Embed Size (px)

Citation preview

Teagasc National Farm Survey

2018 Results

Emma Dillon, Brian Moran, John Lennon &Trevor Donnellan

Agricultural Economics and Farm Surveys Department,

Rural Economy Development Programme

ISBN 978-1-84170-653-5

Teagasc National Farm Survey 20182

ACKNOWLEDGEMENTS

The authors wish to thank all who contributed to the Teagasc National Farm Survey

2018 - the farmers who participate voluntarily, the Central Statistics Office who

select the sample and provide the population weights. Grateful acknowledgement

is due to the Teagasc research staff involved in the collection and validation of the

farm data: J. Colgan, A Curley, L. Deane, L. Delaney, P. Harnett, P. Healy, P.

Madden, J. McConnon, E. McGrath, K. McNamara, M. Nicholson, J. Robinson, J.

Teehan and to M. Moloney for the administration of the survey.

Teagasc National Farm Survey 20183

TABLE OF CONTENTS

SUMMARY 2018 5

Weather woes in 2018 6

Family Farm Income 2018 8

FFI Distribution 10

Direct Payments 12

Investment and Borrowings 13

Dairy 2018 15

Regional Dairy Analysis 17

Dairy Structural Change 18

Cattle Rearing 2018 19

Cattle Other 2018 21

Regional Cattle Analysis 23

Sheep 2018 24

Tillage 2018 25

Regional Overview & Off-farm Employment 26

Viability Analysis 27

APPENDIX 1 List of tables Teagasc NFS 2018 29

APPENDIX 2 Background notes 82

APPENDIX 3 Classification of farm systems 84

APPENDIX 4 Glossary of terms 86

APPENDIX 5 Teagasc NFS 2017 revised tables 91

Teagasc National Farm Survey 20184

Classification of farms in the Teagasc National Farm Survey

The results of the Teagasc National Farm Survey (NFS) can be decomposed in various ways. One of themost common ways in which the results are presented is on a system basis. By system, the NFS farmsare categorised into one of six farm types: Dairy, Cattle Rearing, Cattle Other, Sheep, Tillage and MixedLivestock. Given that individual farms typically have more than one farm enterprise, a rigorous basis forcategorising farms into each system is required.

The method of classifying farms into farming systems, is based on the EU farm typology as set out inCommission Decision 78/463 and its subsequent amendments. The approach is utilised by all members ofthe EU Farm Accountancy Data Network. The methodology assigns a standard output (SO) to eachtype of animal and each hectare of crop on the farm. Farms are then classified into groups,according to the proportion of total SO which comes from each enterprise. System titles refer tothe dominant enterprise in each group. For example, the cattle rearing system refers to thosefarms where the greater proportion of the farm’s activity relates to suckler beef production. Thereare many other farms (including those in the dairy, sheep and tillage systems) that have a cattleenterprise. The mixed nature of Irish farms is reflected in the individual contribution of livestock andcrop categories to gross output. This is reflected in Table 8C in appendix 1.

Teagasc National Farm Survey 20185

Teagasc National Farm Survey 20186

Very challenging weather conditions wereexperienced on Irish farms during the spring andsummer of 2018. As a result grass growth was wellbelow normal, giving rise to a general foddershortage and a dramatic escalation in concentratefeed use on many farms. Storm and snow conditionsduring spring were swiftly followed by droughtconditions across Ireland and this is reflected inFigure 1 below.

Fig. 1: National Grass Growth 2016 - 2018

Source: Teagasc PastureBase Ireland

Although the farm-level impact of these severeweather conditions was broadly felt, the relativeeffect was farm specific and varied across regionsand systems. Generally, intensively stockedgrassland farms, in particular Dairy farms felt most ofthe brunt, with feed volume and expenditureincreasing dramatically in 2018 compared with theprevious year. On the average Dairy farm,concentrate feed expenditure rose by 43 percent(€12,765) to €42,289, although the particularcircumstances of the individual farm (i.e. stockingrate, pre-existing fodder stocks and farm location)generally dictated the additional feed requirement.Likewise, Dairy farm expenditure on purchased bulkyfeed was up 84 percent to €5,938 on average.

Although much lower in volume terms, purchasedconcentrate costs increased by 39 percent on Tillagefarms, many of whom have a significant cattleenterprise. On average, concentrate feedexpenditure on Tillage farms was €4,661 in 2018.The equivalent figure on Sheep farms was €8,475 (up31 percent). Likewise, Cattle Other farms reportedan average increase of 29 percent in concentratefeed spending to €7,801 with Cattle Rearing farmsless impacted, with average expenditure increasingby 12 percent to €3,973.

Figure 2 illustrates the year-on-year change inconcentrate feed use (kg per dairy cow) from 2017to 2018 across the three NUTS II regions. Thedramatic increase across all areas is evident.Interestingly, poorer weather conditionsexperienced first in the Northern and Westernregion in winter 2017, and the fact that cows tend tobe housed longer there is reflected in the generallyhigher concentrate usage in both years. In 2018, thewide variation in feed use on individual farms in theEastern and Midland and Southern regions isapparent, confirming the context specific nature ofthe fodder deficit and how it was dealt with.

Fig. 2: Change in Avg. Concentrate Feed Use (kg percow) on Dairy farms by NUTS II region 2017 & 2018

Increased expenditure on feed was the main driver inpushing up production costs on farms in 2018, withhigher fertiliser expenditure, contracting charges andfuel prices also a factor. Fertiliser related spendingrose by between 11 and 19 percent on most farms,with expenditure on Cattle Other systems rising by 24

Weather Woes in 2018

Interpreting the boxplots

Boxplots help provide a more in-depthdescription of the data. Here, the greenshaded boxes are representative of between25% and 75% of the population. The linewithin the box represents the median (middle)data point, i.e. half of all farms lie below thiswith half above. The tails at either endcorrespond to the minimum and maximumdata points with extreme outliers removed.

Teagasc National Farm Survey 2018

7

percent. The average spend on fertiliser on Dairyfarms was €13,759. Increased fertiliser usage isindicative of the need to increase fodder stocks laterin 2018, which is also reflected in a rise in spendingon contracting, which rose by 17 percent acrosssystems. Expenditure on contracting charges hasincreased in recent years with more farmers tendingto contract out work to cope with the increasedworkload, in particular on Dairy farms which areexpanding.

Despite unfavourable weather conditions, Irish milkproduction increased by a further 4 percent in 2018due to a strong recovery in the back end of the year.However, a lower milk price combined with thedramatic increase in feed and other costs resulted ina decline in average Dairy farm income of 31 percentto €61,446. This followed on from a record Dairyfarm income in 2017 of €88,829.

Drystock farms were also negatively affected byadverse weather in 2018, the picture varyingsomewhat across individual systems. Althoughaverage costs increased marginally on Cattle Rearingfarms, a reduction in output was the main driver inincome declining by 22 percent to €8,311. Thedecline in Cattle Other farm income was smaller,falling 10 percent to €14,560. Average Sheep farmincomes fell by 23 percent year-on-year, due mainlyto increased production costs. The average farmincome on Sheep farms in 2018 was €13,297.

Only Tillage farms saw a year-on-year increase infarm income in 2018, on average. However, thesituation was highly farm specific with crop mix onindividual farms a factor, as spring crops (especiallybarley) were impacted most by the adverse weather.On average, Tillage farm income rose by 13 percentto €40,650. Although cereal yields for major cropswere down about 23 percent on the 2017 level,harvest prices were up considerably.

The difficult production conditions encountered byfarmers in 2018 took its toll in terms of farmerwellbeing. Data from the Teagasc NFS found thatalmost three-quarters of Dairy farmers reportedelevated stress levels in 2018. The figure was loweron Cattle and Tillage farms at 57 percent and loweston Sheep farms at 37 percent. Unsurprisingly,weather was a major factor with 83 percent of allfarmers citing this. Three-quarters of Dairy andSheep farmers cited workload as a major stressor.Close to half of all farmers felt that financial pressurewas causing them stress in 2018, the figure higheston Sheep farms.

Issues such as security, isolation and succession werenot generally found to be a factor in terms of farmerwellbeing or anxiety. Interestingly, Sheep farmers(37 percent) were most likely to cite compliance as a

stressor, the higher level of participation in Pillar IIschemes by those farmers may be a factor.

Teagasc National Farm Survey 20188

Family Farm Income (FFI), the return from farmingfor farm family labour, land and capital, is theprincipal measure used in the Teagasc National FarmSurvey. FFI varies considerably by farm system, withDairy farms consistently being the most profitable(Figure 3). That said, Dairy farm incomes were worsthit in 2018, falling by almost one-third on average to€61,446. This followed a record income year in 2017and is reflective of the inherent volatility in the dairysystem; unfavourable weather conditions and asubsequent increase in production costs were thekey factor in 2018. The dramatic decline in Dairy FFIwas driven mainly by a 43 percent increase inconcentrate feed expenditure.

Cattle Rearing farms were next worst hit in 2018 withan average reduction in income of 22 percent. Thisresulted in an average FFI of €8,311, the lowest inrecent years. Despite a marginal increase in feedexpenditure on these farms (12 percent on purchasedconcentrates, on average) a decline in output and aslight increase in costs were the key drivers. Averageconcentrate feed expenditure increased by 29 per centon Cattle Other farms in 2018, with total direct ncostsincreasing by 16 percent and FFI declining by 10percent to €14,560.

An average reduction in Sheep farm income of 23percent was experienced, falling to €13,297. Again,this is explained by an increase in concentrate feedexpenditure of close to one-third and an 11 percentrise in overall costs, on average. Conversely, Tillagefarms experienced an increase in average income in2018, up 13 per cent year-on-year to €40,650. Despitea 10 percent increase in overall production costs, grossoutput rose by a slightly larger magnitude. Thesituation on individual Tillage farms varied greatly. Itwas a year of two halves with spring crops particularlynegatively affected, due to late planting and very dryweather conditions over the summer.

Figure 4 reflects system FFI over time, highlighting thegap between Dairy and Drystock farm performance inparticular. The divergence in average income levels onCattle Rearing farms is especially stark. Of note also isthe volatility of Dairy FFI post-milk quota abolition in2015 which highlights the need for resilience to shocksbe they milk price or weather induced. Theimprovement in Tillage farm income over the past twoyears is also noteworthy. Across all systems, averageFFI in 2018 was €23,333, however given the widevariation between systems this figure is not aparticularly useful measure of farm performance.

-

20

40

60

80

100

Dairy CattleRearing

CattleOther

Sheep Tillage

€'0

00

per

farm

Fig. 3: Average FFI by System 2016 - 2018

2016 2017 2018

-

20

40

60

80

100

2012 2013 2014 2015 2016 2017 2018

€'0

00

Fig. 4: Trends in System Average FFI 2012 -2018

Dairy Cattle RearingCattle Other SheepTillage All

Family Farm Income 2018

Teagasc National Farm Survey 20189

The large variation in average farm income acrossfarm systems is related to differences in both farmsize and profitability per hectare (Table 1).

Overall, the average farm size in 2018 was 43hectares and the average income level per hectarewas €541 (down from €692 in 2017). The averagesized Dairy farm in 2018 was 59 hectares. Anaverage FFI of €1,047 per hectare was earned onDairy farms in 2018; this reflects a year-on-yearreduction of €459. The economic return on a perhectare basis was next highest on Tillage farms, at€675, an increase of €75 year-on-year.

The Drystock sector, Cattle and Sheep farms, istypically characterised by lower profitability andsmaller holdings. In 2018, the average income perhectare was lowest on Cattle Rearing farms, wherethe figure fell to €270, compared to €322 in 2017.This average income per hectare was just onequarter of that of their Dairy farm counterparts.Average FFI per hectare on Cattle Other farms was€391 in 2018, falling from €460 the previous year.The equivalent figure on Sheep farms was €276,down from €369 in 2017.

The variation in individual FFI per hectare acrossfarms systems is illustrated in Figure 5, with half ofall farms reporting a figure within the green box.Those farms at the lower and higher ends of thedistribution are represented by the tails. Themedian Dairy FFI per hectare was €990 in 2018 withaverage Drystock FFI per hectare (particularly onCattle farms) falling well below this.

Unpaid farm family labour should be considered inan evaluation of FFI across systems, particularly asDrystock farmers are more likely to work off-farm.Figure 6 adjusts average system FFI to take accountof unpaid family labour which is measured in annualwork units (AWU). Each unit is equivalent to 1,800hours.

Proportionately, hours worked (both family andhired) are highest on Dairy farms and when FFI isadjusted for same, a median FFI of below €41,329 isreported, with half of all Dairy farms (the greenshaded box) earning between €23,000 and €62,434approximately.

Fig. 5: System Avg. FFI per hectare 2018

Fig. 6: System Avg. FFI per Annual Work Unit 2018

Family labour input on Tillage farms tends to belower, leaving the unpaid labour adjusted FFIrelatively similar (although more varied). OnDrystock farms, Sheep farms tend to be more labourintensive with a higher proportion of Cattle farmersworking off-farm which is reflected in these figures.

Table 1: Average Farm Size & FFI per ha 2018

Size (ha) Income per ha

Dairy 59 €1,047

Cattle Rearing 31 €270

Cattle Other 37 €391

Sheep 48 €276

Tillage 60 €675

All 43 €541

Teagasc National Farm Survey 201810

29 percent of farms across systems had a farmincome of less than €5,000 in 2018 (Figure 7). Afurther 15 percent earned between €5,000 and€10,000, with an additional 31 percent reporting aFFI of between €10,000 and €30,000. Thereforethree-quarters of Irish farms earned less than€30,000 in 2018, with the remaining 25 percentearning in excess of this.

11 percent of farms earned between €30,000 and€50,000 in 2018, with a further 6 percent falling intothe €50,000 to €70,000 category. Of the remainingfarms, 4 percent earned between €70,000 and€100,000, with a further 4 percent earning in excessof this.

Compared to 2017, a higher proportion of farms fellinto the lower income category in 2018 (i.e. thoseearning less than €5,000 increased 8 percentagepoints). Likewise, 29 percent of farms earned morethan €30,000 in 2017, with the figure declining 4percentage points to 25 percent in 2018. This isreflective of the dramatic decline in farm incomes onDairy farms in particular.

Figure 8 reflects aggregate FFI by system in 2018.Although Dairy farms account for only 17 percent ofthe total farm population, 46 percent of totalnational farm income (€992m) was generated onthose farms in 2018. The equivalent figure on Cattlefarms was 29 percent (€625m) although they arerepresentative of 58 percent of the farm population.Sheep farms account for 15 percent of total farmsand 9 percent of aggregate income (€190m) in 2018.Tillage farms are the smallest grouping accountingfor 7 percent of farms and 13 percent of total FFI(€279m) in 2018.

Across the various systems, the contrasting story interms of farm income distribution is evident (Figure9). It is worth noting that 53 percent of Dairy farmsreported a FFI of more than €50,000 in 2018 (downfrom 72 percent in 2017), with 16 percent of theseearning more than €100,000. On the other hand,almost two-thirds of Cattle Rearing farms earned afarm income of €10,000 or less in 2018 (up 6percentage points compared to 2017).

Approximately half of all other Drystock farms fellinto this category in 2018, the proportion being 49percent on Cattle Other farms and 55 percent onSheep farms. The year-on-year volatility in farmincomes is reflected in the change in FFI distributionacross farms each year.

As previously mentioned, it is important to takeaccount of unpaid family labour on farms. Onaverage, there was one unpaid family labour unit (orannual work unit) employed on farms in 2018.

0%

5%

10%

15%

20%

25%

30%

35%

< €5K €5 -€10K

€10 -€30K

€30 -€50K

€50 -€70K

€70 -€100K

>€100K

Fig. 7: Avg. System FFI Distribution 2018

46%

10%

19%

9%

13%

3%Fig. 8: Aggregated FFI by System 2018

Dairy Cattle RearingCattle Other SheepTillage Mixed Livestock

8

6549 55

2218

32

38 27

3121

9 14

19

53

27

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dairy CattleRearing

CattleOther

Sheep Tillage

Fig. 9: Avg. System FFI Distribution 2018

<10,000 10-30,000 30-50,000 >50,000

FFI Distribution 2018

Teagasc National Farm Survey 201811

The amount of unpaid labour supplied was higheston Dairy farms at 1.4 labour units and lowest onCattle Other farms at 0.90. Tillage farms reported afigure of 1 in 2018, with the comparative figures onCattle Rearing and Sheep farms 0.93 and 1.06respectively.

Figure 10 reports average FFI per labour unit in 2018.In adjusting for the additional unpaid labour utilisedon Dairy farms, average FFI was estimated to be€47,815. The equivalent figure on Tillage farms was€43,059. Relatively more hired labour is also utilisedon these systems (0.26 and 0.12 of a labour unitrespectively).

-

10

20

30

40

50

60

70

Dairy CattleRearing

CattleOther

Sheep Tillage

€'0

00

s

Fig. 10: Avg. System FFI per Labour unit 2018

FFI FFI per labour unit

Teagasc National Farm Survey 201812

In general, farm income continues to be highlyreliant on direct payments, the value of whichincreased by 3 percent in aggregate terms in 2018.On average, the total direct payment received perfarm was €17,244. The actual figure and overallcontribution to FFI varies greatly across system asis evident from Table 2 below. The data indicatesthat market income (before direct payments) isless than zero on Drystock farms, indicating that onaverage these farms do not make a profit fromproduction and are heavily dependent on support.

Although average direct payments are lowest onCattle Rearing farms at €13,098, the reliance onsame and their overall contribution to farm incomewas 158 percent in 2018, the highest on record. Thisindicates that the average suckler farm with a FFI of€8,311, lost over €4,700 of direct payments over thecourse of the year. The picture is similar on otherDrystock farms.

The average payment on Sheep farms in 2018 was€18,980, 143 percent of total FFI. Cattle Other farmsfared slightly better, reporting an average directpayment of €16,226 at 111% of farm income. Due totheir size, Dairy and Tillage farms receive the highestdirect payments overall; however, they are leastreliant on them. The average direct paymentreceived on Dairy farms in 2018 was €21,022,representative of one-third of total FFI. Directpayments on Tillage farms comprised over half of FFIin 2018, at €22,451 on average. It should be notedthat in addition to crop area, many Tillage farmswould also have a large on-farm cattle enterprise.

In terms of individual schemes, payments under theGLAS Agri-Environmental Scheme increased by 12percent year-on-year, reflecting both a rise inparticipants and a higher advance payment rate.Proportionately, Cattle Rearing farms saw the largestaverage increase from GLAS, up 30 percent to €1,957on the average farm.

That said, Sheep farms received the highest GLASpayment on average, at €2,269. Cattle Other andTillage farms received average GLAS payments ofapproximately €1,500 and €1,300 respectively, withthe average Dairy farm receiving €555 in 2018.Average payments received across systems isreflective of the proportion of participant farmswithin the system. More than one-third of all farmsparticipated in GLAS in 2018, the highest proportionon Sheep farms (53 percent). Additional monieswere also allocated under the Areas of NaturalConstraints Scheme (ANC) in 2018. This benefittedall farm systems with the average payment received€1,860. Again, Sheep farms tended to receive mostthrough this scheme at €2,486 on average with Dairyand other Drystock farms receiving approx. €1,800.

The average composition of direct payments acrossfarm systems is contained in Figure 11. The BasicPayment accounted for 79 percent of all paymentsreceived on the average Dairy farm in 2018. Theequivalent figure on Tillage farms was 84 percentwith the proportion on Cattle Rearing farms 57percent and Cattle Other 70 percent. The BasicPayment accounted for 62 percent of payments onthe average Sheep farm in 2018.

Agri-environmental scheme payments wererelatively more important on Drystock farms than ontheir Dairy and Tillage counterparts, accounting forbetween 10 and 15 percent of total payments.Payments received under the ANC scheme were alsoof relatively more importance on those farms.System specific payments such as the Beef DataGenomics Programme and the Sheep WelfareScheme, were of particular importance to CattleRearing and Sheep farms, accounting for over €1,000on the average farm.

-

5

10

15

20

25

Dairy CattleRearing

CattleOther

Sheep Tillage

€'0

00

Fig. 11: Avg. Direct Payments Compositionby System 2018

Single_Farm_Payment Agri-Envt.Areas Nat. Const. BDGPForestry Knowledge TransferDairy payts Organics SchemeMisc. TB compBTAP Sheep Welfare

Table 2: Average value of Direct Payments &Contribution to FFI 2018

DPs FFI contribution

Dairy €21,022 34%

Cattle Rearing €13,098 158%

Cattle Other €16,226 111%

Sheep €18,980 143%

Tillage €22,451 55%

All €17,244 74%

Direct Payments 2018

Teagasc National Farm Survey 201813

Despite difficult conditions, gross new investmenton Irish farms increased by 8 percent in 2018. Onaggregate, this totalled almost €941 millionnationally. Investment on Dairy farms was highest atan average of €31,714 per farm, accounting for morethan half of total investment in 2018. This figure isup 19 percent on 2017, a year in which more than adoubling in investment occurred.

Similarly, investment on Tillage farms increasedstrongly in 2018, increasing by over 34 per cent onaverage to €11,499. Although lower in value terms,investment on the average Cattle Other farmincreased significantly also, up 21 percent to €5,774.On the other hand, lower incomes on Cattle Rearingand Sheep farms were observed and wereassociated with a reduction in investment on thosefarms, the former down 19 percent to €3,913 andthe latter down 32 percent to €4,270.

In terms of financing investment, given the decline ingeneral farm incomes, it is not surprising that overalldebt on Irish farms increased somewhat in 2018.The increase was modest however, up 5 percentoverall. That said, across farm systems, almost two-thirds of farms have no farm business related debt.This figure varies considerably by farm type, six outof ten Dairy farms had borrowings in 2018,compared to only two out of ten on Sheep farms andthree out of ten on Cattle and Tillage farms (Table 3).

Where much of the investment on Dairy farms wasfinanced internally in 2017, average farm debtincreased by 12 percent in 2018 to €121,453.Despite reduced investment on Cattle Rearing andSheep farms, debt increased on average, presumablyto help mitigate the cost-price squeeze.

The average debt on Cattle Rearing farms was up 20percent to €24,882, with the equivalent figure onCattle Other and Sheep farms €36,842 (down 6percent) and €38,657 (up 18 percent). Average debton Tillage farms declined year-on-year (down 16percent) to €55,142.

The majority of farm debt (75 percent) was classifiedas long-term (more than ten years) in 2018 with 81percent of average Dairy farm debt categorised assuch. The comparative figure on Cattle Rearing andOther farms was 73 percent on average with theproportion on Sheep farms a little higher at 77percent. Conversely, only 31 percent of averageTillage farm debt was classified as long-term withanother 35 percent short-term (including overdrafts)and the remaining 34 percent related to leasing orhired purchase.

Figure 12 presents the debt to income ratio for allfarms by system (including those without debt)alongside those with farm related borrowings.Although less than one-third of Cattle farmsreported having debt in 2018, the debt to incomeratio of those with borrowings is relatively high at2.3.

Dairy farms were more likely to have debt than otherfarm types, and were also more likely to have higherlevels of debt, but given their comparatively higherincome levels the average debt to income ratio wasmuch lower at 1.8. The figure on Sheep and Tillagefarms was 1.8 and 0.95 respectively.

0.0

0.5

1.0

1.5

2.0

2.5

Dairy CattleRearing

CattleOther

Sheep Tillage

Fig. 12: Debt to Income Ratios for allFarms & those with Debt in 2018

All Farms Farms with Debt

Table 3: Average Farm Debt by System 2018

Farms withborrowings

Average debt(farms with debt)

Dairy 61% €121,453

Cattle Rearing 30% €24,882

Cattle Other 34% €36,842

Sheep 23% €38,657

Tillage 34% €55,142

All 36% €61,546

Investment 2018

Teagasc National Farm Survey 201814

In terms of the composition of investment acrossfarm systems, Figure 13 illustrates that over half ofthe funds invested on the average Dairy farm in 2018(€16,190) related to buildings, with a further 42percent (€13,384) invested in machinery and theremaining 7 percent (€2,140) allocated to landimprovement. Across the other farm systems,machinery related investment was proportionatelyhigher, accounting for 92 percent of investmentexpenditure on Tillage farms (€10,553 on average)and between 57 percent and 64 percent on Drystockfarms; all spending in the region of €2,500 to €3,300on average in 2018.

The Targeted Agricultural Modernisation Scheme(TAMS) and the Young Farmer Capital InvestmentScheme have assisted on-farm investment in recentyears. Of those Dairy farms participating in TAMS in2018, the average payment received was €20,793.

In terms of future on-farm investment, within the2018 Teagasc NFS, farmers were asked to assesstheir facilities with most reporting that they wereadequate or more than adequate overall.Interestingly, 39 percent of respondents highlightedthe need to further invest in drafting facilities with30 percent reporting that further investment onroadways was required. Furthermore, close to one-quarter of respondents believed an upgrading oftheir cow housing and milking facilities werenecessary.

51

2333

247

42

6458

57 92

7 12 919

0

20

40

60

80

100

Dairy CattleRearing

CattleOther

Sheep Tillage

%

Fig. 13: Avg. Composition of FarmInvestment by System 2018

Buildings Machinery Land improvement

Teagasc National Farm Survey 201815

There were approximately 16,146 Dairy farms, withan average income of €61,446 in 2018, a 31 percentdrop year-on-year. Given very difficult weatherconditions and a subsequent increase in productioncosts, the fact that the milk price held up better thanexpected (down 4 percent) and productionrecovered later in the year (Figure 14) helped toinsulate from a further decline in Dairy FFI in 2018.

The components of dairy FFI on the average farm in2018 are contained in Table 4. Gross output typicallydeclined by 2 percent year-on-year.

There was a 17% increase in total production costs onDairy farms in 2018 compared to 2017. Input costsincreased by 23 percent, with a dramatic increase infeed use volume in particular. Purchased concentratecosts increased by 43 percent, with feed volumereaching an average of 1,353kg per cow. Actual feeduse on individual farms was context specific andrelated to particular farm characteristics such asregion, stocking rate and other farm specific factors.

On an average Dairy farm with a herd of 79 cows,purchased concentrate expenditure totalled €42,289in 2018. Although much lower in value terms,expenditure on purchased bulky feed also increasedstrongly, (up 84 per cent) to €5,938 on average.

Figure 15 demonstrates the variation in concentratefeed use per cow across stocking rate band for 2017and 2018. This confirms the wide variation acrossfarms and clearly shows the large year-on-yearincrease. Feed use per cow on the median farm acrossstocking rates was broadly similar in 2017, with somemore variation at higher levels. The range increasedin 2018, with more heavily stocked farms requiringmarginally more concentrate feed per cow, onaverage.

Fig. 15: Avg. Concentrate Feed Use per Cow byStocking Rate 2018

Fertiliser expenditure also increased in 2018, up 14percent to €13,759 on average. This was due to bothincreased usage to build and replace fodder stocks,and a general increase in price. Likewise, machineryhire expenditure, which relates to contracting chargesalso rose, up 20 per cent to €11,141. Other livestockand veterinary costs remained stable on average,accounting for €10,684 on the average dairy herd.

0

200

400

600

800

1,000

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

De

c

M.l

itre

s

Fig. 14: Irish milk production 2016 - 2018

2016 2017 2018

Table 4: Components of Average Dairy FFI 2018

2018 2018/2017change

Gross Output €213,782 -2%

of which Direct Payts €21,022 +5%

Total Costs €152,336 +17%

of which direct costs €93,493 +23%

of which overheads €58,843 +9%

Family Farm Income €61,446 -31%

Dairy 2018

Teagasc National Farm Survey 201816

Overhead costs also increased on Dairy farms in 2018,although not to the same degree as direct costs, rising9 percent year-on-year. This was due for the mostpart to depreciation costs for buildings, machinery andland, where increases ranged from 18 to 24 percent.Land improvement costs (e.g. roadways, drainage andreseeding) also rose in 2018, up 18 percent from 2017.Hired labour costs continued to increase on Dairyfarms in 2018, on foot of a significant rise the previousyear. On average, expenditure increased by 6 percentto €5,341. Conacre rental charges remained relativelystable in 2018, spending totalling €5,897 on average.Interest paid on loans also increased, up 8 per cent onaverage.

Taking account of farm and herd size, average Dairy FFIin 2018 equated to €1,047 per hectare and €778 percow. Table 5 presents key indicators for Dairy farms in2018. On a per hectare basis, milk productionincreased 1 percent year-on-year to 11,293 litres.Average gross output per hectare declined by 4percent to €4,125, with gross margin declining by 18percent to €2,350.

Just over half of dairy farms reported a farm incomeabove €50,000 in 2018, compared to almost three-quarters in 2017. Of these, 16% earned more than€100,000. This was half of the proportion in thatincome category the previous year. Dairy FFIdistribution is presented in Figure 16 with themovement across income categories apparent,particularly at the lower and higher ends. In 2018, 26per cent of dairy farms earned an income of less than€30,000, a 14 percentage point increase on 2017.Similarly, the proportion of farms earning between€30,000 and €50,000 increased from 15 to 21 percent,with those earning between €50,000 and €70,000going from 15 to 23 per cent. Conversely, thoseearning between €70,000 and €100,000 declined by 9percentage points to 15 per cent.

Taking account of farm scale and intensity, Figure 17illustrates average Dairy FFI in 2018 by farm size class,highlighting the wide variation in return for largerfarms. Approximately 40 percent of Dairy farmsbelong to the 50 to 100 hectares size category, with afurther 35 percent in the 30 to 50 hectare bracket.Smaller farms represent 18 percent of the Dairy farmpopulation, with the remaining 7 percent above 100hectares.

Fig. 17: Avg. Dairy FFI by UAA size 2018

0

5

10

15

20

25

30

35

<30,000 30-50,000 50-70,000 70-100,000 >100,000

%o

ffa

rms

Fig. 16: Dairy FFI distribution 2016-2018

2016 2017 2018

Table 5: Average Dairy Farm Indicators 2018

2018 2018/2017change

Production (litres/ha) 11,293 +1%

Milk price (cent/litre) 36 -4%

Gross Output (€/ha) 4,125 -4%

Direct Costs (€/ha) 1,775 +25%

Gross Margin (€/ha) 2,350 -18%

Teagasc National Farm Survey 201817

Dairy farm structures vary by region. These generallydictate the circumstances and constraints under whichfarms operate. Teagasc NFS data for 2018 isdisaggregated here to NUTS II regions to examineinherent differences. The counties corresponding to theregions referred to are illustrated in Figure 18.

Fig. 18: Irish NUTS II regions

In terms of the proportion of Dairy farms located in eachregion, the vast majority, 11,708 (72 percent) arelocated in the South, which would be considered atraditional dairy area. A further 2,352 are located in theNorthern and Western region, with 2,014 in the Easternand Midlands region, where more recent dairyexpansion has been occurring since the abolition of EUmilk quota.

Table 6 provides an overview of farm structures orcharacteristics by region. On average, Dairy farms in theEastern and Midland region are larger, both in terms ofland area and herd size. The proportion of Dairy farmsoperating on very good soils is much lower in theNorthern and Western region, at 34 percent, comparedto over 60 percent in the other regions. Both hiredlabour costs and farm debt are substantially higher onDairy farms in the Eastern and Midland region withaverage investment also twice as high. There is a higherhired labour component on those farms.

The average Dairy farm in the South invested close to€28,000 in 2018. Both Dairy FFI and that adjusted forunpaid family labour were lowest in the Northern andWestern region in 2018, the latter being €31,793. Theequivalent figures in the Eastern and Midland and theSouthern region were €59,093 and €46,048.

On a per hectare basis, in 2018, FFI was highest in theSouthern region at €1,099. The comparative figures forthe Eastern and Midland and Northern and Westernregions were €988 and €884 respectively. Direct costsper cow were higher in the Northern and Westernregion with higher levels of concentrate feedexpenditure providing a partial explanation of the costdifferential. Overhead costs were substantially higheron farms in the Eastern and Midland region at €84,827on average, compared to €50,759 in the Northern andWestern region, and €54,446 in the South. Conacrerental costs on the average Dairy farm in the Eastern andMidland region were highest, at over €9,000 in 2018.When FFI per cow in 2018 is compared, farms in theSouth performed best at €843, a differential of approx.€150 compared to the other two regions.

Figure 19 reports Dairy on-farm investment across theregions in 2018 and reflects the relatively higher figurein the Eastern and Midland region. Proportionately,relatively more (about half) of total investment in theEastern and Midland and Southern regions relates tobuildings compared to the Northern and Western regionwhere the figure is 38 percent. Relatively more is spenton machinery in the Northern and Western.

-

10

20

30

40

50

60

Eastern &Midland

Northern &Western

Southern

€'0

00

Fig. 19: Composition of Dairy FarmInvestment by Region 2018

Buildings Machinery Land improvement

Table 6: Regional Dairy Farm Structures 2018

Nth/West East/Mid South

UAA (ha) 50 71 58

Herd size 62 101 76

Hired labour cost €3,468 €12,266 €3,976

Farm debt €50,096 €148,498 €60,487

Investment €21,360 €56,020 €27,727

FFI €44,266 €69,817 €64,242

FFI per unpaid LU €31,793 €59,093 €46,048

Table 7: Selected Regional Costs and Dairy FFI2018

Nth/West East/Mid South

Direct costs/cow €1,262 €1,232 €1,181

Gross Margin/ha €1,897 €2,189 €2,031

FFI/ha €884 €988 €1,099

FFI/cow €715 €691 €843

Regional Dairy Analysis

Teagasc National Farm Survey 201818

Dramatic structural change has taken place on IrishDairy farms in preparation for, and since the abolitionof EU milk quota in 2015. Overall milk production hasincreased and production efficiency has improved.Figure 20 illustrates the dramatic increase in theaverage volume of milk produced and sold perhectare over the period 2010 to 2018. Apart from adecrease in 2012 due to adverse weather conditionsand the subsequent fodder crisis, and a slowdown in2015 as a result of a lower milk price, production hasincreased strongly over the period. Average milkproduced per hectare in 2018 was 11,293 litres. Thedifference between milk produced and sold is that fedto calves, which tends to be lower when milk price ishigher.

In expanding production and improving productivity(milk yield per cow), Dairy stocking rate has alsoincreased, and this is reflected in Figure 21. In 2010the average Dairy stocking rate was 1.9, this rose to2.06 by 2018.

An increase in average Dairy farm UAA and Forage areais also evident (Figure 22), the former going from 55 to58 hectares over the period. Of that, Dairy forage areaincreased from 34 to 38, on average.

Figure 23 illustrates the growth in average Dairy herdsize, the figure increasing from 65 to 79 since 2010.Regional data indicates much growth in the Eastern andMidland region in particular, where Dairy farms seem tohave more capacity to expand. A concurrent rise in totallivestock units is evident with increased replacementsand retention of other cattle on the farm.

8

9

10

11

12

2010 2012 2014 2016 2018

'00

0lit

res

Figure 20: Avg. Milk Produced & Sold per ha2010 - 2018

Milk produced per ha Milk sold per ha

1.70

1.80

1.90

2.00

2.10

2.20

2010 2012 2014 2016 2018

Figure 21: Avg. Dairy Stocking Rate -Cows per ha 2010 -2018

0

20

40

60

80

2010 2012 2014 2016 2018

Figure 22: Average Dairy UAA & ForageArea 2010 -2018

Dairy Forage Area UAA

0

50

100

150

2010 2012 2014 2016 2018

No

.per

farm

Figure 23: Avg. Dairy Herd Size& Livestock Units 2010 - 2018

Dairy Cows Total Livestock Units

Dairy Farm Structural Change

Teagasc National Farm Survey 201819

In 2018 there were approximately 25,781 Cattle

Rearing farms, with an average income of €8,311.

Suckler cow production is the dominant enterprise on

these farms. A reduction in both area and livestock

units was evident in 2018. Table 8 outlines the key

components of average FFI on Cattle Rearing farms in

2018. Gross output typically declined by 4 percent

year-on-year to €35,990. Direct Payments remained

unchanged, at €13,098 on the average farm.

Total production costs increased in 2018, albeit to a

lesser extent than on other farm systems, up 3

percent compared to the previous year. The main

driver was the 6 percent increase in direct costs,

which equated to €13,440 on the average farm.

Spending on concentrate feed increased by 12 per

cent on average to €3,973, with purchased bulky feed

expenditure also up. Fertiliser expenditure rose by 11

per cent, due to both an increase in usage and price,

the average farm spending €2,502 in 2018. As on

other systems in 2018, spending on contracting

charges also increased on Cattle Rearing farms, up 15

percent to €3,029 on average. In aggregate,

overhead costs increased by 1 percent on Cattle

Rearing farms in 2018, with increases in energy and

fuel (up 5 and 6 percent) and increased depreciation

costs for machinery and land (11 and 8 percent

respectively). Spending on land improvement also

rose slightly in 2018 (up 5 percent).

Table 9 indicates that there was a 5 percent reduction

in farm size to 31 hectares on the average Cattle

Rearing farm in 2018, with the proportion of rented

land declining.

Total livestock units also declined, down 4 percent

compared to 2017, to 35 on average. The average gross

margin on a per hectare basis was €732 in 2018. This

included a Basic Payment of €243.

Figure 24 presents the distribution of income on Cattle

Rearing farms from 2016 to 2018. A dramatic increase in

the proportion of farms reporting an average FFI of less

than €5,000 in 2018 is evident; up 13 percentage points

to 44 per cent. The data indicates that almost two-thirds

of Cattle Rearing farms earned less than €10,000 in 2018.

A further 22 per cent earned between €10,000 and

€20,000, with 11 per cent in the €20,000 to €50,000

category. Only 1% of Cattle Rearing farms earned more

than €50,000 in 2018.

0

10

20

30

40

50

<5,000 5-10,000 10-20,000 20-50,000 >50,000

%o

ffa

rms

Fig. 24: Avg. Cattle Rearing FFI Distribution2016-2018

2016 2017 2018

Table 8: Components of Average Cattle RearingFFI 2018

2018 2018/2017change

Gross Output €35,990 -4%

of which Direct Payts €13,098 -

Total Costs €27,680 +3%

of which direct costs €13,440 +6%

of which overheads €14,240 +1%

Family Farm Income €8,310 -22%

Table 9: Cattle Rearing Average Indicators 2018

2018 2018/2017change

Farm Size (ha) 31 -5%

Livestock Units 35 -4%

Livestock Units per ha 1.14 -

Basic Payment (€/ha) 243 -

Gross Margin (€/ha) 732 -4%

Cattle Rearing 2018

Teagasc National Farm Survey 201820

In disaggregating the data further, Figure 22illustrates the variation in FFI on Cattle Rearing farmsacross size categories, with a broad range reportedfor those farms in the largest size classes in particular.In terms of the overall population, approximately 4percent had a UAA above 100 hectares, with 13percent between 50 and 100 and 38 percent in the 30to 50 hectares bracket. 29 percent of Cattle Rearingfarms were sized between 20 and 30 hectares, withthe remaining 16 percent less than this. The lowprofitability of many Cattle farms is reflected in theviability analysis presented later in the report.

Fig. 25: Avg. Cattle Rearing FFI by Farm Size 2018

Teagasc National Farm Survey 201821

There were approximately 28,239 Cattle Other farms,with an average income of €14,560 in 2018, an 11 percent decline on 2017. Cattle finishing is the dominantenterprise on these farms. In 2018 finished cattleprices increased only marginally due to volatilityacross price categories.

Overall, output value increased by 6 percent in 2018,with an additional 5 percent rise in direct payments.The latter was mainly due to an increase in averagepayments received through the Basic Payment, GLASand the Areas of Natural Constraint scheme.

Table 10 outlines the components of average CattleOther income in 2018. The value of Gross Output was€52,352, with Direct Payments totalling over €16,226on average.

Total costs increased by 14 percent on Cattle Otherfarms year-on-year. In general, direct productioncosts increased by 16 percent, with expenditure onpurchased concentrates up 29 percent to €7,801 onaverage. Expenditure on purchased bulky feed roseby a similar magnitude to €934 on average. As onother systems, expenditure on fertiliser andcontracting charges increased in 2018. Expenditureon fertiliser rose by 24 percent to €3,500 on average,with contracting charges increasing by 14 percent to€3,567. Expenditure relating to livestock andveterinary declined by 1 percent compared to 2017.

On average, overhead costs increased by 12 per centin 2018. Of those, conacre rental expenditure rose by10 percent to €1,327. Depreciation costs alsoincreased strongly, with higher expenditure relatingto machinery operating and energy and fuel alsoevident.

Average concentrate feed use on Cattle Other farms bystocking rate is depicted in Figure 26. This appears tovary most on farms with relatively lower and higherstocking rates.

Fig. 26: Avg. Concentrate Feed use per LivestockUnit on Cattle Other Farms 2018

Table 11 indicates that average UAA on Cattle Otherfarms rose by 6 per cent in 2018 to 37 hectares. Totallivestock units also increased to 50 from 47. Theaverage gross margin per hectare on Cattle Other farmswas €882 in 2018, down from €927 in 2017. Thisincluded a Basic Payment of €305 per hectare.

Figure 27 presents the distribution of average incomeon Cattle Other farms in 2018. The proportion offarms in the lowest income category has increasedsteadily since 2016, accounting for one-third of farmsin 2018.

Table 10: Components of Average Cattle Other FFI2018

2018 2018/2017change

Gross Output €52,352 +6%

of which Direct Payts €16,226 +5%

Total Costs €37,792 +14%

of which direct costs €19,509 +16%

of which overheads €18,283 +12%

Family Farm Income €14,560 -10%

Table 11: Cattle Other Average Indicators 2018

2018 2018/2017change

Farm Size (ha) 37 +6%

Livestock Units 50 +6%

Livestock Units per ha 1.35 -

Basic Payment (€/ha) 305 -1

Gross Margin (€/ha) 882 -5%

Cattle Other 2018

Teagasc National Farm Survey 201822

A further 16 percent earned between €5,000 and€10,000, meaning that just under half of all CattleOther farms earned less than €10,000 in 2018.

A further 23 percent earned between €10,000 and€20,000, indicating that average income on almostthree-quarters of Cattle Other farms fell below€20,000 in 2018. An additional 24 percent earnedbetween €20,000 and €50,000 with only 4 percentearning an FFI above this. It should be noted that 42percent of Cattle Other farm-holders also worked off-farm in 2018.

Figure 28 reflects the variation in average FFI by farmsize with a broad range reported for those farms inthe largest size class in particular. In terms of theoverall population, approximately 5 percent of farmsfall into this size category with 18 percent in the 50 to100 hectares bracket and 29 percent in the 30 to 50hectares category. 25 percent of Cattle Other farmsare sized between 20 and 30 hectares with theremaining 23 percent less than this.

Fig. 28: Avg. Cattle Other FFI by Farm Size 2018

0

5

10

15

20

25

30

35

<5,000 5-10,000 10-20,000 20-50,000 >50,000

%o

ffa

rms

Fig. 27: Cattle Other FFI Distribution2016-2018

2016 2017 2018

Teagasc National Farm Survey 201823

Regional differences in terms of various farm

characteristics, costs and income have already been

outlined for Dairy farms in 2018. Similarly, regional

differences are important on Cattle farms and these

are discussed here across the NUTS II regions

described in Figure 29.

Fig. 29: Irish NUTS II regions

Table 12 provides some information on regionalfarm structures and economic indicators on CattleRearing farms in 2018. Over half of all CattleRearing farms (14,000) are located in the Northernand Western region with over 8,500 located in theSouth and 3,500 in the Eastern and Midland region.Cattle Rearing farms in the Northern and Westernregion tend to be smaller and less intensivelystocked. Only 16 percent operate on very goodsoils, compared to half of the farms across the otherregions.

In 2018 direct costs per hectare were €100 higheron farms in the South at €478, with expenditure onpurchased concentrate feed a factor. Overall, FFIwas higher on average in the Southern region. On aper hectare basis the figure was €293, with thecomparative figures in the Northern and Westernregion and Eastern and Midland regions €271 and€230 respectively. Direct payments per hectarewere also highest in the Northern and Westernregion at €437 per hectare.

The corresponding figures for the Cattle Othersystem (predominantly finishing) are contained inTable 13. The majority of these farms, 11,500 (41percent) are based in the Southern region, withanother 33 percent (over 9,000) based in theNorthern and Western region and the remaining 25percent (7,000) based in the Eastern and Midlandregion.

Cattle Other farms in the Eastern and Midland andSouthern regions were more intensively stocked thanthose farms located in the Northern and Western region.On average, FFI was highest on those farms located in theSouth, at €16,125, in 2018. Gross Output per hectare wasbroadly similar across the three regions in 2018. Grossmargin was on average higher in the South, at €900 perhectare.

On average, costs were higher on Cattle Other farmsbased in the Eastern and Midland region in 2018.Elevated spending on purchased concentrates was themain factor in this, with higher expenditure oncontracting charges, veterinary expenses etc. alsoevident. Overhead costs were substantially lower in theNorthern and Western region, where average spendingon hired labour was much lower. Overall, moreintensively stocked, higher cost farms in the Eastern andMidland region did comparatively worse in 2018. FFI inthe region was €315 on a per hectare basis, with thehighest figure reported on Northern and Western farmsat €453. Direct payments were also highest in this regionat €484 per hectare.

Table 12: Selected Regional Farm Structures onCattle Rearing Farms 2018

Nth/West East/Mid South

UAA (ha) 30 32 33

Livestock units 32 40 38

FFI €7,995 €7,398 €9,557

Gross Output /ha €1,111 €1,203 €1,222

Gross Margin/ha €695 €799 €744

Direct Payts/ha €437 €409 €417

FFI/ha €271 €230 €293

Table 13: Selected Regional Farm Structures onAvg. Cattle Other Farms 2018

Nth/West East/Mid South

UAA (ha) 31 41 40

Livestock units 40 59 51

FFI €13,940 €12,858 €16,125

Gross Output /ha €1,325 €1,434 €1,399

Gross Margin/ha €872 €844 €900

Direct Payts/ha €484 €401 €433

FFI/ha €453 €315 €407

Regional CattleAnalysis

Teagasc National Farm Survey 201824

There were approximately 14,322 Sheep farms withan average income of €13,297 in 2018, a 23 percentreduction on 2017 (Table 12). Despite a slightimprovement in prices early in the year, overall grossoutput on the average Sheep farm declinedmarginally to €50,085. Direct payments were upslightly year-on-year to almost €19,000 on average.This was mainly due to increased payments under theAreas of Natural Constraints Scheme (up 10 percent)and to a lesser extent GLAS (up 5 percent). The SheepWelfare Scheme continued in 2018, providing anaverage payment of €1,000 to participants.

As on most other systems, the main factor in reducedFFI on Sheep farms in 2018 related to increasedproduction costs. Direct costs increased by 15percent on average with purchased concentrate costsincreasing by almost one-third to close to €8,500 (thelargest increase across Drystock systems and morethan twice that of their Cattle Rearing counterparts).The fact that lambing season coincided with most ofthe difficult weather was a real issue in terms ofincreased feeding costs on Sheep farms. Fertiliserexpenditure also increased, up 19 percent to over€3,000 on average. As with the other systems, astrong increase in fodder production costs is evident,with spending on contracting charges up 19 percenton average to €2,338. Overhead costs increased by 7percent to €17,473 in 2018, with some increases inenergy and fuel and depreciation in particular.

On a per hectare basis, the average gross margin onSheep farms was €640 in 2018. This included a BasicPayment of €244. The average sized Sheep farm was48 hectares, with a flock size of 127 ewes.

Figure 30 presents the distribution of income onSheep farms since 2016. What is evident is therelatively large proportion of farms in the lowerincome categories, with one-third of farms earningbelow €5,000 in 2018. The proportion of farmsearning between €10,000 and €20,000 also increased7 percentage points to 22 percent. Conversely, thoseearning between €20,000 and €50,000 declined by 7percentage points to 22 percent. Only 3 per cent ofSheep farms earned above €50,000 in 2018. Thevariation in average Sheep FFI is illustrated in Figure30.

0

5

10

15

20

25

30

35

<5,000 5-10,000 10-20,000 20-50,000 >50,000

%o

ffa

rms

Fig. 30: Average Sheep FFI Distribution2016-2018

2016 2017 2018

Table 12: Components of Average Sheep FFI 2018

2018 2018/2017change

Gross Output €50,085 -1%

of which Direct Payts €18,980 +2%

Total Costs €36,788 +11%

of which direct costs €19,315 +15%

of which overheads €17,473 +7%

Family Farm Income €13,297 -23%

Table 13: Sheep Farm Indicators 2018

2018 2018/2017change

Farm Size (ha) 48 +2%

Number of Ewes 127 -4%

Livestock Units per ha 1.10 -6%

Basic Payment (€/ha) 244 -2%

Gross Margin (€/ha) 640 -11%

Sheep 2018

Teagasc National Farm Survey 201825

On average, Tillage farms were the only ones toreport an annual increase in FFI in 2018.Approximately 6,879 Tillage farms earned anaverage income of €40,650 in 2018. Although,harvest yields were down substantially due to thechallenging weather conditions, prices increased andoverall, the general improvement was sufficient toincrease average margins. This was not the case forall crops however with spring crops especiallyaffected by late planting and adverse summerweather. Table 14 reports the components ofaverage Tillage FFI in 2018. Average gross outputincreased by 11 percent to €116,163. This was dueto a combination of factors, with increased outputvalue for wheat and straw in particular. Some farmsalso benefitted from the growth of forage crops.

In line with the other farm systems, costs increasedon Tillage farms in 2018, increasing by 10 percentoverall to €75,529. This was due to both to increasesin individual cost items and a slight increase inoverall Tillage area on NFS farms which was up 2percent to 37 hectares. Direct costs increased by 12percent year-on-year, with fertiliser the maincomponent, up 19 per cent to €11,763 on theaverage Tillage farm. Expenditure on purchasedseed and crop protection totalled a similar amount,with the former rising by 7 percent and the latter upby 1 percent compared to the previous year. As onother farms, expenditure on contracting chargesrose strongly year-on-year, up 13 percent to €7,596on average. As most Tillage farms also have asignificant cattle enterprise, expenditure onpurchased concentrates also increased in 2018, up39 percent to €4,661 on average.

As on other systems in 2018, overhead costs alsoincreased, rising by 8 percent year-on-year. Withregard to individual cost items, conacre rental costswere up by 12 percent to €5,041 on average. Costsrelating to fuel and electricity also increased, as didthose relating to land improvement anddepreciation.

Data from the Teagasc NFS 2018 indicates that onthe average Tillage farm 33 hectares (over half of allland area) was dedicated to cereals. The averagefarm gross margin was €1,285 per hectare and thisincluded a Basic Payment of €314 (Table 15).

Figure 31 presents the distribution of income ontillage farms from 2016-2018. Of note is the fact that27 percent earned a FFI of more than €50,000. Ofthese, 19 percent earned more than €100,000. Theproportion of Tillage farms earning below €5,000was up 2 percentage points in 2018, at 14 percent,with 9 percent earning between €5,000 and €10,000(up 4 percentage points). One fifth of Tillage farmsearned between €10,000 and €20,000 in 2018, with30 per cent earning between €20,000 and €50,000.

0

10

20

30

40

<5,000 5-10,000 10-20,000 20-50,000 >50,000

%o

ffa

rms

Fig. 31: Avg. Tillage FFI Distribution2016-2018

2016 2017 2018

Table 14: Components of Average Tillage FFI 2018

2018 2018/2017change

Gross Output €116,163 +11%

of which Direct Payts €22,451 -2%

Total Costs €75,529 +10%

of which direct costs €38,824 +12%

of which overheads €36,688 +8%

Family Farm Income €40,650 +13%

Table 15: Avg. Tillage Enterprise Indicators 2018

2018 2018/2017change

Farm Size (ha) 60 -

Hectares of Cereals 33 +3%

Cereal output (€/ha) 1,850 +18%

Basic Payment (€/ha) 314 -4%

Gross Margin (€/ha) 1,285 +10%

Tillage 2018

Teagasc National Farm Survey 201826

Farm income varies widely by region, driven by farmsystem, scale, profitability and direct payments.Those regions where dairying is more prevalent aregenerally more profitable and have a lower relianceon direct payments (Figure 32).

Average family farm income in 2018 was highest inthe South-East at €35,622 and lowest in the Borderregion, where average farm incomes was 2.5 timesless at just over €13,292. This is of course reflectiveof farm composition in those areas, with a higherprevalence of drystock farms in areas where incomesare lower. The relative importance of directpayments is highest in that region, accounting formore than total FFI in 2018 (117 per cent). A similarsituation is evident in the West where the averageFFI was just under €14,000 (with direct paymentscomprising 108%). The equivalent figure for farms inthe Midlands region was 93 per cent. Although muchlower in percentage terms, direct payments accountfor a significant proportion of farm income acrossthe other regions also, ranging between 57 and 67per cent. The relative contribution of directpayments to FFI increased across all regions in 2018.This was due to reduced profitability across systemsand the fact that 2017 was a record year for DairyFFI.

Just over half (51.5 percent) of farm households hadan off-farm income employment source in 2018, aslight increase on 2017. Dairy farm households wereslightly more likely to have an off-farm income,within the household, with the proportion of farmspouses employed off-farm generally higher. Thisreflects the younger demography of these

households. The higher age profile of non-dairy farmhouseholds is reflected in the fact that they weremore than twice as likely to be in receipt of pensionson average.

The proportion of farm households where thespouse was employed off-farm remained static at 33percent, with the same proportion of farmersemployed off-farm (again unchanged at 33 percent)(Figure 33).

The off-farm employment situation differs bysystem, with Cattle farmers more likely to work off-farm. 42 percent of Cattle Other farmers had an off-farm job in 2018; the equivalent figure on CattleRearing farms was 39 percent. A lower proportion ofSheep and Tillage farmers worked off farm (32 and33 percent), whereas only 12 percent of Dairyfarmers were employed off-farm.

The incidence of off-farm employment varies acrossregions and reflects the dominant type of farmingthere (Figure 34). More than 40 percent of farmersin the West worked off-farm in 2018, compared toabout 25 percent in the Southern regions, wherefarmers were less likely to be employed off farm dueto the predominance of dairy farming there.

0

20

40

60

80

100

120

140

0

5

10

15

20

25

30

35

40

B E M SW SE S W

%

€'0

00

Fig. 32: Average FFI & DPs as a % of FFI byRegion 2018

FFI Direct Payts as a % of FFI

0

10

20

30

40

50

60

2008 2010 2012 2014 2016 2018

Fig. 33: Off-Farm Employment2008-2018

Farmer Farmer & Spouse

05

1015202530354045

Border East M'lds S'West S'East South West

%

Fig. 34: Proportion of Farmers EmployedOff-Farm by Region 2018

Regional FFI andOff-farm Employment

Teagasc National Farm Survey 201827

It follows that farms with relatively modest incomescan be viable if the labour input and capitalinvestment is low, and similarly farms with seeminglylarge incomes may not be viable if there is asubstantial labour input and/or significant capitalinvested in machinery and livestock. Farms that arefound not to be economically viable, but have an off-farm income source (either from a job, pension orsocial welfare) within the household, earned by eitherthe farmer or the spouse, are considered to beeconomically sustainable. Farm households areconsidered to be economically vulnerable if they areoperating non-viable farm businesses and neitherthe farmer or spouse works off-farm.

The data indicates that 32 percent of the farmpopulation represented by the Teagasc NFS in 2018were classed as being economically viable (Figure35). This figure varies from year to year dependingon FFI performance across systems. As 2018 saw anaverage decline in FFI across most farms, it is notsurprising that this viability figure declined from 40percent in 2017. The proportion of householdsdefined as sustainable increased slightly to 34percent. This is due to the presence of an off- farmincome source, in which there was a small increase.The remaining 34 percent of farm households weredeemed to be economically vulnerable, having noalternative income source within the household. Thisincreased 3 percentage points year-on-year.

The viability of Irish farms varies across system.Figure 36 indicates the wide differential between theviability of dairy and tillage farms, on average,compared to their drystock counterparts. In 2018,72 percent of Dairy farms were found to be viable(down from 85 per cent in 2017). As a result, therewas an increase in those farm households furthersustained by an off-farm income source (up from 7to 14 percent). The proportion of viable Tillagefarms was 63 percent in 2018. The proportion ofviable Cattle Rearing farms fell a further 7percentage points in 2018 to 11 percent.

Although FFI on other Drystock farms was lessimpacted in 2018, only 26 per cent of Cattle Otherfarms (down 5 percentage points) and 20 per centof Sheep farms were classed as viable (down 8percentage points). As a result, the proportion ofvulnerable Cattle Rearing farms increased 3percentage points in 2018, with the comparativefigure on Cattle Other farms remaining stable andSheep up 3 percentage points on average. Similarly,a 4 percentage point increase in the proportion ofCattle Rearing farms deemed to be sustainable isevident, with this category also increasing similarlyon other Drystock farms.

32%

34%

34%

Fig. 35: Viability of Irish Farming 2018

Viable Sustainable Vulnerable

72

1126 20

63

14

46

3736

19

13

43 3744

18

0

10

20

30

40

50

60

70

80

90

100

Dairy CattleRearing

CattleOther

Sheep Tillage

%

Fig. 36: Viability of Farming by System 2018

Viable Sustainable Vulnerable

A farm business is defined as being economicallyviable if Family Farm Income is sufficient toremunerate family labour at the minimum wage(which is assumed here to be €19,616 per labourunit), and provide a 5 percent return on the capitalinvested in non-land assets, i.e. machinery andlivestock.

Viability 2018

Teagasc National Farm Survey 201828

To put these results in context, the data indicatesthat there were just under 12,000 viable Dairy farmbusinesses in Ireland in 2018, with almost 3,000Cattle Rearing farms and 7,500 Cattle Other farmsconsidered as such.

The number of viable Tillage and Sheep farms wereapproximately 4,500 and 3,000 respectively. Thedata indicates that there were over 21,000 vulnerableCattle farms in 2018 and this does not take accountof those smaller farms with a standard output of lessthan €8,000. Data is collected on those farms everyfive years, most recently in 2015, when half of thesesmall farms were found to be vulnerable, a furtherone-third were considered sustainable and theremainder viable.

The regional figures are stark, with 44 per cent offarms in the South classified as viable compared toonly 16 per cent in the Northern and Western region.The equivalent figure in the Eastern and Midland areais 34 per cent. These figures are reflective of thecomposition of agriculture and the sustainability ofsame across regions. 41 percent of farms in theNorthern and Western region in 2018 werevulnerable, compared to 27 per cent in the South and35 per cent in the Eastern and Midland region. Withregard to those farm households deemed sustainabledue to the presence of an off-farm income source,the proportion in the Southern region and Easternand Midland regions were similar at 29 and 30percent, with the comparative figure in the Northernand Western region higher at 43 percent. Thisreflects the importance of off-farm employment andthe incidence of part-time farming in that region.

Teagasc National Farm Survey 201829

Appendix 1: List of tables Teagasc NFS 2018

TABLE - 01a Farm Financial Results by Size (UAA - Ha) - Dairying SystemTABLE - 01b Resources per Farm by Size (UAA - Ha) - Dairying SystemTABLE - 01c Gross Output and Direct Payments by Size (UAA - Ha) - Dairying SystemTABLE - 01d Direct and Overhead Costs by Size (UAA - Ha) - Dairying SystemTABLE - 01e Demographic Data by Size (UAA - Ha) - Dairying System

TABLE - 02a Farm Financial Results by Size (UAA - Ha) - Cattle Rearing SystemTABLE - 02b Resources per Farm by Size (UAA - Ha) - Cattle Rearing SystemTABLE - 02c Gross Output and Direct Payments by Size (UAA - Ha) - Cattle Rearing SystemTABLE - 02d Direct and Overhead Costs by Size (UAA - Ha) - Cattle Rearing SystemTABLE - 02e Demographic Data by Size (UAA - Ha) - Cattle Rearing System

TABLE - 03a Farm Financial Results by Size (UAA - Ha) - Cattle Other SystemTABLE - 03b Resources per Farm by Size (UAA - Ha) - Cattle Other SystemTABLE - 03c Gross Output and Direct Payments by Size (UAA - Ha) - Cattle Other SystemTABLE - 03d Direct and Overhead Costs by Size (UAA - Ha) - Cattle Other SystemTABLE - 03e Demographic Data by Size (UAA - Ha) - Cattle Other System

TABLE - 04a Farm Financial Results by Size (UAA - Ha) - Sheep SystemTABLE - 04b Resources per Farm by Size (UAA - Ha) - Sheep SystemTABLE - 04c Gross Output and Direct Payments by Size (UAA - Ha) - Sheep SystemTABLE - 04d Direct and Overhead Costs by Size (UAA - Ha) - Sheep SystemTABLE - 04e Demographic Data by Size (UAA - Ha) - Sheep System

TABLE - 05a Farm Financial Results by Size (UAA - Ha) - Tillage SystemTABLE - 05b Resources per Farm by Size (UAA - Ha) - Tillage SystemTABLE - 05c Gross Output and Direct Payments by Size (UAA - Ha) - Tillage SystemTABLE - 05d Direct and Overhead Costs by Size (UAA - Ha) - Tillage SystemTABLE - 05e Demographic Data by Size (UAA - Ha) - Tillage System

TABLE - 07a Farm Financial Results by Size (UAA - Ha) - All SystemsTABLE - 07b Resources per Farm by Size (UAA - Ha) - All SystemsTABLE - 07c Gross Output and Direct Payments by Size (UAA - Ha) - All SystemsTABLE - 07d Direct and Overhead Costs by Size (UAA - Ha) - All SystemsTABLE - 07e Demographic Data by Size (UAA - Ha) - All Systems

TABLE - 08a Farm Financial Results by System of Farming - All FarmsTABLE - 08b Resources per Farm by System of Farming - All FarmsTABLE - 08c Gross Output and Direct Payments by System of Farming - All FarmsTABLE - 08d Direct and Overhead Costs by System of Farming - All FarmsTABLE - 08e Demographic Data by System of Farming - All Farms

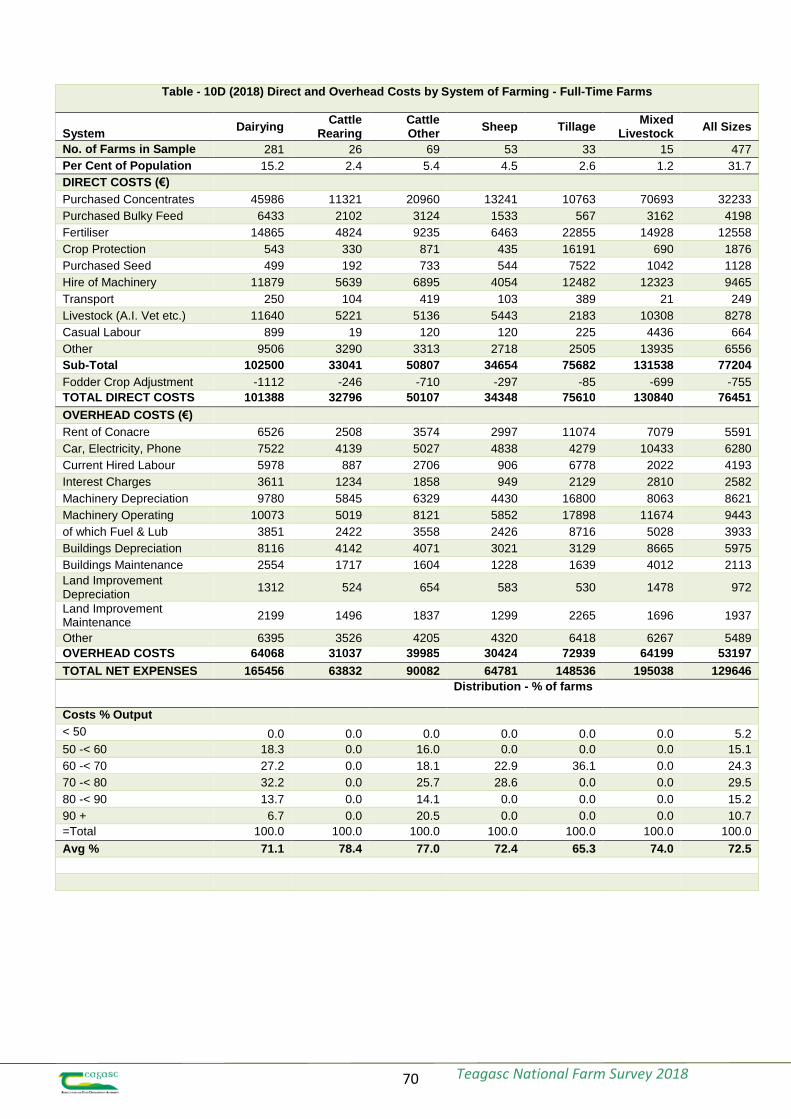

TABLE - 10b Resources per Farm by System of Farming - Full-Time FarmsTABLE - 10c Gross Output and Direct Payments by System of Farming - Full-Time FarmsTABLE - 10d Direct and Overhead Costs by System of Farming - Full-Time FarmsTABLE - 10e Demographic Data by System of Farming - Full-Time Farms

Teagasc National Farm Survey 201830

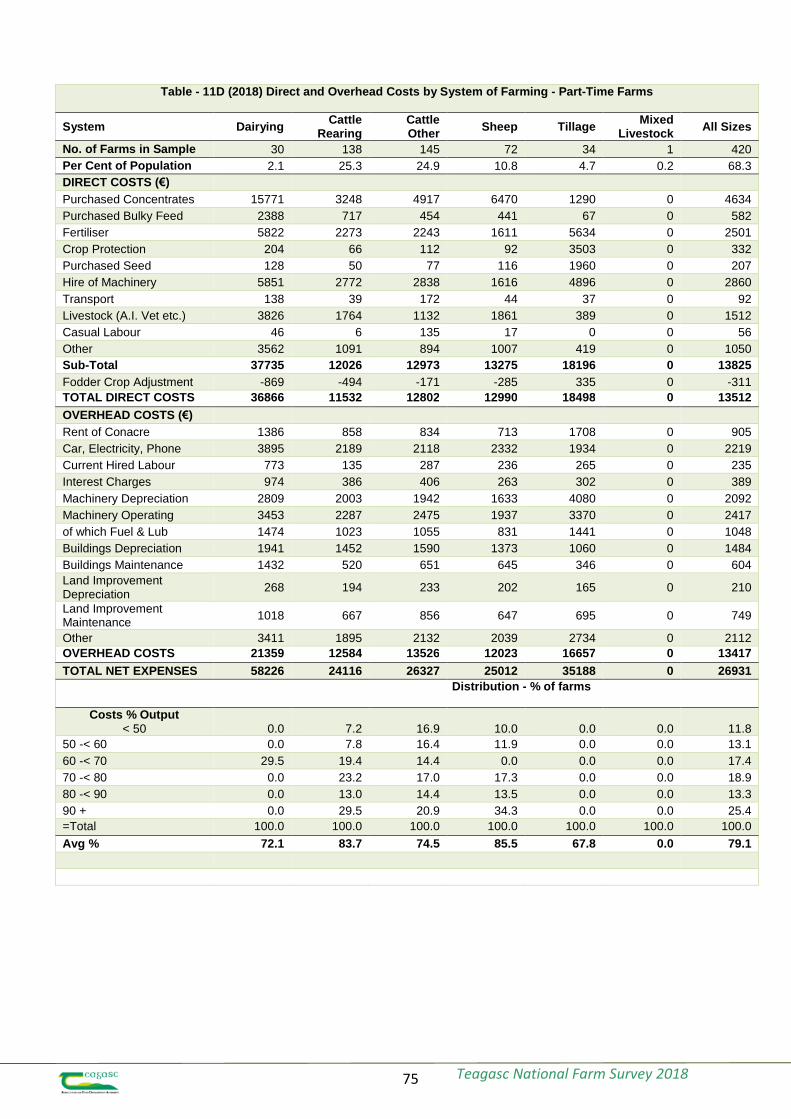

TABLE - 11a Farm Financial Results by System of Farming - Part-Time FarmsTABLE - 11b Resources per Farm by System of Farming - Part-Time FarmsTABLE - 11c Gross Output and Direct Payments by System of Farming - Part-Time FarmsTABLE - 11d Direct and Overhead Costs by System of Farming - Part-Time FarmsTABLE - 11e Demographic Data by System of Farming - Part-Time Farms

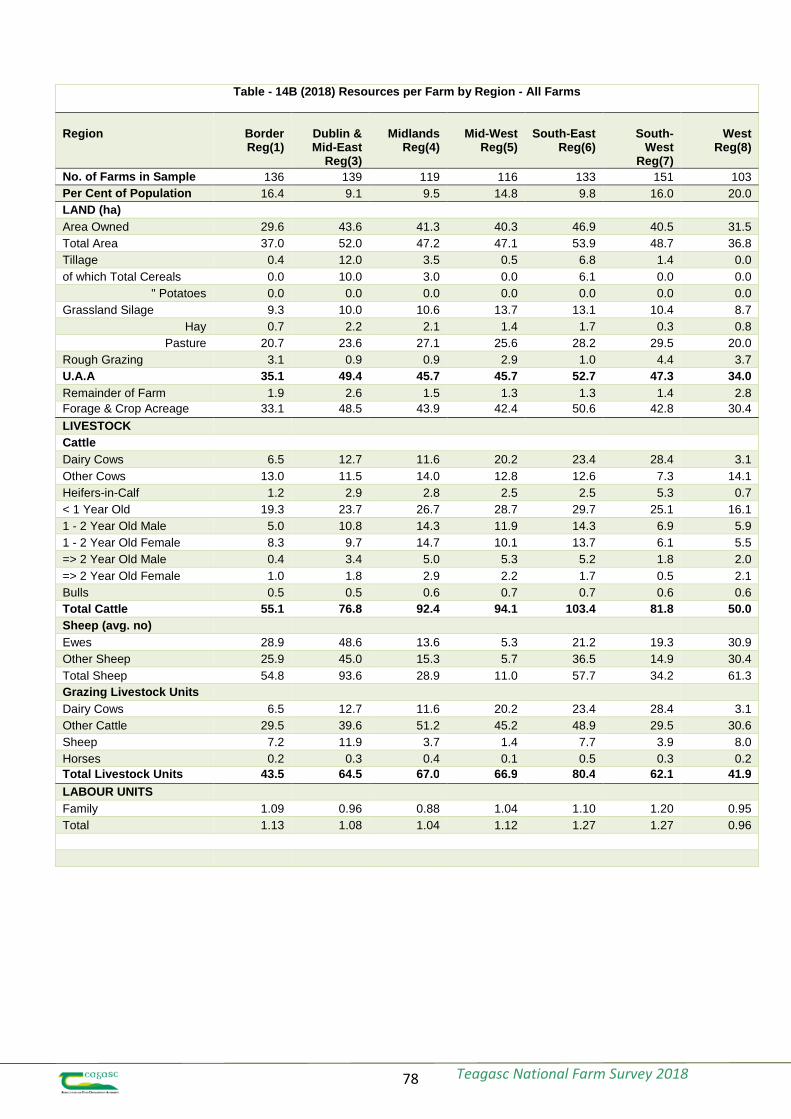

TABLE - 14a Farm Financial Results -- By Region - All FarmsTABLE - 14b Resources per Farm -- By Region - All FarmsTABLE - 14c Gross Output and Direct Payments -- By Region - All FarmsTABLE - 14d Direct and Overhead Costs -- By Region - All FarmsTABLE - 14e Demographic Data -- By Region - All Farms

TABLE - 15a Farm Financial Results by System of Farming - All FarmsTABLE - 15b Resources per Farm by System of Farming - All FarmsTABLE - 15c Gross Output & Direct Payments by System of Farming - All FarmsTABLE - 15d Direct and Overhead Costs by System of Farming - All FarmsTABLE - 15e Demographic Data by System of Farming - All Farms

Teagasc National Farm Survey 201831

Table - 01A (2018) Farm Financial Results by Size (UAA - Ha) - Dairying System

Size (UAA-Ha)2 -

< 2020 -< 30

30 -< 50

50 -< 100

>= 100Hill

FarmsAll

Sizes

No. of Farms in Sample 11 15 76 140 55 14 311

Per Cent of Population 0.7 1.6 5.3 7.0 1.6 0.8 17.4

Overall Results (€)

Gross Output 53599 91814 148735 248048 507779 155247 213782

of which Land / Quota Let 0 0 18 327 404 0 176

Subsidies and DirectPayments

6154 7860 14796 25773 42998 17707 21022

- Direct Costs 26374 42341 62820 106959 228449 74720 93493

=Gross Margin 27225 49472 85915 141089 279330 80526 120289

- Overhead Costs 16231 24697 38970 68227 147201 40814 58843

= Family Farm Income 10994 24776 46944 72861 132130 39712 61446

Net Sales & Receipts 55110 91134 150922 248953 494073 160789 213797

-Current Cash Expenditure 38651 61054 89843 154867 338607 105960 135659

=Cash Income (Approx) 16459 30079 61079 94086 155466 54829 78138

- Net New Investment 9735 8814 17605 29465 85385 29603 28294

=Cash Flow 6724 21266 43474 64621 70081 25226 49845

Asset Values (€)

Machinery 17783 27236 47797 83684 144667 47514 68223

Livestock: Breeding 26959 44708 64378 109977 227061 76401 95399

Trading 4025 10823 17961 38190 86347 18760 31403

Land & Buildings 270509 417771 738838 1242987 2311543 759835 1042119

Gross New Investment 10815 9324 18916 33094 100141 30399 31714

Loans Closing Balance 0 0 35159 73878 316948 36088 74146

Total Standard Output(TSO)

50965.1 82302.1 122542.0 197922.0 382122.5 142192.7 171737.4

Distribution - % of Farms

Soil Group :- (1) 0.0 0.0 57.9 60.7 67.3 0.0 56.0

(2) 0.0 0.0 42.1 39.3 32.7 0.0 38.9

(3) 0.0 0.0 0.0 0.0 0.0 100.0 5.1

=Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Teagasc National Farm Survey 201832

Table - 01 B (2018) Resources per Farm by Size (UAA - Ha) - Dairying System

Size (UAA-Ha) 2 - 20 - 30 - 50 - >= 100 Hill All< 20 < 30 < 50 < 100 Farms Sizes

No. of Farms in Sample 11 15 76 140 55 14 311

Per Cent of Population 0.7 1.6 5.3 7.0 1.6 0.8 17.4

LAND (ha)

Area Owned 12.7 21.3 34.8 55.2 94.0 40.1 46.7

Total Area 15.0 26.5 41.7 72.4 135.7 50.1 60.8

Tillage 0.0 0.0 0.5 0.9 6.0 0.0 1.1

of which Total Cereals 0.0 0.0 0.0 0.0 0.0 0.0 0.6

" Potatoes 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Grassland Silage 5.1 8.1 14.5 24.9 44.8 16.6 20.7

Hay 0.4 0.8 0.5 1.0 1.5 0.1 0.8

Pasture 9.0 15.2 24.0 40.4 74.9 28.8 34.2

Rough Grazing 0.0 0.7 1.7 1.2 1.5 3.4 1.4

U.A.A 14.5 24.8 40.4 69.9 130.0 49.2 58.7

Remainder of Farm 0.5 1.7 1.3 2.4 5.7 0.9 2.2

Forage & Crop Acreage 14.5 24.5 39.9 67.8 127.8 46.9 57.3

LIVESTOCK

Cattle

Dairy Cows 24.5 38.6 57.0 90.1 171.7 66.3 78.6

Other Cows 0.1 1.0 0.5 2.5 4.2 0.9 1.7

Heifers-in-Calf 2.7 4.7 6.4 10.6 26.2 7.2 9.7

< 1 Year Old 7.7 17.3 28.8 56.3 110.7 35.0 46.0

1 - 2 Year Old Male 0.4 2.9 3.6 10.5 20.7 5.8 7.9

1 - 2 Year Old Female 2.8 4.9 9.0 19.2 38.0 7.8 15.2

=> 2 Year Old Male 0.0 0.7 0.6 1.2 1.9 0.3 0.9

=> 2 Year Old Female 0.8 0.2 0.7 1.5 2.2 1.7 1.1

Bulls 0.5 0.6 0.6 1.3 1.9 0.7 1.0

Total Cattle 39.0 70.3 106.6 192.0 376.1 125.0 161.3

Sheep (avg. no)

Ewes 0.0 3.3 3.0 1.8 3.5 2.0 2.4

Other Sheep 0.0 2.3 1.9 1.6 4.7 1.2 1.9

Total Sheep 0.0 5.6 4.9 3.4 8.2 3.2 4.3

Grazing Livestock Units

Dairy Cows 24.5 38.6 57.0 90.1 171.7 66.3 78.6

Other Cattle 7.3 15.6 23.5 49.8 100.1 27.5 40.1

Sheep 0.0 0.8 0.6 0.5 1.0 0.3 0.6

Horses 0.2 0.0 0.0 0.2 0.4 0.0 0.1

Total Livestock Units 32.0 54.9 81.1 140.5 273.3 94.1 119.4

LABOUR UNITS

Family 1.05 1.22 1.31 1.38 1.75 1.36 1.36

Total 1.06 1.27 1.37 1.71 2.71 1.55 1.62

Teagasc National Farm Survey 201833

Table - 01C (2018) Gross Output and Direct Payments by Size (UAA - Ha) - Dairying System

Size (UAA-Ha)2 -

< 2020 -< 30

30 -< 50

50 -< 100

>= 100Hill

FarmsAll

Sizes

No. of Farms in Sample 11 15 76 140 55 14 311

Per Cent of Population 0.7 1.6 5.3 7.0 1.6 0.8 17.4

(€) GROSSOUTPUT

LIVESTOCK

Dairying 43953 70799 116546 183683 381042 118768 161419

of which milk 42465 67645 113329 180813 375142 115462 158166

Cattle 3670 12799 19007 43569 91406 21484 34695

of which Beef Data / BeefGenomics

0 0 0 54 0 39 24

Sheep & Wool 0 473 283 335 522 104 323

of which Sheep CoupledPayments

0 0 0 0 0 0 0

Pigs 0 0 0 0 0 0 0

Poultry 0 0 0 0 0 0 0

Horses 0 13 0 581 236 0 259

Other 0 0 0 0 0 0 0

Sub-Total Livestock 47623 84084 135836 228168 473206 140356 196696

of which DiseaseCompensation

667 0 526 1937 3134 0 1275

CROPS

Wheat 0 0 0 0 0 0 49

Barley - Feeding 0 0 0 0 0 0 466

Barley - Malting 0 0 0 0 0 0 225

Oats 0 0 0 0 0 0 36

Potatoes 0 0 0 0 0 0 0

Other 800 110 336 1023 1375 54 698

of which Forestry Premium 0 0 113 497 247 0 260

Sub-Total Crops 800 110 907 1823 4259 54 1473

TOTAL LIVESTOCK &CROPS

48423 84194 136743 229991 477465 140410 198169

Machinery Hire Revenue 273 1333 59 139 178 0 231

Other Current Receipts 639 15 1058 640 1596 233 780

+ Decoupled DirectPayments / Sub

5487 7808 14020 22910 39444 17667 19249

of which Single FarmPayment

4062 6178 11486 19890 36442 13153 16510

" REPS/GLAS 454 125 360 697 527 1568 555

" DAS 961 1500 1748 1981 1951 2694 1850

" Other Subsidies 9 56 563 718 697 253 549

" AEOS 0 0 46 26 0 0 25

+ Income from Land Let 0 0 18 327 404 0 176

+ Income from Quota Let 0 0 0 0 0 0 0

- Inter-EnterpriseTransfers

1223 1587 3603 6360 11517 3092 5147

TOTAL GROSS OUTPUT 53599 91814 148735 248048 507779 155247 213782

Teagasc National Farm Survey 201834

Table - 01 D (2018) Direct and Overhead Costs by Size (UAA - Ha) - Dairying System

Size (UAA-Ha) 2 - 20 - 30 - 50 - >= 100 Hill All< 20 < 30 < 50 < 100 Farms Sizes

No. of Farms in Sample 11 15 76 140 55 14 311

Per Cent of Population 0.7 1.6 5.3 7.0 1.6 0.8 17.4

DIRECT COSTS (€)

Purchased Concentrates 12782 19151 26572 49477 105273 31837 42289

Purchased Bulky Feed 2199 3439 3920 6378 13457 8568 5938

Fertiliser 2979 5205 9602 15569 34111 12001 13759

Crop Protection 72 45 280 522 1863 351 501

Purchased Seed 5 101 254 382 2035 334 454

Hire of Machinery 3674 5521 8601 12256 24684 9450 11141

Transport 40 156 169 253 563 218 236

Livestock (A.I. Vet etc.) 2944 4783 7350 11841 27397 8283 10684

Casual Labour 0 23 276 1029 2777 510 795

Other 2242 4498 6441 10149 19565 5662 8779

Sub-Total 26936 42921 63465 107856 231726 77214 94576

Fodder Crop Adjustment -563 -580 -645 -898 -3270 -2494 -1082

TOTAL DIRECT COSTS 26374 42341 62820 106959 228449 74720 93493

OVERHEAD COSTS (€)

Rent of Conacre 803 1663 2603 7295 18521 3527 5897

Car, Electricity, Phone 3984 4128 5751 7781 13492 5781 7078

Current Hired Labour 268 910 1013 6509 22035 3758 5341

Interest Charges 754 450 2259 3346 11591 1068 3289

Machinery Depreciation 2181 3491 6267 10823 19511 6337 8927

Machinery Operating 3212 4992 6513 10218 22991 5968 9263

of which Fuel & Lub 1251 1653 2267 4084 8946 2748 3560

Buildings Depreciation 1591 2328 5256 8727 17543 4730 7361

Buildings Maintenance 812 1485 2240 2728 3745 1710 2417

Land ImprovementDepreciation

24 386 820 1391 3046 793 1184

Land ImprovementMaintenance

493 975 1661 2436 3856 1448 2055

Other 2109 3889 4588 6974 10870 5695 6030

OVERHEAD COSTS 16231 24697 38970 68227 147201 40814 58843

TOTAL NET EXPENSES 42605 67038 101791 175185 375656 115534 152336

Distribution - % of farms

Costs % Output 81.5 74.0 68.9 70.3 73.4 72.8 71.2

Teagasc National Farm Survey 201835

Table - 01 E (2018) Demographic Data by Size (UAA - Ha) - Dairying System

Size (UAA-Ha)2 -

< 2020 -< 30

30 -< 50

50 -< 100

>= 100Hill

FarmsAll

Sizes

No. of Farms in Sample 11 15 76 140 55 14 311

Per Cent of Population 0.7 1.6 5.3 7.0 1.6 0.8 17.4

Holder