Embed Size (px)

Citation preview

WP/07/274

Tax Policy: Recent Trends and Coming Challenges

John Norregaard and Tehmina S. Khan

© 2007 International Monetary Fund WP/07/274 IMF Working Paper Fiscal Affairs Department

Tax Policy: Recent Trends and Coming Challenges

Prepared by John Norregaard and Tehmina S. Khan

Authorized for distribution by Isaias Coelho

December 2007

Abstract

This Working Paper should not be reported as representing the views of the IMF. The views expressed in this Working Paper are those of the author(s) and do not necessarily represent those of the IMF or IMF policy. Working Papers describe research in progress by the author(s) and are published to elicit comments and to further debate.

This paper provides an overview of the key economic factors that shape tax policy reform in many high-income countries, developing countries, and/or transition economies. The paper describes and evaluates global and regional developments with respect to tax rates and revenue ratios over the last some 20 years, and discusses selected structural reform initiatives that have been high on the policy agenda over this period. In particular, it focuses on developments relating to experiments with the restructuring of corporate tax, the impact of corporate taxes on FDI, key reform initiatives including dual income taxes and flat taxes, as well as the worldwide spread of the VAT and policy developments associated with climate change and natural resource taxation. JEL Classification Numbers: H20, H21, H23, H24, H25, H26 Keywords: Tax reform, personal income tax, corporate income tax, value-added tax, tax

wedge, tax competition, green taxes Author’s E-Mail Address: [email protected]; [email protected]. Acknowledgements: We are grateful to A. M. Abdel-Rahman, Alexander Klemm, Emil Sunley, Jon Strand, Michael Keen, Sanjeev Gupta, and colleagues in the Tax Policy Division of the IMF for many helpful suggestions and comments. We would also like to thank Asegedech WoldeMariam for her assistance with the VAT map, which could not be reproduced as part of this paper but can be found at http://www.imf.org/external/pubs/ft/wp/2007/maps/vatmap.pdf.

2

Contents Page

I. Introduction............................................................................................................................ 3

II. Factors Shaping International Tax Policy Trends ................................................................ 3

III. Revenue and Tax Rate Developments: Some Empirical Facts........................................... 8 A. Corporate Income Tax.............................................................................................. 8 B. Personal Income Tax .............................................................................................. 10 C. Social Security Contributions and Labor Tax Wedges .......................................... 12

IV. An Overview of Key Tax Policy Trends .......................................................................... 15 A. Addressing the Increased Global Mobility of Capital and Labor: .

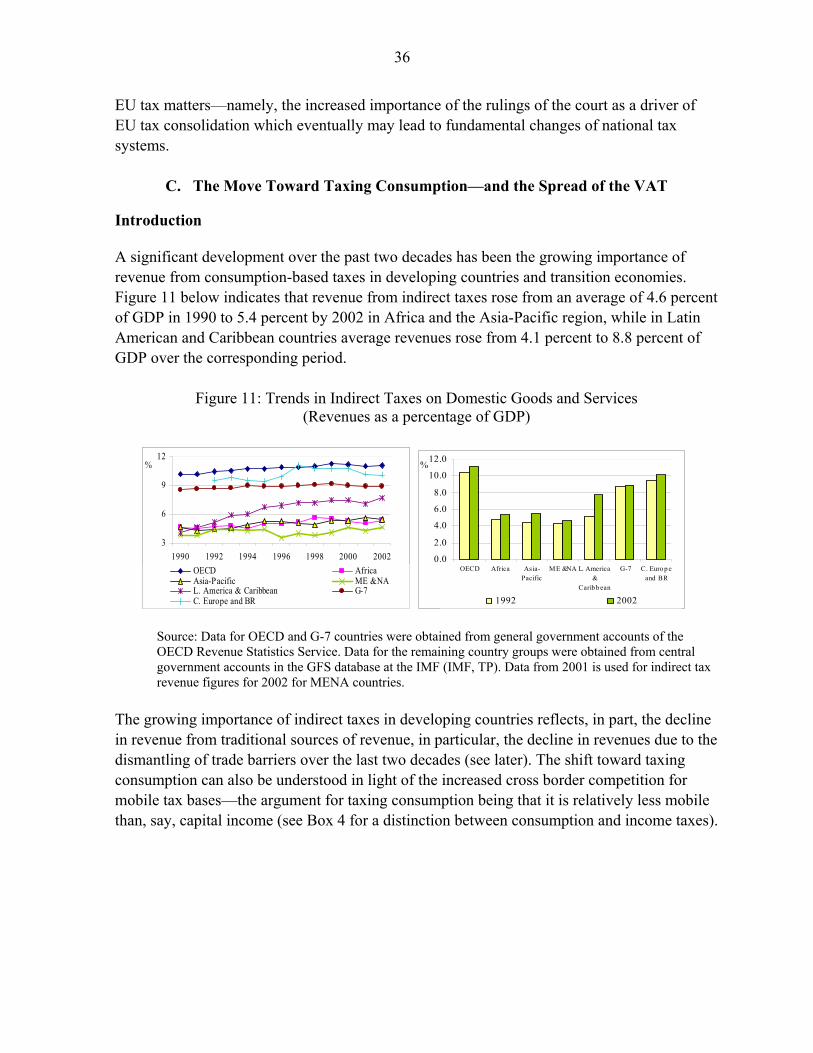

Individual Country Responses................................................................................ 15 B. International Harmonization and Coordination Initiatives..................................... 32 C. The Move Toward Taxing Consumption—and the Spread of the VAT................ 36

V. Concluding Remarks .......................................................................................................... 50 Tables 1. Dual Income Taxes (DIT) in the Nordic Countries, 2005 .................................................. 26 2. Current Flat Taxes............................................................................................................... 29 Figures 1. Statutory CIT Rates, 1993–2006........................................................................................... 8 2. Corporate Tax Revenue, 1990–2003 .................................................................................... 9 3. Top PIT Rates, 1995–2004. ................................................................................................ 11 4. PIT and CIT Revenue.......................................................................................................... 12 5. Tax Wedges in OECD and EU Countries as a Share of of Total Labor Costs in 2006 ...... 13 6. Tax Wedges in Central and Eastern Europe and Central Asia (Excluding EU-10 NMS)

in 2006 ................................................................................................................................ 14 7. Direct and Indirect Taxes and Social Security Contributions............................................. 14 8. Tax Wedge for a “Low-Wage” Employee in OECD Countries ........................................ 15 9. Effective Average Tax Rates on Inbound FDI between OECD Countries,

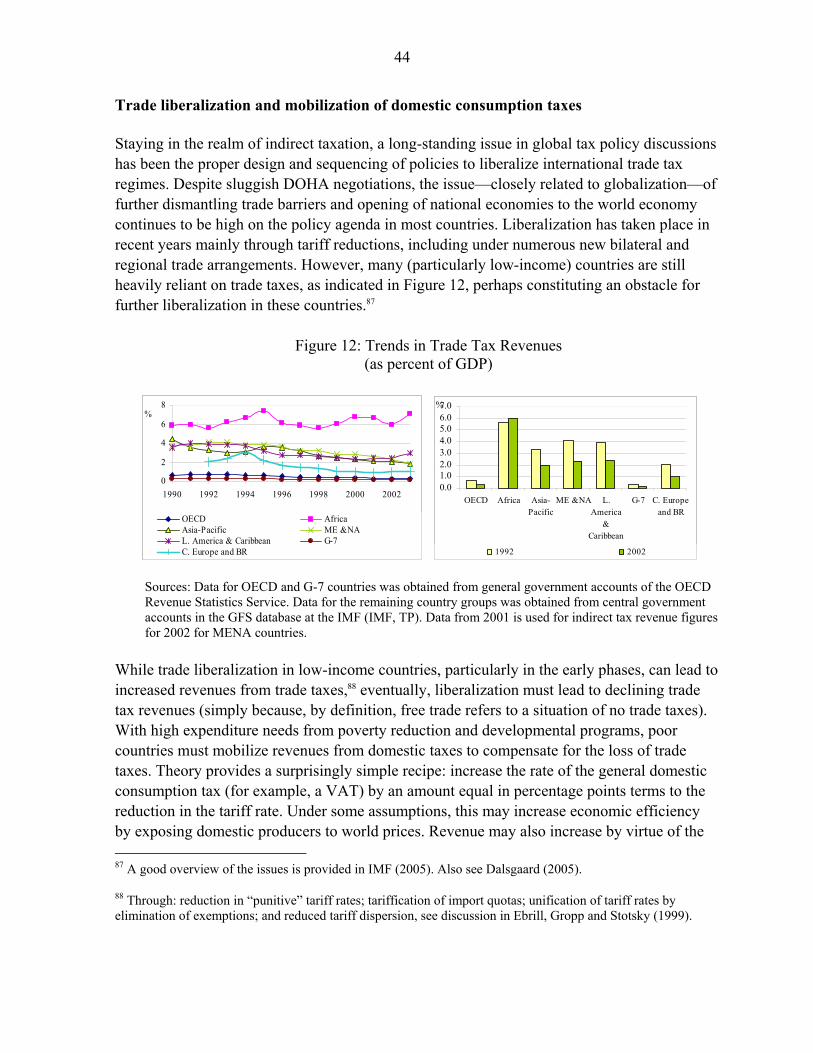

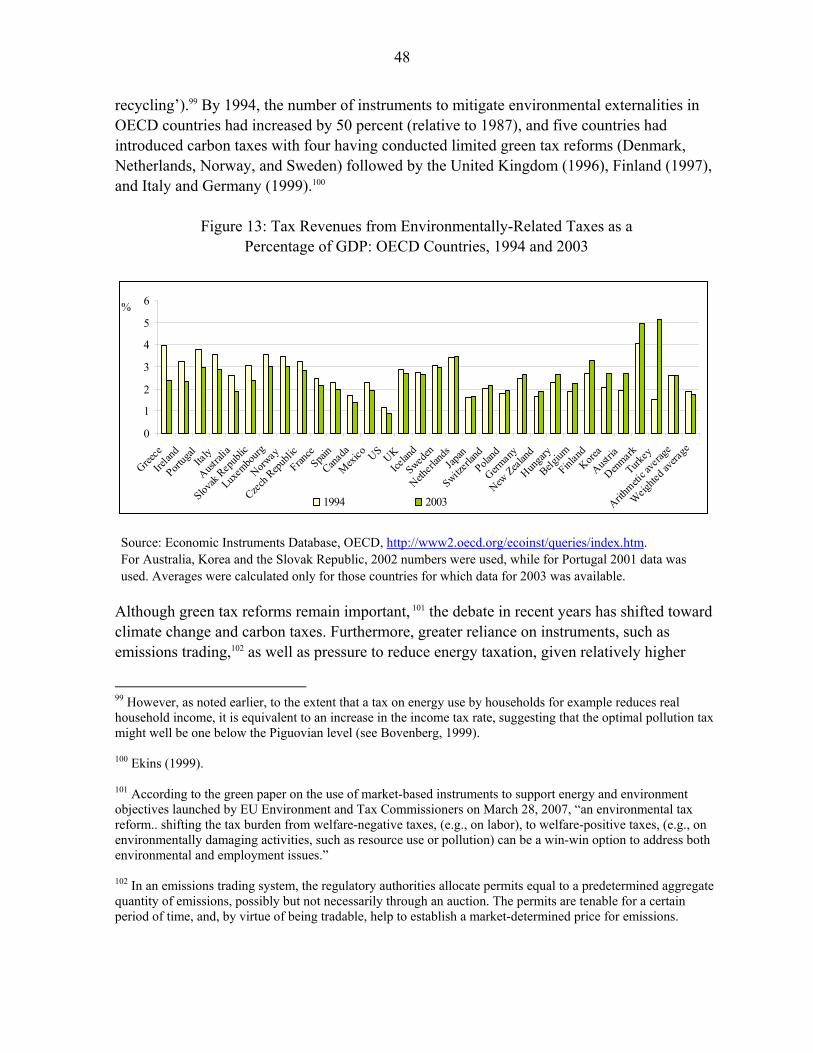

1996 and 2001................................................................................................................... 17 10. Ratio of Total U.S. FDI to GDP for Four Groups of Countries........................................ 19 11. Trends in Indirect Taxes on Domestic Goods and Services ............................................. 36 12. Trends in Trade Tax Revenues ......................................................................................... 44 13. Tax Revenues from Environmentally-Related Taxes as a Percentage of GDP:

OECD Countries, 1994 and 2003 .................................................................................... 48 Boxes 1. FDI and Economic Growth in Ireland: What Role did the Tax System Play? ................... 20 2. Taxes on Capital Income in an Open Economy.................................................................. 25 3. PIT And CIT Loopholes Closed in the Slovak Tax Reform............................................... 30 4. Taxing Consumption vs. Taxing Income............................................................................ 37 References ............................................................................................................................... 53

3

I. INTRODUCTION

While Benjamin Franklin may have been right that death and taxes are the only certain things in life,1 this certainty definitely does not extend to the way taxes are levied: tax systems are continuously changing as countries align their tax systems with evolving economic, political, and administrative conditions.2 This prompts the question whether there are factors at work that “steer” tax reform efforts of different countries, regionally or globally, broadly in the same direction? And if so, what insights can individual countries gain from that process? A central policy issue in recent years has been the implications for the stability of tax bases of economic integration and the ever increasing mobility of capital (physical as well as financial), labor, and goods and services. It is worth noting, though, that the specific policy challenges differ widely across countries, with developing countries focusing, in particular, on attracting investment and raising revenue to promote development, and developed countries predominantly preoccupied by safeguarding their tax bases to preserve the welfare state and to meet the challenges of ageing. This note provides an overview of the key economic factors shaping tax policy reform in many high-income countries, developing countries, and/or transition economies. It discusses selected reform initiatives that have been high on the policy agenda over the last some 20 years,3 and those that are likely to be important in the coming years. Section II discusses some of the more important determining factors that have shaped tax reform initiatives over the same period, while section III provides a summary of quantitative global and regional developments with respect to tax rates and revenue ratios over this period. Section IV discusses selected specific commonalities in actual tax reforms implemented around the globe over the same time span, and section V concludes. Despite the fairly short span of time, a wide spectrum of tax reforms were implemented. Hence, the approach adopted is eclectic and the presentation of the issues to some degree “impressionistic.”

II. FACTORS SHAPING INTERNATIONAL TAX POLICY TRENDS

Truly global tax reform movements, with a majority of countries adopting broadly similar policy measures, rarely occur—perhaps with the global spread of the VAT over the last 40 years as the most notable exception, with the fall in statutory corporate tax rates coming in as a close second (both phenomena dealt with in what follows)4. However, we frequently 1 “In this world, nothing can be said to be certain, except death and taxes.” Benjamin Franklin, 1789, in a letter to Jean-Baptiste Leroy.

2 In fact, a whole “industry” has emerged that on a daily basis scrutinizes and reports on global tax reform initiatives.

3 Useful recent reviews of tax reform trends are provided in Zee (2004) and Owens (2006).

4 In the late 19th and 20th centuries, the most notable evolution was the emergence and global spread of the income tax.

4

observe common patterns, at least on a regional basis, in tax reforms adopted by different countries over a given period. We believe there are, in fact, underlying factors that induce countries to adopt broadly similar approaches to tax reform over given periods of time with the following ones mentioned in no particular order and frequently overlapping: Globalization of economic activity—i.e., the ever increasing ease with which saving and investment, factors of production, and goods and services can move and do move across borders—is the most frequently noted development.5 This increased mobility has far-reaching consequences for tax policy design, and often gives rise to complicated technical issues (e.g., international allocation of taxation rights; taxation of e-commerce), and sensitive issues of cross-border policy coordination (e.g., attempts by the EU to establish a uniform corporate tax base). In some sense, this development has not in itself presented altogether new tax policy issues, since taxation has always affected behavior and thereby tax bases, and governments have always responded by trying to adopt tax systems to minimize costs and preserve tax bases. But globalization has accentuated the need for continuous adaptation and deepened international cooperation (although some would say that there is no need for increased cooperation, tax competition on the whole being beneficial), and increased the stakes by raising the potential costs of not following suit. Important examples that come to mind include the widening popularity of “flat” taxes, the ever growing use of tax-based incentives that countries apply to attract foreign investors, and the ensuing attempts to establish international “rules of the game” to prevent suboptimal outcomes. Another is the continued deepening of international financial intermediation as reflected, for example, in the emergence of significant off-shore financial centers—in large measure driven by attempts to shield investors from taxation in the jurisdictions where they reside. Employment creation and the need to remove labor tax impediments to labor demand and supply, while perhaps not a global phenomenon, has featured high on the policy agenda in many countries, not least in the EU and OECD areas, as well as in most transition economies. This trend could be seen in the broader context of globalization, which has exposed labor markets in many (particularly developed) countries to increasing competition from low-wage economies and forced structural changes, perhaps, most prominently reflected in attempts to reduce aggregate tax wedges on labor in tandem with reformed benefit systems and other flexibility enhancing labor market reforms.6

5 Although land constitutes the only truly immobile factor of production, cross-border land ownership is far from unusual, and changing ownership patterns can be associated with important financial flows with ramifications for tax bases and tax policy.

6 The so-called “flexicurity model” first adopted in Denmark is one such approach, where it is regarded as a mix (“golden triangle”) of flexibility in the labor market (the ability to easily hire and fire workers) combined with social security for workers and proactive labor market policies http://www.bm.dk/sw3792.asp.

5

A subtle change of views on the equity-efficiency tradeoff, while frequently hard to accurately discern in practice or to distinguish clearly from the forces of globalization, may have importantly affected recent tax policy formulation. In one interpretation, not unequivocally supported by empirical evidence, more attention to efficiency aspects of taxation—supported by optimal tax literature,7 actual experience with extremely high marginal income tax rates in the 1970s/1980s as well as evidence that for all their progressivity, tax systems are largely proportional8—may have been a participatory factor behind a number of fairly recent policy trends, such as the larger role accorded to consumption taxes and the apparent sacrifice of the principle of global income taxation in favor of, for example, the dual income tax (DIT) and (both discussed in more detail in what follows). “Herd behavior,” or put somewhat more positively, adopting tax policy reform that for some reason becomes fashionable among economists and politicians at different points in time, is another factor of some potential importance, although its importance is very hard to assess in practice. This behavior is, in part, driven by political economy factors, with governments eager to demonstrate decisiveness, but using reform models that may have proven successful elsewhere. Examples include the move toward global income taxes in the 1980s–90s; and introduction of green taxes in the 1990s, and flat taxes in the 2000s. In some cases, it is hard to distinguish this behavior from the effects of globalization (e.g., DIT). There are prominent examples of this phenomenon taking the form of attempts to emulate success stories (Ireland on “low” taxes, see Box 1, and Russia on flat taxes).9 Again, it could be held, taking the flat tax as an example, that there is nothing inherently innovative in this approach, which adopts the same underlying rationale that was driving the reforms of the 1980s/90s. However, these reforms have provided important cases for research on effects of specific tax reforms.10 Somewhat related to the concept of herd behavior, but, perhaps, more satisfying to economists, is the idea of “yardstick competition,” which represents an alternative explanation for interdependence in tax setting behavior across jurisdictions to the standard direct competition for tax bases: under yardstick competition (or tax mimicking), governments are judged relative to their neighbors, and voters and potential investors take a country’s tax system and tax rate as a signal of its wider competence and attitudes toward business (Besley and Case, 1995). In practice, however, there is an issue of how to distinguish this

7 Diamond and Mirrlees (1981), Atkinson and Stiglitz (1976), Sandmo (1976). Also see Sørensen (2007).

8 Pechman and Okner (1974) , Musgrave, Case and Herman (1974) are early contributions.

9 There are some indications that, in both cases, the impact of tax policy factors may have been misinterpreted and/or overstated, see Box 1 and the discussion of the flat tax in section IV.

10 An interesting question in this regard is what would have happened with the flat tax “movement’ had the Russian flat tax reform failed to increase revenue?

6

phenomenon from standard tax competition using rate reductions and tax incentives to attract tax bases. Initiatives to strengthen regional economic policy coordination, to induce economic integration and to stimulate growth. Again, these initiatives could be seen in the context of globalization as a means of strengthening economic development and competitiveness of regional groupings. Frequently, they are characterized by a dominant tax policy component, as reflected most clearly in the multitude of customs unions established over the last couple of decades and more that are likely to follow—the most recent initiative being the possible establishment of a Central America Customs Union (CACU)—against the backdrop of sluggish Doha negotiations, typically followed by efforts to harmonize also other tax policies. The EU probably constitutes the best known example, but many other examples of deeper regional harmonization efforts exist (including efforts to establish codes of conduct on tax incentives in Latin American and African groupings, similar to that of the EU). There is a broad range of configurations from the highly formalized EU system to simple customs unions without any revenue pooling mechanisms. Devolution of political and fiscal powers to lower level of government which could be seen as complementary to the partial transfer of national fiscal autonomy to supranational “entities,“ have continuously taken place in numerous countries during recent decades.11 While this has been a development of “stealth”, attracting far less attention than some of the issues enumerated above, it has, nevertheless, importantly shaped the structure of countries’ tax systems. There are very large differences across countries in the policies adopted, with no obvious common policy direction, although one common central concern has been proper tax assignment, i.e., which taxes should be raised centrally, and shared one way or the other with sub-national governments, and which are better raised by local governments, such as property taxes (see Ahmed and Brosio (2006), and Norregaard (1997) in Ter-Minassian (ed.,), (1997)), for a comprehensive discussion of these issues). The strong push for increased—and geographically more spread—natural resource exploration, which has followed the broad-based rise in natural resource prices in recent years (in turn, related to the global economic expansion referred to below), has lead to sharply increased attention to natural resource taxation, and has featured with increasing prominence in the policy debate—not least because of the increase in new oil discoveries (as in East Timor, Ghana, Mauritania, and Uganda). A core question in this area relates to how governments can best share the income stream from resource wealth with private extracting companies for the common good of present and future generations (see IMF (2003)12 for a

11 For a recent discussion of fiscal decentralization over the last two decades in Latin America and East Asia, see Escobar-Lemmon (2001) and Wescott (2005).

12 http://www.imf.org/external/pubs/ft/grrt/eng/060705.htm.

7

discussion of these issues). Another issue pertinent to many of these countries (albeit not discussed in this note) is the appropriate design of domestic or non-oil tax systems. Increasing popular and political concerns about pollution, greenhouse gas (GHG) emissions, and climate change has led to stronger pressures for the application of remedial fiscal instruments, including the use of “green” taxes and, more lately, by “carbon” taxes.13 This is, perhaps, the most important recent development that could be suggestive of the direction of future tax policy trends. It has, however, so far basically manifested itself only in developed countries and with fairly limited actual policy action. With green taxes, countries seek to exploit the twin benefits of correcting for environmental externalities, including to mitigate GHG emissions, and apply revenues to reducing taxes on labor in an attempt to stimulate employment growth.14 The extent of truly global externalities associated with GHG emissions would imply the need for close international policy coordination. However, this is an area where the EU—despite potential adverse implication for the competitiveness of EU- based companies—have decided to take a first decisive step, undoubtedly in the hope that others will follow suit, including through accession to the EU-ETS, as discussed in section IV. Cyclical factors, finally, may play an important role in shaping tax policies. There are, for example, signs that this have been the case recently, with the world economy still in the midst of an extraordinary expansion, based on strong global economic fundamentals, and with 2007 set to become the fifth year with sustained growth at the highest level since the late 1960s, at close to 5 percent.15 The resulting cyclical “dividend” has lead to a general easing of budgetary constraints in many countries, and may have provided an incentive that, in part, explains the tax rate reductions described below (although, again, this policy factor is hard to distinguish from effects of globalization). If this is, indeed, a participatory factor, the underlying structural fiscal balances together with automatic fiscal stabilizers may have been severely weakened, contributing to a procyclical, and thereby potentially destabilizing fiscal policy stance. The dangers of weakened structural fiscal balances over the longer term are also particularly relevant for those economies (usually high income and/or transition economies) that are currently facing the combined challenges of increased longevity and reduced population birthrates, and whose costs of financing social pensions and health care systems are expected to climb over time.

13 Although there are some early signs that the appetite for additional environmental taxes in Europe is fading, see discussion in section IV.

14 However, some observers have argued that these taxes are, in fact, quite similar to labor taxes: to the extent that taxes on household energy use reduce the amount of real income available to households, these are equivalent to an increase in income tax. This suggests that the appropriate level of a pollution tax is one below the level otherwise considered optimal if considered purely from the perspective of mitigating a negative environmental externality (Bovenberg, 1999).

15 Assuming that the widespread financial disturbance during mid/end-year will not significantly slow economic growth.

8

III. REVENUE AND TAX RATE DEVELOPMENTS: SOME EMPIRICAL FACTS This section provides basic data on developments in key tax rates and revenue ratios for different regions since the early 1990s, as a background for the conceptual discussion in section IV.

A. Corporate Income Tax (CIT)

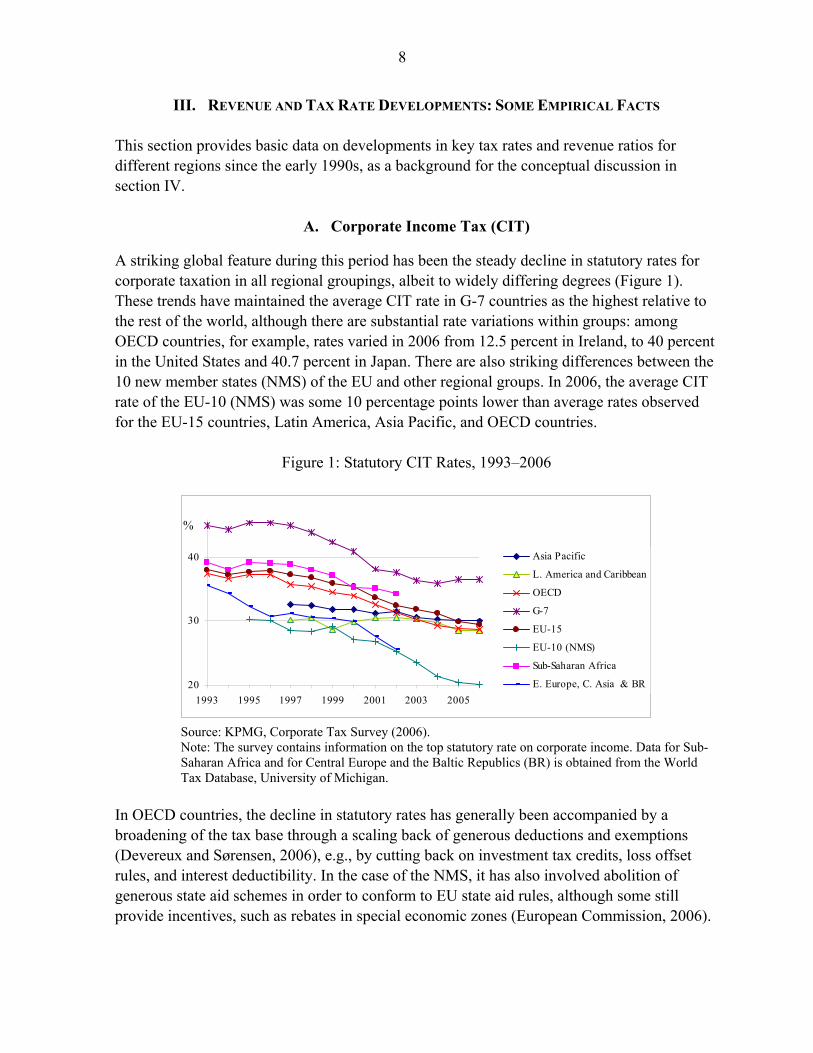

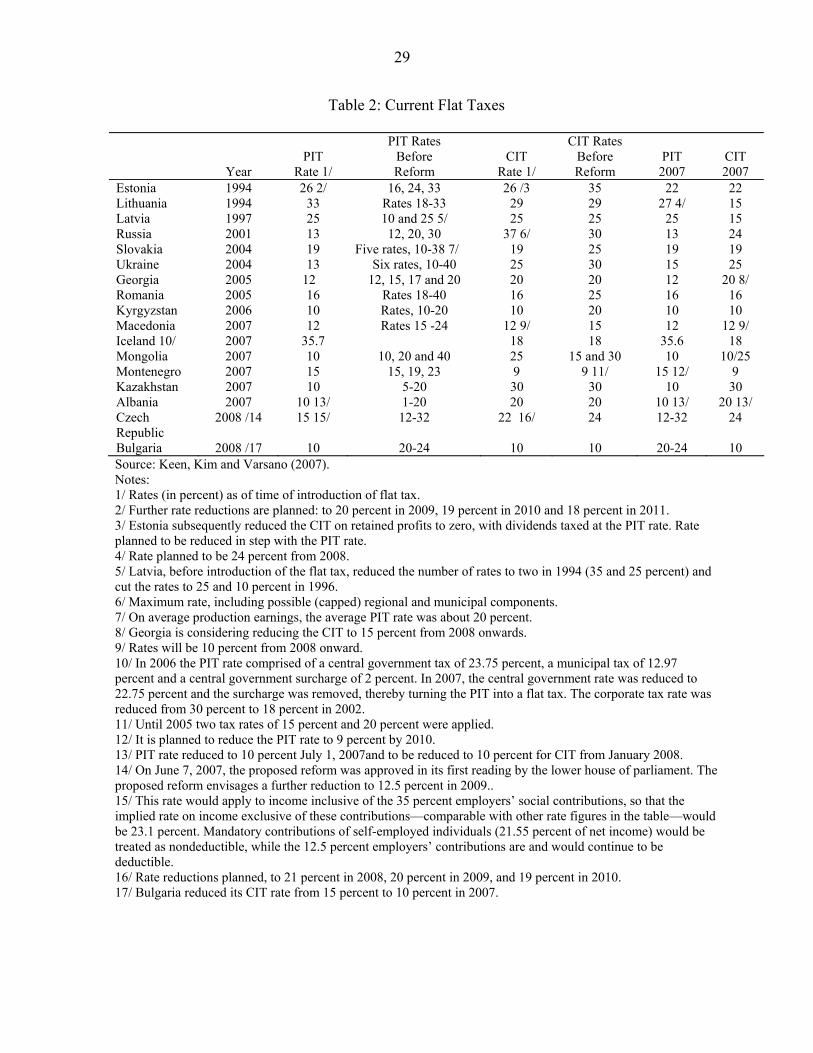

A striking global feature during this period has been the steady decline in statutory rates for corporate taxation in all regional groupings, albeit to widely differing degrees (Figure 1). These trends have maintained the average CIT rate in G-7 countries as the highest relative to the rest of the world, although there are substantial rate variations within groups: among OECD countries, for example, rates varied in 2006 from 12.5 percent in Ireland, to 40 percent in the United States and 40.7 percent in Japan. There are also striking differences between the 10 new member states (NMS) of the EU and other regional groups. In 2006, the average CIT rate of the EU-10 (NMS) was some 10 percentage points lower than average rates observed for the EU-15 countries, Latin America, Asia Pacific, and OECD countries.

Figure 1: Statutory CIT Rates, 1993–2006

20

30

40

1993 1995 1997 1999 2001 2003 2005

%

Asia Pacific

L. America and Caribbean

OECD

G-7

EU-15

EU-10 (NMS)

Sub-Saharan Africa

E. Europe, C. Asia & BR

Source: KPMG, Corporate Tax Survey (2006). Note: The survey contains information on the top statutory rate on corporate income. Data for Sub-Saharan Africa and for Central Europe and the Baltic Republics (BR) is obtained from the World Tax Database, University of Michigan.

In OECD countries, the decline in statutory rates has generally been accompanied by a broadening of the tax base through a scaling back of generous deductions and exemptions (Devereux and Sørensen, 2006), e.g., by cutting back on investment tax credits, loss offset rules, and interest deductibility. In the case of the NMS, it has also involved abolition of generous state aid schemes in order to conform to EU state aid rules, although some still provide incentives, such as rebates in special economic zones (European Commission, 2006).

9

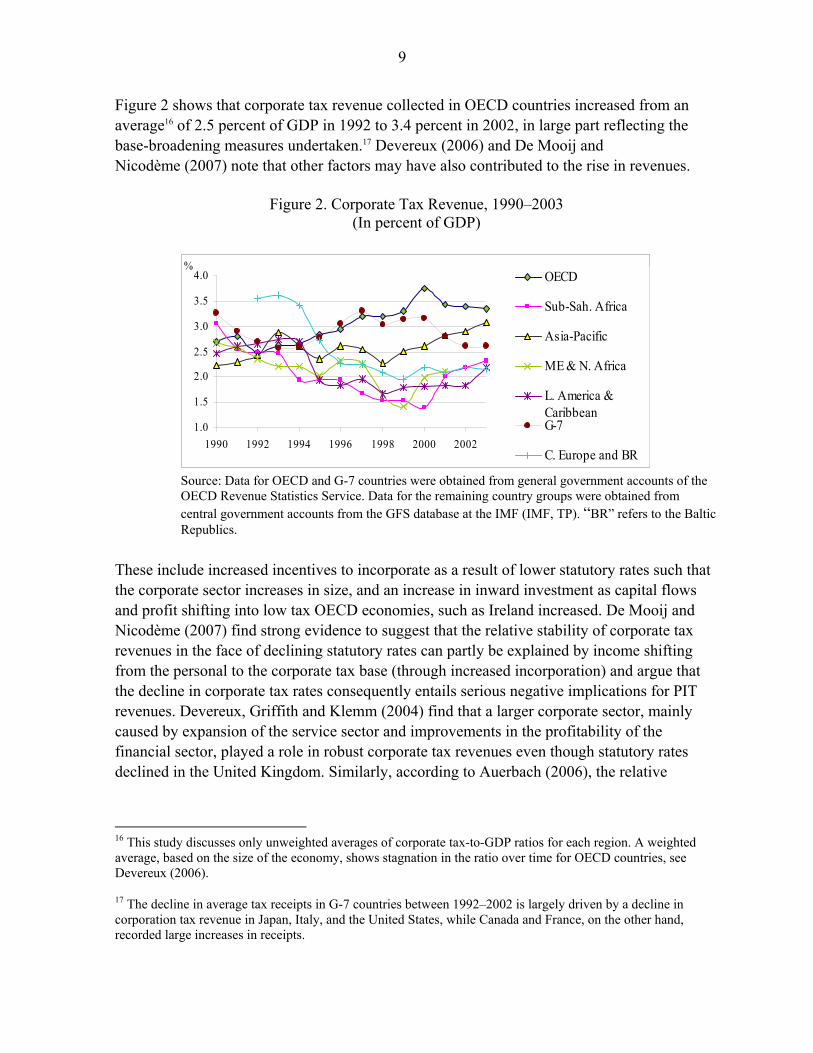

Figure 2 shows that corporate tax revenue collected in OECD countries increased from an average16 of 2.5 percent of GDP in 1992 to 3.4 percent in 2002, in large part reflecting the base-broadening measures undertaken.17 Devereux (2006) and De Mooij and Nicodème (2007) note that other factors may have also contributed to the rise in revenues.

Figure 2. Corporate Tax Revenue, 1990–2003

(In percent of GDP)

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1990 1992 1994 1996 1998 2000 2002

%OECD

Sub-Sah. Africa

Asia-Pacific

ME & N. Africa

L. America &CaribbeanG-7

C. Europe and BR

Source: Data for OECD and G-7 countries were obtained from general government accounts of the OECD Revenue Statistics Service. Data for the remaining country groups were obtained from central government accounts from the GFS database at the IMF (IMF, TP). “BR” refers to the Baltic Republics.

These include increased incentives to incorporate as a result of lower statutory rates such that the corporate sector increases in size, and an increase in inward investment as capital flows and profit shifting into low tax OECD economies, such as Ireland increased. De Mooij and Nicodème (2007) find strong evidence to suggest that the relative stability of corporate tax revenues in the face of declining statutory rates can partly be explained by income shifting from the personal to the corporate tax base (through increased incorporation) and argue that the decline in corporate tax rates consequently entails serious negative implications for PIT revenues. Devereux, Griffith and Klemm (2004) find that a larger corporate sector, mainly caused by expansion of the service sector and improvements in the profitability of the financial sector, played a role in robust corporate tax revenues even though statutory rates declined in the United Kingdom. Similarly, according to Auerbach (2006), the relative

16 This study discusses only unweighted averages of corporate tax-to-GDP ratios for each region. A weighted average, based on the size of the economy, shows stagnation in the ratio over time for OECD countries, see Devereux (2006).

17 The decline in average tax receipts in G-7 countries between 1992–2002 is largely driven by a decline in corporation tax revenue in Japan, Italy, and the United States, while Canada and France, on the other hand, recorded large increases in receipts.

10

stability of financial sector profits in the United States helped to dampen the overall volatility of revenues from the corporate sector. However, in developing or low-income countries, there appears to have been a tendency toward a narrowing of the corporate tax base (or base stagnation) as statutory rates have fallen, leading to a general decline in corporate revenue-to-GDP ratios.18 This is somewhat worrying insofar as corporate tax revenues account on average for approximately one-sixth of total tax revenues in developing countries, i.e., more than in OECD countries. Keen and Simone (2004) document an increase in the use of tax holidays, free trade zones, and tax breaks in some of the poorest developing countries. They note, for instance, that while at the start of the 1990s only one sub-Saharan country offered tax holidays, virtually all did so toward the end of the decade. Corporate tax revenues as a percentage of GDP, however, seem to have improved in some groupings since the late 1990s, although these trends may be largely cyclical indicating buoyant tax revenues in Asia-Pacific region as it emerged from the crisis in 1997–98, as well as sustained economic growth in Africa and Asia in the recent years. These recent gains in corporate tax revenue may also have been importantly affected by buoyant natural resource taxes, particularly pertaining to oil.19

B. Personal Income Tax

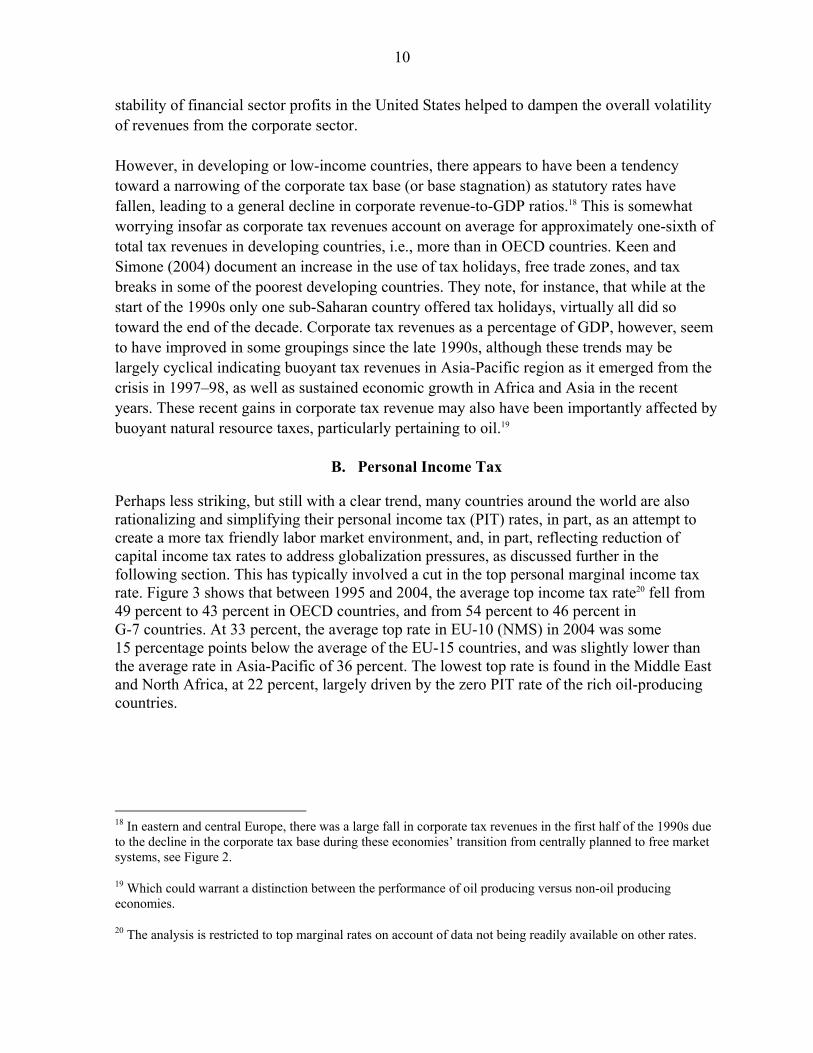

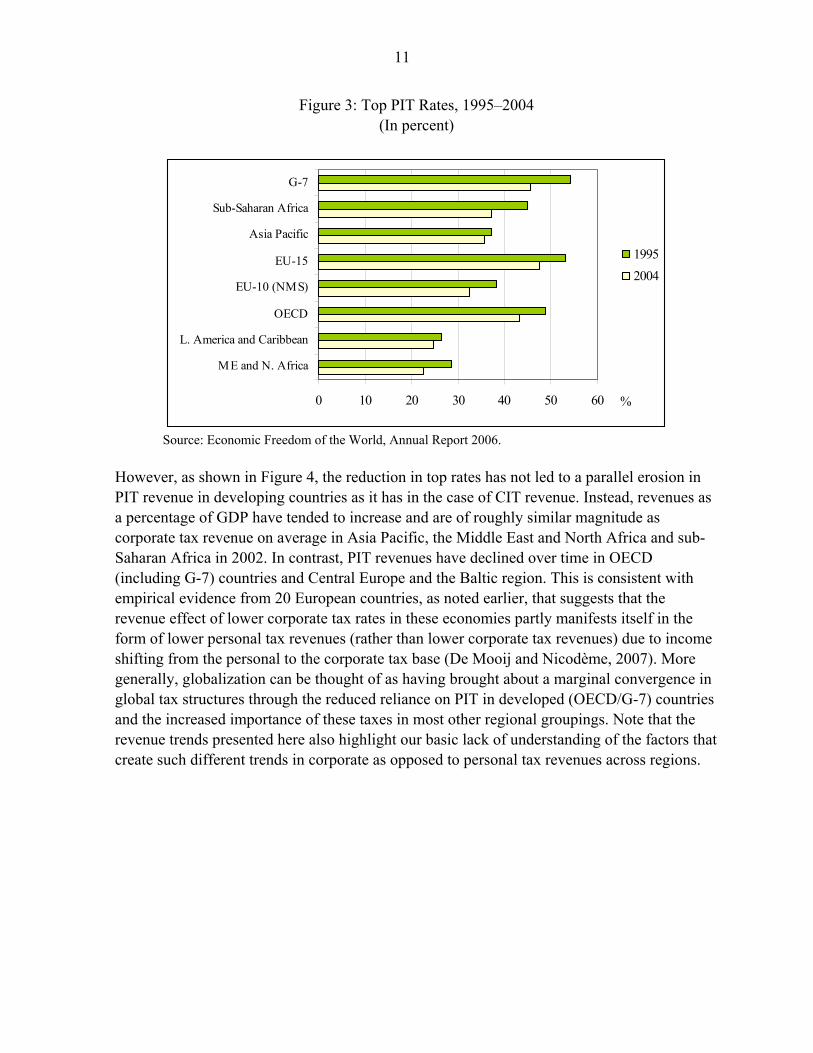

Perhaps less striking, but still with a clear trend, many countries around the world are also rationalizing and simplifying their personal income tax (PIT) rates, in part, as an attempt to create a more tax friendly labor market environment, and, in part, reflecting reduction of capital income tax rates to address globalization pressures, as discussed further in the following section. This has typically involved a cut in the top personal marginal income tax rate. Figure 3 shows that between 1995 and 2004, the average top income tax rate20 fell from 49 percent to 43 percent in OECD countries, and from 54 percent to 46 percent in G-7 countries. At 33 percent, the average top rate in EU-10 (NMS) in 2004 was some 15 percentage points below the average of the EU-15 countries, and was slightly lower than the average rate in Asia-Pacific of 36 percent. The lowest top rate is found in the Middle East and North Africa, at 22 percent, largely driven by the zero PIT rate of the rich oil-producing countries.

18 In eastern and central Europe, there was a large fall in corporate tax revenues in the first half of the 1990s due to the decline in the corporate tax base during these economies’ transition from centrally planned to free market systems, see Figure 2.

19 Which could warrant a distinction between the performance of oil producing versus non-oil producing economies.

20 The analysis is restricted to top marginal rates on account of data not being readily available on other rates.

11

Figure 3: Top PIT Rates, 1995–2004 (In percent)

0 10 20 30 40 50 60

ME and N. Africa

L. America and Caribbean

OECD

EU-10 (NMS)

EU-15

Asia Pacific

Sub-Saharan Africa

G-7

%

19952004

Source: Economic Freedom of the World, Annual Report 2006.

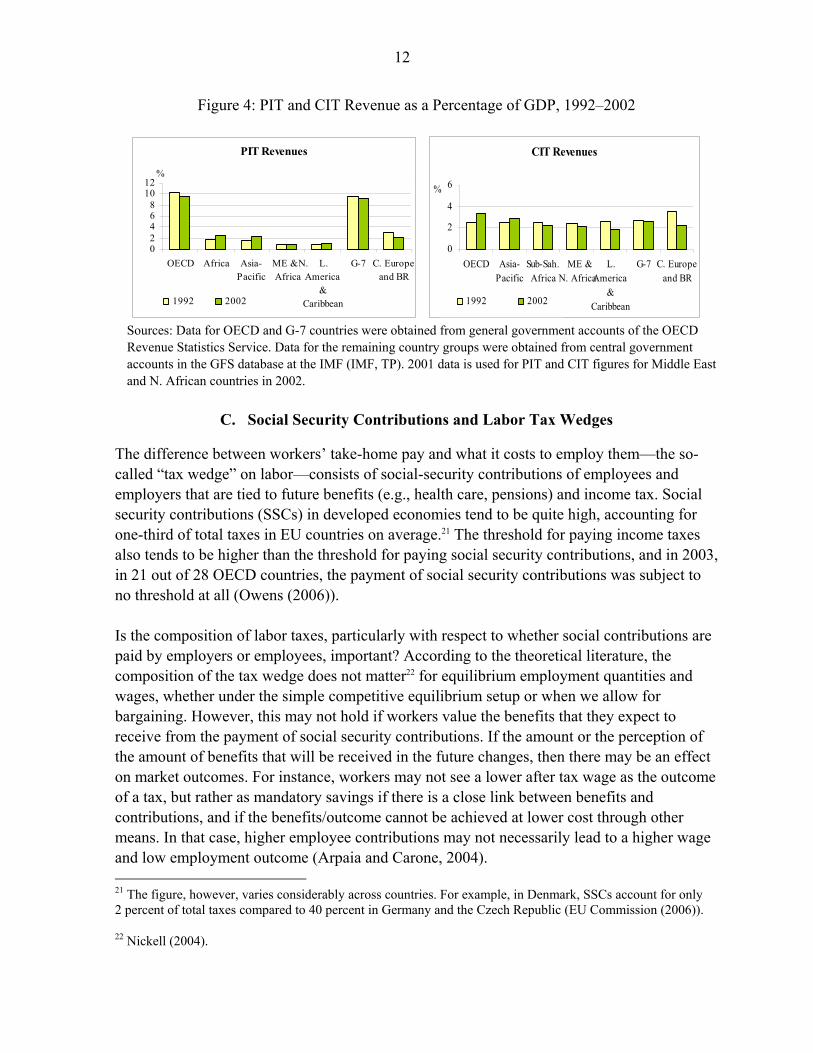

However, as shown in Figure 4, the reduction in top rates has not led to a parallel erosion in PIT revenue in developing countries as it has in the case of CIT revenue. Instead, revenues as a percentage of GDP have tended to increase and are of roughly similar magnitude as corporate tax revenue on average in Asia Pacific, the Middle East and North Africa and sub-Saharan Africa in 2002. In contrast, PIT revenues have declined over time in OECD (including G-7) countries and Central Europe and the Baltic region. This is consistent with empirical evidence from 20 European countries, as noted earlier, that suggests that the revenue effect of lower corporate tax rates in these economies partly manifests itself in the form of lower personal tax revenues (rather than lower corporate tax revenues) due to income shifting from the personal to the corporate tax base (De Mooij and Nicodème, 2007). More generally, globalization can be thought of as having brought about a marginal convergence in global tax structures through the reduced reliance on PIT in developed (OECD/G-7) countries and the increased importance of these taxes in most other regional groupings. Note that the revenue trends presented here also highlight our basic lack of understanding of the factors that create such different trends in corporate as opposed to personal tax revenues across regions.

12

Figure 4: PIT and CIT Revenue as a Percentage of GDP, 1992–2002

PIT Revenues

02468

1012

OECD Africa Asia-Pacific

ME &N.Africa

L.America

&Caribbean

G-7 C. Europeand BR

%

1992 2002

CIT Revenues

0

2

4

6

OECD Asia-Pacific

Sub-Sah.Africa

ME &N. Africa

L.America

&Caribbean

G-7 C. Europeand BR

%

1992 2002

Sources: Data for OECD and G-7 countries were obtained from general government accounts of the OECD Revenue Statistics Service. Data for the remaining country groups were obtained from central government accounts in the GFS database at the IMF (IMF, TP). 2001 data is used for PIT and CIT figures for Middle East and N. African countries in 2002.

C. Social Security Contributions and Labor Tax Wedges

The difference between workers’ take-home pay and what it costs to employ them—the so- called “tax wedge” on labor—consists of social-security contributions of employees and employers that are tied to future benefits (e.g., health care, pensions) and income tax. Social security contributions (SSCs) in developed economies tend to be quite high, accounting for one-third of total taxes in EU countries on average.21 The threshold for paying income taxes also tends to be higher than the threshold for paying social security contributions, and in 2003, in 21 out of 28 OECD countries, the payment of social security contributions was subject to no threshold at all (Owens (2006)). Is the composition of labor taxes, particularly with respect to whether social contributions are paid by employers or employees, important? According to the theoretical literature, the composition of the tax wedge does not matter22 for equilibrium employment quantities and wages, whether under the simple competitive equilibrium setup or when we allow for bargaining. However, this may not hold if workers value the benefits that they expect to receive from the payment of social security contributions. If the amount or the perception of the amount of benefits that will be received in the future changes, then there may be an effect on market outcomes. For instance, workers may not see a lower after tax wage as the outcome of a tax, but rather as mandatory savings if there is a close link between benefits and contributions, and if the benefits/outcome cannot be achieved at lower cost through other means. In that case, higher employee contributions may not necessarily lead to a higher wage and low employment outcome (Arpaia and Carone, 2004). 21 The figure, however, varies considerably across countries. For example, in Denmark, SSCs account for only 2 percent of total taxes compared to 40 percent in Germany and the Czech Republic (EU Commission (2006)).

22 Nickell (2004).

13

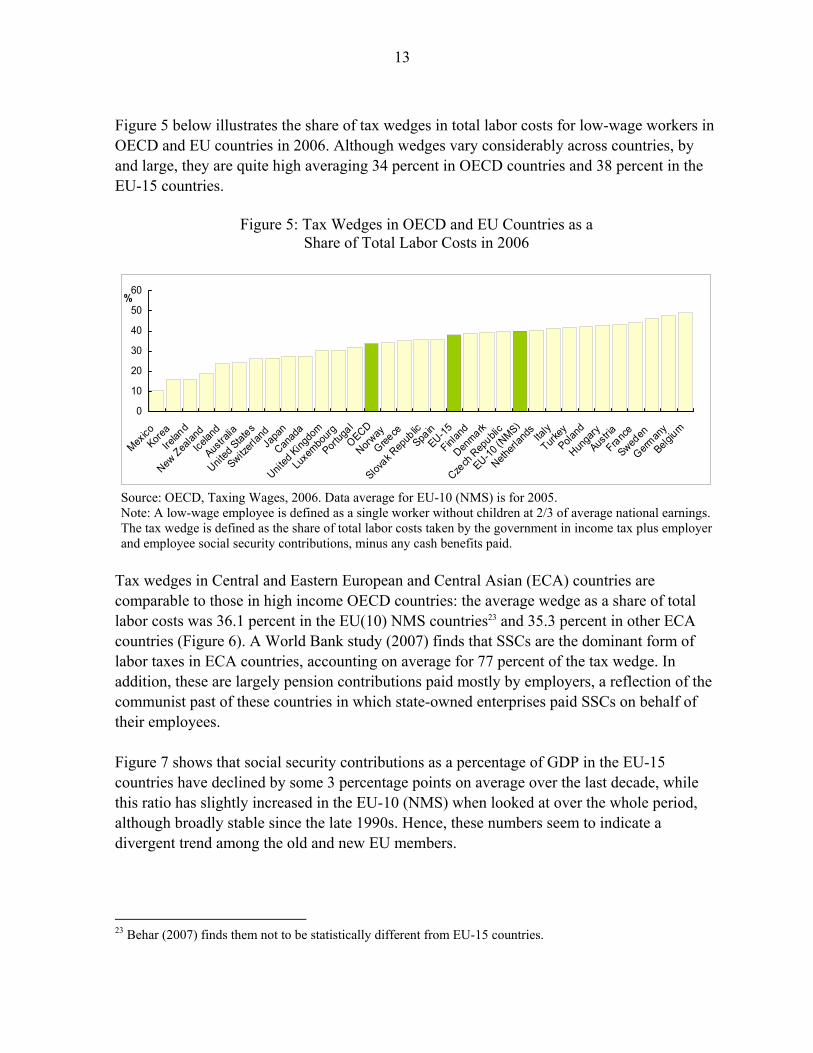

Figure 5 below illustrates the share of tax wedges in total labor costs for low-wage workers in OECD and EU countries in 2006. Although wedges vary considerably across countries, by and large, they are quite high averaging 34 percent in OECD countries and 38 percent in the EU-15 countries.

Figure 5: Tax Wedges in OECD and EU Countries as a Share of Total Labor Costs in 2006

0

10

20

30

40

50

60

Mexico

KoreaIre

land

New Zea

land

Icelan

d

Austra

lia

United

States

Switzerl

and Ja

pan

Canad

a

United

Kingdo

m

Luxe

mbourg

Portug

al

OECD

Norway

Greece

Slovak R

epub

lic

Spain

EU-15

Finlan

d

Denmark

Czech

Rep

ublic

EU-10 (N

MS)

Netherl

ands

Ita

ly

Turkey

Poland

Hunga

ry

Austria

France

Sweden

German

y

Belgium

%

Source: OECD, Taxing Wages, 2006. Data average for EU-10 (NMS) is for 2005. Note: A low-wage employee is defined as a single worker without children at 2/3 of average national earnings. The tax wedge is defined as the share of total labor costs taken by the government in income tax plus employer and employee social security contributions, minus any cash benefits paid.

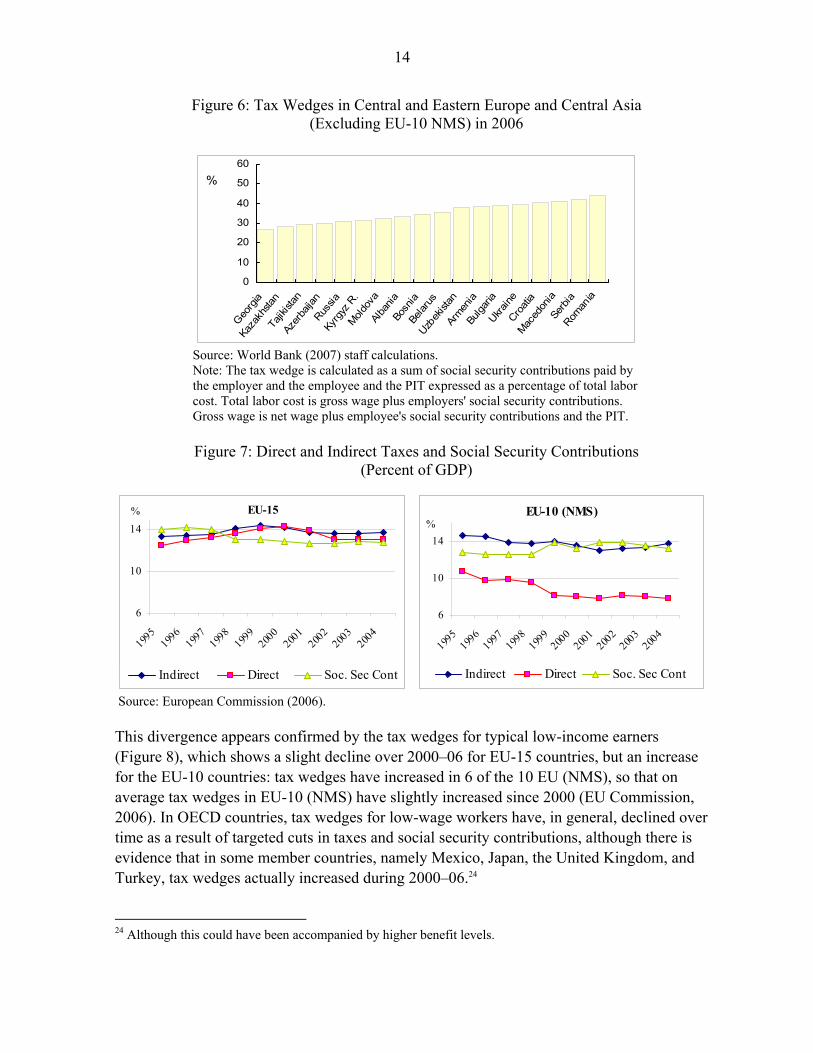

Tax wedges in Central and Eastern European and Central Asian (ECA) countries are comparable to those in high income OECD countries: the average wedge as a share of total labor costs was 36.1 percent in the EU(10) NMS countries23 and 35.3 percent in other ECA countries (Figure 6). A World Bank study (2007) finds that SSCs are the dominant form of labor taxes in ECA countries, accounting on average for 77 percent of the tax wedge. In addition, these are largely pension contributions paid mostly by employers, a reflection of the communist past of these countries in which state-owned enterprises paid SSCs on behalf of their employees. Figure 7 shows that social security contributions as a percentage of GDP in the EU-15 countries have declined by some 3 percentage points on average over the last decade, while this ratio has slightly increased in the EU-10 (NMS) when looked at over the whole period, although broadly stable since the late 1990s. Hence, these numbers seem to indicate a divergent trend among the old and new EU members.

23 Behar (2007) finds them not to be statistically different from EU-15 countries.

14

Figure 6: Tax Wedges in Central and Eastern Europe and Central Asia (Excluding EU-10 NMS) in 2006

0

10

20

30

40

50

60

Georg

iaKa

zakh

stan

Tajik

istan

Azer

baija

nRus

siaKy

rgyz

R.

Moldov

aAl

bania

Bosn

ia Be

larus

Uzbek

istan

Armen

iaBu

lgaria

Ukraine

Croati

aMac

edon

iaSe

rbia

Roman

ia

%

Source: World Bank (2007) staff calculations. Note: The tax wedge is calculated as a sum of social security contributions paid by the employer and the employee and the PIT expressed as a percentage of total labor cost. Total labor cost is gross wage plus employers' social security contributions. Gross wage is net wage plus employee's social security contributions and the PIT.

Figure 7: Direct and Indirect Taxes and Social Security Contributions

(Percent of GDP)

EU-15

6

10

14

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

%

Indirect Direct Soc. Sec Cont

EU-10 (NMS)

6

10

14

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

%

Indirect Direct Soc. Sec Cont

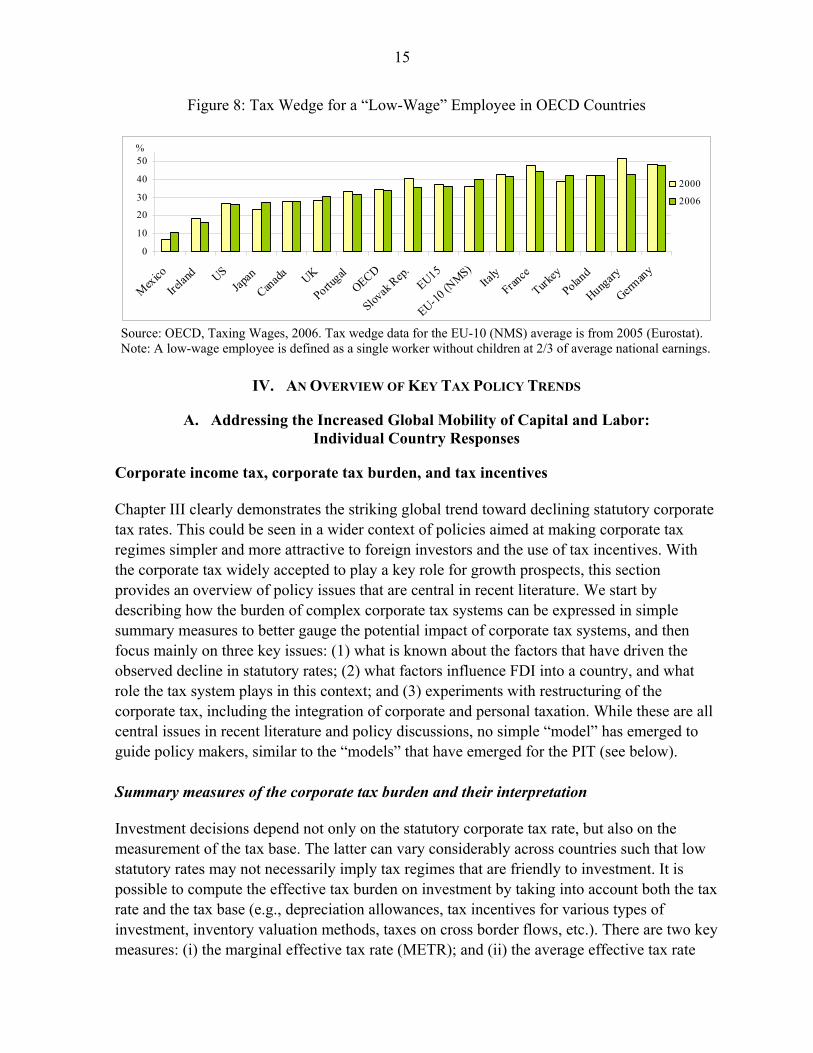

Source: European Commission (2006). This divergence appears confirmed by the tax wedges for typical low-income earners (Figure 8), which shows a slight decline over 2000–06 for EU-15 countries, but an increase for the EU-10 countries: tax wedges have increased in 6 of the 10 EU (NMS), so that on average tax wedges in EU-10 (NMS) have slightly increased since 2000 (EU Commission, 2006). In OECD countries, tax wedges for low-wage workers have, in general, declined over time as a result of targeted cuts in taxes and social security contributions, although there is evidence that in some member countries, namely Mexico, Japan, the United Kingdom, and Turkey, tax wedges actually increased during 2000–06.24 24 Although this could have been accompanied by higher benefit levels.

15

Figure 8: Tax Wedge for a “Low-Wage” Employee in OECD Countries

0

10

20

30

40

50

Mexico

Irelan

d USJap

an

Canada UK

Portugal

OECD

Slovak

Rep.EU15

EU-10 (N

MS)Ita

lyFran

ce

Turkey

Poland

Hungary

Germany

%

2000

2006

Source: OECD, Taxing Wages, 2006. Tax wedge data for the EU-10 (NMS) average is from 2005 (Eurostat). Note: A low-wage employee is defined as a single worker without children at 2/3 of average national earnings.

IV. AN OVERVIEW OF KEY TAX POLICY TRENDS

A. Addressing the Increased Global Mobility of Capital and Labor: Individual Country Responses

Corporate income tax, corporate tax burden, and tax incentives Chapter III clearly demonstrates the striking global trend toward declining statutory corporate tax rates. This could be seen in a wider context of policies aimed at making corporate tax regimes simpler and more attractive to foreign investors and the use of tax incentives. With the corporate tax widely accepted to play a key role for growth prospects, this section provides an overview of policy issues that are central in recent literature. We start by describing how the burden of complex corporate tax systems can be expressed in simple summary measures to better gauge the potential impact of corporate tax systems, and then focus mainly on three key issues: (1) what is known about the factors that have driven the observed decline in statutory rates; (2) what factors influence FDI into a country, and what role the tax system plays in this context; and (3) experiments with restructuring of the corporate tax, including the integration of corporate and personal taxation. While these are all central issues in recent literature and policy discussions, no simple “model” has emerged to guide policy makers, similar to the “models” that have emerged for the PIT (see below). Summary measures of the corporate tax burden and their interpretation Investment decisions depend not only on the statutory corporate tax rate, but also on the measurement of the tax base. The latter can vary considerably across countries such that low statutory rates may not necessarily imply tax regimes that are friendly to investment. It is possible to compute the effective tax burden on investment by taking into account both the tax rate and the tax base (e.g., depreciation allowances, tax incentives for various types of investment, inventory valuation methods, taxes on cross border flows, etc.). There are two key measures: (i) the marginal effective tax rate (METR); and (ii) the average effective tax rate

16

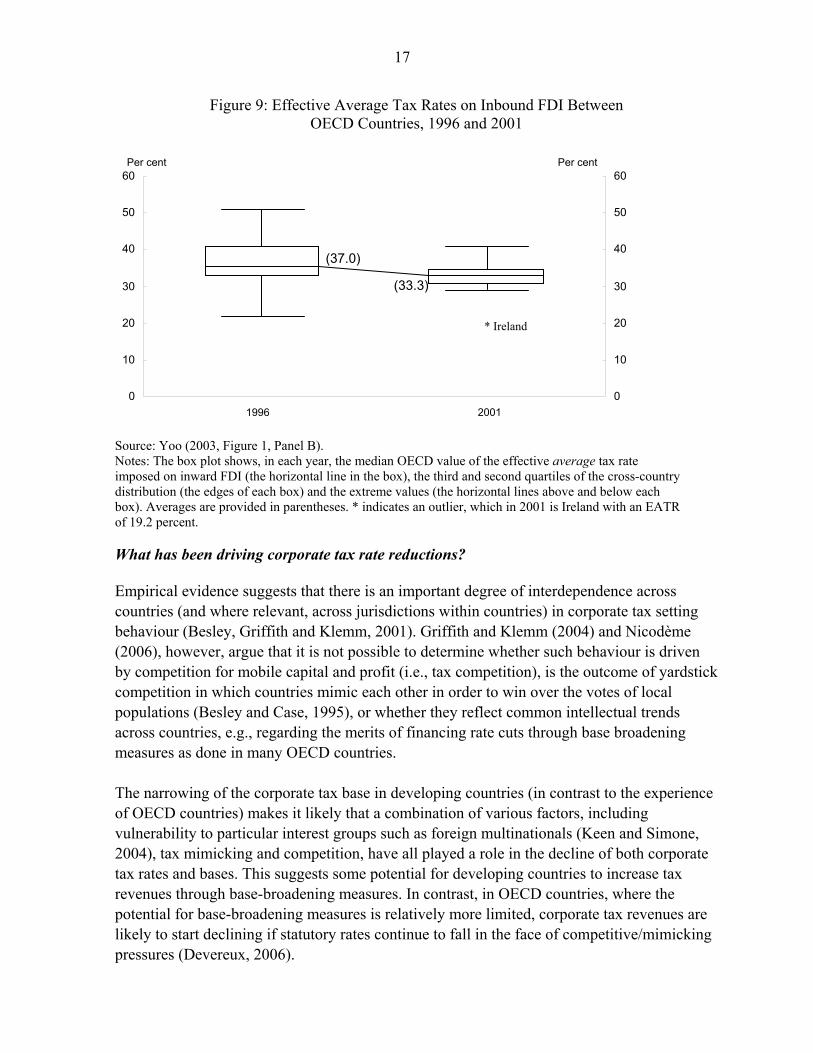

(AETR).25 The METR refers to the intensive margin of capital formation, namely, the scale or level of investment (or, in other words, the effective rate for a project that just breaks even), whereas the AETR refers to the extensive margin, namely the discrete decision of where to locate investment (or the effective rate for a profitable project).26 Consequently, it is the latter concept that is relevant for understanding the capital location decisions of multinational firms and for an insight into the international tax competitiveness of countries (Devereux and Griffith, 1999, 2003). However, it should be noted that statutory rates (possibly in conjunction with withholding taxes) remain relevant for understanding where firms choose to locate their profits (for example, through transfer pricing arrangements), which tend to be even more mobile than capital itself. Evidence suggests that AETRs have fallen significantly in OECD countries, notwithstanding the expansion in the tax base. The figure 9 shows that the average value of AETR on inbound FDI in OECD countries27 fell from 37 percent in 1996 to 33.3 percent in 2001. Although dispersion in AETRs has also declined, there are, nevertheless, considerable differences across countries, with AETRs on inbound FDI estimated at 40 percent in Turkey28 and Japan and 19 percent in Ireland (Yoo, 2003). Deveruex (2007) reports that nine of the ten new member states (NMS) were characterized by the lowest AETRs among EU countries, and that effective rates were likely to be even lower if various tax incentives available in the NMS had been taken into account. While data for developing countries is not easily available, there is some evidence to indicate that AETRs have declined. For instance, Nassar (2007) documents that AETRs in 15 Caribbean countries fell by 10 percentage points to 26 percent between 1985 and 2005.

25 See Devereux and Griffith (2003) for a discussion of hypothetical and accounting-based AETR and METR measures.

26 The AETR measure constructed by Devereux and Griffith (2003) is a weighted average of the METR and the statutory rate adjusted for personal taxes. As they explain, ‘for a marginal investment, it is equal to the METR. As the rate of profit rises, it converges to the adjusted statutory rate. It can, therefore, be interpreted as summarizing the distribution of effective tax rates for an investment project over a range of profitability, with the EMTR representing the special case of a marginal investment.’ 27 Constructed by Yoo (2003), these indicators measure the wedge between pre-tax and posttax return on FDI taking into account home and host country tax policies, interaction of these policies, and taxation of cross-border income. 28 Turkey has since reduced its CIT rate, from 33 percent to 20 percent in 2006, and, therefore, AETRs are likely to be lower.

17

Figure 9: Effective Average Tax Rates on Inbound FDI Between OECD Countries, 1996 and 2001

Source: Yoo (2003, Figure 1, Panel B). Notes: The box plot shows, in each year, the median OECD value of the effective average tax rate imposed on inward FDI (the horizontal line in the box), the third and second quartiles of the cross-country distribution (the edges of each box) and the extreme values (the horizontal lines above and below each box). Averages are provided in parentheses. * indicates an outlier, which in 2001 is Ireland with an EATR of 19.2 percent. What has been driving corporate tax rate reductions? Empirical evidence suggests that there is an important degree of interdependence across countries (and where relevant, across jurisdictions within countries) in corporate tax setting behaviour (Besley, Griffith and Klemm, 2001). Griffith and Klemm (2004) and Nicodème (2006), however, argue that it is not possible to determine whether such behaviour is driven by competition for mobile capital and profit (i.e., tax competition), is the outcome of yardstick competition in which countries mimic each other in order to win over the votes of local populations (Besley and Case, 1995), or whether they reflect common intellectual trends across countries, e.g., regarding the merits of financing rate cuts through base broadening measures as done in many OECD countries. The narrowing of the corporate tax base in developing countries (in contrast to the experience of OECD countries) makes it likely that a combination of various factors, including vulnerability to particular interest groups such as foreign multinationals (Keen and Simone, 2004), tax mimicking and competition, have all played a role in the decline of both corporate tax rates and bases. This suggests some potential for developing countries to increase tax revenues through base-broadening measures. In contrast, in OECD countries, where the potential for base-broadening measures is relatively more limited, corporate tax revenues are likely to start declining if statutory rates continue to fall in the face of competitive/mimicking pressures (Devereux, 2006).

0

10

20

30

40

50

60

1996 20010

10

20

30

40

50

60

(37.0)

(33.3)

* Ireland

Per cent Per cent

18

The impact of taxes on FDI A key question is whether low AETRs or statutory rates are successful in attracting capital flows. Typically, studies focus on FDI out of OECD member countries—in particular, the United States for which data tends to be most reliable (Gordon and Hines, 2002)—and into (mostly) other OECD countries. Empirical evidence for developing countries is generally limited (see Ho and Liu, 2007 for a review of empirical evidence). By and large, evidence suggests that statutory tax rates and AETRs do appear to affect the location of capital (De Mooij and Everdeen, 2006). For example, Hines (1996) finds evidence that the location of foreign investment into the United States is affected by differences in U.S. state CITs. More recently, Buettner and Ruf (2007) find that statutory tax rates play a significant role in the decision by German multinationals on where to locate or hold subsidiaries abroad. However, Devereux and Maffini (2007) and Devereux and Griffith (2003) argue that the empirical literature is fraught with various shortcomings, including (among others) that FDI is an imperfect measure of real investment activity, difficulties inherent in measuring effective tax rates, and a host of issues associated with econometric methodology, such that it is impossible to summarize the results of the empirical literature into a quantitative measure of the impact of the effect of corporation tax on the location of capital. Consequently, estimates of the elasticity of investment to tax rates can vary considerably according to sample type and methodology (Devereux and Maffini, 2007).29 Moreover, a growing body of evidence suggests that other factors also matter for attracting FDI, perhaps more so than tax. A study of FDI in major emerging economies (Brazil, India, China, and Mexico) by McKinsey (2003) found that targeted FDI policies, such as tax holidays, accelerated depreciation, and import duty exemptions (among others) were ineffective in influencing the volume of FDI.30 Furthermore, in many cases, they were counter productive, by contributing directly to fiscal and administrative costs as well as indirectly by lowering productivity or by encouraging inefficient levels of investment. Instead, primary considerations when MNEs invested abroad were macroeconomic stability, the quality of infrastructure and the labor force, the size and growth of the domestic market, and the accessibility of location.

29 De Mooij and Everdeen (2006) compare the outcomes of 31 empirical studies by computing the tax rate elasticity under a uniform definition and report that a 1 percentage point reduction in host country tax typically raises foreign investment by 2.1 percentage points.

30 In contrast, for China, Tseng and Zebreg (2003) note that preferential policies may have been effective in attracting FDI, at least initially, but over time created distortions and a complex tax system that is now being reformed (for example, China has unified the corporate tax for foreign and domestic enterprises effective January 1, 2008).

19

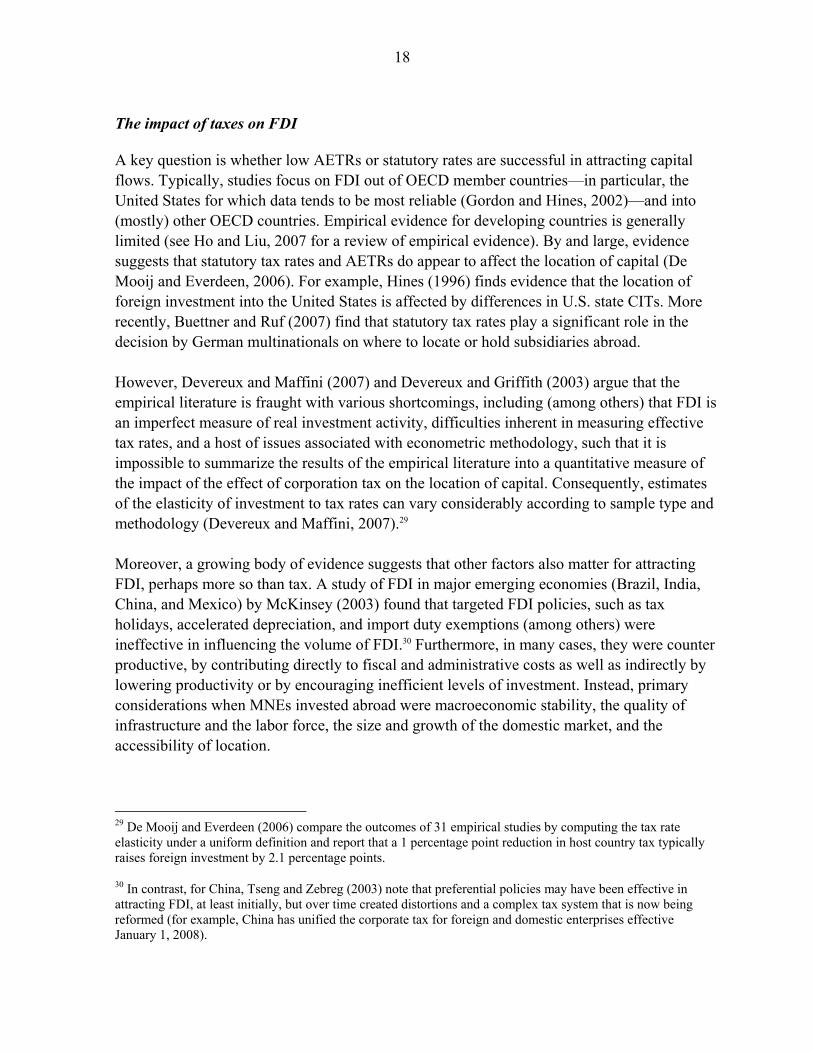

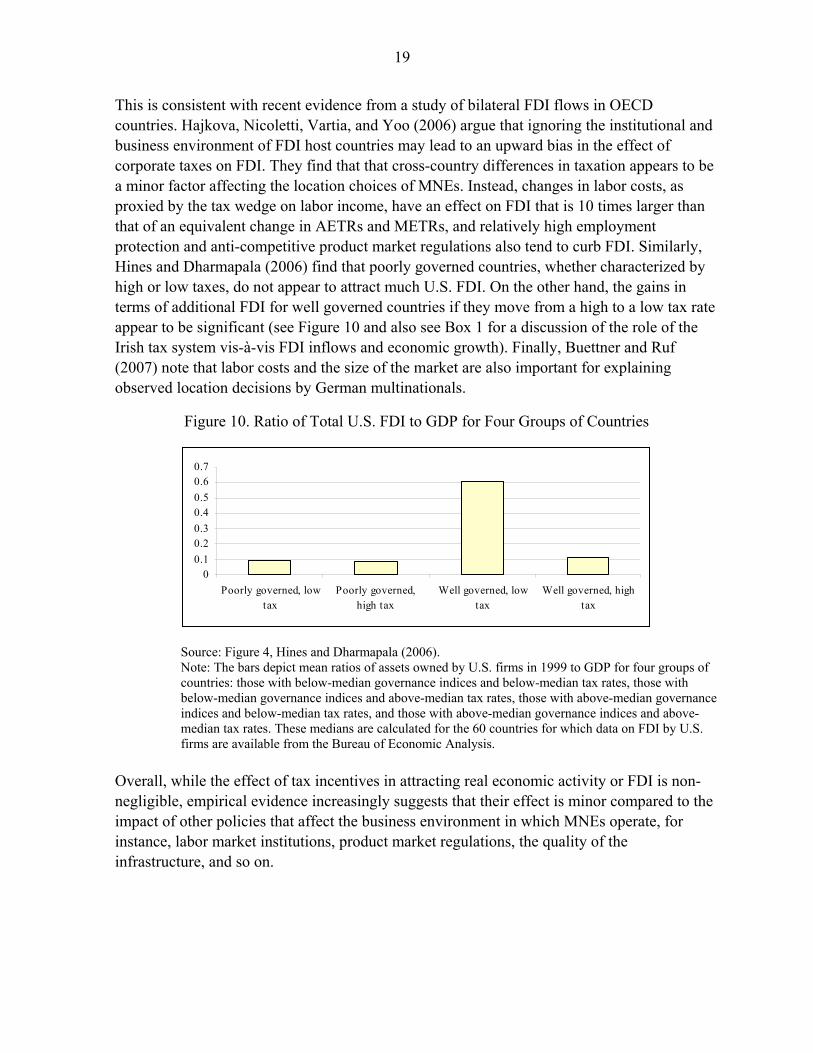

This is consistent with recent evidence from a study of bilateral FDI flows in OECD countries. Hajkova, Nicoletti, Vartia, and Yoo (2006) argue that ignoring the institutional and business environment of FDI host countries may lead to an upward bias in the effect of corporate taxes on FDI. They find that that cross-country differences in taxation appears to be a minor factor affecting the location choices of MNEs. Instead, changes in labor costs, as proxied by the tax wedge on labor income, have an effect on FDI that is 10 times larger than that of an equivalent change in AETRs and METRs, and relatively high employment protection and anti-competitive product market regulations also tend to curb FDI. Similarly, Hines and Dharmapala (2006) find that poorly governed countries, whether characterized by high or low taxes, do not appear to attract much U.S. FDI. On the other hand, the gains in terms of additional FDI for well governed countries if they move from a high to a low tax rate appear to be significant (see Figure 10 and also see Box 1 for a discussion of the role of the Irish tax system vis-à-vis FDI inflows and economic growth). Finally, Buettner and Ruf (2007) note that labor costs and the size of the market are also important for explaining observed location decisions by German multinationals.

Figure 10. Ratio of Total U.S. FDI to GDP for Four Groups of Countries

00.10.20.30.40.50.60.7

Poorly governed, lowtax

Poorly governed,high tax

Well governed, lowtax

Well governed, hightax

Source: Figure 4, Hines and Dharmapala (2006). Note: The bars depict mean ratios of assets owned by U.S. firms in 1999 to GDP for four groups of countries: those with below-median governance indices and below-median tax rates, those with below-median governance indices and above-median tax rates, those with above-median governance indices and below-median tax rates, and those with above-median governance indices and above-median tax rates. These medians are calculated for the 60 countries for which data on FDI by U.S. firms are available from the Bureau of Economic Analysis.

Overall, while the effect of tax incentives in attracting real economic activity or FDI is non-negligible, empirical evidence increasingly suggests that their effect is minor compared to the impact of other policies that affect the business environment in which MNEs operate, for instance, labor market institutions, product market regulations, the quality of the infrastructure, and so on.

20

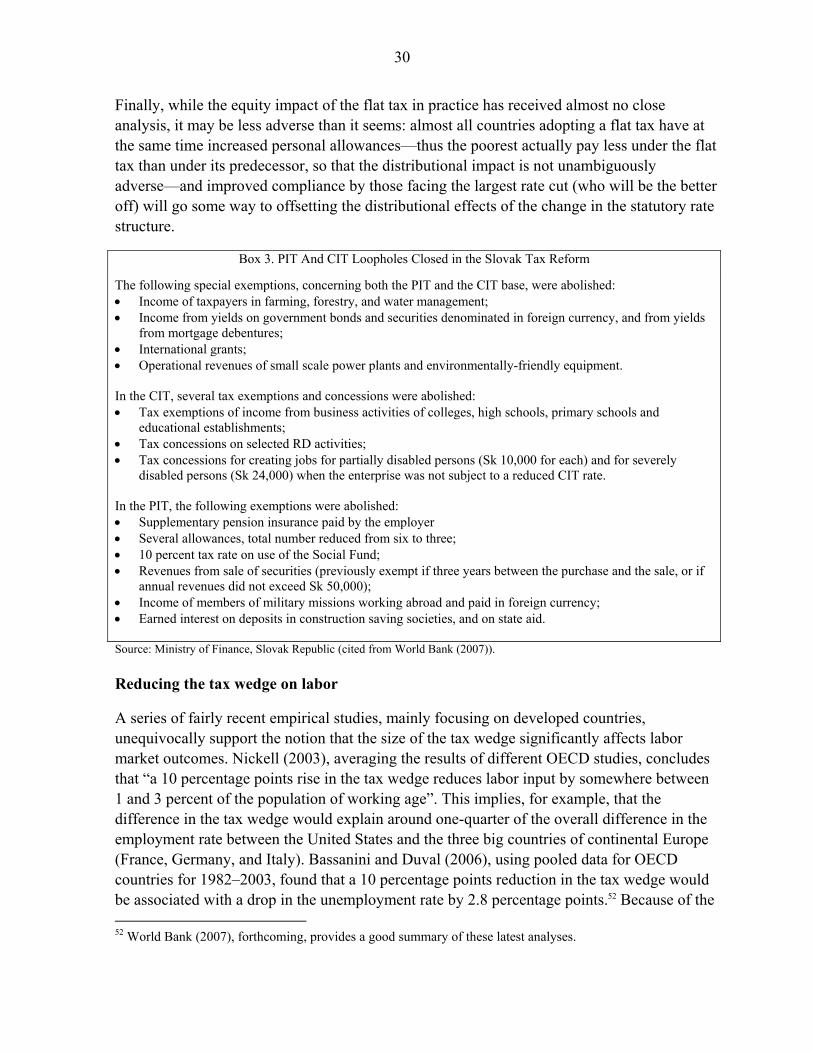

Box 1. FDI and Economic Growth in Ireland: What Role did the Tax System Play?

Average real GDP growth in Ireland was 2.4 percent between 1980 and 1985, but rose to 10 percent between 1995–2000. Current growth rates of roughly 5 percent are still amongst the highest in industrial countries (IMF Article IV, 2006). Unemployment in 2005 was 4.3 percent compared to 16 percent in 1993, and migration outflows reversed themselves in the 1990s. Currently, Irish GDP per capita estimated at US$58,000 per capita31 is the second highest in the EU (after Luxembourg), and the fourth highest in the world. How did a country, once described by The Economist as “poorest of the rich,”32 transform itself and at so rapidly a pace? And what was the role of Irish tax system in this transformation?

Honohan and Walsh (2002) argue that the Irish “miracle” should be viewed as a “delayed” or “deferred…process of bringing more of the population into a modern sector that was already close to the production frontier a quarter of a century ago.” The relevant question according to them is why it took so long for the country to catch up with the rest of the Europe. Claiming that the supply side and institutional preconditions necessary for convergence were already present in the 1970s, they argue that growth was derailed for more than a decade by a combination of various factors, including the oil crises of 1973 and 1979, a lax fiscal policy environment that eroded the competitiveness of Irish labor, and high global interest rates and weak foreign demand in the early 1980s. In a similar vein, Fortin (2002) distinguishes between ‘a long-term productivity boom dating back to the 1950s and 1960s, and a short-term output and employment boom’ starting in the early 1990s. The long-term productivity boom was driven by a shift of economic activity from the primary to the secondary and tertiary sectors—in 1960, approximately 40 percent of the Irish labor was employed in the primary sector compared to approximately 9 percent in 2000 (Fortin, 2002). Other underlying factors included the emergence of a highly skilled labor force due to the introduction of free secondary and low cost higher education in 1966, and an outward looking commercial and industrial policy Ireland joined the EEC in 1973, the Single European Market in 1993, and eventually the EMU in 1999. It also moved away from a protectionist industrial policy toward a regime that was extremely FDI friendly (for instance, through the relaxation of incentives to locate in peripheral regions the ending of restrictions on MNCs to remit profits abroad). In 1956, 100 percent remission known as export profit tax relief (see Honohan and Walsh, 2002) was applied to profits from (mainly manufacturing) exports. This was essentially a zero tax rate applied to profits from export sales. However, it was deemed incompatible with Ireland’s obligations under the Treaty of Rome, and in 1981 was replaced by a 10 percent preferential corporate tax rate applied to profits from the manufacturing industry and internationally-traded services (later extended to certain financial services and raised to 12.5 percent in 2003). The remainder of the corporate sector was, however, taxed at extremely high rates—in 1991 the “standard” rate was 40 percent. As part of an effort to harmonize it with the tax rate on manufacturing, it was gradually reduced to 12.5 percent in 2003. What were the factors that contributed to its economic turnaround in the early 1990s? And what was the contribution, if any, of the low tax on manufacturing? Various studies decline to pinpoint any single factor that caused the acceleration of growth, employment, and FDI (Walsh, 2000, Walsh and Honohan, 2002, Fortin, 2002). Instead, they point to significant improvements in the external trade environment with strong output and income growth in the United States, United Kingdom, and EU after 1993, leading to strong export growth. Exports were also boosted by decline of unit labor costs in manufacturing relative to its trading partners, driven, in part, by the 10 percent devaluation of the exchange rate in 1993, as well as by a long period of wage moderation and peaceful industrial relations starting in 1986. Macroeconomic stability on the domestic front, particularly successful fiscal consolidation after 1987, eventually facilitated a reduction in domestic labor and corporate tax burdens. On the supply side, the expansion in demand was accommodated by the decline in unemployment levels, a sharp increase in the participation of women in the labor force, and a large flow of immigrants into Ireland.

31 2007 estimate. Source: WEO.

32 “Poorest of the Rich: A Survey” The Economist, Jan 15, 1988, Vol 306, No. 7533.

21

Box 1. FDI and Economic Growth in Ireland: What Role did the Tax System Play? (concluded) There was also a substantial surge in FDI worldwide in the 1990s which Walsh (2001) argues Ireland was uniquely well placed to receive, particularly from the United States. This was by virtue of its close linguistic and cultural ties with the United States, an abundant supply of English speaking low cost and highly skilled labor, a modern physical infrastructure on account of large amounts of EU state aid, a stable fiscal and policy environment, and integration into the EU single market which made it a convenient platform for U.S. MNCs wishing to export to the EU. Consequently, net FDI in Ireland which had earlier averaged US$100 million annually between 1986–1990 was ten times larger—US$1.1 billion a year—between 1991–1997 (Fortin, 2000). Fortin (2002),Walsh (2000) and Honohan and Walsh (2002) all emphasize that there were no changes to the tax regime that could be regarded as a trigger for the explosion of FDI into Ireland or the employment boom. The extremely low tax rate on manufacturing profits had been in place since the 1950s. Furthermore, there had actually been an increase in the tax rate in 1981, as described above, followed by a further rise to 12.5 percent in 2003. Nevertheless, the generosity of the Irish tax system—it has the lowest effective and statutory rate of CIT applicable to MNCs among OECD countries—cannot be overlooked. While Walsh and Fortin argue that low tax rates were only one of the many factors that drew U.S. FDI to Ireland, Romalis (2007) provides evidence on Ireland to suggest that low taxes on capital in combination with the substantial decline in trade costs and the dismantling of barriers to trade in the 1990s were indeed a possible trigger for the economic growth and FDI inflow.

Corporate tax systems: experiments with fundamental restructuring

The integration of corporate and PIT systems was widely discussed in the 1980s and 1990s, particularly in OECD countries, with the “benchmark” being full imputation,33 and with (varying) integration systems being a hallmark of many European tax systems. Among others, Australia, Finland, Germany, New Zealand, and the United Kingdom introduced full imputation systems. The basic rationale was that integration relief provided to domestic shareholders can be expected to lower the cost of capital, thus spurring investment, and, at the same time, removing some distortions to the choice of corporate financing as compared to classical systems. However, while some countries have maintained these systems and even developed them further (Australia and New Zealand), others abandoned them and introduced simpler systems in their place (e.g., Finland, Germany, Italy, Portugal, and the United Kingdom) for a variety of reasons: administrative problems associated with the administration of full imputation systems; because of the small open economy context,34 and for some European countries because of the particular EU legal environment.35 It is interesting 33 With full credit given to individual recipients of dividends for the underlying corporate tax paid on those dividends, as opposed to a “classical” system under which dividends paid out from after tax corporate profits, are fully liable to PIT (“double taxation” of dividends).

34 Operating in small open economies, multinationals rely on capital raised in international capital markets with the cost of capital exogenously determined, and thus independent from the degree of integration of domestic PIT and CIT systems (Owens, 2006).

35 The European Court of Justice has ruled that dividends received from foreign countries must be taxed in the same way as dividends received from domestic companies, i.e., if imputation credits are provided to shareholders, they must be provided for both domestic and foreign-source dividend income.

22

to note that at roughly the same time the United States moved toward integration with its 2003 reform, many European countries moved in the opposite direction toward classical tax treatment (Owens, 2006). In a wider sense, this trend away from integration could also be seen as a further distancing from the pure principle of global income taxation.

Prominent examples of more recent experiments with fundamental corporate tax restructuring includes Estonia’s repeal of the standard corporate tax in favor of taxing only dividend distributions.36 In the Estonian model, retained earnings are subject to a zero corporate tax rate, while dividends are taxed at 25 percent (regarded as corporate tax paid). Dividends paid to nonresidents are furthermore subject to a withholding tax at a rate that depends on whether a double taxation agreement is in place or not. While, in principle, attractive in its simplicity and efficiency by treating debt and equity financing broadly uniformly, the model is not altogether without problems: (1) dependent on the initial system, it could well involve a significant revenue loss; (2) it is not fully EU compatible and Estonia has been asked by the EC to change the system as of 2009; (3) it may create new distortions, including locking-in effects for corporate profits; and (4) it raises the issue whether foreign parent companies can credit the tax under preexisting double taxation agreements. Belgium has adopted an “allowance for corporate equity” (similar to what Croatia did in 1994, but later abandoned), in an attempt both to eliminate arbitrary discrimination between debt and equity finance, and move the CIT closer to a pure profit tax. Finally, cash-flow tax systems of corporate taxation, which would involve METRs of zero on new investment and tax only excess profits of enterprises, has frequently been discussed in the literature, and is currently being considered for implementation in Bahrain and East Timor (in January 2008).

A different policy line, but one which could be interpreted as having a broadly similar ultimate objective, has been adopted by Denmark and Germany,37 and aims basically at curtailing interest deductibility of corporations (so, instead of treating dividends like interest as in Belgium, this strategy would—in the extreme—treat interest like dividends).38 In the case of Denmark, a central objective was to prevent future use of leveraged acquisitions financing structures. Combined with a rate reduction from 28 percent to 25 percent, the reform includes a tightening of interest deductibility, effective July 1, 2007, by two cumulative provisions: (1) net interest expenses exceeding DKK 20 million (Euro 2.66 million) would be deductible up to a cap equal to 6.5 percent of the tax value of Danish operating assets plus 20 percent of the value of foreign subsidiaries; and (2) the maximum interest deduction could not exceed 80 percent of earnings before income tax. The German model which aims at stimulating the use of equity capital would deny deductibility of interest

36 Moldova, while keeping the standard corporate tax system, has reduced the CIT rate to zero starting in 2008.

37 With a more limited reform adopted in Canada, see below.

38 This is essentially the “comprehensive business income tax” (CBIT), proposal made by the U.S. Treasury Department in a 1992 report according to which neither the incurred interest on debt nor any imputed return on equity may be deducted against the profit tax base.

23

in excess of 30 percent of income before consideration of interest earned and interest payable (and with exemptions for smaller enterprises and specific circumstances), but interest expenses denied can be carried forward.

The provisions discussed in Canada would, with a transition period to 2012, restrict deductibility of interest on debt related to investments in foreign affiliates (to prevent so- called “double dip structures”), since dividends payable by a subsidiary are in some cases eligible for a 100 percent dividends received deduction. At the same time, the corporate tax rate will be reduced to 18.5 percent by 2011.

The issue of interest deductibility has also attracted some attention in Central American countries, where a Working Group on Tax Coordination for Central America, under the auspices of CACU, is currently attempting to develop a regional standard for interest deductibility.

Dual income tax (DIT)

The idea of levying a flat uniform (relatively low) tax on capital income, separately from the progressive tax on labor income, originated in a formal sense with the Danish tax reform of the late 1980s39 40—quickly followed by similar reforms in Sweden (1991), Norway (1992), and Finland (1993), with the Norwegian and Finnish models coming closest to the strict conceptual framework of a DIT.41 This tax policy innovation broke decisively with the notion of the global income tax, which had dominated tax policy discussions and guided tax reforms during the previous some 30 years, and which, in turn, originated from the well-known Haig-Simons concept of comprehensive or global income of individuals (measured, for example, as consumption plus change in net wealth over a given period) as the appropriate measure of taxable capacity (Zee (2004)). Switching from a global tax to a DIT is seen by some as one indicator of the changing balance between equity and efficiency considerations, although, as already noted, revenue considerations also played a role.42

39 It is noteworthy that the original intention of the Danish reform was to stimulate private saving, including by providing disincentives to debt, by reducing the “tax value” (i.e., reduction in tax liability) for individuals from interest deductibility which prior to the reform was very high owing to the full interest deductibility for all debt, combined with very high marginal tax rates under the progressive PIT. Later DIT reforms emphasized the international mobility of capital income as their primary rationale.

40 Many countries had separate systems of often final withholding on capital income sources (interest and dividend), but mainly for reasons of administrative feasibility.

41 Overviews are provided in Sørensen (1998) and Cnossen (2000). Since the Nordic reforms, few countries have seriously considered introducing full-fledged DITs, but many countries have adopted reforms that build on the basic DIT concept.

42 Some observers (for example, Zee, 2004) interpret this as a fundamental change in the balance between the importance assigned to equity (in particular, horizontal equity, or the equal treatment of individuals with the same (global) income, whether from capital or labor income sources) and economic efficiency considerations, with the latter gaining traction because of increased tax competition and mobility of capital).

24

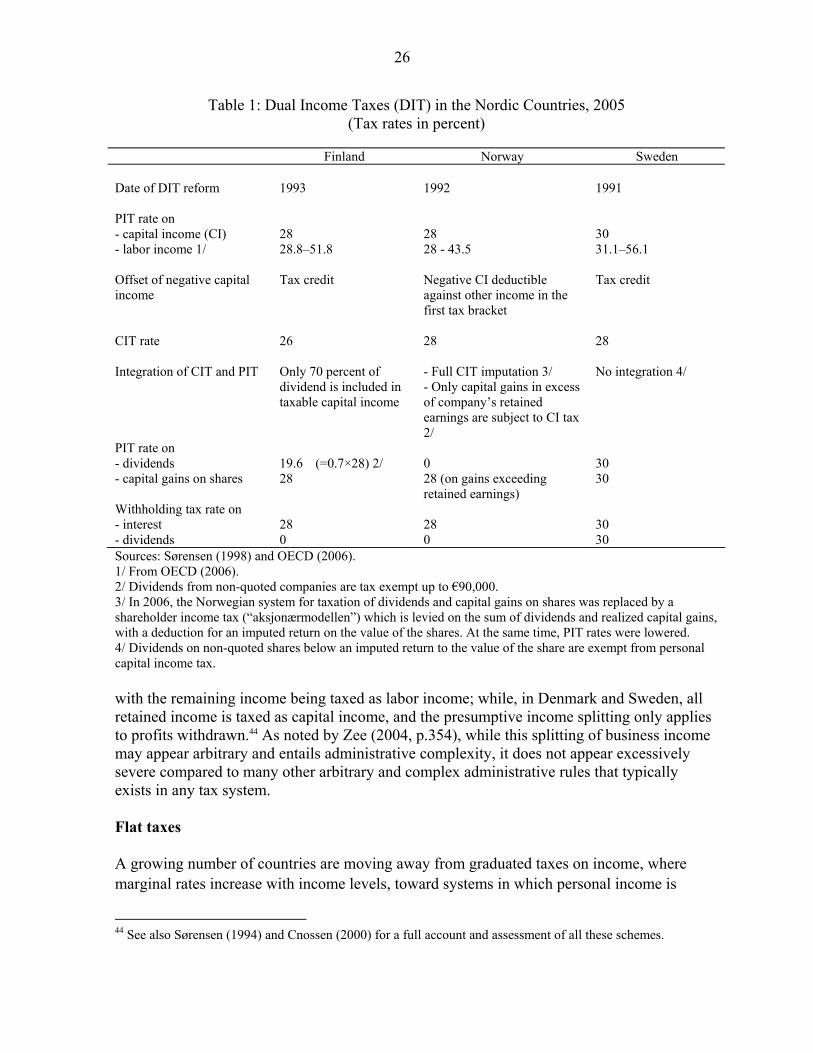

The DIT was (and is) considered to have several attractive features. First, by applying a flat rate to all capital income, tax arbitrage among capital income sources is prevented. Furthermore, because of the “flatness” of the capital income tax, it can, in many cases, conveniently be collected by final withholding. Second, with the global income tax coming under considerable pressure, the DIT was considered a reasonable compromise between several critical considerations: stimulating savings and investment in the face of increased capital mobility; preserving government revenue; and securing a reasonable degree of fairness in taxation. Finally, the tax can also claim some theoretical underpinning in optimal tax theory, as applied to small open economies (see Box 2). While specific practices differ across countries applying the DIT (the DITs in the Nordic countries are summarized in Table 1), its main characteristics are (Zee (2004)):

(1) capital income includes interest, dividends, capital gains, rents, royalties, and business profits;

(2) labor income includes wages and salaries (including imputed labor income of self-employed), pensions and social security benefits, perquisites, and royalties not classified as capital income;

(3) the rate of tax on capital income is uniform (to avoid tax arbitrage and to maintain neutrality) and moderate (to address capital mobility). Under a “pure” DIT, the rate would equal the lowest positive PIT rate; and

(4) the rates on labor income are progressive (for equity and revenue reasons) and

generally higher than the rate on capital income (on account of relatively low labor mobility), but not so high as to provide a strong incentive for the self-employed to disguise labor income as capital income.

The treatment of the self-employed has been considered the Achilles-heel of the DIT, because of the need to separate their income in return to capital and remuneration for labor services under a DIT. This cannot be done in any precise manner. In Finland and Norway, (until 2006),43 a presumptive rate of return on capital determines the share of capital income,

43 The system of mandatory income splitting worked reasonably well in Norway for the self-employed but not for so-called active owners of companies (owner-managers) who managed to avoid mandatory income splitting by inviting “passive” owners into the company. Starting in January 2006, the split model was replaced by additional taxation on distributed profit as ordinary income. Thus, partnerships will still be subject to 28 percent taxation upon all income irrespective of distribution, supplemented by 28 percent additional taxation on distributed profits. In order to compensate for the initial 28 percent taxation, only 72 percent of the distributed profit will be taxable. Furthermore, only the distributed profit exceeding a risk-free interest on the capital invested in the partnership will be taxable. The new regulations, called the “shielding method for partnerships,” will ensure the same level of taxation on both retained and distributed profit as in limited companies. The maximum marginal tax rate of distributed income will be 48.16 percent (0.28+0.72*0.28—see http://www.regjeringen.no/nb/dep/fin/tema/Norsk_okonomi/topics/The-corporate-tax-system-and-taxation-of-capital-income.html?id=418058). At the same time, the top marginal PIT rate has declined. Because these

(continued…)

25

Box 2. Taxes on Capital Income in an Open Economy

Two fundamental distinctions are necessary for understanding the design and impact of taxes on capital income, namely, source vs. residence-based taxes, and taxes on the normal return to capital vs. taxes on rents (see Sørensen, 2006). According to the source principle, the return to capital is taxed only in the country where the investment took place, whereas under the residence principle, returns are taxed in the country of residence of the investor, irrespective of where the investment took place. Typically, corporate income has been taxed under a source-based principle with general agreement that the source country has the first right to tax. Thus, most countries tax income generated only within their own borders, important exceptions being the United Kingdom, United States, and Japan, key capital exporting countries, which operate residence-based (or worldwide) tax systems and grant tax credits for foreign tax paid against domestic tax liabilities. The residence principle, on the other hand, is applied to personal income or wealth tax. However, government authorities often find it extremely hard to monitor and assess the returns on capital income invested abroad, so that, as if applied under a source principle, PIT usually end up falling on capital income invested at home only. The return to capital comprises the normal return to capital as well as rents. For example, the normal rate of return on debt is the market rate of interest (including a risk premium that varies according to the risk characteristics of the debt instrument). Rents are “pure profits” that are earned in excess of the normal market rate of return. In closed economies, the volume of domestic saving and investment will fall with a tax on the normal return to capital. A tax on rents, on the other hand, will be nondistortionary. In contrast, in small open economies, domestic savings and investment are uncoupled from each other. With the domestic interest rate being determined in the world capital market, a source-based tax on capital will not affect the rate of return to domestic savers. However, users of capital are price-takers so that domestic investment falls. Furthermore, if the tax falls on mobile rents, capital outflow occurs as the business activity generating the rent shifts abroad. For firms to break even under the tax, either output prices must rise or other costs must fall. With output prices fixed by competition from imports, the tax will cause the market clearing wage-rate to fall. In other words, in the absence of any location-specific rents, and in the face of perfectly mobile capital, the burden of a source-based tax on capital in an open economy falls entirely on labor (or other relatively immobile domestic factors). In the process, the productivity of labor also falls (on account of the lower capital intensity of production). In contrast, while a direct tax on labor income would also reduce the net wage rate, it would not distort the marginal return to capital invested at home vs. abroad. Neither would it cause a drop in productivity on account of the reduced capital intensity of production. Hence, a labor income tax dominates a source-based tax on capital income (Gordon and Hines (2002), and Sørensen (2006), building on the results of Diamond and Mirrlees (1971)). So, why do source-based capital income taxes survive? Sørensen (2006) points to a number of factors. First, location-specific rents may exist in the form of natural resources, access to market, infrastructure, qualified labor, an agglomeration of economic activities with strong spillover effects, and so on, which allow firms to earn above normal rates of return and governments to impose source-based taxes on rents without causing a capital flight. An additional incentive for governments to do so is if these rents coexist with (some degree of) foreign ownership of the domestic capital stock, which allows some portion of the tax burden to be shifted onto foreigners (Huizinga and Nielsen, 1997). Consistent with this argument, Huizinga and Nicodème (2003) find evidence of a positive relationship between average effective CIT rates and the foreign ownership of companies in Europe. Secondly, capital may not be perfectly and instantaneously mobile. There may be substantial costs to adjusting physical capital across borders, so that the domestic capital stock responds only gradually to source-based capital taxes. Financial instruments (particularly equity) issued in different countries may not be perfect substitutes and with investors wanting to hold diversified portfolios, governments may enjoy a degree of market power over the price of equity. Finally, taxes on capital income, particularly corporation taxes, may serve as a backstop to the PIT such that taxpayers do not have the incentive to shift labor and capital income into a corporate sector free of tax.

adjustments significantly reduce the margin between the top marginal tax rate on labor income and capital income, the incentives to convert labor income to capital income are also reduced (OECD, 2006 www.oecd.org/dataoecd/43/21/36346567.pdf).

26

Table 1: Dual Income Taxes (DIT) in the Nordic Countries, 2005 (Tax rates in percent)

Finland Norway Sweden

Date of DIT reform

1993

1992

1991

PIT rate on - capital income (CI) - labor income 1/

28 28.8–51.8

28 28 - 43.5

30 31.1–56.1

Offset of negative capital income

Tax credit

Negative CI deductible against other income in the first tax bracket

Tax credit

CIT rate

26

28

28

Integration of CIT and PIT

Only 70 percent of dividend is included in taxable capital income

- Full CIT imputation 3/ - Only capital gains in excess of company’s retained earnings are subject to CI tax 2/

No integration 4/

PIT rate on - dividends - capital gains on shares

19.6 (=0.7×28) 2/ 28

0 28 (on gains exceeding retained earnings)

30 30

Withholding tax rate on - interest - dividends

28 0

28 0

30 30

Sources: Sørensen (1998) and OECD (2006). 1/ From OECD (2006). 2/ Dividends from non-quoted companies are tax exempt up to €90,000. 3/ In 2006, the Norwegian system for taxation of dividends and capital gains on shares was replaced by a shareholder income tax (“aksjonærmodellen”) which is levied on the sum of dividends and realized capital gains, with a deduction for an imputed return on the value of the shares. At the same time, PIT rates were lowered. 4/ Dividends on non-quoted shares below an imputed return to the value of the share are exempt from personal capital income tax. with the remaining income being taxed as labor income; while, in Denmark and Sweden, all retained income is taxed as capital income, and the presumptive income splitting only applies to profits withdrawn.44 As noted by Zee (2004, p.354), while this splitting of business income may appear arbitrary and entails administrative complexity, it does not appear excessively severe compared to many other arbitrary and complex administrative rules that typically exists in any tax system. Flat taxes A growing number of countries are moving away from graduated taxes on income, where marginal rates increase with income levels, toward systems in which personal income is

44 See also Sørensen (1994) and Cnossen (2000) for a full account and assessment of all these schemes.

27