Embed Size (px)

Citation preview

Technology’s the answer!

(but what was the question?) Analytic and Transatlantic divisions in responding to climate change

Presentation to HGDC seminar, 19 November 2003

Michael Grubb

Associated Director of Policy, the Carbon Trust

Visiting Professor, Climate Change and Energy Policy, Imperial College London

Senior Research Associate, Department of Applied Economics, Cambridge

Overview

The basic issue of technology-push vs demand-pull: - examples and significance

Economic theory and technology innovation – The different conceptions – evidence, strengths and

weaknesses– Integrated perspectives– Practical problems arising from incomplete theories of

innovation – Some implications for UK strategy – Technology perspectives and Kyoto strategies

Some additional observations on energy policy and technology

Conclusions

The basic issue

Technology is the answer!– All studies agree that low carbon technology is central to

addressing long-term climate change– Technologies adequate to stabilise the atmosphere are not

yet commercially available

But what was the question?– Is this a question of R&D investment by governments to

develop the technologies that can solve the problem (‘technology push’ / exogenous technical change)?

– Or a question of market incentives to promote private sector investment in emerging technologies and learning-by-doing (‘demand pull’ / induced technical change)

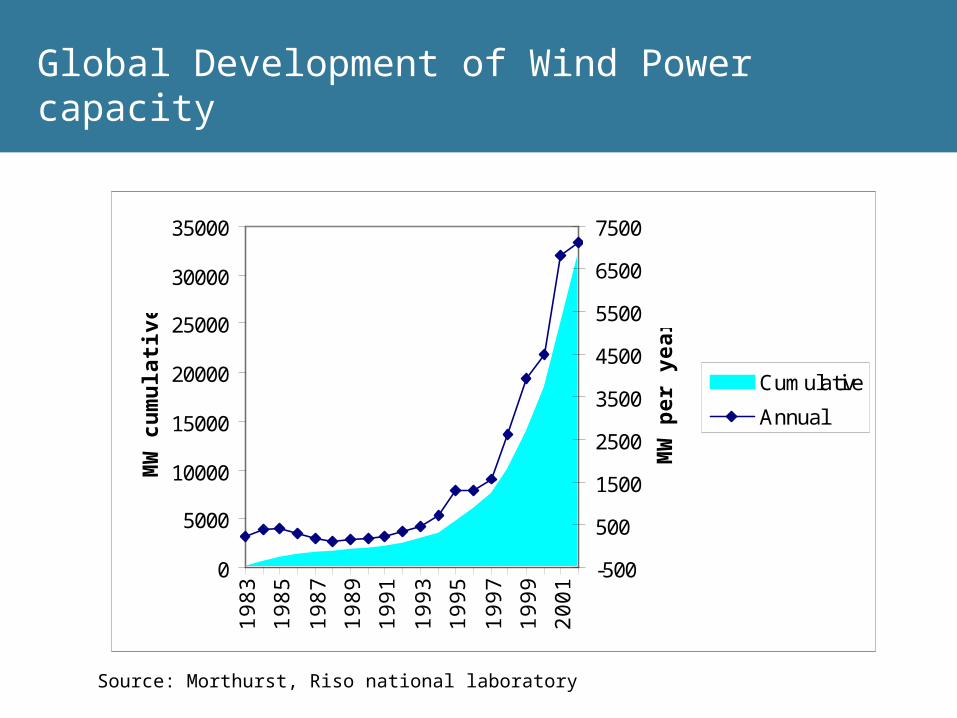

Global Development of Wind Power capacity

0

5000

10000

15000

20000

25000

30000

3500019

83

1985

1987

1989

1991

1993

1995

1997

1999

2001

MW

cu

mu

lati

ve

-500

500

1500

2500

3500

4500

5500

6500

7500

MW

per

yea

r

Cumulative

Annual

Source: Morthurst, Riso national laboratory

Cost trends in wind energy, historic and projections compared to conventional power production

0

2

4

6

8

10

12

1985 1987 1990 1993 1996 1999 2001

Time

c€/k

Wh

Coastal site

Inland site

Gasfired power plantsDenmark Norway

Source: Morthurst, Riso national laboratory

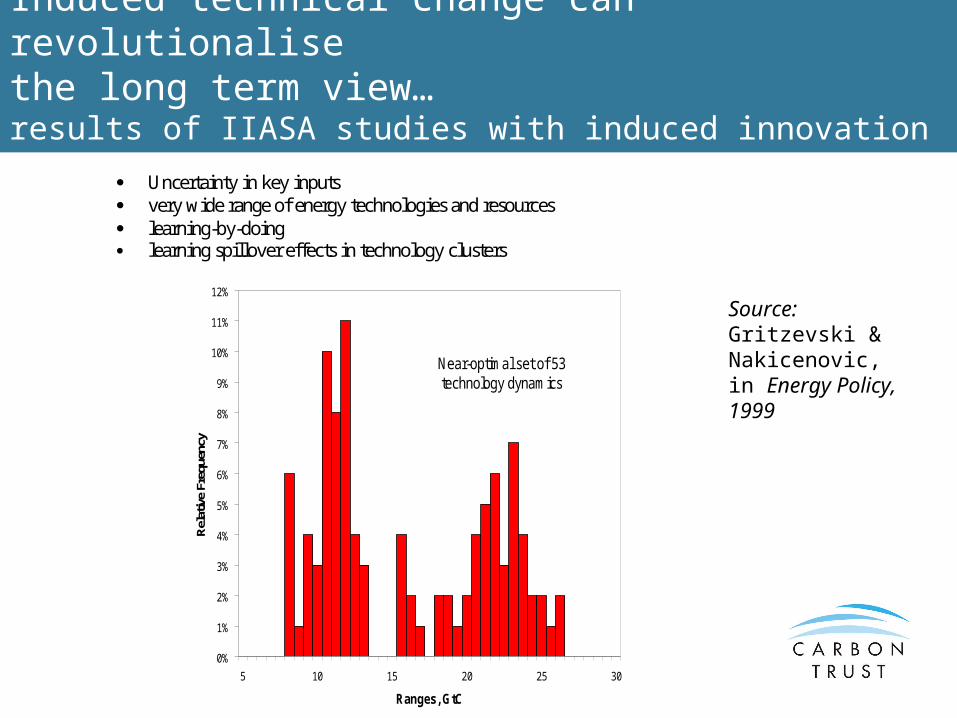

Induced technical change can revolutionalise the long term view… results of IIASA studies with induced innovation

Uncertainty in key inputs very wide range of energy technologies and resources learning-by-doing learning spillover effects in technology clusters

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

5 10 15 20 25 30

Ranges, GtC

Rel

ativ

e Fr

eque

ncy

Near-optimal set of 53 technology dynamics

Source: Gritzevski & Nakicenovic, in Energy Policy, 1999

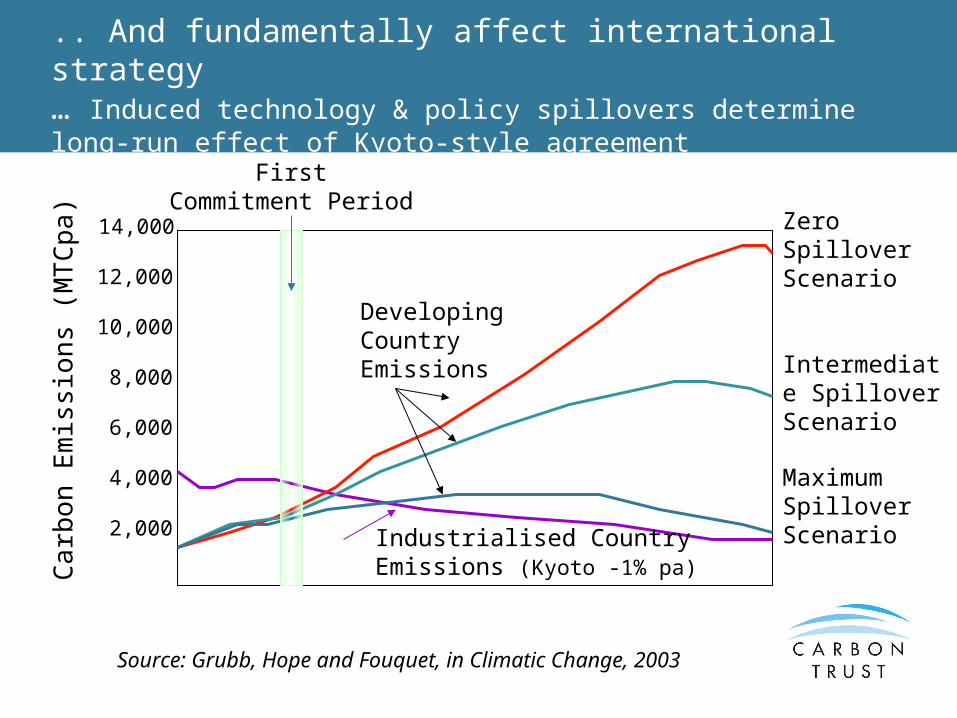

.. And fundamentally affect international strategy … Induced technology & policy spillovers determine long-run effect of Kyoto-style agreement

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Carb

on

Em

issi

on

s (M

TC

pa)

FirstCommitment Period

Zero Spillover Scenario

Intermediate Spillover Scenario

Maximum Spillover ScenarioIndustrialised Country

Emissions (Kyoto -1% pa)

Developing Country Emissions

Source: Grubb, Hope and Fouquet, in Climatic Change, 2003

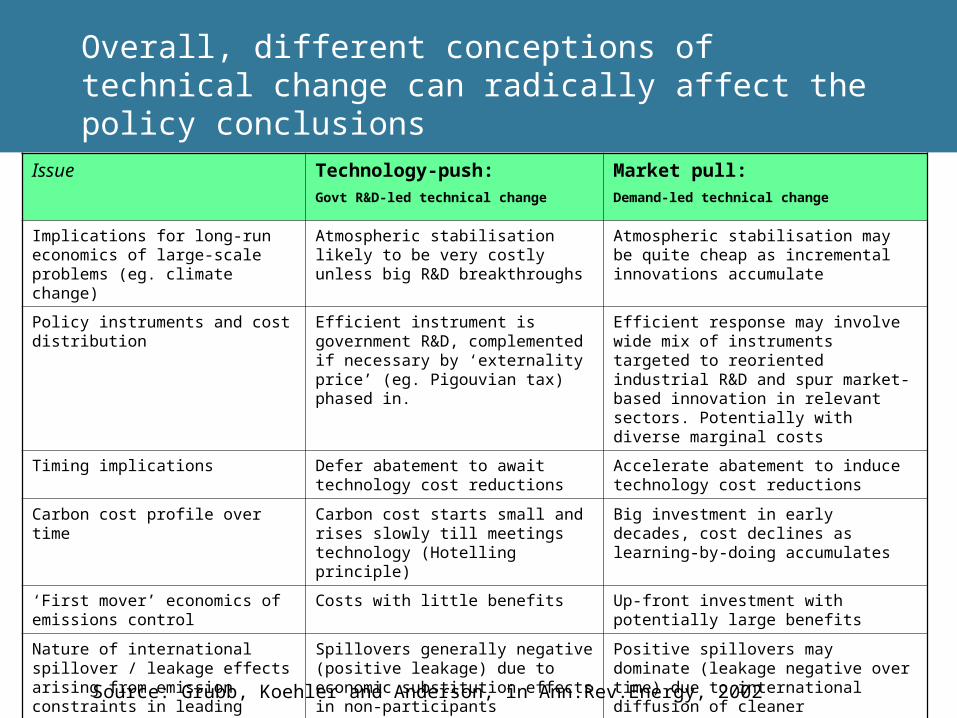

Overall, different conceptions of technical change can radically affect the policy conclusions

Issue Technology-push: Govt R&D-led technical change

Market pull: Demand-led technical change

Implications for long-run economics of large-scale problems (eg. climate change)

Atmospheric stabilisation likely to be very costly unless big R&D breakthroughs

Atmospheric stabilisation may be quite cheap as incremental innovations accumulate

Policy instruments and cost distribution

Efficient instrument is government R&D, complemented if necessary by ‘externality price’ (eg. Pigouvian tax) phased in.

Efficient response may involve wide mix of instruments targeted to reoriented industrial R&D and spur market-based innovation in relevant sectors. Potentially with diverse marginal costs

Timing implications Defer abatement to await technology cost reductions

Accelerate abatement to induce technology cost reductions

Carbon cost profile over time Carbon cost starts small and rises slowly till meetings technology (Hotelling principle)

Big investment in early decades, cost declines as learning-by-doing accumulates

‘First mover’ economics of emissions control

Costs with little benefits Up-front investment with potentially large benefits

Nature of international spillover / leakage effects arising from emission constraints in leading countries

Spillovers generally negative (positive leakage) due to economic substitution effects in non-participants

Positive spillovers may dominate (leakage negative over time) due to international diffusion of cleaner technologies

Source: Grubb, Koehler and Anderson, in Ann.Rev.Energy, 2002

Economic theory and environmental innovation policies

Technology-R&D push – the track record is not encouraging..

The theoretical basis– Classic R&D market failures– The impact of liberalisation

Some classic energy examples:– Nuclear fission– Coal-based synthetic fuels– Nuclear fusion

Basic problems of:– ‘picking winners’– Cooperation vs competition– Policy displacement

Theoretical paradox of the ‘classical’ view– the giant leap – the ‘valley of death’

Demand-led induced technical change – if only markets were so perfect ..

Some classic energy examples:– North sea oil – CCGTs – Wind energy …?

Basic problems of:– Classic R&D failures – Policy stability for environmental innovation– The real world is ‘second best’

Theoretical paradox of the ‘classical’ demand-led view– the need for perfect R&D markets– The need for long term certainty– The need for perfect communication between government,

research, and industry

Diffusion

Integrated perspectives: technologies have to traverse a long, expensive and risky chain of innovation to get from idea to market

Government

Research Consumers

Policy Interventions

Business and finance community

Investments

Market accumula

tion

Commercial-isation

Demon-stration

Applied R&D

Basic R&D

Product/ Technology Push

Market Pull

Source: Foxon (2003) adapted by the author

Diffusion

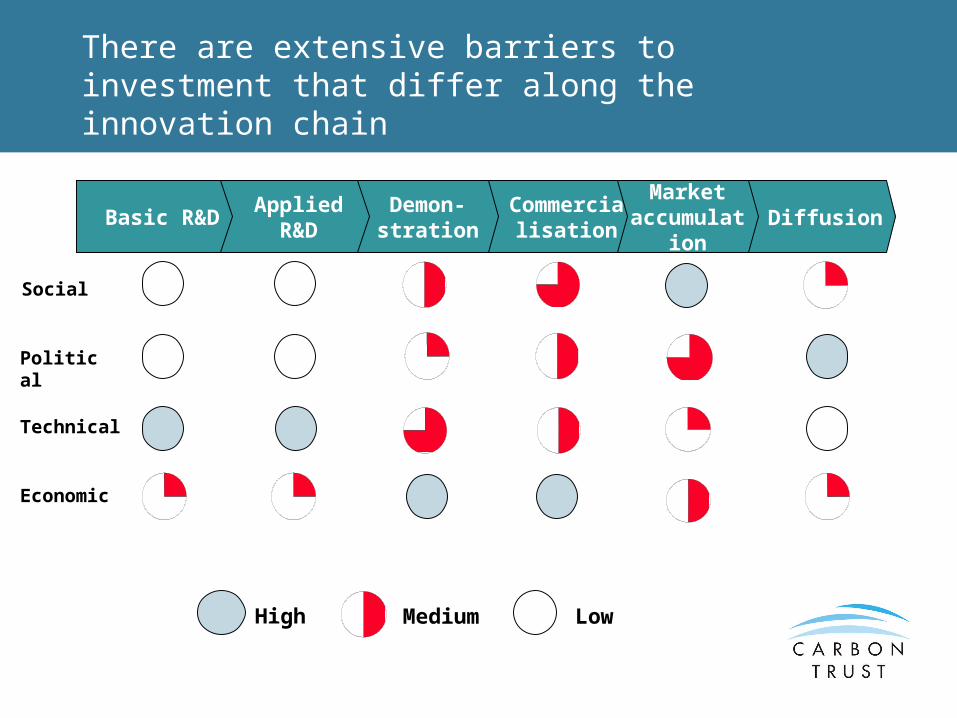

There are extensive barriers to investment that differ along the innovation chain

Market accumula

tion

Commercialisation

Demon-stration

Applied R&D

Basic R&D

Social

Technical

Economic

Political

High Medium Low

n

Diffusion

Market theory is blind to the innovation process – innovation assumed to emerge out of R&D and market pull, with government no-go zone in between

Government

Research Consumers

Carbon trading / taxation

Policy InterventionsC,C,C

Business and finance community

Investments

Market accumula

tion

Commercial-isation

Demon-stration

Applied R&D

Basic R&D

Product/Tech Push

Market Pull

Univ funding

Cofunding, tax breaks

C,C,C: Contentious, constrained, confused …

Consequently we lack integration across the innovation chain

New entrants (technology and corporate) – require €/$ billions, and years, of development– Compete against established incumbants and rules– Rely upon regulation to embody external costs of

incumbants

political signals of future regulation are not ‘bankable’– (‘White paper reactions’)

fierce market competition and regulatory change in electricity has left:

– Financial community extremely risk averse– companies without financial resources for longer term

investment– (‘CMI reactions’)

Some elements of integrated strategies - application for the UK

A range of policy measures are needed to help technologies traverse the innovation chain

Note: ROC excludes recycling; Capital grant based on maximum of 40% of typical capital costsSource: PIU Working Papers (OXERA II Base case cost decline)

0

2

4

6

8

10

12

14

1995 2000 2005 2010 2015 2020 2025

Ele

ctr

icit

y P

ric

e (

p/k

Wh

)

Wholesale Price

ROC (Buyout)

Capital Grants/ Loans

CCL Exemption

Offshore Wave

Energy Crops

Offshore Wind

Onshore Wind

RD&D Grants

Appropriate economic support for specific technologies will vary as costs decline

General support

Technology specific support

Illustrative

Support needs to target advantaged technology groups and build upon comparative advantages- whilst market used to identify winning solutions

High Domestic Resource

High Materiality

Early mover advantage

Value added potential

Co-operate Internationally

BuildOptions

Esti

mate

d im

pact

Technology Groups

UK comparative advantage

Assessment Criteria Funding Prioritisation

Invest Aggressively

Watching brief

Low

Low High

High

Materiality of potential Carbon Trust investments

Est

imat

ed im

pac

t o

n

carb

on

em

issi

on

s

Focus• Buildings (Fabric, Ventilation, Cooling,Integrated Design)• Industry (Combustion technologies, Materials,Process control, Process intensification,Separation technologies);• Hydrogen (Infrastructure, Production,Storage and Distribution);• Fuel cells (Domestic CHP, Industrialand Commercial)• CHP (Domestic micro, Advanced macro)• Biomass for local heat generation

Consider• Solar Photovoltaics• Solar water heating collectors• Photoconversion• Wave (Offshore, Near shore devices andshoreline)• Biomass for local electricity generation• Tidal stream• Coal-bed methane• Electricity storage technologies• Buildings (Lighting, Existing building fabric,Existing building services)• Industry (Waste heat recovery).

Monitor• Buildings (Controls)• Waste to energy• Nuclear fission• Ultra-high efficiency CCGT• Smart metering• Wind• Fuel Cells (Transport, Baseload power• Biomass for Transport• Industry (Alternative Equipment)• CO2 sequestration

Limited• Intermediate energy vectors• HVDC Transmission• High Efficiency AutomotivePower Systems• Nuclear fusion• Cleaner coal combustion• Solar thermal electric• Low head hydro• Tidal (Lagoons, Barrages)• Geothermal

Carbon Trust: Low Carbon Technology Assessment seeks to classify main technologies on these bases

Some implications for Kyoto implementation and strategy

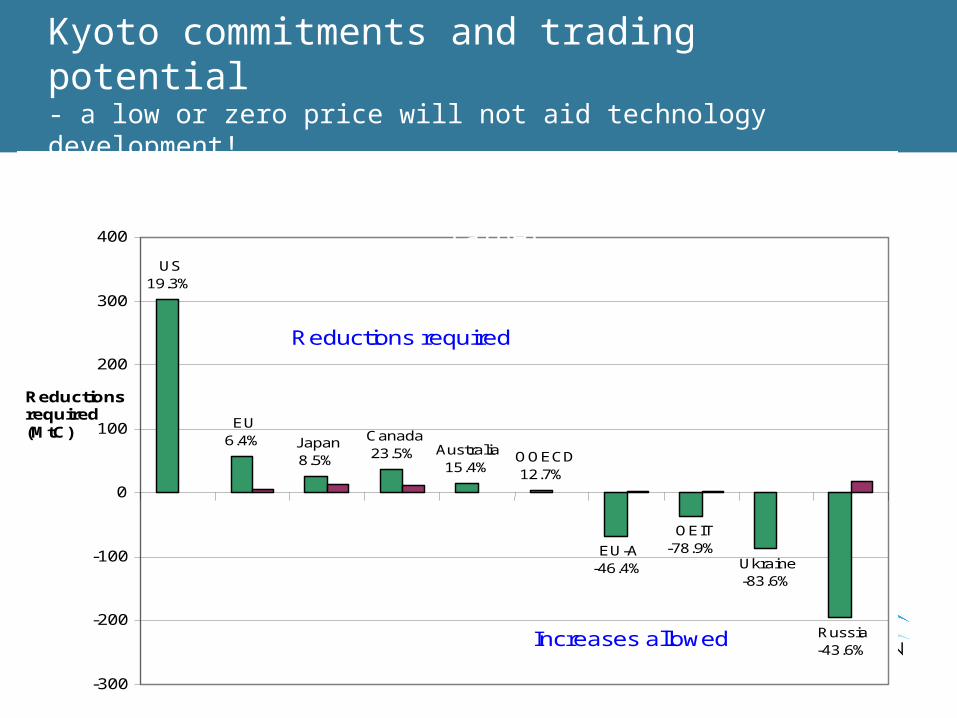

Kyoto commitments and trading potential- a low or zero price will not aid technology development!

EU 6.4%

US 19.3%

Japan 8.5%

Canada 23.5% Australia

15.4% OOECD 12.7%

EU-A -46.4%

OEIT -78.9%

Ukraine -83.6%

Russia -43.6%

-300

-200

-100

0

100

200

300

400

Reductions required (MtC)

Reductions required

Increases allowed

Gap between present (yr 2000) emissions and Kyoto target,and managed forest allowances (MtC/yr)

Analogies with the oil markets?

The oil market: International traded price far greater than marginal cost Major ‘swing’ suppliers have big influence but not monopoly power Price instability has forced restructuring of markets and relationships International collaboration to maintain oil price at ‘reasonable’ levels Strong government-industry interrelationships

Kyoto CP1 carbon market could have all these features (Russia as the Saudi Arabia; EITs as the OPEC; DCs as non-OPEC)

But important differences: Constructed commodity, depends upon institutional credibility (compliance, etc) Heirarchy of ‘environmental and political legitimacy’ Sequentially negotiated allocations CP1 massive supply-demand imbalance created by US pullout

Implications for the Kyoto mechanisms - projects

Heirarchy of value led by project mechanisms:– CDM, small projects

• renewable energy may be highest value • Potential for early start (Delhi, COP8)

– Other CDM– JI – ‘track two’ dependent upon Supervisory Cttee– JI – mainstream, forward trading contingent on meeting eligibility,

probably looser project governance

Removal Units (Annex I sink projects): variable domestic price, low international price

Total volume from international project credits limited

Implications for the Kyoto mechanisms – emissions trading

Heirarchy within AAU trading:

‘Greened’ trading: revenues linked to environmental reinvestment (Russian Green Investment Scheme)

OECD countries that exceed their targets due to domestic action (eg. UK?)

EIT exports governed through non-GIS-type routes (eg. through domestic trading with ‘acceptable’ allocation).

wholesale transfers of AAUs without any linkages or constraints (will this happen at all?)

Some broad conclusions on innovation

‘Supply push’ vs ‘demand pull’ conceptions lead to radically different perceptions and policy prescriptions

An important obstacle to effective policies is inadequate economic combined theories of industrial innovation (and especially environmental innovation):

– ‘standard’ theories yield policies that are limited in their feasibility, effectiveness and dynamic efficiency

– We have no goods tools to design the most dynamically efficient mix of policies

– But it is clear that effective policies are impeded by ‘one size fits all’ application of core policies, such as:

• New Electricity Trading Arrangements (NETA)• European State Aids

Coherent policies need to work across the innovation chain and be clear about strategic priorities and comparative advantages

Kyoto commitments and Kyoto-style structure is a foundational element to give incentives and develop global markets

Supplementary thoughts: On UK energy prospects and energy diversity

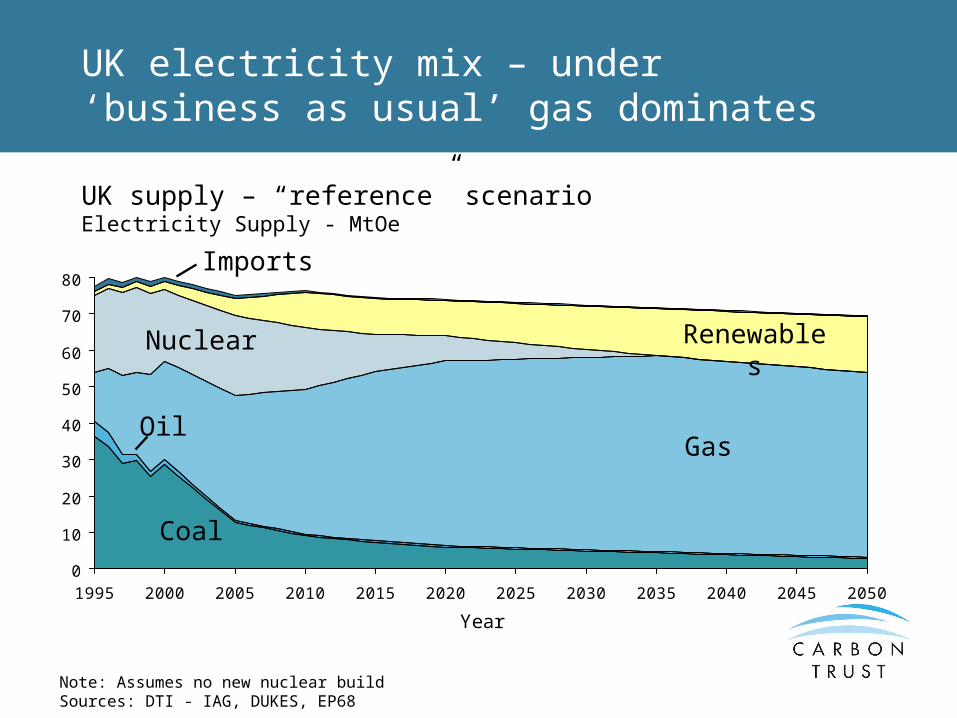

UK electricity mix – under ‘business as usual’ gas dominates

0

10

20

30

40

50

60

70

80

1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Year

Coal

Gas

Nuclear Renewables

Oil

Imports

Note: Assumes no new nuclear buildSources: DTI - IAG, DUKES, EP68

UK supply – “reference” scenarioElectricity Supply - MtOe

Greater effort on variety of renewables would lead to a more diverse set of energy sources

0

10

20

30

40

50

60

70

80

1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Year

Coal

Oil

Gas

NuclearRenewable

s

Imports

Source: CT Strategic framework analysis

UK supply – “Renewable Energy” scenarioElectricity Supply - MtOe

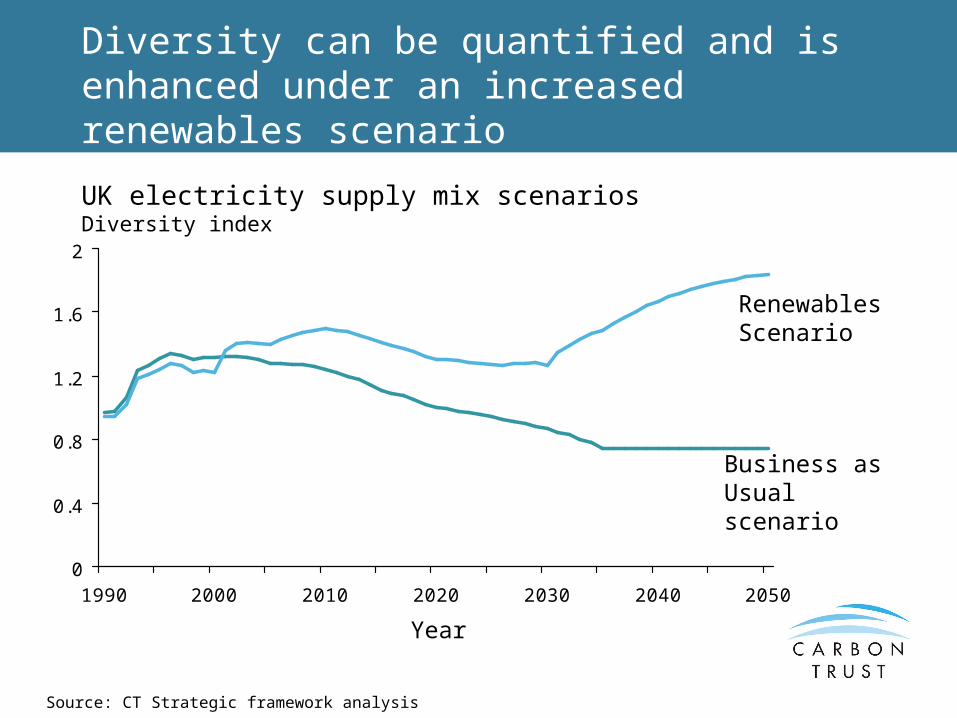

Diversity can be quantified and is enhanced under an increased renewables scenario

0

0.4

0.8

1.2

1.6

2

1990 2000 2010 2020 2030 2040 2050

Year

Renewables Scenario

Business as Usual scenario

UK electricity supply mix scenariosDiversity index

Source: CT Strategic framework analysis

Diversity – index and concentration charge

Diversity index for portfolio of I options = -ipi . ln[pi]

wherepi = the proportional reliance on the ith technology / fuel source

To encourage diversity, could levy a concentration charge, eg.

(exp[pi] – 1) cents /kWh

Would • increase marginal cost of given source as it starts to dominate• give modest boost for new entrants

UK at present relatively diverse –politically palatable starting point!

Conclusions 1: Implications of technology innovation analysis

Modern understanding of the economics of industrial innovation (and especially environmental innovation) need to be codified and applied to inform policy:

– A mix of policies is required for different stages of the innovation chain through from research to market

– Core established policies need to be adapted to avoid being impediments

International economic studies need to incorporate technology (and political) spillovers as well as economic substitution effects

The debate on ‘targets’ vs ‘technology’ is false:– Technology policies without targets (cap & trade) are ineffective– Targets without technology policies are inefficient

Kyoto provides a bedrock of credibility and carbon markets – but much more needs to be done on technology to enable deeper and wider cuts in subsequent negotiating rounds

Conclusions 2: supplementary observations on climate-technology policy

The challenge is not adding abatement costs to ‘do nothing’ future, but is to reorient €/$ trillions of investment over coming decades

– IEA World Investment Outlook

This will not happen without active intervention domestically and internationally

– Innovation is too risky, the ‘bankable’ signals of political declarations and agreements are too weak, and the obstacles to new entrants are too big

Low carbon sources can generally support security objectives, but need appropriate tools to support new entrants rather than protect high carbon existing options

– A ‘concentration charge’ to foster system diversity could be considered