Embed Size (px)

DESCRIPTION

Atty Gonzales

Citation preview

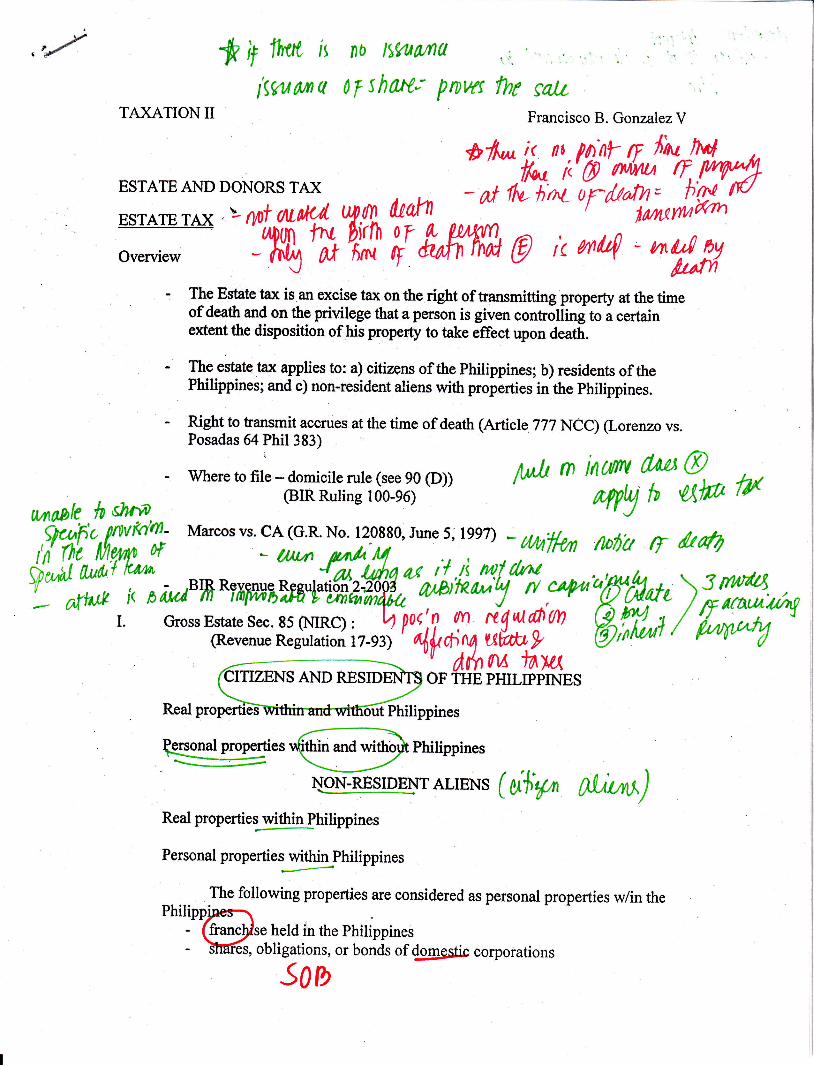

,''/ * if 'ftrtt{ is no ttwana

fiw an q o7 s hax; pnwr fhr cattTAXATION II Francisco B. Gonzalez V

ESTATE AND DONORS TAX

: The Estate tax is an excise tax on ttre right of transmitting property at the timeof death and on th9 nrivile8e that a person is given contolling to a certainextent the disposition of his prgpe{y to take ef[ect upon death.

- Theestate tax applies to: a) citizens ofthe philippines; b) residents of thePhilippines; and c) non-resident aliens with properties inthe philippines.

- Right to tansmit accrues at the time of death (Article 777 NCC) (Lorenzo vs.Posadas 64 Phil 383)

*/r* iino'n\ff ,ff;

lN tMdr,ffW

EsrArE rAx Y Ntu;#%rrlfif^ yfloverview - frU AI firnt tf 6t

- N flvh'rtt- ()F fuafh= h.XlurUYwmn

t@ kwlfi-h,tm

hrt't

ry'@PhilippinesNmmspE,NrALrENs (ut;r/^ Alrr^)

Real properties within P. hilippines

Personal properties withinJhilippines

The following properties are considered as personal properties 1,y7in thePhilippinesl

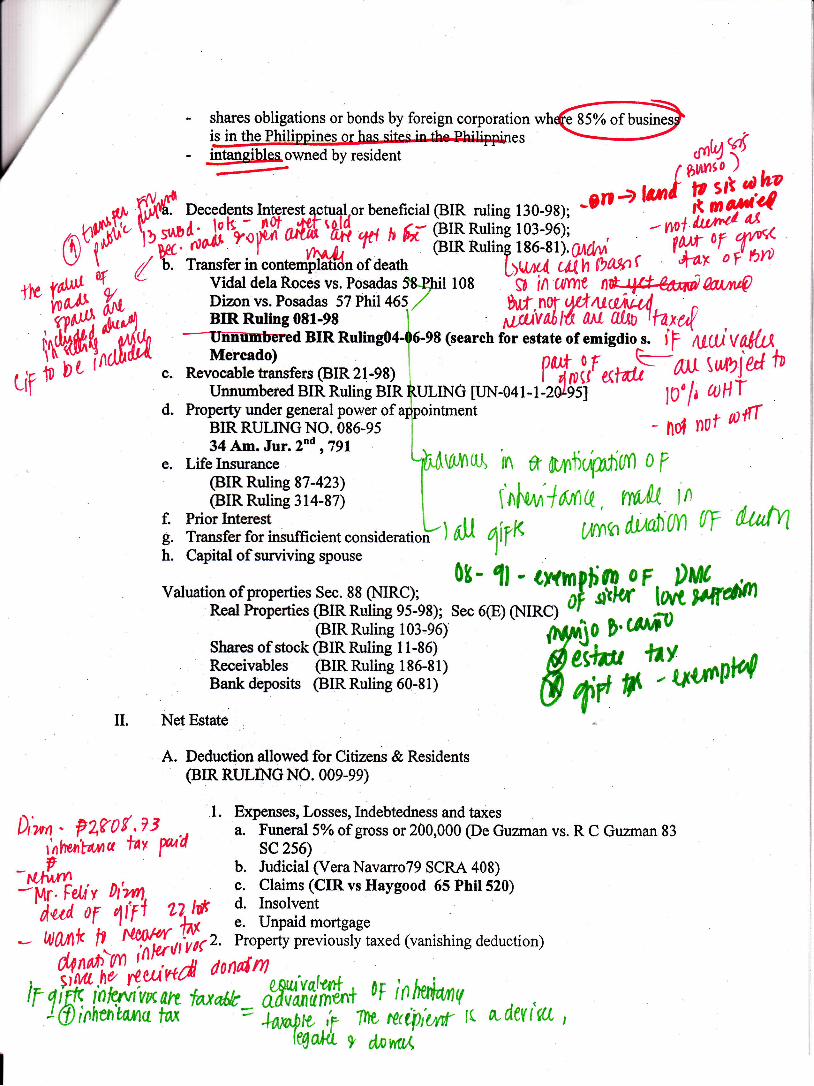

- (fr*.dse held in the Philippines- Mes, obligations, or bonds of {gggic corporations

Soo

- shares obligations or bonds by foreign corporation wh(e 85% of businesiis in the Philippines or has-sites-in rhe-PbiliFlrines --.--.Z - ^:. , VK

{.t:.1|- intaneibles owned by resident

s*'rffiwneob,resrdent 9-?91,-onaffiCI$e ffi ffiii.ffifilf Hli rliry !!#{i**,

-

tu vaV,tl Yn, (; Vidal dela Roces vs. Posadas s8qhil 108 -'SO in f,Uvyre nt-4d4ffi MnA

"" V*ffiWa, 3ffi[sJ;il$l*':\, Writr,Y,#Wry,t , ,'fit{, friA BrR Ruling 08r-e8 l' i$vatlfi NTtlit-ttaxerl

,'sfrt^,ffunlffidBIRRu'ing04.t6-98(searchforestate.r"-isaio|f,.y"*,:w, r lr* W,'iNil'* ". "r"H[frl?*r.*

*,*r,-rr, I ?*{ri, oF ^, \ulrld +t

uf ' unnumbgrea sId. Ruting nfn furrNc pN-041 +zal,iii l0' h UHT -*ff##'fiffiffiffi;:"'fointment

- no, not ViT34Am. Jar.z"d r79l

Lifelnsurance '.^^-- "FlVr,ytOl n fr p-rrfru@lt/ {l 0 F

@IRRulingST-423) | .t ., ,.irrn nuri"E rq-wi t til\tln lLtfiT , rr(t ill ln

i {ffr[*L*r*,**,u*"r"!-) n[ 4lrr wtlatmrn tY dtilvlh. Capital ofsunriving spouse

varuation orpropertie, u." 8-8 11nRgi . lt - J' : :\\l%qi' yo}Yu**RearProperties

Elttffi:1to-i,ht'" 6(E) (NIRCT

i l.u^n

ffiil:;:;-BFiffii;;{?r, &'ff-\'u*pwil. Net Estate

A. Deduction allowed for Citizens & Residents(BrR RULINGNO. ooe-ee)

Dirn . pzro { ; 7 3 - ., t'

:.Tffi:',h'li,]:?H::3T,t3r,rtr,trtuzman vs. R c Guzman 83

itrltwitanu tav yua sc 256)

--,.t^^ b. Judiciai(VeraNavarroTg SCRA 408)!ffiAlv Dtzll :. Claims (bIn vs Haygooa os run siol'iui"i7 t/lyt.?r# I ffiffiT"rtgagev WAI\k tt^ Wl,'frrr. Properiy previou-slf taxed (vanishing deduction)

,r,ffi{i#P;;i! mt#, + ar i n tnnn,t' J'Ainhi,u'.toau tw .-- = Wtlt r**y,|l1,y1-'tt

wdeuitt ,

ry.

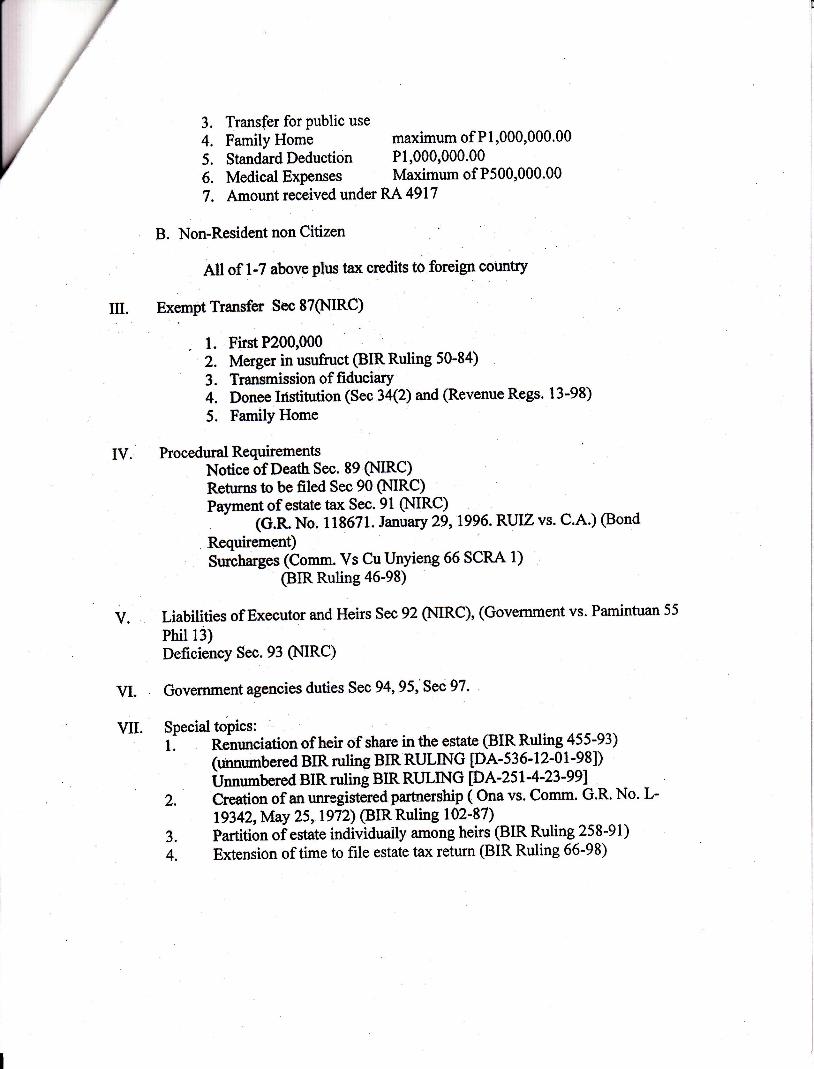

3. Transfer for Public use

4, Family Home maximum of P1,000,000'00

5. Standard Deduction P1,000,000.00

6. Medical Expenses Manimum of P500,000'00

7. Amount received under RA 4917

B. Non-Resident non Citizen

All of 1-7 above plus tax credits to foreign country

Exempt Transfer Sec 87(NIRC)

. l. FirstP200,0002. Merger in usufruct (BIRRuling 50-84)

3. Transmission of fiduciary4. Donee Ifstitution (Sec 34(2) and (Revenue Regs' 13-98)

5. FamilY Home

"*Sotlf#f,t ec. 8 e (N'RC)Returns to be filed Sec 90 (I'[IRC)Paymentof estate tax Sec.91 (NIRC)

(G.R.No. 118671. January 29,1996'RUIZ vs' C'A') (Bond

Requirement)Surcharges (Comm. Vs CuUnyieng 66 SCRA 1)

(BIRRuling 46-98)

Liabilities ofExecutor and Heirs Sec 92 (MRC), (Govemment vs. Pamintuan 55

Phil 13)Deficiency Sec. 93 (NIRC)

Government agencies duties Sec 94,95, Sec 97'

Special topics:l: Rengnciation of heir of share in the estate (BIR Ruling 455-93)

(unnumbered BIR ruling BIR RI'JLINQ PA-f 19-12-01-981)Unnrmbered BIR ruling BIR RITLING [DA-251 4-23'997

2. creation of an umegistired partneNhip ( ona vs. comm. G.R. No. L-

19342, May 25, 1972) (BIR Ruling 1 02-87)

3. Partition oiestate individuaily among heirs @IRRuling 258-91)

4. Extension of time to file estate tax return (BIR Ruling 66-98)

v.

vI.

VII.

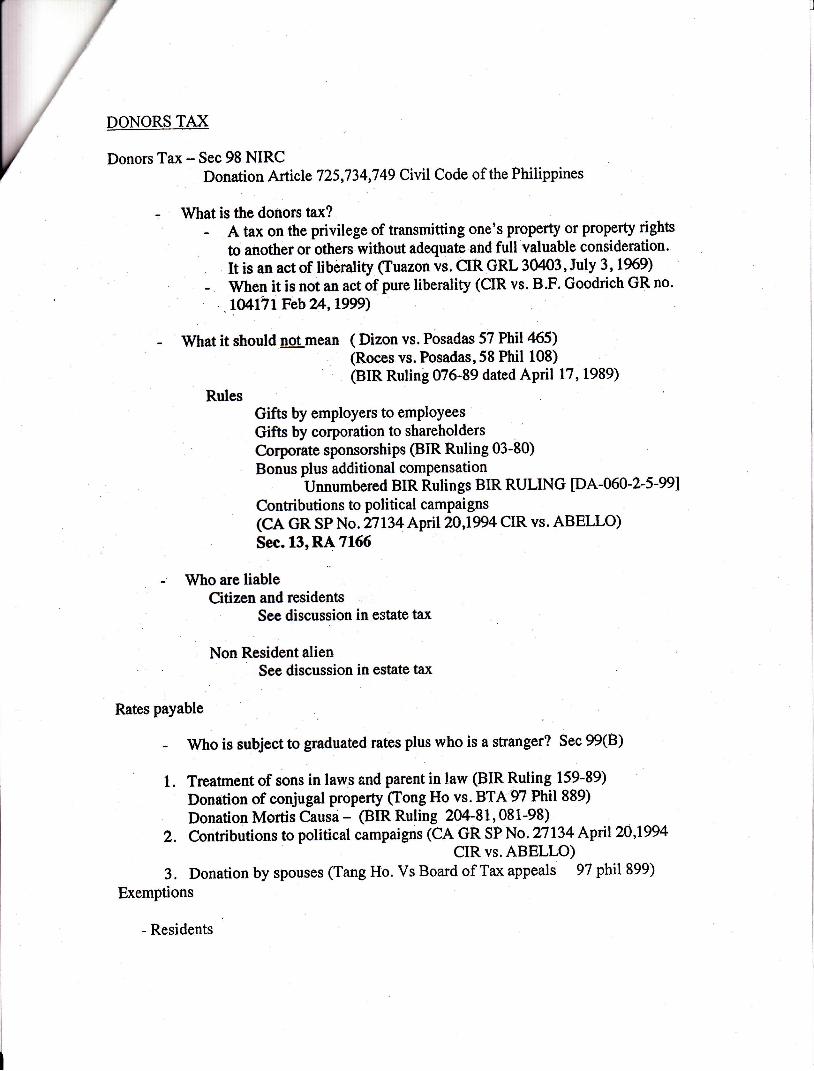

DONORS TAX

Donors Tax - Sec 98 NIRCDonation Article 725,734,749 Civil Code of the Philippines

: What is the donors tax?- .A tax on the privilege of transmitting one's property or property rights

to another or othels without adequate and full valuable consideration.

ft is an act of liberality (Iuazon vs. CIR GRL 30403, July 3, 1969)

When it is not an act of pure liberality (CIR vs. B.F. Goodrich GR no.

lmlit Feb v[,1999)

What it should aEt mean ( Dizon vs.-Posadas :1 llil {|)(Roces vs. Fosadas, 58 Phil 108)

Rules (BIR Rulinb O76-89 dated April 17, 1989)

Gifts by employers to emPloYees

Gifts by corporation to shareholders

Corporate sponsorships (BIR Ruling 03-80)

Bonus plus additional compensationUnnumbered BIR Rulings BIR RULING [DA-060-2-5-991

Contributions to political campai gns

(CA GR SP No. n$4April20,1994 CIR vs. ABELLO)Ss. 13, RA 7166

- Who are liableCitizen and residents

See discussion in estate tax

on Reffi$i::r"" in estate tax

Rates payable

- Who is subject to graduated rates plus who is a stranger? Sec 99(B)

1. Treatment of sons in laws and parent in law (BIR Ruling 159-89)

Donation of conjugal property (fong Ho vs. BTA'97 Phil 889)

Donation Mortis Causa - (BIR Ruling 204-8t,081-98)2. Contributions to political campaiens (CA GX:l

X#lS Apnt2},tee4

3. Donation by spouses (Tang Ho. Vs Board of Tax appeals 97 phil 899)

Exemptions

- Residents

,\

P100,000 Sec 99(A)Donations PromPter NumPtias

- only to their legiiimate, recognized natural, adopted children for the first

10,000.00 bdt not son or daughter in law (see above) .

Gifts to National Government (BIR Rulin 961-98,100-98 )(see special topics)

Gifts to educational and/or charitable organization (BIR Ruling 42-80, 101-

80)

- Non-residents not a citizen:

1. Gifts to Nationat Government (see above)

2. 'Gifts to educational/charitabte organization (see above)

- Credits for Donors Taxes Paid to foreign country

1. General2. Limitation

- Filing of Returns Sec 103 NIRCInformation required, when payable

- Definition for Estat0 plus Donors Tax Sec 1@ NIRC

SpecialTopics

-Ter*ination of trust (BIR Ruting 085-82)

Income tax exempt organization (BIR RulingfiT'8z)Dissolution of conjugal partnership @IR RulinS22U83)Homeowners Association to members (BIR Ruling440'93't

--* r.Repudiation of heir BIR Ruling (25 August 1977) compare with (BIR Ruling 455-

e3)Benefits of a Qualified Donee Institution :Sec 34 (fD(l) and (2XC) NIRC and

Sec 100 (AX3) NIRCTermination of co-ownership (BIR Ruling 145-98 October 9, 1998)

Partition of co-owned propetties (BIR Ruling DA 499-11-18-98 AtB' Yeno, )

RevocationofDonation BirRulingNo. 192-90

3.4.

![[Tax 2] Tax Remedies (cases)](https://img.pdfslide.us/doc/110x75/55cf946c550346f57ba1eda6/tax-2-tax-remedies-cases.jpg)