Embed Size (px)

Citation preview

ADVISOR EDUCATIONAL KIT

ADVISOR EDUCATIONAL KITTABLE OF CONTENTS

I. INTRODUCTION LETTER – OPENING COMMENTS

II. SETTING THE STAGE

a. Realizing the opportunityb. How to capitalize on itc. Having the right mindset

III. WHAT IS NEEDED TO SUCCEED?

a. The right CPAb. The right wealth managerc. The right system; model, tools, strategies, and techniquesd. Knowledge and experiencee. Support (Home Office and local office)

IV. CPA PROSPECTING AND FORMALIZING THE RELATIONSHIP

a. Where to find CPAs to work withb. How to approach themc. How to develop the alliance and secure a productive working relationship

V. THE CPA IS ON BOARD—NOW WHAT?

a. Wealth Management integrationb. Business development is the end gamec. Office Set-Up: ensuring clients remain compliant with AICPA, FINRA, and State

Insurance Departments

VI. MAKING THE MOST OF THE SYSTEM: Alliance Management, Accountability and Support

a. What’s in it for me!b. Helping CPAs help their clientsc. Establishing goals and objectivesd. Measuring results

Hank Zewald is pleased that you have purchased The Client Acquisition Machine. This proven turnkey system is the ultimate client acquisition program in the marketplace. If implemented correctly, The Client Acquisition Machine is one of the most cost-effective and efficient ways to get in front of ideal prospects—A and B clients, high-net-worth individuals/families, business owners, affluent retirees, and C-level executives—on a favorable basis, and it is endorsed by the number one ranked professional advisor in the consumer marketplace, the CPA.*

This Advisor Educational Kit has two primary purposes: 1) to serve as a resource guide and 2) to be used as a training tool. The kit has five key sections:

1. Setting The Stage2. What Is Needed To Succeed3. CPA Prospecting and Formalizing The Relationship4. Wealth Management Integration and Business Development5. Alliance Management, Accountability, and Support

We are absolutely confident that this system can have a dramatic impact on your career and the ease with which you utilize your expertise. Our goal is to equip you with proven systems, tools, strategies, and techniques to build alliances the right way. In addition, we want to mentally prepare you with the right mindset, approach, and confidence to successfully pursue CPAs and ensure profitable and sustainable alliances with CPAs and other key centers of influence.

We are very excited about working with you and helping you capitalize on this tremendous opportunity.

Best of success,

Henry P. ZewaldQuantum Financial PartnersCPA and Managing Partner

*Advisor Today, June 2002.

SECTION 2: SETTING THE STAGEREALIZING THE OPPORTUNITY

As a wealth manager you are always looking for ways to take your business from good to great or from great to greater. The marketplace is filled with programs promising success in the financial services business.

It is well documented that the key difference between a good producer and a great producer is the ability to get in front of and work with A and B clients, high-net-worth individuals/families, business owners, affluent retirees, and C-level executives. Many wealth managers have the skill sets necessary to achieve success in wealth management services; however, many lack access to the affluent markets. Therefore, the key issue on the minds of most wealth managers is finding a proven and sustainable “Client Acquisition” system.

Problem SolvedThe Client Acquisition Machine is an ultimate lead generation program because it puts you in front of the right clients (A and B clients, high-net-worth individuals/families, business owners, affluent retirees, and C-level executives) on a favorable basis, and it’s endorsed by the most trusted advisor in the consumer marketplace, the CPA. If done right, working with CPAs and other financial professionals can transform your business.

Current SituationCPAs and other professionals (e.g., attorneys) are some of the most influential people in the financial marketplace. The typical CPA will service a clientele of between 300-500 people, who look to their tax advisor for guidance and advice. The more affluent individuals are, the greater the role the tax advisor plays in their wealth management. Currently, CPAs and accountants who offer investment and insurance planning services to their clients are in the minority.

However, studies have shown that today’s clients are clearly indicating that they want CPAs to be much more involved in the process of helping them make informed decisions about their financial future. Accordingly, to better meet these demands, more and more CPAs are exploring the possibility of expanding their services beyond tax, accounting, and auditing services to include proactive investment management strategies, insurance strategies, and wealth management services. The question ten years ago was, “Why add financial services?” The question today is, “How do we do it?”

So Why Are CPAs Interested?The knee-jerk assumption would be the desire for additional income. But while that is certainly a significant motivation, a study published in the Journal of Accountancy in June 2002 suggests that “over 75 percent of CPAs who provide or expect to provide wealth management services do so in order to better serve their clients, seeing this addition as a way to enhance their position of trust with their clients.”

Another significant motivator is competitive pressure. In some cases, it’s simply a matter of keeping up with rival CPA firms that have already added wealth management services. But in other cases, CPAs are looking for ways to set themselves apart from competitors that are not offering wealth management services.

CPAs feel pressure from many angles. Besides traditional competitive forces, tax planners are finding that more and more of their services are being commoditized. Do-it-yourself tax planning software is sold at the local Costco and large regional firms flex their muscle by low-balling their tax fees in ways that make it difficult for small firms to compete. Smaller firms need ways to differentiate themselves from everyone else.

Regardless of what motivates CPAs to add wealth management services, the bottom line is that by doing so they can increase the value of their offering to clients and the value of their businesses in a variety of ways, including:

● Increasing revenues by 10-20 percent of their gross billings (e.g., $1,000,000 of gross billings would equal $100,000 -$200,000).

● Providing a more complete solution by helping their clients achieve their financial hopes and dreams.

● Deepening their relationships and increasing the loyalty of their client base.● Setting themselves apart from other CPA firms, keeping themselves from being pigeon-

holed into the traditional tax preparer role.● Creating additional sources of new clients.

ALL WITHOUT MATERIALLY DISRUPTING THEIR DAY-TO-DAY OPERATIONS

The Bottom LineTax advisors are coming into the wealth management services field at an extraordinary rate. However, there is a catch. Most of these professionals still face the sizeable challenge of actually doing it. Most CPAs find they don’t have the time, expertise, or skill set to successfully integrate and deliver these services, and many of them eventually lose their desire and write it off as a failed experiment. A tremendous opportunity awaits, and we can help you make the most of it by providing the tools, training, and coaching you’ll need.

HOW TO CAPITALIZE ON IT

There are many techniques for generating new clients. For obvious reasons, working with CPAs, accountants and other professionals is at the top of the list for many wealth managers. As stated before, these individuals are increasing their interest in adding wealth management services, yet they still lack the time, expertise, skill set, and desire (TESD). So the solution for them is to establish a co-sourcing relationship with a wealth manager like you, who can essentially handle the wealth management services aspects of their firm.

Keep in mind that you’re not the first wealth manager to crack this code. CPAs are inundated with offers from other agents that appear to be similar to the one you’re presenting. So how do you set yourself apart from the pack?

The answer is to offer The Turnkey System, which will help raise you above the fray, and be willing to do what the others are not willing to do. Specifically:

● Learn the system. We are confident you will not find a better system in the marketplace. There is a variety of systems available, but you will find that while most of them may have very good form, few have much substance. Many CPA systems are good at convincing CPAs and other professionals to add wealth management services to their practices and assist them in becoming licensed, but then leave them on their own. Before long, TESD kicks in and their desire dries up.

A case in point—we met with a CPA who had become licensed with another company as part of its CPA system. After five years, the CPA had generated a grand total of $17.00 in commissions or fees. By the time we met with her, she had essentially given up on the process. Needless to say, once she saw The Turnkey System she was very impressed. It’s safe to say that in just a short time using The Turnkey System she’s significantly outperformed her previous output.

Keep in mind, the system is only as good as its user. You won’t be effective implementing a system you don’t understand—your proficiency with The Turnkey System will help create a sense of confidence and security with the CPA.

● Know your audience. If you are going to work with CPAs, you need to understand the CPA industry. If you are partnering with attorneys or P&C firms you better understand these industries as well. The better you understand the professions and businesses of those with whom you are forming an alliance, the better you will understand what motivates them. You’ll know what inherent concerns they have, how they process information, handle situations, and you’ll be able to develop synergistic alliances.

● Follow the system. Edwards Deming, the father of Total Quality Management, stated that 85% of all problems or successes can be attributed to the underlying system. The key to producing predictable results is to proceduralize—to build or utilize a system that when carefully followed is designed to produce a successful outcome. The Turnkey System is not simply a collection of tools and resources; it is a proven system that is designed to produce significant results. Use it!

● Commit to the work. This system is designed for wealth managers who are very serious about making CPA alliances work. This should not be a hobby for you or those with whom you develop alliances. Commit to your goals, develop your action plan, and then go to work. Drive the results!

● The right CPA generates the results. Be patient and selective when it comes to the alliances you develop. Just because a CPA expresses interest in the program, it doesn’t mean that you should immediately move ahead. Our experience has shown that it is not difficult to find a CPA who is interested in adding wealth management services—it’s not a difficult sale. But you need to ask yourself if you’ve found the right ally. Is the CPA’s clientele large enough to support an ongoing relationship? Is the clientele sophisticated enough to suggest the alliance will be profitable? Are your personalities in sync? What is their attitude—reluctantly hopeful or excitedly determined?

Additionally, we receive many requests from advisors looking “outside the box” wondering if they can apply this system with other professionals who are not in the accounting industry.

Although The Turnkey System can be effectively applied with attorneys and P&C firms, we suggest there is an abundance of opportunity within “the box.” There is not much need to look at outside industries or professions for building successful alliances. There are more than 400,000 CPAs in the United States, and they are viewed as the trusted advisors by their clients. Attorneys and P&C firms certainly have influence over their clients, but CPAs and other accounting professionals definitely have influence to a greater degree. We recommend that you keep the odds in your favor by focusing on CPAs and other accounting professionals.

● Develop and harness your own team. To effectively capitalize on this opportunity, you need to develop your own team:

o Key team members can be involved throughout the process to help you select, commit, launch, manage, and conduct business with the right strategic alliance—whether it’s with a CPA, attorney, or P&C firm.

o Advanced Markets and case design. Look to your [INSERT BROKER-DEALER] and key third party resources to make up a powerful team that can help you address the most sophisticated of clients.

o Licensing. Engage with your [INSERT BROKER-DEALER] licensing department as they will be a key resource in helping you and your strategic alliance partner complete all the appropriate paperwork.

o Marketing. Your [INSERT BROKER-DEALER] can be a tremendous resource in creating business development pieces. If you have an idea for business-development support materials that you’d like to create, partner with their market department to create high-quality, professional support materials.

o Administrative Support. Make sure you take the time to train your staff and the staff of your professional alliances to help you optimize your time and resources. This will help you keep your promise to not materially disrupt their day-to-day activities.

● The CPA needs YOU. As important as the CPA, attorney, or P&C firm are to the formula of success, they cannot succeed without you. You are the driver—the creative force who oversees the marketing and prospecting efforts. Knowing the correct solution is one thing, getting the client to implement the correct solution is quite another. You are the one who knows how to help clients make hard decisions and drive results. Do not underestimate your importance in this equation!

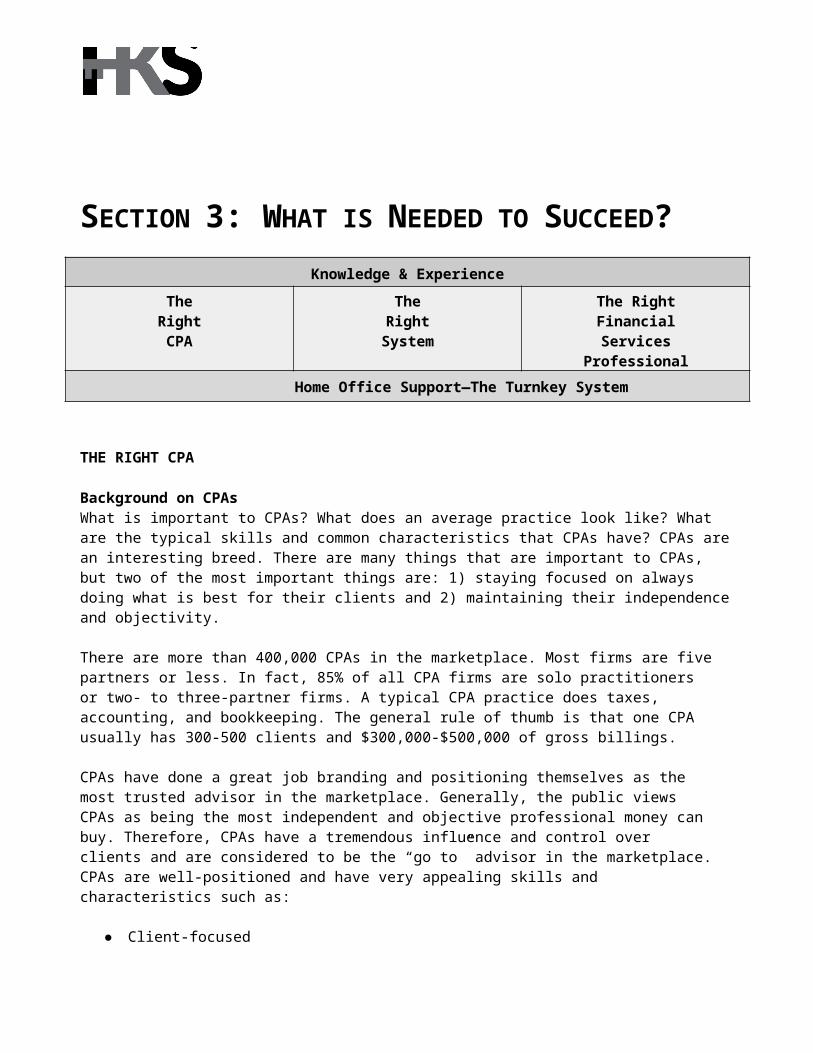

SECTION 3: WHAT IS NEEDED TO SUCCEED?Knowledge & Experience

The Right CPA

The Right

System

The Right Financial Services

ProfessionalHome Office Support—The Turnkey System

THE RIGHT CPA

Background on CPAsWhat is important to CPAs? What does an average practice look like? What are the typical skills and common characteristics that CPAs have? CPAs are an interesting breed. There are many things that are important to CPAs, but two of the most important things are: 1) staying focused on always doing what is best for their clients and 2) maintaining their independence and objectivity.

There are more than 400,000 CPAs in the marketplace. Most firms are five partners or less. In fact, 85% of all CPA firms are solo practitioners or two- to three-partner firms. A typical CPA practice does taxes, accounting, and bookkeeping. The general rule of thumb is that one CPA usually has 300-500 clients and $300,000-$500,000 of gross billings.

CPAs have done a great job branding and positioning themselves as the most trusted advisor in the marketplace. Generally, the public views CPAs as being the most independent and objective professional money can buy. Therefore, CPAs have a tremendous influence and control over clients and are considered to be the “go to” advisor in the marketplace. CPAs are well-positioned and have very appealing skills and characteristics such as:

● Client-focused● Conservative● Detail-oriented● Branded as highly ethical● Independent and objective● Linear thinkers● Adverse to risk● Substance over form

They are very focused on getting the job done right and meeting deadlines. They typically work long hours, especially during tax season. It’s not surprising to see CPAs work 80 hours or more a week during tax season. CPAs are not interested in being salesmen, and they certainly dislike being sold to.

In addition, CPAs are very conscientious about exposing their valued clients to a salesperson. They are very well organized and have great record keeping skills and billing systems in place. They pride themselves on maintaining their independence and objectivity and always putting their clients’ interests first. They have little tolerance for sloppy work and careless mistakes. The more you know about the “CPA mindset,” characteristics, and mode of operation, the better chance you will have developing long-term, productive relationships with them.

The Ideal CPA FirmCPAs/firms who have the following characteristics are the ones with whom you will want to work:

1. A firm that has the proper vision, attitude, and mindset.● Sees value in adding financial services.● Believes that it will be good for their clients.● Is comfortable with getting licensed and sharing in the revenue.● Recognizes that the marketplace is changing.● Is willing to treat the new venture as a business not a hobby.

2. Number of partners: fewer than five (one to three is ideal).3. Gross billings of $300,000–$1 million annually.4. Minimal attest work: less than 25% (audit, review, compilation).5. Focused on wealth management services: investment management, insurance, AUM.

● 10% percent of their time.● Already licensed, but not meeting benchmarks.*● Internal firm champion.

6. Complete partner buy-in. (internal vs. external marketing).7. An upscale clientele: average billing per client of $1000 or more.

The CPA Practice Profile and AICPA Self-Assessment will quickly and clearly help you evaluate the proper CPA firm to work with.

*CPAs who are already licensed are by far the best candidates to align with. They have the proper vision and mindset, and they already have a desire to be in the wealth management services business. The opportunity to work well with them exists because they most likely are not meeting the benchmarks (10–20 percent of their gross billings). We can show them how to achieve their goals and better serve their clients.

Workshop Exercise—Rank in order of best to worst

CPA Firm #1

1. Two-partner firm2. GB—$1.0 Million3. Currently offering

wealth management services

4. Securities registered

CPA Firm #2

1. 10-partner firm2. GB—$7.5 Million3. Not offering wealth

management services, but have set up an RIA

4. Very interested

CPA Firm #3

1. Solo practitioner 2. GB—$300,0003. Used to be

securities registered and offered wealth

elsewhere5. Life & Health licensed6. Frustrated with

the results to date

in learning more

5. Has a great deal of internal resources

management services

4. Looking to expand business

5. Does not want to get licensed or revenue share

THE RIGHT FINANCIAL SERVICES PROFESSIONAL

CPAs are looking for a wealth management services ally with many positive qualities, capabilities, skills, and characteristics. CPAs are looking for a financial services professional who:

● They can trust with their valued clients.● Has the experience and credentials to do the job right.● Has a “we” mentality rather than a “me” mentality.● Is a comprehensive, independent, and objective financial strategist.● Understands their business and is sensitive to the issues they are facing.● Is organized, professional, and has great follow through skills.● Has the infrastructure to support and service the strategic alliance.● Has systems and processes in place to deliver results.● Can offer a full range of products and services with no proprietary pressure.● Has a documented, successful track record.

For obvious reasons, everybody wants to work with CPAs, but very few can effectively and profitably do so. CPAs can be very selective about determining with whom they will work and to whom they will expose their valued clients. Understand that you may be among hundreds of wealth managers all hoping to work with your targeted or prospective CPA. Therefore, you must be fully equipped and prepared as you approach the CPA. You may have only one opportunity to approach a CPA and present the [INSERT PROGRAM NAME]. The focus of [INSERT PROGRAM NAME] is to educate you, train you, and provide you the tools needed for success. The program can empower and differentiate you from others and help you win over the CPA.

Important note: we all understand the comment, “your perception is your reality.” As a wealth manager, you have an idea of who you are and what products and services you provide. Knowing what is important to CPAs and what their perceptions and attitudes are about you and the services you offer is of great importance!

Workshop Exercise – Rank in order of best to worst

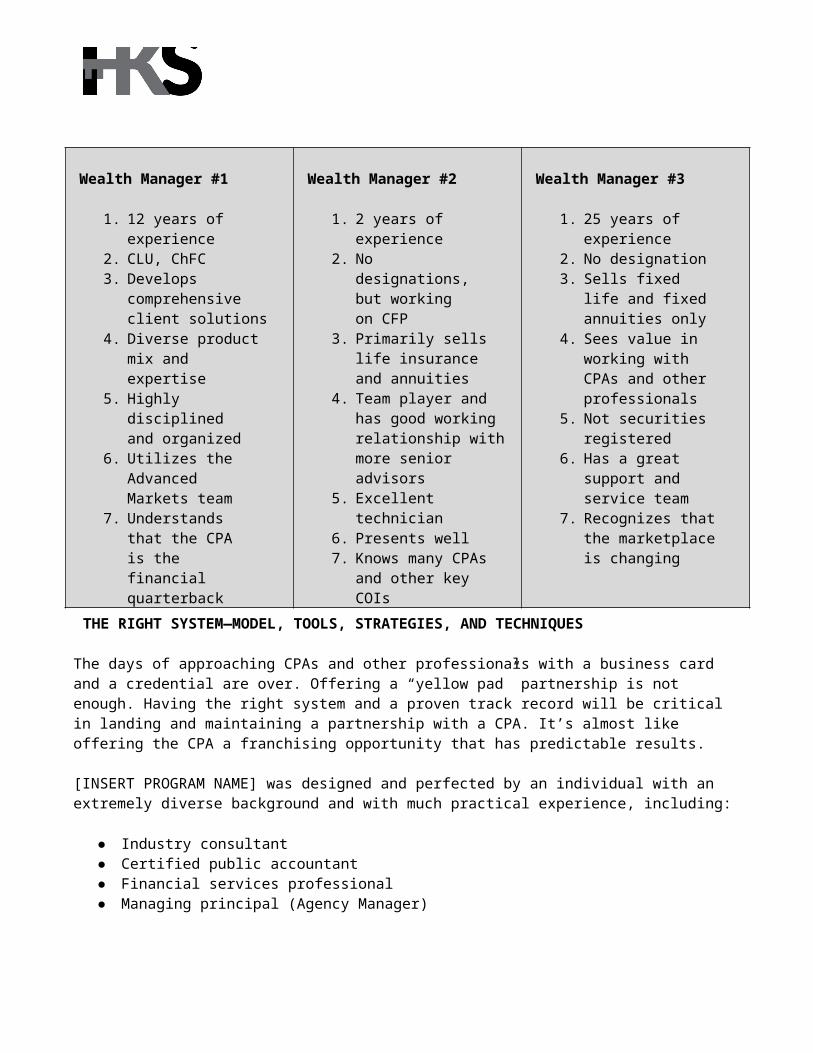

Wealth Manager #1

1. 12 years of experience2. CLU, ChFC3. Develops

Wealth Manager #2

1. 2 years of experience2. No designations,

but working on

Wealth Manager #3

1. 25 years of experience2. No designation3. Sells fixed life and

comprehensive client solutions

4. Diverse product mix and expertise

5. Highly disciplined and organized

6. Utilizes the Advanced Markets team

7. Understands that the CPA is the financial quarterback

CFP3. Primarily sells life

insurance and annuities

4. Team player and has good working relationship with more senior advisors

5. Excellent technician6. Presents well7. Knows many CPAs

and other key COIs

fixed annuities only4. Sees value in

working with CPAs and other professionals

5. Not securities registered6. Has a great support

and service team7. Recognizes that the

marketplace is changing

THE RIGHT SYSTEM—MODEL, TOOLS, STRATEGIES, AND TECHNIQUES

The days of approaching CPAs and other professionals with a business card and a credential are over. Offering a “yellow pad” partnership is not enough. Having the right system and a proven track record will be critical in landing and maintaining a partnership with a CPA. It’s almost like offering the CPA a franchising opportunity that has predictable results.

[INSERT PROGRAM NAME] was designed and perfected by an individual with an extremely diverse background and with much practical experience, including:

● Industry consultant● Certified public accountant● Financial services professional● Managing principal (Agency Manager)

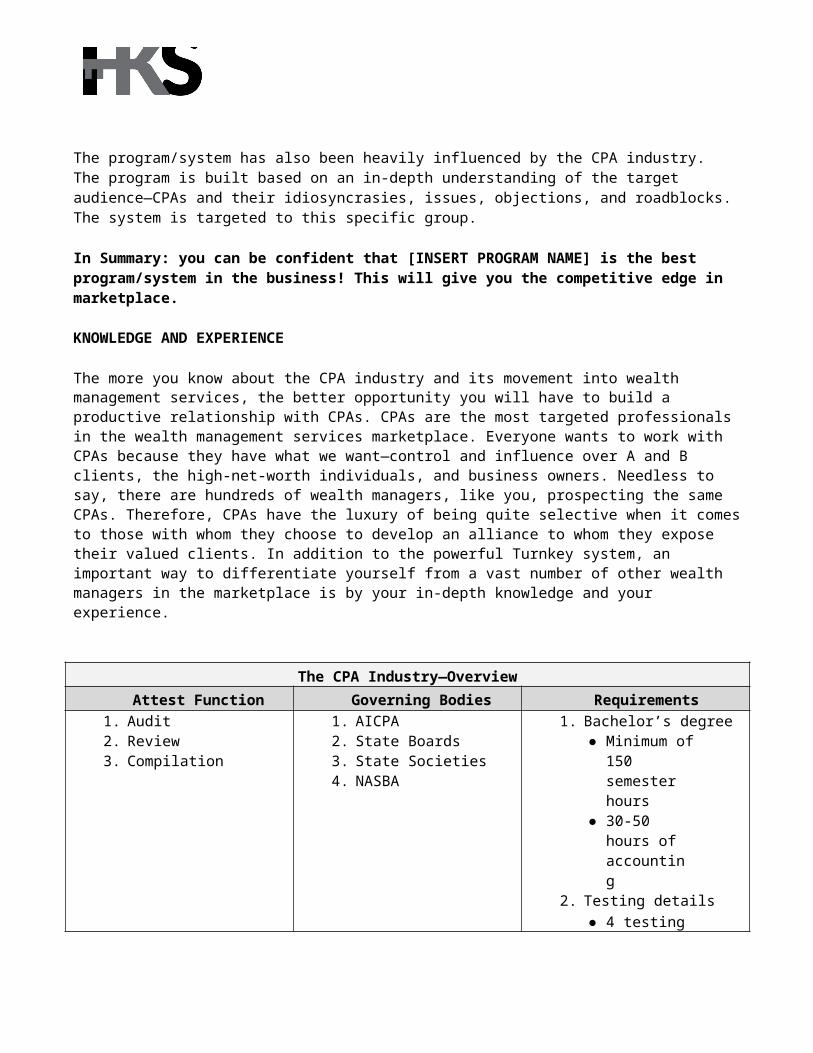

The program/system has also been heavily influenced by the CPA industry. The program is built based on an in-depth understanding of the target audience—CPAs and their idiosyncrasies, issues, objections, and roadblocks. The system is targeted to this specific group.

In Summary: you can be confident that [INSERT PROGRAM NAME] is the best program/system in the business! This will give you the competitive edge in marketplace.

KNOWLEDGE AND EXPERIENCE

The more you know about the CPA industry and its movement into wealth management services, the better opportunity you will have to build a productive relationship with CPAs. CPAs are the most targeted professionals in the wealth management services marketplace. Everyone wants to work with CPAs because they have what we want—control and influence over A and B clients, the high-net-worth individuals, and business owners. Needless to say, there are hundreds of wealth managers, like you, prospecting the same CPAs. Therefore, CPAs have the luxury of being quite selective when it comes to those with whom they choose to develop an alliance to whom they expose their valued clients. In addition to the powerful Turnkey system, an important way to differentiate yourself from a vast number of other wealth managers in the marketplace is by your in-depth knowledge and your experience.

The CPA Industry—OverviewAttest Function Governing Bodies Requirements

1. Audit2. Review3. Compilation

1. AICPA2. State Boards3. State Societies4. NASBA

1. Bachelor’s degree● Minimum of

150 semester hours

● 30-50 hours of accounting

2. Testing details● 4 testing

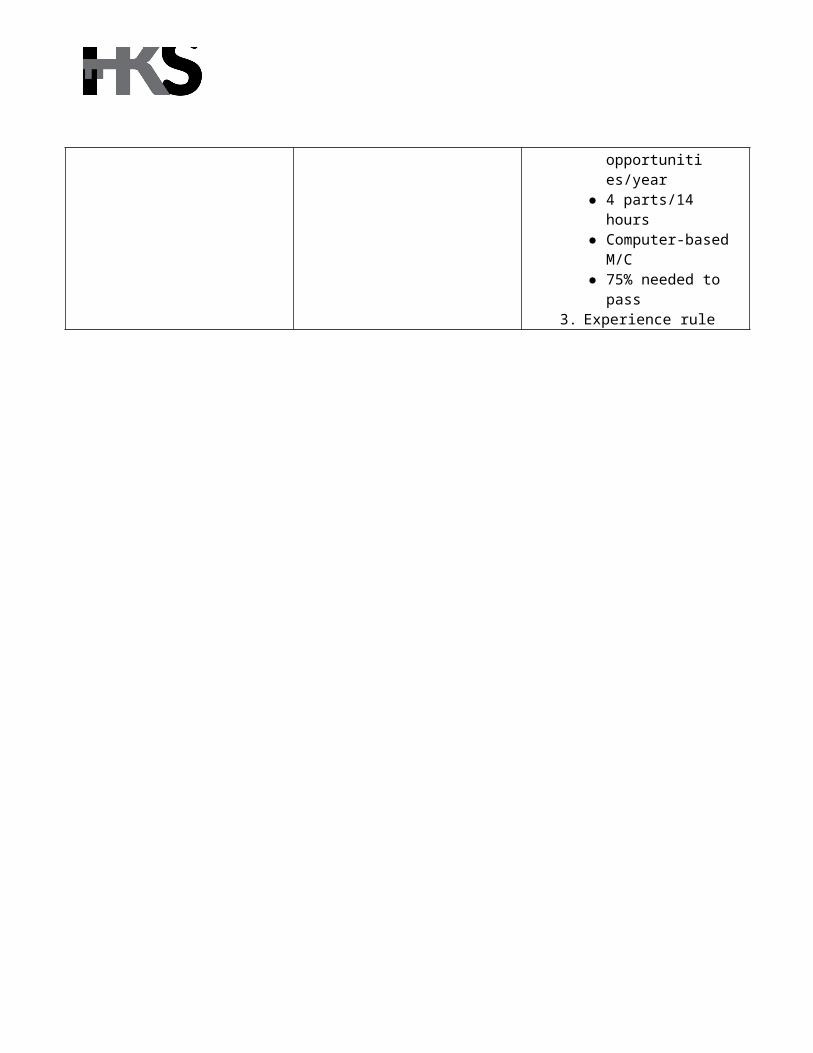

opportunities/year

● 4 parts/14 hours● Computer-based

M/C● 75% needed to pass

3. Experience rule

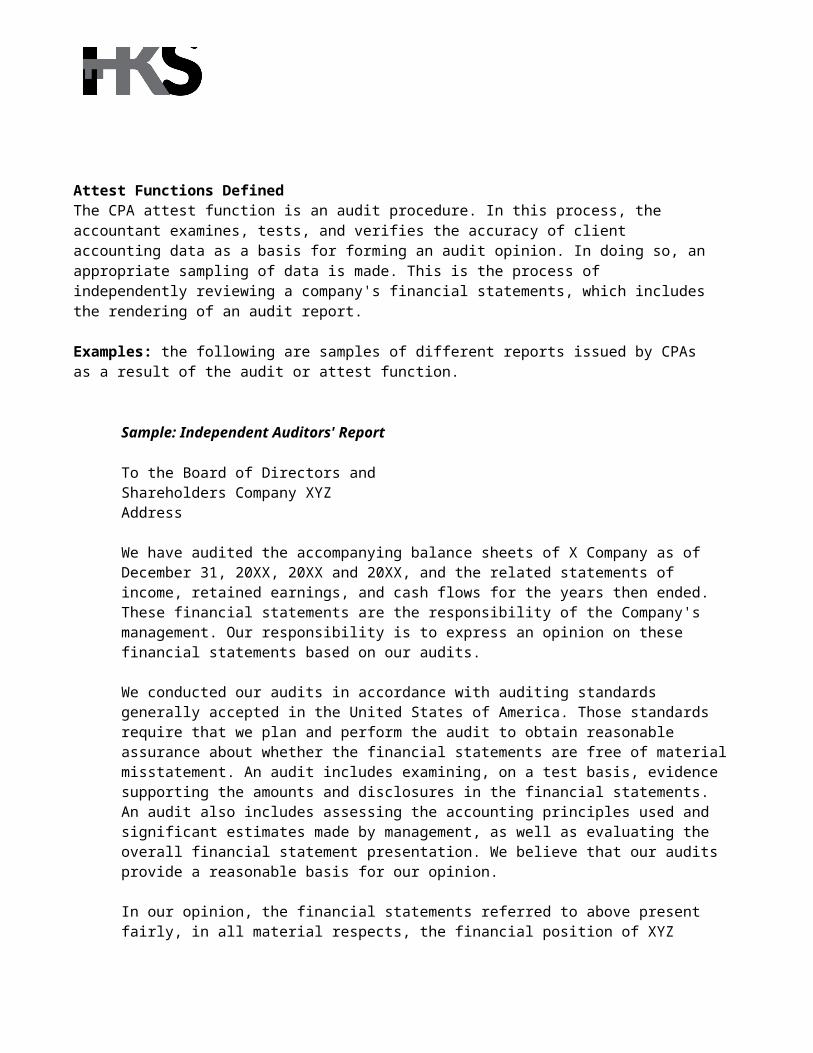

Attest Functions DefinedThe CPA attest function is an audit procedure. In this process, the accountant examines, tests, and verifies the accuracy of client accounting data as a basis for forming an audit opinion. In doing so, an appropriate sampling of data is made. This is the process of independently reviewing a company's financial statements, which includes the rendering of an audit report.

Examples: the following are samples of different reports issued by CPAs as a result of the audit or attest function.

Sample: Independent Auditors' Report

To the Board of Directors and Shareholders Company XYZAddress

We have audited the accompanying balance sheets of X Company as of December 31, 20XX, 20XX and 20XX, and the related statements of income, retained earnings, and cash flows for the years then ended. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of XYZ Company as of December 31, 20XX, 20XX and 20XX, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

(Signature)

(Date)

Sample: "Review" Opinion Letter

Date

To the Board of Directors and Shareholders Company XYZAddress

We have reviewed the accompanying balance sheet of Company XYZ as of December 31, 20XX, 20XX and 20XX, and the related statements of operations, retained earnings, and cash flows for the years then ended, in accordance with statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. All information included in these financial statements is the representation of the management.

A review consists principally of inquiries of company personnel and analytical procedures applied to financial data. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements in order for them to be in conformity with generally accepted accounting principles. Our review was made for the purpose of expressing limited assurance that there are no material modifications that should be made to the financial statements in order for them to be in conformity with generally accepted accounting principles. The information contained in the accompanying schedules of sales, cost of sales, and operating expenses is presented for supplementary analysis purposes. Such information has been subjected to the inquiry and analytical procedures applied in the review of the basic financial statements, and we are not aware of any material modifications that should be made thereto.

Sample: Compilation Letter

Date

Board of Directors of Company XYZ Address

We have compiled the accompanying statement of financial position of Company XYZ, as of June 30, 20XX, 20XX and 20XX and the related statements of income and cash flows for the years then ended, and the accompanying supplementary schedule of cost of sales and operating expenses, which are presented only for supplementary analysis purposes, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants.

A compilation is limited to presenting, in the form of financial statements and supplementary schedules, information that is the representation of management. We have not audited or reviewed the accompanying financial statements and supplementary schedule and, accordingly, do not express an opinion or any other form of assurance on them.

Management has elected to omit (substantially) all of the disclosures required by generally accepted accounting principles. If the omitted disclosures were included in the financial statements, they might influence the user's conclusions about the Company's financial position, results of operations, and its cash flows. Accordingly, these financial statements are not designed for those who are not informed about such matters.

Governing Bodies in Greater Detail

AICPA—American Institute of Certified Public AccountantsThe American Institute of Certified Public Accountants (AICPA) is the national, professional organization for Certified Public Accountants. Its mission is to provide members with the resources, information, and leadership that will enable them to provide valuable services, in the highest professional manner, to benefit the public as well as employers and clients. In fulfilling its mission, the AICPA works with state CPA organizations and gives priority to those areas where public reliance on CPA skills is most significant.

SBA—State Boards of AccountancyThe Board is responsible for licensing and regulating Certified Public Accountants (CPAs) and Public Accountants (PAs) in each respective state. The mission of each state Board of Accountancy is to protect the public by regulating the practice and performance of all services provided by licensed accountants.

SS—State Societies of CPAs The state societies are committed to helping CPAs build and maintain their professional reputation. Membership provides:

● Continuing professional education● Professional recognition● Networking opportunities● Governmental representation at the local and national level● Leadership development● Professional updates● Personal and professional development

NASBA—National Association of State Boards of Accountancy The National Association of State Boards of Accountancy (NASBA) serves as a forum for the all boards of accountancy. NASBA's mission is to enhance the effectiveness of state boards of accountancy. NASBA's goals are to:

● Provide high-quality, effective programs and services.● Identify, research, and analyze major current and emerging issues affecting state boards of

accountancy.● Strengthen and maintain communications with state boards to facilitate the exchange of ideas

and opinions.● Develop and foster relationships with organizations that impact the regulation of public

accounting.

NASBA sponsors a variety of programs and services designed to help us meet our mission and goals. Nobile Wealth Management is an NASBA sponsor, which allows us to provide Continuing Professional Education (CPE) to CPAs.

Where to Go to Gain More Knowledge

1. gotohank.com2. Industry publications

a. Accounting Todayb. Journal of Accountancyc. CPA Leadership Reportd. Financial Planninge. Registered Repf. Investment Advisor

3. Informational Web sites/governing bodiesa. www.AICPA.org b. www.NASBA.org c. Each state society Web site (access via AICPA.org)d. Each board of accountancy Web site (access via AICPA.org)

4. Uniform Accountancy Act (UAA)—find at AICPA.org5. Competitors programs

a. HD Vest—www.hdvest.comb. 1st Global—www.1stglobal.comc. Money Concepts—www.moneyconcepts.comd. Trusted Advisors—www.trustedadvisors.come. CEG Worldwide—www.cegworldwide.com

6. CPAs and accountants themselves

SECTION 4: CPA PROSPECTING ANDFORMALIZING THE RELATIONSHIPWHERE TO FIND CPAS TO WORK WITH

Finding CPAs and other professionals to approach is not difficult. There are over 400,000 CPAs in the marketplace and even more accountants and enrolled agents. There are many ways to meet and establish relationships with these professionals; however, like any type of prospecting, some methods are more effective than others. The following outlines several approaches for finding CPAs (or other professionals) with whom to form an alliance. These are listed in order of effectiveness:

The most effective ways to find CPAs (or other professionals) with whom to form a strategic alliance are:

● First, approach CPAs with whom you already have a relationship. The most effective way to establish a business alliance with a CPA or other professional is by drawing upon relationships you already have. The warmer the relationship, the easier it is to get an appointment and the easier you will be able to establish a relationship. The Turnkey System provides phone scripts to help you obtain the initial appointment with the CPA. Tailor it to your personality and the personality of the professional you are going to approach.

● Second, connect with CPAs of your top clients. If you don’t have any relationships to draw upon, then build on centers of influence to obtain a recommendation. Simply call your A and B clients, find out who their CPA is, and tell them you’d like to call the CPA to set up a time to meet with him or her. Have the client either call the CPA or at least write a note of recommendation on your bio pamphlet to precondition the professional before you call. The Turnkey System also provides phone scripts to assist you in obtaining the initial appointment with the CPA.

● Third, attend CPA association meetings. Whether it’s a local event of the AICPA or an event like a Gear-Up seminar where CPAs can obtain CPE credit, there are many association meetings where you can introduce yourself to CPAs and other professionals. Of all the “cold sourcing,” this is the most effective way to meet many CPAs.

For example, Gear-Up is an organization that holds CPE seminars/courses throughout the United States. These are well attended events—sometimes hundreds of CPAs will attend. You can arrange to become one of the sponsors of the event, which would allow you to set up the [INSERT PROGRAM NAME] display and follow the process outlined in the Turnkey System to help you create interest and future meetings with CPAs.

● Fourth, hold CPE seminars. The Turnkey System provides a two-hour workshop that has been approved for up to two hours of continuing education credit for CPAs. This workshop

outlines the direction the CPA industry is taking regarding financial services, the different approaches being utilized, examples of financial firms involved, the keys to success, and briefly introduces [INSERT PROGRAM NAME] as an example of a system that harnesses the key components of success that the seminar outlines. The wealth manager and/or branch office sponsor these seminars. CPAs receive these types of offers often, so there may not be large turnout. However, in our experience, those who do attend become very interested in signing up. Setting a date for a seminar and inviting the warm or cold leads you have developed is usually a more effective approach than sending out random invitations.

● Fifth, cold call CPAs. As you would imagine, this is the least effective of prospecting approaches, but it is still a viable option. The Turnkey System provides a calling script for this process, though we do not provide a calling list. However, you can purchase mailing lists containing the names of CPA firms, and you can start calling on them either on the telephone or in person.

HOW TO APPROACH THEM

Remember, CPAs and other accounting and tax professionals are heavily prospected by wealth managers. So the warmer the relationship, the easier time you will have obtaining an appointment. The Turnkey System provides a sample phone script for you to use in tailoring your own approach. If you and a CPA share a common client, spend some time selling the client on the concept of having the CPA more involved in his or her overall planning process. Ask your client to call the CPA or write a letter explaining their interest in having the CPA partner with you. See the example below:

Note: you can also use the CPA pre-approach letter. You would write a letter to the CPA and have the client simply write a note of introduction, urging the CPA to meet with you.

HOW TO DEVELOP THE ALLIANCE AND SECURE A PRODUCTIVE WORKING RELATIONSHIP

In our experience, it is not particularly difficult to get CPAs and other professionals interested in forming a strategic alliance. Getting them actually engaged in the process is another story. This section is designed to help you move prospective allies into active engagement with the process.

1. Clearly paint the vision2. Be bold3. Ongoing dialogue and education4. Provide the final push to commit the CPA5. Getting the CPA licensed6. Provide continual follow through

Clearly Paint the VisionThe more clearly CPAs can see what you’re describing, the more apt they are to stay on track. Help them understand the financial impact that adding wealth management services can have on their practice and way of life by setting specific goals with them. For example, if a CPA has gross annual billings of $1,000,000, help him or her understand the financial impact of adding wealth management services by using the [INSERT PROGRAM NAME] benchmark of 10–20 percent—the following example uses 15 percent.

15 percent of $1,000,000 of gross billings = $150,000

Write down $150,000 as the potential additional revenue your alliance can generate for the CPA’s practice. Keep this figure in front of the CPA throughout your discussions. It’s also helpful if you share with CPAs some of the success stories you’ve experienced with other CPAs, so these financial outcomes become realistic to them.

Be BoldOnce CPAs commit to the program, be bold and ask if you have their permission and authority to drive the process until their system is up and running. An example of this request follows:

“Now that we are in agreement about moving forward, do I have your permission, to drive this process to ensure we hit our key milestones and benchmarks?” Then follow up with, “that means I will be calling to follow up and assist you in completing each of the items you’ve committed to. Are you okay with that?”

Ongoing Dialogue and EducationBe prepared to further educate CPAs on the process of adding wealth management services. This may include:

1. Competitors. It may be helpful to talk to prospective CPA allies about the competition or invite them to review systems that compete with our program.

2. Build financial value for the CPA firm and build CPA exit strategies. Help CPAs

understand that building a wealth management services arm for their firms will increase its value for a potential future buy-out. Explain different scenarios where, through your alliance, you will be able to enhance the quality of a CPA’s retirement.

Provide the Final Push to Commit the CPA

Even after completing all of the steps outlined, you may still need to provide additional support before the CPA is finally ready to move from the concept to fully committed ally. Ways to do this include:

1. Client Survey. Studies continue to suggest that the general public would prefer to have CPAs act as quarterbacks for their wealth management planning. Not all CPAs believe that these studies apply to their clients. If this is the case, tell the CPA to ask the clients themselves. They can do this in two ways:

a. Client survey template. Using the Client Surveys found in The Turnkey System has been incredibly effective—especially when used in face-to-face meetings. The process is simple. Train the firm’s assistant to hand every client who walks in the door a clipboard with a Survey on it. The Survey is broad enough that it is a very safe way to ask the client’s opinion on whether or not he or she would like the CPA to begin offering wealth management services. Once completed, have the client take the Survey into the meeting with the CPA. The CPA conducts the meeting as usual then takes the final five minutes to review the Survey with the client. The CPA can then explain why adding wealth management services may be advantageous for clients and can also ask the client to expand a little bit on his or her Survey answers.

b. Phone survey. Have the CPA or office assistant call a sampling of clients (have the CPA call the top 10 clients) and ask these clients the same Survey questions.

2. Ten and then. Begin on a trial basis. Have the CPA bring in ten clients you can provide wealth management services for. The CPA can be involved in the process at whatever level the two of you determine. The goal is to have the CPA witness your process in action and to demonstrate that you are a trustworthy, competent, and amiable professional who will add exceptional value to the CPA’s client relationships. These ten clients should also include the CPA and his or her partners. When they recommend that their clients come in for wealth management consulting, they need to speak from experience. They will be able to provide an endorsement that is based on their own experience with you and your process.

Getting the CPA LicensedThis is a difficult step that is the chief stumbling block for many CPAs. For new wealth managers coming into this industry, there is plenty of motivation to get their exams passed and licenses established because they don’t get paid until they do. CPAs are already earning incomes they are fairly comfortable with, so they don’t always have a sense of urgency about obtaining their license. They like the idea of additional income, but it’s a bonus, not usually a staple in most cases. The following are several ways you can help CPAs through this process:

1. Schedule all classes, tests, and study schedules. Deadlines are some of the most effective motivators. When you’re mapping out the launching process with the CPA, provide a calendar

for scheduling the dates for classes the CPA should take. List the actual exam dates as well. Tell the CPA that you will call the testing center (or help the CPA’s assistant do it) and schedule the exams. You can also help by establishing a study schedule and working with your [INSERT BROKER-DEALER] to obtain necessary study materials.

2. Leverage Licensing. When you are ready for the CPA to get started, contact the [INSERT BROKER-DEALER] registration unit. They will provide you with the appropriate forms to get the licensing process started.

3. Create Incentives. Ideas for effective incentives include offering to pay a portion of the CPA’s licensing fees if the defined timelines are met. You could create different incentive levels, e.g., paying 75% if exams are completed on time; 50% if completed within a broader window, and no reimbursement if completed outside the defined window of time.

Continual Follow ThroughOnce you’ve obtained permission and authority to push the process along, use it. Set up a weekly meeting where you not only provide additional education, but you also help them continue to maintain forward momentum with the set-up process, and follow up on previous assignments and study progress. This weekly meeting sets the pattern for holding regular Financial Planning Days at the CPA’s office. Utilize the CPA Launch Checklist to ensure that you don’t skip any important steps in the process of launching this alliance. Use your staff and the CPA’s staff to keep things in motion both during the launch phase and when the alliance is in full motion.

SECTION 5: THE CPA IS ON BOARD—NOW WHAT?INTRODUCTION

This system is built upon more than 20+ years of experience consulting with financial professionals and CPAs (plus other professionals)—thousands of financial professionals and CPAs across the United States. As you prepare to capitalize on this tremendous opportunity, keep in mind that getting a CPA or other professional to agree to form an alliance with you is the easy part of the process. Once you’ve reached this point, the real work is just beginning—remember these important points:

1. CPA relationships are good, but business development is great! Over the years we have seen many CPA/advisor relationships developed. Obviously, the purpose of strategically aligning with CPAs is to build successful and profitable business relationships. But sometimes advisors develop a false sense of accomplishment when a CPA or attorney agrees to form an alliance with them, even when they have little to show for their efforts. It may feel good to have a relationship on the books, but unless it is a productive one, you are wasting valuable time and resources. Remember that the ideal alliance with a CPA is one that produces exceptional results.

2. Getting the CPA on board is the beginning of the process, not the end. Getting CPAs to add wealth management services to their practices is getting easier. When compared to the past, CPAs are becoming more and more receptive to the idea of offering wealth management services to their clients. In addition, they are realizing that co-sourcing with other professionals is the right way to do it. But the real work doesn’t begin until after the CPA agrees to form an alliance. Therefore, in order to maximize the opportunity, you must execute the key elements of the Turnkey System. Follow the multi-step process: Practice Profile, Client Segmentation, Marketing Plan, Financial Services Integration and practice management with checks and balances. Be assured that The Turnkey System is proven, practical, and profitable.

3. Regularly get the CPA’s permission and authority to move things along. In order to move things along at an acceptable pace, you must take the lead and drive the process. So get the CPA’s permission and authority to do so. It’s important to ask the CPA, “Do I have your permission to drive this process to ensure we move things along?” Most likely you have partnered with a successful, yet very busy CPA. The newly formed wealth management division or offering will not necessarily be a priority for the CPA from the beginning. So, if you don’t take the lead and move the CPA along, this may be a long and frustrating process. Get the CPA to a point where he or she gives you the permission and authority to move the process forward every step of the way.

4. Clearly articulate that this is a business not a hobby. It is important to set the ground rules. Clearly articulate to the CPA that this alliance and adding wealth management services to the

practice will be treated like a business not a hobby. There is no time to dabble and simply go through the motions. Setting goals, developing a marketing plan, implementing specific action items, and monitoring results are expected. [INSERT FIRM NAME] is not interested in “hobby” relationships, and we are quite certain that you, the CPA, are not interested in anything less than a professional “business” relationship. If treated like a real business, the client will be the ultimate beneficiary.

5. Strive to obtain early results ($$$ and satisfied clients). Fast starts are important in any business. The goal to obtain early results will better solidify the relationship and keep the CPA engaged and excited. The two most important goals are to deliver a great experience to the CPA’s valued clients and to put money into the CPAs pocket. Satisfied clients will confirm to the CPA that he or she is doing the right thing.

6. Service, support, and spoil the CPA and their clients. Everyone wants to work with CPAs. Therefore, CPAs have the luxury of picking and choosing whom they want to work with and to whom they will expose their key clients. It is very important that your service is outstanding, that you keep CPAs educated and informed at all times, that you continually demonstrate integrity and professionalism, and that you treat their clients like gold. If you are willing to do this, you will ensure long-term success with your CPA relationships.

7. Do not overextend yourself. The opportunity is so great that most advisors are tempted to find and work with as many CPAs as possible. Our advice to you is focus on quality not quantity. We would suggest that you approach several CPAs with the intention of securing 5 key CPAs to work with. For now, the goal is to have these alliances/partnerships complement your existing business model. Continue to perfect your current business model, while allocating 20-25% of your time to working with CPAs and other professionals. Manage your growth appropriately so that you can be in a position to deliver on your promises.

8. Be willing to tap expertise as necessary. It is common knowledge that no one can be all things to all people. You can’t possibly be an expert in all areas of the wealth management services business. Therefore, your position with the CPA should be two-fold: 1) to serve as an expert in some areas and 2) to become a financial quarterback in other areas by engaging other professionals who have the necessary expertise. The CPA will take great comfort in the fact that the partnership is based upon you and your team of experts. The team approach is always better for the client.

9. Have patience, it takes time. It would be wonderful if we could tell you that success will be immediate, and in some cases results may come early. But for the most part it will take time—time in the prospecting stage as well as the business development stage. This proven turnkey system is truly an exceptional client acquisition program. If done right, The Turnkey System is one of the most cost-effective and efficient programs in the marketplace for getting in front of ideal prospects—A and B clients, high-net-worth individuals/families, and business owners. When successfully implemented, you’ll be able to meet with these people on a favorable basis that is endorsed by the number one ranked professional advisor in the consumer marketplace, the CPA. Expect that it will take 12-18 months to make significant progress. It may come faster than that, but be realistic. The time and energy you put forth will pay big dividends.

10. Follow the system; it’s proven, practical, and profitable. To maximize the opportunity and

experience the full benefits of the program, follow the system. It was developed, enhanced, and perfected by CPAs for CPAs. Most other financial organizations have CPA/advisor alliance programs, but nothing compares to The Turnkey System. If you try to re-create the wheel, you may have some success, but most likely you will not fully capitalize on its full potential. Remember that the Turnkey System is a proven, practical, and profitable business development system:

Proven—It has a long and documented track record of success. (Nothing speaks louder.)Practical—It can be implemented and executed without materially disrupting the CPA’s everyday business. (Overcoming TESD)Profitable—It can substantially enhance financial results for both participants. (CPA and Advisor)

WEALTH MANAGEMENT SERVICES INTEGRATION—THE MODEL ALLIANCE

Getting the CPA firm to this point has taken some time, but it has been relatively easy. You have had several productive meetings, the CPA firm has gone through the profiling process, and the decision has been made that a strategic alliance is worth pursuing. It is important to understand that the CPA firm is offering the wealth management services. You are a hand-selected team member, the backroom technician, and an extension of the practice. Always position the CPA as the “financial quarterback.”

THE IDEAL ALLIANCE LOOK LIKE THIS

1. The CPA agrees to treat the alliance like a business not a hobby.2. The CPA feels comfortable and confident in offering wealth management services.3. The CPA obtains the appropriate licensing.4. The CPA physically sets up space for the wealth management services business.5. The wealth manager has one day each week that is set aside as Financial Planning Day.6. The CPA and his or her staff fill each Financial Planning Day with appointments with A, B, or

C clients.7. The wealth manager and CPA meet quarterly to review the progress of the alliance and

make any adjustments necessary to improve process and results.

BUSINESS DEVELOPMENT IS THE END GAME

There is a false euphoria that arises when a wealth manager establishes a CPA alliance, as if simply getting a CPA to commit to work with you actually accomplishes something of significant value. This is a big step, but obviously the true measuring stick of success is actually meeting with the CPA’s clients and implementing solutions for them. Consider the following concepts as you do this:

1. Cherry picking vs. sustainable growth.2. Organizing around problems.3. Educating the CPA.4. Utilizing marketing resources and the Advanced Markets and Professional

Development team.

Cherry Picking vs. Sustainable GrowthThe cliché of this industry is that a new advisor comes into the career, sells his friends and family, and then is washed up within six months. Sound familiar? Unfortunately, CPAs and other professionals can follow this same pattern unless the alliance is managed effectively. Often, when advisors first form the alliance with a CPA, the CPA will undoubtedly have some low-hanging fruit that can produce substantial results. Without a specific game plan this fruit will dry up, and soon it will be business as usual for the CPA.

The key to avoiding this trap is the Marketing and Business Plan. Take the time to fully utilize this marketing template. It will mean the difference between a flash-in-the-pan alliance vs. a long-term profitable alliance.

Organize Around ProblemsIt is important to understand that marketing does not come naturally to typical CPAs. They are not salesmen, nor do they want to be perceived as salesmen. Most have little, if any, experience with marketing—many of them built their clienteles by either purchasing a mature practice from another CPA (which includes the book of clients), or they were hired by a CPA firm that already had an established clientele, and they eventually worked their way up the latter until they became partners. Once established in the profession, CPAs generally obtain new clients by word of mouth, rather than through active marketing programs. Therefore, the thought of calling clients to invite them for a financial consultation, combined with the fact that they may still have lingering doubts about how their clients will perceive their intentions once they begin receiving commissions, can be very disconcerting.

So how do you handle this obstacle? One way is for CPAs to focus on the problems of their clients. Remember, one of the key reasons CPAs are interested in adding wealth management services is to better serve their clients. So help them serve their clients by educating CPAs about the different financial problems that could seriously affect their clients’ financial well-being. If CPAs were to call clients and suggest that they set up an appointment because wealth management services are now offered in their practices, they may feel awkward. However, CPAs will feel much more comfortable calling their clients about wealth management strategies that could significantly reduce or eliminate the income and/or estate taxes those clients have to pay [e.g., providing estate strategies, offering single-premium life insurance, or setting up a 412(e)(3) plan]. Create a list of core problems that you are an expert at solving, and focus your CPA alliance development endeavors on educating CPAs and helping them with marketing efforts. The more you focus on problems and resolving them, the less call reluctance CPAs may feel.

Important tools that can help with the problem resolution process include:

1. Client Financial Self-Assessment2. Business Owner Financial Self-Assessment3. Audit Brochure(s)4. 412(e) (3) Brochures5. SPL Brochures

Educate the CPAAnother key to developing business is to teach the CPA about the problems that their clients are facing. In some cases, you actually have to reformat a CPA’s financial understanding. In other cases, it

is simply a matter of teaching them new financial concepts, financial solutions, and management techniques.

CPA Roundtable meetings are another resource to help educate and motivate your CPAs. These meetings help provide an arena for them to learn about financial consulting opportunities and how to develop. Roundtables will be held three out of the four quarters per year.

KEY SUCCESS DRIVERS

1. Internal marketing vs. external marketing2. Creation of the Marketing Plan3. Action items that work

OFFICE SET-UP: ENSURING CLIENTS REMAIN COMPLIANT WITH AICPA, FINRA AND STATE INSURANCE DEPARTMENTS

An essential part of the alliance development process is helping CPAs avoid liability issues. CPAs are placing their trust in you. Liability is an area of concern and a reason many CPAs do not add wealth management services to their practices. The more you can do to alleviate this concern the better. Utilize the Compliance department at [INSERT BROKER-DEALER NAME].

SECTION 6: MAKING THE MOST OF THE TURNKEY SYSTEMAlliance Management, Accountability, and SupportESTABLISHING GOALS AND OBJECTIVES

Now that you have enrolled in The Client Acquisition Machine, we want to create every opportunity for your success. Just as we stress to CPAs that adding wealth management services to their practices can be a business driver, not a hobby, we say the same to you. Do not dabble in this!

Make the most of this system by harnessing all the tools, resources, coaching, and support available. We suggest that one of the most important steps you can take to ensure your success is to create the plan on paper before you implement it physically.

One of the most important steps for success is to outline YOUR business plan. There have been many wealth managers and CPAs who have shown great interest in this type of alliance and have had disappointing results or false starts. A chief reason for these disappointments is a lack of strategic planning that maps out the critical components for a successful outcome.

A thorough plan will help you precisely define where you are now and what you want to achieve. This will help you define specific strategies and action plans that help ensure you achieve your goals. An effective action plan should contain the following components:

1. Vision. What will your alliance(s) look like? How many CPA firms (or other professional firms) will you develop alliances with? How much time per week/month will you spend in a professional firm’s office conducting financial planning days? What will your support staff look and act like?

2. Needed resources. Identify all the resources you’ll need to optimize your time, so you spend your peak hours only on those activities that create revenues for your alliance. Consider the resources you already have and how you can better utilize them. Consider the resources inherent within CPA firms. And finally, outline the additional resources you will need to add or draw upon.

3. Marketing Plan. Create a list of potential CPA or other professional prospects and label them A, B, or C.

A—Current relationships. These you could easily contact because of the strength of your relationship with them.

B—CPAs referred by a center of influence. Based on the strength of the center of influence,

you have a good chance of getting an appointment.

C—Luke warm or cold. Make a list of CPAs you know either from your own contact or through others.

Once defined, outline your Marketing Plan. Determine how you will position the meeting—what you will say to them once you have them in a meeting, and how you will utilize the tools and resources of the Turnkey System to increase the probability your meetings will be successful.

4. Business Plan. The business plan brings everything together. Specifically, the Business Plan should contain the following components:

a. Business goals. Set specific goals and outline action plans that help ensure the goals will be achieved. Consider the following categories for your goals:

● Total commissions● Planning fees● Total assets under management● Residual income sources and amounts● Percentage of time spent with professional firms

b. Priorities. Rank your goals according to the areas that present the quickest and simplest return. By prioritizing, you can determine how to best allocate your resources and focus.

c. Action plan. Break down each goal or priority into specific steps that will lead to success. Remember, the more specific the step is, the stronger the possibility will be that you will accomplish it. Stay away from listing vague generalities such as “work harder.”

d. Set timelines. Every good plan has specific benchmarks and deadlines. Determine when each action must be accomplished in order to reach the goals you have envisioned.

MEASURING RESULTS

Know the scoreMonitor your progress toward your goals!!!

Wealth Manager reportingFor tracking purposes, use the CPA business tracking worksheets to keep track of all of the business coming from each CPA relationship. If the business came from a client of a strategic alliance (CPA or other professional), a referral from a client of a strategic alliance, or as additional business on a client who originally came to you from a strategic alliance, add it to the business tracking worksheets. Also, another effective way is to label them in your client relationship database.

ACCOUNTABILITY MEASURES

Ultimately, you’re accountable to yourself, but we’d like to help you in any way we can. Your success is our success. We are highly motivated to help you succeed in moving your practice to a much higher level. You can always reach us to gotohank.com.

![· Web viewAdvisor engages in [insert all activities that take place at location – client interactions, order entry, keeping of books and records, etc.] at the primary office](https://img.pdfslide.us/doc/110x75/5ae9beae7f8b9a585f8b717c/viewadvisor-engages-in-insert-all-activities-that-take-place-at-location-client.jpg)