Embed Size (px)

Citation preview

Tassal Group Limited2018 Annual General MeetingMelbourne, 31 October 2018

1

For

per

sona

l use

onl

y

Allan McCallum Chairman

31st October 2018Melbourne, 31 October 2018

2018 Annual General MeetingChairman’s address

2

For

per

sona

l use

onl

y

Overviewsalmon in growth

Almost half of all seafood eaten in Australia comes from aquaculture. Of this seafood, salmon and prawns continue to share the larger portion of Australian dinner plates, as people turn towards healthier, sustainable sources of protein.

Wild fisheries catches are plateauing, and to protect stocks for the future, aquaculture is a priority solution to address increasing demand for protein today and in coming years.

Salmon farming is essential to our future. With increasing pressure on our planet, access to arable land restrictive, and the ocean 70% of the planet’s footprint, our future food supply will depend more and more on the sea.

This is why the salmon industry must maintain its growth phase ‐ one which needs to be sustainable to meet future generations’ needs. As the leading salmon producer in Australia, Tassal takes its responsibility to deliver on its business and sustainability objectives seriously.

3

For

per

sona

l use

onl

y

OverviewTassal

Tassal is the market leader in the Australian salmon Industry.

Tassal continues to execute on its strategy to be a world leading seafood company producing a high quality/healthy protein by leveraging:

industry leading scientific know how sustainable and efficient production respect for the earth’s resources and the communities

in which it operates prudent commercial management

Our unwavering focus in FY18 was the implementation of industry leading innovations and programs which enhanced our environmental and sustainability credentials.

Tassal also implemented its Community Foundation and Charter, which saw in FY18 a greater level of engagement and investment in community programs in the environment, education, health & wellbeing and social inclusion areas.

We seek to deliver sustainable, competitive growing returns and this year announced our acquisition of the Fortune Group – land, assets and inventory – cementing Tassal as one of the largest footprint tiger prawn farming operations in Australia.

Tassal is the market leader in the Australian salmon Industry

4

For

per

sona

l use

onl

y

Overviewprawns in growth

Tassal continues to invest in strategic growth opportunities which support a sustainable seafood business and strong returns to shareholders:

salmon and prawns comprise 70% retail seafood sales in Australia

no material growth in Australian‐grown prawns supply for 10 years +

high consumer demand and price

Research demonstrates Australian grown tiger prawns are a clear consumer preference.

Currently of the ~60,000 tonnes of prawns in the Australian market, Australian aquaculture accounts for less than 10% of this. In comparison, Australian salmon aquaculture accounts for ~90% of the ~60,000 market tonnes.

Our $31.9 million acquisition of the Fortune Group, includes three prawn farms, supported by a $33 million development program, operational improvements are expected to increase supply growth from 450 tonnes pa to ~3000 tonnes pa within 3 – 5 years.

Tassal targets an EBITDA range of $15million ‐ $25 million within 5 years.

Tassal unlocks large synergies in the seafood supply market

5

For

per

sona

l use

onl

y

Sustainability“The essence of sustainable development is that today’s generations meet their needs without prejudicing future generations’ ability to meet theirs.”

6

For

per

sona

l use

onl

y

Key Highlights

7

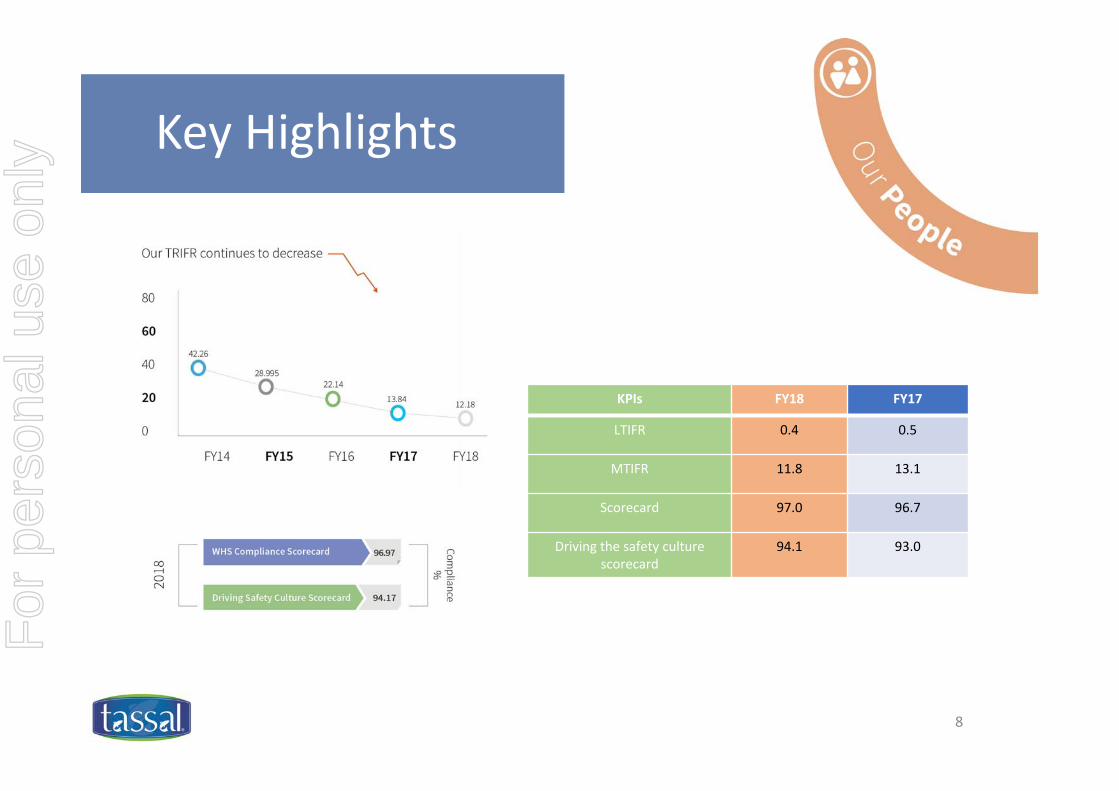

During the reporting period, Tassal was pleased to achieve an improved safety performance and increased revenue growth, while investing significantly in sustainability programs, including:

Producing larger smolt in land‐based nurseries, minimising time spent at sea.

Investing in eco‐aquaculture programs at a number of sites (including Okehampton Bay, Tasman and Dover farms) with the plantation of Giant Kelp to assist reduce nutrients in the environment and rejuvenate a local, threatened species.

Movement towards 100% recycling of soft and hard major plastics (~500 tonnes per annum) via a partnership with Tasmanian based company, Envorinex, which transforms them into second life products.

Accelerated roll‐out of our seal proof sanctuary pens.

Continued focus on selective breeding program in response to climate change.

Established improved biosecurity management practices in Macquarie Harbour via the joint venture approach with Petuna.

Zero antibiotic usage in marine environment.

Increased marine debris clean ups (by 926 per cent in man‐hours compared to 2017).

100 per cent regulatory environmental compliance across leases.

100 per cent Aquaculture Stewardship Council (ASC) certification across harvest produce.

100 per cent fully traceable, responsibly sourced seafood.For

per

sona

l use

onl

y

KPIs FY18 FY17

LTIFR 0.4 0.5

MTIFR 11.8 13.1

Scorecard 97.0 96.7

Driving the safety culture scorecard

94.1 93.0

8

Key Highlights

For

per

sona

l use

onl

y

9

Key Highlights

For

per

sona

l use

onl

y

10

Key HighlightsIn our Salmon marine environment (ie. at sea)

For

per

sona

l use

onl

y

Tassal has implemented a remote feeding strategy, which has commenced with a roll‐out program with all pens to be remotely fed by 31 December 2018.

The implementation commenced at the end of February 2018 and initial analysis is showing both improved growth against previous feeding program (10%+) and pleasingly at a reduced feed conversion ratio (11%+).

Remote feeding will play a pivotal role for Tassal with it contributing to:

Lower fish growing costs Improving environmental

outcomes Improving people safety

outcomes Improving fish health and

welfare

Key Investments – Feed Centre

11

For

per

sona

l use

onl

y

Key Investments – Seal proof pens

Tassal continued the roll out of its seal proof infrastructure “sanctuary pens” targeting areas where seals are the greatest risk to people.

So far a $70 million investment has been made into seal proof pens and this is proving effective, with minimal breaches, reducing risk to people, stock and wildlife through exclusion methodology.

12

For

per

sona

l use

onl

y

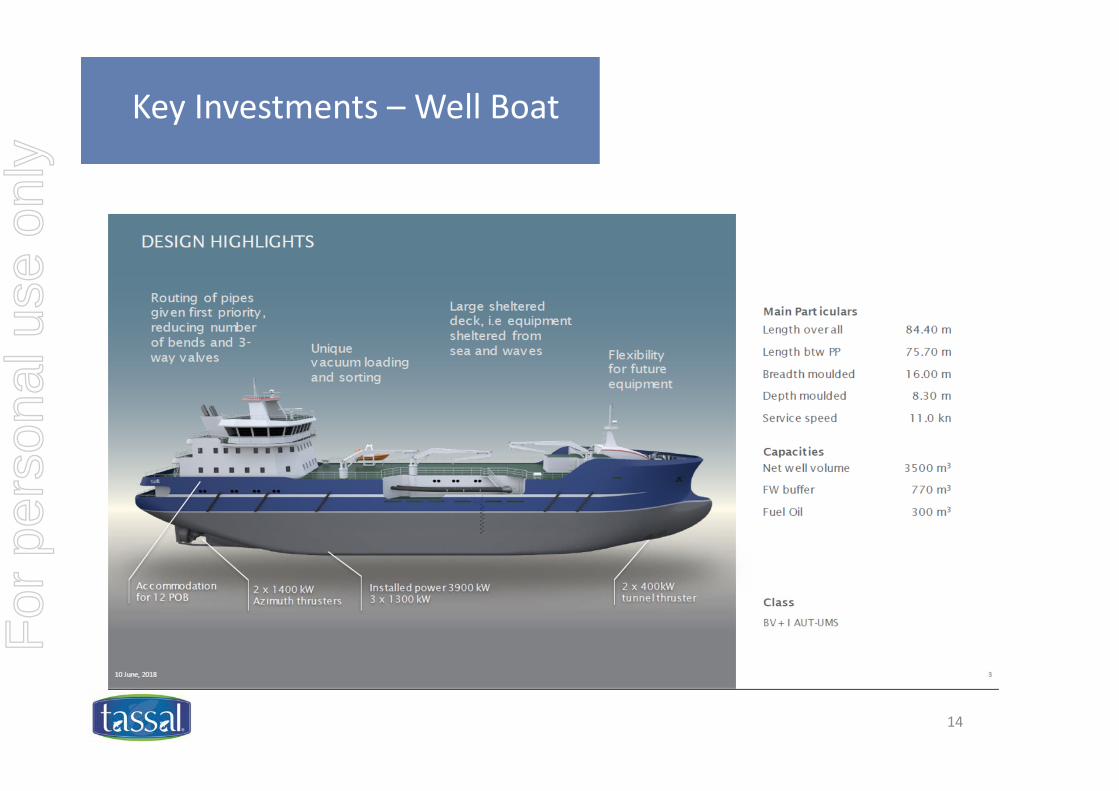

Key Investments – Well Boat

Tassal will be taking possession of a Well Boat under a 10 year lease (with a 5 year option at Tassal’s option) for delivery between September and December 2019. The Well Boat will have a 3,500m3 water capacity – enough to completely bathe one of Tassal’s largest pens circa 3X quicker than current methods.

The Well Boat will also provide additional biomass benefits through improvements in survival, enabling further offshore / higher energy farming and facilitating further lease optimisation from existing leases: Reduced mortality arising from improved bathing techniques and frequency Enabling bathing in higher energy / rougher sites Increased lease optimisation through allowing quicker and more a efficient bathing process Increased lease optimisation through allowing transport of larger smolt to grow‐out sites

The following operational improvements should also result in: A material improvement in the safety risk of fish bathing on farms by a reduction in high risk tasks, manual

handling, diving and towing More efficient use of human resource allocation and overheads to operate farms Improved biosecurity and fish health and welfare Enabling grading fish during a bath, to better manage growth and sales optimisation

13

For

per

sona

l use

onl

y

Key Investments – Well Boat

14

For

per

sona

l use

onl

y

15

Key Risk – Climate Change

Climate plays an important role in Tassal’s salmon operations –particularly summer for salmon farming.

Tassal recognises climate change is likely to present a range of challenges to the aquaculture industry. Without proactive adaptation, salmon and prawn farming may become more vulnerable to disease and/or changes in environmental conditions.

Tassal has developed considerable options for adaptation including selective breeding, modification of farming technologies and practices, and geographic diversification of its salmon marine and prawn farm portfolio.

Tassal has also engaged scientists to identify emerging climate trends and system responses, and to undertake comprehensive broad scale environmental monitoring.

A comprehensive risk management system is used to manage the long‐term risks, issues and opportunities presented by climate change and respond accordingly.

Ultimately, if farmed salmon and prawns are managed effectively for the impacts of climate change, a positive financial benefit may be realised from the increased demand of farmed fish to the reduced availability of global wild stocks as a result of climate change impacts and over‐fishing for wild stocks.

For

per

sona

l use

onl

y

Conclusion

Tassal is the seafood market leader and largest producer in the Australian salmon Industry. It is the most recommended consumer choice as independently surveyed in 2017 and 2018.

We have once again been benchmarked as one of the world’s top salmon farming companies in corporate, social and environmental reporting by seafoodintel.com and recognised by ACIS as the industry leader in sustainability reporting.

We have an unwavering commitment to continue our work with our stakeholders, communities, employees and partners to achieve further improvements in sustainability and responsible farming – and the innovations and programs implemented in the past 12 months are testament to this.

To my fellow Directors and Management, thank you for your support and input over the past 12 months and I know that we are all looking positively to continuing growth across the business in FY2018.

To our shareholders and other stakeholders, your continuing support is appreciated and valued.

Thank you 16

For

per

sona

l use

onl

y

17

For

per

sona

l use

onl

y

“Delivering growing returns”

Mark A RyanManaging Director & CEO

31st October 2018Melbourne, 31 October 2018

2018 Annual General MeetingManaging Director & CEO’s address

18

For

per

sona

l use

onl

y

Delivering growing returns

Over the past 12 months we have seen favourable salmon market dynamics. Industry cost and supply pressures experienced domestically and globally have been offset by strong consumer demand for Tassal’s salmon, which has improved pricing conditions and allowed for further optimisation of our sales mix to maximise margins.

Albeit there are supply pressures in both domestic and global markets, pleasingly, Tassal has been able to increase its supply position for both FY18 and forecast for FY19, ensuring the contribution of record results.

I acknowledge the Board of Directors, the Tassal management team and all staff for their roles in delivering these results.

19

For

per

sona

l use

onl

y

Record Earnings & Profits

Strong operational growth – investment in biomass and infrastructure

Strong growth in revenue Operational strategy of growing larger salmon –

additional harvest biomass and size Strong growth in salmon domestic market per capita

consumption Export market strategically targeted with bigger salmon

Operating earnings growing in line with revenue Favourable domestic salmon market sales mix and

pricing Efficiency benefits flowing from more optimal salmon

harvest biomass and size

Solid operating cashflow

Cash receipts from revenue growth allowed appropriate cash spend in salmon biomass and capital infrastructure

Increase in fully franked dividend

Note:

SGARA benefit Statutory EBITDA benefited by SGARA adjustment of $10.8m

(FY17: increased $32.3m) NPAT $7.6m (FY17: increased $22.6m)

20

For

per

sona

l use

onl

y

Optimising Sales Mix

Strong growth in Salmon Larger harvest biomass and size – strategic focus to

drive efficiency benefits and optimise margins

Continued growth in Seafood (De Costi) Focus on highly innovative product and packaging

formats Higher margin products

Continued growth in domestic market Strong domestic per capita consumption growth Favourable domestic market sales mix

Export market strategically targeted – larger fish focus

21

For

per

sona

l use

onl

y

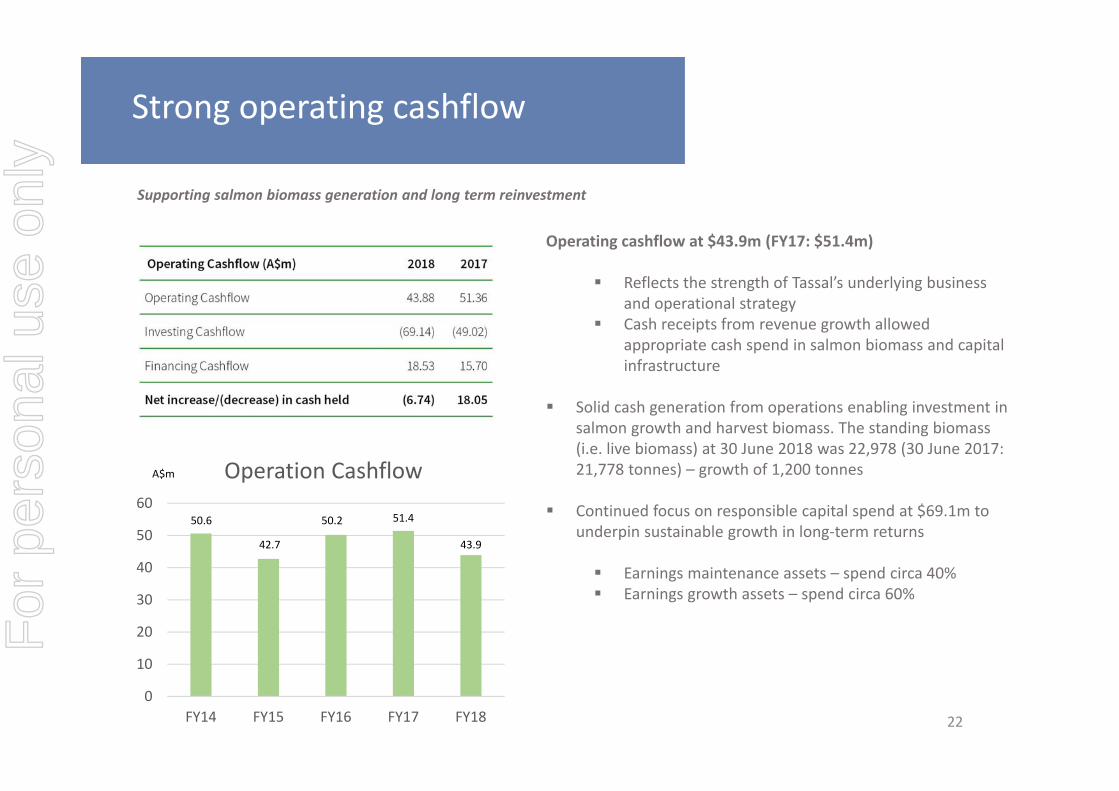

Strong operating cashflow

Supporting salmon biomass generation and long term reinvestment

Operating cashflow at $43.9m (FY17: $51.4m)

Reflects the strength of Tassal’s underlying business and operational strategy

Cash receipts from revenue growth allowed appropriate cash spend in salmon biomass and capital infrastructure

Solid cash generation from operations enabling investment in salmon growth and harvest biomass. The standing biomass (i.e. live biomass) at 30 June 2018 was 22,978 (30 June 2017: 21,778 tonnes) – growth of 1,200 tonnes

Continued focus on responsible capital spend at $69.1m to underpin sustainable growth in long‐term returns

Earnings maintenance assets – spend circa 40% Earnings growth assets – spend circa 60%

0

10

20

30

40

50

60

FY14 FY15 FY16 FY17 FY18

Operation Cashflow

50.6

42.7

50.2 51.4

43.9

A$m

22

For

per

sona

l use

onl

y

Strong balance sheet – significantly de‐risked

Capital raising (share placement and share purchase plan) from 2H17 raised net proceeds of $82.5m

Capital raising, together with solid operating cashflow and responsible biomass growth and capital spend has gearing at 18.7% (FY17: 12.4%)

Conservative Gearing and Funding ratios – supported by capital raising, solid operating cashflow and responsible biomass generation and capital spend

Gearing only 18.7% (FY17: 12.4%), providing flexibility to invest strategically for growth

Appropriate bank funding arrangements in place –structure, headroom and tenor

Funding ratio, i.e. including RPF (net debt + RPF / equity) at 28.5% (FY17: 24.3%)

Operational Return on Assets

SGARA impact removed from calculation

Operational Return on Assets sustainable moving forward

Continuing to generate return > WACC

0.00%

10.00%

20.00%

30.00%

40.00%

FY14 FY15 FY16 FY17 FY18

9.00%

9.50%

10.00%

10.50%

11.00%

FY14 FY15 FY16 FY17 FY18

15.4%17.6%

33.5%

12.4%

18.7%

10.5% 10.6%

9.6%

10.1%10.2%

23

For

per

sona

l use

onl

y

Strong salmon position

Despite a challenging summer 2017/18 for salmon growth … through our continued focus on fish health, risk mitigation, research &development and selective breeding ‐ we finished the year in a strong salmon supply position

4.04.2

3.73.9

4.5

188.8222.9

246.1

312.4

356.5

18,908

23,860

25,411

25,432

30,883

19,268 23

,144

27,177

25,487

30,702

24

For

per

sona

l use

onl

y

25

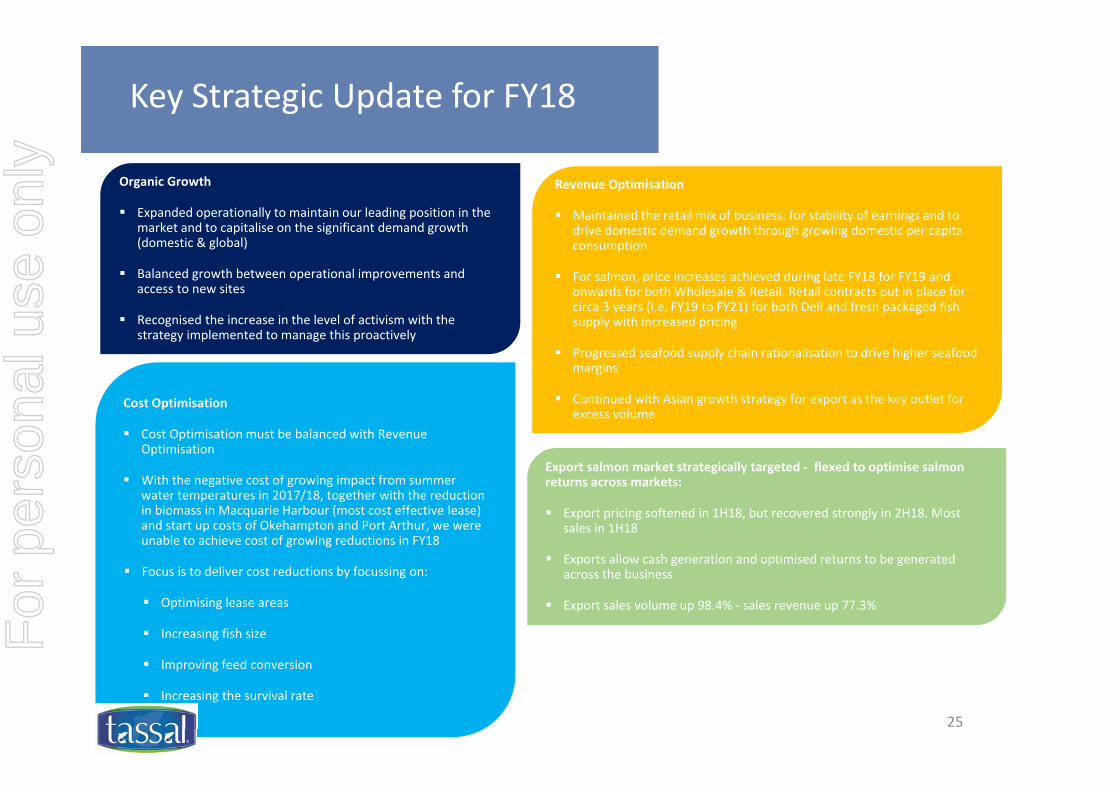

Key Strategic Update for FY18

Export salmon market strategically targeted ‐ flexed to optimise salmon returns across markets:

Export pricing softened in 1H18, but recovered strongly in 2H18. Most sales in 1H18

Exports allow cash generation and optimised returns to be generated across the business

Export sales volume up 98.4% ‐ sales revenue up 77.3%

Cost Optimisation

Cost Optimisation must be balanced with Revenue Optimisation

With the negative cost of growing impact from summer water temperatures in 2017/18, together with the reduction in biomass in Macquarie Harbour (most cost effective lease) and start up costs of Okehampton and Port Arthur, we were unable to achieve cost of growing reductions in FY18

Focus is to deliver cost reductions by focussing on:

Optimising lease areas

Increasing fish size

Improving feed conversion

Increasing the survival rate

Revenue Optimisation

Maintained the retail mix of business, for stability of earnings and to drive domestic demand growth through growing domestic per capita consumption

For salmon, price increases achieved during late FY18 for FY19 and onwards for both Wholesale & Retail. Retail contracts put in place for circa 3 years (i.e. FY19 to FY21) for both Deli and fresh packaged fish supply with increased pricing

Progressed seafood supply chain rationalisation to drive higher seafood margins

Continued with Asian growth strategy for export as the key outlet for excess volume

Organic Growth

Expanded operationally to maintain our leading position in the market and to capitalise on the significant demand growth (domestic & global)

Balanced growth between operational improvements and access to new sites

Recognised the increase in the level of activism with the strategy implemented to manage this proactively

For

per

sona

l use

onl

y

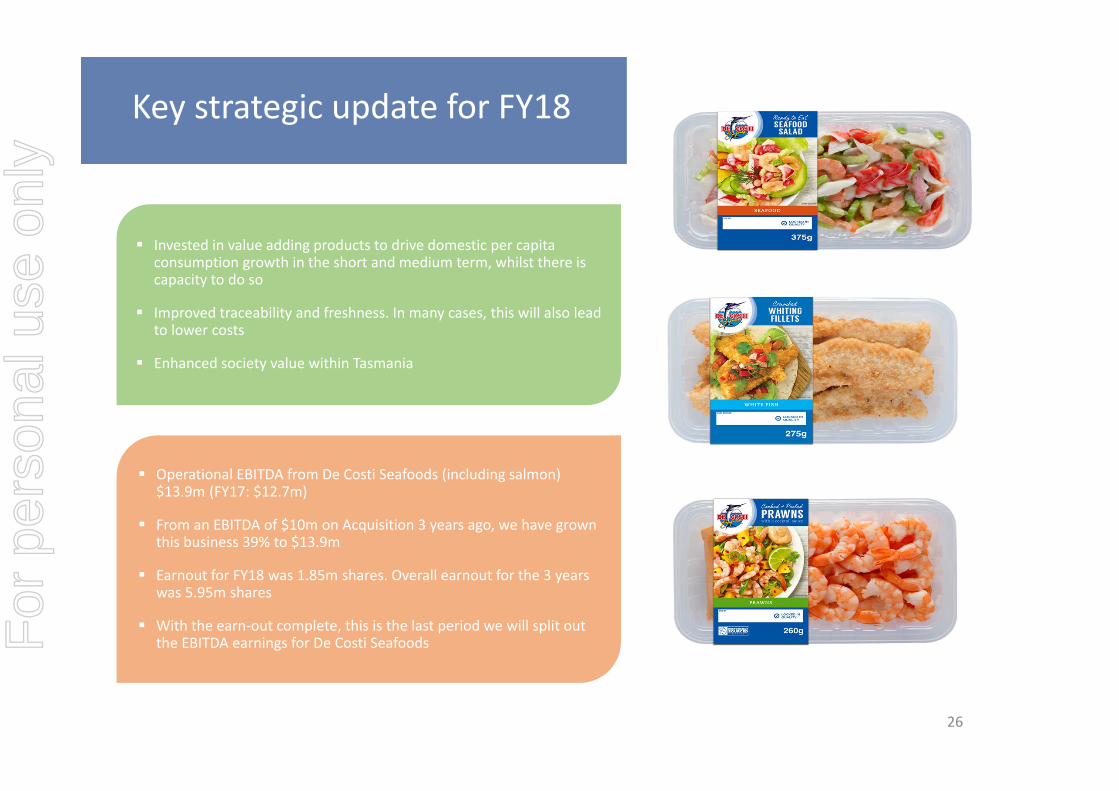

Key strategic update for FY18

Invested in value adding products to drive domestic per capita consumption growth in the short and medium term, whilst there is capacity to do so

Improved traceability and freshness. In many cases, this will also lead to lower costs

Enhanced society value within Tasmania

Operational EBITDA from De Costi Seafoods (including salmon) $13.9m (FY17: $12.7m)

From an EBITDA of $10m on Acquisition 3 years ago, we have grown this business 39% to $13.9m

Earnout for FY18 was 1.85m shares. Overall earnout for the 3 years was 5.95m shares

With the earn‐out complete, this is the last period we will split out the EBITDA earnings for De Costi Seafoods

26

For

per

sona

l use

onl

y

Strategy“Tassal seeks to deliver sustainable, competitive growing returns. Successful aquaculture and its growth is about finding common ground on shared values around environment… and for salmon, respecting the use of shared waterways.”

27

For

per

sona

l use

onl

y

Outlook for FY19

Tassal forecasts an increase in harvest production and sales in FY19, with analysis suggesting a supply shortage for domestic market fulfilment, leading to strong pricing returns and an improved domestic pricing outlook – which should allow improving margin returns.

Analysts are signalling strong demand growth from China with supply likely to be lower than demand, signalling higher international pricing outlooks.

We have delivered fish size growth upwards of 3‐5 years ahead of plan, which supports both improved domestic yields and pricing, but also underpins an Asian export program, requiring very large fish (at a price premium).

We have settled the acquisition of the Fortune Group prawn farms. The acquisition is strategically compelling as it allows us to expand our vertical integration and unlock further synergies in the supply chain with a highly earnings accretive acquisition.

Well Boat will see us bathing fish more efficiently than we currently do from a labour and overhead perspective, plus the Well Boat allows further biomass facilitation when we implement farming further offshore and when considering the use of larger Smolt in our salmon production.

As we had expected, salmon demand and pricing has been strong ‐both domestically and from an export perspective. Supporting this, our fish performance has also been strong.

Pleasingly, the operating performance of our Prawn operations is ahead of our business case.

Opportunities for FY19 adding to the strategic horizon:

28

For

per

sona

l use

onl

y

Outlook for FY19 and onward

In the short to medium term, salmon margin returns are forecast to increase. We believe that there should be more gradual growth curve for salmon biogain from Tasmanian salmon growers. We are well positioned in the short to medium term for responsibly increasing earnings from salmon production … selling more salmon biomass for more.

We believe a continued focus on other seafood species and geographic diversification (salmon and other seafood) remains the right thing to do to ensure increasing shareholder returns … particularly given the strong balance sheet position and to leverage / optimise the supply chain infrastructure that Tassal has in place.

Overall, with the movements in the strategic environment, we remain well placed to achieve our fundamental return targets, with the Well Boat and Feed Centre likely to drive both cost and operational efficiencies in the medium term. We are currently seeing a high demand/low supply thematic across both salmon and other seafood, combined with an improving pricing return environment.

Whether ultimately we achieve the fundamental targets through pricing, improvements and adaption of new technology or species diversification, management believes there is a well‐balanced program in place to continue the shareholder return growth projectile.

Importantly, we are well positioned from a capital and balance sheet perspective to manage this next wave of growth, thereby providing the enabling funding to direct the business to an adaptive future as it unfolds.

Overall, salmon and prawn demand > supply, with pricing outcomes positive and supply growth occurring.

29

For

per

sona

l use

onl

y

Strategic focus

Tassal farms the ocean to produce a high quality/healthy source of protein, leveraging its industry leading scientific know how, being both sustainable and efficient in its production, and respecting the resources of the earth and the wider society in which the company operates: Leveraging the scale of Tassal’s vertically

integrated supply chain to optimise value and ensure product quality and freshness.

Accessing the market via multiple channels (i.e., direct, retail, wholesale and export) to maximise penetration, optimise margins and deliver sustainable growing returns.

Expanding the consumer offer to continually meet more of their seafood requirements.

Tassal has the right strategy in place to be a world leading seafood company

30

For

per

sona

l use

onl

y

Any Questions?

31

For

per

sona

l use

onl

y

Resolutions

31st October 2018

Melbourne, 31 October 2018

2018 Annual General MeetingResolutions

32

For

per

sona

l use

onl

y

33

For

per

sona

l use

onl

y

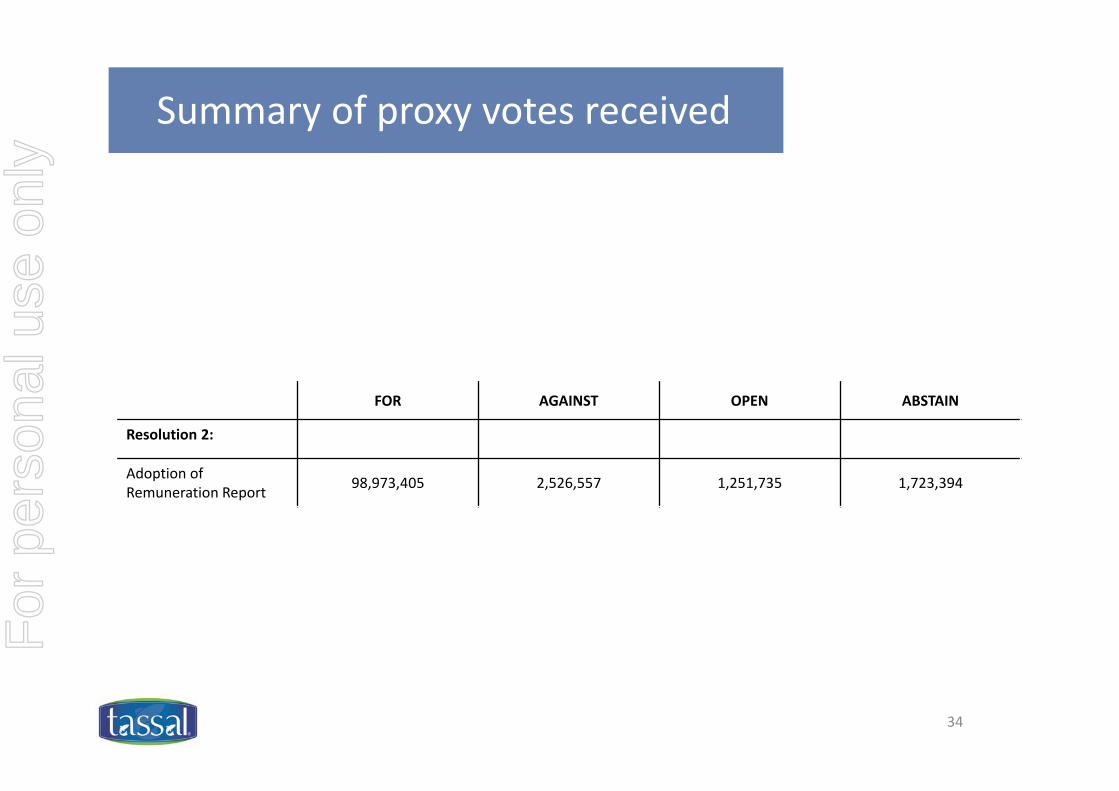

Summary of proxy votes received

FOR AGAINST OPEN ABSTAIN

Resolution 2:

Adoption of Remuneration Report 98,973,405 2,526,557 1,251,735 1,723,394

34

For

per

sona

l use

onl

y

35

For

per

sona

l use

onl

y

Summary of proxy votes received

FOR AGAINST OPEN ABSTAIN

Resolution 3:

Re‐election of Mr Allan McCallum 100,043,830 3,799,670 1,249,863 123,986

36

For

per

sona

l use

onl

y

37

For

per

sona

l use

onl

y

Summary of proxy votes received

FOR AGAINST OPEN ABSTAIN

Resolution 4:

Election of Mr John Watson 102,465,624 1,351,987 1,254,096 145,642

38

For

per

sona

l use

onl

y

39

For

per

sona

l use

onl

y

Summary of proxy votes received

40

FOR AGAINST OPEN ABSTAIN

Resolution 5:

Remuneration of Non‐Executive Directors

57,064,767 45,943,439 1,253,335 213,550

For

per

sona

l use

onl

y

41

For

per

sona

l use

onl

y

Summary of proxy votes received

FOR AGAINST OPEN ABSTAIN

Resolution 6:

Long Term Incentive Plan‐ Grant of 95,819 Performance Rights to Mr Mark Ryan pursuant to the 2018 Performance Rights Package

99,816,554 1,985,539 1,318,035 2,097,221

42

For

per

sona

l use

onl

y

43

For

per

sona

l use

onl

y

This presentation has been prepared by Tassal Group Limited for professional investors. The information contained in this presentation is for information purposes only and does not constitute an offer to issue, or arrange to issue, securities or other financial products. The information contained in this presentation is not investment or financial product advice and is not intended to be used as the basis for making an investment decision. The presentation has been prepared without taking into account the investment objectives, financial situation or particular need of any particular person.

No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in the presentation. To the maximum extent permitted by law, none of Tassal Group Limited, its directors, employees or agents, nor any other person accepts any liability, including, without limitation, any liability arising out of fault. In particular, no representation or warranty, express or implied is given as to the accuracy, completeness or correctness, likelihood of achievement or reasonableness of any forecasts, prospects or returns contained in this presentation nor is any obligation assumed to update such information. Such forecasts, prospects or returns are by their nature subject to significant uncertainties and contingencies.

Before making an investment decision, you should consider, with or without the assistance of a financial adviser, whether an investment is appropriate in light of your particular investment needs, objectives and financial circumstances. Past performance is no guarantee of future performance.

The distribution of this document is jurisdictions outside Australia may be restricted by law. Any recipient of this document outside Australia must seek advice on and observe such restrictions.

Disclaimer

44

For

per

sona

l use

onl

y

![DISK128:[17ZCV1.17ZCV42001]BE42001A.;6 · 2018-01-16 · 11JAN201811554032 9JAN201809010751 11JAN201619580193 11JAN201811554032 January 12, 2018 Dear Fellow Shareholder, I am pleased](https://img.pdfslide.us/doc/110x75/5f0a6a687e708231d42b8619/disk12817zcv117zcv42001be42001a6-2018-01-16-11jan201811554032-9jan201809010751.jpg)