Embed Size (px)

Citation preview

TERMINAL 2LINKEDHOTEL

DEVELOPMENT

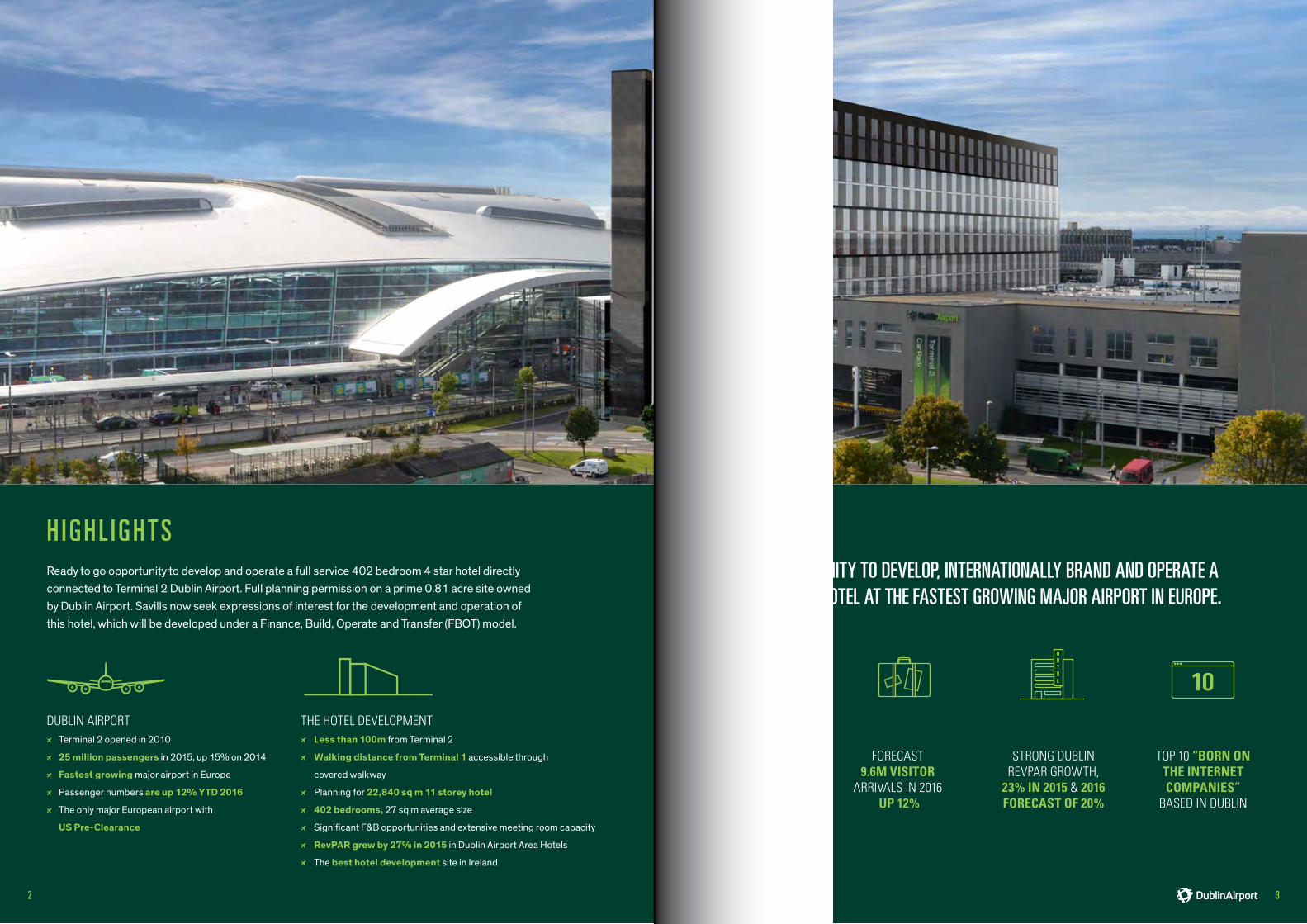

H IGHL IGHTS

Ready to go opportunity to develop and operate a full service 402 bedroom 4 star hotel directly connected to Terminal 2 Dublin Airport. Full planning permission on a prime 0.81 acre site owned by Dublin Airport. Savills now seek expressions of interest for the development and operation of this hotel, which will be developed under a Finance, Build, Operate and Transfer (FBOT) model.

IRISH EMPLOYMENT

GROWTH OF 2.9% FASTEST

IN WESTERN EUROPE

FORECAST 9.6M VISITOR

ARRIVALS IN 2016 UP 12%

STRONG DUBLIN REVPAR GROWTH,

23% IN 2015 & 2016 FORECAST OF 20%

TOP 10 “BORN ON THE INTERNET COMPANIES”

BASED IN DUBLIN

DUBLIN AIRPORT Terminal 2 opened in 2010

25 million passengers in 2015, up 15% on 2014

Fastest growing major airport in Europe

Passenger numbers are up 12% YTD 2016

The only major European airport with

US Pre-Clearance

THE HOTEL DEVELOPMENT Less than 100m from Terminal 2

Walking distance from Terminal 1 accessible through

covered walkway

Planning for 22,840 sq m 11 storey hotel

402 bedrooms, 27 sq m average size

Significant F&B opportunities and extensive meeting room capacity

RevPAR grew by 27% in 2015 in Dublin Airport Area Hotels

The best hotel development site in Ireland

A UNIQUE OPPORTUNITY TO DEVELOP, INTERNATIONALLY BRAND AND OPERATE A TERMINAL LINKED HOTEL AT THE FASTEST GROWING MAJOR AIRPORT IN EUROPE.

HOTEL

32

2014 TORONTO & SAN FRANCISCO

2015 WASHINGTON DC

2016 LOS ANGELES, HARTFORD & NEWARK

In 2016, this will reach 1.3m, driven by Aer Lingus development of Dublin as a gateway. Since 2014, Aer Lingus added the following long-haul routes:

LONG HAUL TRAFFIC ALSO RECORDED SIGNIFICANT GROWTH SINCE 2010 AND ALL THREE MAJOR US CARRIERS NOW OPERATE FROM DUBLIN:

MORE CONNECTING PASSENGERS ARRIVING IN DUBLIN AND STAYING FOR UP TO 2 NIGHTS BEFORE CONTINUING THEIR JOURNEY.

United Airlines (3 routes)

Delta (2 routes & adding Boston in 2017)

American Airlines (4 routes)

Air Canada operates two Dublin routes, while Etihad and Emirates fly twice daily to the Middle East. In 2015, Dublin obtained its first scheduled service to sub-Saharan Africa with Ethiopian Airlines flying to Addis Ababa 3 times a week.

IN 2015, DUBLIN HANDLED OVER 1M CONNECTING PASSENGERS FOR THE FIRST TIME

CONNECTING PASSENGERS AT DUBLIN AIRPORT

LONG HAUL PASSENGER GROWTH AT DUBLIN

HISTORIC TRAFFIC AT DUBLIN AIRPORT

2011

1.4

1.2

1.0

0.8

Mil

lio

ns

0.6

0.4

0.2

0.02012 2013 2014 2015 2016

Exp

Pa

ss

en

ge

rs (

Mil

lio

ns

)

P a x ( M i l l i o n s ) L i n e a r P a x ( M i l l i o n s )

0

5

10

15

20

25

30

2016 Est201420122010200820062004200220001998199619941992199019881986

20112010

4.0

Mil

lio

ns

3.0

2.0

1.0

0.02012 2013 2014 2015 2016

Exp

Dublin to London - second busiest international air route in the world

The only major European airport with US pre-clearance

Terminal 2 opened in 2010

Parallel Runway and Airport Masterplan cater for future growth

As an island nation, with an open economy, global connectivity is critical to Ireland and Dublin Airport handles almost 70% of all Irish air traffic.

Dublin Airport recorded very strong growth during the last 2 years, with annual passenger numbers increasing by over 3m pa in 2015.

Passenger numbers are up 12% YTD 2016.

In 2016 Airport traffic exceeded 100,000 daily passengers 4 times. 47 days in 2016 were busier than the previous busiest day ever.

Dublin Airport is home to Aer Lingus (IAG), Ryanair (the world’s largest international carrier) and 35 other Airlines.

Terminals 1 and 2 and the airport business community on your doorstep.

A vibrant, established and connected business community.

Strategic and established commercial hub.

VOTED NO.1 EUROPEAN AIRPORT FOR PASSENGER SERVICE IN 2015 (15-25M PAX)

DUBLIN AIRPORT WAS THE 2016 WORLD ROUTES AWARD WINNER FOR AIRPORTS IN THE 20-50 MILLION PASSENGERS PER YEAR CATEGORY

54

W I C K LOWMOUNTA I N SN AT I O N A L

PA R K

D U B L I N

M50

M50

M1

M2M3

M4

M7/M8/M9TO

N4

N3

N7

N81N11

N11

TERMINAL 1

TERMINAL 2

HOTEL SITE

PHASE 1

DUBLIN AIRPORTCENTRAL

PHASE 2

DUBLIN AIRPORTCENTRAL2,268

SPACECAR PARK

MALDRONHOTEL

RADISSON HOTEL

LINK

BRI

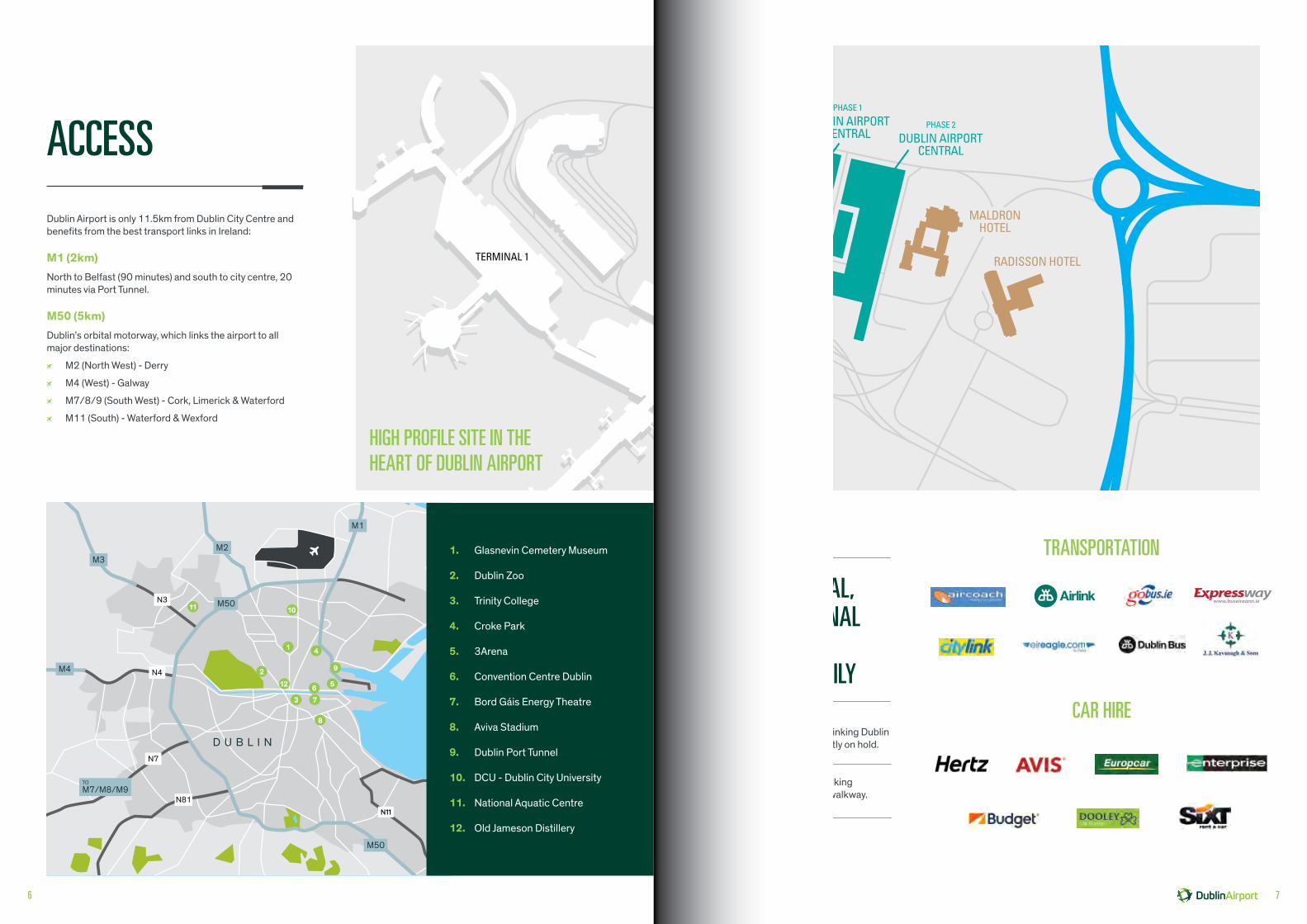

DGEDublin Airport is only 11.5km from Dublin City Centre and

benefits from the best transport links in Ireland:

M1 (2km) North to Belfast (90 minutes) and south to city centre, 20 minutes via Port Tunnel.

M50 (5km) Dublin’s orbital motorway, which links the airport to all major destinations:

M2 (North West) - Derry

M4 (West) - Galway

M7/8/9 (South West) - Cork, Limerick & Waterford

M11 (South) - Waterford & Wexford

Planned Metro North Rail line linking Dublin Airport to City Centre is currently on hold.

Terminals 1 & 2 are within walking distance served by a covered walkway.

OVER 1,400 LOCAL, URBAN & NATIONAL BUS AND COACH DEPARTURES DAILY

ACCESS

8

7

HIGH PROFILE SITE IN THE HEART OF DUBLIN AIRPORT

TRANSPORTATION

CAR HIRE

1. Glasnevin Cemetery Museum

2. Dublin Zoo

3. Trinity College

4. Croke Park

5. 3Arena

6. Convention Centre Dublin

7. Bord Gáis Energy Theatre

8. Aviva Stadium

9. Dublin Port Tunnel

10. DCU - Dublin City University

11. National Aquatic Centre

12. Old Jameson Distillery

3612

10

5

4

92

1

11

76

DUBLIN AIRPORT CENTRAL

*Source: Dublin Airport Central Draft Masterplan February 2016

Dublin Airport Central Masterplan

23

Zone 1 Masterplan

T2 Hotel

DUBLIN AIRPORT HAS A LONG TERM VISION TO ACCOMMODATE FUTURE PASSENGER GROWTH OF UP TO 55M PER ANNUM

DUBLIN AIRPORT CENTRAL*

Create a Business Campus at Dublin Airport. Works commenced in 2015

Newly refurbished ONE Dublin Airport Central fully let to ESB International

A direct link from the new office campus to the Terminal 2 Hotel link bridge is planned

VIBRANT BUSINESS COMMUNITY

A virtual Dublin Airport Central “Chamber of Commerce”

Dedicated tenant focused property team

Large corporate network at Dublin Airport including SR Technics, An Post, Boeing, Aer Lingus Head Office and many more

98

TERMINAL 2 LINKED HOTEL

High profile site with an impressive 11 floor hotel (40m tall)

Full grant of planning until 24th March 2019

The link corridor connecting T2 arrivals & departures, ground transportation and 2,268 space short term car park passes the hotel at main reception floor

Ground Level Road frontage, alternative entrance, fitness suite, retail, ancillary and extensive back of house.

1st floor Meetings & Events floor providing extensive meeting room capacity and F&B opportunities.

2nd floor Main hotel entrance, reception and open plan restaurant and bar.

Upper floors402 Bedrooms with an average area of 27 sq m, including 6 suites. Upper floors will have stunning views of the airport, sea, city and mountains.

Source: STR Global

Floor Function Area sq m

Ground Roadside entrance, Fitness, Retail & Back of House 2,475

1st Meetings & Events / F&B 2,737

2nd Level access to Terminal 2 through concourse, Main Hotel Entrance, Reception and F&B 2,494

3rd to 10th 402 Bedrooms & Suites 1,910 to 1,839

Total 22,840

YTD September 2016 RevPAR growth of 19%.

Dublin Airport Hotels monthly occupancy levels of more than 90% were achieved in four months of 2014, increasing to six months in 2015 and seven months this year.

DUBLIN AIRPORT HOTELS RECORDED STRONG REVPAR GROWTH OF 27% IN 2015

IN 2014, MONTHLY OCCUPANCY WAS OVER 90% FOR 4 MONTHS

SCHEDULE OF ACCOMMODAT ION

1110

Ireland was Europe’s fastest growing economy in 2014 and 2015. Latest estimates reveal Ireland’s domestic economy is growing at a faster rate than any other country in Europe. This is supported by strong jobs growth of 2.9% pa and reduced government deficit which allows for increased expenditure and more robust capital investment.

THE MARKET:

IRELAND

Source: Eurostat

8

7

6

5

4

3

2

1

0

Rom

ania

Irel

and

Swed

en

Esto

nia

Latv

ia

Cro

atia

Serb

ia

Spai

n

Ger

man

y

Mac

edon

ia

Mal

ta

Bul

garia

Fran

ce

Net

herla

nds

Bel

gium

Pola

nd

Slov

enia

Finl

and

Slov

akia

Lith

uani

a

Den

mar

k

Aust

ria

Port

ugal

Italy

Cze

ch R

epub

lic

Gre

ece

Uni

ted

Kin

gdom

Hun

gary

FINAL CONSUMPTION EXPENDITURE AND GROSS CAPITAL FORMATION (Q2 ‘15 - Q2 ‘16)

% C

HAN

GE

Y/Y

20% of new US investment in Europe comes to Ireland.

THE ONLY ENGLISH SPEAKING COUNTRY IN THE EUROZONE (339M PEOPLE)

SIGNIFICANT SHARE OF EUROPEAN FDI (FOREIGN DIRECT INVESTMENT)

IRELAND CONTINUES TO DELIVER A STRONG PERFORMANCE IN ECONOMIC, CORPORATE AND LEISURE METRICS.

1312

With 1.9m people (greater area), Dublin benefited from significant investment in recent years. Vibrant and affordable, Dublin attracts the world’s top creative talent, who aspire to work in the tech capital of Europe. It offers a city with a sense of history, creativity, a lively mixed-use city center, diverse retail offerings and multiple leisure activities on a much smaller footprint than megacity rivals.

Excellent standard of living supporting a positive work/ life balance.

Thriving social scene, proving integral for networking.

Thousand-year history and Georgian elegance, Dublin attracts tourists from all corners of the globe.

Dublin’s cultural offering and global reputation for hospitality makes it a highly popular tourist destination. In 2015, Ireland welcomed a record 8.6m overseas visitors.

Infrastructure improvements have further boosted Dublin’s appeal, these include:

Improvements to the M50, Dublin’s primary orbital motorway and on-going cross city Luas line.

Source: Fáilte Ireland

TOP DUBLIN ATTRACTIONS 2015 VISITOR NUMBERS

Guinness Storehouse 1,498,124

Dublin Zoo 1,105,005

National Aquatic Centre 991,554

Book of Kells, Trinity College 767,996

St Patricks Cathedral 532,042

Jameson Distillery 282,056

1.9 MILLION POPULATION

9.6 MILLION OVERSEAS VISITORS IN 2016 (F)

THE ONLY ENGLISH SPEAKING CAPITAL IN THE EUROZONE

THE MARKET:

DUBLINIRELAND’S POLITICAL, ECONOMIC AND CULTURAL CENTRE, IS A LIVELY AND CONTEMPORARY CAPITAL BRIMMING WITH PERSONALITY AND CHARM.

Aviva Stadium Croke Park Stadium Bord Gais Theatre 3Arena

1514

The Dublin Docklands or ‘Silicon Docks’ is home to a thriving creative tech industry. Start-ups, scale-ups and established global corporations compete for skilled employees, which a vibrant city like Dublin attracts. A combination of high-quality urban environments, a young & highly educated workforce, favourable regulatory environment (including 12.5% corporation tax) and affordable property costs.

Dublin has emerged as a haven for creative talent. It is a highly attractive investment location and is the EMEA headquarters of many of the world’s major companies.

DUBLIN HOSTS: European headquarters for more than

1,200 international companies

More than 50% of the world’s leading financial services firms

9 out of the top 10 global ICT companies

9 out of the top 10 global pharmaceutical companies

All of the top 10 “born on the internet” companies

THE MARKET:

DUBLIN

DUBLIN IS CONSIDERED ‘EUROPE’S SILICON VALLEY’

EVENTS:Dublin Airport works with Ireland’s leading tourism operators including Fáilte Ireland, promoting Dublin, the Region and the nation as the key provider of tourist visitation.

1716

Source: STR

8,000

9,000

10,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

2008

2009

2010

2011

2013

2014

2015

2016

(F)

2011

Great Britain Other Europe USA & Canada Other Areas

€160

€140

€120

ADR

Occupancy€100

€80

€60

€40

€20

€0

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(f)

2017

(f)

2018

(f)

ADR Occupancy

IRISH HOTEL PERFORMANCE AFFORDABLE DUBLIN

EUROPEAN CITIES ADR 2015

Dublin remains relatively inexpensive compared to other European Capitals with the city average daily rate (ADR) ranked 15th among European Cities.

EUROPEAN REVPAR 2015

Dublin achieved Occupancy of 82% in 2015, second only to London. Dublin places 12th overall in European city RevPAR rankings.

OVERSEAS ARRIVALS

In 2015, the number of foreign residents visiting Ireland exceeded the previous high achieved in 2007, with 8.6 million visitors, up 13.7% on 2014.

January to September 2016 arrivals were up 12% on prior year. If full year 2016 growth is 12%, then arrivals would total 9.6m in 2016.

DUBLIN HOTEL PERFORMANCE 2007 TO 2018F

STR reported very strong RevPAR growth in 2015 (+23.4%) with high occupancies now allowing for ADR to finally exceed the 2007 level. Average occupancy in Dublin was 82% in 2015 at an ADR of €112. Forecast RevPAR growth in 2016 is 20% & 7% in 2017.

A competitive set for Dublin Airport hotels had RevPAR growth of 19% September YTD 2016.

210

240

270

180

150

120

90

60

30

0

Gen

eva

Paris

Zuric

h

Tel A

viv

Lond

on

Mila

n

Rom

e

Amst

erda

m

Cop

enha

gen

Bar

celo

na

Fran

kfur

t

Edin

burg

h

Ista

nbul

Athe

ns

Dub

lin

Bru

ssel

s

Man

ches

ter

Vien

na

Hel

sink

i

Mad

rid

Ber

lin

Lisb

on

Mos

cow

Prag

ue

Buc

hare

st

Bud

apes

t

Sain

g Pe

ters

burg

Sofia

War

saw

Viln

ius

Bra

tisla

va

AD

R (E

UR

O)

175

200

225

150

125

100

75

50

25

0

Paris

Gen

eva

Lond

on

Zuric

h

Tel A

viv

Mila

n

Rom

e

Amst

erda

m

Cop

enha

gen

Edin

burg

h

Bar

celo

na

Dub

lin

Fran

kfur

t

Man

ches

ter

Ista

nbul

Athe

ns

Bru

ssel

s

Vien

na

Ber

lin

Lisb

on

Hel

sink

i

Mad

rid

Prag

ue

Bud

apes

t

Buc

hare

st

War

saw

Mos

cow

Sain

t Pet

ersb

urg

Viln

ius

Sofia

Bra

tisla

va

REV

PAR

(EU

RO

)

In comparison to similar sized international cities, Dublin is relatively under-subscribed from a brand perspective. This is an excellent opportunity for a major brand to enter Dublin at the highest profile location.

HOTEL BRANDS

1918

Source: Savills

DUBLIN AIRPORT HOTEL PERFORMANCE DUBLIN HOTEL DEVELOPMENT

LIMITED DUBLIN HOTEL PIPELINE

According to the ITIC, Dublin needs an additional 5,000 hotel bedrooms by 2020. However, the real pipeline in Dublin is small and growing from a zero base. The seven years from 2009 to 2015 saw just 4 new hotel openings.

DUBLIN PIPELINE 2016 TO 2018

In 2016, Savills expect Dublin room supply to grow by 1.4% mainly due to:

AM:PM predicts less than 950 additional bedrooms (net of closures) in Dublin before 2019.

2 0 1 0 THE GIBSON

D U B L I N 1

HOLIDAY INN EXPRESS D U B L I N 1

2 0 1 3 THE MARKER

D U B L I N 2

MORAN RED COW D U B L I N 2 2 ( E X T E N S I O N )

2 0 1 4 THE DEAN

D U B L I N 2

THE NORTH STAR D U B L I N 1 ( E X T E N S I O N )

2 0 1 5 THE TEMPLE BAR INN

D U B L I N 2

CLYDE COURT HOTEL D U B L I N 4 ( C L O S E D )

OPENED OCTOBER 2016 PHASED OPENING H2 2016 DUE TO OPEN LATE 2016 CLOSED JANUARY 2016

187 Bedrooms 52 Bedrooms 99 Bedrooms252 Bedrooms

202 Bedrooms 152 Bedrooms 78 Bedrooms 185 Bedrooms

Savills expect approximately 1,500 additional bedrooms will be added to Dublin hotel supply between 2016 and 2018, of which the majority will be delivered in 2018.

A 141 bedroom extension at the Dalata plc. owned Clayton Hotel Dublin Airport is expected to be the first major addition to airport bedroom supply, before the expected opening of the Terminal 2 linked hotel in late 2019.

R108

R108

L3132

L313

2

R108

R108

SANTRY AVE

SWOR

DS R

D

SWOR

DS R

D

SWORDS RD

DUBL

IN R

D

CLON

SHAU

GH R

D

BASKIN LN

MAL

AHID

E RD

MAL

AHID

E RD

MAL

AHID

E RD

NAUL RD

M50

M50

M1

R139

12

3

4

5

6

78 10

9

TERMINAL 2LINK HOTEL

DUBLIN AIRPORT HOTELS RECORDED STRONG REVPAR GROWTH OF 27% IN 2015 AND 19% YTD

SEPTEMBER 2016, NOW DRIVEN MAINLY BY ADR.

MONTHLY OCCUPANCY LEVELS OF MORE THAN 90% WERE ACHIEVED IN FOUR MONTHS OF 2014, INCREASING TO SIX

MONTHS IN 2015 AND SEVEN MONTHS THIS YEAR.

MAP HOTEL NAME KM TO AIRPORT STAR BEDROOMS

Terminal 2 Linked Hotel Terminal 4 402

1 Maldron Hotel Dublin Airport 0.4 4 251

2 Radisson Blu Hotel Dublin Airport 0.5 4 229

3 Carlton Hotel Dublin Airport 1.7 4 100

4 Travelodge - Dublin Airport North Swords Hotel 3.7 3 130

5 Premier Inn Dublin Airport Hotel 3.1 3 155

6 Clayton Hotel Dublin Airport 4.6 4 469

7 Holiday Inn Express Dublin Airport 3.3 3 114

8 Crowne Plaza Dublin Airport 3.3 4 204

9 Metro Hotel Dublin Airport 5.1 3 88

10 Hilton Dublin Airport 7.1 4 166

New Rooms 2018New Rooms 2017New Rooms 2016

-550

-350

-150

150

350

550

750

Dublin 1 Dublin 2 Dublin 4 Dublin 6 Dublin 8 Dublin 22 Dublin Airport

2120

* Internal layout can be amended. * Internal layout can be amended.

GROUND FLOOR* FIRST FLOOR*

RAMP NOTREQUIRED

NOW

PABXROOM

LIFT LIFT

LIFT LIFT

FIREESCAPE

STAIR

LEISURE AND FITNESS FACILITY PLANT

ROOM

LOST AND FOUND

MAINTENANCEROOM

STATIONARYSTORE

CROCKERYSTORE

DRYGOODS

KEGSTORE

BOTTLESTORE

OP

ERATIN

GR

OO

M

BIN STORE

HEALTH AND WELLNESS FACILITIES

HOTEL FOYER

LAYBY / DROP

OFF

CRECHE

LAUNDRY

BEAUTY TREATMENTFACILITY

SWITCHROOM

TRANS ROOM

SERVICE YARD

GOODSDROP

OFF

FOOTPATH

LINENSTORE

HOTELACCESS

ROAD

FIRE FIGHTING

LIFT

GASMETERROOM

RAMP NOTREQUIRED

NOW

GIVE WAY

RIGHTTURN ONLY

RIGHTTURN ONLY

STAFF CHANGES AND CANTEEN

HOTEL GIFT SHOP

SERVICELIFT

SERVICELIFT

LUG

GA

GE

STORE

SERVICELIFT

ESCAPESTAIR

ACCESSBARRIER

ACCESSBARRIER

ACCESSBARRIER

ACCESSBARRIER

LANESMERGEAFTER

BARRIER

LANESMERGEAFTER

BARRIER

LANESMERGEAFTER

BARRIER

LANESMERGEAFTER

BARRIER

ENTRANCEPLAZA

HEIGHTRESTRICTION

SIGN

FIREEXIT

FIREESCAPE

STAIR

LAYBY / DROP

OFF

HOTELACCESS

ROAD

ENTRANCEPLAZA

HEIGHTRESTRICTION

SIGN

MTG10

MTG03

MTG02

MTG01

MTG05

MTG04

MTG07

MTG06

MTG08

MTG09

MULTI - PURPOSEROOM

BREAKOUTAREA

BREAKOUTAREA

BREAKOUTAND

CIRCULATIONAREA

BREAKOUTAND

CIRCULATIONAREA

OFFICE ANDCLOAKROOM

KITCHEN

FIREFIGHTING

LIFT

TOILETS

DISABLEDREFUGESPACE

EXT.TERRACE

VOIDOVER CAR PARK

ENTRANCE LEVEL

MTG13

MTG12

MTG11

MEET &GREET

MTG10RESTAURANT

VIP /CREW

LOUNGE

STORES

STO

RE

KITCHEN

RIGHTTURNONLY

GIV

E W

AY

RIGHTTURNONLY

GIV

E W

AY

F IREEXIT

SERVICELIFT

LIFT

LIFT LIFT

SERVICELIFT

SERVICELIFT

FIREFIGHTING

LIFT

DISABLEDREFUGESPACE

T2 LINK BRIDGE

HOTEL FLOORPLANS

DROP OFF

SECONDARY ENTRANCE

LEISURE

ANCILLARY

BACK OF HOUSE

MEETINGS & EVENTS

FOOD & BEVERAGE

2322

* Internal layout can be amended. * Internal layout can be amended.

SECOND FLOOR* CONCOURSE

HOTEL ENTRANCE

LOBBY / RECEPTION

BAR

RESTAURANT

TYPICAL BEDROOM FLOOR* FLOOR 3 TO 8

51 BEDROOMS AVERAGE SIZE 27 SQ M

FLOOR 9 & 10 45 BEDROOMS / 3 SUITES AVERAGE SUITE SIZE 42 SQ M

LAYBY / DROP

OFF

HOTELACCESS

ROAD

ENTRANCEPLAZA

HEIGHTRESTRICTION

SIGN

LOBBY

KIOSK

LUGGAGE

COFFEE AREA

FOYER

REC

EPTIO

N

PORTER

ENTRANCELOBBY

REC

EPTIO

N/ A

DM

IN

BAR

RESTAURANT

TOILETS

KITCHEN

OPEN KITCHEN

FUTURE BRIDGELINK TO GTC

PUBLIC CONCOURSE TO GTC

ACCESS TO GTC(FUTURE)

ACCESS TO T2

MEETERS AND GREETERS SEATING

MEET &GREET

FIREFIGHTING

LIFT

FIREEXIT

FIREEXIT

SERVICELIFT

LIFTLIFT

LIFT

SERVICELIFT

SERVICEDUCT

VOID +FEATURE STAIR

EXT.TERRACE

T2 LINK BRIDGE

FIREFIGHTING

LIFT

FIREEXIT

FIREEXIT

6 NO. TICKET VALIDATIONMACHINES (BY OTHERS)

4 NO. TICKET VALIDATION MACHINES

ATM ROOM

FIREESCAPE

STAIR

LAYBY / DROP

OFF

HOTELACCESS

ROAD

ENTRANCEPLAZA

HEIGHTRESTRICTION

SIGN

31

30

33

32

35

34

29

28

27

26

25

24

23

37

36 22

21

39

40

38 20

19

42

41

44

43

46

45

48

47

50

51

49

14

13

12

11

10

9

8

7

6

5

4

3

2

1

18

17

16

15

FLOOR OVERCONCOURSE FLOOR

FIREFIGHTING

LIFT

DISABLEDREFUGESPACE

WHEELCHAIRACCESSIBLE

WHEELCHAIRACCESSIBLE

WHEELCHAIRACCESSIBLE

DISABLEDREFUGESPACE

SERVICEDUCTLIFT

LIFT

LIFT

LIFT SERVICELIFT

LINENROOM

FIREFIGHTING

LIFT

T2 LINK BRIDGE

LAYBY / DROP

OFF

HOTELACCESS

ROAD

ENTRANCEPLAZA

HEIGHTRESTRICTION

SIGN

31

30

33

32

35

34

29

28

27

26

25

24

23

37

36 22

21

39

40

38 20

19

42

41

44

43

46

45

48

47

50

51

49

14

13

12

11

10

9

8

7

6

5

4

3

2

1

18

17

16

15

FLOOR OVERCONCOURSE FLOOR

FIREFIGHTING

LIFT

DISABLEDREFUGESPACE

WHEELCHAIRACCESSIBLE

WHEELCHAIRACCESSIBLE

WHEELCHAIRACCESSIBLE

DISABLEDREFUGESPACE

SERVICEDUCTLIFT

LIFT

LIFT

LIFT SERVICELIFT

LINENROOM

FIREFIGHTING

LIFT

T2 LINK BRIDGE

All on the same level as the link to terminal 2, arrivals and car park pedestrian entrance.

2524

TENURE The development is being undertaken using an FBOT (Finance, Build, Operate, Transfer) approach to the build and operation of the hotel.

PROCESS & TIMELINE It is anticipated that an RFI will run from late 2016 to early 2017. Based on RFI submissions, it is anticipated that a small number of interested parties will be issued with an RFT in Q1 2017, with an anticipated submission date in Q2 2017.

VIEWING Strictly by appointment with the sole selling agents, Savills Hotels & Leisure.

AGENT Tom Barrett +353 (1) 618 1415 [email protected]

Aaron Spring +353 (1) 618 1446 [email protected]

Andrew Sherry +353 (1) 618 1452 [email protected]

DUBLIN AIRPORT

Lisa Jordan +353 (87) 356 3027 [email protected]

Savills Ireland and the Vendor/Lessor give note that the particulars and information contained in this brochure do not form any part of any offer or contract and are for guidance only. The particulars, descriptions, dimensions, references to condition, permissions or licences for use or occupation, access and any other details, such as prices, rents or any other outgoings are for guidance only and are subject to change. Maps and plans are not to scale and measurements are approximate. Whilst care has been taken in the preparation of this brochure intending purchasers, Lessees or any third party should not rely on particulars and information contained in this brochure as statements of fact but must satisfy themselves as to the accuracy of details given to them. Neither Savills Ireland nor any of its employees have any authority to make or give any representation or warranty (express or implied) in relation to the property and neither Savills Ireland nor any of its employees nor the vendor or lessor shall be liable for any loss suffered by an intending purchaser/Lessees or any third party arising from the particulars or information contained in this brochure. Prices quoted are exclusive of VAT (unless otherwise stated) and all negotiations are conducted on the basis that the purchasers/lessees shall be liable for any VAT arising on the transaction. This brochure is issued by Savills Ireland on the understanding that any negotiations relating to the property are conducted through it. All maps produced by permission of the Ordnance Survey Ireland Licence No AU 001799 © Government of Ireland.

26