Embed Size (px)

Citation preview

Taxation Implications

of IFRSBy Taiwo Oyedele FCA, FCCA, FCTI, CISA

Partner, PwC

2011 MCPE

Position for graphic or image

The Institute of Chartered Accountants of Nigeria

Position for graphic or image

Objectives

At the end of this session, participants should be able to:

• Explain the principles of IFRS

• Identify the tax implications of IFRS

Taxation implications of IFRS

• Manage the impact of IFRS on their organisations

2

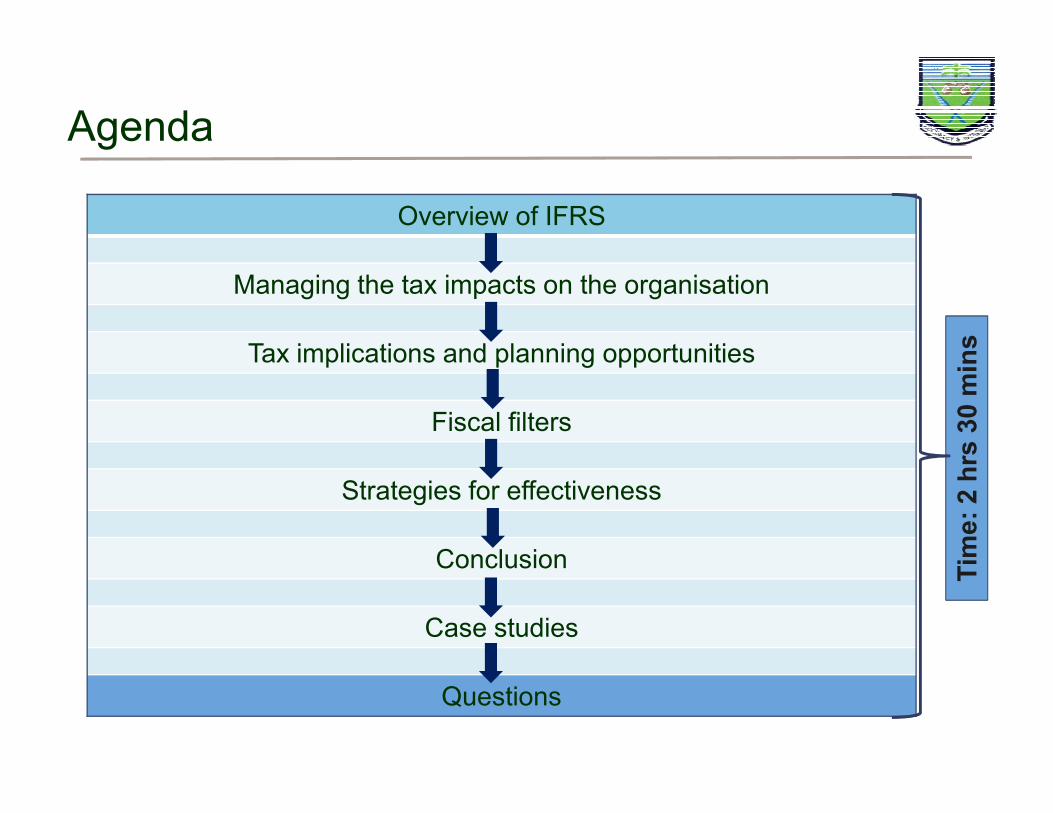

Agenda

Overview of IFRS

Managing the tax impacts on the organisation

Tax implications and planning opportunities

Fiscal filters

Time: 2 hrs 30 mins

Fiscal filters

Strategies for effectiveness

Conclusion

Case studies

Questions

Time: 2 hrs 30

Overview of IFRS

• IFRSs have been developed primarily to meet the information needs of

shareholders, lenders and other investors. These needs do not always align

with those of the tax authorities (e.g. extensive use of fair value and the

application of substance over form).

• Taxable profit of any specific period may differ between two standards,

however, the cumulative earnings of an entity over time will tend to be the

Taxation implications of IFRS

however, the cumulative earnings of an entity over time will tend to be the

same as the individual transactions are cashed.

• From taxation point of view, however, there are additional variables that

may influence tax position such as impairment and treatment of tax losses

etc.

4

Overview of IFRS

• IFRS stands for International Financial Reporting Standards issued by the

International Accounting Standards Board (IASB).

• Body was previously known as International Accounting Standards

Committee issuing International Accounting Standards (IAS).

• Essentially, IFRS comprises of four types of documents:

Taxation implications of IFRS

- International Accounting Standards (IASs);

- International Financial Reporting Standards (IFRSs);

- Interpretations of the International Financial Reporting Interpretations

Committee (IFRICs) formerly the Standing Interpretations Committee

(SICs); and

- IASB Framework for the Preparation and Presentation of Financial

Statements

5

Overview of IFRS

By comparison, Nigerian GAAP is made up of the following:

• The Companies and Allied Matters Act (CAMA) LFN 2004

• Statements of Accounting Standards (SAS) issued by the Nigerian

Accounting Standards Board (NASB)

Taxation implications of IFRS

Accounting Standards Board (NASB)

• Other local legislation and industry specific Guidelines such as BOFIA,

Prudential Guidelines, Insurance Act and SEC Rules

• International best practice (optional)

6

Overview of IFRS – gaining ground worldwide

Taxation implications of IFRS

7

Require or permit IFRS Converging/converting to adopt IFRS Pursing convergence but no plan to adopt yet

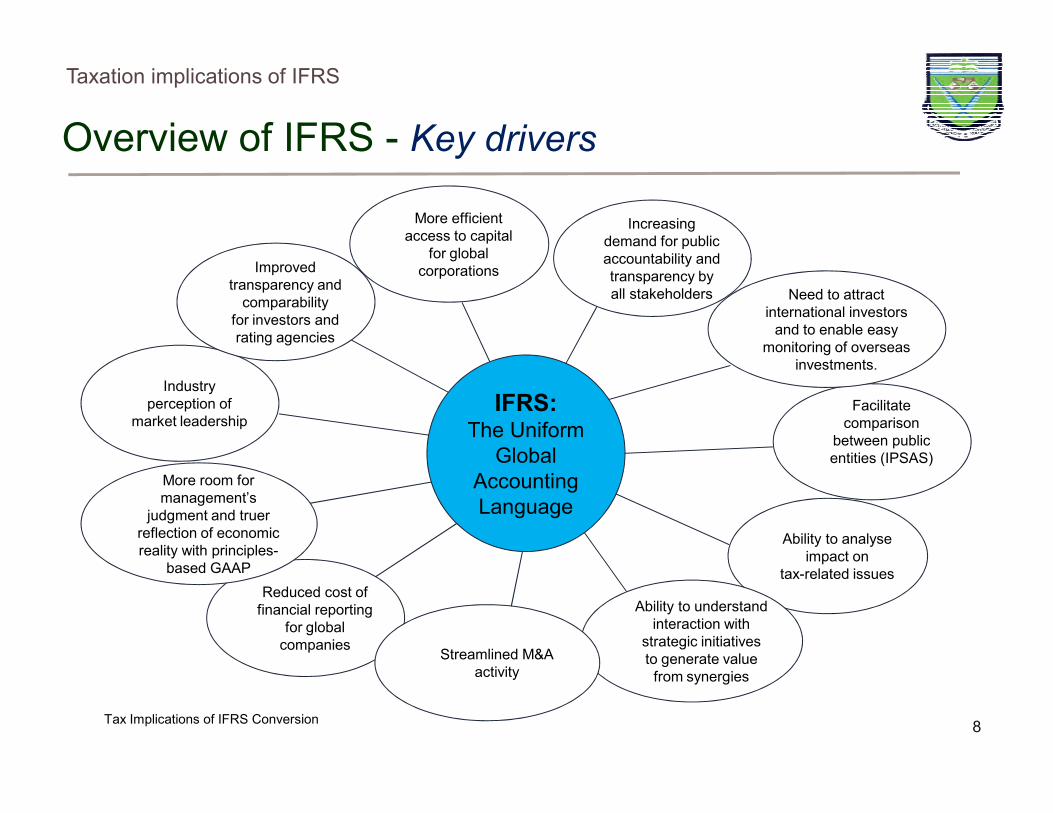

Overview of IFRS - Key drivers

Taxation implications of IFRS

IFRS:

Increasing

demand for public

accountability and

transparency by

all stakeholders

Facilitate

Industry

perception of

Improved

transparency and

comparability

for investors and

rating agencies

More efficient

access to capital

for global

corporations

Need to attract

international investors

and to enable easy

monitoring of overseas

investments.

8Tax Implications of IFRS Conversion

IFRS:The Uniform

Global

Accounting

Language

Reduced cost of

financial reporting

for global

companies

Facilitate

comparison

between public

entities (IPSAS)

More room for

management’s

judgment and truer

reflection of economic

reality with principles-

based GAAP

perception of

market leadership

Ability to analyse

impact on

tax-related issues

Ability to understand

interaction with

strategic initiatives

to generate value

from synergies

Streamlined M&A

activity

Overview of IFRS

Taxation implications of IFRS

9

Overview of IFRS – conversion roadmap

Listed & significant public entities (SPEs)

• Entities with listed securities (domestic and foreign stock exchanges)

• Government business entities e.g. NNPC

• Unquoted entities required by law to file returns with regulatory authorities

Taxation implications of IFRS

• Unquoted entities required by law to file returns with regulatory authorities

(excluding returns with CAC & tax authorities) e.g. private banks and

insurance companies

10

Transition Date:2010

Reporting Date:2012

Overview of IFRS – conversion roadmap

Other public interest entities (Other PIEs)

• Unquoted or private entities which are of significant public interest because

of their nature of business, size, number of employees or their corporate

status which require wide range of stakeholders.

• Examples are large not for profit entities such as charities and pension

Taxation implications of IFRS

• Examples are large not for profit entities such as charities and pension

funds and may include publicly owned entities and other entities where

there is a potentially significant effect on financial stability.

11

Transition Date:2011

Reporting Date:2013

Overview of IFRS – conversion roadmap

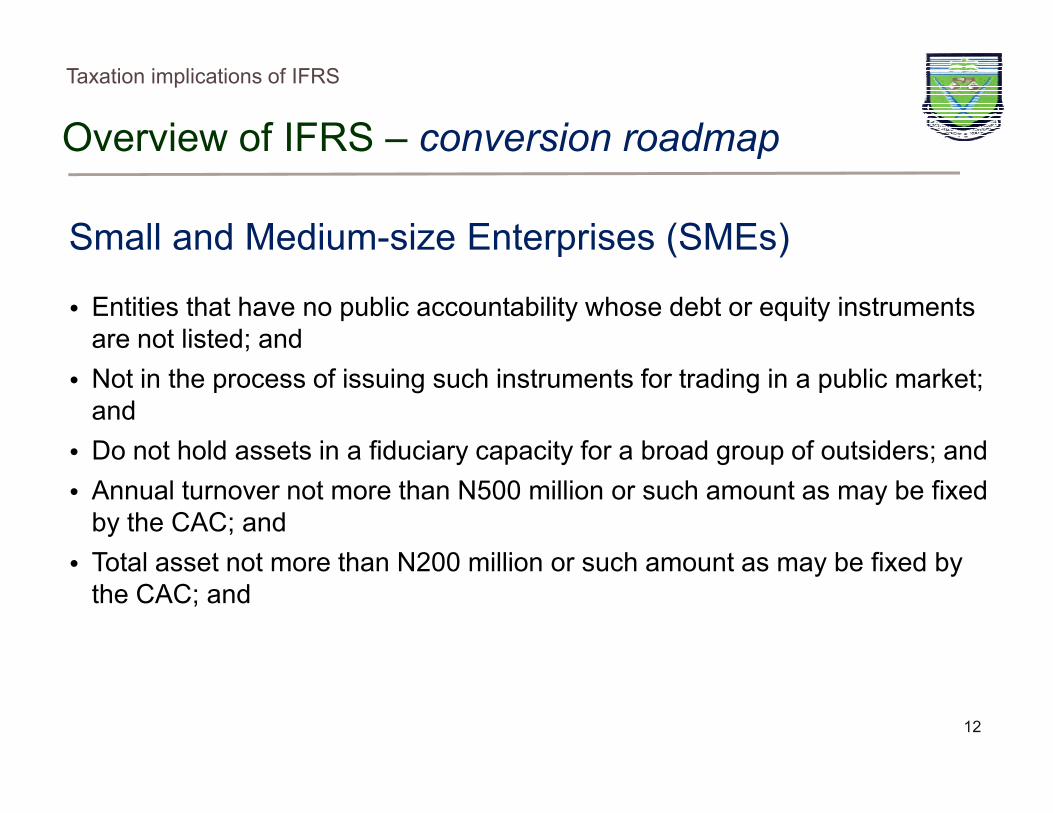

Small and Medium-size Enterprises (SMEs)

• Entities that have no public accountability whose debt or equity instruments

are not listed; and

• Not in the process of issuing such instruments for trading in a public market;

and

Taxation implications of IFRS

and

• Do not hold assets in a fiduciary capacity for a broad group of outsiders; and

• Annual turnover not more than N500 million or such amount as may be fixed

by the CAC; and

• Total asset not more than N200 million or such amount as may be fixed by

the CAC; and

12

Overview of IFRS – conversion roadmap

Small and Medium-size Enterprises (SMEs)

• No Board member is a foreigner; and

• No member is a government or a government corporation or agency or its

nominee, and

Taxation implications of IFRS

nominee, and

• The directors among them hold not less than 51 percent of its equity

share capital.

13

Transition Date:2012

Reporting Date:2014

Overview of IFRS – conversion roadmap

Transition date – To Dos

• Awareness

• Planning (people, systems & process)

Taxation implications of IFRS

• Training

• Assessment & impact analysis

• Transition adjustments (Recognise, De-

recognise, Reclassify & Re-measure)

14

Overview of IFRS – conversion roadmap

Reporting date – To Dos

• Interim reporting based on IFRS (Listed entities and SPEs)

• Statutory audit

• File IFRS returns (CAC, FIRS, SEC, CBN, NAICOM etc)

Taxation implications of IFRS

• File IFRS returns (CAC, FIRS, SEC, CBN, NAICOM etc)

• Investors communication

• Compliance monitoring

• Training

15

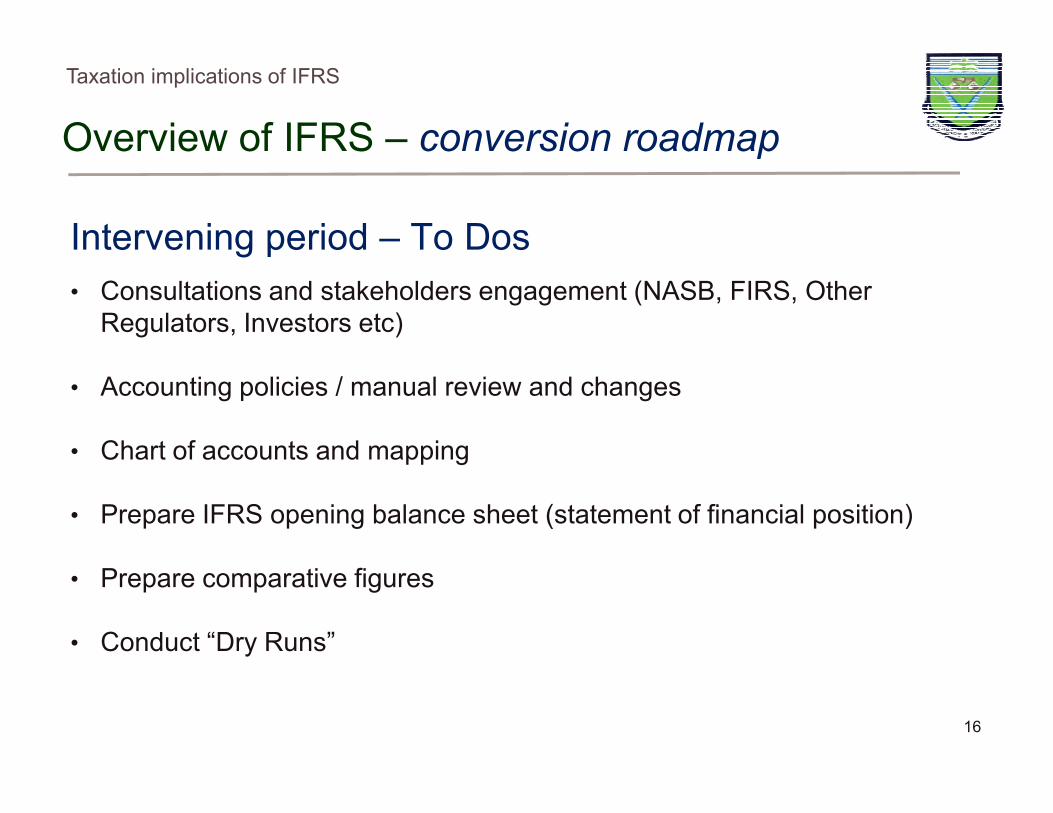

Overview of IFRS – conversion roadmap

Intervening period – To Dos

• Consultations and stakeholders engagement (NASB, FIRS, Other

Regulators, Investors etc)

• Accounting policies / manual review and changes

Taxation implications of IFRS

• Chart of accounts and mapping

• Prepare IFRS opening balance sheet (statement of financial position)

• Prepare comparative figures

• Conduct “Dry Runs”

16

Overview of IFRS – conversion roadmap

Intervening period – To Dos

• Legislative changes

• Communicate transition to

stakeholders

Taxation implications of IFRS

stakeholders

• Present a reconciliation of

shareholders’ equity and net income

between N-GAAP and IFRS

• Training

17

Overview of IFRS – conversion roadmap

Post Conversion – To Dos

• Monitor changes in IFRS and market practice

• Sustain benefits from the transition process

Taxation implications of IFRS

• Supervision, monitoring and enforcement of IFRS implementation

• Capacity building and support – establish experts units at the NASB,

CBN, NDIC and NAICOM to tackle new or revised standards

18

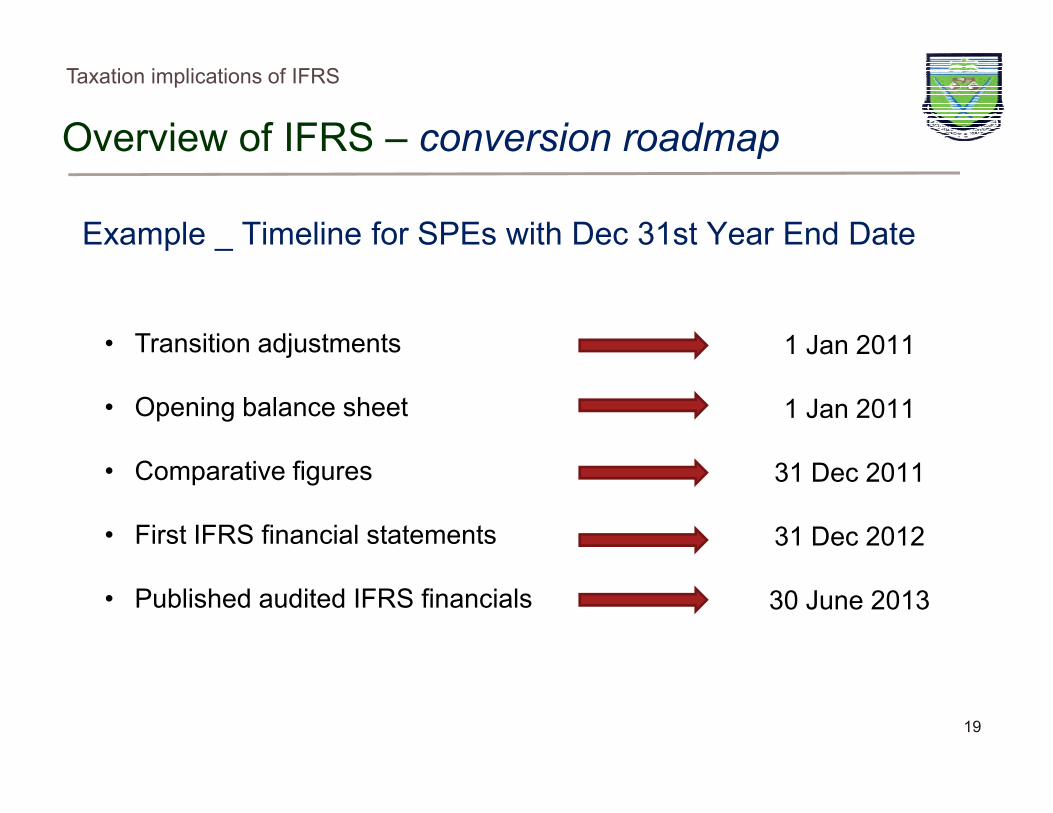

Overview of IFRS – conversion roadmap

Example _ Timeline for SPEs with Dec 31st Year End Date

Taxation implications of IFRS

• Transition adjustments

• Opening balance sheet

1 Jan 2011

1 Jan 2011

19

• Opening balance sheet

• Comparative figures

• First IFRS financial statements

• Published audited IFRS financials

1 Jan 2011

31 Dec 2011

31 Dec 2012

30 June 2013

Managing the tax impacts on the organisation

Practical Issues

• First time adoption (IFRS 1) – minimum requirements, exceptions,

mandatory and optional exemptions

• Group entities (parent vs subsidiaries in different categories)

Taxation implications of IFRS

• Changes in legislation (CAMA, ISA, BOFIA, CITA etc)

• Transition guidelines

• Knowledge gap (professionals, regulators & preparers)

• Early adoption issues

• Tight conversion deadline and implications of non-compliance

20

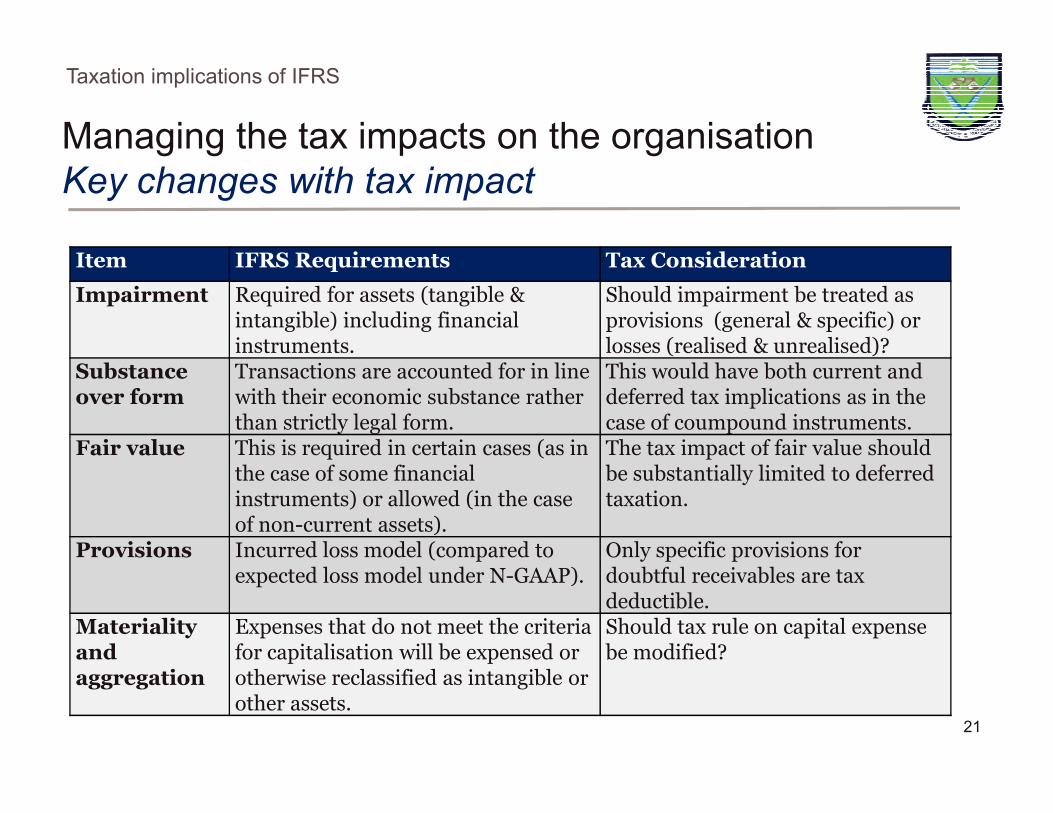

Managing the tax impacts on the organisation

Key changes with tax impact

Taxation implications of IFRS

Item IFRS Requirements Tax Consideration

Impairment Required for assets (tangible & intangible) including financial instruments.

Should impairment be treated as provisions (general & specific) or losses (realised & unrealised)?

Substanceover form

Transactions are accounted for in line with their economic substance rather

This would have both current and deferred tax implications as in the

21

over form with their economic substance rather than strictly legal form.

deferred tax implications as in the case of coumpound instruments.

Fair value This is required in certain cases (as in the case of some financial instruments) or allowed (in the case of non-current assets).

The tax impact of fair value should be substantially limited to deferred taxation.

Provisions Incurred loss model (compared to expected loss model under N-GAAP).

Only specific provisions for doubtful receivables are tax deductible.

Materialityandaggregation

Expenses that do not meet the criteriafor capitalisation will be expensed or otherwise reclassified as intangible or other assets.

Should tax rule on capital expense be modified?

Managing the tax impacts on the organisationKey changes with tax impact

Taxation implications of IFRS

• Companies may have to

include qualitative impact

analysis of IFRS

implementation in their 2010

financial statements

1.1.11 31.12.11

Shareholders’ equity in accordance with NGAAP

Impairment of assets

Fair value adjustments

22

financial statements

• Present in the 2011 accounts

a reconciliation between

current GAAP and IFRS:

o Shareholders’ equity as of

1.Jan.2011 & 31.Dec.2011

o Net income at 31.Dec.2011

Fair value adjustments

Intangible assets

Non current assets

Revenue recognition

Consolidation

Deferred taxes

(...)

Shareholders’ equity in accordance with IFRS

Impact of IFRS adoption

Managing the tax impacts on the organisationWhat do we have to do differently?

Taxation implications of IFRS

• Government to amend relevant reporting legislation, regulations and

tax rules

• Keep separate tax books / maintain parallel books of accounts?

• Record keeping, chart of accounts and mapping

23

• Record keeping, chart of accounts and mapping

• Preparation and presentation of financial statements

• Measurement bases for assets and liabilities

• Revenue recognition

• Disclosure requirements, nomenclature and format

• Impact on audit of tax and tax compliance

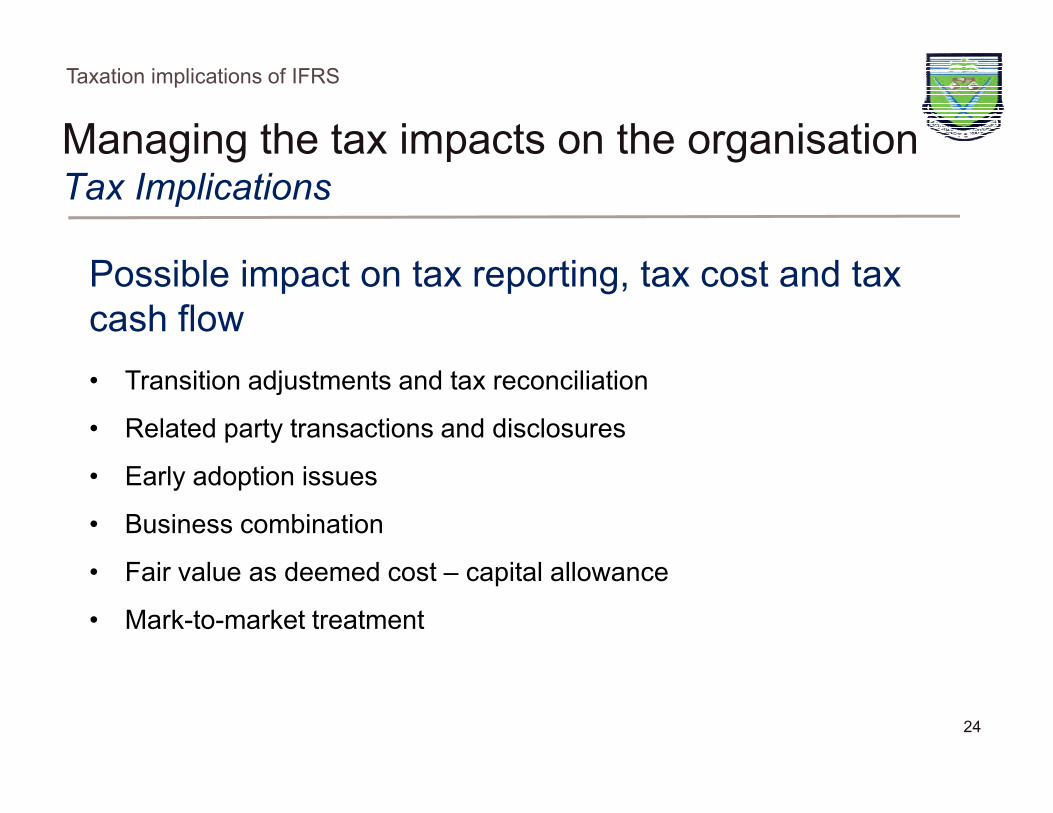

Managing the tax impacts on the organisationTax Implications

Taxation implications of IFRS

Possible impact on tax reporting, tax cost and tax

cash flow

• Transition adjustments and tax reconciliation

24

• Related party transactions and disclosures

• Early adoption issues

• Business combination

• Fair value as deemed cost – capital allowance

• Mark-to-market treatment

Managing the tax impacts on the organisationTax Implications

Taxation implications of IFRS

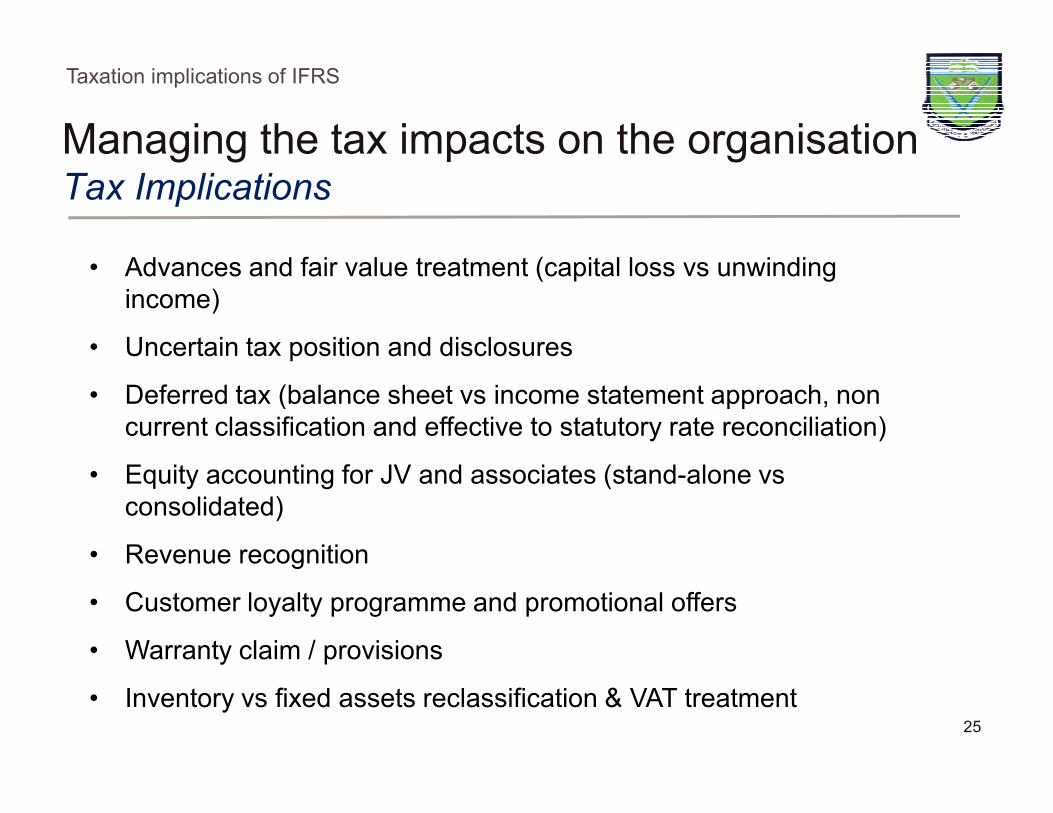

• Advances and fair value treatment (capital loss vs unwinding

income)

• Uncertain tax position and disclosures

• Deferred tax (balance sheet vs income statement approach, non

25

• Deferred tax (balance sheet vs income statement approach, non

current classification and effective to statutory rate reconciliation)

• Equity accounting for JV and associates (stand-alone vs

consolidated)

• Revenue recognition

• Customer loyalty programme and promotional offers

• Warranty claim / provisions

• Inventory vs fixed assets reclassification & VAT treatment

Managing the tax impacts on the organisationTax Implications

Taxation implications of IFRS

• Leases (finance vs operating) – different tax treatment

• Substance over form (equity vs liability classification e.g. preference

shares)

• Uncertain tax positions & disclosure requirements

26

• Uncertain tax positions & disclosure requirements

• Depreciation of intangible assets

• Componentisation of assets

• Functional and reporting currency vs tax returns currency

• Segment reporting vs tax filing and other income taxation

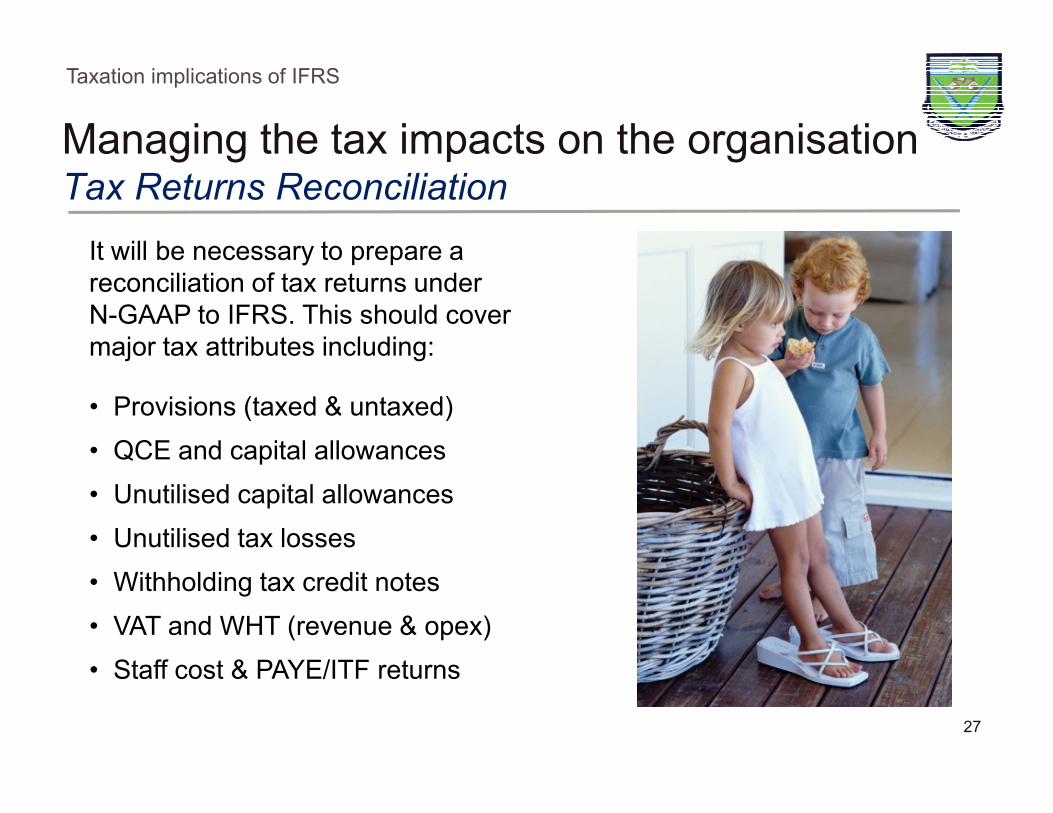

Managing the tax impacts on the organisationTax Returns Reconciliation

Taxation implications of IFRS

It will be necessary to prepare a

reconciliation of tax returns under

N-GAAP to IFRS. This should cover

major tax attributes including:

• Provisions (taxed & untaxed)

27

• Provisions (taxed & untaxed)

• QCE and capital allowances

• Unutilised capital allowances

• Unutilised tax losses

• Withholding tax credit notes

• VAT and WHT (revenue & opex)

• Staff cost & PAYE/ITF returns

Tax Planning Opportunities

Taxation implications of IFRS

• Review of tax reporting systems and processes

• Embedding chart of accounts into Extensible Business Reporting

Language (XBRL) for tax analysis

• Cash advances and staff loan – possible classification of write off as

employees benefit (subject to PAYE implications)

28

employees benefit (subject to PAYE implications)

• Re-appraising the tax cycle and tax management framework (tax

planning, provisions, resourcing, compliance, reporting and tax

dispute resolution etc)

• Provisions and impairments to be treated as specific as much as

possible

• Ensure proper record keeping and explanation to support tax

treatment in the event of a tax enquiry

Fiscal Filter

Taxation implications of IFRS

Tax limitations of IFRS transition can be surpassed by the introduction

of “fiscal filters" to cushion the tax burden. Thus, the taxable income will

consider the IFRS accounting profit, adjusted to reflect the

requirements of tax legislation. This model:

- Introduces a high level of flexibility in fiscal reporting;

29

- Introduces a high level of flexibility in fiscal reporting;

- Avoids the need for a double accounting system;

- Eliminates almost all effects on tax revenues from IFRS adoption

“Fiscal filters" should have two primary functions: the preservation of

tax base (e.g. capital gains roll over, losses and revaluation reserves)

and the minimisation of effects from the transition adjustments.

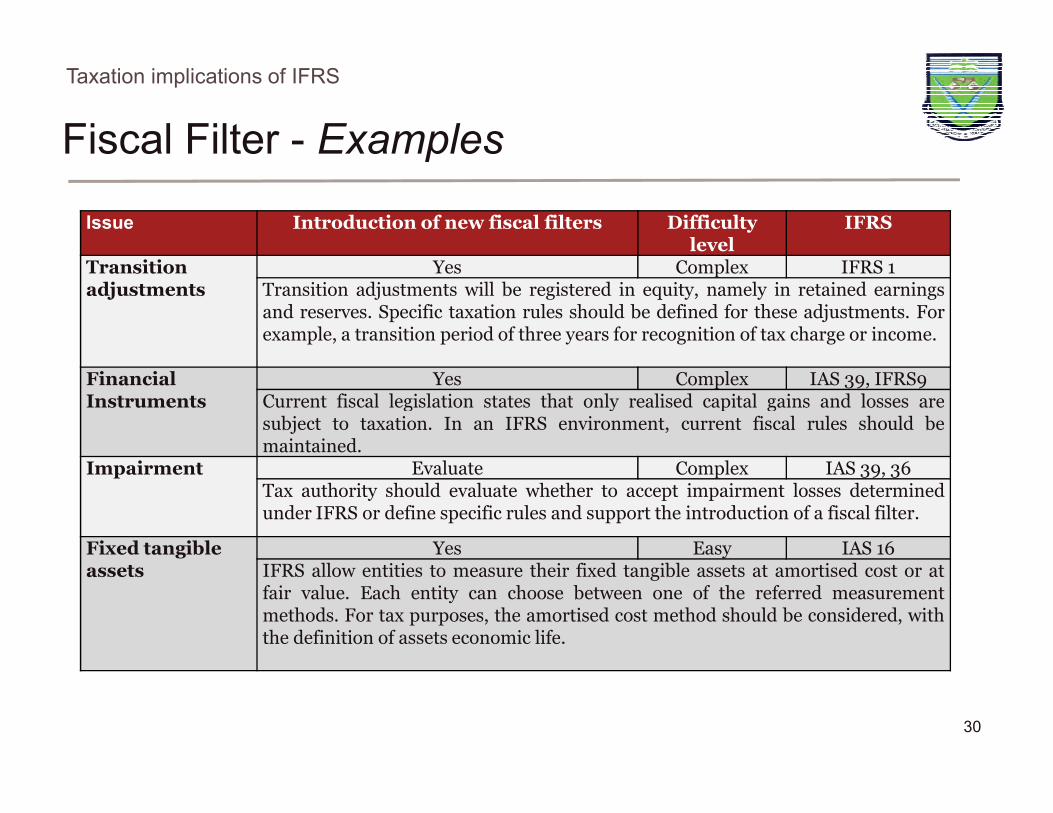

Fiscal Filter - Examples

Taxation implications of IFRS

Issue Introduction of new fiscal filters Difficulty level

IFRS

Transitionadjustments

Yes Complex IFRS 1Transition adjustments will be registered in equity, namely in retained earningsand reserves. Specific taxation rules should be defined for these adjustments. Forexample, a transition period of three years for recognition of tax charge or income.

FinancialInstruments

Yes Complex IAS 39, IFRS9Current fiscal legislation states that only realised capital gains and losses are

30

Instruments Current fiscal legislation states that only realised capital gains and losses aresubject to taxation. In an IFRS environment, current fiscal rules should bemaintained.

Impairment Evaluate Complex IAS 39, 36Tax authority should evaluate whether to accept impairment losses determinedunder IFRS or define specific rules and support the introduction of a fiscal filter.

Fixed tangible assets

Yes Easy IAS 16IFRS allow entities to measure their fixed tangible assets at amortised cost or atfair value. Each entity can choose between one of the referred measurementmethods. For tax purposes, the amortised cost method should be considered, withthe definition of assets economic life.

Strategies for effectiveness

Taxation implications of IFRS

• Be proactive. Carry out a detailed plan, develop a budget, set KPIs and

develop a conversion strategy which should be agreed and properly

documented

• Consider using a project team with a clear timetable of action points

attached to individuals with appropriate authority to ensure accountability

• Set clear milestones and request regular progress reports

31

• Set clear milestones and request regular progress reports

• Appoint a senior personnel (possibly the CFO / Finance Director) to carry

out the oversight function and project monitoring

• Involve external professionals to leverage best practice

• For multinationals, consider exchange programme or secondment for key

staff to countries already reporting under IFRS

• Report regularly to stakeholders (board, shareholders, regulators etc)

• Use the conversion opportunity to reassess tax, accounting and reporting

processes and consider how to optimise value and other benefits

Conclusion

• IFRS is driving the revolutionary world of accounting with over 100

countries worldwide either requiring or permitting its use.

• There is no doubt that conversion to IFRS is a huge task and a big

challenge.

Its revolutionary impact requires a great deal of decisiveness and

Taxation implications of IFRS

• Its revolutionary impact requires a great deal of decisiveness and

commitment.

• It is a new world order in corporate reporting that will alter not only the

financial accounting and reporting landscape in Nigeria but also tax

accounting, tax cash flow and tax distributable reserves.

32

Conclusion

Taxation implications of IFRS

• Given the interrelationship between accounting measurements and

taxation, as part of the conversion process, companies need to

consider the possible impact of the changes on their tax accounting

methods, and possible impacts on taxable profits, tax assets and

liabilities and tax distributable reserves.

• For instance, extensive use of fair value under IFRS may give rise to

33

• For instance, extensive use of fair value under IFRS may give rise to

differences in recognised income and carrying values of assets and

liabilities and a resulting difference in current and deferred tax liability

or asset.

• Consider impact on communication with external stakeholders

including the tax authorities.

• Considering these factors, a successful conversion requires not only

the commitment of the finance team, but also demands full involvement

of the tax team.

Conclusion

Taxation implications of IFRS

“In a time of drastic change it is the learners who inherit the future. The learned usually find

themselves equipped to live in a world that no longer exists.

34

Eric Hoffer, U.S. philosopher.

Thank youThe views and opinions expressed in this presentation are those of the author and do not in any way represent the views of the author’s employer or the

Institute of Chartered Accountants of Nigeria. You should not act upon the information contained in this publication without obtaining specific professional

advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication. The

author does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance

on the information contained in this publication or for any decision based on it.

Financial Reporting Nigeria Limited (FRNL ) is a wholly owned subsidiary of Financial Reporting Incorporated (FRI) based in

England and Wales.

FRNL is involved in assisting entities with corporate reporting and financial advisory. The company has been operating in Nigeria

for many years. As a company incorporated in Nigeria, RPNL prepares its accounts under Nigerian GAAP, essentially SAS, for

statutory reporting purposes including filing of returns with regulatory authorities (the Corporate Affairs Commission and the

Federal Inland Revenue Service).

However, the Consolidated Financial Statements of the parent entity FRI and its subsidiaries are prepared in accordance with

International Financial Reporting Standards (IFRS).

Case Study

Taxation implications of IFRS

Given that the FRI group does not report under Nigerian GAAP, FRNL has to prepare its financial information in line with IFRS as

a “voluntary preparer” for group reporting purposes.

However, the Federal Government of Nigeria in a bid to improve transparency of financial reporting has announced a mandatory

conversion to IFRS with different conversion dates for different categories of entities between 2012 and 2014.

Questions

1. Discuss the categories of reporting entities for conversion purposes as contained in the IFRS conversion roadmap

issued by the Federal Government of Nigeria.

2. In your opinion, which category does FRNL fall into and why?

3. Based on your response to (2) above, state the transition and reporting dates for FRNL and two activities each to be

performed under each of the dates identified.

4. What are the differences (if any) between the voluntary IFRS accounts prepared by FRNL for group reporting and the

mandatory IFRS adoption for local reporting?

5. What are the challenges FRNL is likely to face in the IFRS transition process and what are your recommendations to

minimise the impact?

35