Embed Size (px)

Citation preview

Telecommunications Market Development

in Russia

AprilApril 2002 2002

2

OJSC SvyazinvestState Mustcom75% -1 share

25% +1 share

ГосударствоRostelecom(LD and

international traffic)

74 regional operators

51%Over 25%

Over 50%

Services:

• Local traffic

• LD and international traffic

• Radio & TV broadcasting

• Data transmission & Internet

• Wireless communication

MGTSKostroma GTSKomisvyazSakhalinsvyaz

Telecom companies not incorporated in the holding company:Chechnya IngushetiaTyva TatarstanBashkiria ChukotkaYakutia

Svyazinvest is the Russia’s Leading Telecommunications Group

3

The Holding Company’s Performance Improved in 2001

2.62

3.15

1.3

1.9

0

0.5

1

1.5

2

2.5

3

3.5

2000 2001

0

0.5

1

1.5

2

2.5

3

Gross income(left scale)

Roll out oftelephone lines(right scale)

$, bn Lines, mln

4

Target indicators for 2010:Increase in telephone lines from 31.2 mln to 47.7 mlnGrowth of mobile subscribers from 8.3 mln to 22.2 mlnGrowth of the Internet users from 2.5 mln to 26.1 mlnIncrease in digitalisation of networks in Russia from 26% to 94%Volume of non-governmental investments - $33 bn

• To ensure satisfaction of growing demand in telecoms services and advanced development of the national telecoms infrastructure • To ensure provision of generally accessible telecoms services to every urban and rural community in Russia• To improve the infrastructure efficiency and investment attractiveness of the telecoms sector, to create conditions for a fair competition

Concept’s Guidelines

• Creating conditions for balanced dynamic development of the telecoms market

• Involving all market players in the solution of state social tasks

• Improving state regulation methods

Objectives Results are achieved by:

5

Svyazinvest Structural Problems

Disintegration of the holding company –

78 regional operators (after completion of intra-

regional mergers)

• high costs

• poor marketing

• inefficient management

• low degree of transparency

• low market capitalization and liquidity of shares

• difficulty in implementing large-scale projects

• inconvenience for customers

• ….

OBJECTIVE Increase in efficiency and investment attractiveness

Indicators Compared to SBC Compared to Verizon

Lines 1/220 1/230

Revenue 1/2500 1/3000

Capitalization 1/10000 1/8000

Svyazinvest average regional operator versus American companies

6

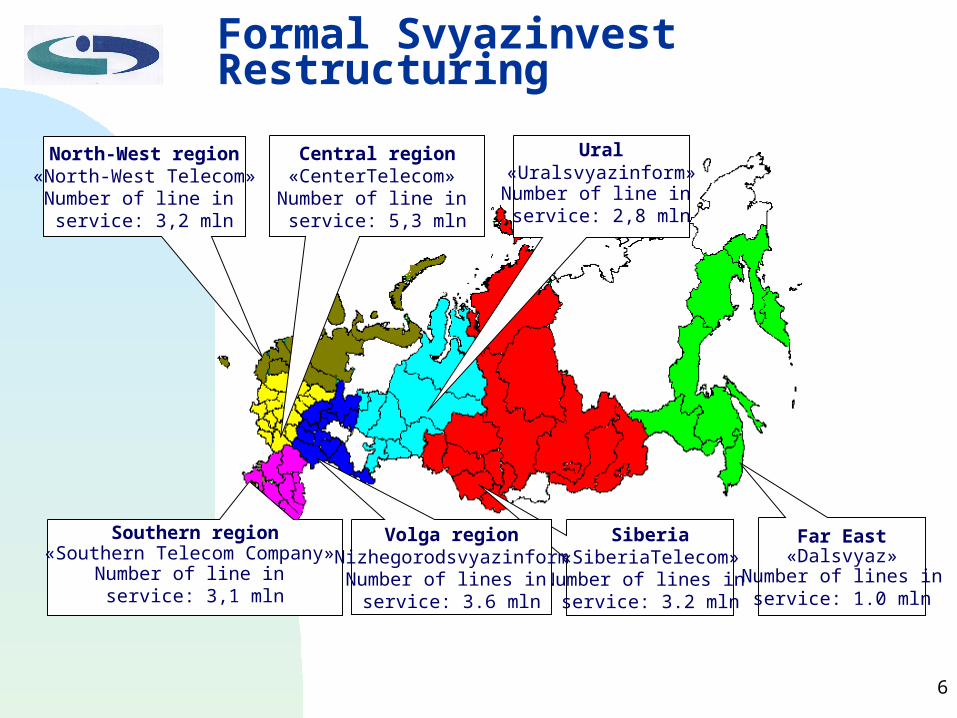

North-West region«North-West Telecom»

Number of line in service: 3,2 mln

Central region«CenterTelecom» Number of line in service: 5,3 mln

Southern region«Southern Telecom Company»

Number of line in service: 3,1 mln

Far East«Dalsvyaz»

Number of lines in service: 1.0 mln

Siberia«SiberiaTelecom»Number of lines in

service: 3.2 mln

Ural«Uralsvyazinform»Number of line in service: 2,8 mln

Volga regionNizhegorodsvyazinform

Number of lines in service: 3.6 mln

Formal Svyazinvest Restructuring

7

1.2

6.7

2.7 3.0 2.9

9.0

0

1

2

3

4

5

6

7

8

9

Telenor(Norw ay)

Sonera(Finland)

MATAV(Hungary)

CeskyTelecom

PortugalTelecom

Market capitalization ($, bn)

Main telephone lines (million)

Comparison with European Operators

Average market capitalization in 2001

1.0

2.73.0 3.2 3.2 3.3

5.2

2.63.0

3.43.6

4.1

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

Far East Urals South Siberia North-West Volga Center(excluding

MGTS)

Telenor(Norw ay)

Sonera(Finland)

MATAV(Hungary)

CeskyTelecom

PortugalTelecom

8

2.5

8

10

15

13

22

35

32

23

31

Russia (current tariff)

Russia (economicallyfeasible costs)

Estonia

Latvia

Lithuania

Poland

Czech Republic

Hungary

Brazil

Argentina

8

Average Monthly Charges for Local Calls ($ in month)

9

North-West

95 %

5 %

Urals

97 %

3 %

Siberia

93 %

7 %

South

97 %

3 %

- In favour of the restructuring

- Against the restructuring

Center

95 %

5 %

97 %

3 %

Far East

98 %

2 %

Volga

Restructuring: Distribution of Shareholders’ Votes

10

Corporate Restructuring Is a Natural Follow-Up to the Merger Process

Corporate restructuring

Technicalpolicy

Marketingpolicy

HRpolicy

Financial andeconomic

policy

OJSC Svyazinvest

TTransition to the economically feasible cost calculation of telecoms servicesIIntroducing advanced corporate governance methods RReporting under IASUUnification of accounting policies

Providing mega-regional companieswith a marketingpolicy

Technical audit of regional operatorsGuidelines of development of a mega-regional companyDrafting a general strategic development plan for the period ending 2007

Recruiting and training qualified personnelImproving the system of incentives

11

Svyazinvest Intends to Create an Effective System of Business Planning and Control

in Mega-Regional Companies

Tasks

Unification ofaccounting

policies

Elaboration of an economically feasible

cost calculationmethodology

Working outbudgeting

procedures IAS

Creating a tariff policy for a mega-regional company

Phasing in and broadscale application of tools used in business planning, budgeting and control

Ensuring transparency of a mega-regional company’s activity

12

Regional market valuation to identify its major development trends

Working out guidelines of a marketing strategy for a mega-regional company and elaboration of methodological recommendations on market research and identifying marketing strategies

Identifying a medium-term marketing strategy for mega-regional companies

Advanced training of marketing personnel

Svyazinvest is Striving to Provide Mega-Regional Companies with a Strong

Marketing Strategy

Main tasks at the current stage:

13

Svyazinvest is Taking Steps to Integrate Telecom Networks within Mega-Regional

Companies

Main tasks:

WWorking out a general development plan for mega-regional companies and Rostelecom as integral parts of the interconsistent communications network of the Russian Federation for the period ending 2007 on the basis of two research papers:

system network solutions concerning the development of infocommunications networks of mega-regional companies and Rostelecom as integral parts of the interconsistent communications network of the Russian Federation for the period ending 2007;

working out guidelines for the development of infocommunications networks of mega-regional companies and Rostelecom.

14

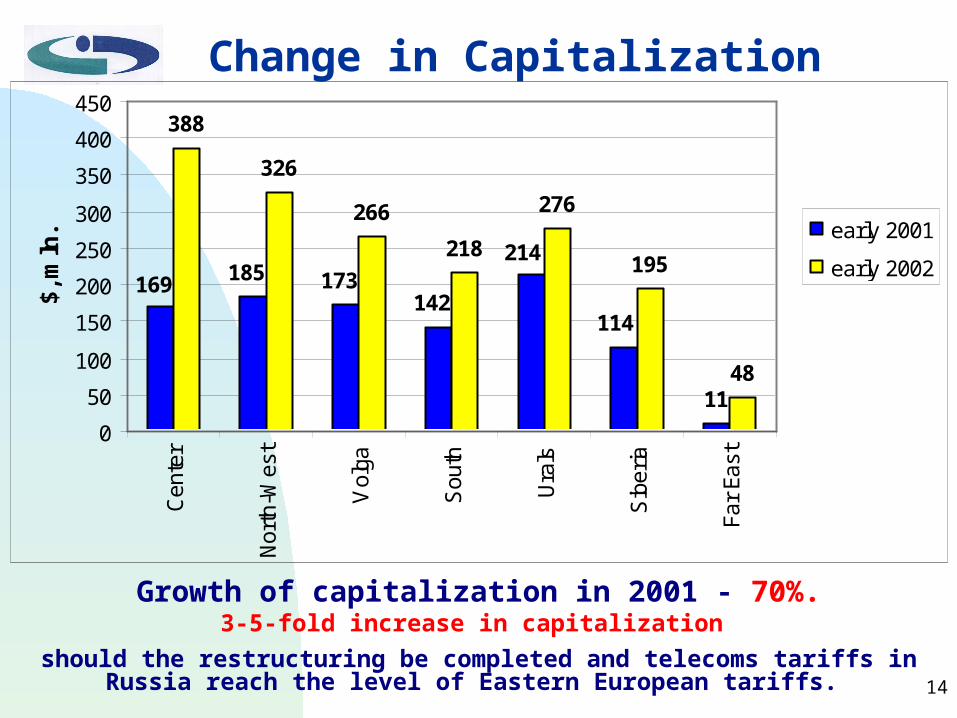

Change in Capitalization

11

388

326

266 276

195

48

214

114142

173185169

218

0

50

100

150

200

250

300

350

400

450

Cen

ter

Nor

th-W

est

Vol

ga

Sou

th

Ura

ls

Sib

eria

Far

East

$, m

ln. early 2001

early 2002

Growth of capitalization in 2001 - 70%.3-5-fold increase in capitalization

should the restructuring be completed and telecoms tariffs in Russia reach the level of Eastern European tariffs.

15

Results of Investment

2.4 million

new telephone lines

about 60 000 km

of trunk cable

Or

Cost saving due to the

restructuring~$ 200 mln

Additional investment

opportunities~$ 1 bn

16

Thank you!

AprilApril 2002 2002