Embed Size (px)

Citation preview

SeminarVAT Act 2013

Tax

September 2013

Strictly Privateand Confidential

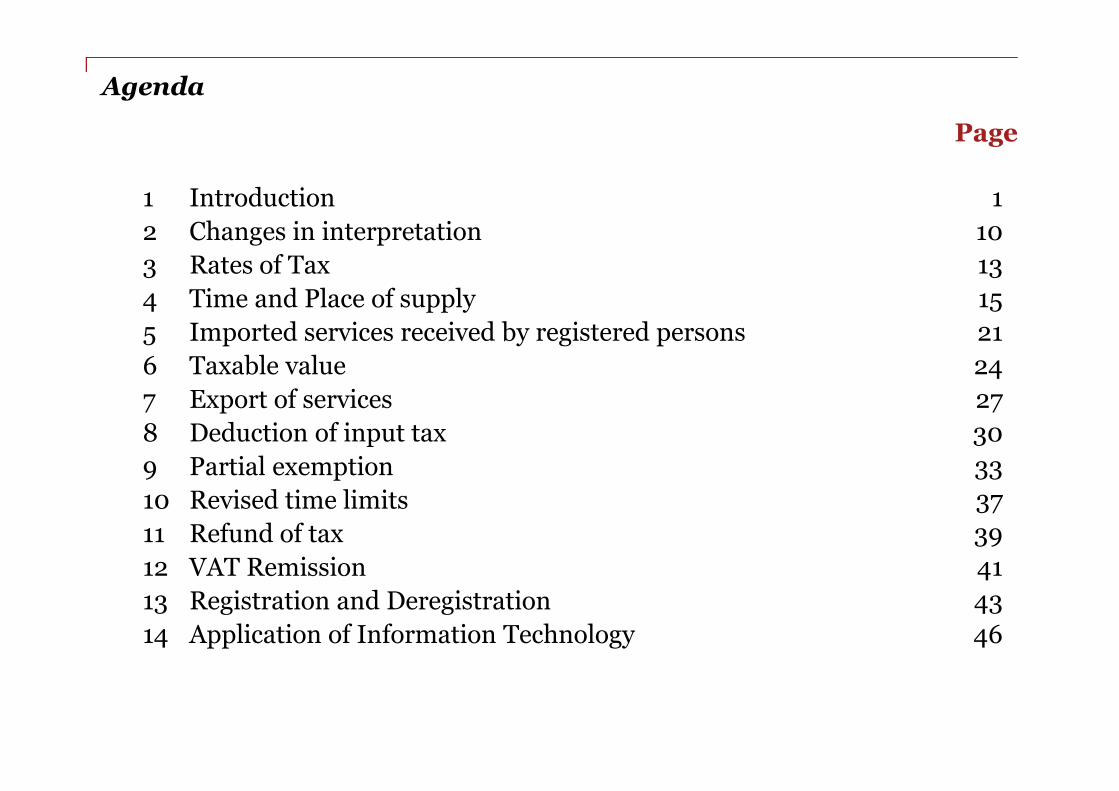

Agenda

1 Introduction 1

2 Changes in interpretation 10

3 Rates of Tax 13

4 Time and Place of supply 15

5 Imported services received by registered persons 21

6 Taxable value 24

7 Export of services 27

8 Deduction of input tax 30

9 Partial exemption 33

10 Revised time limits 37

11 Refund of tax 39

12 VAT Remission 41

13 Registration and Deregistration 43

14 Application of Information Technology 46

Page

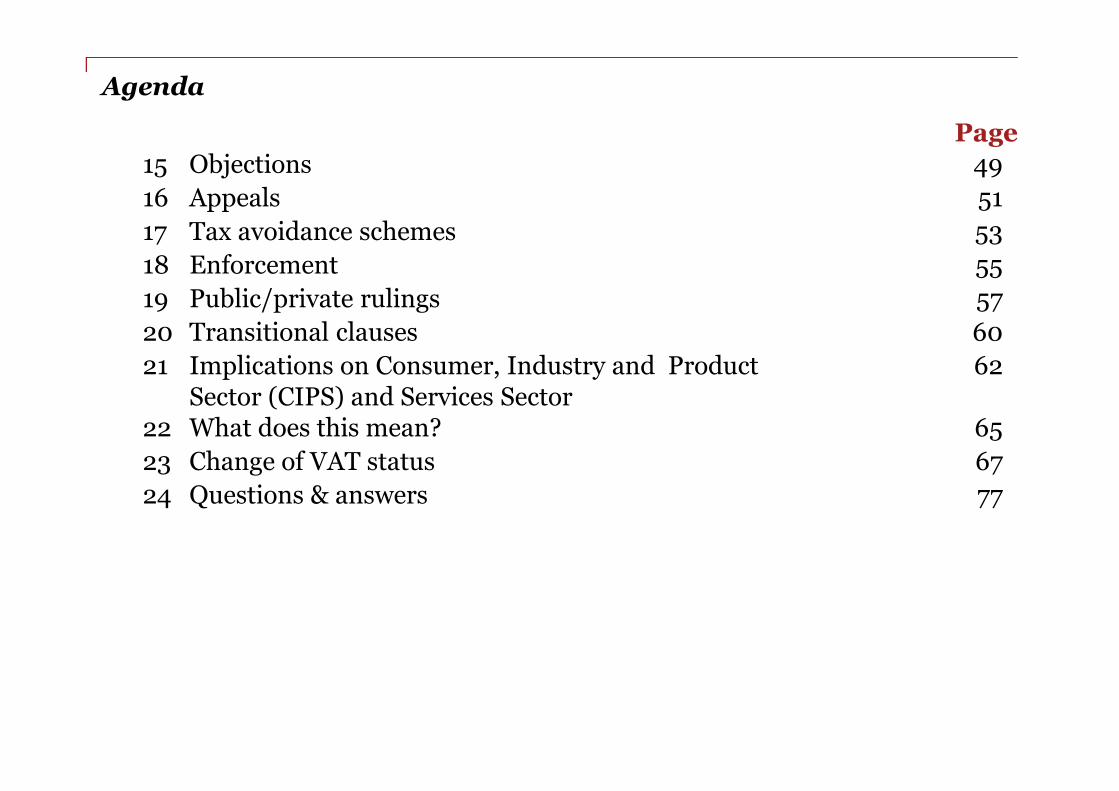

Agenda

15 Objections 49

16 Appeals 51

17 Tax avoidance schemes 53

18 Enforcement 55

19 Public/private rulings 57

20 Transitional clauses 60

21 Implications on Consumer, Industry and ProductSector (CIPS) and Services Sector

62

22 What does this mean? 65

23 Change of VAT status 67

24 Questions & answers 77

Page

PwCSeptember 2013

Introduction

1

Seminar • VAT Act 2013

PwCSeptember 2013

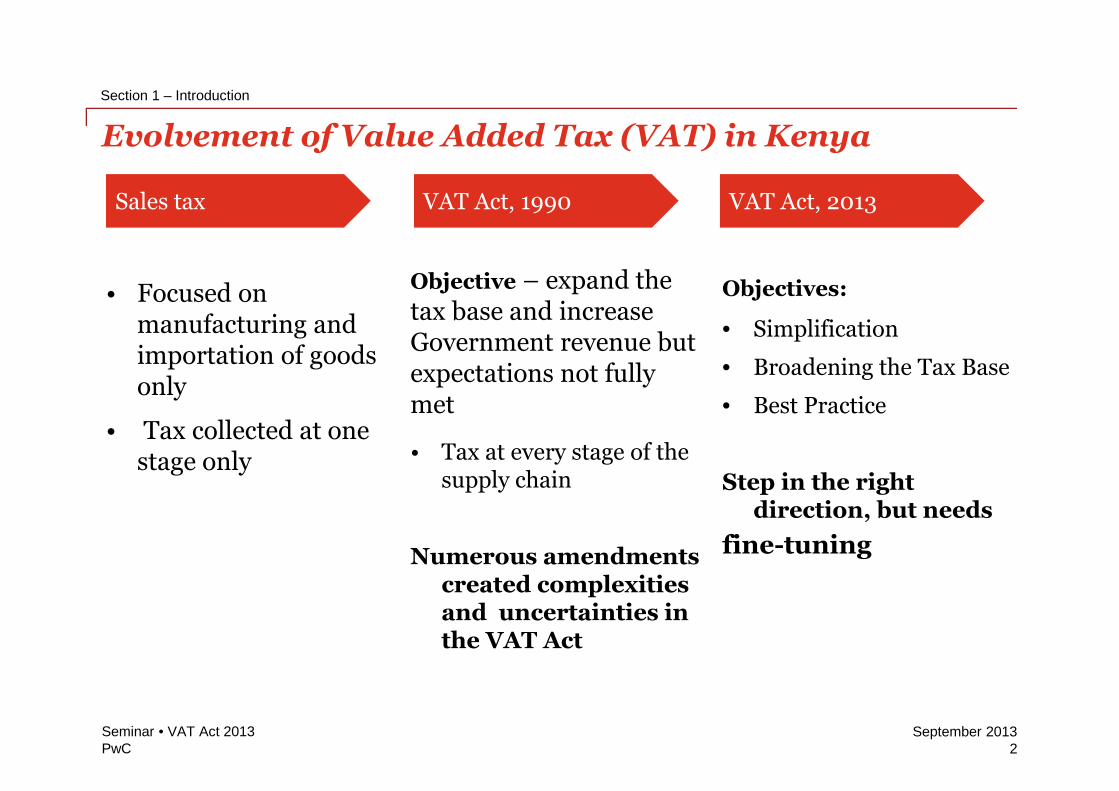

• Focused onmanufacturing andimportation of goodsonly

• Tax collected at onestage only

Objective – expand thetax base and increaseGovernment revenue butexpectations not fullymet

• Tax at every stage of thesupply chain

Numerous amendmentscreated complexitiesand uncertainties inthe VAT Act

Objectives:

• Simplification

• Broadening the Tax Base

• Best Practice

Step in the rightdirection, but needs

fine-tuning

Evolvement of Value Added Tax (VAT) in Kenya

2Seminar • VAT Act 2013

Section 1 – Introduction

Sales tax VAT Act, 1990 VAT Act, 2013

PwCSeptember 2013

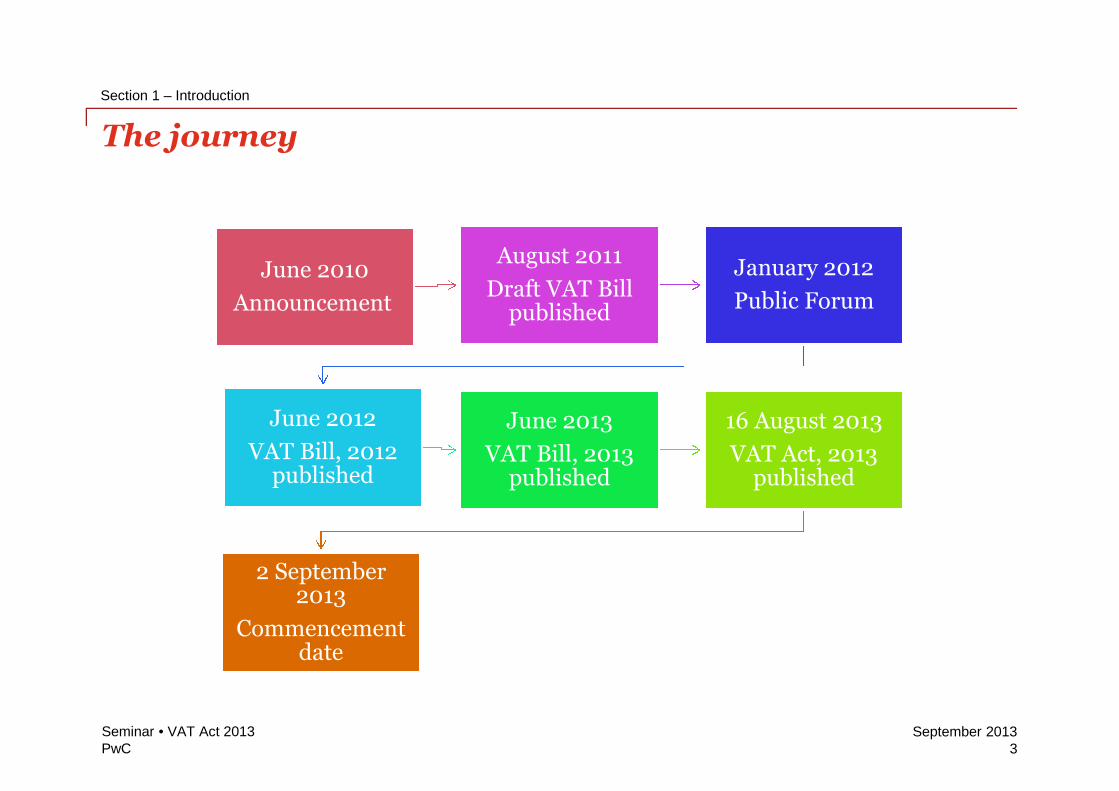

June 2010

Announcement

August 2011

Draft VAT Billpublished

January 2012

Public Forum

June 2012

VAT Bill, 2012published

June 2013

VAT Bill, 2013published

16 August 2013

VAT Act, 2013published

2 September2013

Commencementdate

The journey

3Seminar • VAT Act 2013

Section 1 – Introduction

PwCSeptember 2013

• Import/Export of services ;

• Simplified administrativeprocedures e.g. on transfer of abusiness as a going concern

Positive aspects

4Seminar • VAT Act 2013

Section 1 – Introduction

PwCSeptember 2013

• VAT status change on basiccommodities

• Abolition of VAT remission

Disappointments

5Seminar • VAT Act 2013

Section 1 – Introduction

PwCSeptember 2013

• Expansion of scope of business

• Persons covered

• Change in status of taxable supplies – shift to from zero/exempt to standard

Broadening the tax base

6Seminar • VAT Act 2013

Section 1 – Introduction

PwCSeptember 2013

Per the Repealed Act

Trade, commerce or manufacture or any concern in the nature of trade,commerce and manufacture;

VAT ACT,2013

a) Trade, commerce, manufacture, vocation or occupation;

b) Any activity carried on by a person continuously or regularly, whether or notfor gain or profit and which involves, in part or in whole the supply ofgoods or services for consideration; and

c) A supply of property by way of lease, licence, or similar arrangement.

Business

7Seminar • VAT Act 2013

Section 1 – Introduction

PwCSeptember 2013

An individual, company, partnership, association of persons, trust, estate, thegovernment, a foreign government, or a political subdivision of the governmentor foreign government

Company…

Company means a company as defined in the Companies Act or a corporatebody formed under any other written law including a foreign law.

Person …Now defined

8Seminar • VAT Act 2013

Section 1 – Introduction

PwCSeptember 2013

• Any person who supplies taxable goods or services for consideration will berequired to register for VAT ( subject to threshold)

The implications re business and persons

9Seminar • VAT Act 2013

Section 1 – Introduction

PwCSeptember 2013

Changes in interpretation

10

Seminar • VAT Act 2013

PwCSeptember 2013

11Seminar • VAT Act 2013

Section 2 – Changes in interpretation

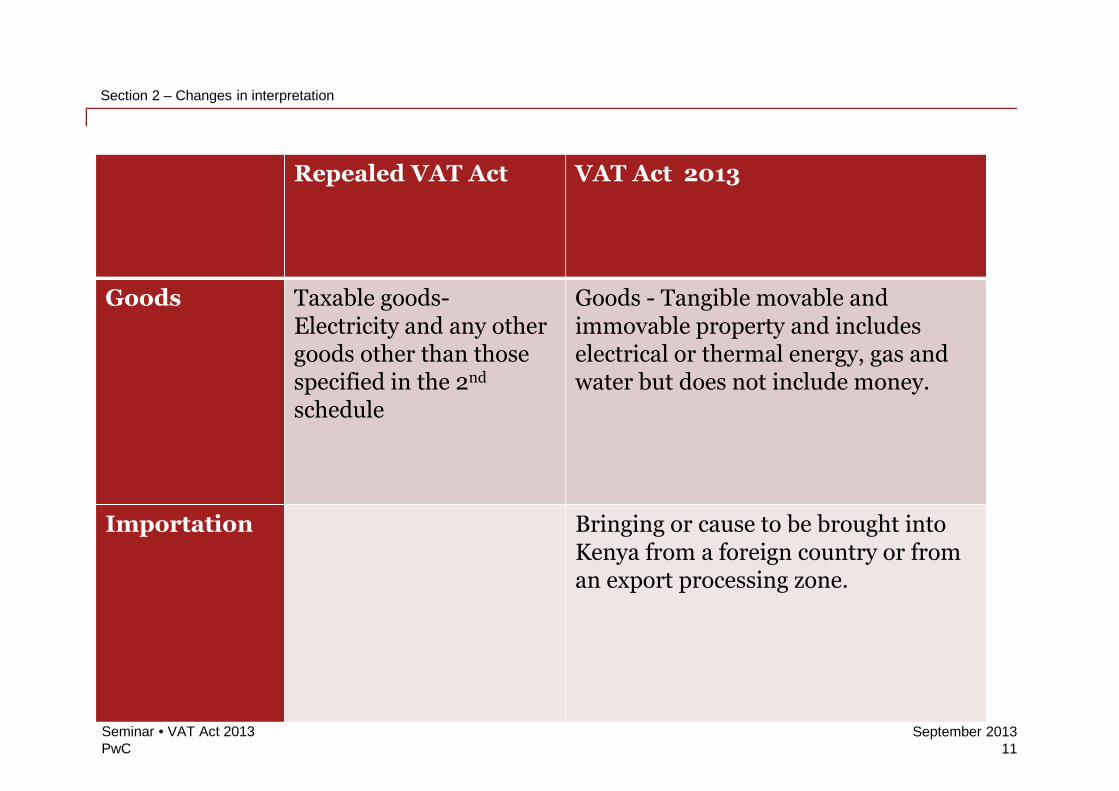

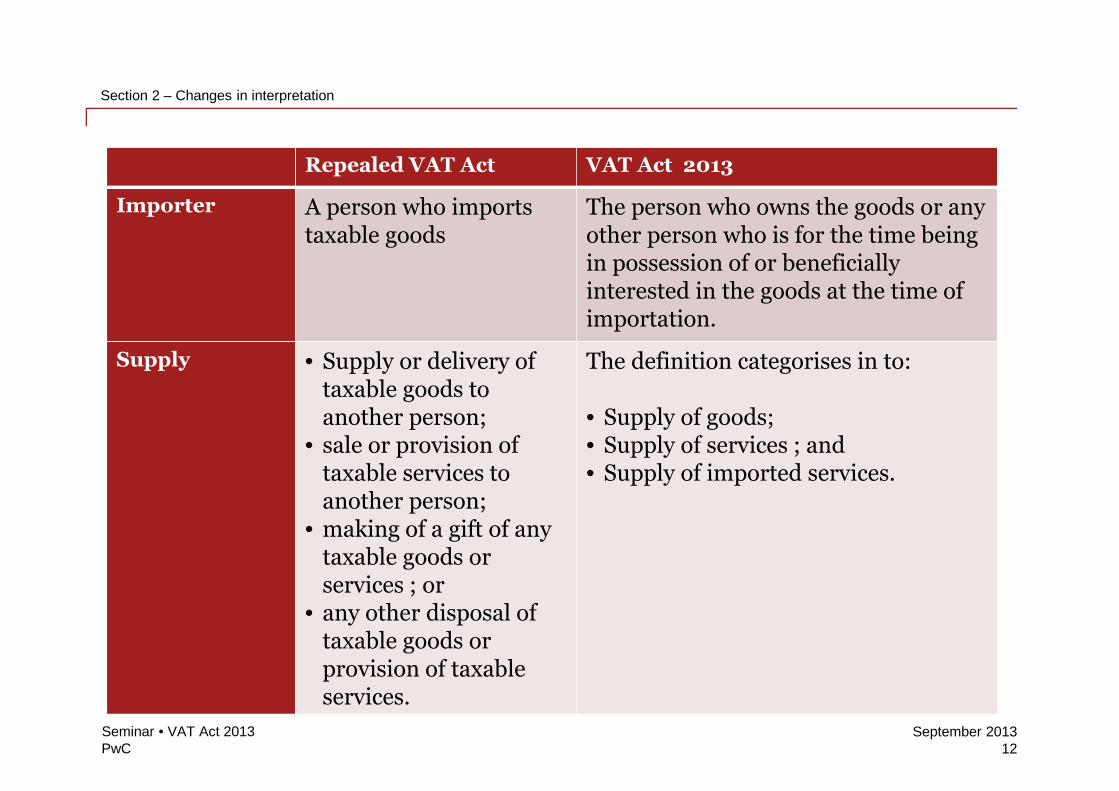

Repealed VAT Act VAT Act 2013

Goods Taxable goods-Electricity and any othergoods other than thosespecified in the 2nd

schedule

Goods - Tangible movable andimmovable property and includeselectrical or thermal energy, gas andwater but does not include money.

Importation Bringing or cause to be brought intoKenya from a foreign country or froman export processing zone.

PwCSeptember 2013

Repealed VAT Act VAT Act 2013

Importer A person who importstaxable goods

The person who owns the goods or anyother person who is for the time beingin possession of or beneficiallyinterested in the goods at the time ofimportation.

Supply • Supply or delivery oftaxable goods toanother person;

• sale or provision oftaxable services toanother person;

• making of a gift of anytaxable goods orservices ; or

• any other disposal oftaxable goods orprovision of taxableservices.

The definition categorises in to:

• Supply of goods;• Supply of services ; and• Supply of imported services.

12Seminar • VAT Act 2013

Section 2 – Changes in interpretation

PwCSeptember 2013

Rates of Tax

13

Seminar • VAT Act 2013

PwCSeptember 2013

• Two rates for VAT:

0% for zero rated supplies; and

16% for any other supply.

• 12% rate scrapped thereforeelectrical energy and industrial oilsnow taxable at 16%.

Rates of tax

14Seminar • VAT Act 2013

Section 3 – Rates of Tax

PwCSeptember 2013

Time and Place of supply

15

Seminar • VAT Act 2013

PwCSeptember 2013

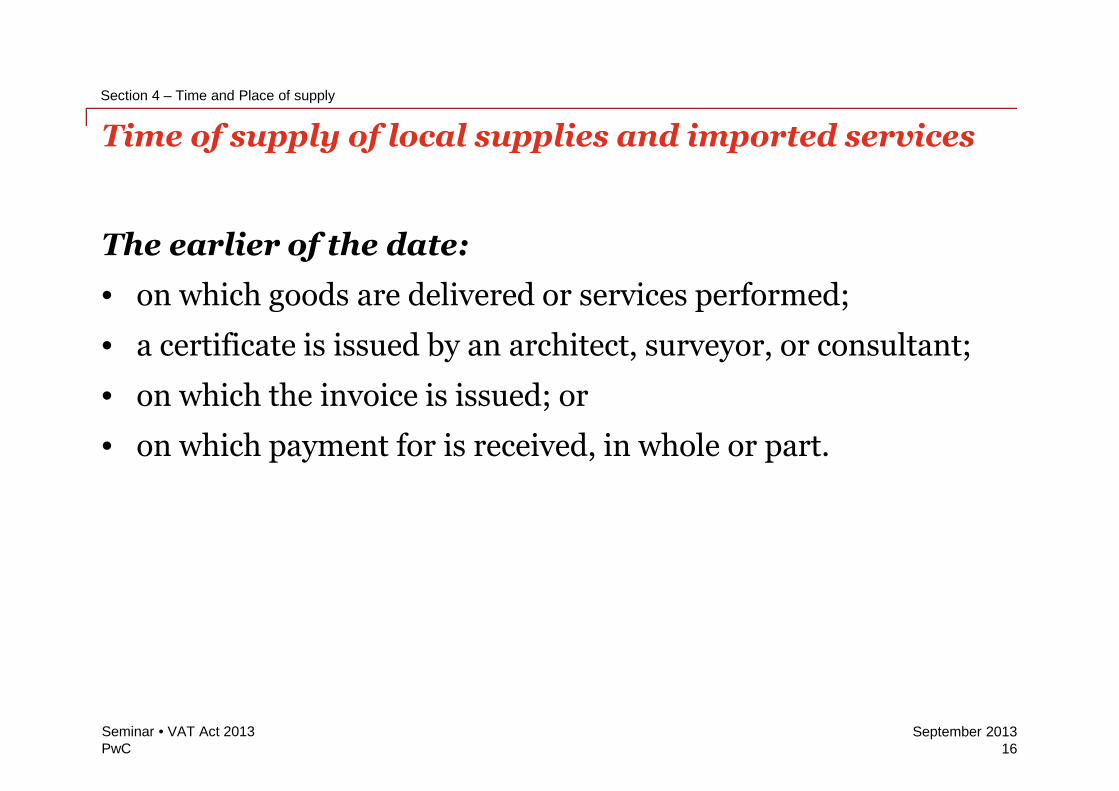

The earlier of the date:

• on which goods are delivered or services performed;

• a certificate is issued by an architect, surveyor, or consultant;

• on which the invoice is issued; or

• on which payment for is received, in whole or part.

Time of supply of local supplies and imported services

16Seminar • VAT Act 2013

Section 4 – Time and Place of supply

PwCSeptember 2013

17Seminar • VAT Act 2013

Section 4 – Time and Place of supply

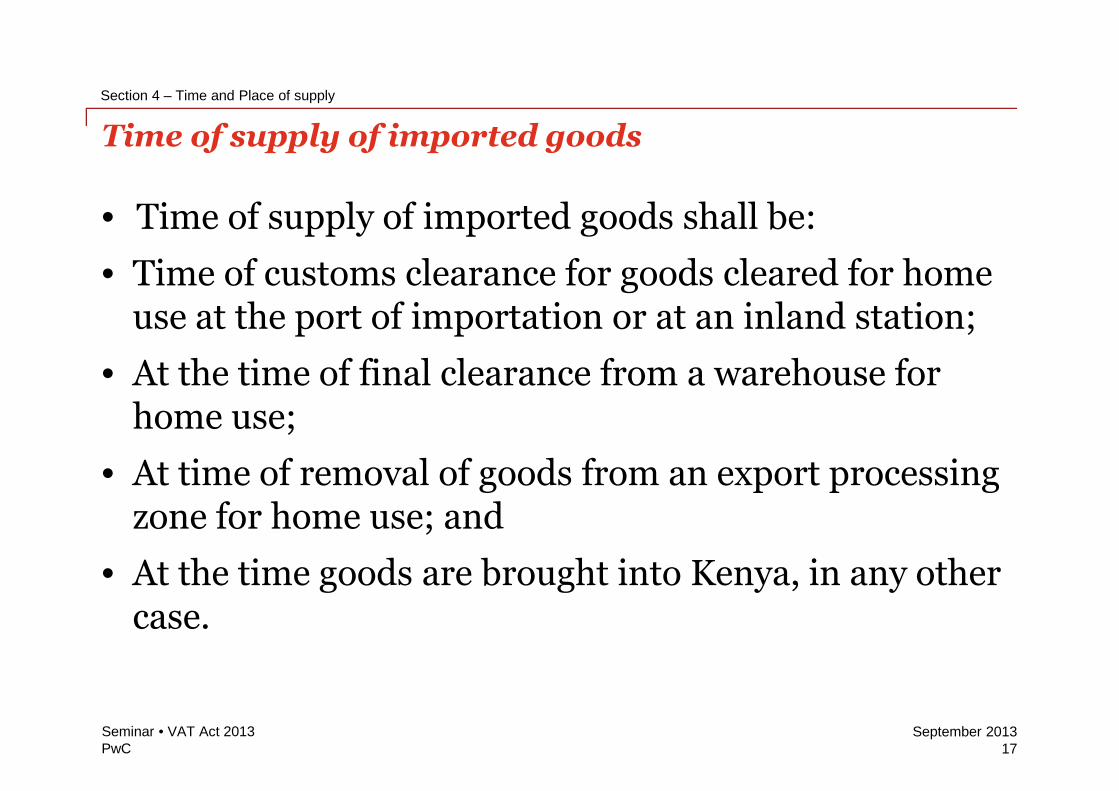

• Time of supply of imported goods shall be:

• Time of customs clearance for goods cleared for homeuse at the port of importation or at an inland station;

• At the time of final clearance from a warehouse forhome use;

• At time of removal of goods from an export processingzone for home use; and

• At the time goods are brought into Kenya, in any othercase.

Time of supply of imported goods

PwCSeptember 2013

18Seminar • VAT Act 2013

Section 4 – Time and Place of supply

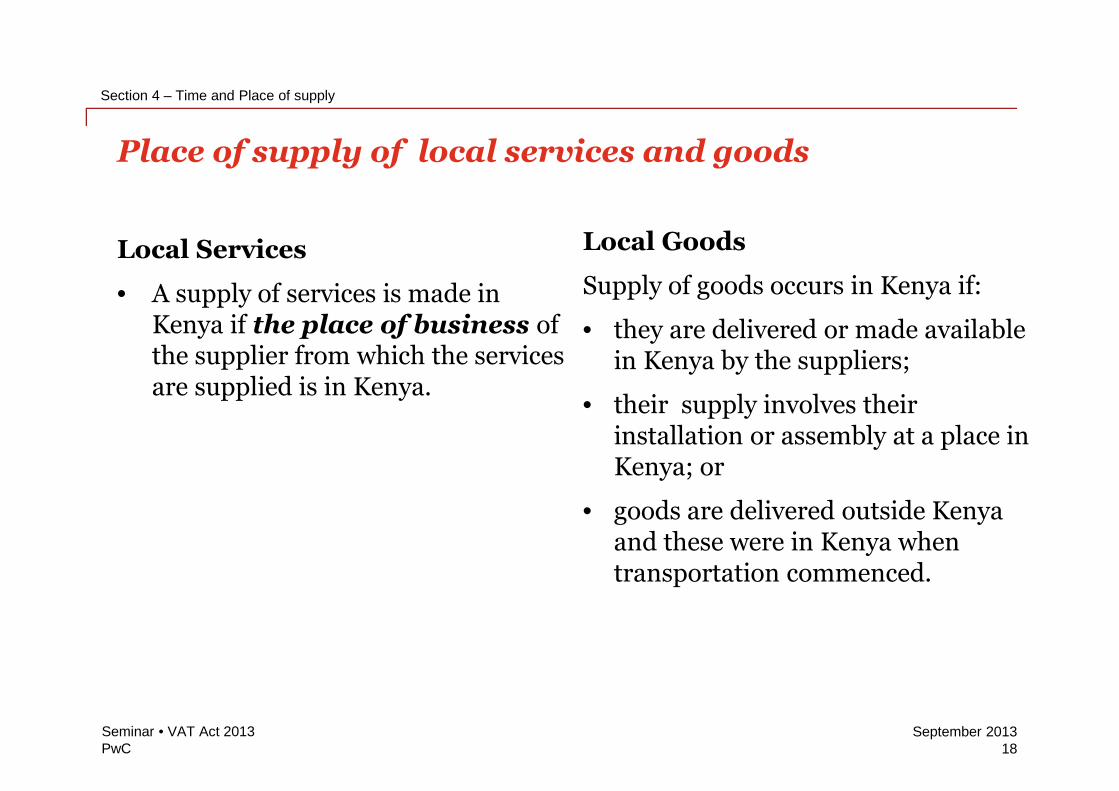

Local Services

• A supply of services is made inKenya if the place of business ofthe supplier from which the servicesare supplied is in Kenya.

Local Goods

Supply of goods occurs in Kenya if:

• they are delivered or made availablein Kenya by the suppliers;

• their supply involves theirinstallation or assembly at a place inKenya; or

• goods are delivered outside Kenyaand these were in Kenya whentransportation commenced.

Place of supply of local services and goods

PwCSeptember 2013

Section 4 – Time and Place of supply

19Seminar • VAT Act 2013

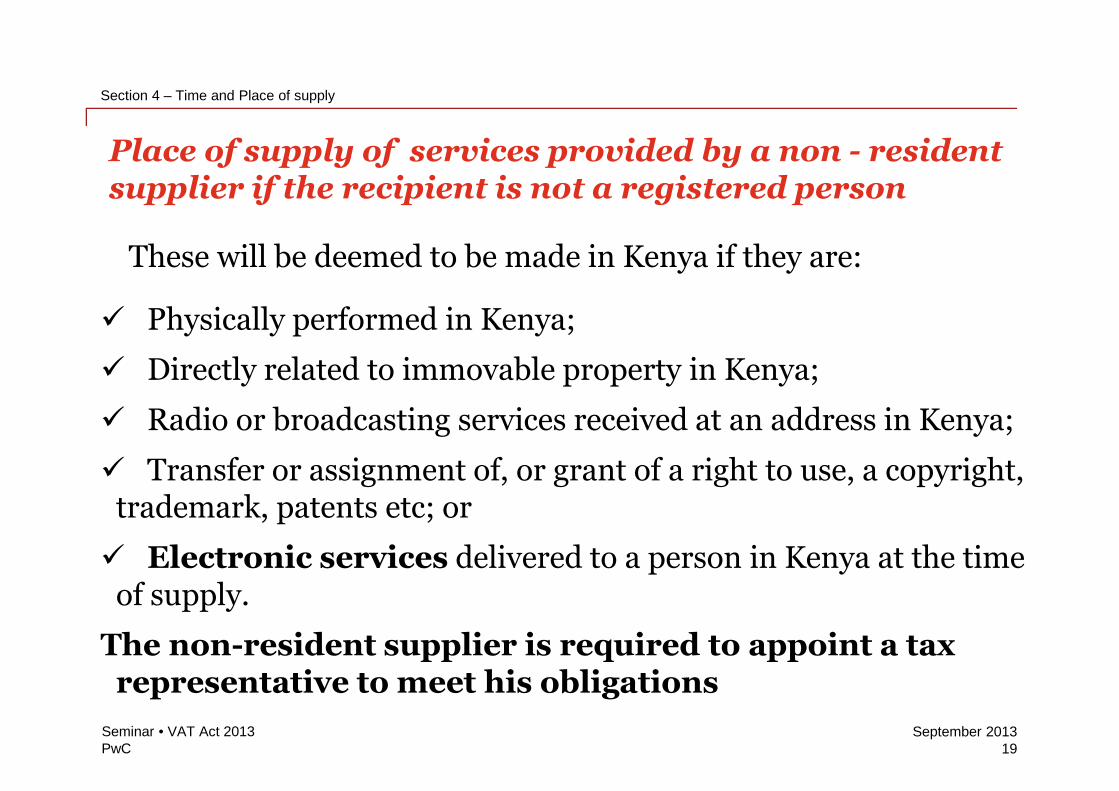

These will be deemed to be made in Kenya if they are:

Physically performed in Kenya;

Directly related to immovable property in Kenya;

Radio or broadcasting services received at an address in Kenya;

Transfer or assignment of, or grant of a right to use, a copyright,trademark, patents etc; or

Electronic services delivered to a person in Kenya at the timeof supply.

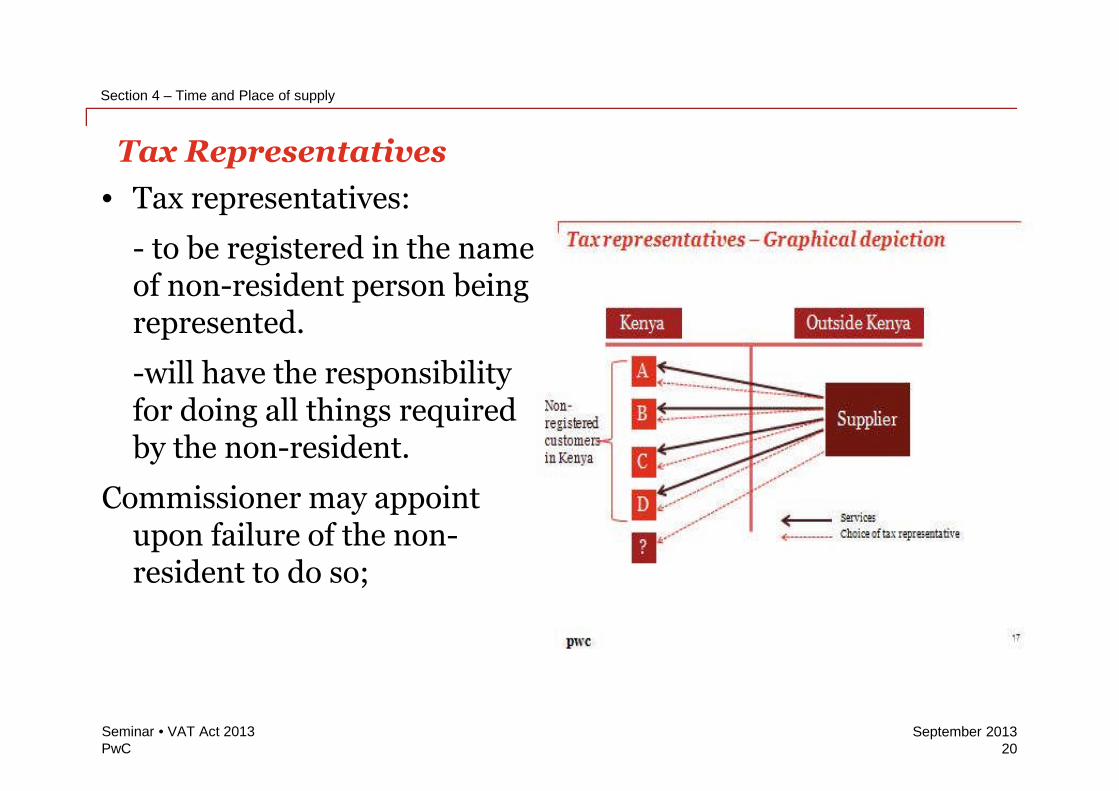

The non-resident supplier is required to appoint a taxrepresentative to meet his obligations

Place of supply of services provided by a non - residentsupplier if the recipient is not a registered person

PwCSeptember 2013

Section 4 – Time and Place of supply

20Seminar • VAT Act 2013

• Tax representatives:

- to be registered in the nameof non-resident person beingrepresented.

-will have the responsibilityfor doing all things requiredby the non-resident.

Commissioner may appointupon failure of the non-resident to do so;

Tax Representatives

PwCSeptember 2013

Imported services received byregistered persons

21

Seminar • VAT Act 2013

PwCSeptember 2013

Section 5 – Imported services received by registered persons

22Seminar • VAT Act 2013

Accounting for VAT

This will be accounted for as follows:

1. Fully taxable persons

Will get credit for full input tax payableby having the taxable value of theimported services reduced to zero andwill be accounted for as output in theVAT 3 return.

2. Mixed supplies persons

Registered persons will get credit forthe part of input tax that relates totaxable supplies.

VAT on imported services received by registered persons

A registeredperson will

be deemed tohave made a

taxablesupply tohimself.

PwCSeptember 2013

Section 5 – Imported services received by registered persons

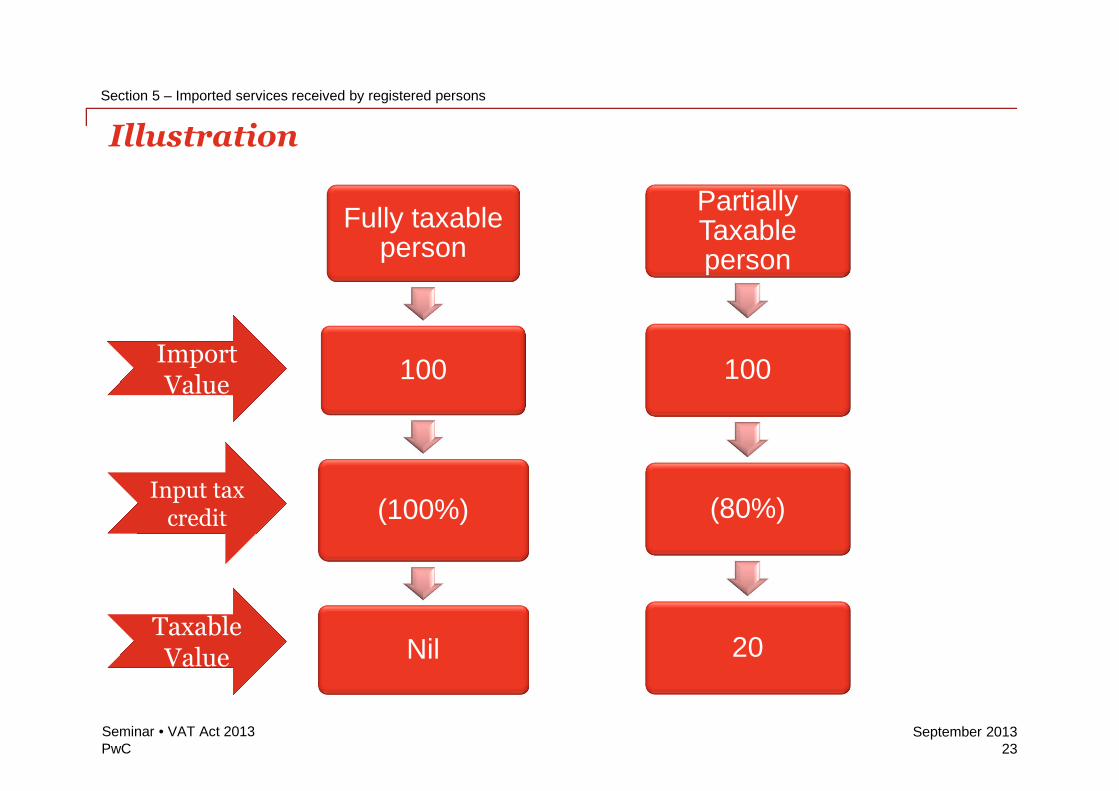

Fully taxableperson

100

(100%)

Nil

PartiallyTaxableperson

100

(80%)

20

ImportValue

Input taxcredit

TaxableValue

23Seminar • VAT Act 2013

Illustration

PwCSeptember 2013

Taxable value

24

Seminar • VAT Act 2013

PwCSeptember 2013

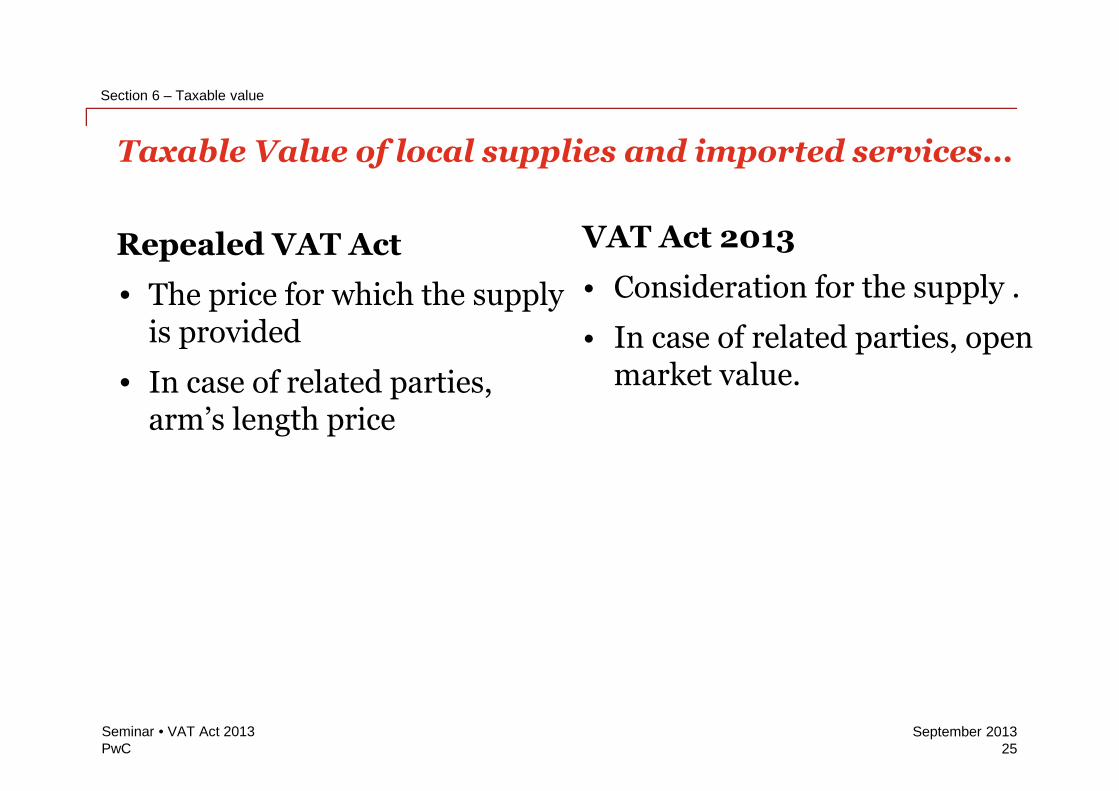

25Seminar • VAT Act 2013

Section 6 – Taxable value

Repealed VAT Act

• The price for which the supplyis provided

• In case of related parties,arm’s length price

VAT Act 2013

• Consideration for the supply .

• In case of related parties, openmarket value.

Taxable Value of local supplies and imported services...

PwCSeptember 2013

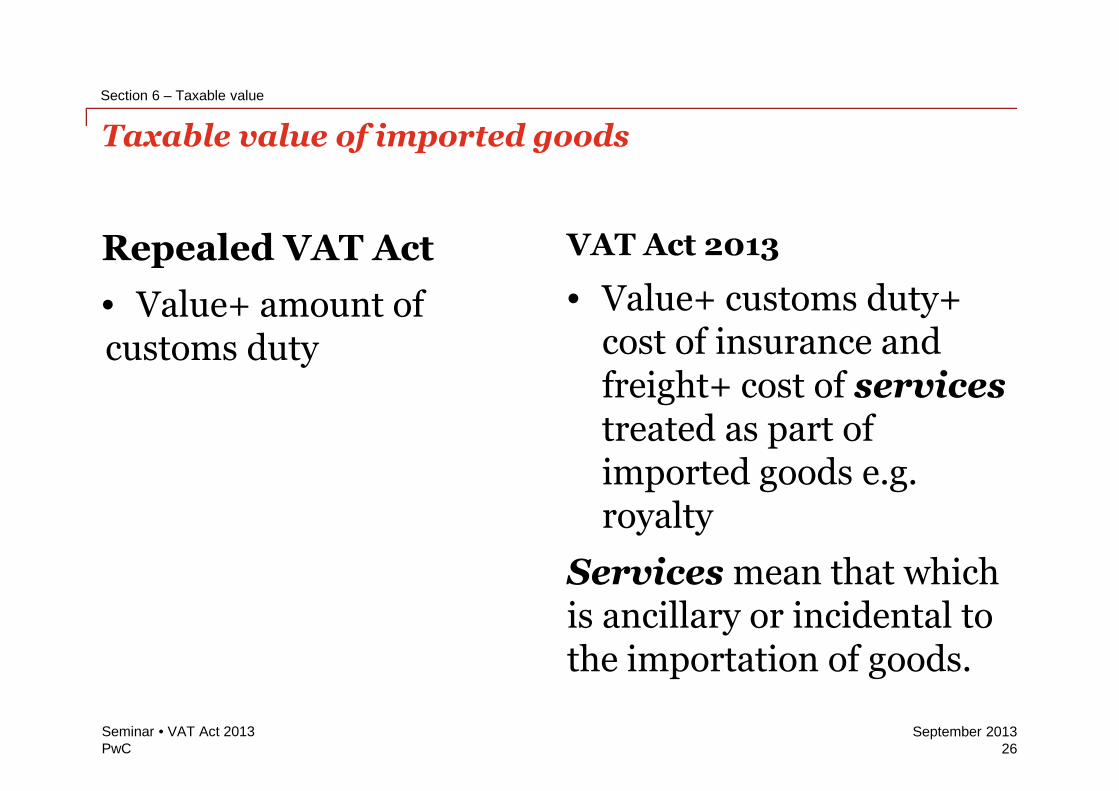

Repealed VAT Act

• Value+ amount ofcustoms duty

VAT Act 2013

• Value+ customs duty+cost of insurance andfreight+ cost of servicestreated as part ofimported goods e.g.royalty

Services mean that whichis ancillary or incidental tothe importation of goods.

Taxable value of imported goods

26Seminar • VAT Act 2013

Section 6 – Taxable value

PwCSeptember 2013

Export of services

27

Seminar • VAT Act 2013

PwCSeptember 2013

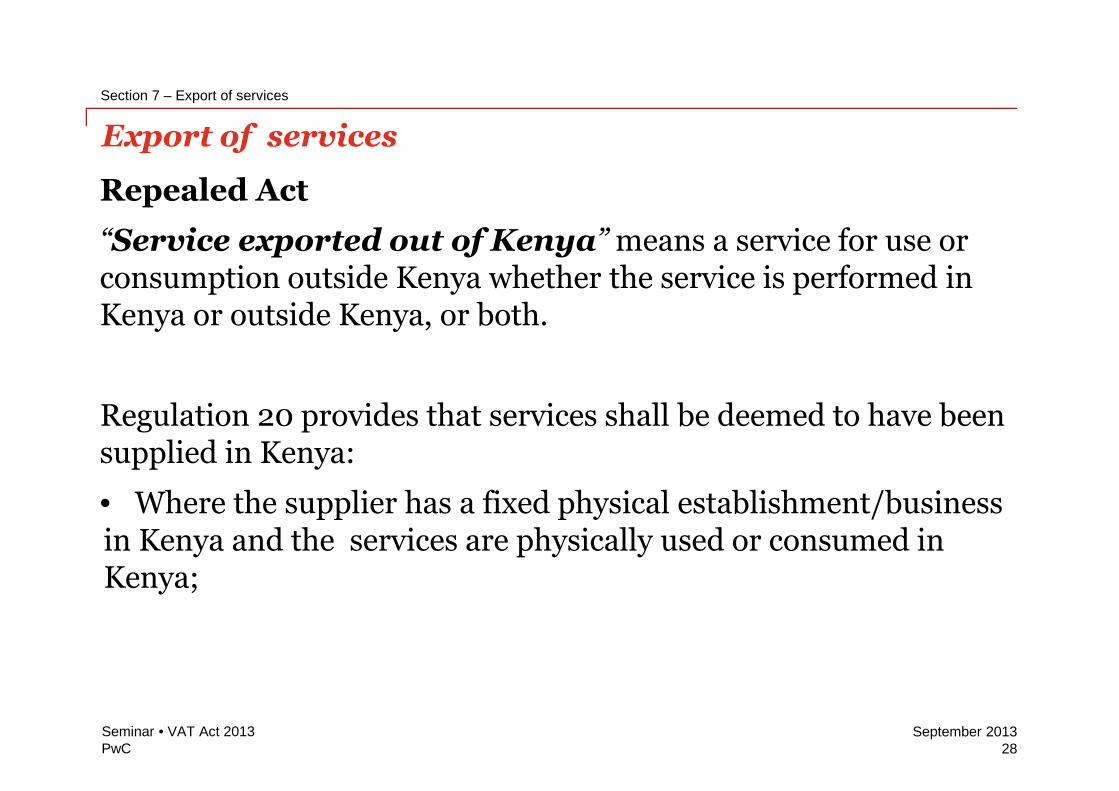

Repealed Act

“Service exported out of Kenya” means a service for use orconsumption outside Kenya whether the service is performed inKenya or outside Kenya, or both.

Regulation 20 provides that services shall be deemed to have beensupplied in Kenya:

• Where the supplier has a fixed physical establishment/businessin Kenya and the services are physically used or consumed inKenya;

Export of services

28Seminar • VAT Act 2013

Section 7 – Export of services

PwCSeptember 2013

VAT Act 2013

Section 8(1) provides that a supply of services is made in Kenya ifthe place of business of the supplier from which the services aresupplied is in Kenya.

The definition of ‘service exported out of Kenya’ means a serviceprovided for use or consumption outside Kenya.

Implication

The VAT Act 2013 has provided for clarity in respect of‘consumption’ of an export of service based on the destinationprinciple.

Export of services

29Seminar • VAT Act 2013

Section 7 – Export of services

Non-resident

PwCSeptember 2013

Deduction of input tax

30

Seminar • VAT Act 2013

PwCSeptember 2013

Section 8 – Deduction of input tax

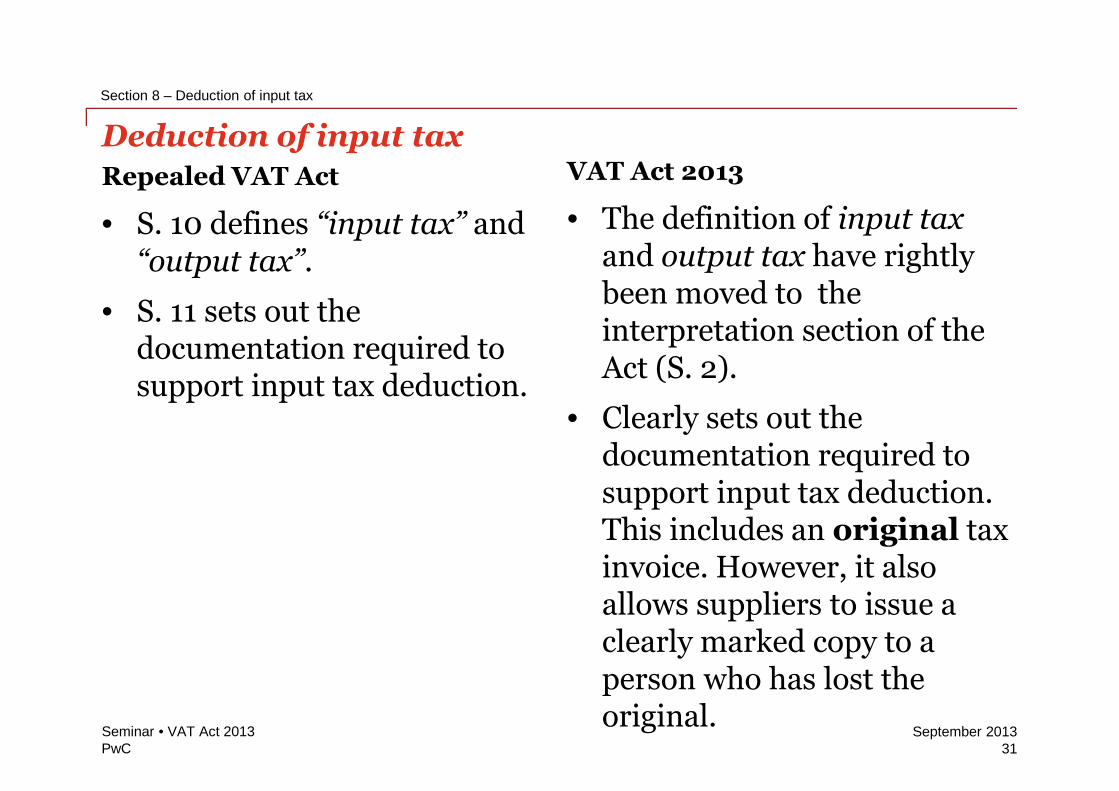

Repealed VAT Act

• S. 10 defines “input tax” and“output tax”.

• S. 11 sets out thedocumentation required tosupport input tax deduction.

VAT Act 2013

• The definition of input taxand output tax have rightlybeen moved to theinterpretation section of theAct (S. 2).

• Clearly sets out thedocumentation required tosupport input tax deduction.This includes an original taxinvoice. However, it alsoallows suppliers to issue aclearly marked copy to aperson who has lost theoriginal.

Deduction of input tax

31Seminar • VAT Act 2013

PwCSeptember 2013

32Seminar • VAT Act 2013

Section 8 – Deduction of input tax

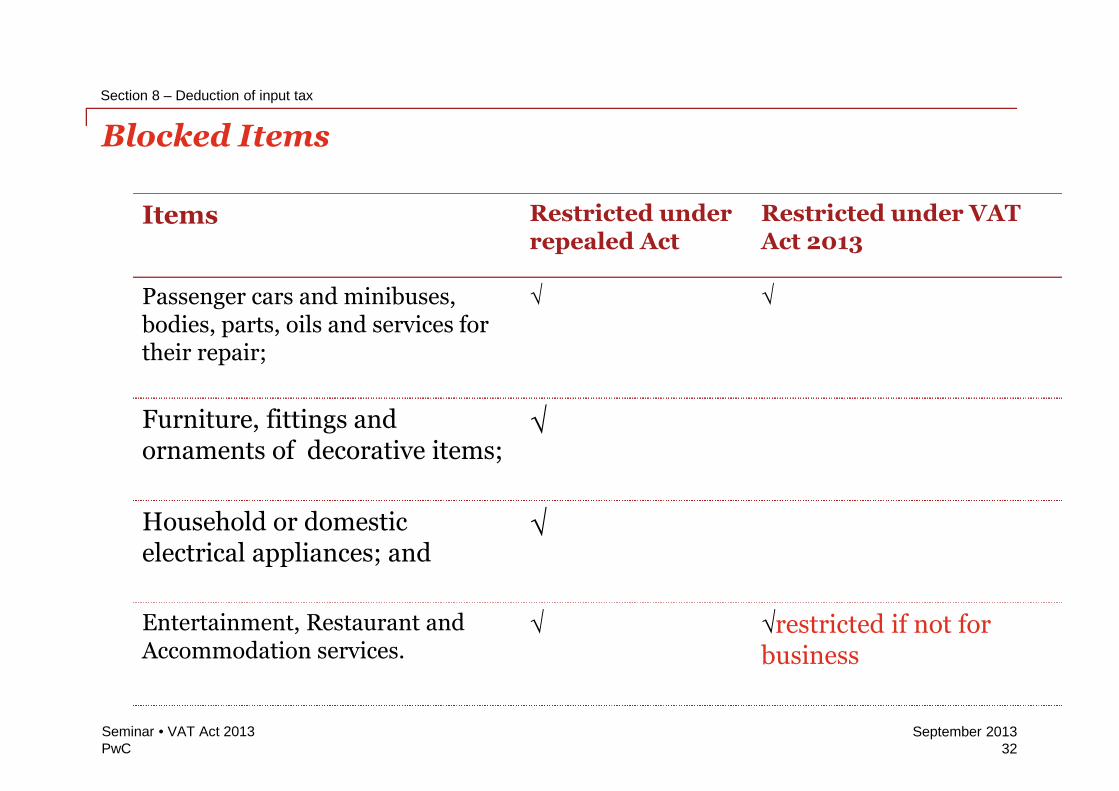

Items Restricted underrepealed Act

Restricted under VATAct 2013

Passenger cars and minibuses,bodies, parts, oils and services fortheir repair;

√ √

Furniture, fittings andornaments of decorative items;

√

Household or domesticelectrical appliances; and

√

Entertainment, Restaurant andAccommodation services.

√ √restricted if not forbusiness

Blocked Items

PwCSeptember 2013

Partial exemption

33

Seminar • VAT Act 2013

PwCSeptember 2013

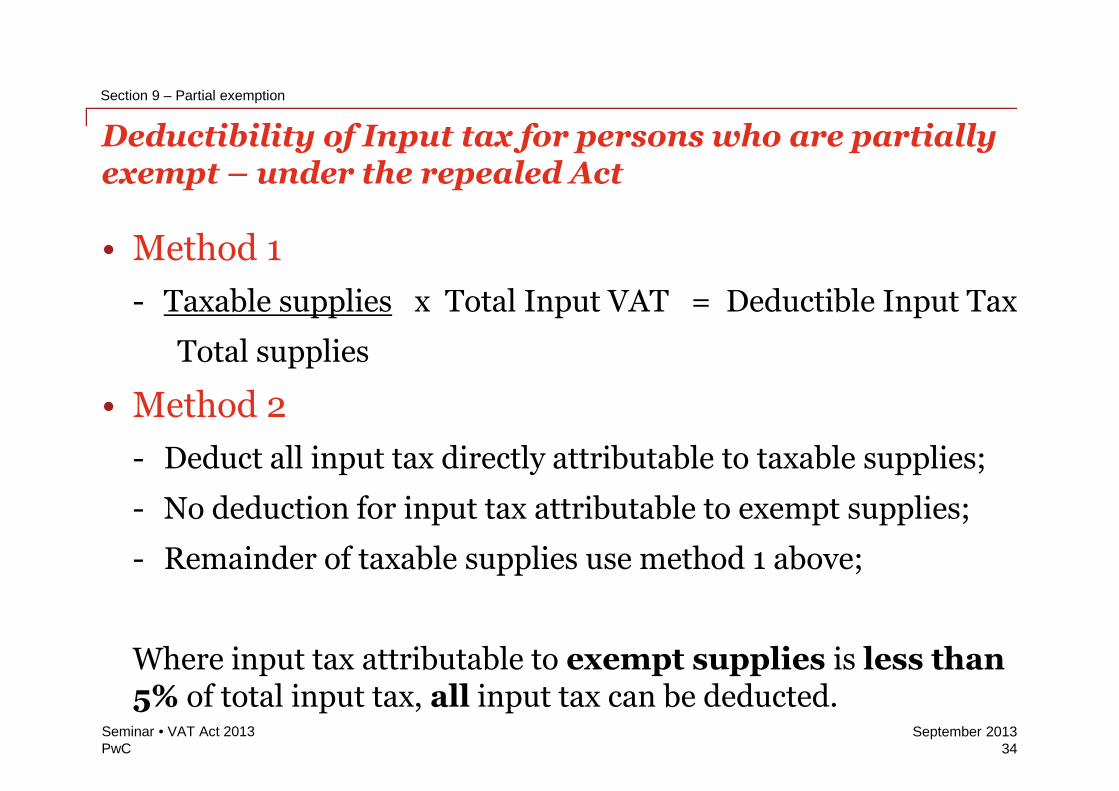

• Method 1

- Taxable supplies x Total Input VAT = Deductible Input Tax

Total supplies

• Method 2

- Deduct all input tax directly attributable to taxable supplies;

- No deduction for input tax attributable to exempt supplies;

- Remainder of taxable supplies use method 1 above;

Where input tax attributable to exempt supplies is less than5% of total input tax, all input tax can be deducted.

Deductibility of Input tax for persons who are partiallyexempt – under the repealed Act

34Seminar • VAT Act 2013

Section 9 – Partial exemption

PwCSeptember 2013

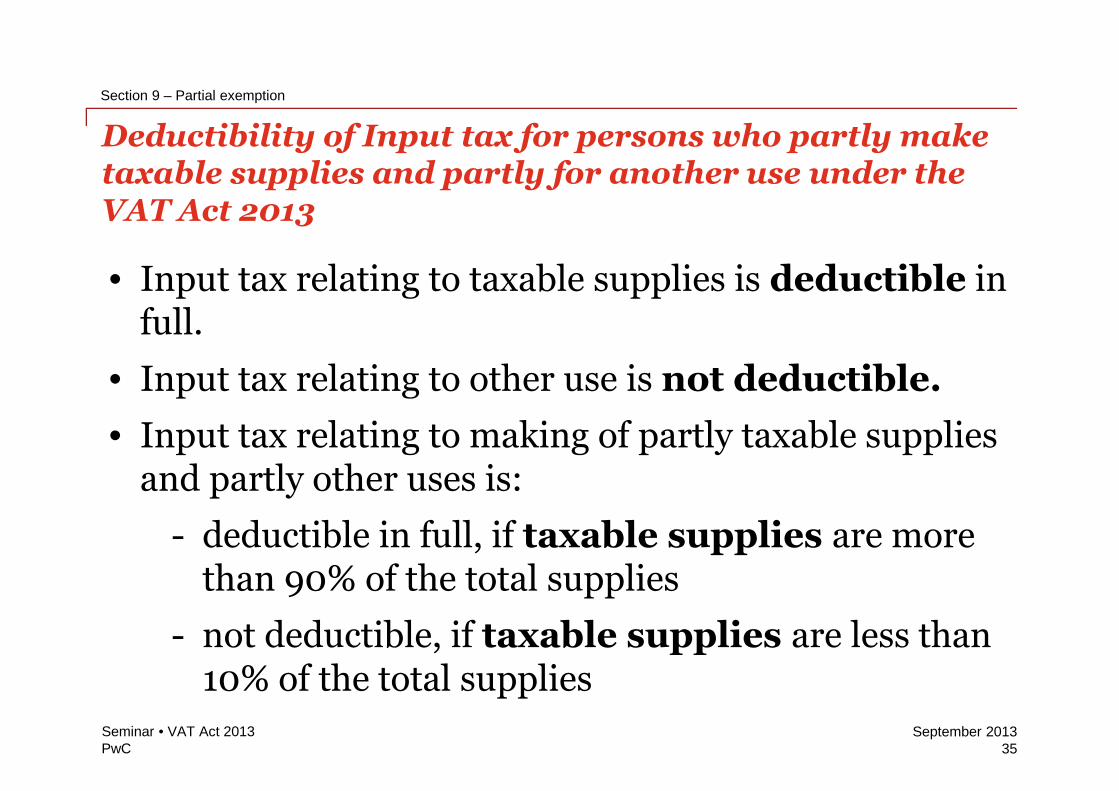

• Input tax relating to taxable supplies is deductible infull.

• Input tax relating to other use is not deductible.

• Input tax relating to making of partly taxable suppliesand partly other uses is:

- deductible in full, if taxable supplies are morethan 90% of the total supplies

- not deductible, if taxable supplies are less than10% of the total supplies

Deductibility of Input tax for persons who partly maketaxable supplies and partly for another use under theVAT Act 2013

35Seminar • VAT Act 2013

Section 9 – Partial exemption

PwCSeptember 2013

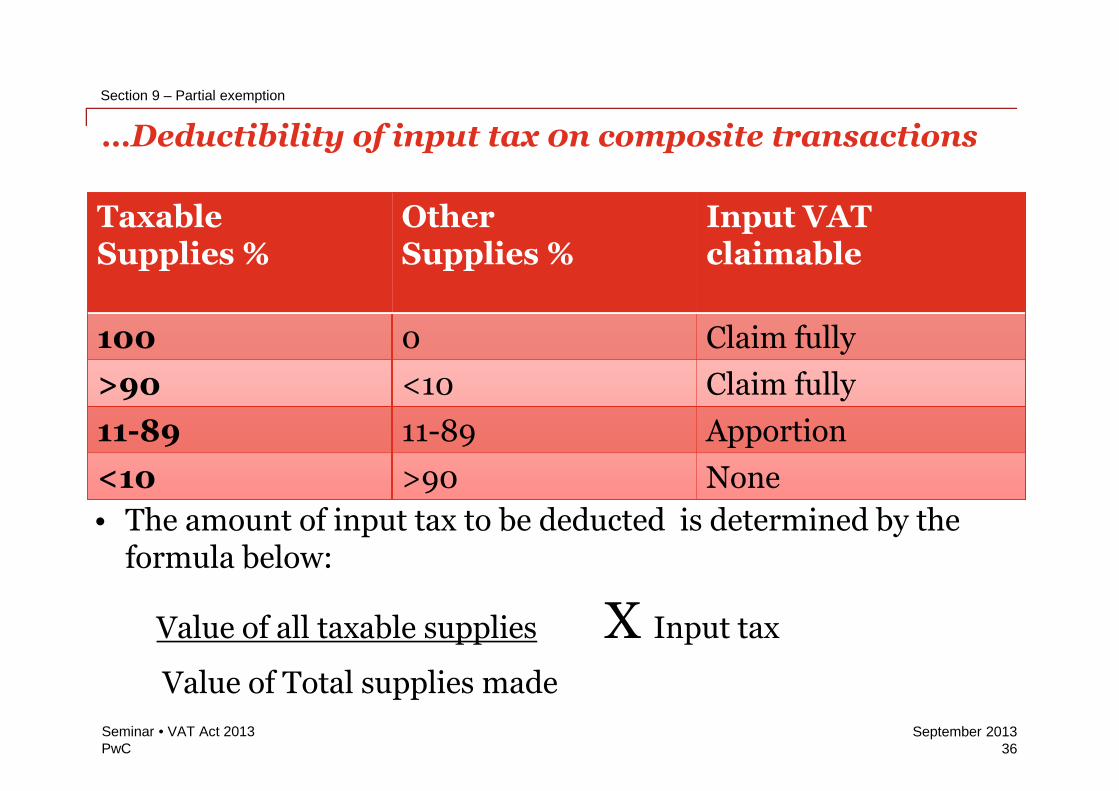

• The amount of input tax to be deduced is determined by the formula below:

Value of all taxable supplies X Total input tax

Total supplies made

• The amount of input tax to be deducted is determined by theformula below:

Value of all taxable supplies X Input tax

Value of Total supplies made

…Deductibility of input tax 0n composite transactions

36Seminar • VAT Act 2013

Section 9 – Partial exemption

TaxableSupplies %

OtherSupplies %

Input VATclaimable

100 0 Claim fully

>90 <10 Claim fully

11-89 11-89 Apportion

<10 >90 None

PwCSeptember 2013

Revised time limits

37

Seminar • VAT Act 2013

PwCSeptember 2013

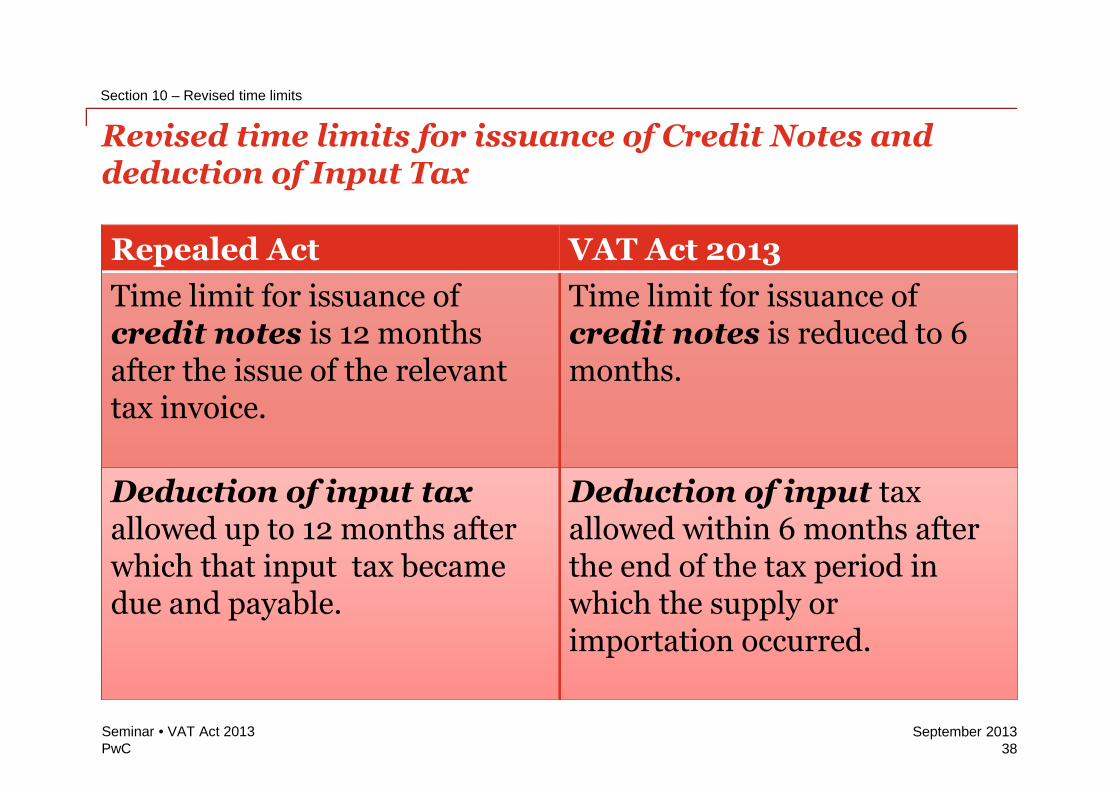

Repealed Act VAT Act 2013

Time limit for issuance ofcredit notes is 12 monthsafter the issue of the relevanttax invoice.

Time limit for issuance ofcredit notes is reduced to 6months.

Deduction of input taxallowed up to 12 months afterwhich that input tax becamedue and payable.

Deduction of input taxallowed within 6 months afterthe end of the tax period inwhich the supply orimportation occurred.

Revised time limits for issuance of Credit Notes anddeduction of Input Tax

38Seminar • VAT Act 2013

Section 10 – Revised time limits

PwCSeptember 2013

Refund of tax

39

Seminar • VAT Act 2013

PwCSeptember 2013

40Seminar • VAT Act 2013

Section 11 – Refund of tax

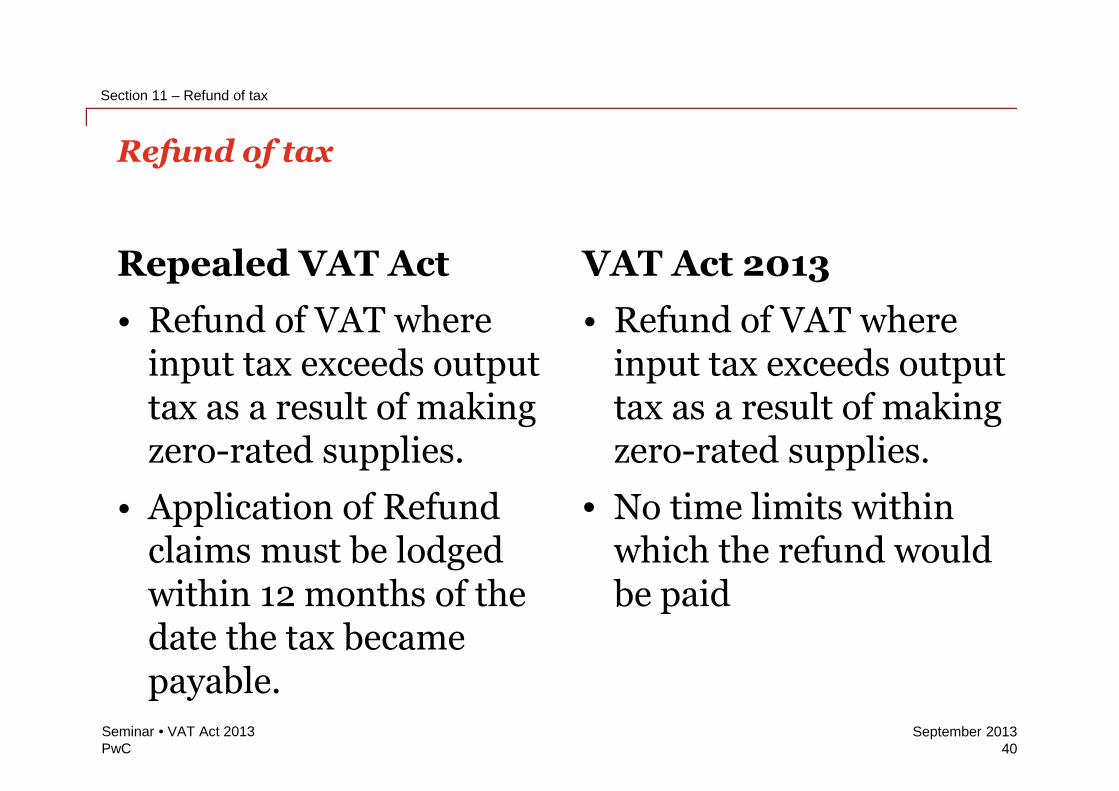

Repealed VAT Act

• Refund of VAT whereinput tax exceeds outputtax as a result of makingzero-rated supplies.

• Application of Refundclaims must be lodgedwithin 12 months of thedate the tax becamepayable.

VAT Act 2013

• Refund of VAT whereinput tax exceeds outputtax as a result of makingzero-rated supplies.

• No time limits withinwhich the refund wouldbe paid

Refund of tax

PwCSeptember 2013

VAT Remission

41

Seminar • VAT Act 2013

PwCSeptember 2013

Section 12 – VAT Remission

42Seminar • VAT Act 2013

• VAT Remission is abolished!

• Remission already granted under therepealed Act shall continue toremain in force for a period of 5years.

• Companies likely to be affected:

- who purchase equipment not underchapter 84 and 85;

- are in the hotel constructionbusiness; and

- in the oil exploration business

- who applied for TREO

VAT Remission

PwCSeptember 2013

Registration and Deregistration

43

Seminar • VAT Act 2013

PwCSeptember 2013

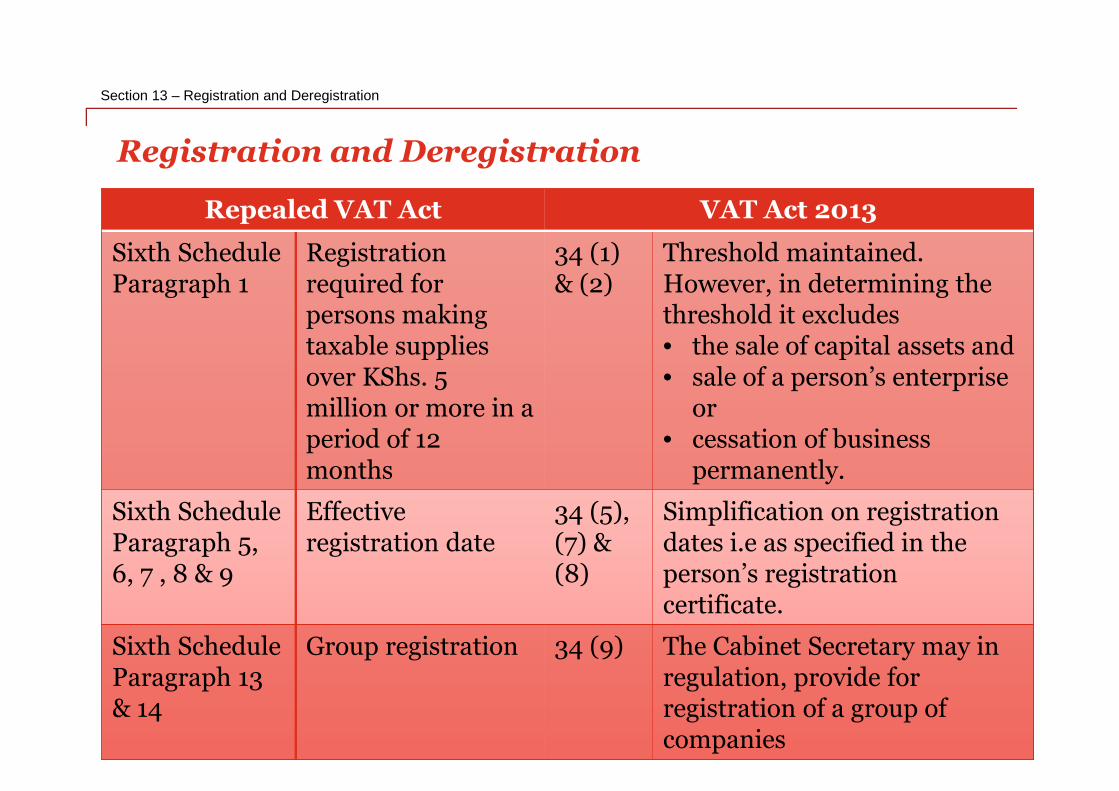

Section 13 – Registration and Deregistration

44Seminar • VAT Act 2013

Repealed VAT Act VAT Act 2013

Sixth ScheduleParagraph 1

Registrationrequired forpersons makingtaxable suppliesover KShs. 5million or more in aperiod of 12months

34 (1)& (2)

Threshold maintained.However, in determining thethreshold it excludes• the sale of capital assets and• sale of a person’s enterprise

or• cessation of business

permanently.

Sixth ScheduleParagraph 5,6, 7 , 8 & 9

Effectiveregistration date

34 (5),(7) &(8)

Simplification on registrationdates i.e as specified in theperson’s registrationcertificate.

Sixth ScheduleParagraph 13& 14

Group registration 34 (9) The Cabinet Secretary may inregulation, provide forregistration of a group ofcompanies

Registration and Deregistration

PwCSeptember 2013

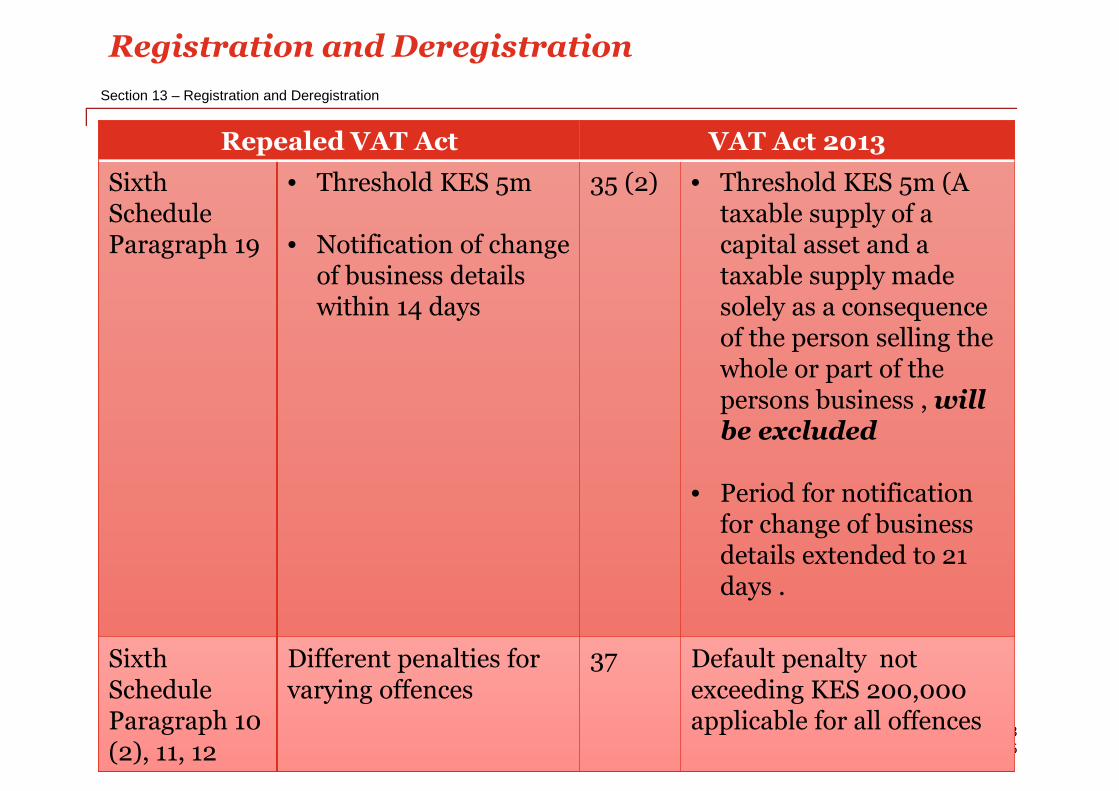

Section 13 – Registration and Deregistration

45Seminar • VAT Act 2013

Repealed VAT Act VAT Act 2013

SixthScheduleParagraph 19

• Threshold KES 5m

• Notification of changeof business detailswithin 14 days

35 (2) • Threshold KES 5m (Ataxable supply of acapital asset and ataxable supply madesolely as a consequenceof the person selling thewhole or part of thepersons business , willbe excluded

• Period for notificationfor change of businessdetails extended to 21days .

SixthScheduleParagraph 10(2), 11, 12

Different penalties forvarying offences

37 Default penalty notexceeding KES 200,000applicable for all offences

Registration and Deregistration

PwCSeptember 2013

Application of InformationTechnology

46

Seminar • VAT Act 2013

PwCSeptember 2013

47Seminar • VAT Act 2013

Section 14 – Application of Information Technology

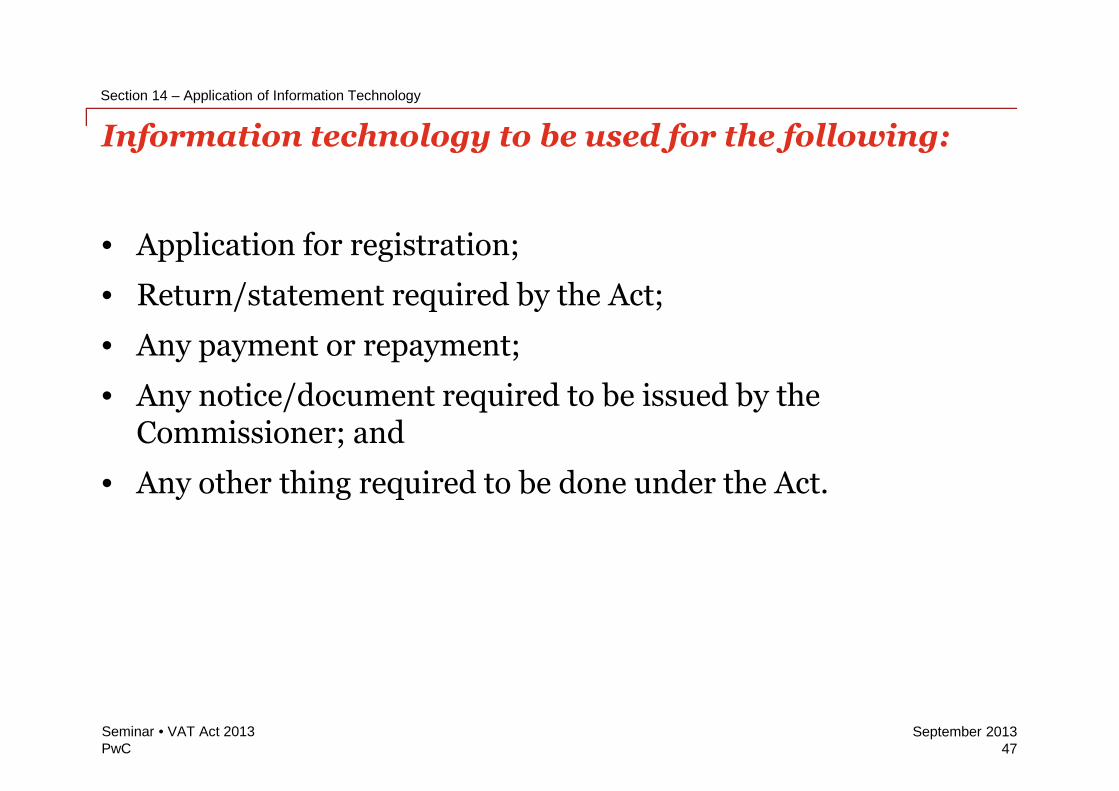

• Application for registration;

• Return/statement required by the Act;

• Any payment or repayment;

• Any notice/document required to be issued by theCommissioner; and

• Any other thing required to be done under the Act.

Information technology to be used for the following:

PwCSeptember 2013

48Seminar • VAT Act 2013

Section 14 – Application of Information Technology

Powers given to theCommissioner to establish andoperate:

• a procedure for electronicfiling of tax returns or otherdocuments by registeredpersons;

• electronic service of noticesand other documents; and

• provide written conditions forelectronic returns and notices.

Application of Information Technology

iTax

PwCSeptember 2013

Objections

49

Seminar • VAT Act 2013

PwCSeptember 2013

Section 15 – Objections

Repealed VAT Act

• No time limit withinwhich the Commissionerwas to respond to theobjections of assessmentssubmitted by tax payers.

VAT Act 2013

The Commissioner to:

• respond within 30 days after he hasreceived the notice of objection.

• to send out a notice within 15 dayssetting out an amendment orconfirming the assessment.

• Where the Commissioner fails tocommunicate within 60 days, heshall be deemed to have agreed toamend the assessment inaccordance with the objection.

Objections

50Seminar • VAT Act 2013

PwCSeptember 2013

Appeals

51

Seminar • VAT Act 2013

PwCSeptember 2013

• VAT appeals provisions excluded from the VAT Act2013 in light of the Tax Appeals Tribunal Bill 2013.

• However, transitional clauses provide for subsidiarylegislation to remain in force until new subsidiarylegislation is enacted.

Implications

• Any notifications to appeal to the Tribunal can still beeffected.

Appeals

52Seminar • VAT Act 2013

Section 16 – Appeals

PwCSeptember 2013

Tax avoidance schemes

53

Seminar • VAT Act 2013

PwCSeptember 2013

Repealed Act

Non-existent in the repealed Act.

VAT Act 2013

• A scheme is entered into when a person obtains a taxbenefit.

• Where a scheme is entered into, the Commissionershall make an adjustment and issue an assessment ofany tax liability.

Tax avoidance schemes

54Seminar • VAT Act 2013

Section 17 – Tax avoidance schemes

PwCSeptember 2013

Enforcement

55

Seminar • VAT Act 2013

PwCSeptember 2013

• Commissioner may require the production of recordsand information in respect of tax liability in order toascertain the correctness of the tax declared by the taxpayer.

• Audit to be concluded within 6 months, however, KRAcan request for extension in writing.

• Where audit is not concluded within 6 months, aregistered person can be issued with an interimcertificate indicating the progress of the audit.

Enforcement

56Seminar • VAT Act 2013

Section 18 – Enforcement

PwCSeptember 2013

Public/private rulings

57

Seminar • VAT Act 2013

PwCSeptember 2013

Repealed VAT Act

KRA would issue non-binding

• Information Letters;

• Public notices; and

• Technical circulars.

VAT Act 2013

The Commissioner is requiredto make public notices to appearin at least 2 daily newspapersspecifying;

• Subject matter;

• ID number of subject matter;and

• Effective date of ruling.

Withdrawal of publicnotice to be published innewspapers.

Public ruling

58Seminar • VAT Act 2013

Section 19 – Public/private rulings

PwCSeptember 2013

Repealed VAT Act

Specific rulings were issued tothe tax payer in respect of atechnical issue.

VAT Act 2013

Commissioner to issue privateruling upon application of theregistered person.

Private ruling

59Seminar • VAT Act 2013

Section 19 – Public/private rulings

PwCSeptember 2013

Transitional clauses

60

Seminar • VAT Act 2013

PwCSeptember 2013

61Seminar • VAT Act 2013

Section 20 – Transitional clauses

• The clauses under the repealed Actshall still remain in force for purposesof:

the assessment and collection of anytax or recovery of penalty;

subsidiary legislation consistentwith the VAT Act 2013;

remission already granted for thenext five years;

tax due to be paid or refunded, butwas not so paid or refunded; it shallbe paid or refunded as though itwere a sum due under the currentregime.

Transitional clauses

PwCSeptember 2013

Implication to the Extractive Sector

64

Seminar • VAT Act 2013

PwCSeptember 2013

• Upstream Oil & Gas Companies

• Geothermal power companies

• Mining Companies

• Subcontractors

• ---By extension we coverdownstream matters

Who falls under the Extractice industry cluster

64Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

Scraped !!

Repealed Act provided for a VAT remission taxable supplies purchased by theOil and Gas companies specifically for exploration.

VAT Act 2013 has abolished VAT remission scheme.

Relief?

Remission already granted under the repealed Act shall continue to remain inforce for a period of 5 years.

This is only for approved spend!

Extractive sector - Tax remission

65Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

Reason to smile?

VAT Act, 2013 has granted tax exemption to tax supplies imported or purchasedfor direct and exclusive use in the extractive industry.

However, there is ambiguity as the Act is not clear on whether exemptionextends to services.

Relief on administration burden?

It is subject to judgment as to whether the new law has brought any relief on theadministrative burden associated with the process

Extractive sector - Tax exemption

66Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

a) Imported services where the recipient is a registered person

Under S 10 (1), states that if a supply of imported taxable services is made to aregistered person the registered person shall be deemed to have made a taxablesupply to himself.

Under 10 (3), the output tax for the deemed supply has to be paid by theregistered person at the time of supply.

b) Supplies by a non-resident person where the recipient is a non-resident

The supply is deemed to be supplied in Kenya

The non resident is required to appoint a tax representative.

ARE You registered person or not….

Extractive sector - Registration status

67Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

b) Subcontractors

Certain subcontractors provideservices exclusively to the extractiveindustry.

These services have been exemptedunder Para 29 &30 of the FirstSchedule to the VAT Act 2013.

Currently these subcontractors areregistered for VAT, will they apply forderegistration now that theirservices to this sector are exempt?

Extractive sector - Registration status

68Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

1. Specialised Motor vehicles (SMV) used inthis sector

Under the Act, Motor vehicles do not qualify for taxexemption. Need to get specialised motor vehiclesfor the extractive sector defined and exempted

2. Recommendation process on VATexemption

The Act provides that for the exemption to begranted, it has to be approved by the cabinetsecretary for energy/ mining. However, no guidanceon the recommendation process.

Extractive sector - Key areas of discussions

69Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

Exempt goods of chapter 84 &85

• All plant, machinery, electrical andmechanical appliances under chapters84 and 85 of the East AfricanCommunity Common External Tariff(CET) e.g

- generators , refrigerators

- computer hardware software,processors and monitors including

- machinery for sorting, screening,separating, washing, crushing andgrinding most of which were zerorated in the old VAT Act are nowexempt.

- KRA is currently reviewingclassification of goods todetermine which ones fall underequipment (taxable at 16%) andplant and machinery that areexempt from VAT.

Implications of the New VAT Act 2013 to the Extractiveindustry

68Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

Equipment for geothermalenergy

• In the repealed Act , goodsincluding motor vehicles importedor purchased for use in geothermalwas eligible for VAT remission.

• In the new VAT Act, taxablesupplies excluding motor vehiclespurchased or imported for use ingeothermal is exempt.

Implications Extractive Industry Cont.….

69Seminar • VAT Act 2013

Section 22 – Implication to the Extractive Sector

PwCSeptember 2013

What does this mean?

70

Seminar • VAT Act 2013

PwCSeptember 2013

Change of VAT status

67

Seminar • VAT Act 2013

PwCSeptember 2013

The Act has significantly reduced the number of exemptand zero rated supplies. All other supplies are nowtaxable at the standard rate of 16% except items listed inthe First and Second Schedule.

Reduction in zero rated and exemptsupplies…

68Seminar • VAT Act 2013

Section 23 – Change of VAT status

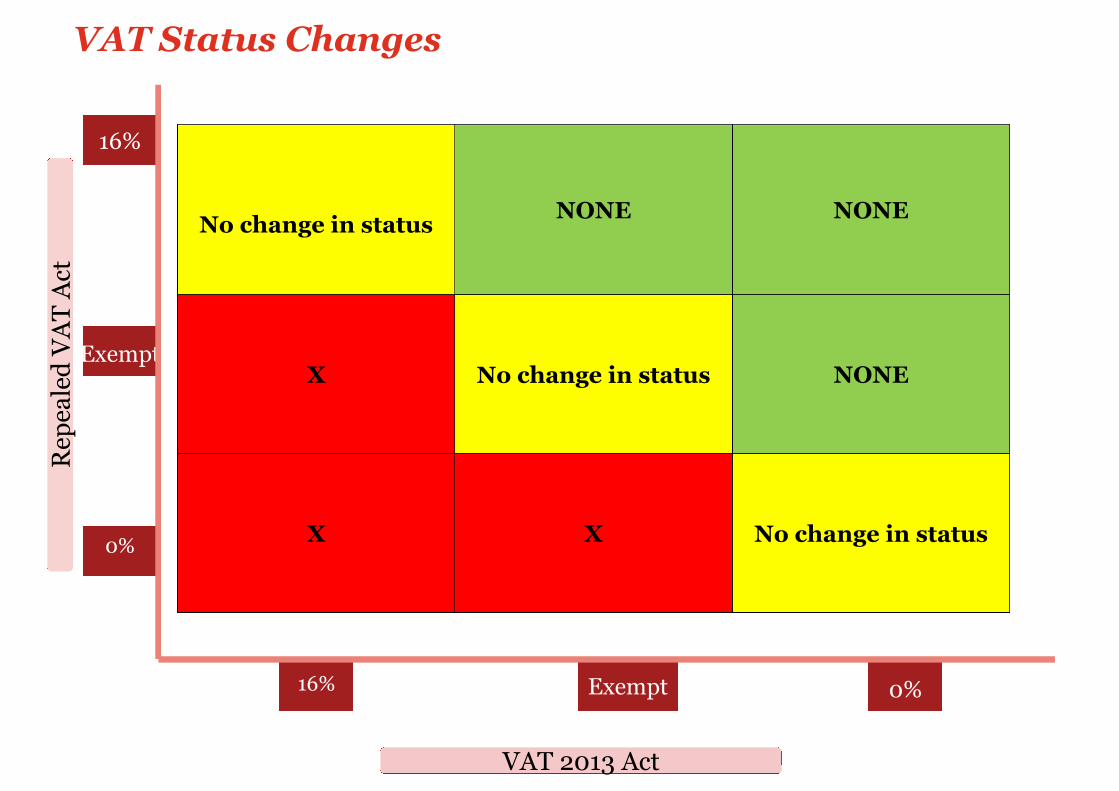

16%

Exempt

0%

16% Exempt 0%

A

VAT 2013 Act

Rep

eale

dV

AT

Act

None

C None

VAT Status Changes

No change in statusNONE NONE

X No change in status NONE

X X No change in status

PwCSeptember 2013

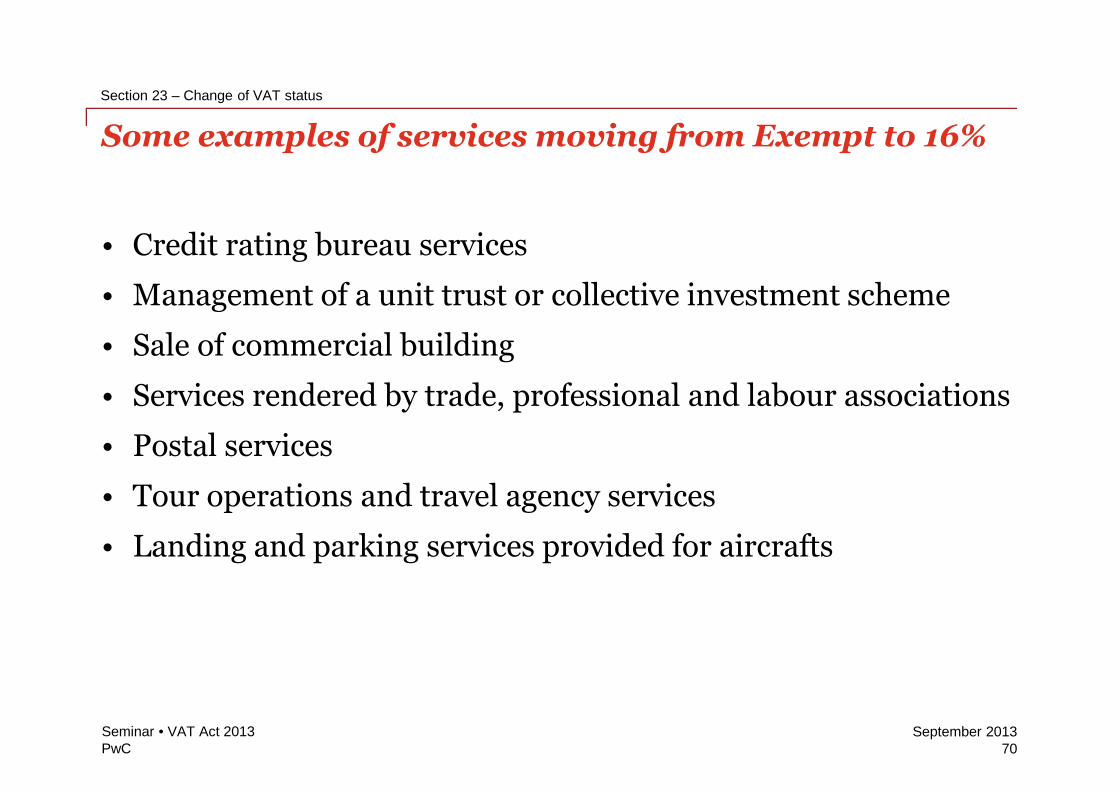

• Credit rating bureau services

• Management of a unit trust or collective investment scheme

• Sale of commercial building

• Services rendered by trade, professional and labour associations

• Postal services

• Tour operations and travel agency services

• Landing and parking services provided for aircrafts

Some examples of services moving from Exempt to 16%

Section 23 – Change of VAT status

Seminar • VAT Act 201370

PwCSeptember 2013

• Flour (rice, rye, groats and meal of wheat/maize, potatoes, driedleguminous vegetables)

• Cut flowers and flower buds

• Rocket launchers/Artillery/military weapons

Some examples of goods moving from Exempt to 16%

Section 23 – Change of VAT status

Seminar • VAT Act 201371

PwCSeptember 2013

• Electricity supply of electrical energy to domestic householdsbelow 200 KW

• Transport services for unprocessed agricultural/ agro forestproduce

• construction services in relation to grain silos

Some examples of services moving from Zero rated to16%

Section 23 – Change of VAT status

Seminar • VAT Act 201372

PwCSeptember 2013

• Goods used by the President

• Goods for the official use of the Armed Forces

• Residues and waste from the food industries; prepared animal

• Milk

• Newspapers and books

• Solar equipment and accessories

• Agricultural tractors

Some examples of goods moving from Zero rated to 16%

Section 23 – Change of VAT status

Seminar • VAT Act 201373

PwCSeptember 2013

• Milk specially prepared for infants

• Ordinary, gluten and unleavened bread.

• Wheat Flour

• Maize flour

• Cereal (except wheat, rye and barley seeds )

• Organic chemicals

• Pharmaceutical products

• Fertilizer

• Sanitary towels (pads) and tampons.

Some examples of goods moving from Zero rated toExempt

Section 23 – Change of VAT status

Seminar • VAT Act 201374

PwCSeptember 2013

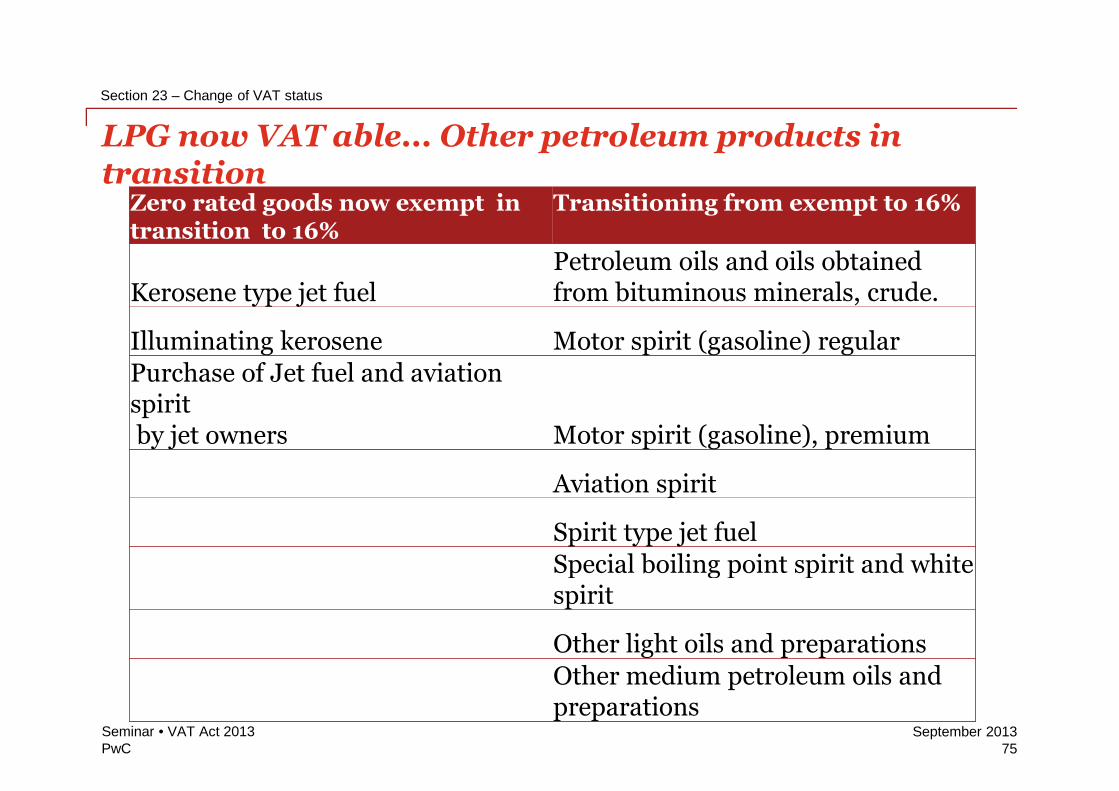

LPG now VAT able... Other petroleum products intransition

Section 23 – Change of VAT status

Seminar • VAT Act 201375

Zero rated goods now exempt intransition to 16%

Transitioning from exempt to 16%

Kerosene type jet fuelPetroleum oils and oils obtainedfrom bituminous minerals, crude.

Illuminating kerosene Motor spirit (gasoline) regularPurchase of Jet fuel and aviationspiritby jet owners Motor spirit (gasoline), premium

Aviation spirit

Spirit type jet fuelSpecial boiling point spirit and whitespirit

Other light oils and preparationsOther medium petroleum oils andpreparations

PwCSeptember 2013

An example:

Are phones and computer software taxable @ 16% or still exemptas phones are under chapter 85

Chapter 84, 85 – Interpretation

What is Plant and machinery

76Seminar • VAT Act 2013

Section 23 – Change of VAT status

PwCSeptember 2013

Questions & answers

77

Seminar • VAT Act 2013