Embed Size (px)

Citation preview

&tate of Jowa

Iowa Administrative

Code Supplement

Biweekly

January 18, 1995

PHYLLIS BARRY ADMINISTRATIVE CoDE EDITOR

KATHLEEN BATES DEPUTY EDITOR

PUBLISHED BY THE

STATE OF IOWA UNDER AUTHORITY OF IOWA CODE SECTION 17 A.6

IAC Supp. PREFACE lAC 1/18/95

Since the Iowa Administrative Procedure Act [Iowa Code chapter 17 A] took effect July 1, 1975, over 100 agencies have complied with statutory requirements relating to rule making. The Code of Iowa is implemented by administrative rules contained in the "Iowa Administrative Code" which constitutes 18 loose-leaf volumes and one volume of Index.

Pursuant to Iowa Code section 17A.6, the Iowa Administrative Code [lAC] Supplement is published biweekly, beginning July 14, 1975.

The Supplement contains replacement pages to be inserted in the loose-leaf lAC according to instructions in the respective Supplement. Replacement pages incorporate amendments to existing rules or entirely new rules which have been adopted by the agency and filed with the Administrative Rules Coordinator as provided in Iowa Code sections 7.17, 17A.4 to 17A.6. [It is necessary to refer to the Iowa Administrative Bulletin* to determine the specific change.] The Supplement may also contain new or replacement pages for "General Information," "Style and Form," "Chapter 17 A" and other governing statutes, "Uniform Rules," "Table of Rules Implementing Statutes," and "Index."

When formal Objections to rules are filed by the Administrative Rules Review Committee, Governor or Attorney General, the text will be published with the rule to which the Objection applies.

Any Delay by the Administrative Rules Review Committee of the effective date of filed rules will also be published in the Supplement.

Each page in the Supplement contains a line at the top similar to the following:

lAC 1118/95 Revenue and Finance[701] Ch 39, p.21

This indicates a page in the lAC published on January 18, 1995. It relates to the Revenue and Finance Department, Agency No. 701, and is page 21 of Chapter 39.

If a rule appearing on this page is subsequently amended, it will be reprinted in amended form and the new page to be inserted will be included in a biweekly Supplement. The new page to be inserted will carry a later date, perhaps in this form:

lAC 2/1/95 Revenue and Finance[701] Ch 39, p.21

*Section 17A.6 has mandated that the "Iowa Administrative Bulletin" be published in pamphlet form. The Bulletin will contain Notices of Intended Action, Filed Rules, effective date Delays, Economic Impact Statements, and text of formal Objections to rules filed by the Administrative Rules Review Committee, Governor, or Attorney General.

In addition, the Bulletin shall contain all Proclamations and Executive Orders of the Governor which are general and permanent in nature, as well as other materials which are deemed fitting and proper by the Committee.

~

'.........'

\...I

\.-I

~

lAC Supp. 1118/95 Instructions

INSTRUCTIONS FOR

Updating Iowa Administrative Code with Biweekly Supplement

Page 1

NOTE: Please review the "Preface" for both the Iowa Administrative Code and Biweekly Supplement and follow carefully the updating instructions.

The boldface entries in the left-hand column of the updating instructions correspond to the tab sections in the lAC Binders.

Obsolete pages of lAC are listed in the column headed "Remove Old Pages." New and replacement pages in this Supplement are listed in the column headed "Insert New Pages." It is important to follow instructions in both columns.

Editor's phone: (515) 281-3355 or (515) 281-8157

UPDATING INSTRUCTIONS

AGRICULTURE AND LAND STEWARDSHIP DEPARTMENT[21]

Accountancy Examining Board[193A]

Environmental Protection Commission[567]

January 18, 1995, Biweekly Supplement

[Previous Supplement dated 114/95]

IOWA ADMINISTRATIVE CODE

Remove Old Pages*

Analysis, p. 3a, 4 Ch 11, p. 1 - Ch 12, p. 2 Ch 47, p. 7 - Ch 48, p. I Ch 85, p. 9- Ch 85, p. I2

Ch 3, p. 1, 2 Ch 3, p. 5 - Ch 4, p. 1

Analysis, p. 2a, 2b Ch 20, p. 3 - Ch 20, p. 6 Ch 22, p. 43, 44 Ch 37, p. I - Ch 38, p. 1

Insert New Pages

Analysis, p. 3a, 4 Ch 11, p. 1- Ch 12, p. 2 Ch 47, p. 7 - Ch 48, p. I Ch 85, p. 9- Ch 85, p. 12

Ch 3, p. 1- Ch 3, p. 2a Ch 3, p. 5 - Ch 4, p. I

Analysis, p. 2a, 2b Ch 20, p. 3 - Ch 20, p. 6 Ch 22, p. 43, 44 Ch 3I, p. 1 - Ch 38, p. 1

*It is recommended that "Old Pages" be retained indefinitely in a place of your choice. They may prove helpful in tracing the history of a rule.

Page2 Instructions lAC Supp. 1/18/95

Remove Old Pages* Insert New Pages

REVENUE AND FINANCE DEPARTMENT[701] Analysis, p. 9, 9a Analysis, p. 9, 9a

Ch 18, p. 1, 2 Ch 18, p. 1 - Ch 18, p. 2a Ch 18, p. 51 Ch 18, p. 51 Ch 34, p. 3 - Ch 37, p. 1 Ch 34, p. 3 - Ch 37, p. 1 Ch39, p.l7, 18 Ch 39, p. 17- Ch 39, p. 24

Index Volume "S" Tab, p. 13- 18 "S" Tab, p. 13- 18 "S" Tab, p. 23, 24 "S" Tab, p. 23- 24a "T" Tab, p. 55, 56 "T" Tab, p. 55 - 56a

TAB Insert divider tab numerically

*It is recommended that "Old Pages" be retained indefinitely in a place of your choice. They may prove helpful in tracing the history of a rule.

~

lAC 1118/95 Agriculture and Land Stewardship(21] Analysis, p.3a

CHAPTER 46 \..,I CROP PESTS

46.1(177A) Nursery stock 46.2(177 A) Hardy 46.3(177 A) Person 46.4(177A) Nursery growers 46.5(177A) Nursery 46.6(177 A) Nursery dealer 46. 7(177 A) Out-of-state nursery growers

and nursery dealers 46.8(177A) Nursery inspection 46.9(177A) Nursery dealer certificate 46.10(177A) Proper facilities

~....,/ 46.11(177A) Storage and display 46.12(177A) Nursery stock viability qualifi

cations 46.13(177A) Certificates 46.14(177A) Miscellaneous and service

inspections 46.15(177 A) Insect pests and diseases

CHAPTER 47 ORGANIC FOOD PRODUCTION

47.1(190B) Purpose 47.2(190B) Definitions and terms 47.3(190B) Standards 47 .4( 190B) Exceptions 47.5(190B) Treated seed, transplants and

propagating parts 47.6(190B) Records 47. 7(190B) Sworn statements 47.8(1908) Prohibitions 4 7. 9( 190B) Organic advisory committee

CHAPTER 48 PESTICIDE ADVISORY COMMITTEE

48.1 (206) Function 48.2(206) Staff

. 48.3(206) Advisors \w,J 48.4(206) Meetings

48.5(206) Open records 48.6(206) Budget 48. 7(206) Review of pesticide applicator

instructional course and examination

CHAPTER 49 Reserved

CHAPTER 50 IOWA FARMERS MARKET/WOMEN

INFANTS CHILDREN PROGRAM 50.1 ( 159) Authority and scope 50.2( 159) Severability 50.3(159) Program description and goals 50.4( 159) Def_initions

GENERAL PROVISIONS

50.5( 159) Administration and agreements 50.6(159) Distribution of benefits 50. 7( 159) Recipient responsibilities 50.8(159) Farmers market authorization

and priority 50.9(159) Vendor certification 50.10(159) Certified vendor oBligations 50.11(159) Certified vendor noncompliance

sanctions 50.12(159) Appeal 50.13( 159) Deadlines

CHAPTERS 51 to 57 Reserved

CHAPTER 58 NOXIOUS WEEDS

58.1 (317) Definition 58.2(317) Purple loosestrife 58.3(317) Records ·

CHAPTER 59 SORGHUM

59.1 ( 189) Sorghum-labeling and sales

Analysis, p.4 Agriculture and Land Stewardship[21] lAC ll/14/90

CHAPTER 60 POULTRY

60.1 ( 168) Egg-type chickens, meat-type chickens, turkeys, domestic waterfowl, domestic game birds and exhibition poultry.

60.2(168) License for dealers of baby chicks or domestic fowls

HEALTH REQUIREMENTS COVERING THE INTRASTATE MOVEMENT OF POULTRY

60.3(163) Turkeys

CHAPTER 61 DEAD ANIMAL DISPOSAL

61.1(163) Dead animal disposal-license 61.2(163) Animal disposal-persons defined 61.3(163) Disposing of dead animals by

-cooking 61.4(163) License fee 61.5(163) Certificate issuance 61.6(163) Filing certificate 61.7(163) License renewal 61.8 to 61.10 Reserved 61.11(163) Disposal plant plans 61.12(163) Disposal plant specifications 61.13 and 61.14 Reserved 61.15(163) Conveyances requirements 61.16(163) Disposal plant trucks 61.17(163) Disposal employees 61.18(163) Tarpaulins 61.19(163) Disposal vehicles-disinfection 61.20 to 61.22 Reserved 61.23(163) Rendering plant committee 61.24(163) Rendering plant-spraying 61.25(163) Penalty 61.26 and 61.27 Reserved 61.28(163) Anthrax 61.29(163) Anthrax-disposal 61.30(163) Hog-cholera-carcasses 61.31(163) Noncommunicable diseases-

carcasses 61.32(163) Carcass disposal-streams 61.33(163) Improper disposal

CHAPTER 62 REGISTRATION OF IOWA-FOALED

HORSES AND IOWA-WHELPED DOGS 62.1(99D) Definitions 62.2(99D) Iowa horse and dog breeders'

fund 62.3(99D) Forms 62.4(99D) Disciplinary procedures 62.5 to 62.9 Reserved

THOROUGHBRED DIVISION 62.10(99D) Iowa thoroughbred stallion

requirements 62.11 (99D) Notification requirements 62.12(99D) Stallion qualification and appli

cation procedure 62.l3(99D) Application information 62.14(99D) Breeding record-report of

mares bred 62.15(99D) Iowa-foaled horses and brood

mares 62.16(99D) Iowa-foaled horse status 62.17 to 62.19 Reserved

lAC 9/6/89, 6/23/93 Agriculture and Land Stewardship(21]

CHAPTER 11 APPLE GRADING

Ch 11, p.1

21-11.1(73GA,HF331) Federal standards adopted. "Iowa Standards for Grades of Apples" are hereby established by the adoption of "United States Standards for Grades of Apples" (effective September 1, 1964, as amended October 1, 1966, July 25, 1972, and March 25, 1976) with additions set forth in 21-11.2(73GA,HF331).

21-11.2(73GA,HF331) Premium utility grade apple. Premium utility grade shall be used only by Iowa apple growers on apples grown and packed in the state of Iowa. Apples qualifying for this grade must meet the following standards.

1. These apples shall meet the requirements of the U.S. No. 1 Hail Grade as provided in the United States Standards for Grades of Apples.

2. Chieftain and Empire varieties. These two varieties must comply with the "Color Requirement" in U.S. Standards, Section 51.305. The minimum requirement for Chieftain and Empire will be: U.S. Extra Fancy 66 percent, U.S. Fancy 33 percent, U.S. No. 1, 25 percent.

21-11.3(73GA,HF331) Inspection fees. Fees for each inspection request shall be formulated and assessed to cover all costs associated with the inspection of apples.

11.3(1) The fees shall be the sum of the following: a. The hourly wage rate received for inspectors. b. Mileage at the rate set by the state for government travel. c. Any per diem expenses properly associated with the inspection at the rate set for govern-

ment employees. d. A 6 percent fee assessed by USDA as cooperator in the inspection service. e. A 14.91 percent administrative overhead charge excluding the 6 percent assessed by USDA. 11.3(2) In cases where inspectors are required to work more than 40 hours per week, the

fee shall reflect 1.5 times the hourly wage rate received by the inspectors performing the inspection service plus all other due considerations as outlined in subrule 11.3(1).

These rules are intended to implement 1989 Iowa Acts, House File 331. [Filed emergency 8/18/89-published 9/6/89, effective 8/18/89]

Ch 12, p.1 Agriculture and Land Stewardship[21] lAC 1118/95

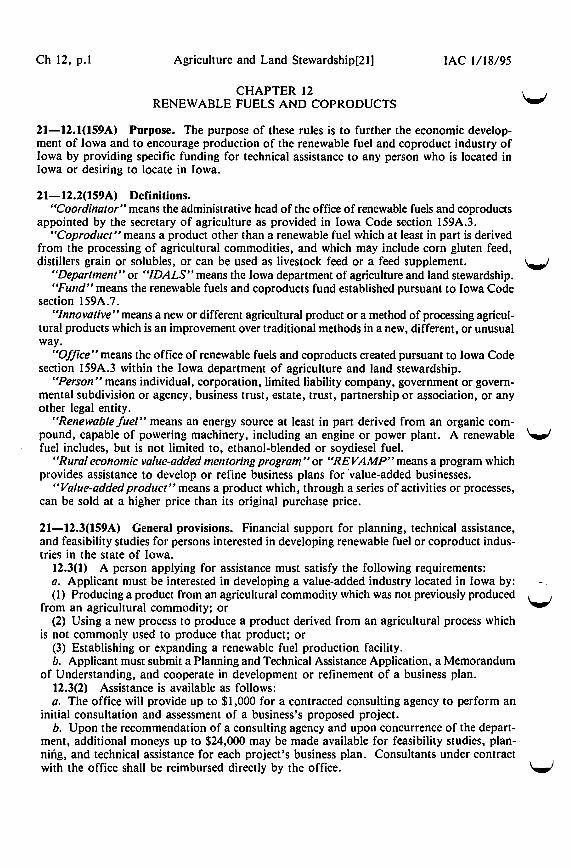

CHAPTER 12 RENEW ABLE FUELS AND COPRODUCTS

21-12.1(159A) Purpose. The purpose of these rules is to further the economic development of Iowa and to encourage production of the renewable fuel and coproduct industry of Iowa by providing specific funding for technical assistance to any person who is located in Iowa or desiring to locate in Iowa.

21-12.2(159A) Definitions. "Coordinator" means the administrative head of the office of renewable fuels and coproducts

appointed by the secretary of agriculture as provided in Iowa Code section 159A.3. ucoproduct" means a product other than a renewable fuel which at least in part is derived

from the processing of agricultural commodities, and which may include corn gluten feed, distillers grain or solubles, or can be used as livestock feed or a feed supplement.

"Department'' or "IDALS" means the Iowa department of agriculture and land stewardship. "Fund" means the renewable fuels and coproducts fund established pursuant to Iowa Code

section I 59 A. 7. "Innovative" means a new or different agricultural product or a method of processing agricul

tural products which is an improvement over traditional methods in a new, different, or unusual way.

"Office" means the office of renewable fuels and coproducts created pursuant to Iowa Code section 159A.3 within the Iowa department of agriculture and land stewardship.

"Person, means individual, corporation, limited liability company, government or governmental subdivision or agency, business trust, estate, trust, partnership or association, or any other legal entity.

"Renewable fuel" means an energy source at least in part derived from an organic compound, capable of powering machinery, including an engine or power plant. A renewable fuel includes, but is not limited to, ethanol-blended or soydiesel fuel.

"Rural ecohomic value-added mentoring program" or "REVAMP" means a program which provides assistance to develop or refine business plans for ·value-added businesses.

"Value-added product" means a product which, through a series of activities or processes, can be sold at a higher price than its original purchase price.

21-12.3(159A) General provisions. Financial support for planning, technical assistance, and feasibility studies for persons interested in developing renewable fuel or coproduct industries in the state of Iowa.

12.3(1) A person applying for assistance must satisfy the following requirements: a. Applicant must be interested in developing a value-added industry located in Iowa by: ( 1) Producing a product from an agricultural commodity which was not previously produced

from an agricultural commodity; or (2) Using a new process to produce a product derived from an agricultural process which

is not commonly used to produce that product; or (3) Establishing or expanding a renewable fuel production facility. b. Applicant must submit a Planning and Technical Assistance Application, a Memorandum

of Understanding, and cooperate in development or refinement of a business plan. 12.3(2) Assistance is available as follows: a. The office will provide up to $1,000 for a contracted consulting agency to perform an

initial consultation and assessment of a business's proposed project. b. Upon the recommendation of a consulting agency and upon concurrence of the depart

ment, additional moneys up to $24,000 may be made available for feasibility studies, planning, and technical assistance for each project's business plan. Consultants under contract with the office shall be reimbursed directly by the office.

lAC 1/18/95 Agriculture and Land Stewardship[21] Ch 12, p.2

c. Any and all additional costs shall be paid entirely by the applicant. 12.3(3) Applications shall be processed by the coordinator on a first-come, first-served

basis, based upon the receipt of documents by the office. Application materials may be obtained from Office of Renewable Fuels and Coproducts, Department of Agriculture and Land Stewardship, Wallace State Office Building, East 9th and Grand Avenue, Des Moines, Iowa 50319, (515)281-6936. Any person may resubmit an application with revisions as long as fees paid by the office remain under the maximum amount per project.

21-12.4(159A) Renewable fuels motor vehicle fuels decals. All motor vehicle fuel kept, offered or exposed for sale or sold at retail containing over 1 percent of a renewable fuel shall be identified with a decal located on front of the motor vehicle fuel pump and placed between 30 11 and 50 11 above the driveway level or in an alternative location approved by the department. The appearance of the decal shall conform to the following standards adopted by the renewable fuels and coproducts advisory committee:

12.4(1) The only two sizes of decals approved are the following: a. A design of 1.25" by 4 11

•

b. A design of 2 11 by 6 11•

12.4(2) All labels shall have the word "with" in letters a minimum of .1875 11 high, and the name of the renewable fuel in letters a minimum of .5 11 high.

12.4(3) The use of color, design and wording shall be approved by the renewable fuels and co products advisory committee. The coordinator may receive input from any party, including the weights and measures bureau of the department, in recommending the color, design, and wording. The advisory committee shall approve the color, design, and wording of the decal to promote the use of renewable fuels.

12.4(4) All black and white fuel pump stickers shall be replaced by approved colorful fuel pump decals effective July 1, 1995.

These rules are intended to implement Iowa Code section 159A.8. [Filed 6/4/93, Notice 3/31/93-published 6/23/93, effective 7/28/93*]

[Filed emergency 9/9/94-published 9/28/94, effective 9/9/94] [Filed emergency 12/30/94 after Notice 9/28/94-published l/18/95, effective 12/30/94]

CHAPTERS 13 and 14 Reserved

*Effective date of 21-Chapter 12 delayed seventy days by the Administrative Rules Review Committee at its meeting held July 8, 1993; delay lifted by this Committee on 9/IS/93.

lAC 1/18/95 Agriculture and Land Stewardship[21] Ch 47, p.7

is organic, organically grown, or by a derivative of the word "organic,'' unless the product, including all of its ingredients, conforms to the requirements of Iowa Code chapter 1908 and Iowa Administrative Code 21-Chapter 47.

47 .8(2) Food that contains one or more organic ingredients may contain an information _statement on the label, such as: "Contains organic rye flour" in letters not to exceed one-half the height of the letters used in the product identity. The word "organic" also must precede the name of each organic ingredient identified in the list of ingredients.

21-47.9(1908) Organic advisory committee. 47 .9(1) Membership. The advisory committee shall have nine members to be appointed

by the secretary of agriculture. Membership shall consist of the following: a. One representative of the Iowa department of agriculture and land stewardship. b. One representative of Iowa state university extension service who is a specialist in organic

or sustainable agriculture. c. Three producers of organic products including grains, fruits, vegetables, livestock or

textiles. d. Three handlers of organic products including processors, distributors or retailers. e. One consumer representing the general interests of the organic industry in Iowa. 47 .9(2) Function. The committee shall provide advice to the secretary of agriculture regard

ing organic production regulations, both state and federal, and other matters of concern to the organic industry as determined by the committee.

47 .9(3) Administrative procedures. The committee shall establish administrative procedures and shall elect officers to terms established by the committee. All members of the committee shall serve at the pleasure of the secretary.

47.9(4) Compensation. Members of the advisory committee shall be reimbursed for actual and necessary expenses incurred by them in the discharge of their official duties.

47 .9(5) Advisors. The organic advisory committee may solicit input from advisors without restriction as determined by the committee.

47 .9(6) Staff. Staff assistance is provided through the department of agriculture and land stewardship as designated by the secretary of agriculture.

47 .9(7) Open records. All public records of the committee are available for public inspection during business hours. Requests to obtain records may be made by mail, telephone or in person to the secretary's office, department of agriculture and land stewardship. Records requiring more than five copies may be obtained upon payment of the actual cost for copying.

These rules are intended to implement Iowa Code chapter 1908. [Filed 11/1/89, Notice 8/23/89-published 11/29/89, effective 1/3/90] [Filed 3/25/91, Notice l/23/91-published 4/17/91, effective 5/22/91]

[Filed 12/21/94, Notice 10/26/94-published 1/18/95, effective 2/22/95]

Ch 48, p.1 Agriculture and Land Stewardship[21] lAC 5/11194

CHAPTER 48 PESTICIDE ADVISORY COMMITTEE

21-48.1(206) Function. The pesticide advisory committee was created by Iowa Code chapter 206 and is charged with the responsibility of assisting the secretary in obtaining scientific data and coordinating agricultural chemical regulatory, enforcement, research and educational functions of the state.

48.1(1) Organization and operation location. The pesticide advisory committee is located within the Department of Agriculture and Land Stewardship, Henry A. Wallace Building, Des Moines, Iowa 50319. The department's office hours are from 8 a.m. to 4:30p.m., Monday through Friday.

48.1(2) Membership. The pesticide advisory committee consists of nine members as set forth in Iowa Code section 206.23.

21-48.2(206) Staff. Staff assistance is provided through the department of agriculture and \,) land stewardship as designated by the secretary of agriculture.

21-48.3(206). Advisors. The pesticide advisory committee may solicit input from advisors without restriction as determined by the committee.

21-48.4(206) Meetings. The pesticide advisory committee meets annually to elect a chairperson but may meet at other times as directed by the secretary or designee. Meetings may be called by the chairperson or on request by four members of the committee.

All committee meetings shall comply with Iowa Code chapter 21. A quorum of two-thirds of the committee members must be present to transact business. Action by the committee requires a vote of a majority of those on the committee. Meetings follow Robert's Rules of Order. Minutes of each meeting are available from the Secretary of Agriculture, Department of Agriculture and Land Stewardship, Henry A. Wallace Building, Des Moines, Iowa 50319.

21-48.5(206) Open records. All public records of the committee are available for public inspection during business hours. Requests to obtain records may be made by mail, by telephone or in person to the secretary's office, department of agriculture and land stewardship. Minutes of the committee meetings may be obtained without charge. Other records requiring more than five copies may be obtained upon payment of the actual cost for copying.

21-48.6(206) Budget. The pesticide advisory committee shall submit an annual budget to the secretary of agriculture.

21-48.7(206) Review of pesticide applicator instructional course and examination. The pes-ticide advisory committee shall meet at least once annually to review pesticide applicator cer- '....,; tification instructional courses and examinations. The purpose of the annual review is to discuss topics of current concern that may be incorporated in pesticide applicator instructional courses and appropriate examinations. The committee shall review and evaluate the various instruc-tional programs recently conducted and recommend options to increase overall effectiveness.

These rules are intended to implement Iowa Code section 206.23. [Filed 11/1189, Notice 9/20/89-published 11/29/89, effective 113/90]

[Filed emergency 1/10/90-published 2/7/90, effective 1/10/90] [Filed emergency 10/8/93-published 10/27/93, effective 10/8/93]

[Filed 4/20/94, Notice 10/27/93-published 5/11194, effective 6/15/94]

CHAPTER 49 Reserved

lAC 7/27/88 Agriculture and Land Stewardship[21] Ch 85, p.9

21-85.45(215) LP-gas meter registration. The location of all LP-gas liquid meters in retail trade shall be listed, by the owner, with the department of agriculture and land stewardship.

This rule is intended to implement Iowa Code section 215.20.

21-85.46(215) Reporting new LP-gas meters. Upon putting a new or used meter into service in the state of Iowa, the user shall report to the weights and measures division.

This rule is intended to implement Iowa Code section 215.20.

21-85.47 Rescinded, effective 11/27/85.

21-85.48(214A,215) Advertisement of the price of liquid petroleum products for retail use. 85.48(1) Nothing in this rule shall be deemed to require that the price per gallon or liter

or any grade or kind of liquid petroleum product sold on the station premises be displayed or advertised except on the liquid petroleum metering distribution pumps.

85.48(2) Petroleum product retailers, if they elect to advertise the unit price of their petroleum products at or near the curb, storefront or billboard, shall display the price per gallon or liter. The advertised price shall equal the computer price settings shown on the metering pump.

85.48(3) Notwithstanding the provisions of subrule 85.48(2), cash only prices may be posted by the petroleum marketer on the following basis:

a. Cash only prices must be disclosed on the posted sign as "cash only" or similar unequivocal wording in lettering 3 " high and ~ " in stroke when the whole number price being shown is 36 inches or less in height; or in lettering, at least 6" high and YJ" in stroke when the whole number price is more than 36 inches in height.

b. Cash prices posted or advertised must be available to all customers, regardless of type of service (e.g., full service or self-service); or grade of product (e.g., regular, unleaded, gasohol and diesel).

c. Cash and credit prices or discounts must be prominently displayed on the dispenser. d. A chart showing applicable cash discounts expressed in terms of both the computed and

posted price shall be available to the customer on the service station premises. 85.48(4) On all outside display signs, the whole number shall not be less than 6" in height

and not less than 3/a " in stroke, and any fraction shall be at least one-third of the size of the whole number in both height and width.

85.48(5) The price must be complete, including taxes without any missing numerals or fractions in the price.

85.48(6) Price advertising signs shall identify the type of product (e.g., regular, unleaded, gasohol and diesel), in lettering at least 3" high and~" in stroke when the whole number price being shown is 36 inches or less in height, or in lettering at least 6" high and YJ " in stroke when the whole number price is more than 36 inches in height.

85.48(7) A price advertising sign shall display, if in liters and may display if in gallons, the unit measure at least in letters of 3" minimum.

85.48(8) Directional or informational signs for customer location of the type of service or product advertised shall be clearly and prominently displayed on the station premises in a manner not misleading to the public.

85.48(9) The advertising of other commodities or services offered for sale by petroleum retailers in s~ch a way as to mislead the public with regard to petroleum product pricing shall be prohibited.

Ch 85, p.IO Agriculture and Land Stewardship[21] lAC 1/18/95

85.48(10) Weights and measures motor vehicle fuels decals. All motor vehicle fuel kept, offered or exposed for sale or sold at retail containing over 1 percent of a renewable fuel shall be identified with a decal located on front of the motor vehicle fuel pump and placed between 30 11 and 50 11 above the driveway level or in an alternative location approved by the department. The appearance of the decal shall conform to the following standards adopted by the renewable fuels and coproducts advisory committee:

a. The only two sizes of decals approved are the following: (1) A design of 1.25" by 4". (2) A design of 2" by 6 ". b. All labels shall have the word "with" in letters a minimum of .1875" high, and the name

of the renewable fuel in letters a minimum of .5" high. c. The use of color, design and wording shall be approved by the renewable fuels and co

products advisory committee. The coordinator may receive input from any party including the weights and measures bureau of the department in recommending the color, design, and wording. The advisory committee shall approve the color, design, and wording to promote the use of renewable fuels.

d. All black a uel pump stickers shall be replaced by approved colorful fuel pump deca ecuv ~fitiacyl) 1995.

85.48(11) At· · e icle fuel kept, offered or exposed for sale at retail containing over 1 percent methyl tertiary butyl ether shall be identified as "Contains MTBE" or "MTBE blend" in black lettering no less than V2 11 in height, Y. 11 in stroke, with directly below "METHYL TERTIARY BUTYL ETHER" in black lettering no less than 20-point type size to be placed 30 11 to 40" above driveway level on the front of the (>Umps.

Additional wording or statements may be allowed upon submission to and approval by the department. Approval shall be based upon factual information or scientific data provided by the applicant and a determination that the wording is not misleading to consumers.

85.48(12) Any wholesale dealer, retail dealer, pipeline, refinery, barge or bulk plant in this state that sells or holds for sale natural gasoline raffinate below the minimum 87 octane (R + M)/2 requirement of Iowa Code section 214A.2 that is intended or is to be blended with an oxygenate octane enhancer or higher gasoline components shall register with the department.

85.48(13) All retail shipments of blended natural gasoline/raffinate must be accompanied by a certificate showing the true standards and tests of such blended motor fuel that was obtained by the methods referred to in Iowa Code section 214A.2. The certificate must accompany the shipping document or bill of lading before such blended fuel can be received or unloaded.

85.48(14) Octane rating of fuel offered for sale shall be posted on the pump in a conspicuous place.

85.48(15) Any gasoline labeled as "leaded" shall be produced with the use of any lead additive or contain more than 0.05 grams of lead per gallon or more than 0.005 grams of phosphorus per gallon. As used in this subrule, "lead additive" means any substance containing lead or lead compounds.

This rule is intended to implement Iowa Code sections 214A.3, 214A.16 and 215.18.

21-85.49(214A,215) Gallonage determination for retail sales. The method of determining gallonage on gasoline or diesel motor vehicle fuel for retail sale shall be on a gross volume basis. Temperature correction or any deliberate methods of heating shall be prohibited.

This rule is intended to implement Iowa Code sections 214A.3 and 215.18.

21-85.50 and 85.51 Reserved.

lAC 7/27/88 Agriculture and Land Stewardship[21] Ch 85, p.ll

MOISTURE-MEASURING DEVICES 21-85.52(215A) Testing devices. All moisture-measuring devices will be tested against a measuring device which will be furnished by the department and all moisture-measuring devices wiU be inspected to determine whether they are in proper operational condition and supplied with the proper accessories.

This rule is intended to implement Iowa Code section 215A.2.

21-85.53(215A) Rejecting devices. Moisture-measuring devices may be rejected for any of the following reasons:

85.53(1) The moisture-measuring device tested is found to be out of tolerance with the measuring device used by the department by one of the inspectors so assigned by more than one-half of 1 percent on grain under 20 percent moisture content.

85.53(2) The person does not have available the latest charts for type of device being used. 85.53(3) The person does not have available the proper scale or scales and thermometers

for use with the type of device being used. 85.53(4) The moisture-measuring device is not free from excessive dirt, debris, cracked

glass or is not kept in good operational condition at all times. This rule is intended to implement Iowa Code section 215A.6.

21-85.54(215,215A) Specifications and standards for moisture-measuring devices. The specifications and tolerances for moisture-measuring devices are those established by the United States Department of Agriculture as of November 15, 1971, in chapter XII of GR instruction 916-6, equipment manual, used by the federal grain inspection service; and those recommended by National Bureau of Standards and published in National Bureau of Standards Handbook 44 as of July 1, 1985.

This rule is intended to implement Iowa Code section 215A.3.

21-85.55 Renumbered as 55.28(215), lAC 12/4/85.

21-85.56 Renumbered as 55.29(215), lAC 12/4/85.

21-85.57(215)* Testing high-moisture grain. When testing high-moisture grain the operator of a moisture-measuring device shall use the following procedure: Test each sample six times adding the six measurements thus obtained and dividing the total by six to obtain an average which shall be deemed to be the moisture content of such sample.

This rule is intended to implement Iowa Code section 215A.7.

21-85.58 to 85.62 Reserved.

HOPPER SCALES 21-85.63(215) Hopper scales. A "hopper scale" is a scale designed for weighing bulk commodities whose load-receiving element is a tank, box, or hopper mounted on a weighing element; and includes automatic hopper scales, grain hopper scales, and construction material hopper scales.

85.63(1) Installation. A hopper scale used for commercial purposes shall be so located, or such facilities for normal access thereto shall be so provided that the test weights of the weights and measures official, in the denominations customarily provided, and in the amount deemed necessary by the weights and measures official for the proper testing of the scale, may readily be brought to the scale by customary means; otherwise it shall be the responsibility

• Objection, see ftlcd rule published in lAC Supp. S/3176, 6/14/76 (Prior to S/3178, ru!c 30-SS.46)

Ch 85, p.I2 Agriculture and Land Stewardship[21] lAC 1/18/95

of the scale owner or operator to supply such special facilities, as required by the weights and ~ J

measures official. The hopper scale shall have extended angle iron with hooks 14 inches from ~ edge to hopper, in all four corners, to allow the inspector to hook his chain and binder to 500# weight (or 1000# weight) for testing.

85.63(2) Method of hopper scale testing. The method to be used in testing the scale for weighing accuracy shall be by the suspension of standard test weights at each comer of the weighbridge, suspended from a point as near as possible over the center of the main bearing. A suitable permanent device to which the suspension equipment may be connected shall be properly located and placed on each comer of the weighbridge. There is to be no obstruction, such as machinery, spouting or insufficient wall clearance, etc., that will interfere with the free suspension of the weights.

85.63(3) Approved by department. Newly installed hopper scales must be approved by the department; this approval shall be based upon blueprints and specifications submitted for this purpose. ~

This rule is intended to implement Iowa Code sections 215.10 and 215.18. [IDR 1952, p.iO, 1954, 1958, 1962]

[Amended 11/18/63, 9/14/65, 12/14/65, 11/21166, 11/15/67, 8/30/68, 9/10/69, 9/22/69, 9/15/70, 12/17/71, 3/15/73, 7/10/74]

[Filed 4/13/76, Notice 2/9/76--published 5/3/76, effective 6/7 /76] [Filed 10/14/76, Notice 9/8/76--published 11/3/76, effective 12/9/76] [Filed 3/18/77, Notice 2/9/77-published 4/6/77, effective 5/12/77] [Filed 9/2/77, Notice 7/13/77-published 9/21177, effective 111178]

[Filed 3/2/78, Notice 12/28/77-published 3/22/78, effective 4/26/78] [Filed emergency 7/13/79-published 8/8/79, effective 7/16/79]

[Filed 11/20/81, Notice 10/14/81-published 12/9/81, effective 1113/82] [Filed 517/82, Notice 3/31182-published 5/26/82, effective 6/30/82] [Filed 6/4/82, Notice 4/28/82-published 6/23/82, effective 7/28/82] ~

[Filed emergency 2/15/83-published 3/2/83, effective 2/15/83] [Filed 1 I 13/84, Notice 12/7 /83-published 2/1/84, effective 3/7 /84]

[Filed 10/4/85, Notice 8/28/85-published 10/23/85, effective 11/27/85] [Filed 1111185, Notice 9/25/85-published 11120/85, effective 12/25/85] [Filed 1/15/86, Notice 12/4/85-published 2/12/86, effective 3/19/86]

[Filed emergency 7/8/88 after Notice of 6/1/88-published 7/27/88, effective 7/8/88] [Filed emergency 11127/89-published 12/13/89, effective 11/27/89] [Filed 4113/90, Notice 12/13/89-published 5/2/90, effective 6/6/90]

[Filed 12/24/90, Notice 7/11/90-published 1123/91, effective 2/27/91) [Filed emergency 9/9/94-published 9/28/94, effective 9/9/94]

[Filed emergency 12/30/94 after Notice 9/28/94-published 1118/95, effective 12/30/94]

CHAPTERS 86 to 89 Reserved

'~

lAC 1118/95 Accountancy[193A] Ch 3, p.l

CHAPTER 3 CERTIFICATE OF CERTIFIED PUBLIC ACCOUNT ANT

[Prior to 7/13188, see Accountancy, Board of [10))

193A-3.1(542C) Colleges or universities recognized by the board. Iowa Code sections 542C.5 and 542C.20, in providing for educational qualifications for a certificate as a certified public accountant or a permit to practice public accounting, refer to colleges or universities "recognized by the board.'' For such purpose, the board recognizes the state-supported educational institutions that have been granted collegiate status by this state, the American Assembly of Collegiate Schools of Business, and the regional accrediting bodies listed in the current publication of Accredited Institutions of Post Secondary Education which listing is made a part of these rules by reference.

This rule is intended to implement Iowa Code section 542C.5.

193A-3.2(542C) An accounting concentration. 3.2(1) On or before December 31,2000, Iowa Code sections 542C.5 and 542C.20, in provid

ing for educational requirements for a certificate as a certified public accountant, refer to "substantially the equivalent of an accounting concentration, including related courses in other areas of business administration.'' This particular requirement will be deemed to have been met, for example, in the case of:

a. A certification by a school recognized by the board as offering an accounting major that a candidate's nonaccounting degree, supplemented by additional courses, is the equivalent of education received by its accounting majors, or

b. A baccalaureate degree obtained from a college or university recognized by the board with a nonaccounting major if it is appropriately supplemented by courses in accounting and related business subjects from the same or other similarly qualified institutions.

In any case, whether the candidate has a nonaccounting degree supplemented by additional courses or has a degree with a major in accounting, the candidate shall have satisfactorily completed 48 semester hours, or the equivalent thereof, in accounting and related subjects. Not less than 24 hours shall be in accounting courses (of which at least one course shall be in auditing) and the remainder may be in the subjects of economics, statistics, business law, finance, business management, marketing, business communication, or other businessrelated subjects.

3.2(2) On or after January 1, 2001, candidates will be deemed to have met the educational requirement if, as part of the 150 semester hours of education, they have met one of the following four conditions. With each of the conditions listed below, the minimum accounting hours do not include elementary accounting (principles of accounting), business law, internships or life experience.

a. Earned a graduate degree with a concentration in accounting from a program that is accredited in accounting by an accrediting agency recognized by the board.

b. Earned a graduate degree in business from a program that is accredited in business by an accrediting agency recognized by the board and completed at least 24 semester hours in accounting including courses covering the subjects of financial accounting, auditing, taxation, and management accounting.

c. Earned a baccalaureate degree in business or accounting from a program that is accredited in business by an accrediting agency recognized by the board and completed at least 24 semester hours in accounting courses covering the subjects of financial accounting, auditing, taxation, and management accounting.

d. Earned a baccalaureate or higher degree and completed the following hours from an accredited institution recognized by the board:

Ch 3, p.2 Accountancy[ 193A] lAC 1118/95

(1) At least 24 semester hours in accounting courses covering the subjects of financial accounting, auditing, taxation, and management accounting, and

(2) At least 24 additional semester hours in business-related courses, not including internships or life experience. Quarter hours will be accepted in lieu of semester hours at a 3:2 ratio; that is, three quarter hours is equivalent to two semester hours.

3.2(3) The board will consider correspondence study, and study in other schools not meeting the above requirements, on an individual basis as to candidates who are nonaccounting majors and majors needing supplemental credits in accounting and related subjects, if the candidate can provide evidence that such study would be acceptable for credit by a college or university recognized by the board; provided, however, that at least 18 of the required hours in accounting and at least 16 of the required hours in related subjects must be obtained in a college or university recognized by the board.

3.2(4) The applicant's claim to college or university credits must be confirmed by an official transcript of credit issued by the institution in question. The applicant shall be responsible for having such transcripts sent to the board at the time of making application. The applicant shall also be responsible for having any institution not listed under rule 193A-3.1(542C) furnish the board evidence that it meets the accreditation requirements of the board. In addition, the applicant is responsible for all material being in possession of the board by the deadline for filing applications. Otherwise, the application shall be considered incomplete and shall be disapproved by the board.

3.2(5) Graduates of foreign colleges or universities shall have their education evaluated by a foreign credentials evaluation advisory service specified by the board.

193A-3.3(542C) Acceptable experience. 3.3(1) With respect to the three years' continuous experience required by Iowa Code sec

tion 542C.5, subsection 2, prior to December 31, 2000, the board will consider any three-year period of service as continuous even though part of the three-year experience is immediately prior to service in any branch of the armed forces of the United States and the balance of the experience is immediately after such armed forces service. The three years' continuous experience does not need to be for the same employer.

3.3(2) Credit may be allowed for part-time experience at the discretion of the board. 3.3(3) The required experience shall have been in public practice and a significant part

of the experience shall have been directed toward the expression of an opinion on financial statements. Applicants are expected to obtain for the board a statement from each of the applicant's employers supporting the required experience beginning with the most recent. This statement shall be attested to by a partner or shareholder of each employer or sole practitioner employer and shall describe the extent of the applicant's experience in the following areas:

a. Experience in applying a variety of auditing procedures and techniques to the usual and customary financial transactions recorded in accounting records.

b. Experience in the preparation of audit working papers covering the examination of the accounts usually found in accounting records.

c. Experience in the planning of the program of audit work including the selection of the procedures to be followed.

d. Experience in the preparation of written explanations and comments on the findings of the examinations and on the content of the accounting records.

e. Experience in the preparation and analysis of financial statements together with explanations and notes thereon.

The applicant is responsible for such material being in the possession of the board by the deadline for filing applications. Otherwise the application shall be considered incomplete and shall be disapproved by the board.

~

\.w)

'.,)

~

~

lAC 1/5/94, 1/18/95 Accountancy[ 193A] Ch 3, p.2a

193A-3.4(542C) Examination applications. 3.4(1) Individuals desiring to take the examination for qualification as a certified public

accountant should apply on the form provided by the board's administrator. Different forms will be provided for original examinations and reexaminations.

3.4(2) To be eligible to take the examination the applicant shall have fulfilled the requirements of Iowa Code section 542C.5(1) at the date the examination is held. The applicant shall also have fulfilled the requirements of section 542C.5(2) unless the applicant is specifically exempted from doing so under other provisions contained in section 542C.5. Reexamination applicants will be considered to have fulfilled these requirements thereafter.

3.4(3) A nonrefundable proctoring fee shall be collected from candidates who wish to be proctored in Iowa.

193A-3.5(542C) Deadline for filing applications. Examinations are ordinarily held in May and November of each year, and all applications to take the examinations must be filed during the period January I to the last day of February for the next May examination and during the period of July 1 to August 31 for the next November examination. Applications will not be considered as filed until they are complete in all respects. Applications shall be deemed filed on the date received by the board, or if mailed, the date postmarked (but not metered), whichever is earlier. Late applications will not be accepted.

This rule is intended to implement Iowa Code section 542C.5.

193A-3.6(542C) Content and grading of the examination. 3.6{1) The board may make use of the uniform certified public accountant's examination

prepared by the American Institute of Certified Public Accountants under a plan of cooperation with the boards of all states and territories of the United States.

rl -·

lAC 1/18/95 Accountancy[193A] Ch 3, p.5

193A-3.11(542C) Refunding of examination fees. Examination fees shall not be refunded ~except as follows:

1. An applicant who is admitted but fails to attend the examination shall be rebated 50 percent of the prescribed fee provided notification that the applicant will not be present is received by the board 30 calendar days prior to the beginning of the examination.

2. Fifty percent of the prescribed fee shall be returned to applicants whose application has been submitted and examined but who are found not qualified to take the examination.

3. In hardship cases, when the applicant for the examination is prevented from attending for such reasons as unexpected illness, death in the family, or call to active military service, 50 percent of the fee may be returned provided that under the circumstances it was not possible for the applicant to notify the board at least 30 calendar days prior to the beginning of the examination that the applicant could not be present.

, 193A-3.12(542C) Review of examination papers. Examination papers may be reviewed by :.....,.) an unsuccessful candidate only after grading has been reviewed and passed upon by the board,

and then only by the candidate and one other person whom the candidate may invite to review them, and only in the offices of the board. This rule comprehends review by a candidate of the candidate's own papers only, for educational benefit, and is not to be construed as providing a basis for seeking regrading. The board shall not regrade papers.

193A-3.13(542C) Destroying examination papers. The board may, in its discretion, destroy examination papers within six months after the examination pursuant to procedures under Iowa Code chapter 304.

193A-3.14(542C) Obtaining the certificate. Candidates who successfully pass the examination shall make application for their certificate on a form that may be obtained from the

......,_,; board office.

193A-3.15(542C) Obtaining a certificate by reciprocity. 3.15(1) A person desiring a certificate as a certified public accountant in this state on the

basis of holding a certificate in another state (or other acceptable qualification in another country) must apply upon a form that may be obtained from the board office. A nonrefundable application fee will be charged each applicant.

3.15(2) In the case of an application for a certificate as a certified public accountant in this state by the holder of a certificate, license, or degree in a foreign country as referred to in the last paragraph of Iowa Code section 542C.5, the burden is on the applicant to furnish information satisfactory to the board that the applicant's qualification in such other country is in full force and effect and was equivalent to the qualifications required in this state for the granting of a certificate as a certified public accountant.

~ 3.15(3) If the applicant has been in continous practice for at least seven years immediately prior to making application for an Iowa CPA certificate, the board shall consider the applicant to possess the equivalent of the qualifications under Iowa Code section 542C.5(2).

3.15(4) The board shall not waive the requirements of Iowa Code section 542C.5(1) unless the state or foreign country of which the applicant is a resident has a policy of issuing reciprocal certificates to applicants who are residents of Iowa.

These rules are intended to implement Iowa Code chapter 542C. [Filed and effective September 22, 1975]

[Filed 9/27/78, Notice 8/23/78-published 10/18/78, effective 11/22178] [Filed 6/22/88, Notice 3/9/88-published 7/13/88, effective 8/17/88] [Filed 8/ 1191, Notice 51 15/91-published 8/21191, effective 9/25/91)

[Filed 12/30/92, Notice 10/28/92-published 1120/93, effective 2/24/93] ~ [Filed 12/17/93, Notice 10/13/93-published 115/94, effective 2/9/94]

[Filed 12/30/94, Notice 10/12/94-published 1/18/95, effective 2/22/95]

Ch 4, p.1 Accountancy[ 193A] lAC 1/5/94

CHAPTER 4 LICENSE OF ACCOUNTING PRACTITIONER

[Prior to 7/13/88, see Acwuntancy, Board of (10))

193A-4.1(542C) Application for license. Rescinded lAB 8/21191, effective 9/25/91.

193A-4.2(542C) Definition of "principal." Rescinded lAB 8/21191, effective 9/25/91.

193A-4.3(542C) Acceptable experience for license. Rescinded lAB 8/21191, effective 9/25/91.

193A-4.4(542C) Examination application. 4.4(1) Individuals desiring to take the examination to qualify for a license as an account

ing practitioner shall apply on a form that may be obtained from the board office. Different forms will be provided for original examinations and reexaminations.

4.4(2) To be eligible to take the examination, the applicant must meet the requirements of Iowa Code sections 542C.7(1), and 542C.8(1), 542C.8(2), 542C.8(3) or 542C.8(4) at the time of filing the application.

193A-4.5(542C) Deadline for filing applications. Examinations are ordinarily held in May and December of each year and all applications to take the examinations must be filed during the period January 1 through the last day of February for the next May examination, and during the period July 1 to September 30 for the next December examination. Applications will not be considered as filed until they are complete in all respects. Applications shall be deemed filed on the date received by the board, or if mailed, the date postmarked (but not metered), whichever is earlier. Late applications will not be accepted.

This rule is intended to implement Iowa Code section 542C.8.

193A-4.6(542C) Acceptable experience to take examination. The experience requirements of Iowa Code sections 542C.8(1) and 542C.8(2) shall be continuous but not necessarily for one employer. No credit shall be given for part-time experience.

193A-4. 7(542C) Major in accounting. In determining whether the requirement in Iowa Code section 542C.8(3) as to a "major in accounting" has been met, the board will follow the rule associated with Iowa Code section 542C.5 relating to the requirement of a "concentration in accounting."

193A-4.8(542C) Transcripts required. The applicant's claim to college, university, business school, or correspondence school credit must be confirmed by an official transcript of credit issued by the institution in question. The applicant shall be responsible for having such transcripts sent to the board at the time of making application. The applicant shall also be responsible for having the institution furnish the board evidence that it meets the accreditation requirements of the board. The applicant is also responsible for all such material being in possession of the board by the deadline for filing the application, otherwise the application shall be considered incomplete and disapproved by the board.

193A-4.9(542C) Admittance prior to completing educational requirements. The board may admit to the examination described in Iowa Code section 542C.11 any candidate who will complete the educational requirements set for~h in section 542C.8(3) within 120 days immediately following the date of the examination. However, the board shall not report the results of the examination until the candidate has met the educational requirements or the experience requirements of section 542C.8(1) or 542C.8(2).

lAC 11/9/94 Environmental Protection[567] Analysis, p.2a

\._,) 22.136(455B) Acid rain permit issuance CHAPTER24 procedures- EXCESS EMISSION completeness 24.1(4558) Excess emission reporting

22.137(455B) Acid rain permit issuance 24.2(4558) Maintenance and repair procedures-statement requirements of basis

22.138(455B) Issuance of acid rain permits CHAPTER 25 22.139(4558) Acid rain permit appeal MEASUREMENT OF EMISSIOI\ ~

procedures 25.1(4558) Testing and sampling of new 22.140(455B) Permit revisions-general and existing equipment 22.141(4558) Permit modifications 25.2(4558) Continuous emission 22.142( 4558) Fast-track modifications monitoring under the acid 22.143(4558) Administrative permit rain program

'.,.,) amendment 22.144(455B) Automatic permit CHAPTER26

amendment PREVENTION OF AIR POLLUTION 22.145(455B) Permit reopenings EMERGENCY EPISODES 22.146(4558) Compliance certification- 26.1(4558) General

annual report 26.2(4558) Episode criteria 22.147(4558) Compliance certification- 26.3(4558) Preplanned abatement

units with repowering strategies extensions plans 26.4(4558) Actions taken during episodes

22.148 to 22.199 Reserved 22.200(4558) Definitions for voluntary CHAPTER27

operating permits CERTIFICATE OF ACCEPTANCE 22.201(4558) Eligibility for voluntary 27.1(4558) General

\..,./ operating permits 27.2(4558) Certificate of acceptance 22.202(4558) Requirement to have a 27.3(4558) Ordinance or regulations

Title V permit 27.4(4558) Administrative organization 22. 203( 4558) Voluntary operating permit 27.5(4558) Program activities

applications 22.204(4558) Voluntary operating permit

fees CHAPTER 28 22.205(4558) Voluntary operating permit AMBIENT AIR QUALITY

processing procedures STANDARDS 22.206(4558) Permit content 28.1(4558) Statewide standards 22.207(4558) Relation to construction

permits CHAPTER29

~ 22.208(4558) Suspension, termination, QUALIFICATION IN VISUAL

and revocation of DETERMINATION OF THE voluntary operating OPACITY OF EMISSIONS permits 29.1(4558) Methodology and qualified

CHAPTER23 observer

EMISSION STANDARDS CHAPTER 30 FOR CONTAMINANTS TEMPORARY AIR TOXICS FEE

23.1(4558) Emission standards 30.1(4558) Authority, purpose and 23.2(4558) Open burning applicability 23.3(4558) Specific contaminants 30.2(4558) Fee schedule 23.4(4558) Specific processes 30.3(4558) Form, manner, time and place 23.5(4558) Anaerobic lagoons of filing \,.) 23.6(4558) Alternative emission limits 30.4(455B) Reports and record keeping

(the "bubble concept") 30.5(4558) Failure to pay fees

Analysis, p.2b Environmental Protection[567]

CHAPTER 31 NONA TT AINMENT AREAS

31.1 ( 455B) Permit requirements relating to nonattainment areas

31.2(455B) Conformity of general federal actions to the Iowa state implementation plan or federal implementation plan

CHAPTERS 32 to 34 Reserved

TITLE Ill

WITHDRAWAL, DIVERSION, STORAGE :AND USE OF WATER

DIVISION A WATER WELL CONSTRUCfiON:

GENERAL STANDARDS AND REGISTRATION OF CONTRACfORS

CHAPTERS 35 to 37 Reserved

lAC 1/18/95

lAC 1/18/95 Environmental Protection[567] Ch 20, p.3

"EPA conditional method,. means any method of sampling and analyzing for air pollutants that has been validated by the administrator but that has not been published as an EPA reference method.

"EPA reference method" means any method of sampling and analyzing for an air pollutant as described in 40 CFR 51, Appendix M, as amended through July 20, 1993; 40 CFR 52, Appendices D and E, as amended through July 20, 1993; 40 CFR 60, Appendix A, as amended through May 17, 1993; 40 CFR 61, Appendix B, as amended through June 25, 1993; 40 CFR 63, Appendix A, as amended through October 27, 1993; and 40 CFR 75, Appendices A, B, and H, as amended through July 20, 1993.

"Equipment" means equipment capable of emitting air contaminan:ts to produce air pollution such as fuel burning, combustion or process devices or apparatus including but not limited to fuel-burning equipment, refuse burning equipment used for the burning of fuel or other combustible material from which the products of combustion are emitted; and including but not limited to apparatus, equipment or process devices which generate heat and may emit products of combustion, and manufacturing, chemical, metallurgical or mechanical apparatus or process devices which may emit smoke, particulate matter or other air contaminants. -

"Excess air" means that amount of air supplied in addition to the theoretical quantity necessary for complete combustion of all fuel or combustible waste material present.

"Excess emission" means any emission which exceeds the applicable emission standard prescribed in 567-Chapter 23 or rule 567-22.5(455B).

"Director,. means the director of the department of natural resources or the director's designee.

"Existing equipment" means equipment, machines, devices or installations that are in operation prior to September 23, 1970.

"Foundry cupola" means a stack-type furnace used for melting of metals consisting of, but not limited to, the furnace proper, tuyeres, fans or blowers, tapping spout, charging equipment, gas cleaning devices and other auxiliaries.

"Fugitive dust" means any airborne solid particulate matter emitted from any source other than a flue or stack.

"Garbage" means all solid and semisolid putrescible and nonputrescible animal and vegetable wastes resulting from the handling, preparing, cooking, storing and serving of food or of material intended for use as food, but excluding recognized industrial by-products.

"Gas cleaning device" means a facility designed to remove air contaminants from gases exhausted from equipment as defined herein.

"Goal" means a level of air quality which is expected to be obtained. "Heating value" means the heat released by combustion of one pound of waste or fuel

measured in BTU on an as received basis. For solid fuels, the heating value shall be determined by use of ASTM Standard D20 15-66.

"Incinerator" means a combustion apparatus designed for high temperature operation in which solid, semisolid, liquid or gaseous combustible refuse is ignited and burned efficiently, and from which the solid residues contain little or no combustible material.

"Initiation of construction. installation or alteration" means significant permanent modification of a site to install equipment, control equipment or permanent structures. Not included are activities incident to preliminary engineering, environmental studjes, or acquisition of a site for a facility.

"Landscape waste" means any vegetable or plant wastes except garbage. The term includes trees, tree trimmings, branches, stumps, brush, weeds, leaves, grass, shrubbery and yard trimmings.

"Level" means a certain specified degree, quality or characteristic. "Malfunction" means any sudden and unavoidable failure of control equipment or of a

process to operate in a normal manner. Any failure that is caused entirely or in part by poor

Ch 20, p.4 Environmental Protection[567] lAC 1120/93

maintenance, careless operation, lack of an adequate maintenance program, or any other preventable upset condition or preventable equipment breakdown shall not be considered a malfunction.

"New equipment" means except for any equipment or modified equipment to which 567-subrule 23.1(2) applies, any equipment or control equipment not under construction or for which components have not been purchased on or before September 23, 1970, and any equipment which is altered or modified after such date, which may cause the emission of air contaminants or eliminate, reduce or control the emission of air contaminants.

"Odor" means that which produces a response of the human sense of smell to an odorous substance.

''Odorous substance'' means a gaseous, liquid, or solid material that elicits a physiological response by the human sense of smell.

"Odorous substance source" means any equipment, installation operation, or material which emits odorous substances; such as, but not limited to, a stack, chimney, vent, window, opening, basin, lagoon, pond, open tank, storage pile, or inorganic or organic discharges.

"Objective" means a certain specified degree, quality or characteristic expected to be attained. "One-hour period, means any 60-minute period commencing on the hour. "Opacity" means the degree to which emissions reduce the transmission of light and obscure

the view of an object in the background (See 567-Chapter 29). "Open burning" means any burning of combustible materials where the pr:oducts of

combustion are emitted into the open air without passing through a chimney or stagk. -"Particulate matter" means any material, except uncombined water, that exists in a finely

divided form as a liquid or solid at standard conditions . .. Parts per million (PPM)" means a term which expresses the volumetric concentration of one

material in one million unit volumes of a carrier material. "Plan documents" means the reports, proposals, preliminary plans, survey and basis of design

data, general and detail construction plans, profiles, specifications and all other information pertaining to equipment.

"PM1o, means particulate matter with an aerodynamic diameter less than or equal to a nominallO micrometers as measured by an EPA-approved reference method .

.. Privileged communication" means information other than air pollutant emissions data the release of which would tend to affect adversely the competitive position of the owner or operator of the equipment.

"Process" means any action, operation or treatment, and all methods and forms of manufacturing or processing, that may emit smoke, particulate matter, gaseous matter or other air contaminant.

"Process weight" means the total weight of all materials introduced into any source operation. Solid fuels charged will be considered as part of the process weight, but liquid and gaseous fuels and combustion air will not.

"Process weight rate" means continuous or long-nin steady-state source operations, the total process weight for the entire period of continuous operation or for a typical portion thereof, divided by the number of hours of such period or portion thereof; or for a cycHcai or batch source operation, the total process weight for a period that covers a complete operation or an integral number of cycles, divided by the number of hours of actual process operation during such a period. Where the nature of any process or operation, or the design of any equipment is such as to permit more than one interpretation of this definition, the interpretation that results in the minimum value for allowable emission shall apply.

"Refuse" means garbage, rubbish and all other putrescible and nonputrescible wastes, except sewage and water-carried trade wastes.

"Residential waste" means any refuse generated on the premises as a result of residential activities. The term includes landscape waste grown on the premises or deposited thereon by the elements, but excludes garbage, tires and trade wastes.

lAC 10/12/94 Environmental Protection[567] Ch 20, p.5

"Rubbish" means all waste materials of nonputrescible nature. '..,) "Salvage operations" means any business, industry or trade engaged wholly or in part in

salvaging or reclaiming any product or material, including, but not limited to, chemicals, drums, metals, motor vehicles or shipping containers.

"Shutdown" means the cessation of operation of any control equipment or process equipment or process for any purpose.

usix-minute period" means any one of the ten equal parts of a one-hour period. "Smoke" means gas-borne particles resulting from incomplete combustion, consisting

predominantly, but not exclusively, of carbon, and other combustible material, or ash, that form a visible plume in the air.

"Smoke monitor" means a device using a light source and a light detector which can automatically measure and record the light-obscuring power of smoke at a specific location in the flue or stack of a source.

\,..,) "Source operation" means the last operation preceding the emission of an air contaminant, and which results in the separation of the air contaminant from the process materials or in the conversion of the process materials into air contaminants, but is not an air pollution control operation.

"Standard conditions" means a gas temperature of 70° F and a gas pressure of 29.92 inches of mercury absolute.

"Standard cubic foot (SCF)" means the volume of one cubic foot of gas at standard conditions. _

"Standard metropolitan statistical area (SMSA)" means an area which has at least one city with a population of at least 50,000 and such surrounding areas as geographically defined by the U.S. Bureau of the Budget (Department of Commerce).

ustartup, means the setting into operation of any control equipment or process equipment or process for any purpose.

~ "Stationary source" means any building, structure, facility or installation which emits or may emit any air pollutant.

"Theoretical air" means the exact amount of air required to supply the required oxygen for complete combustion of a given quantity of a specific fuel or waste.

uTotal suspended particulate, means particulate matter as measured by an EPA-approved reference method.

"Trade waste" means any refuse resulting from the prosecution of any trade, business, industry, commercial venture (including farming and ranching), or utility or service activity, and any governmental or institutional activity, whether or not for profit.

"Urban area" means any Iowa city of I 00,000 or more population in the current census and all Iowa cities contiguous to such city.

"Variance" means a temporary waiver from rules or standards governing the quality, nature, duration or extent of emissions granted by the commission for a specified period of time.

'..I uvolatile organic compound" means any compound included in the definition of volatile organic compound found at 40 CFR section 51.100(s) as amended through November 30, 1993.

567-20.3(4558) Air quality forms generally. The following forms are used by the public to apply for various departmental approvals and to report on activities related to the air programs of the department. All forms may be obtained from the central office:

Administrative Support Station-Environmental Protection Division Iowa Department of Natural Resources Henry A. Wallace Building 900 East Grand Des Moines, Iowa 50319

Ch 20, p.6 Environmental Protection[567] lAC 1/18/95

Properly completed forms should be submitted in accordance with the instructions to the form. Where not specified in the instructions, forms should be submitted to the program operations division.

20.3(1) Application for a permit to install or alter equipment or control equipment. All applications for a permit to install or alter equipment or control equipment pursuant to 567-22.1(4558) shall be made in accordance with the instructions for completion of application Form 6, "Application and Permit to Install or Alter Equipment or Control Equipment" (542-3190). Applications submitted which are not fully or properly completed will not be reviewed until such time as a complete submission is made. A permit to install or alter equipment or control equipment will be denied when the application does not meet all requirements

· for issuance of such permit. 20.3(2) Application for variance from open burning rules. All applications for variance

from open burning rules pursuant to 567-22.2(4558) shall be made in accordance with the instructions for completion of application Form 7, "Application for Variance from Open Burning Rules" (542-3204).

20.3(3) Air pollution preplanned abatement strategy forms. The submission of standby plans for the reduction of emissions of air contaminants during the periods of an air pollution episode, as requested by the director pursuant to 567-22.3(4558), shall be made in accordance with the instructions for completion of application forms provided by the department.

20.3(4) Air contaminant emissions survey forms. The submission of emissions information pursuant to 567-subrule 22.2(3) shall be made in accordance with instructions for completion of survey forms provided by the department.

20.3(5) Notification of corrective action in response to notice of vehicle emission violation. "Vehicle Emission Violation," Form 10, is a postcard informing the department, in response to a notice of vehicle emission violation by a gasoline-powered or diesel-powered vehicle, pursuant to 567-subparagraphs 23.3(2)"d"(2) and (3), that corrective action has been taken. It requests that the recipient specify what repairs were made to eliminate further violation of vehicle emission rules.

20.3(6) Temporary air toxicsfeeform. Form 542-1413 shall be completed in accordance with the instructions for completion of the form provided by the department.

These rules are intended to implement Iowa Code section 17 A.3 and chapter 4558, division II. [Filed emergency 6/3/83-published 6/22/83, effective 7/1/83]

[Filed 8/24/84, Notice 5/9/84-published 9/12/84, effective 10/18/84] [Filed emergency 11/14/86-published 12/3/86, effective 12/3/86] [Filed emergency 9/22/87-published 10/21/87, effective 9/22/87]

[Filed 10/28/88, Notice 7/27 /88-published 11 I 16/88, effective 12/21 /88] [Filed emergency 10/25/91, after Notice 9/18/91-published 11/13/91, effective 11/13/91]

[Filed 12/30/92, Notice 9/16/92-published 1/20/93, effective 2/24/93) [Flied 9/23/94, Notice 6/22/94-published 10/12/94, effective 11/16/94] [Filed 12/30/94, Notice 10/12/94-published 1/18/95, effective 2/22/95]

'~

lAC 3/16/94, 1/18/95 Environmental Protection[567] Ch 22, p.43

For purposes of nitrogen oxides emissions, the applicable limitation established by regulations promulgated by the administrator pursuant to section 407 of the Act, as modified by an acid rain permit appJication submitted to the department, and an acid rain permit issued by the department, in accordance with rules implementing section 407 of the Act.

"Acid rain emissions reduction requirement" means a requirement under the acid rain program to reduce the emissions of sulfur dioxide or nitrogen oxides from a unit to a specified level or by a specified percentage.

"Acid rain permit" means the legally binding written document, or portion of such document, issued by the department (following an opportunity for appeal pursuant to 561-Chapter 7 as adopted by reference at 567-Chapter 7), including any permit revisions, specifying the acid rain program requirements applicable to an affected source, to each affected unit at an affected source, and to the owners and operators and the designated representative of the affected source or the affected unit.

"Acid rain program •• means the national sulfur dioxide and nitrogen oxides air pollution control and emissions reduction program established in accordance with Title IV of the Act, rules 22.120(4558) to 22.147(4558), 40 CFR Parts 72, 73, 75, 77, and 78 as amended through July 30, 1993, and regulations implementing sections 407 and 410 of the Act .

.. Act .. means the Clean Air Act, 42 U.S.C. §7401, et seq., as amended by Public Law No. 101-549 (November 15, 1990).

"Actual SOz emissions rate .. means the annual average sulfur dioxide emissions rate for the unit (expressed in lb/mmBtu), for the specified calendar year; provided that, if the unit is listed in the National Allowance Database (NADB), the "1985 actual S02 emissions rate" for the unit shall be the rate specified by the administrator in the NADB under the data field "S02RTE."

"Administrator .. means the administrator of the United States Environmental Protection Agency or the administrator's duly authorized representative .

.. Affected source .. means a source that includes one or more affected units. "Affected unit" means a unit that is subject to any acid rain emissions reduction require

ment or acid rain emissions limitation . .. Affiliate .. shall have the meaning set forth in section 2(a)(11) of the Public Utility Hold

ing Company Act of 1935, 15 U.S.C. 79b(a)(ll}, as of November 15, 1990 . .. Allocate .. or .. allocation .. means the initial crediting of an allowance by the administra

tor to an allowance tracking system unit account or general account . .. Allowance, means an authorization by the administrator under the acid rain program to

emit up to one ton of sulfur dioxide during or after a specified calendar year . .. Allowance deduction .. or udeduct when referring to allowances" means the permanent

withdrawal of allowances by the administrator from an allowance tracking system compliance subaccount to account for the number of the tons of S02 emissions from an affected unit for the calendar year, for tonnage emissions estimates calculated for periods of missing data as provided in rule 567-25.2(455B), or for any other allowance surrender obligations of the acid rain program.

"Allowances held .. or "hold allowances .. means the allowances recorded by the administrator, or submitted to the administrator for recordation in accordance with 40 CFR 73.50 as amended through July 30, 1993, in an allowance tracking system account.

.. Allowance tracking system •• or uA TS, means the acid rain program system by which the administrator allocates, records, deducts, and tracks allowances .

.. Allowance tracking system account, means an account in the allowance tracking system established by the administrator for purposes of allocating, holding, transferring, and using allowances .

.. Allowance transfer deadline .. means midnight of January 30 or, if January 30 is not a business day, midnight of the first business day thereafter and is the deadline by which al-

Ch 22, p.44 Environmental Protection[567] lAC 3/16/94

lowances may be submitted for recordation in an affected unit's compliance subaccount for~ the purposes of meeting the unit's acid rain emissions limitation requirements for sulfur diox-ide for the previous calendar year.

"Authorized account representative" means a responsible natural person who is authorized, in accordance with 40 CFR Part 73 as amended through July 30, 1993, to transfer and otherwise dispose of allowances held in an allowance tracking system general account; or, in the case of a unit account, the designated representative of the owners and operators of the affected unit.

~~Basic Phase II allowance allocations" means: (I) For calendar years 2000 to 2009 inclusive, allocations of allowances made by the ad

ministrator pursuant to section 403 and section 405 (b)(1), (3), and (4); (c)(l), (2), (3), and (5); (d)(1), (2), (4), and (5); (e); (f); (g)(l), (2), (3), (4), and (5); (h)(l); (i); and G).

(2) For each calendar year beginning in 2010, allocations of allowances made by the administrator pursuant to section 403 and section 405 (b)(1), (3), and (4); (c)(1), (2), (3), and '..~ (5); (d)(1), (2), (4), and (5); (e); (f); (g)(l), (2), (3), (4), and (5); (h)(1) and (3); (i); and G).

~~Boiler" means an enclosed fossil or other fuel-fired combustion device used to produce heat and to transfer heat to recirculating water, steam, or any other medium.

"Certificate of representation., means the completed and signed submission required by 40 CFR 72.20 as amended through July 30, 1993, for certifying the appointment of a designated representative for an affected source or a group of identified affected sources authorized to represent the owners and operators of such source(s) and of the affected units at such source(s) with regard to matters under the acid rain program.

''Certifying official'' means: (1) For a corporation, a president, secretary, treasurer, or vice-president of the corporation

in charge of a principal business function, or any other person who performs similar policy or decision-making functions for the corporation;

(2) For partnership or sole proprietorship, a general partner or the proprietor, respectively; "-"' and

(3) For a local government entity or state, federal, or other public agency, either a principal executive officer or ranking elected official.

"Coal" means all solid fuels classified as anthracite, bituminous, subbituminous, or lignite by the American Society for Testing and Materials Designation ASTM 0388-92 "Standard Classification of Coals by Rank."

"Coal-derived fuel" means any fuel, whether in a solid, liquid, or gaseous state, produced by the mechanical, thermal, or chemical processing of coal (e.g., pulverized coal, coal refuse, liquefied or gasified coal, washed coal, chemically cleaned coal, coal-oil mixtures, and coke).