Embed Size (px)

Citation preview

TEEKAYTEEKAY

TEEKAY TANKERS Q4 AND FISCAL 2015 EARNINGS PRESENTATION

February 19, 2016

2

Forward Looking Statements

This presentation contains forward-looking statements (as defined in Section 21E of the Securities Exchange Act of 1934,

as amended) which reflect management’s current views with respect to certain future events and performance, including

statements regarding: future dividend payout ratio; the impact of the U.S. government’s decision to lift the ban on crude oil

exports, including new trade routes for mid-size tankers; the crude oil and refined product tanker market fundamentals,

including the balance of supply and demand in the tanker market, estimated growth in the world tanker fleet, estimated

growth in global oil demand, crude oil tanker demand and OPEC crude oil supply; tanker fleet utilization, spot tanker rates,

the potential for localized floating storage and port delays and future newbuild ordering; the effect of lower global oil

prices, including the potential impact on oil stockpiling, refinery throughput and bunker fuel prices; the impact of the tanker

market on the Company’s earnings, free cash flow, net asset value, future dividends and financial leverage, including the

estimated dividend payout range; the delivery of one chartered-in Aframax tanker; the impact of the lightering Aframax

tanker acquisition on the Company’s earnings and free cash flow per share; and the impact on the Company’s debt

maturity profile and financial flexibility as a result of the new $900 million long-term debt facility, including the Company’s

scheduled repayments. The following factors are among those that could cause actual results to differ materially from the

forward-looking statements, which involve risks and uncertainties, and that should be considered in evaluating any such

statement: changes in the production of, or demand for, oil or refined products; changes in trading patterns significantly

affecting overall vessel tonnage requirements; greater or less than anticipated levels of tanker newbuilding orders and

deliveries and greater or less than anticipated rates of tanker scrapping; changes in global oil prices; changes in

applicable industry laws and regulations and the timing of implementation of new laws and regulations; the amount of

cash reserves established by the Company’s Board of Directors; actual payout ratio determined by the Company’s Board

of Directors; increased costs; and other factors discussed in Teekay Tankers’ filings from time to time with the United

States Securities and Exchange Commission, including its Report on Form 20-F for the fiscal year ended December 31,

2014 and on Form 6-K for the quarters ended March 31, 2015, June 30, 2015 and September 30, 2015. The Company

expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any forward-looking

statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in

events, conditions or circumstances on which any such statement is based.

3

Recent Highlights • Q4-15 Financial Results

○ Generated adjusted net income1 of

$48.5 million, or $0.31 per share,

versus adjusted net income of

$18.6 million, or $0.21 per share in

Q4-14

○ Generated free cash flow1 of $74.0

million, or $0.48 per share, versus

$31.7 million, or $0.35 per share in

Q4-14

• Implemented new earnings-based

variable dividend policy

• Acquired two purpose-built lightering

Aframaxes for $80 million en bloc to

bolster strategic US Gulf presence

• Refinanced majority of fleet through

new five-year, ~$900 million debt

facility

(1) See the Q4-15 earnings release for explanations and reconciliations of these non-

GAAP measures to the most directly comparable financial measures under GAAP.

4

• Distribute 30% to 50% of quarterly adjusted net income, while maintaining minimum

quarterly dividend of $0.03 per share

○ Significantly increased dividend from $0.03 per share to $0.12 per share in Q4-15

• New dividend policy provides investors opportunity to directly participate in Company’s

strong free cash flow

• Maintains financial flexibility and allows for continued balance sheet delevering

Dividend Increase Rewarding shareholders while continuing to build financial strength

Annual Dividend Per Share1

(1) Based on estimated results for fiscal year 2016 assuming current fleet

(2) Aframax equivalent TCE: Suezmax = 1.30x, LR2 = 1.00x, MR = 0.70x

(3) Based on 40% dividend payout

(4) Pro-forma to include Q1-15 vessel acquisitions that were committed for in Q4-14

60%4

55%

46%

72%

43%

40%

30%

40%

50%

60%

70%

80%

Q4-2013 Q4-2014 Q4-2015 Q4-2016

Net Debt to Book Capitalization

Financial Leverage3

Aframax Equivalent TCE2

$25,000

$30,000

$35,000

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$10,000 $15,000 $20,000 $25,000 $30,000 $35,000

$ P

er

Sh

are

Aframax Equivalent TCE2

Payout range based

on new variable

dividend policy

Dividend Floor

5

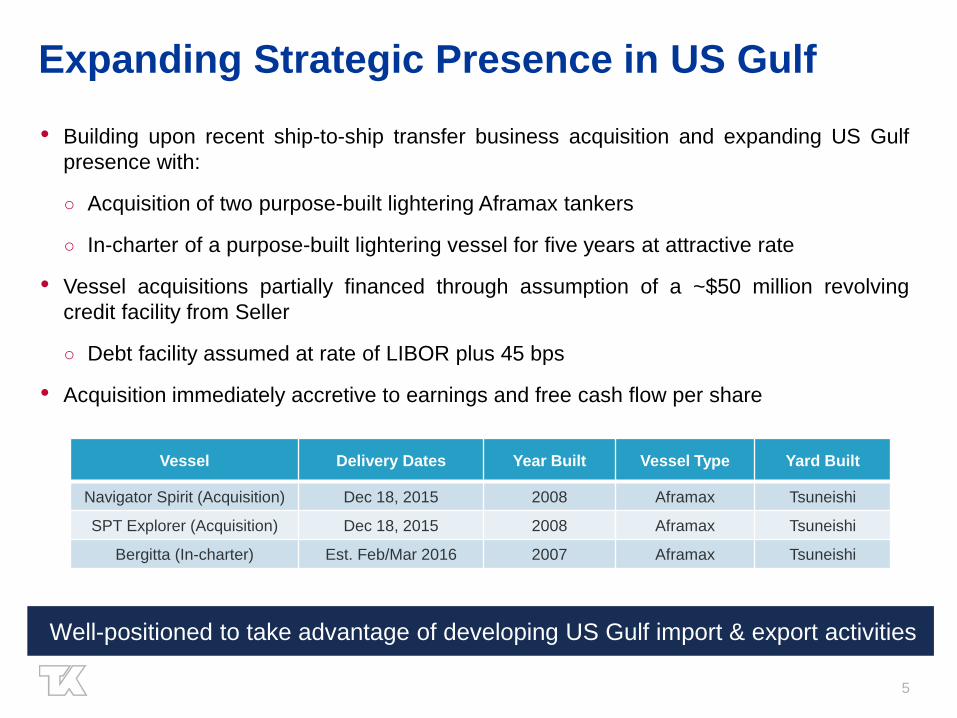

Vessel Delivery Dates Year Built Vessel Type Yard Built

Navigator Spirit (Acquisition) Dec 18, 2015 2008 Aframax Tsuneishi

SPT Explorer (Acquisition) Dec 18, 2015 2008 Aframax Tsuneishi

Bergitta (In-charter) Est. Feb/Mar 2016 2007 Aframax Tsuneishi

Expanding Strategic Presence in US Gulf

• Building upon recent ship-to-ship transfer business acquisition and expanding US Gulf

presence with:

○ Acquisition of two purpose-built lightering Aframax tankers

○ In-charter of a purpose-built lightering vessel for five years at attractive rate

• Vessel acquisitions partially financed through assumption of a ~$50 million revolving

credit facility from Seller

○ Debt facility assumed at rate of LIBOR plus 45 bps

• Acquisition immediately accretive to earnings and free cash flow per share

Well-positioned to take advantage of developing US Gulf import & export activities

6

Secured New Debt Facility

• Completed ~$900 million debt facility in January 2016 which includes both term loan and

revolving credit facility components

○ 1.4 times oversubscribed

○ Used to refinance 36 existing vessels

○ Replaces five facilities including TNK’s two bridge loans which matured in January

2016 and its main revolving credit facility which was scheduled to mature in November

2017

• Provides financial flexibility while extending debt maturity profile to 2021

2016 2017 2018 2019 2020 2021

0

100

200

300

400

500

600

700

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19

$ M

illio

ns

Pre-refinancing (Scheduled Repayments) Pre-refinancing (Bullet Payments)

Post-refinancing (Scheduled Repayments) Post-refinancing (Bullet Payments)

Scheduled Debt Repayment Profile (Assumes Revolving Credit Facilities are Fully Drawn)

7

0

10,000

20,000

30,000

40,000

50,000

60,000

US

D/d

ay

2015 Crude Tanker Rates

Suezmax Aframax

0 10,000 20,000 30,000 40,000 50,000

Aframax

Suezmax

$ / day

Annual Average Crude Tanker Rates

2015

2014

2013

2012

2011

2010

2009

2015: Strongest Crude Tanker Rates In 7 Years

Source: 90% Clarksons

Low fleet growth and surging demand gave rise to rate volatility

• The strong tanker market in 2015 was driven by a combination of factors:

○ Low crude tanker fleet growth of ~2%

○ 1.0 mb/d increase in OPEC crude oil production led by Saudi Arabia and Iraq

○ 5-year high global oil demand growth of 1.7 mb/d

○ Strong refining margins, strategic & commercial stockpiling and lower bunker prices

were all driven by the lowest crude oil prices seen in 11 year (averaging $52 / bbl)

8

2016: Strong Demand Fundamentals Intact

93.5

94.0

94.5

95.0

95.5

96.0

96.5

97.0

Q1-2016 Q2-2016 Q3-2016 Q4-2016

Millio

n b

bl /

day

Rising Global Oil Demand

Source: IEA

0

50

100

150

200

250

300

350

400

2016 Stockbuild Storage Capacity

Millio

n B

arr

els

2016 Stock build vs. Spare Storage Capacity

New Capacity -China

New Capacity -Other

Available USStorage

Source: IEA

Low oil prices are positive for tanker demand

• Global oil demand is expected to grow by ~1.2 mb/d

• Increase in crude trade volumes due to rising OPEC supply (Iran +0.5 mb/d)

• Ullage delays / floating storage as a result of rising global oil inventories

• Vessel fuel costs expected to remain low due to weak global bunker prices

9

New Trade Routes for Mid-Size Tankers US import / export changes & Panama Canal expansion create opportunities

PANAMA CANAL

Expansion from Q2-16 may drive transshipment

opportunities through the Canal:

• US crude & product to Asia on Aframaxes / LR2s

• WCSA crude to USG / Caribs or CBS to USWC and Asia

US GULF

New import / export dynamics have the potential to drive

increased demand for STS services via:

• A return to long haul imports from WAF and Middle East

• Reverse lightering for new US crude exports

• The US is now free to export surplus light sweet crude to markets in Europe and Asia

• Volume of trade dependent on relative pricing between US crude and international grades (exports

will increase when US crude is trading at a discount)

• Conversely, US Atlantic Coast refineries may import more WAF crude on Suezmaxes when US crude

is trading at a premium

10

Fleet Utilization Remains High in 2016 Demand growth is sufficient to largely offset higher tanker fleet growth

78%

80%

82%

84%

86%

88%

90%

92%

-2%

0%

2%

4%

6%

8%2

00

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6E

% F

lee

t U

tili

za

tio

n

% S

up

ply

/ D

em

an

d G

row

th

Tanker Demand Growth Tanker Supply Growth Fleet Utilization

Source: Clarksons / Internal Assumptions

• Tanker ordering is expected to moderate in 2016 as owners face additional cost of NOx Tier

III compliance.

• Tighter credit conditions and lack of private equity interest in the sector will dampen new-build

demand

○ No tanker orders have been placed in 2016-to-date

• Ballast Water Treatment Systems (BWTS) legislation could give upside to scrapping in the

next 12-24 months

11

Q1-16 Spot Earnings Update

• Spot rates averaged significantly higher year-on-year in Q4-15

• Strong demand fundamentals lead to continued strength in Q1-16

Suezmax Aframax LR2

Q1-16 spot ship

days 1,717 1,369 731

Q1-16 % booked

to-date 63% 54% 54%

$39,433

$30,708

$24,899

$40,580

$28,393 $27,120

$-

$10,000

$20,000

$30,000

$40,000

$50,000

Suezmax Aframax RSA LR2

Q1-15 Actual Q1-16 to-date

$26,627 $25,677

$21,884

$41,430

$31,575

$26,468

$-

$10,000

$20,000

$30,000

$40,000

$50,000

Suezmax Aframax RSA LR2

Q4-14 Actual Q4-15 Actual

12

Building our brand, our capabilities and our financial strength

Focusing on core segments, aligning sea and shore capabilities to

drive our operational excellence

Expansion and modernization of our fleet • Invested ~$1 billion in 19 modern Suezmax, Aframax and LR2 tankers

• Reduced our fleet age profile by 2 years

• Generated $42 million of net income through 15 in-chartered vessels

Refocusing customer strategy by consolidating Teekay Tanker brand • Brought technical management back in-house

• Brought all our fleet’s commercial management back under Teekay control

• Added new services dimension in form of Ship-to-Ship transfer capabilities

Enhancing financial strength and rewarding shareholder loyalty • Reduced financial leverage to 55% in 2015

• Implemented higher pay-out variable dividend policy

• Refinanced debt facilities

2015 Year in Review

13

APPENDIX

14

Fleet Employment Profile

(1) 50/50 profit share if earnings are above $12,000/day and $13,000/day, respectively

(2) 50/50 profit share if earnings are between $16,000 and $24,000 /day plus 75/25 profit share in TNK’s favor if earnings are above

$24,001/day

(3) The Company’s ownership interest in this vessel is 50%. 50/50 profit share if earnings are above $40,500/day

In-Charter Portfolio

Aframax 2008

Aframax 2008

Aframax 2008

Aframax 2008

Aframax 2009

Aframax 2008

Aframax 2008

Aframax 2008

Aframax 2003

Aframax 2007

Aframax 2002

LR2 2006

LR2 2009

LR2 2001

Out-Charter Porfolio

Aframax 2004

Aframax 2005

Aframax 2008

Aframax 2004

Aframax 2005

Aframax 2004

Aframax 2004

LR2 2001

Suezmax 2012

Suezmax 2006

Suezmax 2006

Suezmax 2009

Suezmax 2004

VLCC 2013

4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

$12,000 (1)

$18,600

$25,000

$21,000

Optional Period

$32,906

$29,000

$24,900

$17,750

$17,750

$18,500

$20,500

$16,000 (2)

$16,250

$18,900

$22,000

$22,000

$15,600

$16,750

$24,000

$19,500

$18,066

$32,906

$18,066

$25,000

$37,500 (3)

$28,000

$19,500

$22,750

Optional Period

$13,000(1)

Optional Period

$26,000 Optional Period

Optional Period

$15,500

15

Drydock & Offhire Schedule

Teekay Tankers

Segment

Vessels

Total

Off-hire

Days

Vessels

Total

Off-hire

Days

Vessels

Total

Off-hire

Days

Vessels

Total

Off-hire

Days

Vessels

Total

Off-hire

Days

Spot Tanker 1 10 1 23 1 14 - - 3 47

Fixed-Rate Tanker 1 91 - 15 - - - - 1 106

2 101 1 38 1 14 - - 4 153

Note:

(1) In the case that a vessel drydock straddles between quarters, the drydock has been allocated to the quarter in which majority of drydock days occur.

(2) Only owned vessels were accounted for in this schedule.

March 31, 2016 (E) June 30, 2016 (E) September 30, 2016 (E) December 31, 2016 (E) Total 2016

16

Q4-15 vs. Q3-15 Results

• $40m increase from the Principal vessels acquired during Q3-15 and Q4-15;

• $2m increase from a full quarter impact of the full service lightering and lightering

support business from the acquisition of SPT; and partially offset by

• $2m decrease from heavier drydocking activity;

• $2m decrease due to employment changes;

• $1m decrease due to lower average realized spot TCE rates; and

• $1m decrease due to the sale of the Mahanadi Spirit .

• $10m increase due to the purchase of the Principal vessels;

• $3m increase due to timing/scope of repair and planned maintenance activities;

and

• $2m increase from a full quarter of operations for the ship-to-ship transfer

business.

Time charter hire expense (23,403) (22,600) • Increase mainly due to higher time-charter rates on two vessels from exercising

of options to extend.

Depreciation and amortization (25,130) (17,399) • Increase mainly due to the impact of the Principal vessels acquired and higher

drydock amortization costs.

General and administrative expenses (6,217) (4,138) • Increase due to higher costs associated with additional administrative, legal and

strategic support related to recent acquisitions and refinancing activity.

Income from operations 54,599 45,070

Net interest expense and realized loss on derivative

instruments

(10,002) (6,351) • Increase due to higher interest and loan cost amortization expense associated

with the bridge loan, which was to partially finance the purchase of the Principal

vessels.

• $2m increase in equity income from TIL is primarily due to a full quarter of

operations of their newly acquired vessels and higher average spot rates earned in

Q4-15; and

Equity income • $1m increase in equity income from TTOL is mainly due to higher management

fee income due to the new full services lightering pool commenced in November

2015.

Other expense (1,661) (1,341) Other expense consists mainly of freight tax expenses.

Adjusted net income attributable to shareholders

of Teekay Tankers 48,542 40,297

Adjusted net income per share 0.31 0.30

(1) Adjusted net income attributable to the shareholders of Teekay Tankers is a non-GAAP financial measure. Both periods exclude the results of Entities under Common Control. Please refer to Appendix A to the Q4-15

and Q3-15 Earnings Releases.

Vessel operating expenses (33,574)

($’000’s, except share and per share data)

Q3-15 Adjusted

(unaudited)(1) Comments

Net revenues 122,781

2,919

Q4-15 Adjusted

(unaudited)(1)

157,907

(48,558)

5,606