Embed Size (px)

Citation preview

Tax Obligations of LGUs, Foundations

and NGOs

Duties & Obligations To register

To withhold

To remit the taxes withheld and to file the applicable Withholding Tax Returns

To submit Annual Information Returns

To issue Withholding Tax Certificate

To register with Revenue District Office having jurisdiction over the head office/principal office or branch or facility before payment of any tax due/ before or upon filing of any applicable tax return, statement or declaration as required by the Code, as amended.

- Sec. 236 of NIRC; Revenue Regulations No. 11- 2008

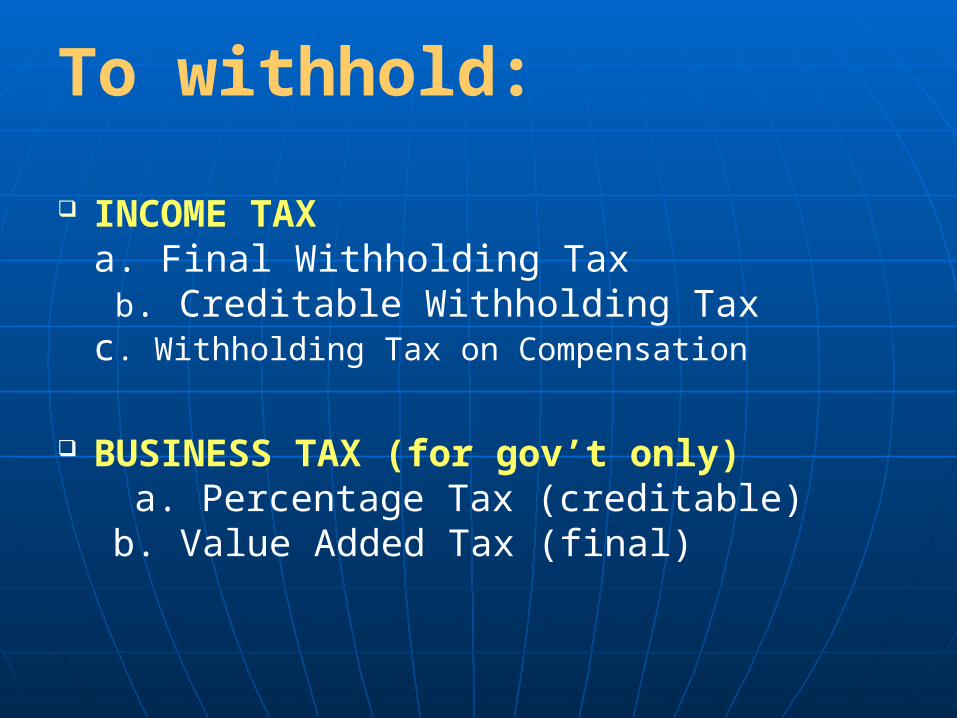

To withhold:

INCOME TAXa. Final Withholding Tax

b. Creditable Withholding Tax c. Withholding Tax on Compensation

BUSINESS TAX (for gov’t only) a. Percentage Tax (creditable)

b. Value Added Tax (final)

WITHHOLDING TAXWITHHOLDING TAX

A manner of collecting a kind A manner of collecting a kind of tax which is an advance of tax which is an advance payment of the tax due.payment of the tax due.

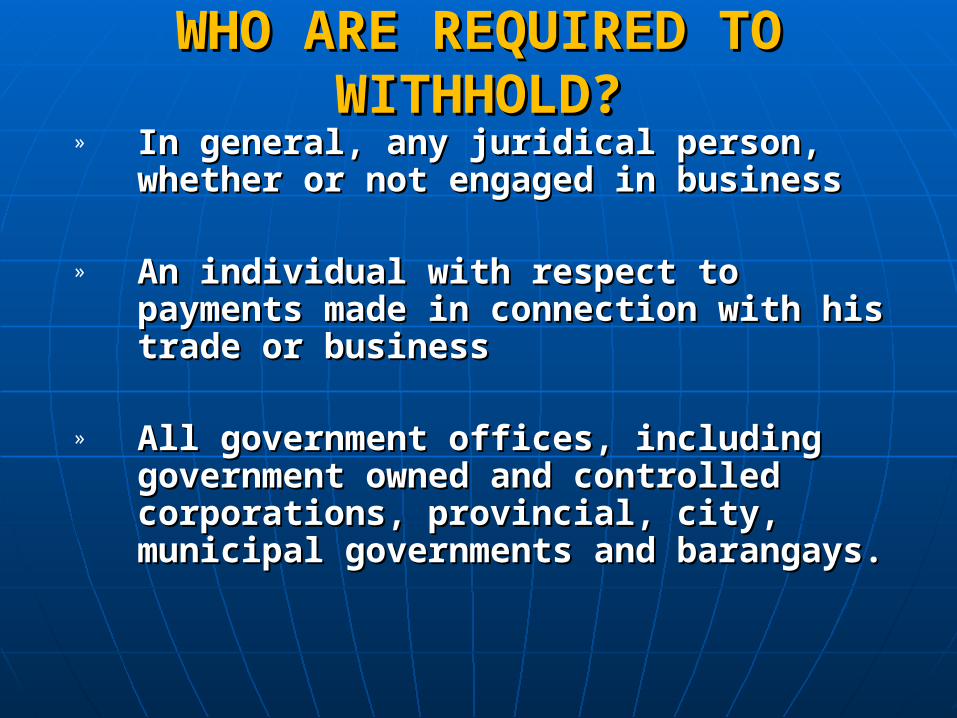

WHO ARE REQUIRED TO WHO ARE REQUIRED TO WITHHOLD?WITHHOLD?

» In general, any juridical person, In general, any juridical person, whether or not engaged in businesswhether or not engaged in business

» An individual with respect to payments An individual with respect to payments made in connection with his trade or made in connection with his trade or business business

» All government offices, including All government offices, including government owned and controlled government owned and controlled corporations, provincial, city, municipal corporations, provincial, city, municipal governments and barangays.governments and barangays.

REVENUE MEMORANDUM ORDER NO. 8-REVENUE MEMORANDUM ORDER NO. 8-2003 dated March 3, 20032003 dated March 3, 2003

Identified the Government officials designated as withholding agents personally responsible for the correct withholding of tax and its timely remittances.

RESPONSIBILITY OF GOVERNMENT RESPONSIBILITY OF GOVERNMENT OFFICIALSOFFICIALS

They are charged with the DUTY to correctly withhold taxes on compensation, expanded and final withholding taxes as well as government money payments to persons registered as NVAT and VAT taxpayers and the timely remittance of taxes withheld.

GOVERNMENT OFFICEGOVERNMENT OFFICE RESPONSIBLE OFFICIALRESPONSIBLE OFFICIAL

1.) Local Government Units1.) Local Government Units

a. Provincesa. Provinces

b. Citiesb. Cities

c. Municipalitiesc. Municipalities

d. Barangaysd. Barangays

Governor, Provincial Treasurer, Governor, Provincial Treasurer,

Provincial Accountant Provincial Accountant

Mayor, City Treasurer, City AccountantMayor, City Treasurer, City Accountant

Mayor, Municipal Treasurer, Municipal Mayor, Municipal Treasurer, Municipal

AccountantAccountant

Barangay Captain and Barangay Barangay Captain and Barangay

TreasurerTreasurer

2.) National Government Agencies2.) National Government Agencies Heads of offices – officials, holding the Heads of offices – officials, holding the

highest positionshighest positions

Chief AccountantsChief Accountants

Other persons holding similar positionsOther persons holding similar positions

in departments, bureaus, agencies,in departments, bureaus, agencies,

and instrumentalities officially and instrumentalities officially

designated as such by the head designated as such by the head

officeoffice

3.) Government Owned or Controlled 3.) Government Owned or Controlled

Corporations (GOCC)Corporations (GOCC)Head of offices (official holding the Head of offices (official holding the

highest positions)highest positions)

Chief AccountantsChief Accountants

Other persons holding similar positionsOther persons holding similar positions

officially designated as such by the officially designated as such by the

head officehead office

GOVERNMENT OFFICEGOVERNMENT OFFICE RESPONSIBLE OFFICIALRESPONSIBLE OFFICIAL

4.) Other Government Offices 4.) Other Government Offices

Head of offices (official holding the Head of offices (official holding the

highest positions)highest positions)

Chief AccountantsChief Accountants

Other persons holding similar positionsOther persons holding similar positions

officially designated as such by the officially designated as such by the

head officehead office

5.) Government Offices with 5.) Government Offices with Decentralized Accounting System Decentralized Accounting System and/or Branches/ Regional Offices/ and/or Branches/ Regional Offices/ District Offices registered with their District Offices registered with their respective RDO’srespective RDO’s

Head of such Offices/Regional/District Head of such Offices/Regional/District

Offices (persons holding the highest Offices (persons holding the highest

positions)positions)

Chief AccountantsChief Accountants

Other persons holding similar positions Other persons holding similar positions designated such as:designated such as:

BIR Regional Offices – Regional BIR Regional Offices – Regional DirectorDirector

BIR Chief, Finance DivisionBIR Chief, Finance Division

DECS – Regional DirectorDECS – Regional Director

DECS – Chief, Budget & Finance DECS – Chief, Budget & Finance Division Division

All these officials shall be EQUALLY LIABLE to the penalties as prescribed under the Tax Code.

RESPONSIBILITY AND LIABILITY of these officials under this Memorandum SHALL NOT BE DELEGATED TO SUBORDINATE OFFICIALS OR EMPLOYEES.

A.A. Fails or causes the failure to deduct and Fails or causes the failure to deduct and withhold any internal revenue tax under withhold any internal revenue tax under any of the withholding tax laws and any of the withholding tax laws and implementing regulations.implementing regulations.

B.B. Fails or causes the failure to remit the Fails or causes the failure to remit the taxes deducted and withheld within the taxes deducted and withheld within the time prescribed by law.time prescribed by law.

C.C. Fails or causes the failure to file a return Fails or causes the failure to file a return or statement within the time prescribed, or statement within the time prescribed, or render or furnish a false or fraudulent or render or furnish a false or fraudulent return or statement required under return or statement required under withholding tax laws & regulations.withholding tax laws & regulations.

PUNISHABLE ACTS OR OMMISSIONS

EVERY OFFICER OR EMPLOYEE OF THE EVERY OFFICER OR EMPLOYEE OF THE GOVERNMENT OF THE REPUBLIC OF GOVERNMENT OF THE REPUBLIC OF THE PHILIPPINES OR ANY OF ITS THE PHILIPPINES OR ANY OF ITS AGENCIES AND INSTRUMENTALITIES, AGENCIES AND INSTRUMENTALITIES, ITS POLITICAL SUBDIVISIONS, AS ITS POLITICAL SUBDIVISIONS, AS WELL AS GOCCS CHARGED WITH THE WELL AS GOCCS CHARGED WITH THE DUTY TO DEDUCT AND WITHHOLD DUTY TO DEDUCT AND WITHHOLD ANY INTERNAL REVENUE TAX AND TO ANY INTERNAL REVENUE TAX AND TO REMIT THE SAME IN ACCORDANCE REMIT THE SAME IN ACCORDANCE WITH THESE REGULATIONS SHALL, WITH THESE REGULATIONS SHALL, UPON CONVICTION FOR EACH ACT OR UPON CONVICTION FOR EACH ACT OR OMISSION, HEREIN SPECIFIED, BE OMISSION, HEREIN SPECIFIED, BE FINED IN A SUM OF NOT LESS THAN FINED IN A SUM OF NOT LESS THAN P5000.00 BUT NOT MORE THAN P5000.00 BUT NOT MORE THAN P50,000.00 OR IMPRISONED FOR A P50,000.00 OR IMPRISONED FOR A TERM OF NOT LESS THAN 6 MONTHS TERM OF NOT LESS THAN 6 MONTHS AND ONE DAY BUT NOT MORE THAN AND ONE DAY BUT NOT MORE THAN TWO YEARS, OR BOTH.TWO YEARS, OR BOTH. (Section 272 (Section 272 of NIRC)of NIRC)

WHEN TO WITHHOLD?WHEN TO WITHHOLD? The obligation of the payor to The obligation of the payor to

deduct and withhold the tax deduct and withhold the tax arises at the time an income arises at the time an income payment is paid or payable, payment is paid or payable, whichever comes first. The term whichever comes first. The term “payable” means the date the “payable” means the date the obligation becomes due, obligation becomes due, demandable or legally demandable or legally enforceable . enforceable .

WHO ARE EXEMPTED FROM WHO ARE EXEMPTED FROM WITHHOLDING?WITHHOLDING?

» National government and its National government and its instrumentalities, including instrumentalities, including provincial, city or municipal provincial, city or municipal governmentsgovernments

» Persons enjoying exemption Persons enjoying exemption from payment of income taxes from payment of income taxes pursuant to the provisions of pursuant to the provisions of any law, general or specialany law, general or special

To remit the taxes withheld & to file withholding tax returns

The taxes withheld shall be remitted and the return shall be filed in triplicate copies on or before the 10th day of the month following the month in which withholding was made except taxes for December which shall be filed/paid on or before January 15 of the succeeding year.

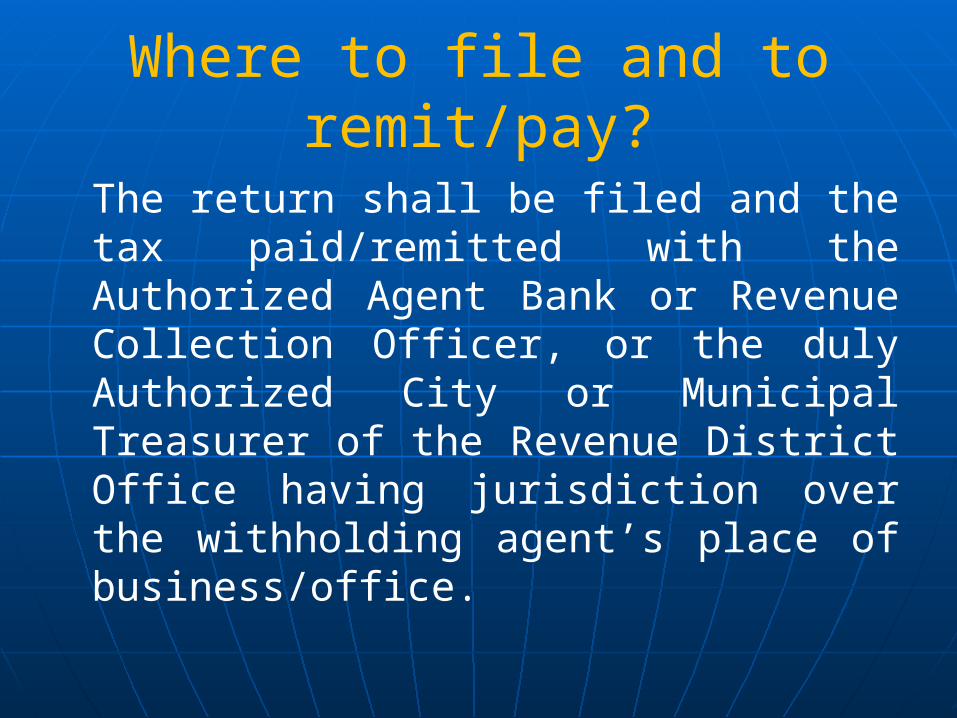

Where to file and to remit/pay?

The return shall be filed and the tax paid/remitted with the Authorized Agent Bank or Revenue Collection Officer, or the duly Authorized City or Municipal Treasurer of the Revenue District Office having jurisdiction over the withholding agent’s place of business/office.

To submit Annual Information Returns

BIR Form No. 1604 CF– Annual Information Return of Income Taxes Withheld on Compensation & Final Withholding Taxes - shall be filed in triplicate to the Revenue District Office where the payor/employer is registered as Withholding Agent on or before January 31 of the following year, together with the alphabetical list of employees.

BIR Form No. 1604E – Annual Information Return of Creditable Income Taxes Withheld

- shall be filed in triplicate together with the Annual Alphalist of Payees to Revenue District Office where the payor is registered as Withholding Agent on or before March 1 of the following year

Revenue Regulations No. 2-2006 Revenue Regulations No. 2-2006 dated December 1, 2005dated December 1, 2005

MONTHLY ALPHALIST OF PAYEESMONTHLY ALPHALIST OF PAYEES Is a consolidated alphalist of income Is a consolidated alphalist of income

earners from whom taxes have been earners from whom taxes have been withheld for a given period. This is withheld for a given period. This is required to be submitted as an required to be submitted as an attachment to the monthly attachment to the monthly withholding tax returns (1601e, withholding tax returns (1601e, 1601f, 1600) 1601f, 1600)

Not more ten (10) payees- hard copyNot more ten (10) payees- hard copy More than ten (10) payees-electronic More than ten (10) payees-electronic

copycopy

To issue Withholding Tax Certificate BIR Form No. 2316 – Certificate of Compensation Payment/Tax

Withheld (with or without taxes withheld)- shall be furnished to the employee in triplicate on or

before January 31 of the succeeding calendar year or if employment is terminated before the close of such calendar year, on the day on which the last payment of compensation is made.

BIR Form No 2307 – Certificate of Creditable Tax Withheld at Source- Creditable Income Tax shall be issued in quadruplicate

on or before 20th day following the close of the taxable quarter or upon request/demand of the payee.

- Creditable Percentage Tax shall be issued in quadruplicate on or before the 5th of the following month. (RR No. 12- 2001)

BIR Form No. 2306 – Certificate of Final Tax Withheld at Source- shall be issued in quadruplicate within ten (10) days

following the month the withholding was made.

THANK YOU!!!

Telephone Nos. 545 -9910 /545 -3573Telephone Nos. 545 -9910 /545 -3573

BIR WEBSITE:BIR WEBSITE:

www.bir.gov.phwww.bir.gov.ph

REVENUE DISTRICT OFFICE No. 056REVENUE DISTRICT OFFICE No. 056Calamba CityCalamba City