Embed Size (px)

Citation preview

TAXATION BULLETINBUDGET & REVENUE MEASURES 2014/2015

An independent member of UHY InternationalYour Business Our Focus

CONTENTS

1 – Jamaica 2013/14 Budget Highlights

32 – Top 5 Ministries base on Budget Allocation

3 – PROVISION FOR INFRASTRUCTURAL DEVELOPMENT4 – ECONOMIC REFORM PROGRAMME5 – REVENUE MEASURES APPENDICES:

4

59

10

Your Business Our Focus

1 – JAMAICA 2014/15BUDGET HIGHLIGHTS

The Hon. Peter Phillips, Minister of Finance & Planning presented to Parliament the

Government’s plan to fund the 2014-15 Expenditure Budget of J$539.3 billion.

He noted that the budget for FY 2014/2015 is consistent with the targets set

under the extended fund facility EFF negotiated with the IMF and that Expenditure has to be controlled and kept in line with the country's ability to fund government's operations.

In his presentation he identified the following as essential for growth:

easy access to affordable credit,'

efficient ,facilitative government institutions supportive of investments;

a legal system that resolves disputes impartiallyand speedily; and,

a society which will view positively and reward those who achieve successful

business investments.

Expenditure Summary

Your Business Our Focus

Recurrent Expenditure(Government of

Projects)

Multi/BilateralProjects)

Total Capital(Recurrent and Capital

)

Expenditure Summary

Total Expenditure (Recurrent and Capital )

Total Capital Expenditure (A +B)

CAPITAL B (Funded by Multi/Bilateral Projects)

CAPITAL A (Government of Jamaica Funded Projects)

Recurrent Expenditure

J$- J$200,000,000,000.00 J$400,000,000,000.00 J$600,000,000,000.00

C

APITAL

A

CAPIT

AL B

(Fund

ed by

Total

Expen

diture

Jamaica Funded Expenditure (A +B)

2013/2014 J$358,371,026,000.00 J$120,076,055,000.00 J$22,262,746,000.00 J$142,338,801,000.00 J$500,709,827,000.00

2014/2015 J$404,654,188,000.00 J$109,258,039,000.00 J$25,440,043,000.00 J$134,698,082,000.00 J$539,352,270,000.00

2 – T O P 5 M IN IS T R I E S B A S E

O N B U D G E T A L L OCA T I ON

TO P 5 M IN IST R IESJ$600,000,000,000.00

J$500,000,000,000.00J$400,000,000,000.00J$300,000,000,000.00J$200,000,000,000.00J$100,000,000,000.00

J$-

RECURRENT CAPITAL A CAPITAL B TOTAL

The Ministry of Finance to the 2014/2015 Budget Allocation accounting for J$267.6 Billion of the Total Budgetof J$539.3 Billion. Debt Servicing represents J$233 Billion of the J$267.6 Billion granted to the Ministry ofFinance.

Your Business Our Focus

TOTALMinistries Total Estimates for FY 2014/2015

Ministry of Finance J$ 267,613,863,000.00Ministry of Education J$ 80,364,693,000.00

Ministry of Health J$ 35,674,344,000.00Ministry of National Security J$ 16,542,831,000.00Ministry of Transport, Works and Housing J$ 16,527,918,000.00OTHER MINISTRIES J$ 122,628,621,000.00

Total J$ 539,352,270,000.00

3 – P R O V I S I O N

F O R I N F R A S T R U C T

U R A L D E V E L O P M E

N TCentral Government Capital Budget

• Over $8bn or approximately 23% of the Central Government Capital Budget has been reserved forinfrastructural works to be carried out through the Ministry of Transport Housing and Works during2014/2015. Some of the major projects which will be undertaken include:

$4bn for the Major Infrastructural Project (MIDP)funded by China EXIM Bank to undertakereconstruction of bridges; commence rehabilitation of main roads and through the JEEP, to repairworks on community roads, retaining walls and drainage structures.

$1.7bn for The Jamaica Economical Housing Project to complete works in St Ann and LuanaGardens in St Elizabeth;

$689.7m complete the drainage rehabilitation works remaining on the Sandy Gully under theKingston Metropolitan Area Drainage Project

$689.73m to the Transportation Infrastructure Project to complete road construction inWestmoreland, Hanover, St Thomas, and St Catherine

$494m to the Road Rehabilitation Project, to commence road construction works inClarendon

$273m to the Road Improvement Programme, to undertake maintenance of the North CoastHighway and upgrade of traffic signals at select intersections

Your Business Our Focus

3 – P R O V I S I O N F O R

I N F R A S T R U C T U

R A L D E V E L O P M

E N TPUBLIC BODIES CAPITAL BUDGET

The Capital Expenditure included in the Central Government's budget will be enhanced by theInvestment and Capital Expenditure of other public bodies.• Investment infrastructure and other capital projects of the public bodies are estimated at $53.9 billion.

ROADS

• Approximately $1.6 billion will be spent on road rehabilitation by the road maintenance fund.

Your Business Our Focus

3 – PROVISION FORINFRASTRUCTURALDEVELOPMENT

HOUSING

• Approximately $26.3 billion will be spent on housing solution by both the NationalHousing Trust (NHT)and the Housing Agency of Jamaica (NAJ).

• The National Housing Trust expenditure of $22.4 billion would result in the creation of7678 new loans;

• 2465 housing starts and 2163 completion.

•In addition to these housing solutions, NHT has provided for $971 billion to support aprogram for special subsidies and grants to facilitate access by contributors in the lower income bracket.

•Housing Agency of Jamaica is expected to spend $2.9billion to work on White Hall- Phasein Westmoreland, Boscobel in St. Mary and Luana Gardens in St. Elizabeth.

3

Your Business Our Focus

3 – PROVISION FORINFRASTRUCTURALDEVELOPMENT

WATER

• The National Water Commission capital programme is estimated at $6.3 billion of which $1. 9billion will be spent on non revenue water relieve stations, pipeline and installation of residential and domestic metres.

• The Rural Water Supply Project will benefit from an expenditure of $1.8 billion.

$0.8 billion will be spent on the PORTMORE Sewage Project and the Tanks and Pump Projectwill get another $1 billion.

Your Business Our Focus

4 – ECONOMIC

PROGRAMMEREFORM

The Economic Reform Programme since last year includes quantitative andb e n c h m a r k s . Some of the legislative achievements includes :

amended the Administration Act to strengthen tax administration by providing,other things, access to third party information and requiring

mandatory e-filing for certain types of tax payers and for certain taxes;

Secured Interest in Personal Property Act to enhance access to credit

especially for non-traditional businesses, such as those in the creative

industries and cultural sector and in agriculture;

Charities Act and harmonized the treatment of Charities across tax types,

in addition to removing ministerial discretion for granting of waivers for

charities and charitable purposes;

Fiscal Incentives Legislation which has lowered the effective tax rate f o r

business o p er at or s

Amendments to the Financial Administration and Audit Act and the Public

Bodies Management Act which strengthened the legally binding

fiscal rules to ensure a sustainable budget balance and debt reduction.

Amendments to the Securities Act to include provisions which seek to

combat the establishment and proliferation of unlawful financial

organizations and implemented a legal and regulatory framework conducive

to the operation of Collective Investment Schemes;

Your Business Our Focus

5 – REVENUEMEASURES

The Government announced revenue measures amounting to J$6.68 Billionfor the Fiscal Year 2014/2015. The details are as follows:

1. Modification of the alcohol regime to unify the Specific SCT on all alcoholicbeverages

a) House Members are being asked to recall that the tax regime for alcoholhas been subject to systematic modification since 2010, when beers and stouts were distinguished from other alcoholic beverages. In 2010, the taxation of alcoholic beverages, with the exception of White Over-proof Rum, was amended from an ad valorem rate of thirty per cent to a specific rate per litre of pure alcohol (l.p.a), with a higher rate being accorded to beers and stouts. At the time the rate for beers and stouts was determined at $1,120 per I.p.a and for all other alcoholic beverages (except White Over proof Rum) at $960 per I.p.a..

b) The regime was subsequently amended in 2012 to provide for WhiteOver-proof rum to be taxed at the rate of $960 per I.p.a,the same rate as other non beer/stout alcoholic beverages.

c) The modified regime at the time also provided for a concessionary ratefor tourism entities, of $450 per I.p.a,which was later supplanted by a rate of $700 per I.p.a in FY2012/2013.

d) Based on Government commitment to provide for a standard rate oftaxation and to reduce any existing anomalies, it is being proposed that a single specific SCT rate based on alcohol content be applied across the board.

e) The recommended rate is $1,120.00per I.p.a.

Estimated

Revenue Gain $0.844 billion. The effective date for implementation

isApril 22, 2014.

Your Business Our Focus

5 – REVENUEMEASURES

2. Increase in the age limit of second sale vehicles on which GCT will beapplicable. Whilst maintaining t h e rates

a) The House is advised that the proposal to increase the age limit of secondhand sale vehicles to which GCT is applicable from eight (8) years to ten(10) years was extensively discussed at the tax sub-committeeParliament and was agreed to by the Parliamentary Committee.

of

b) The current r a t e s , which were i n i t i a l l y a m e n d e d in FY 2012/2013,outlined in Table I will remain unchanged.

as

Table I: GCT Rates to be Retained for Second Sale Vehicles.To be applicable to Vehicles ten (10) years and under

Motor CarsMotors

Motors

Motors

Cars (cc rating

Cars (cc rating

Cars (cc rating

0 - 1999 cc)

2000 cc - 2999 cc)

3000 & upwards)

$10,000.00

$15,000.00

$20,000.00

Motor Trucks (cwt)

Trucks - 0 - 30

Trucks - 31-60

Trucks above 61 and up

$10,000.00

$10,000.00

$25,000.00

Estimated Revenue Gain $0.026 billion. The effective date for implementation isApril I, 2014.

11

5 – REVENUEMEASURES

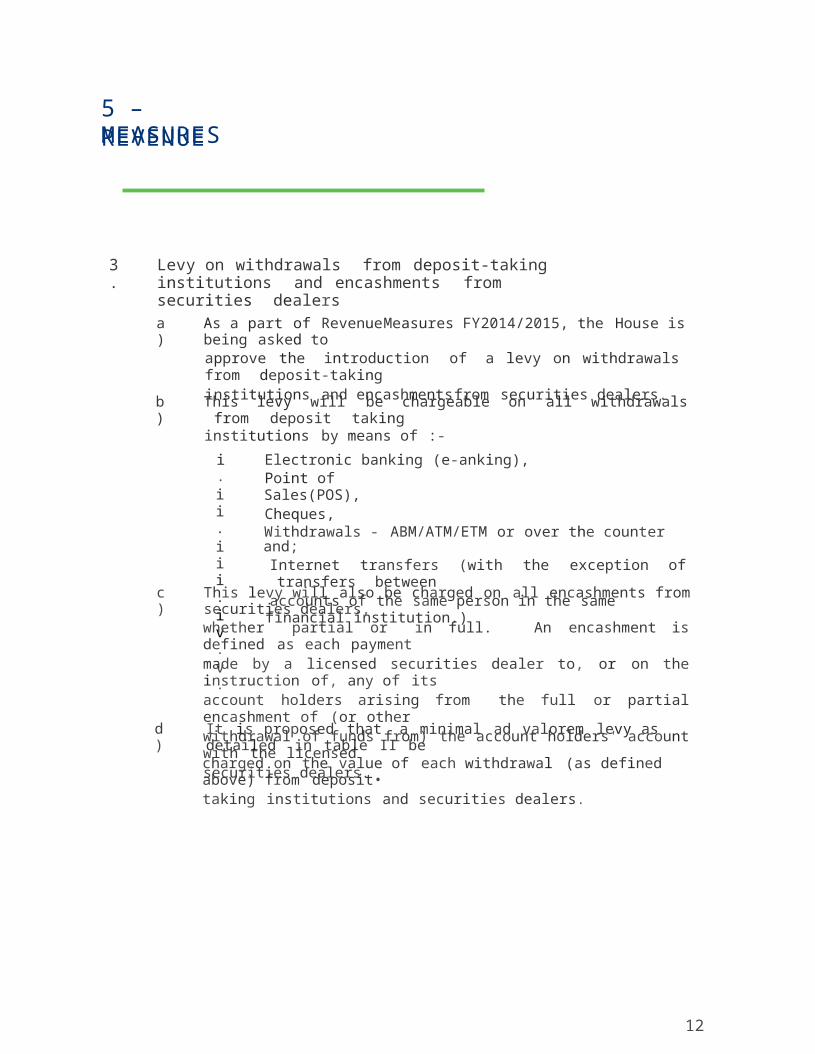

3. Levy on withdrawals from deposit-taking institutions and encashments fromsecurities dealers

a) As a part of RevenueMeasures FY2014/2015, the House is being asked toapprove the introduction of a levy on withdrawals from deposit-taking institutions and encashmentsfrom securities dealers.b) This levy will be chargeable on all withdrawals from deposit takinginstitutions by means of :-

i.ii. iii. iv. v.

Electronic banking (e-anking),Point of Sales(POS), Cheques,Withdrawals - ABM/ATM/ETM or over the counter and;Internet transfers (with the exception of transfers

between accounts of the same person in the same financial institution.)

c) This levy will also be charged on all encashments from securities dealers,whether partial or in full. An encashment is defined as each payment made by a licensed securities dealer to, or on the instruction of, any of its account holders arising from the full or partial encashment of (or other withdrawal of funds from) the account holders' account with the licensed securities dealers.d) It is proposed that a minimal ad valorem levy as detailed in table II becharged on the value of each withdrawal (as defined above) from deposit•taking institutions and securities dealers.

12

5 – REVENUEMEASURES

Table D: Levy Rates on Withdrawals from depositsecurities dealers

Value of Transaction

taking Institutions and

Levy Rate

Less than One (1) Million Dollars

0.1%

One (1) Million to Five (5) Million Dollars 0.09%

Greater than Five (5) Million - Less thanDollars

Twenty (20) Million 0.075%

Greater than Twenty (20) Million Dollars 0.05%

e) The House is being asked to note that for withdrawals of $1,000; $5000

and $10,000 the associated tax payable would be $1.00, $5.00 and $10.00 respectively.The House is advised that a similar tax has been introduced in a numberof countries. Included in this listing are Argentina, Brazil, Peru, andColumbia.

f)

g) The tax will be collected by the financial institutions and paid over on amonthly basis to the Tax Administration Jamaica. The financial institutions will be required to file the requisite returns to Tax Administration Jamaica (TAJ) and report to the relevant regulator, detailing the value and volume of the these transactions.

Estimated Revenue Gain $2.25 billion. The effective date for implementationis June 1, 2014.

13

5 – REVENUEMEASURES

4. Increase in premium tax for regionalized and non-regionalized LifeAssurance companies

a) The House is advised that regionalized and non-regionalized LifeAssurance companies are required to pay as per Section 48 of the Income Tax Act a rate of 3.0 and 4.0 per cent, respectively of gross premiums earned per year.

b) The proposal seeks to provide for a unified rate of 5.5%, which wouldresult in an increase by 2.5 and 1.5 percentage points for regionalized and non-regionalized companies respectively.

Estimated Revenue Gain $0.276 billion.The tax will be applicable for theassessment 2014 in relation to the first four months will be charged

remaining eight (8) months of year ofstatutory Income for the said year. The at the old rate of tax. There after the

increased rate will be effective for every subsequent year of assessment.

5. Increase in Investment Tax for insurance companies

a) The House is reminded that throughout the reform initiatives, taxation in

respect to insurance companies have remained unchanged.

b) In the aim of providing for a unified taxation rate, it is being proposedthat this be increased by five percentage points to twenty percent (20%).

Estimated Revenue Gain $0.701 billion.

The tax will be applicable for theassessment 2014 in relation to the first four months will be charged

remaining eight (8) months of year ofstatutory Income for the said year. The at the old rate of tax. There after the

increased rate will be effective for every subsequent year of assessment.

14

5 – REVENUEMEASURES

6. Increase in the Asset Tax

a) The House is advised that the modified asset tax was introduced in FY2012/2013. The following increase is being proposed :-

(1) For the specified entities regulated by the Bank of Jamaica (BOJ)andthe Financial Services Commission (FSC).(i.e. comprising Deposit TakingInstitutions (OTIs),Insurance companies and Security Dealers),the rate of0.14 per cent applied to the taxable value of the assets will be increased to 0.25 per cent.(2) For other entities, the new tax rates to be payable in accordance withthe schedule set out in the table below. The House is being asked to note however that the last two (2) categories, which represent micro and small businesses,the rates remain unchanged. This is also shown in table ill:Table DI: Proposed Rates for "Other

Entities"(not regulated by the BoJ or FSC)Asset Value Annual Tax (J$)

At least $50M 200,000

At least SSM but less than $50M 150,000

100,000At least $500,000 but less than $5M

RATES FOR THE FOLLOWING CATEGORIES REMAIN

At least $50,000 but less than $500,000

UNCHANGED

Less than $50,000

b) The House is advised that the tax remains an annual tax with filing/duedate of March 15. The tax is not allowable as a deduction under theIncome Tax Act.

Estimated Revenue Gain $1.788 billion. The tax is effective as per year ofassessment.

15

5 – REVENUEMEASURES

7. Modification of the duty regime for specified motor vehicles

a) The House is being asked to recall that via Ministry Paper No. 32, duringFY 2012/2013, there was an increase in the rates of select list C items, by ten percentage points in order to meet revenue needs.b) Based on GoJ commitment to rate reduction, the following changes areproposed:-

Reduction of the customs duty (CET)rate by ten percentage

(i)points for vehicles 2000 cc and above, a

to 20%.

reduction from 30%

(ii) Modification of SCT rates by ten percentage points for petrol\ diesel vehicles over 3500 cc and Hybrid vehicles asbelow:-

per Table IV

Table IV: Changes in the SCT Rates (Petrol and Diesel Vehicles) Description of Current Rate

Dealer Rates

30 % (petrol)23 % (diesel)

0%

Proposed RateVehicles

20 % (petrol)13 % (diesel)

10%

Exceeding 3500 cc (Diesel and Petrol)

Hybrid

Individual Rates

40% (petrol)30% (diesel)

0%

30% (petrol)20% (diesel)

10%

Exceeding 3500 cc (Diesel and Petrol)

Hybrid

Estimated Revenue Gain $0.250 billion. The effective date for implementation

is

May 1, 2014.

16

5 – REVENUEMEASURES

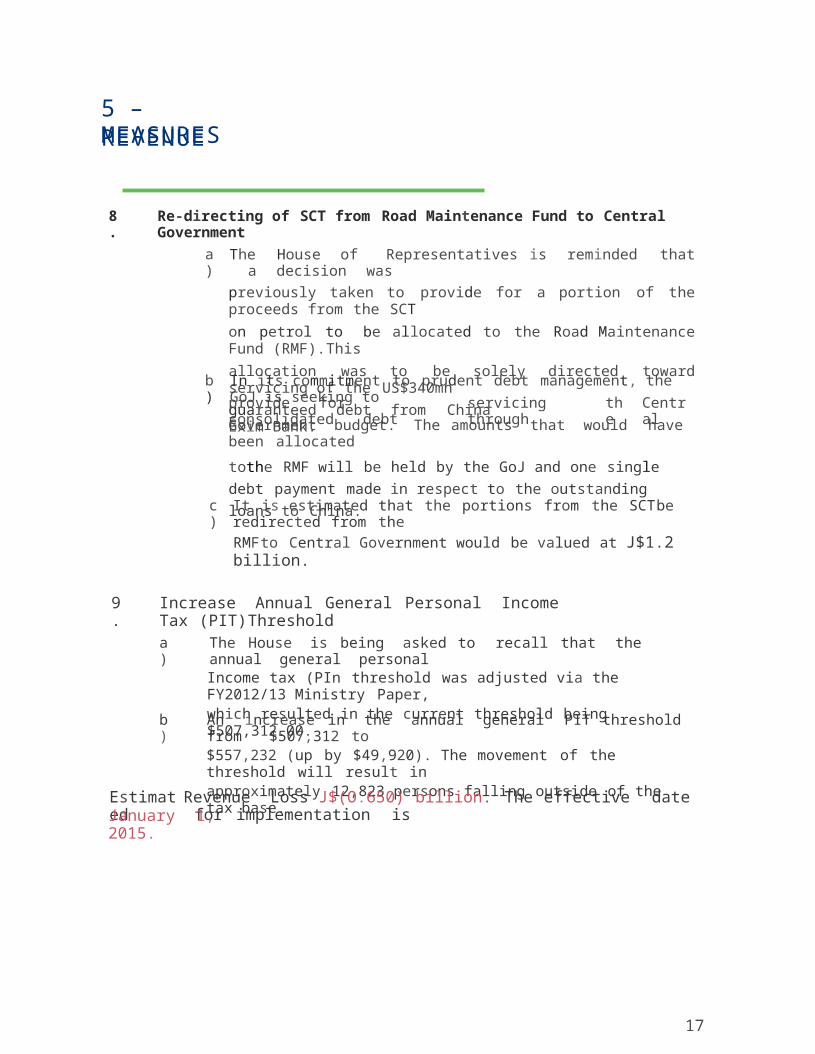

8. Re-directing of SCT from Road Maintenance Fund to Central Government

a) The House of Representatives is reminded that a decision was

previously taken to provide for a portion of the proceeds from the SCT

on petrol to be allocated to the Road Maintenance Fund (RMF).This

allocation was to be solely directed toward servicing of the US$340mn

guaranteed debt from China Exim Bank.

b) In its commitment to prudent debt management, the GoJ is seeking toprovide for consolidated debt servicing through the Central

Government budget. The amounts that would have been allocated

tothe RMF will be held by the GoJ and one single debt payment

made in respect to the outstanding loans to China.

c) It is estimated that the portions from the SCTbe redirected from the

RMFto Central Government would be valued at J$1.2 billion.

9. Increase Annual General Personal Income Tax (PIT)Threshold

a) The House is being asked to recall that the annual general personalIncome tax (PIn threshold was adjusted via the FY2012/13 Ministry Paper, which resulted in the current threshold being $507,312.00.

b) An increase in the annual general PIT threshold from $507,312 to$557,232 (up by $49,920). The movement of the threshold will result in approximately 12,823 persons falling outside of the tax base.Estimated Revenue Loss J$(O.650) billion. The effective date for implementation is

January 1, 2015.

17

5 – REVENUEMEASURES

SUMMARY OF 2014/2015 REVENUE MEASURES

Description of Revenue Measures Revenue Impact

$ BillionModification of the alcohol regime to unify the

Specific SeT on all alcoholic beverages - ($1,120)

Increase in age limit of second salevehicles on which GCTwill be applicable (from 8 to 10 years) levy on withdrawals from deposit-taking institutions and encashmentsfrom securities dealersIncrease in premium tax for regionalized and non- regionalized life Assurancecompanies. (Up to5.5%)

1.

$ 0.844

2.

$ 0.026

3.

$ 2.250

4.

$ 0.276

Investment tax for insurance companies (up to

20%)Increase in Asset TaxModification of duty regime for specified motor vehiclesRedirecting of portion of SCTfrom the Road Maintenance Fund to Central Government Increased Annual GeneralPITThreshold ($557,232)

5.$

$0.701

1.7886.

7.$ 0.250

8.

$ 1.200

$ (0.650)9.

TOTAL $ 6.68Billion

18

6 – APPENDICES:

Recurrent Expenditure Capital A Capital B

Recurrent (Government of

Projects)

CAPITAL B (Funded

Projects)Total Capital

Total Expenditure

Capital )

Expenditure Summary

Total Expenditure (Recurrent and Capital )

Total Capital Expenditure (A +B)

CAPITAL B (Funded by Multi/Bilateral Projects)

CAPITAL A (Government of Jamaica Funded…

Recurrent Expenditure

J$- J$200,000,000,000.00J$400,000,000,000.00J$600,000,000,000.00

CAPITAL A

Expenditure Jamaica Funded by

Multi/Bilateral Expenditure (A

+B) (Recurrent and

2013/2014 J$358,371,026,000. J$120,076,055,000. J$22,262,746,000.0 J$142,338,801,000. J$500,709,827,000.2014/2015 J$404,654,188,000. J$109,258,039,000. J$25,440,043,000.0 J$134,698,082,000. J$539,352,270,000.

2014-2015 Jamaica Budget

5

Head No. and Title StatutoryGross

Expenditure to be Voted

Appropriations in Aid

Net Expenditure to be Voted

Net provisions in Estimates (Including Statutory )

0100 His Excellency the Governor-General andStaff

0200 Houses of Parliament

0300 Office of the Public Defender

0400 Office of the Contractor-General

0500 Auditor General

0600 Office of the Services Commissions

0700 Office of the Children's Advocate

0800 Independent Commission of Investigations

1500 Office of the Prime Minister

1510 Jamaica Information Service

Total Office of the Prime Minister

1600 Office of the Cabinet

1649 Management Institute for National Development

Total Office of the Cabinet

1700 Ministry of Tourism and Entertainment

2000 Ministry of Finance and Planning

2011 Accountant General

2012 Jamaica Customs Agency

2018 Public Debt Servicing (Interest Charges)

2019 Pensions

2056 Tax Administration Jamaica

Total Ministry of Finance and Planning

2600 Ministry of National Security

2622 Police Department

2624 Department of Correctional Services

2653 Passport, Immigration and Citizenship Agency

Total Ministry of National Security

2800 Ministry of Justice

2823 Court of Appeal

2825 Director of Public Prosecutions

2826 Family Courts

2827 Resident Magistrates' Courts

2828 Revenue Court

2829 Supreme Court

2830 Administrator General

2831 Attorney General

105,759.0 64,547.0 - 64,547.0 170,306.0

9,224.0 752,094.0 - 752,094.0 761,318.0

8,537.0 66,916.0 - 66,916.0 75,453.0

8,431.0 220,753.0 - 220,753.0 229,184.0

5,583.0 532,915.0 10,000.0 522,915.0 528,498.0

5,849.0 173,729.0 - 173,729.0 179,578.0

- 99,309.0 - 99,309.0 99,309.0

- 334,258.0 - 334,258.0 334,258.0

-

-

3,021,305.0

383,257.0

416,981.0

62,424.0

2,604,324.0

320,833.0

2,604,324.0

320,833.0

- 3,404,562.0 479,405.0 2,925,157.0 2,925,157.0

-

-

344,607.0

333,428.0

-

194,299.0

344,607.0

139,129.0

344,607.0

139,129.0

- 678,035.0 194,299.0 483,736.0 483,736.0

- 3,764,122.0 2,229,050.0 1,535,072.0 1,535,072.0

-

-

-

132,669,123.0

18,494,432.0

-

32,526,214.0

491,286.0

4,464,953.0

-

6,565,691.0

4,857,756.0

-

-

2,403,953.0

-

-

-

32,526,214.0

491,286.0

2,061,000.0

-

6,565,691.0

4,857,756.0

32,526,214.0

491,286.0

2,061,000.0

132,669,123.0

25,060,123.0

4,857,756.0151,163,555.0 48,905,900.0 2,403,953.0 46,501,947.0 197,665,502.0

-

-

-

-

13,471,229.0

28,942,246.0

4,917,859.0

1,540,081.0

140,000.0

300,000.0

35,000.0

1,224,893.0

13,331,229.0

28,642,246.0

4,882,859.0

315,188.0

13,331,229.0

28,642,246.0

4,882,859.0

315,188.0

- 48,871,415.0 1,699,893.0 47,171,522.0 47,171,522.0

-

97,892.0

6,530.0

-

-

-

374,315.0

-

-

1,033,378.0

75,246.0

263,889.0

186,716.0

1,134,577.0

2,621.0

487,700.0

319,379.0

529,375.0

117,450.0

-

-

-

-

-

-

140,379.0

-

915,928.0

75,246.0

263,889.0

186,716.0

1,134,577.0

2,621.0

487,700.0

179,000.0

529,375.0

915,928.0

173,138.0

270,419.0

186,716.0

1,134,577.0

2,621.0

862,015.0

179,000.0

529,375.0

Statutory provisions and Provisions to be Voted

$’000

Recurrent

2014-2015 Jamaica Budget

6

Head No. and Title StatutoryGross

Expenditure to be Voted

Appropriations in Aid

Net Expenditure to be Voted

Net provisions in Estimates (Including Statutory )

2832 Trustee in Bankruptcy

2833 Office of the Parliamentary Counsel

2852 Legal Reform Department

2854 Court Management Services

Total Ministry of Justice

3000 Ministry of Foreign Affairs and Foreign Trade

4000 Ministry of Labour and Social Security

4100 Ministry of Education

4200 Ministry of Health

4220 Registrar General's Department and IslandRecords Office

4234 Bellevue Hospital

4235 Government Chemist

Total Ministry of Health

4500 Ministry of Youth and Culture

4551 Child Development Agency

Total Ministry of Youth and Culture

5100 Ministry of Agriculture and Fisheries

5300 Ministry of Industry, Investment andCommerce

5338 The Companies Office of Jamaica

Total Ministry of Industry, Investment andCommerce

5600 Ministry of Science, Technology, Energy andMining

5639 Post and Telecommunications Department

Total Ministry of Science, Technology, Energy and Mining

6500 Ministry of Transport, Works and Housing

6550 National Works Agency

Total Ministry of Transport, Works andHousing

6700 Ministry of Water, Land, Environment andClimate Change

6746 Forestry Department

6747 National Land Agency

6748 National Environment and Planning Agency

Total Ministry of Water, Land, Environment and Climate Change

7200 Ministry of Local Government andCommunity Development

Total Recurrent

-

-

-

-

43,647.0

80,708.0

47,537.0

203,407.0

-

-

-

-

43,647.0

80,708.0

47,537.0

203,407.0

43,647.0

80,708.0

47,537.0

203,407.0

478,737.0 4,408,180.0 257,829.0 4,150,351.0 4,629,088.0

- 3,137,002.0 136,653.0 3,000,349.0 3,000,349.0

- 2,872,746.0 610,000.0 2,262,746.0 2,262,746.0

- 78,742,324.0 450,000.0 78,292,324.0 78,292,324.0

-

-

-

-

34,971,273.0

753,519.0

1,174,686.0

28,479.0

200,352.0

753,519.0

-

-

34,770,921.0

-

1,174,686.0

28,479.0

34,770,921.0

-

1,174,686.0

28,479.0

- 36,927,957.0 953,871.0 35,974,086.0 35,974,086.0

-

-

1,817,413.0

1,847,732.0

18,413.0

1,860.0

1,799,000.0

1,845,872.0

1,799,000.0

1,845,872.0

- 3,665,145.0 20,273.0 3,644,872.0 3,644,872.0

- 4,442,647.0 914,432.0 3,528,215.0 3,528,215.0

-

-

1,839,065.0

330,140.0

74,607.0

330,140.0

1,764,458.0

-

1,764,458.0

-

- 2,169,205.0 404,747.0 1,764,458.0 1,764,458.0

-

-

2,984,218.0

1,906,278.0

65,255.0

360,000.0

2,918,963.0

1,546,278.0

2,918,963.0

1,546,278.0

- 4,890,496.0 425,255.0 4,465,241.0 4,465,241.0

-

-

5,156,197.0

1,693,994.0

2,307,543.0

1,179,355.0

2,848,654.0

514,639.0

2,848,654.0

514,639.0

- 6,850,191.0 3,486,898.0 3,363,293.0 3,363,293.0

-

-

-

-

1,249,204.0

475,438.0

1,525,668.0

725,820.0

117,342.0

3,700.0

1,120,000.0

49,484.0

1,131,862.0

471,738.0

405,668.0

676,336.0

1,131,862.0

471,738.0

405,668.0

676,336.0

- 3,976,130.0 1,290,526.0 2,685,604.0 2,685,604.0

- 9,228,343.0 343,024.0 8,885,319.0 8,885,319.0

151,785,675.0 269,178,921.0 16,310,108.0 252,868,813.0 404,654,488.0

Statutory provisions and Provisions to be Voted

$’000

Recurrent

2014-2015 Jamaica Budget

7

Head No. and Title StatutoryGross

Expenditure to be Voted

Appropriations in Aid

Net Expenditure to be Voted

Net provisions in Estimates (Including Statutory )

Statutory provisions and Provisions to be Voted

$’000

Recurrent

2014-2015 Jamaica Budget

2013-2014 2013-2014 Expenditure,

3

1500A Office of the Prime Minister

1600A Office of the Cabinet

2000A Ministry of Finance and Planning

2600A Ministry of National Security

2800A Ministry of Justice

4000A Ministry of Labour and Social Security

4100A Ministry of Education

4200A Ministry of Health

4500A Ministry of Youth and Culture

5100A Ministry of Agriculture and Fisheries

5300A Ministry of Industry, Investment and Commerce

5600A Ministry of Science, Technology, Energy and Mining

6500A Ministry of Transport, Works and Housing

6700A Ministry of Water, Land, Environment and Climate Change

7200A Ministry of Local Government and Community Development

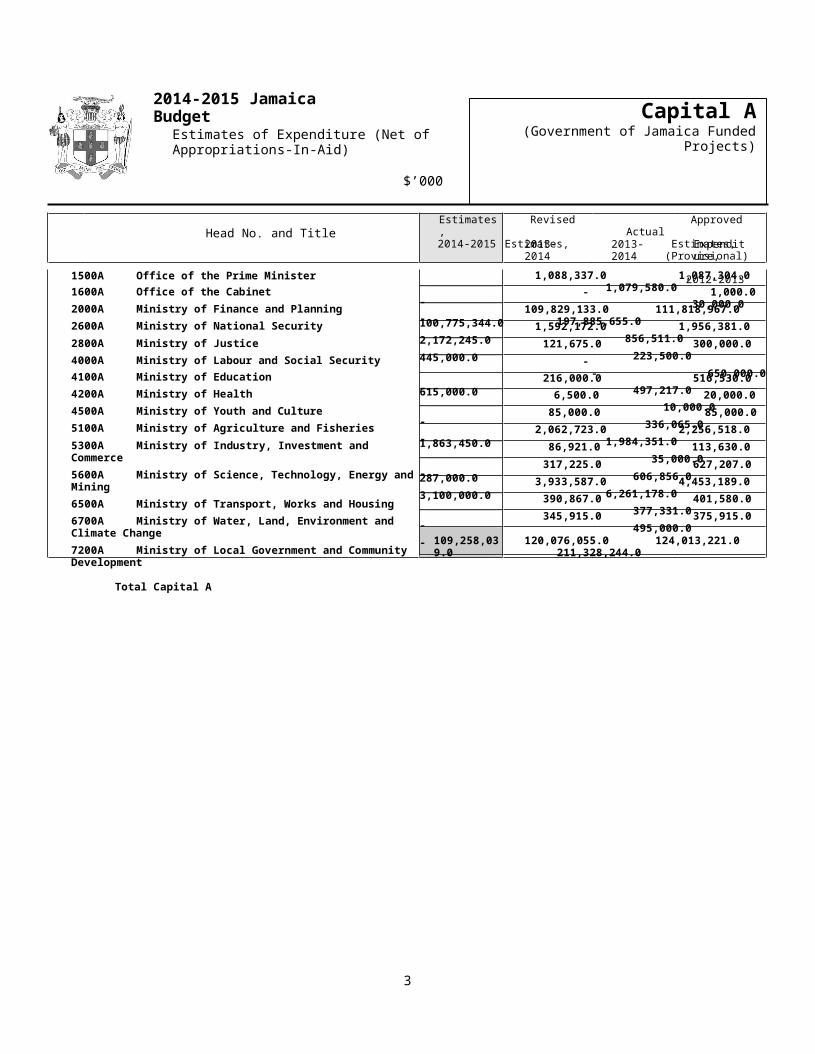

Total Capital A

- 1,088,337.0 1,087,304.0 1,079,580.0

- - 1,000.0 30,000.0

100,775,344.0 109,829,133.0 111,818,967.0 197,885,655.0

2,172,245.0 1,592,172.0 1,956,381.0 856,511.0

445,000.0 121,675.0 300,000.0 223,500.0

- - - 650,000.0

615,000.0 216,000.0 516,530.0 497,217.0

- 6,500.0 20,000.0 10,000.0

- 85,000.0 85,000.0 336,065.0

1,863,450.0 2,062,723.0 2,256,518.0 1,984,351.0

- 86,921.0 113,630.0 35,000.0

287,000.0 317,225.0 627,207.0 606,856.0

3,100,000.0 3,933,587.0 4,453,189.0 6,261,178.0

- 390,867.0 401,580.0 377,331.0

- 345,915.0 375,915.0 495,000.0

109,258,039.0 120,076,055.0 124,013,221.0 211,328,244.0

Head No. and TitleEstimates,2014-2015

Revised Approved ActualEstimates, Estimates, (Provisional)

2012-2013

Estimates of Expenditure (Net ofAppropriations-In-Aid)

$’000

Capital A(Government of Jamaica Funded Projects)

2014-2015 Jamaica Budget

4

Head No. and Title

Estimates,2014-2015

Revised Approved ActualEstimates, Estimates, (Provisional)2013-2014 2013-2014 Expenditure,

2012-2013

1500B Office of the Prime Minister

1600B Office of the Cabinet

1700B Ministry of Tourism and Entertainment

2000B Ministry of Finance and Planning

2600B Ministry of National Security

2800B Ministry of Justice

3000B Ministry of Foreign Affairs and Foreign Trade

4000B Ministry of Labour and Social Security

4100B Ministry of Education

4200B Ministry of Health

4500B Ministry of Youth and Culture

5100B Ministry of Agriculture and Fisheries

5300B Ministry of Industry, Investment and Commerce

5600B Ministry of Science, Technology, Energy and Mining

6500B Ministry of Transport, Works and Housing

6700B Ministry of Water, Land, Environment and Climate Change

7200B Ministry of Local Government and Community Development

Total Capital B

Total Capital (A + B)

Grand Total Recurrent and Capital

1,651,841.0 1,916,645.0 1,885,335.0 1,851,869.0

278,928.0 142,189.0 168,180.0 203,210.0

14,392.0 5,530.0 11,753.0 -

1,643,182.0 1,237,428.0 1,122,811.0 367,307.0

1,039,357.0 1,329,693.0 1,482,476.0 1,199,357.0

357,903.0 201,406.0 230,000.0 205,526.0

75,000.0 42,082.0 134,172.0 43,000.0

5,544,504.0 4,696,053.0 4,887,152.0 3,742,605.0

1,457,369.0 1,510,518.0 1,730,686.0 1,711,094.0

903,423.0 548,205.0 714,370.0 1,613,035.0

173,678.0 203,905.0 248,864.0 255,961.0

505,888.0 569,516.0 622,573.0 1,326,251.0

3,800.0 49,350.0 - 1,044.0

800,298.0 514,347.0 636,353.0 381,260.0

10,579,264.0 8,282,023.0 11,267,911.0 9,146,808.0

279,973.0 938,239.0 1,065,904.0 1,379,223.0

131,243.0 75,617.0 180,506.0 41,786.0

25,440,043.0 22,262,746.0 26,389,046.0 23,469,336.0

134,698,082.0 142,338,801.0 150,402,267.0

520,886,579.0

234,797,580.0

539,352,570.0 500,709,827.0 602,531,232.0

Estimates of Expenditure (Net ofAppropriations-In-Aid)

$’000

Capital B(Multilateral / Bilateral Projects)

1111 TAXATION BULLETIN-REVENUE MEASURES

Your Business Our Focus

LET US HELP YOU ACHIEVE

FURTHER BUSINESS SUCCESS

Please do not hesitate to

contact us if you require any clarification or additional information.Please use any of the following to contact our firm:Head Office :

Unit 34,Winchester Business

Centre 15 Hope Road,

Kingston 10Tel : 876-9084007Fax : 876-7540380

Em ail:[email protected]

Branch Offices:

Oxford House, 6 Oxford Road ,Kingston 5,Tel: (876) 926-3562 to 4

Fax: (876) 929-1300

Montego Bay-Shop EU 6, WhitterVillage,Ironshore, St. Jam esTel : 876-9533793/953-8486Fax: 953-3058

Mandeville-Shop B , C a l e d o n i aPlaza,Manchester Tel : 962-6369

Fax: 754-0380

M a l l

Ocho Rios-101B Main Street,St. Ann

Tel : 9748772Fax:876-974-5373

www.dawgen.com

![Arnold and Commissioner of Taxation (Taxation) … and Commissioner of Taxation (Taxation) [2017] AATA 1318 PAGE 2 OF 26 CATCHWORDS TAXATION AND REVENUE – appeal …](https://img.pdfslide.us/doc/110x75/5af2c9387f8b9ac2469120bc/arnold-and-commissioner-of-taxation-taxation-and-commissioner-of-taxation.jpg)