, Mill. euros Adjusted EBITA, % of revenue

3,3 3,5

01234

2017 2018

+6%

Physician appointments, millions

66,9 70,9

020406080

2017 2018

+4 %-p.

NPS, appointments

150

0

200

100 50

2018 2017

70

170 +143%

Personal health plans, thousands

660

1 000

0

500

1 000

2017 2018

+52%

Oma Terveys -users, thousands

Strong performance in all areas

© Terveystalo

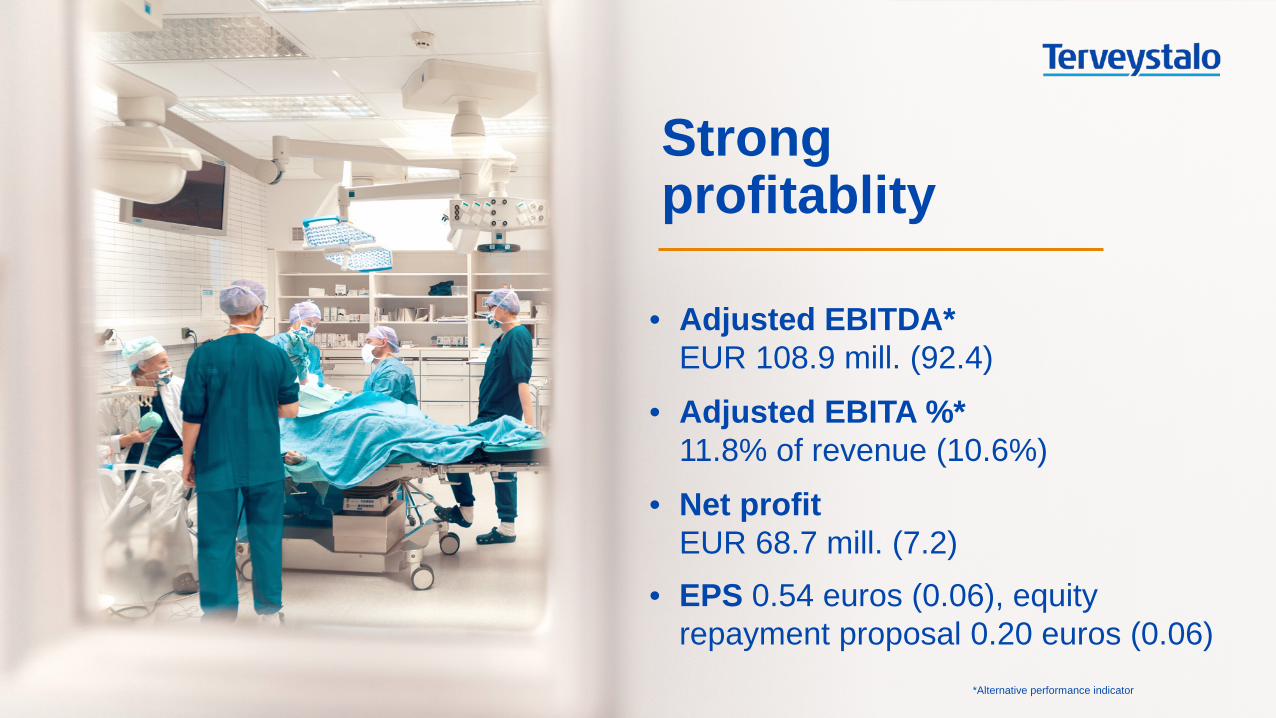

Strong profitablity

• Adjusted EBITDA* EUR 108.9 mill. (92.4)

• Adjusted EBITA %* 11.8% of revenue (10.6%)

• Net profit EUR 68.7 mill. (7.2)

• EPS 0.54 euros (0.06), equity repayment proposal 0.20 euros (0.06)

*Alternative performance indicator

© Terveystalo

Outlook

• Employment and consumer confidence remain at a high level.

• If the health care and social welfare reform is delayed, demand in public outsourcings is expected to grow.

• Should the reform move forward it would enable private service providers to offer publicly funded health center services basically similar to the current services.

• Corporate customers keep up a steady demand, and the relative share of preventive services is increasing.

• Private customer demand remains likewise at a steady level but new capacity on the market decreases Terveystalo’s revenue growth. This capacity growth has reached its peak, however.

11.3.2019 21

terveystalo.com #terveystalo

Q & A

terveystalo.com #terveystalo

FINANCIAL PERFORMANCE

• Steady demand in the corporate and private customer groups. • Increased clinic and hospital capacity in private health care

has created intense competition, especially in Finland’s major cities, with the exception of the Helsinki metropolitan area.

• Significant capacity growth has stalled, however, and the demand for Terveystalo’s services has remained strong.

• The Government proposal on the health care and social welfare reform is still being reviewed by the Constitutional Law Committee.

• If the health care and social welfare reform is delayed, demand in public outsourcings is expected to grow.

• Should the reform move forward it would enable private service providers to offer publicly funded health center services basically similar to the current services.

11.3.2019 24

Market review

© Terveystalo

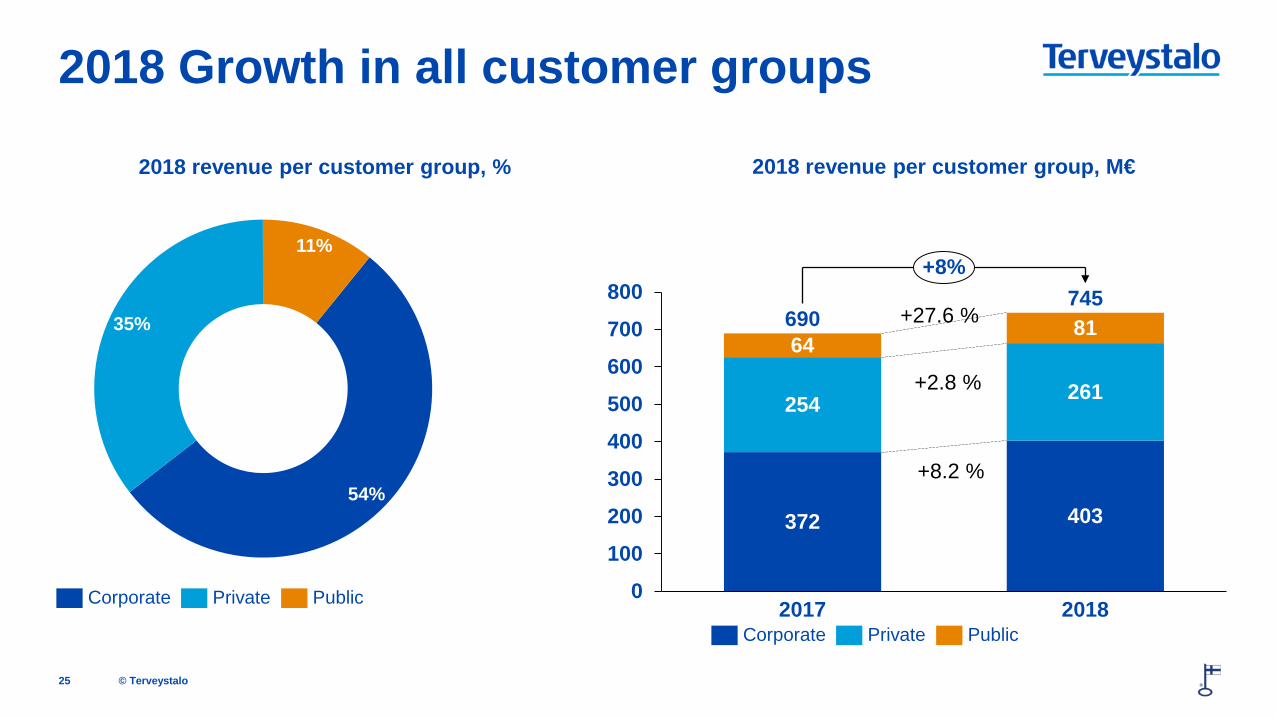

© Terveystalo

2018 revenue per customer group, M€

25

2018 Growth in all customer groups

372 403

254 261

64 81

0

100

200

300

400

500

600

700

800

2018 2017

690 745

+8%

Corporate Private Public

+27.6 %

+2.8 %

+8.2 % 54%

35%

11%

Corporate Private Public

2018 revenue per customer group, %

© Terveystalo

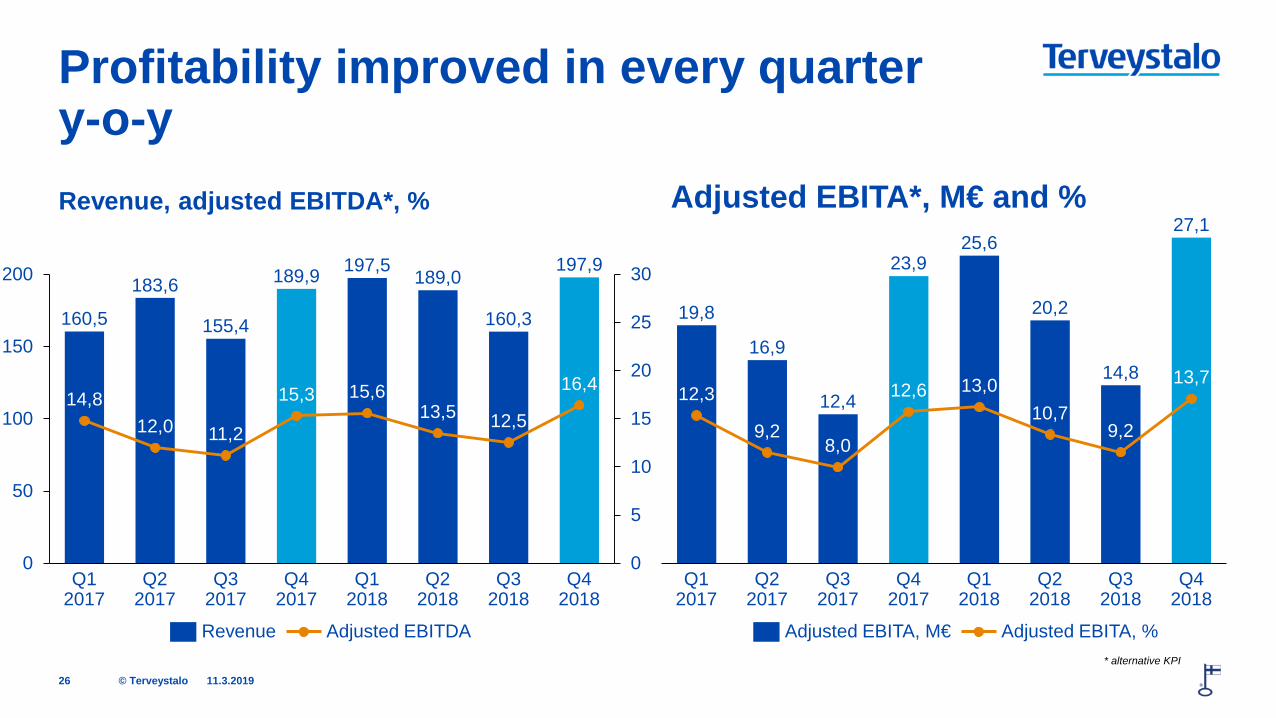

Revenue, adjusted EBITDA*, % Adjusted EBITA*, M€ and %

11.3.2019 26

Profitability improved in every quarter y-o-y

160,5

183,6

155,4

189,9 197,5 189,0

160,3

197,9

14,8 12,0 11,2

15,3 15,6 13,5 12,5

16,4

0

5

10

15

20

25

30

0

50

100

150

200

Q1 2018

Q1 2017

Q4 2017

Q3 2017

Q2 2017

Q4 2018

Q2 2018

Q3 2018

Adjusted EBITDA Revenue

19,8

16,9

12,4

23,9 25,6

20,2

14,8

27,1

12,3

9,2 8,0

12,6 13,0 10,7

9,2

13,7

Q2 2017

Q1 2017

Q3 2017

Q4 2017

Q4 2018

Q2 2018

Q1 2018

Q3 2018

Adjusted EBITA, M€ Adjusted EBITA, % * alternative KPI

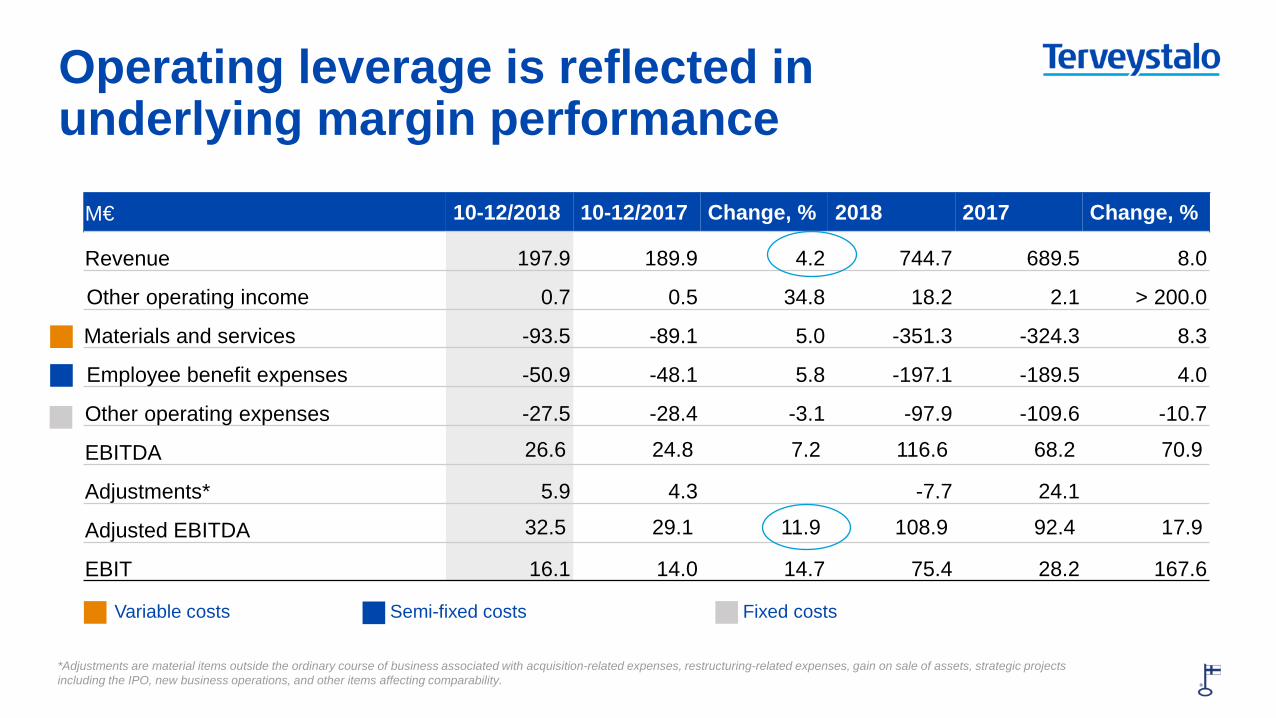

© Terveystalo

Operating leverage is reflected in underlying margin performance

M€ 10-12/2018 10-12/2017 Change, % 2018 2017 Change, %

Revenue 197.9 189.9 4.2 744.7 689.5 8.0

Other operating income 0.7 0.5 34.8 18.2 2.1 > 200.0

Materials and services -93.5 -89.1 5.0 -351.3 -324.3 8.3

Employee benefit expenses -50.9 -48.1 5.8 -197.1 -189.5 4.0

Other operating expenses -27.5 -28.4 -3.1 -97.9 -109.6 -10.7

EBITDA 26.6 24.8 7.2 116.6 68.2 70.9

Adjustments* 5.9 4.3 -7.7 24.1

Adjusted EBITDA 32.5 29.1 11.9 108.9 92.4 17.9

EBIT 16.1 14.0 14.7 75.4 28.2 167.6

11.3.2019 27 27

Group P&L *Adjustments are material items outside the ordinary course of business associated with acquisition-related expenses, restructuring-related expenses, gain on sale of assets, strategic projects including the IPO, new business operations, and other items affecting comparability.

Variable costs Fixed costs Semi-fixed costs

© Terveystalo

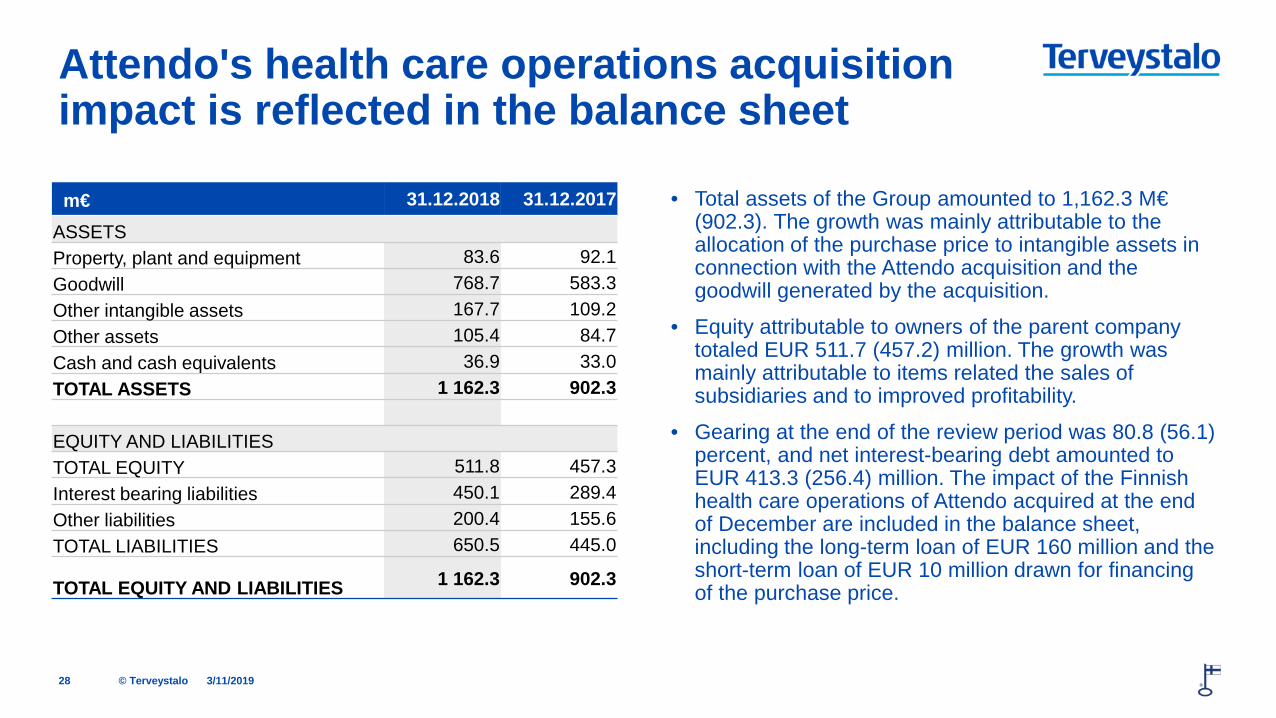

Attendo's health care operations acquisition impact is reflected in the balance sheet

m€ 31.12.2018 31.12.2017

ASSETS Property, plant and equipment 83.6 92.1 Goodwill 768.7 583.3 Other intangible assets 167.7 109.2 Other assets 105.4 84.7 Cash and cash equivalents 36.9 33.0 TOTAL ASSETS 1 162.3 902.3

EQUITY AND LIABILITIES TOTAL EQUITY 511.8 457.3 Interest bearing liabilities 450.1 289.4 Other liabilities 200.4 155.6 TOTAL LIABILITIES 650.5 445.0

TOTAL EQUITY AND LIABILITIES 1 162.3 902.3

• Total assets of the Group amounted to 1,162.3 M€ (902.3). The growth was mainly attributable to the allocation of the purchase price to intangible assets in connection with the Attendo acquisition and the goodwill generated by the acquisition.

• Equity attributable to owners of the parent company totaled EUR 511.7 (457.2) million. The growth was mainly attributable to items related the sales of subsidiaries and to improved profitability.

• Gearing at the end of the review period was 80.8 (56.1) percent, and net interest-bearing debt amounted to EUR 413.3 (256.4) million. The impact of the Finnish health care operations of Attendo acquired at the end of December are included in the balance sheet, including the long-term loan of EUR 160 million and the short-term loan of EUR 10 million drawn for financing of the purchase price.

3/11/2019 28

© Terveystalo

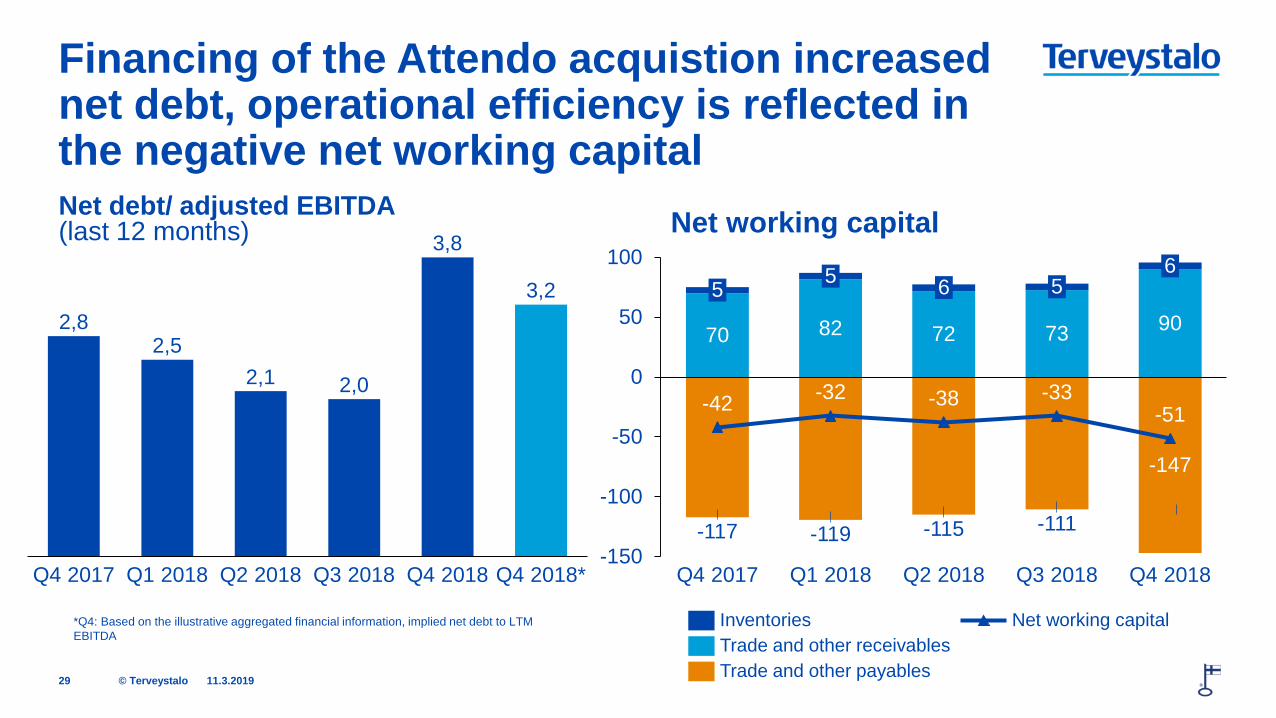

Net debt/ adjusted EBITDA (last 12 months) Net working capital

11.3.2019 29

Financing of the Attendo acquistion increased net debt, operational efficiency is reflected in the negative net working capital

70 82 72 73 90

-117 -119 -115 -111

-147

-42 -32 -38 -33 -51

-150

-100

-50

0

50

1005 5 6

Q4 2017 Q1 2018 Q2 2018

5

Q3 2018

6

Q4 2018

Trade and other payables

Inventories Trade and other receivables

Net working capital *Q4: Based on the illustrative aggregated financial information, implied net debt to LTM EBITDA

2,8 2,5

2,1 2,0

3,8

3,2

Q4 2017 Q1 2018 Q2 2018 Q4 2018 Q3 2018 Q4 2018*

© Terveystalo

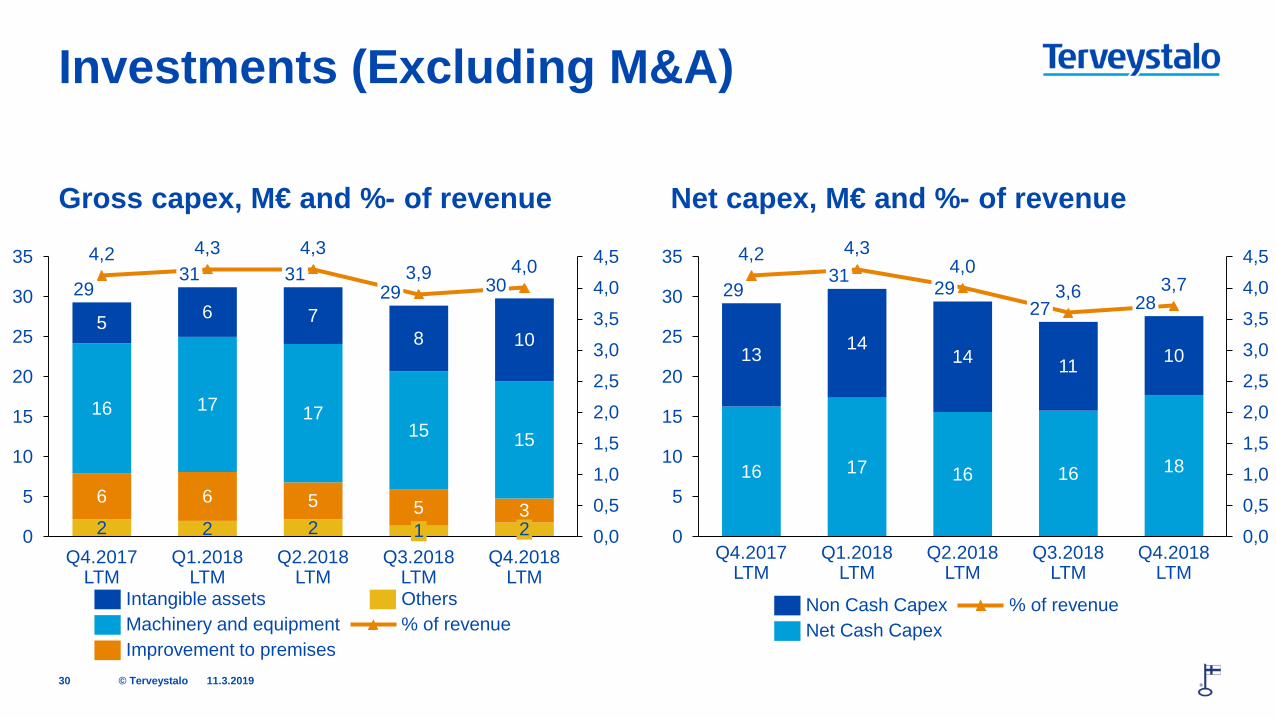

Gross capex, M€ and %- of revenue Net capex, M€ and %- of revenue

11.3.2019 30

Investments (Excluding M&A)

2 2 2

6 6 5 5 3

16 17 17 15 15

5 6 7 8 10

4,2 4,3 4,3 3,9 4,0

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

0

5

10

15

20

25

30

35

Q1.2018 LTM

30

Q4.2017 LTM

1 Q2.2018

LTM Q3.2018

LTM

31

2 Q4.2018

LTM

29 31

29

% of revenue Machinery and equipment Intangible assets

Improvement to premises

Others

16 17 16 16 18

13 14 14 11 10

4,2 4,3 4,0

3,6 3,7

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

0

5

10

15

20

25

30

35

Q4.2018 LTM

Q4.2017 LTM

Q2.2018 LTM

Q1.2018 LTM

Q3.2018 LTM

29 31

29 27 28

Non Cash Capex Net Cash Capex

% of revenue

© Terveystalo

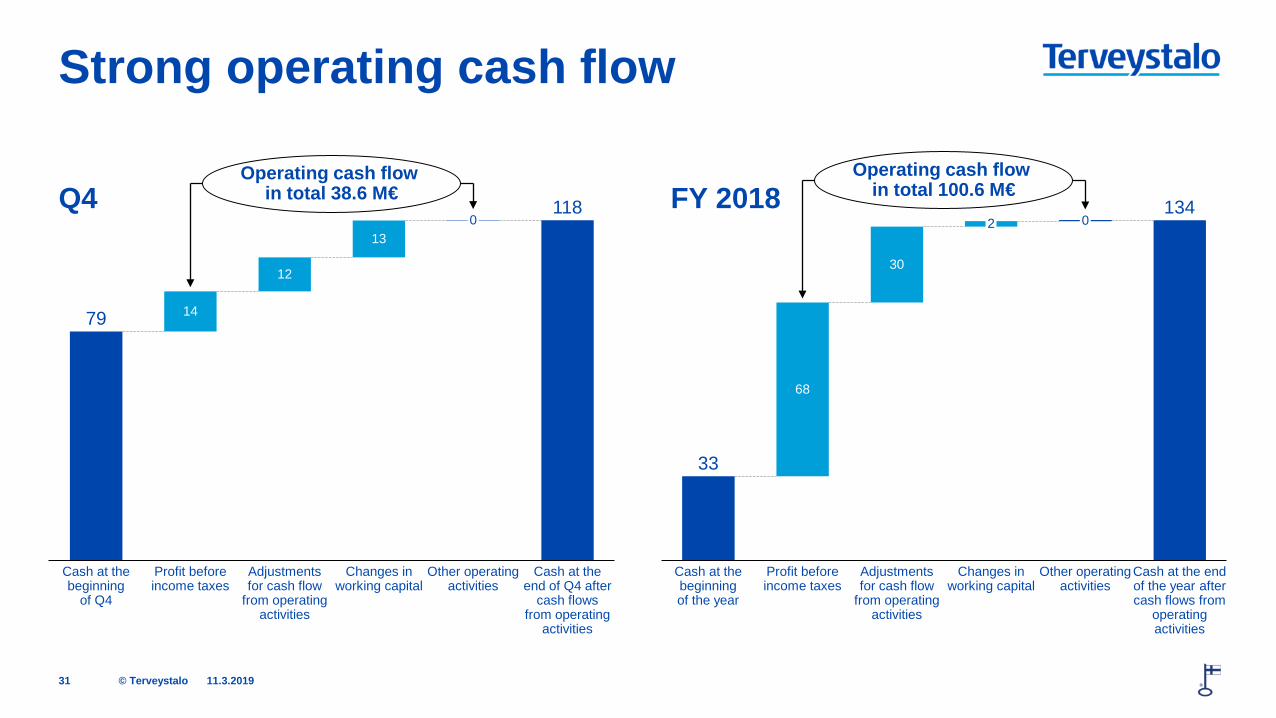

Q4 FY 2018

11.3.2019 31

Strong operating cash flow

79

118

14

12

13

Changes in working capital

Profit before income taxes

Cash at the beginning

of Q4

Cash at the end of Q4 after

cash flows from operating

activities

Adjustments for cash flow

from operating activities

0

Other operating activities

Operating cash flow in total 38.6 M€

33

134

68

30

Changes in working capital

Other operating activities

2

Cash at the beginning of the year

Profit before income taxes

Adjustments for cash flow

from operating activities

0

Cash at the end of the year after cash flows from

operating activities

Operating cash flow in total 100.6 M€

© Terveystalo

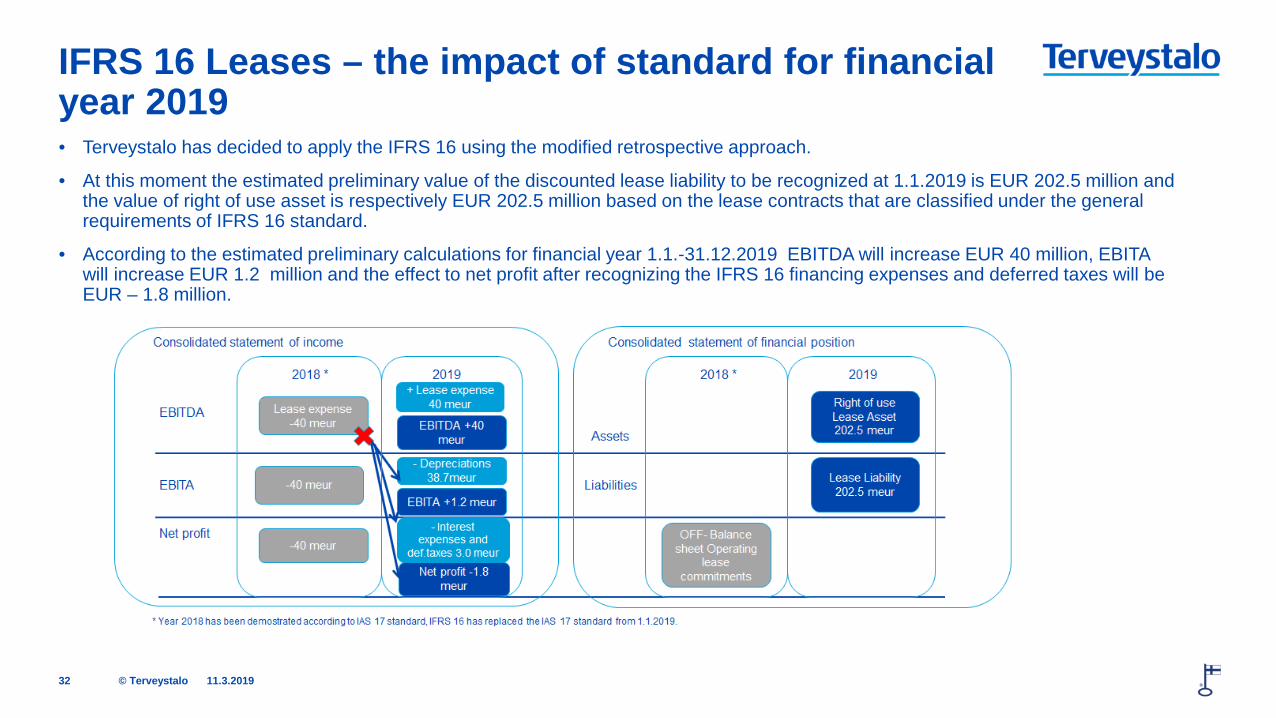

IFRS 16 Leases – the impact of standard for financial year 2019

11.3.2019 32

• Terveystalo has decided to apply the IFRS 16 using the modified retrospective approach.

• At this moment the estimated preliminary value of the discounted lease liability to be recognized at 1.1.2019 is EUR 202.5 million and the value of right of use asset is respectively EUR 202.5 million based on the lease contracts that are classified under the general requirements of IFRS 16 standard.

• According to the estimated preliminary calculations for financial year 1.1.-31.12.2019 EBITDA will increase EUR 40 million, EBITA will increase EUR 1.2 million and the effect to net profit after recognizing the IFRS 16 financing expenses and deferred taxes will be EUR – 1.8 million.

terveystalo.com #terveystalo

APPENDIX SLIDES

© Terveystalo

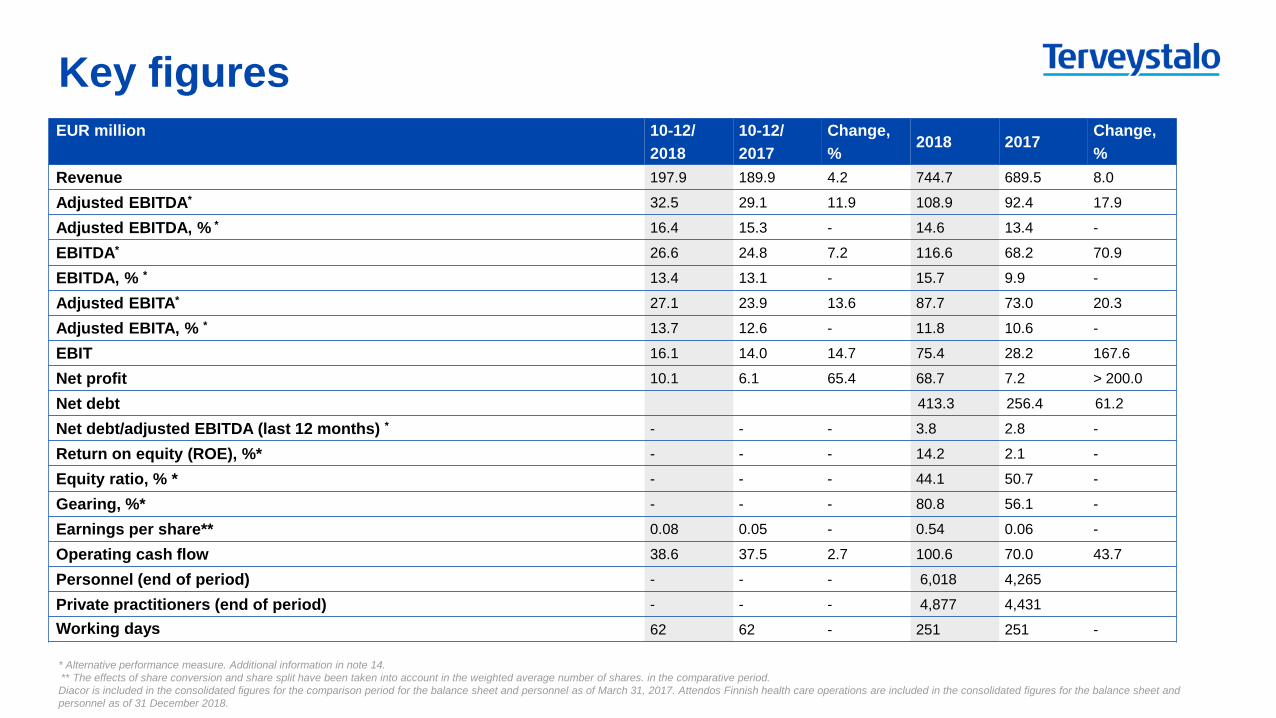

Key figures

3/11/2019 34 * Alternative performance measure. Additional information in note 14. ** The effects of share conversion and share split have been taken into account in the weighted average number of shares. in the comparative period. Diacor is included in the consolidated figures for the comparison period for the balance sheet and personnel as of March 31, 2017. Attendos Finnish health care operations are included in the consolidated figures for the balance sheet and personnel as of 31 December 2018.

EUR million 10-12/ 2018

10-12/ 2017

Change, %

2018 2017 Change, %

Revenue 197.9 189.9 4.2 744.7 689.5 8.0

Adjusted EBITDA* 32.5 29.1 11.9 108.9 92.4 17.9

Adjusted EBITDA, % * 16.4 15.3 - 14.6 13.4 -

EBITDA* 26.6 24.8 7.2 116.6 68.2 70.9

EBITDA, % * 13.4 13.1 - 15.7 9.9 -

Adjusted EBITA* 27.1 23.9 13.6 87.7 73.0 20.3

Adjusted EBITA, % * 13.7 12.6 - 11.8 10.6 -

EBIT 16.1 14.0 14.7 75.4 28.2 167.6

Net profit 10.1 6.1 65.4 68.7 7.2 > 200.0

Net debt 413.3 256.4 61.2

Net debt/adjusted EBITDA (last 12 months) * - - - 3.8 2.8 -

Return on equity (ROE), %* - - - 14.2 2.1 -

Equity ratio, % * - - - 44.1 50.7 -

Gearing, %* - - - 80.8 56.1 -

Earnings per share** 0.08 0.05 - 0.54 0.06 -

Operating cash flow 38.6 37.5 2.7 100.6 70.0 43.7

Personnel (end of period) - - - 6,018 4,265

Private practitioners (end of period) - - - 4,877 4,431

Working days 62 62 - 251 251 -

© Terveystalo

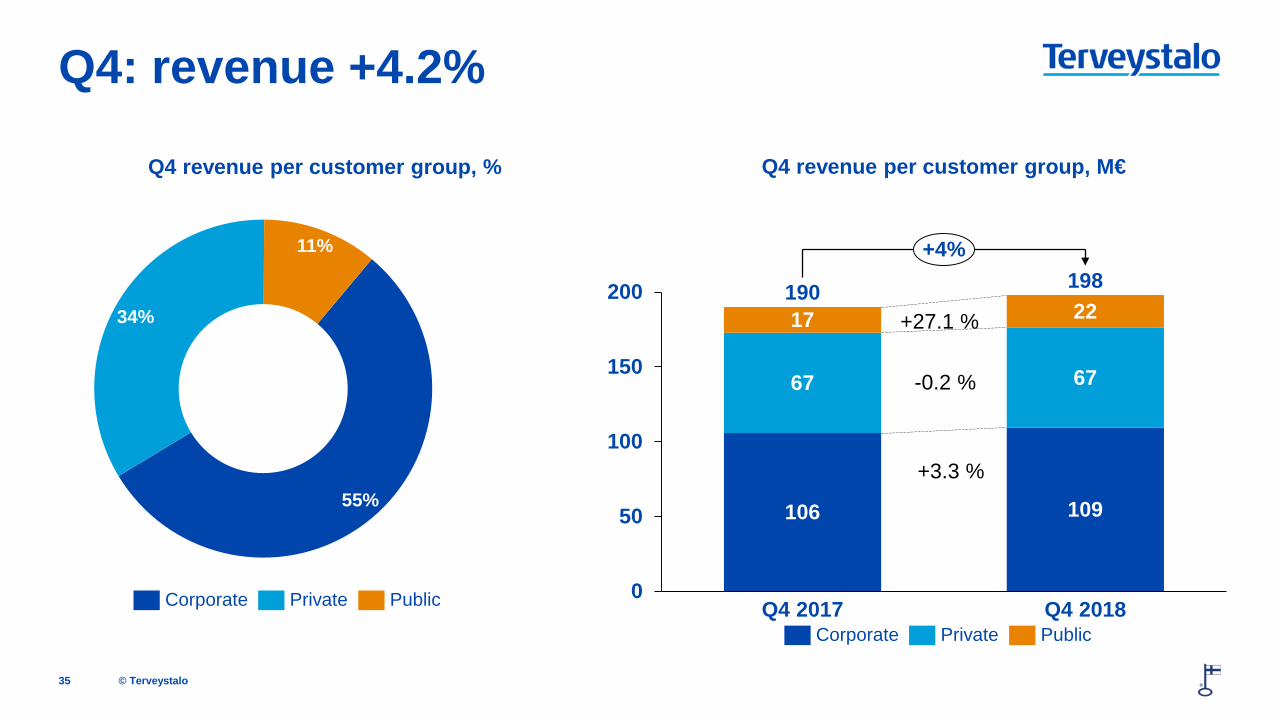

Q4 revenue per customer group, M€

35

Q4: revenue +4.2%

106 109

67 67

17 22

0

50

100

150

200

Q4 2017 Q4 2018

190 198 +4%

Corporate Public Private

+27.1 %

-0.2 %

+3.3 % 55%

34%

11%

Corporate Private Public

Q4 revenue per customer group, %

© Terveystalo

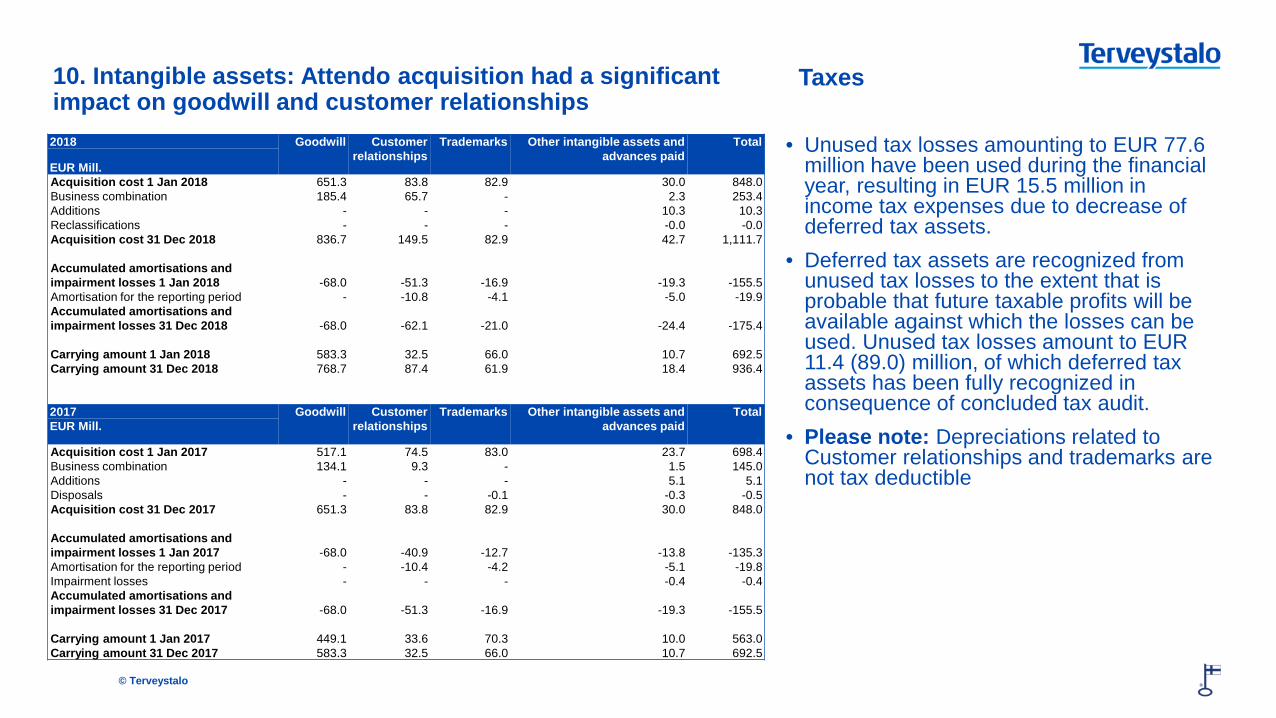

2018 Goodwill Customer relationships

Trademarks Other intangible assets and advances paid

Total

EUR Mill. Acquisition cost 1 Jan 2018 651.3 83.8 82.9 30.0 848.0 Business combination 185.4 65.7 - 2.3 253.4 Additions - - - 10.3 10.3 Reclassifications - - - -0.0 -0.0 Acquisition cost 31 Dec 2018 836.7 149.5 82.9 42.7 1,111.7 Accumulated amortisations and impairment losses 1 Jan 2018 -68.0 -51.3 -16.9 -19.3 -155.5 Amortisation for the reporting period - -10.8 -4.1 -5.0 -19.9 Accumulated amortisations and impairment losses 31 Dec 2018 -68.0 -62.1 -21.0 -24.4 -175.4 Carrying amount 1 Jan 2018 583.3 32.5 66.0 10.7 692.5 Carrying amount 31 Dec 2018 768.7 87.4 61.9 18.4 936.4 2017 Goodwill Customer

relationships Trademarks Other intangible assets and

advances paid Total

EUR Mill.

Acquisition cost 1 Jan 2017 517.1 74.5 83.0 23.7 698.4 Business combination 134.1 9.3 - 1.5 145.0 Additions - - - 5.1 5.1 Disposals - - -0.1 -0.3 -0.5 Acquisition cost 31 Dec 2017 651.3 83.8 82.9 30.0 848.0 Accumulated amortisations and impairment losses 1 Jan 2017 -68.0 -40.9 -12.7 -13.8 -135.3 Amortisation for the reporting period - -10.4 -4.2 -5.1 -19.8 Impairment losses - - - -0.4 -0.4 Accumulated amortisations and impairment losses 31 Dec 2017 -68.0 -51.3 -16.9 -19.3 -155.5 Carrying amount 1 Jan 2017 449.1 33.6 70.3 10.0 563.0 Carrying amount 31 Dec 2017 583.3 32.5 66.0 10.7 692.5

10. Intangible assets: Attendo acquisition had a significant impact on goodwill and customer relationships

Taxes

• Unused tax losses amounting to EUR 77.6 million have been used during the financial year, resulting in EUR 15.5 million in income tax expenses due to decrease of deferred tax assets.

• Deferred tax assets are recognized from unused tax losses to the extent that is probable that future taxable profits will be available against which the losses can be used. Unused tax losses amount to EUR 11.4 (89.0) million, of which deferred tax assets has been fully recognized in consequence of concluded tax audit.

• Please note: Depreciations related to Customer relationships and trademarks are not tax deductible

© Terveystalo

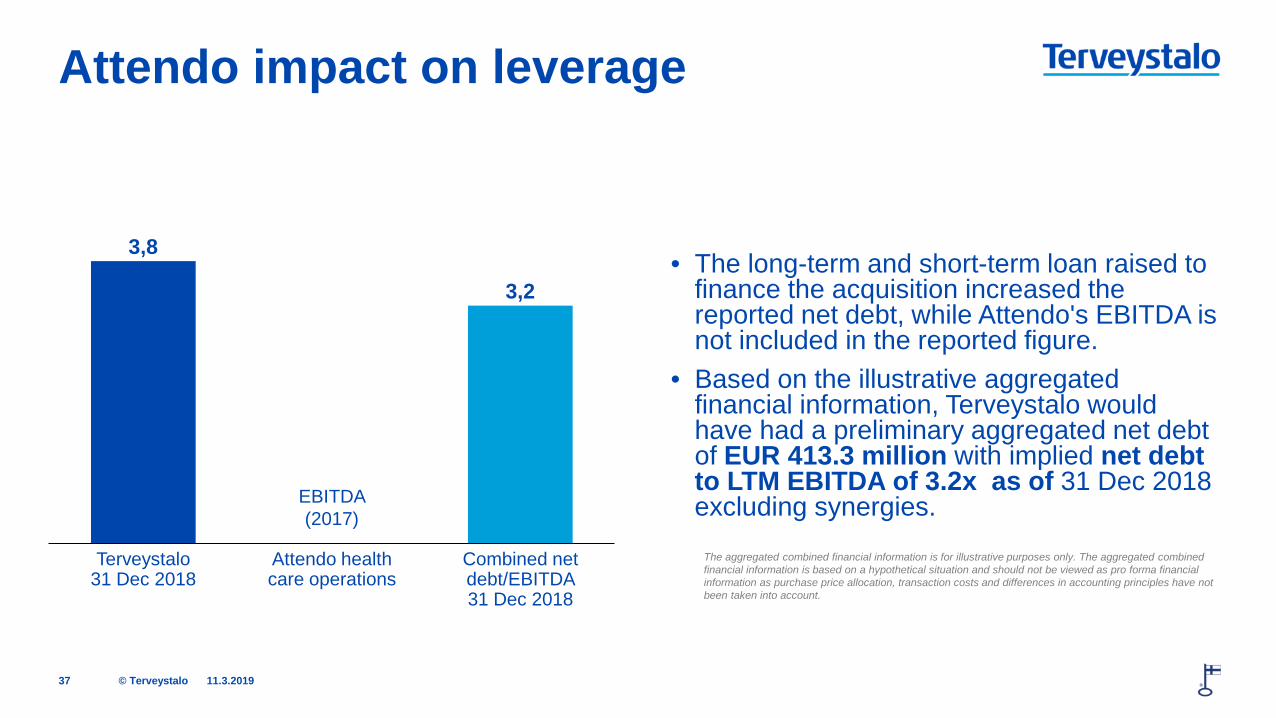

• The long-term and short-term loan raised to finance the acquisition increased the reported net debt, while Attendo's EBITDA is not included in the reported figure.

• Based on the illustrative aggregated financial information, Terveystalo would have had a preliminary aggregated net debt of EUR 413.3 million with implied net debt to LTM EBITDA of 3.2x as of 31 Dec 2018 excluding synergies.

11.3.2019 37

Attendo impact on leverage

The aggregated combined financial information is for illustrative purposes only. The aggregated combined financial information is based on a hypothetical situation and should not be viewed as pro forma financial information as purchase price allocation, transaction costs and differences in accounting principles have not been taken into account.

3,8

3,2

Attendo health care operations

Terveystalo 31 Dec 2018

Combined net debt/EBITDA 31 Dec 2018

EBITDA (2017)

© Terveystalo

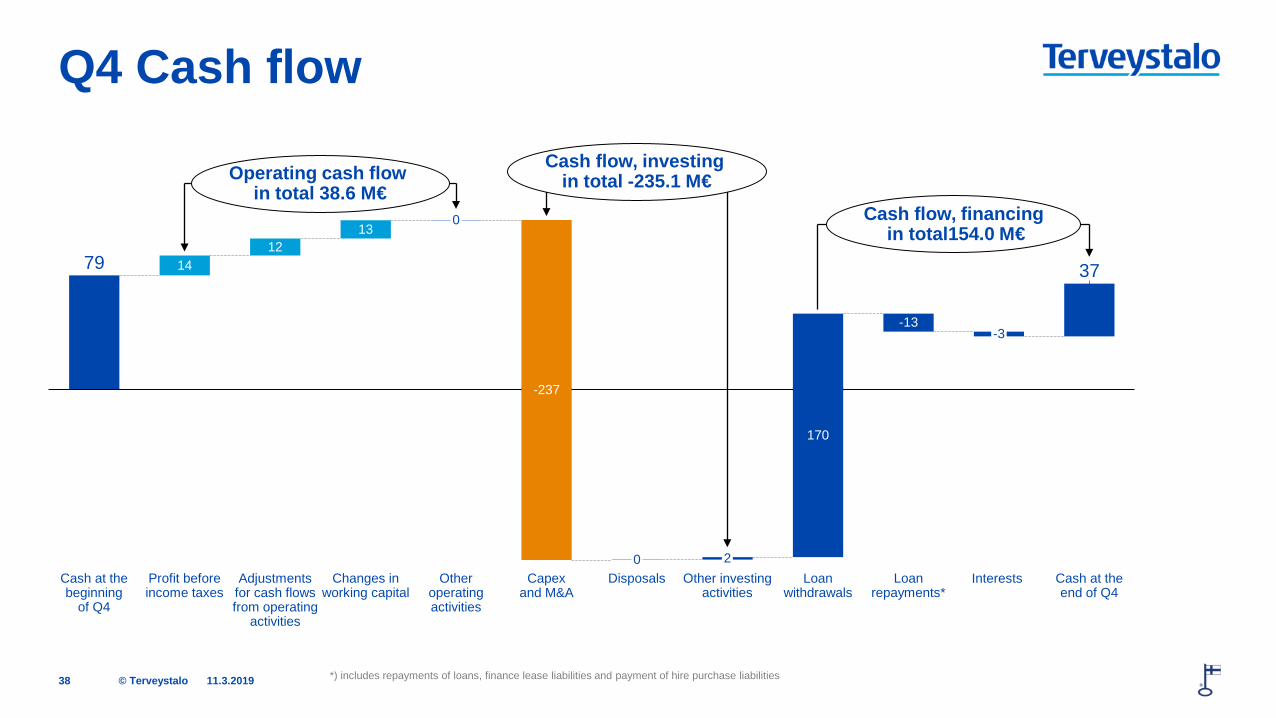

Q4 Cash flow

11.3.2019 38

79 14 12

13

37

-3 -13

Interests Loan withdrawals

Other investing activities

2 0 Cash at the end of Q4

Capex and M&A

-237

170

Other operating activities

Disposals Changes in working capital

0

Adjustments for cash flows from operating

activities

Cash at the beginning

of Q4

Profit before income taxes

Loan repayments*

Operating cash flow in total 38.6 M€

Cash flow, investing in total -235.1 M€

Cash flow, financing in total154.0 M€

*) includes repayments of loans, finance lease liabilities and payment of hire purchase liabilities

© Terveystalo

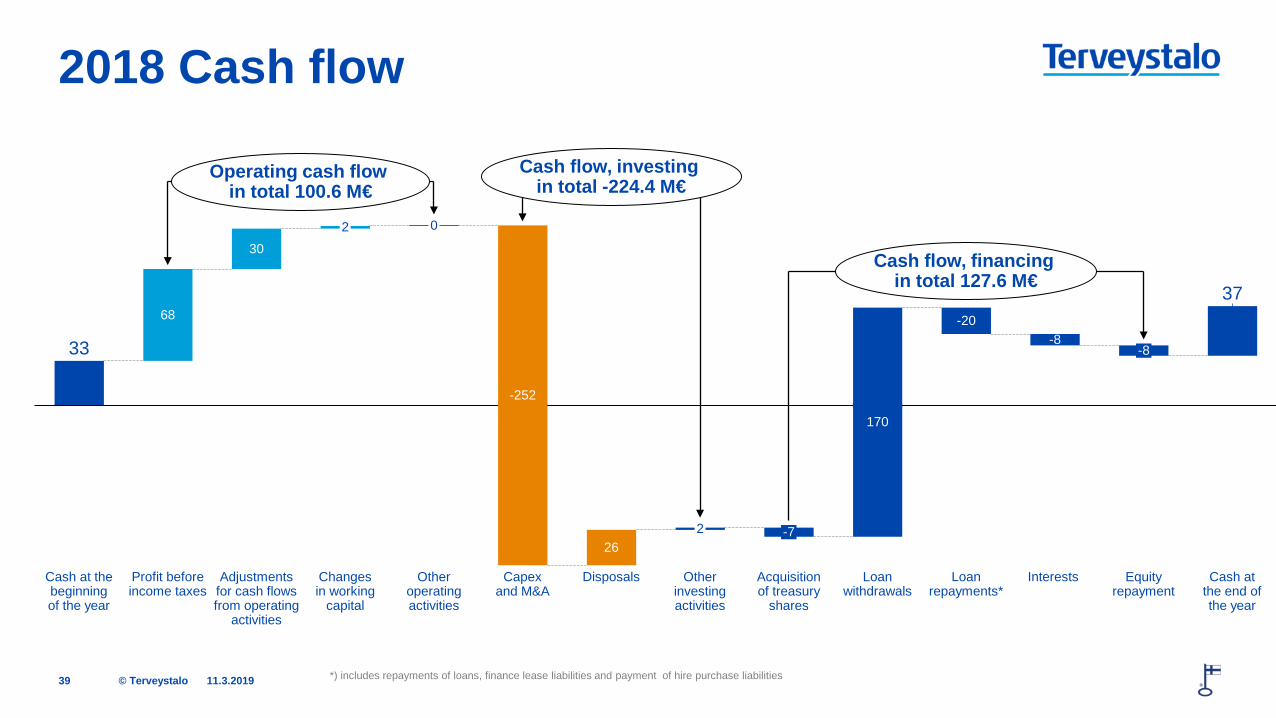

2018 Cash flow

11.3.2019 39

33

68

30

37

0

-252

Capex and M&A

26

170

Other investing activities

Loan withdrawals

-20

Loan repayments*

-8

Interests

-8

Equity repayment

2

Cash at the beginning of the year

Adjustments for cash flows from operating

activities

Profit before income taxes

2

Acquisition of treasury

shares

Changes in working

capital

Disposals

-7

Other operating activities

Cash at the end of the year

Operating cash flow in total 100.6 M€

Cash flow, investing in total -224.4 M€

Cash flow, financing in total 127.6 M€

*) includes repayments of loans, finance lease liabilities and payment of hire purchase liabilities

© Terveystalo

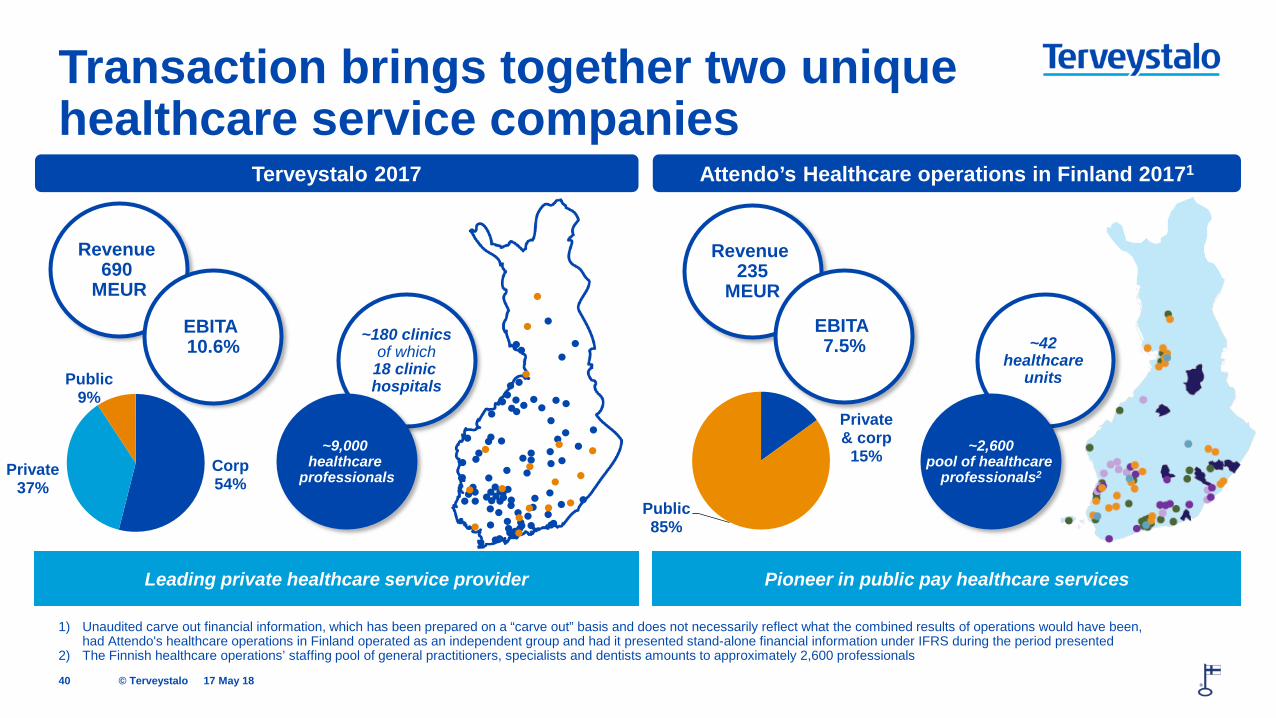

Transaction brings together two unique healthcare service companies

40

1) Unaudited carve out financial information, which has been prepared on a “carve out” basis and does not necessarily reflect what the combined results of operations would have been, had Attendo's healthcare operations in Finland operated as an independent group and had it presented stand-alone financial information under IFRS during the period presented

2) The Finnish healthcare operations’ staffing pool of general practitioners, specialists and dentists amounts to approximately 2,600 professionals

Terveystalo 2017

Corp 54%

Private37%

Public 9%

Revenue 690

MEUR

~180 clinics of which

18 clinic hospitals

~9,000 healthcare

professionals

Revenue 235

MEUR

Attendo’s Healthcare operations in Finland 20171

~42 healthcare

units

~2,600 pool of healthcare

professionals2

Leading private healthcare service provider Pioneer in public pay healthcare services

EBITA 10.6%

EBITA 7.5%

Private & corp

15%

Public 85%

17 May 18

© Terveystalo

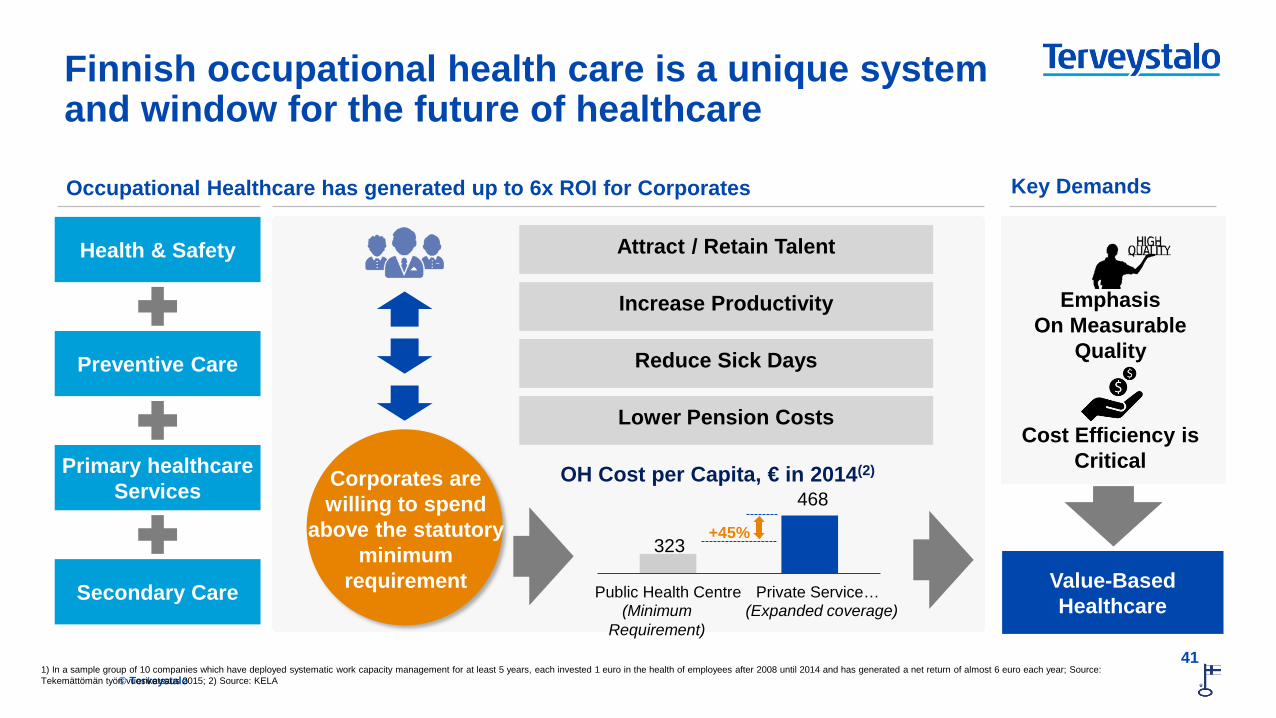

Finnish occupational health care is a unique system and window for the future of healthcare

Attract / Retain Talent

Increase Productivity

Lower Pension Costs

Reduce Sick Days

Value-Based Healthcare

Occupational Healthcare has generated up to 6x ROI for Corporates

Key Demands

Health & Safety

Preventive Care

Primary healthcare Services

Emphasis On Measurable

Quality

Cost Efficiency is Critical

Secondary Care

OH Cost per Capita, € in 2014(2)

323

468

Public Health Centre Private Service…

+45%

(Minimum Requirement)

(Expanded coverage)

Corporates are willing to spend

above the statutory minimum

requirement

41 1) In a sample group of 10 companies which have deployed systematic work capacity management for at least 5 years, each invested 1 euro in the health of employees after 2008 until 2014 and has generated a net return of almost 6 euro each year; Source: Tekemättömän työn vuosikatsaus 2015; 2) Source: KELA

© Terveystalo

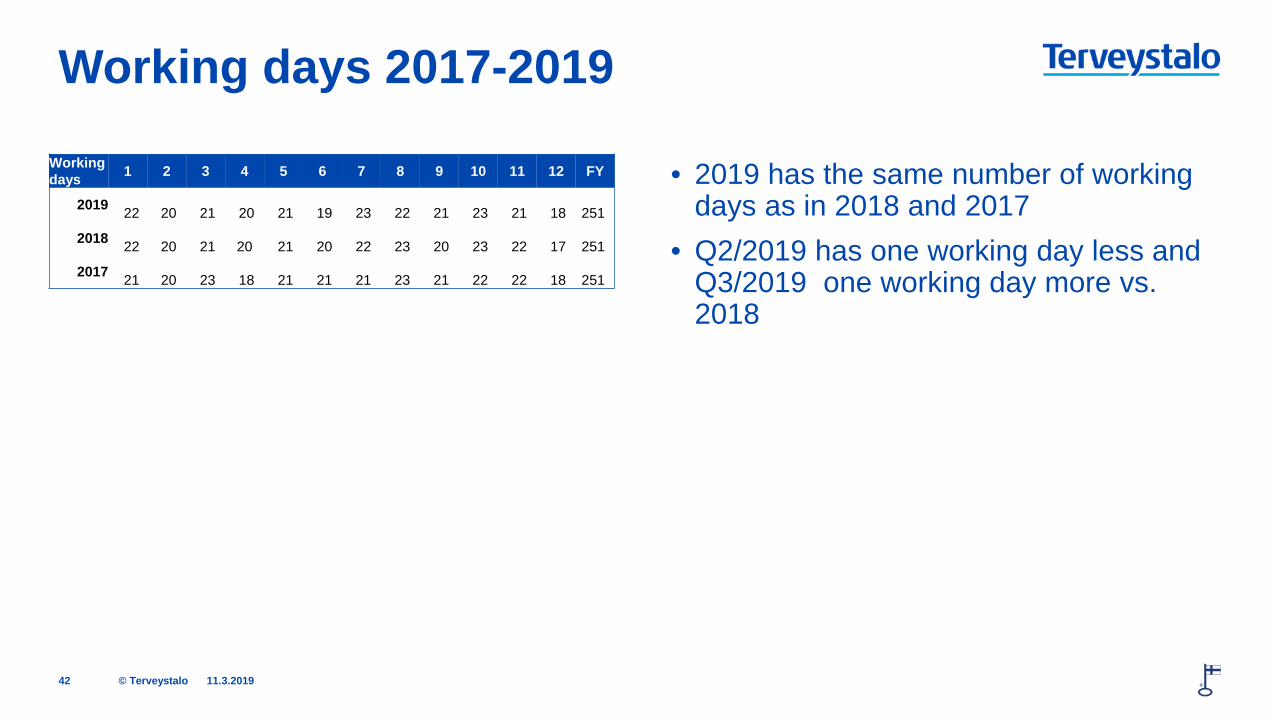

Working days 2017-2019

Working days 1 2 3 4 5 6 7 8 9 10 11 12 FY

2019 22 20

21

20

21

19

23

22

21

23

21

18

251

2018 22 20

21

20

21

20

22

23

20

23

22

17

251

2017 21 20

23

18

21

21

21

23

21

22

22

18

251

• 2019 has the same number of working days as in 2018 and 2017

• Q2/2019 has one working day less and Q3/2019 one working day more vs. 2018

11.3.2019 42

terveystalo.com #terveystalo