Embed Size (px)

Citation preview

Telecommunications Industry UpdatePresentation to WTA

Frank GallagherColorado Springs, ColoradoSeptember 13, 2016

2

Overview

September 2016WTA 2016 Fall Meeting

Purpose

▫ Snapshot of industry fundamentals

▫ Summary of financial impact of regulatory trends

▫ Perspectives on sustainable, constructive strategic directions

Background perspective

▫ Investment banker

▫ Strategic advisory services

Four messages

▫ Industry fundamentals and valuations suffering ongoing pressure

▫ Regulatory changes are driving major RLEC strategic change

▫ Strongest companies across the industry are concentrating on scale, growth, diversification and higher-value services

▫ RLECs will be required to increasingly focus on long-term strategic value improvement and evolution of the business plan

3

September 2016WTA 2016 Fall Meeting

4

Telecom Trends at a Glance

Industry continues to go through a fundamental transformation from voice to data

Year-over-year (“YoY”) access line loss rates have been “stable” for the last two years

▫ The five large public RLECs reported average line loss of -3.8% in 2Q16

▫ ≈50% of US households had landline voice service at YE 2015, down from 92% at YE 2004

Broadband subscribership declined in 2Q16

▫ Average YoY subscribers declined by -1.7% in 2Q16

▫ Revenue generating units (access lines, high-speed data, and video subs) continue to decline

Cable MSOs reported slightly declining RGUs of 0.3% for 2Q16 (largely due to Cable One and WOW!)

RLEC RGU decline improved compared to prior quarters and was -1.9% in 2Q16

YoY large carrier revenue change was -1.2% in 2Q16 compared to -0.9% in 1Q16

▫ CenturyLink reported the only top line revenue growth among the RLECs (excluding acquisitions)

EBITDA(1) margins (a measure of operating cash flow) under pressure

▫ Median industry EBITDA margin held steady at 34.5% in 2Q16

▫ EBITDA margins declined for the five large carries held steady

September 2016WTA 2016 Fall Meeting

Source: Company filings, Wall Street Equity Research, and press releases(1) EBITDA is defined as Earnings Before Interest, Taxes, Depreciation, and Amortization

5

Broadband Data and Video Trends

Cable continues to dominate broadband customer additions

▫ YoY net adds of 3.3M for cable and -140K for RLECs in 2Q16

▫ Cable sub growth of 6.8% in 2Q16

▫ Telco sub decline of -1.7% in 1Q16

▫ Cable broadband market share is approaching 66%

▫ ≈79% of US households get broadband service at home, up from 20% in 2004

Cable continues to take share from DSL; FiOS and U-verse account for ≈60% of telco broadband subs

Cable broadband subs (48.2 million) exceed video subs (41.4 million)

Relatively stable competitive dynamics in spite of rising prices

▫ Video subscriber losses continued in 2Q16

▫ Cable lost 400K subscribers YoY, while AT&T and Verizon added subscribers

▫ Cable revenue growth (2.6%) as well as EBITDA growth positive (4.8%) in 2Q16

Pay TV RGUs continue to decline (-0.3% in 2Q16); subs have declined since 4Q09

▫ Approximate video market share: cable 52%, satellite 36%, telco 12%

Broadband Data

Video

Source: UBS Equity Research, and company data

September 2016WTA 2016 Fall Meeting

6

Illustration of an ILEC Strategic Assessment

Strategic assessment of an ILEC that relied on state and federal regulation

▫ Changed illustration to preserve confidentiality for client

▫ Operates two ILECs with modest other non-regulated services

▫ Original model reflects virtuallyunchanged revenues and costs over projection period

Modified analysis assumed . . .

▫ 1% annual regulated revenue declines

▫ 100 basis point annual decline in margin

▫ Assumed 15% EBITDA multiple contraction annually from 5.0x in 2015 to 4.24x in 2034

▫ Comparison of valuation at present with valuation contraction if no strategic change

Conclusion: strategic initiatives necessary, based on current operations, or divest

September 2016WTA 2016 Fall Meeting

7

Wireless Industry Update and Trends

Source: Company filings, UBS Equity Research, Bank of America Merrill Lynch Research, and press releases

September 2016WTA 2016 Fall Meeting

Primary Trends

AT&T & Verizon remain dominant carriers controlling ≈66% of subs• Sprint and T-Mobile each hold ≈15% shares

Current battlefield is mobile video 5G launches expected for 2020 and capex is moving toward this event

SubscribersConnection growth rate slowing as penetration exceeds 100%All major carriers experience net subscriber gains in 2Q16 Postpaid subscribership increased ≈4.0% YoY ≈19% of wireless subs are prepaid

ARPU and Data

Sector ARPU declined by 7.0%, compared to a 6.3% decline in 2Q16• Aggressive service discounts and phone payment plans

T-Mobile declined by 3.9% (best) while Verizon declined by 9% (worst) Increasing demand driving data growth

Devices ≈75% of handset sales on equipment installment plans (EIP)• EIP devices represent ≈53% of postpaid subscribers

88% smartphone penetrationConnected device net adds continue to outpace smartphones

Financials Service revenue declined for AT&T, VZW, and Sprint T-Mobile was the only company to grow at 9.1%Average national carrier EBITDA margin increased in 2Q16• Growth reflects the change to EIP device sales

-10%

-5%

0%

5%

10%

15%

1Q13 1Q14 1Q15 1Q16

Total Service Revenue Growth

Service ARPU Growth

EBITDA Margin

-15%

-10%

-5%

0%

5%

1Q13 1Q14 1Q15 1Q16

0%

10%

20%

30%

40%

50%

1Q13 1Q14 1Q15 1Q16

8

September 2016WTA 2016 Fall Meeting

9

Assessing the RLEC Timeline from Telecom Act to Present

Long-term trends

▫ Movement toward models with assumptions, creating winners and losers

▫ “Sufficient and predictable” support is shifted to a capped budget

▫ Loss of political and intellectual “bench” in legislative and regulatory bodies

▫ Federal trends are influencing state outcomes

▫ Less predictability and fracturing of high-cost system

▫ Revision to the allowed federal rate of return

September 2016WTA 2016 Fall Meeting

1996

Telecom ActSection 254

2000

Rural Task Force affirms RLEC

diversity and use of embedded

costs

2001

Rural reforms of ICC/USF based

on assumed diversity

2011

FCC reforms of USF/ICC

2015/2016

FCC work on rural mechanisms and models / ROR

10

Notable Recent Developments

FCC is pushing for models to “simplify” the regime, but winners accepting the model will put pressure on overall funding

FCC has reduced the federal allowed rate of return

▫ Reduction of ROR level to 9.75% v. the current 11.25%, lowered annually by 0.25%

▫ Likely to affect subsequent state processes where commissions/legislatures are limited

Trade organizations working with FCC on A-CAM (alternative CAF model)

▫ Cost consultants developing forecasting models using current A-CAM model

▫ Precise returns are not yet clear

▫ “Political” problem is that the rural coalition’s interests are splintering

No movement on the contribution mechanism

Potential for increased municipal broadband activity

Legal challenges to key “reforms” and orders

September 2016WTA 2016 Fall Meeting

11

Projecting the Future Based on Federal Trends

Not possible to predict future of rural regulation with certainty but . . .

▫ Support funding is not likely to grow appreciably, and more likely will fall short of emerging obligations

▫ Again, new regulation is reducing the effective lobby power of rural carriers

▫ Political and regulatory support will likely weaken further

Rural model is changing

▫ From voice-centric services to data-centric services

▫ From predictable regulatory support systems to lesser or unpredictable regimes

▫ From low-cost capital to higher-cost (higher-risk) capital

▫ From primarily residential services to growing percentage of business/carrier services

Strategic model of the future

▫ Relies on no/lower regulatory support mechanisms

▫ Becomes less uniform in terms of services to low-cost versus high-cost customers

▫ Requires defensible network and services versus competitors

▫ Increases the need for cost and capital management

▫ Rewards companies that identify and execute on a clearly-defined strategic plan

September 2016WTA 2016 Fall Meeting

12

September 2016WTA 2016 Fall Meeting

13

Telco Strategic Approaches

Strategic approaches to …▫ Increase scale of ops & revenue base in target markets; almost always foundational▫ Enhance strategic flexibility and optionality to improve long-term viability▫ Reduce reliance on support and voice revenues

Pure-play telco transactions are important but often transitional strategic steps

Common transaction criteria within the industry include▫ Focus on sustainable data-centric services (Internet, transport, and fiber-to-tower)▫ Meaningful synergy/cost saving opportunities ▫ Strong growth and/or diversification potential ▫ High-quality, well-positioned network▫ Reasonable price relative to strategic value (cash-flow accretive)▫ Positive impact on overall financial position

Increase scope and scale of landline operations through M&A

Rationalize cost structures over a larger revenue base

Increase Scope & Scale

Reduce regulatory exposure

Geographic diversification

Expand network assets and business lines-CLEC & fiber

Enter business services-data centers, managed services, cloud services

Diversification

Grow telco scope and scale

Simultaneously pursue business diversification

Hybrid

September 2016WTA 2016 Fall Meeting

14

Every Large Carrier is Engaged in a Dramatic Transformation

M&A activity allows us to discern strategic thinking of companies

▫ Companies re-position through divestitures, acquisitions, partnerships, JVs, etc.

▫ Major strategic change is a consistent pattern over time

▫ Most often accelerates when there are fundamental new industry forces

Focus on larger carriers with lessons for smaller carriers

▫ Large carriers have opportunities that are different from those at RLECs

▫ Large-carrier M&A is instructive and creates “movement” that may offer opportunities for RLECs

Small carriers are contending with essentially the same forces as large carriers

▫ Similar migrations to diversity and gain scale

▫ RLECs have more meaningful regulatory risk

A principle can be articulated for a fundamentally changing industry▫ A proactive transformative strategy is needed in such an industry,

▫ To continuously increase the scale/scope of operations,

▫ With a view to supporting better market control, and flexible options,

▫ While stabilizing and/or improving company valuation

September 2016WTA 2016 Fall Meeting

15

CenturyLink

Pattern in M&A and strategic activity

▫ More than two decade history of major and transformative acquisitions of wireline assets

▫ Extraordinary team whose skill set is acquisitions

▫ Improve properties and generate better revenues

▫ Recent thrust toward diversification

Strategic goals

▫ Conservative capitalization to preserve ability to acquire in a timely way

▫ Recent acquisitions have been stock-for-stock

▫ Gain wireline scale which provides strategic flexibility and optionality

▫ Improve and upgrade plant, notably in defensible markets

▫ Increased exposure to more competitive urban / suburban markets where competition is “more mature”

▫ More enterprise data centric

▫ Focused on regaining revenue growth

September 2016WTA 2016 Fall Meeting

16

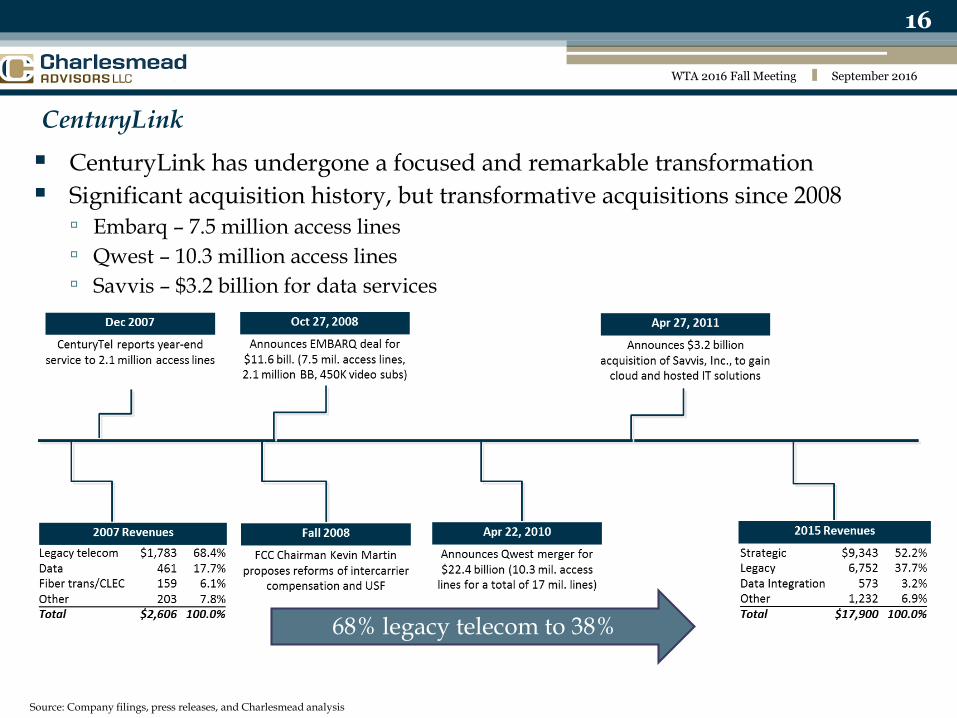

CenturyLink

CenturyLink has undergone a focused and remarkable transformation

Significant acquisition history, but transformative acquisitions since 2008

▫ Embarq – 7.5 million access lines

▫ Qwest – 10.3 million access lines

▫ Savvis – $3.2 billion for data services

September 2016WTA 2016 Fall Meeting

Source: Company filings, press releases, and Charlesmead analysis

68% legacy telecom to 38%

17

Frontier Communications Corp.

Pattern in M&A and strategic activity

▫ Long history of acquisitions of wireline assets to gain scale

▫ No apparent geographic limitations

▫ Focus on broadband-ready plant and “lead with broadband” services

Strategic goals

▫ Gain wireline scale which provides strategic flexibility and optionality while leveraging core competencies

We “like the scale deals because they involve businesses that we know, that we run today. . . We know what the underlying operating issue are. We know what the economics are.”

▫ Drive cash flow growth through scale economies and enhanced operating efficiency

▫ Revenue and customer stability / growth through increased market share in underserved acquired markets (80% broadband share in residential markets; 83% of households can get 6 Mbps and 55% can get 20 Mbps)

▫ Increased exposure to more competitive urban / suburban markets

September 2016WTA 2016 Fall Meeting

18

Frontier Communications Corp.

Tracking strategic progress and transformation

▫ Serve 29 states across the U.S. post-acquisition of VZ ops in CA/TX/FL

▫ Significant ongoing growth in customer base through wireline acquisitions

Acquired and integrated operations with approx. 2.5 million RGUs (no video) by YE 2006

Prior to VZ CA/TX/FL deal, approx. 6.9 million RGUs (incl. AT&T CT ops)

Pro forma for CA/TX/FL approx. 13.9 million RGUs (incl. 1.8 million video subs)

▫ Post-acquisition pro forma revenues approx. $11.7 billion, up from $2.0 billion at YE 2006

September 2016WTA 2016 Fall Meeting

21% data/internet to 42%

19

Consolidated Communications

Pattern in M&A and strategic activity

▫ History of acquiring wireline assets to gain scale

▫ Acquisitions often include diversification opportunities

▫ No apparent geographic limitations; focus on relatively sizeable opportunities resulting in “clusters” across the U.S. (CA, IL, KS, TX, PA, MN/IA) with some critical mass

▫ Emphasis on video / IPTV and broadband plant that is video-capable

▫ Significant focus on fiber-rich targets

Strategic goals

▫ Gain wireline scale which provides strategic flexibility and optionality while leveraging core competencies; expand platform for future opportunities

▫ Drive cash flow growth through scale economies and enhanced operating efficiency

▫ Increased exposure to more competitive urban / suburban markets

▫ Reduce reliance on regulatory revenue streams

September 2016WTA 2016 Fall Meeting

20

Consolidated Communications

September 2016

Source: Company filings, press releases, and Charlesmead analysis

WTA 2016 Fall Meeting

9% broadband/data/internet to 51%

Tracking strategic progress and transformation

▫ Multiple operating clusters in seven states across the U.S.; larger, more diversified

▫ Emphasis on business, fiber (regional networks, FTTT), and data services

Data/internet/broadband has grown from 9% of revenues in 2005 to approx. 51% in 2015

Pro forma for Enventis, 78% of revenues from business and broadband services

Voice revs are approx. 40% of total from approx. 80% in 2005

21

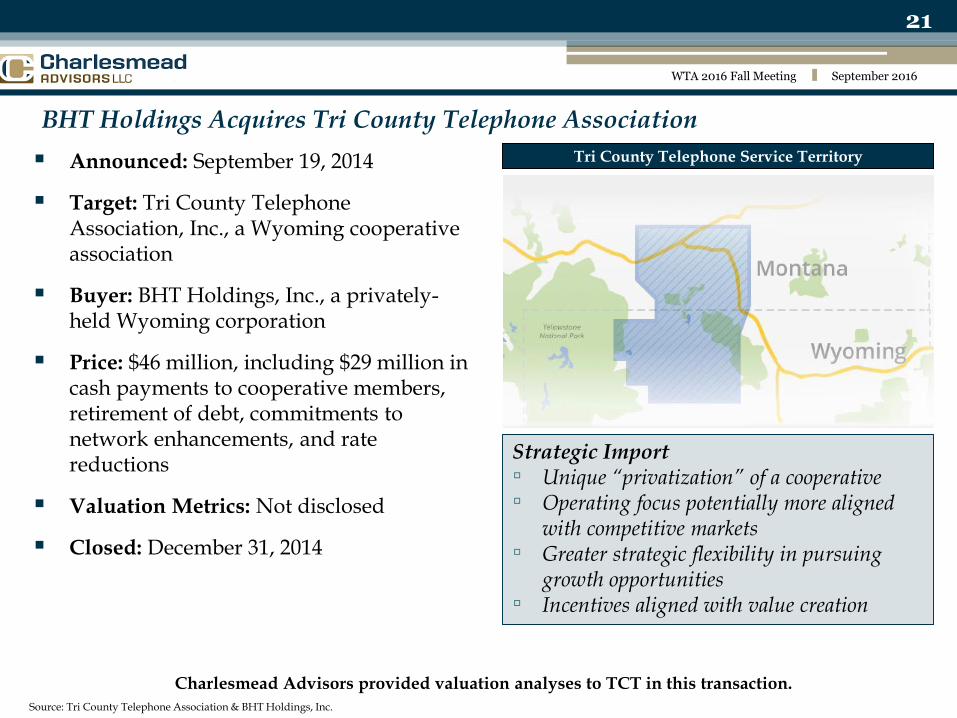

BHT Holdings Acquires Tri County Telephone Association

Announced: September 19, 2014

Target: Tri County Telephone Association, Inc., a Wyoming cooperative association

Buyer: BHT Holdings, Inc., a privately-held Wyoming corporation

Price: $46 million, including $29 million in cash payments to cooperative members, retirement of debt, commitments to network enhancements, and rate reductions

Valuation Metrics: Not disclosed

Closed: December 31, 2014

September 2016WTA 2016 Fall Meeting

Charlesmead Advisors provided valuation analyses to TCT in this transaction.

Tri County Telephone Service Territory

Strategic Import▫ Unique “privatization” of a cooperative▫ Operating focus potentially more aligned

with competitive markets▫ Greater strategic flexibility in pursuing

growth opportunities▫ Incentives aligned with value creation

Source: Tri County Telephone Association & BHT Holdings, Inc.

22

Ritter Communications Acquires Millington Telephone Co.

September 2016WTA 2016 Fall Meeting

Announced: September 25, 2012

Target: Millington Telephone Company, Inc. and Millington CATV, Inc.

Buyer: Ritter Communications Holdings, Inc.

Price: Not disclosed

Valuation: Not disclosed

Closed: December 11, 2012

Charlesmead Advisors served as exclusive financial advisor to Ritter Communications in this transaction.

Source: Ritter Communications press release

Strategic Import▫ Enhanced scope & scale▫ Further diversification into CATV▫ Increased exposure to more urban markets

(Memphis)

Combined Service Territory Map

Fayetteville

Fort Smith

Little Rock

Hot Springs

MemphisSomerville

Brownsville

BlythevilleJonesboro

MarkedTree

MountainHome

Millington

Ritter Counties Served

Ritter Fiber Network

Millington Service Territory

Interstate Highways

Legend

23

EATEL Acquires Vision Communications and Venyu Solutions

September 2016WTA 2016 Fall Meeting

Vision Communications

▫ Announced: September 20, 2011

▫ Closed: January 5, 2012

▫ Price: Undisclosed

▫ Assets: Headquartered in Larose, Vision serves residential and commercial customers in central and southern Lafourche and southern Jefferson Parishes; ≈9,850 access lines

Venyu Solutions

▫ Closed: August 31, 2013

▫ Price: Undisclosed

▫ Assets: Venyu is a national provider of data center, managed hosting, cloud, virtualization, and data protection solutions

Strategic Import▫ Enhanced scope & scale▫ Diversification into CATV & data

centers/managed services▫ Reduced regulatory exposure▫ Geographic diversification – telco and data

centers

EATEL Pro Forma Service Territory

Charlesmead Advisors served as exclusive financial advisor to EATEL in these transactions.

Source: EATEL Corporation

EATEL Markets

Vision Markets

Venyu Facilities

Legend

`

24

Internet Infrastructure - Selected Carrier Investments

September 2016WTA 2016 Fall Meeting

> Comporium has been the principal investor since founding in 2007

> Operates four data centers in South Carolina providing an integrated suite of managed services/infrastructure solutions for business applications

> Services include colocation, dedicated Internet access, data backup & recovery, network monitoring, virtualized dedicated services, and security

> Acquired 2012: Two data centers and disaster recovery space located within a 120,000 square foot facility in Winston-Salem, North Carolina; 30,000 square-foot facility in Raleigh; currently expanding into Charlotte

> Remote hands, cloud services, managed database, firewall, VPNs, data protection, advanced server, desktop, network, and application monitoring

> Formed through the combination of several acquisitions

> Vital Support Systems (Des Moines) – June 2012. Three data centers totaling 130,000 sq. ft. in Madison; Des Moines and Cedar Falls, IA

> OneNeck IT Services (Scottsdale) – June 2011: leading hosted application management and MSP offering a suite of ERP outsourcing solutions

> VISI (Twin Cities) acquired March 2010. Operates two data centers and over 70,000 gross square feet; serving 10,000 business and residential customers

> Acquired 2013: Operates data center facilities in Baton Rouge and Shreveport-Bossier City, Louisiana; currently expanding operations

> Offers cloud hosting, colocation, managed hosting, colocation hosting, cloud backup, and disaster recovery

ILEC Data Center Description

Source: Company filings, press releases, and investor presentations.

BLM Acquisition Corp.

> Acquired June 2015 by 32 rural telcos from Catalyst Investors

> Plan to provide telecom, broadband, and IT services to suburban and rural populations throughout the United States

25

September 2016WTA 2016 Fall Meeting

26

Illustrative Strategy Based on Value Creation

September 2016WTA 2016 Fall Meeting

Current and next slide highlight strategic “logic”

This initial slide outlines illustrative assumptions

▫ No change in business growth rates

▫ No change in valuation multiples

▫ Percentage contribution from illustrative segment revenues

▫ ILEC plus end-user broadband (DSL/fiber) in illustration starts at 65% of total revenues

▫ Goal is to change the telco’s underlying valuation, not through passive financial investments, but through strategic investments in core businesses supporting customer-enterprises and data services

Assumed % of Yr 0

revenues

Assumed annual

revenue growth

EBITDA

margins

EBITDA as %

of total rev

Assumed

EBITDA multiple

Base year

EBITDA

ILEC voice 40% -5% 35% 14.0% 5.0x 14.00$

Broadband / DSL 25% 2% 30% 7.5% 6.0x 7.50$

Fiber to the tower 10% 10% 70% 7.0% 6.5x 7.00$

Fiber transport 10% 10% 60% 6.0% 7.0x 6.00$

Data center 15% 15% 37% 5.6% 11.0x 5.55$

100% 40.1% 40.05$

27

Illustrative Valuation with Growth Initiatives

September 2016WTA 2016 Fall Meeting

Value is created through cash-flow growth and higher-multiple businesses

Strategic value transformation is the goal

▫ LEC/Broadband change from 44% of value in Year 0 to 23% in Year 7

▫ LEC/Broadband cash flows contract by 13% over 7 years (LEC voice declines by 30%)

▫ Total value rises in Year 7 v. Year 0 by 65% in spite of net ILEC/BB contraction

▫ 7-year valuation CAGR is 7.4% and YOY growth rate is accelerating

Key message is that the new segments have growth opportunities AND higher valuations which can dramatically alter the long-term viability and valuation of the communications service provider

ILEC (Voice) Broadband Fiber-to-the-Tower Fiber Transport Data Center

28

Regulatory Changes are Driving RLEC Strategic Change

The 2011 Transformation Order has fundamentally altered the financial model

▫ Loss of terminating access and contracting USF have changed the income statement

▫ Complexity and unpredictability have increased balance sheet risk

▫ Valuation of the RLEC business continues to be pressured

Constructive responses for rural carriers include

▫ Acquisitions to increase scale and geographic diversity

▫ Significant services in support of wireless towers

▫ Fiber transport

▫ Data centers

Cooperatives

▫ Evaluating acquisitions

▫ Considering data centers

▫ Assessing structural changes including privatizing

September 2016WTA 2016 Fall Meeting

29

Summary

Regulatory changes are ongoing and significant

▫ Changing balance sheet and income statement risk

▫ Driving new strategic choices

▫ New changes have the potential to raise the RLEC risk

Data opportunities are significant

▫ Good growth

▫ Sustainable demand

▫ Exceptional valuations

Strategic planning is critical

▫ Viability of long-term business

▫ Preservation or creation of value

September 2016WTA 2016 Fall Meeting

30

Representative Transactions (1)

September 2016WTA 2016 Fall Meeting

(1) Includes transactions completed by Charlesmead professionals at predecessor firms.

Have Acquired

Heartland

Communications from

Advisor to Buyers

August 2016

Has Sold Spectrum

Licenses to

Advisor to Seller

December 2013

Advisor to Buyer

August 2013

Has Acquired Has Sold its Wireless

Partnership Interest to

Advisor to Seller

November 2013

Have Sold Their

Equity Interest in

BPB BIDCO to

Advisor to Sellers

May 2014

Has Sold Its Wireless

Tower Portfolio to

Advisor to Seller

December 2013

Has Acquired

Advisor to Buyer

December 2011

Has Acquired

Advisor to Buyer

January 2012

Has Acquired

Spectrum from

Advisor to Buyer

February 2012

Has Sold Spectrum

Licenses to

Advisor to Seller

July 2012

Has Acquired

Advisor to Buyer

December 2012

Has Sold Its Wireless

Operation to

Advisor to Seller

July 2013

Has SoldFremont Telcom Company and

Fretel Communications, LLC to

Advisor to Seller

January 2013

Advisor to Seller

April 2013

Has Sold Certain

Wireless Assets to

Advisor to Seller

June 2013

Has Sold Spectrum

Licenses to

Has Sold Its Wireless

Tower Portfolio to

Advisor to Seller

December 2012

Has sold Its Wireless

Operation to

Advisor to Seller

May 2015

Has Sold Spectrum

Licenses to

Advisor to Seller

January 2015

Has Sold Its North

Carolina Operations to

Advisor to Seller

May 2015

Has Sold its

Operation to

Valuation for Seller

December 2014

Big Horn Telecom

Holdings, Inc.

Has sold Tower

Assets to

Advisor to Seller

July 2015

Has Sold Certain

Arkansas and

Oklahoma

Operations to

Advisor to Seller

December 2015

Advisor to Sellers

March 2014

Have Sold Their

Wireless Partnership

Interests to

Has Sold Spectrum

Licenses to

Advisor to Seller

May 2016

Advisor to Seller

February 2016

Has Sold Spectrum

Licenses to

Advisor to Seller

March 2016

Has Sold Spectrum

Licenses to