Embed Size (px)

Citation preview

TAX LAW

Academic Year 2006 / 2007

Tax Law LIUC - Academic Year 2006/2007

2

• Direct Taxes are generally imposed on:

– profits and capital of businesses;– income and net worth of individuals.

• Indirect taxes are levied on consumptions

Income taxesGeneral issues

Tax Law LIUC - Academic Year 2006/2007

3

Income taxesGeneral issues

SOURCE JURISDICTION

• Income may be taxable under the tax laws of a country because of a link between that country and the activities which generated the income.

Tax Law LIUC - Academic Year 2006/2007

4

Income taxesGeneral issues

RESIDENCE JURISDICTION

• A country may also impose a tax because of a nexus between the country and the person earning the income. Person subject to the residence jurisdiction of a country generally are taxable on their worldwide income, without reference to the source of the income.

Tax Law LIUC - Academic Year 2006/2007

5

Income taxesTaxable income

The determination of the items to be included in the tax base is a central question in all income tax systems:

• Global system

• Schedular system

Tax Law LIUC - Academic Year 2006/2007

6

Income taxesTaxable income

• Global system typically has a single, comprehensive concept of income and a single rate structure.

• Schedular system focuses on particular classes or categories of receipts and often has different rates and substantive and procedural rules for each class.

Tax Law LIUC - Academic Year 2006/2007

7

Income taxesTaxable income

• Global system may have schedular elements (eg. limitation on deduction incurred in different categories of activities).

• Schedular system may have a global character (eg. Income and losses are combined in the final income calculation).

Tax Law LIUC - Academic Year 2006/2007

8

Income taxesTaxable income

The global system of many countries have become partially schedularised by the use of withholding taxes on certain types of income (eg. dividends and interest) and lower tax rates on capital income

Most frequent categories of income– Business income– Income from professional services– Income from employment – Income from immovable properties– Income from capital– Other income

Tax Law LIUC - Academic Year 2006/2007

9

Income taxesTaxable income

The concept of taxable income effectively defines the income tax base of person for a tax period, usually defined as gross income less total deductions allowed.

• Gross income is the total amount “derived” by a person during the tax period. It does not include amounts which are exempt from tax.

• Total deduction corresponds to the total of expenses incurred by a person during the tax period.

Tax Law LIUC - Academic Year 2006/2007

10

Income taxesTaxable income

• Deductions for expenses which have been incurred in deriving amounts included in gross income.

• Deductions for capital allowances (eg. Depreciation and amortisation provisions).

• Tax relief on personal expenses.

Tax Law LIUC - Academic Year 2006/2007

11

Income taxesTaxable income

In determining the correct amount of gross income as well as of deductions, a tax system must specify the basic structural rules which are aimed at:

• identifying; and

• evaluating

the correct amount of gross income and of deductions.

Tax Law LIUC - Academic Year 2006/2007

12

Income taxesTaxable income

The identification a certain item of income, or an expense incurred by the taxpayer, gives rise to the need for apportionment rules. Where different rules apply to different categories of income, it is necessary to apportion the income/expense between the different categories of income.

Evaluation issues are mainly related to situations where the income is derived as a benefit in kind (eg. an employee fringe benefit)

Tax Law LIUC - Academic Year 2006/2007

13

Income taxesTax relief on personal expenses

• Income tax system is usually indifferent to the manner in which a taxpayer chooses to spend money (other than money spent to drive taxable income). As a consequence a taxpayer’s taxable income should be the same regardless of whether the taxpayer saves the income derived, consumes it, or gives it away.

• However, a number of countries do use income tax system to provide relief for certain personal expenses. This is the case, for example, of:

• life insurance premiums;• charitable contributions;• interest expenses;and • medical expenses.

Tax Law LIUC - Academic Year 2006/2007

14

Income taxesTax relief on personal expenses

• The aim of such relief may be of a different nature:

– encouraging the development of charitable organisation to fulfil various functions that are considered socially important;

– granting a tax relief to those persons who need medical treatment;

– provide for a tax incentive to those who makes relevant personal investment, such as the acquisition of private dwelling.

Tax Law LIUC - Academic Year 2006/2007

15

Income taxesTax relief on personal expenses

• Tax relief may be granted either through:

– tax deduction (i.e. subtraction from the taxable income); or

– tax offset (i.e. deduction on the taxes due).

In the first case the tax relief increases with the taxpayer’s taxable income and, hence, marginal rates.

In case of tax offset, once established the level of relief, it will the same for taxpayers in all level of taxable income and marginal rates.

Tax Law LIUC - Academic Year 2006/2007

16

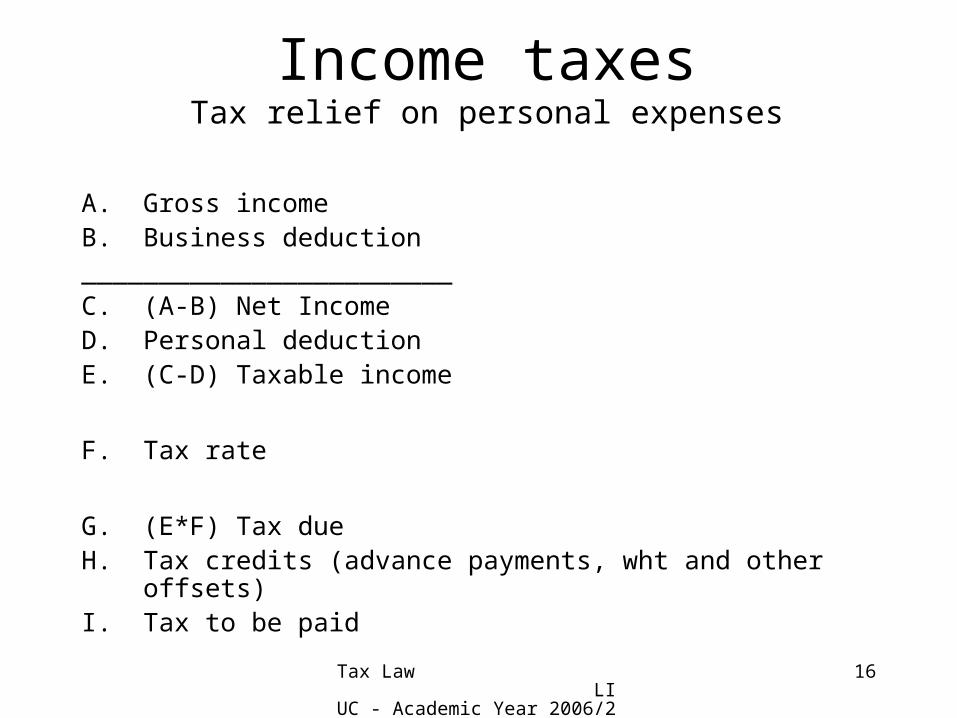

Income taxesTax relief on personal expenses

A. Gross incomeB. Business deduction________________________C. (A-B) Net IncomeD. Personal deductionE. (C-D) Taxable income

F. Tax rate

G. (E*F) Tax dueH. Tax credits (advance payments, wht and other offsets)I. Tax to be paid

Tax Law LIUC - Academic Year 2006/2007

17

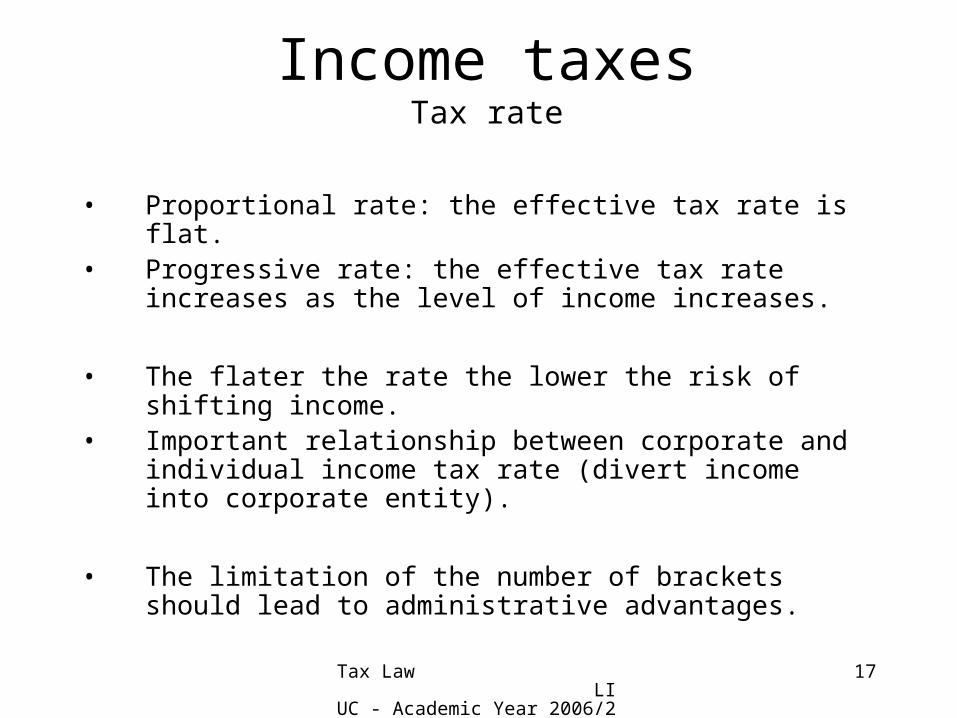

Income taxesTax rate

• Proportional rate: the effective tax rate is flat.• Progressive rate: the effective tax rate increases as the level

of income increases.

• The flater the rate the lower the risk of shifting income.• Important relationship between corporate and individual

income tax rate (divert income into corporate entity).

• The limitation of the number of brackets should lead to administrative advantages.

Tax Law LIUC - Academic Year 2006/2007

18

Income taxesTiming issues

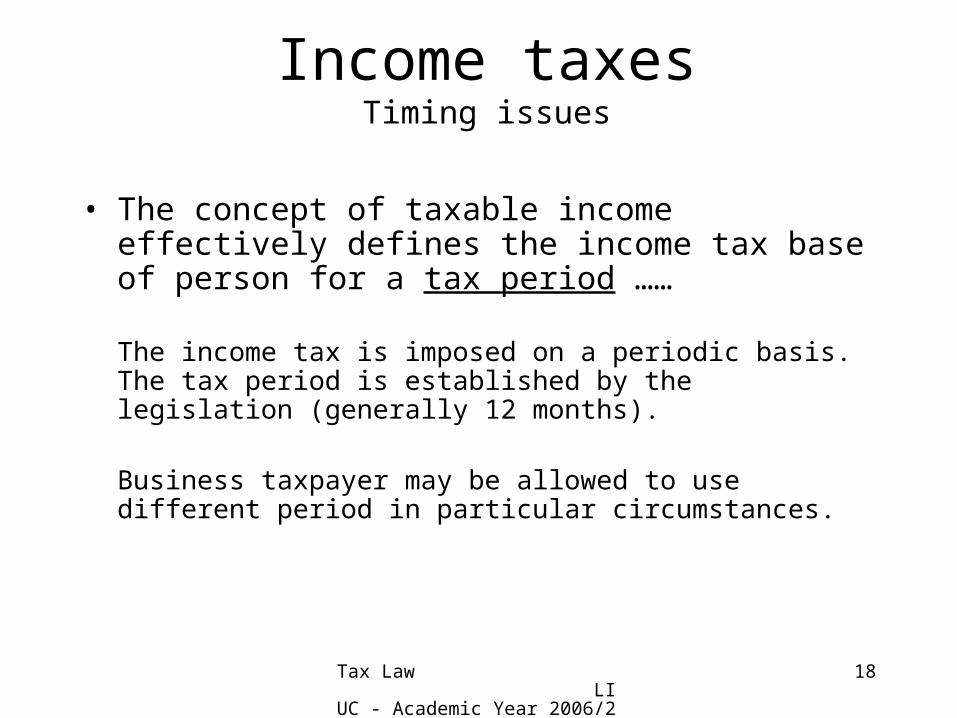

• The concept of taxable income effectively defines the income tax base of person for a tax period ……

The income tax is imposed on a periodic basis. The tax period is established by the legislation (generally 12 months).

Business taxpayer may be allowed to use different period in particular circumstances.

Tax Law LIUC - Academic Year 2006/2007

19

Income taxesTiming issues

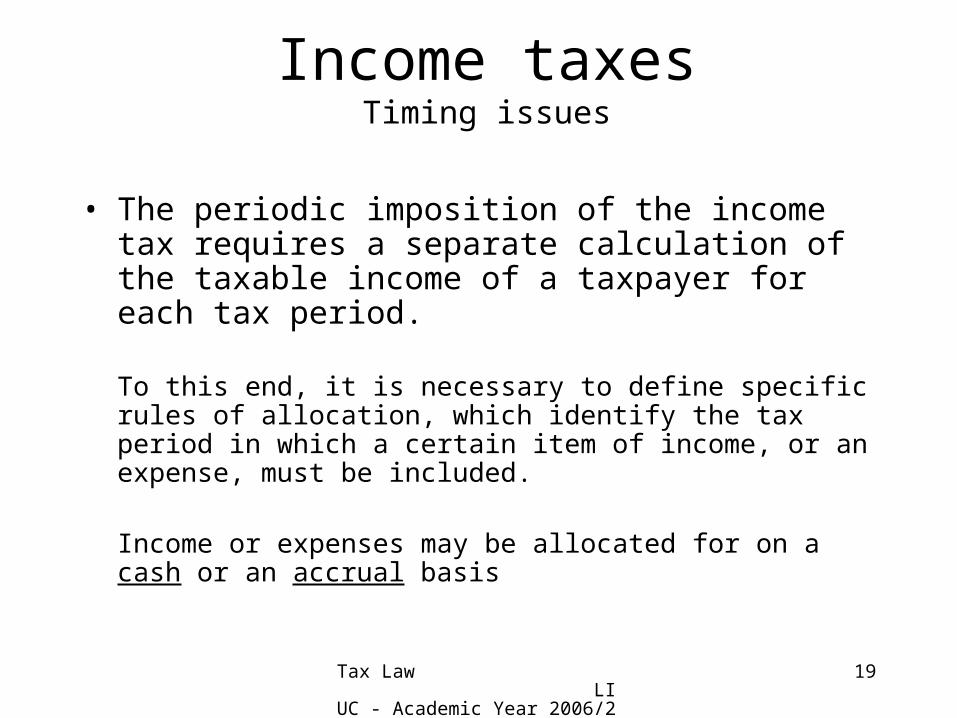

• The periodic imposition of the income tax requires a separate calculation of the taxable income of a taxpayer for each tax period.

To this end, it is necessary to define specific rules of allocation, which identify the tax period in which a certain item of income, or an expense, must be included.

Income or expenses may be allocated for on a cash or an accrual basis

Tax Law LIUC - Academic Year 2006/2007

20

Income taxesTiming issues

Under the cash method, income is derived in the tax period in which it is actually received by, made available to, or, in the case of benefit, provided to the taxpayer.

The cash method is usually applied in determining:

– income from employment;– income from capital.

Tax Law LIUC - Academic Year 2006/2007

21

Income taxesTiming issues

Under the accrual method, income is derived in the tax period in which the right to receive the income arises, and expenses are accounted for in the tax period in which the obligation to pay arises.

The accrual method usually requires a proper accounting system which is able to calculate the correct amount of income and expenses which are attributable to a given tax period. Therefore, it is generally applied to business taxpayers.

Tax Law LIUC - Academic Year 2006/2007

22

Income taxesThe taxpayer

The taxpayer is the person liable for tax.

The term taxpayer does not necessarily identify a person who is obliged to pay tax in a particular tax period (indeed the taxpayer’s liability may be also satisfied by a person other than the taxpayer itself eg. withholding tax).

A taxpayer may also be required to fulfil certain administrative requirements, such as filing a tax return or provide information to the tax authorities.

Tax Law LIUC - Academic Year 2006/2007

23

Income taxesThe taxpayer

The primary distinction for taxpayers is made between:

• individuals; and

• legal entities.

Tax Law LIUC - Academic Year 2006/2007

24

Income taxesThe taxpayer

As with regard to individuals the relevant issue is to define the tax unit.

A wide range of tax units is used in different jurisdictions for imposing tax on individuals; the main possibilities are:– individuals;– married couples;– families.

If couples or families (however defined) are treated as the tax unit, then taxable income is calculated by reference to the income and deductions of all persons included in the tax unit.

Tax Law LIUC - Academic Year 2006/2007

25

Income taxesThe taxpayer

The relevant consequence for the definition of tax unit is the tax rate structure.

Indeed, progressive tax rates and tax-free zone have an important impact on the difference between aggregation, splitting and separate unit systems.

On the other hand,when the individual tax rates are relatively flat, the difference between income aggregation and income splitting are minimal.

Tax Law LIUC - Academic Year 2006/2007

26

Income taxesThe taxpayer

Many tax systems provide some relief for the cost of supporting dependents, such relief may be granted through:

– income splitting with dependents;

– deductions for the support of dependents;

– refundable or non-refundable tax offsets.

Tax Law LIUC - Academic Year 2006/2007

27

Income taxesThe taxpayer

Under the income splitting and deductions system, the higher the individual’s income, the greater the value of the relief.

As a consequence, in such cases relief is provided inversely with the taxpayer’s need.

Many countries moved to a tax offset system.

Tax Law LIUC - Academic Year 2006/2007

28

Income taxesThe taxpayer

As far as legal entities are concerned, the definition of taxpayer plays a crucial role in determining whether an entity is entitled to Treaty benefit.

To this end, it becomes important to distinguish between transparent and non-transparent entity for tax purposes.

Tax Law LIUC - Academic Year 2006/2007

29

Income taxesDefining residence

To exercise residence jurisdiction, a country must provide rules that classify individuals and legal entities either as residents or as non-residents.

Tax Law LIUC - Academic Year 2006/2007

30

Income taxesDefining residence

Individuals• Formal criteria (registration in the Registry of resident

population; residence status for visa or immigration purposes; citizenship)

• Mechanical test (days of presence test):– 183 day test– Cumulative presence test considering a certain numbers of

years.

• Fact and circumstances test– (..)– (…)

Tax Law LIUC - Academic Year 2006/2007

31

Income taxesDefining residence

Factors which are usually considered relevant in determining the residence of an individual:

– maintenance of a dwelling or an abode that is available for the taxpayer’s use;

– place where the individual engages in income-producing activities;

– location of the individual’s family;– social ties to the country.

Tax Law LIUC - Academic Year 2006/2007

32

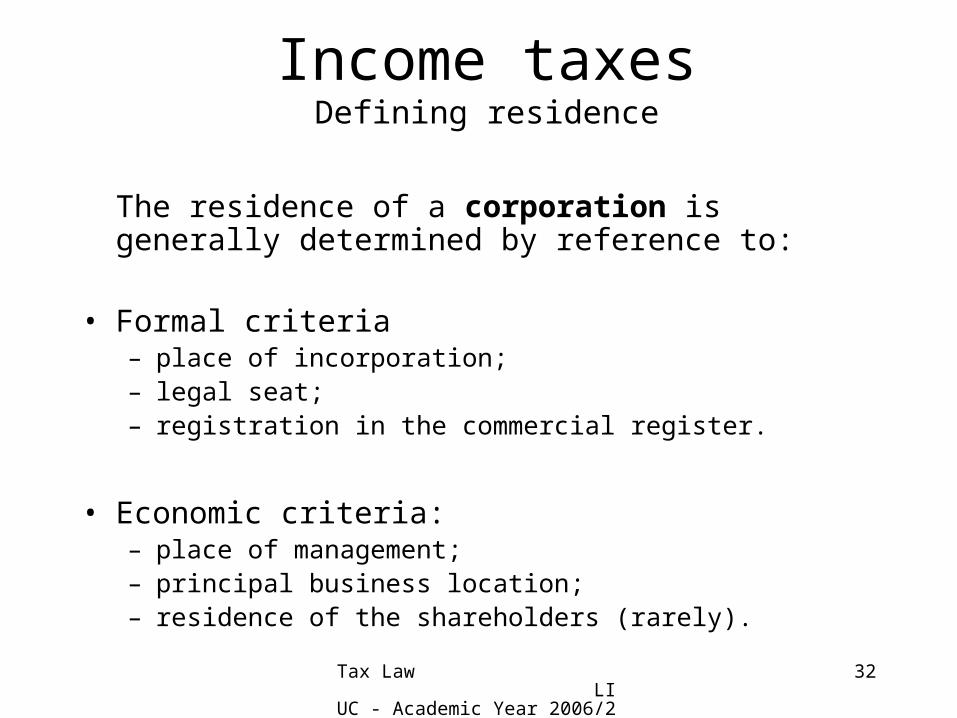

Income taxesDefining residence

The residence of a corporation is generally determined by reference to:

• Formal criteria– place of incorporation;– legal seat;– registration in the commercial register.

• Economic criteria:– place of management;– principal business location;– residence of the shareholders (rarely).

Tax Law LIUC - Academic Year 2006/2007

33

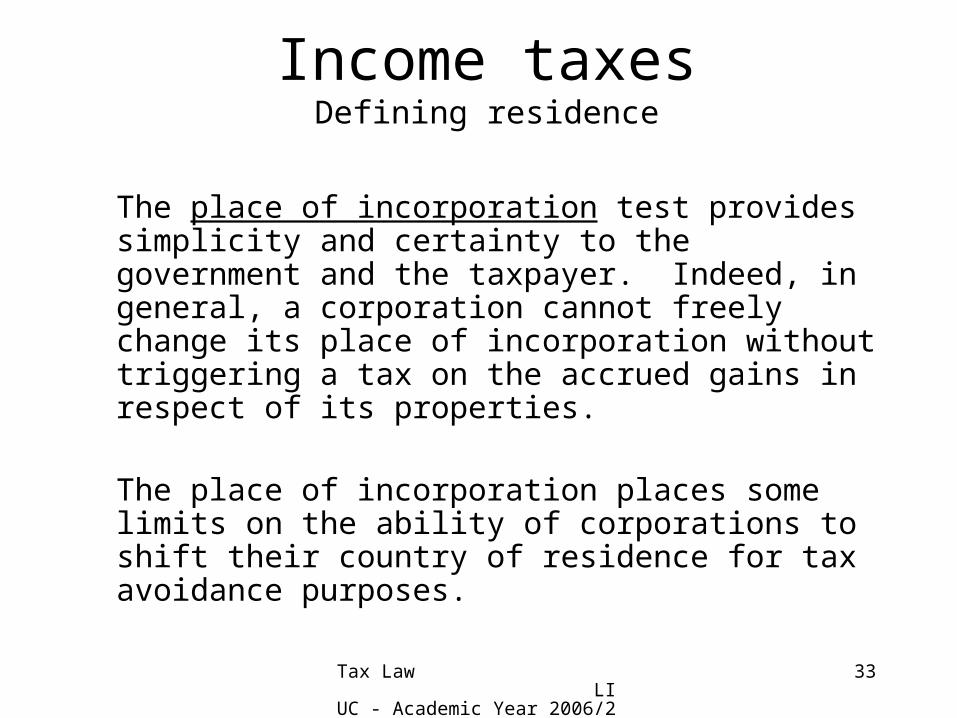

Income taxesDefining residence

The place of incorporation test provides simplicity and certainty to the government and the taxpayer. Indeed, in general, a corporation cannot freely change its place of incorporation without triggering a tax on the accrued gains in respect of its properties.

The place of incorporation places some limits on the ability of corporations to shift their country of residence for tax avoidance purposes.

Tax Law LIUC - Academic Year 2006/2007

34

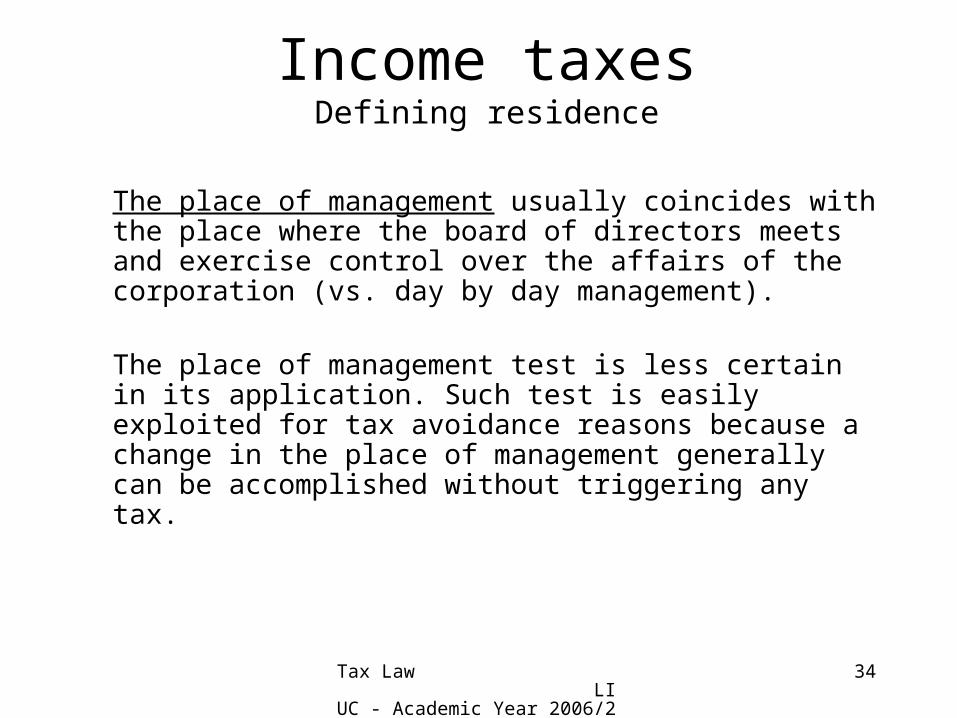

Income taxesDefining residence

The place of management usually coincides with the place where the board of directors meets and exercise control over the affairs of the corporation (vs. day by day management).

The place of management test is less certain in its application. Such test is easily exploited for tax avoidance reasons because a change in the place of management generally can be accomplished without triggering any tax.

Tax Law LIUC - Academic Year 2006/2007

35

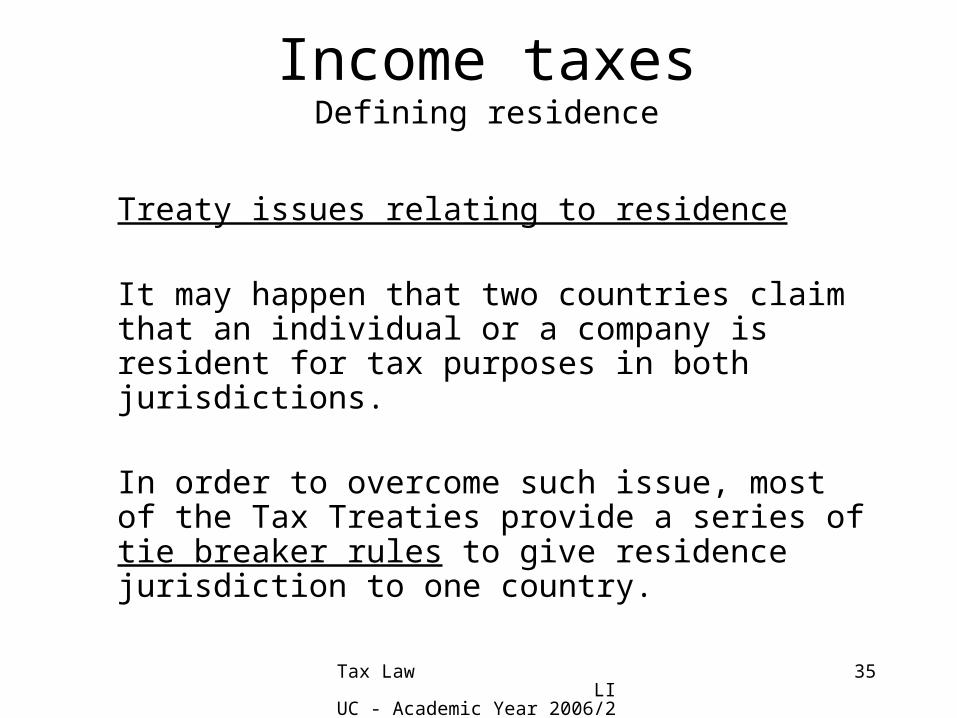

Income taxesDefining residence

Treaty issues relating to residence

It may happen that two countries claim that an individual or a company is resident for tax purposes in both jurisdictions.

In order to overcome such issue, most of the Tax Treaties provide a series of tie breaker rules to give residence jurisdiction to one country.

Tax Law LIUC - Academic Year 2006/2007

36

Income taxesDefining residence

As with regard to individuals, the following tie breaker rules shall be applicable:

1. the place where the individual has permanent home;

2. the country in which the center of the individual’s vital interest is located;

3. the place where the individual’s habitual dwelling;

4. the country of citizenship.

Tax Law LIUC - Academic Year 2006/2007

37

Income taxesDefining residence

For legal entities resident in two countries, Tax Treaty provisions makes the entity a resident of the country its effective management is located.

Tax Law LIUC - Academic Year 2006/2007

38

Income taxesEconomic and juridical double taxation

The term “double taxation” is used in many different contexts (eg. international or domestic).

In general:

• economic double taxation occurs when the same item of income is taxed twice in the hands of different taxable person; whilst

• juridical double taxation occurs when the same item of income is taxed twice in the hands of the same taxable person.

Tax Law LIUC - Academic Year 2006/2007

39

Income taxesEconomic and juridical double taxation

Juridical double taxation is usually the consequence of the application of a withholding tax on certain payments, such as dividends, interest and royalties considerations.

Economic double taxation is the direct consequence of taxation of business income produced through a legal entity and then distributed to the shareholders.

Tax Law LIUC - Academic Year 2006/2007

40

Income taxesEconomic and juridical double taxation

There are several methods for granting relief from “double taxation”:

• deduction method;

• exemption method;

• credit method.

Tax Law LIUC - Academic Year 2006/2007

41

Income taxesEconomic and juridical double taxation

According to the “deduction method”, the tax rules allow the taxpayer to claim a deduction for taxes paid on the same item of income. In this case, taxes are treated as expenses of the business.

Within an international context, foreign-source income earned by residents of a country that uses the “deduction method” is taxable at a higher effective rate than it would be under either the “credit method” or the “exemption method”.

Tax Law LIUC - Academic Year 2006/2007

42

Income taxesEconomic and juridical double taxation

Under the “exemption method”, the tax rules provides the taxpayer with an exemption for income which has been already subject to tax.

Within an international context, the “exemption method” is generally the most favourable to the taxpayer when the foreign effective tax rate is less than the domestic effective tax rate.

Under a variation of the “exemption method” the income, although exempt, is taken into account in determining the rate applicable to the taxapayer’s taxable income - “exemption with progression”

Tax Law LIUC - Academic Year 2006/2007

43

Income taxesEconomic and juridical double taxation

Under the “credit method”, the taxes already paid on the same income reduce taxes payable by the taxpayer.

Within an international context, the taxes paid abroad are usually “topped up” by domestic taxes so that the combined domestic and foreign tax rate on the foreign-source income is equal to the tax rate. Credit countries do not pay tax refunds when their taxpayers pay a foreign income tax at an effective rate that is higher than the domestic effective tax rate - “ordinary tax credit”.

Tax Law LIUC - Academic Year 2006/2007

44

Business Income Introduction

• Both individuals and legal persons engage in business activities.

• When an activity may be characterised as a business?

• If business income is not defined in tax law, reference is made to the commercial law provisions

IN GENERAL, A BUSINESS IS A COMMERCIAL OR INDUSTRIAL ACTIVITY OF AN INDIPENDENT NATURE UNDERTAKEN FOR PROFITS.

Tax Law LIUC - Academic Year 2006/2007

45

Business Income Introduction

Two basics model are used to determine the taxable income arising from business activities:

• The receipts-an-outgoings system

• The balance-sheet system

Tax Law LIUC - Academic Year 2006/2007

46

Business Income Introduction

The receipts-an-outgoings system

• the determination of taxable business income is based on the calculation of all recognised income amounts derived by the taxpayer in the tax period and all deductible expenses incurred by the taxpayer in the same tax period.

Tax Law LIUC - Academic Year 2006/2007

47

Business Income Introduction

Balance-sheet method

• The starting point is the commercial income arising from financial accounting, to which adjustments are added to take into account differences between tax rules and financial accounting rules.

Tax Law LIUC - Academic Year 2006/2007

48

Business Income Introduction

Business income is generally calculated on an accrual basis:

• Revenues are derived when the right to receive the income arises.

• Expenses are incurred when the obligation to pay arises.

• For corporations, the accrual method is also the basis of financial accounting where specific regulations are provided.

Tax Law LIUC - Academic Year 2006/2007

49

Business Income Definition of business assets

In determining business income, in general, revenues include both gains from ongoing commercial activities and gains on the disposal of business assets.

The concept of business assets should include not only assets physically used in, or held by the business, but also investment assets related to a business activity.

This is achieved through a broad definition of business assets that includes all assets used, ready for use, or held for the purpose of a business.

Tax Law LIUC - Academic Year 2006/2007

50

Business Income Definition of business assets

The inclusion in business income of gains arising on the disposal of business assets needs to be coordinated with any special regime applying to specific types of assets, such as:

• Inventories, which give rise to revenues.• Depreciable and amortisable assets, which give

rise to capital gains/losses.• Other assets (eg. Participation in companies),

which may produce capital gains or losses.

Tax Law LIUC - Academic Year 2006/2007

51

Business Income Determination

Tax rules related to assets should define:

• Timing rules for the realization of gain or losses.• Cost base of an assets.• Determination of gain or loss.

Tax Law LIUC - Academic Year 2006/2007

52

Business Income Determination

Timing rules for the realization of gain or losses.

• Gain or loss is realised when the taxpayer ceases to own the asset. In this respect, it is crucial to identify the concept of disposal which should includes not only sales, but also exchanges, losses, gifts, etc.

• Another relevant issue is the change of tax regime applicable to a particular asset (eg. From business asset to personal one or vice versa).

Tax Law LIUC - Academic Year 2006/2007

53

Business Income Determination

Cost base

• Cost base is equal to the consideration given for the acquisition of an asset, plus any ancillary cost incurred in the acquisition of the asset (eg. Legal and registration fee, transfer taxes, etc.). Such base should also include any capital expenditure incurred to improve the assets

Consideration received

• The consideration received is equal to the price received.

Tax Law LIUC - Academic Year 2006/2007

54

Business Income Determination

Market value / Arm’s length principle

• In kind consideration should be determined at market value.• Related parties may be tempted of manipulating transfer

prices for tax driven reasons• Arm’s length price of a certain transaction is the price that

unrelated parties would have agreed upon, given the same circumstances of such a transaction

Non-recognition rule

• Sometimes particular non-recognition rules are provided. It is the case, for example, of the tax position of an assets that is rolled over into another asset in case of new investment.

Tax Law LIUC - Academic Year 2006/2007

55

Business Income Deduction of expenses

In general, all costs incurred to derive business income should be recognised for the purpose of determining net income.

• Sometimes tax laws use restrictive language such as “ordinary and necessary” when defining deductible expenses.

• In other cases, reference is made to expenses that are “wholly and exclusively” incurred to derive income subject to tax (this definition may create problems in respect to expenses incurred to derive exempt income).

Tax Law LIUC - Academic Year 2006/2007

56

Business Income Deduction of expenses

Expenses and other negative items of income shall be deductible if and to the extent that they relate to activities or assets which produce revenue or other receipts which are included in the taxable income.

The literal analysis of the above provision leads to a wide interpretation of the concept of inherence. Accordingly, shall be deductible from the taxable income all those costs that are functional to the business activity, even if they are not strictly related to a specific revenue.

Tax Law LIUC - Academic Year 2006/2007

57

Business Income Deduction of expenses

Tax laws provides for specific limitations in respect to certain type of expenses, such as:

• personal expenses;• capital expenses;• Policy-motivated restrictions (eg. no tax deduction

for fines, penalties, bribes etc.);• passive interest (see thin capitalisation rules);• expenses that have elements of both business and

personal consumption (eg. entertainment, meal and refreshment).

Tax Law LIUC - Academic Year 2006/2007

58

Business Income Deduction of expenses

Research and development costs• It is difficult to certainly determine benefits and useful life of

research and development.• As a consequence, generally, presumptive rules are provided:

– amortization in short period of time (2/3 years);– entire depreciation in the year when expenses are incurred.

Advertising / Marketing expenses• In principle ordinary marketing expenses should be

distinguished from extraordinary marketing expenses, the second providing benefits for more than one period.

• In practice, also in such a case it is difficult to determine benefits and useful life, so that presumptive rules are provided.

Tax Law LIUC - Academic Year 2006/2007

59

Business Income Deduction of expenses / Depreciation

Capital assets• Capital business assets very often have a useful life

which is longer than one tax period.• To accomplish with the accrual principle the cost of

such assets should be split among tax periods in which the assets contribute to the income production (depreciation/amortisation plan).

– a depreciation/amortisation plan must consider:– the cost of the asset;– the period of useful life;– the residual value at the end of the “useful period”.

Tax Law LIUC - Academic Year 2006/2007

60

Business Income Deduction of expenses / Depreciation

Tangible properties (examples)• buildings;• industrial plants;• equipments.

Intangible properties (examples)• term limited rights;• goodwill.

Tax Law LIUC - Academic Year 2006/2007

61

Business Income Depreciation rates and methods

Economically depreciation should reflect the benefit that the property contributed to the activity in the period.

From a tax perspective depreciation should reflect the decrease in value of the property:

– straight line depreciation;– declining balance depreciation;– units of production depreciation.

Tax Law LIUC - Academic Year 2006/2007

62

Business Income Corporate-shareholder taxation

Almost all countries impose a tax on earnings of corporations separate from the tax on individuals’ income.

Such a system implies an economic double taxation of the income produced by corporations when distributed to the owners.

Countries have different approaches to economic double taxation:

• Classic system (double taxation).• Dividend deduction (Avoidance/mitigation of double taxation

at a corporate level).• Exemption, imputation system (avoidance/mitigation of

double taxation at a shareholder level).

Tax Law LIUC - Academic Year 2006/2007

63

Business Income Corporate-shareholder taxation

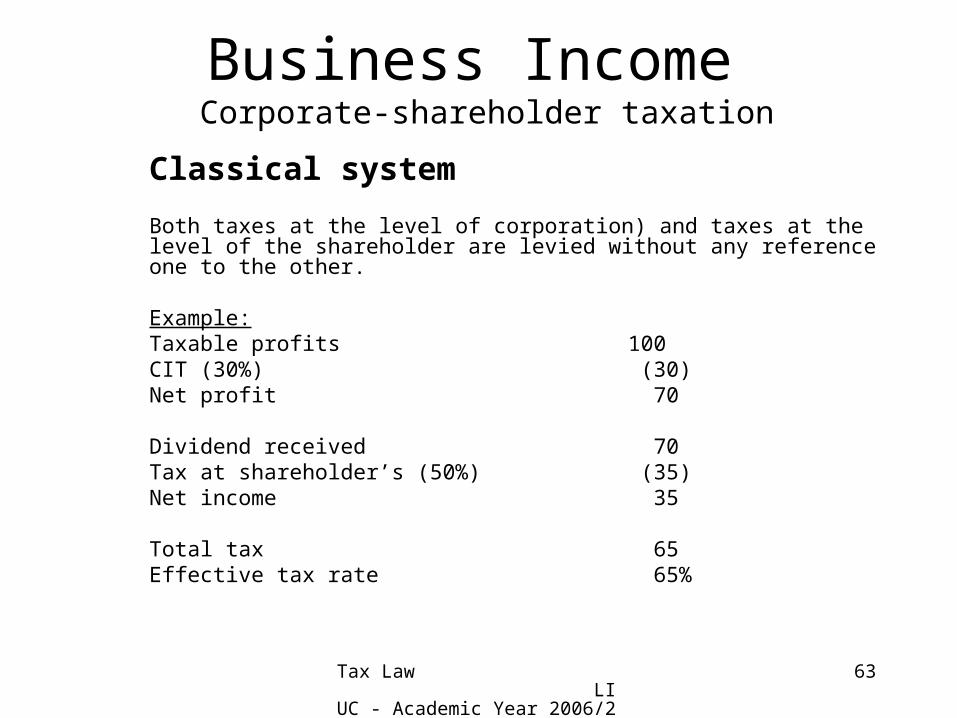

Classical system

Both taxes at the level of corporation) and taxes at the level of the shareholder are levied without any reference one to the other.

Example:Taxable profits 100CIT (30%) (30)Net profit 70

Dividend received 70Tax at shareholder’s (50%) (35)Net income 35

Total tax 65Effective tax rate 65%

Tax Law LIUC - Academic Year 2006/2007

64

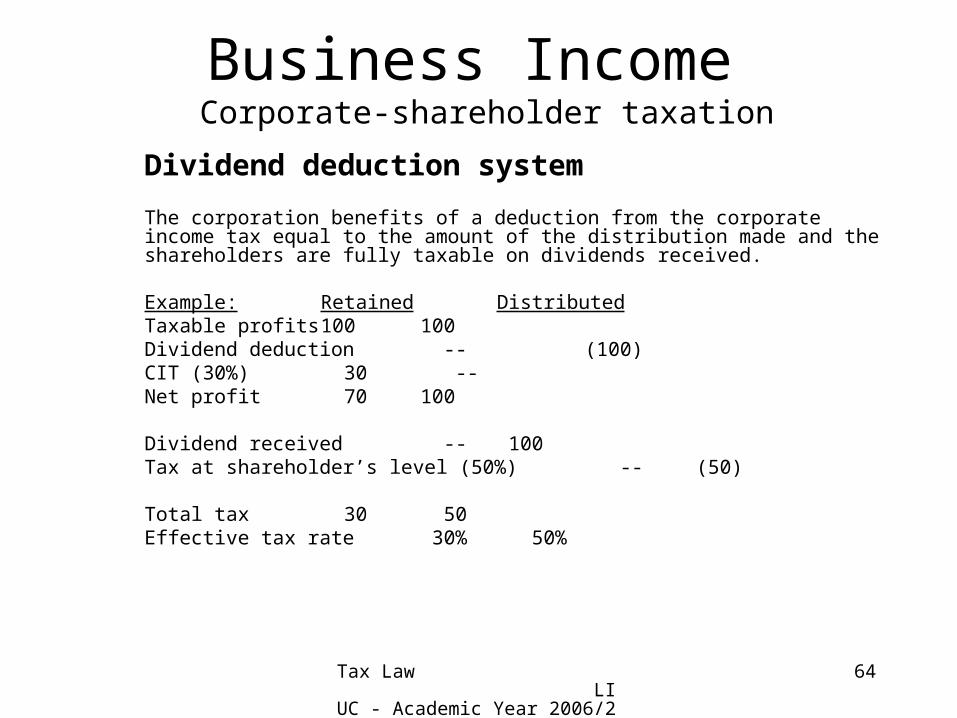

Business Income Corporate-shareholder taxation

Dividend deduction system

The corporation benefits of a deduction from the corporate income tax equal to the amount of the distribution made and the shareholders are fully taxable on dividends received.

Example: Retained DistributedTaxable profits 100 100Dividend deduction -- (100)CIT (30%) 30 --

Net profit 70 100

Dividend received -- 100 Tax at shareholder’s level (50%) -- (50)

Total tax 30 50Effective tax rate 30% 50%

Tax Law LIUC - Academic Year 2006/2007

65

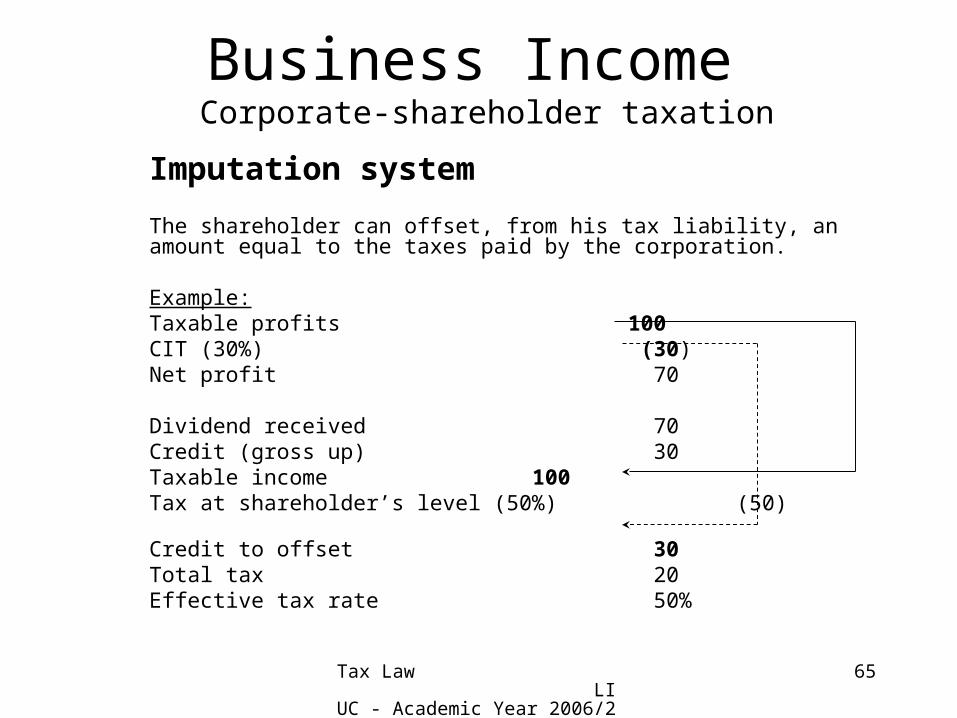

Business Income Corporate-shareholder taxation

Imputation system

The shareholder can offset, from his tax liability, an amount equal to the taxes paid by the corporation.

Example:Taxable profits 100 CIT (30%) (30)Net profit 70

Dividend received 70Credit (gross up) 30Taxable income 100Tax at shareholder’s level (50%) (50)

Credit to offset 30Total tax 20Effective tax rate 50%

Tax Law LIUC - Academic Year 2006/2007

66

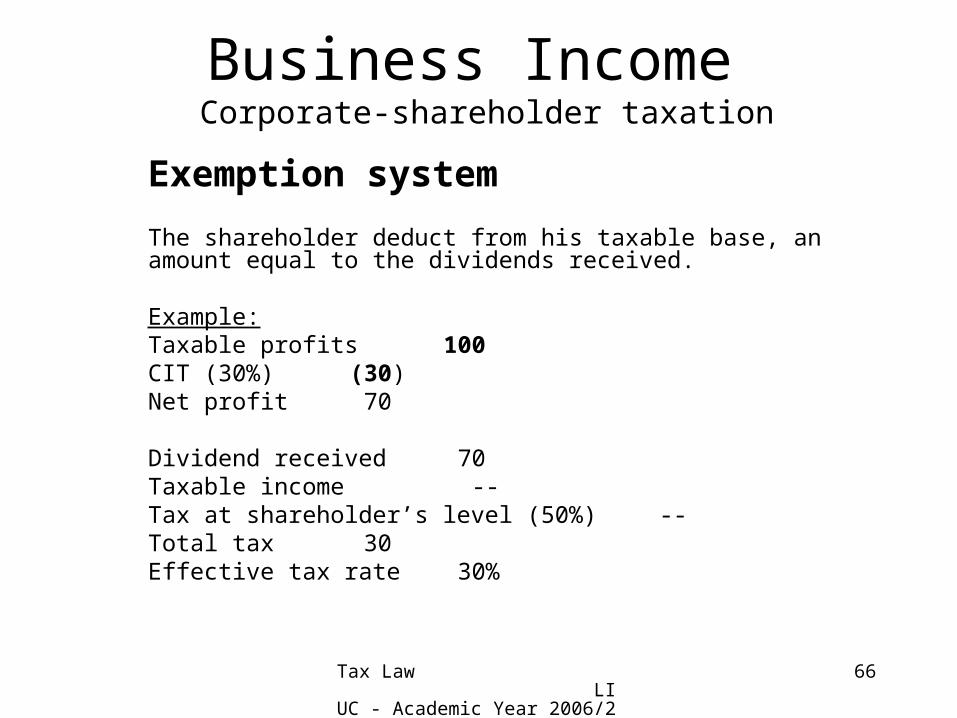

Business Income Corporate-shareholder taxation

Exemption system

The shareholder deduct from his taxable base, an amount equal to the dividends received.

Example:Taxable profits 100 CIT (30%) (30)Net profit 70

Dividend received 70Taxable income --Tax at shareholder’s level (50%) --Total tax 30Effective tax rate 30%

Tax Law LIUC - Academic Year 2006/2007

67

Investment Income Introduction

• Under schedular system, characterization determines which tax regime applies to the income

• Under a global system, there may be a specific inclusion rule for investment income or special timing or administrative rules.

Tax Law LIUC - Academic Year 2006/2007

68

Investment Income

• Under schedular system, characterization determines which tax regime applies to the income

• Under a global system, there may be a specific inclusion rule for investment income or special timing or administrative rules.

Tax Law LIUC - Academic Year 2006/2007

69

Investment Income

The definition of investment income, usually, includes:

• Annuities• Dividends• Interest• Rent• Royalties• Capital gains on the disposal of investment assets

Tax Law LIUC - Academic Year 2006/2007

70

Investment Income

AnnuitiesA taxpayer purchasing a commercial annuity provides an “annuity provider” with a capital sum that is returned with compensation conceptually similar to interest in fixed payments over specified term or, in case of life annuity, over the taxpayer’s life (eg. insurance scheme).

Tax Law LIUC - Academic Year 2006/2007

71

Investment Income

InterestInterest is the compensation earned by a creditor for the use of his or her money during the period of the loan (debt obligation).

RoyaltiesPayments received as a consideration for the use of, or the right to use, any copyright of literary, artistic or scientific work including patent, trade mark, design or model, plan, secret formula or process.

Tax Law LIUC - Academic Year 2006/2007

72

Investment Income

RentAny amount received as consideration for the use and occupation of, or right to use or occupy, immovable property.

DividendsIncome from shares, “jouissance” shares or “jouisance” rights and other rights, not being debt-claims, participating in corporate profits.

Tax Law LIUC - Academic Year 2006/2007

73

Investment Income

Interest, dividends and capital gains on shares……are usually subject to a special tax regime (eg. withholding tax, substitute tax etc.)

Tax Law LIUC - Academic Year 2006/2007

74

VATIntroduction

• The purpose of a turnover tax is to tax goods destined for personal consumption….

• …also services are to be included.

• Business income taxes are levied on the business activity whilst VAT is levied on each transaction.

Tax Law LIUC - Academic Year 2006/2007

75

VATIntroduction

• VAT, as levied in Europe, covers all stages of production and distribution.

• The deduction of input VAT prevents from cumulation.

• Within the chain of production and distribution VAT does not influence the price of goods or service, unless exemption are applied…indeed, whatever tax the one business is charging, the other business will deduct it, at same moment.

Tax Law LIUC - Academic Year 2006/2007

76

VATIntroduction

• The most essential record is the invoice which must list the VAT paid so that business purchasers are able to claim credit for VAT already paid preceding business sellers.

• This facilitates calculation of the tax and also provides a clear audit trail.

• It is possible that, in a given period, the deduction claimed exceeds the tax due. IN particular this will happen in case of large investments, then the difference will be refunded to the tax payer.

Tax Law LIUC - Academic Year 2006/2007

77

VATIntroduction

• Art. 99 of the (original) EEC Treaty instructed the commission as follows:

“The commission shall consider how the legislation of the various member states concerning turnover taxes, excise duties and other form of indirect taxation (…) can be harmonised in the interest of the common market.”

• 1960, the Commission, through reports issued by different working groups and committee, recommends that Member States adopt the VAT.

Tax Law LIUC - Academic Year 2006/2007

78

VATIntroduction

• The first Directive of 11 April 1967, together with the second directive of the same date, instructed the Member States to replace the existing turnover tax systems by a common system of “Tax on Value Added”.

• France already had VAT (minor changes were made to the previous system).

• Germany implemented VAT in 1968.

• Netherlands did it as well in 1969.

• Luxembourg complied in 1970.

Tax Law LIUC - Academic Year 2006/2007

79

VATIntroduction

• A third directive extended the deadline for the implementation of the first and second directive until 1972.

• Belgium introduced VAT in 1971.

• Fourth and Fifth directive extended the time limit for Italy, which implemented it in 1973.

• On 17 May 1977, The Sixth directive was adopted with the aim of further harmonise the various national laws.

• (…)

Tax Law LIUC - Academic Year 2006/2007

80

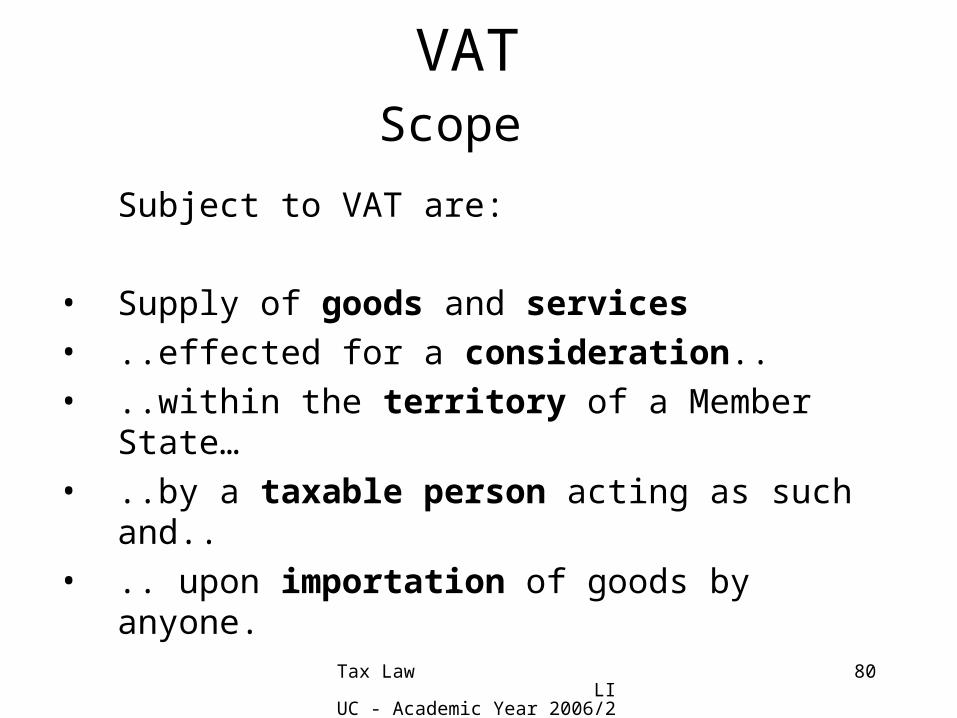

VATScope

Subject to VAT are:

• Supply of goods and services

• ..effected for a consideration..

• ..within the territory of a Member State…

• ..by a taxable person acting as such and..

• .. upon importation of goods by anyone.

Tax Law LIUC - Academic Year 2006/2007

81

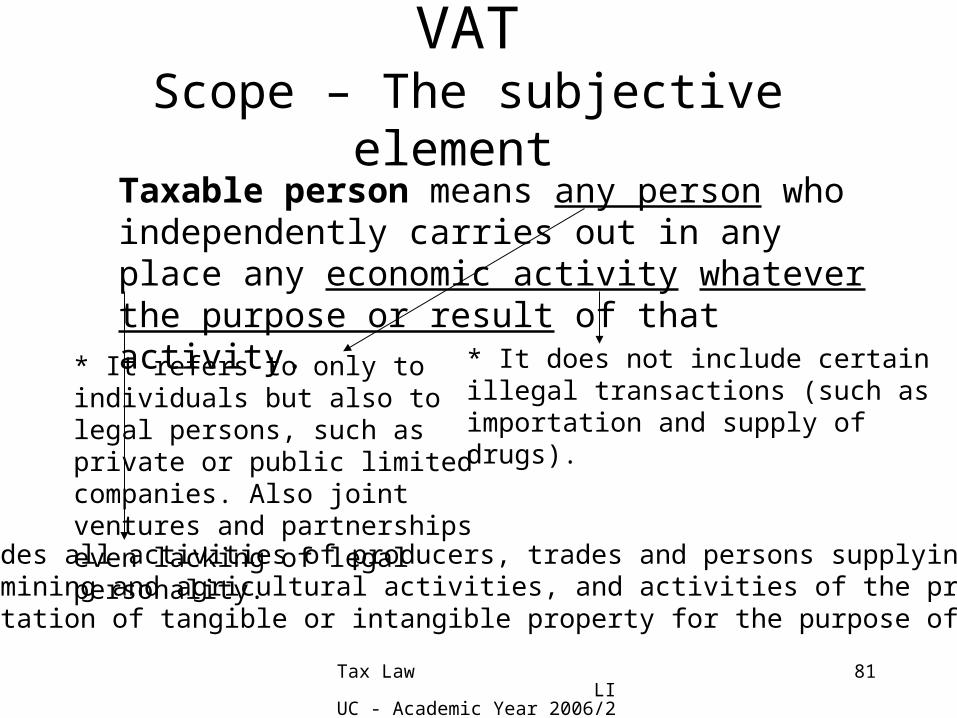

VATScope – The subjective element Taxable person means any person who independently carries out in any place any economic activity whatever the purpose or result of that activity.

* It refers to only to individuals but also to legal persons, such as private or public limited companies. Also joint ventures and partnerships even lacking of legal personality.

* It does not include certainillegal transactions (such as importation and supply of drugs).

* It includes all activities of producers, trades and persons supplying services, including mining and agricultural activities, and activities of the professions and the exploitation of tangible or intangible property for the purpose of obtainingincome.

Tax Law LIUC - Academic Year 2006/2007

82

VATScope – The objective element

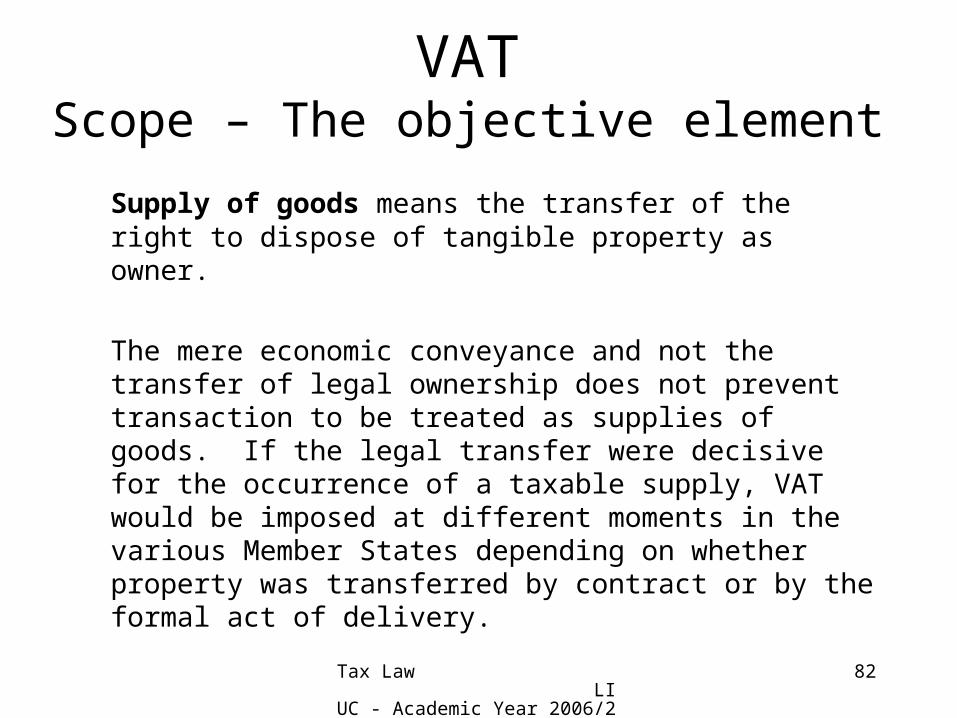

Supply of goods means the transfer of the right to dispose of tangible property as owner.

The mere economic conveyance and not the transfer of legal ownership does not prevent transaction to be treated as supplies of goods. If the legal transfer were decisive for the occurrence of a taxable supply, VAT would be imposed at different moments in the various Member States depending on whether property was transferred by contract or by the formal act of delivery.

Tax Law LIUC - Academic Year 2006/2007

83

VATScope – The objective element

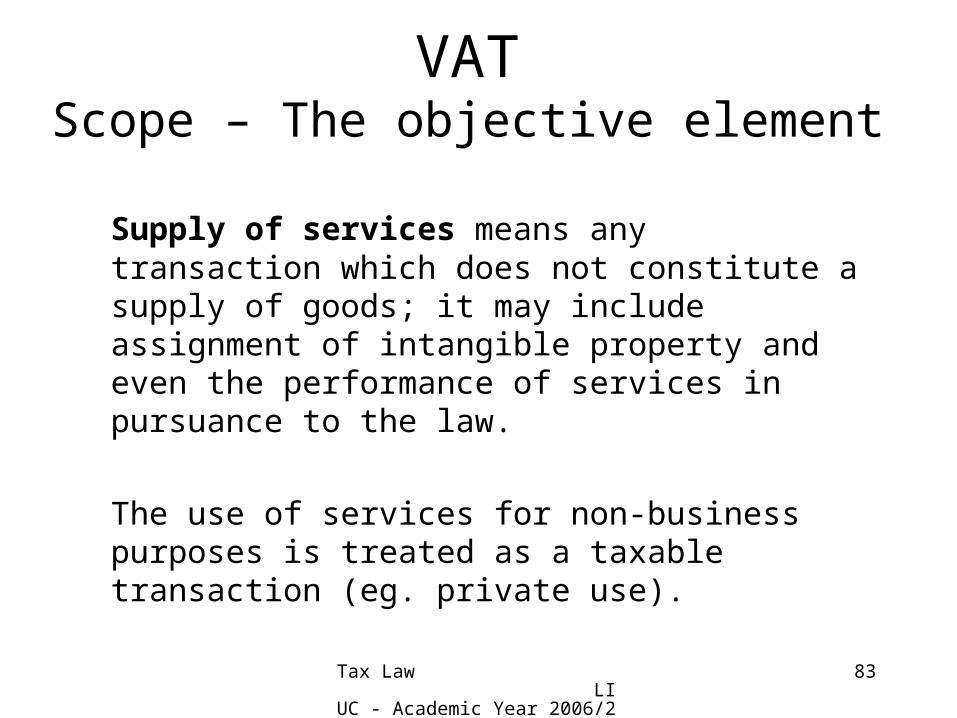

Supply of services means any transaction which does not constitute a supply of goods; it may include assignment of intangible property and even the performance of services in pursuance to the law.

The use of services for non-business purposes is treated as a taxable transaction (eg. private use).

Tax Law LIUC - Academic Year 2006/2007

84

VATScope – The territoriality element

The general rule with regard to the place of supply of services is that it is deemed to be the place where the supplier has established his business or has fixed establishment from which the services is supplied.

Exceptions:– services connected with immovable properties;– transportation services;– other services such as cultural, artistic, scientific or

entertainment activities;– Intangible services such as technical and consultancy services

Tax Law LIUC - Academic Year 2006/2007

85

VATScope – The territoriality element

Supply of goods

Goods that are not dispatched or transported, are treated as being supplied at the place where the goods are the supply takes place.

In case the goods are transported, the place of supply is deemed to be where the transportation commences.

Tax Law LIUC - Academic Year 2006/2007

86

VATRates

• The original provisions of the Sixth directive stipulated that rates to were to be fixed by the Member States themselves, but the standard rate applicable to the supply of goods and services and the importation of goods must be the same in order to fulfil the requirements of neutrality.

• Member States were permitted to apply increased or reduced rates to certain categories of supplies.

Tax Law LIUC - Academic Year 2006/2007

87

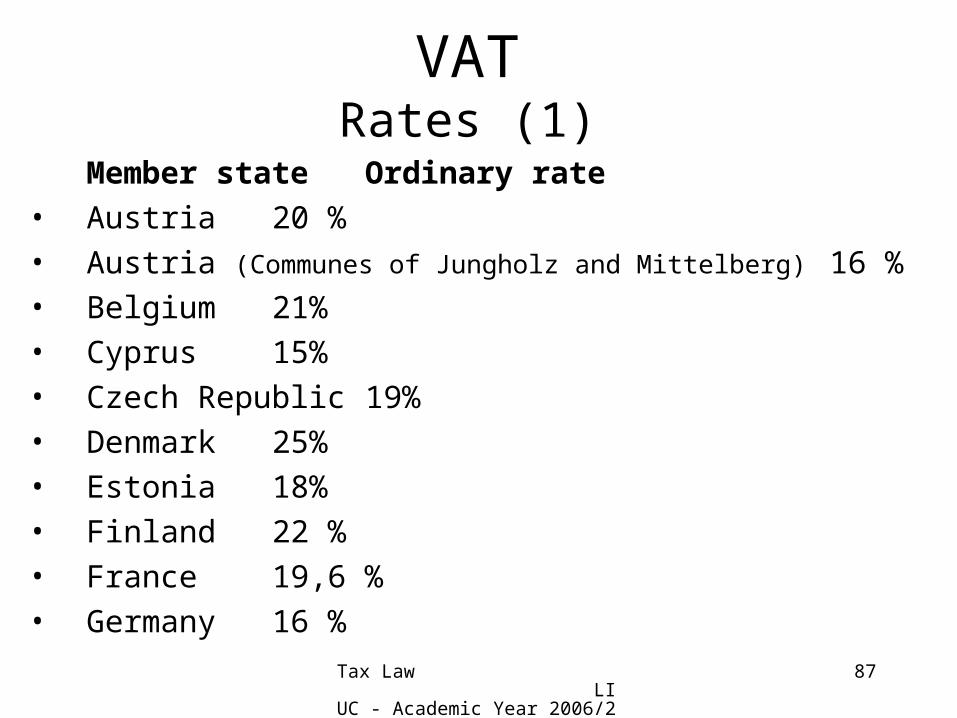

VATRates (1)

Member state Ordinary rate• Austria 20 %• Austria (Communes of Jungholz and Mittelberg) 16 %• Belgium 21%• Cyprus 15%• Czech Republic 19%• Denmark 25%• Estonia 18%• Finland 22 %• France 19,6 %• Germany 16 %

Tax Law LIUC - Academic Year 2006/2007

88

VATRates (2)

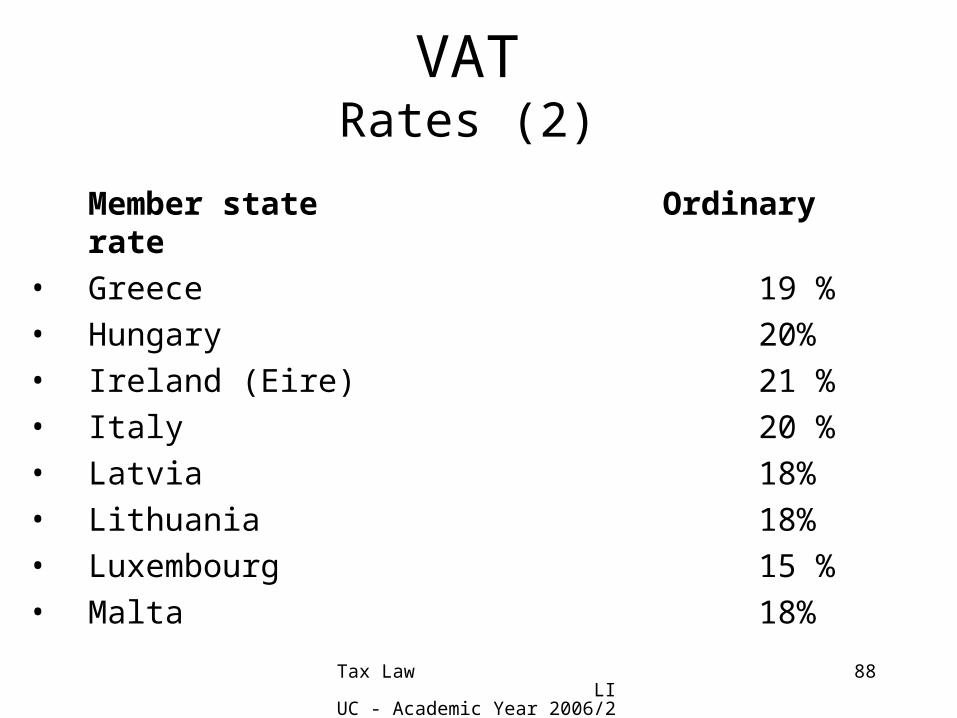

Member state Ordinary rate• Greece 19 %• Hungary 20% • Ireland (Eire) 21 %• Italy 20 %• Latvia 18%• Lithuania 18%• Luxembourg 15 %• Malta 18%

Tax Law LIUC - Academic Year 2006/2007

89

VATRates (3)

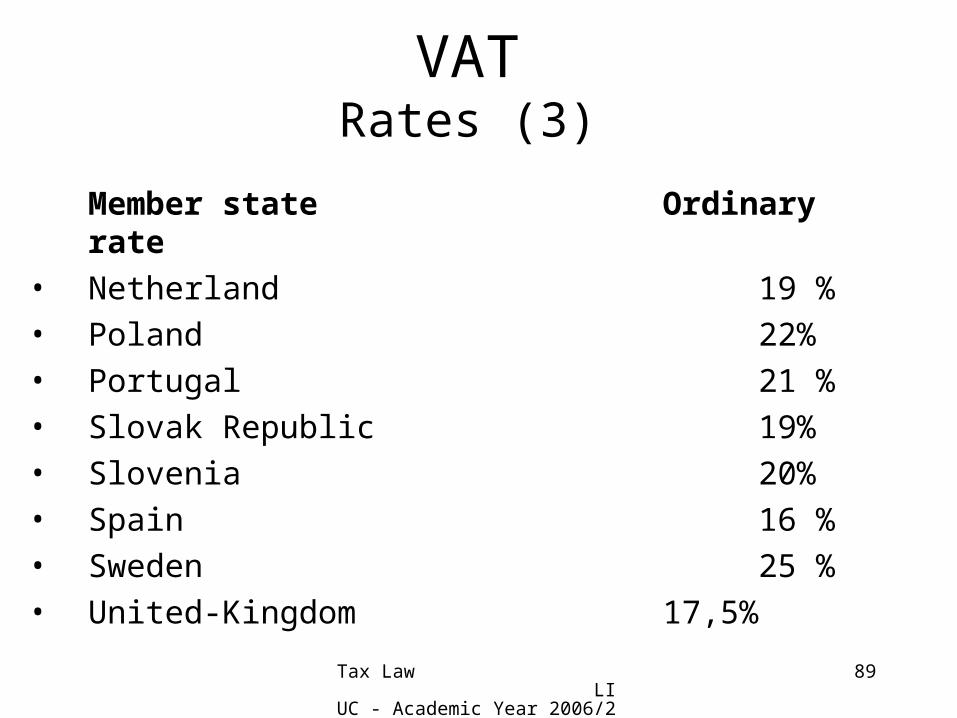

Member state Ordinary rate• Netherland 19 %• Poland 22%• Portugal 21 %• Slovak Republic 19%• Slovenia 20%• Spain 16 %• Sweden 25 %• United-Kingdom 17,5%

Tax Law LIUC - Academic Year 2006/2007

90

VATPro-rata

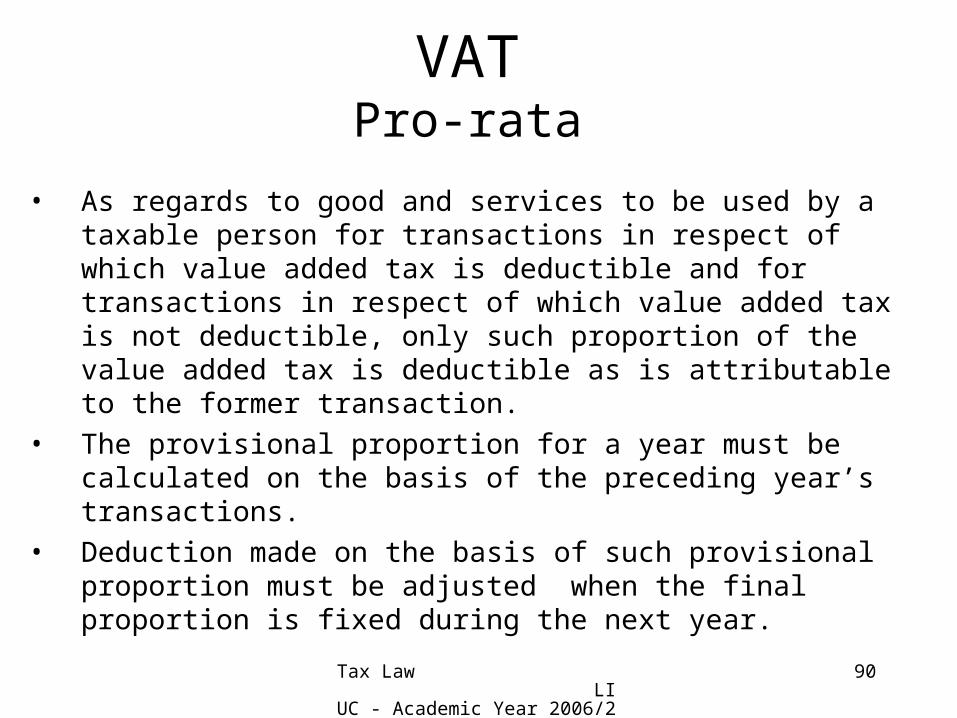

• As regards to good and services to be used by a taxable person for transactions in respect of which value added tax is deductible and for transactions in respect of which value added tax is not deductible, only such proportion of the value added tax is deductible as is attributable to the former transaction.

• The provisional proportion for a year must be calculated on the basis of the preceding year’s transactions.

• Deduction made on the basis of such provisional proportion must be adjusted when the final proportion is fixed during the next year.

Tax Law LIUC - Academic Year 2006/2007

91

VATPro-rata

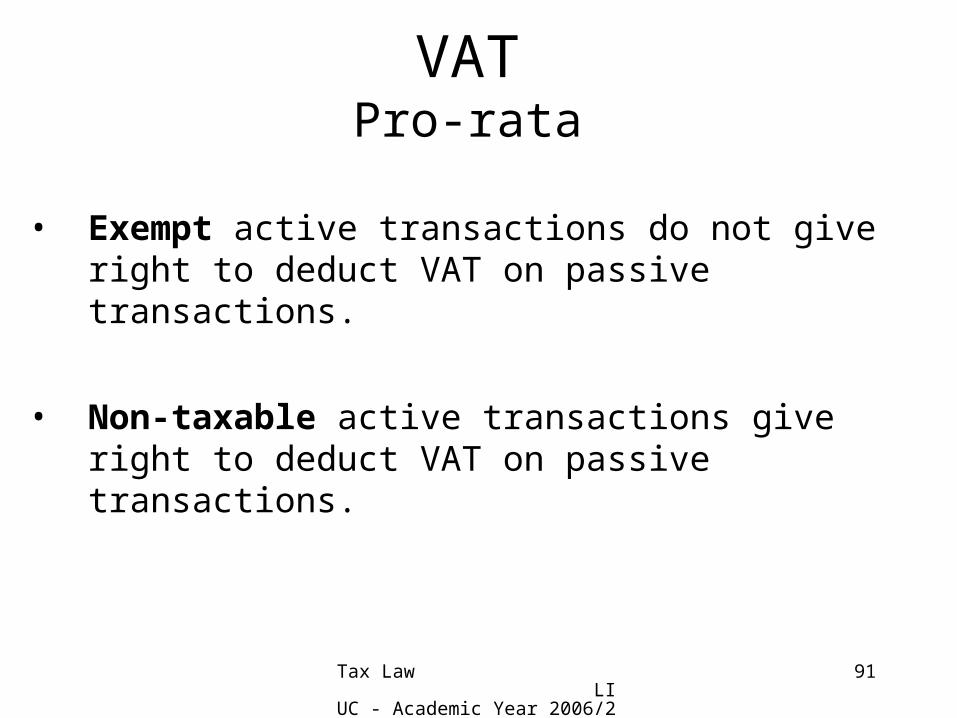

• Exempt active transactions do not give right to deduct VAT on passive transactions.

• Non-taxable active transactions give right to deduct VAT on passive transactions.