Embed Size (px)

Citation preview

Feature

Talent and InnovationEnhancing Productivityand Performance

Personality

Joel KornreichGroup CEOAlliance Bank Malaysia

PUBLISHED BY ASIAN INSTITUTE OF FINANCE | www.ai f .org.myISSUE 27 2017 | PP18302/11/2013 (033704) | ISSN 2462-1226

Talent and Innovation

CONTENTS Issue 27, 2017

Features

5Talent and Innovation: Enhancing Productivity and Performance

22Enhancing Digital Trust in Financial Services: A Multisensory Approach

Personality

16Joel Kornreich Group Chief Executive Officer Alliance Bank Malaysia Berhad

Talking Points

11Knowing the Unknowable with Quantum Computing

28Major Forces Transforming Banking

34From Talent to Culture: Driving Innovation through Human Capital

AIF Board of Directors Editorial Team

Chief EditorDr Raymond Madden, FRSA

EditorNeil Smith

Publications ManagerParamjeet Kaur

DISCLAIMER: The Asian Institute of Finance does not represent nor warrant the completeness, accuracy, timeliness or adequacy of this material and it should not be relied on as such. The Asian Institute of Finance neither accepts nor assumes any responsibility or liability whatsoever for any data, errors or omissions that may be contained in this material or for any consequences or results obtained from the use of this information. This publication does not necessarily reflect the views or the positions of the Asian Institute of Finance. (838740P)

Published by: Asian Institute of Finance Unit 1B-05 Level 5 Block 1B, Plaza Sentral

Jalan Stesen Sentral 5 50470 Kuala Lumpur

Printed by: Percetakan Okid Sdn Bhd No. 2, Jalan SS13/3C

Subang Jaya Industrial Estate 47500 Subang Jaya, Selangor okidpress.com

Tan Sri Muhammad bin IbrahimChairman of the BoardGovernor, Bank Negara Malaysia

Tan Sri Dato’ Seri Ranjit Ajit SinghVice Chairman of the BoardChairman, Securities Commission Malaysia

Tan Sri Azman HashimChairman, AmBank Group & Chairman,Asian Institute of Chartered Bankers

Datuk Seri Dr Nik Norzrul ThaniNik Hassan ThaniExecutive Chairman, Zaid Ibrahim & Co

Mr Kung Beng HongDirector, Alliance Finance Group Berhad & Alliance Bank Malaysia Berhad

Mr Hashim HarunChairman, The Malaysian Insurance Institute (MII)

Mr Ken PushpanathanChairman of the AIF Audit Committee

Our latest edition of Asian Link entitled ‘Talent and Innovation’ explores the relationship between these two key organisational factors and how a new working environment powered by data, algorithms, automation, artificial intelligence and FinTech is emerging. The business landscape is rapidly evolving driven by technological disruption where some organisations sense opportunity, others are buckling under the pressure of change.

This edition’s personality section features an interview with Joel Kornreich, Group Chief Executive Officer of Alliance Bank Malaysia Berhad, who talks about a

company-wide culture of innovation where people from all parts of the bank are able to contribute new ideas. He also highlights that Alliance is adapting to changing consumer habits by launching a mobile banking app.

As technological disruption breaks down markets and creates new ones, a company’s ability to innovate is vital. With the theme ‘Talent and Innovation: Enhancing Productivity and Performance’, our AIF International Symposium 2017 explored the relationship between talent and innovation in improving business productivity and performance. In an article we share some of the key insights and learnings from the Symposium.

In a special address at the Khazanah Megatrends Forum on 3 October 2017 in Kuala Lumpur, John McFarlane, Chairman, Barclays Bank PLC, UK, explored some of the major forces reshaping the banking sector including technology, competition and regulation, and how best to steer banks through this changing environment and create a more sustainable future.

According to Arvind Krishna, Senior Vice President, Hybrid Cloud, and Director at IBM Research, we must start looking at new ways to keep up with the unprecedented workloads and how quantum computing will play an essential role in making that possible.

In collaboration with the Imagineering Institute, AIF has conducted a new study entitled ‘Enhancing Digital Trust in Banking and Insurance’ which demonstrates how visual and auditory cues can impact the way in which consumers perceive, feel and engage with financial services online.

Ehon Chan, Executive Director, ASEAN Centre of Entrepreneurship, Malaysian Global Innovation & Creativity Centre (MaGIC), suggests that, although the immediate and most obvious place to start for any financial services organisation looking to innovate is to jump straight to technology, actually the best place to start is by transforming its human capital, culture and ways of working.

I hope you find this edition of Asian Link insightful and an interesting read. We welcome feedback on our articles and do follow us on LinkedIn.

Dr Raymond MaddenChief Executive Officer, AIF

EDITOR'S NOTE

4 Asian Link | Issue 27 2017

TalenT and InnovaTIon enhancIng ProducTIvITy and Performance

The AIF International Symposium 2017 examined the relationship between innovation and improving business productivity and performance from the context of human capital development and talent management.

nnovation has become a core driver of future business performance and growth. In line with the changing demographics of a more mobile, diverse and global workforce, and to remain competitive, companies must maximise their capacity to develop an innovative and skilled workforce by revamping their talent management strategies.

The AIF International Symposium 2017 themed ‘Talent and Innovation: Enhancing Productivity and Performance’, which had over 20 expert speakers and attracted some 200 delegates, addressed this critical issue of improving business performance through innovation from the context of human capital development.

As with most challenges in business, the solution comes down to people. Organisations will need to ensure they have the right talent with the right skills, while encouraging a culture of innovation where employees are encouraged to come up with new ideas and try new things. HR professionals will need to ensure their organisations have effective people strategies and processes in place to foster a culture of innovation and deliver future productivity gains and improved business performance.

I

FEATURE

Issue 27 2017 | Asian Link 5

Opening RemarksDr Raymond Madden, Chief Executive Officer, Asian Institute of Finance, Malaysia

In his welcoming remarks, Dr Raymond Madden, Chief Executive Officer, Asian Institute of Finance (AIF), stressed that the banking and insurance industries must innovate to improve performance and productivity.

Dr Madden explained that the Symposium this year will be discussing innovation, performance and productivity and there will be some interesting lessons and some painful takeaways. Innovation is a much-used buzzword these days but how do we innovate within large multi-level and hierarchical organisations? We have been talking about performance for a long time now and have moved away from KPIs to better annual measurements, but is that working for us? Are our organisations productive enough? The general productivity index in Malaysia is 3.4% but the government wants this to increase to 3.7% and this is something we need to focus on as we move to becoming a fully developed nation by 2020.

He further added that the Economic Planning Unit (EPU) of the Prime Minister’s Office approached

AIF to engage with our Symposium audience as part of its outreach and engagement programme for Transformasi Nasional 2050 (TN50) – a Government-led initiative to chart the direction of Malaysia for the next 30 years until the year 2050. He said that delegates would be asked their views on several key issues relating to the TN50 initiative.

Finally, Dr Madden said that AIF is launching a report on the relationship between trust and visual aesthetics, multisensory perception and the design of online space in the financial services industry (FSI). This study was undertaken

in collaboration with the Imagineering Institute. The study entitled ‘Enhancing

Digital Trust in Banking and Insurance’ is the first of its kind in Malaysia and the

region, and demonstrates how visual and auditory cues can impact the way in which consumers perceive, feel and engage with financial services, and captures the interaction effects between various sense-perception stimuli in terms of online trust in financial services.

FEATURE

6 Asian Link | Issue 27 2017

KEYNOTE 1Innovating the Future

Bill Fischer, Professor of Innovation Management, IMD

Professor Bill Fischer, in his keynote presentation entitled ‘Innovating the Future’, said that innovation is a social phenomenon and is more about people: customers, colleagues and choices. He also said that we live in an increasingly digital world which is changing our perceptions of nearly everything.

Professor Fischer explained that (a) innovation has always been a legitimate part of doing business, but today's innovation is different – things happening around us will result in different outcomes; (b) disruption is an industry phenomena and completely normal, but it is also not a strategy – we have to come up with strategies that respond to these disruptions in an intelligent manner; (c) what happens in response to change is not normal and what we are seeing today is new forms of innovation delivered in new ways by new players – the real change occurring around us is in the way innovation is playing out and what that means for the competitive balance within organisations; and (d) innovation is going to change the way we do business, the expectations of our customers and the way we design work – if we want to attract new talent, we need to accept and adapt to the changes that are coming our way.

As a result, the future will be increasingly ‘unknown’ — with new technologies, new business models, new and unexpected competitors – yet organisations have no choice but to continue to develop products, hire talent, build teams and move forward despite this unprecedented disequilibrium. We see leadership increasingly becoming more customer-experience-centric, more experimental, faster, smarter, more open and more inclusive.

In his closing, Professor Fischer emphasised that innovation should be a verb, not a noun.

keynotes KEYNOTE 2So You Think You Have 20/20 Vision?

Zia Zaman, Chief Executive Officer, LumenLab, MetLife Innovation Centre Pte Ltd

As we look ahead to predict the changes about to take place across industries, there is only one place to start – the evolving customer – according to Zia Zaman in his keynote presentation. The rise of new business models, the emergence of new modes of interaction and the enabling technologies which will impact business were examined in his session.

Zia Zaman explained that we are living in the experience economy where consumers use brands on the basis of how well we deliver value to customers. For example, Amazon, Grab and Lazada have created very good experiences for customers which are now the norm and the expectation we have become used to. This has led to a widening gap between the experiences we deliver in the financial services industry and the experiences customers have in other industries.

He then spoke about the ‘Asiafication’ of demand whereby the demand curve is now bending towards Asia. Since about 2011 we have started to see that people are innovating in Asia for Asia and that ‘Asiafication’ of demand is a good reason why MetLife wants to start here.

Zia Zaman highlighted some of the initiatives being undertaken by MetLife. For example, LumenLab, MetLife’s Innovation Centre, is leading the way by commercialising new businesses and promoting culture change. By leveraging a common process, LumenLab’s Test and Learn framework is changing culture by promoting customer-oriented behaviours that will future-proof MetLife.

He further added that by 2020 consumer trends will create a world of work with less certainty and security which in turn will impact employees in many ways including an increase in self-driven careers and an increasing recognition of the importance of wellness and emotional wellbeing.

Zia Zaman ended with four forecasts for 2022: (a) annual absenteeism costs will increase by 10% due to depression; (b) 40% of employees will be contractors; (c) 30% of employees will be part timers; and (d) 5% of employees will quit to become entrepreneurs.

Issue 27 2017 | Asian Link 7

KEYNOTE 3Innovation and Productivity Agenda: Driven by Purpose and Values

Alois Hofbauer, Chief Executive Officer, Nestlé (Malaysia) Berhad & Region Head of Malaysia, Singapore and Brunei

Alois Hofbauer emphasised that purpose and values help organisations become more innovative which in turn makes them more productive. He also argued that for a company to be successful over the long-term and create value for shareholders, it must create value for society.

He said that Nestlé as an organisation is driven by its purpose to enhance the quality of life and contribute to a healthier future; and is guided by a set of values rooted in respect – respect for self, respect for others, respect for diversity (for example 38 nationalities work in Nestlé Malaysia) and respect for the future.

He further added that Nestlé strives for a continuous innovative and productive mindset in order to fulfill consumers’ evolving needs, while staying true to its long-term and sustainable business approach. Alois Hofbauer then shared Nestlé’s innovation journey. He said that the Malaysian consumer is at the heart of Nestlé’s innovations and consumers’ needs are addressed through ‘insperiences’, authenticity and creating a healthy lifestyle by innovating beyond products.

He explained that ‘insperiences’ are about the personalisation of products, for example personalising ‘Kit Kat’ by creating your own flavours, designs and packaging. Authenticity is about natural and clean labels such as ‘Just Milk’– which is milk without anything added to it. Nestlé promotes healthy lifestyles through healthy food such as oat noodles.

He stressed that a culture of innovation is the catalyst to sustained success and Nestlé Malaysia believes everybody can innovate and contribute to the purpose. Nestlé creates shared value by working with external parties to develop new variants of their products and with the Ministry of Education to create entrepreneur jobs for young students in universities.

KEYNOTE 4Navigating the Digital Age

Olivier Crespin, Chief FinTech Officer, CIMB

Olivier Crespin stated that a confluence of forces from changing consumer dynamics to digital-led disruption will reshape many industries. As such, companies and their employees must adapt and evolve to stay relevant.

He stressed that today’s consumer is moving from limited interactions to personal digital engagement where services rendered and value for money determine the brands selected. He asked whether the financial services industry is ready for the disruption coming its way? Banks must push the boundaries and use the power of artificial intelligence and analytics to personalise, guide and assist their consumers in day-to-day transactions. They have to combine the prudence of a bank with the agility of a start-up.

He said people need banking, not banks and in that context banks need to consider the rise of the digital consumer, technology innovation, easy and quick access to information, the ability to do anything, anywhere and new forms of digital competition. All digital solutions must address some key factors including: (a) people want to save time in their daily transactions so developing an App instead of a call centre is something to consider; (b) people want to be recognised and called by their names and expect the bank to know them – we can enhance this by using data analytics; (c) people want to successfully plan their retirement, lifetime goals and education for their children; (d) people want peace of mind, financial security and trust; and (e) banks must bring the whole ecosystem together to add value to consumers.

He concluded by saying that the industry must maintain trust, security, expertise, risk monitoring and payment and settlement infrastructure while at the same time enhancing client-centric communications, analytics, speed and regulations overall and the ecosystem in order to move ahead.

FEATURE

8 Asian Link | Issue 27 2017

Plenary 1Harnessing Innovation for Business Growth

Abdullah Arshad, Cheah Kar Fei, Rafiza Ghazali.Moderator: Laurence Smith

Laurence Smith, Advisory Board Member, SmartUp.io and former MD & Group Head of Learning & Talent Development, DBS Bank, Singapore, moderated this session and the panellists were Cheah Kar Fei, Culture & Learning Specialist, Mindvalley; Rafiza Ghazali, Senior Vice President, Group Innovation & Performance Management, Group Strategy & Innovation, Sime Darby Berhad; and Abdullah Arshad, Chief Operating Officer, Agensi Inovasi Malaysia (AIM).

The panel examined how innovation must be part of any organisation’s business culture and used as an engine for growth. Innovation is vital and new ideas, technical, operational and commercial, should be harnessed, integrated and exploited as a strategic imperative.

Rafiza Ghazali said that being innovative is about customer-centricity, culture and execution capability. She explained that enabling a culture of innovation means allowing the generation of new ideas, validating these ideas to see if they bring any solutions to customers, implementing the solutions and recognising the effort put in by people, typically all within a very short period of time.

Cheah Kar Fei said that innovation must be made a part of the recruitment and selection process. He added that innovation also means making small changes which can actually bring about positive long-term impacts to any company and that organisations must believe in people over process and instill and celebrate a culture of learning.

Abdullah Arshad explained that innovation will not be innovation until it creates value, otherwise it is only an invention. Innovation has to start with leadership. A culture of innovation is the end result of innovative leadership.

Laurence Smith added that a validated learning approach may be useful – this is when we try out initial ideas with minimum effort before actually developing a full blown service which customers may not want. Either way we will benefit from innovation – whether or not the solutions are accepted by customers – as we would have gone through a validated learning process.

Plenary 2Raising Productivity amid Technological Disruption

Nadiah Tan Abdullah, Dato’ Mohd. Razali Hussain, Noorliza Nuruddin.Moderator: Faris H. Hadad-Zervos

The pace of technological change today is staggering. The extent to which technological change can have a positive or negative impact is actually the extent to which we are prepared for it. In other words government and institutional policies and private sector responses should be ready not only to exploit the positive aspects of technological change for productivity but also to mitigate the negative ones. If institutions and people are proactive, technology can make us more productive, but conversely if we are not prepared we can be harmed by it – particularly for workers who have routine jobs which could be substituted by automation.

These issues were discussed in the second plenary session involving Nadiah Tan Abdullah, Chief Human Resources Officer, SP Setia Berhad; Dato’ Mohd. Razali Hussain, Director-General, Malaysia Productivity Corporation (MPC); Noorliza Nuruddin, Head of Human Capital and Facilities Management Division, Human Resources Development Fund (HRDF); and Faris H. Hadad-Zervos, Country Manager Malaysia, East Asia and Asia Pacific World Bank, as moderator.

Dato’ Mohd. Razali Hussain said that, from the perspective of the MPC, the main challenges for raising productivity in Malaysia, particularly in view of digitalisation, are technology, the future workforce, innovation, robust ecosystems and changing mindsets.

According to Noorliza Nuruddin the key considerations in enhancing labour productivity in Malaysia for both the public and private sectors include skill levels in the workforce, the influx of foreign workers, the creation of technical jobs, developing professional human resource management in SMEs and the need to improve the socio-economic mobility of the workforce.

Nadiah Tan Abdullah explained that as businesses we need to look at how to adapt to this new landscape of technological disruption and continue to exist while meeting the expectations of today’s customers. She highlighted four key dimensions – the highly skilled workforce of the future, innovative leadership, one ecosystem including governance and regulations, and talent mobility.

panel discussions

Issue 27 2017 | Asian Link 9

Plenary 3Achieving Peak Performance through People

Karin Clarke, Florence Foo, Tricia Lim.Moderator: Salika Suksuwan

Achieving peak performance is one of the biggest challenges facing organisations today. Leaders must continuously challenge their teams’ performance and keep them engaged and results-focused. To foster a culture of high performance many organisations are moving away from the conventional performance rating system and this is gaining momentum.

Salika Suksuwan, Executive Director, Human Capital, PwC Malaysia, moderated the panel made up of: Karin Clarke, Director, Global Solutions, APAC, Kelly Outsourcing and Consulting Group; Florence Foo, Head of Human Resources, Standard Chartered Bank Malaysia; and Tricia Lim, Head of Performance and Rewards, Maxis Berhad.

Tricia Lim said it is important to ensure that individual goals are correctly set and aligned to the overall business strategy. Instead of annual performance reviews, real-time conversations and feedback will help create a culture of high performance.

Florence Foo shared that real-time feedback is very important but the occurrence is still low as people are busy with their day-to-day tasks. However, regular coaching conversations can help guide employees to perform at an optimum level.

Fundamentally the responsibility for performance management belongs to the line managers and not human resources, said Karin Clarke. Human resources is merely a vehicle to guide managers to have structured conversations with their staff in relation to their performance. The mindset of leaders and managers need to change to this reality.

Plenary 4The Role of HR in Developing Innovative Talent and Fostering a Culture of Innovation

Haroon Bhatti, Marcela Mihanovich, Fazilah Yusof.Moderator: Jaya Kohli

HR plays a vital role in shaping corporate culture. This culture must be able to accommodate innovation, as creativity and innovation have become increasingly important determinants of successful performance and growth in the longer-term. Fostering a culture where innovation can thrive requires some common elements to be aligned including innovative leadership, effective people strategies and good conversations. So what is the role of HR in developing innovative talent and fostering a culture of innovation?

This topic was discussed by Haroon Bhatti, Chief Human Resource Officer, Digi Telecommunications; Marcela Mihanovich, Country Human Resource Officer, Citi Malaysia; and Fazilah Yusof, Chief Human Resource Officer, Prudential BSN Takaful Berhad; with Jaya Kohli, Director, Strategy, Policy Development & Research, Asian Institute of Finance (AIF), moderating.

Haroon Bhatti explained that creating a culture of innovation is probably one of the most difficult tasks as there is often inertia in organisations in particular in terms of wanting to do things as they have always been done. He discussed how Digi has made significant progress in encouraging its employees to start thinking in terms of lean start-ups and to embrace design methodology.

Marcela Mihanovich emphasised that HR and an organisation’s managers will have to work together to foster a culture of innovation. Things have to be done differently and it will be difficult until you get into the rhythm of things. It is important that people have open mindsets and are willing to learn and adapt moving forward. She said that HR must start conversations on change management to prepare employees for future changes.

Fazilah Yusof said that the role of HR is to partner with line managers and get buy-in from the leadership team as both of these will be key in ensuring that innovation works for the organisation. Recruiting innovative employees is dependent on the organisation’s readiness to adapt innovation moving forward and at the point of recruiting there must be some ways of identifying innovative traits within candidates. Organisations must also re-skill existing employees and identify employees who are potentially innovative.

FEATURE

10 Asian Link | Issue 27 2017

Issue 27 2017 | Asian Link 11

Arvind Krishna, Senior Vice President, Hybrid Cloud, and Director at IBM Research, says that we must look to new ways to keep up with the unprecedented workloads computers will face. Quantum computing will play an essential role in making that possible.

Knowing the Unknowable with Quantum Computing

espite historic gains in computing power, the world’s biggest mysteries and greatest opportunities still lie beyond the

capacity of the classical systems we use today. And, without a new computing paradigm based on quantum mechanics, they always will.

For decades the technology industry has been guided by Moore’s Law: the observation that the number of transistors per square inch on integrated circuits will double every year. This fundamental insight made everything else that defined the technology revolution possible, from home computers, to supercomputers, to smartphones. But as the limits to silicon-based transistors and circuits bring us closer to the end of Moore’s Law, we must look to new ways to keep up with the unprecedented workloads computers will face. Quantum computing will play an essential role in making that possible.

D

Arvind Krishna

TALKING POINTS

TALKING POINTS

12 Asian Link | Issue 27 2017

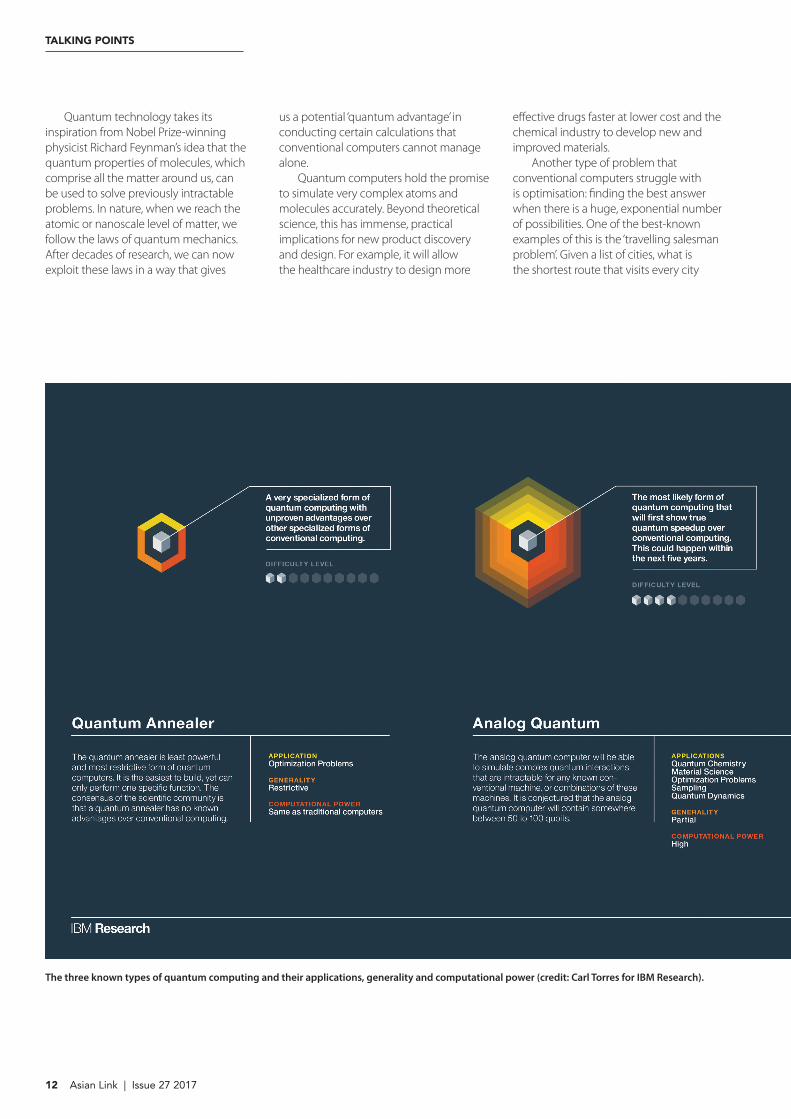

The three known types of quantum computing and their applications, generality and computational power (credit: Carl Torres for IBM Research).

Quantum technology takes its inspiration from Nobel Prize-winning physicist Richard Feynman’s idea that the quantum properties of molecules, which comprise all the matter around us, can be used to solve previously intractable problems. In nature, when we reach the atomic or nanoscale level of matter, we follow the laws of quantum mechanics. After decades of research, we can now exploit these laws in a way that gives

us a potential ‘quantum advantage’ in conducting certain calculations that conventional computers cannot manage alone.

Quantum computers hold the promise to simulate very complex atoms and molecules accurately. Beyond theoretical science, this has immense, practical implications for new product discovery and design. For example, it will allow the healthcare industry to design more

effective drugs faster at lower cost and the chemical industry to develop new and improved materials.

Another type of problem that conventional computers struggle with is optimisation: finding the best answer when there is a huge, exponential number of possibilities. One of the best-known examples of this is the ‘travelling salesman problem’. Given a list of cities, what is the shortest route that visits every city

Issue 27 2017 | Asian Link 13

once and returns to the starting place? The answer has powerful applications for complex equations that underpin many industrial and computer processes.

As the number of cities added to the problem grows, this becomes an intensely difficult problem to solve, even with the fastest computers. Yet a quantum computer could find the optimal answer with ease.

What other practical problems might quantum computers help us solve? They could help us determine the most profitable investment portfolio in the financial industry; the most efficient use of resources in manufacturing; and optimal routes for logistics in transportation and retail industries, to name a few. The possibilities are endless, and that is why we are so excited about quantum computing.

Building these systems is no easy task. A quantum computer looks nothing like the ones we have on our desks or in our offices. The chips must be kept in large dilution refrigerators due to the need to maintain their quantum properties. When we build our quantum chips, we put them inside a refrigerator that is colder than outer space because quantum mechanical states are exquisitely fragile and delicate. Anything can interfere with the successful functioning of the chip such as heat, noise or electromagnetic waves. Signals come in through wires into the refrigerator. A sequence of microwave pulses lets us know what the quantum chip is doing.

We leverage silicon technology to build our quantum chips, but the device looks and functions very differently to silicon chips. In classical computing, we calculate with this notion of bits, zeros and ones. We build transistors or tiny switches that turn on and off to represent the zero and one states. This is how we store information and do calculations. In quantum computing, we have a qubit, which stands for quantum bit, and because of the unique nature of quantum mechanics, a qubit can be either a zero or one state, or both at the same time. This is called superposition.

It sounds improbable, but this property of superposition can massively increase our ability to compute, exponentially. By exploiting the inherent, quantum mechanical properties of physical matter, we can do things that are impossible to do with classical computers.

... quantum computers hold the promise to simulate very complex atoms and molecules accurately. Beyond theoretical science, this has immense, practical implications for new product discovery and design.

TALKING POINTS

14 Asian Link | Issue 27 2017

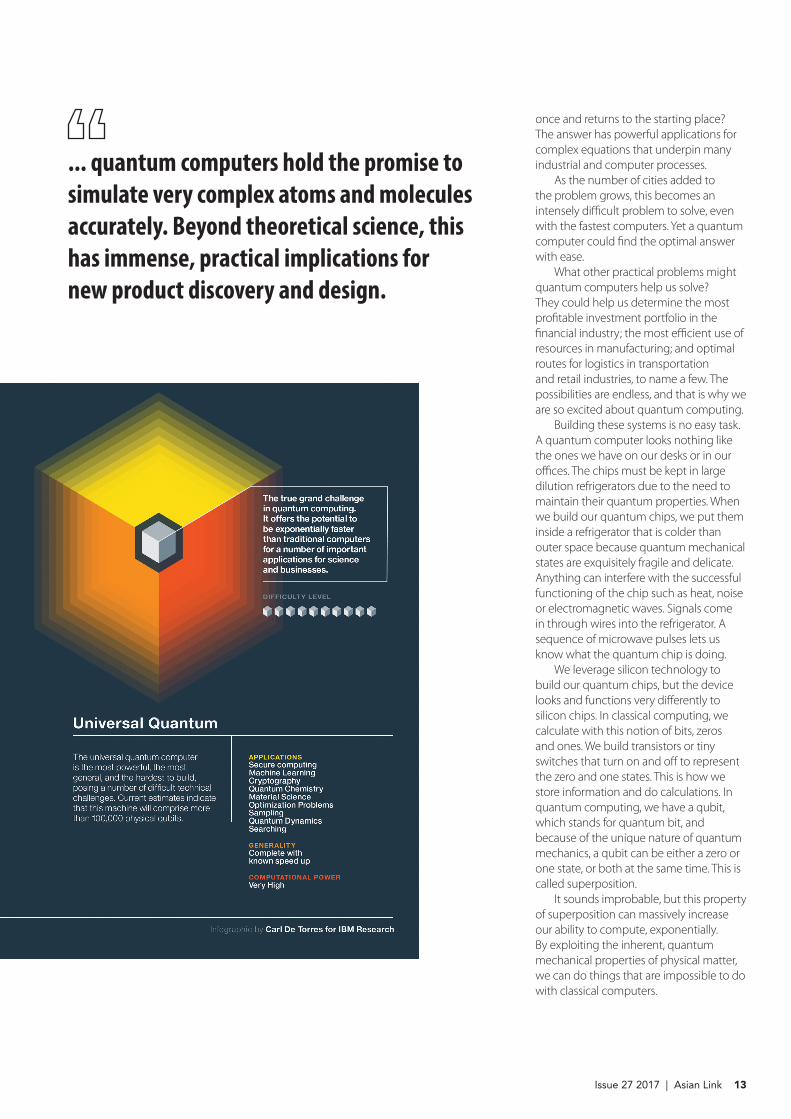

We have gone to great lengths to build massive computers to understand how molecules behave or perform hard optimisation problems, which is very expensive computationally. In contrast, a quantum system made of just 50-100 qubits would be too complex to be simulated by today's fastest and most powerful supercomputers.

We are making significant progress. In 2015 IBM Research announced an important breakthrough in methods to detect and measure the two types of errors that will occur in any real quantum computer, known as bit-flip and phase-flip. This was a necessary step toward quantum error correction, a critical requirement for building a practical and reliable large-scale quantum computer.

Then, in 2016, we launched the ‘IBM Quantum Experience’. It enables anyone to explore quantum computing and use a real five qubit quantum processor for free via the IBM Cloud. The platform, which can be accessed on any desktop or mobile device, has allowed us to grow a robust quantum computing

ecosystem and expand universal quantum computing to the developer community. So far, there have been tens of thousands of users across the globe who have run more than one million experiments.

This year, IBM announced a major milestone in the history of computing: the launch of an industry-first initiative to build commercially available universal quantum computing systems. This distinction of ‘universal’ is important, because it is the only class of quantum computer that has been proven theoretically to vastly accelerate the solution to certain problems. Other systems currently on the market have been shown to leverage quantum effects, but have not yet demonstrated any advantage over an optimised classical computer system with real problems.

Quantum computers will augment, not replace, classical computers. Classical computers will continue to carry a large share of the computational workload involved in activities like advanced research and development.

The gold coloured coaxial cables are used to send inputs and outputs from inside the fridge (credit: IBM Research).

We have gone to great lengths to build massive computers to understand how molecules behave or perform hard optimisation problems, which is very expensive computationally.

Issue 27 2017 | Asian Link 15

A universal quantum computer’s role will be as an accelerator for specific types of problems.

Indeed, the most powerful quantum systems of the next decade will be hybrids of quantum computers with classical computers to control logic and operations with large amounts of data. For example, quantum computing will improve artificial intelligence and machine learning by finding the best answers within a huge, exponential number of possibilities.

Our goal at IBM is to produce universal quantum systems with 50 qubits or more for select industry partners within the next few years. This is the size at which the system may be capable of handling problems that are impractical to solve using any classical computer, no matter how large.

Recently, we announced our most powerful quantum processor: a 17 qubit prototype that will be the basis for the first IBM Q commercial systems and will enable early-access clients to begin exploring practical applications in business and science. Additionally, we have upgraded

the IBM Q experience with a 16 qubit processor to facilitate education and research. Developers, researchers and programmers can sign up for access through a new software developer kit.

Because a quantum computer’s power depends on more than just adding qubits, we have also adopted a new metric to characterise the computational power of quantum systems: Quantum Volume. Quantum Volume accounts for the number and quality of qubits, circuit connectivity, and error rates of operations. Over the next few years, we intend to increase the Quantum Volume of future systems significantly by improving all aspects of the processors, including incorporating 50 or more qubits.

Moving forward, the scientific and technical community must come to a consensus about when quantum computing has achieved technological maturity. Some believe this should be based on a quantum system’s ability to perform obscure scientific measurements. At IBM, we believe that quantum computers must demonstrate

the capacity to solve critical problems of major business, societal, and intellectual importance to become viable. We are now aggressively working toward that goal.

We are only at the beginning of a long and fascinating journey to a quantum future. Achieving our ultimate objective of a large-scale, universal, fault-tolerant quantum computer will require many new scientific advances and years of research and development. Given the enormous challenges the world faces that are out of reach of today’s conventional computers, this is a vital undertaking – and one upon which the future of human discovery depends.

Arvind Krishna is Senior Vice President, Hybrid Cloud, and Director of IBM Research.

Image of the IBM Q Lab at the T.J. Watson Research Center, New York where IBM is building commercially available universal quantum computing systems. “IBM Q” quantum systems and services will be delivered via the IBM Cloud platform.

PERSONALITY

16 Asian Link | Issue 27 201716 Asian Link | Issue 27 2017

PERSONALITY

Issue 27 2017 | Asian Link 17Issue 27 2017 | Asian Link 17

Joel KornreichJoel Kornreich was appointed Group Chief Executive Officer of Alliance Bank Malaysia Berhad in April 2015. Prior to joining Alliance, he was with Citigroup for 20 years in various roles around the world, and is well known for his successful management of consumer banking businesses, built around superior service and innovative solutions.

Joel shares his views as a leader and in particular on how technology disruption and changing consumer habits are transforming a company-wide culture of innovation at Alliance.

PERSONALITY

18 Asian Link | Issue 27 2017

Q. What were your previous experiences that contributed to who you are as a banker? A» I started my professional career as a product manager with Unilever. While it has nothing to do with banking, this is where I picked up on the importance of research and marketing. It also taught me to be highly attuned to my numbers and to monitor performance in real time.

Early in my banking career I became a branch manager. That was also very useful in teaching me about banking operations and customer service. Other notable experiences include managing a consumer bank in Indonesia in my early thirties, which was really fantastic, as the opportunity of a systems change allowed me to reshape processes and client service experience.

Much later, negotiating settlements related to the Lehman Brothers collapse with consumer advocacy groups in several countries seeking compensation for investment losses as well as negotiating with unions, taught me how to approach various situations. You need to be very systematic, extremely detailed, look at the situation from the other party’s perspective and always be respectful.

I believe you learn at every turn and pick up skills and knowledge that you can apply on the condition, of course, that you approach every experience as a learning experience. Q. What are your key business philosophies? A» Well, first, values are key to everything. Most important to me are integrity,

I believe you learn at every turn and pick up skills and knowledge that you can apply on the condition, of course, that you approach every experience as a learning experience.

same: the need for banks to hold more capital, much more stringent liquidity requirements, stricter rules on knowing your customers and their needs, as well as on disclosures related to investment products.

The capital and liquidity rules along with the compliance costs of all these measures, have resulted in a structural reduction worldwide of profitability for financial institutions.

At the same time, technology disruption and changing consumer habits which are now accelerating, will change the face of banking. For example, the reduction in the number of bank branches is a worldwide phenomenon that will undoubtedly accelerate and the disintermediation of banks will also continue. Capital markets will have a larger share of lending than they do today, especially in countries like Malaysia where they are still underrepresented, accounting for only one third of all lending compared to two-thirds in the US. And, of course, Alibaba/Alipay and their peers are actually banks and are aiming for a large share of banking revenues in payments and lending.

Q. What have been some of your challenges as Group CEO of Alliance Bank in Malaysia? What are some of the changes you have implemented so far and have you seen any results?A» Well, I would say that my challenges as Group CEO are probably not that different from those faced by my colleagues at other financial institutions in Malaysia: the need to balance a fairly high consumer leverage with the continued demand for credit; inefficient pricing of risk; and

fairness and consistency, openness and transparency, ownership and teamwork.

As a leader, teamwork also means you must recognise that there are things you are good at and that others can count on you to help the organisation move forward. Then there are things you are really not that good at, and you must surround yourself with people who are much better than you in these things, so you can all succeed together.

For the rest, I try to focus on the purpose.

In the case of banking, we are here to manage risk by being the best we can possibly be at channeling excess financial resources from depositors and investors to those who need them for projects or consumption. We are also here, in a general sense, to help improve the financial lives of those we serve. Success comes by fulfilling these purposes, in a way that is continually better, faster, more convenient and relevant to the clients we serve.

Q. What are the recent trends and challenges in the Asian and Malaysian banking sectors? A» The banking sector is in a significant phase of mutation. These changes are primarily driven by shifts in public perception and their changing needs. I do not think this is unique to Asia or Malaysia.

First, the Global Financial Crisis of 2008 had, and continues to have, profound effects. It eroded the public trust in banks, owing to the multiple bailouts and direct public impacts such as investment losses or constrained access to credit. These issues were more pronounced in the US than here, but their consequences are the

Issue 27 2017 | Asian Link 19

to catch up in important areas such as compliance in anti-money laundering (AML), customer needs discovery and service and the need to adapt to changing customer habits and technology.

We first focused on improving the efficiency of the bank by putting in place a focus on risk-adjusted returns and at the same time improving our capital and liquidity positions. As a result, our margins which had been in a multiyear decline recovered to a very healthy 2.3%, third highest in the industry, and our return on equity (ROE), currently at 10.7%, improved to number two in the industry, while our CASA ratio1 stands at 35%, also near the top of our peer group.

In the meantime, we defined our strategy which is to be the most important relationship for the financial success of business owners, and we are now executing it under the banner and vision of ‘Building Alliances to Improve Lives’. This has led us to launch innovative value propositions, such as ‘Alliance One Account’, which consolidates consumer debts into one product and helps people lower their monthly payments and save money, or ‘Alliance Cash2Home’, which uses facial recognition and optical character recognition to allow foreign workers to open an account and remit money home instantly without any paperwork.

We are also reconfiguring our branch network, accelerating our SME business with new products and simplified processes and will soon be launching our mobile banking service.

Q. Being a small and less well-known bank in Malaysia, what is Alliance doing to promote awareness among consumers?A» ’Alliance One Account‘ was our first significant foray into digital media, including social media mass marketing, and it is exceeding our expectations. This is something we will be accelerating in the coming months. Our primary focus is clearly to help business owners succeed in their business ventures and also to protect and grow their personal finances and those of their stakeholders, their employees and business partners. In addition, we will have a few very compelling consumer offers, such as ‘Alliance One Account’, that we will advertise.

Q. The younger generations, namely Gen Y and Gen Z, are online savvy and generally prefer to conduct financial transactions on mobile devices. How is Alliance Bank addressing this and what products and services can we expect?A» Consumer habits are changing fast, and not only for younger generations. We are of course adapting, such as with the upcoming launch of our mobile banking app, and in some cases, where we believe it fits our strategy centred on business owners, as in the example of ‘Alliance Cash2Home’.

1 The CASA ratio of a bank is the ratio of deposits in current and saving accounts to total deposits. A higher CASA ratio indicates a lower cost of funds, because banks do not usually give any interest on current account deposits and the interest on saving accounts is usually very low 3-4%.

RETURN ON EQUITY (ROE)

CASARatio

NET INTEREST MARGIN (NIM)

10.7%

2.32%

35%

Aboveindustry average

improved to

PERSONALITY

20 Asian Link | Issue 27 2017

... the reduction in the number of bank branches is a worldwide phenomenon that will undoubtedly accelerate and the disintermediation of banks will also continue.

Issue 27 2017 | Asian Link 21

To enhance a company-wide culture of innovation, we have invested in many workshops where people from all parts of the organisation are able to contribute ideas and projects, while we have instituted company-wide rituals such as weekly huddles where we all get to contribute to the transformation projects.

As a minimum, consumers expect to be able to do everything on their mobile phones and we will fulfil this need. But you can also expect Alliance Bank to launch more innovative products like ‘Alliance Cash2Home’ in the future as well.

Q. What is the bank’s growth strategy for the future?A» We are very focused on our core competencies and we have defined our mission as providing innovative solutions that are fast, simple and responsive, and aligned to our customers’ needs.

This is the case for ‘Alliance One Account‘, which we are scaling up, and also with our SME lending programmes, which we are improving. These, along with more convenient consumer-lending propositions, will fuel our growth. We are also continuing to grow our commercial and corporate businesses, primarily thanks to the quality of our relationship with our clients, of which we are very proud of.

Q. How is digital disruption affecting the banking landscape particularly in terms of talent management and human capital development?A» Talent in digital and technology development and creativity is scarce in the industry. But the new way of working around these issues is to have a very good, fairly small core team at the bank, and to supplement that with partnerships, whether with FinTechs, or larger technology firms to deliver solutions to the market.

Q. Given recent trends in financial services, namely ‘FinTech’, how important is enhancing innovation at Alliance and what are you doing to create an innovative culture?A» Two years ago, we created a Group Transformation team to look at digital and lifestyle banking offerings at the bank. We are fortunate that our Group Chief Operating Officer, who leads the transformation team, comes from a culture of technology start-ups and transformation. The team came up with ‘Alliance Cash2Home’, as well as other

retail innovations that are in our pipeline in addition to developing our mobile banking solution.

To enhance a company-wide culture of innovation, we have invested in many workshops where people from all parts of the organisation are able to contribute ideas and projects, while we have instituted company-wide rituals such as weekly huddles where we all get to contribute to the transformation projects.

Q. What advice can you give for young professionals embarking on a career in banking today?A» Whether in banking or anywhere else, try to figure out what motivates you, what you like, and what you are good at. Make sure you approach what you do with an open mind, the desire to learn and grow, and remember that life is not a straight line. You will have ups and downs, but know that the downs are more often than not a great opportunity to learn and bounce back. Do not get discouraged by failures: reflect on them and move on.

Most importantly, make sure you stick to your values. Integrity is not negotiable: keep your moral compass straight, always. And of course, try to make a difference for the good. Knowing that you helped others along the way, your family, colleagues and clients, is surely the most satisfying feeling of achievement you can get.

Q. How do you find time to relax?A» Everyone must absolutely make the time to relax and switch off. It is indispensable to being productive in the long run: you need to be stimulated by new ideas, recharge your batteries and have the time to reflect in order to advance. With your nose to the grindstone non-stop, you risk not learning and, most importantly, not having perspective. In my case, I love to read and reflect on what I can learn and observe. To disconnect completely, I collect stamps and engravings, for the history they evoke and to admire the art of engraving and design.

Joel Kornreich is Group Chief Executive Officer, Alliance Bank Malaysia Berhad.

AIF conducted a study to demonstrate how visual and auditory cues can impact the way in which consumers perceive, feel and engage with financial services. As digitalisation continues apace, it is important that the industry embraces the concept of enhancing consumer trust in its online presence through multisensory aesthetics.

enhancIng dIgITal TrusT In fInancIal servIcesA Multisensory Approach

22 Asian Link | Issue 27 2017

FEATURE

ncreased trust in online banking and insurance products and services could enhance the appeal of a range of financial

services products by converting more users to digital. Can a multisensory approach to online financial services enhance digital trust? A study of the relationship between trust and visual aesthetics, multisensory perception and the design of online space in the financial services industry (FSI) was undertaken by the Asian Institute of Finance (AIF) in conjunction with the Imagineering Institute1.

I

A first of its kind in Malaysia, if not we believe in the region, this study was undertaken not only to test how sensory cues can impact the way in which consumers perceive, feel and engage with financial services, but also to capture the interaction effects between various sense-perception stimuli in terms of online trust in financial services.

The FSI is likely to continue to digitalise with an ever-increasing momentum, meeting consumer expectations for real-time, ubiquitous service convenience.

Issue 27 2017 | Asian Link 23

1 The Imagineering Institute is a new research lab with the vision ‘Invent the Future of Internet’. It is the first independent multi-disciplinary internet and digital media research and development institute focusing on internet, digital media and mixed reality research, while providing an entrepreneurial incubation space for start-ups.

http://imagineeringinstitute.org/about/

The FSI is likely to continue to digitalise with an ever-increasing momentum, meeting consumer expectations for real-time, ubiquitous service convenience. In the future consumer interactions are likely to be multimodal, where customers will be faced with multisensory stimuli. Hence, a crucial issue in the digitalisation process is managing and consolidating the high volume of multimodal customer data coming in a range of formats, such as texts, voice logs, images and videos. Building on the literature of visual aesthetics and trust, as well as multisensory perception and design, our research focused on how visual and auditory information influences trust in relation to financial services. For example, previous research has shown that there is a tendency for people to match shapes and colours: circles are associated with red, squares with blue and triangles with

yellow2. Similar tendencies are reported for sound features3. Also studies have suggested that generally people feel more pleasant and involved when they are exposed to fast music (versus slow music) in online stores4. Therefore, by using sounds that people trust, could trust in online banking and insurance be enhanced?

In conjunction with the Imagineering Institute, a series of tests were run. First we assessed unilaterally how visual features and auditory features influence trust in online banking and insurance services. The objective of the preliminary scenarios was to assess the way in which customers associate different colours, shapes and sound features with trust. Subsequently, another two multisensory experiments tested the joint effects of visual and auditory stimuli on digital trust, using multiple website templates designed for banking and insurance

services. One multisensory scenario tested these effects in an international context while another tested these for selected samples in South East Asia. The main multisensory tests were run only after establishing what stimuli were viewed as being ‘trustful’ versus ‘distrustful’ at the preliminary stage. The idea was to test the more or less ‘trusted’ design elements to see whether they would influence trust in online banking and insurance environments.

Unisensory findingsThe results suggest that certain colours (e.g. blue and white), shape features (e.g. symmetry) and sound features (e.g. silence or ascending tones) enhance trust, whereas others tend to hinder it (e.g. red, asymmetry and descending tones).

Figure 1: Summary of the percentage of ‘trust’ responses as a function of colour, brightness and hue

83%

68%

64%

79%

51%

56%

35% 34%

54% 62%

33%

54%

31%

43%

Bright Dull

White Blue Purple Black Green Red Yellow

40%

52%

25%

41%

BlueWhite Black Red

Bright Dull77%

66%

73%

78%

46%

56%

Purple

40%

66%

Green

44%

47%

Yellow

FEATURE

24 Asian Link | Issue 27 2017

2 N. Chen, K. Tanaka and K. Watanabe, ‘Colour-shape associations revealed with implicit association tests’, PloS one, vol. 10, no. 1, pp. e0116954, 2015.3 V. S. Ramachandran and E. M. Hubbard, ‘Synaesthesia – a window into perception, thought and language’, Journal of Consciousness Studies, vol. 8, no. 12,

pp. 3-34, 2001.4 F. F. Cheng, C. S. Wu and D. C. Yen, ‘The effect of online store atmosphere on consumer’s emotional responses – an experimental study of music and colour’,

Behaviour & Information Technology, vol. 28, no. 4, pp. 323-334, 2009.

Banking Insurance

Colours and trustWe evaluated the way in which people trust colour features, namely hue and brightness. Seven colours were used as stimuli in the study, both in bright and dull versions, giving a total of 14 colour stimuli. The results of both the banking and insurance groups revealed consistent results in terms of the most trusted colour dimensions: white and blue are trusted more than any of the other colours and dull colours are consistently trusted more than bright colours (Figure 1).

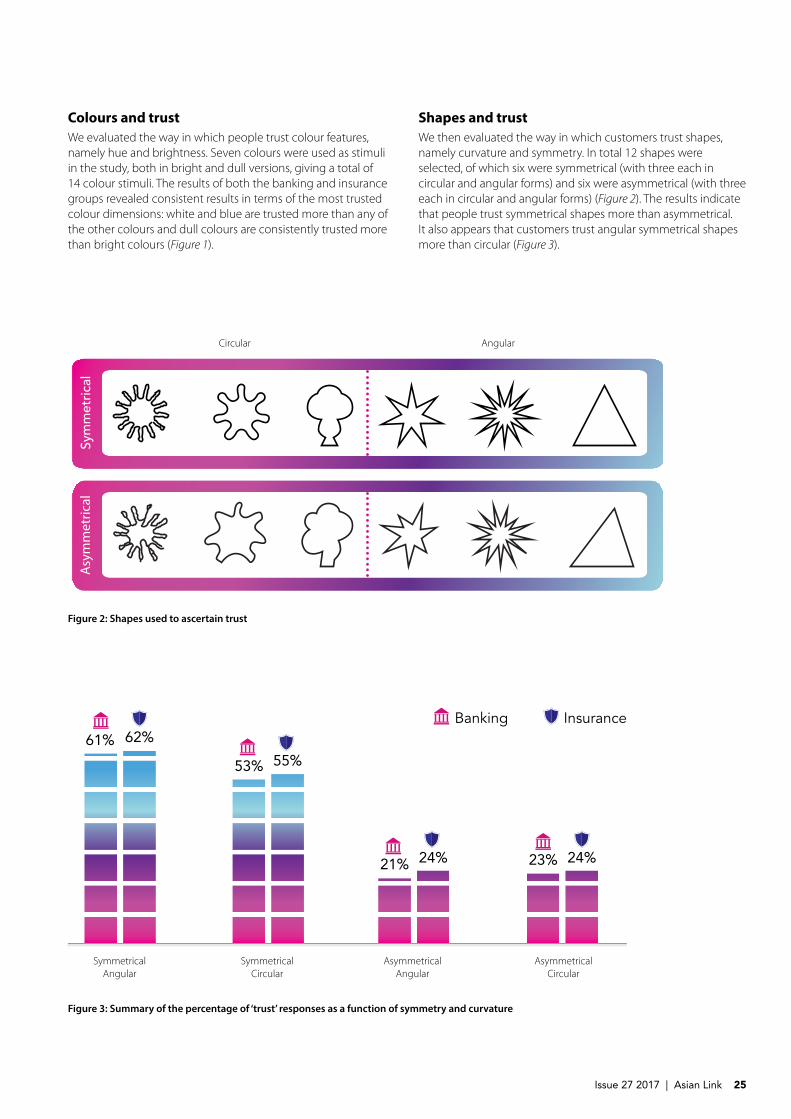

Shapes and trustWe then evaluated the way in which customers trust shapes, namely curvature and symmetry. In total 12 shapes were selected, of which six were symmetrical (with three each in circular and angular forms) and six were asymmetrical (with three each in circular and angular forms) (Figure 2). The results indicate that people trust symmetrical shapes more than asymmetrical. It also appears that customers trust angular symmetrical shapes more than circular (Figure 3).

Figure 2: Shapes used to ascertain trust

Figure 3: Summary of the percentage of ‘trust’ responses as a function of symmetry and curvature

Sym

met

rica

l

Circular Angular

Asy

mm

etric

al

53% 55%

24%21%

SymmetricalAngular

SymmetricalCircular

AsymmetricalAngular

AsymmetricalCircular

23% 24%

62%61%

Banking Insurance

SymmetricalAngular

SymmetricalCircular

AsymmetricalAngular

AsymmetricalCircular

Issue 27 2017 | Asian Link 25

Sound and trustWe then evaluated the way in which customers trust sound features, namely volume, speed, direction and pitch. Significant associations were found between trust in online banking and ascending (versus descending) sounds, and with low (versus high) pitch. Indeed, at the unisensory stage, ascending sounds were significantly associated with trust in both online banking and insurance services.

With the increasing digitalisation of the FSI as well as FinTech disruption, building consumer trust has never been more crucial. Not only do organisations need to build trust into the fabric of their digital operations, but this needs to be communicated to customers.

Figure 4: Summary of the percentage of ‘trust’ responses as a function of sound features

Banking Insurance

Fast Slow Fast Slow HighVolume

LowVolume

HighVolume

LowVolume

Ascending Descending High Pitch Low Pitch

28%

25%

12%15%

32%

48%

56% 56%

Fast Slow Fast Slow HighVolume

LowVolume

HighVolume

LowVolume

Ascending Descending High Pitch Low Pitch

24%

34%

19%21% 22%

49%

29%

57%

Multisensory findingsThe multisensory findings revealed that trust was enhanced in yellow hue websites for all samples particularly for insurance services and customers trusted white designs significantly more than any of the other colours. Customers also trusted blue designs more than red.

The results revealed that customers trust symmetrical designs more than asymmetrical for both banking and insurance services. The effect of symmetry was much more pronounced for insurance websites. As for the effect of sound, customers trusted the designs more when there were no sounds than when they were accompanied by either ascending or descending tones.

FEATURE

26 Asian Link | Issue 27 2017

Figure 5: Mean ‘trust’ responses as a function of colour, symmetry and sound for banking websites

Figure 6: Mean ‘trust’ responses as a function of colour, symmetry and sound for insurance websites

Symmetrical

Asymmetrical

Sound

Colour

Ascending

31%

18% 63% 39%

14% 63% 37%

36%

32%

17% 66% 39%

14% 62% 38%

Silence

33%

33%

18% 65% 38%

14% 62% 38%

Descending

36%

Symmetrical

Asymmetrical

Sound

Colour

30%

38% 54% 62%

20% 36% 39%

50%

33%

45% 62% 64%

24% 39% 48%

45%

30%

37% 54% 55%

20% 36% 38%

48%

Ascending SilenceDescending

Cross-country findingsWe then assessed the cross-cultural effects by conducting multisensory tests in four different South East Asian countries namely Indonesia, Malaysia, Philippines and Singapore. The results indicated that the effects of colour hue in banking are significant in all four countries. Customers from all the countries trust the white designs significantly more than any of the other colours. Yellow is the second most trusted colour in Singapore. For banking websites red designs are the least trusted in all countries. Insurance customers trusted white and yellow designs significantly

more than blue and red designs in all South East Asian countries. As for insurance, yellow is the most trusted colour in all countries. Customers also trust blue designs more than red designs except in Malaysia.

These cross-country differences indicate that digital customer engagement strategies need to appeal to local and regional tastes and expectations.

With the increasing digitalisation of the FSI as well as FinTech disruption, building consumer trust has never been more crucial. Not only do organisations need to build trust into the fabric of

their digital operations, but this needs to be communicated to customers. The relevance of the study is to demonstrate to FSI players the importance of enhancing digital trust through online multisensory aesthetics. The findings indicate that financial services institutions should consider multisensory factors when developing their online presence. Striking the right multisensory balance may enhance consumer digital trust.

Elma Berisha is General Manager, Strategy, Policy Development & Research, AIF.

Issue 27 2017 | Asian Link 27

TALKING POINTS

28 Asian Link | Issue 27 2017

John McFarlane, Chairman, Barclays Bank PLC, UK, explores the scale of issues faced by the banking sector as a result of the three crises which have transformed the shape of banking worldwide together with the degree of change forced upon it by technology, competition and regulation, and how best to steer banks through these changes and create a more sustainable future.

have spent 42 years in banks and led firms as CEO or Chairman for almost half of this. Frankly, though it has been a

fascinating learning experience, often it is been less than a fun ride, involving three crises, particularly the most recent one in 2008 which has transformed the shape of banking worldwide. The decade since has seen more change in this sector than experienced since the days of the Medici, and the decade ahead will augur even greater change as the digital age takes root.

Since much of our discussions here will be on technology, I will simply cover it in passing. What I will concentrate on is the current state of banking, how we got here, and some thoughts on the way forward. Given the scale of the issues faced by the sector as a result of the crisis and the degree of change forced upon it by technology, competition, and

I

John McFarlane

Major Forces Transforming Banking

Issue 27 2017 | Asian Link 29

half the assets it had ten years ago.We forget at our peril, banking is

cyclical, leveraged on the economic cycle. Yet in my 42 years I have never seen a business plan that has built in a cyclical effect. All plans go up and in good times there is sheer disbelief that anything could go wrong.

While plans inevitably go up, realities often go down. When that happens in banking, given the high financial leverage, if we overextend in normal or good times, at one extreme we cease to exist, or end up in intensive care for a long time.

Another factor that emerged post-crisis was the realisation that a significant degree of misselling and market manipulation by traders had occurred. Conduct regulation expanded considerably as did the cost of compliance. This led to considerably, and some yet unresolved, customer restitution, fines and penalties, let alone potential civil legal action. In all cases of conduct breach, incentive remuneration was present.

Quinlan and Associates published a report that the top 50 banks globally since 2009 have paid US$342 billion in fines and penalties. It is estimated in the report that the total economic impact will ultimately be US$1 trillion including collateral impacts.

Bank failure is inevitably followed by regulatory tightening. Prior to the crisis, prudential regulators have doubled the level of required capital for banks, and for systemic ones, up to two and a half times. This has been accompanied by the requirement additionally to hold an even larger amount of loss-absorbing

regulation, I will conclude as to how best to steer our companies through this and create a more sustainable future.

Ten years ago, the two largest banks in the world were British, RBS and Barclays. Today, the top eight ranked by capital, are either from China or the US, the largest from China. Today Barclays and RBS rank 16th and 21st.

What is especially interesting is the ranking by market to book value. This is an important way of looking at companies, since financially, the value of the company is the sum of the capital invested plus the present value of excess returns over the cost of capital. If the ratio is high it signifies high expected return or intangible value. More concerning, if lower than one, i.e. not expected to produce the cost of capital, then the present value of excess returns, or intangible value is negative.

Of the top ten banks on this measure, three are American, two Canadian, two Brazilian, and one each from Australia, India and Hong Kong. So, there are indeed many good and performing banks. These banks tend to be largely domestic.

At the other end of the scale, one-third of the top 60 banks are still trading below book value, and many significantly so, nine years after the crisis. The ones trading at a significant discount to book tend to be those who were most impacted by the global financial crisis especially in the UK and Europe, or the legacy of historical issues with the Japanese economy.

So, what can we learn from this? It is hardly surprising that the strongest banks are from the largest markets or healthiest economies, as banks are only as good as the environment they operate in. Similarly, those most negatively impacted are from countries where there are more subdued economies and low or negative interest rates, and this is part of the reason they are having the greatest difficulty in recovering.

This is not the only explanation. In general, prior to the crisis, banks significantly overextended themselves, entered markets not natural for them, such as sub-prime mortgages in the US, took too much risk, were undercapitalised or underfunded and therefore are now paying the price by shrinking to the point of potential viability. Barclays today has

Ten years ago, the two largest banks in the world were British, RBS and Barclays. Today, the top eight ranked by capital, are either from China or the US, the largest from China.

Quinlan and Associates

Top 50 Banks Globally since

2009

paid

US$342billion

in fines and penalties

TOTAL ECONOMIC IMPACT

US$1 trillion including collateral

impacts

TALKING POINTS

30 Asian Link | Issue 27 2017

It was the advanced economies that bore the brunt of the pain from the global financial crisis largely fostered by artificially low long-term interest rates, leading to financial and real property bubbles, and then only to endure another decade of low or negative interest rates arising from the efforts of governments to stimulate their economies artificially.

debt such that, in the event of failure, the burden going forward will largely be met by shareholders and debtholders rather than the state.

This additional capital requirement has potential negative impacts on the economy exacerbated by lower lending, lower profits and therefore lower taxation collected.

With the additional capital burden, returns have fallen proportionally, raising questions as to the viability of existing business models. Banks are therefore faced with accepting lower, utility-like returns or adjusting their business models to focus on higher growth, higher return, lower capital-absorbing activities such as wealth and investment management and away from lower yielding capital hungry activities such as wholesale lending and markets.

It has meant much of the traditional branch network of banks is rapidly becoming redundant as customers switch to mobile services, as well as uneconomic for other than high added-value face-to-face services, transactions and advice. Over the long run, even much of this will be replaced by automation.

In Denmark and Sweden, banks have rapidly moved away from providing teller and ATM services, in favour of card and electronic payments, enabling banks at the same time to optimise their branch networks for more complex services and for the digital age.

The safety of the banking system has clearly been enhanced, such that the too big to fail issue has been resolved, but its future is less certain due to a number of

factors including the level of political and economic uncertainty.

Uncertainty is bad for business.We cannot hide from the reality that

we are facing an unusual level of political uncertainty ranging from a different style of leadership in the US, traditional players in Europe being cast aside for newer models, Brexit, and not to mention the Middle East and North Korea.

While global growth appears superficially normal, its makeup consists of materially higher than average growth in China, India and younger emerging economies in Asia, South Asia and Africa, offset by below par growth in advanced economies.

The UK for example was recently the fastest growing of the G7, and is now the slowest. Going further back in time, prior to it joining the EU it had the slowest growth of the major European countries, and prior to the exit referendum, the highest. Quite telling.

It was the advanced economies that bore the brunt of the pain from the global financial crisis largely fostered by artificially low long-term interest rates, leading to financial and real property bubbles, and then only to endure another decade of low or negative interest rates arising from the efforts of governments to stimulate their economies artificially.

In the US for example the Fed printed a trillion new dollars, taking its balance sheet to US$4 trillion, never before seen. In many European countries people pay to hold cash in bank accounts. In the UK, low investment returns have taken the public-sector retirement deficit to around

US$2.4 trillion, completely un-funded and therefore a burden on current and future taxation.

Clearly there is a need to get off this treadmill and to move gradually towards normality, but easier said than done. Most commentators believe we are in for a period of rising interest rates, but note this – in the US since 1950 there have been 13 periods of interest rate tightening by the FED which in 10 of the 13 resulted in recession.

So, the question is, where does banking go from here?

A recent Bain study contrasted the shifts in market capitalisation over the past decade in US banking and technology firms. The only giant American banks to increase their market capitalisation over that time were JPMorgan Chase and Wells Fargo. In contrast, the market cap of Apple and Amazon went from US$10 and US$16 billion respectively to US$618 and US$358 billion. Apple is now twice the market value of the largest US bank, and larger than all banks globally.

We are seeing a shift in investment towards tomorrow’s sectors and faster growing economies from banking to technology, and from Western economies to large population, fast growing economies with low per capita incomes, such as China, India and Indonesia.

For banking, it means a shift towards FinTech and lower cost technological solutions, taking advantage of cloud-based systems and mobile devices. It is also a move away from cash to digital payments. Traditional branches are being closed as people are no longer using

Issue 27 2017 | Asian Link 31

... as consumers and businesses rapidly embrace mobile technologies, mobile payments and other real-time solutions, banks need urgently to reinvent themselves as financial technology companies that provide banking services.

them. Denmark and Sweden are almost cashless societies, with a shift away from tellers and ATMs towards card, mobile and other touch and voice devices to purchase goods and services.

All of this in turn makes it possible to offer banking services to the unbanked. In this respect, it is striking that in India over a billion people will have digital identities, which in turn opens up banking and helps bring about a cashless society. This in turn reduces the black economy and enhances the collection of government sales taxes.

The adoption of mobile and online technologies by consumers has been exponential. Online retail sales account for 17% of US sales, largely dominated by Amazon, EBay, Apple and Samsung who are growing above 20% per annum.

Ant Financial which is associated with Alibaba, is the most valuable FinTech company in the world and operates the world’s largest mobile payments platform. Estimates of its future IPO value are greater than that of the leading banks in many countries. Some speculate that technology companies such as Facebook and Google could control customer access, leaving banks to be utility subcontractors of the most heavily regulated services.

Accordingly, as consumers and businesses rapidly embrace mobile technologies, mobile payments and other real-time solutions, banks need urgently to reinvent themselves as financial technology companies that provide banking services.

The opportunity created by the digital economy for those who are innovative, lean and agile is immense, as is the very real threat from new lean and agile competitors.

Inevitably banks have been rapidly adopting FinTech solutions such as mobile apps and blockchain to their businesses, customer channels, technologies and operations. This will also involve using algorithms and customer data as a competitive advantage in tailoring services to individuals.

For banks, it will require massive innovation and investment in platforms, technology and digital channels in order to be competitive in the future, as well as a radical reduction in cost. These and emerging regulatory changes to open markets to new competitors, for example the payments system, are likely to put sustained near-term pressure on bank profitability.

Standing back from all of this, how we view the future and how we plan for it fundamentally needs to change. Opportunities come to those with a unique offering so innovation is key, particularly technological. At the same time, how we handle risk also needs to change.

There are therefore significant implications as to how banks plan strategically for the future, as to how to survive, how to innovate, how to become competitive and productive. They need to determine what sort of companies they want to be long-term and to avoid the pitfalls of the past. This poses very significant challenges for bank boards and management.

Traditionally planning for the future generally starts with the reality of where we are today, and moves this base forward. The essence of strategic planning, however, is two-fold, firstly to consider alternatives to plans to

TALKING POINTS

32 Asian Link | Issue 27 2017

sponsor innovation and creativity and select the best option. Then it is about embracing a vision of what we want to become, while at the same time, having a clear understanding of where we are. The challenge is then to shift what we have to what we want.

At some point, of course, it is necessary to be clear as to how we will achieve it, but not necessarily upfront, if we have confidence in the vision. For example, in May 1961 when President Kennedy said the US will have a man on the moon by the end of that decade, they did not know how they were going to do it. They would work it out over time.

The cognitive dissonance of holding both the vision and the reality in our minds at the same time, is what opens up creativity in the subconscious, to see and create new opportunities to drive us towards our vision, as well as recognising threats that might derail us, so we can work around them.

From this process an agenda is formed that becomes sharper through time and from which execution plans can be developed. In this respect, personally I like to ensure that the organisation has no more than three priorities at any point in time.

As an example, the median bank in the top 60 has US$60 billion in equity capital invested in today’s proposition. Traditional planning would be to start with the existing business and plan how to take it forward from here, reallocating resources to the best opportunities and away from the weakest. That will certainly improve the business going forward, but does it take us to the best outcome possible?

Imagine instead, like FinTech companies, the bank had a clean sheet of paper and we gave them US$60 billion to create a banking business in any way they wanted, they would do things very differently, including only investing in the fastest growing and highest return propositions and markets, and using the latest technologies and the most efficient processes and locations. They are unlikely to invest in some or all of our existing ones.

It is easier and less costly to start afresh with the new propositions based on the latest technologies than to change existing business models and platforms. Now I realise this is academic, as we do not start with a clean sheet of paper, but at least we know the best way to invest US$60 billion, and this gives us a new strategic challenge to transform our existing proposition into the new one to the maximum extent possible, rather than simply taking the existing way forward incrementally.

Given the propensity of many banks for getting into difficulty in cyclical downturns the principle of planning for the best and hoping the worst does not happen is no longer viable. Instead it involves creating a new distinctive future, while at the same time insuring against adverse circumstances. For banking there is no choice. It means embracing the new and shedding the old. It means leaving something on the table in good times, to protect ourselves when things eventually turn down.

But it is not just a lesson for banks. Truly outstanding companies focus on making a long and lasting

The institutionalisation of capital has had a significant impact on short-termism. Whereas shareholders purport to seek superior long-term returns, in reality many are consumed by short-term performance.

contribution to all their stakeholders, as well as producing superior financial outcomes. Their leaders are very clear on why their people should devote their working lives to the adventure, why a customer should deal with them and not with another, why suppliers should give them priority, why the community should trust them and why investors should invest long-term in them.

At the same time, sadly, I have been disillusioned by the predominantly short-term and financial orientation of others, and the breaches of fiduciary duty and ethics that have occurred, particularly in my own profession. So why is it that a few enterprises succeed and are successful over decades while most falter and are left by the wayside, in relatively short order?

As an illustration of this, in the UK, the FTSE 100 index began in 1984. When the index celebrated its 20th anniversary, only 23 of the original 100 remained. This had been a generally consistent finding over time in every major economy.

The reason is industries have life cycles – they grow and fade. Successful companies buy up unsuccessful ones. Companies make mistakes, and fall behind.