Embed Size (px)

Citation preview

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 1/38

INSURANCE & BANKING

at

Post ra uate Dip oma inBanking and Insurance

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 2/38

1. Individual

2.Hindu Undivided Family

3. Company

.

5. Association of persons or Body of Individuals

6. Local authority7. Artificial juridical person

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 3/38

1. Residential status

2. Previous year

3. Assessment year

.

5. Exempted income

6. Gross Total Income7. Deductions

8. Total Income

9. Tax deducted at source

10. Maximum amount not chargeable to tax

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 4/38

Heads of Income under IncomeTax (IT) Act, 1961

1. Salaries

2. House property

3. Business or profession

.

5. Other Sources

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 5/38

Particulars Amount (Rs.)

Salaries XX

House Property XX

Business or Profession XX

Capital Gains XX

Other Sources XX

Deductions XX

Total Income XXXX

Tax payable on Total income ###

Tax deducted at source ##

Self assessment tax ##

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 6/38

Broadly Insurance are of following types:

• Life Insurance

• General Insurance (Other than Life Insurance)• Health Insurance

• Vehicle Insurance

• Crop Insurance

• Plant and Machinery, Stock, Cash Insurance etc.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 7/38

• For Individuals and HUF •

• Benefits by way of Exempted Income• Benefits in form of salary

• • Benefit under the head of Business and profession

• Provisions for Life insurance agents etc.• Insurance recei ts char eable as ca ital ain

• Benefits to Insurance Providers

• TDS Provision of Insurance commission

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 8/38

Benefits by deduction from Grosstotal income

Maximum amount deductible u/s 80C, 80CCC. , , -

Under section 80C1. Payment of Life Insurance Premium:

Subject to maximum of 20% of sum assured. Sumassured does not include any premium agreed to be

returned or any benefit by way of Bonus. o cy s ou e a en on own e, e o e spouse or

any Child. In case of HUF, any member of HUF.

Covers payment made by government employees to

’ .payment made by a person under Children'sEndowment assurance policy.

–

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 9/38

Benefits by deduction from Grosstotal income (contd..)

2. Payment in respect of non-commutabledeferred annuity:

Annuity plan can be taken in the name of theindividual, spouse life or any child of such Individual.

o ene o .

3. Contribution made towards participating in the

Unit Linked Insurance P lan (ULIP) ULIP of UTI and of LIC Mutual fund. It can be covered

in the name of individual, spouse and any child.

Minimum period of holding – 5 years

Consequences if termination made before 5 years: Contribution during the year will not qualify for deduction

Any deduction taken earlier would be deemed to bencome n e year n w c p an s erm na e .

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 10/38

Benefits by deduction from Grosstotal income (contd..)

Under section 80CCC

• P e n s i o n f u n d h e l d w i t h a n I n s u r e r :

Benefit is given only to Individual.

He had deposited any sum under an annuity plan of LICand any other insurer in the Previous year.

The aforesaid amount must be paid out of taxable

income. Not necessary that it should be paid out of theincome of current year.

Surrender value of annuity before maturity date willbecome taxable in the year of receipt of SV.

Receipt of pension by individual or nominee aftermaturity is taxable as income in the year of receipt.

No deduction under this section, if same is alreadyc a me n sec on .

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 11/38

Benefits by deduction from Grosstotal income (contd..)

Under section 80D

• Deduction in respect of Medical insurancepremium:

The benefit is available to Individual and HUF.

Mediclaim Insurance Policy framed by GeneralInsurance Corporation of India and approved by CentralGovernment.

Similar Scheme by any other insurer approved byInsurance Regulatory and Development Authority shallalso be eligible for deduction.

Payment: Can be paid by any mode other than Cash. Must be paid out of Taxable Income.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 12/38

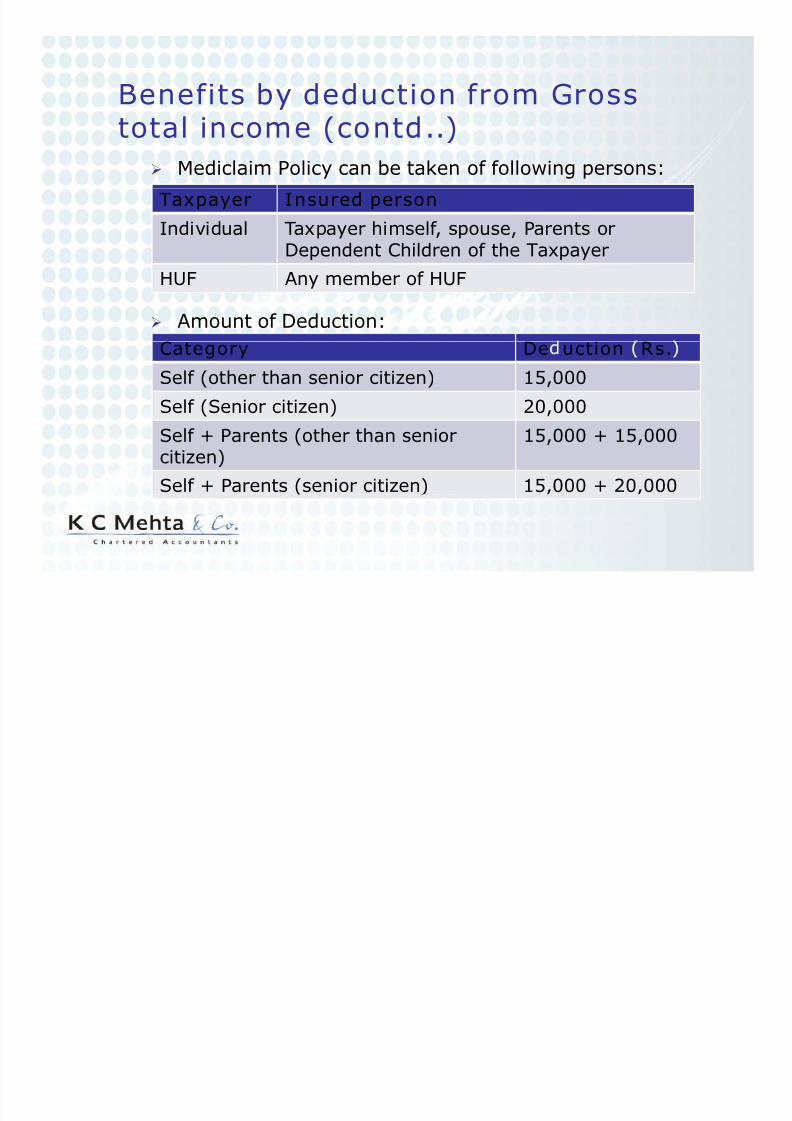

Benefits by deduction from Grosstotal income (contd..)

Mediclaim Policy can be taken of following persons:

Taxpayer Insured person

Individual Taxpayer himself, spouse, Parents orDependent Children of the Taxpayer

Amount of Deduction:

HUF Any member of HUF

Category De uction Rs.

Self (other than senior citizen) 15,000

Self (Senior citizen) 20,000

Self + Parents (other than seniorcitizen)

15,000 + 15,000

Self + Parents (senior citizen) 15,000 + 20,000

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 13/38

1. Say, In P.Y. 2009-10, A has paid for mediclaim insurances. on mse . e as a so pa s. or

mediclaim for his parents. The deduction u/s 80D are tobe calculated:

Deduction will be Rs. 15000+ 15000= Rs. 30000

A is not senior Citizen but his parents are senior citizen,

A and His parents both are senior citizens:

Deduction will be Rs. 20000+20000=40000

ssume, e as a en me c a m on y on mse an paRs. 35000/- then deduction will be 15000 and 20000 if heis senior citizen

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 14/38

Benefits by deduction from Grosstotal income (contd..)

Under section 80DD

•For medical treatment of dependent being aperson w ith disability

Tax a er must be resident Individual or HUF.

The taxpayer has two options:

He incurs the expenditures himself for treatment, trainingand rehabilitation of dependent disabled person.

He has taken a policy under any scheme framed by LIC orany other insurer for maintenance of dependent disabledperson. Annuity should be for the benefit of disabled.

w y yspouse, child, parent and brother or sister in case of individual and any member in case of HUF.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 15/38

Benefits by deduction from Grosstotal income (contd..)

Person with disability means as defined in Disabilityqua oppor un es an pro ec ons o r g s an u

participation) Act, 1995. It includes autism, cerebralpalsy or multiple disability, etc.

.

Assessee required to furnish a certificate from medical

authority in Form-10IA or as prescribed in Disabilities.

No deduction if also claimed under section 80U

Benefits:

-. .

If disability is severe, higher deduction of Rs. 100000.Severe Disability means disability of 80% or more.

Taxabilit of maturit roceeds if disabled ersonpredeceases the person who makes contribution

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 16/38

Under section 10(10A):• Any annuity plan of LIC from any fund set up.

• Payment received by way of Commutation of pension.

• Commutation is a Lum sum a ment in lieu of periodical payment.

Under section 10(10D): • insurance policy is not chargeable to tax.

• Exceptions:

.

• Any sum received under Key man insurance policy.

• Sum received from a policy issued after 31st March, 2003,where premium paid exceeds 20% of sum assured. But if received on death, then will not be taxable.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 17/38

Assurance on Life of an employee:

Amount paid by Taxability

Employer Taxable as salary

Any third person Taxable as income of other source u/s 56

Exceptions:• Group insurance scheme

’ • Fidelity Guarantee Scheme

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 18/38

Benefits under Business orProfession

Deduction of Insurance premium expenses:

Section Nature of expense30 Insurance against damage and destruction of

31 Insurance against risk of damage anddestruction of machinery, plant and furniture

,

36(1)(ia) Allowed only to Federal Milk Co-operativeSociety for insurance on lives of Cattle

employees is allowed as deduction

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 19/38

Provisions of adhoc deduction fromcommission income to LIC agents

• Circular no. 594 dt. 27/02/91, 648 dt. 30/03/93 and.

commission income earned by LIC agents, UTIagents, Post office/Government securities agents

• Commission earned is less than Rs. 60000/-:Commission Adhoc

deductionMaximumdeduction

First year’s Commission 50% of same Rs.20,000

Renewal Commission 15% of same

’ and renewal commissionare not separable

.year’s and renewalcommission

. ,

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 20/38

Insurance Receipts chargeable asCapital Gains

Under section 45(1A)• ompensa on rece ve on amage or es ruc on o

i. a capital assetii. destruction is result of four circumstances:

oo , yp oon, urr cane, yc one, ar qua e or anyconvulsion of nature.

(ii) Riot or civil disturbance

(iii) Accidental fire explosionv ct on y an enemy or to com at ng an enemy

• Profits and gains arising from such receipts will bechargeable under the head of Capital Gains.

• Taxable in the year in which such money or assets received.• Sale consideration when assets received: FMV of other

assets received on the date of recei t .

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 21/38

Under section 10(23BBE):Income of Insurance Regulatory and Development

authority is exempt from Tax.

Under section 10(25A):Income of Employee’s State Insurance Fund set up

under the provision of Employee's State Insurancec , s exemp rom ax.

Under section10(23AAB):

Any income of a fund set up by LIC of India on orafter 1st August, 1996 or any other insurer approvedby Controller of IRDA is exempt from Income Tax.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 22/38

• No TDS is required to be deducted

U/s 193 for Interest on Securities

U/s 194 for Dividend

in case of investments made by

i. Life Insurance corporation

ii. General Insurance Corporation of India

iii. Four companies formed under General insurance,

iv. Any other insurer

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 23/38

Under section 194D:• Person responsible to deduct tax is the person who is

responsible for paying to a resident any income by way of remuneration, reward, commission for soliciting and

• Applicable rate: 10% (No surcharge or EC, SHEC)

• If recipient does not furnish PAN then TDS Rate will be @

20% w.e.f. 1st April 2010.• Time for deduction: Credit to account or payment of same

(by any mode), whichever is earlier.

• Threshold limit: Rs. 5,000/-.

• o e uc on cer ca e urn s e .• Lower rate deduction as per section 197

• Certificate in form no.16A.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 24/38

• Taxability of Interest Income of deposits.

• Allowability of Interest expenditure incurred

• Deduction of Interest for Housing loan• Deduction of Interest under Business and profession

• De uction rom t e Gross tota Income

• Benefits to Banking companies

• Deduction for Provision for Bad Debts• Deduction for transfer to special reserve

• Deduction from Gross Total Income

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 25/38

• Taxable under the head “Income from other”

• If interest earned from money lending or investmentbusiness, taxable under head of “Profits and gains

”.

• Interest Income may arise from

Saving bank a/c

Recurring deposits

Fixed Deposits

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 26/38

Under section 10(4)• n case o a non-res en n v ua , any ncome y

way of interest on moneys standing to his credit onNon-resident (External) Account in any bank in India

Under section 10(15)

• Interest received by a non-resident or resident but

not ordinarily resident in India on deposit made afterarc , n an o s ore an ng un .

• Interest payable by a Scheduled bank to a Non-resident and RNOR on deposits (approved by RBI) in

• Interest payable by ICICI, IFCI, IDBI, EXIM Bank,NHB, SIDBI or any money borrowed before 1st June,2001 from sources outside India.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 27/38

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 28/38

Deduction of Interest expenditureunder Business or Profession

• Conditions:

• The assessee must have borrowed money.

• The money so borrowed should be for the purpose of business.

• Interest is paid or payable on such borrowing.

• The loan can be taken from Banks/ Financial

Institutions or from unsecured sources.• If above conditions are satisfied, interest will be

deductible on the basis of system of accountingsubject to section 43B and 40A(3).

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 29/38

Section 43B has a general rule of certain expenditures.

•Interest on any loan or borrowing from a publicfinancial institution as ICICI Bank, IFCI, IDBI, LIC and

investment corporation

•Interest on any loan and advances taken from a-

Exception: If payment of said interest is actually made

Income.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 30/38

• Assessee incurs an expenditure which is otherwise. , .

• The payment (or aggregate of payment mad to aperson in a day) in respect of the above

. , .

• Payment is made otherwise than by an accountpayee cheque or account payee draft (cash, bearer

, .

• If above conditions are satisfied, then fullexpenditure is not allowed as deduction.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 31/38

Under section 80C (maximum deduction Rs. 1 lac)

• r nc pa repaymen o oan a en rom spec e

sources for construction/purchase of residentialproperty•

years or more in Scheduled bank

Under section 80E (Interest on education loan)

•

financial institution by an individual.

• The loan has been taken for higher education.

•

• Assessee has paid interest on such loan out of hisincome chargeable to tax.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 32/38

Provision for bad-debts expenses

• It is an allowable to rural branches of

Commercial Banks (Section 36(1)(viia))

situated in a place which has population of not more than 10000 according to previous

.

• Deduction under this section will be availablefirst before deduction of actual Bad debts u/s

.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 33/38

Amount deductible in respect of provision for Bad &Doubtful Debts

In case of In case of In case of

bank & NonScheduledBank

, ,

SIIC

Bank

Total Income

(Before any

7.5% of Such Income

5% of SuchIncome

5% of SuchIncome

chapter VI)

Aggregateavera e advance

10% of SuchAdvances

made by RuralBranches

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 34/38

ABC, a financial institution bank, is eligible to claim the.

this deduction is 160 lacs for the A.Y. 2010-11. PFDD hasopening balance of Rs. 1 lac. ABC wants to write off 14.

36(1)(vii)/(viia).

Provision for Bad and Doubtful Debt A/c (Rs. in lacs)

To Debtors 14 B Balance b/f 1

(Being bad debts written off)

By Profit and Loss a/c

(deduction eligible u/s

36(1)(viia), i,e, 5% of 160 Lacs)

8

By Profit and loss a/c(being deduction u/s 36(1)(vii) 5

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 35/38

1. Governed by Section 36(i)(viii)

2. Deduction is available toi. ICICI, IFCI, IDBI, LIC, UTI, IDFCL, PFI notified by the

ii. A financial corporation established by Government.

iii. Government company u/s 617 of Companies Act

.

v. Co-Operative Bank

vi. A Housing finance company

vii. ny o er nanc a corpora on nc u ng a pu ccompany.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 36/38

Transfer to Special Reserve(contd..)

• They are engaged in business of providing long term

i. Industrial developmentii. Agricultural development

.

iv. Construction and purchase of residential houses

• Amount of deduction – lowest of .

ii. 20% of profit derived from business activities

iii. 200% of (Paid up capital and general reserve as on-

on first day of the previous year)• Withdrawal from special reserve is chargeable to tax

in the ear in which the amount is withdrawn.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 37/38

Under section 80LA• e assessee s

• A Scheduled bank having offshore banking unit ina special economic zone.

special economic zone.• A unit of International financial service centre

• The ross total income includes income derived fromabove units from the business of banking

• A report of Chartered Accountant in from no. 10CCFcertifying the deduction should be furnished with

.• Amount of deduction:

100% income deductible for five consecutive.

8/7/2019 Taxation Aspects of Insurance Banking Final

http://slidepdf.com/reader/full/taxation-aspects-of-insurance-banking-final 38/38

Thank ou…