Embed Size (px)

Citation preview

See important disclosures, including any required research certifications, beginning on page 19

China Consumer Discretionary

What's new: We are downgrading our rating on Guangzhou Automobile

(GAC) by 2 notches to Sell (5) and revising our earnings forecasts for

2016-17. We are doing this as we believe the current share price has

factored in the market’s expectations of strong earnings over this period but

fails to reflect the impact of a likely slowdown (vs. 1H16) in GAC’s Japan

JV sales volume growth and margin erosion for GAC Motor’s main growth

driver, its popular GS4 SUV, in 2H16.

What's the impact: Japan JV sales volume growth likely to slow in

2H16E. Unlike other analysts, we assume GAC Toyota’s sales volume

growth will be limited by its capacity constraints until 2018, when it adds

220,000 units, and that it is also facing the impact of a high base effect.

Similarly, we expect this high base to have a negative effect on GAC

Honda, slowing its sales volume growth for 2H16 (-0.1% YoY), vs. a 2%

YoY actual decline for 2Q16 and 27% YoY growth for 1Q16.

GAC Motor also facing high base and slowing margin improvement.

GAC Motor’s sales volume growth is now mostly driven by its Trumpchi

GS4, launched in May 2015. However, given tough competition from

domestic SUV OEMs, and corresponding ASP cuts by peers (Haval 6 and

CS75), we expect its sales growth to slow to around 26% YoY for 2H16E,

from 170% YoY for 1H16. Likewise, we don’t expect GAC Motor’s 2H16E

gross margin to perform as well as it did for 1Q16 (up 5pp YoY, PRC

GAAP), with expansion of only 2.5pp YoY for full-year 2016E.

Despite these headwinds, we raise our overall GAC 2016-18E revenue by

2-7% and core EPS by 1-3% on our overall higher sales volume

assumptions. Accordingly, our 12-month TP rises to HKD8.50, from

HKD8.30, on unchanged target PER of 8x on the average of our 2016-17E

EPS (previously 2016E).

What we recommend: We think the current share price reflects the

market’s expectations of strong 1H16 results, and thus recommend

investors take profit now before investor sentiment turns weak in 2H16. The

current share price implies 2016-17E PERs of 9-10x, which we see as

unattractive, particularly if we factor in the declining popularity of Japanese

brands in China. The key upside risk: stronger-than-expected PV sales.

How we differ: Our target price is lower than the consensus view

(HKD10.5), due mainly to our revised 2016-18E EPS being 9-13% lower

and our target multiple (8x) being lower (consensus: 8.6x). This reflects our

concern that sentiment on the stock would turn weaker in 2H16 on its

slower sales volume growth.

20 July 2016

Guangzhou Automobile Group

Downgrading: time to take profit

Unlike the market, we see lower 2H16 sales growth from Japan JVs

Gross margin for its popular GS4 likely to come under pressure in 2H16

Downgrading our rating on the stock to Sell (5) from Hold (3)

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

Guangzhou Automobile Group (2238 HK)

Target price: HKD8.50 (from HKD8.30)

Share price (19 Jul): HKD10.38 | Up/downside: -18.1%

Kelvin Lau(852) 2848 4467

Brian Lam(852) 2532 4341

Forecast revisions (%)

Year to 31 Dec 16E 17E 18E

Revenue change 1.7 7.1 7.0

Net profit change 0.7 1.8 3.4

Core EPS (FD) change 0.7 1.8 3.4

80

109

138

166

195

4

6

7

9

11

Jul-15 Oct-15 Jan-16 Apr-16

Share price performance

Gzhou Auto (LHS) Relative to HSI (RHS)

(HKD) (%)

12-month range 4.88-10.42

Market cap (USDbn) 8.61

3m avg daily turnover (USDm) 15.41

Shares outstanding (m) 6,435

Major shareholder GZ Auto Industry Grp (57.6%)

Financial summary (CNY)

Year to 31 Dec 16E 17E 18E

Revenue (m) 47,350 52,559 55,456

Operating profit (m) 1,083 1,210 1,292

Net profit (m) 5,625 6,123 6,750

Core EPS (fully-diluted) 0.874 0.951 1.049

EPS change (%) 34.2 8.8 10.2

Daiwa vs Cons. EPS (%) (9.4) (13.3) (11.6)

PER (x) 10.2 9.4 8.5

Dividend yield (%) 3.1 3.4 3.8

DPS 0.282 0.307 0.338

PBR (x) 1.3 1.2 1.1

EV/EBITDA (x) 13.3 10.9 9.1

ROE (%) 13.8 13.6 13.6

2

Guangzhou Automobile Group (2238 HK): 20 July 2016

Table of contents

Time to change direction ......................................................................................... 6

Valuation no longer cheap .................................................................................................6

Japan OEMs sales volume unlikely to surprise ..................................................................7

GAC Motor may see more margin pressure in 2H16 ..........................................................9

GAC Fiat may break even this year, but its earnings contribution is likely to be limited .... 10

Our counter-consensus view ............................................................................................ 12

Valuation and recommendation .............................................................................14

New 12-month target price of HKD8.50 ........................................................................... 14

Risks to our view .............................................................................................................. 14

Appendix ..................................................................................................................16

3

Guangzhou Automobile Group (2238 HK): 20 July 2016

How do we justify our view?

Growth outlook Valuation Earnings revisions

Growth outlook GAC: adjusted net profit and growth

We look for GAC’s net profit to rise by 34% YoY to

CNY5.6bn for 2016, on the back of Japanese JV sale

volume growth of 5-7% (but lower than 1H16). We expect

GAC Motor’s sales in 2016 to be driven by its GS4 model,

boosting GAC Motor’s gross margin by 2-3pp. Meanwhile,

we expect GAC Fiat to turn from a net loss of CNY500m

for 2015 to breaking even on the strong performance of the

Cherokee, but still unlikely to record a net profit due to the

recent additional capacity coming online at its factory in

Guangzhou. For 2017 and 2018, we forecast net profit

growth of 9% YoY and 10% YoY, respectively, mainly

driven by GAC Motor’s growing sales and GAC Fiat’s

improved margin.

Source: Company, Daiwa forecasts

Valuation GAC: 12-month forward PER (x)

We raise our 12-month TP to HKD8.5 (from HKD8.30),

based on an unchanged target PER of 8x on the average

of our 2016-17E EPS, which is at the low end of the target

PER range of 7-11x that we apply to the auto OEMs in our

universe.

We think GAC’s Japanese JV sales volume will be limited

by capacity constraints in 2H16 and affected by the fierce

competition from both the European brands in the tier-1

cities and domestic brands in the lower-tier cities.

Meanwhile, we don’t expect GAC’s domestic brand to be

able to sustain the fat gross margin of 1Q16 as we expect

more promotions due to the competition.

Source: Bloomberg, Daiwa forecasts

Earnings revisions GAC: consensus 2016-17E EPS revisions

We have been seeing the Bloomberg consensus make

upward earnings revisions for the stock since April 2016

due to GAC Motor’s improved gross margin and its

satisfactory 4Q15-1Q16 earnings. However, we think the

current share price now reflects the market’s expectations

for 2016 and 2017. Our EPS forecasts for 2016-17E are

now 9-13% below consensus, as we assume weaker PV

sales volume growth for GAC Honda and GAC Toyota on

the capacity constraints and high base effect, and

because we see limited margin expansion for GAC Motor

due to the severe competition in the domestic SUV market.

Source: Bloomberg

(80%)

(30%)

20%

70%

120%

170%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2011 2012 2013 2014 2015E 2016E 2017E 2018E

Net profit (LHS) YoY Growth (RHS)

(CNYm)

5

7

9

11

13

15

Jul-1

3

Sep

-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep

-15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

PER +1 SD Average PER -1 SD

(PER)

0.35

0.45

0.55

0.65

0.75

0.85

0.95

1.05

1.15

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb

-16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

(CNY)

2016E 2017E

4

Guangzhou Automobile Group (2238 HK): 20 July 2016

Financial summary

Key assumptions

Profit and loss (CNYm)

Cash flow (CNYm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Volume - GAC Honda (unit) 362,000 316,000 435,000 480,000 580,000 620,000 634,000 646,000

Volume - GAC Toyota (unit) 274,000 250,000 303,000 374,000 403,000 418,000 430,000 450,000

Volume - GAC Motor (unit) 31,000 59,000 109,000 135,000 195,000 328,000 373,000 384,000

Volume Growth - GAC Honda (%) (6.2) (12.7) 37.7 10.3 20.8 6.9 2.3 1.9

Volume Growth - GAC Toyota (%) 1.9 (8.8) 21.2 23.4 7.8 3.7 2.9 4.7

Volume Growth - GAC Motor (%) (20.5) 90.3 84.7 23.9 44.4 68.2 13.7 2.9

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Vehcicle-related operations 10,719 12,713 18,124 21,560 28,285 45,877 50,791 53,335

Other revenue 266 251 700 823 1,133 1,473 1,767 2,121

Other Revenue 0 0 0 0 0 0 0 0

Total Revenue 10,984 12,964 18,824 22,383 29,418 47,350 52,559 55,456

Other income 836 8 117 357 412 663 736 776

COGS (10,560) (12,274) (16,830) (19,831) (25,975) (40,633) (45,094) (47,565)

SG&A (1,806) (2,147) (2,784) (3,724) (3,904) (6,298) (6,990) (7,376)

Other op.expenses 0 0 0 0 0 0 0 0

Operating profit (545) (1,449) (672) (814) (48) 1,083 1,210 1,292

Net-interest inc./(exp.) (41) (193) (169) (307) (310) (166) (168) (156)

Assoc/forex/extraord./others 4,643 2,641 3,470 4,187 4,744 5,152 5,563 6,146

Pre-tax profit 4,057 1,000 2,629 3,066 4,386 6,068 6,605 7,283

Tax 110 65 (101) (131) (400) (759) (826) (910)

Min. int./pref. div./others 105 69 124 259 226 316 343 379

Net profit (reported) 4,272 1,134 2,653 3,194 4,212 5,625 6,123 6,749

Net profit (adjusted) 4,272 1,134 2,653 3,194 4,212 5,625 6,123 6,750

EPS (reported)(CNY) 0.695 0.178 0.412 0.496 0.654 0.874 0.951 1.049

EPS (adjusted)(CNY) 0.695 0.178 0.412 0.496 0.654 0.874 0.951 1.049

EPS (adjusted fully-diluted)(CNY) 0.695 0.178 0.412 0.496 0.652 0.874 0.951 1.049

DPS (CNY) 0.209 0.091 0.160 0.160 0.200 0.282 0.307 0.338

EBIT (545) (1,449) (672) (814) (48) 1,083 1,210 1,293

EBITDA (55) (781) 279 402 1,600 2,934 3,411 3,856

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Profit before tax 4,057 1,000 2,629 3,066 4,386 6,068 6,605 7,283

Depreciation and amortisation 490 668 951 1,216 1,648 1,851 2,201 2,564

Tax paid (81) (117) (172) (85) (91) (759) (826) (910)

Change in working capital (422) 1,555 566 614 3,115 243 433 235

Other operational CF items (4,677) (2,621) (3,426) (4,463) (5,167) (4,415) (4,727) (5,239)

Cash flow from operations (633) 485 548 348 3,891 2,989 3,686 3,933

Capex (2,244) (2,948) (1,904) (3,513) (4,322) (5,025) (5,206) (5,396)

Net (acquisitions)/disposals (1,079) (1,307) (1,077) (89) (1,938) 0 0 0

Other investing CF items 3,056 6,585 3,689 348 7,002 3,776 4,121 4,451

Cash flow from investing (267) 2,329 708 (3,254) 742 (1,249) (1,085) (945)

Change in debt 429 38 4,041 28 (2,469) 2,000 1,500 1,000

Net share issues/(repurchases) 0 0 0 0 0 0 0 1

Dividends paid (686) (1,757) (538) (1,172) (1,068) (1,287) (1,813) (1,974)

Other financing CF items 56 (31) 9 242 165 (487) (587) (659)

Cash flow from financing (201) (1,749) 3,512 (902) (3,372) 226 (900) (1,631)

Forex effect/others 0 0 0 0 0 0 0 1

Change in cash (1,102) 1,065 4,767 (3,807) 1,260 1,966 1,701 1,357

Free cash flow (2,877) (2,463) (1,356) (3,164) (431) (2,036) (1,520) (1,463)

5

Guangzhou Automobile Group (2238 HK): 20 July 2016

Financial summary continued …

Balance sheet (CNYm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

As at 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Cash & short-term investment 8,239 9,316 14,083 10,274 11,548 13,514 15,216 16,573

Inventory 1,537 1,397 2,036 2,661 1,927 3,386 3,758 3,964

Accounts receivable 2,980 3,303 4,725 5,516 8,727 15,152 16,819 17,746

Other current assets 8,903 6,258 5,669 8,434 5,696 5,696 5,696 5,696

Total current assets 21,659 20,274 26,514 26,886 27,898 37,748 41,488 43,978

Fixed assets 4,309 5,927 7,366 8,544 10,581 13,247 15,864 18,430

Goodwill & intangibles 3,257 4,141 4,234 5,547 6,647 7,155 7,543 7,811

Other non-current assets 15,388 19,091 19,729 21,486 22,094 23,469 24,912 26,606

Total assets 44,612 49,434 57,843 62,463 67,220 81,620 89,807 96,825

Short-term debt 2,100 2,515 9,397 9,541 4,279 3,279 2,779 2,779

Accounts payable 4,069 6,376 8,637 10,651 14,077 22,021 24,438 25,777

Other current liabilities 37 139 25 41 300 484 537 566

Total current liabilities 6,206 9,030 18,059 20,232 18,656 25,783 27,754 29,123

Long-term debt 7,737 7,776 4,775 4,769 7,649 10,649 12,649 13,649

Other non-current liabilities 483 564 893 1,212 1,424 1,424 1,424 1,424

Total liabilities 14,426 17,370 23,727 26,214 27,728 37,855 41,826 44,195

Share capital 6,148 6,435 6,435 6,435 6,435 6,435 6,435 6,436

Reserves/R.E./others 23,062 24,707 26,876 29,018 32,211 36,550 40,859 45,637

Shareholders' equity 29,210 31,142 33,311 35,453 38,647 42,985 47,294 52,073

Minority interests 976 922 805 796 845 779 686 557

Total equity & liabilities 44,612 49,434 57,843 62,463 67,220 81,620 89,807 96,825

EV 45,809 42,632 40,086 43,756 40,363 38,957 37,219 35,040

Net debt/(cash) 1,598 975 89 4,036 379 413 212 (145)

BVPS (CNY) 4.751 4.894 5.177 5.509 6.006 6.680 7.350 8.092

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Sales (YoY) 25.6 18.0 45.2 18.9 31.4 61.0 11.0 5.5

EBITDA (YoY) n.a. n.a. n.a. 44.0 298.2 83.3 16.3 13.0

Operating profit (YoY) n.a. n.a. n.a. n.a. n.a. n.a. 11.7 6.9

Net profit (YoY) (0.5) (73.5) 133.9 20.4 31.9 33.6 8.8 10.2

Core EPS (fully-diluted) (YoY) (24.4) (74.4) 131.3 20.4 31.3 34.2 8.8 10.2

Gross-profit margin 3.9 5.3 10.6 11.4 11.7 14.2 14.2 14.2

EBITDA margin n.a. n.a. 1.5 1.8 5.4 6.2 6.5 7.0

Operating-profit margin n.a. n.a. n.a. n.a. n.a. 2.3 2.3 2.3

Net profit margin 38.9 8.7 14.1 14.3 14.3 11.9 11.6 12.2

ROAE 15.6 3.8 8.2 9.3 11.4 13.8 13.6 13.6

ROAA 10.3 2.4 4.9 5.3 6.5 7.6 7.1 7.2

ROCE n.a. n.a. n.a. n.a. n.a. 2.0 2.0 2.0

ROIC (1.9) (4.5) (1.9) (2.1) (0.1) 2.3 2.3 2.2

Net debt to equity 5.5 3.1 0.3 11.4 1.0 1.0 0.4 net cash

Effective tax rate n.a. n.a. 3.8 4.3 9.1 12.5 12.5 12.5

Accounts receivable (days) 96.8 88.4 77.8 83.5 88.4 92.0 111.0 113.7

Current ratio (x) 3.5 2.2 1.5 1.3 1.5 1.5 1.5 1.5

Net interest cover (x) n.a. n.a. n.a. n.a. n.a. 6.5 7.2 8.3

Net dividend payout 30.1 51.1 38.8 32.2 30.6 32.2 32.2 32.2

Free cash flow yield n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Company profile

GAC is engaged in the manufacturing of vehicles and parts, as well as automobile finance and

insurance and related services. It sells passenger vehicles under the Trumpchi marque, passenger

and commercial vehicles under Gonow, SUVs under Changfeng Motor, and buses under GAC Bus.

GAC has also formed JVs with a number of foreign brands, including Honda, Toyota, Mitsubishi and

Fiat to sell passenger vehicles. It sells commercial vehicles through its GAC Bus and GAC Hino

businesses.

6

Guangzhou Automobile Group (2238 HK): 20 July 2016

Time to take profit

Valuation no longer cheap

Time to take a more rational view

The stock is now trading at 2016-17 PERs of 9-10x on our forecasts, which is at the high

end of the range for the conventional auto OEMs (7-11x), and higher than its past-3-year

average 12-month-forward PER of 9x. This includes the 2H13 period, when its PER was at

a high premium to peers due to what see as overly optimistic sentiment on GAC’s earnings

growth for 2013 and 2014.

GAC’s PER reverted to its normal level after 2H13, breaking the 10x level only in 1H15

when the Hang Seng Index rallied strongly on the back of positive sentiment on China’s

stock market due to the launch of the Shanghai-Hong Kong Stock Connect. Thus, we think

the stock’s current valuation is now demanding, especially considering its slowing sales

volume growth and likely lower magnitude of margin improvement in 2H16E vs. 1H16 for

its key brands GAC Honda, GAC Toyota and GAC Motor.

GAC: 12-month forward PER bands (x)

Source: Bloomberg, Daiwa Forecasts

5

6

7

8

9

10

11

12

13

14

15

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb

-16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

PER +1 SD Average PER -1 SD

(PER)

The stock is now trading

at a higher valuation

than its peers and above

its past-3-year average

7

Guangzhou Automobile Group (2238 HK): 20 July 2016

Global automotive OEMs: valuation comparison

Name Bloomberg Trading Share price Rating PER (x) PBR (x) EV/EBITDA(x) Div yield (%) ROE (%)

Code Currency 19-Jul-16 FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E

China H-share listed

Geely Automobile Holdings Lt * 175 HK HKD 4.83 Buy 10.9 9.3 1.6 1.4 4.6 3.5 1.1 1.3 16.0 16.2

BAIC Motor Corp Ltd-H * 1958 HK HKD 6.18 Sell 10.7 9.8 1.1 1.0 4.7 3.8 3.2 3.5 10.4 10.5

BYD Co Ltd-H * 1211 HK HKD 52.55 Buy 23.4 19.6 2.4 2.1 10.4 9.1 n.a. n.a. 11.9 10.9

Great Wall Motor Company-H * 2333 HK HKD 7.05 Hold 7.7 7.5 1.3 1.2 5.1 4.9 4.0 4.1 17.6 16.1

Guangzhou Automobile Group-H * 2238 HK HKD 10.38 Sell 10.2 9.4 1.3 1.2 13.3 10.9 3.1 3.4 13.8 13.6

Dongfeng Motor Grp Co Ltd-H * 489 HK HKD 8.78 Outperform 5.5 5.2 0.7 0.6 7.7 5.8 2.8 2.9 13.3 12.5

Brilliance China Automotive * 1114 HK HKD 8.84 Buy 11.1 8.9 1.7 1.4 n.a. n.a. 1.1 1.4 16.2 17.4

China A-share listed

Byd Co Ltd -A 002594 CH CNY 62.80 NR 33.1 28.4 4.0 3.5 16.4 14.3 0.0 0.0 13.0 13.6

Guangzhou Automobile Group-A 601238 CH CNY 23.50 NR 24.0 19.9 3.4 3.0 37.8 33.3 0.0 0.0 14.9 16.0

Great Wall Motor Co Ltd-A 601633 CH CNY 9.89 NR 10.7 9.6 2.0 1.8 6.4 6.1 0.0 0.0 20.6 19.4

Saic Motor Corp Ltd-A 600104 CH CNY 21.72 NR 7.7 7.3 1.3 1.2 10.7 9.1 0.1 0.1 17.1 16.8

Chongqing Changan Automobi-B 200625 CH HKD 12.10 NR 4.3 4.0 1.1 1.0 24.8 10.8 0.1 0.1 29.1 25.9

Faw Car Company Limited-A 000800 CH CNY 10.82 NR 318.2 470.4 2.0 1.9 17.0 14.9 n.a. n.a. 6.9 6.8

Anhui Jianghuai Auto Co-A 600418 CH CNY 12.60 NR 15.5 12.7 1.8 1.6 7.6 8.4 0.0 0.0 12.4 13.8

Jiangsu Yueda Investment C-A 600805 CH CNY 9.65 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Tianjin Faw Xiali Automobi-A 000927 CH CNY 5.24 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Lifan Industry Group Co Lt-A 601777 CH CNY 11.68 NR 21.6 16.7 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Haima Automobile Group Co-A 000572 CH CNY 5.31 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Shenyang Jinbei Automotive-A 600609 CH CNY 4.88 NR n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

US

Tesla Motors Inc TSLA US USD 225.26 NR 819.1 89.3 17.5 14.6 47.1 24.6 n.a. n.a. n.a 12.3

Ford Motor Co * F US USD 13.65 Hold 6.6 6.6 1.6 1.4 3.0 3.0 0.0 0.0 29.5 22.9

General Motors Co * GM US USD 31.25 Outperform 5.5 5.4 1.1 0.9 2.5 2.5 0.0 0.1 22.2 18.8

Europe

Daimler Ag-Registered Shares DAI GR EUR 57.43 NR 7.3 6.9 1.1 1.0 2.2 2.1 0.1 0.1 15.7 15.0

Bayerische Motoren Werke AG BMW GR EUR 73.16 NR 7.6 7.5 1.0 1.0 6.2 6.1 0.0 0.0 14.1 13.2

Volkswagen AG VoW GR EUR 126.75 NR 6.9 6.0 0.7 0.6 1.4 1.3 0.0 0.0 9.9 10.2

Fiat Chrysler Automobiles NV FCA IM EUR 5.99 NR 4.4 3.5 0.5 0.5 1.5 1.4 0.0 0.0 12.3 14.2

Peugeot SA UG FP EUR 11.84 NR 7.4 6.5 0.9 0.8 1.4 1.4 0.0 0.0 12.8 13.6

Renault SA RNO FP EUR 74.22 NR 6.3 5.6 0.7 0.6 3.4 3.2 0.0 0.0 11.5 12.0

Japan

Honda Motor Co Ltd *, ** 7267 JP JPY 2824.50 Hold 9.3 10.4 0.7 0.7 6.9 7.4 0.0 0.0 7.7 7.1

Nissan Motor Co Ltd *, ** 7201 JP JPY 1043.00 Hold 7.8 7.8 0.9 0.8 2.6 2.7 0.0 0.0 11.2 10.7

Toyota Motor Corp *, ** 7203 JP JPY 5784.00 Outperform 7.7 10.6 1.0 1.0 8.4 10.7 0.0 0.0 13.4 9.9

Korea

Hyundai Motor Co * 005380 KS KRW 130000.00 Buy 5.4 5.2 0.4 0.4 4.2 3.8 3.5 4.0 9.7 9.4

Kia Motors Corp * 000270 KS KRW 41700.00 Outperform 5.9 5.6 0.6 0.6 3.4 3.0 2.9 3.1 11.2 10.7

India

Tata Motors Ltd ** TTMT IN INR 499.25 NR 14.2 10.7 2.2 1.8 4.9 4.1 0.0 0.0 16.4 17.8

Mahindra & Mahindra Ltd ** MM IN INR 1456.60 NR 25.4 20.0 3.2 2.9 14.6 11.8 0.0 0.0 12.4 14.2

Total Weighted average 39.9 13.4 1.8 1.6 8.2 7.3 0.4 0.4 14.1 13.1

High 819.1 470.4 17.5 14.6 47.1 33.3 4.0 4.1 29.5 25.9

Low 4.3 3.5 0.4 0.4 1.4 1.3 0.0 0.0 6.9 6.8

Median 7.8 8.9 1.2 1.1 6.2 5.8 0.0 0.0 13.3 13.6

Source: Bloomberg, *Daiwa forecasts Note: **Mar year-end Pricing as at 19 July 2016

Japan OEMs sales volume unlikely to surprise

Capacity constraints put the brakes on GAC Toyota

According to our discussion with management this week, GAC Toyota hasn't changed its

plans to expand annual capacity by 220,000 units, and this will come online by end-2017

or January 2018. For 1H16, GAC Toyota reported 8% YoY sales volume growth to 209,000

units (approximately 35,000 units a month), mainly due to an increase in the sales of its

Levin sedan (launched in August 2014, its new hybrid launched in March 2016) and its new

version of the Highlander, launched in March 2015.

This is close to its current monthly capacity of close to 32,000 units per month (or 380,000

units a year). However, in our view, 2H16 will be partly affected by the high base in 2H15

(especially for the Highlander) and the likely weak performance of the Camry, whose sales

volume declined by 26.9% YoY in 1H16. We estimate that GAC Toyota would report sales

volume growth of 5% for 2016 and 1% YoY for 2017, with a utilisation rate of 112% and

113%, respectively.

Will likely reach capacity

bottleneck in 2016

8

Guangzhou Automobile Group (2238 HK): 20 July 2016

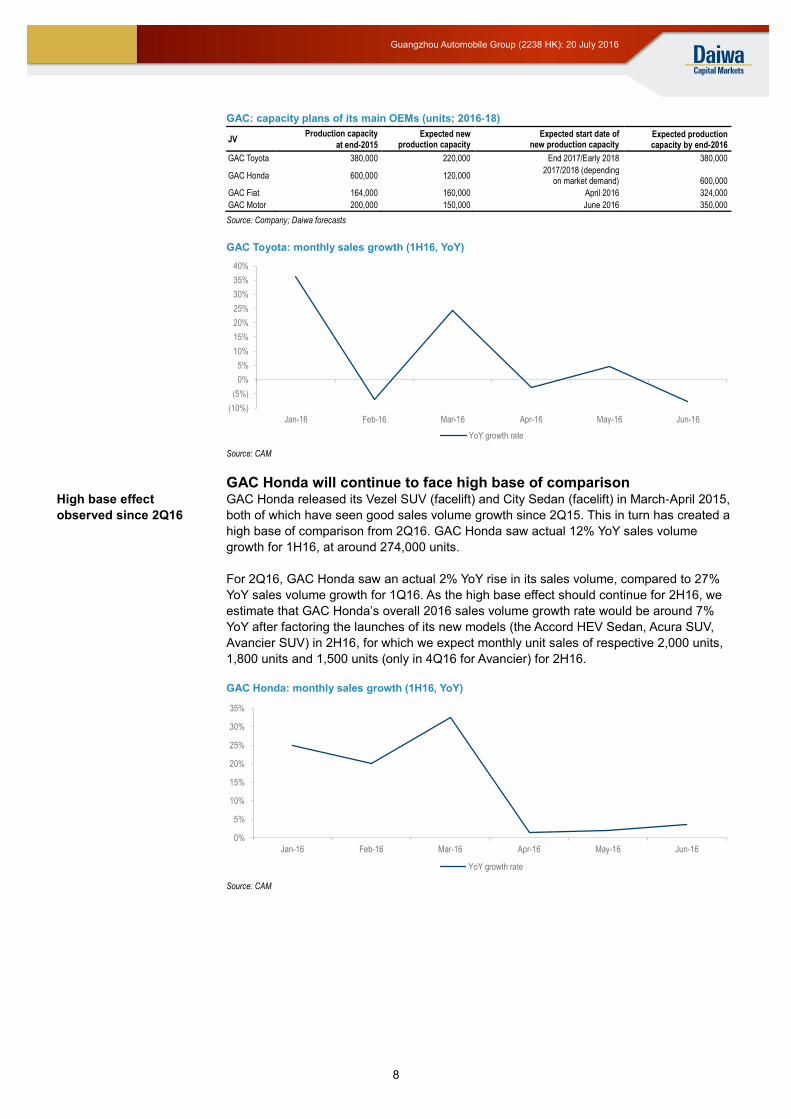

GAC: capacity plans of its main OEMs (units; 2016-18)

JV Production capacity

at end-2015

Expected new production capacity

Expected start date of new production capacity

Expected production capacity by end-2016

GAC Toyota 380,000 220,000 End 2017/Early 2018 380,000

GAC Honda 600,000 120,000 2017/2018 (depending

on market demand) 600,000

GAC Fiat 164,000 160,000 April 2016 324,000

GAC Motor 200,000 150,000 June 2016 350,000

Source: Company; Daiwa forecasts

GAC Toyota: monthly sales growth (1H16, YoY)

Source: CAM

GAC Honda will continue to face high base of comparison GAC Honda released its Vezel SUV (facelift) and City Sedan (facelift) in March-April 2015,

both of which have seen good sales volume growth since 2Q15. This in turn has created a

high base of comparison from 2Q16. GAC Honda saw actual 12% YoY sales volume

growth for 1H16, at around 274,000 units.

For 2Q16, GAC Honda saw an actual 2% YoY rise in its sales volume, compared to 27%

YoY sales volume growth for 1Q16. As the high base effect should continue for 2H16, we

estimate that GAC Honda’s overall 2016 sales volume growth rate would be around 7%

YoY after factoring the launches of its new models (the Accord HEV Sedan, Acura SUV,

Avancier SUV) in 2H16, for which we expect monthly unit sales of respective 2,000 units,

1,800 units and 1,500 units (only in 4Q16 for Avancier) for 2H16.

GAC Honda: monthly sales growth (1H16, YoY)

Source: CAM

(10%)

(5%)

0%

5%

10%

15%

20%

25%

30%

35%

40%

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

YoY growth rate

0%

5%

10%

15%

20%

25%

30%

35%

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

YoY growth rate

High base effect

observed since 2Q16

9

Guangzhou Automobile Group (2238 HK): 20 July 2016

GAC Honda: the Acura GAC Honda: the Avancier

Source: Hexun media Source: Autohome

GAC Motor may see more margin pressure in 2H16

High base likely to weigh on GAC Motor’s sales volume growth

GAC Motor achieved actual sales volume growth of 170% YoY for 1H16 due to strong

sales of its Trumpchi GS4, which was launched in May 2015. However, we believe the high

base in 2H15 will cap the 2H16 YoY sales growth rate at 26%, after factoring in the

contribution from several of its new models (GS8, GS4EV, GS3S PHEV) to be launched in

2H16, resulting in 73% YoY sales growth for 2016, on our estimates.

GAC Motor: monthly sales volume breakdown for 2015 and 1H16

Source: CAM

Improved gross margin for Trumpchi GS4 may not be sustainable in 2H16

GAC Motor’s gross margin rose significantly in 1Q16 (around a 5pp improvement from the

12% for 2015), mainly on the back of economies of scale for the GS4 SUV. But we do not

think such a strong margin can be sustained due to the tougher competition. The increase

in peers’ promotions and more competition from models such as GWM’s Haval H6 and

Changan’s CS75 is likely to have an impact on the selling price of the GS4 in 2H16, which

will be reflected in its gross margin for 2016, in our view. Also, we think GAC Motor’s

150,000 unit new capacity additions, due to start operations in 3Q16, will further weigh on

the business’s gross margin.

China autos OEMs: official price cuts by the main domestic SUVs makers

Automobile OEMs Models Selling price range

currently (CNY’000) Official price cut

(CNY’000) Official price

cut date Avg sales units

per month in 1H16

GAC Trumpchi GS4 100-154 n.a n.a 25,133

Changan CS75 93-158 4-10 Mar-16 16,143

Greatwall Haval H6 88-163 5-30 Mar-16 40,042

Geely Boyue (NL3) 100-158 n.a n.a 4,803

Source: CAM, Autohome,

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb

-16

Mar

-16

Apr

-16

May

-16

Jun-

16

(units)

GS4 GS5 Others

Margin pressure

expected due to likely

ASP declines and new

capacity

10

Guangzhou Automobile Group (2238 HK): 20 July 2016

China autos OEMs: main domestic SUV monthly sales in 1H16

Source: CAM

Apart from the Trumpchi GS4 models, we do not expect GAC Motor to launch any other

models that will be as popular in the near term. All of its models, except for the GS4,

recorded actual negative sales growth for 1H16. For example, the recently launched

version of the GS5, the GS5 Super, has not been well received by consumers.

For 2H16, GAC Motor will launch 3 new models — the GS8 SUV, GA3S PHEV Sedan and

GS4 EV SUV — but we don’t expect any of these to become flagship models for GAC

Motor. The GS8 SUV (to be launched in September/October 2016), positioned at the same

price point as the Haval H8/H9, is likely to be threatened by a number of foreign JV SUVs.

Meanwhile, we estimate that GAC Motor’s NEV models would account for only around

1,000 units a month once they are launched in 3Q16, as the market is still small and GAC

Motor is also fairly new.

GAC Motor: the Trumpchi GS8

Source: Autohome

GAC Fiat may break even this year, but its earnings contribution is likely to be limited

Ramp-up of Cherokee should be a sales driver for GAC Fiat

GAC Fiat launched its Cherokee model in November 2015, and quickly ramped up

production soon afterwards. The Cherokee SUV recorded monthly sales of 8,500-9,200

units for March 2016 to June 2016, and we believe its sales volume will hold steady at this

level for the remainder of 2016.

0

10,000

20,000

30,000

40,000

50,000

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

(units)

Trumpchi CS4 Changan CS75 GWM Haval H6 Geely Boyue (NL3)

GS5 cannot extend the

momentum from GS4

Cherokee and Renegade

are key models for GAC

Fiat

11

Guangzhou Automobile Group (2238 HK): 20 July 2016

GAC Fiat: monthly sales volume breakdown since Cherokee launch

Source: CAM

We see the Cherokee and the recently launched Renegade SUV being the main drivers of

our forecast 254% YoY sales volume growth for GAC Fiat to 146,000 units in 2016.

However, sales volumes for GAC Fiat’s Ottimo and Viaggio sedans were down 26% YoY

and 56% YoY for 1H16, respectively, and we expect its sedan sales to continue to weaken

in 2016 amid tough competition.

New capacity in Guangzhou likely to weigh on profits from Changsha

The Cherokee racked up total sales of 50,000 units in 1H16, during which time GAC Fiat’s

sedan sales totalled 9,000 units, almost fully utilising GAC Fiat’s Changsha plant’s annual

capacity (140K units). However, we believe the sales volume of the new Renegade won’t

come close to reaching the annual capacity of the Guangzhou factory (160k units) this

year, which suggests to us that GAC Motor will face further margin pressure in 2H16.

GAC Fiat: sales volume estimates and utilisation-rate analysis

Source: Company, Daiwa estimates

Launched in June, the Renegade faces intense competition in China and as a result is

unlikely to be a strong sales performer this year, in our view. Unlike the Cherokee, one of

Fiat’s best-selling models globally, the Renegade (launched globally at end-2014) does not

yet seem to be well recognised by customers in China. Priced at between CNY140,000

and CNY210,000, the Renegade faces competition from domestic SUVs such as the GWM

Haval H6, Changan CS75, Geely Boyue and foreign SUVs such as the Honda CR-V,

Toyota RAV4 and Nissan X-Trail, in our view. Renegade’s current order book of around

6,000 units is not an exciting number, in our opinion.

Hence, we believe the subdued performance of the Renegade is likely to result in loss-

making operations for the Guangzhou plant this year, which would wipe out profits earned

from the Cherokee in 2016. Nevertheless, on our forecasts, GAC Fiat would reach break-

even in 2016, moving into the black from a net loss of CNY500m for 2015.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

Cherokee Renegade Ottimo Viaggio

0%

10%

20%

30%

40%

50%

60%

70%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2013 2014 2015 2016E 2017E

(units)

Capacity (LHS) Sales volume (LHS) Utilisation rate (RHS)

We believe the

Renegade faces fierce

competition that will lead

to low utilisation of the

new Guangzhou plant

12

Guangzhou Automobile Group (2238 HK): 20 July 2016

China auto OEMs: comparison of key SUV models

Automotive OEM Model Retail Price

(CNY k) Launch date Launch date of latest facelift Avg sales units per month in 1H16

GAC Fiat Renegade 140-210 Jun-16 Jun-16 n.a

Greatwall Haval 6 88-163 Oct-12 Apr-16 40,042

Changan CS75 93-158 Apr-14 Mar-16 16,143

Geely Boyue (NL3) 100-158 Mar-16 Mar-16 4,803

DF Honda CR-V 180-250 Feb-12 Apr-15 14,247

FAW Toyota RAV4 184-273 Aug-09 Dec-15 8,714

DF Nissan X-rail 182-270 Feb-14 Mar-16 13,493

Changan Mazda CX5 170-250 Aug-13 Jun-15 3,722

Source: CAM, Autohome

GAC Fiat: Cherokee GAC Fiat: Renegade

Source: Sina Source: Sina

Our counter-consensus view

Compared with the market, we are more concerned about the gross profit contribution from the Japan JVs and GAC Motor’s gross margin

We believe the main reason for the 9-13% variance between our 2016-18E earnings

forecasts and those of the Bloomberg consensus is the assumed investment income

contributed by GAC Toyota and GAC Honda. GAC Honda and GAC Toyota would

collectively contribute 70-80% of the implied investment income in 2016 and 2017, on our

forecasts. However, due to the low base effect and capacity constraints, we believe GAC’s

2 Japan JVs will see limited sales growth starting from 2H16, leading to less implied

investment income than the street currently expects. Hence, we believe the market is

overly optimistic on the sales growth of GAC Toyota and GAC Honda for 2H16.

For GAC Motor, we forecast the domestic brand to generate higher sales volume (relative

to our prior forecasts), backed by its forthcoming models for 2H16 (GS8 SUV, GA3S PHEV

Sedan and GS4 EV SUV), which results in a higher revenue forecast than the Bloomberg

consensus expects for 2016. As it stands, we believe that not all analysts have fully

factored in the impact of the forthcoming models.

However, we highlight our non-consensus view on GAC Motor’s gross margin, which we

believe is a more sensitive factor than revenue as far as determining GAC Motor’s net

earnings is concerned. Our 2016-17E gross-margin forecasts for GAC Motor are lower

than the market’s given our expectation of a continuation of tough competition in the

domestic SUV segment, which we think will result in the net profit contribution from the

domestic brand falling short of the market’s expectations.

In contrast to the market’s average 12-month target price of HKD10.5, which implies PERs

of 9.2x for 2016, 8.1x for 2017E and 8.6x on average 2016E-17E EPS (all based on the

Bloomberg consensus), our target price of HKD8.5 is set at 8x the average of our 2016E-

17E EPS forecasts (equivalent to 8.3x PER for 2016E and 7.6x PER for 2017E). Our lower

absolute target price is a function of our more conservative EPS forecasts, as well as our

lower target multiple, which we believe is justified by our expectation of weaker investor

sentiment in 2H16 given slower sales growth.

We are more bearish

than the street on sales

volume growth for GAC

Toyota and GAC Honda

in 2H16E…

…and more cautious on

GAC Motor’s gross

margin

We think investor

sentiment is likely to

cool in the face of slower

sales growth

13

Guangzhou Automobile Group (2238 HK): 20 July 2016

GAC: Daiwa forecasts vs. Bloomberg consensus on key financial metrics

Revenue (CNY m)

Gross profit (CNY m)

Operating profit (CNY m)

Implied Investment Income (CNY m) Net Profit (CNY m)

2016E 2017E 2016E 2017E 2016E 2017E 2016E 2017E 2016E 2017E

Daiwa forecasts 47,350 52,559 6,716 7,465 1,083 1,210 4,986 5,395 5,625 6,123

Bloomberg consensus 40,439 44,521 6,389 6,545 1,644 1,820 5,136 5,850 6,227 7,082

Gross margin Operating margin

Daiwa forecasts

14.2% 14.2% 2.3% 2.3%

Bloomberg consensus

15.8% 14.7% 4.1% 4.1%

Source: Daiwa forecast, Bloomberg Note :Implied investment income refers to the difference between pretax income and operating income as disclosed by Bloomberg, which is the

approximate value of investment income. For consistency, we use the same method to get the implied investment income for Daiwa forecasts

GAC: Daiwa forecasts vs. Bloomberg consensus on target price/valuation

12-month target price (HKD)

Estimated EPS (CNY) Implied target PER

2016E 2017E 2016E-17E

average 2016E 2017E 2016E-17E

average

Daiwa forecasts 8.5 0.87 0.95 0.91 8.3 7.6 8.0

Bloomberg consensus 10.5 0.97 1.10 1.04 9.2 8.1 8.6

Exchange rate, 1HK$ = x CNY 0.85

Source: Bloomberg, Daiwa forecasts

GAC: sales volume/gross margin sensitivity analysis

Assuming a 5% change in the sales volume and the impact on the 2016E net profit (%)

GAC

0.8%

Assuming a 1pp change in the gross margin and the impact on the 2016E net profit (%)

GAC

7.6%

Source: Daiwa estimates

14

Guangzhou Automobile Group (2238 HK): 20 July 2016

Valuation and recommendation

New 12-month target price of HKD8.50

We downgrade our rating on GAC to Sell (5) from Hold (3), and raise our 12-month target

price to HKD8.5 from HKD8.3, on an unchanged 8x PER applied to the average of 2016E-

17E EPS (previously: 2016E only). Our new target price implies 18% potential downside.

We foresee the sales growth of GAC Honda and GAC Toyota being limited in 2016 and

2017 by capacity constraints and harsh competition from European brands in tier-1 cities

and domestic brands in lower-tier cities. On the other hand, we believe GAC Motor will not

sustain the strong margin it recorded in 1Q16, as we expect it to step up promotional

activity in response to the intense competition in the domestic SUV market in 2H16.

Although GAC Honda, GAC Toyota and GAC Motor saw significant YoY sales growth in

1H16, we believe the high-base effect starting from 2H16 will weigh on their overall YoY

sales growth in full-year 2016.

GAC: PER bands (x)

Source: Bloomberg, Daiwa forecasts

GAC: PER-based valuation

2016-17 EPS Average (CNY) 0.91

PE (X) 8.0 x

Exchange rate, 1HK$ = x CNY 0.85

Equity value/share (HKD/share) 8.50

Current price (HKD) (19 July 2016) 10.38

Potential share price upside/downside (%) -18%

Implied target 17E PER 7.6

Source: Daiwa forecasts

Risks to our view

Stronger-than-expected sales for GAC Honda and GAC Toyota

The main risk to our Sell (5) call on GAC is the performance of its Japanese JVs. Although

we believe the capacity constraints and the extent of market competition will limit its sales

growth in 2016 and 2017, GAC Honda’s new SUV models (Acura, Avancier) could perform

better sales-wise than we expect. Also, GAC Toyota could benefit more from its HEV

models than we currently expect.

Weaker-than-expected competition for Trumpchi GS4

Though official price cuts for Trumpchi GS4’s competitors (Greatwall Haval H6, Changan

CS75) underline the extent of competition in the market, there is a possibility that Trumpchi

will maintain its high 4Q15-1Q16 gross margin due to scale economies, presenting an

upside risk to our earnings forecasts.

5

6

7

8

9

10

11

12

13

14

15

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb

-16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

PER +1 SD Average PER -1 SD

(PER)

We downgrade our

rating given our

concerns over the sales

growth of the Japanese

JVs and the margin of

GAC Motor

15

Guangzhou Automobile Group (2238 HK): 20 July 2016

Other company-specific risks include a better-than-expected net margin for GAV Fiat on its

strong SUV performance, and unexpectedly aggressive sales growth for the domestic GAC

Motor brand’s new models to be launched in 2H16.

16

Guangzhou Automobile Group (2238 HK): 20 July 2016

Appendix

GAC: monthly sales for major GAC OEMs in the past 12 months

3Q15 3Q15 3Q15 4Q15 4Q15 4Q15 1Q16 1Q16 1Q16 2Q16 2Q16 2Q16

Sales volume (units) Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

GAC Honda in total 41,984 43,202 50,006 47,423 53,306 99,598 43,008 26,298 53,238 49,012 52,333 50,096

Fit 10,051 8,185 3,372 2,840 8,747 13,147 9,326 6,814 11,455 8,882 8,978 9,629

City 3,471 3,005 6,332 7,632 4,976 8,462 5,370 3,375 4,643 5,145 5,389 5,494

S1 281 278 279 272 6 500 0 1,023 150 234 1,967 780

Crider 6,057 8,930 11,572 11,295 7,819 21,075 7,738 4,261 9,627 5,515 6,002 4,824

Accord 7,927 8,128 11,619 10,102 13,203 27,362 4,779 2,089 10,081 11,402 12,121 11,668

Crosstour 709 883 1,030 942 914 2,032 613 467 615 879 590 632

Vezel 10,085 9,928 11,721 10,790 13,587 18,329 11,998 6,489 14,163 14,193 14,398 14,124

Odyssey 3,403 3,865 4,081 3,550 4,054 8,691 3,184 1,780 2,504 2,762 2,888 2,945

GAC Toyota in total 34,026 31,045 33,014 38,012 37,757 35,782 45,009 18,530 35,524 35,052 38,819 35,818

Yaris 5,830 5,440 4,603 4,476 5,842 3,669 8,544 3,545 4,738 4,949 5,197 3,941

Levin 9,583 8,460 10,357 13,068 11,652 13,569 14,447 6,190 13,994 13,820 15,073 14,592

Camry 9,517 8,500 9,779 10,659 11,212 9,562 13,209 4,119 8,091 7,416 9,346 8,179

Highlander 8,014 7,697 7,907 9,125 8,296 8,795 8,010 4,276 8,393 8,494 8,513 8,413

EZ 1,082 948 368 684 755 187 799 400 308 373 690 693

GAC Motor in total 13,642 16,005 21,867 24,523 28,091 24,500 33,150 16,235 30,053 28,017 30,102 28,560

GA3 510 521 1,170 1,311 1,005 335 688 100 406 758 1,354 396

GA5 61 101 15 183 61 364 206 124 200 320 571 154

GA5 EV 111 142 163 0 0 0 0 0 0 0 0 0

GA6 305 395 619 634 405 408 213 138 650 1,020 1,082 1,088

GA8 0 0 0 0 0 0 0 0 0 0 215 509

GS5 517 529 1,000 1,343 1,970 608 1,531 853 746 846 861 293

GS4 12,138 14,317 18,900 21,052 24,650 22,785 30,512 15,020 28,051 25,073 26,019 26,120

GAC Fiat in total 2,603 2,112 2,100 2,521 4,622 8,357 10,366 7,160 10,742 11,467 9,811 11,232

Ottimo 872 697 829 840 961 1,026 804 448 723 826 411 382

Viaggio 1,731 1,415 1,271 1,681 1,490 1,497 1,255 799 1,015 1,440 496 470

Cherokee 0 0 0 0 2,171 5,834 8,307 5,913 9,004 9,201 8,904 8,702

Renegade 0 0 0 0 0 0 0 0 0 0 0 1,678

YoY growth

GAC Honda in total 54.3% 38.3% 21.9% 5.3% 5.6% -3.8% 25.0% 20.0% 32.4% 1.4% 2.1% 3.5%

Fit 6.1% -2.9% -64.6% -74.0% -33.0% -17.1% 26.4% 48.7% 55.3% -6.2% -16.9% -3.8%

City 23.6% -4.5% 180.3% 340.9% 136.8% 19.4% 291.7% 119.7% 5.5% 28.6% 74.1% 172.0%

S1 170.2% 169.9% 365.0% -13.1% -97.6% 65.0% -100.0% 568.6% -42.5% -19.3% 634.0% 156.6%

Crider -16.5% 4.5% -15.3% -0.4% -5.4% -20.1% 3.5% 24.9% 45.3% -46.6% -49.8% -52.8%

Accord 59.4% 32.4% 24.2% -19.7% 25.6% -6.2% -8.2% -51.2% 30.5% 11.1% 9.3% 3.9%

Crosstour -29.1% -35.2% -34.6% -11.5% -41.3% -48.6% 2.3% -51.8% -65.0% -39.9% -46.8% -31.6%

Vezel n.a n.a n.a 792.5% 40.1% 57.5% 26.8% 24.4% 57.3% 57.4% 49.1% 40.6%

Odyssey 113.0% 10.4% -11.0% -39.2% -19.1% -4.9% 39.2% 1.2% -18.5% -21.6% -12.0% -19.6%

GAC Toyota in total 27.4% 7.0% -6.5% 11.9% 8.5% -5.9% 36.3% -7.1% 24.4% -2.8% 4.7% -7.7%

Yaris -18.3% 22.5% -1.6% 2.6% -7.6% -43.7% 17.1% -9.3% 2.6% -13.9% -21.3% -41.2%

Levin n.a 28.4% 3.7% 18.6% 10.8% 23.3% 58.0% 25.1% 58.1% 9.1% 36.8% 17.8%

Camry -13.7% -24.8% -25.2% -15.7% 19.7% -12.4% -2.5% -55.3% -42.4% -28.0% -10.2% -27.7%

Highlander 19.6% 31.5% 24.9% 93.4% 20.3% 6.3% 408.9% 279.8% 9022.8% 28.1% 4.8% 7.5%

EZ -41.0% 15.8% -70.1% -44.0% -55.4% -85.8% -45.2% -46.4% -68.0% -47.3% -25.2% 17.3%

GAC Motor in total 143.4% 117.5% 111.1% 112.3% 129.2% 34.0% 200.8% 115.5% 179.1% 226.6% 181.9% 121.1%

GA3 15.4% -80.9% -73.9% -73.8% -81.9% -96.1% -86.5% -97.0% -88.6% -62.1% -2.7% -26.7%

GA5 -59.9% 11.0% -92.4% -35.6% -12.9% 147.6% 119.1% 55.0% 334.8% 814.3% 4658.3% -69.3%

GA5 EV n.a n.a n.a -100.0% -100.0% -100.0% -100.0% -100.0% -100.0% -100.0% -100.0% -100.0%

GA6 n.a n.a n.a n.a n.a 385.7% -82.7% -86.3% -68.3% -32.4% 52.2% 234.8%

GA8 n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a

GS5 -89.7% -88.3% -82.4% -78.5% -70.2% -93.5% -65.5% -72.0% -85.1% -83.1% -58.8% -61.9%

GS4 n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a 303.3% 143.6%

GAC Fiat in total -17.7% -34.7% -68.1% -58.1% -38.5% -2.0% 191.7% 263.3% 178.9% 235.4% 238.8% 658.9%

Ottimo -21.7% -51.2% -63.9% -60.6% -53.7% -63.8% 9.1% -10.6% -36.2% -21.6% -54.4% -27.9%

Viaggio -15.5% -21.7% -70.4% -56.8% -72.6% -73.7% -55.4% -45.6% -62.6% -39.1% -75.1% -50.5%

Cherokee n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a

Renegade n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a n.a

17

Guangzhou Automobile Group (2238 HK): 20 July 2016

Source: CAMDaiwa’s Asia Pacific Research Directory

HONG KONG

Takashi FUJIKURA (852) 2848 4051 [email protected]

Regional Research Head

John HETHERINGTON (852) 2773 8787 [email protected]

Regional Deputy Head of Asia Pacific Research

Rohan DALZIELL (852) 2848 4938 [email protected]

Regional Head of Asia Pacific Product Management

Kevin LAI (852) 2848 4926 [email protected]

Chief Economist for Asia ex-Japan; Macro Economics (Regional)

Jonas KAN (852) 2848 4439 [email protected]

Head of Hong Kong and China Property

Cynthia CHAN (852) 2773 8243 [email protected]

Property (China)

Leon QI (852) 2532 4381 [email protected]

Banking (Hong Kong/China); Broker (China); Insurance (China)

Yan LI (852) 2773 8822 [email protected]

Banking (China)

Anson CHAN (852) 2532 4350 [email protected]

Consumer (Hong Kong/China)

Adrian CHAN (852) 2848 4427 [email protected]

Consumer (Hong Kong/China)

Jamie SOO (852) 2773 8529 [email protected]

Gaming and Leisure (Hong Kong/China)

Dennis IP (852) 2848 4068 [email protected]

Power; Utilities; Renewables and Environment (Hong Kong/China)

John CHOI (852) 2773 8730 [email protected]

Head of Hong Kong and China Internet; Regional Head of Small/Mid Cap

Kelvin LAU (852) 2848 4467 [email protected]

Head of Automobiles; Transportation and Industrial (Hong Kong/China)

Brian LAM (852) 2532 4341 [email protected]

Transportation – Railway; Construction and Engineering (China)

Thomas HO (852) 2773 8716 [email protected]

Custom Products Group

PHILIPPINES

Patricia Tamase (63) 2 797 3024 [email protected]

Banking

SOUTH KOREA

Sung Yop CHUNG (82) 2 787 9157 [email protected]

Pan-Asia Co-head/Regional Head of Automobiles and Components; Automobiles; Shipbuilding; Steel

Mike OH (82) 2 787 9179 [email protected]

Banking; Capital Goods (Construction and Machinery)

Iris PARK (82) 2 787 9165 [email protected]

Consumer/Retail

SK KIM (82) 2 787 9173 [email protected]

IT/Electronics – Semiconductor/Display and Tech Hardware

Thomas Y KWON (82) 2 787 9181 [email protected]

Pan-Asia Head of Internet & Telecommunications; Software – Internet/On-line Game

Kevin JIN (82) 2 787 9168 [email protected]

Small/Mid Cap

TAIWAN

Rick HSU (886) 2 8758 6261 [email protected]

Head of Regional Technology; Head of Taiwan Research; Semiconductor/IC Design (Regional)

Christie CHIEN (886) 2 8758 6257 [email protected]

Banking; Insurance (Taiwan); Macro Economics (Regional)

Steven TSENG (886) 2 8758 6252 [email protected]

IT/Technology Hardware (PC Hardware)

Christine WANG (886) 2 8758 6249 [email protected]

IT/Technology Hardware (Automation); Pharmaceuticals and Healthcare; Consumer

Kylie HUANG (886) 2 8758 6248 [email protected]

IT/Technology Hardware (Handsets and Components)

Helen CHIEN (886) 2 8758 6254 [email protected]

Small/Mid Cap

INDIA

Punit SRIVASTAVA (91) 22 6622 1013 [email protected]

Head of India Research; Strategy; Banking/Finance

Saurabh MEHTA (91) 22 6622 1009 [email protected]

Capital Goods; Utilities

SINGAPORE

Ramakrishna MARUVADA (65) 6499 6543 [email protected]

Head of Singapore Research; Telecommunications (China/ASEAN/India)

Royston TAN (65) 6321 3086 [email protected]

Oil and Gas; Capital Goods

David LUM (65) 6329 2102 [email protected]

Banking; Property and REITs

Shane GOH (65) 64996546 [email protected]

Property and REITs; Small/Mid Cap (Singapore)

Jame OSMAN (65) 6321 3092 [email protected]

Transportation – Road and Rail; Pharmaceuticals and Healthcare; Consumer (Singapore)

18

Guangzhou Automobile Group (2238 HK): 20 July 2016

Daiwa’s Offices

Office / Branch / Affiliate Address Tel Fax

DAIWA SECURITIES GROUP INC

HEAD OFFICE Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6753 (81) 3 5555 3111 (81) 3 5555 0661

Daiwa Securities Trust Company One Evertrust Plaza, Jersey City, NJ 07302, U.S.A. (1) 201 333 7300 (1) 201 333 7726

Daiwa Securities Trust and Banking (Europe) PLC (Head Office) 5 King William Street, London EC4N 7JB, United Kingdom (44) 207 320 8000 (44) 207 410 0129

Daiwa Europe Trustees (Ireland) Ltd Level 3, Block 5, Harcourt Centre, Harcourt Road, Dublin 2, Ireland (353) 1 603 9900 (353) 1 478 3469

Daiwa Capital Markets America Inc. New York Head Office Financial Square, 32 Old Slip, New York, NY10005, U.S.A. (1) 212 612 7000 (1) 212 612 7100

Daiwa Capital Markets America Inc. San Francisco Branch 555 California Street, Suite 3360, San Francisco, CA 94104, U.S.A. (1) 415 955 8100 (1) 415 956 1935

Daiwa Capital Markets Europe Limited, London Head Office 5 King William Street, London EC4N 7AX, United Kingdom (44) 20 7597 8000 (44) 20 7597 8600

Daiwa Capital Markets Europe Limited, Frankfurt Branch Neue Mainzer Str. 1, 60311 Frankfurt/Main, Germany (49) 69 717 080 (49) 69 723 340

Daiwa Capital Markets Europe Limited, Paris Representative Office 17, rue de Surène 75008 Paris, France (33) 1 56 262 200 (33) 1 47 550 808

Daiwa Capital Markets Europe Limited, Geneva Branch 50 rue du Rhône, P.O.Box 3198, 1211 Geneva 3, Switzerland (41) 22 818 7400 (41) 22 818 7441

Daiwa Capital Markets Europe Limited, Moscow Representative Office

Midland Plaza 7th Floor, 10 Arbat Street, Moscow 119002, Russian Federation

(7) 495 641 3416 (7) 495 775 6238

Daiwa Capital Markets Europe Limited, Bahrain Branch 7th Floor, The Tower, Bahrain Commercial Complex, P.O. Box 30069, Manama, Bahrain

(973) 17 534 452 (973) 17 535 113

Daiwa Capital Markets Hong Kong Limited Level 28, One Pacific Place, 88 Queensway, Hong Kong (852) 2525 0121 (852) 2845 1621

Daiwa Capital Markets Singapore Limited 6 Shenton Way #26-08, OUE Downtown 2, Singapore 068809, Republic of Singapore

(65) 6220 3666 (65) 6223 6198

Daiwa Capital Markets Australia Limited Level 34, Rialto North Tower, 525 Collins Street, Melbourne, Victoria 3000, Australia

(61) 3 9916 1300 (61) 3 9916 1330

DBP-Daiwa Capital Markets Philippines, Inc 18th Floor, Citibank Tower, 8741 Paseo de Roxas, Salcedo Village, Makati City, Republic of the Philippines

(632) 813 7344 (632) 848 0105

Daiwa-Cathay Capital Markets Co Ltd 14/F, 200, Keelung Road, Sec 1, Taipei, Taiwan, R.O.C. (886) 2 2723 9698 (886) 2 2345 3638

Daiwa Securities Capital Markets Korea Co., Ltd. 20 Fl.& 21Fl. One IFC, 10 Gukjegeumyung-Ro, Yeongdeungpo-gu, Seoul, Korea

(82) 2 787 9100 (82) 2 787 9191

Daiwa Securities Co. Ltd., Beijing Representative Office Room 301/302,Kerry Center,1 Guanghua Road,Chaoyang District,

Beijing 100020, People’s Republic of China

(86) 10 6500 6688 (86) 10 6500 3594

Daiwa (Shanghai) Corporate Strategic Advisory Co. Ltd. 44/F, Hang Seng Bank Tower, 1000 Lujiazui Ring Road, Pudong, Shanghai China 200120 , People’s Republic of China

(86) 21 3858 2000 (86) 21 3858 2111

Daiwa Securities Co. Ltd., Bangkok Representative Office 18th Floor, M Thai Tower, All Seasons Place, 87 Wireless Road,

Lumpini, Pathumwan, Bangkok 10330, Thailand (66) 2 252 5650 (66) 2 252 5665

Daiwa Capital Markets India Private Ltd 10th Floor, 3 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra East, Mumbai – 400051, India

(91) 22 6622 1000 (91) 22 6622 1019

Daiwa Securities Co. Ltd., Hanoi Representative Office Suite 405, Pacific Palace Building, 83B, Ly Thuong Kiet Street, Hoan Kiem Dist. Hanoi, Vietnam

(84) 4 3946 0460 (84) 4 3946 0461

DAIWA INSTITUTE OF RESEARCH LTD

HEAD OFFICE 15-6, Fuyuki, Koto-ku, Tokyo, 135-8460, Japan (81) 3 5620 5100 (81) 3 5620 5603

MARUNOUCHI OFFICE Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6756 (81) 3 5555 7011 (81) 3 5202 2021

New York Research Center 11th Floor, Financial Square, 32 Old Slip, NY, NY 10005-3504, U.S.A. (1) 212 612 6100 (1) 212 612 8417

London Research Centre 3/F, 5 King William Street, London, EC4N 7AX, United Kingdom (44) 207 597 8000 (44) 207 597 8550

19

Guangzhou Automobile Group (2238 HK): 20 July 2016

Important Disclosures and Disclaimer

This publication is produced by Daiwa Securities Group Inc. and/or its non-U.S. affiliates, and distributed by Daiwa Securities Group Inc. and/or its non-U.S. affiliates, except to the extent expressly provided herein. This publication and the contents hereof are intended for information purposes only, and may be subject to change without further notice. Any use, disclosure, distribution, dissemination, copying, printing or reliance on this publication for any other purpose without our prior consent or approval is strictly prohibited. Neither Daiwa Securities Group Inc. nor any of its respective parent, holding, subsidiaries or affiliates, nor any of its respective directors, officers, servants and employees, represent nor warrant the accuracy or completeness of the information contained herein or as to the existence of other facts which might be significant, and will not accept any responsibility or liability whatsoever for any use of or reliance upon this publication or any of the contents hereof. Neither this publication, nor any content hereof, constitute, or are to be construed as, an offer or solicitation of an offer to buy or sell any of the securities or investments mentioned herein in any country or jurisdiction nor, unless expressly provided, any recommendation or investment opinion or advice. Any view, recommendation, opinion or advice expressed in this publication may not necessarily reflect those of Daiwa Securities Group Inc., and/or its affiliates nor any of its respective directors, officers, servants and employees except where the publication states otherwise. This research report is not to be relied upon by any person in making any investment decision or otherwise advising with respect to, or dealing in, the securities mentioned, as it does not take into account the specific investment objectives, financial situation and particular needs of any person. Daiwa Securities Group Inc., its subsidiaries or affiliates, or its or their respective directors, officers and employees from time to time have trades as principals, or have positions in, or have other interests in the securities of the company under research including market making activities, derivatives in respect of such securities or may have also performed investment banking and other services for the issuer of such securities. The following are additional disclosures.

Ownership of Securities

For “Ownership of Securities” information, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Investment Banking Relationship

For “Investment Banking Relationship”, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Japan

Daiwa Securities Co. Ltd. and Daiwa Securities Group Inc.

Daiwa Securities Co. Ltd. is a subsidiary of Daiwa Securities Group Inc.

Investment Banking Relationship

Within the preceding 12 months, the subsidiaries and/or affiliates of Daiwa Securities Group Inc. * has lead-managed public offerings and/or secondary offerings (excluding straight bonds) of the securities of the following companies: Mirae Asset Life Insurance Co Ltd (085620 KS); China Reinsurance Group Corporation (1508 HK).

*Subsidiaries of Daiwa Securities Group Inc. for the purposes of this section shall mean any one or more of: Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司), Daiwa

Capital Markets Singapore Limited, Daiwa Capital Markets Australia Limited, Daiwa Capital Markets India Private Limited, Daiwa-Cathay Capital Markets Co., Ltd., Daiwa Securities Capital Markets Korea Co., Ltd.

Hong Kong

This research is distributed in Hong Kong by Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司) (“DHK”) which is regulated by the Hong Kong Securities and Futures

Commission. Recipients of this research in Hong Kong may contact DHK in respect of any matter arising from or in connection with this research. Relevant Relationship (DHK)

DHK may from time to time have an individual employed by or associated with it serves as an officer of any of the companies under its research coverage.

Singapore

This research is distributed in Singapore by Daiwa Capital Markets Singapore Limited and it may only be distributed in Singapore to accredited investors, expert investors and institutional investors as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. By virtue of distribution to these category of investors, Daiwa Capital Markets Singapore Limited and its representatives are not required to comply with Section 36 of the Financial Advisers Act (Chapter 110) (Section 36 relates to disclosure of Daiwa Capital Markets Singapore Limited’s interest and/or its representative’s interest in securities). Recipients of this research in Singapore may contact Daiwa Capital Markets Singapore Limited in respect of any matter arising from or in connection with the research.

Australia

This research is distributed in Australia by Daiwa Capital Markets Australia Limited and it may only be distributed in Australia to wholesale investors within the meaning of the Corporations Act. Recipients of this research in Australia may contact Daiwa Capital Markets Stockbroking Limited in respect of any matter arising from or in connection with the research.

India

This research is distributed in India to Institutional Clients only by Daiwa Capital Markets India Private Limited (Daiwa India) which is an intermediary registered with Securities & Exchange Board of India as a Stock Broker, Merchant Bank and Research Analyst. Daiwa India, its Research Analyst and their family members and its associates do not have any financial interest save as disclosed or other undisclosed material conflict of interest in the securities or derivatives of any companies under coverage. Daiwa India and its associates may have received compensation for any products other than Investment Banking (as disclosed) or brokerage services from the subject company in this report during the past 12 months. Unless otherwise stated in BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action, Daiwa India and its associates do not hold more than 1% of any companies covered in this research report. There is no material disciplinary action against Daiwa India by any regulatory authority impacting equity research analysis activities as of the date of this report.

Taiwan

This research is distributed in Taiwan by Daiwa-Cathay Capital Markets Co., Ltd and it may only be distributed in Taiwan to institutional investors or specific investors who have signed recommendation contracts with Daiwa-Cathay Capital Markets Co., Ltd in accordance with the Operational Regulations Governing Securities Firms Recommending Trades in Securities to Customers. Recipients of this research in Taiwan may contact Daiwa-Cathay Capital Markets Co., Ltd in respect of any matter arising from or in connection with the research.

Philippines

This research is distributed in the Philippines by DBP-Daiwa Capital Markets Philippines, Inc. which is regulated by the Philippines Securities and Exchange Commission and the Philippines Stock Exchange, Inc. Recipients of this research in the Philippines may contact DBP-Daiwa Capital Markets Philippines, Inc. in respect of any matter arising from or in connection with the research. DBP-Daiwa Capital Markets Philippines, Inc. recommends that investors independently assess, with a professional advisor, the specific financial risks as well as the legal, regulatory, tax, accounting, and other consequences of a proposed transaction. DBP-Daiwa Capital Markets Philippines, Inc. may have positions or may be materially interested in the securities in any of the markets mentioned in the publication or may have performed other services for the issuers of such securities.

For relevant securities and trading rules please visit SEC and PSE links at http://www.sec.gov.ph/irr/AmendedIRRfinalversion.pdf and http://www.pse.com.ph/ respectively.

Thailand

This research is distributed to only institutional investors in Thailand primarily by Thanachart Securities Public Company Limited (“TNS”).

This report is prepared by analysts who are employed by Daiwa Securities Group Inc. and/or its non-U.S. affiliates. This report is provided to you for informational purposes only and it is not, and is not to be construed as, an offer or an invitation to make an offer to sell or buy any securities. Neither Thanachart Securities Public Company Limited, Daiwa Securities Group Inc. nor any of their respective parent, holding, subsidiaries or affiliates, nor any of their respective directors, officers, servants and employees accept any liability whatsoever for any direct or consequential loss arising from any use of this research or its contents.

The information and opinions contained herein have been compiled or arrived at from sources believed to be reliable. However, Thanachart Securities Public Company Limited, Daiwa Securities Group Inc. nor any of their respective parent, holding, subsidiaries or affiliates, nor any of their respective directors, officers, servants and employees make no representation or warranty, express or implied, as to their accuracy or completeness. Expressions of opinion herein are subject to change without notice. The use of any information, forecasts and opinions contained in this report shall be at the sole discretion and risk of the user.

Daiwa Securities Group Inc. and/or its non-U.S. affiliates perform and seek to perform business with companies covered in this research. Thanachart Securities Public Company Limited, Daiwa Securities Group Inc., their respective parent, holding, subsidiaries or affiliates, their respective directors, officers, servants and employees may have positions and financial interest in securities mentioned in this research. Thanachart Securities Public Company Limited, Daiwa Securities Group Inc., their respective parent, holding, subsidiaries or affiliates may from time to time perform investment banking or other services for, or solicit investment banking or other business from, any entity mentioned in this research. Therefore, investors should be aware of conflict of interest that may affect the objectivity of this research.

United Kingdom

This research report is produced by Daiwa Securities Co. Ltd. and/or its affiliates and is distributed in the European Union, Iceland, Liechtenstein, Norway and Switzerland. Daiwa Capital Markets Europe Limited is authorised and regulated by The Financial Conduct Authority (“FCA”) and is a member of the London Stock Exchange and Eurex. This publication is intended for investors who are not Retail Clients in the United Kingdom within the meaning of the Rules of the FCA and should not therefore be distributed to such Retail Clients in the United Kingdom. Should you enter into investment business with Daiwa Capital Markets Europe’s affiliates outside the United Kingdom, we are obliged to advise that the protection afforded by the United Kingdom regulatory system may not apply; in particular, the benefits of the Financial Services Compensation Scheme may not be available. Daiwa Capital Markets Europe Limited has in place organisational arrangements for the prevention and avoidance of conflicts of interest. Our conflict management policy is available at

20

Guangzhou Automobile Group (2238 HK): 20 July 2016

http://www.uk.daiwacm.com/about-us/corporate-governance-regulatory.

Germany

This document is distributed in Germany by Daiwa Capital Markets Europe Limited, Niederlassung Frankfurt which is regulated by BaFin (Bundesanstalt fuer Finanzdienstleistungsaufsicht) for the conduct of business in Germany.

Bahrain

This research material is distributed in Bahrain by Daiwa Capital Markets Europe Limited, Bahrain Branch, regulated by The Central Bank of Bahrain and holds Investment Business Firm – Category 2 license and having its official place of business at the Bahrain World Trade Centre, South Tower, 7th floor, P.O. Box 30069, Manama, Kingdom of Bahrain. Tel No. +973 17534452 Fax No. +973 535113

United States

This report is distributed in the U.S. by Daiwa Capital Markets America Inc. (DCMA). It may not be accurate or complete and should not be relied upon as such. It reflects the preparer’s views at the time of its preparation, but may not reflect events occurring after its preparation; nor does it reflect DCMA’s views at any time. Neither DCMA nor the preparer has any obligation to update this report or to continue to prepare research on this subject. This report is not an offer to sell or the solicitation of any offer to buy securities. Unless this report says otherwise, any recommendation it makes is risky and appropriate only for sophisticated speculative investors able to incur significant losses. Readers should consult their financial advisors to determine whether any such recommendation is consistent with their own investment objectives, financial situation and needs. This report does not recommend to U.S. recipients the use of any of DCMA’s non-U.S. affiliates to effect trades in any security and is not supplied with any understanding that U.S. recipients of this report will direct commission business to such non-U.S. entities. Unless applicable law permits otherwise, non-U.S. customers wishing to effect a transaction in any securities referenced in this material should contact a Daiwa entity in their local jurisdiction. Most countries throughout the world have their own laws regulating the types of securities and other investment products which may be offered to their residents, as well as a process for doing so. As a result, the securities discussed in this report may not be eligible for sales in some jurisdictions. Customers wishing to obtain further information about this report should contact DCMA: Daiwa Capital Markets America Inc., Financial Square, 32 Old Slip, New York, New York 10005 (Tel no. 212-612-7000).

Ownership of Securities

For “Ownership of Securities” information please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Investment Banking Relationships

For “Investment Banking Relationships” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action. DCMA Market Making

For “DCMA Market Making” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Research Analyst Conflicts

For updates on “Research Analyst Conflicts” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action. The principal research analysts who prepared this report have no financial interest in securities of the issuers covered in the report, are not (nor are any members of their household) an officer, director or advisory board member of the issuer(s) covered in the report, and are not aware of any material relevant conflict of interest involving the analyst or DCMA, and did not receive any compensation from the issuer during the past 12 months except as noted: no exceptions.

Research Analyst Certification

For updates on “Research Analyst Certification” and “Rating System” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action. The views about any and all of the subject securities and issuers expressed in this Research Report accurately reflect the personal views of the research analyst(s) primarily responsible for this report (or the views of the firm producing the report if no individual analysts[s] is named on the report); and no part of the compensation of such analyst(s) (or no part of the compensation of the firm if no individual analyst[s)] is named on the report) was, is, or will be directly or indirectly related to the specific recommendations or views contained in this Research Report.

The following explains the rating system in the report as compared to relevant local indices, unless otherwise stated, based on the beliefs of the author of the report.

"1": the security could outperform the local index by more than 15% over the next 12 months. "2": the security is expected to outperform the local index by 5-15% over the next 12 months. "3": the security is expected to perform within 5% of the local index (better or worse) over the next 12 months. "4": the security is expected to underperform the local index by 5-15% over the next 12 months. "5": the security could underperform the local index by more than 15% over the next 12 months. Disclosure of investment ratings

Rating Percentage of total

Buy* 65.8%

Hold** 21.8%

Sell*** 12.4%

Source: Daiwa

Notes: data is for single-branded Daiwa research in Asia (ex Japan) and correct as of 30 June 2016. * comprised of Daiwa’s Buy and Outperform ratings. ** comprised of Daiwa’s Hold ratings. *** comprised of Daiwa’s Underperform and Sell ratings. Additional information may be available upon request.

Japan - additional notification items pursuant to Article 37 of the Financial Instruments and Exchange Law (This Notification is only applicable where report is distributed by Daiwa Securities Co. Ltd.)

If you decide to enter into a business arrangement with us based on the information described in materials presented along with this document, we ask you to pay close attention to the following items.

In addition to the purchase price of a financial instrument, we will collect a trading commission* for each transaction as agreed beforehand with you. Since commissions may be included in the purchase price or may not be charged for certain transactions, we recommend that you confirm the commission for each transaction.

In some cases, we may also charge a maximum of ¥ 2 million (including tax) per year as a standing proxy fee for our deposit of your securities, if you are a non-resident of Japan.

For derivative and margin transactions etc., we may require collateral or margin requirements in accordance with an agreement made beforehand with you. Ordinarily in such cases, the amount of the transaction will be in excess of the required collateral or margin requirements.

There is a risk that you will incur losses on your transactions due to changes in the market price of financial instruments based on fluctuations in interest rates, exchange rates, stock prices, real estate prices, commodity prices, and others. In addition, depending on the content of the transaction, the loss could exceed the amount of the collateral or margin requirements.

There may be a difference between bid price etc. and ask price etc. of OTC derivatives handled by us.

Before engaging in any trading, please thoroughly confirm accounting and tax treatments regarding your trading in financial instruments with such experts as certified public accountants. *The amount of the trading commission cannot be stated here in advance because it will be determined between our company and you based on current market conditions and the content of each transaction etc.

When making an actual transaction, please be sure to carefully read the materials presented to you prior to the execution of agreement, and to take responsibility for your own decisions regarding the signing of the agreement with us.

Corporate Name: Daiwa Securities Co. Ltd. Financial instruments firm: chief of Kanto Local Finance Bureau (Kin-sho) No.108 Memberships: Japan Securities Dealers Association, The Financial Futures Association of Japan Japan Securities Investment Advisers Association Type II Financial Instruments Firms Association