Embed Size (px)

Citation preview

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 1/53

COMMISSIONER OF INTERNAL REVENUE, petitioner, vs. SEAGATE TECHNOLOGY

(PHILIPPINES, respon!ent. "G.R. No. #$%&''. Fer)*r+ ##, --$.

Business companies registered in and operating from the Special Economic Zone in Naga, Cebu — like

herein respondent — are entities exempt from all internal revenue taxes and the implementing rulesrelevant thereto, including the value-added taxes or !"# !lthough export sales are not deemed exempt

transactions, the$ are nonetheless %ero-rated# &ence, in the present case, the distinction bet'een exemptentities and exempt transactions has little significance, because the net result is that the taxpa$er is not

liable for the !"# (espondent, a !"-registered enterprise, has complied 'ith all re)uisites for claiming

a tax refund of or credit for the input !" it paid on capital goods it purchased# "hus, the Court of "ax

!ppeals and the Court of !ppeals did not err in ruling that it is entitled to such refund or credit#

*acts+

# (espondent. is a resident foreign corporation dul$ registered 'ith the Securities and Exchange

Commission to do business in the /hilippines, 'ith principal office address at the ne' Cebu "o'nship

0ne, Special Economic Zone, Baranga$ Cantao-an, Naga, Cebu1

2# /etitioner. is sued in his official capacit$, having been dul$ appointed and empo'ered to perform

the duties of his office, including, among others, the dut$ to act and approve claims for refund or tax credit1

3# (espondent. is registered 'ith the /hilippine Export Zone !uthorit$ 4/EZ!5 and has been issued

/EZ! Certificate No# 67-899 pursuant to /residential :ecree No# ;;, as amended, to engage in themanufacture of recording components primaril$ used in computers for export# Such registration 'as made

on ; <une 6671

9# (espondent. is !" 4alue !dded "ax5.-registered entit$ as evidenced b$ !" (egistration

Certification No# 67-8=3-888;88- issued on 2 !pril 6671

># !" returns for the period !pril 66= to 38 <une 666 have been filed b$ respondent.1

;# !n administrative claim for refund of !" input taxes in the amount of /2=,3;6,22;#3= 'ith

supporting documents 4inclusive of the /2,2;7,6=#89 !" input taxes sub?ect of this /etition for

(evie'5, 'as filed on 9 0ctober 666 'ith (evenue :istrict 0ffice No# =3, "alisa$ Cebu1

7# No final action has been received b$ respondent. from petitioner. on respondent@s. claim for

!" refund#

A"he administrative claim for refund b$ the respondent. on 0ctober 9, 666 'as not acted upon b$ thepetitioner. prompting the respondent. to elevate the case to the C"!. on <ul$ 2, 2888 b$ 'a$ of /etition

for (evie' in order to toll the running of the t'o-$ear prescriptive period#

A*or his part, petitioner. # # # raised the follo'ing Special and !ffirmative :efenses, to 'it+

# (espondent@s. alleged claim for tax refundcredit is sub?ect to administrative routinar$

investigationexamination b$ petitioner@s. Bureau1

2# Since @taxes are presumed to have been collected in accordance 'ith la's and regulations,@ the

respondent. has the burden of proof that the taxes sought to be refunded 'ere erroneousl$ or illegall$collected # # #1

3# n Citibank, N#!# vs# Court of !ppeals, 2=8 SC(! 9>6 46675, the Supreme Court ruled that+

A! claimant has the burden of proof to establish the factual basis of his or her claim for tax creditrefund#A

9# Claims for tax refundtax credit are construed in @strictissimi ?uris@ against the taxpa$er# "his is due

to the fact that claims for refundcredit partake of. the nature of an exemption from tax# "hus, it is

incumbent upon the respondent. to prove that it is indeed entitled to the refundcredit sought# *ailure onthe part of the respondent. to prove the same is fatal to its claim for tax credit# &e 'ho claims exemption

must be able to ?ustif$ his claim b$ the clearest grant of organic or statutor$ la'# !n exemption from the

common burden cannot be permitted to exist upon vague implications1

># Dranting, 'ithout admitting, that respondent. is a /hilippine Economic Zone !uthorit$ 4/EZ!5

registered Eco%one Enterprise, then its business is not sub?ect to !" pursuant to Section 29 of (epublic

!ct No# 4(!.5 76; in relation to Section 83 of the "ax Code, as amended# !s respondent@s. business is

not sub?ect to !", the capital goods and services it alleged to have purchased are considered not used in!" taxable business# !s such, respondent. is not entitled to refund of input taxes on such capital goods

pursuant to Section 9#8;# of (evenue (egulations No# 4((.57-6>, and of input taxes on services

pursuant to Section 9#83 of said regulations#

;# (espondent. must sho' compliance 'ith the provisions of Section 289 4C5 and 226 of the 667

"ax Code on filing of a 'ritten claim for refund 'ithin t'o 425 $ears from the date of pa$ment of tax#@

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 2/53

A0n <ul$ 6, 288, the "ax Court rendered a decision granting the claim for refund#A

Sole ssue

/etitioner submits this sole issue for our consideration+

Ahether or not respondent is entitled to the refund or issuance of "ax Credit Certificate in the amount of

/2,22,622#;; representing alleged unutili%ed input !" paid on capital goods purchased for the period

!pril , 66= to <une 38, 666#A

"he Court@s (uling

"he /etition is unmeritorious#

Sole ssue+

Entitlement of a !"-(egistered /EZ! Enterprise to a (efund of or Credit for nput !"

No doubt, as a /EZ!-registered enterprise 'ithin a special economic %one, respondent is entitled to thefiscal incentives and benefits = provided for in either /: ;; 6 or E0 22;# 8 t shall, moreover, en?o$ all

privileges, benefits, advantages or exemptions under both (epublic !ct Nos# 4(!5 7227 and 7=99#

/referential "ax "reatment

Fnder Special Ga's

f it avails itself of /: ;;, not'ithstanding the provisions of other la's to the contrar$, respondent shall not

be sub?ect to internal revenue la's and regulations for ra' materials, supplies, articles, e)uipment,

machineries, spare parts and 'ares, except those prohibited b$ la', brought into the %one to be stored,

broken up, repacked, assembled, installed, sorted, cleaned, graded or other'ise processed, manipulated,manufactured, mixed or used directl$ or indirectl$ in such activities# 3 Even so, respondent 'ould en?o$ a

net-operating loss carr$ over1 accelerated depreciation1 foreign exchange and financial assistance1 and

exemption from export taxes, local taxes and licenses#

Comparativel$, the same exemption from internal revenue la's and regulations applies if E0 22; > is

chosen# Fnder this la', respondent shall further be entitled to an income tax holida$1 additional deduction

for labor expense1 simplification of customs procedure1 unrestricted use of consigned e)uipment1 access to

a bonded manufacturing 'arehouse s$stem1 privileges for foreign nationals emplo$ed1 tax credits ondomestic capital e)uipment, as 'ell as for taxes and duties on ra' materials1 and exemption from

contractors@ taxes, 'harfage dues, taxes and duties on imported capital e)uipment and spare parts, export

taxes, duties, imposts and fees, ; local taxes and licenses, and real propert$ taxes#

! privilege available to respondent under the provision in (! 7227 on tax and dut$-free importation of ra'

materials, capital and e)uipment = — is, ipso facto, also accorded to the %one 6 under (! 76;#

*urthermore, the latter la' — not'ithstanding other existing la's, rules and regulations to the contrar$ —

extends to that %one the provision stating that no local or national taxes shall be imposed therein# Noexchange control polic$ shall be applied1 and free markets for foreign exchange, gold, securities and future

shall be allo'ed and maintained# Banking and finance shall also be liberali%ed under minimum BangkoSentral regulation 'ith the establishment of foreign currenc$ depositor$ units of local commercial banks

and offshore banking units of foreign banks#

n the same vein, respondent benefits under (! 7=99 from negotiable tax credits for locall$-produced

materials used as inputs# !side from the other incentives possibl$ alread$ granted to it b$ the Board of

nvestments, it also en?o$s preferential credit facilities and exemption from /: =>3#

Fro/ t0e *ove12ite! 3*4s, it is i//e!i*te3+ 23e*r t0*t petitioner en5o+s pre6erenti*3 t*7 tre*t/ent. t isnot sub?ect to internal revenue la's and regulations and is even entitled to tax credits# "he !" on capital

goods is an internal revenue tax from 'hich petitioner as an entit$ is exempt# !lthough the transactions

involving such tax are not exempt, petitioner as a !"-registered person, ho'ever, is entitled to theircredits#

Nature of the !" and

the "ax Credit Hethod

ie'ed broadl$, the !" is a uniform tax ranging, at present, from 8 percent to 8 percent levied on ever$

importation of goods, 'hether or not in the course of trade or business, or imposed on each sale, barter,

exchange or lease of goods or properties or on each rendition of services in the course of trade or business

as the$ pass along the production and distribution chain, the tax being limited onl$ to the value added to

such goods, properties or services b$ the seller, transferor or lessor# t is an indirect tax that ma$ be shifted

or passed on to the bu$er, transferee or lessee of the goods, properties or services# !s such, it should be

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 3/53

understood not in the context of the person or entit$ that is primaril$, directl$ and legall$ liable for its

pa$ment, but in terms of its nature as a tax on consumption# n either case, though, the same conclusion is

arrived at#

"he la' that originall$ imposed the !" in the countr$, as 'ell as the subse)uent amendments of that la',has been dra'n from the tax credit method# Such method adopted the mechanics and self-enforcement

features of the !" as first implemented and practiced in Europe and subse)uentl$ adopted in Ne'Zealand and Canada# Fnder the present method that relies on invoices, an entit$ can credit against or

subtract from the !" charged on its sales or outputs the !" paid on its purchases, inputs and imports#

f at the end of a taxable )uarter the output taxes charged b$ a seller are e)ual to the input taxes passed on

b$ the suppliers, no pa$ment is re)uired# t is 'hen the output taxes exceed the input taxes that the excess

has to be paid# f, ho'ever, the input taxes exceed the output taxes, the excess shall be carried over to thesucceeding )uarter or )uarters# Should the input taxes result from %ero-rated or effectivel$ %ero-rated

transactions or from the ac)uisition of capital goods, an$ excess over the output taxes shall instead be

refunded to the taxpa$er or credited against other internal revenue taxes#

Zero-(ated and Effectivel$

Zero-(ated "ransactions

A3t0o)80 ot0 *re t*7*3e *n! si/i3*r in e66e2t, 9ero1r*te! tr*ns*2tions !i66er 6ro/ e66e2tive3+ 9ero1r*te!

tr*ns*2tions *s to t0eir so)r2e.

Zero-rated transactions generally refer to the export sale of goods and supply of services# "he tax rate is set

at %ero# hen applied to the tax base, such rate obviousl$ results in no tax chargeable against the purchaser#

T0e se33er o6 s)20 tr*ns*2tions 20*r8es no o)tp)t t*7, )t 2*n 23*i/ * re6)n! o6 or * t*7 2re!it

2erti6i2*te 6or t0e VAT previo)s3+ 20*r8e! + s)pp3iers#

Effectivel$ %ero-rated transactions, ho'ever, refer to the sale of goods or supply of services to persons or

entities whose exemption under special laws or international agreements to which the Philippines is a

signatory effectively subjects such transactions to a zero rate # !gain, as applied to the tax base, such ratedoes not $ield an$ tax chargeable against the purchaser# T0e se33er 40o 20*r8es 9ero o)tp)t t*7 on s)20

tr*ns*2tions 2*n *3so 23*i/ * re6)n! o6 or * t*7 2re!it 2erti6i2*te 6or t0e VAT previo)s3+ 20*r8e! +

s)pp3iers.

Zero (ating and

Exemption

n terms of the !" computation, %ero rating and exemption are the same, but the extent of relief that

results from either one of them is not#

!ppl$ing the destination principle to the exportation of goods, automatic zero rating is

pri/*ri3+ inten!e! to e en5o+e! + t0e se33er 40o is !ire2t3+ *n! 3e8*33+ 3i*3e 6or t0e VAT, /*:in8 s)20se33er intern*tion*33+ 2o/petitive + *33o4in8 t0e re6)n! or 2re!it o6 inp)t t*7es t0*t *re *ttri)t*3e to

e7port s*3es# Effective zero rating, on the contrar$, is inten!e! to ene6it t0e p)r20*ser 40o, not

ein8 !ire2t3+ *n! 3e8*33+ 3i*3e 6or t0e p*+/ent o6 t0e VAT, 4i33 )3ti/*te3+ e*r t0e )r!en o6 t0e t*7

s0i6te! + t0e s)pp3iers.

n both instances of %ero rating, there is total relief for the purchaser from the burden of the tax# But in an

exemption there is onl$ partial relief, because the purchaser is not allo'ed an$ tax refund of or credit for

input taxes paid#

Exempt "ransactionand Exempt /art$

"he ob?ect of exemption from the !" ma$ either be the transaction itself or an$ of the parties to the

transaction#

!n exempt transaction, on the one hand, involves goods or services 'hich, b$ their nature, are specificall$

listed in and expressl$ exempted from the !" under the "ax Code, 'ithout regard to the tax status —

!"-exempt or not — of the part$ to the transaction# ;8 ndeed, such transaction is not sub?ect to the!", but the seller is not allo'ed an$ tax refund of or credit for an$ input taxes paid#

!n exempt part$, on the other hand, is a person or entit$ granted !" exemption under the "ax Code, a

special la' or an international agreement to 'hich the /hilippines is a signator$, and b$ virtue of 'hich its

taxable transactions become exempt from the !"# Such part$ is also not sub?ect to the !", but ma$ be

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 4/53

allo'ed a tax refund of or credit for input taxes paid, depending on its registration as a !" or non-!"

taxpa$er#

!s mentioned earlier, the !" is a tax on consumption, the amount of 'hich ma$ be shifted or passed on

b$ the seller to the purchaser of the goods, properties or services# hile the liabilit$ is imposed on one person, the burden ma$ be passed on to another# "herefore, if a special la' merel$ exempts a part$ as a

seller from its direct liabilit$ for pa$ment of the !", but does not relieve the same part$ as a purchaserfrom its indirect burden of the !" shifted to it b$ its !"-registered suppliers, the purchase transaction is

not exempt# !ppl$ing this principle to the case at bar, the purchase transactions entered into b$ respondent

are not !"-exempt#

Special la's ma$ certainl$ exempt transactions from the !"# &o'ever, the "ax Code provides that those

falling under /: ;; are not# /: ;; is the precursor of (! 76; — the special la' under 'hich respondent'as registered# "he purchase transactions it entered into are, therefore, not !"-exempt# "hese are sub?ect

to the !"1 respondent is re)uired to register#

ts sales transactions, ho'ever, 'ill either be %ero-rated or taxed at the standard rate of 8 percent,

depending again on the application of the destination principle#

f respondent enters into such sales transactions 'ith a purchaser — usuall$ in a foreign countr$ — for use

or consumption outside the /hilippines, these shall be sub?ect to 8 percent# f entered into 'ith a purchaserfor use or consumption in the /hilippines, then these shall be sub?ect to 8 percent, unless the purchaser is

exempt from the indirect burden of the !", in 'hich case it shall also be %ero-rated#

Since the purchases of respondent are not exempt from the !", the rate to be applied is %ero# ts

exemption under both /: ;; and (! 76; effectivel$ sub?ects such transactions to a %ero rate, because the

eco%one 'ithin 'hich it is registered is managed and operated b$ the /EZ! as a separate customs territor$#

"his means that in such %one is created the legal fiction of foreign territor$# Fnder the cross-border

principle of the !" s$stem being enforced b$ the Bureau of nternal (evenue 4B(5, no !" shall be

imposed to form part of the cost of goods destined for consumption outside of the territorial border of the

taxing authorit$# f exports of goods and services from the /hilippines to a foreign countr$ are free of the!", then the same rule holds for such exports from the national territor$ — except specificall$ declared

areas — to an eco%one#

Sales made b$ a !"-registered person in the customs territor$ to a /EZ!-registered entit$ are considered

exports to a foreign countr$1 conversel$, sales b$ a /EZ!-registered entit$ to a !"-registered person in

the customs territor$ are deemed imports from a foreign countr$# !n eco%one — indubitabl$ a geographical

territor$ of the /hilippines — is, ho'ever, regarded in la' as foreign soil# "his legal fiction is necessar$ to

give meaningful effect to the policies of the special la' creating the %one# f respondent is located in anexport processing %one 'ithin that eco%one, sales to the export processing %one, even 'ithout being

actuall$ exported, shall in fact be vie'ed as constructivel$ exported under E0 22;# Considered as export

sales, such purchase transactions b$ respondent 'ould indeed be sub?ect to a %ero rate#

"ax Exemptions

Broad and Express

!ppl$ing the special la's 'e have earlier discussed, respondent as an entit$ is exempt from internalrevenue la's and regulations#

"his exemption covers both direct and indirect taxes, stemming from the ver$ nature of the !" as a tax

on consumption, for 'hich the direct liabilit$ is imposed on one person but the indirect burden is passed on

to another# Respon!ent, *s *n e7e/pt entit+, 2*n neit0er e !ire2t3+ 20*r8e! 6or t0e VAT on its s*3es nor

in!ire2t3+ /*!e to e*r, *s *!!e! 2ost to s)20 s*3es, t0e e;)iv*3ent VAT on its p)r20*ses. Ubi lex non

distinguit, nec nos distinguere debemus# here the la' does not distinguish, 'e ought not to distinguish#

Horeover, the exemption is both express and pervasive for the follo'ing reasons+

*irst, (! 76; states that Ano taxes, local and national, shall be imposed on business establishments

operating 'ithin the eco%one#A = Since this la' does not exclude the !" from the prohibition, it is

deemed included# Exceptio firmat regulam in casibus non exceptis# !n exception confirms the rule in casesnot excepted1 that is, a thing not being excepted must be regarded as coming 'ithin the purvie' of the

general rule#

Horeover, even though the !" is not imposed on the entit$ but on the transaction, it ma$ still be passed

on and, therefore, indirectl$ imposed on the same entit$ — a patent circumvention of the la'# "hat no !"shall be imposed directl$ upon business establishments operating 'ithin the eco%one under (! 76; also

means that no !" ma$ be passed on and imposed indirectl$# Iuando ali)uid prohibetur ex directo

prohibetur et per obli)uum# hen an$thing is prohibited directl$, it is also prohibited indirectl$#

Second, 'hen (! =79= 'as enacted to amend (! 76;, the same prohibition applied, except for real

propert$ taxes that presentl$ are imposed on land o'ned b$ developers# "his similar and repeated

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 5/53

prohibition is an unambiguous ratification of the la'@s intent in not imposing local or national taxes on

business enterprises 'ithin the eco%one#

"hird, foreign and domestic merchandise, ra' materials, e)uipment and the like Ashall not be sub?ect to # # #

internal revenue la's and regulationsA under /: ;; — the original charter of /EZ! 4then E/Z!5 that 'aslater amended b$ (! 76;# No provisions in the latter la' modif$ such exemption#

!lthough this exemption puts the government at an initial disadvantage, the reduced tax collection

ultimatel$ redounds to the benefit of the national econom$ b$ enticing more business investments and

creating more emplo$ment opportunities#

*ourth, even the rules implementing the /EZ! la' clearl$ reiterate that merchandise — except those

prohibited b$ la' — Ashall not be sub?ect to # # # internal revenue la's and regulations # # #A if brought to theeco%one@s restricted area for manufacturing b$ registered export enterprises, of 'hich respondent is one#

"hese rules also appl$ to all enterprises registered 'ith the E/Z! prior to the effectivit$ of such rules#

*ifth, export processing %one enterprises registered 'ith the Board of nvestments 4B05 under E0 22;

patentl$ en?o$ exemption from national internal revenue taxes on imported capital e)uipment reasonabl$

needed and exclusivel$ used for the manufacture of their products1 on re)uired supplies and spare part for

consigned e)uipment1 and on foreign and domestic merchandise, ra' materials, e)uipment and the like —

except those prohibited b$ la' — brought into the %one for manufacturing# n addition, the$ are givencredits for the value of the national internal revenue taxes imposed on domestic capital e)uipment also

reasonabl$ needed and exclusivel$ used for the manufacture of their products, as 'ell as for the value ofsuch taxes imposed on domestic ra' materials and supplies that are used in the manufacture of their export

products and that form part thereof#

Sixth, the exemption from local and national taxes granted under (! 7227 are ipso facto accorded to

eco%ones# n case of doubt, conflicts 'ith respect to such tax exemption privilege shall be resolved in favor

of the eco%one#

!nd seventh, the tax credits under (! 7=99 — given for imported ra' materials primaril$ used in the production of export goods, and for locall$ produced ra' materials, capital e)uipment and spare parts used

b$ exporters of non-traditional products — shall also be continuousl$ en?o$ed b$ similar exporters 'ithin

the eco%one# ndeed, the latter exporters are like'ise entitled to such tax exemptions and credits#

"ax (efund as

"ax Exemption

"o be sure, statutes that grant tax exemptions are construed strictissimi ?uris against the taxpa$er andliberall$ in favor of the taxing authorit$#

"ax refunds are in the nature of such exemptions# !ccordingl$, the claimants of those refunds bear the

burden of proving the factual basis of their claims1 and of sho'ing, b$ 'ords too plain to be mistaken, that

the legislature intended to exempt them# n the present case, all the cited legal provisions are teeming 'ith

life 'ith respect to the grant of tax exemptions too vivid to pass unnoticed# n addition, respondent easil$

meets the challenge#

(espondent, 'hich as an entit$ is exempt, is different from its transactions 'hich are not exempt# "he end

result, ho'ever, is that it is not sub?ect to the !"# "he non-taxabilit$ of transactions that are other'isetaxable is merel$ a necessar$ incident to the tax exemption conferred b$ la' upon it as an entit$, not upon

the transactions themselves# Nonetheless, its exemption as an entit$ and the non-exemption of its

transactions lead to the same result for the follo'ing considerations+

*irst, the contemporaneous construction of our tax la's b$ B( authorities 'ho are called upon to execute

or administer such la's 'ill have to be adopted# "heir prior tax issuances have held inconsistent positions

brought about b$ their probable failure to comprehend and full$ appreciate the nature of the !" as a tax

on consumption and the application of the destination principle# (evenue Hemorandum Circular No#4(HC5 79-66, ho'ever, no' clearl$ and correctl$ provides that an$ !"-registered supplier@s sale of

goods, propert$ or services from the customs territor$ to an$ registered enterprise operating in the eco%one

— regardless of the class or t$pe of the latter@s /EZ! registration — is legall$ entitled to a %ero rate#

Second, the policies of the la' should prevail# (atio legis est anima# "he reason for the la' is its ver$ soul#

n /: ;;, the urgent creation of the E/Z! 'hich preceded the /EZ!, as 'ell as the establishment of export

processing %ones, seeks Ato encourage and promote foreign commerce as a means of # # # strengthening ourexport trade and foreign exchange position, of hastening industriali%ation, of reducing domestic

unemplo$ment, and of accelerating the development of the countr$#A

(! 76;, as amended b$ (! =79=, declared that b$ creating the /EZ! and integrating the special

economic %ones, Athe government shall activel$ encourage, promote, induce and accelerate a sound and

balanced industrial, economic and social development of the countr$ # # # through the establishment, among

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 6/53

others, of special economic %ones # # # that shall effectivel$ attract legitimate and productive foreign

investments#A

Fnder E0 22;, the AState shall encourage # # # foreign investments in industr$ # # # 'hich shall # # meet the

tests of international competitiveness,. accelerate development of less developed regions of the countr$,.and result in increased volume and value of exports for the econom$#A *iscal incentives that are cost-

efficient and simple to administer shall be devised and extended to significant pro?ects Ato compensate formarket imperfections, to re'ard performance contributing to economic development,A and Ato stimulate the

establishment and assist initial operations of the enterprise#A

isel$ accorded to eco%ones created under (! 76; 'as the government@s polic$ — spelled out earlier in

(! 7227 — of converting into alternative productive uses the former militar$ reservations and theirextensions, as 'ell as of providing them incentives to enhance the benefits that 'ould be derived from

them in promoting economic and social development#

*inall$, under (! 7=99, the State declares the need Ato evolve export development into a national effortA in

order to 'in international markets# B$ providing man$ export and tax incentives, the State is able to drive

home the point that exporting is indeed Athe ke$ to national survival and the means through 'hich the

economic goals of increased emplo$ment and enhanced incomes can most expeditiousl$ be achieved#A

"he "ax Code itself seeks to Apromote sustainable economic gro'th # # #1 # # # increase economic activit$1

and # # # create a robust environment for business to enable firms to compete better in the regional as 'ell asthe global market#A !fter all, international competitiveness re)uires economic and tax incentives to lo'er

the cost of goods produced for export# State actions that affect global competition need to be specific and

selective in the pricing of particular goods or services#

!ll these statutor$ policies are congruent to the constitutional mandates of providing incentives to needed

investments, 2= as 'ell as of promoting the preferential use of domestic materials and locall$ produced

goods and adopting measures to help make these competitive# 26 "ax credits for domestic inputs

strengthen back'ard linkages# (ightl$ so, Athe rule of la' and the existence of credible and efficient publicinstitutions are essential prere)uisites for sustainable economic development#A

!" (egistration, Not !pplicationfor Effective Zero (ating,

ndispensable to !" (efund

(egistration is an indispensable re)uirement under our !" la'# /etitioner alleges that respondent did

register for !" purposes 'ith the appropriate (evenue :istrict 0ffice# &o'ever, it is no' too late in theda$ for petitioner to challenge the !"-registered status of respondent, given the latter@s prior

representation before the lo'er courts and the mode of appeal taken b$ petitioner before this Court#

"he /EZ! la', 'hich carried over the provisions of the E/Z! la', is clear in exempting from internal

revenue la's and regulations the e)uipment — including capital goods — that registered enterprises 'ill

use, directl$ or indirectl$, in manufacturing# E0 22; even reiterates this privilege among the incentives it

gives to such enterprises# /etitioner merel$ asserts that b$ virtue of the /EZ! registration alone of

respondent, the latter is not sub?ect to the !"# Conse)uentl$, the capital goods and services respondenthas purchased are not considered used in the !" business, and no !" refund or credit is due# "his is a

non se)uitur# B$ the !"@s ver$ nature as a tax on consumption, the capital goods and services respondenthas purchased are sub?ect to the !", although at %ero rate# (egistration does not determine taxabilit$

under the !" la'#

Horeover, the facts have alread$ been determined b$ the lo'er courts# &aving failed to present evidence to

support its contentions against the income tax holida$ privilege of respondent, petitioner is deemed to have

conceded# t is a cardinal rule that Aissues and arguments not ade)uatel$ and seriousl$ brought belo'

cannot be raised for the first time on appeal#A "his is a Amatter of procedureA and a A)uestion of fairness#A

*ailure to assert A'ithin a reasonable time 'arrants a presumption that the part$ entitled to assert it eitherhas abandoned or declined to assert it#A

"he B( regulations additionall$ re)uiring an approved prior application for effective %ero rating cannot prevail over the clear !" nature of respondent@s transactions# "he scope of such regulations is not A'ithin

the statutor$ authorit$ # # # granted b$ the legislature#

*irst, a mere administrative issuance, like a B( regulation, cannot amend the la'1 the former cannot

purport to do an$ more than interpret the latter# "he courts 'ill not countenance one that overrides thestatute it seeks to appl$ and implement#

0ther than the general registration of a taxpa$er the !" status of 'hich is aptl$ determined, no provision

under our !" la' re)uires an additional application to be made for such taxpa$er@s transactions to be

considered effectivel$ %ero-rated# !n effectivel$ %ero-rated transaction does not and cannot become exempt

simpl$ because an application therefor 'as not made or, if made, 'as denied# "o allo' the additional

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 7/53

re)uirement is to give unfettered discretion to those officials or agents 'ho, 'ithout fluid consideration, are

bent on den$ing a valid application# Horeover, the State can never be estopped b$ the omissions, mistakes

or errors of its officials or agents#

Second, grantia argumenti that such an application is re)uired b$ la', there is still the presumption ofregularit$ in the performance of official dut$# (espondent@s registration carries 'ith it the presumption that,

in the absence of contradictor$ evidence, an application for effective %ero rating 'as also filed and approvalthereof given# Besides, it is also presumed that the la' has been obe$ed b$ both the administrative officials

and the applicant#

"hird, even though such an application 'as not made, all the special la's 'e have tackled exempt

respondent not onl$ from internal revenue la's but also from the regulations issued pursuant thereto#

Genienc$ in the implementation of the !" in eco%ones is an imperative, precisel$ to spur economicgro'th in the countr$ and attain global competitiveness as envisioned in those la's#

! !"-registered status, as 'ell as compliance 'ith the invoicing re)uirements, is sufficient for the

effective %ero rating of the transactions of a taxpa$er# "he nature of its business and transactions can easil$

be perused from, as alread$ clearl$ indicated in, its !" registration papers and photocopied documents

attached thereto# &ence, its transactions cannot be exempted b$ its mere failure to appl$ for their effective

%ero rating# 0ther'ise, their !" exemption 'ould be determined, not b$ their nature, but b$ the

taxpa$er@s negligence — a result not at all contemplated# !dministrative convenience cannot th'artlegislative mandate#

"ax (efund or

Credit in 0rder

&aving determined that respondent@s purchase transactions are sub?ect to a %ero !" rate, the tax refund or

credit is in order#

!s correctl$ held b$ both the C! and the "ax Court, respondent had chosen the fiscal incentives in E0 22;

over those in (! 76; and /: ;;# t opted for the income tax holida$ regime instead of the > percent preferential tax regime#

"he latter scheme is not a perfunctor$ aftermath of a simple registration under the /EZ! la', for E0 22;also has provisions to contend 'ith# "hese t'o regimes are in fact incompatible and cannot be availed of

simultaneousl$ b$ the same entit$# hile E0 22; merel$ exempts it from income taxes, the /EZ! la'

exempts it from all taxes#

"herefore, respondent can be considered exempt, not from the !", but onl$ from the pa$ment of incometax for a certain number of $ears, depending on its registration as a pioneer or a non-pioneer enterprise#

Besides, the remittance of the aforesaid > percent of gross income earned in lieu of local and national taxes

imposable upon business establishments 'ithin the eco%one cannot outrightl$ determine a !" exemption#

Being sub?ect to !", pa$ments erroneousl$ collected thereon ma$ then be refunded or credited#

Even if it is argued that respondent is sub?ect to the > percent preferential tax regime in (! 76;, Section

29 thereof does not preclude the !"# 0ne can, therefore, counterargue that such provision merel$

exempts respondent from taxes imposed on business# "o repeat, the !" is a tax imposed on consumption,not on business# !lthough respondent as an entit$ is exempt, the transactions it enters into are not

necessaril$ so# "he !" pa$ments made in excess of the %ero rate that is imposable ma$ certainl$ berefunded or credited#

Compliance 'ith !ll (e)uisites

for !" (efund or Credit

!s further enunciated b$ the "ax Court, respondent complied 'ith all the re)uisites for claiming a !"

refund or credit#

*irst, respondent is a !"-registered entit$# "his fact alone distinguishes the present case from Contex, in

'hich this Court held that the petitioner therein 'as registered as a non-!" taxpa$er# &ence, for being

merel$ !"-exempt, the petitioner in that case cannot claim an$ !" refund or credit#

Second, the input taxes paid on the capital goods of respondent are dul$ supported b$ !" invoices and

have not been offset against an$ output taxes# !lthough enterprises registered 'ith the B0 after :ecember

3, 669 'ould no longer en?o$ the tax credit incentives on domestic capital e)uipment — as provided for

under !rticle 364d5, "itle , Book of E0 22; — starting <anuar$ , 66;, respondent 'ould still have thesame benefit under a general and express exemption contained in both !rticle 7745, Book of E0 22;1

and Section 2, paragraph 2 4c5 of (! 7227, extended to the eco%ones b$ (! 76;#

"here 'as a ver$ clear intent on the part of our legislators, not onl$ to exempt investors in eco%ones from

national and local taxes, but also to grant them tax credits# "his fact 'as revealed b$ the sponsorship

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 8/53

speeches in Congress during the second reading of &ouse Bill No# 926>, 'hich later became (! 76;, as

sho'n belo'+

AH(# (EC"0# # # # Some of the incentives that this bill provides are exemption from national and local

taxes1 # # # tax credit for locall$-sourced inputs # # #A

xxx xxx xxx

AH(# :EG H!(# # # # "o advance its cause in encouraging investments and creating an environment

conducive for investors, the bill offers incentives such as the exemption from local and national taxes, # # #

tax credits for locall$ sourced inputs # # #A

!nd third, no )uestion as to either the filing of such claims 'ithin the prescriptive period or the validit$ ofthe !" returns has been raised# Even if such a )uestion 'ere raised, the tax exemption under all the

special la's cited above is broad enough to cover even the enforcement of internal revenue la's, including

prescription#

Summar$

"o summari%e, special la's expressl$ grant preferential tax treatment to business establishments registered

and operating 'ithin an eco%one, 'hich b$ la' is considered as a separate customs territor$# !s such,respondent is exempt from all internal revenue taxes, including the !", and regulations pertaining

thereto# t has opted for the income tax holida$ regime, instead of the > percent preferential tax regime# !sa matter of la' and procedure, its registration status entitling it to such tax holida$ can no longer be

)uestioned# ts sales transactions intended for export ma$ not be exempt, but like its purchase transactions,

the$ are %ero-rated# No prior application for the effective %ero rating of its transactions is necessar$# <ein8

VAT1re8istere! *n! 0*vin8 s*tis6*2tori3+ 2o/p3ie! 4it0 *33 t0e re;)isites 6or 23*i/in8 * t*7 re6)n! o6 or

2re!it 6or t0e inp)t VAT p*i! on 2*pit*3 8oo!s p)r20*se!, respon!ent is entit3e! to s)20 VAT re6)n! or

2re!it.

COMMISSIONER OF INTERNAL REVENUE, petitioner, vs. CE<U TOYO CORPORATION,

respon!ent. "G.R. No. #=>-?%. Fer)*r+ #', --$.

(uling+

Both the Commissioner of nternal (evenue and the 0ffice of the Solicitor Deneral argue that respondent

Cebu "o$o Corporation, as a /EZ!-registered enterprise, is exempt from national and local taxes,

including !", under Section 29 of (ep# !ct No# 76; and Section 86 2 of the N(C# "hus, the$contend that respondent Cebu "o$o Corporation is not entit3e! to *n+ re6)n! or 2re!it on inp)t t*7es it

previo)s3+ p*i! *s provi!e! )n!er Se2tion =.#-%1# o6 Reven)e Re8)3*tions No. ?1>$, not4it0st*n!in8

its re8istr*tion *s * VAT t*7p*+er. For petitioner 23*i/s t0*t s*i! re8istr*tion 4*s erroneo)s *n! !i! not

2on6er )pon t0e respon!ent *n+ ri80t to 23*i/ re2o8nition o6 t0e inp)t t*7 2re!it.

"he respondent counters that it availed of the income tax holida$ under E#0# No# 22; for four $ears from

!ugust 7, 66> making it exempt from income tax but not from other taxes such as !"# &ence, according

to respondent, its export sales are not exempt from !", contrar$ to petitioner@s claim, but its export salesis sub?ect to 8J !"# Horeover, it argues that it 'as able to establish through a report certified b$ an

independent Certified /ublic !ccountant that the input taxes it incurred from !pril , 66; to :ecember3, 667 'ere directl$ attributable to its export sales# Since it did not have an$ output tax against 'hich

said input taxes ma$ be offset, it had the option to file a claim for refundtax credit of its unutili%ed input

taxes#

Considering the submission of the parties and the evidence on record, 'e find the petition bereft of merit#

/etitioner@s contention that respondent is not entitled to refund for being exempt from !" is untenable#

"his argument turns a blind e$e to the fiscal incentives granted to /EZ!-registered enterprises underSection 23 of (ep# !ct No# 76;# Note t0*t )n!er s*i! st*t)te, t0e respon!ent 0*! t4o options 4it0

respe2t to its t*7 )r!en. It 2o)3! *v*i3 o6 *n in2o/e t*7 0o3i!*+ p)rs)*nt to provisions o6 E.O. No. ',

t0)s e7e/pt it 6ro/ in2o/e t*7es 6or * n)/er o6 +e*rs )t not 6ro/ ot0er intern*3 reven)e t*7es s)20*s VAT@ or it 2o)3! *v*i3 o6 t0e t*7 e7e/ptions on *33 t*7es, in23)!in8 VAT )n!er P.. No. '' *n! p*+

on3+ t0e pre6erenti*3 t*7 r*te o6 $B )n!er Rep. A2t No. ?>#'. Both the Court of !ppeals and the Court of

"ax !ppeals found that respondent availed of the income tax holida$ for four 495 $ears starting from

!ugust 7, 66>, as clearl$ reflected in its 66; and 667 !nnual Corporate ncome "ax (eturns, 'here

respondent specified that it 'as availing of the tax relief under E#0# No# 22;# &ence, respondent is notexempt from !" and it correctl$ registered itself as a !" taxpa$er# n fine, it is engaged in taxable

rather than exempt transactions#

T*7*3e tr*ns*2tions *re t0ose tr*ns*2tions 40i20 *re s)5e2t to v*3)e1*!!e! t*7 eit0er *t t0e r*te o6 ten

per2ent (#-B or 9ero per2ent (-B# n taxable transactions, the seller shall be entitled to tax credit for the

value-added tax paid on purchases and leases of goods, properties or services#

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 9/53

An e7e/ption /e*ns t0*t t0e s*3e o6 8oo!s, properties or servi2es *n! t0e )se or 3e*se o6 properties is

not s)5e2t to VAT (o)tp)t t*7 *n! t0e se33er is not *33o4e! *n+ t*7 2re!it on VAT (inp)t t*7 previo)s3+

p*i! # "he person making the exempt sale of goods, properties or services shall not bill an$ output tax to his

customers because the said transaction is not sub?ect to !"# T0)s, * VAT1re8istere! p)r20*ser o6 8oo!s,

properties or servi2es t0*t *re VAT1e7e/pt, is not entit3e! to *n+ inp)t t*7 on s)20 p)r20*ses !espite t0e

iss)*n2e o6 * VAT invoi2e or re2eipt #

No', having determined that respondent is engaged in taxable transactions sub?ect to !", let us then

proceed to determine 'hether it is sub?ect to 8J or %ero 48J5 rate of !"# "o begin 'ith, it must be

recalled that generall$, sale of goods and suppl$ of services performed in the /hilippines are taxable at the

rate of 8J# &o'ever, export sales, or sales outside the /hilippines, shall be sub?ect to value-added tax at

8J if made b$ a !"-registered person# Un!er t0e v*3)e1*!!e! t*7 s+ste/, * 9ero1r*te! s*3e + * VAT1

re8istere! person, 40i20 is * t*7*3e tr*ns*2tion 6or VAT p)rposes, s0*33 not res)3t in *n+ o)tp)t t*7.

Ho4ever, t0e inp)t t*7 on 0is p)r20*se o6 8oo!s, properties or servi2es re3*te! to s)20 9ero1r*te! s*3e

s0*33 e *v*i3*3e *s t*7 2re!it or re6)n!.

n principle, the purpose of appl$ing a %ero percent 48J5 rate on a taxable transaction is to exempt the

transaction completel$ from !" previousl$ collected on inputs# t is thus the onl$ true 'a$ to ensure that

goods are provided free of !"# hile the %ero rating and the exemption are computationall$ the same,

the$ actuall$ differ in several aspects, to 'it+

4a5 ! %ero-rated sale is a taxable transaction but does not result in an output tax 'hile an exemptedtransaction is not sub?ect to the output tax1

4b5 "he input !" on the purchases of a !"-registered person 'ith %ero-rated sales ma$ be allo'ed

as tax credits or refunded 'hile the seller in an exempt transaction is not entitled to an$ input tax on his

purchases despite the issuance of a !" invoice or receipt#

4c5 /ersons engaged in transactions 'hich are %ero-rated, being sub?ect to !", are re)uired to

register 'hile registration is optional for !"-exempt persons#

n this case, it is undisputed that respondent is engaged in the export business and is registered as a !"

taxpa$er per Certificate of (egistration of the B(# *urther, the records sho' that the respondent is sub?ectto !" as it availed of the income tax holida$ under E#0# No# 22;# /erforce, respondent is sub?ect to !"

at 8J rate and is entitled to a refund or credit of the unutili%ed input taxes, 'hich the Court of "ax !ppeals

computed at /2,>=,79#9;, but 'hich 'e find — after recomputation — should be /2,>=,79#>2#

"he Supreme Court 'ill not set aside lightl$ the conclusions reached b$ the Court of "ax !ppeals 'hich,

b$ the ver$ nature of its functions, is dedicated exclusivel$ to the resolution of tax problems and has

accordingl$ developed an expertise on the sub?ect, unless there has been an abuse or improvident exercise

of authorit$# n this case, 'e find no cogent reason to deviate from this 'ell-entrenched principle# "hus, 'eare persuaded that indeed the Court of !ppeals committed no reversible error in affirming the assailed

ruling of the Court of "ax !ppeals#

MANUEL G. A<ELLO, OSE C. CONCEPCION, TEOORO . REGALA, AVELINO V. CRUD,

petitioners, vs. COMMISSIONER OF INTERNAL REVENUE *n! COURT OF APPEALS,

respon!ents. "G.R. No. #-?#. Fer)*r+ %, --$.

*acts+

:uring the 6=7 national elections, petitioners, 'ho are partners in the !ngara, !bello, Concepcion, (egala

and Cru% 4!CC(!5 la' firm, contributed /==2,;;#3 each to the campaign funds of Senator Edgardo

!ngara, then running for the Senate# n letters dated !pril 2, 6==, the Bureau of nternal (evenue 4B(5

assessed each of the petitioners /2;3,832#;; for their contributions# 0n !ugust 2, 6==, petitioners

)uestioned the assessment through a letter to the B(# "he$ claimed that political or electoral contributions

are not considered gifts under the National nternal (evenue Code 4N(C5, and that, therefore, the$ are not

liable for donor@s tax# "he claim for exemption 'as denied b$ the Commissioner#

(uling+

Section 6 of the National nternal (evenue Code 4N(C5 reads+

4!5 "here shall be levied, assessed, collected and paid upon the transfer b$ an$ person, resident or

nonresident, of the propert$ b$ gift, a tax, computed as provided in Section 62

4B5 "he tax shall appl$ 'hether the transfer is in trust or other'ise, 'hether the gift is direct orindirect, and 'hether the propert$ is real or personal, tangible or intangible#

"he N(C does not define transfer of propert$ b$ gift# &o'ever, !rticle = of the Civil Code, states+

n matters 'hich are governed b$ the Code of Commerce and special la's, their deficienc$ shall be

supplied b$ the provisions of this Code#

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 10/53

"hus, reference ma$ be made to the definition of a donation in the Civil Code# !rticle 72> of said Code

defines donation as+

# # # an act of liberalit$ 'hereb$ a person disposes gratuitousl$ of a thing or right in favor of another, 'ho

accepts it#

:onation has the follo'ing elements+ 4a5 the reduction of the patrimon$ of the donor1 4b5 the increase in the patrimon$ of the donee1 and, 4c5 the intent to do an act of liberalit$ or animus donandi#

"he present case falls s)uarel$ 'ithin the definition of a donation# /etitioners, the late Hanuel D# !bello ,

<ose C# Concepcion, "eodoro :# (egala and !velino # Cru%, each gave /==2,;;#3 to the campaign

funds of Senator Edgardo !ngara, 'ithout an$ material consideration# !ll three elements of a donation are

present# "he patrimon$ of the four petitioners 'ere reduced b$ /==2,;;#3 each# Senator Edgardo!ngara@s patrimon$ correspondingl$ increased b$ /3,>38,;9>#296 # "here 'as intent to do an act of

liberalit$ or animus donandi 'as present since each of the petitioners gave their contributions 'ithout an$

consideration#

"aken together 'ith the Civil Code definition of donation, Section 6 of the N(C is clear and

unambiguous, thereb$ leaving no room for construction# n (i%al Commercial Banking Corporation v#

ntermediate !ppellate Court 8 the Court enunciated+

t bears stressing that the first and fundamental dut$ of the Court is to appl$ the la'# hen the la' is clear

and free from an$ doubt or ambiguit$, there is no room for construction or interpretation# !s has been ourconsistent ruling, 'here the la' speaks in clear and categorical language, there is no occasion for

interpretation1 there is onl$ room for application 4Cebu /ortland Cement Co# v# Hunicipalit$ of Naga, 29

SC(! 78= 6;=.5

here the la' is clear and unambiguous, it must be taken to mean exactl$ 'hat it sa$s and the court has no

choice but to see to it that its mandate is obe$ed 4Chartered Bank Emplo$ees !ssociation v# 0ple, 3=

SC(! 273 6=>.1 Gu%on Suret$ Co#, nc# v# :e Darcia, 38 SC(! 6;6.1 Iui?ano v# :evelopment

Bank of the /hilippines, 3> SC(! 278 678.5#

0nl$ 'hen the la' is ambiguous or of doubtful meaning ma$ the court interpret or construe its true intent#

!mbiguit$ is a condition of admitting t'o or more meanings, of being understood in more than one 'a$, or

of referring to t'o or more things at the same time# ! statute is ambiguous if it is admissible of t'o or more

possible meanings, in 'hich case, the Court is called upon to exercise one of its ?udicial functions, 'hich is

to interpret the la' according to its true intent#

Second ssue

Since animus donandi or the intention to do an act of liberalit$ is an essential element of a donation,

petitioners argue that it is important to look into the intention of the giver to determine if a political

contribution is a gift# /etitioners@ argument is not tenable# *irst of all, donative intent is a creature of the

mind# t cannot be perceived except b$ the material and tangible acts 'hich manifest its presence# "his

being the case, donative intent is presumed present 'hen one gives a part of ones patrimon$ to another'ithout consideration# Second, donative intent is not negated 'hen the person donating has other

intentions, motives or purposes 'hich do not contradict donative intent# "his Court is not convinced thatsince the purpose of the contribution 'as to help elect a candidate, there 'as no donative intent# /etitioners@

contribution of mone$ 'ithout an$ material consideration evinces animus donandi# "he fact that their

purpose for donating 'as to aid in the election of the donee does not negate the presence of donative intent#

"hird ssue

/etitioners maintain that the definition of an Aelectoral contributionA under the 0mnibus Election Code is

essential to appreciate ho' a political contribution differs from a taxable gift# Section 694a5 of the saidCode defines electoral contribution as follo's+

"he term AcontributionA includes a gift, donation, subscription, loan, advance or deposit of mone$ oran$thing of value, or a contract, promise or agreement to contribute, 'hether or not legall$ enforceable,

made for the purpose of influencing the results of the elections but shall not include services rendered

'ithout compensation b$ individuals volunteering a portion or all of their time in behalf of a candidate or

political part$# t shall also include the use of facilities voluntaril$ donated b$ other persons, the mone$

value of 'hich can be assessed based on the rates prevailing in the area#

Since the purpose of an electoral contribution is to influence the results of the election, petitioners again

claim that donative intent is not present# /etitioners attempt to place the barrier of mutual exclusivit$

bet'een donative intent and the purpose of political contributions# "his Court reiterates that donative intent

is not negated b$ the presence of other intentions, motives or purposes 'hich do not contradict donative

intent#

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 11/53

/etitioners 'ould distinguish a gift from a political donation b$ sa$ing that the consideration for a gift is

the liberalit$ of the donor, 'hile the consideration for a political contribution is the desire of the giver to

influence the result of an election b$ supporting candidates 'ho, in the perception of the giver, 'ould

influence the shaping of government policies that 'ould promote the general 'elfare and economic 'ell- being of the electorate, including the giver himself#

/etitioners@ attempt is strained# "he fact that petitioners 'ill someho' in the future benefit from the election

of the candidate to 'hom the$ contribute, in no 'a$ amounts to a valuable material consideration so as to

remove political contributions from the purvie' of a donation# Senator !ngara 'as under no obligation to

benefit the petitioners# "he proper performance of his duties as a legislator is his obligation as an elected

public servant of the *ilipino people and not a consideration for the political contributions he received# n

fact, as a public servant, he ma$ even be called to enact la's that are contrar$ to the interests of his benefactors, for the benefit of the greater good#

n fine, the purpose for 'hich the sums of mone$ 'ere given, 'hich 'as to fund the campaign of Senator

!ngara in his bid for a senatorial seat, cannot be considered as a material consideration so as to negate a

donation#

*ourth ssue

/etitioners raise the fact that since 636 'hen the first "ax Code 'as enacted, up to 6== the B( never

attempted to sub?ect political contributions to donor@s tax# "he$ argue that+# # # t is a familiar principle of la' that prolonged practice b$ the government agenc$ charged 'ith the

execution of a statute, ac)uiesced in and relied upon b$ all concerned over an appreciable period of time, is

an authoritative interpretation thereof, entitled to great 'eight and the highest respect# # # #

"his Court holds that the B( is not precluded from making a ne' interpretation of the la', especiall$

'hen the old interpretation 'as fla'ed# t is a 'ell-entrenched rule that

# # # erroneous application and enforcement of the la' b$ public officers do not block subse)uent correct

application of the statute 4/G:" v# Collector of nternal (evenue, 68 /hil# ;7;5, and that the Dovernment isnever estopped b$ mistake or error on the part of its agents 4/ineda v# Court of *irst nstance of "a$abas,

>2 /hil# =83, =871 Benguet Consolidated Hining Co# v# /ineda, 6= /hil# 7, 7295#

Seventh ssue

/etitioners )uestion the fact that the Court of !ppeals decision is based on a B( ruling, namel$ B(

(uling No# ==-399, 'hich 'as issued after the petitioners 'ere assessed for donor@s tax# "his Court does

not need to delve into this issue# t is immaterial 'hether or not the Court of !ppeals based its decision onthe B( ruling because it is not pivotal in deciding this case# !s discussed above, Section 6 4no' Section

6=5 of the N(C as supplemented b$ the definition of a donation found in !rticle 72> of the Civil Code, is

clear and unambiguous, and needs no further elucidation#

Eighth ssue

/etitioners next contend that tax la's are construed liberall$ in favor of the taxpa$er and strictl$ against the

government# "his rule of construction, ho'ever, does not benefit petitioners because, as stated, there is hereno room for construction since the la' is clear and unambiguous#

Fin*33+, t0is Co)rt t*:es note o6 t0e 6*2t t0*t s)se;)ent to t0e !on*tions invo3ve! in t0is 2*se, Con8ress

*pprove! Rep)3i2 A2t No. ?#'' on Nove/er $, #>>#, provi!in8 in Se2tion #% t0ereo6 t0*t

po3iti2*3e3e2tor*3 2ontri)tions, !)3+ reporte! to t0e Co//ission on E3e2tions, *re not s)5e2t to t0e

p*+/ent o6 *n+ 8i6t t*7 # "his all the more sho's that the political contributions herein made are sub?ect to

the pa$ment of gift taxes, since the same 'ere made prior to the exempting legislation, and (epublic !ct

No# 7;; provides no retroactive effect on this point#

COMMISSIONER OF INTERNAL REVENUE, petitioner, vs. HANTE TRAING CO., INC.,

respon!ent. "G.R. No. #%'>?$. M*r20 %#, --$.

: E C S 0 N

C!GGE<0, S(#, < p+

"he !ntecedents

"he respondent is a corporation dul$ organi%ed and existing under the la's of the /hilippines# Being

engaged in the sale of plastic products, it imports s$nthetic resin and other chemicals for the manufacture of

its products# *or this purpose, it is re)uired to file an mport Entr$ and nternal (evenue :eclaration

4Consumption Entr$5 'ith the Bureau of Customs under Section 38 of the "ariff and Customs Code#

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 12/53

Sometime in 0ctober 6=6, Gt# icente !moto, !cting Chief of Counter-ntelligence :ivision of the

Economic ntelligence and nvestigation Bureau 4EB5, received confidential information that the

respondent had imported s$nthetic resin amounting to />,>66,8=#88 but onl$ declared /9>,>3=,;69#>7#

!ccording to the informer, based on photocopies of 77 Consumption Entries furnished b$ another informer,

the 6=7 importations of the respondent 'ere understated in its accounting records# !moto submitted areport to the EB Commissioner recommending that an inventor$ audit of the respondent be conducted b$

the nternal n)uir$ and /rosecution 0ffice 4/05 of the EB#

!cting on the said report, <ose "# !lmonte, then Commissioner of the EB, issued Hission 0rder No# 36=-

=6 ; dated November 9, 6=6 for the audit and investigation of the importations of &antex for 6=7# "he

/0 issued subpoena duces tecum and ad testificandum for the president and general manager of the

respondent to appear in a hearing and bring the follo'ing+

# Books of !ccounts for the $ear 6=71

2# (ecord of mportations of S$nthetic (esin and Calcium Carbonate for the $ear 6=71

3# ncome tax returns K attachments for 6=71 and

9# (ecord of tax pa$ments#

&o'ever, the respondent@s president and general manager refused to compl$ 'ith the subpoena, contending

that its books of accounts and records of importation of s$nthetic resin and calcium bicarbonate had been

investigated repeatedl$ b$ the Bureau of nternal (evenue 4B(5 on prior occasions# "he /0 explainedthat despite such previous investigations, the EB 'as still authori%ed to conduct an investigation pursuant

to Section 2;-! of Executive 0rder No# 27# Still, the respondent refused to compl$ 'ith the subpoenaissued b$ the /0# "he latter forth'ith secured certified copies of the /rofit and Goss Statements for 6=7

filed b$ the respondent 'ith the Securities and Exchange Commission 4SEC5# &o'ever, the /0 failed to

secure certified copies of the respondent@s 6=7 Consumption Entries from the Bureau of Customs since,

according to the custodian thereof, the original copies had been eaten b$ termites#

n a Getter dated <une 2=, 668, the /0 re)uested the Chief of the Collection :ivision, Hanila

nternational Container /ort, and the !cting Chief of the Collection :ivision, /ort of Hanila, to

authenticate the machine copies of the import entries supplied b$ the informer# &o'ever, Chief of theCollection :ivision Herlita :# "omas could not do so because the Collection :ivision did not have the

original copies of the entries# nstead, she 'rote the /0 that, as gleaned from the records, the follo'ing

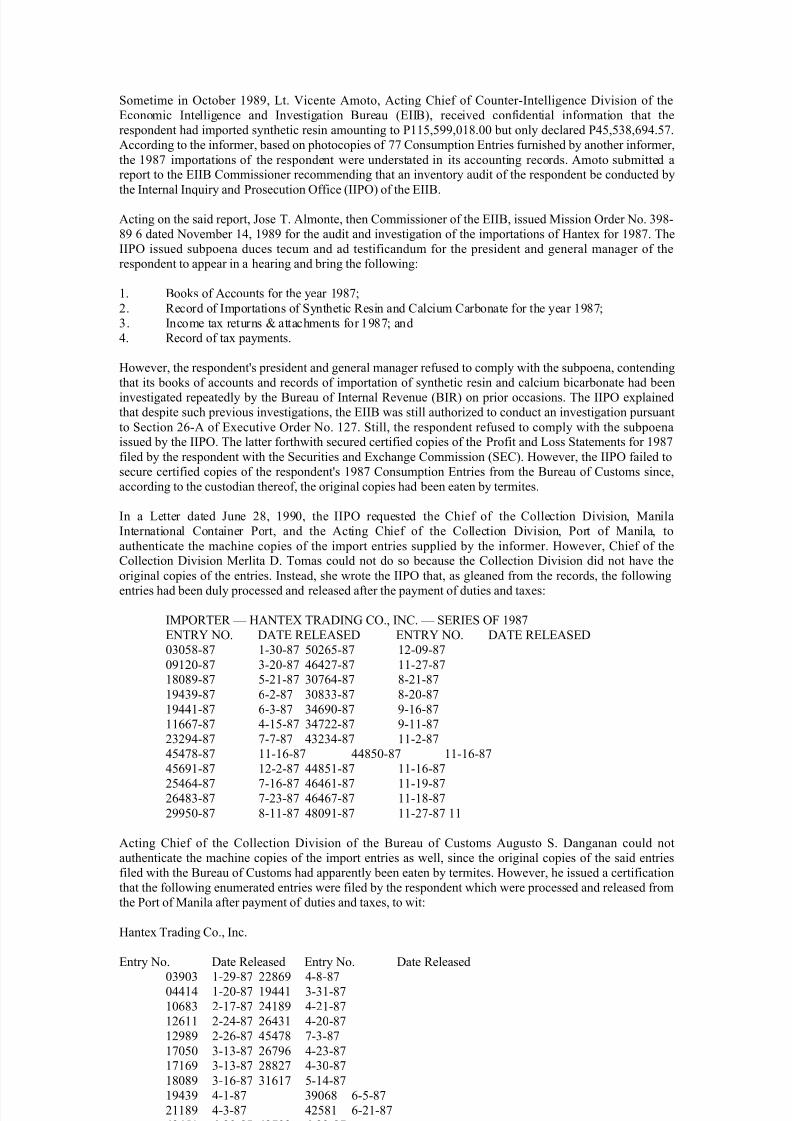

entries had been dul$ processed and released after the pa$ment of duties and taxes+

H/0("E( — &!N"EL "(!:ND C0#, NC# — SE(ES 0* 6=7

EN"(M N0# :!"E (EGE!SE: EN"(M N0# :!"E (EGE!SE:

838>=-=7 -38-=7 >82;>-=7 2-86-=7

8628-=7 3-28-=7 9;927-=7 -27-=7=8=6-=7 >-2-=7 387;9-=7 =-2-=7

6936-=7 ;-2-=7 38=33-=7 =-28-=7

699-=7 ;-3-=7 39;68-=7 6-;-=7

;;7-=7 9->-=7 39722-=7 6--=7

23269-=7 7-7-=7 93239-=7 -2-=7

9>97=-=7 -;-=7 99=>8-=7 -;-=7

9>;6-=7 2-2-=7 99=>-=7 -;-=7

2>9;9-=7 7-;-=7 9;9;-=7 -6-=72;9=3-=7 7-23-=7 9;9;7-=7 -=-=7

266>8-=7 =--=7 9=86-=7 -27-=7

!cting Chief of the Collection :ivision of the Bureau of Customs !ugusto S# :anganan could not

authenticate the machine copies of the import entries as 'ell, since the original copies of the said entries

filed 'ith the Bureau of Customs had apparentl$ been eaten b$ termites# &o'ever, he issued a certification

that the follo'ing enumerated entries 'ere filed b$ the respondent 'hich 'ere processed and released from

the /ort of Hanila after pa$ment of duties and taxes, to 'it+

&antex "rading Co#, nc#

Entr$ No# :ate (eleased Entr$ No# :ate (eleased

83683 -26-=7 22=;6 9-=-=78999 -28-=7 699 3-3-=7

8;=3 2-7-=7 29=6 9-2-=7

2; 2-29-=7 2;93 9-28-=7

26=6 2-2;-=7 9>97= 7-3-=7

78>8 3-3-=7 2;76; 9-23-=77;6 3-3-=7 2==27 9-38-=7

=8=6 3-;-=7 3;7 >-9-=7

6936 9--=7 368;= ;->-=7

2=6 9-3-=7 92>= ;-2-=7

939> ;-26-=7 92763 ;-23-=7

9276> ;-23-=7 9>977 7-3-=7

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 13/53

3>>=2 not received =>=38 -3-=7

9>;6 7-3-=7 =;;>8 not received

9;=7 7-=-=7 =7;97 -=-=7

9;927 7-3-=7 ===26 -23-=7

>7;;6 =-2-=7 62263 2-3-=7;297 =-2=-=7 63262 2-7-=7

;3=7 6-2-=7 6;3>7 2-;-=7;;=>6 6->-=7 6;=22 2->-=7

;7=68 6-7-=7 6==23 not received

;=> 6->-=7 6692= 2-2=-=7

;6679 6-29-=7 66926 2-2=-=7

7223 8-2-=7 6699 2-2=-=7

77;== 8-;-=7 898; ->-=7=92>3 -8-=7 8987 -=-=7

=>>39 --=7 83= -6-=7 2

Bienvenido D# *lores, Chief of the nvestigation :ivision, and Gt# Geo :ionela, Gt# icente !moto and Gt#

(olando Datmaitan conducted an investigation# "he$ relied on the certified copies of the respondent@s

/rofit and Goss Statement for 6=7 and 6== on file 'ith the SEC, the machine copies of the Consumption

Entries, Series of 6=7, submitted b$ the informer, as 'ell as excerpts from the entries certified b$ "omas

and :anganan#

Based on the documentsrecords on hand, inclusive of the machine copies of the Consumption Entries, theEB found that for 6=7, the respondent had importations totaling /8>,7;,>27#88 4inclusive of advance

sales tax5# Compared 'ith the declared sales based on the /rofit and Goss Statements filed 'ith the SEC,

the respondent had unreported sales in the amount of /;3,832,6=6#7, and its corresponding income tax

liabilit$ 'as /9,6;,637#7=, inclusive of penalt$ charge and interests#

EB Commissioner !lmonte transmitted the entire docket of the case to the B( and recommended the

collection of the total tax assessment from the respondent#

0n *ebruar$ 2, 66, :eput$ Commissioner :eoferio, <r# issued a Hemorandum to the B( !ssistant

Commissioner for Special 0perations Service, directing the latter to prepare a conference letter advising the

respondent of its deficienc$ taxes#

Hean'hile, as ordered b$ the (egional :irector, (evenue Enforcement 0fficers Saturnino :# "orres and

ilson *ilamor conducted an investigation on the 6=7 importations of the respondent, in the light of the

records elevated b$ the EB to the B(, inclusive of the photocopies of the Consumption Entries# "he$

'ere to ascertain the respondent@s liabilit$ for deficienc$ sales and income taxes for 6=7, if an$# /er"orres@ and *ilamor@s (eport dated Harch ;, 66 'hich 'as based on the report of the EB and the

documentsrecords appended thereto, there 'as a prima facie case of fraud against the respondent in filing

its 6=7 Consumption Entr$ reports 'ith the Bureau of Customs# "he$ found that the respondent had

unrecorded importation in the total amount of /78,;;,;69#88, and that the amount 'as not declared in its

income tax return for 6=7# "he :istrict (evenue 0fficer and the (egional :irector of the B( concurred

'ith the report#

Based on the said report, the !cting Chief of the Special nvestigation Branch 'rote the respondent andinvited its representative to a conference at 8+88 a#m# of Harch 9, 66 to discuss its deficienc$ internal

revenue taxes and to present 'hatever documentar$ and other evidence to refute the same# ; !ppended tothe letter 'as a computation of the deficienc$ income and sales tax due from the respondent, inclusive of

increments+

B# Computations+

# Cost of Sales (atio !2! =>#962623J

2# Fndeclared Sales — mported !3B 8,876,96#;

3# Fndeclared Dross /rofit B2-!3 >,6;6,3;#;

C# :eficienc$ "axes :ue+

# :eficienc$ ncome "ax B3 x 3>J >,>=6,2;#88

>8J Surcharge C x >8J 2,769,;38#>8

nterest to 22=6 C x >7#>J 3,23,=2>#8=

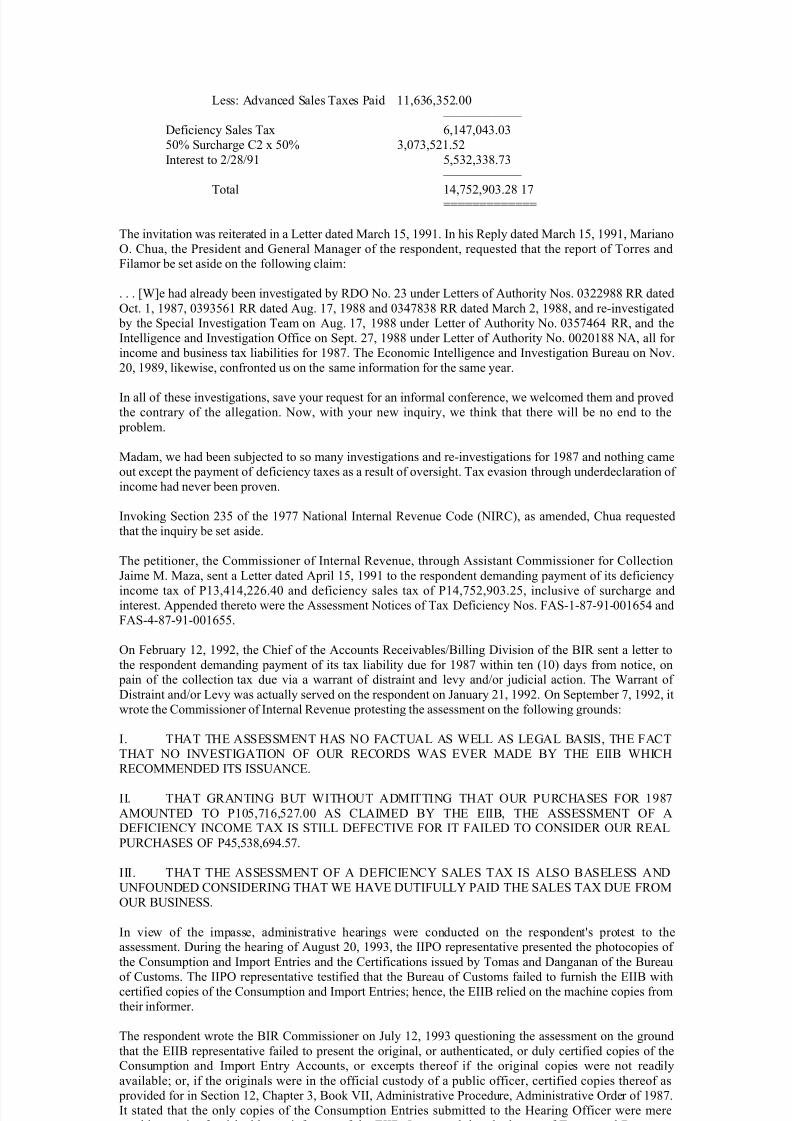

"otal ,>67,=2>#>=2# :eficienc$ Sales "ax

at 8J 7,268,8=2#72

at 28J 8,963,32#3

"otal :ue 7,7=3,36>#83

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 14/53

Gess+ !dvanced Sales "axes /aid ,;3;,3>2#88

:eficienc$ Sales "ax ;,97,893#83

>8J Surcharge C2 x >8J 3,873,>2#>2

nterest to 22=6 >,>32,33=#73

"otal 9,7>2,683#2= 7OOOOOOOOOOOOO

"he invitation 'as reiterated in a Getter dated Harch >, 66# n his (epl$ dated Harch >, 66, Hariano

0# Chua, the /resident and Deneral Hanager of the respondent, re)uested that the report of "orres and

*ilamor be set aside on the follo'ing claim+

# # # .e had alread$ been investigated b$ (:0 No# 23 under Getters of !uthorit$ Nos# 83226== (( dated

0ct# , 6=7, 8363>; (( dated !ug# 7, 6== and 8397=3= (( dated Harch 2, 6==, and re-investigated

b$ the Special nvestigation "eam on !ug# 7, 6== under Getter of !uthorit$ No# 83>79;9 ((, and the

ntelligence and nvestigation 0ffice on Sept# 27, 6== under Getter of !uthorit$ No# 8828== N!, all for

income and business tax liabilities for 6=7# "he Economic ntelligence and nvestigation Bureau on Nov#

28, 6=6, like'ise, confronted us on the same information for the same $ear#

n all of these investigations, save $our re)uest for an informal conference, 'e 'elcomed them and provedthe contrar$ of the allegation# No', 'ith $our ne' in)uir$, 'e think that there 'ill be no end to the

problem#

Hadam, 'e had been sub?ected to so man$ investigations and re-investigations for 6=7 and nothing came

out except the pa$ment of deficienc$ taxes as a result of oversight# "ax evasion through underdeclaration of

income had never been proven#

nvoking Section 23> of the 677 National nternal (evenue Code 4N(C5, as amended, Chua re)uested

that the in)uir$ be set aside#

"he petitioner, the Commissioner of nternal (evenue, through !ssistant Commissioner for Collection

<aime H# Ha%a, sent a Getter dated !pril >, 66 to the respondent demanding pa$ment of its deficienc$

income tax of /3,99,22;#98 and deficienc$ sales tax of /9,7>2,683#2>, inclusive of surcharge andinterest# !ppended thereto 'ere the !ssessment Notices of "ax :eficienc$ Nos# *!S--=7-6-88;>9 and

*!S-9-=7-6-88;>>#

0n *ebruar$ 2, 662, the Chief of the !ccounts (eceivablesBilling :ivision of the B( sent a letter to

the respondent demanding pa$ment of its tax liabilit$ due for 6=7 'ithin ten 485 da$s from notice, on pain of the collection tax due via a 'arrant of distraint and lev$ andor ?udicial action# "he arrant of

:istraint andor Gev$ 'as actuall$ served on the respondent on <anuar$ 2, 662# 0n September 7, 662, it

'rote the Commissioner of nternal (evenue protesting the assessment on the follo'ing grounds+

# "&!" "&E !SSESSHEN" &!S N0 *!C"F!G !S EGG !S GED!G B!SS, "&E *!C"

"&!" N0 NES"D!"0N 0* 0F( (EC0(:S !S EE( H!:E BM "&E EB &C&

(EC0HHEN:E: "S SSF!NCE#

# "&!" D(!N"ND BF" "&0F" !:H""ND "&!" 0F( /F(C&!SES *0( 6=7

!H0FN"E: "0 /8>,7;,>27#88 !S CG!HE: BM "&E EB, "&E !SSESSHEN" 0* !:E*CENCM NC0HE "!L S S"GG :E*EC"E *0( " *!GE: "0 C0NS:E( 0F( (E!G

/F(C&!SES 0* /9>,>3=,;69#>7#

# "&!" "&E !SSESSHEN" 0* ! :E*CENCM S!GES "!L S !GS0 B!SEGESS !N:

FN*0FN:E: C0NS:E(ND "&!" E &!E :F"*FGGM /!: "&E S!GES "!L :FE *(0H

0F( BFSNESS#

n vie' of the impasse, administrative hearings 'ere conducted on the respondent@s protest to theassessment# :uring the hearing of !ugust 28, 663, the /0 representative presented the photocopies of

the Consumption and mport Entries and the Certifications issued b$ "omas and :anganan of the Bureau

of Customs# "he /0 representative testified that the Bureau of Customs failed to furnish the EB 'ithcertified copies of the Consumption and mport Entries1 hence, the EB relied on the machine copies from

their informer#

"he respondent 'rote the B( Commissioner on <ul$ 2, 663 )uestioning the assessment on the ground

that the EB representative failed to present the original, or authenticated, or dul$ certified copies of theConsumption and mport Entr$ !ccounts, or excerpts thereof if the original copies 'ere not readil$

available1 or, if the originals 'ere in the official custod$ of a public officer, certified copies thereof as

provided for in Section 2, Chapter 3, Book , !dministrative /rocedure, !dministrative 0rder of 6=7#

t stated that the onl$ copies of the Consumption Entries submitted to the &earing 0fficer 'ere mere

machine copies furnished b$ an informer of the EB# t asserted that the letters of "omas and :anganan

'ere unreliable because of the follo'ing+

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 15/53

n the said letters, the t'o collection officers merel$ submitted a listing of alleged import entr$ numbers

and dates released of alleged importations b$ &antex "rading Co#, nc# of merchandise in 6=7, for 'hich

the$ certified that the corresponding duties and taxes 'ere paid after being processed in their offices# n

said letters, no amounts of the landed costs and advance sales tax and duties 'ere stated, and no particularsof the duties and taxes paid per import entr$ document 'as presented#

"he contents of the t'o letters failed to indicate the particulars of the importations per entr$ number, and

the said letters do not constitute as evidence of the amounts of importations of &antex "rading Co#, nc# in

6=7#

"he respondent cited the follo'ing findings of the &earing 0fficer+

# # # ".hat the import entr$ documents do not constitute evidence onl$ indicate that the tax assessments in

)uestion have no factual basis, and must, at this point in time, be 'ithdra'n and cancelled# !n$ ne'

findings b$ the /0 representative 'ho attended the hearing could not be used as evidence in this hearing,

because all the issues on the tax assessments in )uestion have alread$ been raised b$ the herein taxpa$er#

"he respondent re)uested ane' that the income tax deficienc$ assessment and the sales tax deficienc$

assessment be set aside for lack of factual and legal basis#

"he B( Commissioner 38 'rote the respondent on :ecember 8, 663, den$ing its letter-re)uest for the

dismissal of the assessments# 3 "he B( Commissioner admitted, in the said letter, the possibilit$ that thefigures appearing in the photocopies of the Consumption Entries had been tampered 'ith# She averred,

ho'ever, that she 'as not proscribed from rel$ing on other admissible evidence, namel$, the Getters of

"orres and *ilamor dated !ugust 7 and 22, 668 on their investigation of the respondent@s tax liabilit$# "he

Commissioner emphasi%ed that her decision 'as final#

"he respondent forth'ith filed a petition for revie' in the C"! of the Commissioner@s *inal !ssessment

Getter dated :ecember 8, 663 on the follo'ing grounds+

*irst# "he alleged 6=7 deficienc$ income tax assessment 4including increments5 and the alleged 6=7

deficienc$ sales tax assessment 4including increments5 are void ab initio, since under Sections ;4a5 and

964b5 of the "ax Code, the Commissioner shall examine a return after it is filed and, thereafter, assess thecorrect amount of tax# "he follo'ing facts obtaining in this case, ho'ever, are indicative of the

incorrectness of the tax assessments in )uestion+ the deficienc$ interests imposed in the income and

percentage tax deficienc$ assessment notices 'ere computed in violation of the provisions of Section

2964b5 of the N(C of 677, as amended1 the percentage tax deficienc$ 'as computed on an annual basis

for the $ear 6=7 in accordance 'ith the provision of Section 63, 'hich should have been computed inaccordance 'ith Section ;2 of the 677 N(C, as amended b$ /res# :ecree No# 669 on a )uarterl$ basis1

and the B( official 'ho signed the deficienc$ tax assessments 'as the !ssistant Commissioner for

Collection, 'ho had no authorit$ to sign the same under the N(C#

Second# Even granting arguendo that the deficienc$ taxes and increments for 6=7 against the respondent

'ere correctl$ computed in accordance 'ith the provisions of the "ax Code, the facts indicate that the

above-stated assessments 'ere based on alleged documents 'hich are inadmissible in either administrative

or ?udicial proceedings# Horeover, the alleged bases of the tax computations 'ere anchored on mere presumptions and not on actual facts# "he alleged undeclared purchases for 6=7 'ere based on mere

photocopies of alleged import entr$ documents, not the original ones, and 'hich had never been dul$certified b$ the public officer charged 'ith the custod$ of such records in the Bureau of Customs#

!ccording to the respondent, the alleged undeclared sales 'ere computed based on mere presumptions as

to the alleged gross profit contained in its 6=7 financial statement# Horeover, even the alleged financial

statement of the respondent 'as a mere machine cop$ and not an official cop$ of the 6=7 income and

business tax returns# *inall$, the respondent 'as follo'ing the accrual method of accounting in 6=7, $et,

the B( investigator 'ho computed the 6=7 income tax deficienc$ failed to allo' as a deductible item the

alleged sales tax deficienc$ for 6=7 as provided for under Section 384c5 of the N(C of 6=;#

"he Commissioner did not adduce in evidence the original or certified true copies of the 6=7 Consumption

Entries on file 'ith the Commission on !udit# nstead, she offered in evidence as proof of the contents

thereof, the photocopies of the Consumption Entries 'hich the respondent ob?ected to for beinginadmissible in evidence# She also failed to present an$ 'itness to prove the correct amount of tax due from

it# Nevertheless, the C"! provisionall$ admitted the said documents in evidence, sub?ect to its final

evaluation of their relevanc$ and probative 'eight to the issues involved#

0n :ecember , 667, the C"! rendered a decision, the dispositive portion of 'hich reads+

N "&E GD&" 0* !GG "&E *0(ED0ND, ?udgment is hereb$ rendered :ENMND the herein petition#

/etitioner is hereb$ 0(:E(E: "0 /!M the respondent Commissioner of nternal (evenue its deficienc$

income and sales taxes for the $ear 6=7 in the amounts of /,=2,3>8#2; and /2,;;8,3=2#9;,

respectivel$, plus 28J delin)uenc$ interest per annum on both deficienc$ taxes from !pril >, 66 until

full$ paid pursuant to Section 2=34c5435 of the 6=7 "ax Code, 'ith costs against the petitioner#

8/13/2019 Taxation Cases 2005

http://slidepdf.com/reader/full/taxation-cases-2005 16/53

S0 0(:E(E:#

"he C"! ruled that the respondent 'as burdened to prove not onl$ that the assessment 'as erroneous, but

also to adduce the correct taxes to be paid b$ it# "he C"! declared that the respondent failed to prove thecorrect amount of taxes due to the B(# t also ruled that the respondent 'as burdened to adduce in

evidence a certification from the Bureau of Customs that the Consumption Entries in )uestion did not belong to it#

0n appeal, the C! granted the petition and reversed the decision of the C"!# "he dispositive portion of the

decision reads+

*0(ED0ND /(EHSES C0NS:E(E:, the /etition for (evie' is D(!N"E: and the :ecember ,667 decision of the C"! in C"! Case No# >;2 affirming the 6=7 deficienc$ income and sales tax

assessments and the increments thereof, issued b$ the B( is hereb$ (EE(SE:# No costs#

"he (uling of the Court of !ppeals

The CA held that the income and sales tax deficiency assessments issued by the petitioner were unlawful

and baseless since the copies of the import entries relied upon in computing the deficiency tax of the

respondent were not duly authenticated by the public officer charged with their custody, nor verified underoath by the !!" and the "!# investigators$ The CA also noted that the public officer charged with the

custody of the import entries was never presented in court to lend credence to the alleged loss of theoriginals$ The CA pointed out that an import entry is a public document which falls within the provisions of

%ection &', #ule &() of the #ules of Court, and to be admissible for any legal purpose, %ection )*, #ule

&() of the #ules of Court should apply$ Citin8 t0e r)3in8 o6 t0is Co)rt in Co33e2tor o6 Intern*3 Reven)e v.

<enip*+o, t0e CA r)3e! t0*t t0e *ssess/ents 4ere )n3*46)3 e2*)se t0e+ 4ere *se! on 0e*rs*+

evi!en2e. The CA also ruled that the respondent was deprived of its right to due process of law$

"he C! added that the C"! should not have ?ust brushed aside the legal re)uisites provided for under the

pertinent provisions of the (ules of Court in the matter of the admissibilit$ of public documents,considering that substantive rules of evidence should not be disregarded# t also ruled that the certifications

made b$ the t'o Customs Collection Chiefs under the guise of supporting the respondent@s alleged tax

deficienc$ assessments invoking the best evidence obtainable rule under the "ax Code should not be permitted to supplant the best evidence rule under Section 7, (ule 38 of the (ules of Court#

*inall$, the C! noted that the tax deficienc$ assessments 'ere computed 'ithout the tax returns# "he C!

opined that the use of the tax returns is indispensable in the computation of a tax deficienc$1 hence, this

essential re)uirement must be complied 'ith in the preparation and issuance of valid tax deficienc$assessments#

"he /resent /etition

"he Commissioner of nternal (evenue, the petitioner herein, filed the present petition for revie' under

(ule 9> of the (ules of Court for the reversal of the decision of the C! and for the reinstatement of theruling of the C"!#

!s gleaned from the pleadings of the parties, the threshold issues for resolution are the follo'ing+ 4a5