Embed Size (px)

Citation preview

MESSAGE OF THE CHAIRMAN AND THE CHIEF EXECUTIVE OFFICER

I. CORPORATE INFORMATION

1.General information

2.History and development

3.Organization and management structure

4.Development orientations

5.Risks

II. BUSINESS PERFORMANCE IN 2013

1. Operations, financial conditions and business results of 2013

2.Organization and personnel

3.Investment in Debt Management and Asset Exploitation Company (Eximbank AMC)

4.Number of shares and shareholding structure of Eximbank

III. REPORTS AND ASSESSMENTS OF THE BOARD OF MANAGEMENT

1. Evaluation of business performance

2. Financial conditions

3. Improvements in organization structure, policy and management

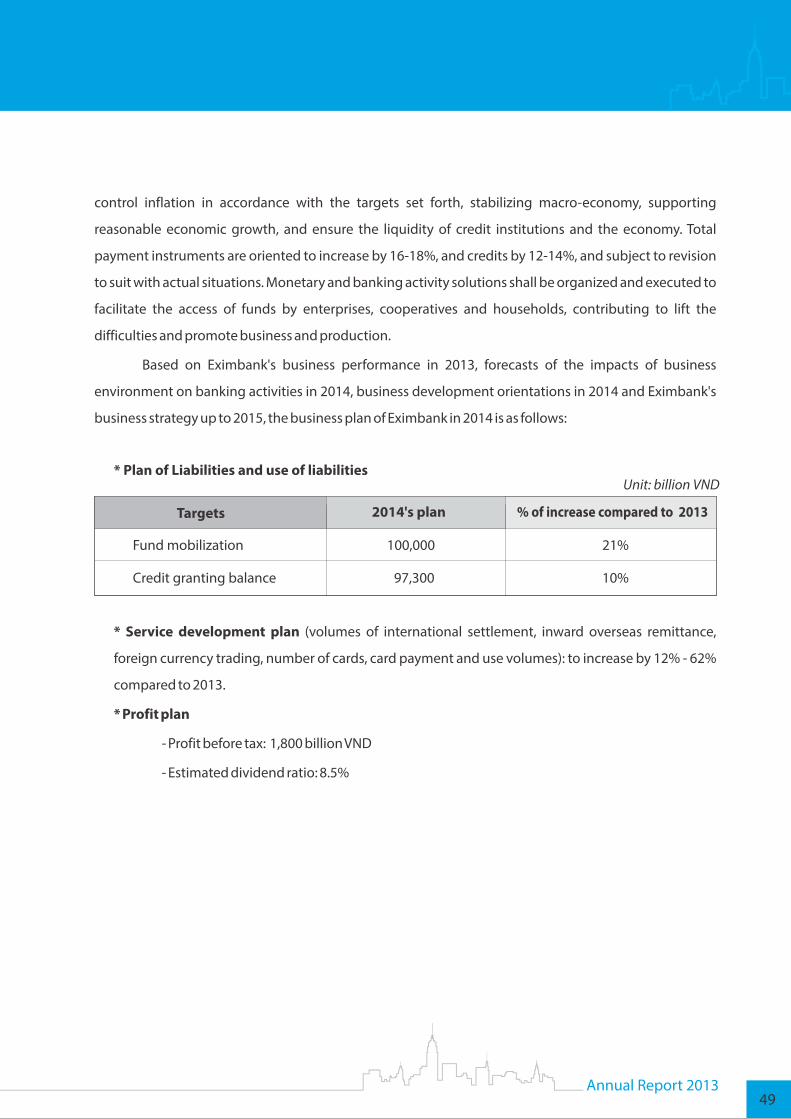

4. Business plan in 2014

IV. THE BOARD OF DIRECTORS' EVALUATION OF THE PERFORMANCE OF THE BANK

1. The Board of Directors' evaluation of operational aspects of the Bank

2. The Board of Directors' evaluation of the performance of the Board of Management

3. Plans and orientations of the Board of Directors

V. CORPORATE GOVERNANCE

1.The Board of Directors

2.The Board of Supervisors

3.Transactions, remunerations, and interests of the Board of Directors, the Board of Supervisors and

the Board of Management

VI. FINANCIAL STATEMENTS

1.Consolidated financial statements

2.Opinions of internal auditors

MILESTONES IN 2013

AWARDS

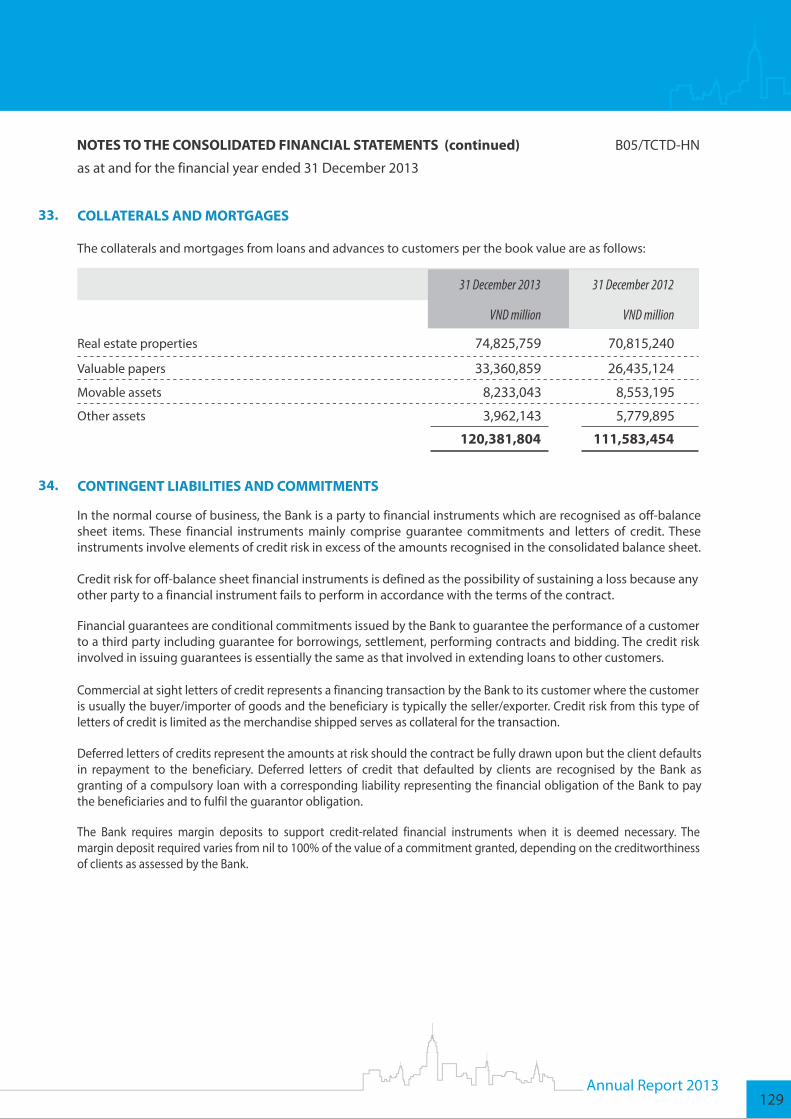

COMMUNITY-ORIENTED ACTIVITIES

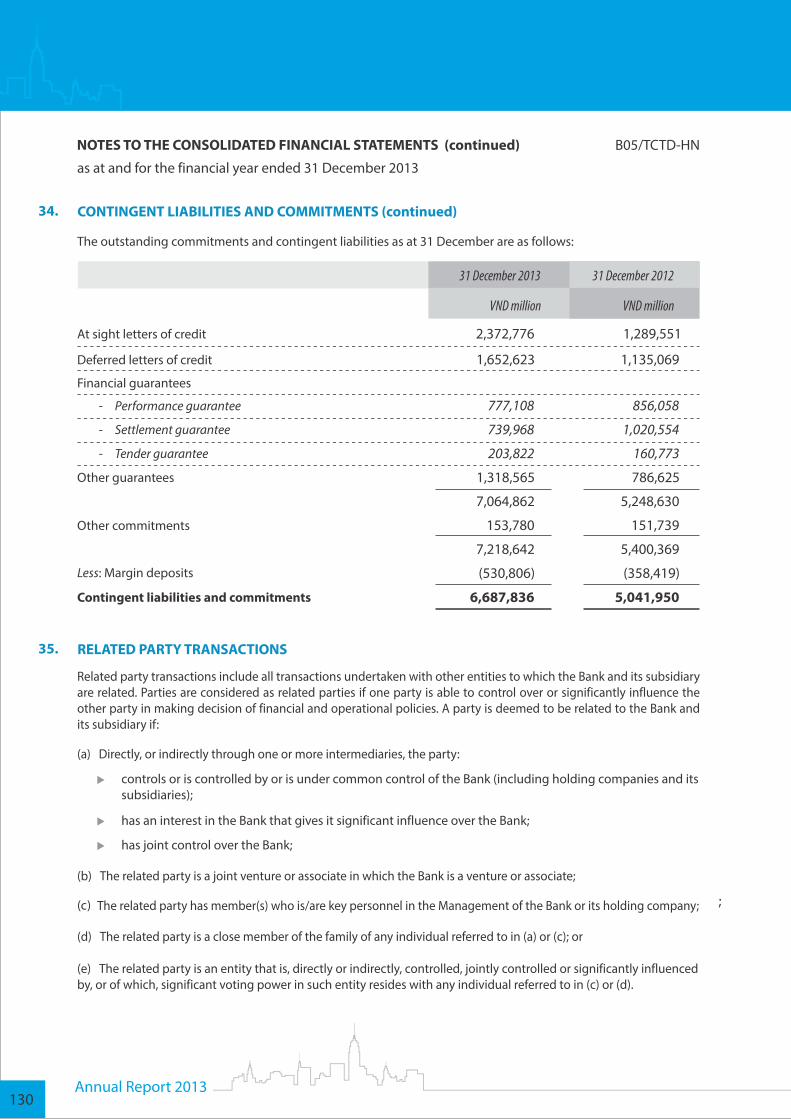

OPERATING NETWORK

Annual Report 20133

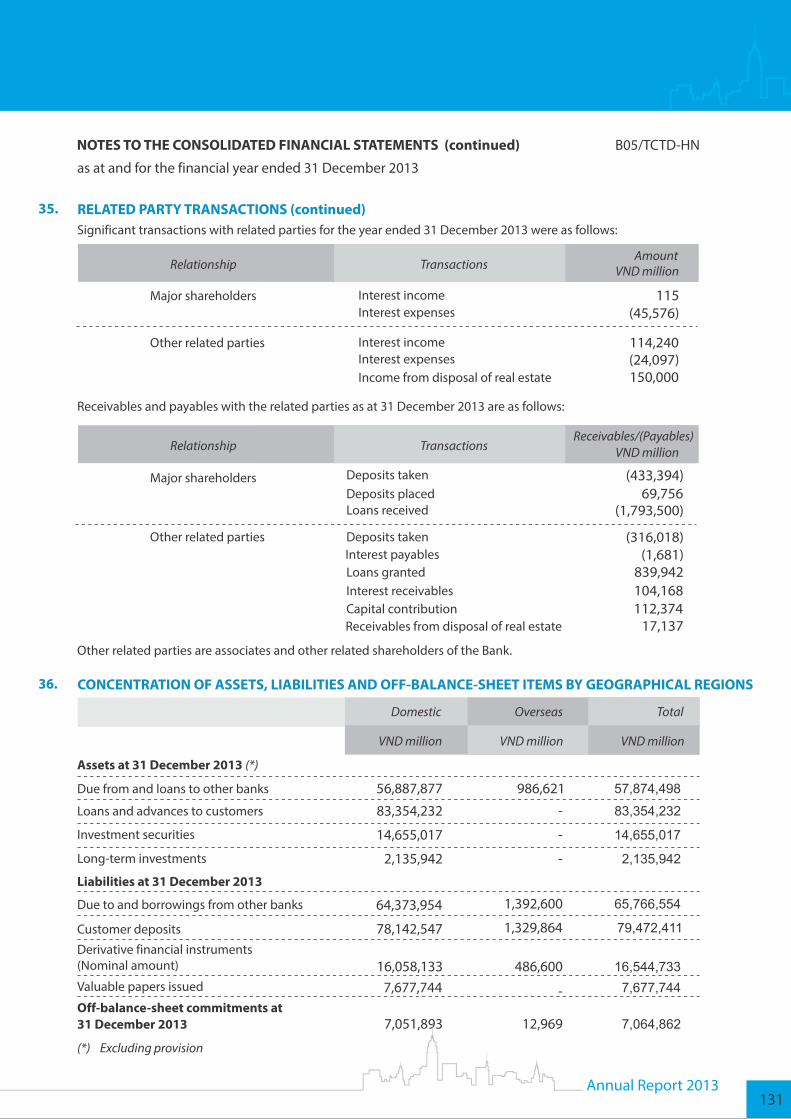

TABLE OF CONTENTS

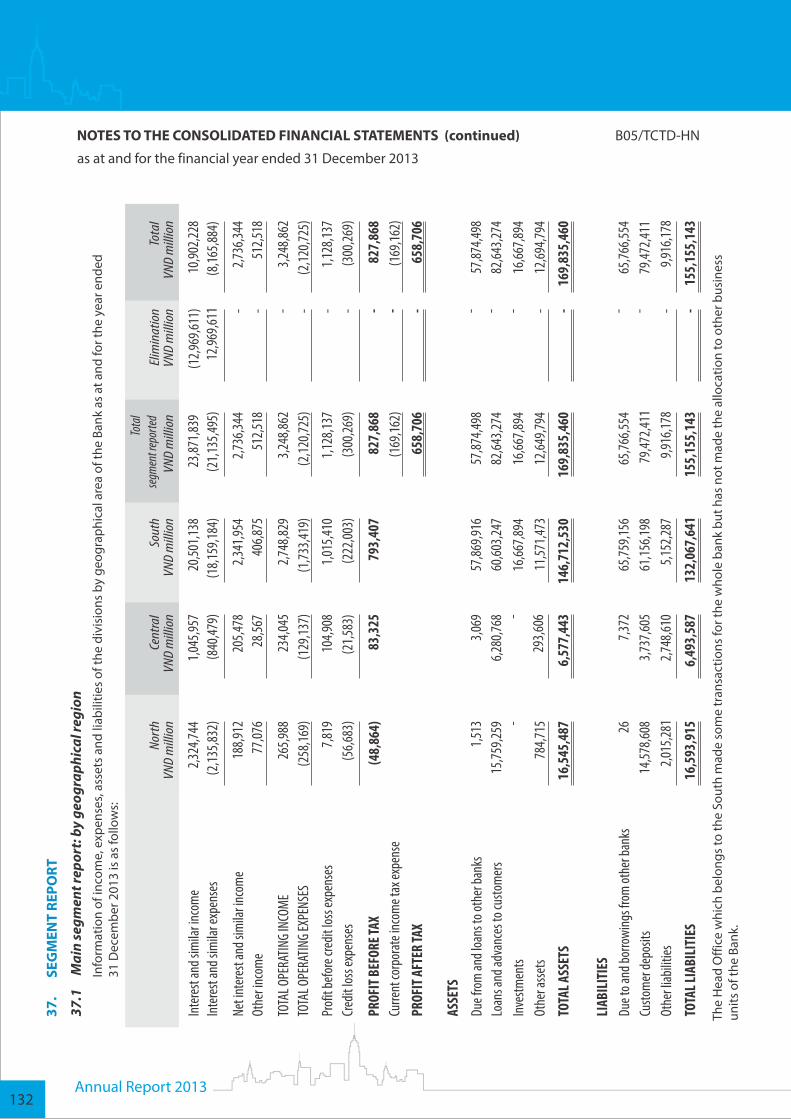

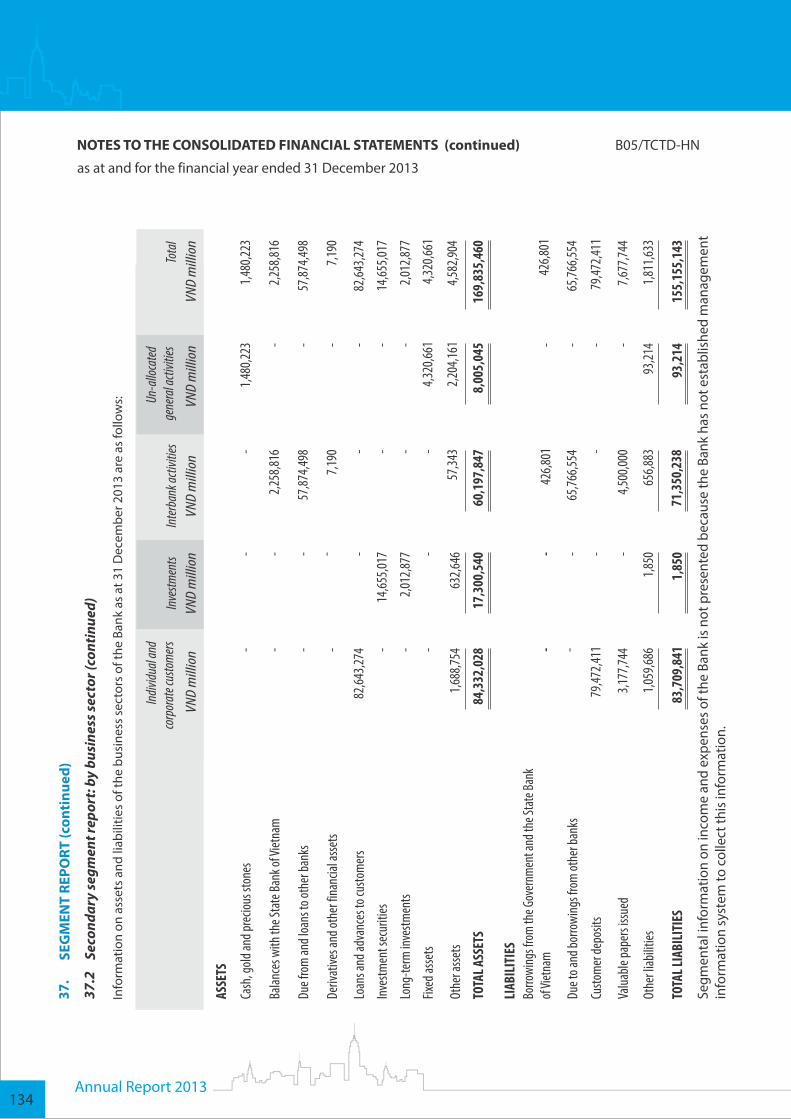

4

7

18

34

50

54

75

150

152

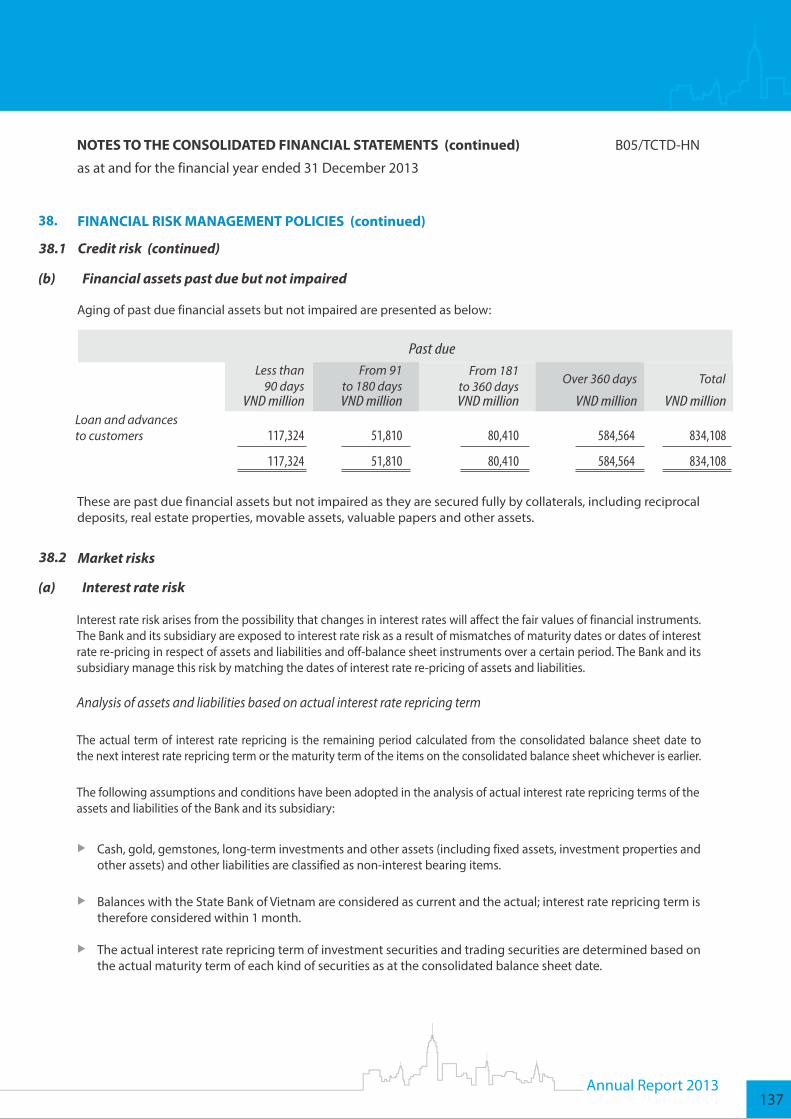

154

156

MESSAGE OF THE CHAIRMAN AND THE CHIEF EXECUTIVE OFFICER

MESSAGE OF THE CHAIRMAN AND THE CHIEF EXECUTIVE OFFICER

On behalf of the members of the Board of Directors, Board of Management and all of Eximbank's employees, we would like to extend our sincere thanks to valued Shareholders, Customers, domestic and international partners, especially the State Bank of Vietnam, for having always accompanied and assisted our Bank. We really look forward to receiving your continued support, companion, and heartfelt comments so as for Eximbank to further improve and develop solidly and robustly in the forthcoming time.

In the context of unfavourable business environment in 2013, Eximbank made lots of attempts to

execute its targets and attained the following results:

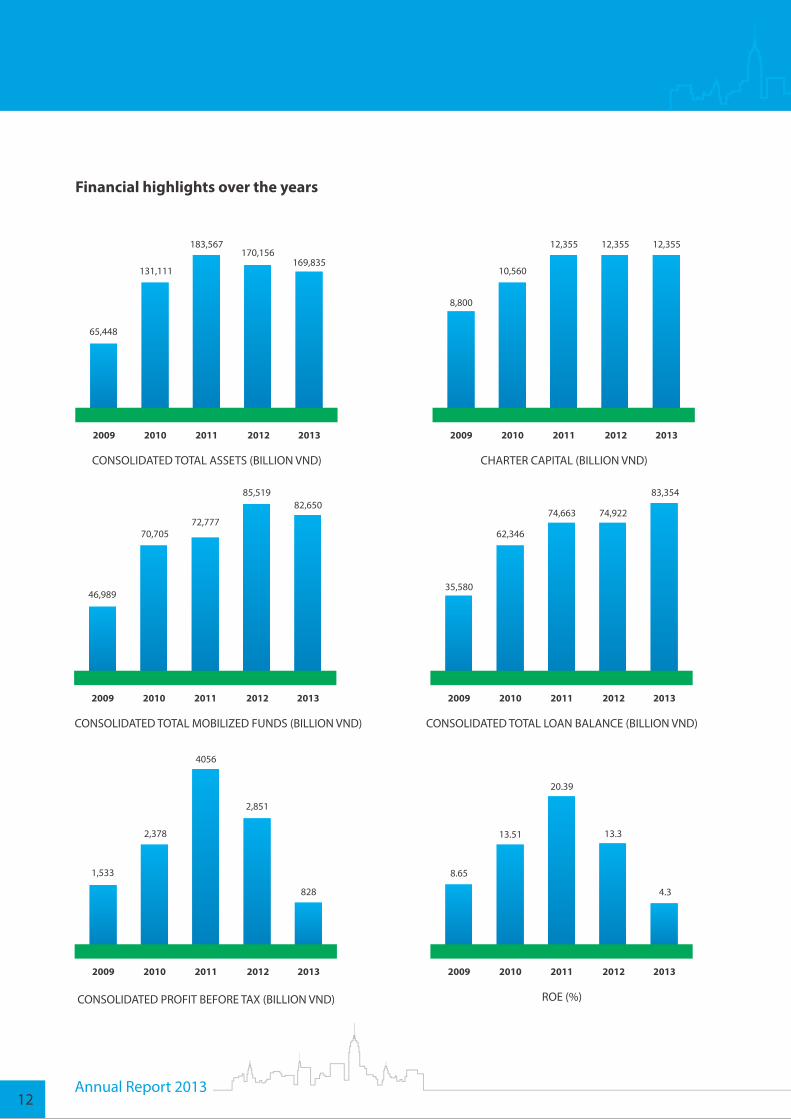

Total assets : VND169,835 billion, fulfilling 85% of the plan

Deposits : VND 82,650 billion, fulfilling 75% of the plan

Loans : VND 83,354 billion, fulfilling 97% of the plan

Profit before tax : VND 828 billion, fulfilling 26% of the plan

NPL ratio : 1.98%.

Although the business results of 2013 did not come up to the targeted plan, Eximbank still achieved certain results over the general performance of the whole banking industry. The Bank has taken initiative in transforming its business model in line with conditions of the economy with such solutions as restructuring the organization model from Head Office to branches, refining the operational apparatus, and gathering resources for the sales cadre; setting up new centralized business models namely as Assets Valuation Center, Card Sales Center, Retail Banking Center, Gold Trading Center; upgrading the operating quality of Transaction Offices to strengthen competitiveness; and promoting to settle loans and sell loans to VAMC, etc.

In the year, thanks to its endeavours in overcoming difficulties to achieve the objectives as set out in its banking operations, Eximbank was selected and presented by both domestic and foreign prestigious financial Magazines with such valuable awards as Top 1,000 World Banks by The Banker; Best Bank in Vietnam by EuroMoney; Best Managed Bank by The Asian Banker; Excellence in International Payment by The Bank of New York Mellon; and Top 50 Golden Products and Services by Vietnam Intellectual Property Association, etc.

Apart from business development, Eximbank has also made contributions to the society such as providing medical support to the poor in form of sponsoring health insurance cards, constructing medical service units and consolidating the healthcare network; donating educational aids to Scholarship Funds and Educational Promotion Associations, building schools; and sponsoring to build houses, bridges, showing gratitude to the families with meritorious services to the revolution.

Annual Report 20135

Turning to 2014, Eximbank's orientations are to continue perfecting the business model, strengthen financial capability, develop infrastructure – technology, enhance the quality of senior management and the staff, and focus on “customer servicing quality enhancement” through improving service quality, servicing attitude and customer care policy in order to carry out the proposed targets being:

Deposit reaches 100,000 billion VND (up 21% from 2013); Credit granting balance reaches 97,300 billion VND (up 10% from 2013); Profit before tax reaches 1,800 billion VND (up 117% from 2013); and NPL ratio does not exceed 3% (NPL ≤ 3%).

With the accomplishments in 2013, the Board of Directors, Board of Management together with all staff and officers in the whole network of Eximbank shall be determined to overcome the difficulties and challenges, successfully complete the planned targets set out for 2014, and effectively contribute to the general development of the whole banking industry and the economy.

On behalf of the members of the Board of Directors, Board of Management and all of Eximbank's employees, we would like to extend our sincere thanks to valued Shareholders, Customers, domestic and international partners, especially the State Bank of Vietnam, for having always accompanied and assisted our Bank. We really look forward to receiving your continued support, companion, and heartfelt comments so as for Eximbank to further improve and develop solidly and robustly in the forthcoming time.

FOR THE BOARD OF DIRECTORS CHIEF EXECUTIVE OFFICER CHAIRMAN

LE HUNG DUNG NGUYEN QUOC HUONG

6Annual Report 2013

MESSAGE OF THE CHAIRMAN AND THE CHIEF EXECUTIVE OFFICER (continued)

I. CORPORATE INFORMATION

I.General InformationRegistered Vietnamese name

Ngân hàng thương mại cổ phần Xuất nhập khẩu Việt Nam

Registered English name

Vietnam Export Import Commercial Joint Stock Bank (Vietnam Eximbank)

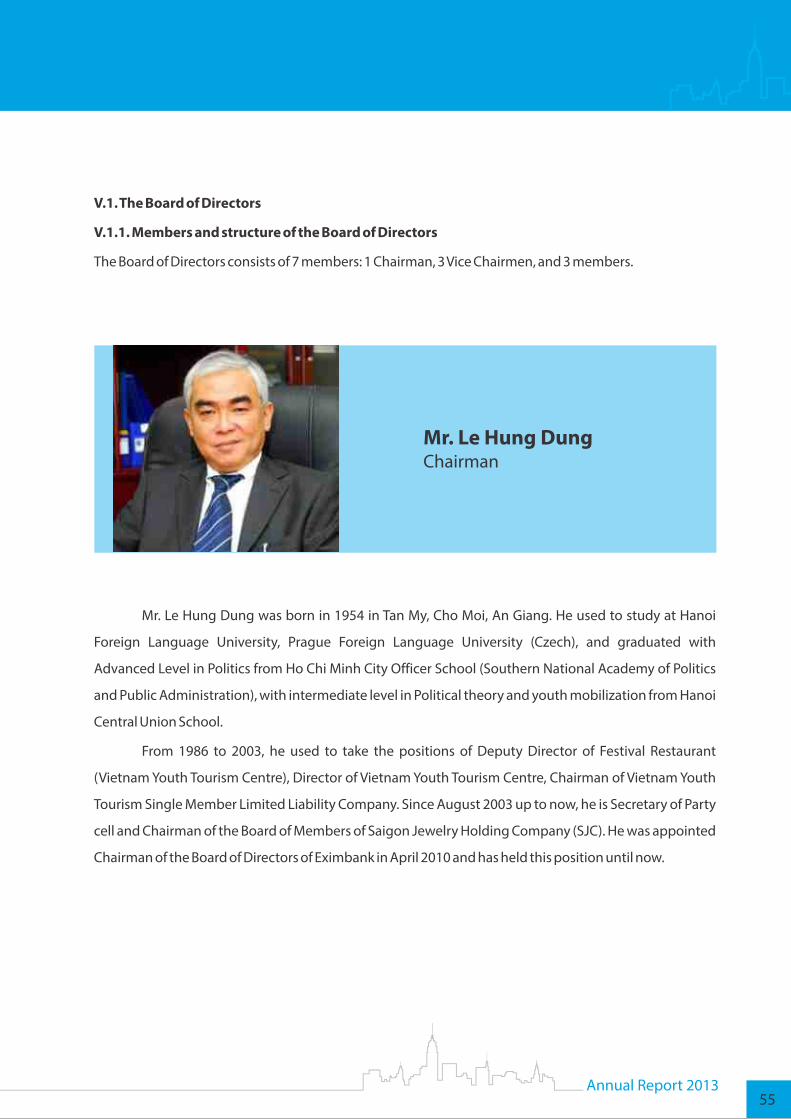

Chairman of the Board of Directors

Mr. Le Hung Dung

Chief Executive Officer

Mr. Nguyen Quoc Huong

Registered Head Office address

Level 8 – Suite No. L8-01-11 + 16, VINCOM CENTER,

72 Le Thanh Ton Street, Ben Nghe Ward, District 1, Ho Chi Minh City, Vietnam

Office address

Level 8 – Suite No. L8-01-11 + 16, VINCOM CENTER,

72 Le Thanh Ton Street, Ben Nghe Ward, District 1, Ho Chi Minh City, Vietnam

Tel: (84.8) 38.210.056 Fax: (84.8) 38.216.913

Website: http://www.eximbank.com.vn

Regulator

The State Bank of Vietnam

Auditor

ERNST & YOUNG Viet Nam Co., Ltd.thAddress: The 28 Floor, Bitexco Financial Tower, 2 Hai Trieu Street, District 1, Ho Chi Minh City,

Vietnam

Date of first registration

23/07/1992rdDate of registration for the 23 modification

23/12/2013

Authority of first registration

Department of Planning and Investment of Ho Chi Minh City

Business Operation Licenseth11/NH-GP dated 06 April 1992

Tax registration certificate number

0301179079

Stock information

Ho Chi Minh City Stock Exchange

Stock name

Vietnam Export Import Commercial Joint Stock Bank (Eximbank)

Stock code: EIB

8Annual Report 2013

I.2. History and development

I.2.1. History

Vietnam Export Import Commercial Joint Stock Bank is one of the first commercial joint stock

thbanks of Vietnam, being established on 24 May 1989 under Decision No.140/CT by the Chairman of the

Council of Ministers with the original name being Vietnam Export Import Bank.

thVietnam Export Import Bank officially came into operation on 17 January 1990 and received its

thLicense of Operation No.11/NH-GP dated 06 April 1992 by the Governor of the State Bank of Vietnam

allowing the Bank to operate for a term of 50 years with the registered charter capital of 50 billion VND

(equivalent to 12.5 million USD at the time of establishment) under the new name being Vietnam Export

Import Commercial Joint Stock Bank (or “Eximbank” in short).

I.2.2. Business lines

Eximbank's major business lines include: short, medium and long term fund mobilization in form

of savings deposits, payment deposits, certificates of deposit; receipt of funds entrusted for investment;

receipt of funds from domestic and foreign credit institutions; short, medium and long term lending;

discount of commercial papers, State bonds and valuable papers; foreign exchange trading; international

settlements; investment in securities and valuable papers; payment services and issuance of domestic

cards, international Visa, MasterCard, and Visa Debit cards; cash services; package financial services for

overseas study; financial advisory services; corporate bond trading; and other banking services, etc.

I.2.3. Business locations

Eximbank's Head Office is located at the Level 8 – Suite No. L8-01-11 + 16, Vincom Center, 72 Le

Thanh Ton Street, Ben Nghe Ward, District 1, Ho Chi Minh City, Vietnam. At the end of 2013, Eximbank's

network comprises of 206 banking units at cities and provinces nationwide, including: Main Transaction

Office, 41 Branches, 162 Transaction Offices, 01 Savings Fund, and 01 Transaction Point.

Currently, Eximbank's transaction network has covered 20 provinces and cities nationwide, including

Hanoi, Hai Phong, Nghe An, Quang Ninh, Quang Ngai, Quang Nam, Da Nang, Hue, Nha Trang, Lam Dong,

Dac Lac, Binh Duong, Dong Nai, Ba Ria – Vung Tau, Ho Chi Minh City, Long An, An Giang, Tien Giang, Can

Tho and Bac Lieu.

Annual Report 20139

I.2.4. Listing

Eximbank obtained the approval from Ho Chi Minh City Stock Exchange (HOSE) to list its shares

thfrom 20 October 2009 under Decision No.128/QD-SGDHCM.

Stock name: Stock of Vietnam Export Import Commercial Joint Stock Bank.

Stock type: Common

Par value: VND10,000 per share

Total listed volumes: 1,235,522,904 shares

Total listed value: 12,355,229,040,000 VND (as per par value)

I.2.5. Prominent events through years of operation

1991 & 1992: Entrusted by the State Bank of Vietnam and the Ministry of Finance to carry out part

of the Swedish non-refundable finance program extended to Vietnamese entities having demands for

importing goods from Sweden.

1993: Join the Electronic Clearing System of the State Bank.

1995: Join SWIFT (Society for Worldwide Interbank Financial Tele communication) network;

Selected as 1 among 6 Vietnamese banks to participate in the Bank Modernization Project

organized by the State Bank and funded by the World Bank.

1997: Become a principal member of MasterCard International.

1998: Become an official member of Visa International.

2003: Launch the online Intra-bank Payment System in the whole network.

2005: Be the first bank in Vietnam to issue international Visa Debit cards.

2007: Sign strategic partnership agreements with 17 domestic and foreign investors, especially

the strategic alliance agreement with Sumitomo Mitsui Banking Corporation (SMBC) of Japan.

2008: Increase the charter capital to 7,220 billion VND.

2009: Raise the charter capital to VND 8,800 billion VND and officially listed on Ho Chi Minh City

Stock Exchange.

2010: Increase the charter capital to 10,560 billion VND.

10Annual Report 2013

2011: Increase the charter capital to VND 12,355 billion;

Selected by The Banker magazine to appear in its Top 1,000 World Banks and Top 25 Banks by

Asset Growth in 2010.

2012: Presented “ Best Domestic Bank in Vietnam 2012” award by the AsiaMoney magazine;

Continue to be ranked in the Top 1,000 World Banks 2012 by The Banker magazine;

Officially launch the new set of brand identity.

2013: Awarded by The Asian Banker Magazine with “Best Managed Bank in Vietnam 2013”; by

EuroMoney Magazine with “Best Bank in Vietnam 2013”; and continue to be ranked in the Top 1,000 World

Banks 2013 by The Banker magazine.

Eximbank is one of the first banks issuing JCB-branded international card in Vietnam.

Annual Report 201311

46,989

70,70572,777

85,51982,650

2009 2010 2011 2012 2013

CONSOLIDATED TOTAL MOBILIZED FUNDS (BILLION VND)

35,580

62,346

74,663

2009 2010 2011 2012 2013

74,922

83,354

1,533

2,378

4056

2,851

828

2009 2010 2011 2012 2013

8.65

13.51

20.39

2009 2010 2011 2012 2013

ROE (%)

13.3

4.3

CONSOLIDATED TOTAL LOAN BALANCE (BILLION VND)

CONSOLIDATED PROFIT BEFORE TAX (BILLION VND)

12Annual Report 2013

Financial highlights over the years

65,448

131,111

183,567170,156

169,835

2009 2010 2011 2012 2013

CONSOLIDATED TOTAL ASSETS (BILLION VND)

8,800

10,560

12,355

2009 2010 2011 2012 2013

CHARTER CAPITAL (BILLION VND)

12,355 12,355

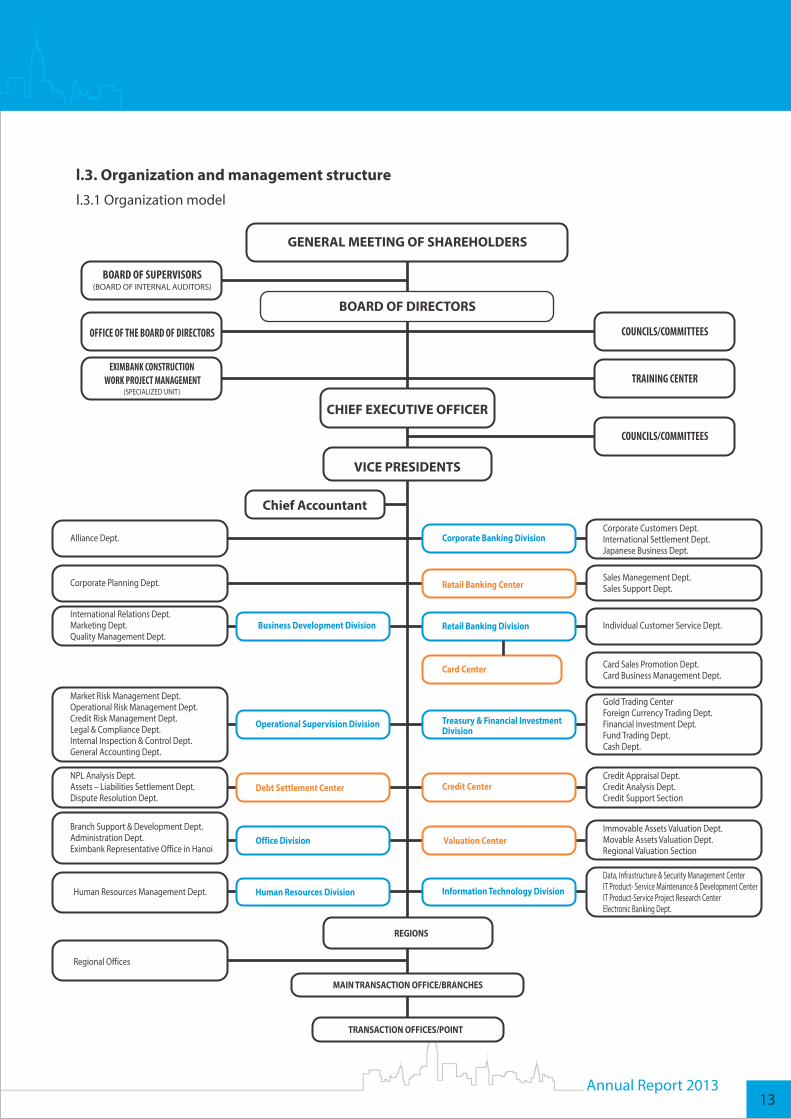

I.3. Organization and management structureI.3.1 Organization model

Annual Report 201313

BOARD OF SUPERVISORS(BOARD OF INTERNAL AUDITORS)

OFFICE OF THE BOARD OF DIRECTORS

EXIMBANK CONSTRUCTION WORK PROJECT MANAGEMENT

(SPECIALIZED UNIT)

BOARD OF DIRECTORS

COUNCILS/COMMITTEES

GENERAL MEETING OF SHAREHOLDERS

CHIEF EXECUTIVE OFFICER

VICE PRESIDENTS

Chief Accountant

TRAINING CENTER

COUNCILS/COMMITTEES

Alliance Dept.

Corporate Planning Dept.

International Relations Dept.Marketing Dept.Quality Management Dept.

Market Risk Management Dept.Operational Risk Management Dept.Credit Risk Management Dept.Legal & Compliance Dept.Internal Inspection & Control Dept.General Accounting Dept.

Business Development Division

Operational Supervision Division

NPL Analysis Dept.Assets – Liabilities Settlement Dept.Dispute Resolution Dept.

Branch Support & Development Dept.Administration Dept.Eximbank Representative Office in Hanoi

Human Resources Management Dept.

Regional Offices

Debt Settlement Center

Office Division

Human Resources Division

REGIONS

MAIN TRANSACTION OFFICE/BRANCHES

TRANSACTION OFFICES/POINT

Corporate Banking Division

Retail Banking Center

Retail Banking Division

Card Center

Treasury & Financial Investment Division

Credit Center

Valuation Center

Information Technology Division

Corporate Customers Dept.International Settlement Dept.Japanese Business Dept.

Sales Manegement Dept.Sales Support Dept.

Individual Customer Service Dept.

Card Sales Promotion Dept.Card Business Management Dept.

Gold Trading CenterForeign Currency Trading Dept.Financial Investment Dept.Fund Trading Dept.Cash Dept.

Credit Appraisal Dept.Credit Analysis Dept.Credit Support Section

Immovable Assets Valuation Dept.Movable Assets Valuation Dept.Regional Valuation Section

Data, Infrastructure & Security Management CenterIT Product- Service Maintenance & Development CenterIT Product-Service Project Research CenterElectronic Banking Dept.

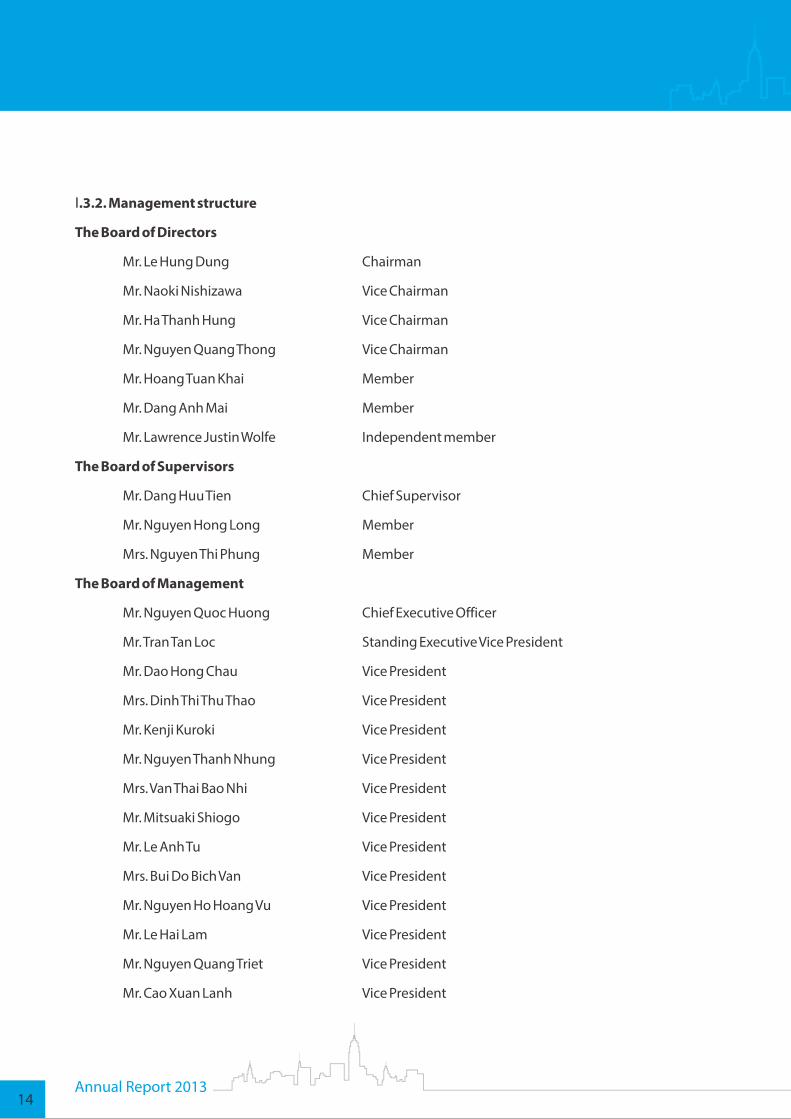

I.3.2. Management structure

The Board of Directors

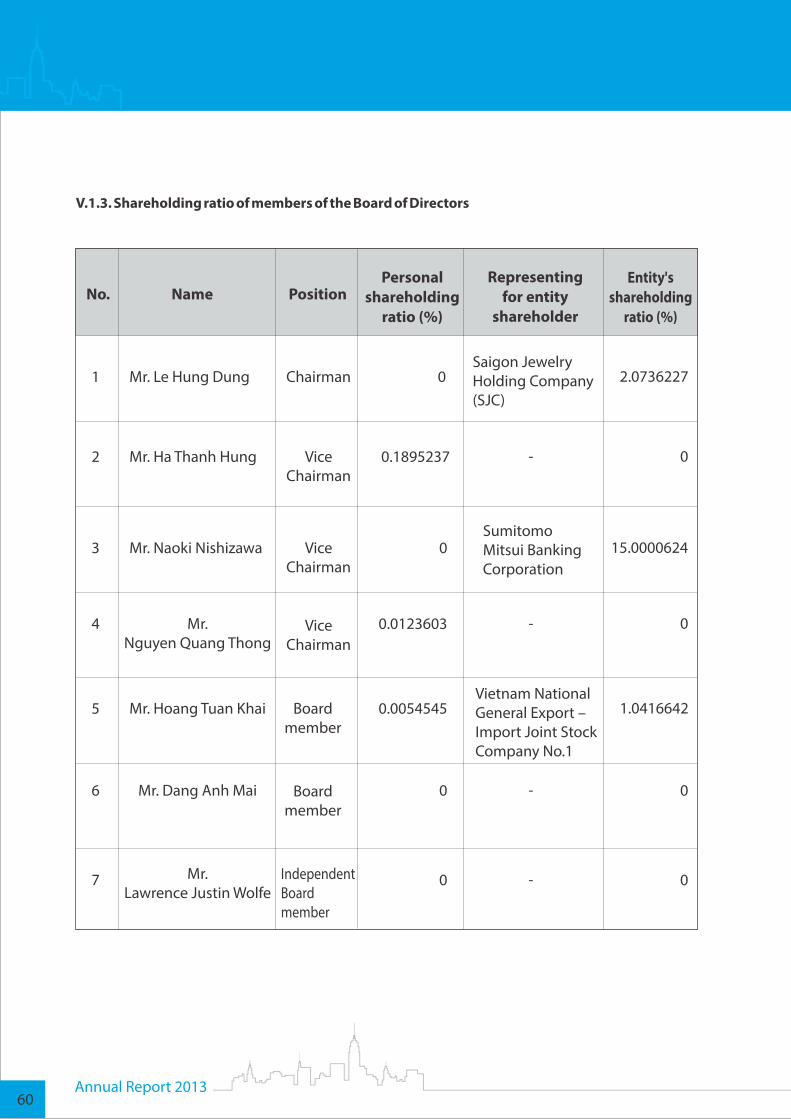

Mr. Le Hung Dung Chairman

Mr. Naoki Nishizawa Vice Chairman

Mr. Ha Thanh Hung Vice Chairman

Mr. Nguyen Quang Thong Vice Chairman

Mr. Hoang Tuan Khai Member

Mr. Dang Anh Mai Member

Mr. Lawrence Justin Wolfe Independent member

The Board of Supervisors

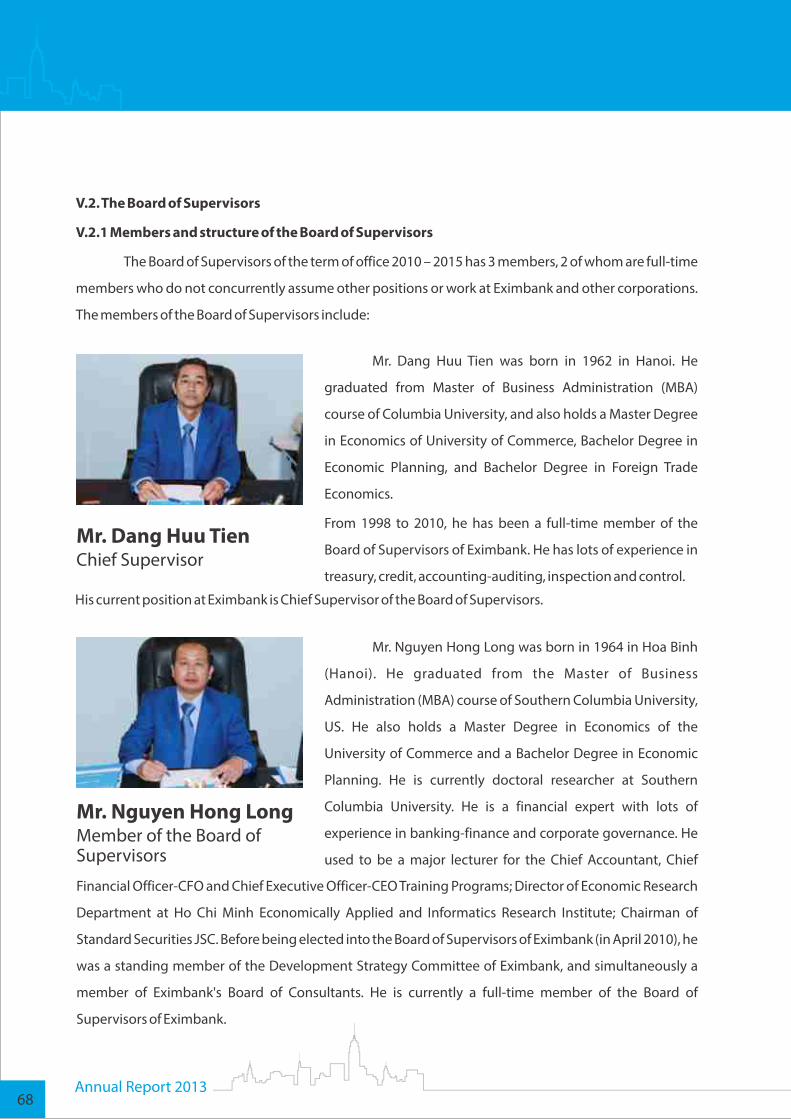

Mr. Dang Huu Tien Chief Supervisor

Mr. Nguyen Hong Long Member

Mrs. Nguyen Thi Phung Member

The Board of Management

Mr. Nguyen Quoc Huong Chief Executive Officer

Mr. Tran Tan Loc Standing Executive Vice President

Mr. Dao Hong Chau Vice President

Mrs. Dinh Thi Thu Thao Vice President

Mr. Kenji Kuroki Vice President

Mr. Nguyen Thanh Nhung Vice President

Mrs. Van Thai Bao Nhi Vice President

Mr. Mitsuaki Shiogo Vice President

Mr. Le Anh Tu Vice President

Mrs. Bui Do Bich Van Vice President

Mr. Nguyen Ho Hoang Vu Vice President

Mr. Le Hai Lam Vice President

Mr. Nguyen Quang Triet Vice President

Mr. Cao Xuan Lanh Vice President

14Annual Report 2013

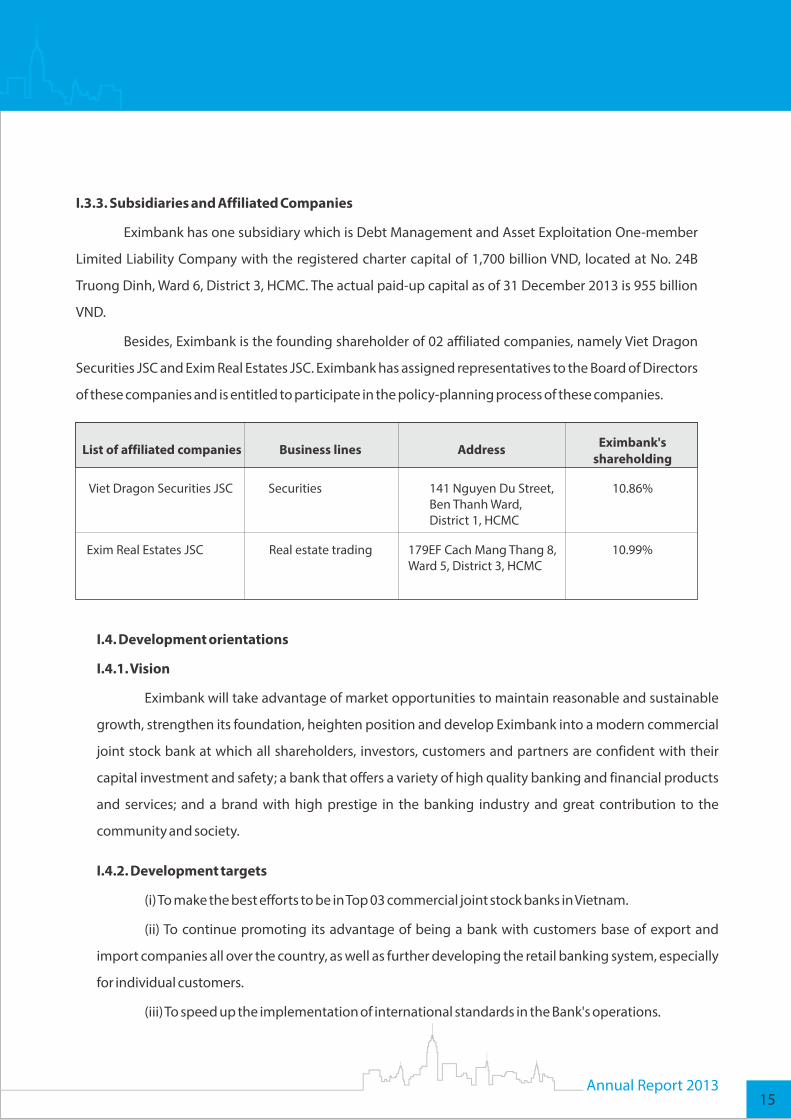

I.3.3. Subsidiaries and Affiliated Companies

Eximbank has one subsidiary which is Debt Management and Asset Exploitation One-member

Limited Liability Company with the registered charter capital of 1,700 billion VND, located at No. 24B

Truong Dinh, Ward 6, District 3, HCMC. The actual paid-up capital as of 31 December 2013 is 955 billion

VND.

Besides, Eximbank is the founding shareholder of 02 affiliated companies, namely Viet Dragon

Securities JSC and Exim Real Estates JSC. Eximbank has assigned representatives to the Board of Directors

of these companies and is entitled to participate in the policy-planning process of these companies.

List of affiliated companies Business lines Address Eximbank'sshareholding

Viet Dragon Securities JSC Securities 141 Nguyen Du Street, Ben Thanh Ward, District 1, HCMC

10.86%

Exim Real Estates JSC Real estate trading 179EF Cach Mang Thang 8, Ward 5, District 3, HCMC

10.99%

I.4. Development orientations

I.4.1. Vision

Eximbank will take advantage of market opportunities to maintain reasonable and sustainable

growth, strengthen its foundation, heighten position and develop Eximbank into a modern commercial

joint stock bank at which all shareholders, investors, customers and partners are confident with their

capital investment and safety; a bank that offers a variety of high quality banking and financial products

and services; and a brand with high prestige in the banking industry and great contribution to the

community and society.

I.4.2. Development targets

(i) To make the best efforts to be in Top 03 commercial joint stock banks in Vietnam.

(ii) To continue promoting its advantage of being a bank with customers base of export and

import companies all over the country, as well as further developing the retail banking system, especially

for individual customers.

(iii) To speed up the implementation of international standards in the Bank's operations.

Annual Report 201315

I.4.3.Development orientatons up to 2015 and vision up to 2020

Eximbank has developed business development plans up to 2015 and vision up to 2020, focusing

on the following areas:

- Maintaining reasonable credit growth, in accordance with the State Bank's orientations from

time to time.

- Promoting the fund mobilization from individual customers as well as economic entities to

increase Eximbank's market shares; changing the fund mobilization structure, thereby increasing more

deposits from corporate customers and funds with longer terms, etc.

- Enhancing risk management, applying international standards into the Bank's operations to

ensure safe and sustainable development.

- Continuing with brand promotion programs to bring Eximbank brand as the top bank brand in

Vietnam.

- Investing in infrastructure construction and network development to serve for banking

activities, strengthening the presence of Eximbank in Ho Chi Minh City, Hanoi and other cities and

provinces with great economic potentialities, at commercial centers, industrial zones and export

processing zones, etc.

- Further concentrating on preserving and improving environmental quality, protecting human

rights, and complying with regulations on labor, employment and other social policies during the course

of operation of Eximbank.

I.5. Risks

The Bank is aware of and takes control over risks that are likely to affect its business activities or

the execution of its general objectives, including:

a) Credit risk is the loss that is likely to happen with respect to the Bank's loans due to customers'

failure or inability to perform part or whole of their obligations as committed;

b) Market risk is the risk arising out of market fluctuations causing adverse impacts on the Bank's

income and (or) capital, including:

(i) Interest rate risk is the risk resulted from adverse volatilities of interest rates causing negative

impacts on the Bank's income and (or) capital. Interest rate risk may arise from:

- Difference in the times of interest rate fixation (revaluation risk);

16Annual Report 2013

- Changes of the relationship among different market interest rates;

- Changes of the interest rate relationship among different tenors (yield curve risk);

- Interest-linked option products.

(ii) Exchange rate risk is the risk resulted from exchange rate volatilities causing negative impacts

on the Bank's income and (or) capital.

(iii) Investment value risk is the risk resulted from price fluctuations of stocks, bonds and other

capital and securities investments, leading to the diminution of investments held by the Bank.

c) Liquidity risk is the risk arising when the Bank is unable to meet all of its capital obligations

which fall due; or suffers great losses to perform such obligations.

d) Operational risk is the risk of causing losses to the Bank by reasons of insufficient or erroneous

internal procedures, human mistakes, faulty or inappropriate internal systems, or impacts of external

incidents.

Annual Report 201317

II. BUSINESS PERFORMANCE IN 2013

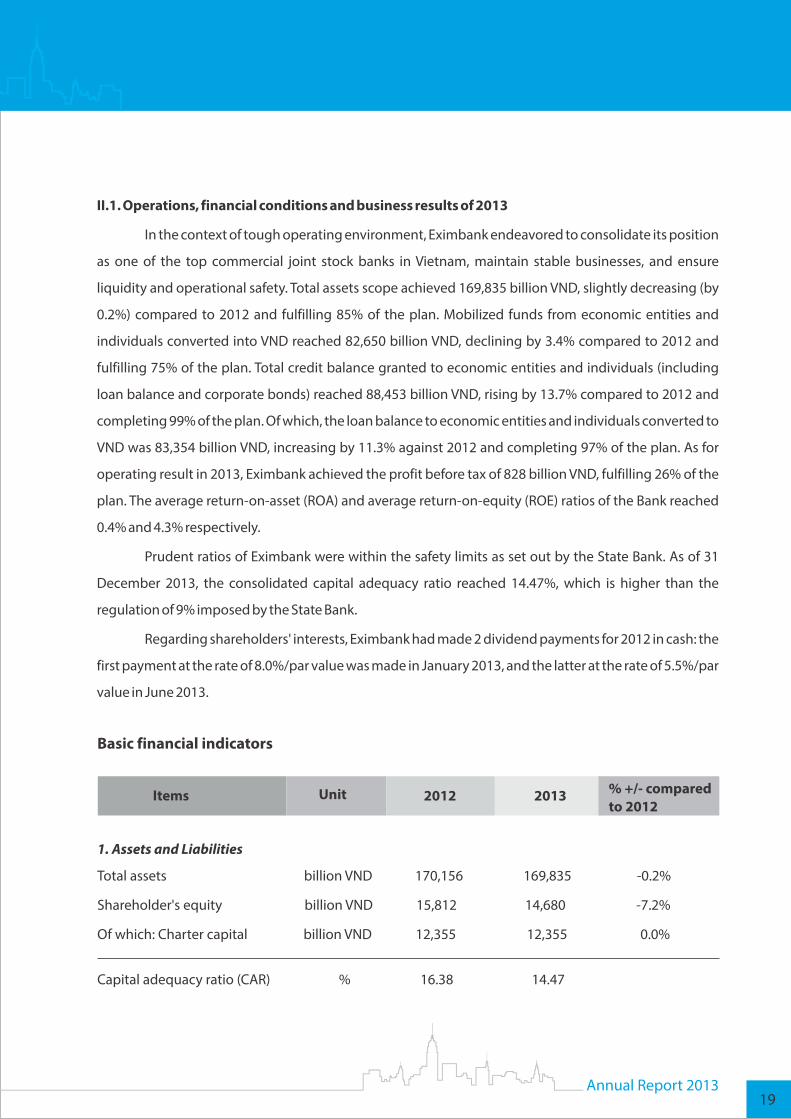

II.1. Operations, financial conditions and business results of 2013

In the context of tough operating environment, Eximbank endeavored to consolidate its position

as one of the top commercial joint stock banks in Vietnam, maintain stable businesses, and ensure

liquidity and operational safety. Total assets scope achieved 169,835 billion VND, slightly decreasing (by

0.2%) compared to 2012 and fulfilling 85% of the plan. Mobilized funds from economic entities and

individuals converted into VND reached 82,650 billion VND, declining by 3.4% compared to 2012 and

fulfilling 75% of the plan. Total credit balance granted to economic entities and individuals (including

loan balance and corporate bonds) reached 88,453 billion VND, rising by 13.7% compared to 2012 and

completing 99% of the plan. Of which, the loan balance to economic entities and individuals converted to

VND was 83,354 billion VND, increasing by 11.3% against 2012 and completing 97% of the plan. As for

operating result in 2013, Eximbank achieved the profit before tax of 828 billion VND, fulfilling 26% of the

plan. The average return-on-asset (ROA) and average return-on-equity (ROE) ratios of the Bank reached

0.4% and 4.3% respectively.

Prudent ratios of Eximbank were within the safety limits as set out by the State Bank. As of 31

December 2013, the consolidated capital adequacy ratio reached 14.47%, which is higher than the

regulation of 9% imposed by the State Bank.

Regarding shareholders' interests, Eximbank had made 2 dividend payments for 2012 in cash: the

first payment at the rate of 8.0%/par value was made in January 2013, and the latter at the rate of 5.5%/par

value in June 2013.

Basic financial indicators

Items Unit 2012 2013 % +/- compared to 2012

1. Assets and Liabilities

Total assets billion VND 170,156 169,835 -0.2%

Shareholder's equity billion VND 15,812 14,680 -7.2%

Of which: Charter capital billion VND 12,355 12,355 0.0%

Capital adequacy ratio (CAR) % 16.38 14.47

Annual Report 201319

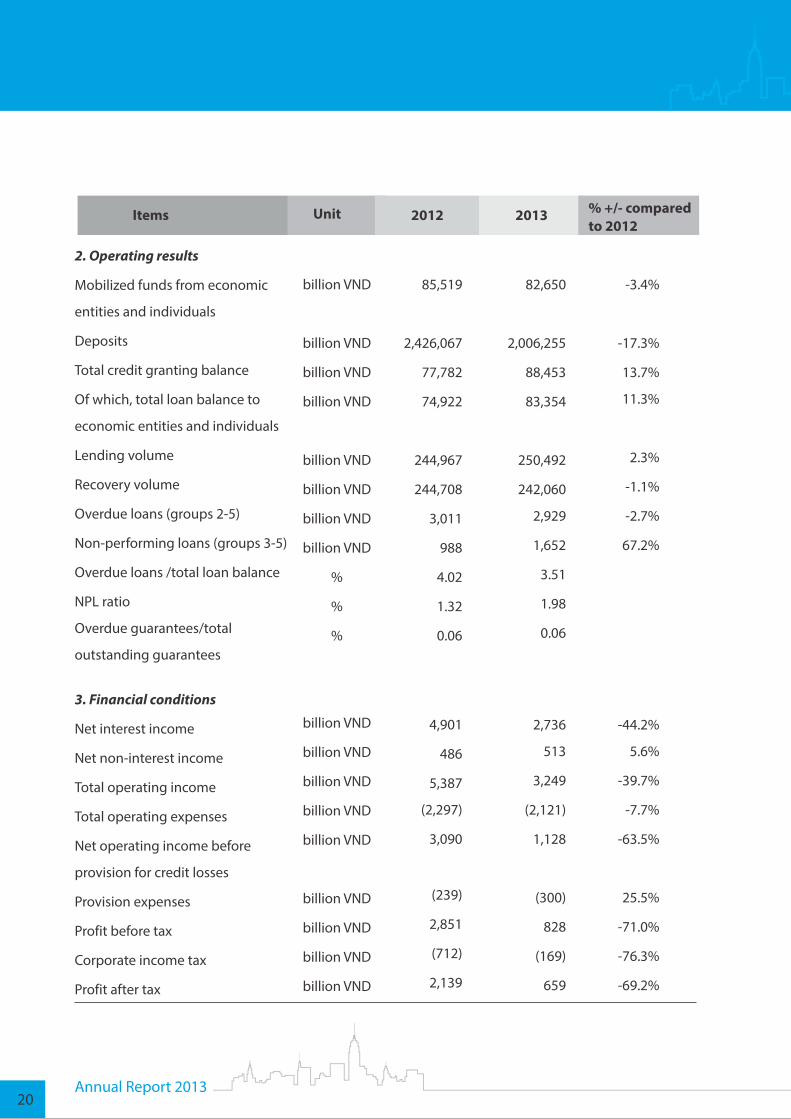

2. Operating results

Mobilized funds from economic

entities and individuals

Deposits

Total credit granting balance

Of which, total loan balance to

economic entities and individuals

Lending volume

Recovery volume

Overdue loans (groups 2-5)

Non-performing loans (groups 3-5)

Overdue loans /total loan balance

NPL ratio

Overdue guarantees/total

outstanding guarantees

billion VND

billion VND

billion VND

billion VND

billion VND

billion VND

billion VND

billion VND

%

%

%

85,519

2,426,067

77,782

74,922

244,967

244,708

3,011

988

4.02

1.32

0.06

82,650

2,006,255

88,453

83,354

250,492

242,060

2,929

1,652

3.51

1.98

0.06

-3.4%

-17.3%

13.7%

11.3%

2.3%

-1.1%

-2.7%

67.2%

3. Financial conditions

Net interest income

Net non-interest income

Total operating income

Total operating expenses

Net operating income before

provision for credit losses

Provision expenses

Profit before tax

Corporate income tax

Profit after tax

billion VND

billion VND

billion VND

billion VND

billion VND

billion VND

billion VND

billion VND

billion VND

4,901

486

5,387

(2,297)

3,090

(239)

2,851

(712)

2,139

2,736

513

3,249

(2,121)

1,128

(300)

828

(169)

659

-44.2%

5.6%

-39.7%

-7.7%

-63.5%

25.5%

-71.0%

-76.3%

-69.2%

Items Unit 2012 2013 % +/- compared to 2012

20Annual Report 2013

Items Unit 2012 2013 % +/- compared to 2012

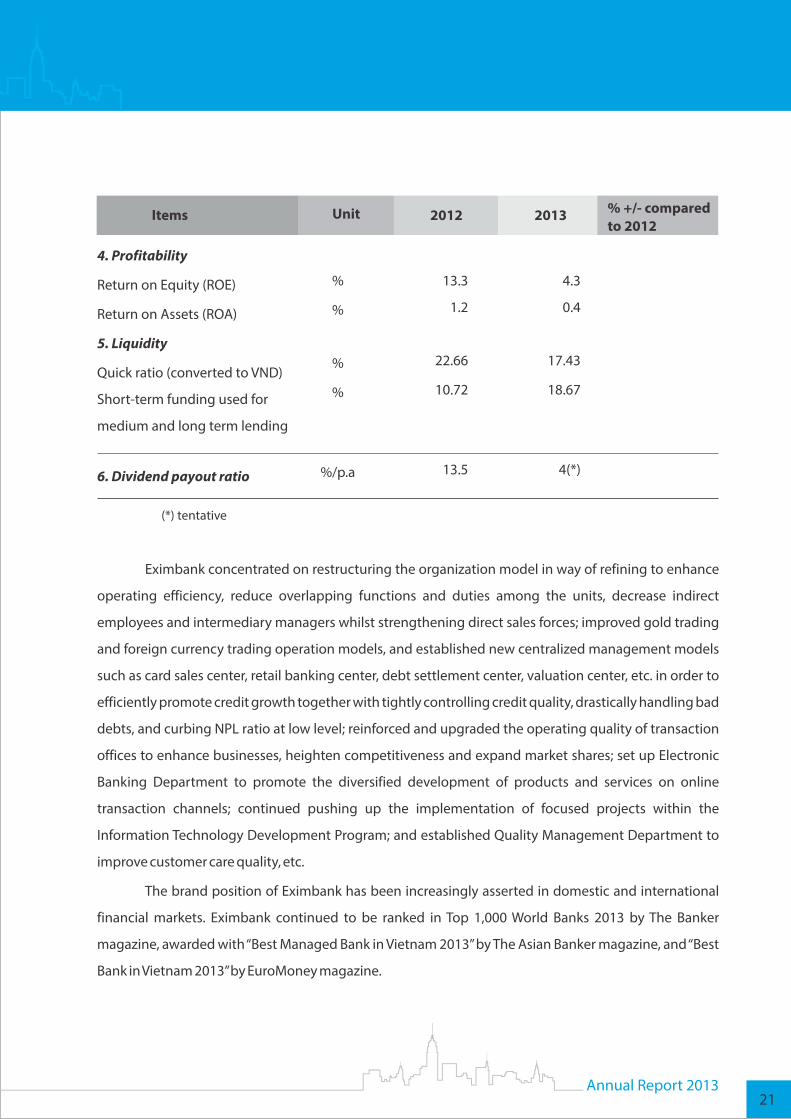

4. Profitability

Return on Equity (ROE)

Return on Assets (ROA)

5. Liquidity

Quick ratio (converted to VND)

Short-term funding used for

medium and long term lending

6. Dividend payout ratio

%

%

%

%

%/p.a

13.3

1.2

22.66

10.72

13.5

4.3

0.4

17.43

18.67

4(*)

(*) tentative

Eximbank concentrated on restructuring the organization model in way of refining to enhance

operating efficiency, reduce overlapping functions and duties among the units, decrease indirect

employees and intermediary managers whilst strengthening direct sales forces; improved gold trading

and foreign currency trading operation models, and established new centralized management models

such as card sales center, retail banking center, debt settlement center, valuation center, etc. in order to

efficiently promote credit growth together with tightly controlling credit quality, drastically handling bad

debts, and curbing NPL ratio at low level; reinforced and upgraded the operating quality of transaction

offices to enhance businesses, heighten competitiveness and expand market shares; set up Electronic

Banking Department to promote the diversified development of products and services on online

transaction channels; continued pushing up the implementation of focused projects within the

Information Technology Development Program; and established Quality Management Department to

improve customer care quality, etc.

The brand position of Eximbank has been increasingly asserted in domestic and international

financial markets. Eximbank continued to be ranked in Top 1,000 World Banks 2013 by The Banker

magazine, awarded with “Best Managed Bank in Vietnam 2013” by The Asian Banker magazine, and “Best

Bank in Vietnam 2013” by EuroMoney magazine.

Annual Report 201321

Appointed as Acting Chief Executive Officer in September 2013 and officially appointed as Chief

Executive Officer in December 2013. He is currently the Chief Executive Officer of Vietnam Export Import

Commercial Joint Stock Bank.

Holding a Master degree of Economics, he has been working for the Bank since 1993 and making

great contributions to its development during the last 21 years. He used to hold such positions as Deputy

Director and then Director of Credit Department, Director of Corporate Credit Department, Director of

Credit Management Department, and Vice President cum Director of Main Transaction Office No. 1.

Appointed in March 2007, and currently being the Standing Executive Vice President of Vietnam

Export Import Commercial Joint Stock Bank.

Holding a Ph.D. of Economics in Finance – Credit, he started working for Vietnam Export Import

Commercial Joint Stock Bank since 1994 and has made extensive contributions to the Bank's

development throughout his 20 years of service. He used to hold various positions, namely Deputy

Director of Transaction Accounting Department, Deputy Director and then Director of Credit Card

Department, Assistant to the Chief Executive Officer cum Deputy Chief of the Development Project

Section, Secretary of the Board of Directors cum Deputy Chief of the Office of the Board of Directors of

Eximbank.

Mr. Nguyen Quoc HuongChief Executive Officer

Mr. Tran Tan LocStanding Executive Vice President

II.2.1 Introduction of the Board of Management

II.2.ORGANIZATION AND PERSONNEL

22Annual Report 2013

Appointed in April 2004, holding a Master degree of Economics, and currently being the Vice

President of Vietnam Export Import Commercial Joint Stock Bank.

He has been working for the Bank since 1992 and, throughout such 22 years, made lots of

contributions to the development of the Bank. He used to be Deputy Director and then Director of

Treasury Department.

Appointed in December 2007, holding a Master degree of Economics, and currently being the

Vice President of Vietnam Export Import Commercial Joint Stock Bank.

She has served the Bank for the past 23 years and used to hold such positions as Deputy Director

and then Director of Transaction Accounting Department, Director of Corporate Customer Services

Department, Deputy Director of Main Transaction Office No.1, and Head of Retail Banking Division.

Mr. Dao Hong ChauVice President

Mrs. Dinh Thi Thu ThaoVice President

Annual Report 201323

Appointed in July 2008, and currently being the Vice President of Vietnam Export Import

Commercial Joint Stock Bank cum Co-Director of Alliance Department.

He has been serving Sumitomo Mitsui Banking Corporation since 1989 and used to be the Senior

Vice President of the Representative Office of Sumitomo Mitsui Banking Corporation in Ho Chi Minh City

from 2005 to 2006.

Appointed in November 2010, holding a Master degree of Economics, and currently being the

Vice President of Vietnam Export Import Commercial Joint Stock Bank.

During his 19 years of service for the Bank since 1995, he has made lots of contributions to the

development of the Bank. He used to hold such positions as Deputy Director of Asset Management and

Exploitation Department, Deputy Director of Planning and Treasury Department, Deputy Director of Nha

Trang Branch, Deputy Director of Corporate Credit Department, Deputy Director and then Director of

Credit Management Department and Head of Operational Supervision Division.

Mr. Kenji KurokiVice President

Mr. Nguyen Thanh NhungVice President

24Annual Report 2013

Appointed in May 2012, holding a Master degree of Economics, and currently being the Vice

President of Vietnam Export Import Commercial Joint Stock Bank.

Throughout her 20 years of service, she has greatly contributed to the Bank's development. She

used to hold such positions as Deputy Director of Credit Department, Director of Corporate Credit

Department, and Head of Corporate Banking Division.

Appointed in June 2012, holding a Bachelor degree of Economics, and currently being the Vice

President of Vietnam Export Import Commercial Joint Stock Bank.

He has been serving Sumitomo Mitsui Banking Corporation since 1986. He used to hold such

positions as Vice President of JRI America Company, and Senior Vice President of SMBC America

Information System Division from May 2005 to February 2012.

Mrs. Van Thai Bao NhiVice President

Mr. Mitsuaki ShiogoVice President

Annual Report 201325

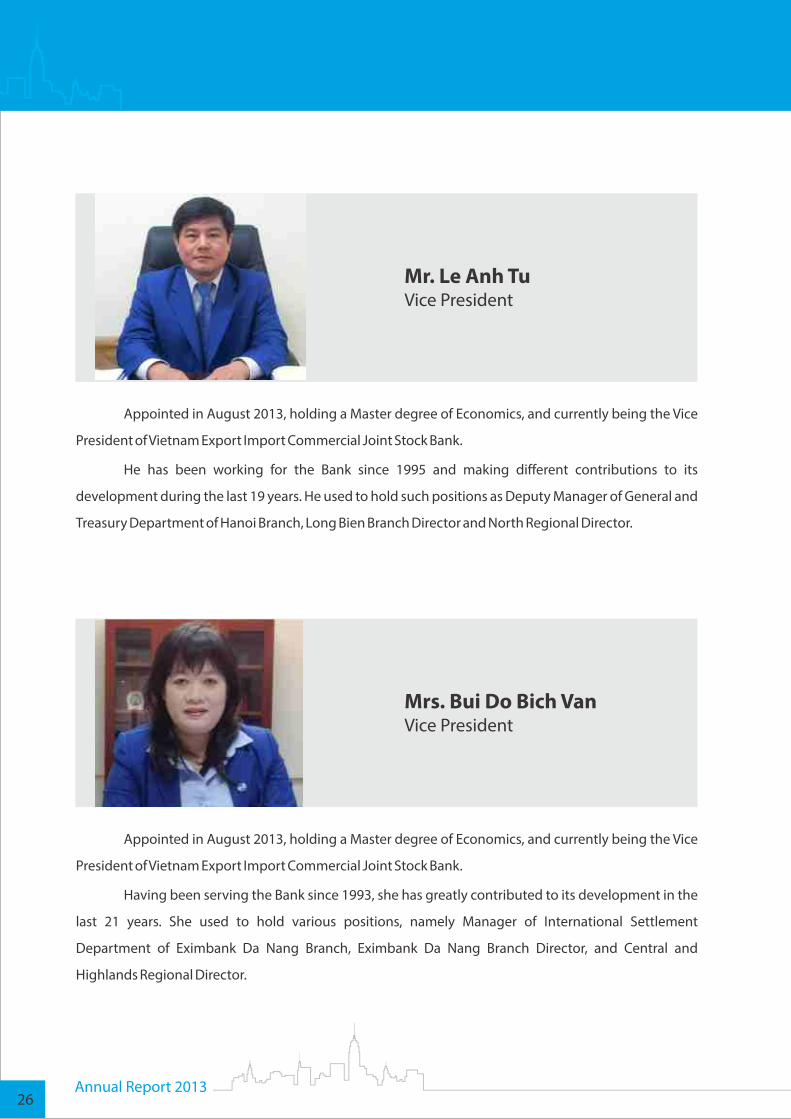

Appointed in August 2013, holding a Master degree of Economics, and currently being the Vice

President of Vietnam Export Import Commercial Joint Stock Bank.

He has been working for the Bank since 1995 and making different contributions to its

development during the last 19 years. He used to hold such positions as Deputy Manager of General and

Treasury Department of Hanoi Branch, Long Bien Branch Director and North Regional Director.

Appointed in August 2013, holding a Master degree of Economics, and currently being the Vice

President of Vietnam Export Import Commercial Joint Stock Bank.

Having been serving the Bank since 1993, she has greatly contributed to its development in the

last 21 years. She used to hold various positions, namely Manager of International Settlement

Department of Eximbank Da Nang Branch, Eximbank Da Nang Branch Director, and Central and

Highlands Regional Director.

Mr. Le Anh Tu Vice President

Mrs. Bui Do Bich VanVice President

26Annual Report 2013

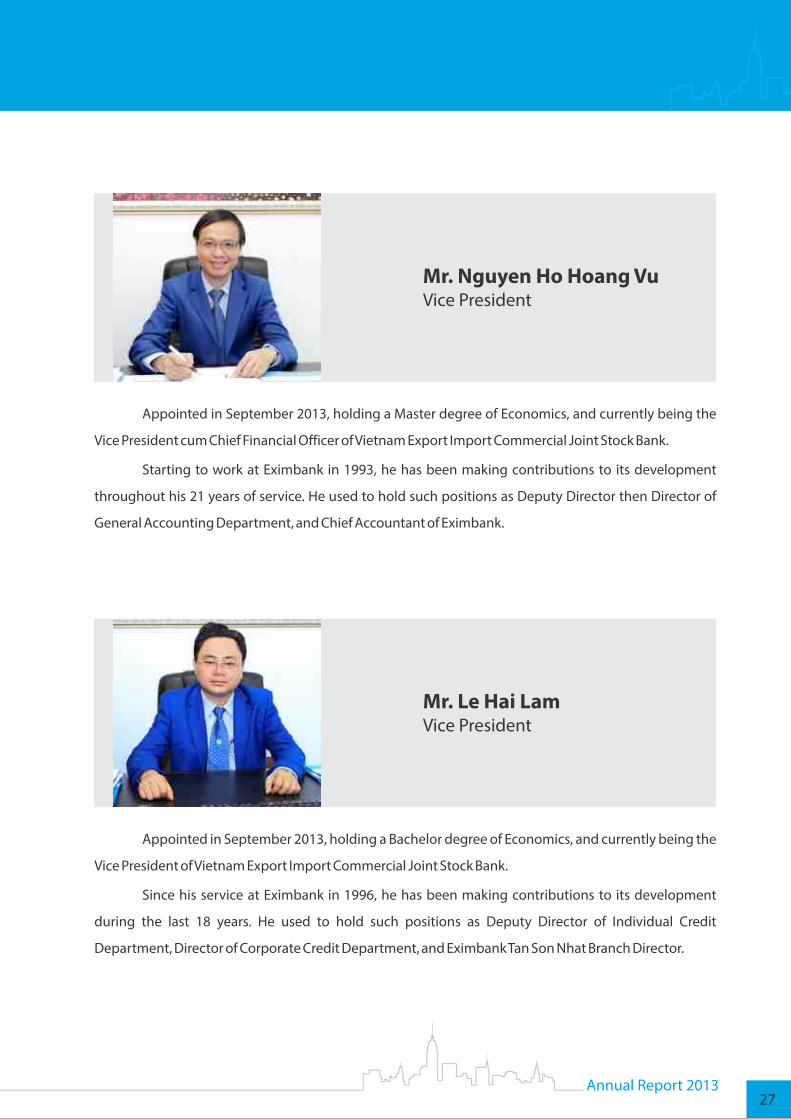

Appointed in September 2013, holding a Master degree of Economics, and currently being the

Vice President cum Chief Financial Officer of Vietnam Export Import Commercial Joint Stock Bank.

Starting to work at Eximbank in 1993, he has been making contributions to its development

throughout his 21 years of service. He used to hold such positions as Deputy Director then Director of

General Accounting Department, and Chief Accountant of Eximbank.

Appointed in September 2013, holding a Bachelor degree of Economics, and currently being the

Vice President of Vietnam Export Import Commercial Joint Stock Bank.

Since his service at Eximbank in 1996, he has been making contributions to its development

during the last 18 years. He used to hold such positions as Deputy Director of Individual Credit

Department, Director of Corporate Credit Department, and Eximbank Tan Son Nhat Branch Director.

Mr. Nguyen Ho Hoang VuVice President

Mr. Le Hai LamVice President

Annual Report 201327

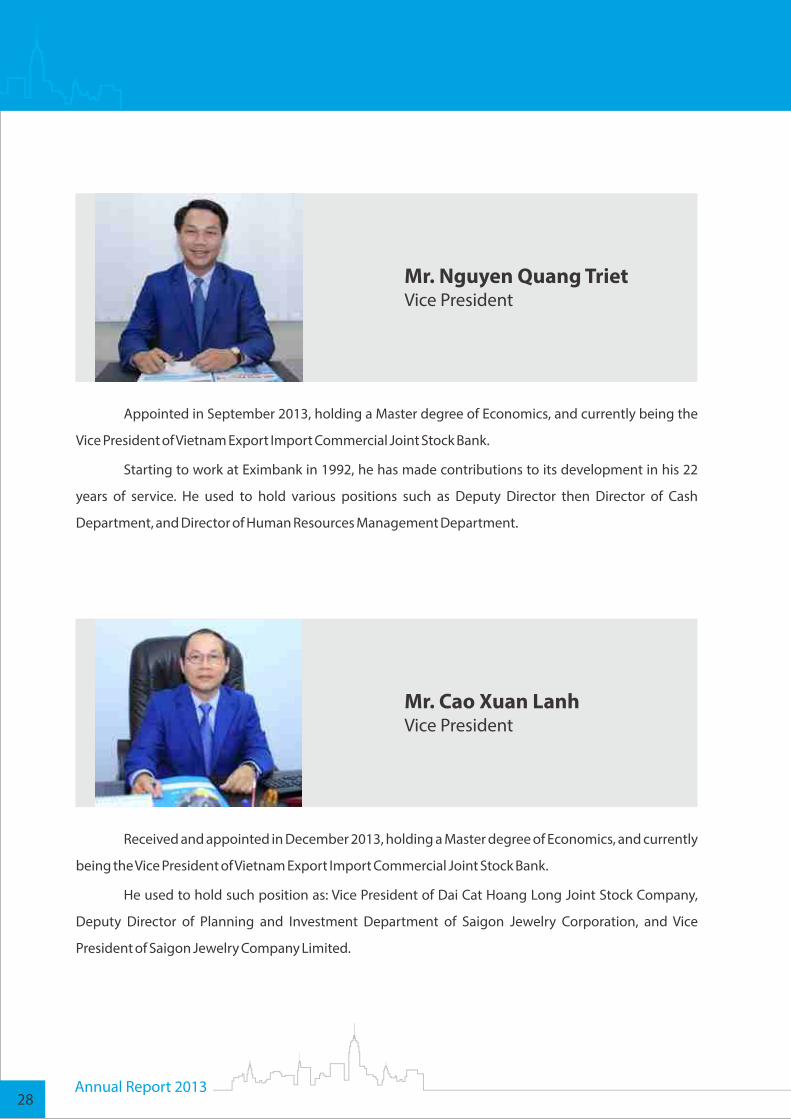

Appointed in September 2013, holding a Master degree of Economics, and currently being the

Vice President of Vietnam Export Import Commercial Joint Stock Bank.

Starting to work at Eximbank in 1992, he has made contributions to its development in his 22

years of service. He used to hold various positions such as Deputy Director then Director of Cash

Department, and Director of Human Resources Management Department.

Received and appointed in December 2013, holding a Master degree of Economics, and currently

being the Vice President of Vietnam Export Import Commercial Joint Stock Bank.

He used to hold such position as: Vice President of Dai Cat Hoang Long Joint Stock Company,

Deputy Director of Planning and Investment Department of Saigon Jewelry Corporation, and Vice

President of Saigon Jewelry Company Limited.

Mr. Nguyen Quang TrietVice President

Mr. Cao Xuan LanhVice President

28Annual Report 2013

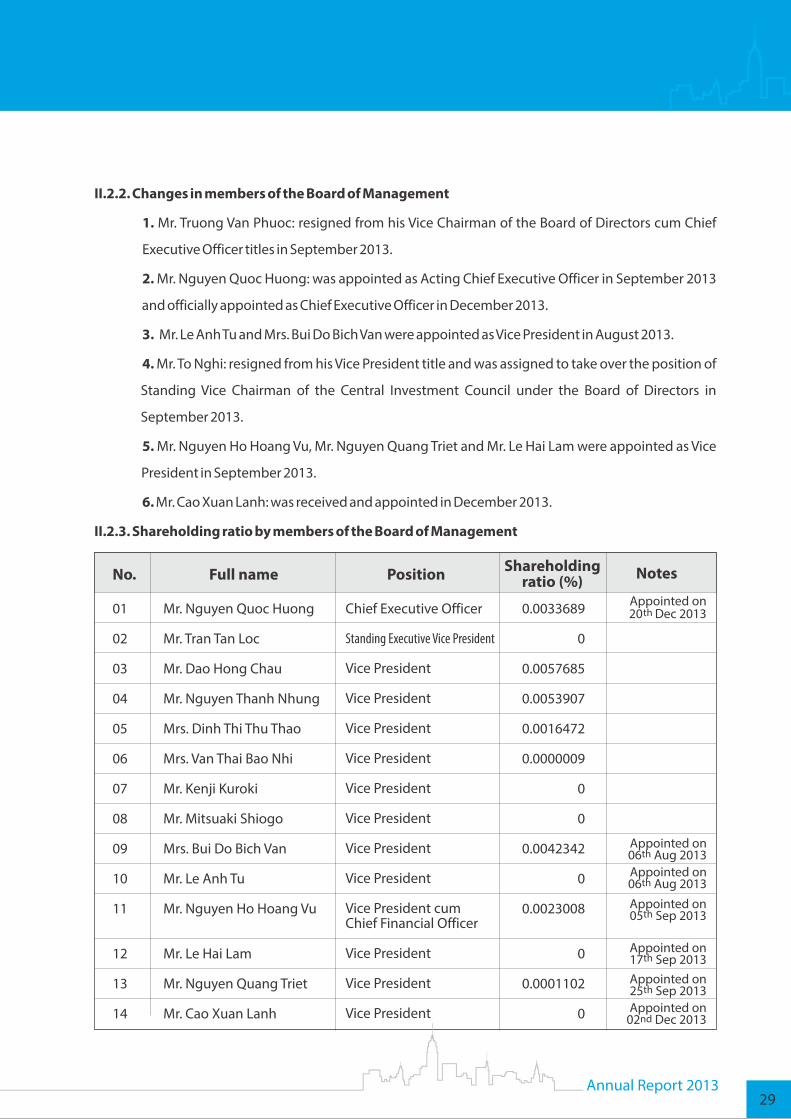

II.2.2. Changes in members of the Board of Management

1. Mr. Truong Van Phuoc: resigned from his Vice Chairman of the Board of Directors cum Chief

Executive Officer titles in September 2013.

2. Mr. Nguyen Quoc Huong: was appointed as Acting Chief Executive Officer in September 2013

and officially appointed as Chief Executive Officer in December 2013.

3. Mr. Le Anh Tu and Mrs. Bui Do Bich Van were appointed as Vice President in August 2013.

4. Mr. To Nghi: resigned from his Vice President title and was assigned to take over the position of

Standing Vice Chairman of the Central Investment Council under the Board of Directors in

September 2013.

5. Mr. Nguyen Ho Hoang Vu, Mr. Nguyen Quang Triet and Mr. Le Hai Lam were appointed as Vice

President in September 2013.

6. Mr. Cao Xuan Lanh: was received and appointed in December 2013.

II.2.3. Shareholding ratio by members of the Board of Management

No. Full name Position Shareholding ratio (%)

01

02

03

04

05

06

07

08

09

10

11

12

13

14

Mr. Nguyen Quoc Huong

Mr. Tran Tan Loc

Mr. Dao Hong Chau

Mr. Nguyen Thanh Nhung

Mrs. Dinh Thi Thu Thao

Mrs. Van Thai Bao Nhi

Mr. Kenji Kuroki

Mr. Mitsuaki Shiogo

Mrs. Bui Do Bich Van

Mr. Le Anh Tu

Mr. Nguyen Ho Hoang Vu

Mr. Le Hai Lam

Mr. Nguyen Quang Triet

Mr. Cao Xuan Lanh

Chief Executive Officer

Standing Executive Vice President

Vice President

Vice President

Vice President

Vice President

Vice President

Vice President

Vice President

Vice President

Vice President cumChief Financial Officer

Vice President

Vice President

Vice President

0.0033689

0

0.0057685

0.0053907

0.0016472

0.0000009

0

0

0.0042342

0

0.0023008

0

0.0001102

0

Appointed onth 20 Dec 2013

Notes

Appointed on th06 Aug 2013

Appointed on th05 Sep 2013

Appointed on th17 Sep 2013

Appointed on th25 Sep 2013

Appointed on nd02 Dec 2013

Annual Report 201329

Appointed on th06 Aug 2013

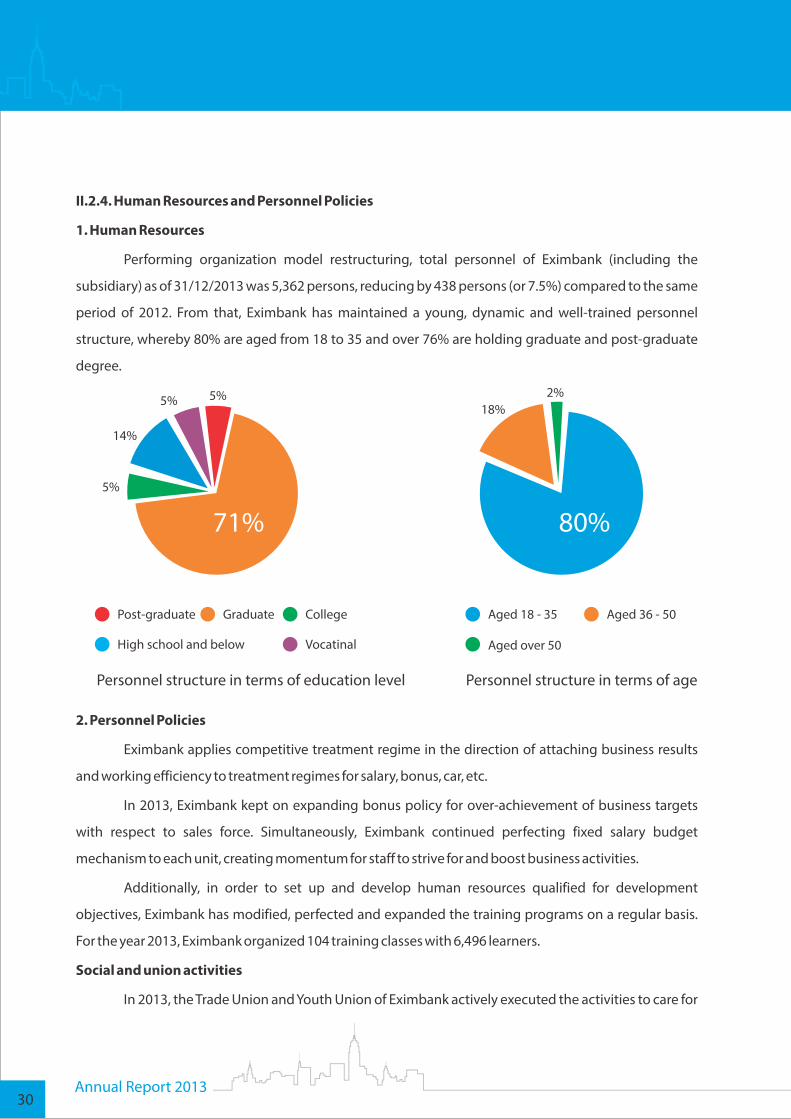

II.2.4. Human Resources and Personnel Policies

1. Human Resources

Performing organization model restructuring, total personnel of Eximbank (including the

subsidiary) as of 31/12/2013 was 5,362 persons, reducing by 438 persons (or 7.5%) compared to the same

period of 2012. From that, Eximbank has maintained a young, dynamic and well-trained personnel

structure, whereby 80% are aged from 18 to 35 and over 76% are holding graduate and post-graduate

degree.

5%

14%

5% 5%

Post-graduate Graduate College

High school and below Vocatinal

71% 80%

18%2%

Aged 18 - 35 Aged 36 - 50

Aged over 50

Personnel structure in terms of education level Personnel structure in terms of age

2. Personnel Policies

Eximbank applies competitive treatment regime in the direction of attaching business results

and working efficiency to treatment regimes for salary, bonus, car, etc.

In 2013, Eximbank kept on expanding bonus policy for over-achievement of business targets

with respect to sales force. Simultaneously, Eximbank continued perfecting fixed salary budget

mechanism to each unit, creating momentum for staff to strive for and boost business activities.

Additionally, in order to set up and develop human resources qualified for development

objectives, Eximbank has modified, perfected and expanded the training programs on a regular basis.

For the year 2013, Eximbank organized 104 training classes with 6,496 learners.

Social and union activities

In 2013, the Trade Union and Youth Union of Eximbank actively executed the activities to care for

30Annual Report 2013

spiritual life of staff such as music shows, sports events, professional competitions, cooking competitions,

photogenic staff competitions etc., which created ebullient atmosphere and receives response with

great enthusiasm from the majority of employees.

Going forward the tradition from the first days of establishment till now, in 2013, Eximbank

continued participating in and contributing to charity and social security activities, namely as programs

of buying health insurance cards for poor patients; “surmounting the fate”; “connecting dreams, crossing

rivers and lakes for learning”; “light of belief”; “for beloved Truong Sa pupils”; sponsoring for the

construction of bridges, roads, medical service units, gratitude houses; supporting scholarship funds,

charity social funds, etc.

II.3. Investment in Debt Management and Asset Exploitation Company (Eximbank AMC)

II.3.1. Business characteristics of the company

III.3.1.1. Form of capital ownership

The Debt Management and Asset Exploitation One-member Limited Liability Company

(Eximbank AMC) was established under Decision No. 157/2010/EIB/QD-HDQT dated 21 April 2010 of the

bank's Chairman of the Board of Directors and Decision No. 754/QD-NHNN dated 01 April 2010 of the

State Bank of Vietnam.

Eximbank AMC's Business Registration Certification No. 0310280974 was granted by the

Department of Planning and Investment on 24 August 2010 with the initial registered charter capital of

VND300 billion. The second amendment was made on 08 September 2011, the third on 30 March 2012,

the eighth on 12 November 2013 with the registered charter capital of VND1,700 billion. The paid-up

charter capital as of 31 December 2013 was VND955 billion.

III.3.1.2. Business sector, business lines and main business activities

Receive and manage outstanding loans of Vietnam Export Import Commercial Joint Stock Bank and the

collaterals related to loans to settle and recover funds in the quickest time;

Proactively sell collaterals, distrained and sequestered properties under the discretion of Vietnam Export

Import Commercial Joint Stock Bank at market price as approved by the Standing Board of Directors;

Restructure outstanding loans; handle collaterals; perform other activities under the authorization of

Vietnam Export Import Commercial Joint Stock Bank in accordance with law regulations.

Buy and sell outstanding loans of other credit institutions, and of the asset management companies of

other commercial banks as stipulated by law.

Annual Report 201331

No. Shareholder Number of shares Shareholding ratio (%)

- Major shareholders (owning 5% of charter capital and upwards)

- Shareholders owning less than 5% of charter capital

1

348,636,855 28.218

886,886,049 71.782

Entity shareholder 769,145,420 62.253

- Domestic 435,777,768 35.271

- Foreign 333,367,652 26.982

Individual shareholder 466,377,484 37.747

- Domestic 464,155,938 37.568

- Foreign 2,221,546 0.180

2

- Foreign shareholder 335,589,198 27.162

- Domestic shareholder 899,933,706 72.838

- State shareholders 169,680,492 13.733

- Other shareholders 1,065,842,412 86.267

- Founding shareholders 0 0

3

4

II.3.2. Summary of the operation, financial conditions and business results of AMC

In 2013, Eximbank AMC performed three main functions: managing and exploiting assets; acting

as the developer of some construction works of Eximbank and Eximbank AMC under the Bank's

authorization; and develop the warehouses to manage the pledged/mortgaged commodities of the

units within Eximbank's network.

Some financial targets of Eximbank AMC as of 31/12/2013:

- Total assets: 968,146 million VND.

- Owners' equity: 955,000 million VND.

- Profit before tax: 1,528 million VND.

- Profit after tax: 1,209 million VND.

II.4. Number of shares and shareholding structure of Eximbank

II.4.1. Number of shares

As at 31/12/2013, number of shares: 1,235,522,904 shares

Number of transferable shares: 1,008,878,326 shares

Number of non-transferable shares as regulated at clause 1 Article 56 –

Law on Credit Institutions 2010: 226,644,578 shares

II.4.2. Shareholding structure

32Annual Report 2013

Details of major shareholders

No. Name Line of business

Contact address Number of shares

Holding ratio (%)

1 Commercial Joint-stock Bank for Foreign Trade of Vietnam (Vietcombank)

Banking 198 Tran Quang Khai Street, Hoan Kiem District, Hanoi

101,245,131 8.195

2 VOF Investment Ltd Đầu tư tài chính

P.O Box 2208, Road Town, Tortola, B.V.I

62,062,517 5.023

3 SUMITOMO MITSUI BANKING CORP.

1-2 Marunouchi 1-chome, Chiyoda-ku, Tokyo 100-0005 Japan

185,329,207 15.000Ngân hàng

II.4.3. Changes in Shareholders' equity

Eximbank did not increase its charter capital in the year 2013

II.4.4. Treasury stock transactions

On 06/12/2013, Eximbank issued Notice No. 489A/2013/EIB/TGD regarding anticipated

redemption of 11,000,000 EIB shares for treasury stock and on 17/01/2014 Eximbank reported in the

official dispatch No. 156/2014/EIB/TGD the completed buyback of 6,090,000 shares for treasury stock

with average trading price of VND12,853/share by order-matching method and the official dispatch No.

157/2014/EIB/TGD the number of outstanding shares with voting right (1,229,432,904 shares).

II.4.5. Other securities: none

Cộng 348,636,855 28.218

Annual Report 201333

III. REPORTS AND ASSESSMENTS OF THE BOARD OF MANAGEMENT

III.1. Evaluation of business performance

In 2013, although the business performance dealt with many impediments and challenges,

Eximbank still maintained its growth pace with respect to major targets such as loan balance to

customers growing by 11.3%; funds mobilized from economic entities and individuals despite dropping

down by 3.4% but increasing by 17.4% compared to 2012 should the decrease in gold mobilized funds as

regulated by the State Bank be excluded; NPL ratio being curbed at a fairly low rate compared to the

whole industry. As for the profit target, with the policy of sharing difficulties with customers by reducing

lending rates, offering various credit packages with preferential interest rates and creating favourable

conditions for the enterprises to effectively approach the funds at low cost, net interest income

accordingly dropped down and profit before tax only completed 26% of the plan. Regarding the

governance and administration, Eximbank performed strong and comprehensive restructuring from the

Head Office to Branches, strengthened the sales force, consolidated and increased customer base,

established centralized management models, focused on developing retail banking activities and

electronic banking, upgraded operating quality of the transaction offices, continuously innovated

products and services and set up suitable products to customers' needs, enhanced service quality,

reinforced risk management, tightly controlled credit quality, boosted brand promotion, etc., which

helped gradually surmount the limitations and outstandings to further improve business efficiency of

the whole network and lay safe and solid foundation for development in the coming years.

III.1.1. Retail Banking

Retail fund mobilization

As of 31/12/2013, funds mobilized from individual customers reached 54,865 billion VND, down

15.3% compared to the early year. If the decrease in gold mobilized funds as regulated by the State Bank

was excluded, mobilized funds from individual customers still posted good growth, rising by 10%

compared to the early year with retail customer base accounting for up to 96% of the total number of

customers (equivalent to more than 760,000 individual customers), surging by 16% from the early year.

Such result showed customers' great trust in Eximbank in the context that Vietnamese banking sector

encountered with many challenges and obstacles in 2013.

Eximbank has always been proactive, timely and flexible in its mobilization policies, actively

monitored and grasped the market, promptly given out better customer care solutions, made

diversification in combination with modern technology, enhanced products/services, thus meeting the

demands of different retail customer segments.

Annual Report 201335

Main products and services offered to individual customers of Eximbank are: Online Savings

Deposit, Savings Deposit in Installments, Phuc Bao An Savings Deposit, Savings Deposit For Beloved

Children, Truong Phat Loc Savings Deposit, Salary Accumulation Savings Deposit, etc. Besides, there are

many attractive promotion programs with diversified, practical and high-valued gift portfolio, and

multiple utilities such as deposit in one place - withdrawal in different places, registration for automatic

transfer of interest or automatic funds transfer, etc. together with Eximbank VIP service with many

prominent privileges, priority servicing and enjoyment of high-class service.

Retail credits

Credit growth in the year 2013 faced with many impediments under the common context of the

economy with inventories and purchasing power not being much improved, resulting to decrease in

customers' needs for borrowing funds. Besides, with the restricted corporate credit demand, many banks

focused on exploiting solutions to increase retail credits in order to boost credit growth.

Eximbank had strived to overcome the tough situation, taken the initiative to transform business

model in line with economic conditions, and officially established Retail Banking Center to strengthen

retail banking activities. Simultaneously, Eximbank implemented various lending programs at

preferential interest rates in combination with reducing lending rates to help share difficulties with

customers. Thanks to that, retail credit balance in 2013 reached 29,018 billion VND (accounting for 35% of

the total loan balance of the whole Eximbank's network), up 10% from the early year (or 2,550 billion

VND).

In 2014, Eximbank orients to keep on perfecting its business model and enhancing retail sales

force competence for the target of increasing market share in conjunction with improving credit quality

and customer service quality.

Card issuance and acquiring

In 2013, total number of cards issued reached 132,972 cards, raising the total number of issued

cards to 1,286,855 cards. Card use volume reached 10,822 billion VND, growing by 21% compared to

2012.

Eximbank's merchant network achieved 2,672 units with 4,928 POS's and 260 ATMs distributed in

major locations nationwide. Total acquiring volume during 2013 through the channels was quite

satisfactory with 10,925 billion VND, up 21% over the same period last year.

Presently, Eximbank has connected to the ATM, POS system with 46 banks in the 2 big card

alliances in Vietnam (Smartlink, Banknet), expanded POS payment system and diversified types of

36Annual Report 2013

businesses accepting card payment to satisfy customers' needs for card use.

In addition to the expansion and investment in the acceptance network and connection to the

banks, in 2013 with an aim to enhance card service quality, Eximbank launched many products and

services, increased facilities and customer care programs, prominently as JCB credit card, MasterCard

Debit card, Teacher Card Paypass card products; international card online transaction authentication

service; transaction identification and authentication by fingerprint service, utilities enhancement on

Internet Banking and Mobile Banking (card issuance registration, domestic and international card

lock/unlock, inquiry for card limit, payment for statement balance of credit card, registration for card

services, etc.), preferential and promotional programs with multiple forms and ample and diversified

substance.

Services

Inward remittance payment: total retail inward remittance volume through Eximbank in 2013

achieved nearly 293 million USD, increasing by 22% (or 54 million USD) compared to 2012; number of

transactions also rose by 34%. In the year, Eximbank attracted more than 11,000 clients receiving inward

remittance, mostly from the US, Singapore, Germany and Australia. MoneyGram express service gained

strong growth rate with the volume increasing by 74% compared to 2012, attracting more than 17,000

transactions.

Outward overseas remittance: total outward overseas remittance volume of retail customers in

2013 reached more than 202 million USD, rising by 30% against 2012. Of which, overseas study

remittance volume continued its growth pace and gained more than 165 million USD, accounting for

82% of total overseas remittance volume, increasing by 30% compared to 2012. With the fast – safe –

handy criteria, competitive fee policies, worldwide correspondent network, and years of experience in

overseas study remittance, Eximbank always creates psychology of confidence and satisfaction for

customers on professionalism and customer- servicing attitude of staff and officers upon banking with

Eximbank.

III.1.2. Corporate Banking

Corporate fund mobilization

In 2013, domestic economy continued its stagnancy with number of enterprises being dissolved

and ceasing its operations higher than the two previous years, making not only credit activity but also

fund mobilization from corporate customers of Eximbank deal with many difficulties.

In the context that credits still grow restrictedly, Eximbank had made efforts to reduce lending

rates to attract corporate customers; thanks to that, corporate fund mobilization still gained encouraging

Annual Report 201337

results. New customer development was also boosted, actively contributing to raise fund mobilization.

As of end of 2013, total mobilization from corporate customers achieved 27,785 billion VND, growing by

34% compared to 2012.

Corporate customer services

According to the orientation to build up Eximbank into a modern bank providing a variety of high

quality products and services, and to enhance its competitiveness, in the year 2013, Eximbank continued

perfecting, developing and newly launching lots of products and services, offering many more facilities

to customers.

Traditional services like collection and payment on behalf of customers, payroll, domestic and

overseas funds transfer for payment, etc. are always paid with special attention for innovations in terms of

procedures and technology to have them performed quickly and precisely.

In order to satisfy customers' increasing needs, Eximbank has incessantly invested in engineering

technology and human resources to improve and perfect Internet Banking service. At the moment,

Eximbank's Internet Banking service has well accommodated transaction demands of customers.

Besides, Eximbank also expands its association and partnership to launch other utility services,

and cooperates with State agencies, public service suppliers, and many other units to offer diversified

collection services.

Corporate credits

During the tough period of the economy and with the non-thriving production and business of

the enterprises, Eximbank has implemented many supportive policies to the enterprises such as

reducing lending rates, launching lots of preferential product packages to meet customers’ demands, etc.

In addition, in the year 2013, Eximbank set up sales force (RM) in order to seek for new customers, which

has initially brought positive results. Thanks to that, loan balance in 2013 posted fairly good growth. As of

31/12/2013, loan balance of corporate customers reached 54,336 billion VND, rising by 12% compared to

the early year.

International settlement

2013 was still a hard and challenging year to the operations of Vietnamese banking system in

general and international settlement activity in particular, which stemmed from complicated

evolvements of the local and international economy, perfunctory operation or bankruptcy of Vietnam's

export and import companies, leading to the shrinkage in both quantity and value of international

settlement transactions and activities at the banks.

38Annual Report 2013

However, with the advantages in terms of brand name, high-quality human resources, flexible

policies, proper product packages, and a wide correspondent network throughout the markets of

America, Japan, Singapore, Taiwan, Hong Kong, Korea, China and EU region, etc., international settlement

activity at Eximbank just slightly contracted compared to 2012 as import bills volume increase was not

sufficient to compensate for the export bills volume decrease.

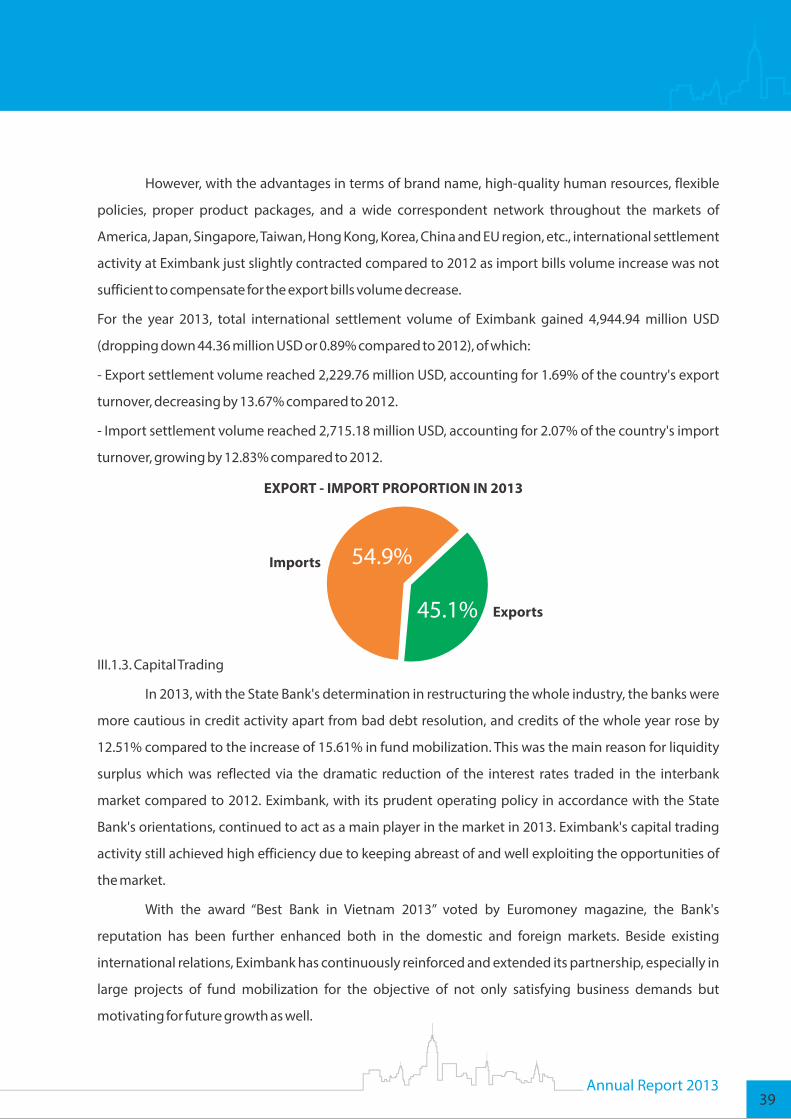

For the year 2013, total international settlement volume of Eximbank gained 4,944.94 million USD

(dropping down 44.36 million USD or 0.89% compared to 2012), of which:

- Export settlement volume reached 2,229.76 million USD, accounting for 1.69% of the country's export

turnover, decreasing by 13.67% compared to 2012.

- Import settlement volume reached 2,715.18 million USD, accounting for 2.07% of the country's import

turnover, growing by 12.83% compared to 2012.

45.1%

54.9%

EXPORT - IMPORT PROPORTION IN 2013

Imports

Exports

III.1.3. Capital Trading

In 2013, with the State Bank's determination in restructuring the whole industry, the banks were

more cautious in credit activity apart from bad debt resolution, and credits of the whole year rose by

12.51% compared to the increase of 15.61% in fund mobilization. This was the main reason for liquidity

surplus which was reflected via the dramatic reduction of the interest rates traded in the interbank

market compared to 2012. Eximbank, with its prudent operating policy in accordance with the State

Bank's orientations, continued to act as a main player in the market in 2013. Eximbank's capital trading

activity still achieved high efficiency due to keeping abreast of and well exploiting the opportunities of

the market.

With the award “Best Bank in Vietnam 2013” voted by Euromoney magazine, the Bank's

reputation has been further enhanced both in the domestic and foreign markets. Beside existing

international relations, Eximbank has continuously reinforced and extended its partnership, especially in

large projects of fund mobilization for the objective of not only satisfying business demands but

motivating for future growth as well.

Annual Report 201339

Transaction figures in 2013

III.1.4. Foreign Currency Trading

The stability of the foreign exchange market during the year 2013 brought favourable conditions

to export and import activity of the enterprises which is Eximbank's traditional strength. So as to enhance

foreign exchange service quality, Eximbank has continuously diversified products and services serving

for export and import customers to increase utilities for them and simultaneously raise competitiveness

and transaction volume.

Concerning system administration with respect to foreign currency trading, Eximbank has

established and improved the internal trading system in way of modernity, transaction time reduction,

and cost mitigation. Eximbank has also strengthened its governance on foreign currency trading in line

with international standards and Vietnamese market conditions, kept on fostering and heightening

professional competence for trading officers of the whole network.

Accordingly, foreign currency trading activity of Eximbank in 2013 still maintained growth pace

and achieved positive results. Foreign currency trading volume of 2013 reached 41.093 billion USD,

increasing by 44% compared to 2012.

III.1.5. Gold Trading

In 2013, the gold market experienced unpredictable fluctuations with sharp reduction of both

international gold price and domestic gold price. Besides, the State Bank continued tightening its

management over gold trading activity. Since March 2013, the State Bank for the first time organized the

auction to sell gold bars to the market, marking a big change in its managing and regulating the gold

trading activity. With 76 auctions in 2013, the State Bank had supplied to the market nearly 70 tons of gold

bars for price stabilization.

The revision and change in the State Bank's policy affected gold trading result of Eximbank as one

of the 6 members participating the gold price stabilization program of the State Bank since early 2012.

In 2013, Eximbank kept on expanding retail market to every customer, which is treated as the

Target 2012 2013 (+)/(-) against 2012

Volumes

VND (billion VND)

USD (million USD)

Receiving/Borrowing

Depositing/Lending

202,549

367,988

6,733

5,618

287,054

270,120

9,511

4,944

+41.72%

-26.59%

+42.26%

-12.00%

Receiving/Borrowing

Depositing/Lending

40Annual Report 2013

main business strategy in gold trading activity. Eximbank has organized a force of specialized gold

trading officers to strengthen the marketing and customer care. In addition, with the advantage of being

licensed by the State Bank to sell and purchase gold bars at more than 200 banking units nationwide, in

2013, Eximbank continued to be among the leading banks in terms of gold bar trading activity in

Vietnam.

Gold purchase and sale volume in 2013 of Eximbank was 4.5 million taels, down 50% compared to

2012.

III.1.6. Financial Investment

In 2013, Vietnam's economy was still exposed to difficulties, deposit and lending rates were in

declining tendency; real estate market remained frozen; stock market just made slight recovery and

swayed in a narrow range with market liquidity being still low.

Facing such obstacles, Eximbank had restructured its investment portfolio to ensure safety and

effectiveness, tightly control the capital, and comply with the law stipulations. As for capital contribution

for share purchase, Eximbank did not make new disbursements, just focusing on divesting from the non-

potential enterprises. For bond investment, Eximbank concentrated on investing in bonds of those with

stable business operation, high rate of return and security assets. In 2013, Eximbank made considerable

disbursement to such bonds, thus making not a small contribution to the Bank's total income.

As at end of 2013, the value of capital contribution and securities investment was 16,791 billion

VND (increasing by 18% compared to the early year). Of which, investments in bonds and valuable papers

were 14,653 billion VND (surging by 25% compared to the early year), accounting for 87.3% and

investments in stocks (including investments and capital contribution for share purchase, associates)

were 2,138 billion VND, accounting for 12.7%.

III.1.7. Customer Base Development

Eximbank's customer base has kept its fair growth pace thanks to incessant efforts in setting up

professional sales force, improving servicing quality, and innovating products and services. Total number

of customers of Eximbank as at end of 2013 nearly reached 796 thousand customers, growing by 16.3%

compared to 2012. Of which:

Retail customers accounted for 96%, increasing by 16.5% from the early year (or 108 thousand

customers).

Corporate customers made up 4%, rising by 13.3% from the early year (or 4 thousand customers).

Annual Report 201341

III.2. Financial conditions

III.2.1. Assets

In 2013, Eximbank had entirely reduced its gold mobilized funds as per the State Bank's

regulation and focused on developing mobilized funds from economic entities and residents, making

Eximbank's scope of total assets remain at a nearly equivalent level compared to 2012. In terms of fund

use, Eximbank attached special importance to heightening efficiency of fund use channels, concentrated

on pushing credit balance increase through maintaining and promoting traditional strength as corporate

lending, approaching big projects, gradually growing retail loan balance on the basis of building

professional sales force, strengthening marketing, expanding customer base, improving operational

handling procedures, enhancing competitiveness of existing credit products in combination with

researching new credit products to satisfy customers' diversified demands for funds. Besides, Eximbank

continued revising and perfecting fund transfer pricing (FTP) mechanism in line with actual business

situation, contributing to effectively manage sources of funds of the whole network and boost credit

growth.

In terms of income structure, earnings from credit activities were still the major source of income

of the Bank. In the previous year, responding to the State Bank's policy, Eximbank had lowered lending

interest rates to share with borrowing customers part of their obstacles, causing net interest income of

the Bank to shrink, which affected Eximbank's profit.

The average return-on-asset ratio (ROA) was 0.4%

The average return-on-equity ratio (ROE) was 4.3%

III.2.2. Credit Quality

Performing the orientation of the State Bank in bad debt handling, credit quality management,

Eximbank has applied necessary measures to recover and dispose of bad debts. As of end of 2013,

Eximbank controlled its NPL ratio at low level (1.98% of total loan balance).

III.3. Improvements in organization structure, policy and management

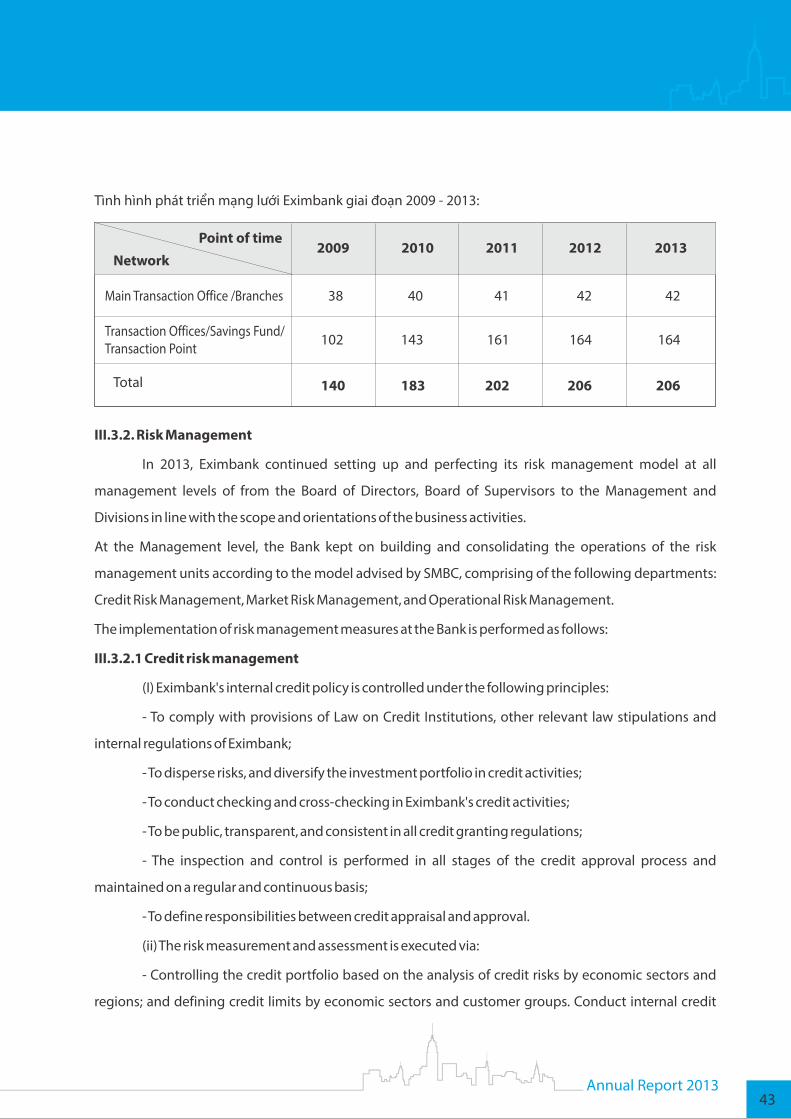

III.3.1. Network Development

In 2013, Eximbank put into operations 2 more Transaction Offices (Hoi An Transaction Office and

Bien Hoa Transaction Office), and terminated operation of 2 Transaction Points at Phu Hung Securities

Corporation – Can Tho City Branch and KimEng Securities Joint Stock Company – Can Tho City Branch. As

of 31/12/2013, Eximbank's operation network comprised of 206 banking units (including Main

Transaction Office, 41 Branches, 162 Transaction Offices, 01 Savings Fund and 01 Transaction Point).

42Annual Report 2013

Tình hình phát triển mạng lưới Eximbank giai đoạn 2009 - 2013:

III.3.2. Risk Management

In 2013, Eximbank continued setting up and perfecting its risk management model at all

management levels of from the Board of Directors, Board of Supervisors to the Management and

Divisions in line with the scope and orientations of the business activities.

At the Management level, the Bank kept on building and consolidating the operations of the risk

management units according to the model advised by SMBC, comprising of the following departments:

Credit Risk Management, Market Risk Management, and Operational Risk Management.

The implementation of risk management measures at the Bank is performed as follows:

III.3.2.1 Credit risk management

(I) Eximbank's internal credit policy is controlled under the following principles:

- To comply with provisions of Law on Credit Institutions, other relevant law stipulations and

internal regulations of Eximbank;

- To disperse risks, and diversify the investment portfolio in credit activities;

- To conduct checking and cross-checking in Eximbank's credit activities;

- To be public, transparent, and consistent in all credit granting regulations;

- The inspection and control is performed in all stages of the credit approval process and

maintained on a regular and continuous basis;

- To define responsibilities between credit appraisal and approval.

(ii) The risk measurement and assessment is executed via:

- Controlling the credit portfolio based on the analysis of credit risks by economic sectors and

regions; and defining credit limits by economic sectors and customer groups. Conduct internal credit

NetworkPoint of time

2009 2010 2011 2012 2013

Main Transaction Office /Branches 38 40 41 42 42

Transaction Offices/Savings Fund/Transaction Point

102 143 161 164 164

Total 140 183 202 206 206

Annual Report 201343

scoring in order to frequently monitor and assess customers' creditworthiness.

- Setting up the list of security assets, providing for the loan-to-value ratio to serve as the basis for

determining the expected losses upon risk occurrence;

- Performing internal credit scoring and rating of customers periodically, and assessing their

financial capabilities, business conditions and loan recovery ability regularly;

- Conducting loan classification as per regulations of the State Bank and international standards

to fully evaluate the Bank's credit quality.

(iii) In the tough economic conditions that implied lots of credit risks in 2013, Eximbank

continued centralizing credits to the Head Office to ensure close control in credit granting. The

centralization of credit activities to the Head Office is executed through:

- Centralizing appraisal and approval at the Head Office with respect to loans with high risk levels,

loans without security assets and loans to the sectors or industries being restricted for credit extension by

Eximbank;

- Most of the security asset appraisal being centralized at the Head Office;

- Internal inspection and control officers of the Head Office being assigned to perform the tasks at

each Branch so as to monitor each credit file before disbursement.

III.3.2.2 Operational risk management

(I) Ensure inspection and cross-checking in the operations;

(ii) Inspection and monitoring being conducted before, during, and after execution of important

operations such as credit, payment, cash by the Head Office's Internal Inspection and Control

Department;

(iii) Establish and manage the approval limits on transaction systems in line with new business

operation model and risk restriction;

(iv) Establish and operate “Operational Diary” to record and warn on operational errors in the

whole network of the Bank;

(v) Launch the system of money laundering prevention and combat to monitor and prevent fraud

and suspicious transactions;

(vi) Coordinate with relevant units to set up provisions on business continuity such as responses

regarding liquidity, response to IT incidents and processing of information crisis.

44Annual Report 2013

III.3.2.3 Market risk management

- Interest rate risk management: Eximbank regulates interest rates in an active and flexible

direction with respect to each type of products and services from time to time; keeps close track of

interest rate movements in the market, forecasts on moving tendency of interest rates; analyzes interest

rate spread and simulates possibilities that interest rates may impact profit; computes fluctuations of the

Bank's net asset value according to interest rate movements by NPV model; monitors and reports net

interest margin in order to ensure expected profit target.

- Exchange rate risk management: Eximbank manages exchange rate risks through: analyzing

and monitoring exchange rate movements in the market daily; monitoring developments of the local

and international economic situation, monetary policy of the State Bank likely affecting the exchange

rate so as to give out forecasts on exchange rate; controlling gold and foreign currency position as

regulated; regularly evaluating and analyzing gold and foreign currency position in the whole network in

order to ensure exchange rate changes will not impact much on Eximbank's profit;

In addition, Eximbank also uses hedging measures against exchange rate risks through derivative

operations, including: option transactions, forward contracts, currency swap contracts to hedge for

foreign exchange transactions.

- Liquidity risk management: Eximbank tightly controls the compliance with the State Bank's

regulations on liquidity; makes analysis and reports on liquidity risks via asset-liability analysis table

according to actual maturity period, and prudent ratios. Eximbank has also perfected its regulations on

solvency management and on prudent ratios in the Bank's operations.

III.3.3. Information Technology System

With the objective of building a modern and versatile bank on ground of state-of-art technology,

the Information Technology (IT) system of Eximbank in 2013 continued to be perfected and developed

with the following accomplishments:

(1) Eximbank kept on accelerating the implementation of key projects in the IT Development

Program so as to satisfy the requirements of the business development strategy in the period of 2011 –

2015 and visions up to 2020, specifically:

- Eximbank focused on speeding up the progress of organizing the bidding for the Korebank

replacement project to ensure project completion in 2016;

- Eximbank entered into the Memorandum of Understanding (MoU) with Schneider Electric IT

Annual Report 201345

Vietnam to implement the construction of a modern Data Center meeting international standards and

the State Bank's requirements.

(2) With the business strategy focusing on retail sales promotion, Eximbank established the

Electronic Banking Department to boost diversified development of products and services on online

transaction channels, gradually making these services be advantage of Eximbank;

(3) Applying advanced banking technology and always placing the goals of security and safety

for customers at top priority, Eximbank has officially launched to customers the “Banking transaction

authentication by fingerprint” technology which helps ensure safety and confidence for customers upon

transacting with the bank;

(4) Eximbank continued reviewing and setting up security policy with respect to transaction

systems such as keeping on implementing phase 2 of the PCI DSS compliance project; putting into

operation the centralized Internet access control system which helps prevent and limit information safety

risks when users access Internet, equipping with the attack prevention and combat system; and

perfecting the network and security system at the Disaster Recovery Center.

The achievements of IT system in 2013 serve as the premise to move forward with the IT

development strategy up to 2015 and contribute to the business operations in accordance with the

Bank's general strategy.

III.3.4. Training and Human Resources Development

In 2013, following the Board of Directors' and the Board of Management's guideline on business

model revision and sales-driven development, training activity of Eximbank also evolved in way of

training on sales knowledge, skills and experience for Eximbank's staff. During the year, the Training

Center of Eximbank organized 104 training courses with 6,496 learners, exceeding the proposed plan by

30%. Of which, 40 classes were held to train for sales officers with 3,081 learners, accounting for nearly

39%.

In addition, training courses for Branch Directors and Transaction Office Managers also received

high appreciation as they have helped to enhance knowledge, skills and experience in management and

business for learners.

For the training orientations in the forthcoming time, Eximbank will continue to focus on training

the sales officers, organizing training classes for stand-by Branch Directors and Transaction Office

Managers to prepare for the succeeding human resources, training and updating new knowledge,

46Annual Report 2013

regulations and policies for operational employees.

III.3.5. Cooperation with Foreign Strategic Shareholder

thIn the year 2013 which marked the 40 anniversary of the establishment of diplomatic relations

with Japan, Vietnam received new wave of investment from Japanese investors in the fields of from

precision engineering, supporting industries to breeding and agricultural production. Eximbank has

cooperated with its strategic shareholder, Sumitomo Mitsui Banking Corporation (SMBC), to deploy

Business Matching service, thereby referring and supporting customers to search for partners and new

markets for their products and services. With an extensive network and large database of the two banks,

the Business Matching service brings about many benefits, solves output for enterprises, increases

customer base, and creates premises for the parties' sustainable development.

Apart from the Corporate Banking services, SMBC continued supporting Eximbank to boost retail

banking activities by building professional cadre of consultants and sales officers, and cross-selling

packaged products and services to enterprises' employees. Through the relationship with Japanese

automobile manufacturers, Cedyna Financial Corporation and Sumitomo Mitsui Card Company –SMCC,

which are subsidiaries of Sumitomo Mitsui Financial Group – SMFG, have coordinated with Eximbank to

strengthen card sales business, auto loans, electronic banking services, Mobile Banking, as well as

increase the merchants together with special offers exclusively for Eximbank's customers.

In order to increase customer satisfaction and improve operational quality, Eximbank has set up

the Quality Management Department with a mission to establish the policies, regulations and

guidedance on quality, and coordinate with the Training Center to consistently implement the same

throughout the network. Moreover, the Asia Pacific Training Center of SMBC has also helped organize