Embed Size (px)

Citation preview

FOREIGN BANK AND FINANCIALACCOUNTS REPORT (“FBAR”)

OUTLINE

* * *

Edward M. Robbins, Jr., Esq.Hochman, Salkin, Rettig, Toscher & Perez, P.C.

9150 Wilshire Boulevard, Suite 300Beverly Hills, California 90212

Tel. No. (310) 281-3200Fax No. (310) 859-1430

Email: [email protected]

FOREIGN ACCOUNT REPORTING ANDCOMPLIANCE UPDATE

Presented byEdward M. Robbins, Jr., Esq.

CONTENTS

OUTLINE

I. BANK SECRECY ACT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

II. FBAR STATUTORY AND REGULATORY AUTHORITY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

III. DELEGATION OF AUTHORITY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

IV. PURPOSE OF THE FBAR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

V. IRS EFFORTS TO INCREASE COMPLIANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

VI. FBAR - IN GENERAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

VII. WHO MUST FILE THE FBAR? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

VIII. DEFINITION OF A UNITED STATES PERSON . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

IX. DEFINITION OF FINANCIAL ACCOUNTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

X. DEFINITION OF FOREIGN ACCOUNTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

XI. DEFINITION OF FINANCIAL INTEREST . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

XII. DEFINITION OF SIGNATURE OR OTHER AUTHORITY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

XIII. EXEMPTIONS FROM FILING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

XIV. ACCOUNT VALUE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

XV. REPORTING FOR JOINT ACCOUNTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

XVI. RECORDKEEPING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

XVII. PENALTIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

XVIII. TAXPAYER EDUCATION AND GUIDANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

XIX. NEW IRS EXAMINATION PROCEDURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

XX. CRIMINAL PROSECUTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

XXI. RECENT IRS INITIATIVES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

XXII. HIRE ACT OF 2010 & FACTA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

APPENDIX

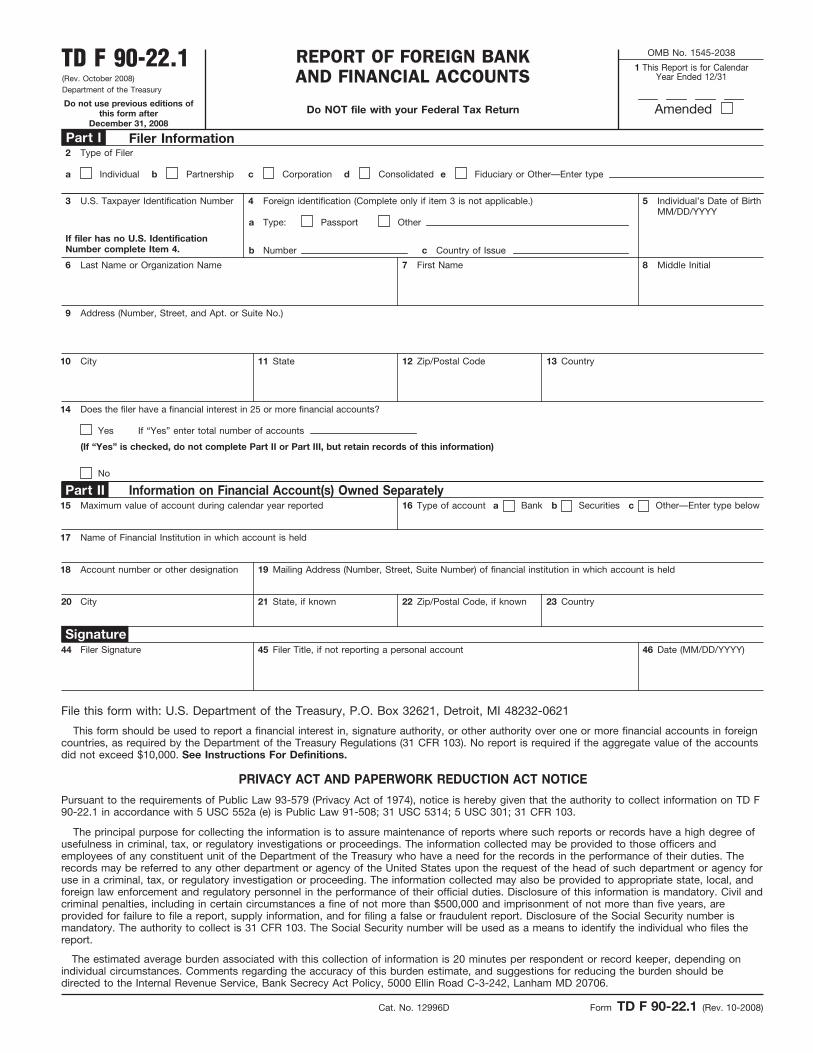

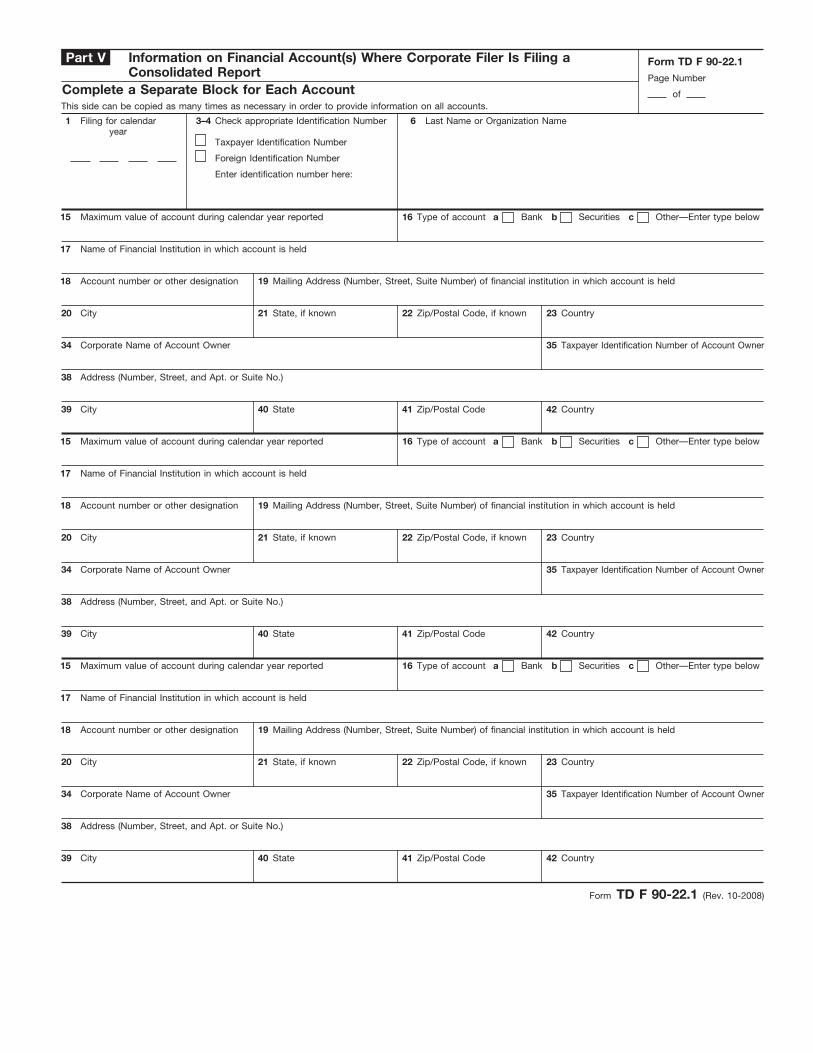

( TD F 90-22.1, REPORT OF FOREIGN BANK AND FINANCIAL ACCOUNTS- Form and Instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1

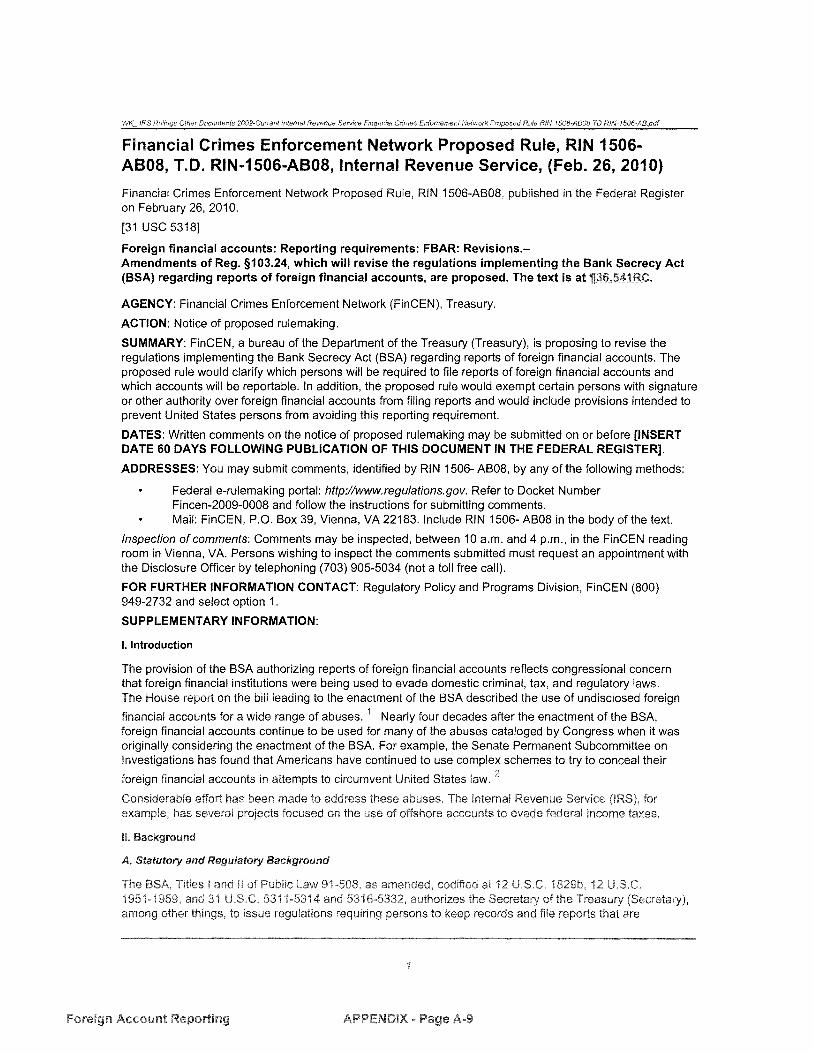

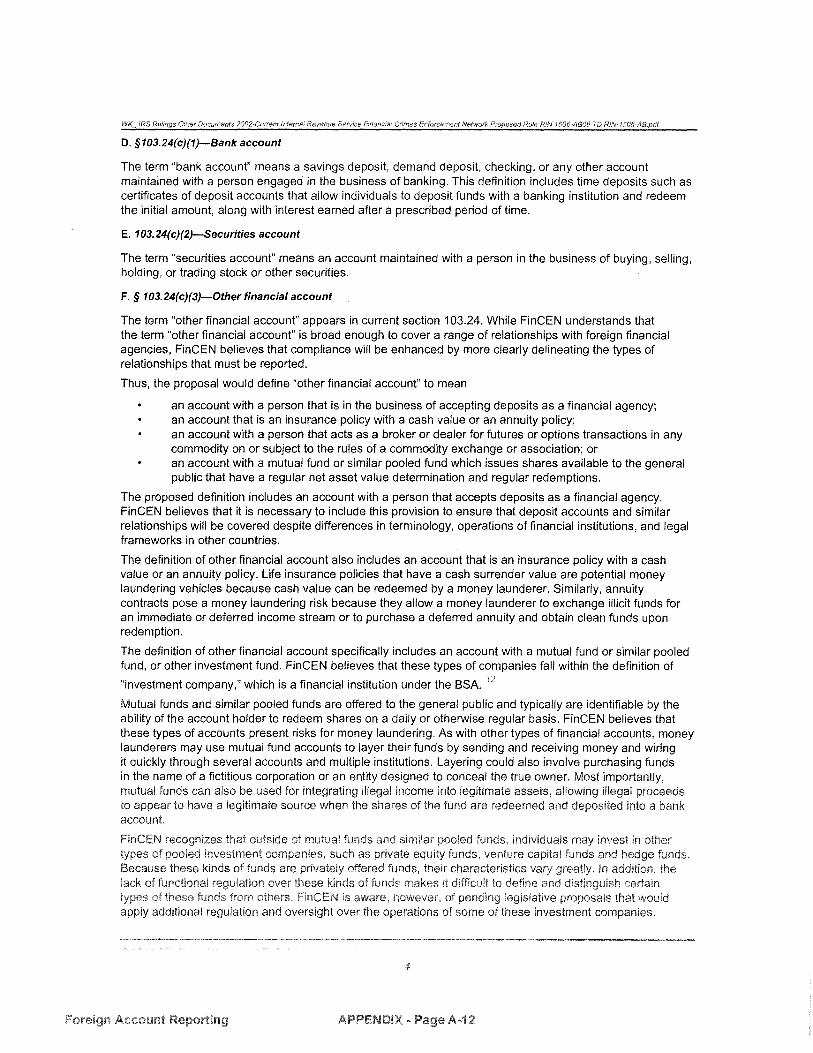

( Financial Crimes Enforcement Network Proposed Rule, RIN 1506-AB08,T.D. RIN-1506-AB08, Internal Revenue Service, February 26, 2010 . . . . . . . . . . . . . . . . . . . . . A-9

( Announcement 2010-16, I.R.B. 2010-11, March 15, 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-29

( Notice 2010-23, I.R.B. 2010-11, February 26, 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-30

( “Epilog: The IRS Penalty Memos and the Voluntary Disclosure of OffshoreAccounts,” by Charles P. Rettig and Kathryn Keneally, CCH Journal of Tax

Practice and Procedure (December 2009 – January 2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-32

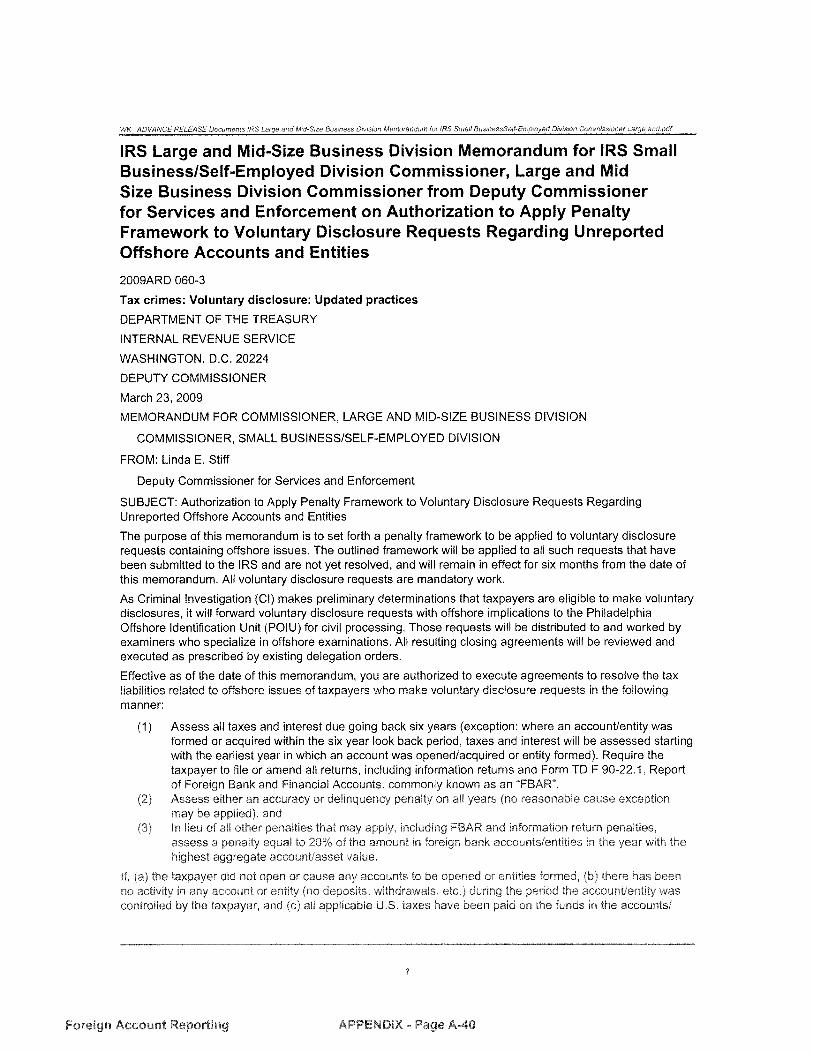

( Memorandum on Routing of Voluntary Disclosure Cases, March 23, 2009 . . . . . . . . . . . . . . . A-38

( Memorandum to Apply Penalty Framework to Voluntary Disclosure RequestsRegarding Unreported Offshore Accounts and Entities, March 23, 2009 . . . . . . . . . . . . . . . . . . A-40

( Memorandum on Emphasis on and Proper Development of Offshore ExaminationCases. Managerial Review, and Revocation of Last Chance Compliance Initiative.March 23, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-42

( “FBAR Enforcement – Five Years Later,” by Steven Toscher and Michel R. Stein,CCH Journal of Tax Practice and Procedure (June – July 2008) . . . . . . . . . . . . . . . . . . . . . . . . A-46

( FAQs Regarding Report of Foreign Bank and Financial Accounts (FBAR) - Financial Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-67

( FAQs Regarding Report of Foreign Bank and Financial Accounts (FBAR) - Filing Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-71

1Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

FOREIGN ACCOUNT REPORTING AND COMPLIANCE UPDATE

I. BANK SECRECY ACT

The Foreign Bank and Financial Accounts Report (“FBAR”) reporting requirements aregrounded in the Bank Secrecy Act (BSA) of 1970, as amended, which authorizes theSecretary of the Treasury (“Secretary”) to require residents or citizens of the UnitedStates (or a person in, and doing business in the United States) to keep records and/or filereports concerning transactions with any foreign agency. The provisions of the Actresulted from Congressional concern that foreign financial institutions located injurisdictions having laws of secrecy with respect to bank activity were being extensivelyused to violate or evade domestic criminal tax and regulatory requirements.

II. FBAR STATUTORY AND REGULATORY AUTHORITY

Statutory authority for the FBAR is 31 U.S.C. § 5314. Section 5314 directs the Secretaryof the Treasury to require a resident or citizen of the United States, or a person in anddoing business in the United States, to keep records and/or file reports when makingtransactions or maintaining a relationship with a foreign financial agency.

31 U.S.C. § 5321(a)(5) establishes civil penalties for violations of the FBAR reportingand recordkeeping requirements.

Pursuant to this authority, the Treasury promulgated regulations under §103.24:

(a) Each person subject to the jurisdiction of the United States (except aforeign subsidiary of a U.S. person) having a financial interest in, orsignature or other authority over, a bank, securities or other financialaccount in a foreign country shall report such relationship to theCommissioner of the Internal Revenue for each year in which suchrelationship exists, and shall provide such information as shall be specifiedin a reporting form prescribed by the Secretary to be filed by such persons. . . .

FBAR issues can be researched at:

A. 31 U.S.C. §5314 of the United States Code

B. 31 C.F.R. Part 103 of the Code of Federal Regulations

2Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

C. Instructions to the FBAR (which contain some rules not found in statute orregulations)

D. Internal Revenue Manual 4.26.16 (covering FBAR law)

E. Internal Revenue Manual 4.26.17 (covering FBAR procedures)

III. DELEGATION OF AUTHORITY

The Bank Secrecy Act (BSA) gave the Department of Treasury authority to establishrecordkeeping and filing requirements for United States persons with financial interestsin or signature authority, or other authority over financial accounts maintained withfinancial institutions in foreign countries. This provision of the law requires that a FormTD F 90-22.1, Report of Foreign Bank and Financial Accounts (FBAR) be filed if theaggregate balances of such foreign accounts exceed $10,000 at any time during the year.

On April 10, 2003, the Financial Crimes and Enforcement Network (FinCEN) delegatedenforcement authority to the Internal Revenue Service (IRS). The IRS is now responsiblefor:

A. Investigating possible civil violations.

B. Assessing and collecting civil penalties.

C. Issuing administrative rulings.

D. Take any other action reasonably necessary for enforcement of these and relatedprovisions, including the pursuit of injunctions.

IV. PURPOSE OF THE FBAR

The FBAR rules were established because of the utility of the information required incriminal, tax, and other regulatory matters and in the conduct of intelligence orcounterintelligence activities including analysis to protect against international terrorism.The reports filed as a result of this regulation provide leads to investigators that facilitatethe identification and tracking of illicit funds or unreported income, as well as providingadditional prosecutorial tools to combat money laundering and other crimes.

V. IRS EFFORTS TO INCREASE COMPLIANCE

3Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

Recently, Congress, the Treasury Department and the IRS have taken steps to increasecompliance--reflecting a serious effort to curb abuse in the use of offshore accounts. TheDepartment of Justice Tax Division has also added its resources to the enforcementeffort.

A. Office of Fraud/BSA - A significant step–adding some institutional continuity--was the establishment of a new IRS organization, the Office of Fraud/BSA(consisting of four territories, with about 310 field examiners reporting tomanagers located in 33 field offices nationwide) which has primary jurisdictionfor civil FBAR enforcement. Congress also expanded the civil penalties forviolations of FBAR reporting requirements, adding a new penalty for non-willfulfailures and increasing the penalty for willful violations – to potentially draconianlevels. Most recently, the IRS issued new Delegation Order 4-35 (March 24,2008), which establishes responsibility in the IRS for the various FBARenforcement functions within the IRS and has updated the Internal RevenueManual (IRM) to provide guidance to IRS personnel involved in the newenforcement initiative.

B. Education - The IRS has also made serious efforts to educate, tax professionalsand the public about the FBAR reporting requirements including hosting a IRSNational Phone Forum on FBARs in 2007.

C. Some IRS Success - It appears that FBAR compliance has improved. In 2001,the number of FBAR forms filed with the Treasury was 177,151. At the time, itwas believed that there may have been as many as one million U.S. taxpayersrequired to file an FBAR in any given year. The recent data for 2007 shows thatthere were more than 322,000 filings, almost twice the number. This representsa compliance rate of around 30% (assuming IRS estimates are correct) – leavingroom for improvement and fertile ground for IRS enforcement.

VI. FBAR - IN GENERAL

The FBAR is not a tax return, but a report filed with the Treasury stating that the personfiling has a financial interest in, or signatory authority over, financial accounts in aforeign country with an aggregate value exceeding $10,000 at any time during thetaxable year. As part of the FBAR reporting requirement, persons are instructed toindicate on their Form 1040, Schedule B, Part III, whether the individual has an interestin a financial account in a foreign country by checking “Yes or “No” in the appropriatebox. The Schedule B then directs the taxpayer to file the FBAR, which is used to reporta financial interest in or signatory authority over bank accounts in a foreign country. The

4Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

deadline for filing an FBAR for each calendar year is on or before June 30th thefollowing year - and this date cannot be extended.

The FBAR is not attached to the taxpayer’s individual income tax return. It is thereforenot subject to the stringent disclosure restrictions of Internal Revenue Code ("IRC”)Section 6013 (relating to confidentiality and disclosure of return information) and theinformation contained in the FBAR can be shared with other Federal, state and localagencies.

The prescribed Department of Treasury form is known as the Report of Foreign Bankand Financial Accounts TD F 90-22.1 (last revised in October 2008) (otherwise referredto as “FBAR”) and is available on the IRS website at www.irs.ustreas.gov. Theinstructions to the FBAR explain how compliance with the statute is achieved and setsforth in detail the required information and those person obligated to comply with theFBAR reporting requirements.

The FBAR is filed by mailing it to the U.S. Department of Treasury, P.O. Box 32621,Detroit, Michigan 48232-0621. The FBAR is considered filed when it is received inDetroit, not when it is postmarked.

VII. WHO MUST FILE THE FBAR?

A United States person must file an FBAR report if that person has financial interest in,signature authority or other authority over any financial account (s) in a foreign countryand the aggregate value of these account(s) exceeds $10,000 at any time during thecalendar year.

In order to determine whether or not the FBAR is required, all of the following arerequired:

A. The filer is a United States (“US”) Person;

B. The US Person has a financial account;

C. The financial account is in a foreign country;

D. The US Person has a financial interest in the account or signature or otherauthority over the foreign financial account; and

5Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

E. The aggregate amount(s) in the account(s) valued in dollars exceed $10,000 at anytime during the calendar year.

VIII. DEFINITION OF A UNITED STATES PERSON

A “United States person” is a citizen or resident of the United States.

A. Citizen - Look for US birth certificate or naturalization papers.

B. Resident - Not defined in FBAR instructions, statute or regulations. Look to

1. Green Card Test

2. Substantial presence test

3. Persons file a first year election on his income tax return to be treated as aresident alien

C. A person living in and doing business in the United States.

D. The term "person" includes individuals and all forms of business entities, trusts,and estates.

1. A certificate of incorporation from a US State establishes that thecorporation is a US person.

2. A foreign subsidiary of a US person is not subject to the FBAR filingrequirements. The US parent will be considered to have a financial interestin any foreign financial account owned by its subsidiary.

3. A corporation that owns directly or indirectly more than 50 percent interestin one or more other entities is permitted to file a consolidated FBAR. Theconsolidated report must include the list of entities. An authorized officialof the parent corporation should sign the consolidated FBAR.

IX. DEFINITION OF FINANCIAL ACCOUNTS

A financial account is:

A. Bank accounts such as savings accounts, checking accounts, and time deposits.

6Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

B. Securities accounts such as mutual funds, brokerage accounts, and securitiesderivatives accounts.

C. Accounts where the assets are held in a commingled fund and the account ownerholds an equity interest in the fund.

D. Any other account(s) maintained in a foreign financial institution or with a persondoing business as a financial institution.

E. An insurance policy having a cash surrender value.

F. NOT individual bonds, notes, or stock certificates held by the filer.

X. DEFINITION OF FOREIGN ACCOUNTS

Foreign financial accounts include accounts that are located outside all geographicalareas of the United States, including outside the:

- United States- Northern Mariana Islands - District of Columbia - American Samoa - Guam - Puerto Rico - U.S. Virgin Islands - Trust Territories of the Pacific Islands

The location of the account, and not the nationality of the financial institution with whichthe account is held, determines whether the account is in a foreign country. Anyfinancial account that is located in a foreign country should be reported, even if theaccount is held with a branch of a US financial institution located abroad.

XI. DEFINITION OF FINANCIAL INTEREST

Financial interest includes accounts for which the U.S. person is the owner of record orhas legal title, whether the account is maintained on his or her own benefit or for thebenefit of others including non-United States persons.

7Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

A. Financial interest also includes accounts where the owner of record or holder oflegal title is a person acting as an agent, nominee, or in some other capacity onbehalf of a U.S. person.

Example: John, a U.S. citizen who resides in Mexico, granted his brotherPaul, a U.S. citizen, a Power of Attorney to access his Mexican bankaccounts. Paul is the owner of record.

John has a financial interest in the account. Paul is acting onlyas an attorney on behalf of John. Paul also has a financialinterest in the account, since he is the owner of record. BothJohn and Paul must file an FBAR.

Example: Given the information in the above example, if Paul is a Mexicancitizen, must he file the FBAR?

No. Paul is not considered to be a U.S. person.

B. Financial interest in an account also includes a corporation in which a U.S. persondirectly or indirectly owns more than 50 percent of the total value of the shares ofstock.

Example: A Florida corporation that owns 100% of a foreigncompany that has foreign financial accounts has to file an FBARbecause the corporation is a U.S. person and the owner of record orholder of legal title is a corporation that directly owns more than50% of the total value of the shares of stock.

Example: A U.S. person who owns 75% of the Florida corporation in theprevious example has to file an FBAR because he indirectly owns morethan 50% of the total value of shares of stock of the foreign corporation.

C. Financial interest also includes an account where the owner of record or holder oflegal title is:

1. A partnership in which the U.S. person owns interest in more than 50% ofthe profits.

8Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

2. A trust in which the U.S. person either has a present beneficial interest inmore than 50% of the assets or receives more than 50% of the currentincome.

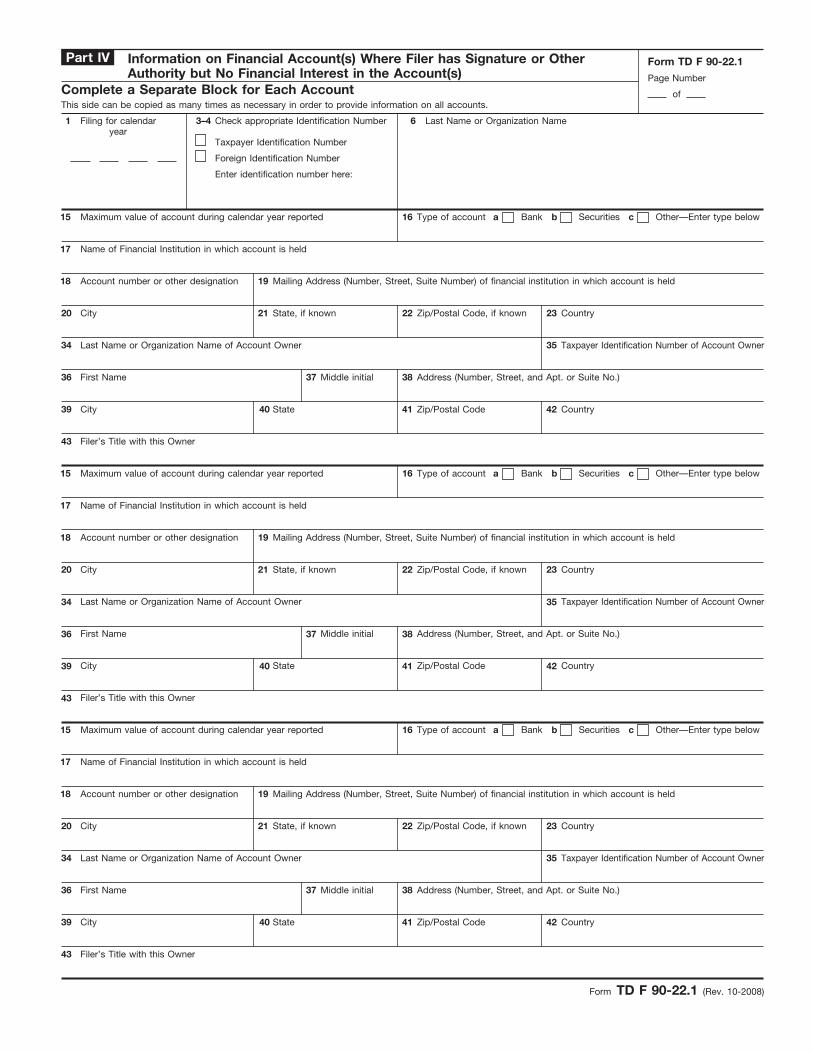

XII. DEFINITION OF SIGNATURE OR OTHER AUTHORITY

A person having signature or other authority over a financial account must file the FBAReven if the person has no financial interest in the account.

A U.S. person has account signature authority if that person can control the dispositionof money or other property in the account by delivery of a document containing hissignature to the bank or other person with whom the account is maintained.

A person with other authority over an account is one who can exercise power that iscomparable to signature authority over an account by direct communication, either orallyor by some other means to the bank or other person with whom the account ismaintained.

Example: A person who has the power to direct how an account is investedbut cannot make disbursements or deposits to the account does not have tofile an FBAR because the person has no power of disposition.

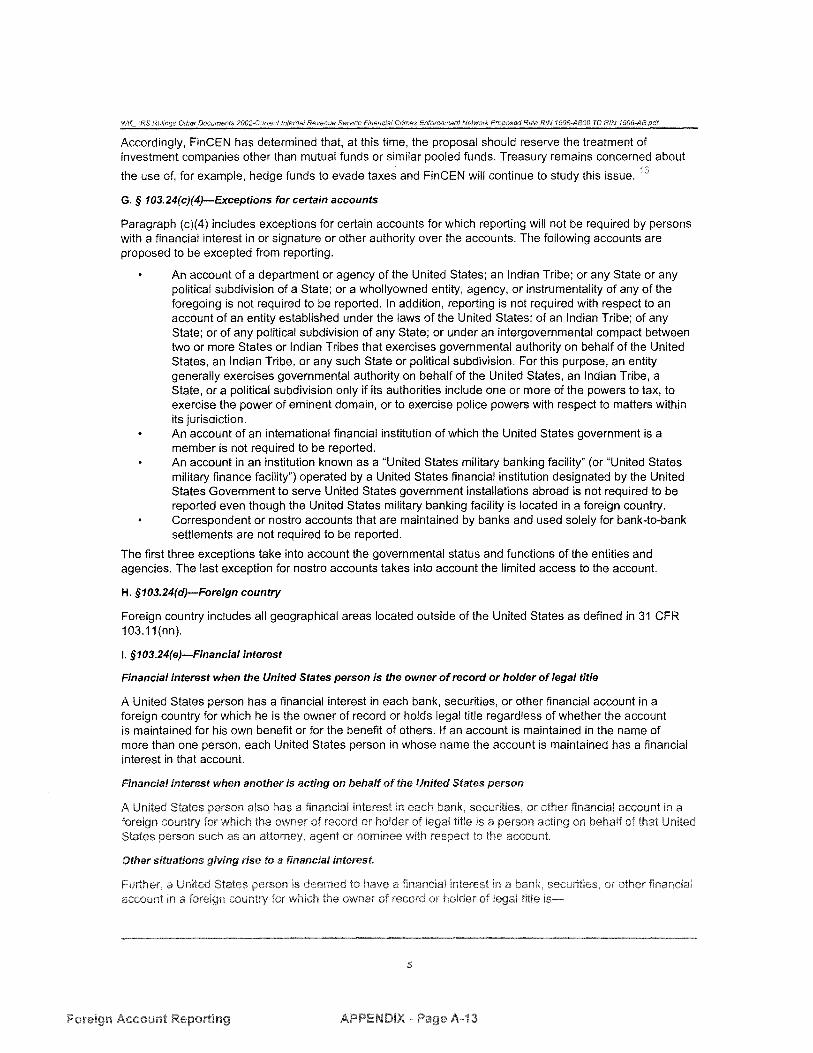

XIII. EXEMPTIONS FROM FILING

The following types of accounts and persons are exempt from the FBAR filingrequirement:

A. Accounts held in a military banking facility operated by a United States financialinstitution designated by the United States Government to serve U.S. Governmentinstallations located abroad.

B. Officers or employees of a bank under the supervision of the Comptroller of theCurrency, the Board of Governors of the Federal Reserve System, the Office ofThrift Supervision, or the Federal Deposit Insurance Corporation are exempt fromfiling the FBAR, if that officer or employee has NO personal financial interest inthe account.

C. Officers or employees of a domestic corporation whose equity securities are listedon national securities exchanges, or which has assets exceeding $10 million and

9Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

500 or more shareholders of record, need not file an FBAR concerning the othersignature authority over a foreign financial account of the corporation, if:

1. the officer or employee has NO personal financial interest in the account,and

2. has been advised in writing by the chief financial officer of the corporationthat the corporation has filed a current report which includes that account.

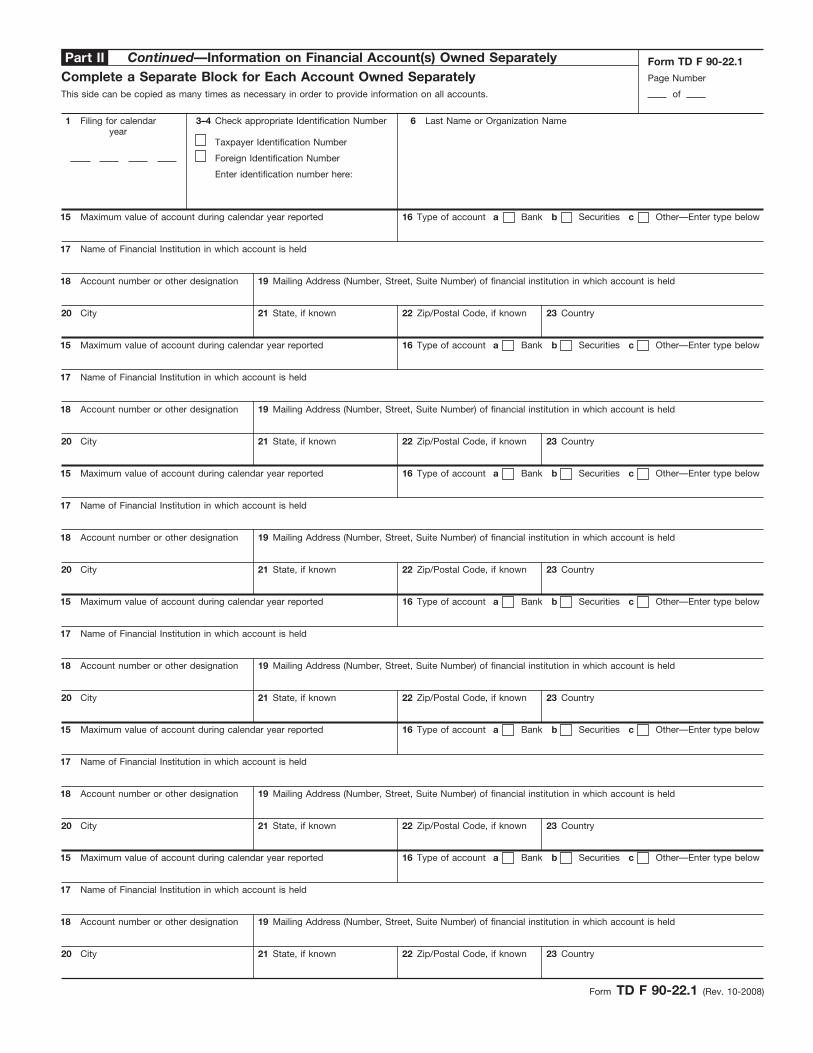

XIV. ACCOUNT VALUE

The FBAR is required for each calendar year during which the aggregate amount(s) inthe account(s) exceeded $10,000 valued in U.S. dollars at any time during the calendaryear. The maximum value of an account is the largest amount of currency and non-monetary assets that appear on any quarterly or more frequent account statement issuedfor the applicable year.

Example: If the statement closing balance is $9,000 but at any time duringthe year a balance of $15,000 appears on a statement, the maximum valueis $15,000.

If a periodic account statement is not issued, the maximum account value is the largestamount of currency and/or monetary instruments in the account at any time during theyear. If the account value exceeds $10,000 on any account statement at any timeduring the calendar year an FBAR must be filed.

Convert foreign currency by using the official exchange rate in effect at the end of theyear in question for converting the foreign currency into U. S. dollars. Historicalexchange rates will be needed to determine the value in a foreign account in prior years.

The value of stock, other securities, or other non-monetary assets in an account reportedon the FBAR is the fair market value at the end of the calendar year, or if withdrawnfrom the account earlier in the year, at the time of the withdrawal.

If the filer had a financial interest in more than one account, each account is valuedseparately in accordance with the previous paragraphs.

.

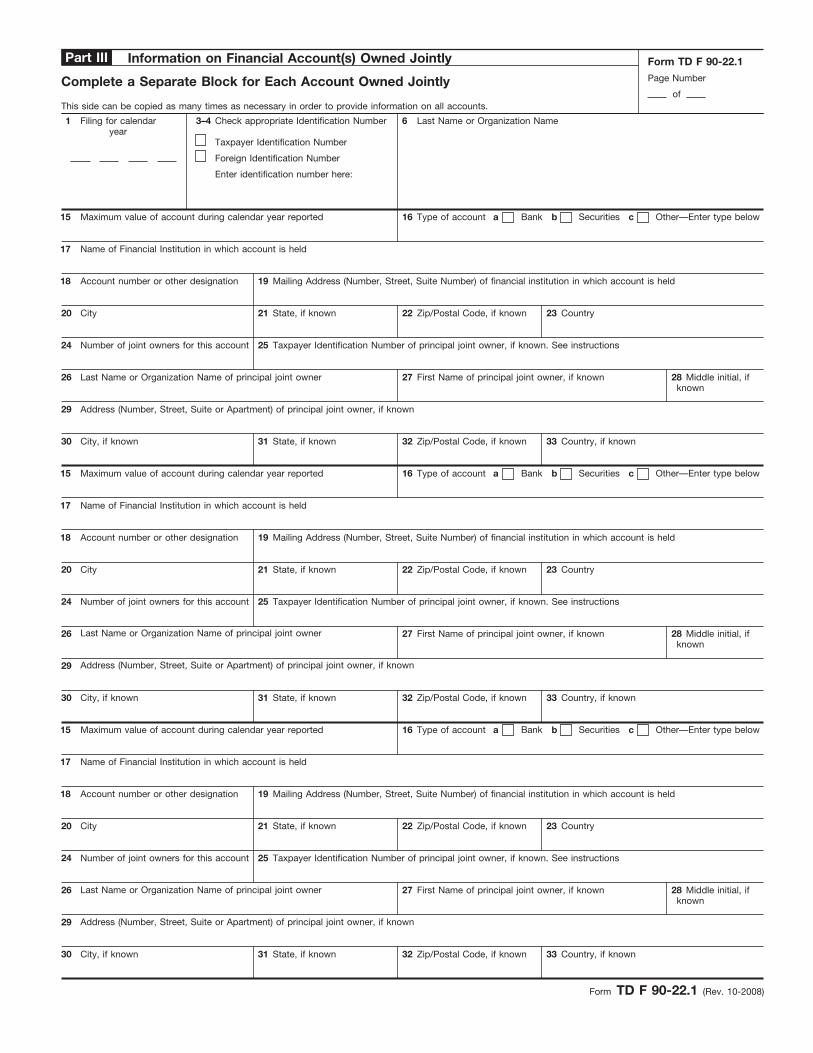

XV. REPORTING FOR JOINT ACCOUNTS

10Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

If two persons jointly maintain an account, or if several persons each own a partialinterest in an account, then each U.S. person has a financial interest in that account andeach person must file an FBAR.The IRS will accept a single FBAR for an account jointly held by husband and wife. Aspouse having a joint financial interest in an account with the filing spouse should beincluded as a joint account owner in Part III of the FBAR. The filer should write (spouse)on line 26 after the last name of the joint spousal owner. If the only reportable accountsof the filer's spouse are those reported as joint owners, the filer's spouse need not file aseparate report. If the accounts are owned jointly by both spouses, the filer's spouseshould also sign the report. It should be noted that if the filer's spouse has a financialinterest in other accounts that are not jointly owned with the filer or has signature orother authority over other accounts, the filer's spouse should file a separate report for allaccounts including those owned jointly with the other spouse.

XVI. RECORDKEEPING

FBAR records should be kept for five years from the due date of the report which is June30 of the following calendar year. The records should contain the following:

A. Name maintained on each account.

B. Number or other designation of the account.

C. Name and address of the foreign bank or other person with whom the account ismaintained.

D. Type of account.

E. Maximum value of each account during the reporting period.

Retaining a copy of the FBAR is not required. However, a copy of the FBAR formcontains most of the required information (but not address of foreign institution ormaximum values).

XVII. PENALTIES

11Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

The IRS has been delegated authority to assess FBAR civil penalties. The main penaltiesapplicable to FBARs are the (1) Non-Willful and (2) Willful penalties. The Job CreationAct of 2004 (“Jobs Act) added a new civil penalty for violations of FBAR reportingrequirements, whether or not the violation was willful, and an increased the existingpenalty for willful violations.

The FBAR penalties are determined per account, not per unfiled FBAR, for each personrequired to file. Penalties apply for each year of violation. As noted below, however,examiners are expected to exercise discretion, taking into account the facts andcircumstances of case, in determining whether penalties should be asserted and the totalamount of penalties to be asserted.There may be multiple FBAR civil penalties assessments arising from one account.There may be multiple penalties assessments if there is more than one account owner orif a person other than the account owner has signature or other authority over the foreignaccount. Each person can be liable for the full amount of the penalty.

A. Non-Willful Penalty - Under the changes, which apply to violations after October22, 2004 (the date of Jobs Act enactment), that is, FBAR forms due on or aferJune 30, 2005, the IRS may now impose a civil monetary penalty not exceeding$10,000, on anyone who violates, or causes any violation, of the FBAR reportingrequirement rules. This penalty, which did not previously exist, eliminates theneed for the IRS to prove willfulness - a main barrier to its ability to impose anyFBAR civil penalty in the past.

1. The penalty may be waived, however, if both of the following are met:

a. “such violation was due to reasonable cause”; and

b. “the amount of the transaction or the balance in the account at thetime of the transaction was properly reported.”

2. Reasonable Cause

a. With respect to the first part of the waiver provision – the“reasonable cause” requirement, the IRS will most likely turn to thereasonable cause standard set forth in existing Internal RevenueCode (“IRC”) sections, regulations and internal revenue manualprovisions.

3. Properly Reported

12Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

a. It is less certain what Congress meant by the reporting requirement– that is, “the amount of the transaction or the balance in the accountat the time of the transaction was properly reported.”

b. The Senate Finance Committee Report (S. Rep. No. 108-192) shedssome light on congressional intent by stating that “[t]he penalty maybe waived if any income from the account was properly reported onthe income tax return and there was reasonable cause for the failureto report. However, it is unclear what actions besides the reportingof income will satisfy the reporting requirement, and there are manyunanswered questions.

(1) Would checking “yes” on the Form 1040, Schedule B, PartIII, be sufficient to satisfy the reporting requirement?

(2) Does prior year reporting of income from the account orFBAR reporting satisfy this requirement?

(3) Also, how does one report the amount of the transaction in thecontext of the FBAR?

(4) Upon whom does the burden of proof rest with respect to non-willful penalty?

(5) Is reporting some, but not all, of the income from a foreignaccount sufficient to satisfy the reporting requirement? Atleast for the last question, it would appear that reporting “any”of the income would be sufficient.

c. The IRS interprets the provision to mean that the examiner musthave received the delinquent FBARs from the non-filer in order toavoid application of the non-willful penalty.

B. Willful Penalty - The Jobs Act also increased the civil penalty for willfulviolations. Under the changes, the civil penalty for willful violations has beenincreased to the greater of $100,000 or 50 percent of the amount of the transactionor the balance in the account at the time of the violation.

13Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

1. This is a significant increase from the penalty that applies to violationsexisting on or before October 22, 2004, where the civil penalty amount islimited to the greater of $25,000 or the balance in the account at the timeof violation, up to a maximum of $100,000 per violation.

Example: Under the new statute, if an individual with aforeign financial account containing $1 million is found to bein willful violation of the statute, the penalty could be as muchas $500,000 - a very steep penalty indeed.

2. Willful Standard

a. The willfulness penalty applies to any person who has willfullyviolated the FBAR reporting or recordkeeping provisions.

b. The test for willfulness is whether there was a voluntary, intentionalviolation of a known legal duty.

c. The burden of establishing willfulness is on the IRS.

d. If it is determined that the violation was due to reasonable cause, thewillfulness penalty should not be asserted.

e. Willfulness is shown by the person’s knowledge of the reportingrequirements and the person’s conscious choice not to comply withthe requirements. In the FBAR situation, the only thing that a personneed know is that he has a reporting requirement. If a person has thatknowledge, the only intent needed to constitute a willful violation ofthe requirement is a conscious choice not to file the FBAR.

f. Examples: The following examples from the Internal RevenueManual illustrate situations in which willfulness may be present:

(1) A person admits knowledge of, and fails to answer, a questionconcerning signature authority over foreign bank accounts onSchedule B of his income tax return. When asked, the persondoes not provide a reasonable explanation for failing toanswer the Schedule B question and for failing to file theFBAR. A determination that the violation was willful likelywould be appropriate in this case.

14Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

(2) A person files the FBAR, but omits one of three foreign bankaccounts. The person had closed the omitted account at thetime of filing the FBAR. The person explains that theomission was due to unintentional oversight. During theexamination, the person provides all information requestedwith respect to the omitted account. The information provideddoes not disclose anything suspicious about the account, andthe person reported all income associated with the account onhis tax return. The willfulness penalty should not apply absentother evidence that may indicate willfulness.

(3) A person filed the FBAR in earlier years but failed to file theFBAR in subsequent years when required to do so. Whenasked, the person does not provide a reasonable explanationfor failing to file the FBAR. In addition, the person may havefailed to report income associated with foreign bank accountsfor the years that FBARs were not filed. A determination thatthe violation was willful likely would be appropriate in thiscase.

(4) A person received a warning letter informing him of theFBAR filing requirement, but the person continues to fail tofile the FBAR in subsequent years. When asked, the persondoes not provide a reasonable explanation for failing to filethe FBAR. In addition, the person may have failed to reportincome associated with the foreign bank accounts. Adetermination that the violation was willful likely would beappropriate in this case.

C. Penalty Mitigation Guidelines

Recognizing its discretionary authority, and in order to promote consistency byIRS employees in exercising this discretion, the IRS has adopted PenaltyMitigation Guidelines for Calculation of FBAR Civil Penalty for its personnel.

Penalties should be asserted only to promote compliance with the FBAR reportingand recordkeeping requirements. In exercising their discretion, examiners shouldconsider whether the issuance of a warning letter and the securing of delinquent

15Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

FBARs, rather than the assertion of a penalty, will achieve the desired result ofimproving compliance in the future.

FBAR civil penalties have varying upper limits, but no floor. The examiner hasdiscretion in determining the amount of the penalty, if any. Examiner discretionis necessary because the total amount of penalties that can be applied under thestatute can greatly exceed an amount that would be appropriate in view of theviolation.

Examiners are expected to exercise discretion, taking into account the facts andcircumstances of each case, in determining whether penalties should be assertedand the total amount of penalties to be asserted. Because FBAR penalties do nothave a set amount, IRS has developed penalty mitigation guidelines to assistexaminers in the exercise of their discretion in applying these penalties. Themitigation guidelines are only intended as an aid for the examiner in determiningan appropriate penalty amount.

1. Guidelines For Violations Occurring Prior to October 23, 2004

a. Four Conditions - If all four of the following conditions aresatisfied, the Penalty Mitigation Guidelines would subject a personto less than the maximum authorized FBAR penalty. The Guidelinesgenerally provide that the amount of the penalty imposed would belimited to a percentage (i.e., either 5% or 10%) of the maximumamount in the foreign account (up to a maximum penalty of$100,000) for each foreign account that should have been reported,depending upon the amount in each account. In contrast, forsituations where a person does not qualify for the FBAR penaltyreduction (i.e., where the taxpayer fails to satisfies any one of thefour conditions), then generally the maximum penalty authorizedwill be asserted.

(1) The person has no history of past FBAR penalty assessment;

(2) No money passing through any of the foreign accountsassociated with the person was from an illegal source or usedto further a criminal purpose;

(3) The person cooperated during the examination; and

16Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

(4) The IRS did not determine a civil fraud penalty against theperson for an underpayment for the year in question due to thefailure to report income related to any amount in a foreignaccount.

2. Mitigation Guidelines - The method of calculating the penalty under theGuidelines varies from account to account depending upon the applicablepenalty Level involved. The Guidelines set forth four penalty Levels.

a. Level I Penalty. A Level I penalty applies if the maximumaggregate balances for all unreported foreign accounts that shouldhave been reported does not exceed $20,000. For Level I cases, thepenalty will be 5% of the maximum balance during the calender yearfor each of the foreign accounts that should have been reported.

b. Level II Penalty. A Level II penalty applies if the maximumbalance during the year for an unreported account that should havebeen reported is not more than $250,000 (and the Level 1 penalty isnot applicable). For Level II cases, the penalty will be 10% of themaximum balance during the calender year for each of the foreignaccounts that should have been reported.

c. A Level III Penalty. A Level III penalty applies if the maximumbalance during the year for an unreported account that should havebeen reported is greater than $250,000 but not more than $1 million. For Level III cases, the penalty will be the lesser of: a) 10% of themaximum balance during the calender year for each of the foreignaccounts that should have been reported; or b) the amount in theaccount as of the last day for filing the FBAR (unless this amount isless than $25,000, in which case the penalty is $25,000).

d. A Level IV Penalty. A Level IV penalty applies if the maximumbalance during the year that should have been reported exceeds $1million. For Level IV cases, the penalty will be the lesser of: a)$100,000; or b) the amount in the account as of the last day for filingthe FBAR (unless this amount is less than $25,000, in which case thepenalty is $25,000).

3. Guidelines For Violations Occurring After October 22, 2004

17Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

a. Four Conditions - If all four of the following conditions aresatisfied, the Penalty Mitigation Guidelines would subject a personto less than the maximum authorized FBAR penalty.

(1) The person has no history of past FBAR penalty assessmentsand no history of criminal tax or BSA convictions for thepreceding ten years.

(2) No money passing through any of the foreign accountsassociated with the person was from an illegal source or usedto further a criminal purpose;

(3) The person cooperated during the examination; and

(4) The IRS did not determine a civil fraud penalty against theperson for an underpayment for the year in question due to thefailure to report income related to any amount in a foreignaccount.

b. Mitigation Guidelines for Non-Willful Penalty The method ofcalculating the penalty under the Guidelines varies from account toaccount depending upon the applicable penalty Level involved. TheGuidelines set forth three penalty Levels for non-willful violations.

(1) A Level I Non-Willful Penalty. If the aggregate balance ofall accounts held during the year does not exceed $50,000,then the penalty for each violation is $500, not to exceed atotal of $5,000 in penalties.

(2) A Level II Non-Willful Penalty. If the aggregate balance ofthe accounts is over $50,000, but less than $250,000, thepenalty is, per violation, the lesser of $5,000 or 10 per cent ofthe highest balance in the account during the year for whichthe account should have been reported.

(3) A Level III Non-Willful Penalty. For violations regarding anaccount exceeding $250,000, the penalty per violation is thestatutory maximum of $10,000.

18Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

4. Mitigation Guideline for Willful Penalty. The method of calculating thepenalty under the Guidelines varies from account to account dependingupon the applicable penalty Level involved. The Guidelines set forth fourpenalty Levels for non-willful violations.

a. A Level I Willful Penalty. If the maximum aggregate balance for allaccounts to which the violations relate did not exceed $50,000, LevelI applies to all accounts . Determine the maximum balance during thecalendar year for each account. Add the various maximums to findthe maximum aggregate balance. The Level I penalty is the greaterof $1,000 per violation or 5% of the maximum account balanceduring the calendar year for each Level I account.

b. A Level II Willful Penalty. If Level I does not apply and if themaximum account balance to which the violations relate at any timeduring the calendar year did not exceed $250,000, Level II appliesto that account. The Level II penalty assessed for each account is thegreater of $5,000 per violation or 10% of the maximum accountbalance during the calendar year for each Level II account.

c. A Level III Willful Penalty. If the maximum account balance towhich the violations relate at any time during the calendar yearexceeded $250,000 but did not exceed $1,000,000, Level III appliesto that account. The Level III penalty assessed for each account is thegreater of 10% of the maximum account balance during the calendaryear for each Level III account or 50% of the closing balance in theaccount as of the last day for filing the FBAR .

d. A Level IV Willful Penalty. If the maximum account balance towhich the violations relate at any time during the calendar yearexceeded $1 million, Level IV, the statutory maximum, applies tothat account. The Level IV penalty is the statutory maximum appliedto each account. It is the greater of $100,000 or 50% of the closingbalance in the account as of the last day for filing the FBAR.

D. Criminal Penalties - The Jobs Act made no changes to criminal FBAR penaltiesunder IRC §5322. Criminal violations of the FBAR rules can still result in a fineof not more than $ 250,000 or 5 years in prison or both. Where the failure to filean FBAR is part of a pattern of illegal activity, the statute provides for a fine ofup to $500,000 and imprisonment of up to 10 years or both.

19Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

1. The statute states that the civil penalty can be imposed despite the fact thata criminal penalty is imposed with respect to the same violation.

E. Statute of Limitations to Assess Penalties - The Secretary has six years to assessa FBAR civil penalty, and once assessed, a limitation period of two years fromthe date of assessment to bring an action to recover an unpaid penalty. The statuteof limitations for criminal BSA violations is five years.

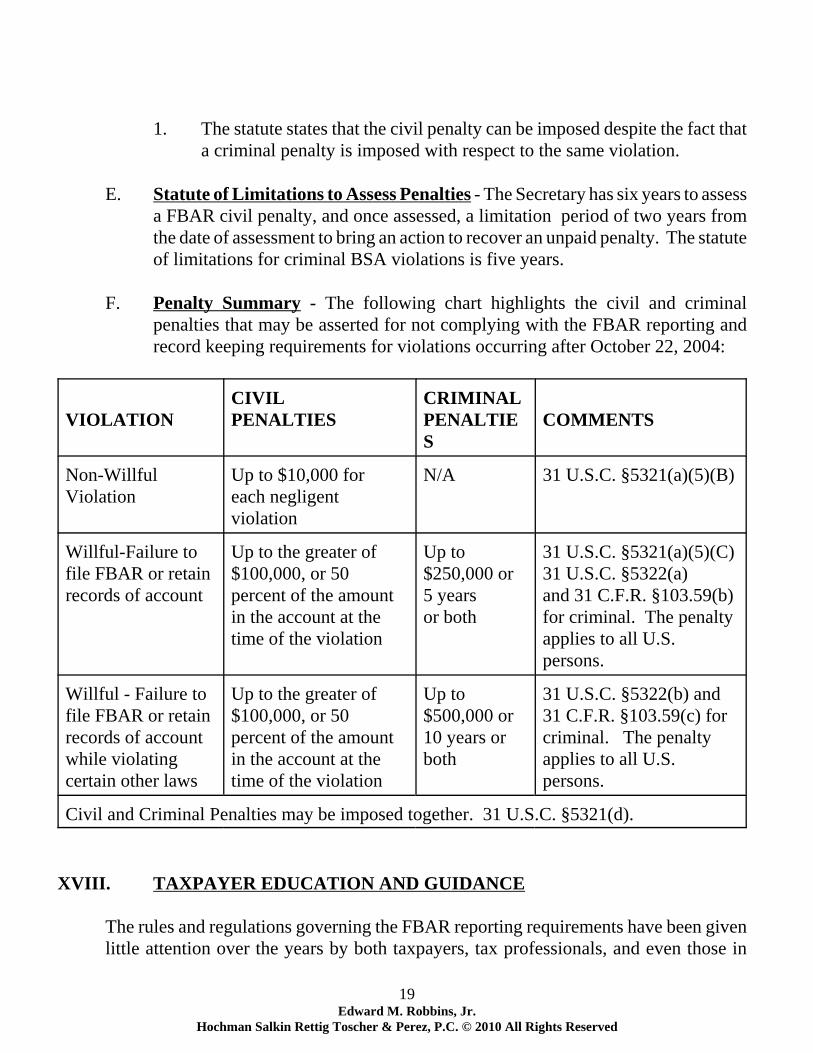

F. Penalty Summary - The following chart highlights the civil and criminalpenalties that may be asserted for not complying with the FBAR reporting andrecord keeping requirements for violations occurring after October 22, 2004:

VIOLATIONCIVIL PENALTIES

CRIMINALPENALTIES

COMMENTS

Non-WillfulViolation

Up to $10,000 foreach negligentviolation

N/A 31 U.S.C. §5321(a)(5)(B)

Willful-Failure tofile FBAR or retainrecords of account

Up to the greater of$100,000, or 50percent of the amountin the account at the time of the violation

Up to$250,000 or5 yearsor both

31 U.S.C. §5321(a)(5)(C)31 U.S.C. §5322(a)and 31 C.F.R. §103.59(b)for criminal. The penaltyapplies to all U.S.persons.

Willful - Failure tofile FBAR or retainrecords of accountwhile violatingcertain other laws

Up to the greater of$100,000, or 50percent of the amountin the account at thetime of the violation

Up to$500,000 or10 years orboth

31 U.S.C. §5322(b) and31 C.F.R. §103.59(c) forcriminal. The penaltyapplies to all U.S.persons.

Civil and Criminal Penalties may be imposed together. 31 U.S.C. §5321(d).

XVIII. TAXPAYER EDUCATION AND GUIDANCE

The rules and regulations governing the FBAR reporting requirements have been givenlittle attention over the years by both taxpayers, tax professionals, and even those in

20Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

Government charged with enforcing these requirements. Since the IRS took overenforcement responsibilities from FINCEN in 2003, much more attention is being paidto the reporting requirements. While many issues remain outstanding, the IRS has madesubstantial progress.

Historically, taxpayers and their advisors seeking to determine whether there was aFBAR filing obligation were limited to consulting the instructions attached to the form.That, however, is changing with the IRS establishing a unit where taxpayers and theirclients can seek guidance. While many questions remain, many have been answered –at least from the IRS’ viewpoint.

On June 20, 2007, the IRS held a National Phone Forum to disseminate information tothe public regarding the FBAR. The IRS provided an overview of the FBAR’spurpose, reporting requirements, penalties and compliance initiatives. As part of theprogram, the tax community was offered the opportunity to submit questions. In whatproved to be a valuable component to the Forum, the IRS disseminated in writing thequestions and answers from the Program. The FBAR Questions and Answers (FBARQ&A) indicate that they were approved by the SB/SE Counsel on October 22, 2007. TheFBAR Q&A provided a valuable source of information to guide tax professionals andtheir clients about FBAR compliance issues. Many previously unanswered questionswere addressed in the Q&A FBAR and some of the more significant issues are discussedbelow.

A. Aggregate Value - The FBAR reporting requirement is triggered if the aggregatevalue of the financial accounts exceeds $10,000 at any time during the calendaryear. The FBAR Q&A clarifies that the largest value during the year isdetermined separately for each account (including those that did not exceed$10,000) and then the accounts are added together. If the aggregate value of theboth accounts exceed $10,000, then all accounts must be included on the FBARform. The aggregate value is determined using the largest amount that appearson the bank statement, and not merely the ending balance. Thus, if a taxpayer hadtwo accounts during the year and at one point one account had $5,100 and $5,000of the account was transferred to another account during the year, the IRS expectsan FBAR to be filed–even though the taxpayer never had more than $5,100 duringthe year.

B. Due Diligence Regarding FBARs - Circular 230 requires that a practitionerexercise due diligence in preparing or assisting in the preparation or, approvingand filing of tax returns, documents or other papers relating to IRS matters. TheFBAR Q&A states that in most cases, if (1) the preparer asks if the taxpayer had

21Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

a foreign account and the answer is no, and (2) if the preparer has no reason tobelieve that the taxpayer has foreign investment account, that should be sufficientto demonstrate due diligence on the part of the tax preparer.

The FBAR Q & A would seem to require that all preparers ask the taxpayer thisquestion – which does not seem to have been the practice in the past – at least formost preparers. While the foreign bank account question is found in most taxorganizers sent to taxpayers, they are not used in all cases and in many cases, thetaxpayers never complete the organizer. Moreover, most tax return softwareprograms default to the answer “no” when it comes to this question. The IRSwould no doubt like to enlist tax preparers in their effort to increase FBARcompliance and given increased IRS enforcement focus on preparers and preparerpenalties, it is not too far afield to anticipate that if a taxpayer violation is found,the focus could turn to the preparer as to whether due diligence was exercisedunder Circular 230.

C. Fax Signatures - The FBAR requires a signature, but does not contain a penaltyof perjury statement. The FBAR Q&A states that the IRS does not accept a faxsignature on the FBAR. However, if the taxpayer is pressed for time, the FBARshould be filed with a fax signature. The taxpayer should follow up with anAmended FBAR with an original signature with an explanation of the why theoriginal signature was obtained late.

D. Foreign Branch of US Bank - The FBAR Q&A states that a bank account in abranch of a United States bank that is located in a foreign country is considereda foreign account requiring the FBAR disclosure requirements. However, anaccount with a US military banking facility that services US Governmentinstallations overseas need not be reported on an FBAR, even though the accountmay be located in foreign country. For FBAR reporting purposes, Puerto Rico,the Virgin Islands, Northern Mariana Islands and the Territories and Possessionof the United States are not considered to be foreign countries.

E. Foreign Life Insurance Policies & Other Assets - The term “financial accounts”for FBAR reporting purposes is broadly defined to include any bank, securities,savings, demand, checking, deposit, time deposit or any other account maintainedwith a financial institution. The FBAR Q&A states that if the cash surrendervalue insurance policy can be used to store cash that can be withdrawn at a latertime, it would be treated as a financial account for FBAR reporting purposes. Ifthe policy is located overseas, and the cash surrender value exceeds $10,000, thepolicy holder should report the policy on an FBAR. Policies acquired in the

22Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

United States from an insurance agent in the United States are not policies locatedoverseas.

According to the FBAR Q&A, an account holding gold bullion is considered areportable account. Whereas an investment in an interest bearing security issuedby a foreign government, such as savings bonds, acquired through a bank in theUnited States or mutual funds located in the United States that invest in securitieslocated in a foreign country, does not create a FBAR obligation. Lines of creditor an ownership interest in real estate are not interests in foreign financialaccounts.

F. Postmarks - Tax returns are considered timely on the day they are mailed. FBARs are not tax returns and according to the FBAR Q&A, are considered filedon the day they are received, not on the date they were mailed.

G. Delinquent FBARs, Penalties and Voluntary Disclosures - The IRS providedimportant insight how it will treat taxpayers with no previous knowledge of theFBAR requirement who would like to get into compliance. The FBAR Q&Astates that the taxpayer should file any FBAR that was required during the past sixyears and attach an explanation as to why the FBARs were delinquent. Nopenalty will assessed if there was reasonable cause for not filing the FBAR.

It was stated during the Forum that the IRS does not have a formal voluntarydisclosure policy specifically related to FBARS, but it was suggested that it wouldbe highly unlikely that the IRS would investigate and attempt to penalizetaxpayers who voluntarily come forward and file.

XIX. NEW IRS EXAMINATION PROCEDURES

On January 1, 2007, the IRS revised the Internal Revenue Manual (“IRM”) provisionsrelating to the Bank Secrecy Act Chapter (IRM 4.26.17) to set forth FBAR examinationprocedures not previously formalized in writing. On May 5, 2008, the IRS revised IRM4.26.17, modifying and superceding portions of IRM 4.26.17.

The new manual provisions set forth the procedures to be followed by IRS examiners inthe Small Business/Self Employed (SB/SE) division who are responsible for enforcingcompliance with the reporting and record keeping requirements of the FBAR. Theseprovisions also provide helpful guidance for tax professionals whose clients are underFBAR examination. The new IRM provisions sets forth procedures for initiating and

23Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

closing FBAR investigations, investigation procedures, and procedures for potentialreferrals of FBAR violations for criminal enforcement.

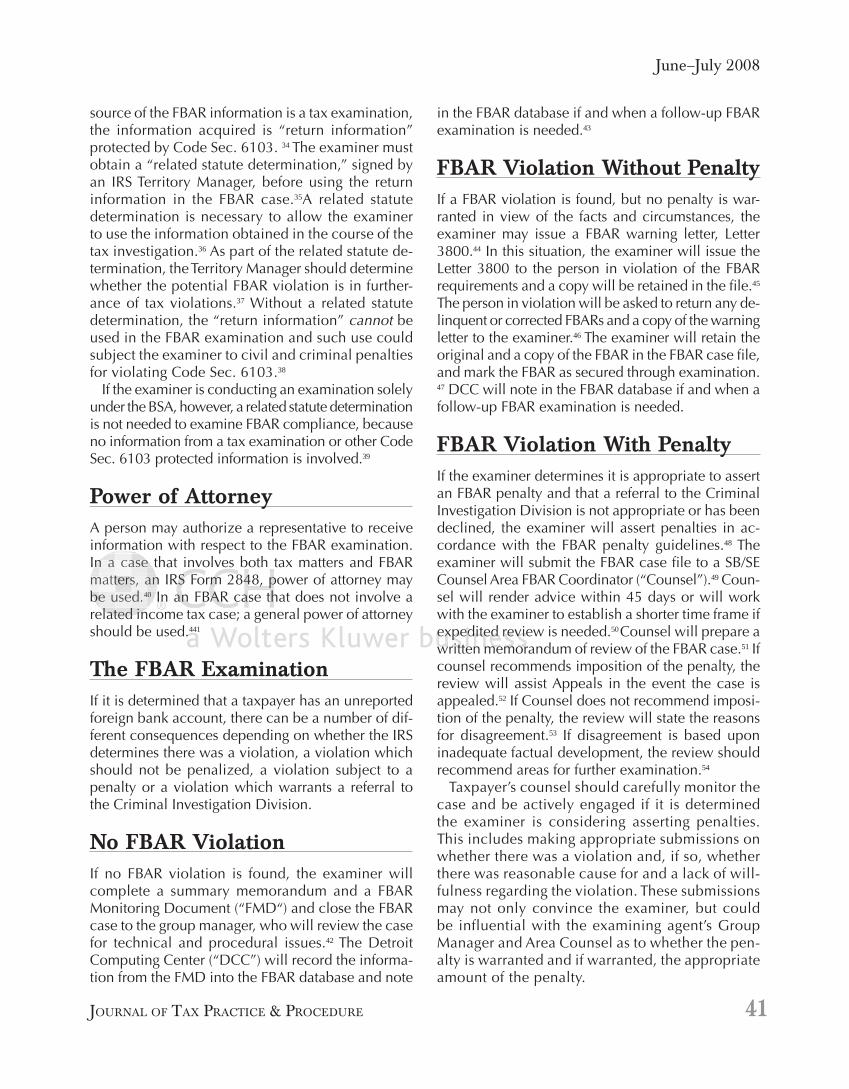

A. Section 6103 Privacy Issues - A FBAR examination can be initiatedindependently of a BSA or tax examination or can be initiated in the course of atax or other BSA examination. Internal Revenue Manual provisions are gearedto prevent the unauthorized use of information obtained by the IRS in a taxinvestigation for FBAR purposes. If the source of the FBAR information is a taxexamination, the information acquired is “return information” protected by IRCSection 6103. The examiner must obtain a “related statute determination,” signedby an IRS Territory Manager, before using the return information in the FBARcase. A related statute determination is necessary to allow the examiner to use theinformation obtained in the course of the tax investigation. As part of the relatedstatute determination, the Territory Manager should determine whether thepotential FBAR violation is in furtherance of tax violations. Without a relatedstatute determination, the “return information” cannot be used in the FBARexamination and such use could subject the examiner to civil and criminalpenalties for violating Section 6103. If the examiner is conducting an examinationsolely under the BSA, however, a related statute determination is not needed toexamine FBAR compliance, because no information from a tax examination orother Section 6103 protected information is involved.

B. Power of Attorney - A person may authorize a representative to receiveinformation with respect to the FBAR examination. In a case that involves bothtax matters and FBAR matters, an IRS Form 2848, power of attorney may beused. In an FBAR case that does not involve a related income tax case, a generalpower of attorney must be used.

C. The FBAR Examination - If it is determined that a taxpayer has an unreportedforeign bank account, there can be a number of different consequences –depending on whether the IRS determines there was a violation, a violation whichshould not be penalized, a violation subject to a penalty or a violation whichwarrants a referral to the Criminal Investigation Division.

1. No FBAR Violation. If no FBAR violation is found, the examiner willcomplete a summary memorandum and a FBAR Monitoring Document(FMD) and close the FBAR case to the group manager, who will review thecase for technical and procedural issues. The Detroit Computing Center(“DCC”) will record the information from the FMD into the FBAR

24Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

database and note in the FBAR database if and when a follow-up FBARexamination is needed.

2. FBAR Violation without Penalty. If a FBAR violation is found, but nopenalty is warranted in view of the facts and circumstances, the examinermay issue a FBAR warning letter, Letter 3800. In this situation, theexaminer will issue the Letter 3800 to the person in violation of the FBARrequirements and a copy will be retained in the file. The person inviolation will be asked to return any delinquent or corrected FBARs and acopy of the warning letter to the examiner. The examiner will retain theoriginal and a copy of the FBAR in the FBAR case file, and mark theFBAR as secured through examination and note in the FBAR database ifand when a follow-up FBAR examination is needed.

3. FBAR Violation With Penalty. If the examiner determines it isappropriate to assert an FBAR penalty and that a referral to the CriminalInvestigation Division is not appropriate or has been declined, the examinerwill assert penalties in accordance with the FBAR penalty guidelines. Theexaminer will submit the FBAR case file to a SB/SE Counsel Area FBARCoordinator (“Counsel”). Counsel will render advice within 45 days or willwork with the examiner to establish a shorter time frame if expeditedreview is needed. Counsel will prepare a written memorandum of reviewof the FBAR case. If counsel recommends imposition of the penalty, thereview will assist Appeals in the event the case is appealed. If Counseldoes not recommend imposition of the penalty, the review will state thereasons for disagreement. If disagreement is based upon inadequate factualdevelopment, the review should recommend areas for further examination.

a. Taxpayer’s counsel should carefully monitor the case and be activelyengaged if it is determined the examiner is considering assertingpenalties – including making appropriate submissions on whetherthere was a violation and, if so, whether there was reasonable causefor the violation. These submissions may not only convince theexaminer, but could be influential with the examining agent’s GroupManager and Area Counsel as to whether the penalty is warrantedand if warranted, the appropriate amount of the penalty.

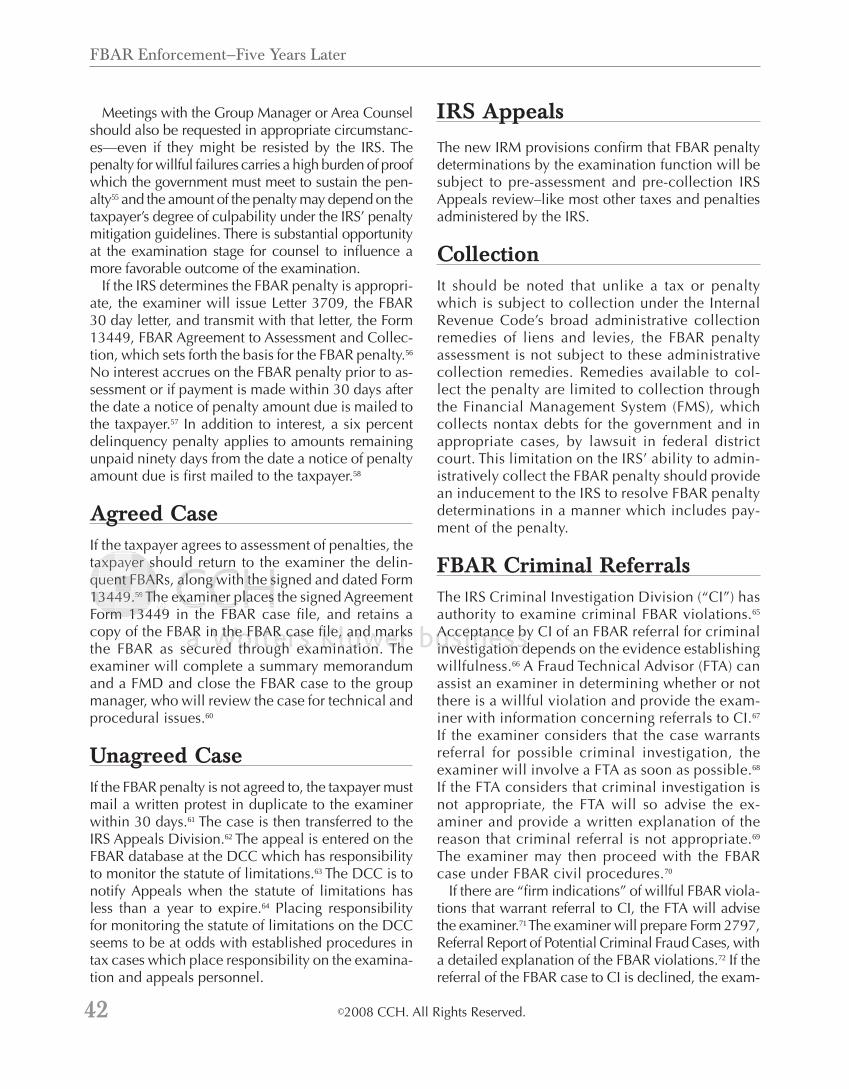

b. Meetings with the Group Manager or Area Counsel should also berequested in appropriate circumstances – even if they might be

25Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

resisted by the IRS. The penalty for willful failures carries a highburden of proof which the government must meet to sustain thepenalty and the amount of the penalty may depend on the taxpayer’sdegree of culpability under the IRS’ penalty mitigation guidelines.There is substantial opportunity at the examination stage for counselto influence a more favorable outcome of the examination.

c. If the IRS determines the FBAR penalty is appropriate, the examinerwill issue Letter 3709, the FBAR 30 day letter, and transmit with thatletter, the Form 13449, FBAR Agreement to Assessment andCollection, which sets forth the basis for the FBAR penalty. Nointerest accrues on the FBAR penalty prior to assessment or ifpayment is made within 30 days after the date a notice of penaltyamount due is mailed to the taxpayer. In addition to interest, a sixpercent delinquency penalty applies to amounts remaining unpaidninety days from the date a notice of penalty amount due is firstmailed to the taxpayer.

4. Agreed Case - If the taxpayer agrees to assessment of penalties, thetaxpayer should return to the examiner the delinquent FBARs, along withthe signed and dated Form 13449. The examiner places the signedAgreement Form 13449 in the FBAR case file, and retains the original anda copy of the FBAR in the FBAR case file, and marks the FBAR assecured through examination. The examiner will complete a summarymemorandum and a FMD and close the FBAR case to the group manager,who will review the case for technical and procedural issues.

5. Unagreed Case - If the FBAR penalty is not agreed to, the taxpayer mustmail a written protest in duplicate to the examiner within 30 days. The caseis then transferred to the IRS Appeals Division. The appeal is entered onthe FBAR database at the DCC which has responsibility to monitor thestatute of limitations. The DCC is to notify Appeals when the statute oflimitations has less than a year to expire. Placing responsibility formonitoring the statute of limitations is the DCC seems to be at odds withestablished procedures in tax cases which place responsibility on theexamination and appeals personnel.

6. IRS Appeals - The new IRM provisions confirm that FBAR penaltydeterminations by the examination function will be subject to pre-collection

26Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

IRS Appeals review–like most other taxes and penalties administered bythe IRS.

7. Collection - It should be noted that unlike a tax or penalty which is subjectto collection under the Internal Revenue Code’s broad administrativecollection remedies of liens and levies, the FBAR penalty assessment is notsubject to these administrative collection remedies. Remedies available tocollect the penalty would be similar to any other creditor and enforcedcollection would require a lawsuit in federal court. This limitation on theIRS’ ability to administratively collect the FBAR penalty should providean inducement to the IRS to resolve FBAR penalty determinations in amanner which includes payment of the penalty.

8. FBAR Criminal Referrals - The IRS Criminal Investigation Division(“CI”) has authority to examine criminal FBAR violations. Acceptance byCI of an FBAR referral for criminal investigation depends on the evidenceestablishing willfulness. A Fraud Technical Advisor (FTA) can assist anexaminer in determining whether or not there is a willful violation andprovide the examiner with information concerning referrals to CI. If theexaminer considers that the case warrants referral for possible criminalinvestigation, the examiner will involve a FTA as soon as possible. If theFTA considers that criminal investigation is not appropriate, the FTA willso advise the examiner and provide a written explanation of the reason thatcriminal referral is not appropriate. The examiner may then proceed withthe FBAR case under FBAR civil procedures.

a. If there are “firm indications” of willful FBAR violations thatwarrant referral to CI, the FTA will advise the examiner. Theexaminer will prepare Form 2797, Referral Report of PotentialCriminal Fraud Cases, with a detailed explanation of the FBARviolations. If the referral of the FBAR case to CI is declined, theexaminer follows procedures where material violations exist andcivil penalties are asserted. If the referral is accepted, the examinerwill place a transmittal memorandum in file indicating acceptance,complete the FMD showing CI acceptance and forward the FMD toDCC, which will enter the information on the FBAR database andnote on the FBAR database that a follow-up FBAR civil examinationis needed and monitor the statute of limitations. After completion ofthe criminal case, the examiner will forward any delinquent or

27Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

corrected FBARs to DCC and commence any appropriate civilFBAR penalty action.

XX. CRIMINAL PROSECUTIONS

A. Background - Historically, criminal prosecutions for FBAR violations have beenrare, but we do not expect this trend to continue. Between 1996 and 1998, JusticeDepartment statistics reveal that only nine indictments were filed charging failureto comply with the FBAR disclosure requirements, and for 1999 and 2000, no onewas charged. During the period 1995 to 2002, there were only three convictions.Reasons stated by the Treasury for these low prosecutorial statistics are strictbanking secrecy laws making it difficult to obtain admissible evidence withrespect to undisclosed foreign bank accounts and prosecutorial selection ofviolations for criminal conduct associated with the concealment of foreignaccounts, such as tax evasion, fraud, money laundering, and for false statementson a tax return for failing to check the box on Schedule B (which have greater juryappeal), in lieu of failure to comply with the FBAR disclosure requirements.

B. Past Criminal Prosecutions - Most of the criminal prosecutions with respect toforeign bank accounts arose with respect to non-FBAR criminal statutes. Forexample, a taxpayer who provides a false answer to the foreign bank question onSchedule B of the for Form 1040 can be prosecuted pursuant to IRC §7206(1).That section criminally punishes a taxpayer who willfully makes and subscribesany return under penalties of perjury which he does not believe to be true andcorrect as to every material matter. A person who knowingly answers “no” on theSchedule B when the answer is “yes” runs the risk of facing prosecution under thisprovision. The Justice Department considers such conduct a basis for prosecution,as evident from its Criminal Tax Manual §12.08[6], and has brought prosecutionagainst taxpayers. Moreover, a person may not avoid criminal prosecution byfailing to provide an answer to the foreign bank account question -- failing toanswer “yes” or “no” could be considered knowingly signing a return that is nottrue and correct as to every material matter under IRC §7206(1). Also, ataxpayer’s omission from his income tax return of income from a foreign bankaccount in the form of interest, dividends or capital gains can result in criminalexposure under IRC §7201 and IRC §7206(1). Lastly, if multiple individuals areinvolved the government can also bring conspiracy charges under 18 USC §371.

C. Future Criminal Prosecutions - The criminal tax bar can expect to see a newtrend in criminal enforcement of the FBAR rules. Sections 5321 and 5322 remainviable and potent weapons that the IRS can use to reach its objective to seek out

28Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

and punish those with undisclosed foreign accounts. Any lawyer with UnitedStates clients with overseas financial accounts, including those who are beneficialowners, must consider a whole host matters in preparation for the June 30thdeadline, including determining the nature and extent of the overseas financialaccounts, who has a financial interest in the accounts, who has signatory authorityover the accounts, and what is the aggregate value of the accounts in dutifullyassessing the need to file comply with the FBAR requirements. The tax barshould be on notice that the failure to timely file the FBAR may now more thanever be the subject of a criminal prosecution in ways never previously consideredby the United States Government.

XXI. RECENT IRS INITIATIVES

A. While most IRS enforcement actions are not public because of taxpayer privacylaws, the government’s enforcement is becoming more public and seems to havean ongoing place in the pages of the New York Times and Wall Street Journal.There was a time when many U.S. taxpayers took comfort in foreign bank secrecylaws and other impediments to the IRS obtaining information on foreign incomegenerating activities. Not so any more. The “comfort” is proving to be false–especially for those taxpayers who are now in the cross-hairs of U.S. taxenforcement.

1. UBS and Liechtenstein Accounts. In February, 2008 the IRS announcedit was investigating more than 100 Americans with bank accounts inLiechtenstein. UBS AG, Switzerland’s largest bank, was investigated bythe United States into whether it helped clients evade taxes. As part of thisinvestigation, the Department of Justice is expected to seek to obtain thenames of high income United States citizens holding accounts UBS –estimated to be up to 50,000 taxpayers. Recently, the Department of Justicecharged a former UBS AG banker and a Liechtenstein consultant withhelping clients–U.S. taxpayers--avoid taxes.

2. IRS Penalty Framework Memoranda. On March 26, 2009, the IRS releasedseveral Memoranda dated March 23, 2009 announcing a “penaltyframework” for taxpayers who come forward as part of a voluntarydisclosure to address offshore tax-related issues. This penalty frameworkwas in place for about six months - from March 23, 2009 until October 15,2010. For taxpayers who have made a voluntary disclosure (likelyincluding those who began the voluntary disclosure process before theissuance of the IRS Memoranda dated March 23, 2009) the IRS has

29Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

announced it will enter into agreements to resolve tax liabilities relating tooffshore tax-related issues on the following terms:

a. The taxpayer will be required to file or amend income tax returns forsix years, including information returns and Form TD F 90-22.1Report of Foreign Bank and Financial Accounts (commonly knownas an “FBAR”), and tax and interest will be assessed for these sixyears. In cases where the offshore account was opened or theoffshore entity was formed within the past six years, the IRS willrequire filing and payment from the earliest year in issue.

b. The IRS will assess either a 20% accuracy-related or a 25%delinquency penalty on the income tax for each year. These penaltiesare based on the amount of tax determined to be due for each yearwith respect to the amended income tax returns. This is a lowerpenalty than the potentially applicable 75% civil fraud penalty.However, in many similar cases in the past, practitioners have beenable to avoid the 20% accuracy-related penalty. Participation in this“penalty framework” requires at present acceptance of thesepenalties.

c. In lieu of all other potential penalties, including the FBAR penaltyand information return penalties, the IRS will assess a additionalpenalty equal to 20% of the amount in the offshore account orforeign entity on any day during the year with the highest aggregateaccount and asset value. This penalty may be reduced to 5% underthe following very limited circumstances - if :

(1) The taxpayer did not open or cause any foreign accounts to beopened or foreign entities formed,

(2) There has been no activity in any offshore account or entity(no deposits, withdrawals, etc.) during the period theaccount/entity was controlled by the taxpayer, and

(3) All applicable U.S. taxes have been paid on the fundsdeposited in the foreign accounts/entities (where onlyaccount/entity earnings have escaped U.S. taxation).

30Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

d. IRS field personnel are authorized to enter into closing agreementswithin the foregoing guidelines. It is not clear whether there isdiscretion within the ranges between 5% and 20% for the FBARpenalty. These guidelines are new and it is not yet possible todetermine how they will ultimately be implemented by the IRS fieldpersonnel. However, in other similar situations, IRS field personnelhave interpreted such memoranda as their “marching orders” andhave moved forward without attempting to exercise any possiblediscretion.

e. These guidelines will apply only over the stated period. Theforegoing provide a degree of certainty regarding the civil penaltiesto be applied. Those not participating in the foregoing penaltyinitiative would retain the ability to argue against penalties based onreasonable cause, non-willfulness, etc. To protect the integrity of thepenalty initiative it could be difficult for the IRS to administrativelyagree to lesser penalties. However, the relevant statutes have notchanged. It is presently difficult to determine the potential resolutionof civil penalties for those who do not participate in the foregoingpenalty initiative. It is assumed that, thereafter, the IRS will requiremore significant civil penalties.

3. IRS Frequently Asked Questions Regarding Quiet Disclosures. On May 6,2009, the IRS issued Frequently Asked Questions (“FAQs”) regarding thePenalty Memoranda. Question No. 10 now seems to require an affirmativecontact of IRS criminal investigation to be deemed a “voluntary disclosure”in this context. Such a contact would require participation in their penaltyinitiative as described in Penalty Memoranda dated March 23, 2009.Importantly, with respect to “quiet” disclosures, the IRS FAQs state thatsuch disclosures run the “risk of being examined and potentially criminallyprosecuted for all applicable years. . . the IRS has identified, and willcontinue to identify, amended tax returns reporting increases and income.The IRS will be closely reviewing these returns to determine whetherenforcement action is appropriate.”

XXII. HIRE ACT OF 2010 & FACTA

A. On March 18, 2010, President Obama signed the Hiring Incentives to RestoreEmployment Act (Pub.L No. 111-14) (“HIRE Act”). The HIRE Act created taxbreaks for businesses hiring new workers through a payroll tax holiday and other

31Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

measures. To pay for these tax breaks, the HIRE Act set forth provisions thathave far reaching implications for foreign institutions that may have US clientsand broadens reporting requirements for foreign assets, through incorporation(with some modifications) of the Foreign Account Tax Compliance Act of 2009.(“FACTA”).

B. The FACTA provisions of the HIRE Act affects three areas: (1) Increasedreporting for individuals with foreign assets; (2) Substantive changes in U.S.federal income tax law; and (3) Disclosure and compliance issues for foreignfinancial institutions. This outline summaries some of the HIRE Act provisions.

C. Disclosures with Respect to Foreign Assets

1. Under existing law, every US person who has a financial interest in, orsignature authority over, bank, securities or financial accounts in a foreigncountry must file an FBAR for each calendar year in which the aggregatevalue of the accounts exceeds $10,000.

2. Foreign Asset Disclosure. Beginning with the 2011 tax year (that is, for taxyears beginning after March 18, 2010), in addition to the existing FBARreporting requirements, US individuals who hold any interest in a specifiedforeign financial asset during the tax year must attach to their tax returns forthe year certain information with respect to each asset if the aggregate valueof all assets exceed $50,000 (or a higher dollar amount prescribed by theSecretary of the Treasury). New §6038D(a).

a. Specified Foreign Financial Asset. Specified foreign financialassets, include:

(1) Depository, custodial accounts or other financial accountmaintained at a foreign financial institutions; OR

(2) To the extent not held in an account at a financial institution,

(a) Any foreign issued stock or securities

(b) Any interests in a foreign investment fund orderivatives with a foreign counterparty; OR

(c) Any interest in a foreign entity. New §6038D(b)

32Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

b. Disclosure. The information required to be disclosed must includethe maximum value of the asset during the tax year. (New§6038D(c))

(1) For financial accounts, the taxpayer must disclose the nameand address of the financial institution, and the accountnumber.

(2) For stock or security, the taxpayer must disclosure name andaddress of the issuer and such other information as isnecessary to identify the class or issue of stock

(3) In the case of any other instrument, contract or interest, ataxpayer must provide any information necessary to identifythe instrument, contract or interest, along with the names andaddresses of all issuers and counterparties.

3. Failure to Disclose Penalty. Individuals who fail to make the requireddisclosures are subject to a penalty of $10,000 for the tax year, which mayincrease to $50,000 if the failure continues for more than 90 days afternotification by the IRS. (New §6038D(d))

a. Reasonable Cause Exception. The Failure to Disclose Penalty maynot be imposed on any individual who can show that the failure isdue to reasonable cause and not willful neglect. (New §6038D(g)).The fact that a foreign jurisdiction would impose a civil or criminalpenalty on the taxpayer for disclosing is not reasonable cause.

b. In addition to the Failure to Disclose Penalty with respect to foreignassets, a 40-percent accuracy related penalty can be imposed on anyunderstatement of tax attributable to a transaction involving anundisclosed foreign financial asset (see below).

4. Comments. The new disclosure provisions of the HIRE Act not onlybroadens the reporting requirements, they also add duplication andcomplexity to an already complicated foreign financial accountingreporting regime. The FBAR reporting regime, once largely unenforced andhistorically with much regulatory or other official guidance has gainedmuch attention recently since civil enforcement was delegated to the IRS

33Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

in 2003. The new focus has shown gaps in the current reporting regimewhich the new legislation is attempting to fill. The HIRE Act, broadens thereporting requirements and extends the rules to ownership of foreign assets,such as foreign stocks or securities and interests in foreign entities, notcovered by the FBAR reporting regime. While the threshold reportingrequirement amount - $50,000 - exceeds the threshold relating to FBARs,the amount is low enough to affect many if not most taxpayers with foreignassets. Other significant differences exist. While the FBAR reportingregime covers those having signatory or other authority, the new reportingregime focuses on ownership. Unfortunately the different reportingregimes will likely create confusion among taxpayers and professionalssuggesting that the Congress will need to look at these different regimesand consolidate them in a single foreign asset reporting regime.

D. Underpayment Penalty Attributable to Undisclosed Foreign Financial Assets

1. A 40-percent accuracy-related penalty (double the otherwise applicablepenalty) is imposed for the underpayment of tax that is attributable to anundisclosed foreign financial asset understatement. New §6662(b)(7) and(j). a. For this purpose, an undisclosed foreign financial asset

understatement for any tax year is the portion of the understatementfor the year that is attributable to any transaction involvingundisclosed foreign financial asset.

b. Thus, if a taxpayer fails to disclose amounts held in a foreignfinancial account, any underpayment of tax related to the transactionthat gave rise to income would be subject to the penalty provision,as would any underpayment related to interest, dividends or otherincome accrued on such undisclosed amounts. The new 40-percentpenalty is subject to the same defenses that are otherwise availablefor §6662 penalties.

c. The penalty applies starting with tax year 2011 (i.e, tax yearsbeginning after March 18, 2010)

2. Comment The new penalty provisions of the HIRE Act are in manyrespects less draconian than the FBAR penalties and gives the IRSassessment and collection remedies unavailable with respect to the FBARpenalty. These additional Code penalties will likely create a bias within the

34Edward M. Robbins, Jr.

Hochman Salkin Rettig Toscher & Perez, P.C. © 2010 All Rights Reserved

IRS to impose these new penalties, rather than the FBAR penalties. Itwould seem the existing FBAR penalties were more than sufficient to serveas a deterrent to the non-compliant in the wake of the current attentionforeign compliance has been afforded by the IRS. Nevertheless, thelegislation adds a new layer of penalties under the Code.

3. Comment. Unlike with a typical Internal Revenue Code tax or penaltywhich is subject to collection under the Internal Revenue Code’s broadadministrative collection remedies of liens and levies, the FBAR penalty isnot subject to these administrative collection remedies. Remedies availableto collect the FBAR penalty are limited to collection through the FinancialManagement System, which collects non-tax debts for the government andin appropriate cases, by law suits filed in federal district court. The HIREAct penalties will give the IRS the ability to assess and collect these newpenalties through its broad administrative powers, including levy and lien.