Embed Size (px)

Citation preview

12/17/13

1

Technical Convening on Agricultural Inputs (Seed &

Fert.) Policy in Africa

Mr. Argent Chuula, CEO ACTESA

! Burundi Comoros D.R. Congo Djibouti Egypt Eritrea Ethiopia Kenya Libya Seychelles Madagascar Malawi Mauritius Rwanda Sudan South Sudan Swaziland Uganda Zambia Zimbabwe Mozambique Botswana Tanzania

All COMESA Member States/ Plus Mozambique, Botswana, Tanzania, e.t.c

..00 CCOOMMEESSAA // AACCTTEESSAA’’ss RReeggiioonn

.

AALLLLIIAANNCCEE CCOOMMMMOODDIITTYY TTRRAADDEE IINN

EEAASSTTEERRNN AANNDD SSOOUUTTHHRREENN AAFFTTEERRIICCAA –– AACCTTEESSAA

!1. A Specialised Agency of COMESA.

2. Stemmed from the need of having an implementing Agency for CAADP pillars 2 on market access and 3 on Food Security

3. Established by COMESA Heads of States

on 9th June 2009 to implement agricultural activities on staple foods with a focus on small scale farmers in the ESA region.

12/17/13

2

!THE$PROBLEM!

AACCTTEESSAA SSTTRRAATTEEGGIICC RROOLLEE 1. Channels policy issues between the public and

private sector and other stakeholders

2. An information hub for use by producers, traders, UN agencies and other agricultural organisations.

3. Facilitates and co-ordinates activities of implementing partners at regional and national level

4. Co-ordinates the mobilization of resources for implementing partners on agricultural activities in the region

ACTESA$

COMESA$POLICY$ORGANS$

PRIVATE$SECTOR$

FARMERS$ORGANISATIONS$

AACCTTEESSAA SSTTRRAATTEEGGIICC RROOLLEE

MEMBER$STATES$

DEVELOPMENT$PARTNERS$

12/17/13

3

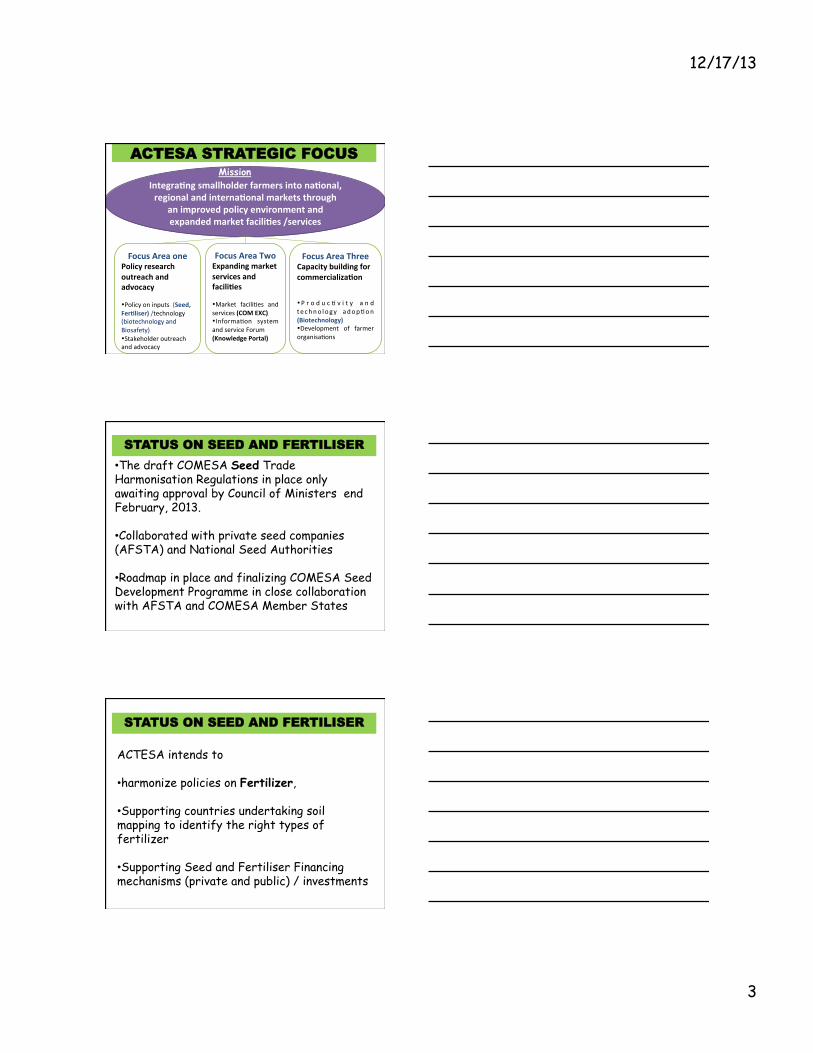

AACCTTEESSAA SSTTRRAATTEEGGIICC FFOOCCUUSS

Integra;ng$smallholder$farmers$into$na;onal,$

regional$and$interna;onal$markets$through$

an$improved$policy$environment$and$

expanded$market$facili;es$/services$

Focus$Area$one$Policy$research$

outreach$and$advocacy$Prioritysues:$ Policy!on!inputs!!(Seed,$Fer;liser)!/technology!(biotechnology!and!Biosafety)! Stakeholder!outreach!

and!advocacy!$$

Focus$Area$Two$Expanding$market$

services$and$facili;es$$$Priority$Issues:$ Market! facili=es! and!

services!(COM$EXC)$ Informa=on! system!

and!service!Forum!(Knowledge$Portal)$

$

Focus$Area$Three$Capacity$building$for$

commercializa;on$Prioty$Issues:$

P r o d u c = v i t y ! a n d!t e c h n o l o g y! a d o p = o n!(Biotechnology)$ Development! of! farmer!

organisa=ons!$

Mission

SSTTAATTUUSS OONN SSEEEEDD AANNDD FFEERRTTIILLIISSEERR

The draft COMESA Seed Trade Harmonisation Regulations in place only awaiting approval by Council of Ministers end February, 2013. Collaborated with private seed companies

(AFSTA) and National Seed Authorities Roadmap in place and finalizing COMESA Seed

Development Programme in close collaboration with AFSTA and COMESA Member States

SSTTAATTUUSS OONN SSEEEEDD AANNDD FFEERRTTIILLIISSEERR ACTESA intends to

harmonize policies on Fertilizer,

Supporting countries undertaking soil

mapping to identify the right types of fertilizer Supporting Seed and Fertiliser Financing

mechanisms (private and public) / investments

12/17/13

1

Current'situa+on'of'seed'harmoniza+on'and'implementa+on'in'Africa!

Jus+n'Rakotoarisaona'Secretary'General,'The'African'Seed'Trade'Associa+on'(AFSTA)'

Technical'convening'mee+ng'Addis'–'Ababa'

December'5,'2013'

OUTLINES!

! Main!objec3ves!of!the!harmoniza3on!

Key!areas!for!harmoniza3on!

! Situa3on!of!harmoniza3on!in!the!Regional!

Economic!Communi3es!(RECs)!

! Membership!to!RECs!in!Eastern!and!Southern!

Africa!(ASARECAHEAC/COMESA/SADC)!

! Implementa3on!

! Conclusion!

MAIN!OBJECTIVES!OF!THE!HARMONIZATION!!

Free! movement! of! seed! with! a! view! to!

promo3ng! crossHborder! seed! trade! for!beRer!

seed!supply!for!farmers;!

Mo3va3on! of! private! sector! to! invest! in! the!

seed!sector!because!of!increased!seed!market!

size!–!country!to!regional!based!seed!market.!

12/17/13

2

BACKGROUND!INFORMATION!

RECs:!COMESA,!SADC,!EAC!and!ECOWAS!

(ECCAS!has!not!ini3ated!harmoniza3on):!

harmoniza3on!all!at!implementa3on!stage!

Areas!for!harmoniza3on!

– Phytosanitary!Measures!and!seed!Import/Export!

Procedures!and!Documenta3on;!

– Standards!for!Seed!Cer3fica3on!– Variety!Evalua3on,!Release!and!Registra3on;!– Plant!Breeders’!Rights!(SADC)!

COMESA Burundi Comoros DR Congo Djibouti Egypt Eritrea Ethiopia Kenya Libya Madagascar Malawi Mauritius Rwanda Seychelles Sudan Swaziland Uganda Zambia Zimbabwe

SADC Angola Botswana DR Congo Lesotho Madagascar Malawi Mauritius Mozambique Namibia Swaziland Tanzania Zambia Zimbabwe South Africa Seychelles

EAC Burundi Kenya Rwanda Tanzania Uganda

ASARECA Burundi DRC Ethiopia Eritrea Kenya Madagascar Rwanda Sudan Tanzania Uganda

COMESA

ASARECA

SADC

EAC

SITUATION!IN!COMESA!

Ini3ated! in! 2008! and! adopted! by! the! COMESA!

Ministers! of! Agriculture! in! September! 2013;!

Expected! to! be! adopted! by! the! Council! of!

Ministers!in!February!2014!(final!adop3on);!

No! significant! differences! in! the! harmonized!

seed! regula3ons! of! COMESA,! SADC! and! EAC!

paving' the'way' for'a' tripar0te'agreement' for'the'three'RECs'(COMESA/SADC/EAC);!!

Draf! roadmap! for! its! implementa3on! already!

defined! by! COMESA/ACTESA! in! partnership!

with!the!African!Seed!Trade!Associa3on!(AFSTA)!

12/17/13

3

SITUATION!IN!SADC!

The!SADC!Protocol!on!seed!regula3ons!harmoniza3on!has!been!recently!signed!

by!11!Member!States!and!has!become!

enforceable;!

SADC!Seed!Center!has!been!established!in!2013!in!Lusaka,!Zambia!for!its!

implementa3on;!!

SITUATION!IN!ASARECA/EAC!

ASARECA!has!spearheaded!the!harmoniza3on!in!

EAC;!

Ini3ated!in!1999!and!reached!common!

agreement!in!2002!for!10!countries;!

Kenya,!Uganda,!and!Tanzania!opera3onalized!the!ASARECA/EAC!variety!

release!system!(regional!variety!list!available!

for!the!three!countries);!

Member!States!aligning!their!na3onal!seed!

law!to!the!ASARECA/EAC!common!

agreement.!

SITUATION!IN!ECOWAS!

Adopted!by!the!ECOWAS!Council!of!Ministers!

in!May!2008;!

The!West!African!Seed!CommiRee!(WASC)!in!

charge!of!the!implementa3on.!However,!it!is!

not!yet!established;!

CORAF/WECARD!is!taking!the!lead!for!its!

implementa3on;!

!Harmoniza3on!extended!to!cover!the!

Member!States!of!CILSS!and!WAEMU!!

12/17/13

4

IMPLEMENTATION!

Seed! sector! of! Member! States! at! different!

level! of! development;! there! is! need! to! uplif!

the! ones,! which! are! s3ll! lagging! behind! to!

opera3onalize!the!harmoniza3on;!

Implementa3on! is! challenging! since! the!

agreements!were!reached!a!few!years!ago!but!

not!yet!a!reality!to!boost!the!seed!trade;!

Requires! more! commitment! (human! and!

technical)! from! Member! States! and! an!

efficient!coordina3on/implementa3on!Unit.!

CONCLUSION!

Harmoniza3on! of! seed! regula3ons! and!

policies!should!boost!seed!trade!in!Africa!

to!improve!livelihood!of!African!farmers;!

Public!and!Private!Partnership!is!a!crucial!e lement! for! the! success! of! i ts!

implementa3on.!

1

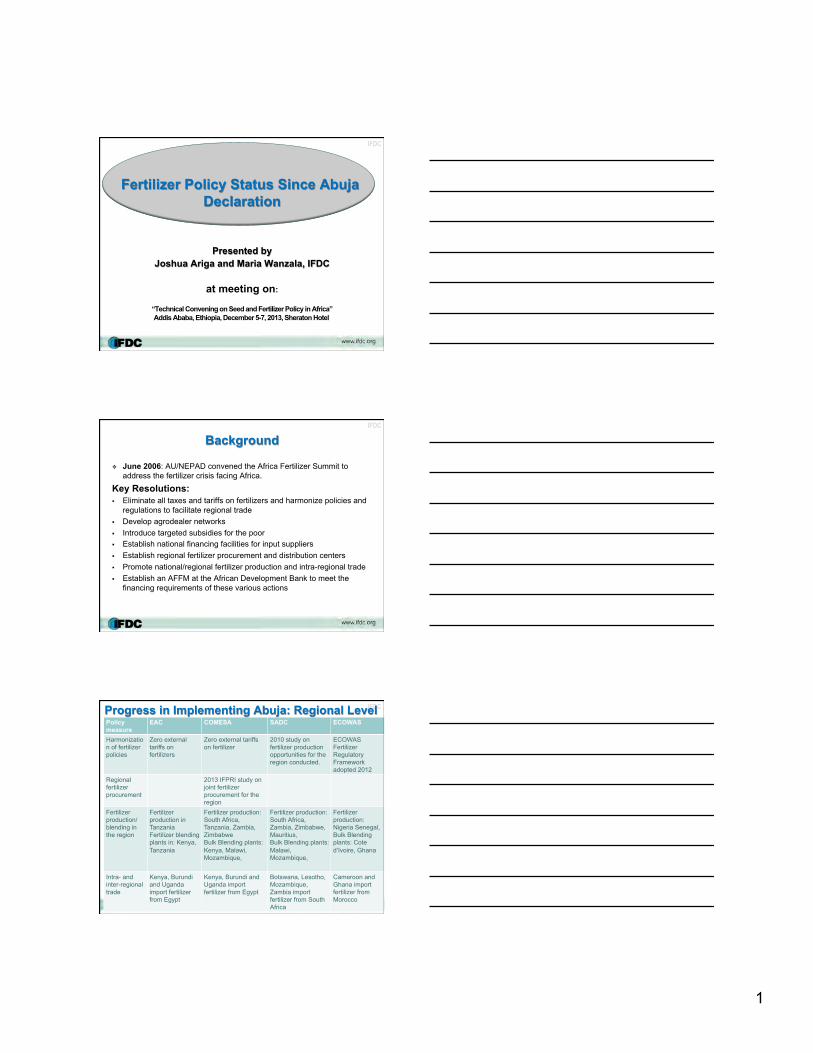

IFDC

Fertilizer Policy Status Since Abuja

Declaration

Presented by Joshua Ariga and Maria Wanzala, IFDC

at meeting on:

“Technical Convening on Seed and Fertilizer Policy in Africa” Addis Ababa, Ethiopia, December 5-7, 2013, Sheraton Hotel

IFDC

Background ! June 2006: AU/NEPAD convened the Africa Fertilizer Summit to

address the fertilizer crisis facing Africa.

Key Resolutions: " Eliminate all taxes and tariffs on fertilizers and harmonize policies and

regulations to facilitate regional trade " Develop agrodealer networks " Introduce targeted subsidies for the poor " Establish national financing facilities for input suppliers " Establish regional fertilizer procurement and distribution centers " Promote national/regional fertilizer production and intra-regional trade " Establish an AFFM at the African Development Bank to meet the

financing requirements of these various actions

IFDC

Policy measure

EAC COMESA SADC ECOWAS

Harmonization of fertilizer policies

Zero external tariffs on fertilizers

Zero external tariffs on fertilizer

2010 study on fertilizer production opportunities for the region conducted.

ECOWAS Fertilizer Regulatory Framework adopted 2012

Regional fertilizer procurement

2013 IFPRI study on joint fertilizer procurement for the region

Fertilizer production/ blending in the region

Fertilizer production in Tanzania Fertilizer blending plants in: Kenya, Tanzania

Fertilizer production: South Africa, Tanzania, Zambia, Zimbabwe Bulk Blending plants: Kenya, Malawi, Mozambique,

Fertilizer production: South Africa, Zambia, Zimbabwe, Mauritius, Bulk Blending plants: Malawi, Mozambique,

Fertilizer production: Nigeria Senegal, Bulk Blending plants: Cote d’Ivoire, Ghana

Intra- and inter-regional trade

Kenya, Burundi and Uganda import fertilizer from Egypt

Kenya, Burundi and Uganda import fertilizer from Egypt

Botswana, Lesotho, Mozambique, Zambia import fertilizer from South Africa

Cameroon and Ghana import fertilizer from Morocco

Progress in Implementing Abuja: Regional Level

2

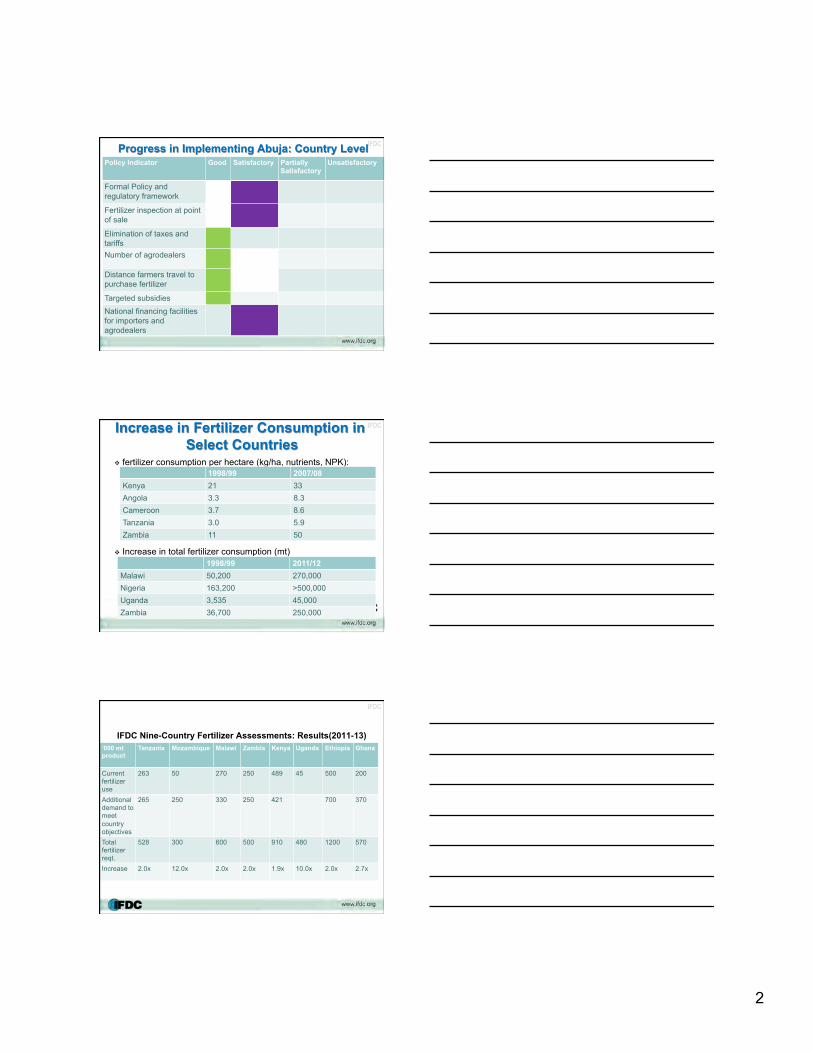

IFDC Progress in Implementing Abuja: Country Level Policy Indicator Good Satisfactory Partially

Satisfactory Unsatisfactory

Formal Policy and regulatory framework

Fertilizer inspection at point of sale

Elimination of taxes and tariffs Number of agrodealers

Distance farmers travel to purchase fertilizer

Targeted subsidies National financing facilities for importers and agrodealers

IFDC Increase in Fertilizer Consumption in Select Countries

! fertilizer consumption per hectare (kg/ha, nutrients, NPK):

! Increase in total fertilizer consumption (mt)

1998/99 2007/08 Kenya 21 33 Angola 3.3 8.3 Cameroon 3.7 8.6 Tanzania 3.0 5.9 Zambia 11 50

1998/99 2011/12 Malawi 50,200 270,000 Nigeria 163,200 >500,000 Uganda 3,535 45,000 Zambia 36,700 250,000

IFDC

IFDC Nine-Country Fertilizer Assessments: Results(2011-13)

‘000 mt product

Tanzania Mozambique Malawi Zambia Kenya Uganda Ethiopia Ghana

Current fertilizer use

263 50 270 250 489 45 500 200

Additionaldemand to meet country objectives

265 250 330 250 421 700 370

Total fertilizer reqt.

528 300 600 500 910 480 1200 570

Increase 2.0x 12.0x 2.0x 2.0x 1.9x 10.0x 2.0x 2.7x

3

IFDC

Policy Status and Constraints in 9 Countries

! Policy Status - Fertilizer subsidy in all

countries (except Uganda)

- Private sector imports in all countries except Ethiopia

- Formal fertilizer act in all countries (exceptions: Zambia’s is outdated; Uganda has a draft)

- No tax on imports (Tanzania, Kenya,

- Blending services available: Kenya, Malawi, Ghana, Ethiopia

- Zambia: ban on foreign currency trade has created exchange rate risks for international traders

! Key Policy Constraints - Ad hoc state intervention in imports (e.g. Kenya, Zambia)

- High cost and limited access to finance

- High transport & transaction costs due to: slow port discharge; poor port, road and rail infrastructure; small vessels; low ton trucks

- Border points (slow clearance, bureaucracy)

- Outdated recommendations, poor information on correct use and benefits of fertilizers

- Low adoption of blends; low yields due to wrong fertilizers

- Limited access to output markets, including storage and warehouse receipt system

- Inspection/regulations hinder product mix by limiting product set

IFDC

Policy Recommendations – National Level ! Expert advice on alternative subsidy approaches that will allow private sector

development ! PPPs for some port functions to expedite clearance (e.g. loading and unloading) ! Expert assistance to draft fertilizer policies and strategies ! Governments create predictable and stable policy environment (cease ad hoc market

intervention) ! Provide information and training to farmers and agrodealers on fertilizer benefits and

update recommendations ! Widen set of fertilizer products by soil testing and crop specific fertilizers ! Finance for private sector blending activities ! Invest in agrodealer networks (training and financing via risk-sharing arrangements) ! Link farmers to output markets (processing farms, buyers) ! New fertilizer products will require revamping extension services and capacity building

for agrodealers and farmers to determine appropriate blends and encourage adoption

IFDC

Policy Recommendations – Regional Level

! Update and/or draft national fertilizer policy and quality regulations. Ensure they are aligned to regional regulatory frameworks

! Develop national fertilizer policy in harmony with regional business interests for importers and dealers

! Handle infrastructure upgrades regionally

4

IFDC

Key Principles to Guide Input Policy

! Increase farmer physical proximity and access to input and output markets (rural roads, storage, processing, warehouse receipt systems, outgrower schemes, One-Acre fund model)

! Create incentives for increased private sector investment and engagement in the fertilizer space (predictable policy, finance)

! Use public funds efficiently – include complementary inputs in subsidy schemes (improved seeds, irrigation, extension, credit) in subsidy programs) and make them “smart” i.e. distribute via the private sector (sustainability)

! Facilitate farmer access to the most appropriate fertilizers for their soil type and crop mix to increase use efficiency and maximize their return

IFDC

12/17/13&

1&

Private&Sector&Perspec3ve&on&Seed&Policy&

Voices&from&the&Field&&

Addis&Ababa,&Dec.&6,&2013&

Who&Are&the&Voices?&

This&compila3on&is&based&on&100+&field&visits&to&African&seed&companies&in&12&

countries,&2008&K&2013&&&Ethiopia,&Rwanda,&Uganda,&Kenya,& &Tanzania,&

Malawi,&Mozambique,&Zambia,& &Ghana,&Nigeria,&Burkina&Faso&and&Mali&

Most&of&the&themes&are&common,&but&some&are&specific&to&individual&countries&

(e.g.&package&size&in&Ethiopia)&

12/17/13&

2&

General&Business&Environment&

! A"posi've"general"business"environment"that"is"

characterized"by"freedom"to"operate"and"low"levels"

of"bureaucracy,"including:"ease"of"licensing,"

registra'on,"filings;"access"to"bank"financing"at"

reasonable"rates;"ability"to"source"equipment"and"

supplies"from"outside"the"country;"fair"taxes;"ability"

to"brand"their"product;"etc.&

4&

General&Business&Environment&

! Support"for"a"robust"compe''ve"environment,"

which"will"raise"quality"and"lower"prices"for"farmers"

(e.g.,"a"level"playing"field"which"does"not"favour"a"

parastatal)&

! An"absence"of"subsidy"programs"that"drive"longE

term"market"distor'ons&! A"longEterm"view"of"the"business"environments"–"

local,"regional,"con'nental,"global,"and"the"unique"

requirements"of"each&

5&

Legisla3on&and&Regula3ons&! Clear,"forwardElooking"legisla'on,"including"recogni'on"of"local,"regional,"and"global"export"

markets&

! Clear"regulatory"frameworks"that"draw"strongly"on"

private"sector"ar'cula'on"of"costs,"needs,"and"

seasonal"issues"surrounding"seed"produc'on&

! “Form"that"follows"func'on”"–"e.g."export"

standards"for"export"seed,"but"more"prac'cal"

reputa'onEdriven"and"licenseEdriven"frameworks"

for"na'onal"markets&6&

12/17/13&

3&

Legisla3on&and&Regula3ons&

! A"seed"release"policy"that"is"not"excessively"lengthy"or"bureaucra'c"

! Clearly"ar'culated"and"effec'vely"implemented"

seed"company"regula'ons"that"are"tough"and"fair,"

but"not"onerous.""Ul'mately,"these"regula'ons"

should"migrate"towards"“good"conduct”"models"for"

companies"that"have"demonstrated"quality"

standards"and"ability"to"selfEregulate&

7&

Research&

! FarmerEresponsive"breeding"and"research"efforts"to"

develop"costEintensive"public"goods"that"cannot"be"

funded"privately"

! "Seed"company"exposure"to"the"breeding"pipeline,"and"

ability"to"test"material"in"onEfarm"condi'ons"before"it"is"

released"&

! Support"in"building"human"capacity"by"sharing"the"

talent"in"the"government"breeding"talent"pool,"either"

via"secondment,"frequent"interac'on,"or"dedicated"

trainings&

8&

Research&

! Breeding"ac'vi'es"to"support"ongoing"product"line"upgrades"and"evolu'on,"especially"for"orphan"crops&

! An"“open"architecture”"system"for"germplasm"

acquisi'on"for"both"commercial"produc'on"and"for"

breeding&

9&

12/17/13&

4&

Policy&in&Prac3ce&! A"liberalized"founda'on"seed"environment,"ideally"with"

technical"support"for"parent"seed""produc'on"if"needed"

un'l"company"can"produce"parent"seed"on"its"own""&

! "High"quality,"consistent"supply"of"inputs"under"government"control,"such"as"breeder"seed,"and"

founda'on"seed"if"companies"are"not"allowed"to"

produce"it"themselves.""This"supply"should"be"driven"by"

dialogue"with"the"seed"company"for"up"to"two"years"

before"delivery.""(Note"that"ideally"companies"will"be"

allowed"to"produce"their"own"founda'on"seed.)&

& 10&

Policy&in&Prac3ce&! "Transparency"about"variety"licensing"and"alloca'on"process"for"parental"seed"

! Transparency"in"subsidies"and"tenders,"focusing"on"qualified"private"sector"en''es"&

! Adequate"funding"for"local"regulatory"agencies"&! Lack"of"governmentEimposed"barriers"between"the"

company"and"the"ul'mate"customer,"the"farmer.""That"

is,"a"clear"path"between"the"seed"company"and"the"

farmer,"without"forcing"the"seed"company"to"go"

through,"e.g.,"a"coop"(although"they"may"choose"to"do"

so.)&11&

Policy&in&Prac3ce&

! MarketEbased"pricing,"driven"by"what"customers"

are"willing"to"pay"for"the"value"they"receive"from"

the"company.""(Value"is"a"combina'on"of"price,"

product"characteris'cs,"consistency"of"supply,"

convenience,"packaging,"etc.)&

! Prosecu'on"of"fake"seed"purveyors"&! An"appropriate"level"of"quality"control"on"pointEofEsale"outlets,"such"as"license"renewal"condi'ons,""

including"coop"distribu'on"sites&

12&

12/17/13&

5&

Support&and&S3mula3on&! Financial"support"for"research"and"capacity"investments,"which"might"range"from"a"matching"

investment"fund"(with"a"cap)"to"a"relaxa'on"of"import"

du'es"and"taxes"when"the"company"is"impor'ng"

research"or"produc'on/processing"equipment&

! Interest"rate"“buyEdown”"or"guaranty"fund"for"seed"companies"and"agrodealers"to"help"to"increase"quality"

seed"produc'on"and"dissemina'on"

! Assistance"with"access"to"land,"and"especially"land"with"irriga'on"poten'al&

13&

Support&and&S3mula3on&! Appropriately"synched"extension"work"to"strengthen"farmer"prac'ces,"including"building"demand"for"

improved"inputs&

! Facilita'on"of"open"dialogue"about"how"to"con'nually"improve"the"system,"always"keeping"the"farmer"at"the"

heart"of"the"mission.""This"should"include"regular"

mee'ngs"between"government"policyEmakers"and"

implementers,"researchers,"and"the"private"sector"to"

ensure"that"ac'vi'es"and""needs"are"appropriately"

coordinated"(as"was"done"so"successfully"in"India)&

14&

Food&for&Thought…&

What&cons3tutes&private§or&voice?&&&

What&cons3tutes&government&voice?&

How&do&we&achieve&open,&construc3ve&dialogue&and&joint&learning?&

12/17/13&

1&

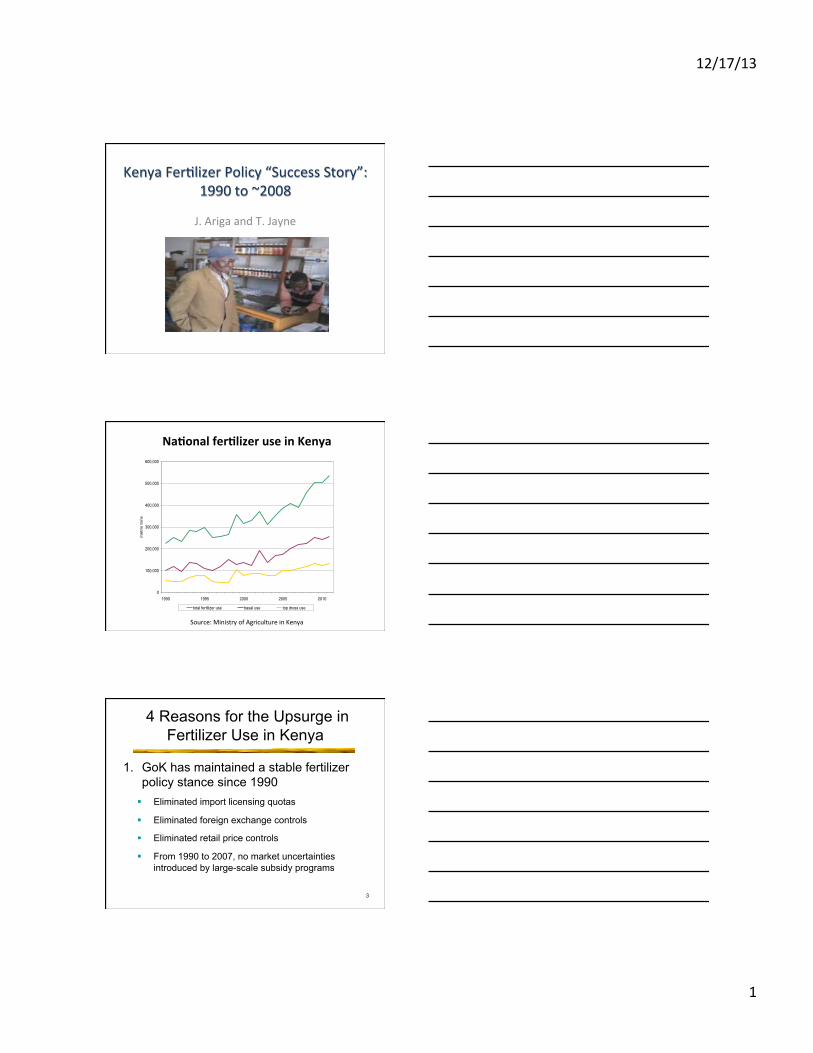

Kenya&Fer.lizer&Policy&“Success&Story”:&&&1990&to&~2008&

J.&Ariga&and&T.&Jayne&

0

100,000

200,000

300,000

400,000

500,000

600,000

1990 1995 2000 2005 2010

me

trix

to

ns

total fertilizer use basal use top dress use

Na#onal'fer#lizer'use'in'Kenya'

Source:&Ministry&of&Agriculture&in&Kenya&

3

4 Reasons for the Upsurge in Fertilizer Use in Kenya

1. GoK has maintained a stable fertilizer policy stance since 1990 ! Eliminated import licensing quotas

! Eliminated foreign exchange controls

! Eliminated retail price controls

! From 1990 to 2007, no market uncertainties introduced by large-scale subsidy programs

12/17/13&

2&

4

4 Reasons for the Upsurge in Fertilizer Use in Kenya

2. In response to stable input policy environment, private sector investment in fertilizer distribution expanded rapidly ! 10-11 importers ! 500 wholesalers ! 8,000 retailers

5

4 Reasons for the Upsurge in Fertilizer Use in Kenya

3. In response to expansion of input stockists, small farmers’ are now much closer to fertilizer retailers ! 1997: 7.4kms ! 2000: 5.6kms ! 2004: 3.7kms ! 2007: 3.2kms

Kms'to'nearest'fer#lizer'seller'

Coastal'

Lowlands'

Eastern'

Lowlands'

Western'

Lowlands'

Western'

trans'

HPMZ' Western'

Highlands'

Central'

Highlands'

1997' 28.3' 9.8' 15.9' 6.3' 5.0' 3.3' 2.7'

2007' 9.9' 2.7' 3.8' 3.6' 3.6' 2.4' 1.3'

change'in'km'

L18.4' L7.1' L12.1' L2.7' L1.4' L0.9' L1.4'

12/17/13&

3&

7

Reasons for the Upsurge in Fertilizer Use in Kenya

4. Greater competition among importers and wholesalers has led to declining fertilizer marketing costs

Price&of&DiIammonium&Phosphate&(DAP)&in&Mombasa&and&Nakuru&(constant&2012&Kenyan&shillings&per&50&kg&bag)&

0

1000

2000

3000

4000

5000

6000

7000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

KSH

per

50

kg b

ag o

f DA

P (r

eal 2

012

pric

es)

Mombasa CIF Nakuru wholesale

Source: Yearly average fertilizer prices come from the Ministry of Agriculture in Kenya. Prices were deflated to 2012 levels using the CPI from the Kenya National Bureau of Statistics (KNBS).

Decline&in&marke.ng&margins&

Increased&domes.c&market&compe..on& Alliances&with&interna.onal&partners&

– access&to&cheaper&credit&– KnowIhow&conferred&to&local&firms&"&cost&reduc.ons&

12/17/13&

4&

end&

Recent&Evidence&on&Input&Subsidy&Programs&

Economists&have&focused&on&market&failures&as&primary&cause&of&low&fer.lizer&use& This&characteriza.on&has&served&as&ra.onale&for&ISPs& Rela.vely&liZle&analysis&of&whether&low&use&of&fer.lizer&reflects&low&profitability&of&use&

12/17/13&

5&

Low&crop&response&rates&to&fer.lizer&applica.on&leads&to&both:&&– Low&profitability&– Low&B/C&ra.os&of&fer.lizer&subsidy&programs&

Distribution of expected MPs of nitrogen at the district, soil group, year level

0.0

2.0

4.0

6

Den

sity

0 10 20 30 40 50expected marginal physical product of nitrogen

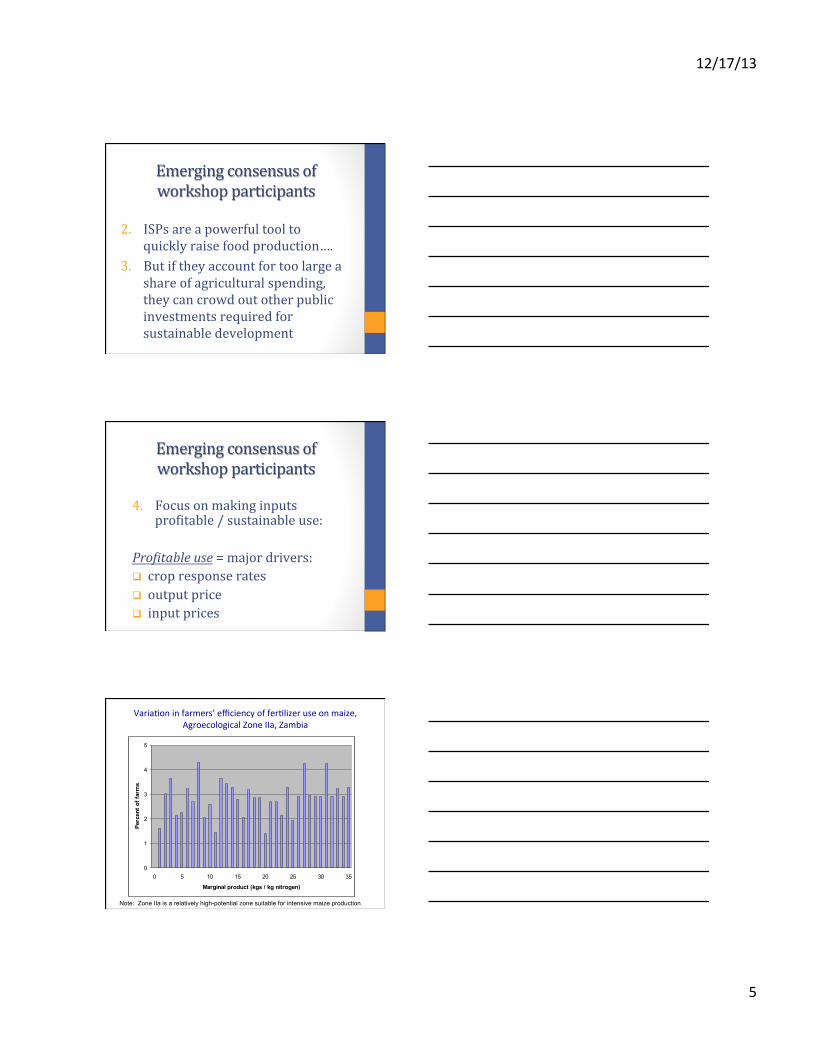

Varia.on&in&farmers’&efficiency&of&fer.lizer&use&on&maize,&Agroecological&Zone&IIa,&Zambia&

0

1

2

3

4

5

0 5 10 15 20 25 30 35

Marginal product (kgs / kg nitrogen)

Per

cent

of

farm

s

Note: Zone IIa is a relatively high-potential zone suitable for intensive maize production

12/17/13&

6&

16

Basal Productivity, NR II, Zambia

Maize yield response to basal fertilizer over soil acidity ranges Soil pH 3.1 - 4.3 4.4 - 5.4 5.5 - 7.1 Average partial effect of basal fertilizer application (kg/kg)

2.140** (0.01)

3.735*** (0.00)

7.552*** (0.00)

% of sample 51% 47% 2% **,&***&denotes&significance&at&the&5%&and&1%&level&respec.vely,&delta&method&pIvlaues&in&parentheses&

17

From'Larson'and'Oldham,''Mississippi'State'University'Extension'Service,'2008.''

Unresolved&problem:&

Low&crop&response&rates&are&a&major&underlying&problem&that&impedes&both&– Effec.ve&demand&for&fer.lizer&&– B/C&ra.o&of&ISPs&– Most&ISPs&evaluated&in&our&study&had&B/C&ra.os&less&than&1.0&

– Evaluated&under&a&range&of&alterna.ve&assump.ons&and&plausible&prices&

12/17/13&

7&

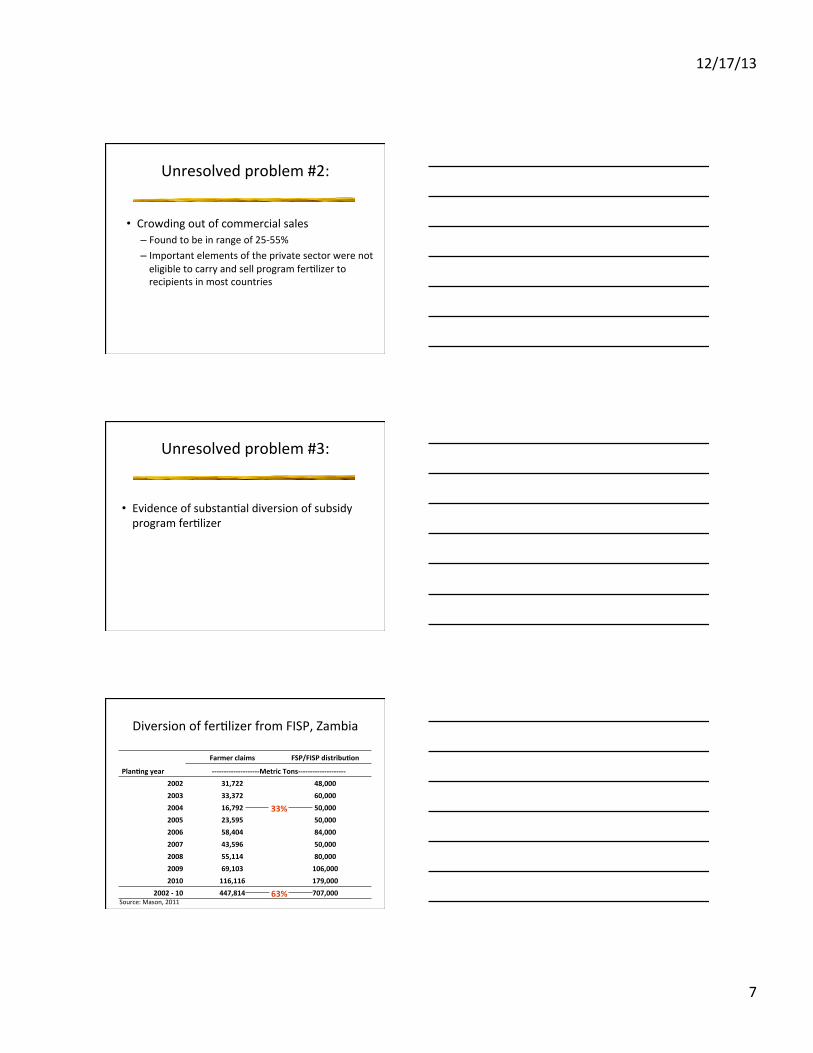

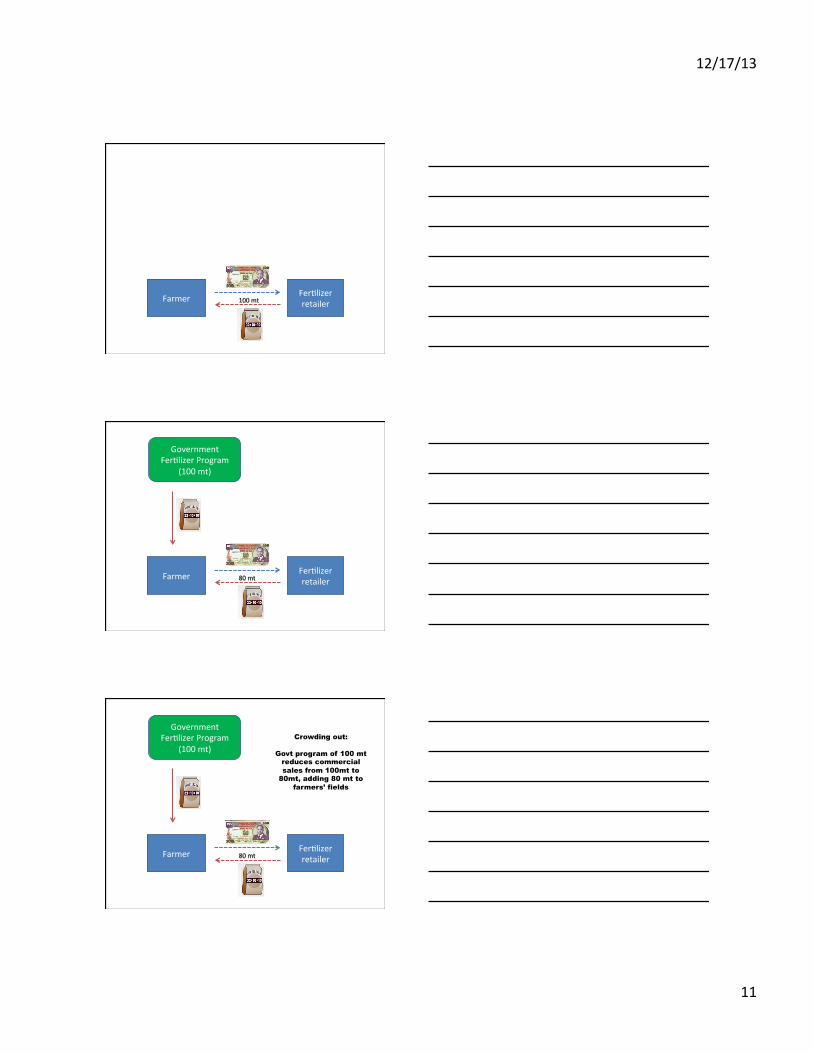

Unresolved&problem:&

Crowding&out&of&commercial&sales&– Found&to&be&in&range&of&25I55%&– Important&elements&of&the&private§or&were¬&eligible&to&carry&and&sell&program&fer.lizer&to&recipients&in&most&countries&

Unresolved&problem:&

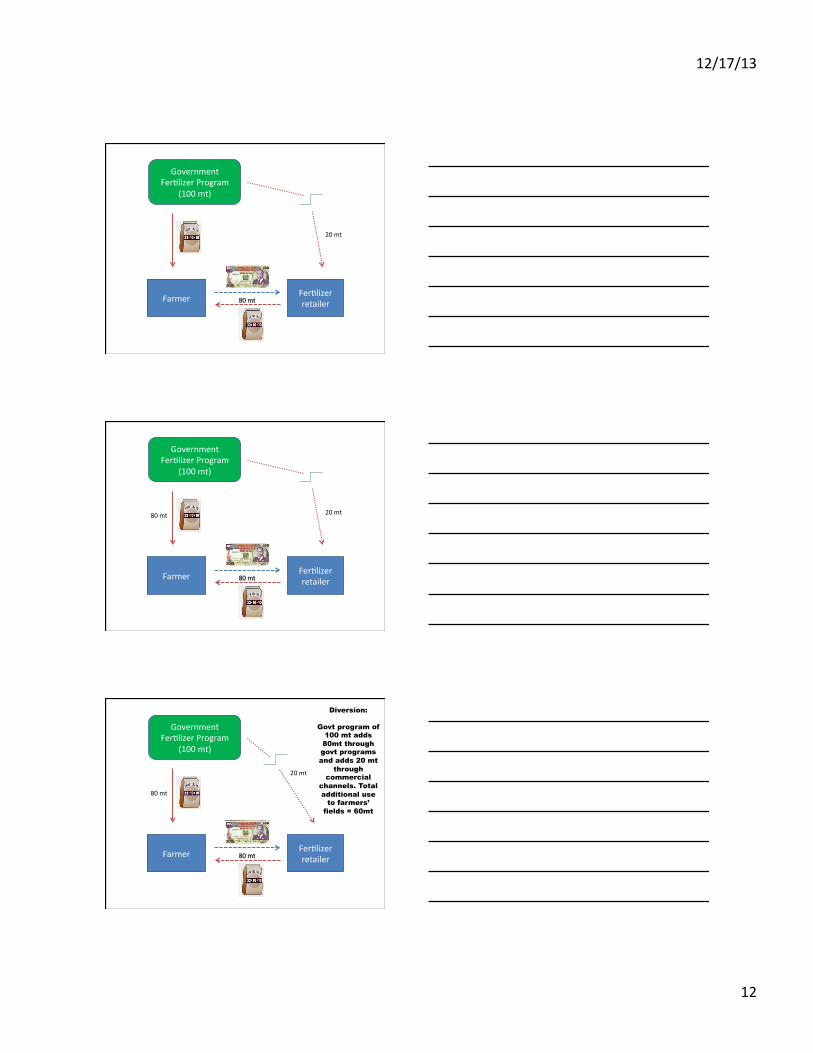

Evidence&of&substan.al&diversion&of&subsidy&program&fer.lizer&

21

Diversion&of&fer.lizer&from&FISP,&Zambia&&

Farmer'claims' FSP/FISP'distribu#on'

Plan#ng'year' LLLLLLLLLLLLLLLLLLLLMetric'TonsLLLLLLLLLLLLLLLLLLLL'

2002' 31,722' 48,000'

2003' 33,372' 60,000'

2004' 16,792' 50,000'

2005' 23,595' 50,000'

2006' 58,404' 84,000'

2007' 43,596' 50,000'

2008' 55,114' 80,000'

2009' 69,103' 106,000'

2010' 116,116' 179,000'

2002'L'10' 447,814' 707,000'Source:&Mason,&2011&

33%'

63%'

12/17/13&

8&

Unresolved&problem&

ISPs¬&targeted&to&the&poor,&and&hence&have&rela.vely&liZle&effect&on&poverty& The&ar.cles&in&the&SI&found&liZle&evidence&that&

– ISPs&reduce&food&prices&or&increase&wage&rates&– Fer.lizer&targeted&to&wealthier&smallholders&can&use&fer.lizer&more&efficiently&than&poor&farmers&

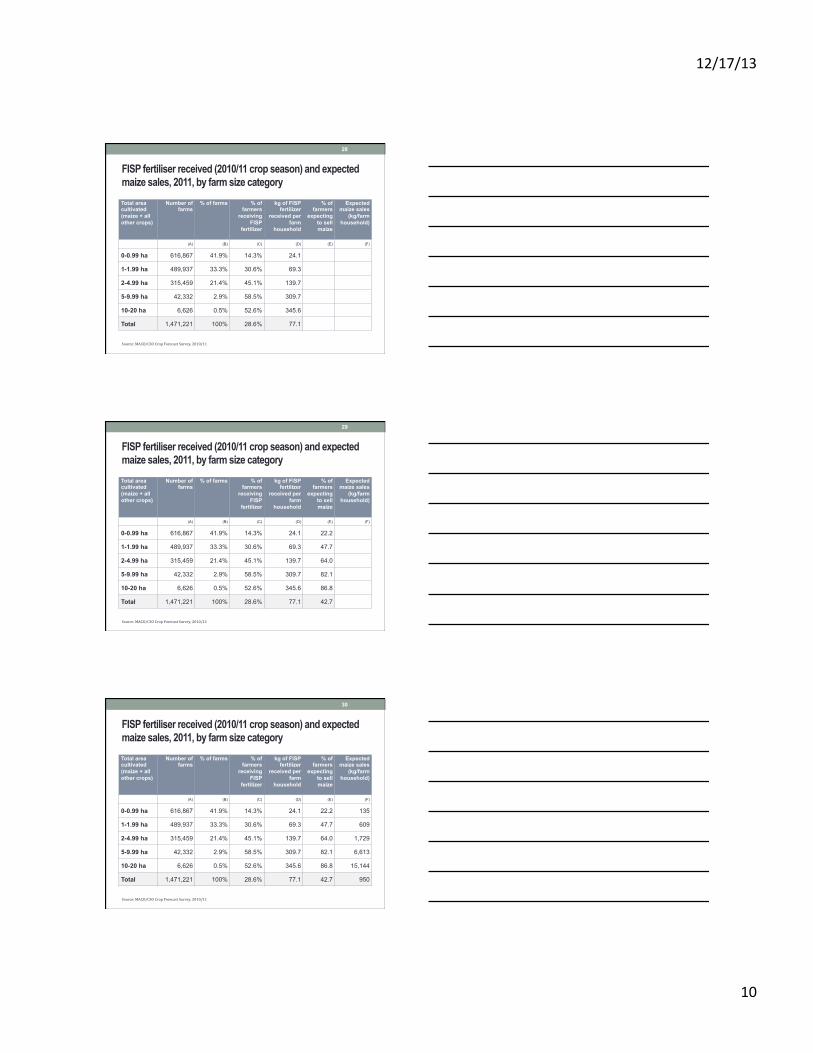

23&

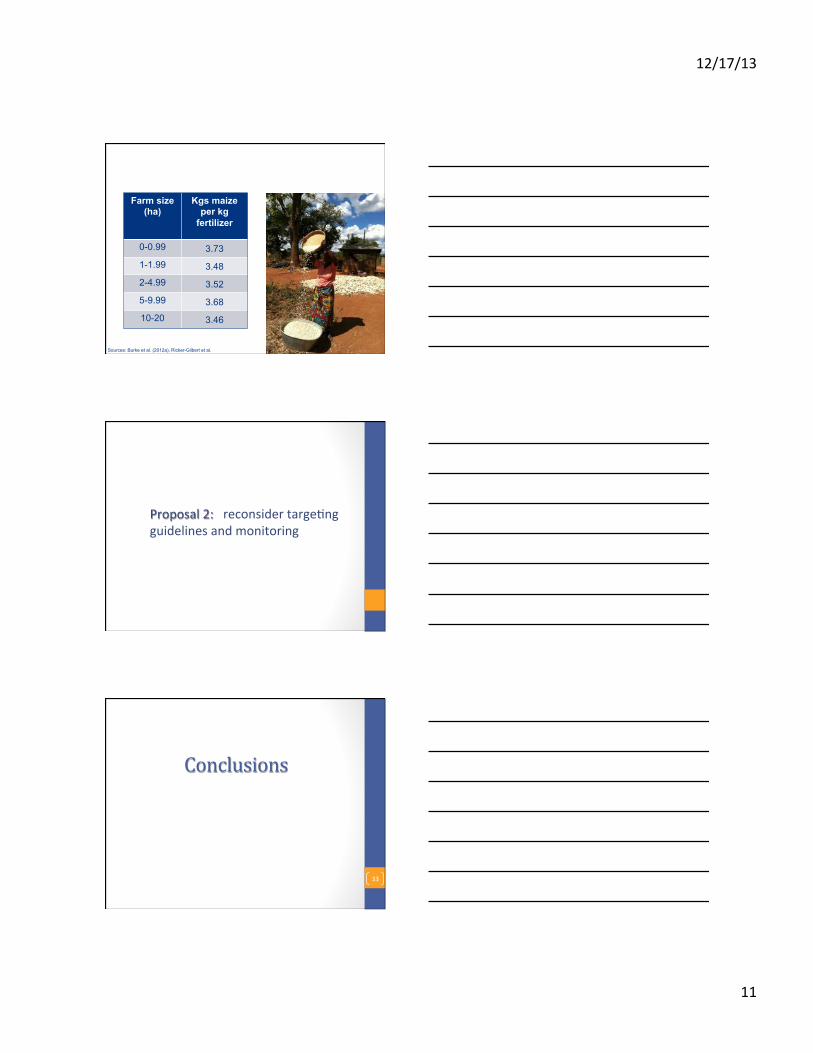

Farm size (ha)

Kgs maize per kg

fertilizer

0-0.99 3.73

1-1.99 3.48

2-4.99 3.52

5-9.99 3.68

10-20 3.46

Sources:&Burke&et&al.&(2012a),&RickerIGilbert&et&al.&&

24&

IFPRI&review&of&rate&of&return&studies:&Returns

Subsidies Negative – 12% Investments - research & extension 35% to 70%

- roads 20% to 30% - education 15% to 25% - communications 10% to 15% - irrigation 10% to 15%

If'we'believe'these'findings,'they'have'major'implica#ons'

12/17/13&

9&

Conclusions)

25&

Conclusions)1. ISPs)would)be)more)effective)if)adequate)

resources)were)allocated)to)complementary)public)investments)

2. More)balanced)public)expenditure)patterns)could)more)effectively)promote)national)policy)objectives)

3. Many)of)the)“smart)subsidy”)concepts)were)not)implemented)in)practice)

4. There)remain)concrete)steps)for)improving)ISP)effectiveness)–)but)not)clear)whether)they)are)feasible)to)achieve)

26&

Thank&you&

12/17/13&

10&

Distribution of MVCRs at the village, year level

0.2

.4.6

.8

Den

sity

0 2 4 6marginal value cost ratio

Farmer& Fer.lizer&&retailer&

Farmer& Fer.lizer&&retailer&

12/17/13&

11&

Farmer& Fer.lizer&&retailer&100&mt&

Farmer& Fer.lizer&&retailer&

Government&Fer.lizer&Program&&

(100&mt)&

80&mt&

Farmer& Fer.lizer&&retailer&

Government&Fer.lizer&Program&&

(100&mt)&

80&mt&

Crowding out:

Govt program of 100 mt reduces commercial sales from 100mt to

80mt, adding 80 mt to farmers’ fields

12/17/13&

12&

Farmer& Fer.lizer&&retailer&

Government&Fer.lizer&Program&&

(100&mt)&

20&mt&

80&mt&

Farmer& Fer.lizer&&retailer&

Government&Fer.lizer&Program&&

(100&mt)&

80&mt& 20&mt&

80&mt&

Farmer& Fer.lizer&&retailer&

Government&Fer.lizer&Program&&

(100&mt)&

80&mt&

20&mt&

80&mt&

Diversion:

Govt program of 100 mt adds 80mt through govt programs and adds 20 mt

through commercial

channels. Total additional use

to farmers’ fields = 60mt

12/17/13&

1&

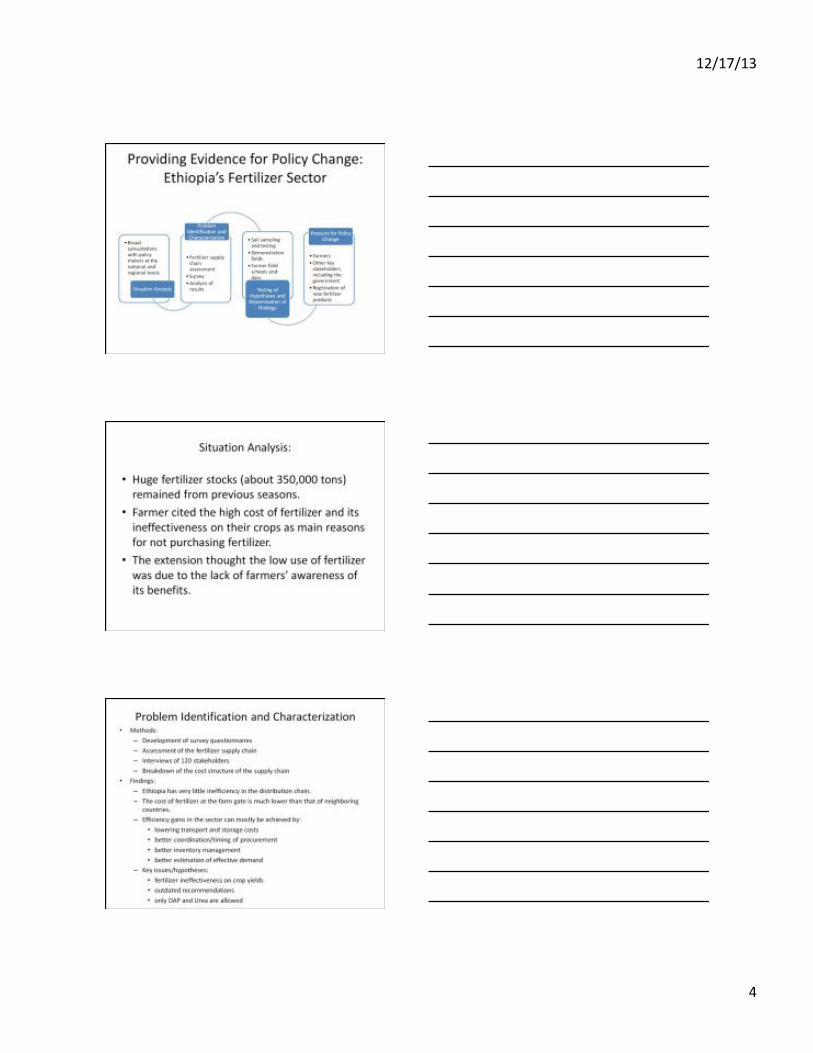

Soil%Fer)lity%Management%in%Ethiopia%

2&

Agenda%

! Issues&! Approaches&

! EthioSIS&! Fer7lizer&blending&! Soil&test&based&fer7lizer&recommenda7ons&&

3&

Agenda%

! Issues&! Approaches&

! EthioSIS&! Fer7lizer&blending&! Soil&test&based&fer7lizer&recommenda7ons&&

12/17/13&

2&

4&SOURCE:&FAO;ATA;&AfSIS&

Exis%ng(soil(maps(in(Ethiopia(are(obsolete(with(limited(soil(fer%lity(informa%on(resul%ng(in(par%al(u%liza%on(of(soil(fer%lity(informa%on(on(

agricultural(ac%vi%es( ! The%world%soil%map%was%published%in%1970s%by%FAO%and%UNESCO%at%a%resolu)on%of%1:5M,%which%was%then%focused%to%1:2M%for%Ethiopia%by%1984%

! The%soil%map%is%based%on%soil%surveys%conducted%in%the%1930s%to%1970s%

! The%map%is%generated%using%soil%informa)on%and%technology%from%the%1960s%N%spa)al%informa)on%technologies%were%not%used%

! The%map%show%soil%types%in%Ethiopia%and%there%distribu)on%%%

Soil&informa7on&management&is&a&key&boJleneck:&Ethiopian&soil&informa7on&are&outdated,&lack&detail,&and&have&limited&use&in&suppor7ng&soil&conserva7on&and&land&management&efforts&&&

Extracted(for(Ethiopia(at(a(scale(of(1:2M(from(the(world(soil(map(of(FAO/UNESCO(((

5&

1817161615141313

08/09&07/08&06/07&05/06&04/05&03/04& 10/11&09/10&

443435393634

2522

07/08& 10/11&09/10&08/09&06/07&05/06&04/05&03/04&

Annual%Growth%Rate%%(CAGR)%

2003/04S10/11&≈%10%%

2003/04S10/11&≈%5%%

Total%cereal%yield%Qt/ht%from%2003/04N2010/11%

Total%fer)lizer%applied%for%cereal%crop%0000’%tones%from%2003/04N2010/11%

Source:&CSA;&Agricultural&Sample&Survey&2003/04S11,&

! Blanket%%applica)on%of%DAP%and%UREA%is¬&considerate&of&crop&need,&soil&nutrient&dynamics&and&agroSecological&factors&

&! 100%KG%of%DAP%and%Urea%is&applied&across&the&country&for&all&crops&providing&only&Nitrogen&and&Phosphorus%

%&%%&! Due&to&absence&of&updated%

and%detailed%informa)on%other&deficiencies&have¬&been&observed&&&

&! The&government&is&working&address&the&issue&by&developing&soil%Informa)on%atlas%and&introducing&fer)lizer%blending%to%the%country%&

Annual%Growth%%Rate%%(CAGR)%

Ethiopia’s&investment&in&fer7lizer&has¬&paid&off;&growth&in&fer7lizer&use&has¬&resulted&in&commensurate&increases&in&yield&requiring&alterna7ves&such&as&enhancing&local&fer7lizer&produc7on&&

6&

Agenda%

! Issues&! Approaches&

! EthioSIS&! Fer7lizer&blending&! Soil&test&based&fer7lizer&recommenda7ons&&

12/17/13&

3&

7&

EthioSIS,&in&addi7on&to&conduc7ng&soil&and&land&resource&assessments,&focuses&&on&extensive&soil&fer7lity&mapping&that&will&determine&the¤t&level&of&nutrient&deple7on,&and&allow&soil&and&crop&specific&fer7lizer&recommenda7ons&

! Soil%and%vegeta)on%samples%have%been%collected%and%analyzed%that%include%physical,%chemical%proper)es,%land%features%texture%and%organic%ma`er%%%%%%

8&

Diga&Woreda&nutrient&status&

[N]&ppm& [P]&ppm& [K]&ppm&

[S]&ppm& [Ca]&ppm& [Mg]&ppm&

“Best”¤t&topsoil¯oSnutrient&(N,&P,&K,&S,&Ca&&&Mg)&concentra7on&predic7ons&(to&be&validated)&

12/17/13&

4&

[Mn]&ppm&

[B]&ppm&

[Cu]&ppm&[Zn]&ppm&

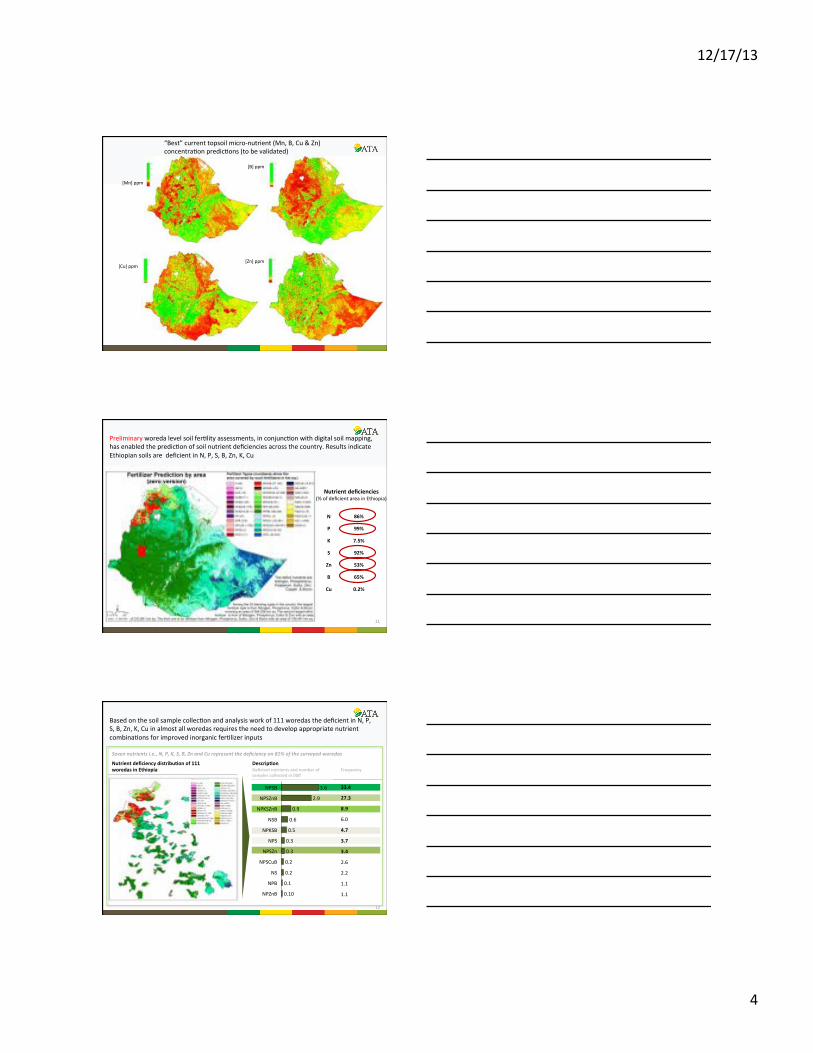

“Best”¤t&topsoilµSnutrient&(Mn,&B,&Cu&&&Zn)&concentra7on&predic7ons&(to&be&validated)&

11&

N% 86%%

P% 99%%

K% 7.5%%

S% 92%%

Zn% 53%%

B% 65%%

Cu% 0.2%%

Nutrient%deficiencies%%(%&of&deficient&area&in&Ethiopia)&

Preliminary&woreda&level&soil&fer7lity&assessments,&in&conjunc7on&with&digital&soil&mapping,&has&enabled&the&predic7on&of&soil&nutrient&deficiencies&across&the&country.&Results&indicate&Ethiopian&soils&are&&deficient&in&N,&P,&S,&B,&Zn,&K,&Cu&

12&

Based&on&the&soil&sample&collec7on&and&analysis&work&of&111&woredas&the&deficient&in&N,&P,&S,&B,&Zn,&K,&Cu&in&almost&all&woredas&requires&the&need&to&develop&appropriate&nutrient&combina7ons&for&improved&inorganic&fer7lizer&inputs&

Nutrient%deficiency%distribu)on%of%111%woredas%in%Ethiopia%%%

NPZnB&

NPSZn&

0.2&NPSCuB&

0.2&NS&

0.1&NPB&

0.10&

NPKSB&

0.3&NPS&

0.3&

0.5&

NSB& 0.6&

NPKSZnB& 0.9&

NPSZnB& 2.9&

NPSB& 3.6&

Deficient%nutrients%and%number%of%samples%collected%in%000’%

Descrip)on%Frequency%%

33.4%

27.3%

8.9%

6.0&

4.7%

3.7%

3.4%

2.6&

2.2&

1.1&

1.1&

Seven(nutrients(i.e.,(N,(P,(K,(S,(B,(Zn(and(Cu(represent(the(deficiency(on(81%(of(the(surveyed(woredas((

12/17/13&

5&

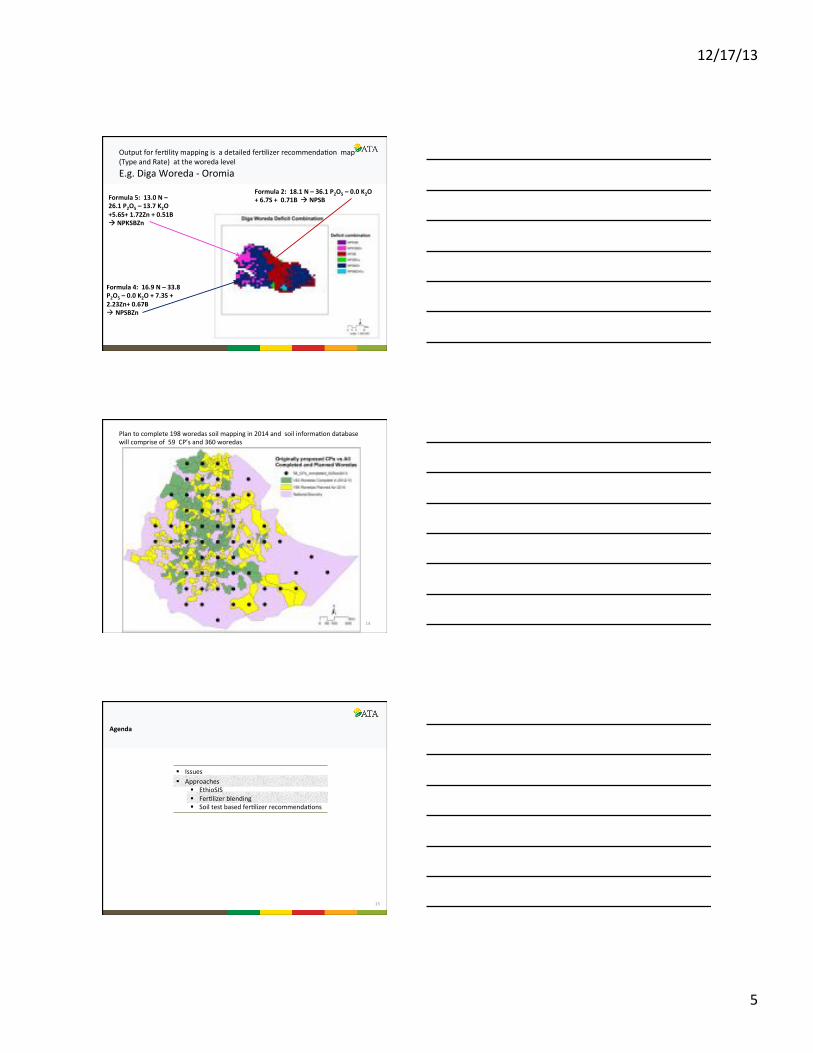

Output&for&fer7lity&mapping&is&&a&detailed&fer7lizer&recommenda7on&&map&(Type&and&Rate)&&at&the&woreda&level&&E.g.&Diga&Woreda&S&Oromia&

Formula%2:%%18.1%N%–%36.1%P2O5%–%0.0%K2O%+%6.7S%+%%0.71B%%!!%NPSB%

Formula%4:%%16.9%N%–%33.8%P2O5%–%0.0%K2O%+%7.3S%+%2.23Zn+%0.67B%" NPSBZn%

Formula%5:%%13.0%N%–%26.1%P2O5%–%13.7%K2O%+5.6S+%1.72Zn%+%0.51B%!!%NPKSBZn&

14&

Plan&to&complete&198&woredas&soil&mapping&in&2014&and&&soil&informa7on&database&&will&comprise&of&&59&&CP’s&and&360&woredas&

15&

Agenda%

! Issues&! Approaches&

! EthioSIS&! Fer7lizer&blending&! Soil&test&based&fer7lizer&recommenda7ons&&

12/17/13&

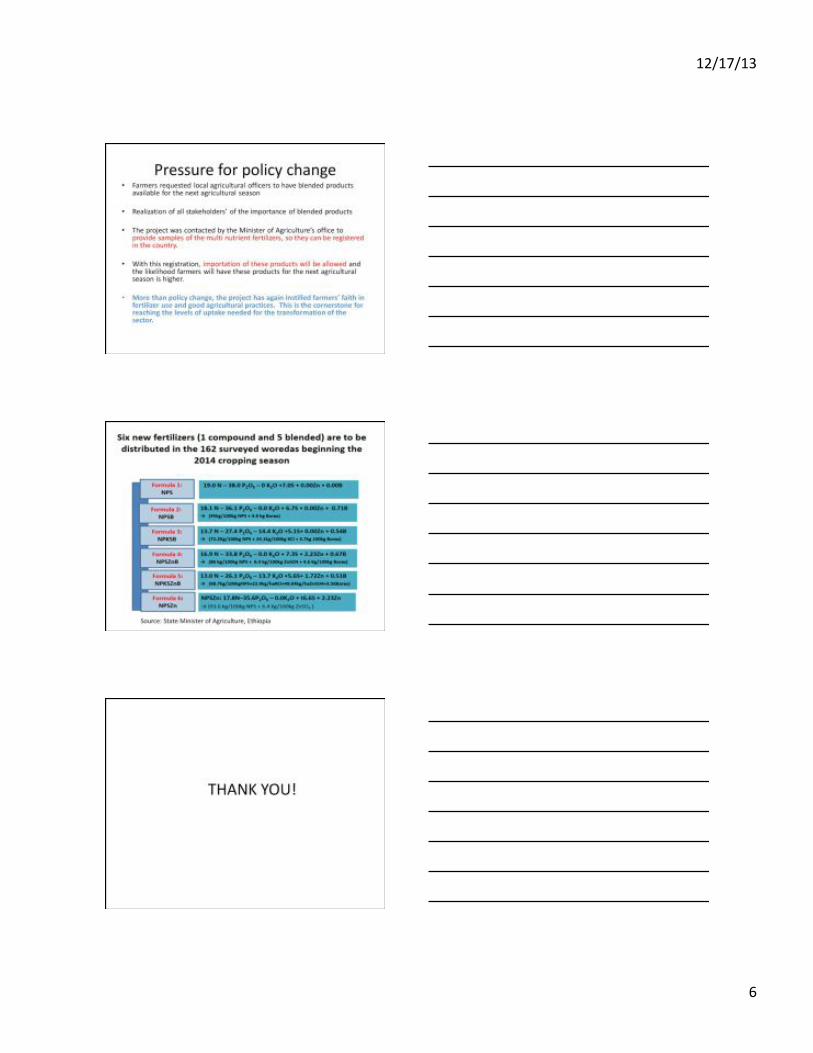

6&

16&

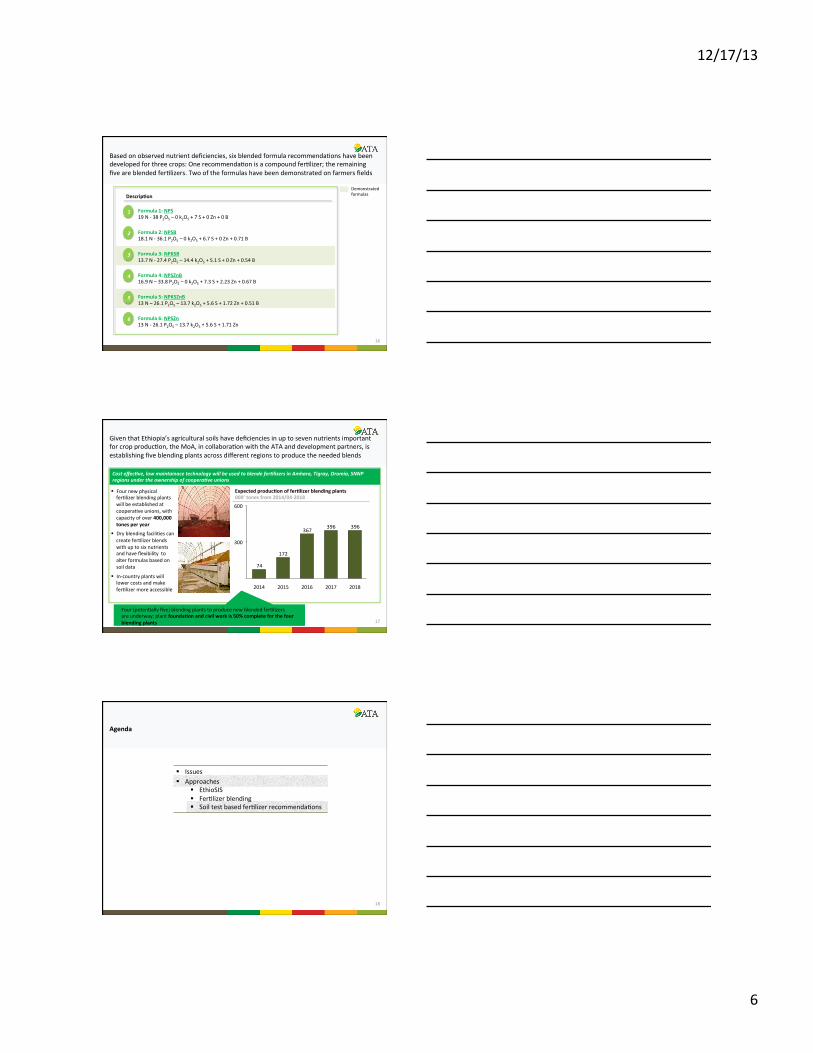

Based&on&observed&nutrient&deficiencies,&six&blended&formula&recommenda7ons&have&been&developed&for&three&crops:&One&recommenda7on&is&a&compound&fer7lizer;&the&remaining&five&are&blended&fer7lizers.&Two&of&the&formulas&have&been&demonstrated&on&farmers&fields&

1

2

3

4

5

6

Formula%1:%NPS%19&N&S&38&P2O5&–&0&k2O5&+&7&S&+&0&Zn&+&0&B&&

Formula%2:%NPSB%18.1&N&S&36.1&P2O5&–&0&k2O5&+&6.7&S&+&0&Zn&+&0.71&B&&

Formula%3:%NPKSB%13.7&N&S&27.4&P2O5&–&14.4&k2O5&+&5.1&S&+&0&Zn&+&0.54&B&&

Formula%4:%NPSZnB%16.9&N&–&33.8&P2O5&–&0&k2O5&+&7.3&S&+&2.23&Zn&+&0.67&B&&

Formula%5:%NPKSZnB%13&N&–&26.1&P2O5&–&13.7&k2O5&+&5.6&S&+&1.72&Zn&+&0.51&B&&

Formula%6:%NPSZn%13&N&S&26.1&P2O5&–&13.7&k2O5&+&5.6&S&+&1.71&Zn&

Descrip)on%Demonstrated&formulas&&

17&

Cost(effec%ve,(low(maintainace(technology(will(be(used(to(blende(fer%lizers(in(Amhara,(Tigray,(Oromia,(SNNP(regions(under(the(ownership(of(coopera%ve(unions((((

! Four&new&physical&fer7lizer&blending&plants&will&be&established&at&coopera7ve&unions,&with&capacity&of&over&400,000%tones%per%year%

! Dry&blending&facili7es&can&create&fer7lizer&blends&with&up&to&six&nutrients&and&have&flexibility&&to&alter&formulas&based&on&soil&data&

! InScountry&plants&will&lower&costs&and&make&fer7lizer&more&accessible&

Given&that&Ethiopia’s&agricultural&soils&have&deficiencies&in&up&to&seven&nutrients&important&for&crop&produc7on,&the&MoA,&in&collabora7on&with&the&ATA&and&development&partners,&is&establishing&five&blending&plants&across&different®ions&to&produce&the&needed&blends&

Expected%produc)on%of%fer)lizer%blending%plants%%000’%tones%from%2014/04N2018%

396396367

172

74

600&

300&

2018&2017&2016&2015&2014&

Four&(poten7ally&five)&blending&plants&to&produce&new&blended&fer7lizers&&are&underway;&plant&founda)on%and%civil%work%is%50%%complete%for%the%four%blending%plants%%%

18&

Agenda%

! Issues&! Approaches&

! EthioSIS&! Fer7lizer&blending&! Soil&test&based&fer7lizer&recommenda7ons&&

12/17/13&

7&

19&

In&addi7on&to&the&lack&of&upStoSdate&soil&informa7on&in&the&country,&there&has&been&no&systema7c&development&of&soil&test&based,&or&siteSspecific,&fer7lizer&recommenda7ons&

Systemic%%%

! low&rates&of&fer7lizer&adop7on&may&be&aJributed&to&a&mismatch%between%environmental%condi)ons%and%shortcomings&in&the¤tly&recommended&fer7lizer&technologies&

! Limited%nutrient%applica)on%irrespec)ve&of&the&diverse&agroecological&characteris7cs&of&the&country&and&the&price&efficiency&of&fer7lizer&use&by&the&farmer&&

! Absence%of%site%specific%recommenda)on%based&on&soil&informa7on&resul7ng&in&the&applica7on&of&inadequate&fer7lizer&applica7on&&

! Less%emphasis%on&organic&inputs&and&ISFM&prac7ces&with&increased&focus&on&inorganic&fer7liza7on&

Organiza)onal%system%%%

! Lack%of%standard%research%methodology%and%procedures%on&soil&test&based&fer7lizer&recommenda7on&development&making&extrapola7on&to&a&wider&area&difficult&for&a&na7onal&fer7lizer&recommenda7on&development&

! Lack%of%threshold%values%of%important%nutrients%to&determine&efficient&amount&of&fer7lizer&applica7on&&

Coordina)on%! Lack%of%coordina)on%and%agreement%on&the&na7onal&soil&test&based&fer7lizer&recommenda7on&effort:&miss&alignment&on&the&objec7ves&and&approach&for&developing&soil&test&based&fer7lizer&recommenda7on&at&the&na7onal&level&

Issues%% Descrip)on%%

20&

Soil&test&based&fer7lizer&recommenda7on&package&development&envisages&long%term%and%short%term&strategic&approaches&based&on&dis7nct&ra7onales& Long%term%strategy:&Will&focus&on&the&

development&of&different&fer)lizer%recommenda)on%packages%for%all%crops:&! Characterize&the&country&into&different&agroSecologies&and&soil&types&

! Iden7fy&fer7lizer&trial&modali7es&by&taking&different&crops&and&soil&types&into&considera7on&

! Conduct&different&fer7lizer&trials&using&various&nutrient&composi7on&by&taking&soil&fer7lity&informa7on&into&considera7on&

! Conduct&verifica7on&trials&using&different&trial&methodologies&&

Short%term%strategy:&Will&focus&on&the&development&of&op)mal%fer)lizer%recommenda)on%packages%for%major%cereal%crops&and&soil&fer7lity&condi7ons&&! Characterize&the&country&into&representa7ve&agroSecologies&&

! Iden7fy&fer7lizer&trial&modali7es&by&taking&major&cereal&crops&and&soil&types&into&considera7on&

! Conduct&representa7ve&fer7lizer&trials&! Develop&op7mal&fer7lizer&recommenda7on&packages&for&the&&major&cereal&crops&and&poten7al&high&produc7on&areas&&

Ra)onale….%%

Ra7onale&for&the&short&term&strategy:&! Intensive&and&all&inclusive&fer7lizer&recommenda7on&package&development&in&terms&of&crop&and&area&is&)me%taking%and%cumbersome&requiring&huge&resources&and&7me.&

! The&country&is&in&a%state%of%urgency%for%the%development%of%fer)lizer%recommenda)ons%for&major&cereal&crops&&

! The&short&term&package&development&will&help%to%revise%the%long%term%strategy%that&will&ul7mately&cover&the&en7re&country&and&range&of&crops&

&Ra7onale&for&the&&long&term&strategy&! Ethiopia&is&likely&to&rely&on&the&agricultural§or&as&a&source&of&income&and&employment&for&the&foreseeable%future%%requiring%op)mal%and%up%to%date%fer)lizer%recommenda)on%packages&for&all&crops&given&the&fact&that&increasing&small&holder&farmers’&produc7vity&entails&the&integra7on&of&improved&technology&and&adop7on&

&&&

Two&approaches,&consis7ng&of&longer&term&controlled&trials&and&immediate&results&driven&trials&for&major&crops&in&the&short&term,&are&being&taken&to&address&these&issues&

21&

Some&objec7ves&of&the&soil&test&based&fer7lizer&recommenda7on&efforts&

1

2

3

4

To%develop%guideline%for%fer)lizer%advice%based%on%soil%test%and%crop%response%to%fer)lizers%on%representa)ve%soils%in%different%agroNclima)c%regions%of%the%country%%

To%derive%a%basis%for%fer)lizer%recommenda)ons%%for%desired%yield%targets%suited%to%the%constraints%of%fer)lizer%availability,%seasonal%variability%and%availability%of%credit%to%farmers%%%

Forecas)ng%and%monitoring%the%emergence%of%nutrient%deficiencies%in%areas%of%exploi)ve%agriculture%through%nutrient%indexing%in%wellNdefined%soilNcropNmanagement%systems%in%different%agroNecological%zones%%%%To%iden)fy%sustainable,%profitable%fer)lizer%technology%packages,%with%siteNspecific%recommenda)ons%within%a%GIS%oriented%cropNmodel%framework%%%%

12/17/13&

8&

22&

The&strategy&tries&to&employ&a&sequence&of&approaches/methods&for&assessing&crop&nutrient&requirements&&&&

Diagnosis%of%fer)lizer%requirements%%

Soil%test%/%crop%response%calibra)on%

Integrated%inorganic%and%organic%fer)lizers%

! Several&approaches&are&employed&for&assessing&crop&nutrient&requirement&including:&! Soil%analysis:%a&model&used&to&predict&and&evaluate&soil&fer7lity&via&soil&nutrient&extrac7on&methods&&! Plant%)ssue%analysis:&this&method&assumes&that&plant&growth&is&restricted&when&the&concentra7on&

of&nutrient&in&plant&7ssue&drops&below&“cri7cal&levels”&! Nutrient%deficiency%symptoms:%%this&method&will&help&iden7fy&the&symptoms&that&plants&exhibit&

when&a&nutrient&is&present&in&insufficient&quan77es&for&normal&growth&! Diagnosis%by%fer)lizer%addi)ve/graded%doses:&used&to&determine&the&fer7lizer&rate&at&which&

economic&crop&yield&can&be&obtained&through&filed&experiments&&&&&&&%

(

(

(

2.1%Calibra)on%! Soil&nutrient&supply&levels&are&calibrated&to&crop&response;&response&categories&determined&through&

conduc)ng%different%fer)lizer%response%experiments%at%different%soil%test%levels&2.2:%Recommenda)on%! Based&on&the&calibra)on%categories,%fer)lizer%recommenda)ons%are%developed%for%each%response%

category%by%also%including%such%considera)ons%as%farmers’%ability%to%access%credit%and%markets.&These&recommenda7ons&will&later&be&integrated&with&op7mal&soilScrop&fer7lizer&applica7ons&to&determine&economical&op7ma&and&viable&fer7lizer&applica7on&recommenda7ons&per&site&&&&

! The&op)mal%integra)on%of%organic%and%inorganic%fer)lizers%for%specific&agroSecologies&and&crop&types&will&also&be&integrated&in&the&op7mal&inorganicSorganic&soil&test&based&fer7lize&recommenda7on&development&effort&&&&&&

Approaches%% Descrip)on%

23&

The&implementa7on&of&soil&test&based&fer7lizer&recommenda7ons&will&consist&of&five&key&implementa7on&areas&&&

Implementa)on%areas%%

Implemen)ng%organiza)ons%

Representa)ve%domain%defini)on%

FineNtuning%fer)lizer%blend%formula%

Soil%test%crop%response%calibra)on%

Forecas)ng%fer)lizer%response%

Monitor%long%term%change%

! Data%compila)on:&Collec7on&of&data&from&exis7ng&maps&and&reports&

! Delineate%areas%:&Iden7fy&soil&and&climate&mapping&units&and&overlay&with&crop&produc7on&units&

! Develop%domains:&Map&biophysical&units&overlaying&this&map&and&develop&agroecological&units&&&&&&

! Valida)on:&Validate&soil&fer7lity&map&based&fer7lizer&blend&formula&recommenda7on&for&N,&P,&K,&B,&Zn,&S,&and&Cu&to&validate&site&specific&responses&&&

! Op)mal%nutrient%iden)fica)on:&Conduct&omission&plot&trails&to&determine&appropriate&nutrient&combina7on&fer7lizer&formulas&

( ( ( ( (

! Data%compila)on:&Conduct&measurements&of&crop&yield&response&to&rates&of&applied&nutrients&and&soil&test&for&the&nutrients&&

! Crop%yield%results:%Iden7fy&the&“Percent&Rela7ve&Yield”&&plot&response&curves&

! Interpreta)on:%Interpret&results&of&soil&test&to&yield&response&

! Determine%nutrient%requirement%factor&

! Data%compila)on:&collect&all&relevant&data&sets&including&soil,&crop&response&and&biophysical&informa7on&&

! Grouping:%Iden7fy&and&group&trial&sites&with&similar&characteris7cs&

! Model%development:%Iden7fy&models&to&capture&all&relevant&informa7on&and&extrapolate&the&result&to&a&wider&set&of&agroSecologies&

! Area%iden)fica)on:%Iden7fy&benchmark&sites&that&could&serve&as&long&term&monitoring&sites&

! Follow%up:&Conduct&soil&test&based&fer7lizer&recommenda7ons&to&monitor&change&&

! Update%recommenda)on:&update&fer7lizer&recommenda7ons&based&on&need&&&

Federal Democratic Republic of Ethiopia MOA&

! Development%partners%

! RARI’s%

CONCLUSION&

# Ethiopia& is& using& a& mul7Spronged& approach& to&increase&the&produc7vity&of&smallholder&agriculture&# Soil&fer7lity&mapping&# Fer7lizer&blending&facili7es&# SiteS&and&cropSspecific&fer7lizer&recommenda7ons&

# Preliminary& trials/demonstra7ons& show& promising&results&and&farmer&interest&

# Agricultural& produc7on& in& Ethiopia& will& significantly&shis& from& blanket& use& of& DAP& and& Urea& to& siteSspecific&use&of&a&more&complete&set&of&nutrients&

24&

12/17/13&

1&

IFDC

Policies to facilitate fertilizer blending for better recommendations

John Wendt Peter Heffernan Maria Wanzala

Paul Makepeace

Why$is$fer*lizer$blending$important?$

Different$crops$require$different$nutrients$in$different$quan**es$

IFDC

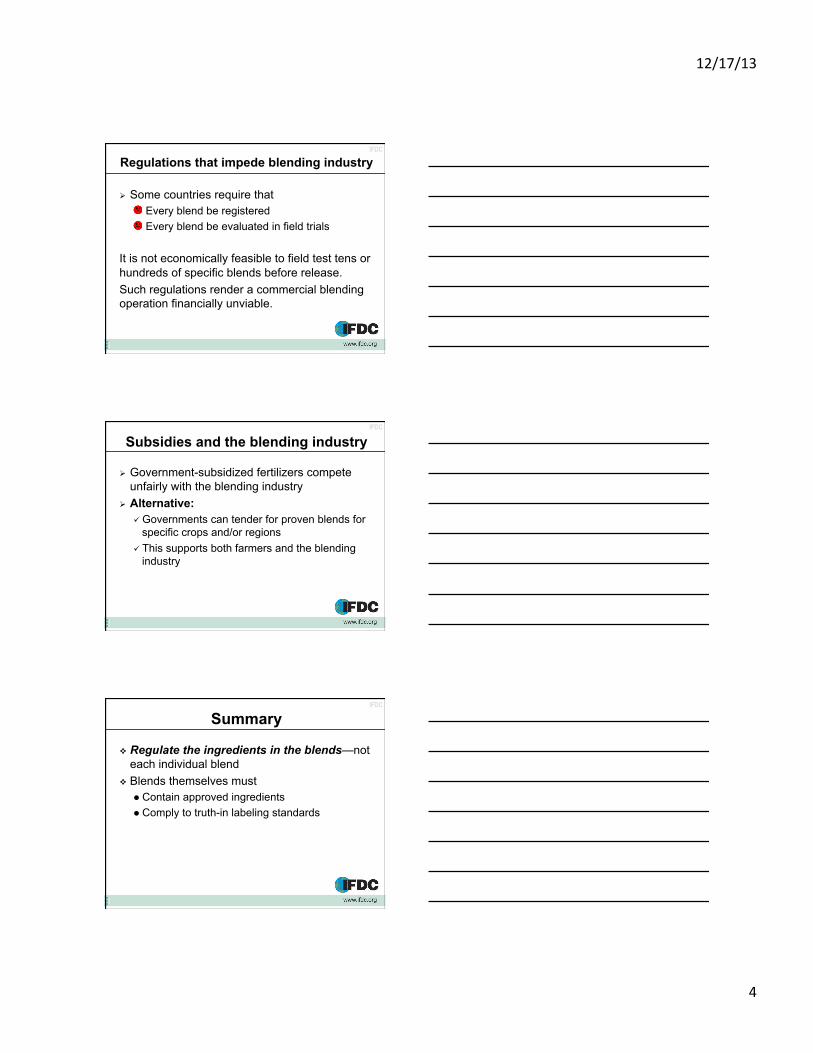

Soils vary in their ability to supply nutrients

0 kg K/ha

30 kg K/ha

60 kg K/ha

0 kg N/ha

30 kg N/ha

50 kg N/ha

70 kg N/ha

Burundi: N and K fertilizers required for 5 tons/ha maize yield

12/17/13&

2&

IFDC Blended fertilizers consider:

! Specific crop requirements

! Soil nutrient supply ! Yield potential (based

on climate, farmer goals)

...to optimize yields and profits

IFDC

Blending in the SSA context

! Many countries have only approved N, P, and K fertilizers

! Other nutrients ( e.g., Mg, S, Zn, B) may limit NPK response

! Countries must address deficiencies of all nutrients in order to optimize yields and realize best economic returns to fertilizers

NPK& NP&+&S,&Zn,&B&

Mozambique:$$Deficiencies$of$S,$Zn,$and$B$limit$NPK$response$

12/17/13&

3&

IFDC

What do commercial blenders do?

! Mix registered fertilizer ingredients for sale ! Mix fertilizer ingredients in response to

tenders and orders ! Some provide soil analytical services and

advice on blend formulations according to soil and crop requirements

! Often work with national and international research organizations to test and improve fertilizers

IFDC

What do commercial blenders do?

" A blender may have access to over 30 registered base fertilizer ingredients

" Active blenders may create hundreds of distinct blends annually

IFDC

Necessary blending regulations

! Registration of competent blending companies

! Registration of ingredients that go into blends " Minimum percentages of nutrients " Limits of contaminants (e.g., cadmium)

! Truth-in-labeling: " Percentages of nutrients in the blend specified " Specified percentages fall within pre-

determined limits

12/17/13&

4&

IFDC

Regulations that impede blending industry

! Some countries require that " Every blend be registered " Every blend be evaluated in field trials

It is not economically feasible to field test tens or hundreds of specific blends before release. Such regulations render a commercial blending operation financially unviable.

IFDC

Subsidies and the blending industry

! Government-subsidized fertilizers compete unfairly with the blending industry

! Alternative: " Governments can tender for proven blends for

specific crops and/or regions " This supports both farmers and the blending

industry

IFDC

Summary

# Regulate the ingredients in the blends—not each individual blend

# Blends themselves must $ Contain approved ingredients $ Comply to truth-in labeling standards

12/17/13&

5&

IFDC

Summary A vibrant blending industry

" Supports fertilizer research " Encourages rapid innovation to improve

fertilizer formulations " Improves returns to fertilizer investments " Increases national production

A positive regulatory environment is key to realizing the potential of fertilizer blending.

Thanks for listening!

12/17/13&

1&

www.afap&partnership.org0

&&&&&0

0

0

0

0

0

0

Agribusiness0Partnership0

Contracts00&

&

&0&&&

&&

December0020130

www.afap&partnership.org0

Agribusiness0Partnership0

Contracts0(APCs)0

The0AFAP0Program0–0December020130

In&return&for&AFAP&assistance:&1. Guarantees&and&financing&

assistance&2. Matching&grants&for&

improved&storage&3. Technical&assistance&and&

training&Businesses0make0a0development0commitment0above0and0beyond0the0company’s00regular0course0of0business0

&

www.afap&partnership.org0

Agribusiness0Partnership0

Contracts0(APCs)0

Current&APC&&pipeline&in&Ghana,&Mozambique&and&Tanzania:&& 920Agribusiness0Partner0

Contracts0

648,8100MT0of0FerOlizer0

Valued0at0$05470Million0

Reaching07,371,1180farmers00

0The0AFAP0Program0–0December020130

12/17/13&

2&

www.afap&partnership.org0

.0

.&

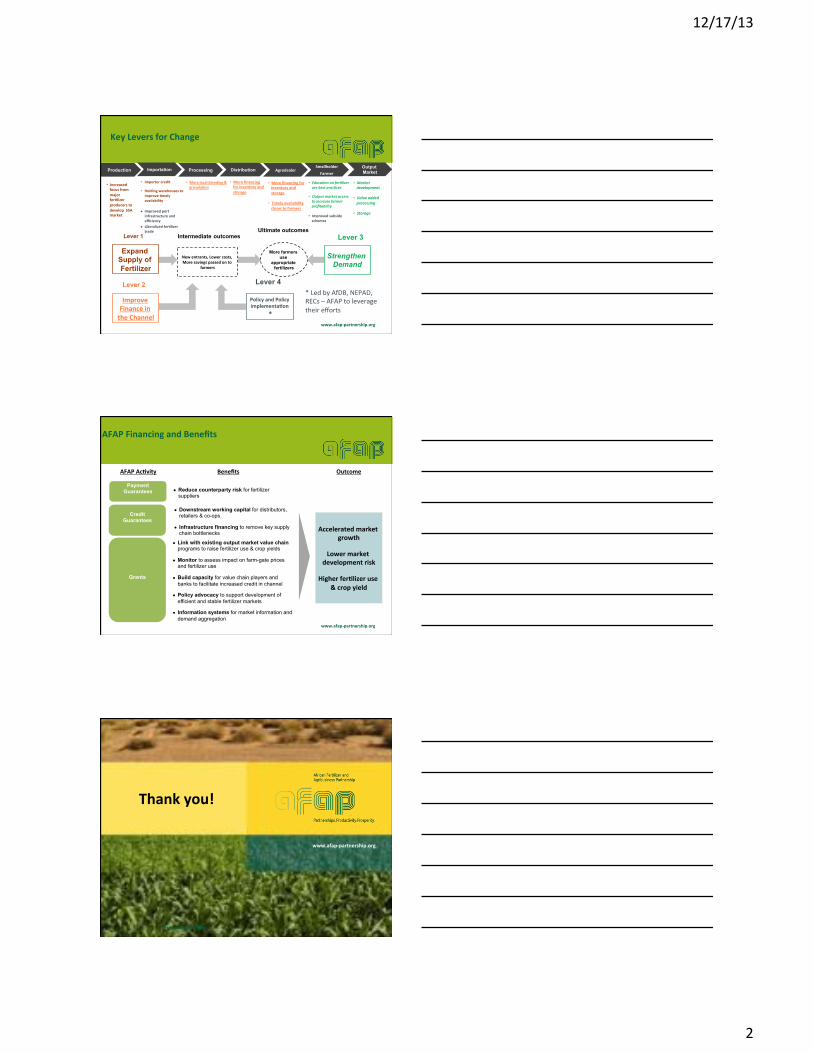

Key0Levers0for0Change00

Production Processing Distribution Agrodealer0Smallholder0

Farmer0

Output Market

Importer0credit0

Holding0warehouses0to0

improve0Omely0

availability0

! Improved0port0

infrastructure0and0

efficiency0

! Liberalized0ferOlizer0

trade0

Importation

Increased0focus0from0

major0ferOlizer0

producers0to0

develop00SSA0market0

More0financing0for0inventory0and0

storage0

More0local0blending0&0

granulaOon0 More0financing0for0inventory0and0

storage0

Timely0availability0

closer0to0farmers0

Educa&on)on)fer&lizer)use)best)prac&ces)

Output)market)access)to)increase)farmer)profitability)

Improved0subsidy0

schemes)

Market)development)

Value)added)processing)

Storage)

Strengthen Demand

Expand Supply of Fertilizer

Improve0Finance0in0

the0Channel

New0entrants,0Lower0costs,0More0savings0passed0on0to0

farmers0

More farmers use

appropriate fertilizers

Intermediate outcomes Lever 1 Lever 3 Ultimate outcomes

Lever 2

Policy0and0Policy0implementaOon0

*0

Lever 4

4&

*&Led&by&AfDB,&NEPAD,&RECs&–&AFAP&to&leverage&their&efforts&

www.afap&partnership.org0

.0

.&

.0

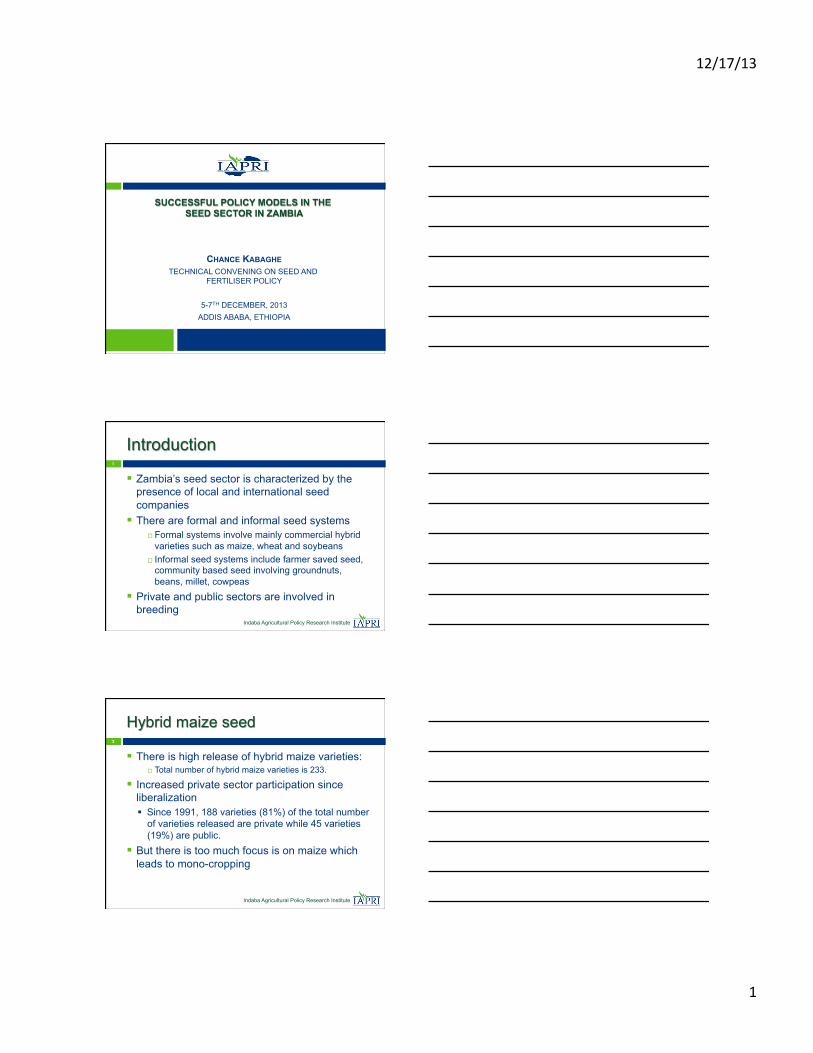

Payment Guarantees

AFAP0Financing0and0Benefits00

Grants

Accelerated0market0growth0

Lower0market0development0risk0

Higher0ferOlizer0use0

&0crop0yield0

! Reduce counterparty risk for fertilizer suppliers

Credit Guarantees

AFAP0AcOvity0 Benefits0 Outcome0

! Downstream working capital for distributors, retailers & co-ops

! Infrastructure financing to remove key supply chain bottlenecks

! Link with existing output market value chain programs to raise fertilizer use & crop yields

! Monitor to assess impact on farm-gate prices and fertilizer use

! Build capacity for value chain players and banks to facilitate increased credit in channel

! Policy advocacy to support development of efficient and stable fertilizer markets

! Information systems for market information and demand aggregation

5

www.afap&partnership.org0

Thank0you!0

PresentaOon0Title0

12/17/13&

1&

&&&&&&&&&&&&&&&

Seed&Policy:&Examples&of&engaging&the&private§or:&Dialogue,&Licensing,&and&Certification&&

&

Jitu&Shah&

AFSTA&President&

The&process&starts&with&the&Identification&of&Key&Players&

Government&Ministries&

Government&AgenciesM&Regulators&

Farmers&

Seed&Merchants&

Research&Institutions&/&Breeders&

Consumers&/&NGO’s&

Seed&Producers&

Policy&Framework&

Policy&&– DrivesMlegislation&&

In&Kenya&The&National&Seed&Policy&is&implemented&&through:M& Seed&and&plant&varieties&act& Plant&protection&act& Suppression&of&noxious&weed&act& Pest&control&act& National&BioMSafety&act&

&

12/17/13&

2&

Legislation&operational&through:M&&

Regulations&– In&Kenya&there&are&

Regulations&&on&National&variety&Release& National&performance&Trials& Regulations&governing&&packaging&of&seed& Plant&import®ulations& National&BioMSafety®ulations&

And&host&of&subsidiary®ulations&detailing&&specific&areas&of&seed&trade& Additional&to&the®ulations&are&published&procedures&and&timelines&for&the&conduct&of&seed&related&business.&

Under&the&Rapid&result&initiative&Govt.&agencies&have&service&level&agreements&with&stakeholders&to&ensure&efficiency.&

&Kenya&Model&

G&O&K&M&Policy&and&legislation& KEPHISM&Regulatory&agency&specifically&for&seed&and&plant&materials.&&

KARI/&KEFRIM&Research&institutions&involved&in&basic&research&and&custodians&of&public&genetic&materials&

KBSM&Government&standards&agency&for&manufacturing& NBAM&Responsible&for&bio&safety®ulation& STAKM&&Seed&Trade&Association&representing&all&seed&industry& KAM&–&Trade&Association&of&Manufactures&in&Kenya&

Kenya&

GOK$Policy$legislation$and$

Regulation$

$KEPHIS,$GOK$Agencies$STAK,$

KAM,$Stakeholder$NGO’s$&

Farmers,$Seed$Traders,$Merchants$

12/17/13&

3&

KEPHISM&Kenya&Plant&health&Inspectorate&services&

Main&agency&responsible&for&Plant&and&Variety&protection&in&Kenya.&Supervisor&and®ulator&for&seed&business.&&

Conducts&NPT’s&and&is&Secretariat&to&the&National&Variety&Release&committee.&

Responsible&for&Seed&certification&

&&&&&&SEED&CERTIFICATION&

KEPHIS&(Govt.&Agency)&is&responsible&for&seed&certification.&– Human&/Technical&resource&Capacity&– Level&playing&field&– Sets&Standards&– International&recognition&(UPOV)&

There&is&a&push&for&self®ulation&but&there&are&challenges:&– Human&capacity&in&private&seed&companies&– International&and&Regional&seed&trade&&– Policing&– Consumer&protection&

&&&&STAKM&Seed&Trade&Association&of&Kenya&

Member&association&for&all&Seed&Stakeholders.&

Represents&the&stakeholder&in®ional&and&international&forums.& Member&of&the&NPT&and&National&Variety&Release&committee.&

Involved&in&development&and&review&of&national&seed&policy&and&attending&to&seed&legislation&and®ulations&

Key&contact&for&seed&industry&to&dialogue&with&government&and&other&stakeholders.&

Organizes&Annual&congress&for&all&stakeholders&to&deliberate&on&matters&in&the&industry.&

12/17/13&

4&

&&Kenya&&seed&acts&review& National&seed&policy&launched&in&July&2011&

Support&legislation&&– Seed&and&plant&varieties&act&2011&

NPT®ulations&2013& Seeds®ulations&2013& Plant&Breeders&Rights®ulations&2013.&

Regulations&review&is&ongoing&¤tly&expected&to&be&finalized&this&week&(49)&and&gazetted&to&operationalize&the&act&by&15th&January&2014.&The&process&is&consultative&and&has&taken&a&long&time.&

&&&&&Consultations&on&the&Process&&

STAK&& Brings&together&all&stakeholders&in&the&seed&and&agribusiness§or&to&deliberate&on&issues&affecting&the&industry& Quarterly&meeting&of&STAK&executive&committee.& Review&STAK&activities& Deliberate&on&matters&touching&on&members& Participation&in&Farmer&Field&days&with&government:&

Issues&raised&are&jointly&owned,&addressed&and&solutions&sought.&

STAK&is&member&of®ional&trade&and&agribusiness&bodies&

Stakeholder&forums&

Periodic&sponsored&forums&and&workshops&on&matters&touching&seed&and&seed&production&where&government&and&other&agencies&were&invited.&– E.g.&Agri&Experience&(an&NGO)&in&Kenya&has&held&3&stakeholder&forums&where&the¤t®ulation&on&the&new&seed&and&plant&varieties&act&have&been&reviewed&before&presentation&to&parliament.&The&Ministry&of&Agriculture&and&a&legal&drafter&from&the&AG’s&office&was&present&to¬e&the&suggested&amendments.&

12/17/13&

5&

&&KARIM&Kenya&Agricultural&Research&Institute&

Govt.&research&institute&mandated&to&conduct&basic&research&in&food&crops,&horticultural&and&industrial&crops,&livestock&and&range&management.&

Custodian&of&public&genetic&materials&available&on&license&to&private§or&for&commercialization.&

Repository&of&agricultural&research&findings.&

&&&&Publicly&developed&varieties&

KARI&offers&varieties&under&license&to&private&companies&for&commercialization.&

– Open&Bids&after&variety&release&for&exclusive&use&&of&materials&for&&a&set&term&

– Private&M.O.U&for&commercialization&and&sharing&of&financial&proceeds&

– Outright&acquisition&of&variety.&&

&&&&Licensing&example&

East&African&Seed&Co.&acquired&exclusive&license&for&it’s&KH&600&15A&and&KH500&43A&maize&variety&from&KARI.&This&has&been&multiplied&by&the&company&and¤tly&on&commercial&sale&in&East&Africa.&

&The&financial&sharing&arrangement&are&entered&into&under&&&&&&&&&&an&MOU&and&the&costs&will&be&absorbed&in&the&pricing.&&

The&effect&on&pricing&of&the&seed&is&minimal&as&the&alternative,&development&of&own&varieties&is&usually&more&expensive&

12/17/13&

6&

SUBSIDY&

Kenya&Seed&company&is&Govt.&owned&and&gets&subsidized&in&its&operation&from&the&Treasury.&There&is&no&formal&subsidy&program&for&seed.&

Fertilizer&subsidy&are&through&the&National&cereals&and&produce&board,&this&is¬&a&formalized&subsidy&as&it&targets&mainly&maize&growers&and&is¬&wide&reaching.&– The&Malawi&example&through&STAM&model&appears&the&workable&model&&&

&&&&Challenges& Government&Policy&/&Subsidies&– Govt.&is&a&major&player&in&seed&trade.&

Distorts&pricing&and&competition&

– Management&of&subsidy&program&&

– Self®ulation& Seed&certification&–&industry&human&capacity&&challenge& Counterfeit&Seed&(Fake&seeds&policing)& Intellectual&Property&protection&

Low&Hybrid&seed&uptake&&&

&&&&&Summary&

National&Seed&policy&driven&by&consultation&with&key&stakeholders.&

Legislation&and®ulations&for&fair&and&level&playing&field.& National&association&of&seed&stakeholders&is&important&to&ensure&representation.&

Private&/Public&partnership.&

12/17/13&

1&

Indaba Agricultural Policy Research Institute

SUCCESSFUL POLICY MODELS IN THE SEED SECTOR IN ZAMBIA

CHANCE KABAGHE TECHNICAL CONVENING ON SEED AND

FERTILISER POLICY

5-7TH DECEMBER, 2013 ADDIS ABABA, ETHIOPIA

Indaba Agricultural Policy Research Institute

1

Introduction

! Zambia’s seed sector is characterized by the presence of local and international seed companies

! There are formal and informal seed systems " Formal systems involve mainly commercial hybrid

varieties such as maize, wheat and soybeans " Informal seed systems include farmer saved seed,

community based seed involving groundnuts, beans, millet, cowpeas

! Private and public sectors are involved in breeding

Indaba Agricultural Policy Research Institute

2

Hybrid maize seed

! There is high release of hybrid maize varieties: " Total number of hybrid maize varieties is 233.

! Increased private sector participation since liberalization ! Since 1991, 188 varieties (81%) of the total number

of varieties released are private while 45 varieties (19%) are public.

! But there is too much focus is on maize which leads to mono-cropping

12/17/13&

2&

Indaba Agricultural Policy Research Institute

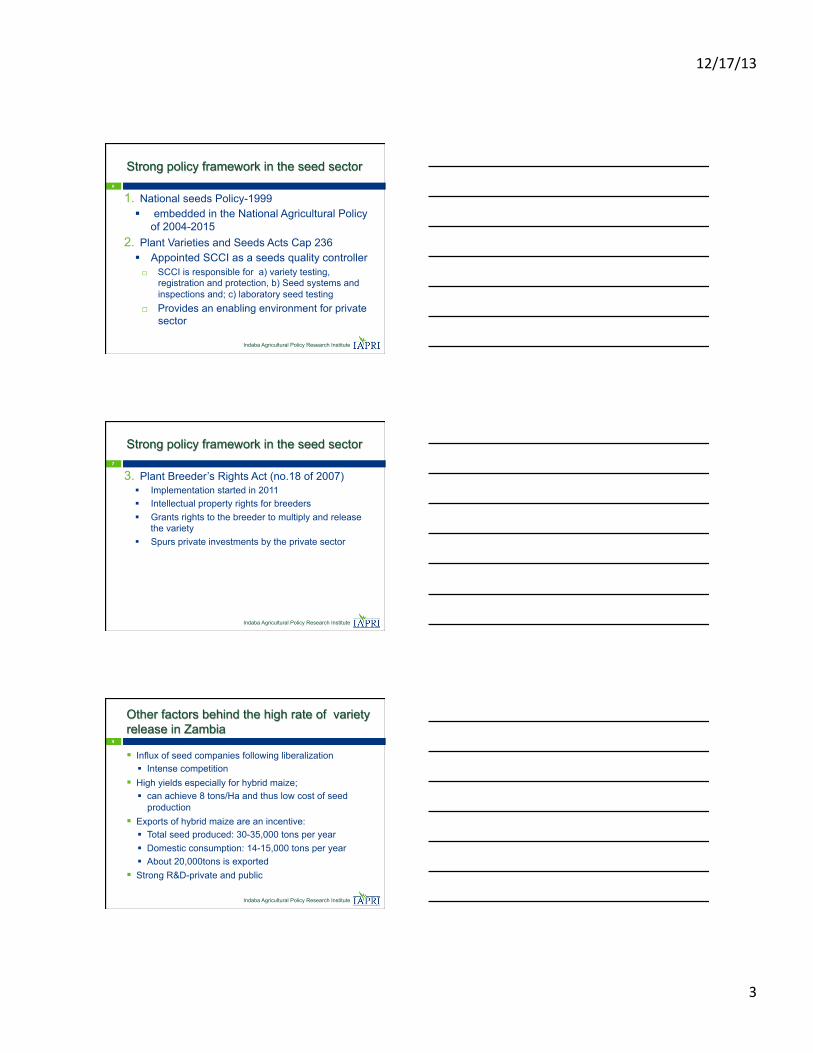

Hybrid maize seeds released in Zambia 3

Period Total varieties released

Public Private

1960-1990 16 16 0 1991-2000 66 14 52 2001-2010 121 7 114 2011-2013 30 8 22 Total 233 45(19%) 118(81%) Source'of'data:'Seed'Control'and'Cer0fica0on'Ins0tute,'Zambia ! There are about 20 formal private seed companies and

over 40 community based NGOs involved in seed ! Government through the Zambia Agricultural Research

institute (ZARI) is also involved in breeding

Indaba Agricultural Policy Research Institute

4

Other important food crops

Crop Total number of varieties released

Public varieties

Private Varieties

Wheat 48 24 24 Sorghum 17 15 2 Pearl millet 11 10 1 Finger millet 7 7 0 Rice 17 15 2 Soya beans 36 12 24 Groundnuts 16 12 4

Source'of'data:'Seed'Control'and'Cer0fica0on'Ins0tute,'Zambia

Indaba Agricultural Policy Research Institute

5

Other important food crops…ctd

! Wheat and soya beans mainly for commercial farmers

! Millet, sorghum, rice, groundnuts are characterized by informal seed systems ! Supported by NGOs and public breeding ! Low interest by commercial seed companies

12/17/13&

3&

Indaba Agricultural Policy Research Institute

6

Strong policy framework in the seed sector

1. National seeds Policy-1999 ! embedded in the National Agricultural Policy

of 2004-2015 2. Plant Varieties and Seeds Acts Cap 236

! Appointed SCCI as a seeds quality controller " SCCI is responsible for a) variety testing,

registration and protection, b) Seed systems and inspections and; c) laboratory seed testing

" Provides an enabling environment for private sector

Indaba Agricultural Policy Research Institute

7

Strong policy framework in the seed sector

3. Plant Breeder’s Rights Act (no.18 of 2007) ! Implementation started in 2011 ! Intellectual property rights for breeders ! Grants rights to the breeder to multiply and release

the variety ! Spurs private investments by the private sector

Indaba Agricultural Policy Research Institute

8

Other factors behind the high rate of variety release in Zambia

! Influx of seed companies following liberalization ! Intense competition

! High yields especially for hybrid maize; ! can achieve 8 tons/Ha and thus low cost of seed

production ! Exports of hybrid maize are an incentive:

! Total seed produced: 30-35,000 tons per year ! Domestic consumption: 14-15,000 tons per year ! About 20,000tons is exported

! Strong R&D-private and public

12/17/13&

4&

Indaba Agricultural Policy Research Institute

Challenges

! Poor rural infrastructure " Long distances for farmers to access inputs

! State interference in maize marketing affects potential maize producers

" Low maize production by commercial farmers affecting demand for seed

! High dependence on rain-fed agriculture ! Fake seed

" Unscrupulous dealers buy commercial maize which they colour and sell as seed

9

Indaba Agricultural Policy Research Institute

10

Conclusions

Zambia has a well developed seed sector with both the private and public sector

The factors behind the high release are: ! Strong policy framework ! Strong enforcement through the SCCI ! Influx of private sector companies following

liberalization ! High yields-lowering the costs of seed

production

Indaba Agricultural Policy Research Institute

11

Recommendations

! Strengthen seed harmonization policies in the region

! Strengthen rural informal/community based seed systems

! Strengthen R&D and variety release for crops such as millet, beans, groundnuts, soya beans

12/17/13&

1&

Indaba Agricultural Policy Research Institute

SUCCESSFUL MODELS FOR PROMOTING INPUT ACCESS FOR SMALL SCALE

FARMERS IN ZAMBIA

BRIAN CHISANGA

TECHNICAL CONVENING ON SEED AND FERTILISER POLICY

5-7TH DECEMBER, 2013

ADDIS ABABA, ETHIOPIA

Indaba Agricultural Policy Research Institute

1

Outline

! Introduction ! Overview of FISP ! Why FISP has not delivered ! Models for enhanced input access among

small scale farmers ! The E-voucher system ! The Lima credit scheme ! Private sector models-Cargill Zambia

! Conclusion and recommendations

Indaba Agricultural Policy Research Institute

2

Introduction

! The major distribution channel for seed and fertiliser for the last decade is FISP

! FISP accounts for 200,000mt or 67% of the national fertiliser requirement for Zambia

! Complementary models of input distribution: ! Led by private sector , farmers’ union, NGOs

among others ! We highlight outcomes of FISP and present

successful models

12/17/13&

2&

Indaba Agricultural Policy Research Institute

3

Overview of FISP

! The main focus of FISP is to: ! Increase maize production through provision of

seed and fertiliser and ! Create an environment for private sector input

supply chains to develop

Indaba Agricultural Policy Research Institute

Overview of FISP…ctd

! 48,000 Mt of fertiliser

! 100,000 beneficiaries

! Input pack per hh: 8*50kg

! Subsidy rate: 50%

! 183,000 Mt of fertiliser (2012/13)

! 900,000+ beneficiaries

! Input pack per hh: 4*50kg

! Subsidy rate:50%

FSP at inception 2002/3 season FISP at present

4

Indaba Agricultural Policy Research Institute

5

Why FISP has not delivered

! Despite increasing aggregate maize production FISP has not delivered as a PRP

! Rural poverty remains high-about 80% ! Reasons:

" Poor targeting of farmers " Delays in distribution " Leakages " Crowding out of private sector " Lack of an exit strategy for farmers " Low fertilizer use efficiency

12/17/13&

3&

Indaba Agricultural Policy Research Institute

Models for enhanced input access among small scale farmers

! Innovative models promoting input access by farmers and private sector growth " E-vouchers –government, FAO and CFU " Lima credit scheme involving ZNFU, Zanaco and

private seed and fertiliser companies " Private sector led models such as Cargil

! Promotes private sector development, rural agro-networks and minimize government spending

6

Indaba Agricultural Policy Research Institute

1. E-voucher system-pilot

! The Zambian government is yet to pilot an e-voucher system

! FAO/CFU piloted an e-voucher project " Covering 37 districts, 55,812 beneficiaries, and 107

agro-dealers ! Reluctance by govt to pilot e-vouchers:

" agro-dealer networks are not adequately developed and capitalised

" Implementation failure and consequences on food security

! May be piloted in the 2014/15 season

7

Indaba Agricultural Policy Research Institute

E-voucher-how it works

! A web-based system accessible on mobile phones

! Realtime registration of beneficiaries and electronic payments of retailers

! Beneficiaries receive a voucher scratch card ! Voucher is redeemed at the nearest retail

outlet ! Agro-dealer receives instant payment through

online account

8

12/17/13&

4&

Indaba Agricultural Policy Research Institute

Benefits of E-vouchers

! E-vouchers address the challenges of FISP: ! Leverage private sector participation ! Reduce costs associated with current FISP –

administrative cost " E-voucher-5% of subsidy budget " Current FISP-35%

! Reduces delays in implementation by reducing tendering

! Farmers have a choice of inputs

9

Indaba Agricultural Policy Research Institute

2. Lima credit scheme

! Provides seed and fertilizer to small scale farmers on loan

! Interest rate: 14% ! Farmers pay 50% upfront and 50% after harvest ! Crops supported: maize and soya beans ! Stakeholders

! ZNFU ! Zanaco ! Seed and fertilizer companies

10

Indaba Agricultural Policy Research Institute

Lima credit scheme…ctd 11

! Present in10 provinces, 41 districts ! Covers 10,596 beneficiaries ! Loan consists of:

! 25 kg seed ! 8*50 kg bag fertiliser

! Beneficiaries identified through contact farmers at information centres

! Extension services provided at information centres

12/17/13&

5&

Indaba Agricultural Policy Research Institute

Lima credit scheme model

12

Contact Farmer

District Farmers Association

Farmer

ZNFU Secretariat

Zanaco Input Suppliers /Service Providers

Indaba Agricultural Policy Research Institute

Lima credit scheme growth trajectory

Season! No. of farmers!

hectarage! DFA! Approved Limit!ZMW!

Utilization of Limit

ZMW!2008/09& 600 600 2 2,000,000 309,000

2009/10& 1,334 2,229 10 4,000,000 3,068,000

2010/11& 1,511 3,320 18 8,000,000 5,090,000

2011/12 4,026 10,088 25 20,000,000 17,484,031

2012/13 10,596 21,508 38 65,000,000 38,175,810

Indaba Agricultural Policy Research Institute

Productivity of scheme beneficiaries 14

Season Yield/ha (tons)

Average ha/farmer

Recovery

2008/09 1.75 1 100% 2009/10 2.5 1.7 98.3% 2010/11 2.5 2.2 - 2011/12 2.7 2.5 - 2012/13 3.2 2.1 100%

12/17/13&

6&

Indaba Agricultural Policy Research Institute

3. Private sector model-Cargill Zambia

! Provides inputs on credit for maize production " For farmers involved in cotton contract farming

! Inputs include: " 10 kg hybrid seed " 4*50kg fertiliser

! Present 10 districts of Eastern Province ! 70,000 households growing cotton and maize ! Payback at harvest ! Recovery rate: 80%

15

Indaba Agricultural Policy Research Institute

3. Private sector model-Cargill Zambia…ctd ! Productivity increased with promotion of CA ! Extension services provided: 150 extension

services

16

Indaba Agricultural Policy Research Institute

Conclusion

! Government led input distribution models have several shortcoming ! Rural poverty rates have remained high ! Can be improved through e-vouchers

! Private models operate more efficiently ! higher yields, production and high loan recovery ! Effective extension systems ! Diversification in production

17

12/17/13&

7&

Indaba Agricultural Policy Research Institute

Recommendations

! Implementation of e-vouchers by the public model

! Create supportive environment for private sector and NGOs models of input distribution to small scale farmers

18

Indaba Agricultural Policy Research Institute

THANK YOU! 19

12/17/13&

1&

Fer*lizer&policy&in&Rwanda:&promo*ng&use,&priva*zing&

trade&&

Presenta*on&to:&Technical&Convening&on&Agricultural&Inputs&Policy&in&Africa&5G7&December&2013,&Addis&Ababa&

By:&David&Gisselquist,&IFDc&

Geography:&long,&costly&transport&

DarGesGSalaam&to&Kigali&– 1,700&kms,&$160/ton&

Mombasa&to&Kigali&– 1,700&kms,&$160/ton&

BUT…imported&agric’l&products&(eg,&rice)&pay&the&same&high&transport&costs&SO…&for&many&crops,&rates&of&return&to&fer*lizer&use&are¬&hurt&by&high&transport&costs&&

Geography:&arable&land/capita&

Popula*on& 11,000,000&

Arable&land& &&1,000,000&ha&

People&per&arable&hectare&

11&

Average&farm&size&per&agric’l&household&

0.5&ha&

12/17/13&

2&

Low&fer*lizer&use&through&2005&

Through&&1980s:&FAO,&GoR&extension,&no&private§or&(1#3%kg/ha)% 1994G1998:&distribu*on&free&or&with&gov’t&

credit,&repayment&low&(2#4%kgha)% 1999G2005:&GoR&gets&out,&removes&import&

du*es,&urges&private&trade,&World&Bank&subsidized&credit&for&importers&(5#6%kgs/ha)%

Priva5zed,%liberalized,%but%use%far%too%low!%What%to%do?%

2007G2012:&S*mula*ng&demand&NOTE:%This%table%applies%only%to%%subsidized%fer5lizers.%Private%traders%import%and%distribute%5,000%tons%of%unsubsidized%fer5lizers,%mostly%for%tea,%coffee%

Extension%to%s5mulate,%educate%farmer%demand%%

Fer5lizer%vouchers%linked%to%intensive%effort%to%promote%specific%food%crops%

Who&imports?& GoR&

Who&distributes?& Private&distributors,&assigned&districts&

Subsidies?& Transport&&from&port&+&targeted&voucher&

Targeted&&credit?& To&distributors,&dealers,&farmers&

Who&sets&prices?& GoR&

Use:&kg/ha& 30&kg/ha&

Low&fer*lizer&use&through&2005&

12/17/13&

3&

2007Gtoday:&gecng&it&right&

Focused&extension&program,&promo*ng&highGyields&for&specific&crops:&hybrid&maize,&potatoes,&rice,&wheat& Government&imports,&but&from&&&&

Latest&policy&changes& 2013:&– GoR&gets&out&of&fer*lizer&imports&for&subsidy&program&– GoR&stops&targeted&fer*lizer&credit&to&distributors,&farmers&– GoR&consolidates&subsidies&in&targeted&vouchers&

2014?&– GoR&wants&eGvouchers&for&easier&monitoring&to&ensure&

subsidized&fer*lizer¬&exported&– his&can&be&done&with&mFarms&smartGphone&repor*ng&by&

importers,&distributors,&agriGdealers&– With&beeer&tracking&of&fer*lizers&sold&against&vouchers,&GoR&can&

allow&anyone&to&import&and&sell&against&vouchers& Compe**ve&markets& price&controls¬&needed& new&products&

Rwanda&relies&on&a®ional&market&Regional)market)thru)Dar)es)Salaam)and)Mombasa)Kenya:&&&&&&&&&&&&&&&&&&500,000&mt&Tanzania:&&&&&&&&&&&&&250,000&&mt&&&&&&&Uganda:&&&&&&&&&&&&&&&&&45,000&mt&Rwanda:&&&&&&&&&&&&&&&&35,000&mt&Burundi:&&&&&&&&&&&&&&&&40,000&mt&So&Sudan:&&&&&&&&&&&&&&minor&Eastern&DRC:&&&&&&&&minor&&Total:&&&&&&&&&&&&&&~&900,000&mt&

12/17/13&

4&

Lots&leh&to&do:&expect&progressive&rapid&growth&in&fer*lizer&use&

country& Rwanda& Bangladesh&Popula*on& 11,000,000& 160,000,000&Arable&land& ~&1,00,000&ha& 9,000,000&ha&People&per&arable&hectare&

11& 18&

Fer*lizer&use&(tons/year)&

35,000&tons& 4,000,000&tons&

Fer*lizer&use&(kg/ha)& 35&kgs/ha& 450&kgs/ha&

12/17/13&

1&

12/17/13&

2&

12/17/13&

3&

12/17/13&

4&

12/17/13&

5&

12/17/13&

6&

12/17/13&

1&

!

Addressing&soil&fer2lity&to&maximize&

impact&of&seed&and&fer2lizer&policies&

Richard&B&Jones&

!

Three%important%parameters%affec0ng%fer0lizer%use%(Yanngen%et#al,%1988)%

The&technical&response&to&fer2lizer&use&– Units&of&output&(O)&from&one&unit&of&nutrient&(N)&(the&O/N&ra2o)&

The&rela2onship&between&output&price&and&fer2lizer&price&– Units&of&output&needed&to&purchase&one&unit&of&nutrient&(PN/PO)&

The&valueJcost&ra2o&(VCR)&– (O/N)/(PN/PO)&

!

Value&cost&ra2o&

This&is&defined&as&the&sales&value&of&the&extra&yield&produced&by&using&fer2lizer÷d&by&

the&cost&of&that&fer2lizer.&Normally,&a&VCR&of&

at#least#two&is&considered&necessary,&although&a&VCR&of&this&level&is&risky&if&there&is&a&danger&

of&drought,&disease&or&crop&prices&falling&

12/17/13&

2&

!

What%are%we%trying%to%do?% Fer2lizer&policy&interven2ons&– Reduce&the&cost&of&fer2lizers&through&improved&efficiencies&in&the&supply&chain&

Increase&technical&response&to&fer2lizer&use&– Integrated&soil&fer2lity&management&(ISFM)&defined&as&“The&applica2on&of&soil&fer2lity&management&prac2ces,&and&the&knowledge&to&adapt&these&to&local&condi2ons,&which&op2mize&fer2lizer&and&organic&resource&use&efficiency&and&crop&produc2vity”&(CIAT,&2011)&

Includes&J&but¬&limited&to&J&appropriate&mineral&fer2lizers,&organic&input&management&and&improved&germplasm&

!

pp

Magnesium ppm 143 139 277 Mg 143

Manganese ppm 76 80 250 Mn 76

Sulphur ppm 14 20 200 S 14

Copper ppm 1.09 2.00 10.00 Cu 1.09

Boron ppm 0.34 0.80 2.00 B 0.34

Zinc ppm 9.54 2.00 20.00 Zn 9.54

Sodium ppm 58 < 133 Na 58

Iron ppm 178 150 350 Fe 178

C.E.C meq/100g 11.56 15.00 30.00 C.E.C 11.56

Aluminium ppm 1108 < 1200 Al 1108

EC (Salts) uS/cm 43 < 800 EC(S) 43

PERCENTAGES AND RATIOS

Calcium % % Ca% 51.19 60 72 51.19

Magnesium % % Mg% 10.28 10 20 10.28

Potassium % % K% 6.64 3 8 6.64

Sodium % (ESP) % Na% 2.18 0 5 2.18

Other Bases % % OB% 5.98 3 10 5.98

Hydrogen % % H% 23.73 10 15 23.73

Total 100.00%

Ca:Mg Ratio % Ca:Mg 4.98 4 7 4.98

COMMENTS

> Low pH can cause deficiencies of phosphorus, calcium, magnesium and molybdenum. > Low Ca levels reduces soil microbial activity and as a result,

!

“4R”Nutrient&Stewardship&Framework&

(IPNI)&&

12/17/13&

1&

IFDC

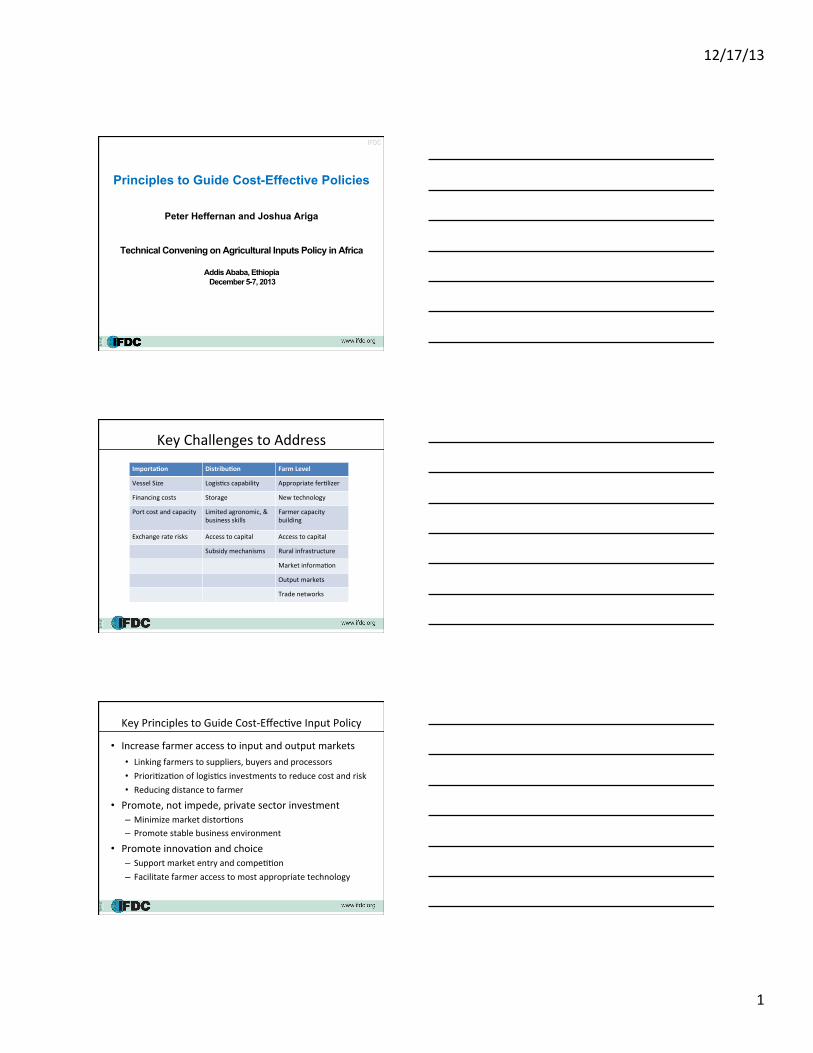

Principles to Guide Cost-Effective Policies

Peter Heffernan and Joshua Ariga

Technical Convening on Agricultural Inputs Policy in Africa

Addis Ababa, Ethiopia December 5-7, 2013

Key&Challenges&to&Address&

Importa(on* Distribu(on* Farm*Level*

Vessel&Size& Logis;cs&capability& Appropriate&fer;lizer&

Financing&costs& Storage& New&technology&

Port&cost&and&capacity& Limited&agronomic,&&&business&skills&

Farmer&capacity&building&

Exchange&rate&risks& Access&to&capital& Access&to&capital&

Subsidy&mechanisms& Rural&infrastructure&

Market&informa;on&

Output&markets&

Trade&networks&

Key&Principles&to&Guide&CostPEffec;ve&Input&Policy&

Increase&farmer&access&to&input&and&output&markets& Linking&farmers&to&suppliers,&buyers&and&processors& Priori;za;on&of&logis;cs&investments&to&reduce&cost&and&risk& Reducing&distance&to&farmer&&

Promote,¬&impede,&private§or&investment&– Minimize&market&distor;ons&– Promote&stable&business&environment&

Promote&innova;on&and&choice&– Support&market&entry&and&compe;;on&– Facilitate&farmer&access&to&most&appropriate&technology&

12/17/13&

2&

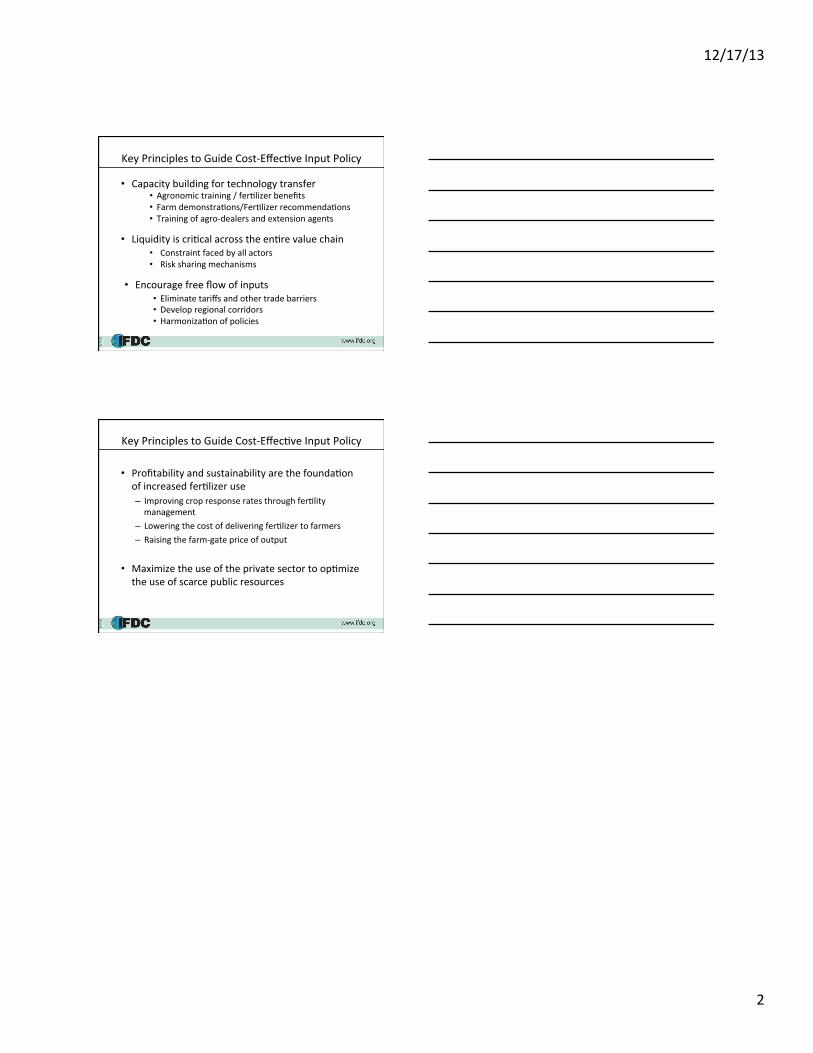

Key&Principles&to&Guide&CostPEffec;ve&Input&Policy&

Capacity&building&for&technology&transfer& Agronomic&training&/&fer;lizer&benefits& Farm&demonstra;ons/Fer;lizer&recommenda;ons& Training&of&agroPdealers&and&extension&agents&&

Liquidity&is&cri;cal&across&the&en;re&value&chain& Constraint&faced&by&all&actors& Risk&sharing&mechanisms&

Encourage&free&flow&of&inputs& Eliminate&tariffs&and&other&trade&barriers& Develop®ional&corridors& Harmoniza;on&of&policies&

Key&Principles&to&Guide&CostPEffec;ve&Input&Policy&

Profitability&and&sustainability&are&the&founda;on&of&increased&fer;lizer&use&&– Improving&crop&response&rates&through&fer;lity&

management&– Lowering&the&cost&of&delivering&fer;lizer&to&farmers&– Raising&the&farmPgate&price&of&output&&&&

Maximize&the&use&of&the&private§or&to&op;mize&the&use&of&scarce&public&resources&

12/17/13&

1&

Input&Subsidy&Programs&in&Sub3Saharan&Africa&

T.S.&Jayne,&Michigan&State&University&&

Technical&Convening&on&Inputs&Policies&in&Africa&December&6,&2013& 1&

Policy&engagement&calendar&date% event% par*cipants% Main%messages%

March&2014&