Embed Size (px)

Citation preview

This article was downloaded by: [Stony Brook University]On: 19 October 2014, At: 23:38Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Europe-Asia StudiesPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/ceas20

Technical Efficiency, AllocativeEfficiency and Profitability inHungarian Small and Medium-SizedEnterprises: A Model with FrontierFunctionsIván Major aa Institute of Economics, The Hungarian Academy of Sciences ,BudapestPublished online: 12 Sep 2008.

To cite this article: Iván Major (2008) Technical Efficiency, Allocative Efficiency and Profitabilityin Hungarian Small and Medium-Sized Enterprises: A Model with Frontier Functions, Europe-AsiaStudies, 60:8, 1371-1396, DOI: 10.1080/09668130802292200

To link to this article: http://dx.doi.org/10.1080/09668130802292200

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoever orhowsoever caused arising directly or indirectly in connection with, in relation to or arisingout of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &

Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

Technical Efficiency, Allocative Efficiency

and Profitability in Hungarian Small and

Medium-Sized Enterprises: A Model with

Frontier Functions

IVAN MAJOR

Abstract

By applying a simple model of frontier production functions, this article shows that Hungarian small

and medium-sized enterprises (SMEs) produce far below their feasible level, given their input

endowment. The SMEs’ under-production is rooted in the allocative inefficiency of small and medium-

sized firms: they use labour in excess while they lack a sufficient level of capital assets. As a consequence

of large inefficiencies, Hungarian SMEs improve profitability by scaling down production rather than

by expansion.

THE ECONOMIC TRANSFORMATION OF CENTRAL AND East European (CEE)

economies has been dominated by a large inflow of foreign capital in all countries

in the region.1 Foreign capital arrived in many different forms and sizes. Foreign

investors acquired formerly state-owned companies or they invested in the

privatisation funds that had been set up by national governments. In addition,

foreigners invested in ‘green field’ developments or they engaged in financial

investments. The presence and the economic activities of the international community

have become decisive in many of the CEE economies. Empirical analyses show that

I am grateful for valuable and helpful comments from two anonymous referees, to Janos Koll}o,

Mihaly Laki, James Rauch, Akos Rona-Tas, Attila K. Soos, the late Marton Tardos, and to

conference participants at the Institute of Economics, HAS and at the University of California San

Diego. Financial support from the Hungarian Science Foundation (OTKA grant no. T 048680) is

thankfully acknowledged.1The countries of Central and Eastern Europe are a very heterogeneous group, including countries

that are now members of the European Union, independent member states that were formerly

members of the Soviet Union, former member states of Yugoslavia, and Albania. While all these

countries share a number of common features from the socialist past, and encountered similar

difficulties during the transition, their paths of development also differ in many respects, including the

importance of foreign participation in their economies and the development of the SME sector.

EUROPE-ASIA STUDIES

Vol. 60, No. 8, October 2008, 1371–1396

ISSN 0966-8136 print; ISSN 1465-3427 online/08/081371-26 ª 2008 University of Glasgow

DOI: 10.1080/09668130802292200

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

the countries that have developed fastest were those that were able to attract the

largest amount of foreign direct investment during the past 18 years (Kornai 2007, pp.

79–111, 136–62; Major 1999b, pp. 59–390; Parker & Saal 2003, pp. 323–476; Pohl et al.

1997).

As well as increasing foreign involvement, the number of domestic companies also

exploded during the transition. Hundreds of thousands of small entrepreneurs started

their business after the dominance of state ownership was abandoned. Most of these

domestic firms remained really small: they operated as family businesses or as a form

of ‘forced entrepreneurship’ that resulted from rapidly growing unemployment. But a

few thousand domestic firms emerged as small and medium-sized enterprises (SMEs)

with similar structures and ambitions to their Western counterparts. A few of these

SMEs turned out to be successful—mostly in special trades, such as confectionery or

other handicraft industries, or in industries where the primary input has been some

special knowledge or talent—but most of them simply survived without experiencing

any significant growth. In general, there is a clear divide between large foreign

corporations on the one hand, and small domestic firms on the other. This article

offers a possible explanation for the moderate success—or failure—of domestic

companies in Hungary and in other transition countries.2 In particular, I shall argue

that most small domestic firms in Hungary and in other CEE countries are either not

flexible enough to adjust to the fairly volatile market conditions they face, or they were

established by their owners for some special purpose, such as, for instance, tax evasion

or simply to move money around.

It is important to note that there are substantial differences between the economic

conditions that Hungarian SMEs operate in and those in other transition countries

beside all the similarities of their heritage and current economic environment. While

SMEs throughout the region suffer from shortages in financial resources, from

bureaucratic red tape and from the weaknesses of the institutional system, especially

from uncertain property rights, Hungarian SMEs have been particularly affected by

the dominant role of foreign businesses, and the impact of the gradualist transition

that has been more prevalent in Hungary than in other CEE countries. I shall

show that the majority of Hungarian SMEs, with a few exceptions, are far away from

their feasible level of technical and economic (or cost-) efficiency.3 I also analyse the

connection between the technical efficiency and profitability of small and medium-

sized companies. I focus on the case of Hungarian SMEs but most of my discussion

also holds for SMEs in other transition economies.

I selected the group of SMEs for several reasons. First, this is the pool of companies

that has been targeted by specific policy measures within most European countries and

also on the level of the European Union. This then raises the question of whether

SMEs will become the foundation of economic development in transition economies.

While global companies have grown from strong domestic industries in the advanced

2There are, of course, exceptions, and we find countries in CEE where the ‘new private sector’ of

domestic SMEs has performed better than in Hungary or in some other CEE countries. Poland may be

one example since it had a more dynamic SME sector in the early and mid-1990s (Gomulka 1994).

Aidis and Mickiewicz (2006) also report impressive results for Lithuanian SMEs.3I use the terms technical and economic efficiency as these notions have been defined by Kumbhakar

and Lovell (2000, pp. 42 and 51, respectively).

1372 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

economies, in transition economies domestic firms have struggled to survive mainly in

niche markets that have been abandoned by the large multinational corporations.

Second, SMEs usually operate with constant or diminishing returns. This feature

renders the analysis fairly simple, for SMEs can be regarded as firms operating in a

perfectly competitive market. Then, we can apply simple production functions,

notably, Cobb–Douglas production4 functions to describe SMEs’ technology without

falling into the trap of an insoluble profit maximisation problem. (Test results on

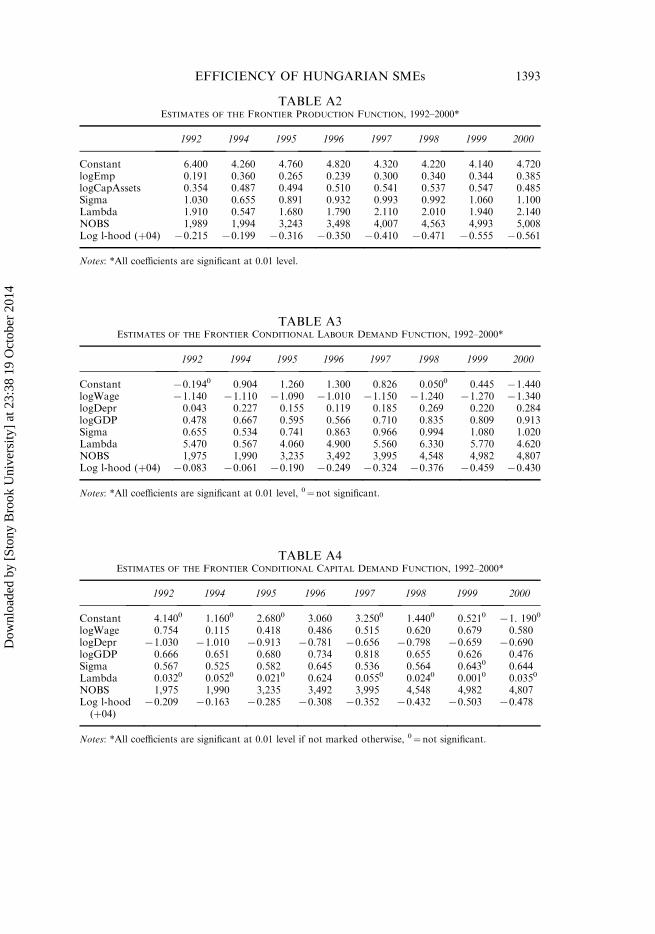

Hungarian SMEs’ diminishing returns are presented in Table A1 in the Appendix.)

The structure of the article is as follows. First, I outline the analytical background

and give a concise literature review. Then I present the basic empirical evidence on the

moderate performance of Hungarian SMEs, before discussing a simple simultaneous

model of technical and allocative efficiency in the following section. This is followed by

a description of the database and the estimation methods and a discussion of the

estimation results.

Methodology and literature review

Economic analyses of corporate performance have favoured measures of productivity

more than profitability measures during the last decades. Nickell (1996), for instance,

referred back to Adam Smith (1776) to argue that ‘since it is productivity growth that

is the cause of the ‘‘wealth of nations’’ . . . emphasis on profitability is rather curious’

(Nickell 1996, p. 725). Nickell suggested that corporate success should be measured by

total factor productivity rather than by profitability. Nickell et al. (1997) used frontier

production functions (FPF) to search for the decisive factors supporting the

companies’ economic success. Frank Knight (1921) argued that corporate profit is

but a residual between revenues and costs that is exposed to numerous uncertain—or

risky—factors beyond the reach of the firms. In addition, companies may have

incentives not to report profits if the rules of taxation or the greed of stockholders

create unfavourable conditions for managers to achieve high profits. A third factor

relates to the age and a fourth relates to the size of the firm as Aidis and Mickiewicz

(2006, p. 862)—and several other studies—point out.

However, the evidence on the firms’ profit in relation to firm size and age is

inconclusive. While, for instance, Becchetti and Trovaro (2002) have found a negative

relationship between firm size and firm growth in advanced Western economies, and

Faggio and Konings (2003) arrived at similar conclusions for CEE countries, Halpern

and K}orosi (2001), and Fries et al. (2003) have shown a positive relationship between

firm size and corporate performance in different transition countries. Similarly, age of

the firm may have a negative or a positive effect on corporate performance, as Aidis

and Mickiewicz (2006) point out. Nevertheless, empirical evidence suggests that

corporate success is strongly related to the profitability of companies. We can expect

that a firm that is not capable of generating at least normal profits will soon go out of

4Cobb–Douglas production functions are built on the realistic assumption that capital and labour

are imperfect substitutes within the firms’ production technology. As data in Tables A1, A2 and A5

show, Cobb–Douglas production functions gave highly significant results for the relationship between

labour and capital inputs and production level of Hungarian SMEs.

EFFICIENCY OF HUNGARIAN SMEs 1373

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

business. Strangely enough however, just the opposite could be observed in the case of

the Hungarian SMEs: the survival rate of the profitable firms has been lower than in

the case of loss-making companies or for firms that just barely break even. This

observation also suggests that in most cases SMEs have been created by their owners

as ‘money movers’ rather than production entities.

It is not obvious how we can assess and measure the corporate performance of

SMEs. Aghion et al. (1994), Brada and Ma (1997), Johnson et al. (2000), Faggio and

Konings (2003), and Aidis and Mickiewicz (2006) consider the increase in sales and the

increase of employment as the most important success indicators of the SMEs’

performance. My results are in line with these findings, but I shall also stress the

difference between increasing employment and high labour intensity. While increasing

employment may indicate that the firm is capable of expanding, high labour intensity

itself may be a sign of allocative inefficiency.

What factors promote and what factors hinder the SMEs’ development in CEE? As

Lazear (2004) pointed out the entrepreneurs’ skills and accumulated knowledge is

critical to the SMEs’ success. Aidis and Mickiewicz (2006) surveyed Lithuanian SMEs

and found that the entrepreneurs’ human capital—their level of education and

previous work experience—had a significant and highly positive impact on the firms’

performance. Laki (1998, 2001) and Lengyel (2002) arrived at a similar conclusion but

they emphasised the entrepreneurs’ social capital—the network of social connections

they had created—beside education and experience in the case of Hungarian SMEs

and in some other CEE countries. Solid property rights, stable regulation and taxation

rules, the low level of bureaucracy and an easy access to business information are also

important facilitating factors of the SMEs’ success, as Earle et al. (1994) and

Commander et al. (1999) emphasise.

Pissarides et al. (2003) and EBRD (2002) emphasise the decisive role of financial

constraints that SMEs face in these countries. The authors point out that limited

access to bank loans, especially to long-term financing, and prohibitively high interest

rates are serious barriers to the growth of SMEs. Their findings are similar to Levine

(1997) who found that ‘thin’ financial markets and the lack of financing for smaller

businesses are major barriers to development in most developing countries. I have also

found that Hungarian SMEs work within tight financial constraints. Financial

institutions have not been keen on offering loans with reasonable terms to small

businesses. However, this situation started to change recently as competition has

become much stronger in the Hungarian financial market as in some other CEE

markets (Johnson et al. 2002).

Unstable property rights, excessive regulation, bureaucratic delays and corruption

have become the major constraining factors mentioned most frequently by

entrepreneurs in several CEE countries (Batra et al. 2003; Laki & Szalai 2006; Aidis

& Mickiewicz 2006). In addition, SMEs also complain about limited demand,

especially during periods of financial distress and an ensuing stabilisation in CEE

countries. Institutional factors may be critical to the development of the SME sector,

but I have no empirical evidence either to support or refute these claims. My intention

in this article is to show that Hungarian SMEs produce below the level their

endowment of input factors would permit. That is, SMEs produce with a low level of

technical efficiency. They also misallocate resources in that SMEs are usually short of

1374 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

capital, while they use more labour than would be efficient given output levels. This

conclusion calls for caution when it comes to policy advice. Abolishing the barriers to

increasing employment by SMEs may not result in a spectacular growth performance

of this sector. I shall apply the simple framework of profit maximisation and cost

minimisation in the following analysis. The basic model of the firms’ behaviour

assumes that profit maximisation is directly related to the minimisation of costs and to

the technical efficiency of the firms. Based on these duality assumptions, Kumbhakar

and Lovell (2000) show that ‘profit efficiency’ is a simultaneous relationship between

the companies’ production, revenues and costs in a competitive environment

(Kumbhakar & Lovell 2000, p. 162). I shall assume that the production and profit

decisions of a firm are interrelated: whenever firms settle for a certain level of technical

inefficiency they directly affect the profit level they will be capable of attaining.

I shall use the tools of frontier analysis in order to address the issues of production

efficiency and profitability. The econometric foundations of the frontier analysis were

initially defined by Amemiya (1973). The frontier production function (FPF) was first

outlined by Aigner et al. (1977). Brada et al. (1997) used FPFs to analyse the change in

efficiency of Czech companies, while Konings and Repkin (1998) conducted an FPF

analysis to measure the efficiency level of Bulgarian and Romanian firms after the

economic transition in the 1990s. Dynamic FPFs were applied by Halpern and K}orosi

(2001) in the analysis of the technical efficiency of the Hungarian corporate sector for

the period of 1994–1998. Kumbhakar and Lovell (2000) gave an extensive account of

the deterministic and the stochastic frontier analysis. I shall apply their results in the

estimation of the stochastic frontier production function of the Hungarian SMEs.

Several studies used simultaneous estimation methods to analyse the relationship

between efficiency and profitability (see, for instance, Reifschneider & Stevenson 1991;

Basu & Fernald 1997; Kumbhakar & Lovell 2000). I have chosen a similar approach.

That is, I will estimate the optimum production level and the level of inputs—labour

and capital—that minimise costs in a simultaneous model. Finally, I shall use the

results from the frontier estimates to analyse the strength of the relationship between

the companies’ profitability on the one hand and the technical and cost—or

allocative—efficiency level of the firms on the other.

Empirical evidence

According to corporate tax files collected by the Hungarian tax administration, 236,644

companies with double-entry book-keeping operated in the Hungarian economy in

2003.5 Of all firms, 844 companies belonged to the group of large corporations,6 while

the rest belonged to the group of medium-sized enterprises (3,560 firms) or to the group

of small companies (232,240 firms). However, only a few thousand of the small firms

5At the moment of writing this is the last year we have data from. All data on the corporate sector

are from The State of Small and Medium-Sized Enterprises. Annual Report, 2003–2004 (Budapest, The

Hungarian Ministry of the Economy and Transport).6Following one of the classification criteria of the European Union, I label a firm a ‘large company’

if it employs at least 250 people, a ‘medium-sized company’ if it employs between 50 and 249

individuals, and a small company if it has between 0 and 49 employees. (The EU takes into account the

firms’ turnover as well as their capital assets when it ranks different corporations.)

EFFICIENCY OF HUNGARIAN SMEs 1375

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

had any employees or produced positive outputs. When I use the term SME it covers

only those small and medium-sized enterprises that actually showed some sign of actual

existence. In addition to the corporate entities, another 717,000 individual entrepre-

neurs and 215,000 one-person companies (‘sole proprietorships’) were registered in the

Hungarian economy.7 The number of large companies accounted for less than 0.4% of

all corporations, but this company group produced 39.1% of the Hungarian economy’s

total output and 48.6% of its GDP in 2003. Large firms accounted for 64.4% of total

Hungarian exports. The large corporations employed 36.8% of all employees, and their

share from all shareholders’ equity amounted to 51.1%.

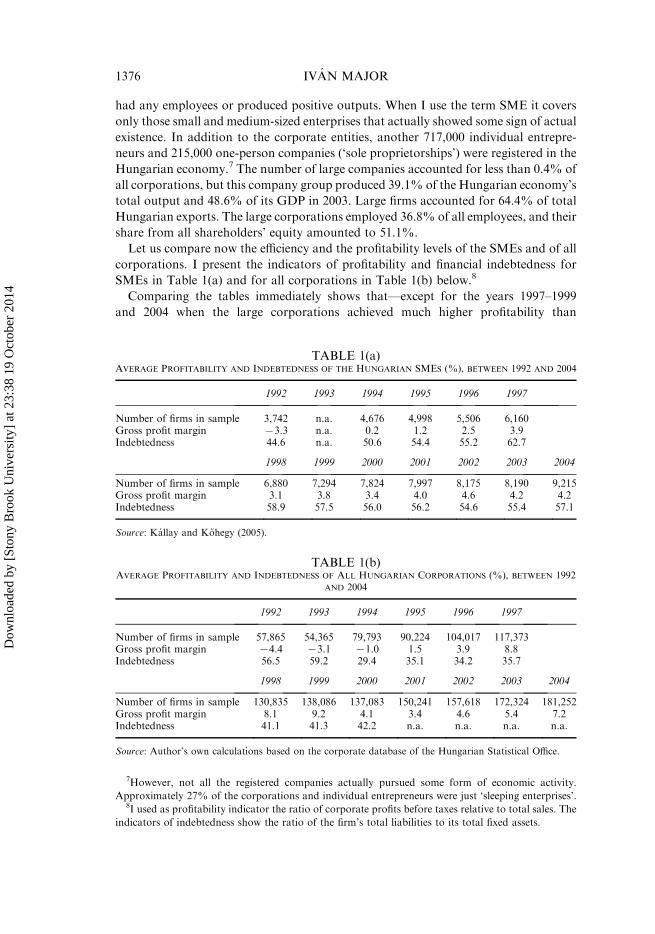

Let us compare now the efficiency and the profitability levels of the SMEs and of all

corporations. I present the indicators of profitability and financial indebtedness for

SMEs in Table 1(a) and for all corporations in Table 1(b) below.8

Comparing the tables immediately shows that—except for the years 1997–1999

and 2004 when the large corporations achieved much higher profitability than

TABLE 1(a)AVERAGE PROFITABILITY AND INDEBTEDNESS OF THE HUNGARIAN SMES (%), BETWEEN 1992 AND 2004

1992 1993 1994 1995 1996 1997

Number of firms in sample 3,742 n.a. 4,676 4,998 5,506 6,160Gross profit margin 73.3 n.a. 0.2 1.2 2.5 3.9Indebtedness 44.6 n.a. 50.6 54.4 55.2 62.7

1998 1999 2000 2001 2002 2003 2004

Number of firms in sample 6,880 7,294 7,824 7,997 8,175 8,190 9,215Gross profit margin 3.1 3.8 3.4 4.0 4.6 4.2 4.2Indebtedness 58.9 57.5 56.0 56.2 54.6 55.4 57.1

Source: Kallay and K}ohegy (2005).

TABLE 1(b)AVERAGE PROFITABILITY AND INDEBTEDNESS OF ALL HUNGARIAN CORPORATIONS (%), BETWEEN 1992

AND 2004

1992 1993 1994 1995 1996 1997

Number of firms in sample 57,865 54,365 79,793 90,224 104,017 117,373Gross profit margin 74.4 73.1 71.0 1.5 3.9 8.8Indebtedness 56.5 59.2 29.4 35.1 34.2 35.7

1998 1999 2000 2001 2002 2003 2004

Number of firms in sample 130,835 138,086 137,083 150,241 157,618 172,324 181,252Gross profit margin 8.1 9.2 4.1 3.4 4.6 5.4 7.2Indebtedness 41.1 41.3 42.2 n.a. n.a. n.a. n.a.

Source: Author’s own calculations based on the corporate database of the Hungarian Statistical Office.

7However, not all the registered companies actually pursued some form of economic activity.

Approximately 27% of the corporations and individual entrepreneurs were just ‘sleeping enterprises’.8I used as profitability indicator the ratio of corporate profits before taxes relative to total sales. The

indicators of indebtedness show the ratio of the firm’s total liabilities to its total fixed assets.

1376 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

SMEs—there has not been any considerable gap between the profitability levels of the

two company groups. The average profit margin of Hungarian SMEs was just slightly

below the profit margin of all the firms. There is, of course, a wide variety among the

firms’ profitability in both groups, but the overall picture is clear: large corporations

were more successful than SMEs during periods of fast growth, but they equally faced

a setback when the Hungarian economy was slowing down. SMEs have been more

indebted than all corporations but the difference between the two groups is not

extremely large. However, if we compare labour productivity of SMEs and that of

large corporations, we can see a substantial difference between the two groups. The

average labour productivity of large corporations was 67% higher than labour

productivity of small and medium-sized firms in 2003, and the gap between the two

groups has been widening during the last decade.

Theory and models

Remaining within the framework of the firm’s basic model, I assume that there are n

firms in the market and each company is a profit maximiser. For simplicity’s sake, let

the production function of each firm be of a Cobb–Douglas type, while the specific

amount of output and inputs (yi,xij) will be different for each company: yi ¼ A �Qmj¼1 x

ajij ;

Pmj¼1 aj � 1. I shall simplify the analysis by limiting the number of input

factors to two: labour—measured by the number of employees—and capital assets.

My main hypothesis is that there are two important sources of under-performance

for the Hungarian SMEs. First, the output of these companies is far away from the

technically efficient level, that is, companies carry out production with a considerable

excess of physical inputs. This fact is usually due to the firms’ limited access to relevant

market information and to other forms of market uncertainties. Secondly, SMEs use

inputs in excess of their cost-efficient level, given their output, technology and factor

prices. I shall call the first factor ‘technical inefficiency’ and the second factor

‘allocative inefficiency’.

The over-utilisation of labour is driven by two factors. Firstly, labour is less

expensive to SMEs than what wage costs would suggest, for a large number of firms

avoid paying the full wage, social benefits included, by forcing their employees to

establish a one person company and then buying the labour services from those one

person firms. As I shall discuss below, many SMEs belong to a network of small or

medium-sized companies. I shall label these firms ‘network companies’. The ‘network

company’ is a member of an organic web of companies, including a few smaller firms

that allocate tasks, resources and costs among the subordinated companies. All the

firms in the network are owned by the same owner or owners. The firm or firms in the

‘core’ group are registered as ‘low income, low cost’ companies and the members of

this group are taxed by the rules of preferential corporate taxation.9 Thus, a network

company has been typically established for the purpose of paying less taxes. In turn, I

shall call a company that does not belong to a group of firms with the same owners a

‘stand-alone firm’. Since official data of the Hungarian Ministry of the Economy and

9This preferential corporate tax is called ‘simplified corporate tax’. The simplified tax was a flat rate

of 15%—it was increased to 25% in 2006—relative to the firm’s total sales.

EFFICIENCY OF HUNGARIAN SMEs 1377

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

Transport for the period of 2001–2004 made it feasible to separate firms that belong to

a network from firms that do not, I shall present the results of the analysis separately

for the so-called ‘network companies’ and for the ‘stand-alone firms’. Secondly,

although most SMEs operate in labour-intensive industries their physical assets are

much more obsolete and less efficient than the physical assets of their larger

counterparts. Consequently, a large share of the excess labour these companies use is a

substitute for the lack of equipment and high-level technology machines.

Paradoxically, small firms hoard more capital than they actually need and use in the

production process. The accumulation of excess capital is due to the financial

constraints most SMEs face. These constraints are much harder for small firms than the

constraints large companies must deal with. SMEs have poorer access to bank loans or

to other forms of external financing than large corporations. Consequently, they can

start capital investments only from their own financial resources. SMEs can meet their

short-term cash flow needs also at a higher cost than large firms. These financial strains

directly result in a hoarding of capital inputs by the small and medium-sized firms.

I shall use a simultaneous model to find the optimal output level and the magnitude

of cost-minimising inputs. To find the technically efficient output level I shall apply a

production frontier:

ln yiðtÞ ¼ a0 þ a1 lnLiðtÞ þ a2 lnKiðtÞ � ui þ vi ð1Þ

where yi(t) is company i’s output level in period t. Li(t) and Ki(t) denote labour and

capital, respectively, and vi and ui are the two-sided random error and the one-sided

systematic error terms, with iid N(0, sv) for random error, and with a truncated

normal distribution of the systematic error term with E(u) �0, and with su standarddeviation for ui.

The firms’ conditional factor demand for labour and for capital is given by:

x1;iðw1;i;w2;i; yiÞ ¼a1a2

� � a1a1þa2� w� a2

a1þa21;i � w

a2a1þa22;i � y

1a1þa2i ; i ¼ 1; . . . ; n

x2;iðw1;i;w2;i; yiÞ ¼a1a2

� �� a2a1þa2� w

a1a1þa21;i � w

� a1a1þa2

2;i � y1

a1þa2i ; i ¼ 1; . . . ; n

ð2Þ

where yi is the maximum amount of output for firm i that can be produced with inputs

(x1,i, x2,i), and (w1,i, w2,i) are the factor prices of labour and capital, respectively.

After taking logs in equation (2) we find:

ln x1;iðw1;i;w2;i; yiÞ ¼ lna1a2

� � a1a1þa2

!� a2a1 þ a2

lnw1;i þa2

a1 þ a2lnw2;i

þ ln1

a1 þ a2yi; i ¼ 1; . . . ; n

ln x2;i w1;i;w2;i; yi� �

¼ lna1a2

� �� a1a1þa2

!þ a1a1 þ a2

lnw1;i �a1

a1 þ a2lnw2;i

þ ln1

a1 þ a2yi; i ¼ 1; . . . ; n

ð3Þ

1378 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

Factor prices would be the same for each firm in a perfectly competitive factor

market. We allow firms to choose different combinations of heterogeneous factor

inputs (labour and capital). Consequently, factor prices become decision variables of

the firms by selecting a specific mix of the heterogeneous input. Then the estimators for

the conditional factor demand functions are given by:

ln x1;i ¼ b0 þ b1 ln w11;i þ b2 ln w

12;i þ b3 ln yi þ x1;i þ e1;i

ln x2;i ¼ g0 þ g1 ln w21;i þ g2 ln w

22;i þ g3 ln yi þ x2;i þ e2;i

ð4Þ

where x1;i ¼ x1;ia1a2

� �� a1a1þa2 , x2;i ¼ x2;i

a1a2

� � a1a1þa2 , w1

1;i ¼�w11;i

�� a1a1þa2 , w1

2;i ¼�w12;i

� a1a1þa2 ,

w21;i ¼

�w21;i

� a2a1þa2 , w2

2;i ¼�w12;i

�� a2a1þa2 , yi is the production frontier of company i, and ei

and xi are the two-sided random error and the one-sided systematic error terms,

respectively, with iid N(0, se) for ei and with a truncated normal distribution for xi.10

Since the ui values measure the companies’ lag behind their production frontier, their

sign will be non-positive, while xi values—that show whether a firm uses too much or

two little of a certain production input—can be either non-negative or non-positive.

The model estimation proceeds in two steps: the production frontier is found first,

then the cost minimising input levels of the production frontier are estimated in the

second phase. The likelihood functions to estimate the systematic error terms were as

follows:

lnLy xij; s2y; l� �

¼ n

2ln

2

p� n ln sy �

Pni¼1

e2i

2s2yþXmi¼1

ln 1� F � eilsy

� �� �� ð5Þ

and

lnLxjj yi; s2xj ; mj� �

¼ n

2ln

2

p� n ln sxj �

Pni¼1

eXj

i

� �22s2xj

þXni¼1

ln 1� Fj �eXj

i mjsxj

! !" #ð6Þ

where

l ¼ susv; ei ¼ ui e

Li ; e

Ki

� �þ vi; s2y ¼ s2u þ s2v ð7Þ

and F is the normal distribution function of ei, and

mj ¼sxjseij

; eXj

i ¼ xijðuiÞ þ eij; s2xj ¼ s2xjj þ s2eij ; j ¼ L;K ð8Þ

where Fj is the normal distribution function of eij.Finally, the firm-specific ui and the xij values can be computed from the frontier

function estimations. Then I use a simple formula to calculate the weighted average

10 Kumbhakar and Lovell (2000, pp. 188–90) outline a nested model approach to estimate technical

and allocative inefficiencies. Their focus is on the misallocation between inputs while I deal with the

over-use of inputs in the current article.

EFFICIENCY OF HUNGARIAN SMEs 1379

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

technical efficiency gap and the weighted average allocative efficiency gaps of the

SMEs, respectively. The average technical efficiency gap and the average allocative

efficiency gaps are as follows:

EðuiÞ ¼ 100 1�Xni¼1

yi � euiyi

!; and EðxijÞ ¼ 100

1�Pmi¼1

xij�exijxijPm

i¼1

xij�exijxij

0BB@

1CCA; j ¼ L;K ð9Þ

Halpern and K}orosi (2001) estimated the dynamic production frontier for all

Hungarian firms with double-entry book-keeping for the period of 1990–1997. They

found that the average technical efficiency gap varied between 12% and 17% in the

entire corporate sector. It was somewhat higher in the group of small and medium-

sized companies (between 13.1% and 18.8%) and somewhat lower in the case of large

corporations (between 11.8% and 17.9%). Technical inefficiencies showed a fairly

stable, somewhat declining trend in the 1990s (Halpern & K}orosi 2001, p. 592). I

obtained substantially larger efficiency gaps in the simultaneous model, as will be

shown below.

Data and estimation methods

I used the panel dataset of all Hungarian SMEs for the period of 1992–2000, and a

subset of network and stand-alone firms for the years 2001–2004. (Individual

proprietorships were not included in the dataset.) The panel dataset consisted of the

variables of the SMEs’ balance sheets and the entries of their corporate tax files.11

I applied the simple definition of SMEs of the European Union: corporations with

less than 250 employees were included in the sample.12 Data for 1993 were missing, as

the Hungarian statistical agencies were unable to compile records that are compatible

with the data in other years. The panel data for the years 1992–2000 comprise all SMEs

that actually operated for at least one year during the period of investigation. Thus, I

had 15,383 observations for each year between 1992 and 2004. However, almost 70% of

these observations had been ‘empty’ in 1992, because most companies did not exist yet.

The share of empty observations was close to 50% in 2000. The number of observations

ranges between 7,900 and 8,500 cases in the period of 2001–2004.

I selected only those SMEs whose total sales, total assets and the number of their

employees were larger than zero.13 When estimating the dynamic production frontier I

11The original dataset was provided by the Hungarian Development Institute of SMEs, an

organisation of the Hungarian Ministry of the Economy and Transport. The primary dataset was

compiled by Kalman K}ohegyi, senior fellow at the Hungarian Development Institute of SMEs. His

contribution is gratefully acknowledged.12I did not apply the refinements of the definition that take into account the firms’ total turnover and

total assets, as well.13Neglecting firms with zero employment or zero capital assets comes at a cost: some of these firms

may belong to so-called ‘network companies’ whose owners deliberately keep the firm on the

borderline between existence and non-existence. As I shall discuss later, networks usually consist of a

company that is used solely to pay the employees of the firm, but I was unable to separate these

network firms and companies in a state of ‘hibernation’ because of the lack of sufficient data. Therefore

I decided to omit all companies with unrealistic indicators from the sample.

1380 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

used the sub-panels of those companies that existed in two consecutive years.

Obviously, the estimation results do not add up to a full time series for the

composition of the sample may have changed period by period.

I estimated the technical efficiency and the allocative efficiency gaps for the entire

group of Hungarian SMEs, and also for three sub-sectors made up as follows:14

agriculture, food- and light industries (AFL), including footwear, clothing, leather ware,

paper and pulp industries, and printing; heavy industry, manufacturing, chemical and

construction industries; and services, including personal services, productive services,

such as telecommunications, transport, energy supply, financial services, and trade.15

The frontier production function I have worked with was as follows:

logValueAddedðtÞ ¼ a0 þ a1 logEmployeesðtÞ þ a2 logTotal assetsðtÞþ a3eLðtÞ þ a4eKðtÞ

ð10Þ

I estimated the following frontier factor demands:

logEmployeesðtÞ

a2ðtÞ

� �¼ b0 þ b1 logValueAddedðtÞ � eðtÞð Þ þ b2 logGrosswageðtÞ

logTotal assetsðtÞ

a3ðtÞ

� �¼ g0 þ g1 logValueAddedðtÞ � eðtÞð Þ þ g2 logDepreciationðtÞ

ð11Þ

As a final step, I used the results from equations (10) and (11) to explain the

profitability gap of the Hungarian SMEs from their maximum attainable profit level. I

defined a separate profit equation for this purpose. We could learn from past experience

and from other studies on Hungarian SMEs (see, for instance, Kallay 2002; K}ohegyi

2001; Laki 1998, 2001; Lengyel 2002; Rona-Tas 1997), that small and medium-sized

businesses are vulnerable to the specific conditions of the financial market, especially to

the availability of bank loans. Therefore, I included the most relevant financial

indicators of the companies’ balance sheets in the profit equation. I also included the

variable of export share (the firm’s annual export relative to its total annual sales), for I

expected that the more an SME is exposed to competition abroad the more efficiently it

will operate. As we shall see in the next section, this has not always been the case. In

addition, I incorporated dummy variables reflecting the ownership structure of

Hungarian SMEs. I included the following ownership dummies in the profit equation:

. OWN1¼ state-owned enterprise;

. OWN2¼domestic private firm;

14The sub-sectors were compiled from the original dataset by using the two-digit industry codes.15The grouping may seem somewhat arbitrary, but my intention was to create groups that are more

or less homogenous as regards their relative labour and capital intensities. An in-depth analysis would

have required separate estimations for each industry but then we would need to work with several

dozen tables that would render the analysis unmanageable. I shall present only the results for the entire

group of SMEs in this article. The main reason why I settled for this solution was that there was not a

tremendous difference among the efficiency gaps of the different groups, and I did not want to

overburden this article with lots of tables.

EFFICIENCY OF HUNGARIAN SMEs 1381

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

. OWN3¼domestic private corporation;

. OWN4¼ foreign-owned firm; and

. OWN5¼municipal company.

The impact of ownership on the firms’ corporate performance needs some

clarification. Several analysts nurtured high expectations about the short run positive

effects of privatisation on corporate performance in CEE. Some of them even argued

that East European privatisations have proven the unquestionable superiority of

private ownership (Pohl et al. 1997). We have overwhelming evidence to suggest that

privatisation reaped results only fairly slowly. In addition, in several cases it was not

private ownership, but foreign ownership that has contributed the most to the

profound changes in corporate performance within the CEE countries.16

The profit equation I used was as follows:

GPROFðtÞ ¼ d0 þ d1euðtÞ þ d2exLðtÞ þ d3exKðtÞ þ d4SHDEBTðtÞ þ d5LDEBTðtÞþ d6MONEYðtÞ þ d7EXPSHðtÞ þ d8OWNðtÞ þ Zt;

ð12Þ

where ‘GPROF’ labels profits before taxes, ‘SHDEBT’ stands for short-term

liabilities, ‘LDEBT’ for long-term liabilities, ‘MONEY’ for the firm’s liquid financial

assets, ‘EXPSH’ for export share, ‘OWN’ for the ownership dummies and Z is the

random error term, all of them in period t. d0– d8 are the estimated parameters of the

OLS model.

Estimation results

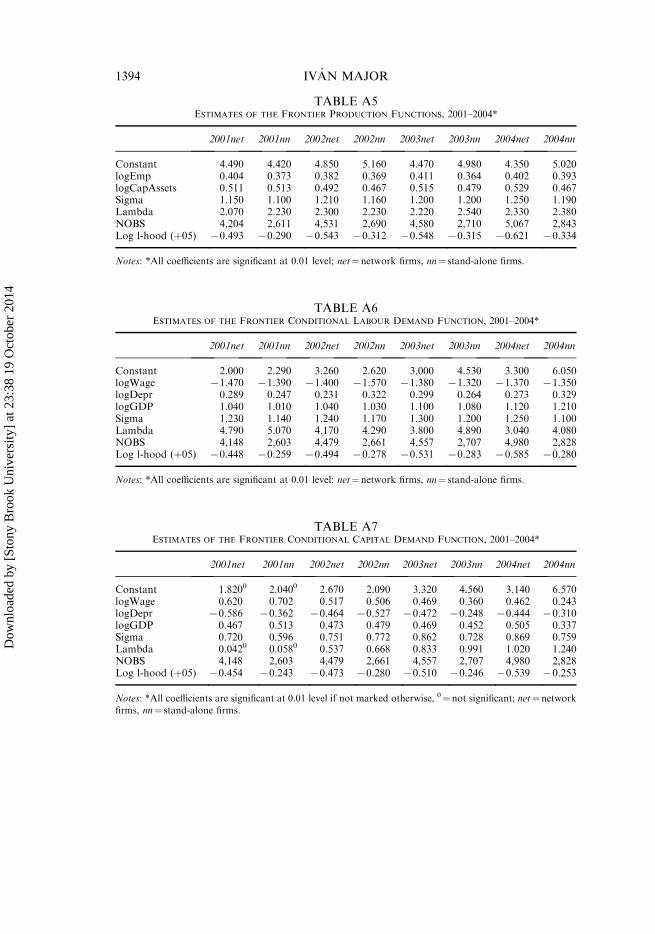

The estimation results of the frontier production functions are presented in the

Appendix. As is shown in the tables, I obtained robust results for the simultaneous

model of the production function and the factor demand functions.

The magnitude of the factors of production had a positive impact on the firms’ output

level but the relative importance of labour and capital changed period by period. Labour

had a somewhat larger impact on the output level than capital in the agro–food–light

(AFL) industry sector between 1992 and 1995. The opposite was true for the period

between 1996 and 1998 when a 1% increase in the firms’ capital stock had twice as large

an effect on output than a 1% increase in employment. Strangely enough, the trend was

reversed between 1999 and 2004 again when the contribution of labour to output was

between 10%and 20% larger than the impact of capital. It was more so in the case of so-

called ‘network firms’ and less so with stand-alone companies.

Capital rather than labour was the decisive factor in the industrial sector between

1994 and 1998. This trend was reversed in 1999, and again between 2000 and 2004.

While a 1% capital increase contributed to output growth between two and three

times more than labour in the first period between 1994 and 1998, the difference

16I have shown this in a previous article (see Major 2002). As is well-known, foreign ownership is not

necessarily private ownership for several Western state-owned companies acquired the assets of firms

in CEE (see also, Aghion et al. 1994; Brada et al. 1997; Commander et al. 1999; Estrin & Hare 1992;

Halpern & K}orosi 2001).

1382 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

between the factors’ impact was reduced to between 2% and 4% between 2001 and

2004. Interestingly enough—but in alignment with the technological progress in

services—capital endowment rather than labour has driven the level of output in the

service sector during the whole period between 1994 and 2004. But the importance of

capital relative to labour declined from the originally very high level—an exponent of

0.067 for capital and 0.004 for labour in 1994, then 0.19 for capital and 0.01 for labour

in 1995—to a small difference of between 3% and 5%. The network firms were the

exceptions from the rule: labour rather than capital had a larger impact on their

output between 2001 and 2004.

The fluctuation in the relative contribution of labour and capital to output seems to

follow the turns in Hungarian economic policy for the years under study. Successive

governments pursued a lax fiscal policy during the initial period of the transition then

between 2000 and 2004 that rendered labour cheap relative to capital. The opposite

was true for the period of fiscal stabilisation between 1995 and 1998 when labour

became relatively more expensive to firms. The results show that SMEs were much

more sensitive to policy changes than large firms and they had a remarkable flexibility

in adjusting to the frequently changing economic and business environment. Johnson

et al. (2000), and Aidis and Mickiewicz (2006) have arrived at a similar conclusion.

Labour has played a more decisive role in shaping the SMEs’ output performance

than historic and international data would suggest. An obvious explanation for this

fact can be that SMEs are usually engaged in production activities that are more

labour intensive and require special human skills. SMEs are frequently organised

around a family tradition in chinaware, personal services or confectionery, that is not

mechanised to the degree that large-scale mass production can be. The higher labour-

intensity of SMEs is also reflected by the fact that the number of SMEs in retail

trading, personal services and handicraft activities has been two or three times higher

than the number of small firms in agriculture, and in the food and light industries, not

to mention the number of small and medium-sized firms in manufacturing, heavy and

chemical industries or in mining. Also, Hungarian SMEs—and SMEs in other CEE

countries—served as buffers for large-scale industries, for a large number of employees

who had lost their jobs in large industries could find work in small businesses.17 A

higher average labour intensity in the SME sector than within the group of large

corporations does not contradict the conclusions of Johnson et al. (2000) and Aidis

and Mickiewicz (2006) that expanding employment may be the most important success

indicator of the small and medium-sized firms.

Higher output always required more employment, and as expected, an increase in

gross wages negatively affected employment with no exception in all three sectors. But

the strength of the effect of gross wage upon output varied by different patterns in the

three sectors. Gross wage had a fairly stable negative coefficient in the agro–food–light

industry (AFL) sector over the whole period of 1992 and 2004. The coefficient grew

substantially—in absolute values—in the industrial sector until 1999, then it slightly

fell back and stabilised at that level. Gross wage has a high and stable impact on

output in services until 2000, then it became smaller and smaller in absolute values.

17This phenomenon is akin to hidden unemployment in the developing world as described by Lewis

(1954) and by Harris and Todaro (1970).

EFFICIENCY OF HUNGARIAN SMEs 1383

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

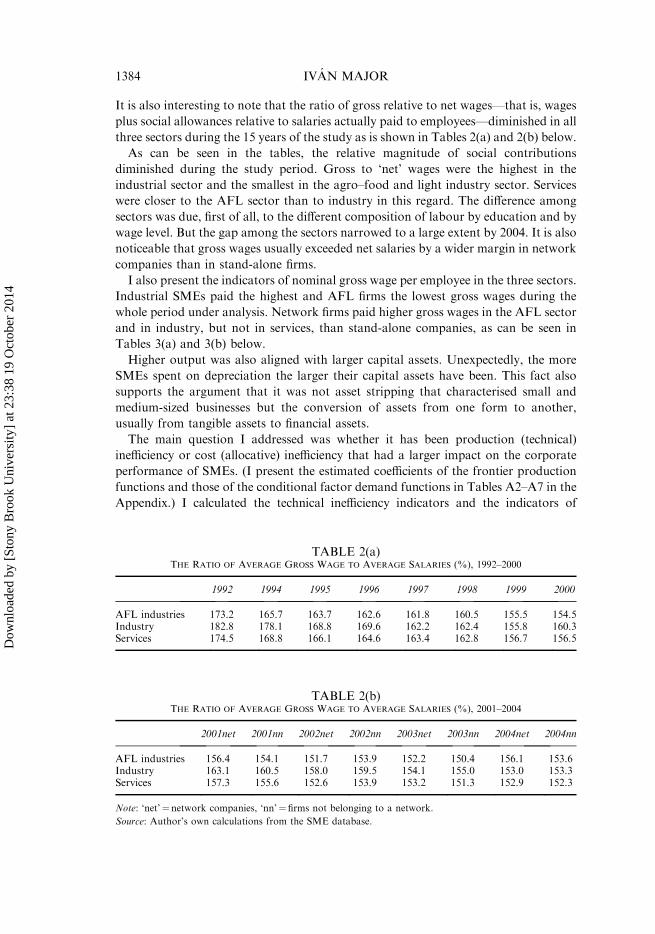

It is also interesting to note that the ratio of gross relative to net wages—that is, wages

plus social allowances relative to salaries actually paid to employees—diminished in all

three sectors during the 15 years of the study as is shown in Tables 2(a) and 2(b) below.

As can be seen in the tables, the relative magnitude of social contributions

diminished during the study period. Gross to ‘net’ wages were the highest in the

industrial sector and the smallest in the agro–food and light industry sector. Services

were closer to the AFL sector than to industry in this regard. The difference among

sectors was due, first of all, to the different composition of labour by education and by

wage level. But the gap among the sectors narrowed to a large extent by 2004. It is also

noticeable that gross wages usually exceeded net salaries by a wider margin in network

companies than in stand-alone firms.

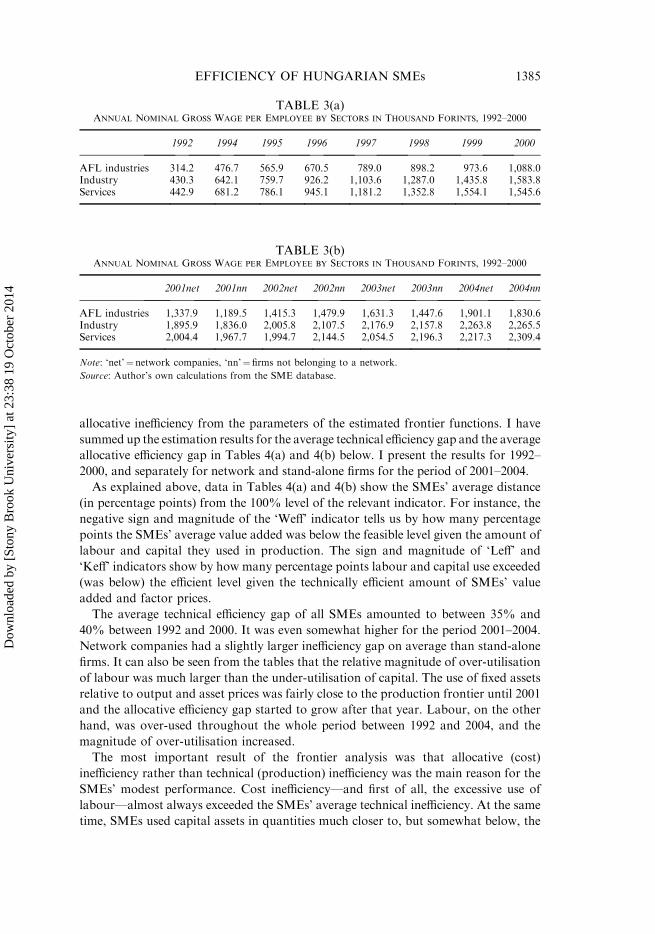

I also present the indicators of nominal gross wage per employee in the three sectors.

Industrial SMEs paid the highest and AFL firms the lowest gross wages during the

whole period under analysis. Network firms paid higher gross wages in the AFL sector

and in industry, but not in services, than stand-alone companies, as can be seen in

Tables 3(a) and 3(b) below.

Higher output was also aligned with larger capital assets. Unexpectedly, the more

SMEs spent on depreciation the larger their capital assets have been. This fact also

supports the argument that it was not asset stripping that characterised small and

medium-sized businesses but the conversion of assets from one form to another,

usually from tangible assets to financial assets.

The main question I addressed was whether it has been production (technical)

inefficiency or cost (allocative) inefficiency that had a larger impact on the corporate

performance of SMEs. (I present the estimated coefficients of the frontier production

functions and those of the conditional factor demand functions in Tables A2–A7 in the

Appendix.) I calculated the technical inefficiency indicators and the indicators of

TABLE 2(a)THE RATIO OF AVERAGE GROSS WAGE TO AVERAGE SALARIES (%), 1992–2000

1992 1994 1995 1996 1997 1998 1999 2000

AFL industries 173.2 165.7 163.7 162.6 161.8 160.5 155.5 154.5Industry 182.8 178.1 168.8 169.6 162.2 162.4 155.8 160.3Services 174.5 168.8 166.1 164.6 163.4 162.8 156.7 156.5

TABLE 2(b)THE RATIO OF AVERAGE GROSS WAGE TO AVERAGE SALARIES (%), 2001–2004

2001net 2001nn 2002net 2002nn 2003net 2003nn 2004net 2004nn

AFL industries 156.4 154.1 151.7 153.9 152.2 150.4 156.1 153.6Industry 163.1 160.5 158.0 159.5 154.1 155.0 153.0 153.3Services 157.3 155.6 152.6 153.9 153.2 151.3 152.9 152.3

Note: ‘net’¼ network companies, ‘nn’¼firms not belonging to a network.

Source: Author’s own calculations from the SME database.

1384 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

allocative inefficiency from the parameters of the estimated frontier functions. I have

summed up the estimation results for the average technical efficiency gap and the average

allocative efficiency gap in Tables 4(a) and 4(b) below. I present the results for 1992–

2000, and separately for network and stand-alone firms for the period of 2001–2004.

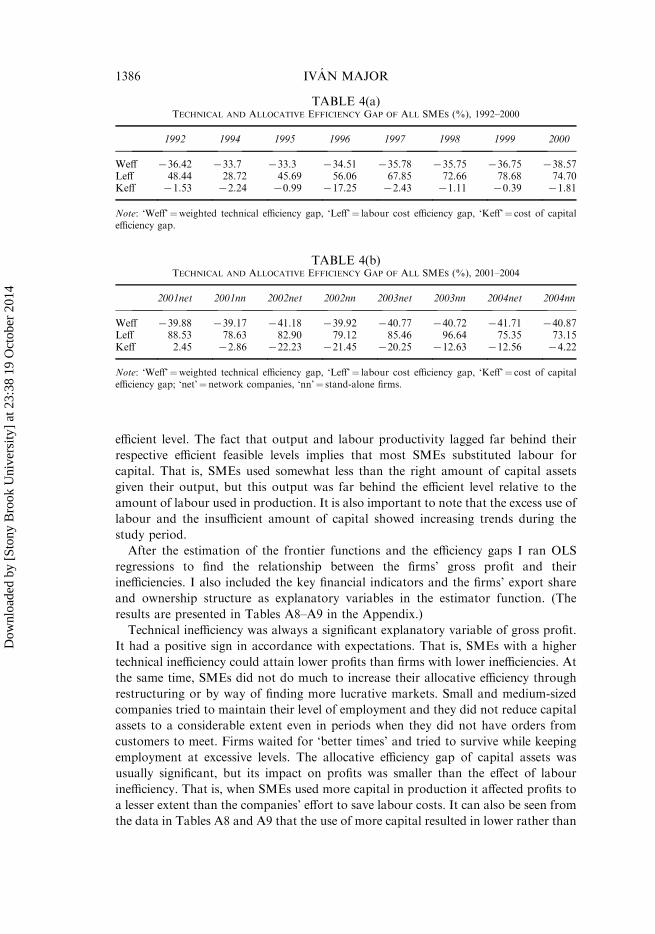

As explained above, data in Tables 4(a) and 4(b) show the SMEs’ average distance

(in percentage points) from the 100% level of the relevant indicator. For instance, the

negative sign and magnitude of the ‘Weff’ indicator tells us by how many percentage

points the SMEs’ average value added was below the feasible level given the amount of

labour and capital they used in production. The sign and magnitude of ‘Leff’ and

‘Keff’ indicators show by how many percentage points labour and capital use exceeded

(was below) the efficient level given the technically efficient amount of SMEs’ value

added and factor prices.

The average technical efficiency gap of all SMEs amounted to between 35% and

40% between 1992 and 2000. It was even somewhat higher for the period 2001–2004.

Network companies had a slightly larger inefficiency gap on average than stand-alone

firms. It can also be seen from the tables that the relative magnitude of over-utilisation

of labour was much larger than the under-utilisation of capital. The use of fixed assets

relative to output and asset prices was fairly close to the production frontier until 2001

and the allocative efficiency gap started to grow after that year. Labour, on the other

hand, was over-used throughout the whole period between 1992 and 2004, and the

magnitude of over-utilisation increased.

The most important result of the frontier analysis was that allocative (cost)

inefficiency rather than technical (production) inefficiency was the main reason for the

SMEs’ modest performance. Cost inefficiency—and first of all, the excessive use of

labour—almost always exceeded the SMEs’ average technical inefficiency. At the same

time, SMEs used capital assets in quantities much closer to, but somewhat below, the

TABLE 3(a)ANNUAL NOMINAL GROSS WAGE PER EMPLOYEE BY SECTORS IN THOUSAND FORINTS, 1992–2000

1992 1994 1995 1996 1997 1998 1999 2000

AFL industries 314.2 476.7 565.9 670.5 789.0 898.2 973.6 1,088.0Industry 430.3 642.1 759.7 926.2 1,103.6 1,287.0 1,435.8 1,583.8Services 442.9 681.2 786.1 945.1 1,181.2 1,352.8 1,554.1 1,545.6

TABLE 3(b)ANNUAL NOMINAL GROSS WAGE PER EMPLOYEE BY SECTORS IN THOUSAND FORINTS, 1992–2000

2001net 2001nn 2002net 2002nn 2003net 2003nn 2004net 2004nn

AFL industries 1,337.9 1,189.5 1,415.3 1,479.9 1,631.3 1,447.6 1,901.1 1,830.6Industry 1,895.9 1,836.0 2,005.8 2,107.5 2,176.9 2,157.8 2,263.8 2,265.5Services 2,004.4 1,967.7 1,994.7 2,144.5 2,054.5 2,196.3 2,217.3 2,309.4

Note: ‘net’¼ network companies, ‘nn’¼firms not belonging to a network.

Source: Author’s own calculations from the SME database.

EFFICIENCY OF HUNGARIAN SMEs 1385

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

efficient level. The fact that output and labour productivity lagged far behind their

respective efficient feasible levels implies that most SMEs substituted labour for

capital. That is, SMEs used somewhat less than the right amount of capital assets

given their output, but this output was far behind the efficient level relative to the

amount of labour used in production. It is also important to note that the excess use of

labour and the insufficient amount of capital showed increasing trends during the

study period.

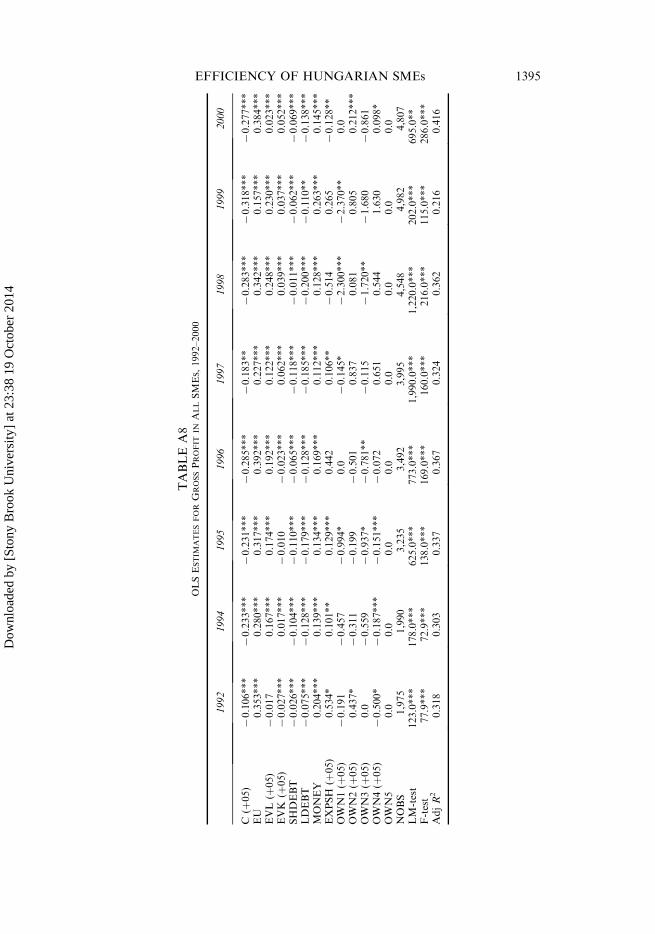

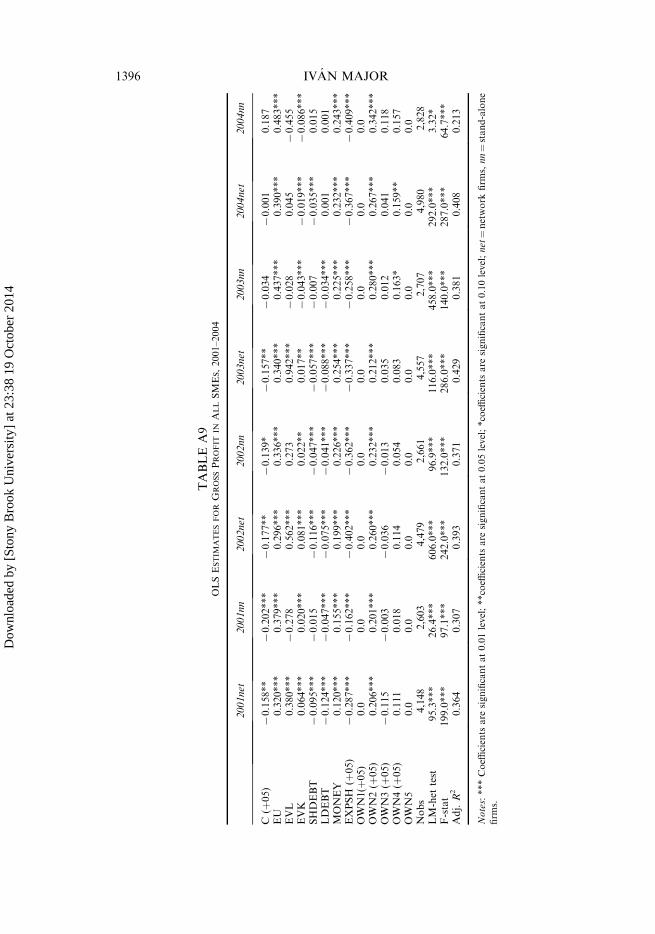

After the estimation of the frontier functions and the efficiency gaps I ran OLS

regressions to find the relationship between the firms’ gross profit and their

inefficiencies. I also included the key financial indicators and the firms’ export share

and ownership structure as explanatory variables in the estimator function. (The

results are presented in Tables A8–A9 in the Appendix.)

Technical inefficiency was always a significant explanatory variable of gross profit.

It had a positive sign in accordance with expectations. That is, SMEs with a higher

technical inefficiency could attain lower profits than firms with lower inefficiencies. At

the same time, SMEs did not do much to increase their allocative efficiency through

restructuring or by way of finding more lucrative markets. Small and medium-sized

companies tried to maintain their level of employment and they did not reduce capital

assets to a considerable extent even in periods when they did not have orders from

customers to meet. Firms waited for ‘better times’ and tried to survive while keeping

employment at excessive levels. The allocative efficiency gap of capital assets was

usually significant, but its impact on profits was smaller than the effect of labour

inefficiency. That is, when SMEs used more capital in production it affected profits to

a lesser extent than the companies’ effort to save labour costs. It can also be seen from

the data in Tables A8 and A9 that the use of more capital resulted in lower rather than

TABLE 4(a)TECHNICAL AND ALLOCATIVE EFFICIENCY GAP OF ALL SMES (%), 1992–2000

1992 1994 1995 1996 1997 1998 1999 2000

Weff 736.42 733.7 733.3 734.51 735.78 735.75 736.75 738.57Leff 48.44 28.72 45.69 56.06 67.85 72.66 78.68 74.70Keff 71.53 72.24 70.99 717.25 72.43 71.11 70.39 71.81

Note: ‘Weff’¼weighted technical efficiency gap, ‘Leff’¼ labour cost efficiency gap, ‘Keff’¼ cost of capitalefficiency gap.

TABLE 4(b)TECHNICAL AND ALLOCATIVE EFFICIENCY GAP OF ALL SMES (%), 2001–2004

2001net 2001nn 2002net 2002nn 2003net 2003nn 2004net 2004nn

Weff 739.88 739.17 741.18 739.92 740.77 740.72 741.71 740.87Leff 88.53 78.63 82.90 79.12 85.46 96.64 75.35 73.15Keff 2.45 72.86 722.23 721.45 720.25 712.63 712.56 74.22

Note: ‘Weff’¼weighted technical efficiency gap, ‘Leff’¼ labour cost efficiency gap, ‘Keff’¼ cost of capitalefficiency gap; ‘net’¼network companies, ‘nn’¼ stand-alone firms.

1386 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

larger profits in some years. There may be several reasons behind this result. If start-up

companies or firms that decided to extensively expand production invested heavily,

lower profits would have been an obvious consequence of the large initial efforts by the

firms and the strategy may have been admissible. If, on the other hand, well-

established companies attained lower profits by expanding their capital base this may

have indicated a deteriorating allocative efficiency at the firms.

The excessive use of labour had a significant and negative impact on profits in most

years. The only exceptions were the years of 2003 and 2004 when drastic changes in the

government’s wage and taxation policies rather than the SMEs’ efforts to increase cost

efficiency led to higher profits in the Hungarian corporate sector. The effect of too

much labour was much stronger on profits than the impact of capital shortages in

most years, as can be seen in Tables A7 and A8 in the Appendix.

Had the problem only been one of technical (production) inefficiency, SMEs could

have improved on their profitability by expanding production. But the excess use of

labour and the insufficient amount of capital rendered efficient expansion unfeasible

for Hungarian SMEs (and for SMEs in the CEE region in general). Since average

allocative inefficiency of the SMEs was larger than technical inefficiency in relative

terms, firms could improve profitability by producing less than feasible, for this

‘rolling back policy’ lowered the magnitude of their losses. The lower than technically

feasible—or optimal—output level served the purpose of keeping the firms afloat by

way of reducing some of the production costs.18

It is worth noting that so-called ‘network firms’ usually had larger coefficients of

technical inefficiency than the stand-alone companies. That is, the same level of

technical inefficiency resulted in lower gross profits in network firms than in stand-

alone companies. But network SMEs have usually been less inefficient than single

firms as we saw before. The allocative inefficiency of capital use affected gross profit

more severely in network companies than in single firms in the AFL sector but the

opposite was true for the industrial sector and for services in the 2000s. That is,

network companies could reduce the adverse effects of capital inefficiencies to a larger

extent than stand-alone firms in the industrial sector and in services. We may conclude

from these results that being a member company of a network has not always been a

blessing, especially in the agricultural and food sector, but it helped firms in the

industrial and service sectors.

The profit of Hungarian SMEs has been very sensitive to short-term and to long-

term financial liabilities. Profits declined when the level of their short-term

indebtedness increased. This was a permanent phenomenon during the 15 years

analysed here, showing that Hungarian SMEs were not treated favourably by the

financial markets. Roman (1991), EBRD (2002) and Pissarides et al. (2003) have also

found that ‘thin’ financial markets and especially the lack of financing for domestic

SMEs were serious barriers to the development of this sector in several CEE countries.

One might argue that short and long-term indebtedness have been endogenous to

profitability, but this has not been the case. A large number of SMEs became indebted

not because they were unable to generate normal profits for their industry, but they

18Koll}o (2001) obtained similar results based on his case study analysis of Hungarian small and

medium-sized companies in the textile industry.

EFFICIENCY OF HUNGARIAN SMEs 1387

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

turned out to be loss-makers because the cost of the loan was exorbitant. Bank loans

have been extremely expensive to SMEs not because these investments turned out to

be more risky to banks, but because banks could comfortably earn much larger

margins on the small number of huge loans that they extended to large corporations.

Banks were also reluctant to offer long-term loans to SMEs. The lack of long-term

investment loans with reasonable conditions pushed these companies into the vicious

circle of short-term liquidity problems. Those SMEs that relied on external financing

could not produce enough net income to repay their dues in most of the cases. But the

effect of short-term and long-term liabilities was not equally strong across sectors and

between periods. Short-term debt had a more significant impact before than after the

year 2000, especially in the initial years of the 1990s. Long-term debt had also been

more significant during the 1990s than in the 2000s, but it was more important in the

second half of the 1990s than in the first years of the decade.

Indebtedness has been significant in most, but not in all, periods after the year 2000.

The main reason for this change was that the loans market had become very

competitive in the late 1990s and banks turned toward small and medium-sized

businesses after the turn of the century. Gross profit of AFL firms and service

companies was more sensitive to indebtedness than the profit of industrial firms. The

difference among sectors is related to the different average size of companies in the

three groups. Industrial SMEs belonged more to the group of medium-sized rather

than to the group of small companies, while SMEs in the AFL industries and in

services were usually small rather than medium-size.

While indebtedness negatively affected profitability, financial assets have always had

a significant and positive impact on the firms’ gross profits. This relationship indicated

that SMEs frequently operated as ‘teller machines’ rather than production units.

Groups of SMEs with the same owners frequently operated as a complex network of

moving money from one company to another.19 Consequently, it is hard to tell

whether an SME went bankrupt because of its poor performance, or because its assets

had been converted into financial assets which were then reallocated to another firm

that belonged to the same group of owners. Policy makers have often accused

Hungarian companies of asset stripping but my results are inconsistent with these

claims. Hungarian SMEs may have converted tangible assets into financial assets

because of poor investment prospects and unstable market expectations (K}ohegyi

2001; Kallay 2002). Nevertheless these companies reinvested their revenues from sales

into financial assets rather than using those assets for personal consumption.

The SMEs’ export share has been a significant explanatory variable of profitability

more often after than before 2000. This was equally true for network and for stand-

alone firms between 2001 and 2004. Obviously, export shares have not played a

significant role in most retail services while the export share of industrial firms and

AFL companies was significant in several years. But it was completely unexpected that

the export share of SMEs usually had a negative rather than a positive sign when it

19I have found evidence of the existence of such ‘money networks’ from interviews with Hungarian

company managers. The estimation results for 2001–2004 also support this assumption, for I have

found a large difference between the production and profitability of so-called ‘network firms’ and

‘stand-alone’ firms, as discussed above.

1388 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

was a significant variable of the profit equation. That is, small and medium-sized firms

that exported could achieve lower profits than SMEs that produced for the domestic

market. This fact clearly signals the difficulties SMEs face when they try to enter

international competition. These companies usually lack the necessary knowledge of

the markets and they do not possess the trading and transportation networks that are

so vital to success in foreign trade, as eloquently described by Lewis (1954) for

developing countries. However, this finding does not have general validity for all CEE

countries. Aidis and Mickiewicz (2006) have found a positive relationship between

exports and firm growth in Bulgaria and Russia, and Batra et al. (2003) produced

similar results for a larger set of countries.

Another interesting result of the profit estimations was that ownership did not usually

play a significant role in the profitability of Hungarian SMEs. When it did have a

significant impact, it mostly occurred in foreign-owned firms, and only rarely in

domestic companies. I had already found this relationship in an earlier study when I

estimated the technical efficiency gap separately for domestic and for foreign-owned

SMEs: I found substantial differences between the two types of companies. Foreign

firms had smaller average efficiency gaps relative to the best practice foreign companies

than their domestic counterparts between 1992 and 2000 (Major 2002). This result

shows that it was foreign rather than private ownership that improved the companies’

performance. Private ownership could not guarantee success alone. The critical issue

was whether formerly state-owned companies had been acquired by foreign or by

domestic investors. Ownership had a significant impact more frequently at industrial

than at AFL firms or at service companies. When ownership was a significant variable it

usually had a positive rather than a negative effect on the SMEs’ profitability.

Conclusions

Can small and medium-sized companies that are usually owned and managed by

domestic owners, become the engine of economic growth in Hungary or in other

transition economies? I addressed the former question by analysing corporate level

data of Hungarian SMEs during the period of 1992–2004. The answer, in short, is a

sad ‘no, they cannot’. I have shown that most SMEs produce far below the feasible

level of output. This inefficiency is mostly due to the excess use of labour in SMEs,

while their capital endowment is extremely low relative to production levels.

I also had the objective to find a sensible method of measuring the magnitude of

inefficiency in the SME sector. The definition and measurement of corporate success

has been a debated issue in microeconomic analysis. My purpose in this article was to

outline a theory and models that define the relationship among the Hungarian SMEs’

technical efficiency, allocative efficiency and profitability. The model that could be

derived from the theory of ‘profit maximisation via technical inefficiency’ helps us

explain the moderate success of small and medium-sized companies in a transition

economy, such as Hungary.

I used stochastic frontier analysis in the estimation of the firms’ technical and

allocative efficiencies, and I constructed a simultaneous model for the estimation of the

frontier production function and the frontier factor demand functions. The models

yielded robust estimation results. The production of Hungarian SMEs—measured by

EFFICIENCY OF HUNGARIAN SMEs 1389

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

the annual gross value added of the companies—increased along with an expanding

use of labour and capital and with larger export shares. The profits of Hungarian

SMEs were strongly and positively influenced by the amount of financial assets.

Financial liabilities were significant explanatory variables of the profit function, and

profits usually declined when liabilities increased. Consequently, Hungarian SMEs

were very sensitive to external financial conditions, although they tried to avoid

dependence on such financial resources.

The estimation results showed that ownership did not play a significant role in the

companies’ profitability. However, I found—as I had also shown in an earlier study

(Major 2002)—that there has been a considerable difference between domestic and

foreign-owned SMEs in technical efficiency and in profitability, with the foreign firms,

on average, being closer to their frontier than their domestic counterparts. Foreign-

owned companies usually adjusted better to the hectically changing market conditions

than domestic companies.

The most important result of the analysis was that the Hungarian SMEs’ technical

efficiency, allocative efficiency and profitability are intimately interrelated. I showed

that profit maximisation was compatible with a deliberate reduction of the firm’s

technical efficiency. Firms could achieve a higher level of profits by reducing the level

of output, for it dampened the impact of allocative inefficiency on gross profits. Larger

technical inefficiency was usually aligned with lower gross profits at ‘network’ SMEs

than at ‘stand-alone’ companies, indicating that inefficiency hit larger network

companies more than it affected single firms.

I have also shown that SMEs operated with diminishing returns and they have

chosen—or they were forced to choose—a ‘perverse’ way of adjustment to harsh

market conditions in order to remain afloat by curbing production. This defensive

behaviour can be reasonable under unfavourable market prospects or in periods when

firms lose their former markets and search for new market niches. At this stage a large

number, although not all, of Hungarian SMEs were in a delicate position as they lost

markets to large, mostly foreign-owned corporations. Consequently, mere survival

could have already been considered as an economic success, therefore expansion with

growing profits remained only most SMEs’ dream for the distant future.

Institute of Economics, The Hungarian Academy of Sciences, Budapest

References

Aghion, P., Blanchard, O.J. & Carlin, W. (1994) The Economics of Enterprise Restructuring in Centraland Eastern Europe, Discussion Paper No. 1058 (London, CEPR).

Aidis, R. & Mickiewicz, T. (2006) ‘Entrepreneurs, Expectations and Business Expansion: Lessons fromLithuania’, Europe-Asia Studies, 58, 6, September, pp. 855–80.

Aigner, D., Lovell, C.A.K. & Schmidt, P. (1977) ‘Formulation and Estimation of Stochastic FrontierProduction Function Models’, Journal of Econometrics, 6, 1, pp. 21–37.

Amemiya, T. (1973) ‘Regression Analysis When the Dependent Variable is Truncated Normal’,Econometrica, 41, 6, pp. 997–1016.

Basu, S. & Fernald, J.G. (1997) ‘Returns to Scale in US Production: Estimates and Implications’,Journal of Political Economy, 105, 2, pp. 249–83.

Batra, G., Kaufmann, D. & Stone, A. (2003) Investment Climate around the World: Voices of the Firmsfrom the World Business Environment Survey (Washington, DC, The World Bank).

1390 IVAN MAJOR

Dow

nloa

ded

by [

Ston

y B

rook

Uni

vers

ity]

at 2

3:38

19

Oct

ober

201

4

Becchetti, L. & Trovaro, G. (2002) ‘The Determinants of Growth for Small and Medium SizedFirms. The Role and Availability of External Finance’, Small Business Economics, 19, 4, pp. 291–306.

Brada, J., King, A. & Ma, C. (1997) ‘Industrial Economics of the Transition: Determinants ofEnterprise Efficiency in Czechoslovakia and Hungary’, Oxford Economic Papers, 49, 1, pp. 104–27.

Commander, S.J., Dutz, M. & Stern, N. (1999) Restructuring in Transition Economies: Ownership,Competition and Regulation, World Bank ABCDE Conference Paper (Washington, DC, TheWorld Bank).

Earle, J.S., Frydman, R., Rapaczynski, A. & Turkewitz, J. (1994) Small Privatization: TheTransformation of Retail Trade and Consumer Services in the Czech Republic, Hungary andPoland (Budapest, London & New York, Central European University Press).

Estrin, S. & Hare, P. (1992) Firms in Transition: Modelling Enterprise Adjustment, Centre for EconomicPerformance (CEP), LSE Discussion Paper No. 89 (London, CEP).

European Bank for Reconstruction and Development (EBRD) (2002) Transition Report (London,EBRD).

Faggio, G. & Konings, J. (2003) ‘Job Creation, Job Destruction and Employment Growth inTransition Countries in the 90s’, Economic Systems, 27, 2, pp. 129–54.

Fries, S., Lysenko, T. & Polanec, S. (2003) The 2002 Business Environment and Enterprise PerformanceSurvey: Results from a Survey of 6,100 Firms, EBRD Working Paper No. 84 (London, EuropeanBank for Reconstruction and Development).

Gomulka, S. (1994) ‘Obstacles to Recovery in Transition Economies’, in Aghion, P. & Stern, N. (eds)(1994) Obstacles to Enterprise Restructuring in Transition, Working Paper No. 16 (London,European Bank for Reconstruction and Development).

Halpern, L. & K}orosi, G. (2001) ‘Efficiency and Market Share in the Hungarian Corporate Sector’,The Economics of Transition, 9, 2, pp. 559–92.

Harris, J.R. & Todaro, M.P. (1970) ‘Migration, Unemployment and Development: A Two-SectorAnalysis’, The American Economic Review, 60, 1, March, pp. 126–42.

Johnson, S., McMillan, J. & Woodruff, C. (2000) ‘Entrepreneurs and the Ordering of InstitutionalReform: Poland, Slovakia, Romania, Russia and Ukraine Compared’, Economics of Transition, 8,1, pp. 1–36.

Johnson, S., McMillan, J. & Woodruff, C. (2002) ‘Property Rights and Finance’, American EconomicReview, 92, 5, pp. 1335–56.

Kallay, L. (2002) ‘Paradigmavaltas a kisvallalkozas-fejlesztesben’ [‘A New Paradigm of theDevelopment Policy of Hungarian SMEs’], Kozgazdasagi Szemle, XLIX, 7–8, pp. 557–73.

Kallay, L. & K}ohegyi, K. (eds) (2005) A kis-es kozepvallalkozasok helyzete. Eves jelentes, 2003–2004[The State of the Small- and Medium-Sized Enterprises. Annual Report, 2003–2004] (Budapest,Ministry of the Economy and Transport).

Knight, F.H. (1921) Risk, Uncertainty and Profit (Reference is to the 1985 edition, Chicago, Universityof Chicago Press).

K}ohegyi, K. (2001) ‘Novekv}o es zsugorodo vallalkozasok’ [‘Growing and Shrinking Companies inHungary’], Kozgazdasagi Szemle, XLVIII, 4, pp. 320–37.

Koll}o, J. (2001) Meddig tart a rendszervaltas? [How Long Would the Economic Transformation Last?],Budapest Working Papers No. 11 (Budapest, Institute of Economics of the Hungarian Academyof Sciences).

Konings, J. & Repkin, A. (1998) How Efficient Are Firms in Transition Countries? Firm-Level Evidencefrom Bulgaria and Romania, CEPR Discussion Paper No. 1839 (London, CEPR).

Kornai, J. (1993) ‘Transzformacios visszaeses’ [‘Transformation Recession’], Kozgazdasagi Szemle,XL, 7–8, pp. 569–99. [In English: Kornai, J. (1995) ‘Transformational Recession: The Example ofHungary’, in Saunders, C. (ed.) (1995) Eastern Europe in Crisis and the Way Out (Houndmills,Macmillan)].

Kornai, J. (2007) Szocializmus, kapitalizmus, demokracia es rendszervaltas [Socialism, Capitalism,Democracy and System Change] (Budapest, Akademiai Kiado).

Kumbhakar, S. & Lovell, K. (2000) Stochastic Frontier Analysis (Cambridge, Cambridge UniversityPress).

Laki, M. (1998) Kisvallalkozas a szocializmus utan [Small Ventures After Socialism] (Budapest,Kozgazdasagi Szemle Foundation).