Embed Size (px)

Citation preview

Scott W. Searle, CFA, (646) [email protected]

Sales (800) 933-6830, Trading (800) 933-6820

COMPANY NOTE | EQUITY RESEARCH | November 06, 2019

Technology: Communications, Wireless & IoT

Inseego Corp. | INSG - $5.31 - NASDAQ | BuyCompany UpdateEstimates Changed, Target Price Changed

Stock Data

52-Week Low - High $3.48 - $6.00Shares Out. (mil) 79.54Mkt. Cap.(mil) $422.363-Mo. Avg. Vol. 1,060,11812-Mo.Price Target $7.50Cash (mil) $13.9Tot. Debt (mil) $145.6Est. 3Yr. EPS Growth 20%Note: Cash reflects $19.7M private placement (8/6/18)

EPS $

Yr Dec —2019E— —2020E— —2021E—Curr Prev Curr

1Q (0.03)A (0.07)E (0.01)E 0.02E2Q (0.03)A (0.04)E 0.02E 0.05E3Q (0.05)A 0.00E 0.04E 0.08E4Q (0.08)E 0.06E 0.07E 0.11E

YEAR (0.19)E (0.05)E 0.12E 0.27EP/E NM NM 43.5x 19.6x

Note: EPS are pro forma adjusted

Revenue ($ millions)

Yr Dec —2019E— —2020E— —2021E—Curr Prev Curr

1Q 48.6A 53.0E 60.3E 72.2E2Q 55.9A 59.5E 66.4E 80.5E3Q 62.7A 69.2E 74.2E 88.3E4Q 53.4E 84.2E 83.0E 97.7E

YEAR 220.5E 265.9E 283.9E 338.7E

7.006.506.005.505.004.504.003.503.00

Dec

-18

Jan-

19

Feb-

19

Mar

-19

Apr

-19

May

-19

Jun-

19

Jul-1

9

Aug

-19

Sep

-19

Oct

-19

Nov

-19

10.0

8.0

6.0

4.0

2.0

0.0

PriceVol (m)

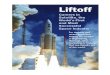

INSG One-Year Price and Volume History

INSG: 3Q Upside Muted by Verizon, But 5G(X55) Ready for 2H20 LiftoffSolid 3Q19 sales upside was muted by 4Q promotional revisions atVerizon, prompting a downward sequential guide. However, despite the near-term headwinds, 5G remains very much on track for an X55 (QualcommSnapdragon) driven inflection in 2H20 as 16 pilots (with 600M subs)commercialize. While we are adjusting NT estimates, 2H20 is largelyunchanged due to accelerating 5G contribution as INSG maintains its 20-25%2020+ CAGR. We initiate 2021 estimates, maintain our Buy rating and raiseour PT to $7.50.

Solid 3Q sales driven by growing carrier diversification: Last night,Inseego reported solid 3Q19 results with sales of $62.7M, up 24% y/y and 12%seq and $3.1M ahead of our estimates, driven predominantly by IoT & MobileSolutions ($45.9M in sales (73% of the mix), up 33% y/y and 15% sequentially.IoT outperformance continues to be driven by early 5G pilot contribution (~5%of sales) and diversification of its 4G carrier base which now includes Verizon(~50%+ customer), AT&T, Sprint, Telstra (Australia, 4Q19) and Bell Canada(1Q20). Enterprise SaaS sales of $16.8M (27% of the mix), up 5% y/y, wereat the high-end of $15-17M guidance and slightly ahead of our expectations($16.2M). GMs of 30.0% were up seq and slightly below our expectations,as IoT & Mobile Solutions made some progress (up 160bp seq to 18.0%)and is expected to improve further with favorable mix (5G and Enterprise)and ongoing cost reduction plans. Op-ex continued to ramp to support anexpanding global array of 5G customers (up $3.1M seq and $1.5M aheadof our estimates). The net result was EBITDA of $4.4M, at the high-end ofguidance $3.0-$4.5M and above our $3.4M estimate.

Verizon promotional shift impacts NT outlook: Strong 3Q19 results weremuted by sequential guidance of $48-55M, down 18% at the midpoint, versusour $64.9M estimate. Combined with higher op-ex the resulting EBITDA rangeof ($3.0M) to $1.0M is below our $5.2M estimate. This was largely the result ofa recent promotional change as well as seasonality at 50%+ customer Verizon.Consequently, we are lowering our 4Q19 and 1H20 expectations, and highlight2H20 estimates driven by 5G commercialization are largely unchanged.

5G and X55 drives 2H20 inflection and a 20-25% CAGR: 5G momentumcontinues to build as highlighted by the growing number of carrierengagements, active trials and customers which stand at 50+, 16 and 10carriers in 9 countries with 600M subs, respectively. This translates to $10M+ in anticipated 2019 5G sales. More importantly, this is a precursor to a 5Gramp in 2H20 driven by commercialization of Qualcomm’s X55 Snapdragonwhich brings more integration, better performance and lower BoM costs. We

Important Disclosures & Regulation AC Certification(s) are located on page 10 to 12 of this report.Roth Capital Partners, LLC | 888 San Clemente Drive | Newport Beach CA 92660 | 949 720 5700 | Member FINRA/SIPC

expect this to translate to an inflecting 5G opportunity in 2H20 and beyonddriving management’s outlook of 20-25% growth in 2020+.

Page 2 of 12

INSEEGO CORP. Company Note - November 6, 2019

5G Momentum Globally Ramps

46 5G networks launched…and growing

Global 5G momentum continues to build with accelerating operator, silicon and device announcements.

According to GSA, the 5G market features 321 operators in 103 countries currently investing in networks.

To date, 46 networks have launched with 27 operators offering 5G FWA or home broadband services (17

full commercial and 10 with limited availability). While these numbers look impressive, we caution patience

(consistent with our past comments and history) as baseband silicon diversity remains non-existent

[Qualcomm (QCOM-NC) is the only commercial merchant supplier] and costs remain high. Additionally,

network coverage remains skeletal, at best, in most geographies with device availability constrained (we

continue to not expect a 5G iPhone until 3Q20, which marks the de facto commercialization of 5G, in our

opinion). The bottom-line, is that 5G is coming but will take time, in-line with past wireless technology

transitions which have taken 7 to 10 years to achieve market leadership.

Figure 1: Global 5G Operator Investments

Source: 5G Networks and Devices: a Global Snapshot, October 2019, Global mobile Suppliers Association – GSA

� 5G fixed wireless gaining momentum heading into 2020: With 27 networks (17 full commercial and

10 with limited availability) 5G Fixed Wireless Access (FWA) is quickly becoming an important market

opportunity for 5G. This spans all frequencies; high-band (> 20GHz or millimeter Wave, mmWave),

mid-band (1-6GHz) and low-band (sub 1GHz). We expect the market to rapidly evolve from limited

availability, or glorified trials at present, to commercial deployments with the availability of more cost

effective 5G NR solutions which has been a gating factor, in our opinion. To that end, leading 5G

silicon supplier Qualcomm (again, the only current commercial merchant 5G supplier) announced the

Snapdragon X55 with 30+ OEM wins which is targeted at FWA markets, both high (millimeter wave)

and mid-band solutions. We expect general 1-2Q20 availability should accelerate larger scale

commercial deployments, but note that ASPs remain high.

Importantly, Inseego (INSG-Buy) is poised to be a leader for FWA home routers and mobile hotspots

with 50+ ongoing operator engagements,16 active trials, and 10 carrier customers in 9 countries

(representing 600M+ mobile subs). However, we caution there will be increased competition, but we

believe Inseego’s product breadth (gigabit-LTE, mobile hotspots, etc.) and increasing global presence

will be a key factor for success in the 5G FWA market.

5G features prominently

despite its early stage and

sparse coverage.

However, FWA provides

some interesting global

opportunities with NR

solutions in 2020.

Page 3 of 12

INSEEGO CORP. Company Note - November 6, 2019

Figure 2: 5G Spectrum Footprint

Source: Inseego Analyst Meeting January 2019

Qualcomm’s X55 Snapdragon is Key

To date, global trials have featured first generation silicon from Qualcomm (the X50 Snapdragon), including

current Inseego solutions. However, acceleration of global deploymenst in both the FWA and mobile

hotspot markets will be tied to commercialization of the next-gen X55 which features greater integration,

better performance and lower overall BoM cost. We expect general availability of the X55 by 1-2Q20 which

will coincide with volume rollouts of current Inseego pilot and carrier customers. We expect this to translate

to accelerating 5G sales for Inseego in 2H20 (Note: Our current expectations reflect 5G sales increasing

from $10M in 2019 to $36M in 2020 with 75% skewed towards the back half).

Page 4 of 12

INSEEGO CORP. Company Note - November 6, 2019

Valuation

5G accelerates in 2H20 driving 20-25% LT growth

Despite the near-term headwinds related to Verizon promotional activity and increased op-ex to support an

expanding global 5G customer base, we remain positive on Inseego. We expect higher op-ex to be partially

offset by expanding IoT & Mobile GMs (18% in 3Q19 to approach 30% by 4Q20 benefitting from a move to

contract manufacturer Foxconn as well as new higher margin 5G and industrial/Enterprise products). While

we lower top-line expectations related to 50%+ customer Verizon’s 4G promotional activity, we expect 5G

sales to accelerate in 2H20. In fact, although our 4Q19 and 1H20 sales estimates decline, our 2H20

estimates are largely unchanged (down approximately $4M and likely conservative, in our opinion).

Additionally, we initiate 2021 sales and EBITDA estimates of $338.7M, up 27% y/y, and $48.1M,

respectively, in-line with long-term target growth of 20% to 25%. Overall, we believe that global 5G trends

remain positive and top-line expectations are conservative given the pipeline of 50+ global mobile

operators. We maintain our Buy rating and raise our PT to $7.50, which reflects 16x EV/annualized 4Q20E

EBITDA.

Figure 3: Inseego 2Q19 Results and 3Q19 Guidance vs Estimates

Description

Range Low

Range High

Prior ROTH

Prior Street

Comments

3Q19

Revenue $58.0M $62.0M $59.7M $59.8M $62.7M: upside from IoT& Mobile

IoT & Mobile $43.0M $45.0M $43.6M Reported $45.9M, up 33% y/y

Ent SaaS $15.0M $17.0M $16.2M Reported $16.8M, up 5% y/y

Adj EBITDA $3.0M $4.5M $3.4M $3.8M Reported EBITDA of $4.4M

4Q19

Revenue $48.0M $55.0M $64.9M $64.2M Down 18% at the midpoint

IoT & Mobile $33.0M $38.0M $48.4M VZ promotion and increased op-ex

Ent SaaS $15.0M $17.0M $16.5M

Adj EBITDA ($3.0M0 $1M $5.2M $5.2M GM headwinds and increase op-ex Source: Inseego 3Q19 earnings release and Roth Capital Partners

Figure 4: Inseego Valuation Comps

Source: ThomsonReuters Eikon, SEC filings, company reports and ROTH Capital

11/6/19 CY2018CY2019CY2020CY2018CY2019CY2020CY2018CY2019CY2020 % O ff

Share Market Ent 52 Wk

Rating Price Cap Value 2018 2019E 2020E 2018 2019E 2020E 2018 2019E 2020E 2018 2019E 2020E High

INSG Buy $5.31 $422 $546 2.7x 2.5x 2.1x 29.6x 57.4x 26.3x NM NM NM (8%) 9% 21% 12%

IoT Solutions

ALRM* Buy $46.27 $2,243 $2,143 5.2x 4.6x 4.0x 23.5x 21.0x 18.8x 36.1x 32.8x 30.6x 23% 15% 13% 35%

CAMP Buy $11.30 $386 $484 1.3x 1.3x 1.2x 9.7x 10.4x 8.7x 10.2x 15.4x 13.5x 1% 2% 4% 44%

DGII Buy $14.10 $397 $310 1.3x 1.2x 1.1x 13.5x 11.1x 9.2x 210.0x 38.7x 29.9x 20% 11% 6% 5%

ITRN NC $24.65 $579 $586 2.2x 2.0x 1.9x 7.4x 7.8x 6.9x 10.3x 13.1x 10.2x 12% 9% 7% 36%

NTGR NC $27.36 $825 $645 0.4x 0.7x 0.6x 6.4x 8.2x 6.7x 11.7x 14.9x 13.1x 6% (33%) 3% 33%

ORBC Buy $4.60 $360 $557 1.9x 2.0x 1.9x 9.6x 8.8x 7.7x NM NM NM 14% (4%) 7% 56%

SWIR Buy $8.92 $323 $239 0.3x 0.3x 0.3x 4.4x 8.4x 6.3x 9.8x 27.9x 11.4x 16% (9%) 3% 55%

USAT NC $6.73 $404 $389 2.8x 2.5x 2.1x 23.7x 26.4x 26.9x 64.6x 107.7x 118.8x 18% 11% 17% 20%

Group Average 1.9x 1.8x 1.7x 13.0x 13.5x 12.0x 57.1x 39.6x 36.2x 14% 0% 8% 36%

* Covered by Darin Aftahi

EV / Sales EV / EBITDA P / E Sales % Chg

Verizon promotional

headwinds and op-ex to

support global 5G

deployments impacts

near-term EBITDA

Page 5 of 12

INSEEGO CORP. Company Note - November 6, 2019

VALUATION

The tripling of INSG since 1/1/18 values the company at an EV/CY21 EBITDA of ~10x, at the higher end ofthe IoT comp range of 10-12x+. However, our 2020 expectations are likely conservative given MiFi strength(including new products) and 5G fixed wireless and mobile hotspot upside. At 16x EV/ annualized 4Q20EEBITDA; we believe INSG could reasonably trade to $7.50.

Impediments to achieving our price target include the success of MiFi, new products (aviation, enterprise and5G), the adoption of 5G services, and currency headwinds.

RISKS

Historic MiFi has been in secular decline: The mobile hotspot market has been in secular decline for severalyears. With increasing embedded broadband functionality in notebooks and laptops, as well as the enablementof hotspot functionality in smartphones, the need for standalone mobile hotspots has been diminished. Afterpeaking at ~$250M in annual sales in 2011-2013, MiFi has declined by approximately 50%. However, webelieve this pressure is abating driven by 1) New product development, i.e. a 1Gbps solution shipping in 4Q18,2) Engagement with new carriers, and 3) Share gains at the expense of ZTE’s US driven shipment bans. Weexpect this business to return to growth in 2019.

Successful expansion of Enterprise SaaS into new verticals (Aviation) and geographies (Europe): TheEnterprise SaaS (Ctrack) business which was acquired via the 2015 DigiCore acquisition maintains a largehistoric component of South African based consumer services (basic vehicle tracking and stolen vehiclerecovery services). This was also characterized by low ARPUs and high churn. Consequently, Inseego hasinvested in features, functionality and channel to address new geographies (Europe) and verticals (Aviation).We believe these are key to the growth strategy which has been showing considerable success with ~45% ofcurrent sales attributable to non-South African services. Additionally, aviation has been building an extremelyhealthy sales funnel.

5G adoption cycle: We continue to maintain a healthy level of skepticism related to the timing of 5G,particularly the widespread commercial availability of mobile 5G services. However, we see the near-termopportunity for fixed wireless 5G services within millimeter wave bands given 1) The wide chucks of availablespectrum and pending auctions, 2) The technological feasibility of near-term services, and 3) The commercialavailability of equipment. Verizon will begin to lead this fixed wireless charge in 4Q18 with the launch of fourmarkets. We estimate that each 25k units translates to approximately $0.04 EPS. We expect limited mobile5G commercial deployments in mid-2019 driven by multimode devices such as next gen MiFi hotspots.

Customer concentration: Inseego sales remain highly concentrated within carrier customers, particularlyVerizon which has represented 51%, 54% and 54% of total sales in 2017, 2016 and 2015, respectively.However, new products, particularly MiFi, and share gains from ZTE are expected to begin to diversify thiscustomer base over the next 12-24 months.

New product success: Inseego has embarked on a major product portfolio campaign that includes 11 newproducts over the next year. This spans the revitalization of the MiFi portfolio, expansion of the vertical marketand geographic focus at Ctrack, as well as the introduction of completely new categories in enterprise andindustrial gateways as well as 5G solutions. Success across these product lines is key to stabilize the six-yearCAGR decline of 9% and return Inseego to growth and profitability.

Rand headwinds: The South African rand is producing near-term headwinds within the domestic Ctrackbusiness. Year to date, the rand is down over 12%. Given that ~50% of Enterprise SaaS sales continue toreside in South Africa this has produced difficult comps which have been compounded by lower ARPUs, higherchurn and an increasing focus to move away from consumer end markets. On the positive side, op-ex relatedto Ctrack is has largely benefited from these same currency headwinds.

Page 6 of 12

INSEEGO CORP. Company Note - November 6, 2019

COMPANY DESCRIPTION

Inseego, a leading provider of mobile, IoT, enterprise and SaaS solutions including mobile hotspots ("MiFi"),wireless modules and embedded solutions, wireless CPEs ("Customer Premise Equipment"), enterprise andindustrial class gateways and SaaS based fleet management and aviation asset tracking applications.

Page 7 of 12

INSEEGO CORP. Company Note - November 6, 2019

Inseego Corp

Fiscal Year Ends December

Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21 Dec-21

Income Statement 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19E 1Q20E 2Q20E 3Q20E 4Q20E 1Q21E 2Q21E 3Q21E 4Q21E 2016 2017 2018 2019E 2020E 2021E

Revenue 46.7 49.1 50.6 56.0 48.6 55.9 62.7 53.4 53.0 59.5 69.2 84.2 72.2 80.5 88.3 97.7 243.6 219.3 202.5 220.5 265.9 338.7

COGS 29.2 31.0 32.4 35.0 33.2 39.3 43.9 36.0 35.2 39.1 45.1 54.2 45.6 50.6 55.4 61.1 151.5 150.5 127.5 152.3 173.7 212.8

Gross Profit 17.6 18.0 18.3 21.1 15.4 16.6 18.8 17.4 17.7 20.4 24.1 30.0 26.6 29.9 32.9 36.6 92.1 68.8 74.9 68.3 92.3 126.0

R&D 4.8 4.8 4.8 5.3 3.3 4.2 6.5 7.2 7.2 7.3 7.5 7.7 7.7 7.9 8.0 8.3 29.8 20.6 19.6 21.2 29.7 31.9

S&M 5.1 5.5 5.6 5.9 6.2 6.4 6.8 7.3 7.3 7.3 7.6 7.9 7.9 8.2 8.4 8.8 29.1 24.3 22.1 26.8 30.2 33.4

G&A 5.9 5.9 5.1 5.9 5.9 5.4 5.9 6.0 6.0 6.0 6.1 6.3 6.3 6.3 6.4 6.5 34.5 29.8 22.8 23.2 24.4 25.4

Operating Income 1.8 1.9 2.8 4.0 0.0 0.6 (0.4) (3.1) (2.8) (0.3) 2.9 8.1 4.7 7.6 10.1 13.0 (1.3) (5.8) 10.5 (2.9) 7.9 35.3

Amortization 2.7 2.3 3.1 2.4 2.4 5.0 2.1 2.1 2.1 2.1 2.1 2.1 2.1 2.1 2.1 2.1 10.6 8.2 10.5 11.6 8.4 8.4

Non-recurring Costs 1.7 0.4 0.0 0.7 0.0 0.8 0.7 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 33.1 8.2 2.8 1.5 0.0 0.0

Operating Income (reported) (2.6) (0.8) (0.3) 1.0 (2.4) (5.2) (3.2) (5.2) (4.9) (2.4) 0.8 6.0 2.6 5.5 8.0 10.9 (45.0) (22.2) (2.8) (16.0) (0.5) 26.9

Net Interest (5.1) (5.1) (5.2) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (5.1) (15.6) (19.3) (20.6) (20.5) (20.5) (20.5)

Other 0.1 (0.4) 17.0 (0.3) 0.3 (0.1) (0.3) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.4 (4.1) 16.3 (0.1) 0.0 0.0

EBT (7.6) (6.4) 11.4 (4.4) (7.2) (10.4) (8.6) (10.3) (10.0) (7.5) (4.3) 0.9 (2.5) 0.3 2.8 5.8 (60.2) (45.6) (7.1) (36.5) (21.0) 6.4

Income Tax 0.4 0.3 0.5 (0.4) 0.2 0.3 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.4 0.2 0.8 1.0 0.9 0.9

Net Income (8.1) (6.7) 10.9 (4.1) (7.4) (10.7) (8.8) (10.6) (10.2) (7.8) (4.5) 0.7 (2.8) 0.1 2.6 5.5 (60.6) (45.9) (7.9) (37.6) (21.9) 5.5

Share (Basic) 60.7 61.5 68.5 73.6 74.4 78.8 79.6 79.8 79.8 80.0 80.2 80.4 80.4 80.6 80.8 81.0 53.9 58.7 66.1 78.1 80.1 80.7

Shares (FD) 60.7 61.5 71.5 73.6 74.4 78.8 79.6 79.8 79.8 80.0 80.2 87.4 80.4 87.6 87.8 88.0 53.9 58.7 66.8 78.1 81.8 85.9

EPS (Basic) - GAAP ($0.13) ($0.11) $0.16 ($0.05) ($0.10) ($0.14) ($0.11) ($0.13) ($0.13) ($0.10) ($0.06) $0.01 ($0.03) $0.00 $0.03 $0.07 ($1.12) ($0.78) ($0.12) ($0.48) ($0.27) $16.00

EPS (FD) ($0.02) ($0.02) ($0.01) $0.02 ($0.03) ($0.03) ($0.05) ($0.08) ($0.07) ($0.04) $0.00 $0.06 $0.02 $0.05 $0.08 $0.11 ($0.16) ($0.29) ($0.03) ($0.19) ($0.05) $7.28

EBITDA (Adj Pro Forma) $4.1M $3.8M $4.7M $5.8M $2.1M $3.0M $4.4M $0.1M $0.4M $2.9M $6.1M $11.3M $7.9M $10.8M $13.3M $16.2M $7.8M $2.3M $18.4M $9.5M $20.8M $48.1M

% of Sales

Gross Margin 37.6% 36.7% 36.1% 37.6% 31.7% 29.8% 30.0% 32.6% 33.5% 34.3% 34.8% 35.7% 36.9% 37.1% 37.2% 37.4% 37.8% 31.4% 37.0% 31.0% 34.7% 37.2%

R&D 10.2% 9.7% 9.4% 9.4% 6.8% 7.6% 10.3% 13.4% 13.5% 12.3% 10.8% 9.2% 10.7% 9.8% 9.1% 8.5% 12.2% 9.4% 9.7% 9.6% 11.2% 9.4%

G&A 12.7% 11.9% 10.1% 10.5% 12.2% 9.6% 9.4% 11.3% 11.4% 10.1% 8.8% 7.4% 8.7% 7.8% 7.2% 6.7% 14.2% 13.6% 11.3% 10.5% 9.2% 7.5%

Op Inc (normalized) 3.8% 3.8% 5.5% 7.2% 0.0% 1.1% (0.6%) (5.9%) (5.3%) (0.5%) 4.2% 9.6% 6.5% 9.4% 11.4% 13.3% (0.5%) (2.6%) 5.2% (1.3%) 3.0% 10.4%

Net Inc (17.2%) (13.6%) 21.6% (7.3%) (15.3%) (19.2%) (14.1%) (19.8%) (19.3%) (13.0%) (6.5%) 0.8% (3.8%) 0.1% 3.0% 5.7% (24.9%) (20.9%) (3.9%) (17.0%) (8.2%) 1.6%

% Change

Revenue (15.6%) (18.1%) (11.9%) 20.4% 3.9% 13.9% 23.9% (4.8%) 9.1% 6.4% 10.4% 57.9% 36.2% 35.3% 27.6% 16.0% (10.0%) (7.7%) 8.9% 20.6% 27.4%

Op Inc (133.3%) (289.1%) (640.3%) 284.7% (99.9%) (68.0%) (112.9%) (177.6%) ######## (152.3%) (907.2%) (358.6%) (267.6%) (2491.3%) 245.2% 60.4% 349.1% (280.5%) (127.5%) (373.8%) 346.2%

EPS (85.3%) (69.6%) (87.3%) (208.2%) 67.1% 28.7% 584.6% (477.4%) 106.7% 27.4% (100.4%) (178.7%) (131.0%) (232.2%) ######## 92.7% 85.7% (89.0%) 489.0% (72.4%) (14140.8%)

Source: SEC filings, company reports and ROTH Capital Partners

Scott W Searle, CFA

(646) 616-2782

Page 8 of 12

INSEEGO CORP. Company Note - November 6, 2019

Inseego Corp

Fiscal Year Ends December

Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21 Dec-21

Sales Model 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19E 1Q20E 2Q20E 3Q20E 4Q20E 1Q21E 2Q21E 3Q21E 4Q21E 2016 2017 2018 2019E 2020E

Revenue Mix

IoT & Mobile Solutions 28.9 31.7 34.6 40.1 32.8 40.0 45.9 36.8 36.3 42.3 51.8 66.5 54.2 61.9 69.5 78.6 187.4 161.0 135.3 155.5 196.9

Hotspot & Other 28.9 31.7 34.6 39.0 31.6 37.7 42.2 31.5 31.2 35.0 38.5 43.8 36.7 38.5 41.0 44.3 187.4 161.0 134.2 143.0 148.5

Enterprise/Industrial 0.0 0.0 0.0 0.5 0.8 1.1 1.1 2.1 3.6 5.1 5.1 6.1 7.1 8.1 0.0 0.0 0.0 2.4 11.9

5G 0.0 1.1 1.2 1.8 3.0 4.2 4.0 5.2 9.7 17.6 12.4 17.4 21.4 26.2 0.0 1.1 10.2 36.4

Enterpise SaaS 17.9 17.3 16.0 16.0 15.8 15.9 16.8 16.6 16.7 17.2 17.5 17.8 18.0 18.6 18.9 19.1 56.2 58.3 67.1 65.0 69.1

Total 46.7 49.1 50.6 56.0 48.6 55.9 62.7 53.4 53.0 59.5 69.2 84.2 72.2 80.5 88.3 97.7 243.6 380.3 202.5 220.5 265.9

Revenue Mix

IoT & Mobile Solutions 62% 65% 68% 72% 68% 72% 73% 69% 69% 71% 75% 79% 75% 77% 79% 80% 77% 42% 67% 71% 74%

Hotspot & Other 62% 65% 68% 70% 65% 67% 67% 59% 59% 59% 56% 52% 51% 48% 46% 45% 77% 42% 66% 65% 56%

Enterprise/Industrial 0% 0% 0% 0% 0% 1% 1% 2% 2% 4% 5% 6% 7% 8% 8% 8% 0% 0% 0% 1% 4%

5G 0% 0% 0% 2% 3% 3% 5% 8% 8% 9% 14% 21% 17% 22% 24% 27% 0% 0% 1% 5% 14%

Enterpise SaaS 38% 35% 32% 28% 32% 28% 27% 31% 31% 29% 25% 21% 25% 23% 21% 20% 23% 15% 33% 29% 26%

% Change (y/y)

IoT & Mobile Solutions (30.3%) (29.4%) (19.1%) 26.2% 13.5% 26.0% 32.6% (8.2%) 10.8% 5.8% 12.7% 80.6% 49.1% 46.4% 34.3% 18.2% (7.8%) (14.1%) (15.9%) 14.9% 26.6%

Hotspot & Other (30.3%) (29.4%) (19.1%) 22.7% 9.3% 18.8% 21.9% (19.1%) (1.1%) (7.1%) (8.8%) 39.0% 17.5% 9.9% 6.4% 1.1% (7.8%) (14.1%) (16.6%) 6.5% 3.9%

Enterprise/Industrial 320.0% 380.0% 363.6% 363.6% 190.5% 97.2% 58.8% 406.4%

5G 273.3% 228.6% 189.7% 225.1% 318.5% 207.8% 235.2% 121.9% 49.0% 257.8%

Enterpise SaaS 27.9% 16.0% 9.2% 8.0% (11.6%) (8.1%) 5.0% 3.8% 5.6% 8.0% 4.0% 7.2% 8.3% 8.0% 7.9% 7.8% 217.4% 3.8% 15.1% (3.1%) 6.2%

Total (15.6%) (18.1%) (11.9%) 20.4% 3.9% 13.9% 23.9% (4.8%) 9.1% 6.4% 10.4% 57.9% 36.2% 35.3% 27.6% 16.0% 10.3% 56.1% (46.8%) 8.9% 20.6%

% Change (seq)

IoT & Mobile Solutions (9.1%) 9.9% 9.1% 15.8% (18.2%) 22.0% 14.9% (19.9%) (1.3%) 16.4% 22.4% 28.4% (18.5%) 14.3% 12.2% 13.1%

Hotspot & Other (9.1%) 9.9% 9.1% 12.5% (19.0%) 19.5% 12.0% (25.4%) (1.0%) 12.2% 10.0% 13.8% (16.3%) 4.9% 6.5% 8.1%

Enterprise/Industrial 50.0% 46.7% 0.0% 90.9% 71.4% 41.7% 0.0% 19.6% 16.4% 14.1%

5G 8.9% 45.9% 66.1% 41.5% (4.2%) 28.6% 86.4% 82.1% (29.5%) 40.1% 23.4% 22.3%

Enterpise SaaS 20.9% (3.0%) (7.6%) (0.3%) (1.1%) 0.8% 5.5% (1.4%) 0.6% 3.2% 1.6% 1.6% 1.6% 3.0% 1.5% 1.5%

Total 0.4% 5.0% 3.2% 10.7% (13.4%) 15.1% 12.2% (14.9%) (0.7%) 12.2% 16.4% 21.7% (14.3%) 11.5% 9.7% 10.6%

Source: SEC filings, company reports and ROTH Capital Partners

Scott W Searle, CFA

(646) 616-2782

Page 9 of 12

INSEEGO CORP. Company Note - November 6, 2019

Regulation Analyst Certification ("Reg AC"): The research analyst primarily responsible for the content of this report certifiesthe following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal viewsabout the subject company or companies and its or their securities. I also certify that no part of my compensation was, is orwill be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Disclosures:ROTH makes a market in shares of Inseego Corp., Alarm.com Holdings, Inc., CalAmp Corp., Digi International, Inc.,ORBCOMM, Inc. and Sierra Wireless, Inc. and as such, buys and sells from customers on a principal basis.

Shares of Inseego Corp. may be subject to the Securities and Exchange Commission's Penny Stock Rules, which may setforth sales practice requirements for certain low-priced securities.

Rating and Price Target History for: Inseego Corp. (INSG) as of 11-05-2019

6

5

4

3

2

1

0Q3 2017 Q1 Q2 Q3 2018 Q1 Q2 Q3 2019 Q1 Q2 Q3 2020

10/12/18I:B:$5

01/14/19B:$6.25

03/08/19B:$6.5

08/07/19B:$7

Created by: BlueMatrix

Rating and Price Target History for: Alarm.com Holdings, Inc. (ALRM) as of 11-05-2019

80

70

60

50

40

30

20Q3 2017 Q1 Q2 Q3 2018 Q1 Q2 Q3 2019 Q1 Q2 Q3 2020

10/03/16I:B:$33.5

11/15/16B:$39

03/16/17B:$40

08/02/17B:$43.5

08/09/17B:$48

11/06/17B:$51

11/09/17B:$52.5

02/28/18B:$51

08/08/18B:$57

09/21/18B:$62

10/23/18B:$58

11/07/18B:$61

01/15/19B:$63

03/01/19B:$66

04/15/19B:$73

04/29/19N:$73

07/16/19N:$55

10/10/19N:$51

Created by: BlueMatrix

Page 10 of 12

INSEEGO CORP. Company Note - November 6, 2019

Rating and Price Target History for: CalAmp Corp. (CAMP) as of 11-05-2019

30

25

20

15

10

5Q3 2017 Q1 Q2 Q3 2018 Q1 Q2 Q3 2019 Q1 Q2 Q3 2020

02/02/18I:B:$28

06/28/18B:$27

12/11/18B:$24

12/21/18B:$23

05/01/19B:$20

06/26/19B:$18

Created by: BlueMatrix

Rating and Price Target History for: Digi International, Inc. (DGII) as of 11-05-2019

15

14

13

12

11

10

9

8Q3 2017 Q1 Q2 Q3 2018 Q1 Q2 Q3 2019 Q1 Q2 Q3 2020

02/02/18I:B:$15

04/27/18B:$16

02/01/19B:$18

Created by: BlueMatrix

Rating and Price Target History for: ORBCOMM, Inc. (ORBC) as of 11-05-2019

14

12

10

8

6

4

2Q3 2017 Q1 Q2 Q3 2018 Q1 Q2 Q3 2019 Q1 Q2 Q3 2020

02/02/18I:B:$14

10/31/18B:$13

03/04/19B:$10

07/31/19B:$9

Created by: BlueMatrix

Page 11 of 12

INSEEGO CORP. Company Note - November 6, 2019

Rating and Price Target History for: Sierra Wireless, Inc. (SWIR) as of 11-05-2019

35

30

25

20

15

10

5Q3 2017 Q1 Q2 Q3 2018 Q1 Q2 Q3 2019 Q1 Q2 Q3 2020

02/02/18I:N:$18

03/27/18B:$22

08/03/18B:$23

Created by: BlueMatrix

Each box on the Rating and Price Target History chart above represents a date on which an analyst made a change to arating or price target, except for the first box, which may only represent the first note written during the past three years.Distribution Ratings/IB Services shows the number of companies in each rating category from which Roth or an affiliatereceived compensation for investment banking services in the past 12 month.

Distribution of IB Services FirmwideIB Serv./Past 12 Mos.

as of 11/06/19Rating Count Percent Count PercentBuy [B] 279 76.86 160 57.35Neutral [N] 47 12.95 18 38.30Sell [S] 4 1.10 2 50.00Under Review [UR] 33 9.09 16 48.48

Our rating system attempts to incorporate industry, company and/or overall market risk and volatility. Consequently, at anygiven point in time, our investment rating on a stock and its implied price movement may not correspond to the stated 12-month price target.

Ratings System Definitions - ROTH employs a rating system based on the following:

Buy: A rating, which at the time it is instituted and or reiterated, that indicates an expectation of a total return of at least10% over the next 12 months.

Neutral: A rating, which at the time it is instituted and or reiterated, that indicates an expectation of a total return betweennegative 10% and 10% over the next 12 months.

Sell: A rating, which at the time it is instituted and or reiterated, that indicates an expectation that the price will depreciateby more than 10% over the next 12 months.

Under Review [UR]: A rating, which at the time it is instituted and or reiterated, indicates the temporary removal of theprior rating, price target and estimates for the security. Prior rating, price target and estimates should no longer be reliedupon for UR-rated securities.

Not Covered [NC]: ROTH does not publish research or have an opinion about this security.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other businessrelationships with the covered companies mentioned in this report in the next three months. The material, information andfacts discussed in this report other than the information regarding ROTH Capital Partners, LLC and its affiliates, are fromsources believed to be reliable, but are in no way guaranteed to be complete or accurate. This report should not be usedas a complete analysis of the company, industry or security discussed in the report. Additional information is available uponrequest. This is not, however, an offer or solicitation of the securities discussed. Any opinions or estimates in this report aresubject to change without notice. An investment in the stock may involve risks and uncertainties that could cause actualresults to differ materially from the forward-looking statements. Additionally, an investment in the stock may involve a highdegree of risk and may not be suitable for all investors. No part of this report may be reproduced in any form without theexpress written permission of ROTH. Copyright 2019. Member: FINRA/SIPC.

Page 12 of 12

INSEEGO CORP. Company Note - November 6, 2019

![Modular Samsung Max-x55 x56 x57 x65 x66 [ET]](https://img.pdfslide.us/doc/110x75/54e8d7d94a7959b17a8b4b02/modular-samsung-max-x55-x56-x57-x65-x66-et.jpg)