Embed Size (px)

Citation preview

1

Nihar Jambusaria [email protected] [email protected]

TAXATION OF ROYALTY AND FEES FOR TECHNICAL SERVICES

TAXATION OF ROYALTY

• WNS acquiring Marketics for $65 million.

• Facebook acquiring Friendfeed for $50 million

4

• Vodafone acquiring Hutch for $19.3 billion.

• Google Inc. acquiring Youtube Inc. for $1.65 billion.

5

6

TAXATION OF ROYALTY AS PER THE INCOME- TAX ACT, 1 961 (ACT)

7

Royalty Transfer of rights in

respect of IPRs

Imparting of information on working of IPRs

Use of IPRs Imparting information

on Technical/ Industrial/

Commercial/ Scientific knowledge, experience

or skill

Use of Industrial/ Commercial/

Scientific Equipment except

equipments mentioned in 44BB

Scope of Section 9(1)(vi)

Status of Payer Coverage

The Government

Resident of India

Non-resident

No exception

Excluded only if

Included only if

In all cases

• For business / profession of

payer outside India • For source of income of

payer outside India. • For business / profession of

payer in India. • For source of income of

payer in India.

Taxability of Royalty Section Royalty

Section 44DA If arising out of PE/ fixed place of profession

Section 115A No PE and in pursuance of agreement with the government or Indian concern

Section 28 Other cases e.g.. Resident making payment to a Resident

10

WHETHER ROYALTY PAYMENTS MADE FROM EXPORT SALES COME UNDER THE EXCLUSION CLAUSE?? Aktiengesellschaft Kuhnle Kopp & Kausch W. Germany vs. BHEL

(262 ITR 513 Madras High Court)

As far as export sales is concerned, that amount is also exempt under section 9(1)(vi) of the Act. Since the source of the royalty is from the source situate outside India, the royalty paid on export sales is not taxable.

CIT vs. Havells India Ltd. (ITA No.55 & 57/2012, 21 May 2012) in which the Delhi High Court held –

We are making a distinction between the source of the income and the source of the receipt of monies. In order to fall within the second exception provided in section 9(1)(vii)(b), the source of income and not receipt should be situated outside India.

11

GENESIS OF EXPLANATION TO CLAUSE (V), (VI) AND (VII) Ishikawajima-Harima Heavy Industries’ (288 ITR 408 SC)

Offshore services should be rendered in India AND used in India for income to be regarded as accruing in India

There must be a direct link with India

There must be sufficient territorial nexus to warrant imposition of tax

Expl is inserted stating that where income is deemed to accrue or arise in India u/s. 9(1)(v),(vi) and (vii), such income shall be included in Total Income of Non-resident whether or not Non-resident has a place of business or Business Connection in India or has rendered services in India.

Explanation added by Finance Act 2007, w.e.f 1.6.1976 updated by Finance Act, 2010

12

EXPLANATION 2 TO SECTION 9(1)(VI) OF THE ACT Description IPRs

► The transfer of all or any rights in respect of:

► The imparting of any information concerning the working or use of:

► The use of any:

Patent, invention, model, design, secret formula or process or trademark or similar property

The imparting of any information concerning

Technical, industrial, commercial or scientific knowledge, experience or skill

► The use or right to use Industrial, commercial or scientific equipment

► The transfer of all or any rights in respect of

Copyright, literary, artistic or scientific work

Services in connection with the above

Explanation 4

Transfer of all or any rights includes right for or to use a computer software (including granting of a license) irrespective of the medium

Explanation 5

• Includes consideration in respect of any right, property or information, whether or not— • the possession or control is with the payer; • it is used directly by the payer; • the location is in India

Explanation 6

"process" includes transmission by satellite , cable, optic fibre, etc. whether or not secret

14

Retrospective w.e.f. 1 June 1976

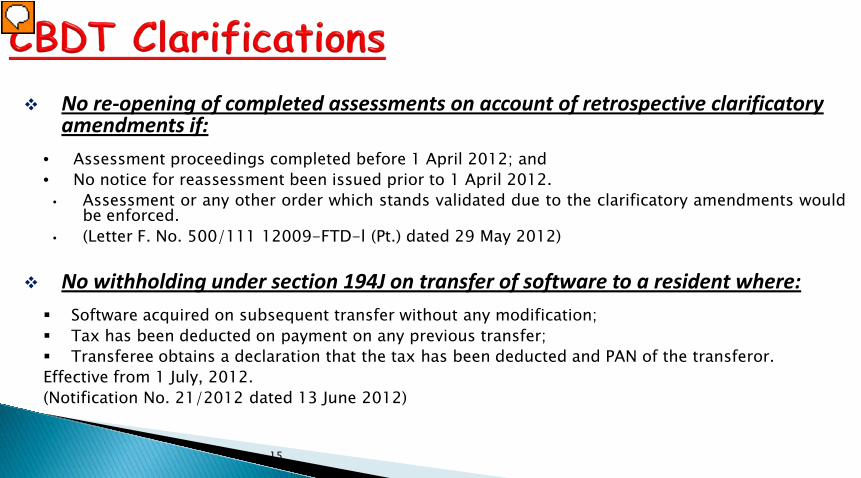

No re-opening of completed assessments on account of retrospective clarificatory

amendments if: • Assessment proceedings completed before 1 April 2012; and • No notice for reassessment been issued prior to 1 April 2012.

• Assessment or any other order which stands validated due to the clarificatory amendments would be enforced.

• (Letter F. No. 500/111 12009-FTD-l (Pt.) dated 29 May 2012)

No withholding under section 194J on transfer of software to a resident where: Software acquired on subsequent transfer without any modification; Tax has been deducted on payment on any previous transfer; Transferee obtains a declaration that the tax has been deducted and PAN of the transferor. Effective from 1 July, 2012. (Notification No. 21/2012 dated 13 June 2012)

15

DOMESTIC PROVSIONS VS. DTAA – WHICH WILL PREVAIL? B4U International Holdings Ltd. vs. DCIT (ITA No. 3326/Mum/2006 dated

28 May 2012)

Coming to the agrument of the Learned Departmental Representative that the amendment to the Finanace Act, 2012 changes the posititon, we find that there is no change in the DTAA between India and USA. Thus, the amendments have no effect on our decision.

DTAA provisions if beneficial to the assessee will reign over the provisions of the Act

Income-tax Act

Section 44DA Net Basis @ 40%*

Article 12 Gross Basis

At treaty rates

Article 7 Net Basis @ 40%

Section 115A

Gross Basis @ 25%*

Tax Treaty

*Plus applicable surcharge & Education Cess

Where PE exists

Where NO PE exists

ARTICLE 12: ROYALTY DEFINITION

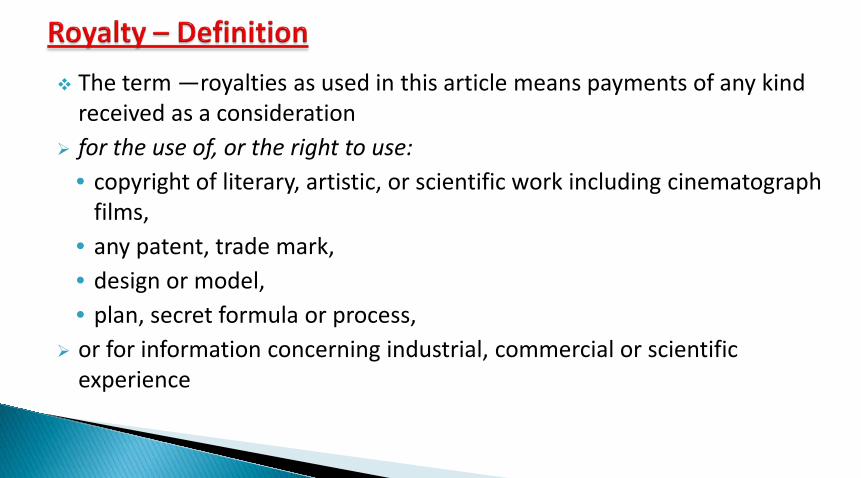

The term ―royalties as used in this article means payments of any kind received as a consideration

for the use of, or the right to use: • any copyright of a literary, artistic or scientific work including cinematograph

films, or films or tapes used for radio or television broadcasting, • Patent and trademark, • plan, design or model, • secret formula or process, • industrial, commercial or scientific equipment

or for information concerning industrial, commercial or scientific experience

The term ―royalties as used in this article means payments of any kind received as a consideration

for the use of, or the right to use: • copyright of literary, artistic, or scientific work including cinematograph

films, • any patent, trade mark, • design or model, • plan, secret formula or process,

or for information concerning industrial, commercial or scientific experience

22

Comparison of definitions: UN Model definition (as given below) v. OECD Model definition (part in bold fonts are included only in UN Model and not in OECD Model):

Means payments of any kind received as a consideration for the use of, or the

right to use, any copyright of literary, artistic or scientific work including cinematograph films, or films or tapes used for radio or television broadcasting, any patent, trade mark, design or model, plan, secret formula or process, or for the use of, or the right to use, industrial, commercial or scientific equipment or for information concerning industrial, commercial or scientific experience

As per OECD Model As per UN Model

copyright of literary, artistic, or scientific work including cinematograph films,

any patent, trade mark, design or model, plan, secret formula or process, or for information concerning industrial,

commercial or scientific experience

Copyright of films or tapes used for radio or television broadcasting

industrial, commercial or scientific equipment

Consideration for use or right to use

25

OECD Model UN Model

If PE Exists

If PE Exists

Article 7 – Permanent

Establishment

Yes

Article 14 – If arising on performance of

independent personnel from fixed place Establishment

Article 7- Permanent Establishment

Article 12 - Royalty No No

Yes

Yes

CONTROVERSIES

ON

ROYALTY TAXATION

Facts: Assessee is engaged in the business of

shipping. Besides owning ship, it also charters ships for which it pays hire charges.

Issue: Payment made for taking ship on time

charter basis would constitute 'royalty' as defined under section 9(1)(vi)(b) of the Income Tax Act, 1961 (Act)?

Assessee contended that ship was not

equipment and consequently there was no question of right to use of any equipment which could be construed as royalty

I Co.

F Co,

Provides ship on time charter basis

Payments

28

It can be treated as Royalty Business Income - Sale of product Capital Gain – Sale of capital asset Various facets of Software Computer software generally described as a programme, or series of programmes, containing

instructions for a computer required either for the operational process (system software) or for accomplishment of other tasks (application software)

It can be transferred via variety of medium eg. tape, disc, fibre, wireless etc. It can be standardized with a wide range of applications or be tailor made It can be integrated in hardware or in independent form

29

Revenue Authorities Taxpayers

Supply of software does not involve any use / right to use of copyright, patent, invention or process

OECD MC –There is no

use / right to use of copyright, patent, invention or process

It is business income

not taxable in India in the absence of any permanent establishment in India

Supply of software involves use / right to use of following:

Copyright Process

Taxable in India

as royalty on gross basis

Whether Royalty?

Whether Business Income?

Software supply

Issue under litigation in a number of cases

Characterisation of receipts from

software supply

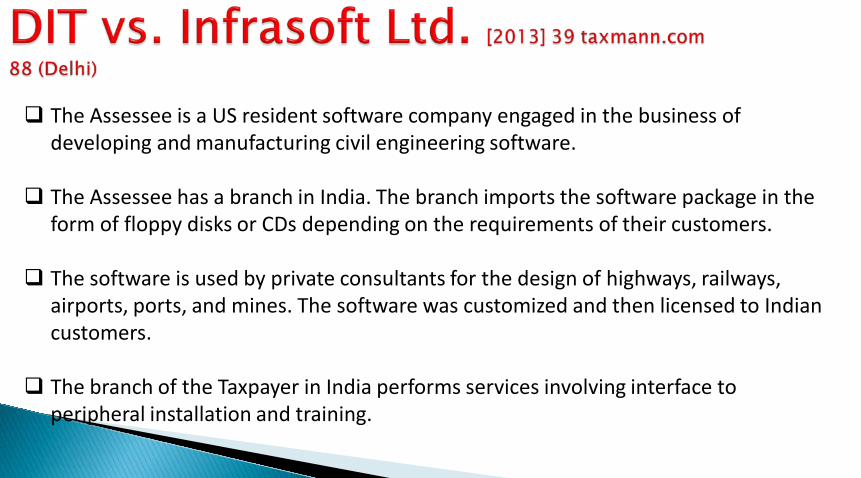

The Assessee is a US resident software company engaged in the business of developing and manufacturing civil engineering software.

The Assessee has a branch in India. The branch imports the software package in the form of floppy disks or CDs depending on the requirements of their customers.

The software is used by private consultants for the design of highways, railways, airports, ports, and mines. The software was customized and then licensed to Indian customers.

The branch of the Taxpayer in India performs services involving interface to peripheral installation and training.

Held: [Distinction between copyright and copyrighted article]

Consideration for

Transfer of Copyright Royalty

Transfer of Right to use

the copyright Royalty

Transfer of copyrighted

material No Royalty

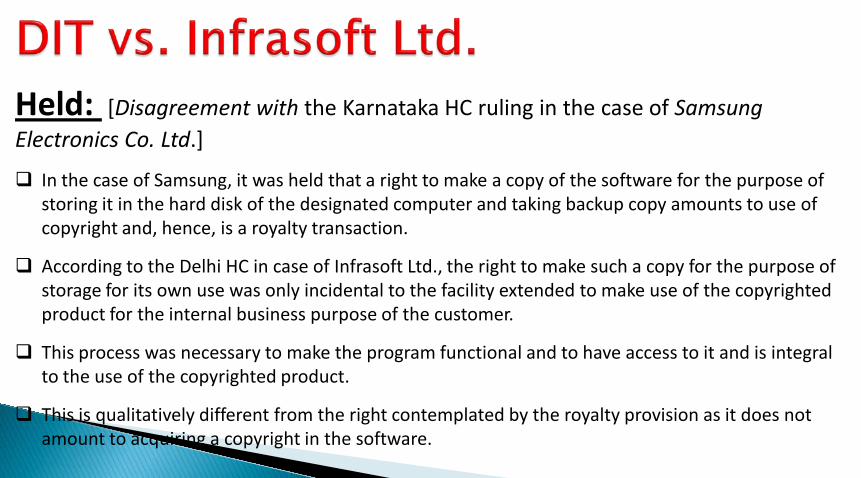

Held: [Disagreement with the Karnataka HC ruling in the case of Samsung Electronics Co. Ltd.]

In the case of Samsung, it was held that a right to make a copy of the software for the purpose of storing it in the hard disk of the designated computer and taking backup copy amounts to use of copyright and, hence, is a royalty transaction.

According to the Delhi HC in case of Infrasoft Ltd., the right to make such a copy for the purpose of storage for its own use was only incidental to the facility extended to make use of the copyrighted product for the internal business purpose of the customer.

This process was necessary to make the program functional and to have access to it and is integral to the use of the copyrighted product.

This is qualitatively different from the right contemplated by the royalty provision as it does not amount to acquiring a copyright in the software.

• ADIT vsTII Team Telecom International (60 DTR 177) (Mum Trib) • Ericsson (2011)16 taxmann.com371(Del HC) • Novell Inc v. DDIT (2011) 16 taxmann.com 186 (Mum ITAT) • Motorola Inc, (95 ITD 269)(Delhi SB) • ADIT v. Tata Communications Ltd. (ITA 1473/Mum/2009) • DassaultSystems K.K. [2010-TIOL-02-ARA-IT] • Solid Works Corporation (Mum) (Trib) • DIT v. Infrasoft Limited [2013] (Delhi) 39 taxmann.com 88

• Samsung Electronics (2011) 16 taxmann.com 141 (KarHC) • Sunray Computers (2011) 16 taxmann.com 268 (KarHC) • AcclerysKK, In re e (2012-TII-10-ARA-INTL) • Citrix Systems Asia Pacific Pty. Ltd. (AAR) • Millennium IT Software Ltd. (2011) 14 taxmann.com 17 • Microsoft Corporation vs. ADIT (2010-TII-141-ITAT-DEL-INTL) • GracemacVs ADIT (ITA Nos 1331 1336/Del/2008)

34

Majority treaties of India do not explicitly include ‘compute software’ in the

definition of Royalty

Specific language including ‘computer software’ in the royalty definition in India’s treaty with the following countries : Malaysia Morocco Namibia Russia Trinidad & Tobago Kazakhstan Kyrgyz Republic

35

Supply of integrated equipment comprising hardware and software where

the supply of software is inextricably linked to supply of the hardware and, both, the hardware and the software, cannot function without each other

Judicial view emerging : Revenue authorities should not split the transaction to separately tax

the payment for software Further, purchase of software is akin to purchase of a copyrighted

article and not purchase of any rights in the software

Lucent Technologies Hindustan Ltd. v. ITO (92 ITD 366) Motorola, Ericson and Nokia 96 TTJ 1 (Del SB) SunaryComputers (P) Ltd 204 Taxman 1 (Karnataka) (HC)

No DTAA with India

Under Income-tax Act, 1961

Taxpayers to withhold tax on software payments

DTAA with India

Treaty definition specifically covers

‘computer software’

Taxpayers to withhold tax on software payments

DTAA with India

Treaty definition DOES NOT specifically cover ‘computer

software’

Litigative

37

Satellite Company

Broadcasting issues

Outside India India Uplinking of signal

Foot print Area

Taxation of Satellite/ Transponders payments – Mechanics

Transponder hire charges

Signals downlinked by

Co.

Facts: The assessee, engaged in broadcasting television channels from

India, received transponder service from Intelsat, a tax resident of USA, in lieu of a fee.

The assessee approached to the AO under 195(2) of I-T Act for Nil withholding tax certificates, for such payment of fees to Intelsat, which was denied by the AO and held that the payments made are in nature of Royalty

Held: The introduction of Explanation 6 by Finance Act 2012 w.r.e.f.01-6-1976 is clarificatory

in nature and, therefore, it does not amend the definition of royalty per se

Any payment for use or right to use of process is in the nature of royalty as per the provisions of Article 12(3) of DTAA as well as per the Explanation 2 of section 9(1)(vi) of the Act.

Since the term 'process' is not defined under the DTAA, therefore, by virtue of Article 3(2) of the India-US DTAA, the meaning of term 'process' as defined in the Act would apply for this purpose

The use of transponder by the assessee for telecasting/broadcasting the Programme involves the transmission by the satellite including up-linking, amplification, conversion for downlinking of signals which falls in the expression 'process' as per Explanation 6 of section 9(1)(vi) and thus payment is in nature of ‘Royalty’

Asia Satellite Telecommunications Co Ltd (2011) 332 ITR 340 (Del) – Pre Amendment

Channel Guide India Ltd. v. ACIT, 25 taxmann.com 25(Mum Trib) – Post Amendment

B4U International Holdings Ltd. v. DCIT, 23 taxmann.com 372 – Post Amendment

ISRO Satellite Centre, In re (2008) 307 ITR 59 (AAR) - Pre Amendment

New Skies Satellite NV [2009] 121 ITD 1 (Delhi) (SB) - Pre Amendment Asianet Communications Ltd (2010) 38 SOT 158 (Mad) – Pre Amendment Viacom 18 Media Pvt. Ltd. [ TS-179-ITAT-2014] – Post Amendment

TAXATION OF FEES FOR TECHNICAL SERVICES AS PER THE ACT

Section 9(1)(vii) of the act provides that the income by the way of FTS shall be deemed to accrue or arise in India, if it is payable by The government, or

A resident, except where the fees are payable

for services utilised in a business or profession carried on by such person outside India, or for the purpose or making or earning any income from any source outside India

A non-resident where the fees are payable.

for services utilised in a business or profession carried on by such person in India , or for the purpose or making or earning any income from any source in India.

Consideration including any

lump sum consideration

Managerial service

Technical services

Consultancy services

Provision of services of technical or

other personnel

Meaning of ‘Fees for Technical Services’

Does not include consideration for any construction, assembly, mining or like project undertaken by its recipient or consideration which would be chargeable under the head salaries.

Managerial services The Oxford Dictionary gives the following meanings to the term “manage”: have control

of, be manager of, operate a tool etc., contrive, deal with person tactfully. The term “managerial” was observed by AAR in case of Intertek services Indian P. Ltd. 175

Taxman 375 as - Manager is a person who manages industry or business or who deals with

administration or the person who organizes other people’s activity. Managerial services essentially involves controlling, directing or administrating the business

Managerial & Consultancy Services can be overlapping: - Raymond Ltd. V/s DCIT (86 ITD

791)

Technical services In the absence of any definition in law, general meaning needs to be adopted

Oxford Dictionary: of a particular subject, craft, etc. Requiring specialized knowledge to be

understood (professional qualification may not be necessary) of applied science and mechanical art; according to strict legal interpretation.

Deduction in respect of royalties, etc., from certain foreign enterprises—technical services—whether managerial services are covered by the term 'technical services'—managerial services do not include any use of tools and machinery while technical services should include the use of tools and machinery. Hence not covered, - J.K. (Bombay)Ltd. V. CBDT (1979) 118 ITR 312 (Delhi HC).

Delivery service requires human intervention and thus, rendering services via sophisticated technology does not amount to technical services CIT v/s Bharti Cellular Limited (330 ITR 239)

Consultancy services “Consult” means to seek information or advice. It can be written or oral Provision of advise by someone, such as a professional who has special qualifications

May overlap with technical and managerial services, if provided by a consultant Hyderabad Tribunal decision in the case of Tecumseh Products (I) Ltd. v. DCIT [2007] 13 SOT

489 – relevant observations: “technical service does not include providing some technical knowledge for manufacturing alone. Technical knowledge includes, management or consultancy services.”

Provision of services of technical or other personnel Caborandum Co. V CIT (1977) 108 ITR 335 -SC Where an American Company had deputed its employees to an Indian Company. Indian Company entered into employment Agreement with deputed employees, the Indian Company paid salaries to these employees which were under the control of Indian company, held it is taxable as salary and not FTS. Mannesmann Demag Lauchhammer V. CIT (1988) 26 ITD 198 – HYD ITAT Where a machinery was imported and post warranty period technical faults were found and and subsequently an agreement was entered with the German company who sent an engineer to India for repair. Payment was made on a per day basis by the Indian Co. along with cost of travel, boarding and lodging it was held to be ‘Provision Of services of Technical personnel’ since it specifically includes in Explanation to S.9(1)(vii).

Issues

Skycell Communications Ltd. v/s DCIT (251 ITR 53) Madras High court held that the fees received for providing a cellular mobile

telephone services was for use of ‘standard facility’.

The fact that the assessee has installed sophisticated technical equipment in the exchange to ensure connectivity to its subscriber, does not on that score, make it a provision of a technical service to the subscriber.

It was contended that the mere collection of a fee for use of a standard facility provided to all those willing to pay for it, does not amount to the fee having been received for technical services

Millennium Infocomm Technologies Ltd V/s. ACIT (117 ITD 114)

ITAT held that providing of hosting space in servers located abroad does not result in providing any technical services and will not be considered as Fees for Technical Services.

Cargo Community Network (p.) Ltd (AAR No. 668 of 2006) Assessee engaged in the business of providing access to internet based Air cargo portal

and payments were made by resident of India for use of portal. AAR took a harsh view that payments for accessing portal hosted in Singapore was both

royalty (for use of equipment) and FTS in terms of subscribers and help desk support in India.

Payments for mineral oil exploration and related activities Applies to NR engaged in the business of providing : Services/ facilities in

connection with prospecting or extracting or production of mineral oils and supplying plant and machinery on hire used/to be used in prospecting or extracting or production of mineral oils.

Deems total income of non resident @10% of gross receipts, effective tax rate to Non-resident - 4%

Section 44BB shall apply only if the payments are not covered under the definition of Fees for Technical Services

Applicability of Section 44BB

Services should not be covered under Section 9(1)(vii)

OR If covered, should fall within exclusion of 9(1)(vii) – ‘’consideration

for any construction, assembly, mining or like project undertaken by the recipient’’

AND Services/facilities should be in connection with prospecting or

extracting or production of mineral oils

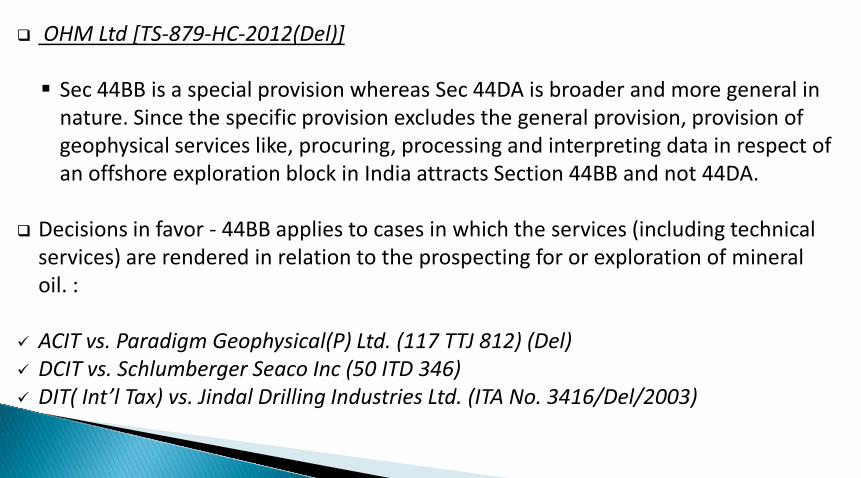

OHM Ltd [TS-879-HC-2012(Del)] Sec 44BB is a special provision whereas Sec 44DA is broader and more general in

nature. Since the specific provision excludes the general provision, provision of geophysical services like, procuring, processing and interpreting data in respect of an offshore exploration block in India attracts Section 44BB and not 44DA.

Decisions in favor - 44BB applies to cases in which the services (including technical

services) are rendered in relation to the prospecting for or exploration of mineral oil. :

ACIT vs. Paradigm Geophysical(P) Ltd. (117 TTJ 812) (Del) DCIT vs. Schlumberger Seaco Inc (50 ITD 346) DIT( Int’l Tax) vs. Jindal Drilling Industries Ltd. (ITA No. 3416/Del/2003)

54

AS PER DTAA

Meaning of FTS under Tax Treaties FTS covers managerial, technical or consultancy services akin to the ITA, but may not have the same

exclusions as under the ITA. India-Singapore Tax Treaty – Relevant Extract "fees for technical services" as used in this Article means payments of any kind to any person in consideration for services of a managerial, technical or consultancy nature (including the provisions of such services through technical or other personnel) if such services: a) ...’’ Definition of FTS under various treaties may be broadly categorized as under – Type 1 – Absence of clause on FTS eg. Mauritius, Myanmar, Philippines, Type 2 – Definition largely at par with ITA eg. Japan Type 3 – Definition contains further condition like ‘make available’ eg. USA, UK, Canada, Netherlands, Singapore Type 4 – Protocol to Treaty - restricts the scope of definition through Most Favoured Nation (MFN) clause eg. Belgium, France, Hungary, Israel, Spain, Sweden, Switzerland 10

Fees for included services DTAAs signed by India having the concept of FTS/ FIS along with the make

available‘ clause (such as Canada, Cyprus, USA, Netherlands, UK)

Deals with Technical Services but, coverage is of FIS Definition of FIS (Refer for example Indo - US Treaty) ―For purposes of this article, “fees for included services” means payments of any kind to any person in consideration for the rendering of any technical or consultancy services (including through the provision of services of technical or other personnel) if such services: a)…………. b)make available technical knowledge, experience, skill, know-how, or

processes, or consist of the development and transfer of a plan or technical design.”

MoU of the India USA Tax Treaty: Technology will be considered "made available" when the person acquiring the

service is enabled to apply the technology The fact that the provision of the service may require technical input by the person

providing the service does not per se mean that technical knowledge, skills, etc., are made available to the person purchasing the service, within the meaning of paragraph 4(b)

Similarly, the use of a product which embodies technology shall not per se be considered to make the technology available

If the services do not ―make available‖ technical knowledge, etc., then, they are outside the ambit of FIS Article and may not be taxable. However, the same may be considered as business income and taxable if the foreign company has a PE in India

Fees for Included Services

Fees for included services Understanding Concept of FIS Extract from Raymond Ltd. V/s. DCIT [86 ITD 791](Mum) ―….. the normal, plain and grammatical meaning of the language employed, in our understanding, is that a mere rendering of services is not roped in unless the person utilising the services is able to make use of the technical knowledge, etc. by himself in his business or for his own benefit and without recourse to the performer of the services in future. The technical knowledge, experience, skill, etc. must remain with the person utilising the services even after the rendering of the services has come to an end. A transmission of the technical knowledge, experience, skills, etc. from the person rendering the services to the person utilising the same is contemplated by the Article. Some sort of durability or permanency of the result of the “rendering of services” is envisaged which will remain at the disposal of the person utilising the services. The fruits of the services should remain available to the person utilising the services in some concrete shape such as technical knowledge, experience, skills, etc.”

Fees for included services MOU signed between India and USA is binding on other countries Tax Treaty? Favourable orders IntertekTesting Services India P Ltd. (307 ITR 418) (AAR) CESC Ltd. (275 ITR 15) (Kolkata) Boston Consultancy Group P Ltd .(94 ITD 31) (Mum) Mckinsey& Co. Inc. (99 ITD 549) Raymond Ltd. (80 TTJ 120) (Mum) Bharti Axa(326 ITR 477) (AAR) Unfavourable orders AAR ruling in the case of PerfettiVan MelleHolding B.V.(AAR No. 869 of 2010) dated 9

December 2011 AAR ruling in the case of Shell India Markets Pvt Ltd(AAR No. 833 of 2009) dated 17 January

2012

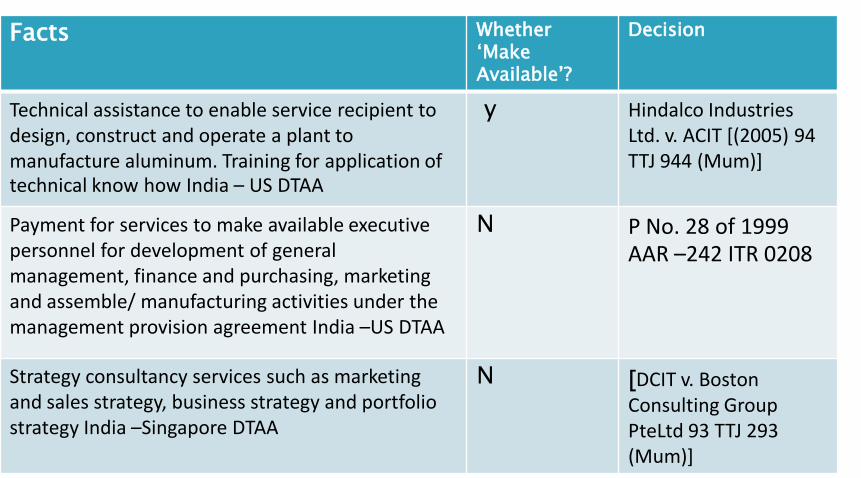

Facts Whether ‘Make Available’?

Decision

Technical assistance to enable service recipient to design, construct and operate a plant to manufacture aluminum. Training for application of technical know how India – US DTAA

y Hindalco Industries Ltd. v. ACIT [(2005) 94 TTJ 944 (Mum)]

Payment for services to make available executive personnel for development of general management, finance and purchasing, marketing and assemble/ manufacturing activities under the management provision agreement India –US DTAA

N P No. 28 of 1999 AAR –242 ITR 0208

Strategy consultancy services such as marketing and sales strategy, business strategy and portfolio strategy India –Singapore DTAA

N [DCIT v. Boston Consulting Group PteLtd 93 TTJ 293 (Mum)]

Facts Whether ‘Make Available’?

Decision

Service of the grading and certification reports for diamonds and other articlesIndia –Singapore DTAA

N Diamond Services International P Limited v. Union of India (Bom) –304 ITR 201

Payment for providing training to crew members India –UK DTAA

N Sahara Airlines Ltd v. DyCIT –83 ITD 11

Payment for operational and support services India –Netherland DTAA

Y PerfettiVan MelleHolding B.V. -AAR No. 869 of 2010)

Data processing services agreement India –UK DTAA

N R. R. Donnelley India Outsource (P) Ltd. –335 ITR 122

Publicity, advertisement and sales services India –USA DTAA

N DIT vsSheraton Ltd. –313 ITR 267