Embed Size (px)

Citation preview

TAXATION OF EMIGRANT & IMMIGRANT EXPATRIATES

Mr. T. P. OSTWAL

June 2011 1T.P.Ostwal & Associates

EXPATRIATES- AN INTRODUCTION

IMMIGRANT EXPAT RESIDENTIAL STATUS – ITA /DTAA

TAX IMPLICATIONS & EXEMPTIONS

June 2011 2T.P.Ostwal & Associates

CONCEPTS – DUAL EMPLOYMENT/ DEPUTATION / SECONDMENT

EMIGRANT EXPATRIATE TAX & ISSUES

DTC PERSPECTIVE AND OTHER GENERAL ISSUES

EXPATRIATES - AN INTRODUCTION

June 2011 3T.P.Ostwal & Associates

WHO IS AN EXPATRIATE?

The term Expatriate has not been defined under the Income Tax Act (‘ITA’)

General meaning of the term:

Expatriate means a person temporarily or permanently residing in a country orculture other than that of a person’s upbringing or residence.

� Typically expatriate refers to an employee working abroad and who comes to workin a country (other than his country of residence) for a short period (say 6 months to5 years). They do not intend to become permanent residents.

June 2011 4T.P.Ostwal & Associates

5 years). They do not intend to become permanent residents.

� Appointment of foreign nationals becomes necessary in case of jointventures and subsidiaries that are fully owned and controlled by theforeign parent entity. Such appointment could be driven by factors likeprotecting trade and technology secrets for strategic reasons.

� The appointment of such foreign nationals is comparable to their salariesdrawn abroad and as such quite high for the Indian employer employingthe foreign nationals. Thus both employment and compensation of theexpatriates require careful thought of registration

EXPATRIATES - NEED??

June 2011 5T.P.Ostwal & Associates

expatriates require careful thought of registration

Social Security

Comp and

benefits

Corporate tax issues

Business need issues

Administration issues

INTERNATIONAL ASSIGNMENT : CHALLENGES –TAX / LEGAL / HR

Social Security planning

Relocation process and Control

Costs of employment / Risks

Corporate Tax, Transfer Pricing,

PE issues,

Package design, Assignment policy, Pensions

June 2011 6T.P.Ostwal & Associates

Immigration services

Withholding

Taxes

Income Taxes

Employment Law

Assignment contracts, Minimum wage requirements

Host and Home country taxation

Tax deduction at source requirements / filings

Work permit/ visa obligations

PE issues, Service tax issues

TYPES OF EXPATRIATE ASSIGNMENTS

June 2011 7T.P.Ostwal & Associates

TAXATION OF IMMIGRANT EXPATRIATES

June 2011 8T.P.Ostwal & Associates

EXPATRIATES

RESIDENTIAL STATUS –ITA /DTAA

June 2011 9T.P.Ostwal & Associates

ITA /DTAA

RESIDENTIAL STATUS – INCOME TAX ACT

Basic Tests:An individual who stays in India for:�� 182 days or more; or�� 60 days or more in a tax year & 365

days or more during preceding 4 taxYears.

Additional Tests:�� Non-resident in India in 9 out of 10

preceding tax years; or��Stays in India for an aggregate period

of 729 days or less in the preceding 7 tax years.

Exceptions :

Period of 60 days substituted by 182 days in following cases:

• An Indian citizen who leaves India during the tax year for the purposes of

June 2011 10T.P.Ostwal & Associates

Resident Not Ordinarily Resident

Non-resident

Passes either of the two basic tests

Passes either of the two basic tests

Fails the basic tests

Fails both the additional tests

Passes both the additional tests

Fails the additional tests

• An Indian citizen who leaves India during the tax year for the purposes of employment outside India as a member of crew of an Indian ship

• Indian citizen or a person of Indian origin who comes on a on a visit to India during the tax year

RESIDENTIAL STATUS – INCOME-TAX

Some judicial precedents worth noting in this case are:

� Day of arrival & departure in India.

� Advance Ruling (233 ITR 462) – Both days should be counted as “inIndia”.

� Jaipur Tribunal (No. 1230 dated. 22.8.86) (ITO V/s. Dr. R. K. Sharma)Only day of departure has to be considered as “in India”.

June 2011 11T.P.Ostwal & Associates

Only day of departure has to be considered as “in India”.

� As per the International Rule of OECD both days should beconsidered.

SCOPE OF TAXATION

Residential status Taxability of Income

(i) Resident All income of the previous year wherever accruingor arising or received by him including incomesdeemed to have accrued or arisen.

(ii)Resident but not ordinaryResident

All Income accruing or arising or deemed to haveaccrued or arisen or received in India. Moreover,all income earned outside India will also beincluded if the same is derived from a business or

June 2011 12T.P.Ostwal & Associates

included if the same is derived from a business orprofession controlled or set up in India.

(iii)Non-Resident All income accruing, arising to or deemed to haveaccrued or arisen or received in India.

RESIDENTIAL STATUS - DTAA

� Dual Residence:

If an individual is a resident of both the countries and if there is DTAA, thenhis residential status shall be determined as per the ‘Tie-breaker’ Rule asunder:

� Permanent Home;

� Centre of vital interests (Personal & economic relations);

� Habitual Abode

� Nationality;

� Mutual Agreement Procedure.� Mutual Agreement Procedure.

� Dual Non-Residence:

� Due to different fiscal year endings, a person may be a non-resident of both - the

home country & the host country.

� Also due to non compliance with the thresholds of both the countries one could

be non resident in both the countries.

� As a non-resident of both countries, he will not be entitled to DTAA relief.

� Domestic relief also may not apply.

June 2011 13T.P.Ostwal & Associates

TAX IMPLICATIONS & EXEMPTIONS

June 2011 14T.P.Ostwal & Associates

EXPATRIATE TAXATION IN INDIA

� Residential status irrelevant when employment is performed in India or income is received in India. The following tax implications arise

� Sec 5 -Income accrues in India.

� Indian salary plus foreign salary is taxable in India.

� Place of payment of salary is irrelevant when employment is performed in India

� Subject to threshold and conditions under domestic law and/ or applicable tax

treaty.treaty.

� Payment for rest period

Therefore when employee is employed abroad and contract is also signed outsideIndia, but renders services in India, Section 9(1)(ii) comes into play and income isdeemed to accrue or arise in India and the same will be liable to tax in India. Alsosalary for rest period before & after services rendered in India is taxable, ifpayment is related to services rendered in India, it is taxable.

� Physical presence determines residential status

June 2011 15T.P.Ostwal & Associates

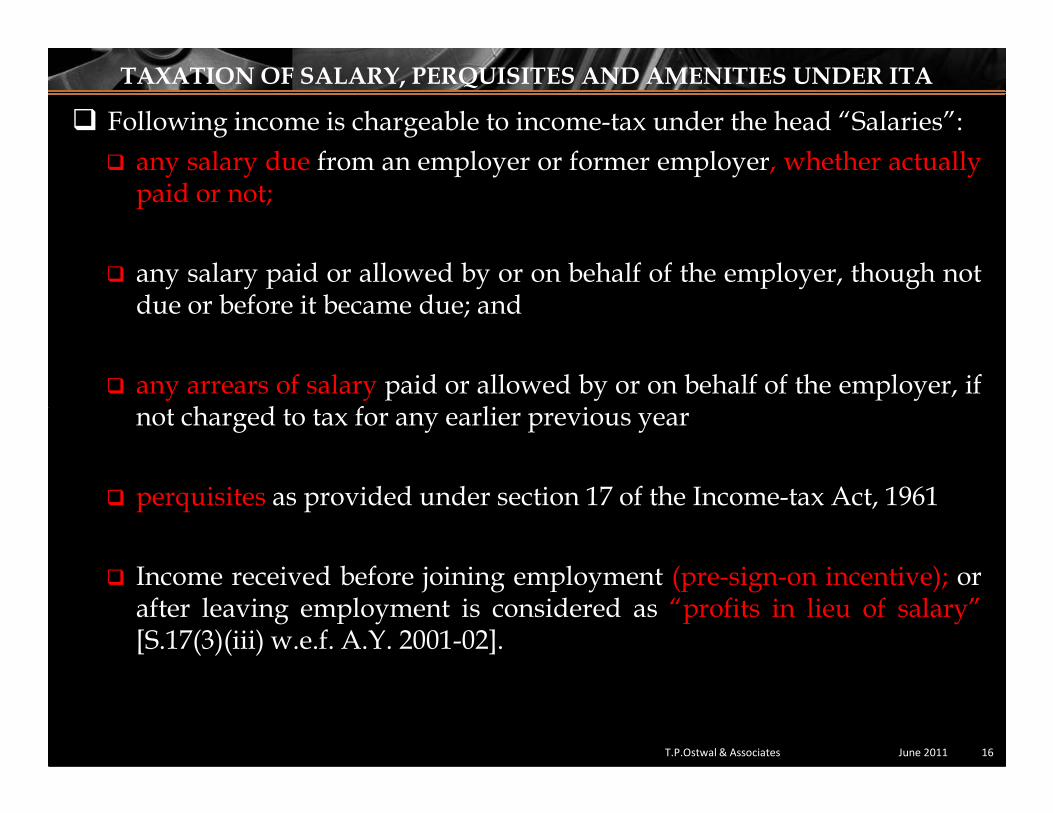

TAXATION OF SALARY, PERQUISITES AND AMENITIES UNDER ITA

� Following income is chargeable to income-tax under the head “Salaries”:

� any salary due from an employer or former employer, whether actuallypaid or not;

� any salary paid or allowed by or on behalf of the employer, though notdue or before it became due; and

� any arrears of salary paid or allowed by or on behalf of the employer, ifnot charged to tax for any earlier previous yearnot charged to tax for any earlier previous year

� perquisites as provided under section 17 of the Income-tax Act, 1961

� Income received before joining employment (pre-sign-on incentive); orafter leaving employment is considered as “profits in lieu of salary”[S.17(3)(iii) w.e.f. A.Y. 2001-02].

June 2011 16T.P.Ostwal & Associates

�Salary to include:

� Wages

� Any annuity or pension

� Any gratuity

� Any fees, commissions, perquisites or

profit in lieu of salary

TAXATION OF SALARY, PERQUISITES AND AMENITIES UNDER ITA

June 2011 17T.P.Ostwal & Associates

profit in lieu of salary

� Any advance salary

� Leave encashment

� Annual accretion to recognized provident

fund

� Contribution by employer to an approved

pension scheme

TAXATION OF SALARY, PERQUISITES AND AMENITIES UNDER ITA

� Sec 17(2)- “perquisites” includes:

� Rent free accommodation;

� Concessional accommodation

� Obligation of employee met by employer;

� Fringe benefits (other than those covered by Chapter XII-H of ITA) as prescribed byRule 3 of Income Tax Rules, 1962.

� Rule 3 of Income Tax Rules, 1962 covers:

� Use of Motor Car;

� Interest free/ Concessional Loan;

� Provision of food and non-alcoholic beverages;

� Gifts/Voucher/Tokens;

� Membership fees/annual fees charged to Credit card;

� Club fees;

� Services of sweeper, gardener, watchman, personal attendant;

� Supply of Electricity, gas, water;

� Education facility to family members of employee;

� Use/transfer of movable asset.June 2011 18T.P.Ostwal & Associates

TAXATION OF SALARY, PERQUISITES AND AMENITIES UNDER ITA

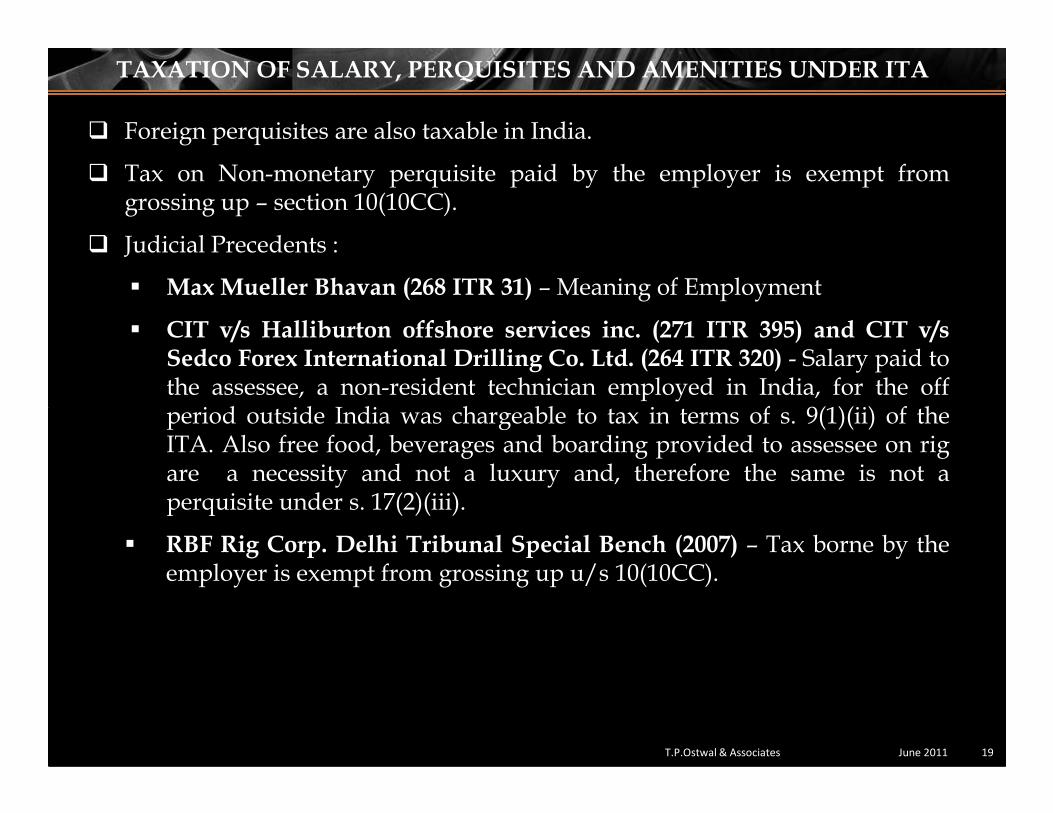

� Foreign perquisites are also taxable in India.

� Tax on Non-monetary perquisite paid by the employer is exempt fromgrossing up – section 10(10CC).

� Judicial Precedents :

� Max Mueller Bhavan (268 ITR 31) – Meaning of Employment

� CIT v/s Halliburton offshore services inc. (271 ITR 395) and CIT v/sSedco Forex International Drilling Co. Ltd. (264 ITR 320) - Salary paid tothe assessee, a non-resident technician employed in India, for the offperiod outside India was chargeable to tax in terms of s. 9(1)(ii) of theperiod outside India was chargeable to tax in terms of s. 9(1)(ii) of theITA. Also free food, beverages and boarding provided to assessee on rigare a necessity and not a luxury and, therefore the same is not aperquisite under s. 17(2)(iii).

� RBF Rig Corp. Delhi Tribunal Special Bench (2007) – Tax borne by theemployer is exempt from grossing up u/s 10(10CC).

June 2011 19T.P.Ostwal & Associates

TAXATION OF SALARY, PERQUISITES AND AMENITIES UNDER ITA

All expatriates are taxed on any compensation received for services rendered in India. Suchcompensation will include salary, fee, commission, profits in lieu of salary, advance salary,perquisite, allowances, etc. Broadly, the taxability of the typical component of an expatriate compensation package will include:

Description Taxable on full

amount

Taxed on a

concessional value

Exempt from

tax

Base Salary ✓

All allowances other than those specifically considered below ✓

Bonus / Commission / Incentive

June 2011 20T.P.Ostwal & Associates

Bonus / Commission / Incentive ✓

Housing Allowance ✓

Rent free accommodation ✓

Temporary accommodation on transfer ✓

Utilities ✓

Children's Education ✓

Medical benefits ✓

Reimbursement of specified expenses ✓✓✓✓

Home leave travel ✓✓✓✓

STOCK OPTIONS - BASICSOption life

Vesting period / grant period Exercise period

0 1 2 3 4 5 6 7

Vesting could be

•Gradual (1/3rd,1/3rd,1/3rd)

• Back ended (10%,10%,80%)

• Cliff (0%,0%, 100%)

Vesting upon fulfillment of conditions

• Service term / loyalty

• Performance

Grant

date

Vesting

dateExercise date Event of allotment

/ transfer

Grant of Options No Tax

No TaxVesting of Options

Events Tax Impact

STOCK OPTION CYCLE

June 2011 22T.P.Ostwal & Associates

Taxable PerquisiteExercise of Options*

No TaxAllotment of Shares

Capital GainsSale of Shares

* Relevant from valuation perspective

• Any exercise of options on or after 1 April 2009 is taxed as perquisite in the hands of

employees

• Tax on perquisite in the hands of employees will be @ 30.90 percent

• Withholding tax on Perquisite by Company = FMV on date of exercise of option less

exercise price paid by employee * 30.90 percent

• FMV on date of exercise becomes the cost base for computing capital gains

• Long Term Capital Gains on sale

TAXATION OF ESOPS

June 2011 23T.P.Ostwal & Associates

• Long Term Capital Gains on sale

– Taxable (Pre listing) in the hands of individual @ 20.60 percent

– Taxation (Post listing) in hands of individual - Nil [sec 10(38)]

• Short Term Capital Gains on sale

– Taxable (Pre listing) in the hands of individual @ 30.90 percent

– Taxation (Post listing) in hands of individual @ 15.45 percent

� Hon’ble SC decision in the case of Infosys Technologies Ltd (297 ITR 167)

� No taxability at the time of issue / vesting of options

� Shares with lock-in conditions do not have a realizable value and hence are of negligible value

� Does the ratio of the said decision apply post introduction of Rule 3(8) r.w.s. 17(2)(vi)?

TAXATION OF ESOPS

June 2011 24T.P.Ostwal & Associates

3(8) r.w.s. 17(2)(vi)?

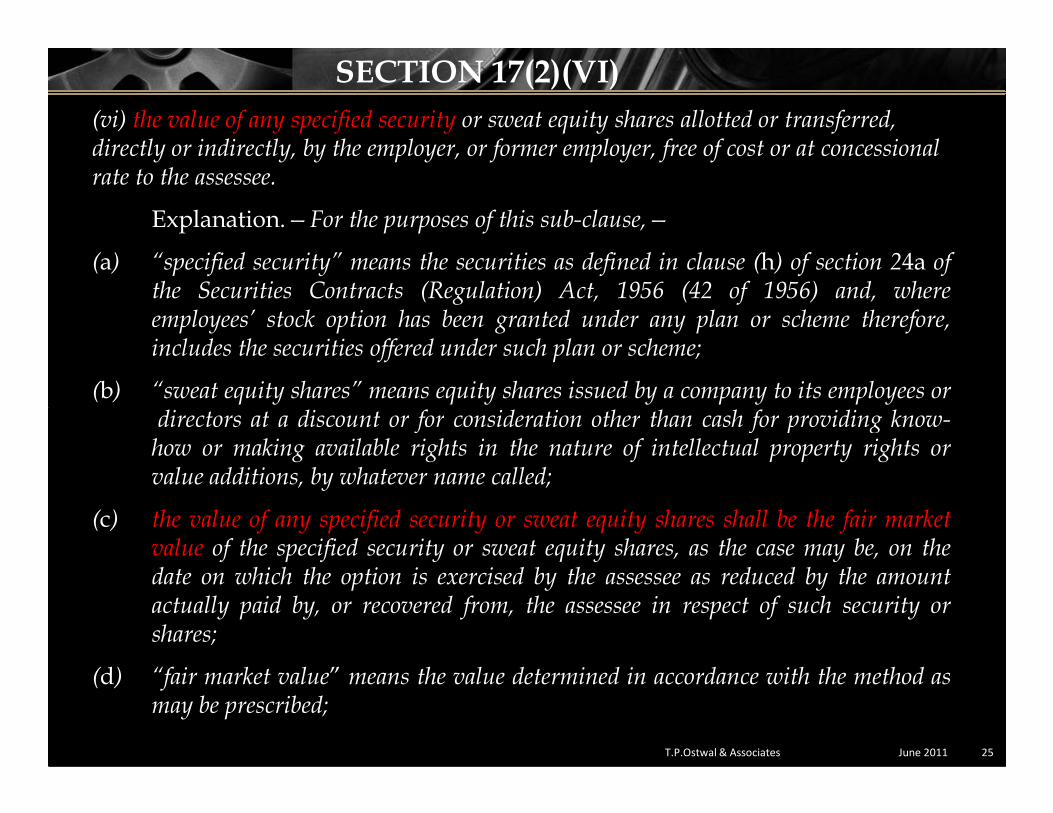

(vi) the value of any specified security or sweat equity shares allotted or transferred, directly or indirectly, by the employer, or former employer, free of cost or at concessional rate to the assessee.

Explanation.—For the purposes of this sub-clause,—

(a) “specified security” means the securities as defined in clause (h) of section 24a ofthe Securities Contracts (Regulation) Act, 1956 (42 of 1956) and, whereemployees’ stock option has been granted under any plan or scheme therefore,includes the securities offered under such plan or scheme;

(b) “sweat equity shares” means equity shares issued by a company to its employees ordirectors at a discount or for consideration other than cash for providing know-

SECTION 17(2)(VI)

June 2011 25T.P.Ostwal & Associates

directors at a discount or for consideration other than cash for providing know-how or making available rights in the nature of intellectual property rights orvalue additions, by whatever name called;

(c) the value of any specified security or sweat equity shares shall be the fair marketvalue of the specified security or sweat equity shares, as the case may be, on thedate on which the option is exercised by the assessee as reduced by the amountactually paid by, or recovered from, the assessee in respect of such security orshares;

(d) “fair market value” means the value determined in accordance with the method asmay be prescribed;

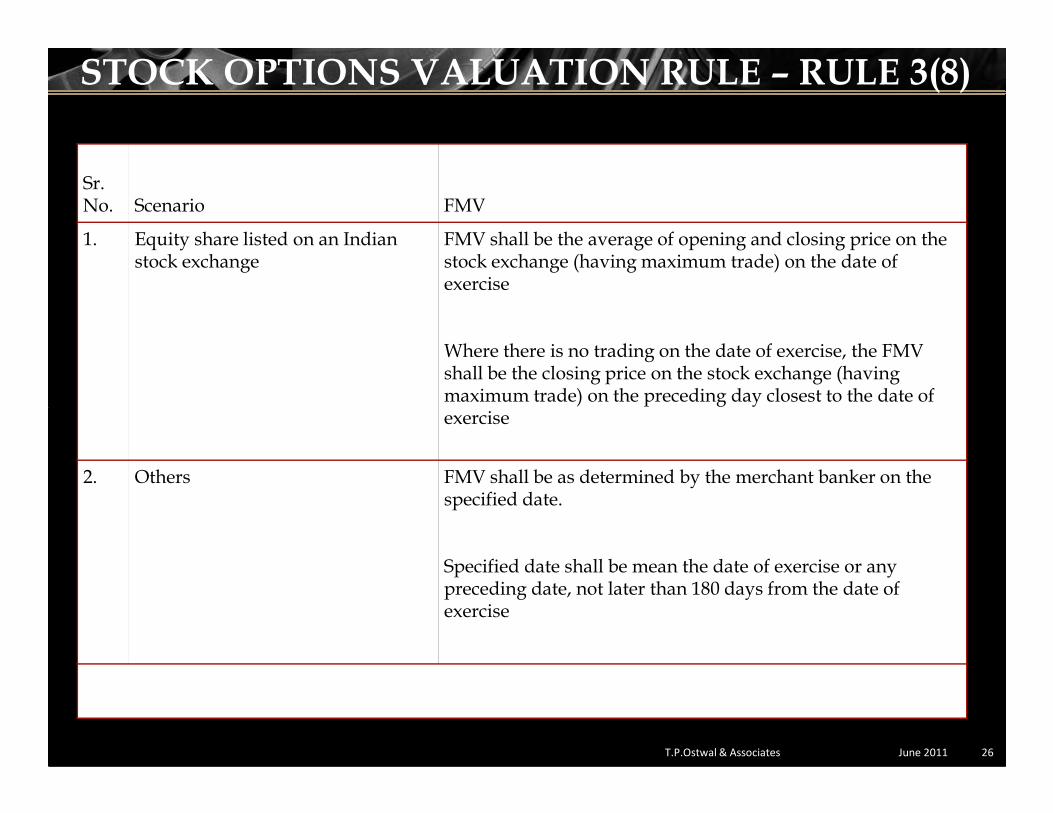

Sr. No. Scenario FMV

1. Equity share listed on an Indian stock exchange

FMV shall be the average of opening and closing price on the stock exchange (having maximum trade) on the date of exercise

Where there is no trading on the date of exercise, the FMV shall be the closing price on the stock exchange (having maximum trade) on the preceding day closest to the date of exercise

STOCK OPTIONS VALUATION RULE – RULE 3(8)

June 2011 26T.P.Ostwal & Associates

exercise

2. Others FMV shall be as determined by the merchant banker on the specified date.

Specified date shall be mean the date of exercise or any preceding date, not later than 180 days from the date of exercise

Timing Mismatches

� Source State may tax at any time

� Residence State forced to grant relief

� Connection between option and service:

STOCK OPTIONS – COMM. ON ART. 15, PARA 12.2 EMPLOYMENT BENEFIT VS. CAPITAL GAIN

Stock option

Art. 15 – benefit

derived from option

until exercised, sold

Art. 13 – option

exercised,

subsequent and service:

� Facts & circumstances

� General guidance in the OECD Commentary

until exercised, sold

or alienatedsubsequent

gain

CONVERSION RATE FOR SALARY EARNED INFOREIGN CURRENCY

� RULE 26 vs. RULE 115

� Rule 26:

For the purpose of deduction of tax at source on any income payable in foreigncurrency, the rate of exchange for the calculation of the value in rupees of suchincome payable to an assessee outside India shall be the telegraphic transferbuying rate of such currency as on the date on which the tax is required tobe deducted at source under the provisions of Chapter XVIIB by the personbe deducted at source under the provisions of Chapter XVIIB by the personresponsible for paying such income.

� Rule 115:

The rate of exchange for the calculation of the value in rupees of any incomeaccruing or arising or deemed to accrue or arise to the assessee in foreigncurrency or received or deemed to be received by him or on his behalf in foreigncurrency shall be the telegraphic transfer buying rate of such currency as onthe specified date.

“specified date” means-

(a) in respect of income chargeable under the head “ Salaries”, the last day of the month immediately preceding the month in which the salary is due, or is paid in advance or in arrears;……………..

Provided that the specified date, in respect of income referred to sub-clauses (a) to(f) payable in foreign currency and from which tax has been deducted at sourceunder Rule 26, shall be the date on which the tax was required to be deductedunder the provisions of the Chapter XVII-B.

CONVERSION RATE FOR SALARY EARNED INFOREIGN CURRENCY

June 2011 29T.P.Ostwal & Associates

under the provisions of the Chapter XVII-B.

� Credit in respect of overseas taxes paid not covered by Rule 115. The exchange rate on the date of payment of overseas tax is relevant.

TAXATION UNDER DTAA

� Governed by Article titled “Dependent Personal Services”;

“Income from Employment”.

� Application restricted to employer – employee relationship

established as per source country understanding.

� Treaty of relevance is that of country of residence of the employee.

June 2011 30T.P.Ostwal & Associates

� Treaty of relevance is that of country of residence of the employee.

� Concerned with cases of general applicability; not concerned with

special categories of employees such as consulate staff, UN

employees,

� Necessity and significance of the Article.

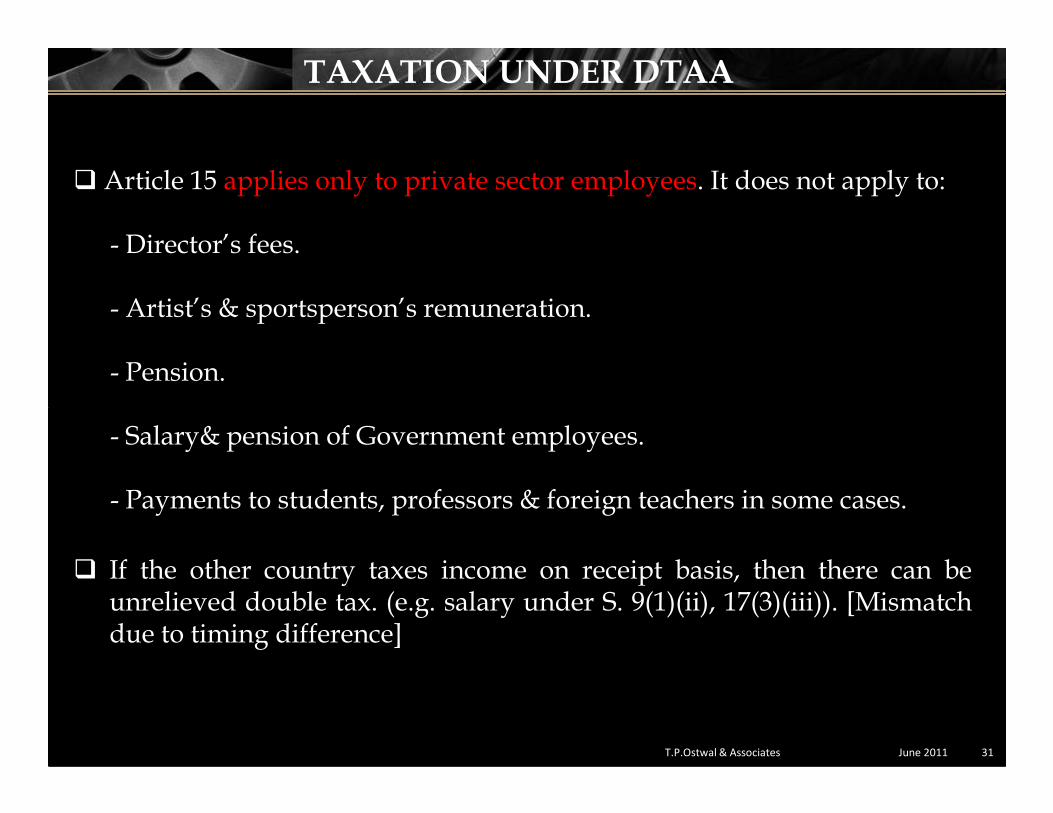

� Article 15 applies only to private sector employees. It does not apply to:

- Director’s fees.

- Artist’s & sportsperson’s remuneration.

- Pension.

TAXATION UNDER DTAA

June 2011 31T.P.Ostwal & Associates

- Salary& pension of Government employees.

- Payments to students, professors & foreign teachers in some cases.

� If the other country taxes income on receipt basis, then there can beunrelieved double tax. (e.g. salary under S. 9(1)(ii), 17(3)(iii)). [Mismatchdue to timing difference]

�Extract from Klaus Vogel on Double Taxation Conventions

at page 899 :

“An employer is someone to whom an employee is committed to supply his

capacity to work and under whose directions the latter engages in his activities

and whose instructions he is bound to obey”

� Performance of duties subject to directions, instructions and

superintendence of the employer.

EMPLOYER – EMPLOYEE RELATIONSHIP

June 2011 32T.P.Ostwal & Associates

superintendence of the employer.

� Employee does not include

� Professionals, freelancers

� Working partner

� Director in his capacity as a Board member

� Distinction between “contract of service” and “contract for service”

� The following are the tests on existence of an “employer-employee‟relation

� Authority to instruct the personnel regarding the manner ofperformance of work

� Control, supervision and responsibility for the place in which the

WHO IS THE EMPLOYER ?

June 2011 33T.P.Ostwal & Associates

Control, supervision and responsibility for the place in which thework is performed

� Bear the remuneration of the personnel� Put the tools and materials necessary for the work at the individual's

disposal

The above mentioned tests have been dealt with in the Supreme Courtdecisions of:*Lakshminarayan Ram Gopal (25 ITR 449); Piyare Lal Adishwar Lal (40 ITR17); Ram Prashad (86 ITR 122)

WHO IS THE EMPLOYER ?

Additional factors laid down recently by various Courts for determiningthe real/economic employer:

� Right to terminate employment

�AT&S India (287 ITR 421)� Tekmark Global Solutions (3 taxmann.com 38)� IDS Software Solutions (2009-TIOL-82-BANG)

� Responsibility of work performance, no warranty from foreign entity

June 2011 34T.P.Ostwal & Associates

Responsibility of work performance, no warranty from foreign entity

� CIT v Morgan Stanley (292 ITR 416)� Dolphin Drilling Ltd (121 TTJ 433)� IDS Software Solutions (2009-TIOL-82-BANG)

� Compliance with regulations and management systems, work schedules

�Dolphin Drilling Ltd (121 TTJ 433)� AT& S India (287 ITR 421)

� Issue of appointment letters with terms and conditions of appointment

� Dolphin Drilling Ltd (121 TTJ 433)

� Powers/duties of secondees regulated by Articles of Association

� IDS Software Solutions (2009-TIOL-82-BANG)

� Impact of a service agreement/ foreign collaboration agreement –Foreign entity under an obligation to provide services?

WHO IS THE EMPLOYER ?

June 2011 35T.P.Ostwal & Associates

Foreign entity under an obligation to provide services?

� AT&S India (287 ITR 421)� Cholamandalam MS General Insurance (2009-TIOL-02-ARA),� M/s Karlstorz Endoscopy India (2010-TII-135-ITAT-DEL-INTL) affirmed by Delhi

HC

�Lien on employment retained

� CIT v Morgan Stanley (292 ITR 416)

�Reimbursement without mark up

In favour of assessee� Cholamandalam MS General Insurance (2009-TIOL-02-ARA)� Tekmark Global Solutions (3 taxmann.com 38)Against the assessee

�Verizon Data Services India (AAR)�AT & S India (287 ITR 421)

� Economic Employer

WHO IS THE EMPLOYER ?

June 2011 36T.P.Ostwal & Associates

�Eli –Lilly & Co (India) Pvt Ltd (2009) 223 CTR (SC) 20�Verizon Data Services India (AAR)�AT&S (287 ITR 421)�IDS Software Solutions (2009 –TIOL-82-BANG)�HCL Infosystems 274 ITR 261 (Del)

Direct Taxes Code, 2010 (DTC)Definition of “employer” [Section 314(88)]A person who controls an individual under an express or impliedemployment contract; and is obliged to compensate him by way of salary

PE EXPOSURE FOR FOREIGN EMPLOYERS

� Presence of employees in India can amount to a PE. Profits attributable to the PEcan be taxable in India.

� If there is an office in India from where the employees work, the place couldbecome a fixed place available to such employer in India and accordingly canamount to a fixed place PE.

� Apart from Fixed place PE, a service PE can be said to exist even if the foreigncompany that is deputing its employee does not have any fixed place of businesscompany that is deputing its employee does not have any fixed place of businessin India.

� Normally, a threshold period is specified in the DTAA for the purpose ofdetermining whether a service PE exists, i.e. if the period for which services arerendered in India exceeds the stipulated time period, a service PE may beconstituted in India. However certain DTAA’s like USA, Australia and Canada donot have a single day threshold if services are rendered to AE.

� In both cases, profits attributable to the PE can be taxable in India.June 2011 37T.P.Ostwal & Associates

PE EXPOSURE FOR FOREIGN EMPLOYERS

Judicial Pronouncements

� Motorola, Ericsson and Nokia – Delhi Tribunal Special Bench (2005).

The manner of operations in India by the employee, gave an impression that there is aPE.

� Director of Income Tax (International Taxation) vs. Morgan Stanley & Co. Inc. (292ITR 416) - US company sending its employees on deputation to resident company fora period of two years on the request of resident company to render their expertservices, resident company constitutes service PE of US company within the meaningof Art. 5(2)(1).

� Rolls Royce Plc v DDIT [122 TTJ 359 (Del Tribunal]

The Tribunal held that Rolls Royce PLC, a UK company engaged in the supply of aeroengines to Indian customers, had a PE in India under the basic rule, because itsemployees visited India frequently and the premises of one of its affiliate companieswas occupied and used during such visits.

While the OECD Commentary recognizes that no formal or legal right to use aparticular place is required for a place to constitute a PE, the Commentary also statesthat mere presence of an enterprise at a particular location does not mean that thelocation is at the disposal of the enterprise.

June 2011 38T.P.Ostwal & Associates

EXEMPTION FROM INDIAN TAX

SHORT STAY EXEMPTION - [SEC 10(6)(VI)] of Income-tax Act, 1961 (“the Act”) –

� 90 day’s rule : Exemption from tax to employee of a foreign enterprise forremuneration received for services rendered in India if:

� The employee is a foreign citizen

� The foreign enterprise is not engaged in any trade or business in

KEY EXEMPTIONS

� The foreign enterprise is not engaged in any trade or business in

India.

� The employee’s aggregate days of stay in India do not exceed 90 days

during the tax year

� His employer does not claim the remuneration paid to him as a deduction under the provisions of the Act.

Conditions are cumulative

June 2011 39T.P.Ostwal & Associates

EXEMPTION FROM INDIAN TAX

SHIP STAY EXEMPTION - SECTION 10(6)(VIII) of the Act

� 90 day’s rule : Exemption from tax to a non resident employee forremuneration received in connection with employment on a foreign ship if:

� The employee is a foreign citizen

� The salary is earned in connection with the employment on a foreign ship

�The employee’s aggregate days of stay in India do not exceed 90 days

June 2011 40T.P.Ostwal & Associates

�The employee’s aggregate days of stay in India do not exceed 90 days

during the tax year.

Conditions are cumulative

Salary earned by a non- resident for services performed outside India on aboard of ship does not accrue or arise in India.

DIT v Prahlad Vijendra Rao 51 DTR 95 / 239 CTR 107. (Karn.)(High Court)

CIT Vs. Goslino Mario and Others –241 ITR 312

Daily allowances were received by foreign technician for meeting expenses(i.e. food and other expenses) while on assignment in India. The technicianswere required to stay away from their homes (normal place of residence)during their stay in India.

EXEMPTION FROM INDIAN TAX

SECTION 10(14) of the Act – TAXATION OF SPECIAL ALLOWANCES

June 2011 41T.P.Ostwal & Associates

The HC held that the daily allowances provided were wholly andnecessarily incurred in performance of duties. Accordingly, the same areexempt u/s 10(14) to the extent such expenses are actually incurred for thatpurpose.

The Supreme court has upheld the above view of the HC.

EXEMPTION FROM TAX

Double Taxation Avoidance Agreement (“DTAA”)

� Expatriate to be resident of the other contracting state but exercisingemployment in India

� As per Article 15(2) of the DTA - Remuneration received not taxable inIndia if following conditions are satisfied:

�Employee does not stay in India for more than 183 days in a 12 monthperiod commencing or ending in a fiscal year,

� Remuneration is paid by a non-resident employer, and� Remuneration is paid by a non-resident employer, and

� Remuneration is not borne by PE/PE has claimed the deduction/deductible expenditure by PE or Fixed Base of employer in India.

Conditions are cumulative

� Judicial Precedent worth noting in this case

Taxpayer not eligible to claim short stay exemption under the India- UKDouble Taxation Avoidance Agreement (‘DTAA’ or ‘the Indo-UKTreaty’) as the salary was paid directly by the Indian subsidiary.

CIT v R. Rajgopal [ TS-222-HC-2011 (MAD)]

June 2011 42T.P.Ostwal & Associates

WHAT DO YOU MEAN BY - “BORNE BY”

�What is the meaning of “borne by”?

- Debiting accounts.- Payment by a PE.- Deduction from profits for taxation.- Attributed to the PE.

�An economic concept rather than an accounting concept

June 2011 43T.P.Ostwal & Associates

�Direct and proximate relation with the PE

�Emphasis on deductibility and not on actual deduction. Some DTAs use the words “deductible”. (Indian DTAs with Australia, Belgium, UK.)

The OECD commentary on Article 15 which deals with ‘Income fromEmployment’ states that the phrase ‘borne by’ must be interpreted in thelight of the underlying purpose of sub paragraph (c) of the Article, which isto ensure that the exception provided for in paragraph does not apply toremuneration that is deductible, having regard to the principles of Article7, in computing the profits of a permanent establishment situated in theState in which the employment is exercised.

MEANING OF ‘BORNE BY’

June 2011 44T.P.Ostwal & Associates

State in which the employment is exercised.

Klaus Vogel in his book ‘Double Taxation Conventions’ states that“Remuneration for dependent personal services is considered to have been‘borne by’ a permanent establishment or fixed base if it can be claimed asa deduction for business expenses when calculating the profits to beattributed to the establishment or base.

� Reimbursement of costs by / to PE – Does it mean PE has “borne” thesalary?A foreign employer initially pays the salary of an employee, but its PEreimburses the foreign employer in a deductible payment which can beidentified as a reimbursement. [Technical Explanation to India-US Tax Treaty]

The test of “deductibility” is said to have been met and remuneration is regardedas “borne by” a PE .

� Remuneration regarded as paid by a non-resident employer (NR) when:

WHAT DO YOU MEAN BY - “BORNE BY”

June 2011 45T.P.Ostwal & Associates

� Remuneration regarded as paid by a non-resident employer (NR) when:It is initially paid by an Indian contractor on behalf of NR Employer andsubsequently recovered from NR employer [Nakazono vs. ACIT (2003) SOT31(Del)]

� The “base erosion” principle is important. If the PE has claimed salary asa deduction, it should be considered as “borne by”.

The employer has been assessed on a presumptive basis (i.e., where taxable profits are determined at a fixed percentage of gross receipts) It was held that the deductibility test is met and the salary would be construed to be ‘borne by’ PE. Merely by virtue of presumptive taxation, it cannot be said that the deduction is not available.

Lloyd Helicopters International P Ltd (2001) 249 ITR 162 (AAR)

The same view has been held in Ensco Maritime Ltd vs DCIT (2004) 91 ITD 459 (Del)

Salary to the Italian expatriate paid by the Italian company and the Indian PE does not bear the salary cost. It was held that the salary of Italian expatriate is not ‘borne

JUDICIAL PRECEDENT – ‘BORNE BY’

June 2011 46T.P.Ostwal & Associates

not bear the salary cost. It was held that the salary of Italian expatriate is not ‘borne by’ PE

CIT v. Elitos S.P.A (2005) 145 Taxman 210

‘Borne by’ means liable to be deducted. Assessment on presumptive basis does not mean expenses not deductible. It has to be deemed that all revenue expenses , including salaries paid are allowed as deduction.

DHV Consultants BV 227 ITR 97 (AAR)

Article 4 (1) –Resident of a Contracting State

Person:Liable to tax under the laws of the contracting state by reason of his domicile,residence, place of management or any other criterion of similar nature but doesnot include person liable to tax only on income from sources in that state.

TREATY APPLICABILITY – “LIABLE TO TAX”

� Divergent interpretations!

� View 1 – “Liable to tax” is a wider term than “subject to tax” and covers not only present but potential tax liability

− M.A Rafique (1995) 213 ITR 317 AAR

June 2011 47T.P.Ostwal & Associates

− M.A Rafique (1995) 213 ITR 317 AAR

− Emirates Fertilizers Trading Company (2005) 272 ITR 0084 AAR

− Green Emirates Shipping & Travels (2006) 99 TTJ 988 (Mum)

− Azadi Bachao Andolan (2003) 263 ITR 706 (SC)

� View 2 – Liable to tax implies existence of tax liability in present and not in future and no benefit could be granted under treaty when there is no tax incidence.

− Cyril Pereira (1999) (239 ITR 650)

− Abdul Razak A. Meman’s case (2005) 276 ITR 306 AAR

TAX EQUALIZATION – HYPO TAX

� An Inbound employee may be taxed at a higher rate in India than in hisHome country. In such a case, he would be disinclined to work in India.

� In order to compensate the inbound employees for such enhanced taxincidence, it is an internationally known practice for the employer to bearsuch additional tax liability of the employees deputed abroad. This practice isknown as “tax equalization”.

� Illustration:

Gross salary 100

Add: Total tax liability in India 30

June 2011 48T.P.Ostwal & Associates

Add: Total tax liability in India 30

Less: Hypothetical tax i.e. (tax that would have been paid in home country)

25

Tax borne by the employer under the “tax equalization” policy

5

Add: Tax on such tax (Bal Fig) 2.15

Tax as grossed up (5*100/70) 7.15

Total salary 117.15

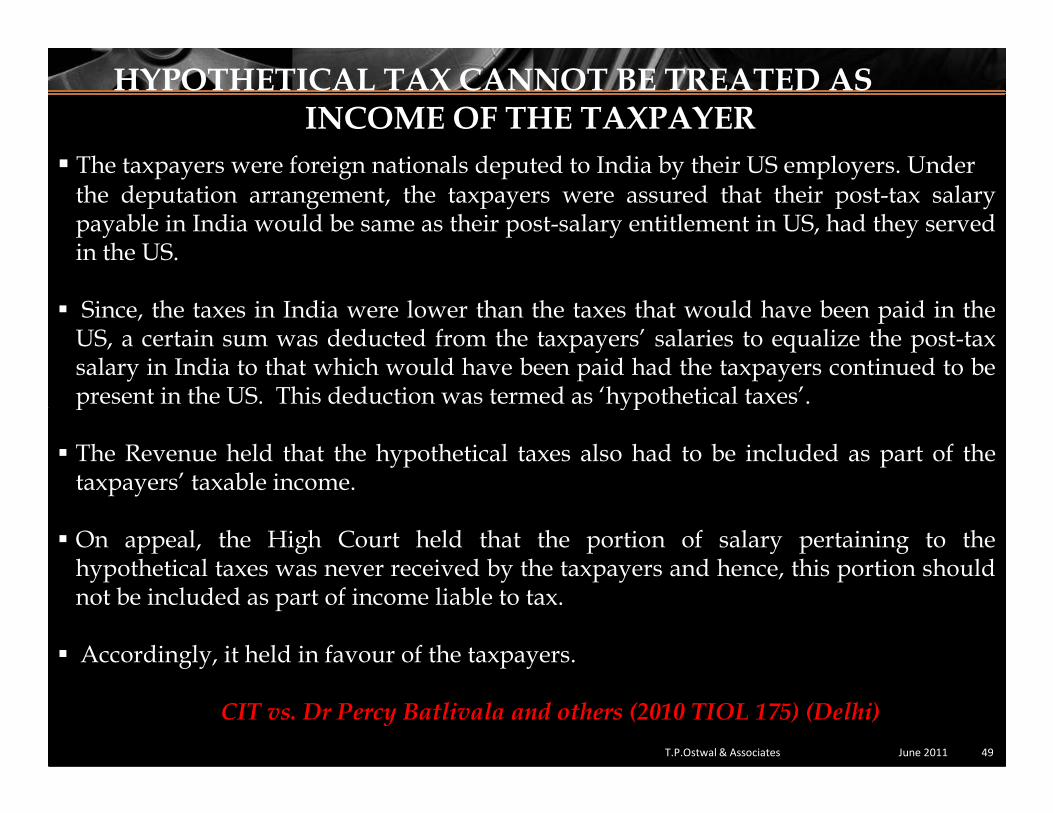

� The taxpayers were foreign nationals deputed to India by their US employers. Underthe deputation arrangement, the taxpayers were assured that their post-tax salarypayable in India would be same as their post-salary entitlement in US, had they servedin the US.

� Since, the taxes in India were lower than the taxes that would have been paid in theUS, a certain sum was deducted from the taxpayers’ salaries to equalize the post-taxsalary in India to that which would have been paid had the taxpayers continued to bepresent in the US. This deduction was termed as ‘hypothetical taxes’.

HYPOTHETICAL TAX CANNOT BE TREATED AS INCOME OF THE TAXPAYER

June 2011 49T.P.Ostwal & Associates

present in the US. This deduction was termed as ‘hypothetical taxes’.

� The Revenue held that the hypothetical taxes also had to be included as part of thetaxpayers’ taxable income.

� On appeal, the High Court held that the portion of salary pertaining to thehypothetical taxes was never received by the taxpayers and hence, this portion shouldnot be included as part of income liable to tax.

� Accordingly, it held in favour of the taxpayers.

CIT vs. Dr Percy Batlivala and others (2010 TIOL 175) (Delhi)

TAXABILITY OF SOCIAL SECURITY CONTRIBUTION OF HOME COUNTRY FOR EXPATRIATE

Mandatory contribution - tax deductible / not taxable

Guiding principles:•Compulsory / mandatory nature•Certain penal implications for default•No vested right conferred on an employee•Overriding title on income from remuneration•No effect on change in employment

Favorable court ruling

June 2011 50T.P.Ostwal & Associates

Favorable court rulingGalloti Raul (1997) 61 ITD 453 (Mum ITAT)

Voluntary contributions� By employer – taxable on accrual

L.W. Russel (1963) 53 ITR 91Dr. Jan Nuyten (1999) 112 Taxmann 238

� By employee – not tax deductible / taxable

TAXABILITY OF OVERSEAS SOCIAL SECURITY CONTRIBUTION

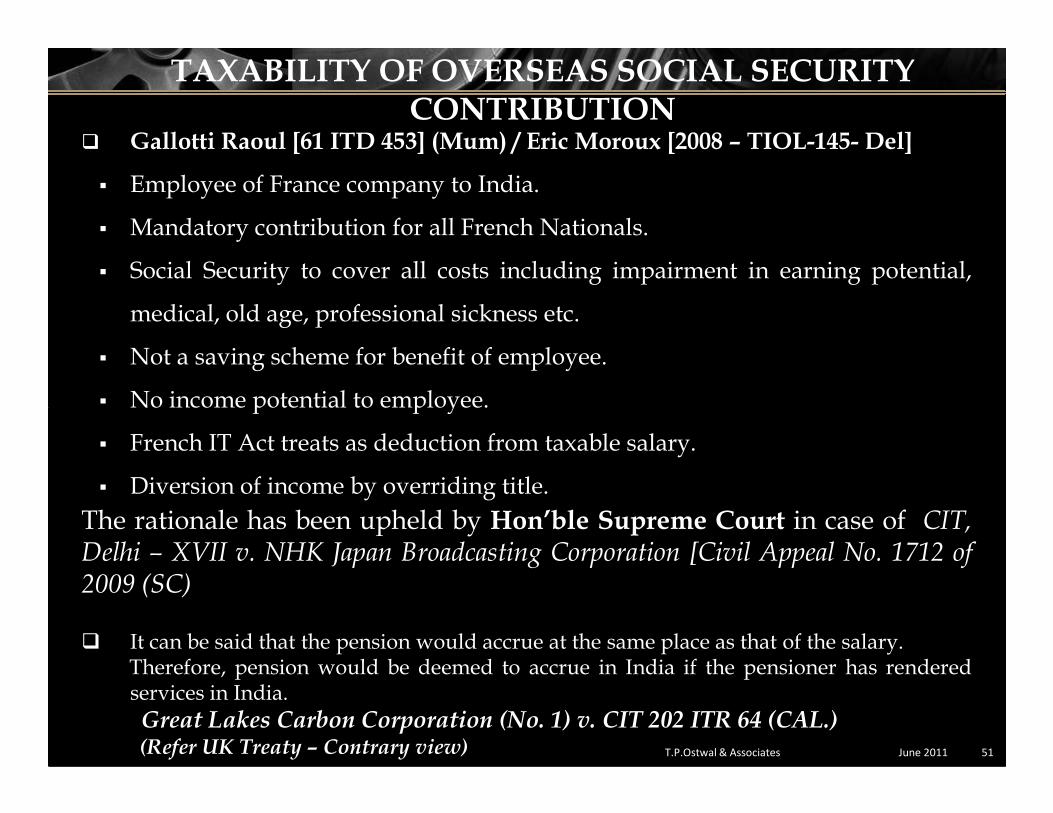

� Gallotti Raoul [61 ITD 453] (Mum) / Eric Moroux [2008 – TIOL-145- Del]

� Employee of France company to India.

� Mandatory contribution for all French Nationals.

� Social Security to cover all costs including impairment in earning potential,

medical, old age, professional sickness etc.

� Not a saving scheme for benefit of employee.

� No income potential to employee.

June 2011 51T.P.Ostwal & Associates

� No income potential to employee.

� French IT Act treats as deduction from taxable salary.

� Diversion of income by overriding title.

The rationale has been upheld by Hon’ble Supreme Court in case of CIT,Delhi – XVII v. NHK Japan Broadcasting Corporation [Civil Appeal No. 1712 of2009 (SC)

� It can be said that the pension would accrue at the same place as that of the salary.Therefore, pension would be deemed to accrue in India if the pensioner has renderedservices in India.

Great Lakes Carbon Corporation (No. 1) v. CIT 202 ITR 64 (CAL.)(Refer UK Treaty – Contrary view)

SUMMARISING JUDICIAL DECISIONS ON SOCIAL SECURITY CONTRIBUTION

� Employer’s contribution towards overseas social security is not

taxable

� ACIT vs Harashima Naoki Tashio, ITA No. 4634/Del

� ACIT vs Eric Matthew Gottesman (2007) 15 SOT 301 (Del)

� ACIT, Circle 47(1) vs Hideki Ishihara in ITA No. 1906/Del/08

� ITO vs Lukas Fole (2009) 124 TTJ (Pune) 965� ITO vs Lukas Fole (2009) 124 TTJ (Pune) 965

� Gallotti Raoul vs ACIT 61 ITD (Bom.) 453

In the above decisions it was held that contribution towards social

security made by the employer in the home country of the foreign

national was held to be not taxable as a perquisite.

June 2011 52T.P.Ostwal & Associates

APPLICABILITY OF INDIAN SOCIAL SECURITY REGIME

�The ministry of labor and Employment have issued a notification extendingthe applicability of the Indian Provident fund and Pension scheme to a newcategory of employees called “International Workers”

� An International Worker (IW) meansa. “an Indian employee” having worked or going to work in a foreign country

with which India has entered into a social security agreement and beingeligible to avail the benefits under a social security programme of thatcountry, by virtue of the eligibility gained or going to gain under the said

June 2011 53T.P.Ostwal & Associates

country, by virtue of the eligibility gained or going to gain under the saidagreement;

a. an employee other than an Indian employee (‘foreign employee”)holdingother than an Indian passport, working for an establishment in India towhich the act applies.

� Every International Worker employed with an establishment in India to whomthe Provident Fund Act applies, would be required to become a member of theProvident Fund, unless he/she qualifies as an “Excluded Employee”

� In relation to the International Worker, the term “Excluded Employee” hasbeen defined to mean an International Worker who is contributing to asocial security programme of his /her country of origin, either as a citizenor as a resident, with which India has entered into a Social SecurityAgreement on reciprocity basis and enjoying the status of detached workerfor the period and terms, as specified in such an agreement.

� A social security agreement is a bi-lateral instrument to protect the interests

APPLICABILITY OF INDIAN SOCIAL SECURITY REGIME

June 2011 54T.P.Ostwal & Associates

� A social security agreement is a bi-lateral instrument to protect the interestsof the workers in the host country. It being a reciprocal arrangementgenerally provides for avoidance of no coverage or double coverage andequality of treatment with the host country workers.

� As of today, Social security agreements have been signed with Belgium,France and Germany. But the date of entry into force is yet to be notified.

International Workers (IW) as defined would be

� Required to contribute 12 percent of salary*

� Matching contribution by employer

� Mandatory for expatriates

� Repatriation of balance possible at end of assignment

* Salary means basic pay, dearness allowance, retaining allowance

APPLICABILITY OF INDIAN SOCIAL SECURITY REGIME

June 2011 55T.P.Ostwal & Associates

* Salary means basic pay, dearness allowance, retaining allowance

Social Security Agreements (SSA)

� An IW is exempt from contributing to Indian PF Scheme, if:

– Contributing to home country social security scheme as a citizen or a

resident

– Is a detached worker for a period specified in the SSA

�In respect of IW, PF rules will apply to an employee irrespective of where thesalary is paid.

� In case of split payroll, the contribution shall be paid on the total salary earned bythe employee.

� Multiple Country Responsibility - In case of employees having responsibilities forother countries in addition to India, contribution is to be made on the “totalsalary”, covering responsibilities outside India also.

APPLICABILITY OF INDIAN SOCIAL SECURITY REGIME

June 2011 56T.P.Ostwal & Associates

�Contribution is payable on the total salary payable even if part of the salary relatesto responsibility outside India.

�There is no minimum period of employment in India required to be eligible formembership.

�Every eligible IW has to be enrolled from the first date of his employment in India.

CONCEPTS – DUAL EMPLOYMENT/ DEPUTATION/ SECONDMENT

June 2011 57T.P.Ostwal & Associates

DEPUTATION/ SECONDMENT

DUAL EMPLOYMENT CONTRACTS

� Meaning:

� An expatriate who has dual / multinational duties signs a separate

contract with the employer for services to be performed at each location

� Advantage:

� Only in case of NR / NOR (physical stay outside India is a must)

� Remuneration of overseas workdays not taxable in India; such servicesshould preferably have no connection with Indian assignment.should preferably have no connection with Indian assignment.

� Documentation:

� Employment contract with the same or two or more entities clearlystating roles and responsibilities

� Split remuneration commensurate with services rendered for each entity

� Time records / working papers to demonstrate work done for respectiveentities

� Physical stay details justifying services rendered outside India

June 2011 58T.P.Ostwal & Associates

SECONDMENT

� Secondment : A secondment is where an employee temporarily changesjob roles within the same company or transfers to another organisation foran agreed period of time. Secondments can be to organisations within theprivate or public sector, or to a non profit making organisation, such as acharity or government body, and usually last between 3 to 24 months.

� During the secondment term, the Receiving party would be considered tobe both the economic and legal employer of the seconded employee. Thereceiving party would normally reimburse all the remuneration payablereceiving party would normally reimburse all the remuneration payableto seconded employees by sending party or pay remuneration to suchemployee so seconded directly.

� In case of Secondment, the seconded employee works under thesupervision, instruction, control and management of receiving party. Theemployee–employer relationship would thus exist in such a casebetween the receiving party and the seconded employee.

June 2011 59T.P.Ostwal & Associates

DEPUTATION

� Deputation : Under a deputation arrangement, there is an agreementbetween the employer and the deputed employee assigning him to renderservices to another company temporarily.

� A deputation agreement provides for a person functioning as a companyemployee to serve under another company temporarily. These agreementscommonly appear in corporate partnerships working abroad on project sites.The agreement provides for the employee's assignment, his duties and theassignment duration, and identifies the entity to whom the employee willreport during the trip.report during the trip.

� Despite the deputation, the employee works under the supervision,instruction, control and management of original employer.

� The employee – employer relationship would thus continue to exist in such acase between the original employer and the deputed employee. Thus underdeputation, the employee continues to be on the pay roll of the originalemployer

June 2011 60T.P.Ostwal & Associates

DEPUTATION/SECONDMENT

Facts

� Parent Co (P Co) enters into a Technical Support Agreement (TSA) withSubsidiary Co (S Co)

� Also seconds its permanent staff as executive directors / senior management(qualified engineers) for routine operations and administration of S Co.

� No secondment agreement executed

� Part salary is paid by P & Co, subsequently reimbursed by S & Co

� Basic / sketchy employment agreement between seconded staff and S CoBasic / sketchy employment agreement between seconded staff and S Co

Issue

� Seconded Employees treated as “technical support services” from parentcompany and thus reimbursement of salary / expenses gets treated as “feesfor technical service” under the TSA, which is subject to withholding tax @10%

� Potential risk of permanent establishment (PE) for parent company sinceemployees posted in India

June 2011 61T.P.Ostwal & Associates

DEPUTATION/SECONDMENT

Recommendations

� Through the secondment agreement, P Co must

� Fully relinquish its key rights (viz. termination, determination of salaryand job responsibilities, renewal of employment , reporting) in favor andbehest of S Co

� Indicate the secondments are not consequent to the TSA between P Co andS Co

�Agree that salary / expenses paid by P Co will be reimbursed on cost to cost�Agree that salary / expenses paid by P Co will be reimbursed on cost to costbasis

� The TSA must specify scope of service / nature of support to be provided toP Co, in a manner that support service are mutually exclusive tosecondment

� Through the employment agreement, S Co must exhibit that it

� Possesses the sole right to fix or agree to specific scope of work, salary,termination criteria, reporting norms for the seconded employees

� Treats the seconded employee at par with other employees

June 2011 62T.P.Ostwal & Associates

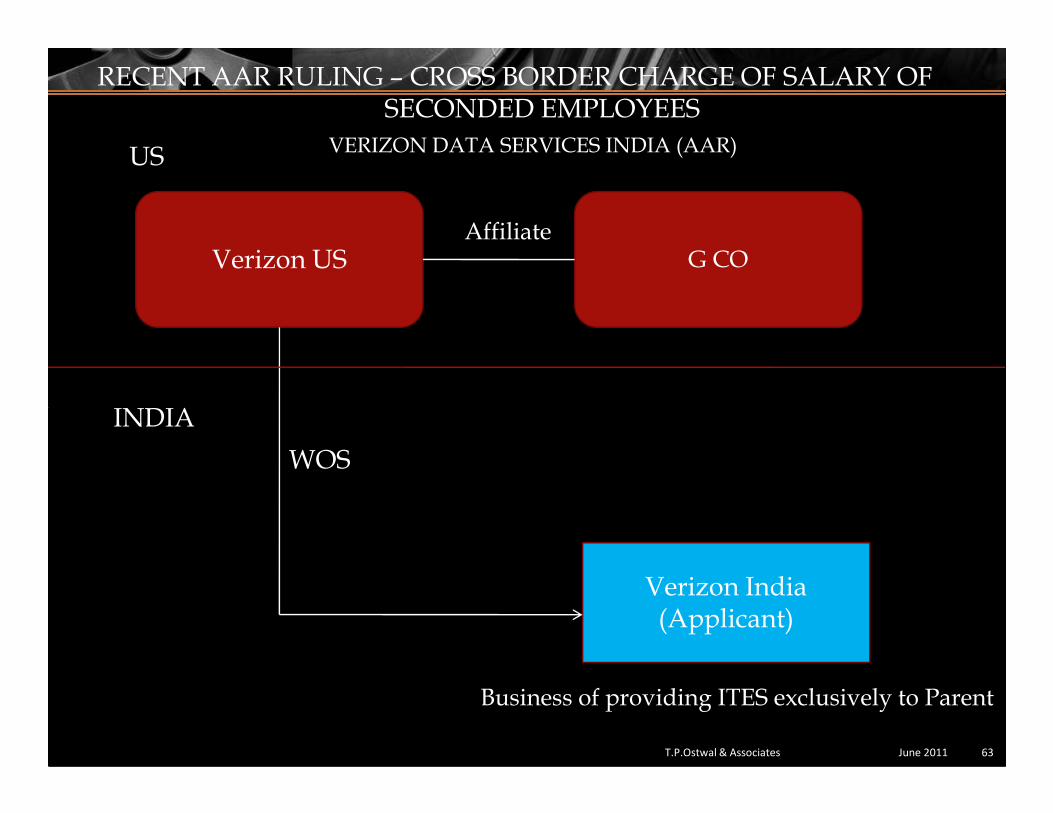

Verizon US G COAffiliate

US

INDIA

RECENT AAR RULING – CROSS BORDER CHARGE OF SALARY OF SECONDED EMPLOYEES

VERIZON DATA SERVICES INDIA (AAR)

June 2011 63T.P.Ostwal & Associates

Verizon India(Applicant)

Business of providing ITES exclusively to Parent

WOS

INDIA

� Issues under consideration� Tax withholding on amounts (representing reimbursements of salary payments and

other benefits paid to seconded employees) by Verizon India to G Co.

�AAR observation and ruling

Employer – Employee relationship

Seconded employees held to be employees of G Co on account of following:

RECENT AAR RULING – CROSS BORDER CHARGE OF SALARY OF SECONDED EMPLOYEES

June 2011 64T.P.Ostwal & Associates

Seconded employees held to be employees of G Co on account of following:

� Agreement provides employees shall remain employees of G Co� Salary paid to seconded employees by G Co� Right of termination with G Co

Fee for included services (FIS)

� Managerial services performed by seconded personnel were employees of G Co� ‘Make available’ criteria’ to be satisfied only in case of technical services and

doesn't apply to managerial or consultancy service

� AAR observation and ruling

� Payments made by Verizon India to G Co held to be FIS under India – US TaxTreaty and FTS under the Act

� Held, tax to be withheld at 20% (on gross basis) on the subject payments

� Impact under the proposed Direct Tax Code

RECENT AAR RULING – CROSS BORDER CHARGE OF SALARY OF SECONDED EMPLOYEES

June 2011 65T.P.Ostwal & Associates

� Impact under the proposed Direct Tax Code

� Emphasis on concept of ‘economic employer’

� ‘Employer’ defined as person who controls individual under express orimplied contract of employment and obliged to compensate him by way ofsalary

�FactsTekmark Global Solutions LLC (“Tekmark?), a tax resident of the USA, deputed its personnel to Lucent Technologies Hindustan Private Limited („Lucent India?)

Deputed personnel remain on the payroll of Tekmark and related costs to be charged to Lucent India.

Such deputed personnel work under the direction, supervision and control of Lucent India

Tekmark is not responsible for the work done / action performed by such deputed

DEPUTATION OF PERSONNEL WOULD RESULT IN SERVICE PE TEKMARK GLOBAL SOLUTIONS LLC

June 2011 66T.P.Ostwal & Associates

Tekmark is not responsible for the work done / action performed by such deputed personnel. Lucent India has a right to send the deputed personnel back to Tekmark if not found suitable.

�Held that: When the services rendered are independent of and not under the control ofTekmark, the deputed persons cannot be considered as constituting permanentestablishment of Tekmark in India.

The actual salary of the deputed personnel reimbursed by the Indian company isonly reimbursement of salary payable by the Indian company, advanced byTekmark.

POINTS TO PONDER

�The AAR, in line with its earlier ruling in the case of AT&S, has reaffirmed itsposition by holding that the Indian entity is required to withhold tax at source atthe time of making reimbursement of salary to its overseas group entity under across border secondment arrangement, since the payment made by the Indianentity would qualify as FTS / FIS under the Act / Treaty.

� It is important to note that the AAR ruling was focused on the fact that overseasentity continued to exercise lien on the seconded employee as it retained theright to terminate the employment of the seconded employees. Based on thiscritical fact, the AAR decided the ruling against the Applicant by holding thatsuch seconded employees continue to be employees of the overseas entity.

June 2011 67T.P.Ostwal & Associates

such seconded employees continue to be employees of the overseas entity.

� Interestingly, it appears that the Tribunal judgments in the case of TekmarkGlobal Solution (Mumbai Tribunal) and IDS Software Solutions (BangaloreTribunal) were not referred to or discussed before the Advance RulingAuthority, wherein similar issue was decided in favour of the taxpayer. TheTribunal in these judgements held that in a situation where seconded employeesare working under the control and supervision of the Indian entity and overseasemployer does not exercises any control, the Indian entity would be treated as‘economic employer’.

TRIANGULAR SITUATION

USCO

Mr. X of Norway

Exploring

business

opportunities

for USCO. � Treaty of relevance: India -Norway treaty.

� Short stay exemption to be calculated based on

India Norway treaty.

India`

FACTORS TO BE ANALYZED WHILE STRUCTURINGDEPUTATION/SECONDMENT

�PE Exposure for the home country

�In case of cross charge of salary costs to Indian Co:�TDS implications on reimbursement of costs

June 2011 69T.P.Ostwal & Associates

�Service tax exposure

�TP Implications in respect of cross charge of costs

VISA REQUIREMENT FOR EXPATRIATES

Foreign nationals can secure visas to enter India in the applicable categorieslisted below:

Foreign Nationals coming to India for employment shall obtain an Employmentvisa from their home country. An employment visa is initially issued for oneyear being subject to fulfillment of certain conditions. The visa can be extendedin India for another year or for the period of employment contract, whichever isearlier. The accommodating family members shall travel on entry visa.

Nature of Visa Purpose

Employment visa Persons intending to take up

June 2011 70T.P.Ostwal & Associates

employment

Business visa Visiting India on Business visits

Tourist visa Visiting India for tourism

Student visa Pursuing studies / academics

Transit visa Persons passing through a country

Journalist visa Media representatives

Conference visa Event organizers or visitors

Entry visa Other purpose not covered elsewhere

RELAXATION OF VISA NORMS FOR ACCOMPANYING SPOUSE OF EXPATRIATE

Present Regulation

Person Type of Visa

Expatriate Employment Visa (‘EV’)

Accompanying Spouse

Entry Visa (“X” visa)

Relaxation by Ministry of Home Affairs

�“X” visa of the spouse of theexpatriate can be convertedinto an “EV”.

�However this can be doneonly with prior approval ofMHA after obtaining a reportfrom FRRO.

June 2011 71T.P.Ostwal & Associates

A spouse who is on “X” visa cannotundertake employment in India. Toundertake employment in such a case,the spouse is required to go back to his/her home country to obtain an “EV”)

from FRRO.

� The applicant must fulfill allthe conditions laid down forthe grant of “EV” as under:-Being a skilled and qualifiedprofessional , and- Drawing a salary of atleastUS$ 25,000 per annum

REGISTRATION REQUIREMENTS

� Generally, all foreign nationals holding a visa (other than a Tourist visa), which

is valid for more than 180 days, must register with the Foreigner’s Regional

Registration Office (FRRO) within 14 days from the date of arrival in India.

However, certain visas specify certain “specific endorsement” for which,

registration formalities are to be processed accordingly. In cities, which do not

have a FRRO office, expatriates must register wit the local police station.

� The documents typically required for FRRO registration are as under:

� Copy of passport including Indian visa page

� Two copies of the letter of representation on the letterhead of the IndianEntity

� Two copies of the letter of sponsorship on the letterhead of the Indian Entity

� Eight Passport size photographs

� Copy of the lease deed of individual’s residential accommodation in Indiaor if residing at a hotel, a letter from the hotel.

June 2011 72T.P.Ostwal & Associates

TAXATION OF EMMIGRANT EXPATRIATES

June 2011 73T.P.Ostwal & Associates

EXPATRIATES

RESIDENTIAL STATUS – OVERSEAS EMPLOYMENT

Indian citizens going for the purpose of employment outside India

� What is “for the purpose of employment outside India”?

The term employment does not mean salaried employment

� Intention of staying abroad on a permanent or semi-permanent basis; not tours

ITO vs. K Y Patel , 33 ITD 714 (ITAT Bombay)

� “employment outside India” refers to “posting” outside India permanently or temporarily

� Merely foreign tours do not imply employment outside India � Merely foreign tours do not imply employment outside India

ITO vs. Abbott Laboratories , 31 ITD 183 (ITAT Bombay)

� Distinction between leaving India for “employment” and “for the purposes of employment”

British Gas India (P) Ltd. , 287 ITR 462 (AAR )

� The place where the contract was entered into, was not important for determining whether employment was outside India.

CIT v. Indo Oceanic Shipping Co Ltd 114 Taxman 722 (Mum)June 2011 74T.P.Ostwal & Associates

� Indian citizen leaving India for employment abroad or as member of

crew of Indian Ship would be treated as resident in that year :

� If no. of days stay in the relevant previous year is 60days & stay in previous 4 years

aggregates to 365 days.

�As per Explanation to section 6(1) (c) 60days would be substituted by 182 days.

For purpose of Explanation (a) to section 6(1)(c), ‘employment’ includes self

RESIDENTIAL STATUS – OVERSEAS EMPLOYMENT

For purpose of Explanation (a) to section 6(1)(c), ‘employment’ includes self

employment like business or profession taken up by assessee abroad

Commissioner of Income-tax v. O. Abdul Razak 198 Taxmann 1

� In the first year, he may be an Indian resident. Foreign salary is taxable in India.

He will get foreign tax credits.

� Different fiscal years may cause rectifications.

June 2011 75T.P.Ostwal & Associates

RESIDENTIAL STATUS – OVERSEAS EMPLOYMENT

�Occasional or casual Visits to India while on deputation abroad excluded

� Day of arrival – excluded; day of departure - included– IBM India seconded employee to IBM US– Secondee in India for 78 days (including a visit from 18 Aug to 6 Sep)– Secondee permanently returned to India on 31 Jan– Secondee spent > 365 days in India during four immediately preceding tax

years– While on secondment, no salary paid in India

June 2011 76T.P.Ostwal & Associates

Tribunal Ruling– 182 days to be substituted for 60 days only in year of departure.– 182 days to be substituted for 60 days only if all entries to India are for visit

purposes.– For computing 60 days, period of stay on visits to India excluded.– Accordingly, Secondee’s stay in India 59 days -Non Resident in India

* Income tax Officer (International Taxation), Bangalore v. Shri Manoj Kumar Reddy 34 SOT 180.

RESIDENTIAL STATUS – OVERSEAS EMPLOYMENT

Employee seconded outside India has left India for the purpose of employment

– ONGC (India) seconded its employee to ONGC NG (a Dutch Company)

– Employee present for 98 days in the year of departure

– During secondment, employee was paid partly in India and partly overseas

– Entire salary cost borne by the Dutch Company

Tribunal Ruling

– Employee left Indian Company to join the Dutch Company which is a separate

June 2011 77T.P.Ostwal & Associates

– Employee left Indian Company to join the Dutch Company which is a separate

entity

– Employee left India for employment outside India

– Hence 60 days to be substituted by 182 days for residency

– Employee is a Non Resident in India.

– Salary paid during the period of secondment not taxable in India.

* Deputy Commissioner of Income tax, Dehradun v. Shri Ashok Kumar (ITA No. 2398/ Del/ 2007)

TAXATION OF PER-DIEM ALLOWANCE

� Sec 2(24)(iiia) of the ITA defines that income includes any special

allowance or benefit, other than perquisite included under sub clause (iii),

specifically granted to the assessee to meet expenses wholly, necessarily

and exclusively for the performance of the duties of an office or

employment of profit.

� Sec 10(14)(i) of ITA provides any such special allowance or benefit, notSec 10(14)(i) of ITA provides any such special allowance or benefit, not

being in the nature of a perquisite within the meaning of clause (2) of

section 17, specifically granted to meet expenses wholly, necessarily and

exclusively incurred in the performance of the duties of an office or

employment of profit as may be prescribed, to the extent to which such

expenses are actually incurred for that purpose shall be exempt from tax.

June 2011 78T.P.Ostwal & Associates

� As per Rule 2BB of Income Tax Rules, the prescribed allowances for Sec

10(14)(i) shall include the following:

any allowance granted to meet the cost of travel on tour or on transfer

(the explanation in the rules provides that any allowance granted to meet

the cost of travel on transfer includes any sum paid in connection with

TAXATION OF PER-DIEM ALLOWANCE

June 2011 79T.P.Ostwal & Associates

transfer, packing and transportation of personal effects on such transfer);

any allowance, whether, granted on tour or for the period of journey in

connection with transfer, to meet the ordinary daily charges incurred by

an employee on account of absence from his normal place of duty.

TAXATION OF PER-DIEM ALLOWANCE

� Thus, on combined reading of the above sections, the outbound employee can

claim exemption if the following conditions are satisfied:

� The allowance must be granted to meet expenses in the performance of

the duties of an office;

� The allowance is granted to the assignee on tour, transfer;� The allowance is granted to the assignee on tour, transfer;

� The allowance is granted to meet the ordinary daily charges;

� The said charges are incurred on account of absence from his normal

place of duty; and

� The exemption is available only to the extent to which the expense is

actually incurred.

June 2011 80T.P.Ostwal & Associates

EMMIGRANTS - SOME ISSUES

� Indian employees sent abroad:

� On payroll of foreign branch or foreign subsidiary,

� On short visits.

� Indian company pays salary in India and abroad in foreign country. Is the Indian salary and foreign salary taxable in India?

� British Gas – 287 ITR 462

� S Mohan – 294 ITR 177.

� TDS by Indian Co.:

� Is it creditable abroad?

� Is it refundable in India?

� Living allowance for visit abroad.

June 2011 81T.P.Ostwal & Associates

FOREIGN TAX CREDIT

� Indian employees earning foreign salary & paying taxes abroad –

Credit for foreign taxes will be available provided that the salary is

taxable in foreign country.

� Foreign tax to be credited against Indian tax on salary only, and not

against tax on any other income.

� Credit can be availed at the time of filing the individual tax return (no� Credit can be availed at the time of filing the individual tax return (no

rules regarding credit at the time of withholding/advance tax

provided).

� It can be availed by submitting the proof of taxes paid in the country

of source (no specific rules prescribed for the same).

June 2011 82T.P.Ostwal & Associates

TDS OBLIGATION UNDER ITA V/S EXEMPTION UNDER DTA.

� The payroll of an outbound employee for rendering services outside

India may not shift outside India and he may continue to receive salary in

India.

� In such cases, the employee may be eligible for relief under the provisions

of paragraph 1 of the Article 15 of the DTA.

� In such cases, if income is chargeable under the head salaries in India, tax� In such cases, if income is chargeable under the head salaries in India, tax

has to be deducted at source while making salary payments.

� By virtue of sub-section (2) of section 90 of the Act, the provisions of the

Act or DTA, whichever are more beneficial to the tax payer, would be

applicable.

� Thus, can the employer consider the relief available to the employee

under the relevant DTA while deducting TDS from salary payments?

June 2011 83T.P.Ostwal & Associates

TDS OBLIGATION UNDER ITA V/S FOREIGN TAX CREDIT

� Outbound employees continue to receive the whole or part of

their salary in India from their Indian employers. The Salary

received in India by such employee is taxable in India.

� Accordingly, certain employers are compelled to deduct tax at

source which may be ultimately refundable since the employee

is eligible for Foreign Tax Credit (‘FTC’) under section 90 or 91is eligible for Foreign Tax Credit (‘FTC’) under section 90 or 91

of the Act.

� Should an employer consider FTC while deducting tax at

source on salary income paid to resident employees who are on

assignment outside India?

June 2011 84T.P.Ostwal & Associates

OTHER GENERAL ISSUES AND DTC PERSPECTIVE

June 2011 85T.P.Ostwal & Associates

PERSPECTIVE

� Section 192 requires a “person responsible for paying” income under thehead “Salaries” to deduct tax at source. Section 204 defines a “personresponsible for paying” such income as the “employer”.

� Thus, Indian employer/ Foreign employer (as the case may be ) is requiredto deduct tax at source u/s. 192.

� In the case of an employee of a Foreign Company who is seconded to its

TAX DEDUCTION AT SOURCE U/S. 192

June 2011 86T.P.Ostwal & Associates

� In the case of an employee of a Foreign Company who is seconded to itsIndian subsidiary such that he gets part of his salary in India and continuesto get the balance in his home country, his full salary becomes taxable inIndia if the short stay exemption is not available even under the relevantDTAA. In such cases, would the Indian Company be liable to TDS on thewhole of the world salary? Or is it that the Foreign Company is liable to taxon the foreign portion and the Indian company on the Indian portion?

� The answer to the above is highlighted in the Honorable Supreme CourtJudgment in case of Eli Lilly & Co (India) Pvt Ltd

OTHER INCOME TAX ISSUES

� The employee will not be liable to tax on his foreign incomes, till he

is a NOR.

� What about his other active income?

Examples:

June 2011 87T.P.Ostwal & Associates

Examples:

- If he trades in shares over a website?

- His retirement account (e.g. 401-K account in USA) where he has

the power to manage the investments? (Advance ruling P-12 – 228

ITR 61)

Is it a source in India (partly or fully)?

� Eli Lilly Inc. Netherlands and Ranbaxy Ltd formed an Indian JV Co. Eli Lilly & Co. India PvtLtd. 4 Employees seconded to JV Co. Employees continued to be on rolls of Foreign Co. ReceivedHome Salary outside India in Foreign Currency from Foreign Company. Salary paid to expats inIndia, JV withheld the tax u/s 192(1). No tax withheld in respect of home salary paid by ForeignCo. outside India.

� Whether Indian JV Co. needs to withhold tax on Home Salary/ Special Allowance paymentsmade by Foreign Co. outside India in foreign currency?

� The salary paid by the foreign company was for services in India the same was deemed to accrue

CIT vs. ELI LILLY & CO (INDIA) PVT LTD & ORS.(2009) 223 CTR (SC) 20

June 2011 88T.P.Ostwal & Associates

� The salary paid by the foreign company was for services in India the same was deemed to accruein India u/s 9 (1) (ii) and the assessee ought to have deducted tax u/s 192 though it was not thepayer;

� Though the payment of salary to the expatriate was made by the foreign company outside India,the withholding provisions did apply as the Act had extra-territorial operation as there was anexus between the said salary and the rendering of services in India.

� Income under the head salaries u/s 9(1)(ii) extends to any salary income earned by theexpatriate employee , whether in India or outside India as long as nexus could be establishedthat the income is earned in respect of the service provided by expatriate employee in India.

� The taxpayer, a French company, entered into a contract for providing drilling

services to ONGC, an Indian company. For providing the services, it engaged the servicesof its non resident associated enterprise (“AE”). The AE deputed certain personnel(“expatriates”) to provide the technical services. As per the agreement with the AE, theexpatriates would continue to remain as employees of the AE.

� The taxpayer did not have any control over the engagement or dismissal of the

expatriates.

FOREIGN COMPANY TREATED AS AN AGENT OF THEEXPATRIATE U/S 163

June 2011 89T.P.Ostwal & Associates

� The Revenue treated the taxpayer as an agent of the expatriates under section 163 of the Actand proceeded to assess the salary income of the expatriates in the hands of the taxpayer, inthe capacity of an agent.

� On appeal, the Tribunal held that there was no nexus between the taxpayer and the incomeearned by the expatriates. It observed that technical assistance fees charged by the AE,which in turn paid the remuneration to the expatriates, could not be treated as an indirectpayment of remuneration by the taxpayer. It held that performance of services by theexpatriates of the AE at the rigs, owned by the taxpayer, would not result in a businessconnection between the taxpayer and the expatriates. Accordingly, the Tribunal held thatthe taxpayer could not be treated as an agent of the expatriates under section 163 of the Act.

Pride Foramer SAS Vs. ACIT (2010 TIOL 110) (Delhi)

OTHER INCOME TAX ISSUES - PAN, RETURN FILING, NOC

� PAN:

� All Inbound employees are required to obtain a PAN by making anapplication to the tax authorities.

� RETURN FILING:

� All Inbound employees must file their tax returns in the prescribed form onor before 31 July. The income tax payable as per the tax return must becomputed and paid before the return is filed.

� NOC:

� Every person, who is not domiciled in India and who has come to India inconnection with business, profession or employment, is required to obtaina No Objection Certificate from the tax authorities before departing fromIndia.

� For this purpose, employees will have to furnish an undertaking obtainedfrom the employer to the effect that the tax payable by such person shall bepaid by the employer.

June 2011 90T.P.Ostwal & Associates

WEALTH TAX & PROFESSION TAX

� Wealth Tax:

� Assets, as defined u/s 2(ea) of Wealth Tax Act, 1957, outside

India are taxable in case of an ordinary resident.

� Sec 6(i) – Assets outside India of foreign citizen and NOR,

are exempt from wealth-tax.

� Profession Tax:

� Profession tax is payable according to the laws of the state in

which the employment is exercised. The same is allowable as

a taxable deduction from salary in the year of payment.

June 2011 91T.P.Ostwal & Associates

DIRECT TAX CODE – EXPATRIATE TAX PERSPECTIVE

Slab Rates

�Beneficial tax slabs proposed to reduce tax burden

�Peek rate of 30 per cent applicable on income exceeding INR 25 lakhs

Residency

�Concept of “Not Ordinarily Resident” abolished

June 2011 92T.P.Ostwal & Associates

�Further, in case of Indian citizens or persons of Indian origin, residingoverseas and visiting India, it is proposed to withdraw the beneficialtreatment that they become residents only when their stay in Indiaexceeds 181 days during the relevant financial year. These individualswill become resident of India if their stay in India exceeds 59 daysduring the relevant financial year and 364 days in the past 4 financialyears. Such individuals will have the risk of attracting global taxation inIndia sooner than later where they have been visiting India frequentlyand spending significant time in India in each financial year.

THANK YOU

June 201193T.P.Ostwal & Associates

T.P. Ostwal & Associates4th floor, Bharat House,

104 Mumbai Samachar Marg, fort, MUMBAI-400001.Tel No.: +91-22-40693900Fax No.: +91-22-40693999Mobile:+919004660107Email: [email protected]

![TAXATION OF EXPATRIATES - B.D Jokhakar & Co. · Taxation of Expatriates TABLE OF CONTENTS Sr. No. Topic Page number ... (10CC)] Expatriates coming into India and working in various](https://img.pdfslide.us/doc/110x75/5b3ffd287f8b9aff118cca0c/taxation-of-expatriates-bd-jokhakar-co-taxation-of-expatriates-table-of.jpg)

![2008 China, Yunnan [Shanghai Expatriates]](https://img.pdfslide.us/doc/110x75/54c6509a4a79591a6d8b4621/2008-china-yunnan-shanghai-expatriates.jpg)