Embed Size (px)

Citation preview

CONTENTS

PART 1 - BUDGET 2007PAGE

2007 BUDGET - TAX PROPOSALSHighlights 1Personal income tax 1

Tax tables 2006/07 1Tax tables 2007/08 1Rebates 2Tax threshold 2Tax saving per annum 2Interest and taxable dividend income exemption 2Monthly monetary caps for tax-free medical scheme contributions 2Annual exclusion for capital gains or losses 2Annual exclusion in year of death for capital gains or losses 2Primary residence exclusion for capital gains or losses 2

Corporate tax rates 3Normal tax (basic rate) 3Tax rates for qualifying small business corporations 3Secondary tax on companies (STC) 3

Other taxes, rates 3Estate duty 3Donations tax 3Capital gains tax 4Transfer duty 4

Savings and retirement reform 5Introduction 5Abolition of retirement fund tax 5Simplifying retirement fund thresholds 5Streamlining the tax regulatory regime for retirement funds 5Foreign collective investment schemes 5Lump sum death benefits 5

Growth business development and job creation 6Reform to the taxation of dividends 6Taxation of gains on long-term equity investments 6Depreciation allowances 7Corporate reorganisation and BEE transactions 7Public Benefit Organisations 8

Implementing the municipal property rates act 8Tax reform measures under review 9

Wage subsidy and social security tax reform 9Small business development 9

Measures to enhance tax administration 9Small business tax amnesty 9Small business amnesty as applied to trusts 10

Miscellaneous amendments - income tax act, 1962 10Residential accommodation fringe benefits 10Exemption for South Africans working abroad 10Streamlining the medical regime 10Incorporation of professional partnerships involving part-time members 10

Budget and Tax Update 2007

i

Permissible use of buildings benefiting from the urban development zone incentive 10Schemes to avoid the reduction of assessed losses upon indirect debt compromises or concessions

11

Foreign companies with South African activities 11Foreign taxpayers receiving passive South African interest and/or royalties 11Loans made in respect of emigrating South African residents 11Changing status of controlled foreign companies 11Deductibility of foreign taxes 11Ambiguous foreign currency cross-references 11National sports organisations 11Simplifying the averaging formula for individual farmers 12General anti-avoidance rule 12Provisional payment system 12Refund payments 12Employee share options 12Reciprocal tax relief for sportspersons 12Employee tax relief for sole proprietors 12

Miscellaneous amendments – value-added tax act, 1991 13E-commerce downloads 13Nominal or passive foreign-controlled local activities 13Dried maize 13Streamlining business reorganisations 13Insurance versus financial services 13Bare dominium financing structures 13Transfer among rental pool members 14Horse-racing industry 14Game-viewing clarification 14Foreign diplomat resale of local purchased vehicles 14Change of use adjustments of fixed property 14Improper use of turnover apportionment method 14Duty-free shops 14Clarifying payment dates 15Documentary evidence for input tax 15Documentary evidence for zero-rated exports 15Electronic storage of cheques, bank deposit slips and other documents 15

Pension funds act, 1956 15Forced early withdrawals from retirement funds 15Defining annuity payments 15Living annuity drawdowns 15

International cooperation for enhanced cross-border enforcement 16Indirect tax proposals 16

Fuel taxes 16Duties on beverages and tobacco products 16

PART 2 - TAX UPDATE

These notes will cover amendments to the legislation promulgated during 2006 and early 2007. You will recognise edited versions of the Explanatory Memoranda which make up the bulk of these notes. We do not intend this to be an exhaustive reference work.

Developments over the last year 17The small business tax amnesty and amendment of taxation laws act 9 of 2006 and second small business tax amnesty and amendment of taxation laws act 10 of 2006

18

Small Business Tax Amnesty 18Persons who may apply for amnesty 18To qualify for amnesty the requirements are that- 19Method and period of application 19Information required in the application 19

Budget and Tax Update 2007

ii

Evaluation and approval 19Review of Commissioner’s decision 19Amnesty Levy 20Example of levy calculation 20Payment of tax amnesty levy 20Scope of the tax amnesty relief 20No prosecution 21Exclusion from the tax amnesty relief 21Treatment of deductions and losses going forward 21Circumstances where approval is void 22Reporting by the Commissioner and Minister 22Waiver of additional tax, penalty and interest 22

Draft regulations 22Information required in application 23Approval of application to waive business tax debt 23Circumstance where not appropriate to waive business tax debt 24Amount to be waived 24Amounts that may not be waived 24Agreement setting out the conditions of waiver 24Commissioner not bound to waiver 24Records of tax debt waived 25Reporting 25

Financial Intelligence Centre Act (FICA) 25Auditing Profession Act (APA) 25

Transfer Duty Act 25Section 9B of the Income Tax Act – Sale of listed shares 25Section 12E of the Income Tax Act – Small business corporation 26Section 12H of the Income Tax Act – Learnership allowance 26Section 56 of the Income Tax Act – Donations tax threshold 27Paragraph 1 of the Fourth Schedule to the Income Tax Act – PAYE on motor vehicle allowance

27

Paragraph 9 of the Seventh Schedule to the Income Tax Act – Residential accommodation

27

Paragraph 10 of the Seventh Schedule to the Income Tax Act – Free or cheap services 27Paragraph 12B of the Seventh Schedule to the Income Tax Act – Medical services 28Section 1 of the Stamp Duties Act, 1968 – Definition of stamp 28Item 14 of Schedule 1 of the Stamp Duties Act – Stamp duty on leases 28Section 1 of the Value-Added Tax Act, 1991 – Municipalities 29

Introduction 29The above is achieved through the following amendments: 29Definition of a ‘designated entity’ 29Definition of an ‘enterprise’ 30Definition of a ‘municipality’ 30Definition of ‘municipal rate’ 31Liability of municipalities for tax and limitation of refunds 31Examples 1 and 2 32

Section 11 of the Value-Added Tax Act – Biofeuls 32Section 27 of the Value-Added Tax Act – Small scale farmers and other vendors 32Section 2 of the Tax on Retirement Funds Act – Tax rate 32Section 1 of the Uncertificated Securities Act, 1998 – Change in beneficial ownership of securities

33

Section 5 and 5A of the Uncertificated Securities Act, 1998 – Change in beneficial ownership of securities

33

Budget and Tax Update 2007

iii

The revenue laws amendment act 33 of 2006 and second revenue laws amendment act 34 of 2006

34

Section 1 of the Income Tax Act, 1962 – Definitions 34Company 34Co-operative 34Shareholder 34Connected person 34Dividend 34

Section 8 of the Income Tax Act – Subsistence allowance 35Section 8C of the Income Tax Act – Vesting of equity instruments 35Section 9D of the Income Tax Act – Controlled foreign companies (CFC) 36

Country of residence 36Foreign business establishment 36‘foreign financial instrument holding company’ 37‘net income’ 38Diversionary transaction rules provide for situation when the above exclusion does not apply. 38Services performed by CFCs 38CFC sale of foreign intangibles 39Matching of intra-group deductions and interest 39CFC ruling escape hatch 39Business establishment waiver for related CFC group employees, equipment and facilities 40Diversionary transaction waiver for centrally located operations 40Passive income waiver for active royalties 40Diversionary transaction and passive income waiver for high-taxed income 40Financial services comparably-taxed waiver 41Commencement date 41

Section 10 of the Income Tax Act – Foreign donor funding 41Section 10 and 30A of the Income Tax Act and Paragraph 65B of the 8 th Schedule to the Income Tax Act – Partial taxation of recreational clubs

41

Introduction 41The new section 10(1)(cO)) 42Capital gains tax 42

The new paragraph 65B of the Eighth Schedule reads as follows: 42The new section 30A 43

Penalties 44Effective Dates 44

Section 10(1)(h) of the Income Tax Act – Interest earned by non-residents 44Section 10(1)(q) of the Income Tax Act – Scholarships and bursaries 44Section 10(1)(y) and (yA) of the Income Tax Act – Domestic and Foreign Government Grants

45

Domestic 45Foreign 46Reasons for change 46Amendments – Domestic 46

1.Anti-double-dipping rules 462.Government scrapping payments 46

Amendments – Foreign 461.Grants 462.Discounted loans and technical assistance 47

Section 11(gB) of the Income Tax Act – Registration of intellectual property 47Section 11B of the Income Tax Act – Registration of intellectual property 47Section 11D of the Income Tax Act – Scientific or technological research and development

47

Position prior to the amendment 47Reasons for change 48The amendment – New section 11D 48

Basic regime 48Part R&D Expenditure 48

Budget and Tax Update 2007

iv

Example: 48Recoupments 49

Examples 49No doubling of the 150% deduction 49

Example 49Government grants 49

Example 50Reporting requirements 50Effective Dates 50Old section 11B 50

Section 12E of the Income Tax Act – Small business corporations 50Introduction 50Small business relief 50Membership in consumer co-operatives and friendly societies 51Investment income 51Personal service 51

Sections 18A, 30 and the 9th Schedule to the Income Tax Act - Public Benefit Organisations (PBOs)

51

Tax rates for PBO trading activities 51Refining the PBO activity list 51

Housing PBOs 51Conservation, environment and animal welfare PBOs 52Foreign established charities 52

Liberalising permissible PBO investments 53Capital gains on disposal of PBO assets 53Definition of PBO - Concept of public benefit 53Administration - Dual registration 54Miscellaneous administration – Provisional tax 54Miscellaneous administration – Withdrawal of approval 54Commencement dates 54

Section 23(k) of the Income Tax Act – Permissible deductions of personal service companies and personal service trusts

55

Section 24I of the Income Tax Act – Foreign currency transactions 55ection 24J of the Income Tax Act – Incurral and accrual of interest 55Section 26B and the Tenth Schedule to the Income Tax Act - Oil and Gas Exploration and Production

55

Section 23(k) of the Income Tax Act – Permissible deductions of personal service companies and personal service trusts

55

Section 24I of the Income Tax Act – Foreign currency transactions 55Section 24J of the Income Tax Act – Incurral and accrual of interest 55Section 26B and the Tenth Schedule to the Income Tax Act - Oil and Gas Exploration and Production

55

New Tenth Schedule override 56List of Tenth Schedule provisions 56

1. Coverage (paragraph 1) 562. Income tax rates (paragraph 2) 563. Dividend tax rates (paragraph 3) 564. Foreign currency gains or losses (paragraph 4) 575. Oil and gas deductions (paragraph 5) 576. Thin capitalisation (paragraph 6) 587. Disposal of oil and gas rights (paragraph 7) 588. Fiscal stability (paragraph 8) 59Effective date 60

Section 37A of the Income Tax Act – Mining environmental rehabilitation funds 60Introduction 60Eligible contributing parties 60Eligible mining rehabilitation funds 61Penalties 61

Budget and Tax Update 2007

v

Effective dates 62Insertion of Part IIA of Chapter III of the Income Tax Act – General anti-avoidance rule 62

The requirements for an impermissible avoidance arrangement summarised 62Section 80L – The definitions 63Section 80A – Impermissible tax avoidance arrangements 63Section 80B – Tax consequences of impermissible tax avoidance 63Section 80C – Lack of commercial substance 64Section 80D – Round trip financing 64Section 80E – Accommodating or tax indifferent parties 65Section 80F – Treatment of connected persons and accommodating or tax indifferent parties 65Section 80G – Presumption of purpose 65Section 80H – Application to steps in or parts of an arrangement 65Section 80I – Use in the alternative 65Section 80J – Notice 65Section 80K – Interest 65Sections 80A to 80L - Commencement date 66

Insertion of Part IIB of Chapter III of the Income Tax Act – Reportable arrangements 66Section 102 of the Income Tax Act – Refunds 67Section 103 of the Income Tax Act – Anti avoidance provisions 67Paragraph 5 of the Second Schedule to the Income Tax Act – Retirement fund withdrawals

67

Amounts payable by Retirement Annuity Funds 67Taxation of withdrawal and retirement benefits – pension and provident funds 68Taxation of withdrawal and retirement benefits 68Effective date 68

Paragraph 1 of the 4th Schedule to the Income Tax Act – Relief for small personal service entities

69

Narrowing the scope of the PSE regime 69Relaxation of client withholding 69Taxation of net profits 69Effective date 70

Paragraph 9 of the 4th Schedule to the Income Tax Act – Withholding tax on lump sums from pensions, provident funds and retirement annuity funds

70

Paragraph 11 of the 8th Schedule to the Income Tax Act – Issue or cancellation of a member’s interest in a close corporation

70

Paragraph 20 of the 8th Schedule to the Income Tax Act – Base cost of assets inherited from a non-resident

70

Paragraph 29(5) of the 8th Schedule to the Income Tax Act – Submission dates of certain valuation date valuations

71

Paragraph 62(e) of the 8th Schedule to the Income Tax Act – Donations and bequests to approved recreational clubs

71

Paragraph 64A(b) of the 8th Schedule to the Income Tax Act – Government scrapping payments

71

Paragraph 67 of the 8th Schedule to the Income Tax Act – Deceased estates and roll over provisions

71

Paragraph 80 of the 8th Schedule to the Income Tax Act – Capital gain attributed to beneficiaries of a trust

72

Section 9 of the Finance and Financial Adjustments Act, 1977 – Tax treatment of different spheres of domestic and foreign government

73

Section 8(27), 10(26) and 16(3)(m) of the Value-Added Tax Act – Excessive consideration 74Section 15(2) of the Value-Added Tax Act – Payment basis of accounting 74Section 16(2) of the Value-Added Tax Act – Time limit to claim input tax 75Section 16(3) of the Value-Added Tax Act – Prize or winnings 75Section 17(2)(a) of the Value-Added Tax Act – Entertainment expenditure 76Section 20(8) of the Value-Added Tax Act – Record keeping for second-hand goods 76Section 22(3) of the Value-Added Tax Act – Deemed output tax on cessation of enterprise 76Section 31(1) of the Value-Added Tax Act – Additional assessment 77Section 41 and 41A of the Value-Added Tax Act – Written decisions by the Commissioner 77

Budget and Tax Update 2007

vi

Section 44(1) of the Value-Added Tax Act – Additional assessment 78Schedule 1 of the Value –Added Tax Act – 2010 FIFA World Cup 78Schedules 1 and 2 of the Revenue Laws Amendment Act, 2006 – Special tax measures relating to the 2010 FIFA World Cup

78

Introduction 78Tax-free bubble concept 78FIFA retail outlets 79Associated persons 79Specifics of Guarantee No. 3 (Customs) 79Specifics of Guarantee No. 4 (Other Taxes, Duties and Levies) 79Government Guarantee No. 4 does not include the following taxes– 80Administrative Aspects 82Date of Implementation 82

Section 14 of the Unemployment Insurance Act – State old-age pensions 82

Budget and Tax Update 2007

vii

PART 1 - BUDGET 2007

2007 BUDGET TAX PROPOSALS

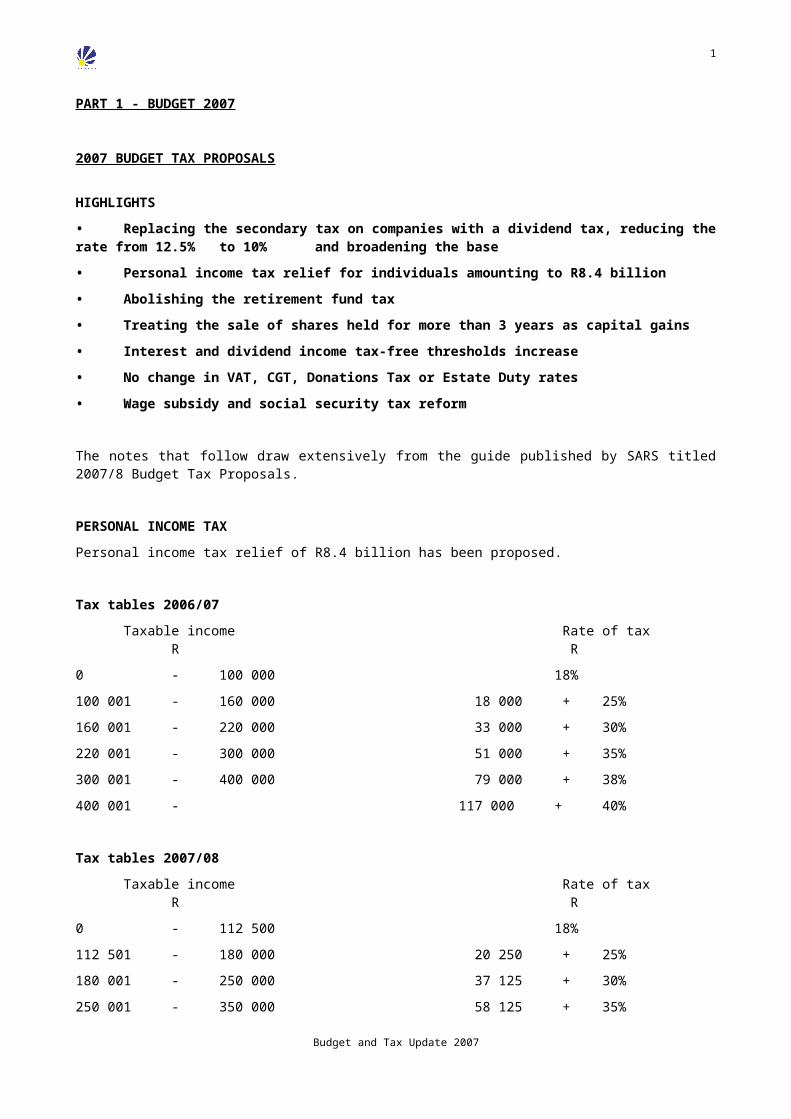

HIGHLIGHTS• Replacing the secondary tax on companies with a dividend tax, reducing the rate from 12.5%

to 10% and broadening the base• Personal income tax relief for individuals amounting to R8.4 billion• Abolishing the retirement fund tax• Treating the sale of shares held for more than 3 years as capital gains• Interest and dividend income tax-free thresholds increase• No change in VAT, CGT, Donations Tax or Estate Duty rates• Wage subsidy and social security tax reform

The notes that follow draw extensively from the guide published by SARS titled 2007/8 Budget Tax Proposals.

PERSONAL INCOME TAXPersonal income tax relief of R8.4 billion has been proposed.

Tax tables 2006/07Taxable income Rate of tax

R R

0 - 100 000 18%

100 001 - 160 000 18 000 + 25%

160 001 - 220 000 33 000 + 30%

220 001 - 300 000 51 000 + 35%

300 001 - 400 000 79 000 + 38%

400 001 - 117 000 + 40%

Tax tables 2007/08Taxable income Rate of tax

R R

0 - 112 500 18%

112 501 - 180 000 20 250 + 25%

180 001 - 250 000 37 125 + 30%

250 001 - 350 000 58 125 + 35%

350 001 - 450 000 93 125 + 38%

450 001 - 131 125 + 40%

Budget and Tax Update 2007

1

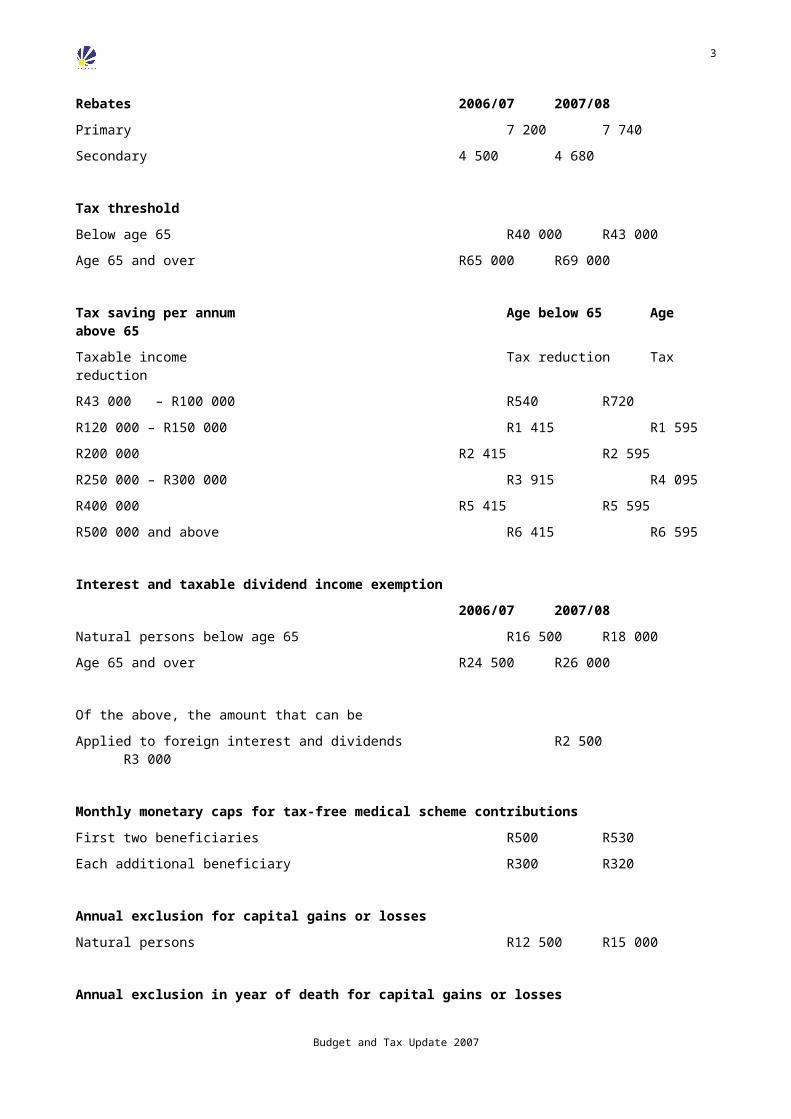

Rebates 2006/07 2007/08Primary 7 200 7 740

Secondary 4 500 4 680

Tax thresholdBelow age 65 R40 000 R43 000

Age 65 and over R65 000 R69 000

Tax saving per annum Age below 65 Age above 65Taxable income Tax reduction Tax reduction

R43 000 – R100 000 R540 R720

R120 000 – R150 000 R1 415 R1 595

R200 000 R2 415 R2 595

R250 000 – R300 000 R3 915 R4 095

R400 000 R5 415 R5 595

R500 000 and above R6 415 R6 595

Interest and taxable dividend income exemption2006/07 2007/08

Natural persons below age 65 R16 500 R18 000

Age 65 and over R24 500 R26 000

Of the above, the amount that can be

Applied to foreign interest and dividends R2 500 R3 000

Monthly monetary caps for tax-free medical scheme contributionsFirst two beneficiaries R500 R530

Each additional beneficiary R300 R320

Annual exclusion for capital gains or lossesNatural persons R12 500 R15 000

Annual exclusion in year of death for capital gains or lossesNatural persons R60 000 R120 000

Primary residence exclusion for capital gains or lossesNatural persons R1 500 000 R1 500 000

Budget and Tax Update 2007

2

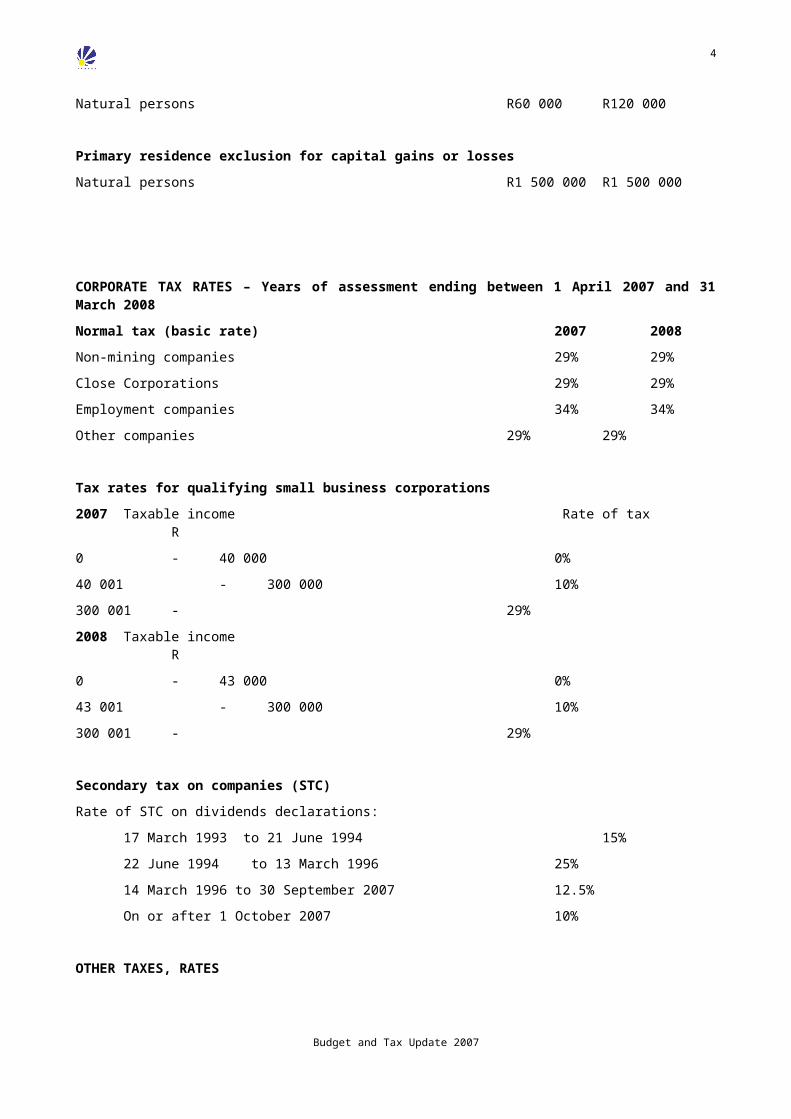

CORPORATE TAX RATES – Years of assessment ending between 1 April 2007 and 31 March 2008Normal tax (basic rate) 2007 2008Non-mining companies 29% 29%

Close Corporations 29% 29%

Employment companies 34% 34%

Other companies 29% 29%

Tax rates for qualifying small business corporations2007 Taxable income Rate of tax

R

0 - 40 000 0%

40 001 - 300 000 10%

300 001 - 29%

2008 Taxable incomeR

0 - 43 000 0%

43 001 - 300 000 10%

300 001 - 29%

Secondary tax on companies (STC)Rate of STC on dividends declarations:

17 March 1993 to 21 June 1994 15%

22 June 1994 to 13 March 1996 25%

14 March 1996 to 30 September 2007 12.5%

On or after 1 October 2007 10%

OTHER TAXES, RATES

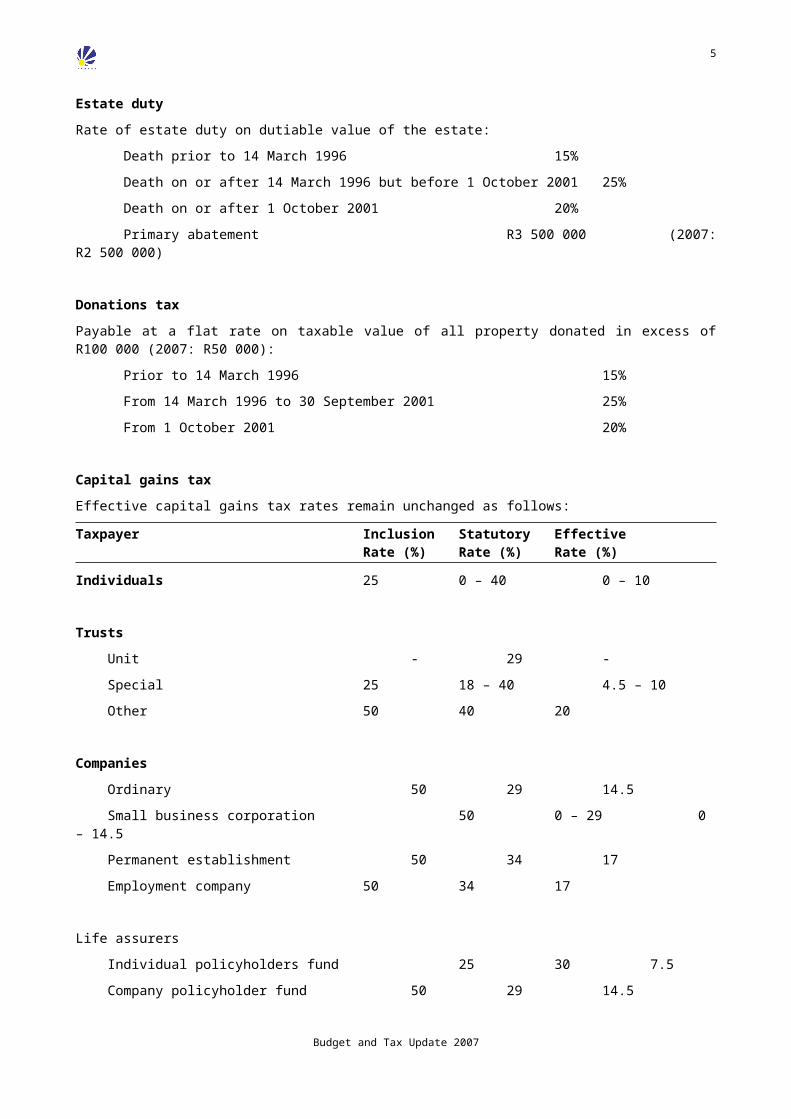

Estate dutyRate of estate duty on dutiable value of the estate:

Death prior to 14 March 1996 15%

Death on or after 14 March 1996 but before 1 October 2001 25%

Death on or after 1 October 2001 20%

Primary abatement R3 500 000 (2007: R2 500 000)

Donations taxPayable at a flat rate on taxable value of all property donated in excess of R100 000 (2007: R50 000):

Prior to 14 March 1996 15%

From 14 March 1996 to 30 September 2001 25%

From 1 October 2001 20%

Budget and Tax Update 2007

3

Capital gains taxEffective capital gains tax rates remain unchanged as follows:

Taxpayer Inclusion Statutory EffectiveRate (%) Rate (%) Rate (%)

Individuals 25 0 – 40 0 – 10

Trusts Unit - 29 -

Special 25 18 – 40 4.5 – 10

Other 50 40 20

Companies Ordinary 50 29 14.5

Small business corporation 50 0 – 29 0 – 14.5

Permanent establishment 50 34 17

Employment company 50 34 17

Life assurers

Individual policyholders fund 25 30 7.5

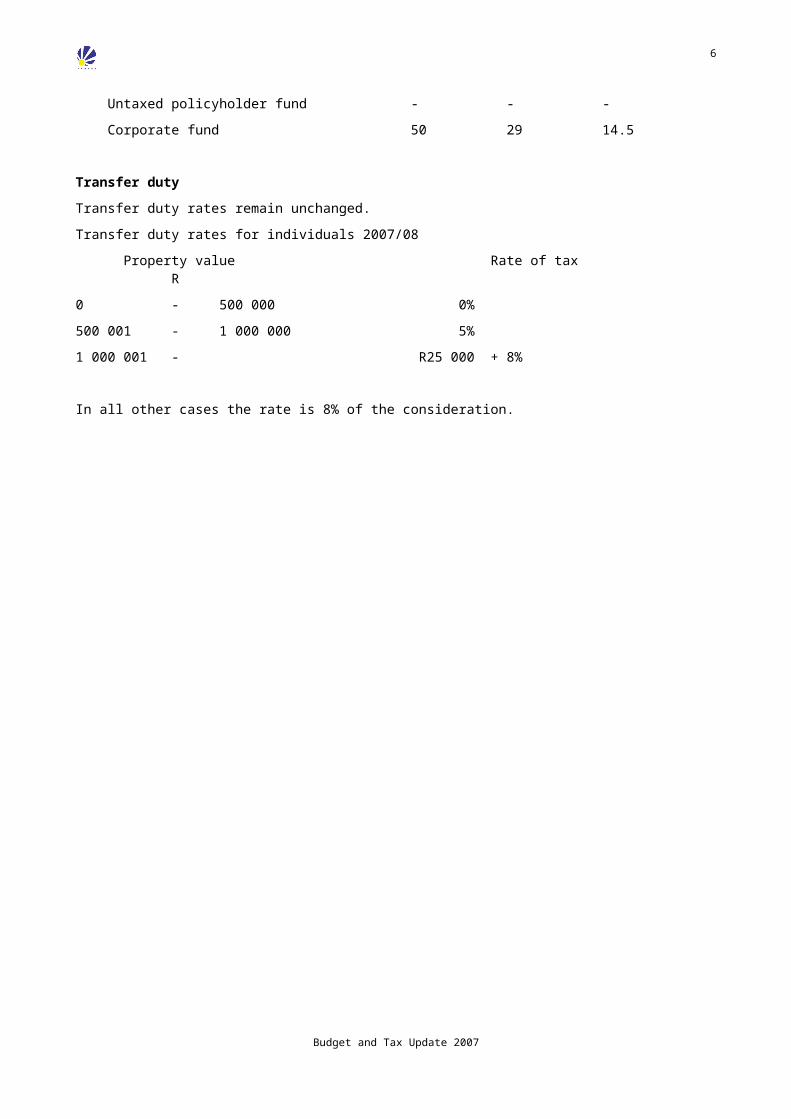

Company policyholder fund 50 29 14.5

Untaxed policyholder fund - - -

Corporate fund 50 29 14.5

Transfer dutyTransfer duty rates remain unchanged.

Transfer duty rates for individuals 2007/08

Property value Rate of taxR

0 - 500 000 0%

500 001 - 1 000 000 5%

1 000 001 - R25 000 + 8%

In all other cases the rate is 8% of the consideration.

Budget and Tax Update 2007

4

SAVINGS AND RETIREMENT REFORMIntroductionThe proposed reforms to retirement saving are aimed at providing an efficient and equitable framework for individuals to provide for their retirement. Mandatory contributions, compulsory preservation, portability and enhanced regulation together provide the foundation for the retirement funding reforms.

The tax treatment of retirement savings must complement these regulatory and institutional reforms. Details of these reforms will be published by the National Treasury in a separate discussion paper, including reforms to the tax system that seek to maintain sufficient incentive to provide adequately for retirement, while addressing inequities and complexity in the current system.

In keeping with practice in many other countries, the reforms will see a shift to an expenditure model of retirement fund taxation, in which contributions to retirement funds are eligible for full or partial deductibility, investment growth is tax exempt and benefits are taxable. As part of this, a uniform and more equitable tax treatment of contributions to pension, provident and retirement annuity funds will be phased in over time, consisting of three parts

• favourable tax treatment of a basic savings element,

• some tax encouragement of a supplementary component, and

• no special tax treatment above a specified ceiling.

The reforms will improve equity and more effectively encourage long-term savings by lower and middle income individuals.

It is hoped the complete package of reforms will be finalised during the course of 2007, following further consultation in the light of social security reform discussions. However, several elements of the reform package outlined below will be implemented in 2007.

Abolition of retirement fund tax Retirement Fund Tax (RFT) on interest and rental income will be abolished with effect from 1 March 2007. This is consistent with the shift to the retirement savings taxation model outlined above. It will result in improved returns for retirement fund members and should be seen as a counterpart to the proposed limitations on tax deductibility of retirement fund contributions by high-income individuals.

Simplifying retirement fund thresholdsThe tax rules permitting lump sum withdrawals upon retirement are overly complex, resulting in unnecessary compliance costs. To alleviate these difficulties, government will simplify the tax system for lump sum withdrawals. To streamline the tax administration process, withholding taxes on lump sum retirement fund payments to persons with taxable income of less than R43 000 per year (the revised income tax threshold) will be abolished.

Streamlining the tax regulatory regime for retirement fundsRetirement funds have to comply with two sets of regulatory legislation, making for an unnecessarily complex regulatory landscape. A streamlined tax administration environment will reduce the indirect costs incurred by retirement fund members, resulting in improved retirement savings. As a first step, regulatory requirements contained in the Income Tax Act and related regulatory notes will effectively be moved to the Pension Funds Act. This will result in reduced regulatory costs without sacrificing oversight.

Foreign collective investment schemesIt has come to government’s attention that foreign collective investment schemes in the hands of long-term insurers are inadvertently subject to a higher level of tax than schemes held directly by beneficiaries. Changes in policyholders’ portfolio preferences can result in foreign collective investment schemes moving in and out of the controlled foreign company regime. This places a large administrative burden on the scheme’s manager to monitor such movements. Legislative amendments to alleviate the higher tax and compliance burden will be introduced.

Lump sum death benefitsThe Income Tax Act provides for certain lump sums paid in respect of the death caused by an occupational injury to be tax-free. However, payments of a similar kind made outside the Compensation for Occupational

Budget and Tax Update 2007

5

Injuries and Diseases Act (1993) framework are as a rule subject to income tax. It is proposed that payments in respect of death while at work be tax-free up to a monetary cap of R300 000.

GROWTH BUSINESS DEVELOPMENT AND JOB CREATION

Reform to the taxation of dividendsWhile dividend taxes are a familiar feature of taxation worldwide, they are typically imposed at a shareholder level, with treaty relief for foreign investors. In South Africa, secondary tax on companies (STC) is provided at the company level as opposed to the shareholder level. Only two other countries, Estonia and India, have a formal dividend tax liability at the company level.

This has meant that international summaries of company tax rates have typically compared the combined company and dividend tax rate in South Africa with the company tax rate in other countries. If compared on a like basis and SA’s combined rate in 2006 is compared with that of the OECD countries, SA would have the 7th lowest rate out of 31.

International investors are also more familiar with a dividend tax at the shareholder level and often enjoy double tax treaty limitations on a dividend tax at this level. That is to say, double tax treaties limit the dividend tax imposed at the shareholder level but not at the company level.

It is widely argued that SA’s STC raises the cost of equity financing to the detriment of economic growth. To help lower the cost of doing business, government proposes to phase out STC and replace it with a dividend tax.

This reform will happen in two phases. The 1st phase takes effect from 1 October 2007 and the 2nd from 2008, depending on the renegotiation of certain double tax treaties. An anti-avoidance measure is also announced with immediate effect.

Anti-avoidance measure

With effect from 21 February 2007 the STC exemption for amalgamation transactions contained in section 44(9) of the Income Tax Act, is withdrawn. This exemption permits a permanent loss of STC, rather than a deferral of tax, which is the intent of the amalgamation provisions.

First phase - 1 October 2007

• STC will be renamed as a dividend tax at company level

• The tax base will be broadened to cover all distributions by companies and not just those from profits, since the determination of what constitutes profits available for distribution can be a complex and uncertain area of SA law. Provision will be made for the tax free return of capital but anti-avoidance provisions will have to address inflated or transitory capital contributions.

• The tax rate will be reduced from the current 12.5% to 10%.

• A more targeted exemption for amalgamation transactions will be introduced, depending on an analysis of the transactions concerned.

Second phase - commencing in 2008

• The formal legal liability for the dividend tax will be moved from the company paying the dividend to the shareholder receiving it.

• The administrative enforcement will be through a withholding tax at company level whereby the company will have to withhold tax of 10% on dividend payments which they must pay to SARS on behalf of the shareholder. The implementation of this phase will depend on the renegotiation of several international tax treaties. The negotiations are aimed at the small number of treaties that provide for a 0% withholding tax rate for substantial shareholders. The negotiations are aimed at ensuring that SA has the right to impose a withholding tax of at least 5% in these cases.

It is envisaged that the withholding tax will be a final withholding tax and that companies paying dividends will have to determine whether a reduced tax rate applies as a result of the application of a double tax treaty.

Taxation of gains on long-term equity investments

Budget and Tax Update 2007

6

Profits realised on the sale of shares can be taxed either as ordinary income or capital gains, depending on facts and circumstances. The current legislation has resulted in some large institutions receiving capital gains tax treatment on the sale of shares, and many other players paying ordinary income tax. In order to provide equitable treatment, all shares disposed of after three years will trigger a capital gains tax event. This proposal will not affect the ordinary income tax treatment of executive employee share schemes. Anti-avoidance rules will be introduced to prevent taxpayers from transferring new assets into shareholdings held for the three year period. The above proposal will take effect on 1 October 2007.

Depreciation allowancesThe tax regime related to depreciation of fixed and moveable assets will be reviewed to ensure a greater degree of consistency. The following interim amendments are proposed.

Rail locomotives, wagons and port assets

One way of reducing the cost of doing business in South Africa is to improve the efficiency of transport networks and ports. It is proposed to reduce the tax depreciation periods for new rail locomotives and rail wagons from 14 years to 5 years. It is also proposed that new quay walls and other port facilities qualify for deductions over 20 years. This would match other infrastructure depreciation periods, such as those applying to aircraft runways.

Commercial buildings

The Income Tax Act provides for the depreciation of buildings used for manufacturing and similar processes. However, it does not provide for tax depreciation for certain commercial buildings. It is proposed that tax depreciation allowances for the economic wear-and-tear of newly constructed commercial buildings (and upgrades) be implemented. It is envisaged that the rate will be 5% per year (write-off period 20 years).

Environmental capital expenses

In line with global trends, South African businesses are increasingly subject to environmental regulatory oversight. However, the Income Tax Act has not kept abreast of the importance of expenditure in this regard. Environmental capital structures (such as dams and tanks) are often not depreciable. In addition, environmental clean-up, restoration and decommissioning are often seen as non-deductible capital expenditures. It is proposed that the above capital expenditures qualify for depreciation allowances or immediate deductions, depending on the circumstances.

Corporate reorganisation and BEE transactionsAn important issue for black economic empowerment (BEE) transactions is the ability of BEE partners to raise financing. Amendments to the Income Tax Act are proposed to ensure that BEE and other similar restructurings do not encounter undue additional tax costs that could undermine necessary financing. Discussions with key role players have revealed the following six areas of concern:

• Share cross-issues: Many BEE structures involve the cross-issue of shares. In some structures, the operating company issues ordinary shares to the BEE entity. In return, the BEE entity issues preference shares (which operate as a quasi-loan) to the operating company. If the ordinary shares reach a predetermined value, the BEE entity sells a portion of the ordinary shares for cash and redeems the preference shares. Rules are required to ensure that the ultimate dual dispositions do not give rise to unwarranted gain while simultaneously ensuring that the proposed structure does not trigger artificial losses.

• Share buybacks of listed shares: BEE restructurings of listed shares frequently involve a two-step transaction. Shares are first purchased from the public before transfer to BEE partners pursuant to a forced sale via section 311 of the Companies Act (1973). Many of those parties forced to sell their listed shares (especially management) then repurchase identical listed shares on the market from non-BEE participants. At issue is the tax triggered on the forced sale for those parties who simply use sale proceeds to repurchase identical shares. It is proposed that these parties be free from tax to the extent that timely repurchases leave them in the same economic position as before.

• Anti-avoidance financial instrument company provisions: While the company rollover rules have gradually changed to accommodate ongoing transactions, recurring problems exist in respect of anti-avoidance rules for companies that mainly contain financial instruments. These anti-avoidance rules were designed to ensure that company restructurings were limited to active companies. However, the calculations required are often

Budget and Tax Update 2007

7

excessively burdensome and often add little value in preventing real avoidance. It is proposed that the financial instrument rules be deleted to the extent possible and/or be mitigated in favour of a simpler anti-avoidance mechanism.

• Intra-group transfers: The company restructuring rules allow for the tax-free rollover of assets within a single group of companies as if the group were a single entity. However, this rollover treatment comes at the price of the de-grouping charge. The de-grouping charge essentially triggers tax on transferred intra-group assets once companies within the group become separated. While the need for the de-grouping charge is accepted, taxpayers have long sought to obtain time limits on its use. It is accordingly proposed that the de-grouping charge apply only if the group break-up occurs within six years after the intra-group asset transfer (in line with the system in the United Kingdom). This proposal will also require re-evaluation of the general ‘group of companies’ definition because certain transactions are giving rise to avoidance through artificial temporary arrangements. As a final matter, ongoing legislative relief is required for various intra-group anomalies (such as an alleged dual charge on transferred mining assets) and avoidance loopholes.

• Connected person sales of depreciable property: As a practical matter, the majority of BEE transactions involve BEE entities that obtain a 26% to 30% shareholding with the pre-existing company shareholder retaining a 70% to 74% shareholding. These situations largely receive relief through the intra-group rules discussed above. At issue are situations where BEE partners (especially with assistance of outsider investors) obtain ownership levels nearing 50%. In these situations, the transfer of depreciable assets to the BEE entity often becomes subject to certain anti-avoidance rules that prevent the BEE entity from depreciating newly obtained assets at currently existing market values. While the general need for these avoidance rules is accepted, it is proposed that these anti-avoidance rules accommodate situations where avoidance is unlikely to be the driver.

• Broad-based share incentive schemes: In 2004, government introduced a tax incentive to facilitate broad-based share employee ownership. As a result, employees can now receive up to R9 000 worth of shares tax-free over a three year period (with companies eligible for up to R3 000 of deductions per annum). This incentive was partly driven by the need to have more broad-based schemes that would include rank-and-file employees. Unfortunately, usage of the incentive appears to be minimal. This incentive will accordingly be reviewed for possible change.

In addition to the relief discussed above, a number of potential avoidance schemes involving corporate reorganisation rules have been identified. As mentioned above, immediate anti-avoidance provisions relating to STC are to be proposed with effect from 21 February 2007. Other potential concerns involving corporate reorganisation rules have been identified and additional measures may be proposed.

Public Benefit OrganisationsThe Income Tax Act allows individuals and companies to deduct donations made to qualifying public benefit organisations (PBOs) up to a maximum of 5% of their taxable income during the tax year. It is proposed that the threshold for tax-deductible donations be increased to 10% for both individuals and companies. The objective of this proposal is to encourage charitable contributions.

In 2005, government introduced a system of partial taxation for PBOs, accompanied by a tax-free income threshold of 5% of gross income or R50 000, whichever is the greater. This means that PBOs that conduct trading activities may continue to do so without losing their tax-exempt status. They will, however, pay income tax on income from trading activities exceeding the relevant threshold. Given the important role played by many PBOs, it is proposed to increase the R50 000 threshold to R100 000.

The tax treatment of national sporting codes that have separated their professional and amateur sporting arms into separate bodies has resulted in certain anomalies. Amendments are proposed to allow the professional and amateur bodies to merge their legal structures so that qualifying expenses incurred by the professional bodies to develop amateur sports can be deducted.

IMPLEMENTING THE MUNICIPAL PROPERTY RATES ACTThe Local Government Municipal Property Rates Act (2004) regulates municipalities’ powers to impose rates on properties. The act provides for the exclusion of certain properties from rates in the national interest; a transparent and fair system of granting relief measures; fair and equitable valuation methods; and objections and appeals processes. The act enhances certainty, uniformity and simplicity in the valuation and rating of properties.

Budget and Tax Update 2007

8

The act took effect on 2 July 2005, and municipalities have four years from this date to fully implement the legislation. However, only a few municipalities are currently implementing a new valuation roll and rating in terms of the act.

Implementation will require all municipalities to properly manage the transition from their old rating practices to the new system. A smooth transition is essential. Municipalities that historically have not rated on the market value of land and buildings combined are expected to reduce the rate charged (percentage or cents per rand) to ensure that there is broad continuity in revenue collected from the expanded tax base.

TAX REFORM MEASURES UNDER REVIEWWage subsidy and social security tax reformIntroduction of a wage subsidy is proposed by 2010. The objectives of such a subsidy are to reduce the direct costs of employment, help alleviate the high rate of joblessness among youth and facilitate the proposed social security reform process. For further discussion of how this aligns with proposed social security reforms, see Chapter 6 of the 2007 Budget Review.

It is envisaged that SARS will administer the social security tax and wage subsidy. As this will be a payroll-based tax and the subsidy will be paid to employers, the PAYE system will, to a large extent, be used as the administrative platform. In addition, SARS will have to gather more specific and regular information about employees, as the tax will require that records be kept to match details of contributing and eligible employees. The challenges that will arise from these large-scale fiscal and institutional arrangements will be taken into account in the SARS modernisation programme.

Small business developmentGovernment policy remains focused on reducing the tax compliance burden for businesses, especially small businesses, to promote entrepreneurship, the formalisation of informal businesses, economic growth and job creation. The National Treasury and SARS have commissioned a small business tax compliance cost study. The results of this study should also support the development of a more simplified tax regime for very small businesses to be introduced in 2008.

MEASURES TO ENHANCE TAX ADMINISTRATIONRecent years have seen a substantial growth in the tax base and, consequently, the volume of work for SARS. At the same time, there is also need for a broader and more integrated tax register to improve the view of potential taxpayers and to simplify registration. SARS has begun modernising its systems and processes, using the benefits of automation and e-business to become more cost effective, to better manage risk and to improve the quality of service. In 2007/08 SARS will place greater emphasis on e-filing, re-engineering of forms, scanning and imaging and greater reliance on third party data to speed up document processing.

SARS has committed to adopting the World Customs Organisation Framework of Standards, resulting in the need to re-engineer business processes and to draft new customs legislation over the medium term. A formal discussion paper on these matters will be released in 2007.

In addition to specific industry focus areas, SARS has identified three cross-industry areas as focal points for 2007/08. These are:

• Trusts, because of their continued use to avoid tax. Initiatives will include greater cooperation with the Master’s office to register trusts and identify risk cases, and the allocation of more specially trained auditors.

• The undervaluation and understatement of stock, which will involve additional audit activity and verification.

• Employees’ tax. Dedicated audit teams have been established and trained to counter abuses in this area.

Small business tax amnesty

Budget and Tax Update 2007

9

The 2006 Budget announced a small business tax amnesty to facilitate the entry of marginalised small businesses into the economic mainstream and to help non-compliant small businesses to regularise their tax affairs and thus avoid potential penalties in future.

Amnesty applications may be made until 31 May 2007. By 13 February 2007, the unit had received 47 489 enquiries and 11 301 amnesty applications. The inflow of applications compares favourably with the exchange control amnesty of 2003/04, in which application volumes peaked in the final weeks of the application period. It is anticipated that the pace of applications for the present campaign will gather pace in the coming weeks and as awareness continues to be raised about the benefits of this process for small businesses.

Small business amnesty as applied to trustsSome technical issues have risen regarding the application of the small business tax amnesty in respect of certain types of trusts. These issues may have to be clarified by legislative amendment depending on the facts.

MISCELLANEOUS AMENDMENTS - INCOME TAX ACT, 1962

Residential accommodation fringe benefitsResidential accommodation provided by an employer to an employee is a fringe benefit unless provided to an employee when the employee is away from the employee’s usual place of residence. This ‘place of residence’ test is wrongfully being applied on a basis similar to the concept of ‘country of residence’. As a result, foreign residents are arguing that accommodation provided by employers to foreign residents for their entire stay within South Africa is not a taxable fringe benefit even if those foreign residents regularly work at a single South African location. The law will be amended to eliminate this interpretation.

Exemption for South Africans working abroadSouth African residents working abroad for more than 183 days over a 12-month period are exempt from income tax on remuneration for services rendered while abroad. However, if a person has rendered services during a 12-month period that meets the requirements (i.e. more than 183 days abroad of which 60 days are for a continuous period) but the remuneration for these services accrues or is received in a later year of assessment during which the 12-month period does not commence or end, the remuneration will not be exempt. This mismatch typically arises in the case of share incentive schemes. The current exemption will be amended to correct the above inconsistency.

Streamlining the medical regimeThe tax regime for medical deductions (especially contributions to medical schemes) was fundamentally changed in 2006. One key aspect of this change was a shift from the two-thirds deduction formula to monthly ceilings, thereby enhancing the equity aspects of this concession. While this change was fundamentally sound, administrative and compliance hurdles continue to arise that may require legislative intervention.

Incorporation of professional partnerships involving part-time membersIn order for audit firms to comply with recent regulatory legislation, certain audit firms need to incorporate their consulting and advisory activities. However, it has come to government’s attention that tax may stand as a barrier to some of these incorporations. Under present law, some incorporations may not be eligible for tax-free rollover relief because certain partners will neither hold the requisite 20% shareholding nor participate on a full-time basis in the business of the newly created company. Legislative amendments may be undertaken, depending on the available facts.

Permissible use of buildings benefiting from the urban development zone incentiveIn 2003, government introduced a tax incentive to encourage the development and renovation of selected urban centres. This incentive is available for buildings that are used solely for trade purposes. The question

Budget and Tax Update 2007

10

has arisen as to impact of the incentive if an urban development zone building was used for purposes other than trade before renovation occurred. The law will be clarified in this regard.

Schemes to avoid the reduction of assessed losses upon indirect debt compromises or concessionsSpecial provisions exist to reduce company assessed losses to the extent that a company’s debts are relieved via compromises or concessions from the lender. Certain taxpayers argue that this reduction of assessed loss can be avoided through indirect means. The law will accordingly be clarified to eliminate this argument.

Foreign companies with South African activitiesForeign companies are subject to different rates of South African tax, depending on the level of their South African activity. Foreign companies with South African sourced income are subject to the standard 29% tax rate, but a higher tax rate applies (34%) if the foreign company generates the income through a South African branch or agency. This higher rate (acting as a proxy for the STC) should apply regardless of whether the foreign company maintains a local branch or agency.

Foreign taxpayers receiving passive South African interest and/or royaltiesForeign taxpayers with passive South African interest income are exempt from tax while passive South African royalties are subject to a flat 12% withholding charge. However, the two tests for distinguishing passive versus active status differ. It is accordingly proposed that both tests be harmonised.

Loans made in respect of emigrating South African residentsTo protect the South African tax base against erosion through the use of loans to South African residents by foreign residents, the tax system disallows the deduction of interest on excessive loans of this nature. However, this anti-avoidance rule may not apply if a loan is made by a South African resident who becomes a foreign resident immediately after the loan is made. This and similar loopholes will be closed.

Changing status of controlled foreign companiesSpecial rules apply when foreign companies acquire or lose controlled foreign company (CFC) status (such as the deemed disposal treatment for capital gains tax purposes). Technical anomalies continue to arise in this area, especially when a chain of foreign companies gain or lose CFC status simultaneously (thereby creating conflicting deemed sale dates for the different foreign companies in the chain). Clarification in this area is required.

Deductibility of foreign taxesSouth African controlled foreign activities are often subject to foreign tax in addition to South African tax. The South African tax system provides clear guidelines for obtaining foreign tax credits, but the law is less clear whether South Africans can deduct foreign taxes if no credit is available (or if a deduction is preferred). It is proposed to freely allow deductions for foreign taxes in lieu of credits.

Ambiguous foreign currency cross-referencesTwo sets of corresponding rules exist for the taxation of currency gains and losses – one for ordinary gain/loss and the other for capital gain/loss. Upon review, it appears that the technical wording of the capital gain/loss currency rules generates confusion due to reliance on cross-references to the ordinary gain/loss currency provisions. This use of cross-references will be removed in favour of more explicit rules.

National sports organisations

Budget and Tax Update 2007

11

National sports organisations typically have a professional arm and an amateur arm. Some organisations have split these two arms into separate entities in order to enjoy public benefit organisation status for the amateur arm. In certain cases, however, this split has proven to be to the organisation’s disadvantage. Measures will be considered to assist with the reintegration of these different arms.

Simplifying the averaging formula for individual farmersThe income-averaging formula for farmers is complex, especially for newly commencing operations. It is proposed to simplify the thresholds within the commencing formula as a first step toward greater simplification.

General anti-avoidance ruleA wholly revised general anti-avoidance rule was approved by Parliament in 2006. Initial indications are that the new rule has already discouraged impermissible tax-avoidance arrangements. However, it would also appear that the new rule is under intense scrutiny by some in an effort to circumvent it. The practical operation of the general anti-avoidance rule will be monitored with appropriate amendments to ensure its effectiveness.

Provisional payment systemThe provisional tax system is problematic in terms of enforcement and compliance ease. Effective provisional tax systems should be simple and require minimal audit intervention. Amendments to the provisional tax system will be considered in order to add certainty, minimise compliance and administrative burdens, and to ensure a coherent penalty/interest structure. Any legislative amendments will become effective only after sufficient time is permitted for taxpayers and SARS computer system changes.

Refund paymentsRefunds of overpaid taxes by cheque result in delays, continue to be subject to fraudulent negotiation and impose significant costs on SARS. In view of the Mzansi initiative to provide bank accounts for low-income earners and the fact that fewer than 2 500 refunds in 2006 were to taxpayers who did not have access to a bank account, consideration will be given to requiring that refunds be made directly into taxpayers’ bank accounts on a similar basis to refunds in terms of the Value-Added Tax Act (1991).

Employee share optionsIn 2004, government substantially revised the tax treatment of share options to prevent executives and other high-income employees from receiving tax preferences for consideration that effectively represents deferred salary. Share-option schemes continue to generate issues that require minor legislative adjustment.

Reciprocal tax relief for sportspersonsFrom July 2006, income earned by foreign visiting entertainers or sportspersons performing within South Africa became subject to South African withholding tax. While this form of taxation is consistent with international norms, some countries provide various forms of reciprocal relief in the case of international tournaments (i.e. involving teams from multiple countries). These countries legislatively elect not to tax foreign visiting sportspersons playing in their countries on condition that the foreign home country provides a similar exemption on the other side. Restated, source taxation is waived in favour of residency country taxation as long as that waiver is reciprocal. Legislation may be considered so that South African sportspersons can benefit from this reciprocity principle.

Employee tax relief for sole proprietorsIn 2006, government acknowledged that the anti-avoidance rules safeguarding employee withholding taxes may have introduced excessive rigidities for small business operators. The 2006 legislative relief involved the

Budget and Tax Update 2007

12

removal of the automatic ‘deemed employee’ triggers, such as: (i) client control or supervision over hours of service performance and over the manner in which duties are performed and (ii) regular payments. However, the above sets of relief applied solely to small businesses operating as trusts and companies. Comparable relief was inadvertently omitted for small businesses operating as sole proprietors. This oversight will be corrected.

MISCELLANEOUS AMENDMENTS – VALUE-ADDED TAX ACT, 1991

E-commerce downloadsThe VAT system operates on a destination basis, thereby taxing goods and services consumed within South Africa. This principle theoretically requires South African users of e-commerce downloads to pay VAT and for foreign providers to register for VAT. There is a growing international trend to require foreign e-commerce suppliers of services to register as VAT vendors in countries in which they supply services. The practical implications of requiring these suppliers of services to register within South Africa will be considered with regard to international practice.

Nominal or passive foreign-controlled local activitiesThe VAT Act prescribes that persons must register as vendors if those persons conduct enterprises and make taxable supplies that exceed or are likely to exceed R300 000 in a 12-month period. This prescription applies equally to domestic and foreign persons. That said, VAT registration for nominal or certain wholly passive activities of foreign persons is impractical when the supply is made to domestic VAT vendors. It is therefore proposed that scope be provided to allow relief in order not to discourage foreign investment and trade.

Dried maizeThe supply of dried maize for human consumption, animal feed or as seeds is zero-rated. On the other hand, the supply of dried maize from one vendor to another for resale is standard-rated unless it is a zero-rated supply. The tax treatment by the supplying vendor depends on the ultimate consumption of the recipient, which is often outside the vendor’s control and probable knowledge. In order to simplify matters, it is proposed that all supplies of dried maize be eligible for zero-rating regardless of the recipient’s intended consumption.

Streamlining business reorganisationsThe Income Tax Act provides extensive relief for company reorganisations (mergers, intra-group transfers and liquidations, etc). The VAT rules indirectly provide relief but further clarification is required. It is proposed that the VAT rules be fully examined in relation to all forms of company reorganisations sanctioned by the Income Tax Act, thereby legislatively remedying any inconsistencies between the two tax systems.

Insurance versus financial servicesShort-term insurance products are generally subject to VAT, whereas long-term insurance products are regarded as financial services that are exempt. At issue is the uncertainty in terms of modern financial practices, especially given the fact that many financial services (such as guarantees) are designed to guard against risk much like insurance products. It is proposed that this distinction be legislatively clarified.

Bare dominium financing structuresIt was mentioned in last year’s Budget that certain taxpayers were entering into bare dominium structures designed to disguise actual financial services as rental payments, thereby misusing the statutory exception to the financial services definition. As a result input credits are claimed even though no subsequent taxable supplies are made. The investigation has now been completed and the VAT implications will be clarified by legislative amendment.

Budget and Tax Update 2007

13

Transfer among rental pool membersA rental pool administrator acts as a VAT representative for the unit owners and is accordingly conducting an enterprise on their behalf. At issue is the VAT treatment of the transfer of units between rental pool members where the unit remains in the rental pool. Theoretically, these transfers should be regarded as going concerns and hence zero-rated. However, due to the current provisions of the VAT Act, the supply of the unit does not qualify as a going concern. It is proposed that legislation be enacted to this effect.

Horse-racing industryIn the horse-racing industry, a number of persons typically have joint ownership of one horse. The financial affairs of the racehorse owners are managed by an administrator. For the sake of administrative simplicity, consideration will be given to treating racehorse administrators as a VAT representative on behalf of the racehorse owners, much like the situation for rental pooling arrangements. Due to difficulties in establishing the tax status of each racehorse owner, the winnings paid by racing operators to racehorse owners are regarded as a single supply. As such, consideration will also be given to zero-rating such supply.

Game-viewing clarificationIt has always been intended that game-viewing drives should be treated as a taxable supply at the standard rate. However, some practitioners are taking positions that undermine this intent due to possible weakness in the technical language. Legislative clarity will be provided to ensure that the supply of game viewing is fully subject to VAT.

Foreign diplomat resale of local purchased vehiclesForeign diplomats receive VAT refunds in respect of locally purchased vehicles and are exempt from tax on importation of imported vehicles. If the foreign diplomats dispose of these vehicles within two years of purchase or importation, rules exist that require partial or full recoupment of the VAT under certain circumstances. This recoupment ensures that foreign diplomats do not receive unfair benefits. The law will be amended to ensure that the rules for the recoupment of VAT on locally purchased vehicles mirror those for imported vehicles. Rules will also be required to ensure that local VAT vendors do not receive notional input credits on these vehicles to the extent foreign diplomats benefit from unrecouped VAT refunds.

Change of use adjustments of fixed propertyVAT-registered property developers acquiring fixed property for resale claim VAT input credits on purchase and levy VAT on the subsequent sale of the property. On the other hand, residential leasing is an exempt activity and therefore no VAT input credits are allowed for fixed property acquired for residential rental purposes. While this rule is fundamentally sound, problems arise when developers change the use for which the property was originally acquired, i.e. from resale to rental. The change of intent should result in a VAT adjustment.

Improper use of turnover apportionment methodCircumstances often arise when a VAT vendor makes mixed supplies of goods or services (some subject to VAT, others exempt). In these situations, questions often arise as to the nature of input credits for purchases to the extent that those purchases cannot be directly allocated to a specific output (i.e. general overheads). Current law provides for a general written ruling prescribing the turnover-based method as being the default method of apportionment. Vendors may, however, use another method if the turnover method does not give an equitable result. Consideration will be given to similarly allow the Commissioner to prescribe another method of apportionment if the turnover-based method does not give an equitable result.

Duty-free shops

Budget and Tax Update 2007

14

Under current administrative practice, South African and foreign travellers benefit from zero-rating when purchasing goods at South African duty-free shops on the basis that these goods are being exported. Although this result is consistent with the destination principle for VAT, legislation is required to support this practice. The VAT Act will be amended accordingly.

Clarifying payment datesVAT requires different payment dates depending on the means of payment (e.g. cash or electronic transfer). However, lack of legislative clarity exists as to the payment dates for the different electronic payments. It is accordingly proposed that the VAT Act be amended to eliminate this confusion.

Documentary evidence for input taxSupporting documentation when claiming input credits is a critical element of a sustainable VAT system. While legislation generally requires this documentation, there are legislative ambiguities in the case of deemed supplies. The VAT Act will be amended to ensure that full documentation requirements exist in terms of deemed supplies (e.g. requiring proof of the claimed amount and the reasons of entitlement) as well as limiting such entitlement to the prescribed five-year period.

Documentary evidence for zero-rated exportsUnder current administrative practice, VAT vendors must provide proper documentation within a three-month period in order to receive zero-rating for exports. Lack of timely documentation results in subsequent standard rating, but VAT vendors may subsequently claim the VAT as input tax if the documentation follows within another nine-month period. Current practice will be clarified in legislation with some possible refinements depending on comments received.

Electronic storage of cheques, bank deposit slips and other documentsModern technology increasingly allows for the effective electronic storage of information. While the tax law generally accounts for this shift, certain relics remain. One relic is the ongoing VAT requirement to maintain paper originals of cheques for a five-year period. This paper requirement is costly for the vendors and inefficient in terms of data searches. It is accordingly proposed to allow for the destruction of paper cheques if digital images (or microfilm) are maintained for the same five-year period (similar to the income tax).

PENSION FUNDS ACT, 1956

Forced early withdrawals from retirement fundsRetirement fund members may be forced to surrender all or part of their retirement fund interests while still being a member of the fund. These forced surrenders may stem from a variety of events, such as housing loan payments and defaults as well as divorce and maintenance orders. Lack of clarity in the law often means that the forced surrender is effectively deferred until a member’s final retirement or withdrawal from the fund. This delayed surrender gives rise to unnecessary tax complications. The Pensions Act will be amended to clarify that the forced withdrawal triggers an immediate severance from the fund (as opposed to a delayed severance upon retirement or withdrawal). Corresponding changes will also be made to the Income Tax Act.

Defining annuity paymentsWhile the term ‘annuity’ has legal meaning in the case law, the term ‘annuity’ lacks precise statutory definition. This definition is critical for determining the tax impact of guaranteed and living annuities, thereby requiring clarification.

Living annuity drawdowns

Budget and Tax Update 2007

15

Currently, living annuities allow pensioners to withdraw retirement funds at an accelerated rate. This rate varies between a 5% minimum to a 20% maximum. However, accelerated withdrawals of this nature often leave pensioners with insufficient funds. In order to limit drawdowns in line with market factors, it is proposed that the permissible drawdown range be shifted to a low of 2.5% and a high of 17.5%.

INTERNATIONAL COOPERATION FOR ENHANCED CROSS-BORDER ENFORCEMENTSouth Africa has an extensive network of treaties for the avoidance of double taxation, which include provisions for the exchange of information and assistance in the collection of taxes. In a regional context, the number of South African businesses active in neighbouring jurisdictions (and vice versa) has highlighted the need for improved mechanisms for implementation of these treaty enforcement provisions. SARS will therefore explore memoranda of understanding with neighbouring jurisdictions in order to achieve more efficient outcomes. This increased level of administrative cooperation will assist in countering avoidance and abuse in respect of the region’s tax systems (such as artificial dual residence, transfer pricing and non-declaration of foreign income). This increased level of administrative cooperation will also accelerate resolution of differences in the interpretation and application of tax treaties as they arise.

INDIRECT TAX PROPOSALS

Fuel taxesThe general fuel levy will be increased by 5 cents with effect from 4 April 2007 to 121 cents per litre on petrol and 105 cents per litre for diesel. The Road Accident Fund levy increases by 5 cents per litre from 36.5 cents per litre to 41.5 cents per litre.

Duties on beverages and tobacco productsDuties on alcoholic beverages are increased by between 8% and 10.5% with the exception of traditional beer which enjoys no increase.

Excise duties on tobacco products will be increased by between 5.3% and 10.7% for all categories of tobacco products. This increases the cost of a 340ml can of malt beer by 5 cents and packet of 20 cigarettes by 52 cents.

Budget and Tax Update 2007

16

TAX UPDATE

DEVELOPMENTS OVER THE LAST YEAR

The Small Business Tax Amnesty and Amendment of Taxation Laws Act 9 of 2006 and Second Small Business Tax Amnesty and Amendment of Taxation Laws Act 10 of 2006 were both promulgated on 25 July 2006. These Amending Acts introduce the small business tax amnesty and in addition deal mainly with the proposals made in the February 2006 Budget speech.

The Revenue Laws Amendment Act 20 of 2006 was promulgated on 7 February 2007 and deals with amendments to the Income Tax Act, Value-Added Tax Act, Transfer Duty Act, Estate Duty Act, Stamp Duty Act, Uncertificated Securities Tax Act and Unemployment Insurance Fund Act. We will cover what are felt to be the more relevant changes.

The Revenue Laws Second Amendment Act 21 of 2006 was promulgated on 7 February 2007 and deals with further amendments to the same Acts referred to above.

Interpretation notes issued in 2006 and early 2007:30 Jan 2007 38 Application and cost recovery fees for binding private rulings

24 Jan 2007 37 Procedures for requesting binding effect in respect of written statements issued by the Commissioner prior to 1 October 2006

24 Jan 2007 36 Scope and impact of section 76I upon written statements issued by the Commissioner prior to 1 October 2006

7 Mar 2006 35 Employees’ tax: Personal Service Companies, Personal Service Trusts and Labour Brokers

12 Jan 2006 34 Exemption from Income Tax: Remuneration derived by a person as an officer or crew member of a ship

Draft interpretation notes issued in 20066 Dec 2006 Learnership allowances, section 12H

23 Nov 2006 Documentary proof required to substantiate a vendor’s entitlement to apply the zero rate to the supplies of goods or services

25 July 2006 Public Benefit Organisations (PBO’s): Trading rules – Partial taxation of trading receipts

19 July 2006 VAT treatment of the supply of goods and services by a municipality

Income tax brochures released by SARS in 2006 and early 2007

Feb 2007 Guide on the deduction of medical expenses

2006 Advanced tax rulings, detailed guide to binding private rulings

2006 Advanced tax rulings, a quick guide to binding private rulings

Sept 2006 Urban development zones, section 13quat

July 2006 Residence basis of taxation for individuals

July 2006 Tax guide on small business

June 2006 Tax guide for foreigners working in South Africa

May 2006 Draft comprehensive guide to secondary tax on companies

Budget and Tax Update 2007

17

March 2006 Income tax and the individual

March 2006 Draft transfer duty handbook

Feb 2006 Tax guide for share owners

The interpretation notes and brochures will not be covered in these notes but can be obtained from the SARS website: www.sars.gov.za.

THE SMALL BUSINESS TAX AMNESTY AND AMENDMENT OF TAXATION LAWS ACT 9 OF 2006 AND SECOND SMALL BUSINESS TAX AMNESTY AND AMENDMENT OF TAXATION LAWS ACT 10 OF 2006

The notes that follow draw extensively from the Explanatory Memorandum on the Small Business Tax Amnesty and Amendment of Taxation Laws Bill, 2006.

Small Business Tax Amnesty

Government has recognised that small businesses play an important role in stimulating economic activity, job creation, poverty alleviation and the general improvement of living standards. Many small businesses operate informally, were historically marginalised and were excluded from the economic mainstream, thus remaining outside of the tax system. It is believed that these small businesses are now keen to regularise their tax affairs but an obstacle is their past non-compliance and the resultant potential tax liabilities, penalties and interest.

The Commissioner’s tax-base broadening efforts and ‘walkabouts’ in informal business areas have indicated that numerous small businesses are not on register or have not made full disclosure to the Commissioner and would like the opportunity for regularisation without fear of tax liabilities arising out of past non-compliance. This also includes taxi operators who want to participate in the taxi recapitalisation program.

The purpose and objective of the tax amnesty is, therefore, to:

• broaden the tax base;

• facilitate the normalisation of the tax affairs of small businesses;

• increase and improve the tax compliance culture; and

• facilitate participation in the taxi recapitalisation programme.

A separate unit within SARS, with regional presence, has been established to process all applications on a confidential basis. To this end, the secrecy provisions of section 4 of the Income Tax Act, 1962, are extended to cover applications for tax amnesty. Section 4 now applies to every person ‘employed or engaged’ by the Commissioner in carrying out the amnesty provisions.

Persons who may apply for amnesty

• a natural person (including the deceased or insolvent estate of a natural person);

• an unlisted company (including a close corporation) that was unlisted throughout the qualifying period and all the shares or members’ interests in the company were held directly by natural persons (including the deceased or insolvent estate of a natural person) throughout the 2006 year of assessment.

• a trust (inter vivos and testamentary) and all the beneficiaries (discretionary and vested) of that trust throughout the 2006 year of assessment were natural persons (including the deceased or insolvent estate of a natural person).

Budget and Tax Update 2007

18

To qualify for amnesty the requirements are that-

• the person must have carried on a business;

• the gross income of the business (or businesses if the person carried on more than one business) for the 2006 year of assessment was not more than R10 million, but if that person’s financial year was not 12 months the amount of R10 million must be adjusted proportionally, and for this purpose a part of a month must be regarded as a full month.

Method and period of application

An applicant must apply for amnesty with the Commissioner on a form SBA-001 and delivered together with all supporting schedules to any SARS office. Application forms must be submitted at any time during the period 1 August 2006 to 31 May 2007.

Information required in the application

The applicant must, in the application, disclose the taxable income in respect of all amounts received by or accrued to (or deemed to have been received by or accrued to) that applicant from the carrying on of business during the 2006 year of assessment.

The applicant must, together with the application for tax amnesty (or within such later period as the Commissioner may allow) furnish-

• an income tax return for the 2006 year of assessment; and

• a statement of all assets (at cost) and liabilities of that applicant as at the end of the 2006 year of assessment.

If it is not possible for the applicant to provide full particulars of any actual amounts in the application or in any return or statement relating to the application, the applicant may provide reasonable estimates of those amounts and must disclose that the amounts provided are estimates. It is important that any estimate provided is not materially wrong as this is one of the circumstances that could result in an approval being void.

Evaluation and approval

The Commissioner must approve an application only if the applicant-

• is a qualifying person as defined above;

• applies on the correct form to the correct address within the period prescribed above;

• provides all the prescribed information.

An application may not be approved if the Commissioner has, before the submission of the application, formally notified the applicant of an audit, investigation or other enforcement action relating to any failure by that applicant to comply with any Act in respect of which application for tax amnesty is made.

This disqualification falls away if the Commissioner has, before the submission of the application for tax amnesty, formally notified the applicant that-

• the notice of audit, investigation or other enforcement action has been withdrawn; or

• the audit or investigation has been concluded.

The Commissioner must deliver to the applicant a notice of his decision to approve or deny the application for tax amnesty and must set out the reasons for any decision to deny that application.

Review of Commissioner’s decision

An applicant whose application for tax amnesty is denied by the Commissioner may object and appeal against that decision in terms of Part III of Chapter III of the Income Tax Act, including the alternate dispute resolution procedures. In addition the tax court has the jurisdiction to hear any appeal against a decision of the Commissioner.

Budget and Tax Update 2007

19

Amnesty Levy

The successful applicants must pay an amnesty levy. The amnesty levy is based on a sliding scale rate and is applied to the taxable income of the applicant for the 2006 year of assessment to the extent that the taxable income is attributable to any amount derived by the applicant from the carrying on of business.

The rates to be applied in the calculating of the tax amnesty levy are-

• 0% of so much of the taxable income as does not exceed R35 000;

• 2% of so much of the taxable income as exceeds R35 000 but does not exceed R100 000;

• 3% of so much of the taxable income as exceeds R100 000 but does not exceed R250 000;

• 4% of so much of the taxable income as exceeds R250 000 but does not exceed R500 000;

• 5% of so much of the taxable income as exceeds R500 000.

In determining the tax amnesty levy no regard must be had to the balance of any assessed loss or assessed capital loss carried forward from any year of assessment preceding the 2006 year of assessment.

The 2006 year of assessment means the year of assessment ending during the period 1 April 2005 to 31 March 2006.

Example of levy calculation

Facts: Mr. A is employed by company B and earns employment (salary) income of R200 000 for the 2006 year of assessment. During this period Mr. A also conducted the business of selling household chemicals to clients after hours. He started the business in 2001 and has never disclosed it to SARS. The turnover of this business is R400 000 for the 2006 year of assessment. His expenses in relation to his business amount to R100 000 for that year. At the end of the 2005 year of assessment Mr. A had an assessed loss of R20 000. Mr. A furthermore earned rental income of R5 000 on the use of his holiday cottage for a month by a friend during the 2006 year of assessment.

Calculation of the tax amnesty levy

Taxable income from carrying on business:

R400 000 less R100 000 (expenses) = R300 000

0% up to R35 000 = R0, 2% of amount over R35 000 and up to R100 000 = R1 300, 3% of amount over R100 000 and up to R250 000 = R4 500, 4% of amount over R250 000 and up to R300 000 = R2 000 Total tax amnesty levy = R7 800

• The employment (salary) income of R200 000 will not be taken into account for purposes of calculating the tax amnesty levy.

• The rental income of R5 000 will not be taken into account for purposes of calculating the tax amnesty levy as it is not attributable to the carrying on of business.

• The assessed loss of R20 000 for the 2005 year of assessment will not be set off against Mr. A’s taxable income for the 2006 year of assessment.

Payment of tax amnesty levy

The levy must be paid to the Commissioner within 12 months from the date on which the notice of approval was delivered to the applicant or a longer period as the Commissioner may allow.

Scope of the tax amnesty relief

If an application for tax amnesty is successful, the applicant is granted relief from the payment of-

• income tax in terms of the Income Tax Act, in respect of any amounts received by or accrued to (or deemed to have been received by or accrued to) the applicant in all years of assessment preceding the 2006 year of assessment from the carrying on of a business. For purposes of the amnesty provisions, ‘carrying on of a business’ includes the earning of investment income incidental to the regular carrying on of a business;

Budget and Tax Update 2007

20

• employees’ tax in terms of the 4th Schedule to the Income Tax Act, in respect of remuneration as defined in that schedule paid to employees on or before 28 February 2006. Please note the word ‘paid’ does not cover amounts unpaid on 28 February 2006 even though they may be due and payable;

• value-added tax in terms of the Value-Added Tax Act, in respect any supply or importation of goods or services on or before 28 February 2006;

• withholding tax on royalties in terms of the Income Tax Act, in respect of any amount paid to a non-resident on or before 28 February 2006;