Embed Size (px)

Citation preview

In-Line

MORGAN STANLEY & CO. LLC

Katy L. Huberty, CFA+1 212 761-6249

James E Faucette+1 212 296-5771

MORGAN STANLEY & CO. INTERNATIONAL PLC+

Louise Singlehurst+44 20 7425-7239

MORGAN STANLEY & CO. INTERNATIONAL PLC, SEOUL BRANCH+

Shawn Kim+82 2 399-4940

MORGAN STANLEY & CO. LLC

Jerry Liu+1 212 761-3735

Meta A Marshall+1 212 761-0430

MORGAN STANLEY & CO. INTERNATIONAL PLC+

Josephine Tay+44 20 7425-3623

Multi-Industry

North America

IndustryView

Technology & BrandsTechnology & BrandsApril 15, 2015

N. America Insight: Wearables AdoptionSurprises Positively; Apple KeyBeneficiary

Our AlphaWise survey of US consumers post Apple Watch launch inearly March indicates wearable penetration doubled and purchaseintention tripled in the past three months. Apple Watch demand alsoincreased 60%, pointing to a stronger than expected product rampwith production the only bottleneck.

Wearables adoption accelerating. In our November 2014 WearableDevices Blue Paper, we predicted the category to be the fastest rampingconsumer device in history. Strong adoption over the 2014 holiday seasonsuggests it is now a mainstream consumer technology category. We expectdemand to top IDC's estimate of 46M units in 2015, and it could even top ourbullish estimate of 70M units though supply constraints remain the keybottleneck. Nearly a quarter of respondents in our AlphaWise US consumersurvey said they own a wearable device, doubling the penetration ratecompared to our prior survey three months ago. One-third of respondentsplan to purchase wearable devices, tripling purchase intention in the last threemonths. These purchasers are willing to spend $155 on average, which ismuch higher than the cheapest popular fitness trackers at $50 and closer tohigh-end products at $200+.

Apple Watch unit demand now tracking above our forecast. Nearly 15%of all US iPhone owners said they “definitely” or “probably” will purchase theApple Watch, much higher than our estimate of 10% of compatible owners(iPhone 5 or newer), and 9% in our December 2014 survey. Extrapolatingsurvey responses to US iPhone owners, our analysis indicates 15M Watchdemand, about 60% more than 9M from our prior survey three months ago.For comparison, our Apple model only assumes 18M Watch shipments inCY15 and 30M in the first 12 months globally. Apple is on Morgan Stanley'sNorth America Best Ideas list, in part due to our above-consensus expectationsfor Watch backed by this and prior surveys and analyses.

Wearables could increase brand loyalty for Samsung. Second only toApple, Samsung saw the biggest increase in purchase intention share in thesurvey, from six to 12 points. Samsung's strategy in wearables is less aboutmarket share and profits, in our view, but more about capturing consumerloyalty and brand. Its distinct brand and design focus, combined with itsengineering prowess, allows it to release wearable devices into the market at afast pace while keeping margins in check.

Garmin's outlook is more mixed. Its current ownership share increased to10% from 8% in the latest survey, but purchase intention decreased to 3%from 8%. Wearable purchasers willing to spend $155 is a positive for Garmin,as it points to the opportunity available at the premium fitness band level

Morgan Stanley does and seeks to do business withcompanies covered in Morgan Stanley Research. As a result,investors should be aware that the firm may have a conflictof interest that could affect the objectivity of MorganStanley Research. Investors should consider MorganStanley Research as only a single factor in making theirinvestment decision.For analyst certification and other important disclosures,For analyst certification and other important disclosures,refer to the Disclosure Section, located at the end of thisrefer to the Disclosure Section, located at the end of thisreport.report.+ = An alysts emp loyed by n on -U .S. a ff ilia tes are n o t reg istered w ith F INRA, mayn o t be associated person s o f th e member an d may n o t be su b ject to NASD/NYSErestriction s on commu n ication s w ith a su b ject compan y, pu b lic appearan ces an dtrad in g secu rities h eld by a research an alyst accou n t.

| April 15, 2015Technology & Brands

1

(~$150-$200), which should help sales of the Vivosmart product, even withincreasing competition.

Higher purchase intent suggests risks for the traditional watchmakers,particularly Swatch. While our survey focuses on US consumers (a smallmarket for traditional Swiss brands), we think the rise in the level of purchaseintention over the past three months is important - and unlikely to be limitedto this consumer group. Our survey also indicates a general view that theApple Watch is a good value. What is not clear is whether or not consumerswill actively be deterred from buying a traditional watch, with the choice ofwearables. This is key to monitor, particularly with wearables buildingpresence in the more premium end of the market (e.g., Apple).

| April 15, 2015Technology & Brands

2

Survey AnalysisSurvey Analysis

Current Wearable LandscapeCurrent Wearable Landscape

Wearables are becoming mainstream devices. In our AlphaWise survey of US adults, 24% said they ownwearables, which today consist of mostly fitness trackers and some smartwatches. Generally, we consider 20%the key inflection point for technology adoption, as growth for other technologies typically accelerated as wepassed this point. We saw this acceleration in adoption in the early 2000s with notebook penetration of PCs, andaround 2010 with smartphone penetration of handsets. Sales of digital music took over 10 years to exceed 20%penetration, but only four years to move from 20% to over 50%. The 24% adoption rate of wearables today isdouble our survey just three months ago, suggesting fitness trackers were a popular purchase and gift this pastholiday season.

Exhibit 1:Exhibit 1: US Wearable Ownership Increased 2x in the Last 3 Months, Reaching 24% Today

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

3

In fact, wearable ownership levels are closing in on notebooks. Note that the US has the highest wearablepenetration of all major countries, according to our global survey in August 2014. We also have to continue tomonitor the sustainability of usage especially as many respondents just started using these devices in the lastthree months. However, if this proves to be a sustainable mainstream product category, we would expectpenetration to continue to increase and close in on smartphone penetration at 67%.

Exhibit 2:Exhibit 2: 20% Is the Key Inflection Point in Technology Adoption

Sou rce: comSco re, eMarketer, Fo rrester, IDC, U S Cen su s B u reau , Morgan Stan ley Research

Exhibit 3:Exhibit 3: Wearable Ownership Is Closing in on Notebooks

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

4

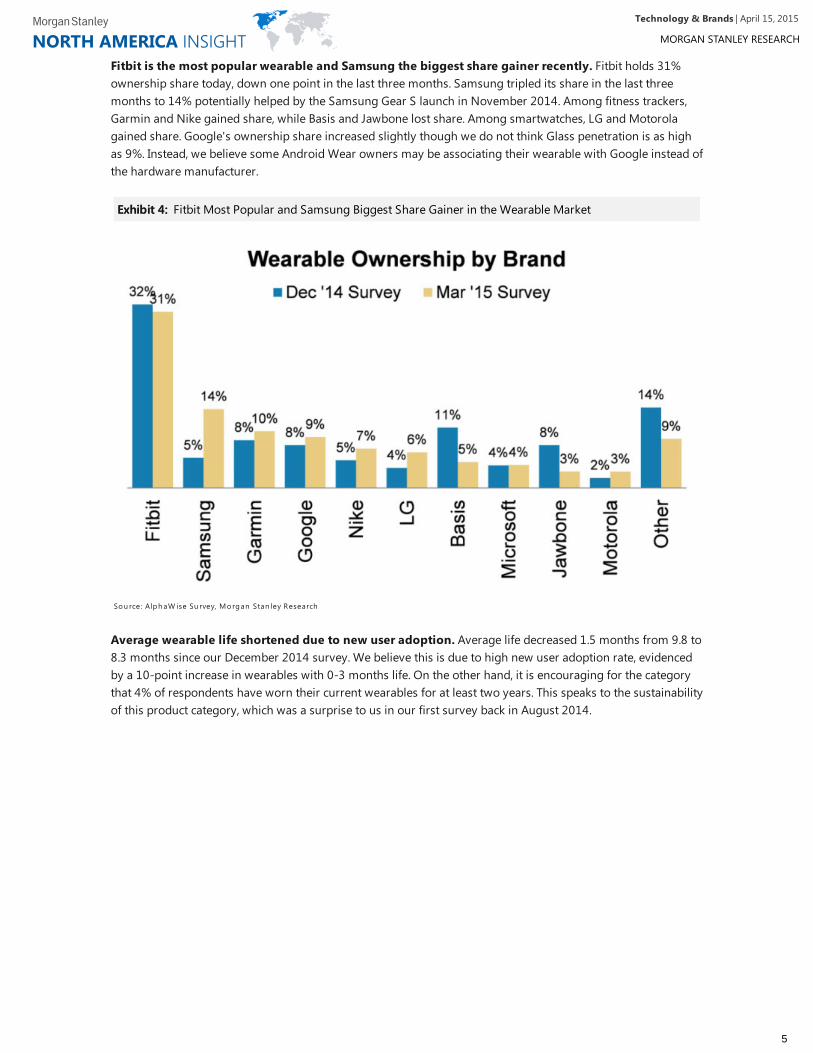

Fitbit is the most popular wearable and Samsung the biggest share gainer recently. Fitbit holds 31%ownership share today, down one point in the last three months. Samsung tripled its share in the last threemonths to 14% potentially helped by the Samsung Gear S launch in November 2014. Among fitness trackers,Garmin and Nike gained share, while Basis and Jawbone lost share. Among smartwatches, LG and Motorolagained share. Google's ownership share increased slightly though we do not think Glass penetration is as highas 9%. Instead, we believe some Android Wear owners may be associating their wearable with Google instead ofthe hardware manufacturer.

Average wearable life shortened due to new user adoption. Average life decreased 1.5 months from 9.8 to8.3 months since our December 2014 survey. We believe this is due to high new user adoption rate, evidencedby a 10-point increase in wearables with 0-3 months life. On the other hand, it is encouraging for the categorythat 4% of respondents have worn their current wearables for at least two years. This speaks to the sustainabilityof this product category, which was a surprise to us in our first survey back in August 2014.

Exhibit 4:Exhibit 4: Fitbit Most Popular and Samsung Biggest Share Gainer in the Wearable Market

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

5

Wearable Purchase IntentionWearable Purchase Intention

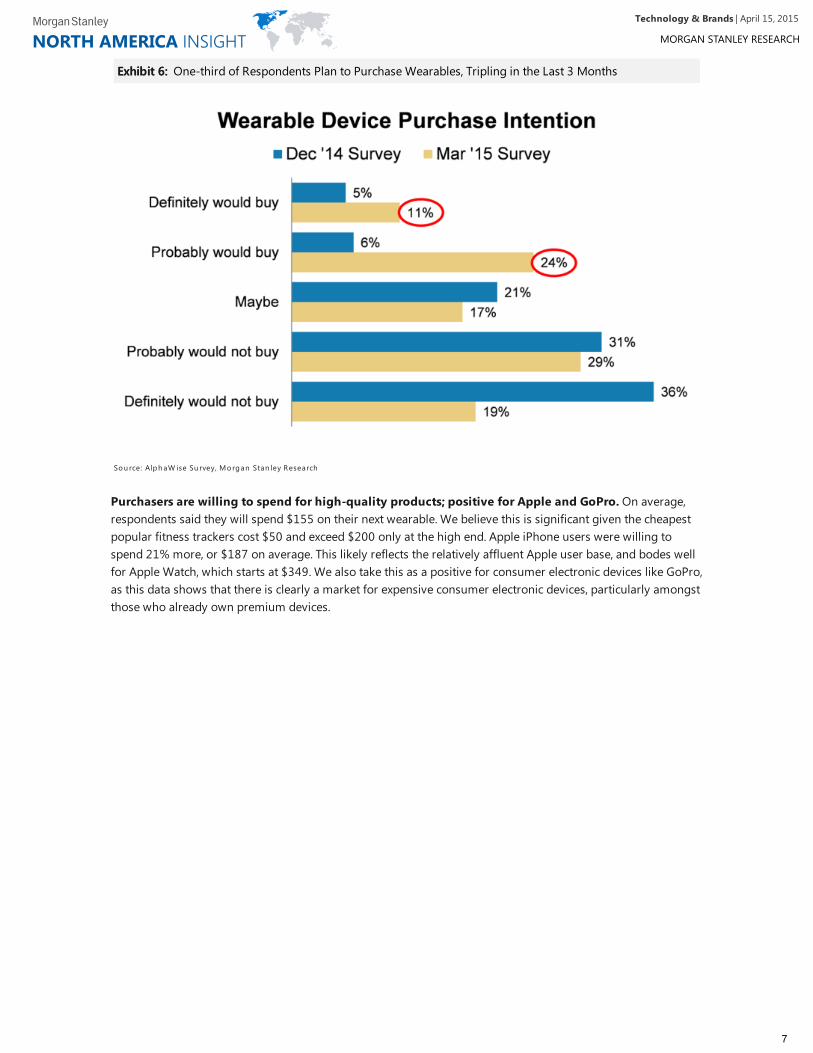

One-third of respondents plan to purchase wearables. Purchase intention tripled in the last three months,again indicating wearables have become a mainstream product. Respondents who chose “definitely would notbuy” dropped by 17 points and “probably would buy” gained 18 points, suggesting people that once thoughtthey would never use these products are now considering them.

Exhibit 5:Exhibit 5: High New User Adoption Decreased Average Wearable Life to 8.3 Months, Though Some HaveNow Worn Their Devices for Over 2 Years

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

6

Purchasers are willing to spend for high-quality products; positive for Apple and GoPro. On average,respondents said they will spend $155 on their next wearable. We believe this is significant given the cheapestpopular fitness trackers cost $50 and exceed $200 only at the high end. Apple iPhone users were willing tospend 21% more, or $187 on average. This likely reflects the relatively affluent Apple user base, and bodes wellfor Apple Watch, which starts at $349. We also take this as a positive for consumer electronic devices like GoPro,as this data shows that there is clearly a market for expensive consumer electronic devices, particularly amongstthose who already own premium devices.

Exhibit 6:Exhibit 6: One-third of Respondents Plan to Purchase Wearables, Tripling in the Last 3 Months

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

7

Apple ImplicationsApple Implications

Apple benefits from stronger wearable demand. The percentage of respondents planning to purchase anApple Watch more than doubled, from 3% in December 2014 to more than 6% in our March survey.

Looking just at the compatible iPhone base, Apple Watch unit demand increased 60% compared toour last survey. We extrapolate Watch demand using only survey responses from iPhone users since theWatch is only compatible with iPhone 5 or newer. This analysis indicates 15M Watch demand, over 60% higherthan 9M three months ago. For reference, we only model 18M Watch shipments globally for CY15 or $8.1B ofrevenue, assuming a $450 ASP, which is likely conservative given Apple's announced Watch pricing. At anaverage gross margin of 44%, we expect Watch to add about $0.35 of EPS. Our Bull Case assumes an additional$6B of Watch revenue, or roughly 25M total units in CY15 at an ASP over $550, which could more than doubleWatch's EPS contribution given higher margins.

Watch supports our platform thesis for Apple. We view the success of Apple Watch as a one of several keyindicators that will convince investors that Apple has the most valuable technology platform - with loyal, repeatusers that purchase multiple devices and services - and that its total addressable market is expanding - withWatch followed by HealthKit, HomeKit, CarPlay, Apple TV, etc. as key new market opportunities. We recentlyincreased our AAPL price target to $160 as we believe its multiple can re-rate to 18x P/E, in-line with othertechnology platform companies.

Exhibit 7:Exhibit 7: Respondents Willing to Spend $155 on Wearables with iPhone Users Willing to Spend $187, or21% More

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

8

Apple has the highest purchase intention share among smartwatches. In our survey, which wasconducted after Apple's Watch keynote on March 9, 19% of wearable purchasers chose Apple, down from 26%three months ago. We believe this may reflect the fact that the Apple Watch only works with iPhone 5 or newer,and that pricing is higher than some of the other smartwatches. Although Apple Watch purchase intention sharefell in the latest survey, the increased overall desire to purchase wearables meant US demand increased, to 15MWatches, and now accounts for a much higher portion of our total estimate of 18M Watch shipments in CY15and 30M in the first 12 months, compared to 9M demand based on our December 2014 survey.

Exhibit 8:Exhibit 8: Apple Watch Purchase Intention Increased Over the Last Three Months

Sou rce: Alph aW ise Su rvey, Morgan Stan ley

Exhibit 9:Exhibit 9: Survey Suggests 15M US Unit Demand for Apple Watch, Extrapolating Purchase Intentions by USiPhone User Base

Sou rce: Alph aW ise Su rvey, comSco re, IDC, Morgan Stan ley Research

| April 15, 2015Technology & Brands

9

Apple's “halo effect” shines through. Among respondents intending to purchase wearables, those thatalready own wearables or Apple devices are more likely to purchase Apple's Watch. We believe users that arefamiliar with wearable use cases and/or Apple products and iOS/app store ecosystem are more willing to investin Apple. In our March survey, Apple's purchase intention share increases 1.5x to 28% among wearable ownersand increases 2x to 37% among iPhone users vs. its share among all wearable purchasers.

Exhibit 10:Exhibit 10: Apple Expected to Become a Wearable Market Leader, Despite Higher Price Point and iPhoneCompatibility Hurdles

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

Exhibit 11:Exhibit 11: Apple Halo Effect Translates to Stronger Watch Demand Among Wearable and iPhone Owners

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

10

Samsung ImplicationsSamsung Implications

Wearables could increase brand loyalty for Samsung. It saw the biggest increase in purchase intentionshare in the survey, from six to 12 points. Samsung's strategy in wearables is less about market share andprofits, in our view, but more about capturing consumer loyalty and brand. Its distinct brand and design focus,combined with its engineering prowess, allows it to release wearable devices into the market at a fast pace whilekeeping margins in check.

Samsung is expanding its wearables portfolio. The company entered the smartwatch market early inSeptember 2013 and capitalized on the popular health and fitness aspect of wearables. It expanded to fourmodels in 2014, including the popular Gear S, which doubles as a full standalone phone with its built-in 3Gtechnology and the Gear 2. Most of demand came primarily from the US, Korea and Western Europe. Samsungplans to provide upgrades to its existing 4-5 running models this year at different price points in themarketplace as well as introduce new concept wearables with its own innovative features.

Garmin ImplicationsGarmin Implications

Garmin gains modest share, but sees the market becoming more competitive. Garmin's share amongcurrent wearable owners increased to 10% from 8% in the latest survey. Purchase intention decreased, however,to 3% from 8%. Increased advertising at the end of the year along with new product (Vivosmart) and discounts(on the Vivofit) likely helped Garmin gain share during the holiday season, although its investments appear tohave come at the expense of 4Q Fitness segment margins. As we mentioned in our 4Q earnings notenote , webelieve the fitness band market will be increasingly competitive in 2015, something which the decreasedGarmin purchase intention and increased number of respondents who don't know which brand they are goingto purchase show.

Market still primarily looking for a device under $200. As can be seen in Exhibit 7, $155 is the averageamount wearable purchasers are looking to spend on their devices, with 40% looking to spend under $100 and28% looking to spend under $200. We take this as a positive for Garmin, as it points to ongoing strength in thefitness band market, even as more premium smartwatches are introduced. Additionally, it points to theopportunity available at the premium fitness band level (~$150-$200), which should help sales of the Vivosmartproduct, even with increasing competition.

Traditional Watch ImplicationsTraditional Watch Implications

Higher purchase intention of wearables is a risk to the traditional watch brands, we believe. With one-third of respondents planning to purchase wearable devices, this suggests 3x the level of purchase intention inthe last three months. We caveat our sample is across US consumers, a relatively small market for the Swiss

Exhibit 12:Exhibit 12: Garmin Gained A Modest Amount ofShare...

Source: AlphaWise Survey, Morgan Stanley Research

Exhibit 13:Exhibit 13: ...But Saw Purchase Intention Decrease

Source: AlphaWise Survey, Morgan Stanley Research

| April 15, 2015Technology & Brands

11

watch industry (US accounts for ~10% all exports), but we think the data is directionally similar in other regionsgiven increased awareness of the wearables category.

There is no clear picture from our survey to show whether consumers will be deterred from buying atraditional watch, although we expect we are at an interesting tipping point. Our survey results showthat wearable buyers/owners are still likely to purchase traditional watches. However, the majority of thosesurveyed who already own a traditional watch are unsure with regards to future appetite. This is key to monitorwe believe. So far, wearables/fitness tracking devices have been primarily bands which sit neatly alongsidetraditional watches. With larger devices (with more functionality) this becomes more difficult we expect.

The Apple Watch ranks well in terms of value for money. This shows strong appetite for additionalfunctionality, in our view. Given the premium price point of the Apple Watch and the view across our surveyrespondents that this is seen as good value, we think this is likely to provide a risk for the traditional watchbrands, particularly at the entry level or more commoditized segment. We think the high-end collectibles marketis largely immune given different purchase criteria (e.g. viewed as a product that holds its value long-term).

Exhibit 14:Exhibit 14: It Is Not Clear Whether Consumers Will be Deterred from Buying a Traditional Watch, or Not, withthe Choice of Wearables at this Stage

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

12

AlphaWise: What Gives Us ConfidenceAlphaWise: What Gives Us Confidence

We conducted two surveys among 1500 US adults who are cell phone users during December 2014 andMarch 2015. Conclusions based on the total sample have a margin of error of 2% at 90% confidenceinterval.

Exhibit 15:Exhibit 15: The Apple Watch is Largely Viewed as Good Value

Sou rce: Alph aW ise Su rvey, Morgan Stan ley Research

| April 15, 2015Technology & Brands

13

$160 Derived from base-case scenario.

Bull $19019x Bull Case CY15e EPS of$10.00

Apple is valued in-line with large-cap platform companiesacross industries. Investors believe Apple's platform can extendinto new products and industries over time. Revenue grows 20%+in CY15 driven by (1) $10B+ additional iPhone revenue from ex-US share gains, (2) $6B+ additional Watch revenue, and (3)accelerating Services revenue growth. Gross margin well above40% reflects higher iPhone, Watch and Services mix, andcomponent cost reductions. We assume a 19x P/E multiple, in-linewith US, large-cap platform companies across industries, or 17xadjusting for Apple’s net cash.

Base $16018x Base Case CY15e EPS of$8.86 or 15x Ex-Cash

Apple is valued as a technology platform company. Investorsincreasingly recognize the value and size of Apple's loyal users andexpanding platform. Revenue grows 13% in CY15 driven by largerscreen iPhone share gains in the US and China, and Watchpenetration into compatible iPhone installed base reaches 10%, vs.7% and 14% post the iPhone and iPad launches. Gross marginexpands 90bps Y/Y due to product mix. We assume an 18x P/Emultiple, in-line with other technology platform companies, or 15xadjusting for Apple’s $142B of net cash.

Investment ThesisInvestment Thesis

Apple has the world's most valuable technologyplatform, and is best positioned to capture more oftheir users' time in areas such as health, cars andhomes, as these platforms expand in the Internetof Things computing era. We believe the companydeserves at least a technology platform multiple of18x, which drives our price target of $160.

Key DebatesKey Debates

Can Apple grow revenue and EPS? Yes, at asingle-digit pace as it takes share in slower growthsmartphone and tablet markets with larger screensand new services. However, new productcategories (like Watch), services (Apple Pay), andpartnerships (HealthKit, HomeKit, CarPlay) couldfurther boost growth near-term with the additionof streaming music, TV and Autos longer-term.

Can Apple accelerate innovation? Yes, we seeWatch as an important barometer of thecompany's innovation capabilities under theleadership of Tim Cook. We are also encouragedby recent additions to Apple's management team,which expand leadership in key areas like retail,design, health, digital content, and recently autos.

Potential CatalystsPotential Catalysts

iPhone 6 and 6 Plus super cycle evidenced bystrong unit demand, ASP and marginimprovement, and share gains

Upcoming Watch and MacBook launches (shipApril 2015), potential new iPad, and potentialstreaming music or TV services

New products and/or services, for example inhealthcare, cars or homes, drive “halo effect” acrossApple's businesses

Expanding points-of-sale, especially in emergingmarkets like China, Brazil and India

Risks to Achieving Price TargetRisks to Achieving Price Target

Maturing markets, and Android and Windowscompetition in smartphones and tablets

Carriers lengthening replacement cycles and/orlower subsidies

Regulatory and legal risk as Apple gains profitshare in mobile devices

Bear $10313x Bear Case CY15e EPS of$7.90

Apple gets a large-cap IT Hardware valuation. Revenue growshigh-single digits as iPhone demand slows materially in C2H15 aslarger screens are not enough to sustain share gains andconsumers react to lower carrier subsidies. Wearables demandtakes longer to build momentum as use cases are not clear. Grossmargin remains flat Y/Y as pricing pressure (in part due tocurrency) offsets mix shift to higher-margin products. P/E multiplefalls to 13x or 10x after adjusting for Apple's net cash balance.

Apple Risk RewardApple Risk Reward

Sector: IT Hardware, Cautious; Stock: AAPL, Overweight

World's Most Valuable Technology Platform Enhanced by New Devices and Services

Sou rce: Th omson Reu ters, Morgan Stan ley Research

| April 15, 2015Technology & Brands

14

Weak global consumer spending and strong USDollar create headwinds

Lack of traction with new product categoriesand/or services limit multiple expansion

| April 15, 2015Technology & Brands

15

W1,600K Base-case scenario. Rounded from multistage residual incomemodel, supported by P/B of 1.2x.

Bull W1,900KBull case 2015e RI, upcycle1.7x BVPS

Macro environment recovers; further upside for handsets,strong share gains in foundry and OLED TV: Demand forconsumer electronics and memory recovers quickly withstabilization of macro environment. Smartphone shipments growfaster while capacity ramp-up at System LSI accelerates. TV shareimproves with OLED product offering.

Base W1,600KBase case 2015e RI, midcycle1.2x BVPS

Mobile strength continues: Handset division generates ~50% ofcore profits. OLED strength also continues with new productofferings and adoption in mid-market smartphones and largerpanels (e.g., tablets). Traditional commodity businesses remaincyclical but less volatile.

Investment ThesisInvestment Thesis

Smartphones to resume strength in 2015: Thisraises overall earnings growth with the broadeningof Galaxy products and displacement of lower-margin feature phones.

Valuation is attractive at 1.1x P/B, near its historicallow of 0.9x in the past 15 years.

The mobile division is past trough margins.Components and new growth drivers (System LSI)should contribute to growth in 2015.

Key Value DriversKey Value Drivers

Smartphone margins and shipments

Supply/demand outlook for memory

Earnings contribution from System LSI and OLED

Potential Upside RisksPotential Upside Risks

Success of Galaxy S6 and progress on mid-marketsmartphones.

Higher global economic growth expectations for2015. Samsung has both liquidity and beta, andhas historically outperformed in a market rally.

Capital returns – higher dividend payout and/orshare buyback

Reversal of provisioning for future lawsuit damages

Risks to Achieving Price TargetRisks to Achieving Price Target

Product cycle, including Apple and new Chinesesmartphone competition

New technology developments

High pricing pressure

Earnings growth – concentration in smartphones

Bear W1,000KBear case 2015e RI, downcycle1.0x BVPS

Prolonged consumption slowdown, competition and legalbattles: Weaker macro conditions stall near-term globalconsumption of IT products. Demand for smartphones slumpsamid rising competition. Legal disputes impair long-termprofitability.

Samsung Risk RewardSamsung Risk Reward

Sector: S. Korea Technology, In-Line; Stock: Samsung Electronics, Overweight

Samsung's risk-reward looks attractive at current levels

Sou rce: Th omson Reu ters, Morgan Stan ley Research

| April 15, 2015Technology & Brands

16

$47 15x CY 16e EPS

Bull $6119x CY 16e EPS

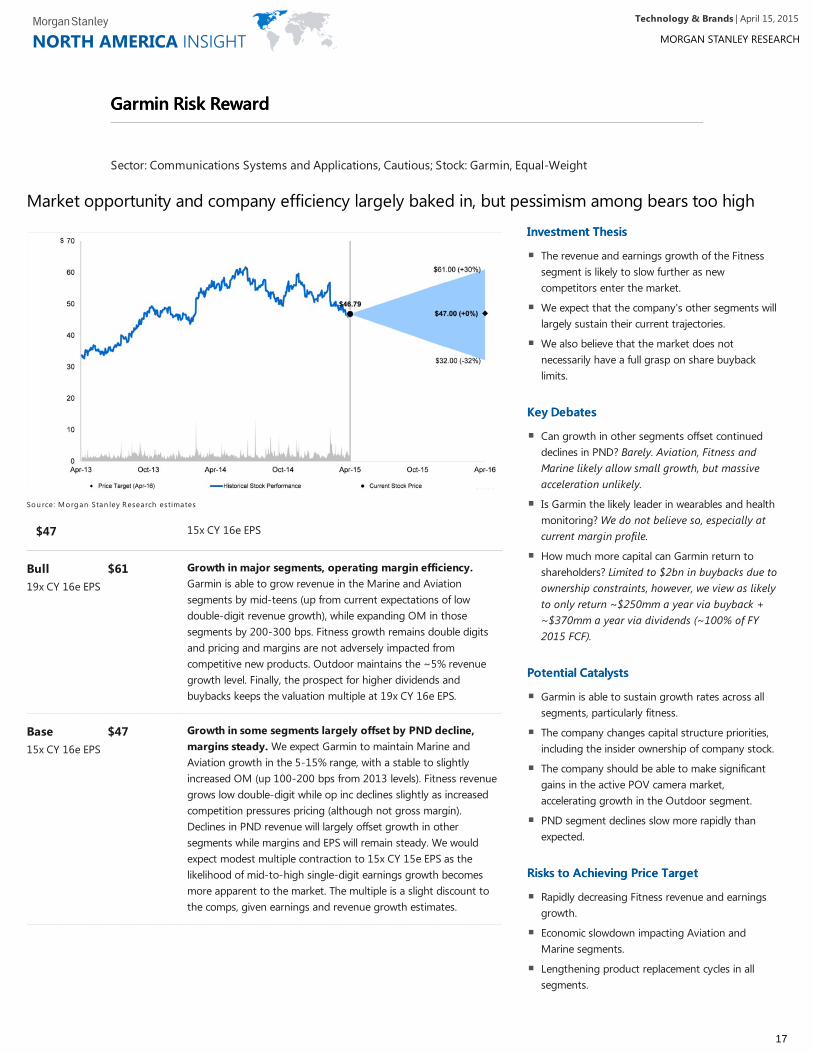

Growth in major segments, operating margin efficiency.Garmin is able to grow revenue in the Marine and Aviationsegments by mid-teens (up from current expectations of lowdouble-digit revenue growth), while expanding OM in thosesegments by 200-300 bps. Fitness growth remains double digitsand pricing and margins are not adversely impacted fromcompetitive new products. Outdoor maintains the ~5% revenuegrowth level. Finally, the prospect for higher dividends andbuybacks keeps the valuation multiple at 19x CY 16e EPS.

Base $4715x CY 16e EPS

Growth in some segments largely offset by PND decline,margins steady. We expect Garmin to maintain Marine andAviation growth in the 5-15% range, with a stable to slightlyincreased OM (up 100-200 bps from 2013 levels). Fitness revenuegrows low double-digit while op inc declines slightly as increasedcompetition pressures pricing (although not gross margin).Declines in PND revenue will largely offset growth in othersegments while margins and EPS will remain steady. We wouldexpect modest multiple contraction to 15x CY 15e EPS as thelikelihood of mid-to-high single-digit earnings growth becomesmore apparent to the market. The multiple is a slight discount tothe comps, given earnings and revenue growth estimates.

Investment ThesisInvestment Thesis

The revenue and earnings growth of the Fitnesssegment is likely to slow further as newcompetitors enter the market.

We expect that the company's other segments willlargely sustain their current trajectories.

We also believe that the market does notnecessarily have a full grasp on share buybacklimits.

Key DebatesKey Debates

Can growth in other segments offset continueddeclines in PND? Barely. Aviation, Fitness andMarine likely allow small growth, but massiveacceleration unlikely.

Is Garmin the likely leader in wearables and healthmonitoring? We do not believe so, especially atcurrent margin profile.

How much more capital can Garmin return toshareholders? Limited to $2bn in buybacks due toownership constraints, however, we view as likelyto only return ~$250mm a year via buyback +~$370mm a year via dividends (~100% of FY2015 FCF).

Potential CatalystsPotential Catalysts

Garmin is able to sustain growth rates across allsegments, particularly fitness.

The company changes capital structure priorities,including the insider ownership of company stock.

The company should be able to make significantgains in the active POV camera market,accelerating growth in the Outdoor segment.

PND segment declines slow more rapidly thanexpected.

Risks to Achieving Price TargetRisks to Achieving Price Target

Rapidly decreasing Fitness revenue and earningsgrowth.

Economic slowdown impacting Aviation andMarine segments.

Lengthening product replacement cycles in allsegments.

Garmin Risk RewardGarmin Risk Reward

Sector: Communications Systems and Applications, Cautious; Stock: Garmin, Equal-Weight

Market opportunity and company efficiency largely baked in, but pessimism among bears too high

Sou rce: Morgan Stan ley Research estimates

| April 15, 2015Technology & Brands

17

Bear $322.5x Net Cash Per Share

Increased competition and market saturation constraingrowth and cause margin compression. Fitness revenue andearnings shrink begin in 2015 as increased competition weighs onvolumes, pricing, and margins. At the same time, niche saturationin Outdoor and Marine hurts growth while a challenging defensespending environment continues to constrain Aviation andGarmin’s share gains in that segment begin to abate. High cashbalances and cash returns to investors limit valuation contractionto 2.5x ~$13 net cash per share (after deducting for expectedrestructuring costs of $1.50 per share).

| April 15, 2015Technology & Brands

18

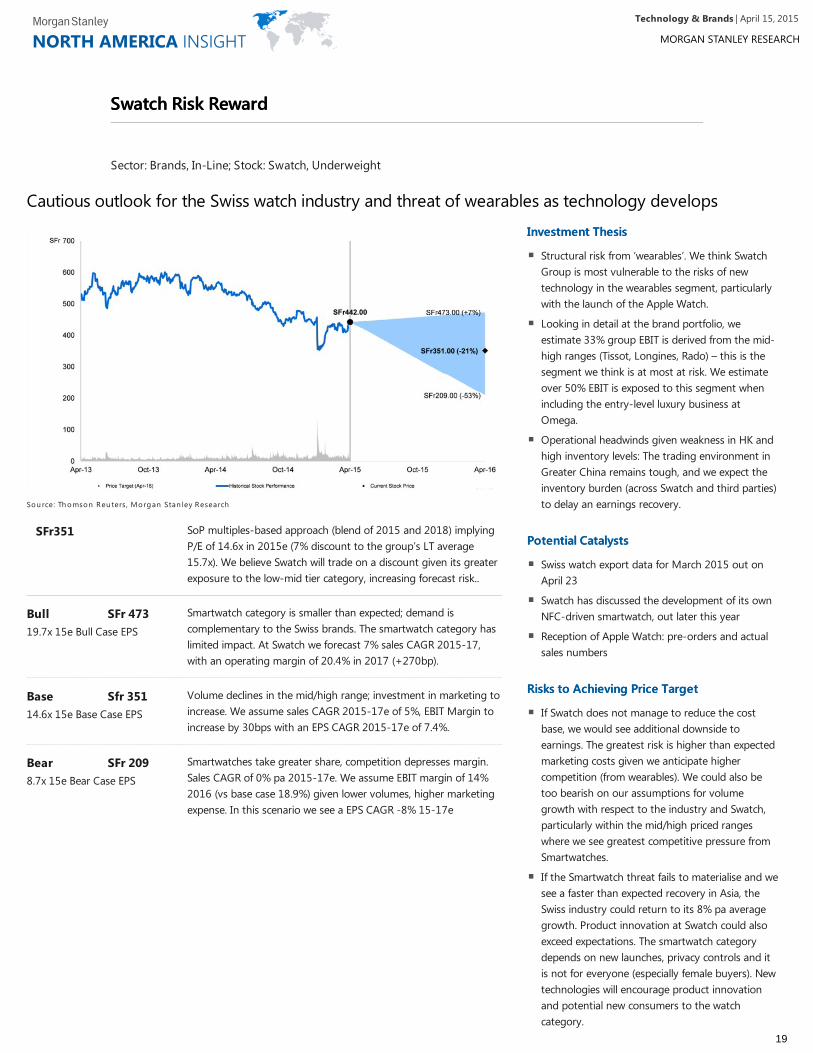

SFr351 SoP multiples-based approach (blend of 2015 and 2018) implyingP/E of 14.6x in 2015e (7% discount to the group’s LT average15.7x). We believe Swatch will trade on a discount given its greaterexposure to the low-mid tier category, increasing forecast risk..

Bull SFr 47319.7x 15e Bull Case EPS

Smartwatch category is smaller than expected; demand iscomplementary to the Swiss brands. The smartwatch category haslimited impact. At Swatch we forecast 7% sales CAGR 2015-17,with an operating margin of 20.4% in 2017 (+270bp).

Base Sfr 35114.6x 15e Base Case EPS

Volume declines in the mid/high range; investment in marketing toincrease. We assume sales CAGR 2015-17e of 5%, EBIT Margin toincrease by 30bps with an EPS CAGR 2015-17e of 7.4%.

Investment ThesisInvestment Thesis

Structural risk from ‘wearables’. We think SwatchGroup is most vulnerable to the risks of newtechnology in the wearables segment, particularlywith the launch of the Apple Watch.

Looking in detail at the brand portfolio, weestimate 33% group EBIT is derived from the mid-high ranges (Tissot, Longines, Rado) – this is thesegment we think is at most at risk. We estimateover 50% EBIT is exposed to this segment whenincluding the entry-level luxury business atOmega.

Operational headwinds given weakness in HK andhigh inventory levels: The trading environment inGreater China remains tough, and we expect theinventory burden (across Swatch and third parties)to delay an earnings recovery.

Potential CatalystsPotential Catalysts

Swiss watch export data for March 2015 out onApril 23

Swatch has discussed the development of its ownNFC-driven smartwatch, out later this year

Reception of Apple Watch: pre-orders and actualsales numbers

Risks to Achieving Price TargetRisks to Achieving Price Target

If Swatch does not manage to reduce the costbase, we would see additional downside toearnings. The greatest risk is higher than expectedmarketing costs given we anticipate highercompetition (from wearables). We could also betoo bearish on our assumptions for volumegrowth with respect to the industry and Swatch,particularly within the mid/high priced rangeswhere we see greatest competitive pressure fromSmartwatches.

If the Smartwatch threat fails to materialise and wesee a faster than expected recovery in Asia, theSwiss industry could return to its 8% pa averagegrowth. Product innovation at Swatch could alsoexceed expectations. The smartwatch categorydepends on new launches, privacy controls and itis not for everyone (especially female buyers). Newtechnologies will encourage product innovationand potential new consumers to the watchcategory.

Bear SFr 2098.7x 15e Bear Case EPS

Smartwatches take greater share, competition depresses margin.Sales CAGR of 0% pa 2015-17e. We assume EBIT margin of 14%2016 (vs base case 18.9%) given lower volumes, higher marketingexpense. In this scenario we see a EPS CAGR -8% 15-17e

Swatch Risk RewardSwatch Risk Reward

Sector: Brands, In-Line; Stock: Swatch, Underweight

Cautious outlook for the Swiss watch industry and threat of wearables as technology develops

Sou rce: Th omson Reu ters, Morgan Stan ley Research

| April 15, 2015Technology & Brands

19

| April 15, 2015Technology & Brands

20

Disclosure SectionThe information and opinions in Morgan Stanley Research were prepared by Morgan Stanley & Co. LLC, and/or Morgan Stanley C.T.V.M. S.A., and/orMorgan Stanley Mexico, Casa de Bolsa, S.A. de C.V., and/or Morgan Stanley Canada Limited. As used in this disclosure section, "Morgan Stanley"includes Morgan Stanley & Co. LLC, Morgan Stanley C.T.V.M. S.A., Morgan Stanley Mexico, Casa de Bolsa, S.A. de C.V., Morgan Stanley CanadaLimited and their affiliates as necessary.For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the MorganStanley Research Disclosure Website at www.morganstanley.com/researchdisclosures, or contact your investment representative or Morgan StanleyResearch at 1585 Broadway, (Attention: Research Management), New York, NY, 10036 USA.For valuation methodology and risks associated with any price targets referenced in this research report, please contact the Client Support Team as follows:US/Canada +1 800 303-2495; Hong Kong +852 2848-5999; Latin America +1 718 754-5444 (U.S.); London +44 (0)20-7425-8169; Singapore +65 6834-6860;Sydney +61 (0)2-9770-1505; Tokyo +81 (0)3-6836-9000. Alternatively you may contact your investment representative or Morgan Stanley Research at 1585Broadway, (Attention: Research Management), New York, NY 10036 USA.Analyst CertificationThe following analysts hereby certify that their views about the companies and their securities discussed in this report are accurately expressed and thatthey have not received and will not receive direct or indirect compensation in exchange for expressing specific recommendations or views in this report:James Faucette, Katy Huberty, Shawn Kim, Louise Singlehurst.Unless otherwise stated, the individuals listed on the cover page of this report are research analysts.Global Research Conflict Management PolicyMorgan Stanley Research has been published in accordance with our conflict management policy, which is available atwww.morganstanley.com/institutional/research/conflictpolicies.Important US Regulatory Disclosures on Subject CompaniesAs of March 31, 2015, Morgan Stanley beneficially owned 1% or more of a class of common equity securities of the following companies covered in MorganStanley Research: Apple, Inc., Danaher, Eaton Corp PLC, GoPro Inc, Honeywell International, Samsung Electronics, Swatch, United Technologies Corp.Within the last 12 months, Morgan Stanley managed or co-managed a public offering (or 144A offering) of securities of 3M Co., ADT Corp, General ElectricCo., GoPro Inc, HD Supply Holdings Inc, Tyco International.Within the last 12 months, Morgan Stanley has received compensation for investment banking services from 3M Co., ADT Corp, General Electric Co.,GoPro Inc, HD Supply Holdings Inc, Lennox International, Tyco International, United Technologies Corp.In the next 3 months, Morgan Stanley expects to receive or intends to seek compensation for investment banking services from 3M Co., ADT Corp, AmetekInc., Apple, Inc., Danaher, Dover, Eaton Corp PLC, Emerson Electric, Garmin Ltd, General Electric Co., GoPro Inc, HD Supply Holdings Inc, HoneywellInternational, Hubbell Inc., Illinois Tool Works, Ingersoll Rand, Lennox International, Proto Labs Inc, Regal-Beloit Corp., Rockwell Automation, SamsungElectronics, SPX Corp, Stanley Black & Decker, Tyco International, United Technologies Corp, W.W. Grainger Inc., Watsco Inc., WESCO InternationalInc..Within the last 12 months, Morgan Stanley has received compensation for products and services other than investment banking services from 3M Co., ADTCorp, Apple, Inc., Danaher, Dover, Eaton Corp PLC, Garmin Ltd, General Electric Co., Honeywell International, Hubbell Inc., Illinois Tool Works, Regal-Beloit Corp., SPX Corp, Stanley Black & Decker, Tyco International, W.W. Grainger Inc., WESCO International Inc..Within the last 12 months, Morgan Stanley has provided or is providing investment banking services to, or has an investment banking client relationshipwith, the following company: 3M Co., ADT Corp, Ametek Inc., Apple, Inc., Danaher, Dover, Eaton Corp PLC, Emerson Electric, Garmin Ltd, General ElectricCo., GoPro Inc, HD Supply Holdings Inc, Honeywell International, Hubbell Inc., Illinois Tool Works, Ingersoll Rand, Lennox International, Proto Labs Inc,Regal-Beloit Corp., Rockwell Automation, Samsung Electronics, SPX Corp, Stanley Black & Decker, Tyco International, United Technologies Corp, W.W.Grainger Inc., Watsco Inc., WESCO International Inc..Within the last 12 months, Morgan Stanley has either provided or is providing non-investment banking, securities-related services to and/or in the past hasentered into an agreement to provide services or has a client relationship with the following company: 3M Co., ADT Corp, Apple, Inc., Danaher, Dover, EatonCorp PLC, Emerson Electric, Garmin Ltd, General Electric Co., Honeywell International, Hubbell Inc., Illinois Tool Works, Lennox International, Regal-BeloitCorp., Rockwell Automation, SPX Corp, Stanley Black & Decker, Tyco International, United Technologies Corp, W.W. Grainger Inc., WESCO InternationalInc..Morgan Stanley & Co. LLC makes a market in the securities of 3M Co., ADT Corp, Ametek Inc., Apple, Inc., Danaher, Dover, Eaton Corp PLC, EmersonElectric, Garmin Ltd, General Electric Co., HD Supply Holdings Inc, Honeywell International, Hubbell Inc., Illinois Tool Works, Ingersoll Rand, LennoxInternational, Proto Labs Inc, Regal-Beloit Corp., Rockwell Automation, SPX Corp, Stanley Black & Decker, Tyco International, United Technologies Corp,W.W. Grainger Inc., Watsco Inc., WESCO International Inc..The equity research analysts or strategists principally responsible for the preparation of Morgan Stanley Research have received compensation based uponvarious factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment bankingrevenues.Morgan Stanley and its affiliates do business that relates to companies/instruments covered in Morgan Stanley Research, including market making,providing liquidity and specialized trading, risk arbitrage and other proprietary trading, fund management, commercial banking, extension of credit,investment services and investment banking. Morgan Stanley sells to and buys from customers the securities/instruments of companies covered in MorganStanley Research on a principal basis. Morgan Stanley may have a position in the debt of the Company or instruments discussed in this report.Certain disclosures listed above are also for compliance with applicable regulations in non-US jurisdictions.STOCK RATINGSMorgan Stanley uses a relative rating system using terms such as Overweight, Equal-weight, Not-Rated or Underweight (see definitions below). MorganStanley does not assign ratings of Buy, Hold or Sell to the stocks we cover. Overweight, Equal-weight, Not-Rated and Underweight are not the equivalent ofbuy, hold and sell. Investors should carefully read the definitions of all ratings used in Morgan Stanley Research. In addition, since Morgan StanleyResearch contains more complete information concerning the analyst's views, investors should carefully read Morgan Stanley Research, in its entirety, andnot infer the contents from the rating alone. In any case, ratings (or research) should not be used or relied upon as investment advice. An investor's decisionto buy or sell a stock should depend on individual circumstances (such as the investor's existing holdings) and other considerations.Global Stock Ratings Distribution(as of March 31, 2015)For disclosure purposes only (in accordance with NASD and NYSE requirements), we include the category headings of Buy, Hold, and Sell alongside ourratings of Overweight, Equal-weight, Not-Rated and Underweight. Morgan Stanley does not assign ratings of Buy, Hold or Sell to the stocks we cover.Overweight, Equal-weight, Not-Rated and Underweight are not the equivalent of buy, hold, and sell but represent recommended relative weightings (seedefinitions below). To satisfy regulatory requirements, we correspond Overweight, our most positive stock rating, with a buy recommendation; we correspondEqual-weight and Not-Rated to hold and Underweight to sell recommendations, respectively.

| April 15, 2015Technology & Brands

21

COVERAGE UNIVERSE INVESTMENT BANKING CLIENTS (IBC)STOCK RATING CATEGORY COUNT % OF TOTAL COUNT % OF TOTAL

IBC% OF RATING

CATEGORYOverweight/Buy 1164 35% 331 43% 28%Equal-weight/Hold 1466 44% 353 46% 24%Not-Rated/Hold 100 3% 11 1% 11%Underweight/Sell 605 18% 80 10% 13%TOTAL 3,335 775

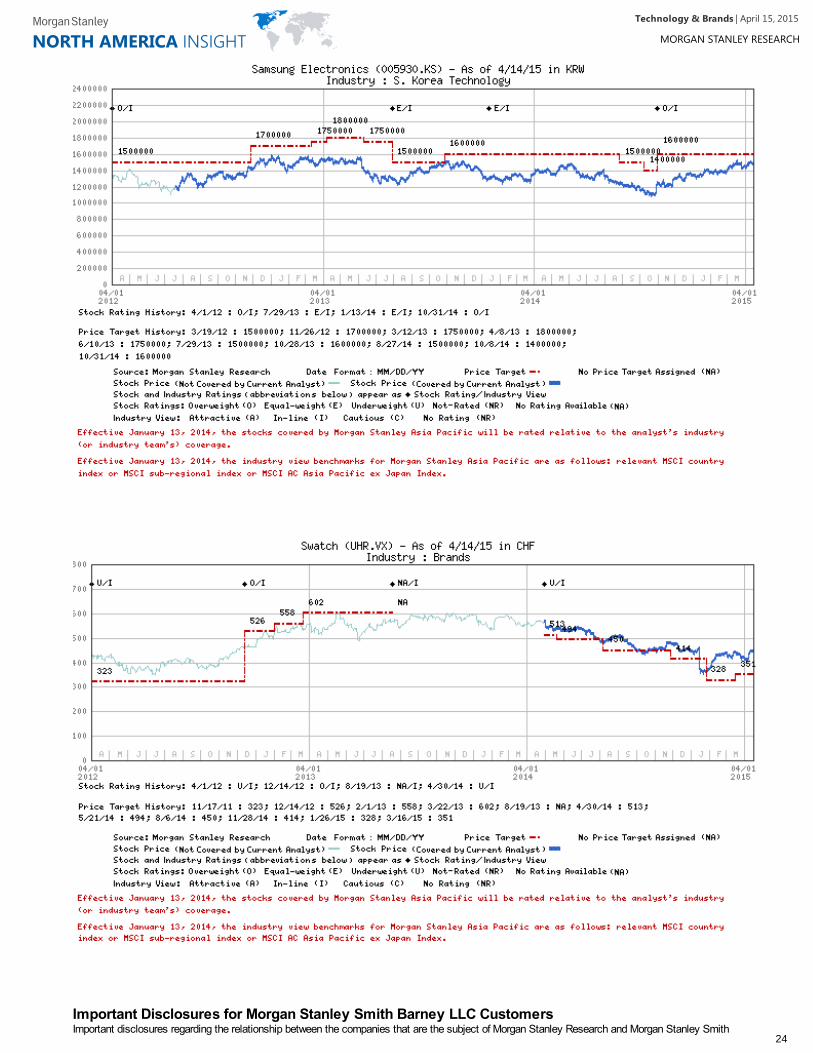

Data include common stock and ADRs currently assigned ratings. Investment Banking Clients are companies from whom Morgan Stanley receivedinvestment banking compensation in the last 12 months.Analyst Stock RatingsOverweight (O). The stock's total return is expected to exceed the average total return of the analyst's industry (or industry team's) coverage universe, on arisk-adjusted basis, over the next 12-18 months.Equal-weight (E). The stock's total return is expected to be in line with the average total return of the analyst's industry (or industry team's) coverageuniverse, on a risk-adjusted basis, over the next 12-18 months.Not-Rated (NR). Currently the analyst does not have adequate conviction about the stock's total return relative to the average total return of the analyst'sindustry (or industry team's) coverage universe, on a risk-adjusted basis, over the next 12-18 months.Underweight (U). The stock's total return is expected to be below the average total return of the analyst's industry (or industry team's) coverage universe, ona risk-adjusted basis, over the next 12-18 months.Unless otherwise specified, the time frame for price targets included in Morgan Stanley Research is 12 to 18 months.Analyst Industry ViewsAttractive (A): The analyst expects the performance of his or her industry coverage universe over the next 12-18 months to be attractive vs. the relevantbroad market benchmark, as indicated below.In-Line (I): The analyst expects the performance of his or her industry coverage universe over the next 12-18 months to be in line with the relevant broadmarket benchmark, as indicated below.Cautious (C): The analyst views the performance of his or her industry coverage universe over the next 12-18 months with caution vs. the relevant broadmarket benchmark, as indicated below.Benchmarks for each region are as follows: North America - S&P 500; Latin America - relevant MSCI country index or MSCI Latin America Index; Europe -MSCI Europe; Japan - TOPIX; Asia - relevant MSCI country index or MSCI sub-regional index or MSCI AC Asia Pacific ex Japan Index.Stock Price, Price Target and Rating History (See Rating Definitions)

| April 15, 2015Technology & Brands

22

| April 15, 2015Technology & Brands

23

Important Disclosures for Morgan Stanley Smith Barney LLC CustomersImportant disclosures regarding the relationship between the companies that are the subject of Morgan Stanley Research and Morgan Stanley Smith

| April 15, 2015Technology & Brands

24

Barney LLC or Morgan Stanley or any of their affiliates, are available on the Morgan Stanley Wealth Management disclosure website atwww.morganstanley.com/online/researchdisclosures. For Morgan Stanley specific disclosures, you may refer towww.morganstanley.com/researchdisclosures.Each Morgan Stanley Equity Research report is reviewed and approved on behalf of Morgan Stanley Smith Barney LLC. This review and approval isconducted by the same person who reviews the Equity Research report on behalf of Morgan Stanley. This could create a conflict of interest.Other Important DisclosuresMorgan Stanley & Co. International PLC and its affiliates have a significant financial interest in the debt securities of 3M Co., ADT Corp, Apple, Inc.,Danaher, Dover, Eaton Corp PLC, Emerson Electric, Honeywell International, Hubbell Inc., Illinois Tool Works, Lennox International, Samsung Electronics,Stanley Black & Decker, Tyco International, United Technologies Corp.Morgan Stanley is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice withinthe meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act.Morgan Stanley produces an equity research product called a "Tactical Idea." Views contained in a "Tactical Idea" on a particular stock may be contrary tothe recommendations or views expressed in research on the same stock. This may be the result of differing time horizons, methodologies, market events, orother factors. For all research available on a particular stock, please contact your sales representative or go to Matrix athttp://www.morganstanley.com/matrix.Morgan Stanley Research is provided to our clients through our proprietary research portal on Matrix and also distributed electronically by Morgan Stanleyto clients. Certain, but not all, Morgan Stanley Research products are also made available to clients through third-party vendors or redistributed to clientsthrough alternate electronic means as a convenience. For access to all available Morgan Stanley Research, please contact your sales representative or goto Matrix at http://www.morganstanley.com/matrix.Any access and/or use of Morgan Stanley Research is subject to Morgan Stanley's Terms of Use (http://www.morganstanley.com/terms.html). Byaccessing and/or using Morgan Stanley Research, you are indicating that you have read and agree to be bound by our Terms of Use(http://www.morganstanley.com/terms.html). In addition you consent to Morgan Stanley processing your personal data and using cookies in accordancewith our Privacy Policy and our Global Cookies Policy (http://www.morganstanley.com/privacy_pledge.html), including for the purposes of setting yourpreferences and to collect readership data so that we can deliver better and more personalized service and products to you. To find out more informationabout how Morgan Stanley processes personal data, how we use cookies and how to reject cookies see our Privacy Policy and our Global Cookies Policy(http://www.morganstanley.com/privacy_pledge.html).If you do not agree to our Terms of Use and/or if you do not wish to provide your consent to Morgan Stanley processing your personal data or using cookiesplease do not access our research.Morgan Stanley Research does not provide individually tailored investment advice. Morgan Stanley Research has been prepared without regard to thecircumstances and objectives of those who receive it. Morgan Stanley recommends that investors independently evaluate particular investments andstrategies, and encourages investors to seek the advice of a financial adviser. The appropriateness of an investment or strategy will depend on an investor'scircumstances and objectives. The securities, instruments, or strategies discussed in Morgan Stanley Research may not be suitable for all investors, andcertain investors may not be eligible to purchase or participate in some or all of them. Morgan Stanley Research is not an offer to buy or sell or thesolicitation of an offer to buy or sell any security/instrument or to participate in any particular trading strategy. The value of and income from yourinvestments may vary because of changes in interest rates, foreign exchange rates, default rates, prepayment rates, securities/instruments prices, marketindexes, operational or financial conditions of companies or other factors. There may be time limitations on the exercise of options or other rights insecurities/instruments transactions. Past performance is not necessarily a guide to future performance. Estimates of future performance are based onassumptions that may not be realized. If provided, and unless otherwise stated, the closing price on the cover page is that of the primary exchange for thesubject company's securities/instruments.The fixed income research analysts, strategists or economists principally responsible for the preparation of Morgan Stanley Research have receivedcompensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues (which include fixed income tradingand capital markets profitability or revenues), client feedback and competitive factors. Fixed Income Research analysts', strategists' or economists'compensation is not linked to investment banking or capital markets transactions performed by Morgan Stanley or the profitability or revenues of particulartrading desks.The "Important US Regulatory Disclosures on Subject Companies" section in Morgan Stanley Research lists all companies mentioned where MorganStanley owns 1% or more of a class of common equity securities of the companies. For all other companies mentioned in Morgan Stanley Research,Morgan Stanley may have an investment of less than 1% in securities/instruments or derivatives of securities/instruments of companies and may trade themin ways different from those discussed in Morgan Stanley Research. Employees of Morgan Stanley not involved in the preparation of Morgan StanleyResearch may have investments in securities/instruments or derivatives of securities/instruments of companies mentioned and may trade them in waysdifferent from those discussed in Morgan Stanley Research. Derivatives may be issued by Morgan Stanley or associated persons.With the exception of information regarding Morgan Stanley, Morgan Stanley Research is based on public information. Morgan Stanley makes every effort touse reliable, comprehensive information, but we make no representation that it is accurate or complete. We have no obligation to tell you when opinions orinformation in Morgan Stanley Research change apart from when we intend to discontinue equity research coverage of a subject company. Facts and viewspresented in Morgan Stanley Research have not been reviewed by, and may not reflect information known to, professionals in other Morgan Stanleybusiness areas, including investment banking personnel.Morgan Stanley Research personnel may participate in company events such as site visits and are generally prohibited from accepting payment by thecompany of associated expenses unless pre-approved by authorized members of Research management.Morgan Stanley may make investment decisions or take proprietary positions that are inconsistent with the recommendations or views in this report.To our readers in Taiwan: Information on securities/instruments that trade in Taiwan is distributed by Morgan Stanley Taiwan Limited ("MSTL"). Suchinformation is for your reference only. The reader should independently evaluate the investment risks and is solely responsible for their investment decisions.Morgan Stanley Research may not be distributed to the public media or quoted or used by the public media without the express written consent of MorganStanley. Information on securities/instruments that do not trade in Taiwan is for informational purposes only and is not to be construed as a recommendationor a solicitation to trade in such securities/instruments. MSTL may not execute transactions for clients in these securities/instruments. To our readers inHong Kong: Information is distributed in Hong Kong by and on behalf of, and is attributable to, Morgan Stanley Asia Limited as part of its regulated activitiesin Hong Kong. If you have any queries concerning Morgan Stanley Research, please contact our Hong Kong sales representatives.Morgan Stanley is not incorporated under PRC law and the research in relation to this report is conducted outside the PRC. Morgan Stanley Research doesnot constitute an offer to sell or the solicitation of an offer to buy any securities in the PRC. PRC investors shall have the relevant qualifications to invest insuch securities and shall be responsible for obtaining all relevant approvals, licenses, verifications and/or registrations from the relevant governmentalauthorities themselves.Morgan Stanley Research is disseminated in Brazil by Morgan Stanley C.T.V.M. S.A.; in Japan by Morgan Stanley MUFG Securities Co., Ltd. and, forCommodities related research reports only, Morgan Stanley Capital Group Japan Co., Ltd; in Hong Kong by Morgan Stanley Asia Limited (which acceptsresponsibility for its contents) and by Bank Morgan Stanley AG, Hong Kong Branch; in Singapore by Morgan Stanley Asia (Singapore) Pte. (Registrationnumber 199206298Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number 200008434H), regulated by the Monetary Authority ofSingapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with,Morgan Stanley Research) and by Bank Morgan Stanley AG, Singapore Branch (Registration number T11FC0207F); in Australia to "wholesale clients"within the meaning of the Australian Corporations Act by Morgan Stanley Australia Limited A.B.N. 67 003 734 576, holder of Australian financial serviceslicense No. 233742, which accepts responsibility for its contents; in Australia to "wholesale clients" and "retail clients" within the meaning of the AustralianCorporations Act by Morgan Stanley Wealth Management Australia Pty Ltd (A.B.N. 19 009 145 555, holder of Australian financial services license No.240813, which accepts responsibility for its contents; in Korea by Morgan Stanley & Co International plc, Seoul Branch; in India by Morgan Stanley India

| April 15, 2015Technology & Brands

25

Company Private Limited; in Indonesia by PT Morgan Stanley Asia Indonesia; in Canada by Morgan Stanley Canada Limited, which has approved of andtakes responsibility for its contents in Canada; in Germany by Morgan Stanley Bank AG, Frankfurt am Main and Morgan Stanley Private WealthManagement Limited, Niederlassung Deutschland, regulated by Bundesanstalt fuer Finanzdienstleistungsaufsicht (BaFin); in Spain by Morgan Stanley,S.V., S.A., a Morgan Stanley group company, which is supervised by the Spanish Securities Markets Commission (CNMV) and states that Morgan StanleyResearch has been written and distributed in accordance with the rules of conduct applicable to financial research as established under Spanishregulations; in the US by Morgan Stanley & Co. LLC, which accepts responsibility for its contents. Morgan Stanley & Co. International plc, authorized bythe Prudential Regulatory Authority and regulated by the Financial Conduct Authority and the Prudential Regulatory Authority, disseminates in the UKresearch that it has prepared, and approves solely for the purposes of section 21 of the Financial Services and Markets Act 2000, research which has beenprepared by any of its affiliates. Morgan Stanley Private Wealth Management Limited, authorized and regulated by the Financial Conduct Authority, alsodisseminates Morgan Stanley Research in the UK. Private UK investors should obtain the advice of their Morgan Stanley & Co. International plc or MorganStanley Private Wealth Management representative about the investments concerned. RMB Morgan Stanley (Proprietary) Limited is a member of the JSELimited and regulated by the Financial Services Board in South Africa. RMB Morgan Stanley (Proprietary) Limited is a joint venture owned equally byMorgan Stanley International Holdings Inc. and RMB Investment Advisory (Proprietary) Limited, which is wholly owned by FirstRand Limited.The information in Morgan Stanley Research is being communicated by Morgan Stanley & Co. International plc (DIFC Branch), regulated by the DubaiFinancial Services Authority (the DFSA), and is directed at Professional Clients only, as defined by the DFSA. The financial products or financial services towhich this research relates will only be made available to a customer who we are satisfied meets the regulatory criteria to be a Professional Client.The information in Morgan Stanley Research is being communicated by Morgan Stanley & Co. International plc (QFC Branch), regulated by the QatarFinancial Centre Regulatory Authority (the QFCRA), and is directed at business customers and market counterparties only and is not intended for RetailCustomers as defined by the QFCRA.As required by the Capital Markets Board of Turkey, investment information, comments and recommendations stated here, are not within the scope ofinvestment advisory activity. Investment advisory service is provided exclusively to persons based on their risk and income preferences by the authorizedfirms. Comments and recommendations stated here are general in nature. These opinions may not fit to your financial status, risk and return preferences.For this reason, to make an investment decision by relying solely to this information stated here may not bring about outcomes that fit your expectations.The following companies do business in countries which are generally subject to comprehensive sanctions programs administered or enforced by the U.S.Department of the Treasury's Office of Foreign Assets Control ("OFAC") and by other countries and multi-national bodies: Samsung Electronics.The trademarks and service marks contained in Morgan Stanley Research are the property of their respective owners. Third-party data providers make nowarranties or representations relating to the accuracy, completeness, or timeliness of the data they provide and shall not have liability for any damagesrelating to such data. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and S&P. Morgan StanleyResearch or portions of it may not be reprinted, sold or redistributed without the written consent of Morgan Stanley.Morgan Stanley Research, or any portion thereof may not be reprinted, sold or redistributed without the written consent of Morgan Stanley.

INDUSTRY COVERAGE: Multi-Industry

COMPANY (TICKER) RATING (AS OF) PRICE* (04/14/2015)

Coe CFA, Nigel3M Co. (MMM.N) U (12/02/2013) $165.99ADT Corp (ADT.N) U (01/12/2015) $42.17Ametek Inc. (AME.N) E (10/03/2012) $52.99Danaher (DHR.N) E (01/12/2015) $85.48Dover (DOV.N) E (12/02/2013) $70.91Eaton Corp PLC (ETN.N) O (09/09/2013) $68.66Emerson Electric (EMR.N) E (01/08/2013) $58.33General Electric Co. (GE.N) E (05/02/2014) $27.73Honeywell International (HON.N) O (01/04/2012) $103.25Hubbell Inc. (HUBb.N) E (02/26/2015) $110.65Illinois Tool Works (ITW.N) U (04/12/2012) $99.49Ingersoll Rand (IR.N) O (01/12/2015) $68.58Lennox International (LII.N) E (02/07/2014) $111.51Regal-Beloit Corp. (RBC.N) E (10/03/2012) $76.75Rockwell Automation (ROK.N) U (01/08/2013) $111.52SPX Corp (SPW.N) O (01/04/2012) $84.42Stanley Black & Decker (SWK.N) E (10/17/2013) $95.93Tyco International (TYC.N) O (07/01/2013) $43.22United Technologies Corp (UTX.N) O (03/27/2013) $117.69

Sang, Michael WHD Supply Holdings Inc (HDS.O) E (05/13/2014) $31.84W.W. Grainger Inc. (GWW.N) O (05/13/2014) $238.15Watsco Inc. (WSO.N) E (05/13/2014) $125.50WESCO International Inc. (WCC.N) E (05/13/2014) $70.01

Schmitz, ScottProto Labs Inc (PRLB.N) E (10/03/2014) $76.56

Stock Ratings are subject to change. Please see latest research for each company.* Historical prices are not split adjusted.

© 2015 Morgan Stanley

| April 15, 2015Technology & Brands

26