Embed Size (px)

Citation preview

Agricultural Production Lending

A Training Toolkit for Loan Officers and Loan Portfolio Managers

2010

Revised version

Table of Contents

CONTENTS

Introduction...............................................................................................................................4Chapter 1: Agricultural Lending to Small Farmers........................................................7

1.1 From Directed Agricultural Credit to Rural Financial Market Development.....7

1.2 The Supply and Demand for Rural Lending...........................................................9

1.3 Lessons from Microfinance.....................................................................................10

1.4 Unique Features of Agricultural Lending..............................................................11

Chapter 2: The Challenges of Agricultural Lending....................................................132.1 The Risks...................................................................................................................13

2.2 The Costs..................................................................................................................18

2.3 The Loan Officer......................................................................................................20

Chapter 3: Basic Features of Agricultural Lending.....................................................233.1 Types of Agricultural Loan Products....................................................................23

3.2 Finding Good Customers.......................................................................................24

3.3 Understanding Agriculture.....................................................................................25

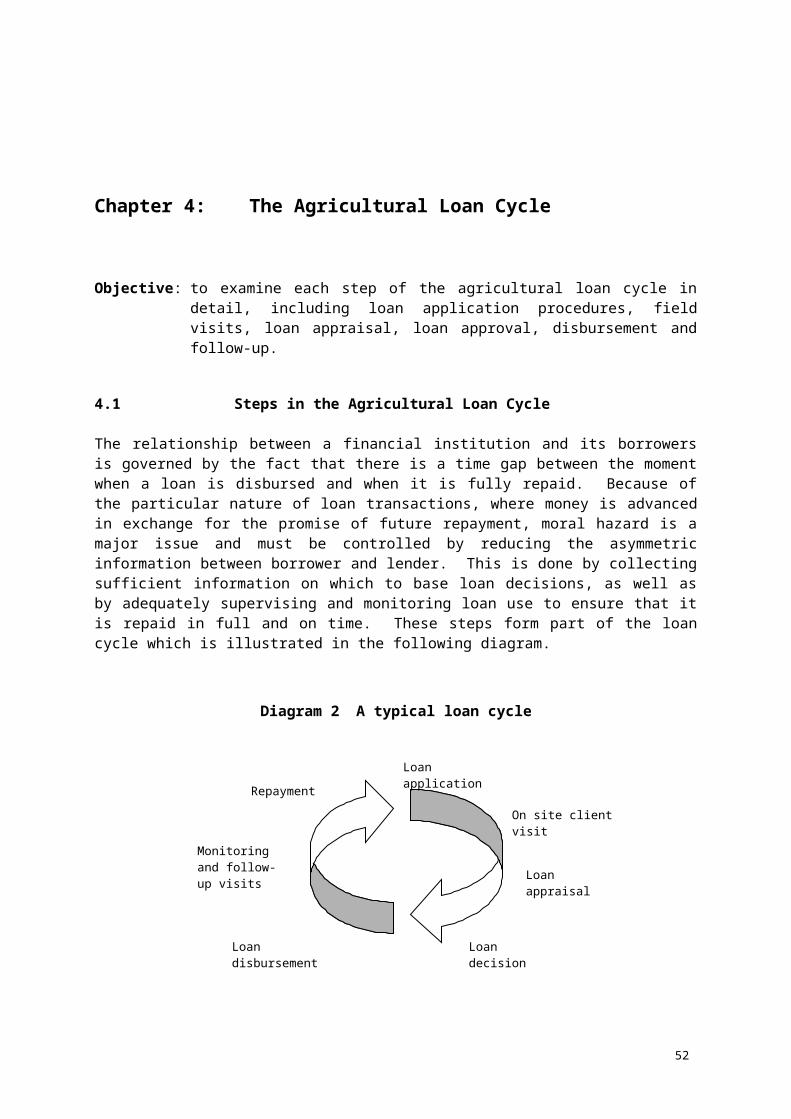

Chapter 4: The Agricultural Loan Cycle......................................................................334.1 Steps in the Agricultural Loan Cycle....................................................................33

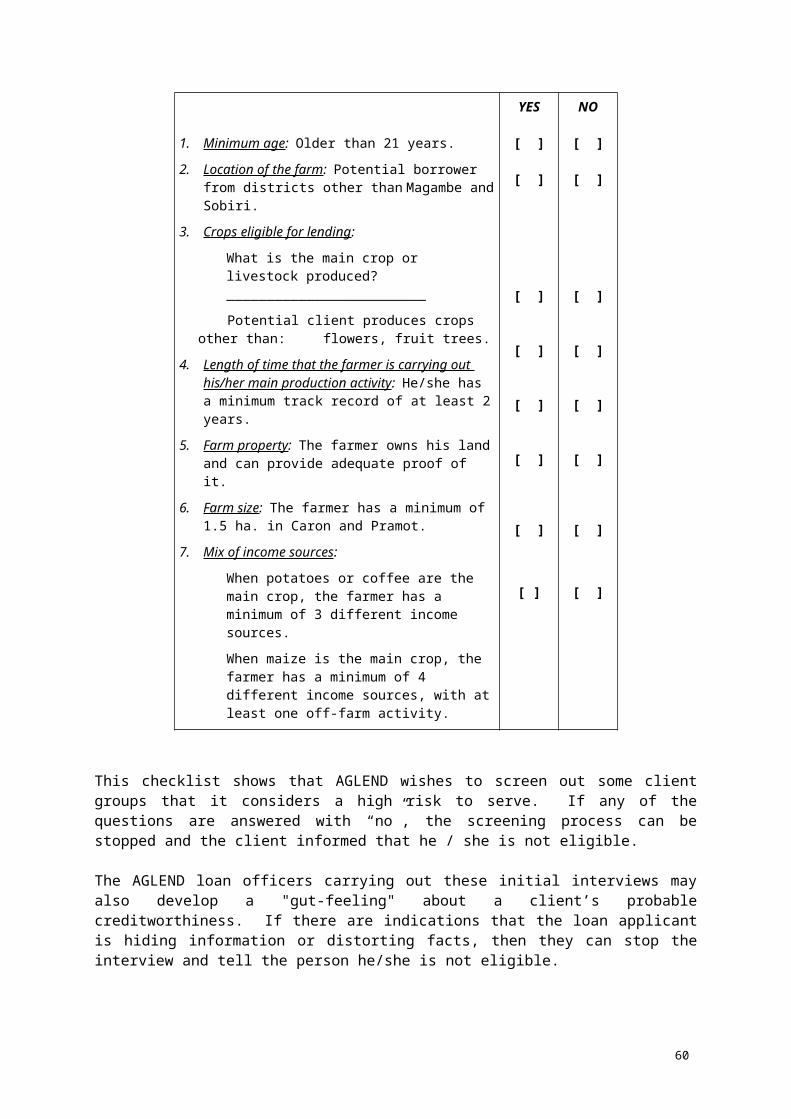

4.2 The Initial Screening of Loan Applicants.............................................................36

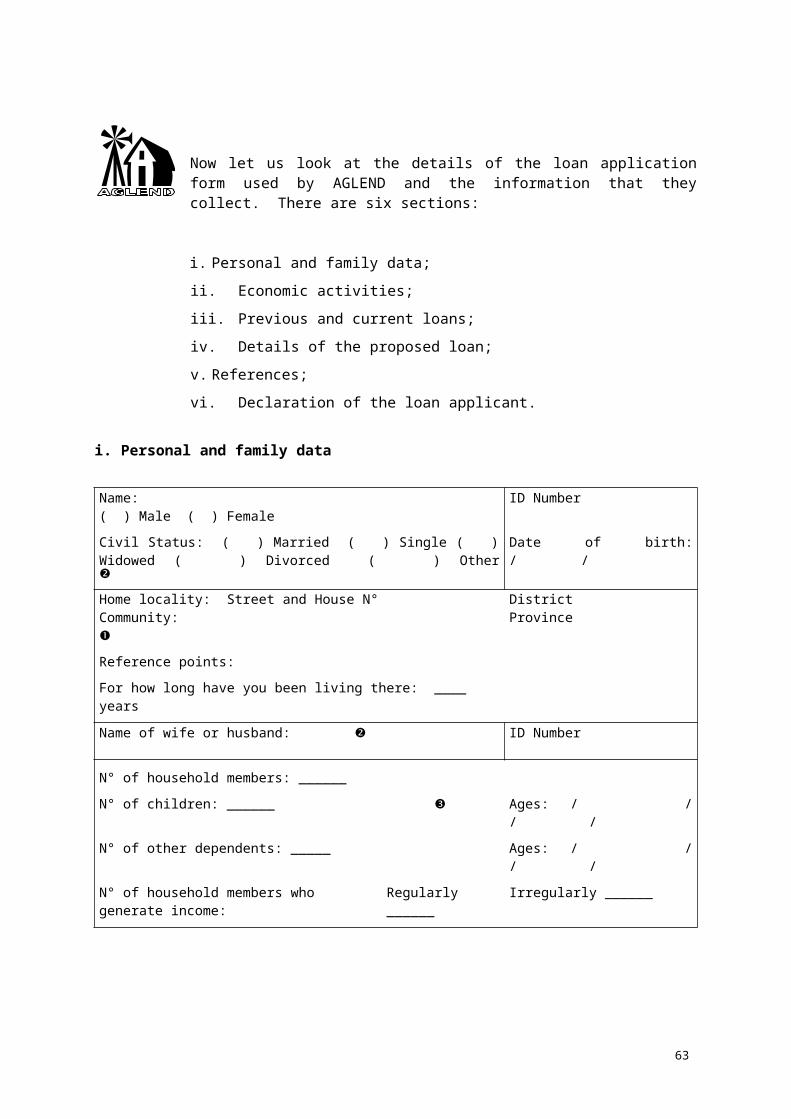

4.3 The Loan Application.............................................................................................39

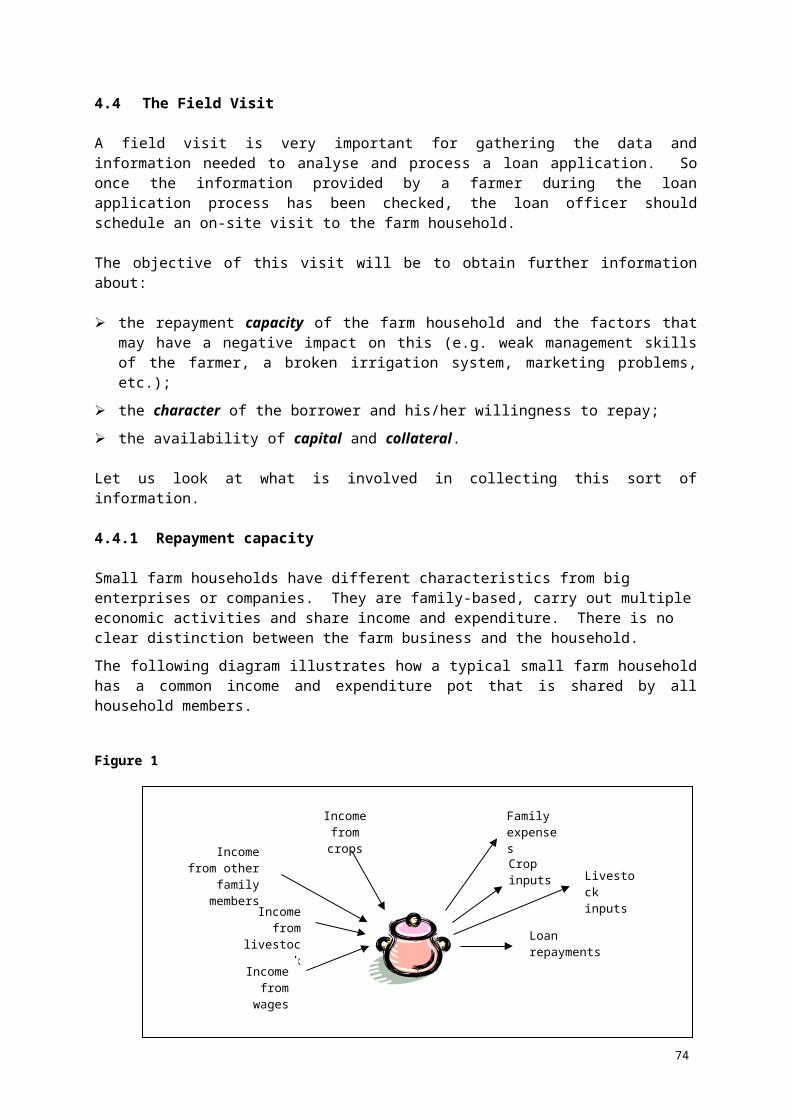

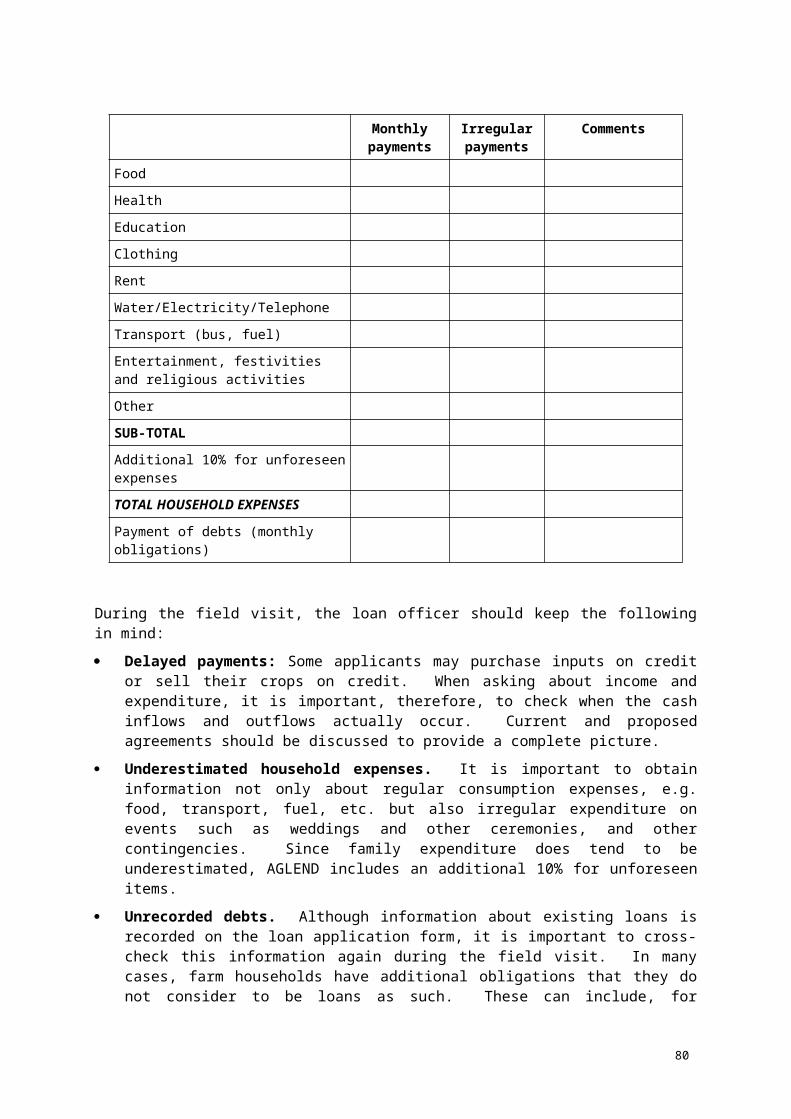

4.4 The Field Visit...........................................................................................................474.4.1 Repayment capacity...................................................................................................47

4.4.2 Character and willingness to repay a loan...............................................................54

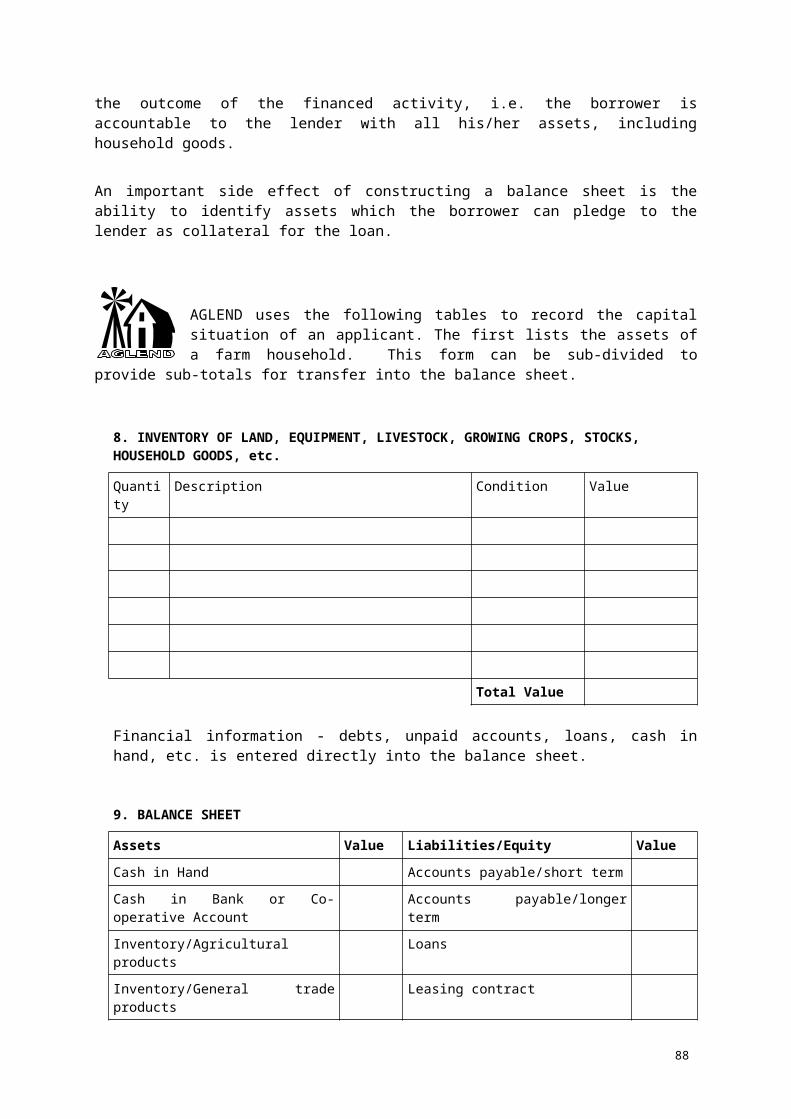

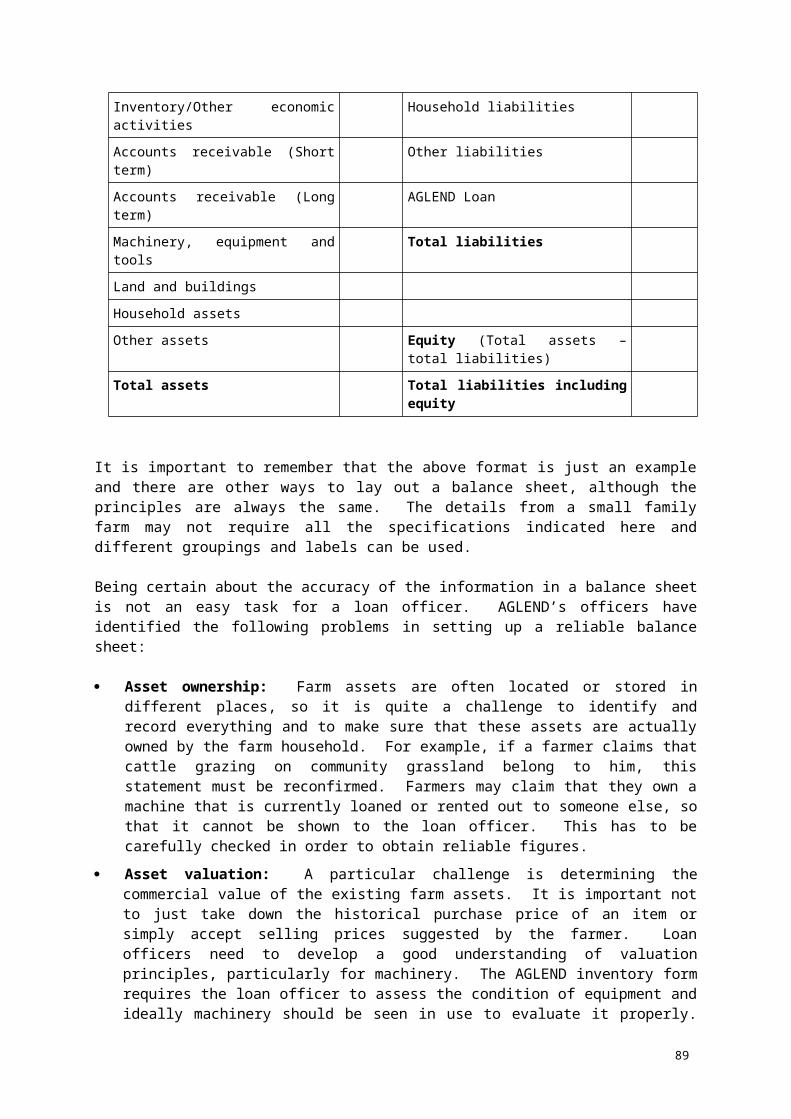

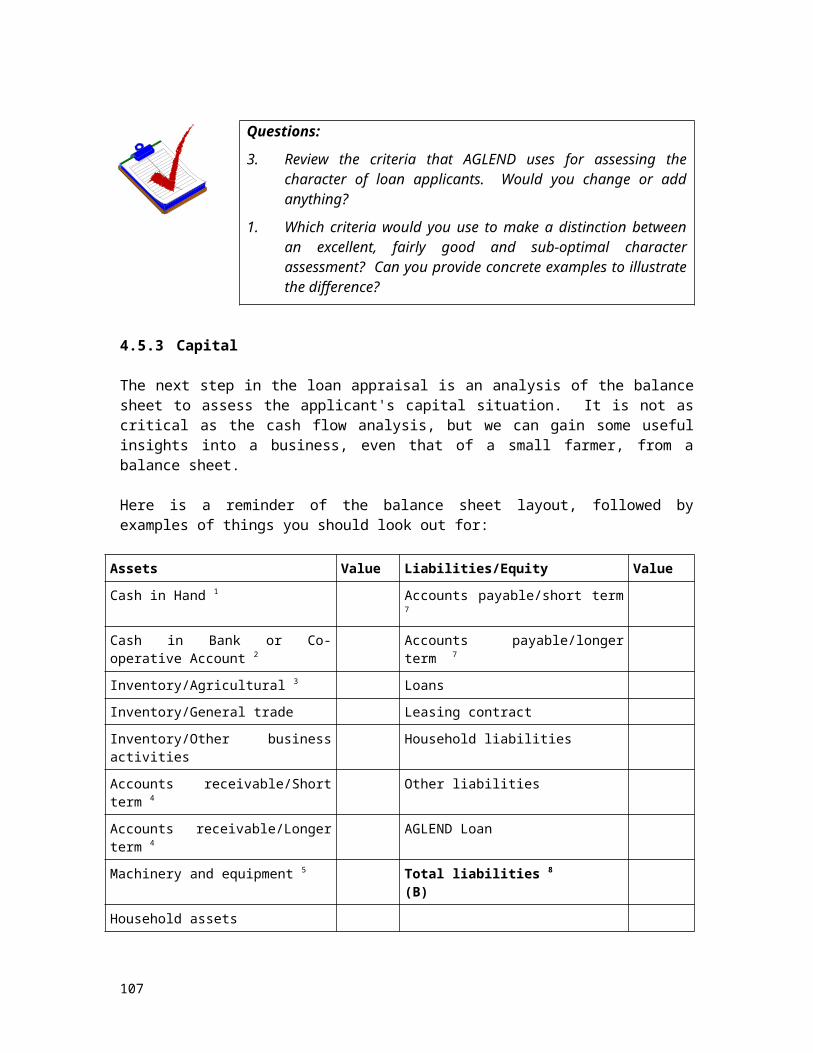

4.4.3. Capital and Loan Collateral......................................................................................55

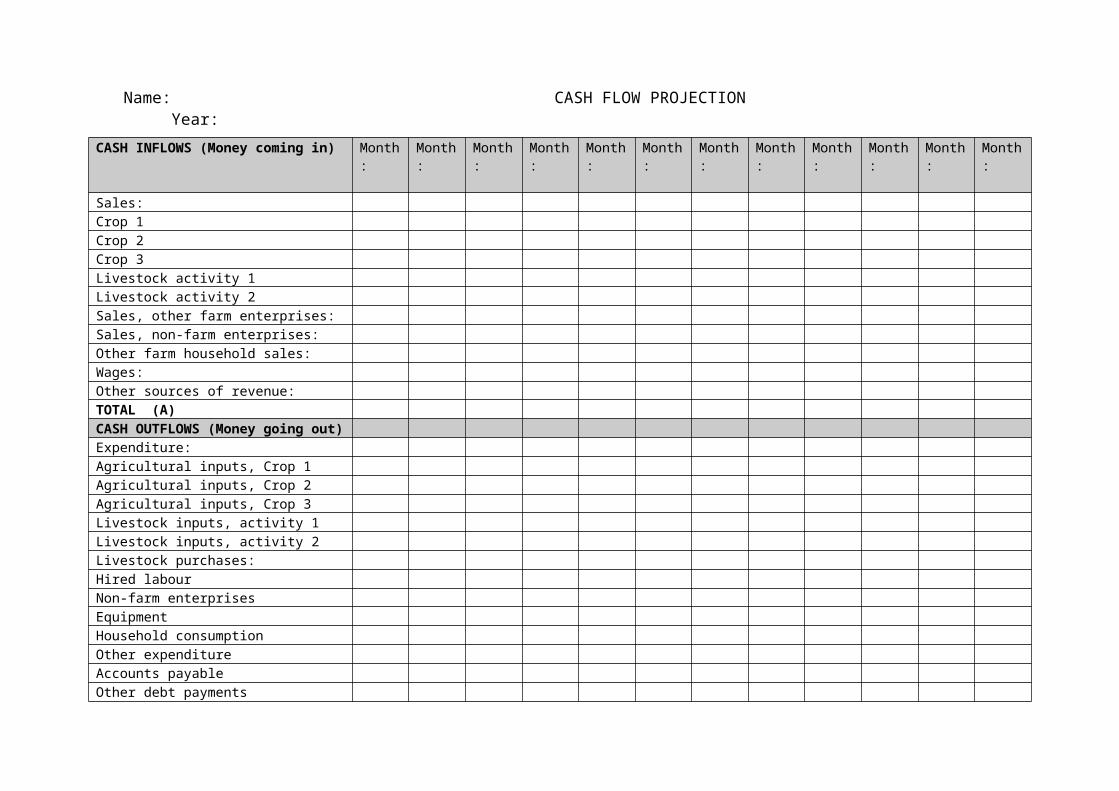

4.5 Loan Appraisal.........................................................................................................584.5.1 Repayment capacity...................................................................................................58

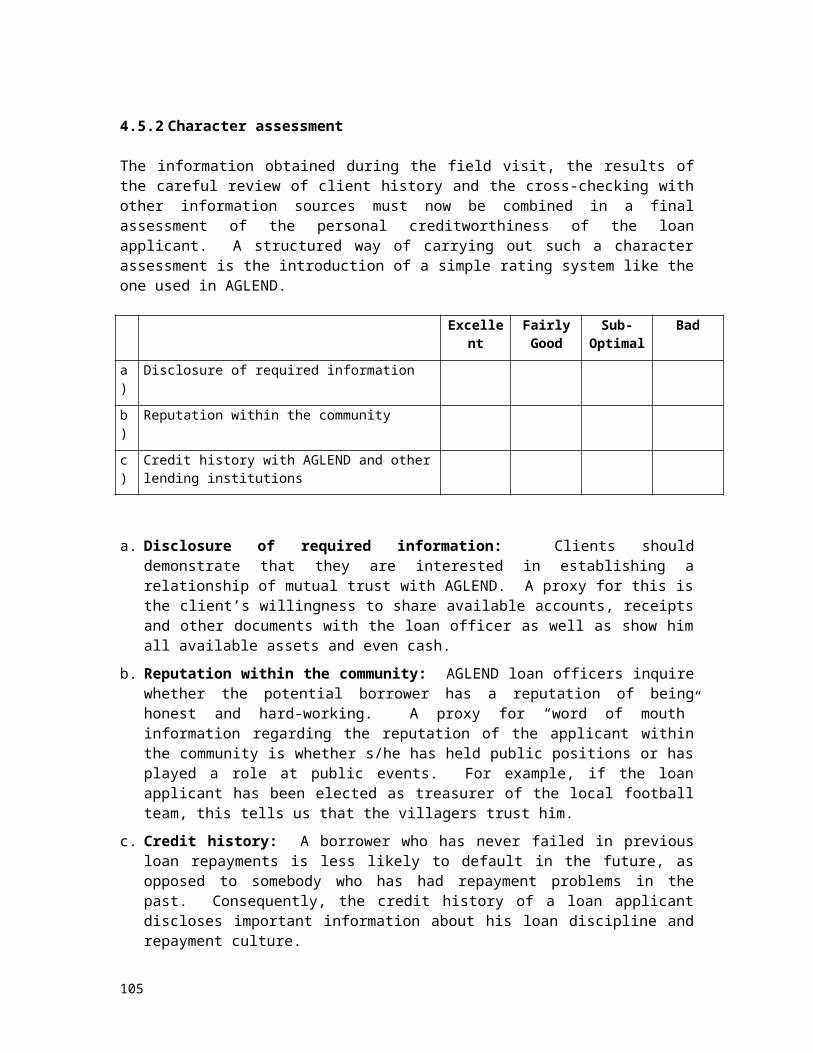

4.5.2 Character assessment................................................................................................67

4.5.3 Capital.........................................................................................................................68

4.5.4 Collateral.....................................................................................................................71

4.5.5 Environmental analysis.............................................................................................72

4.6 Loan Approval and Follow-up................................................................................734.6.1 The Loan file...............................................................................................................73

4.6.2 Loan conditions..........................................................................................................74

4.6.3 The Credit committee................................................................................................78

4.6.4 Loan disbursement.....................................................................................................79

4.6.5 Loan supervision and monitoring.............................................................................80

2

4.7 Managing Late Repayments and Loan Default.....................................................854.7.1 Loan recovery strategy..............................................................................................85

4.7.2 Preventing and managing late repayment...............................................................86

4.7.3 Managing loan default...............................................................................................90

4.7.4 Improving procedures...............................................................................................94

Chapter 5: Agricultural Loan Portfolio Management.................................................965.1. Individual versus Portfolio Risk.............................................................................96

5.2 Loan Portfolio Risk Factors....................................................................................97

5.3 Measuring Loan Portfolio Quality........................................................................102

5.4 Strategies for Active Loan Portfolio Management..............................................106

Chapter 6: Agricultural Value Chain Finance...................................................................1126.1 Background............................................................................................................112

6.2 Value Chains in Agriculture - Concept and Definition.....................................112

6.3 Interlinked Credit Arrangements.......................................................................113

6.4 Opportunities and Challenges for Value Chain Finance.........................................114

TABLES:

Table 1 Comparison of the Old and New Approach to Rural Finance.........................7

Table 2 Supply and Demand Characteristics of Rural Lending.....................................9

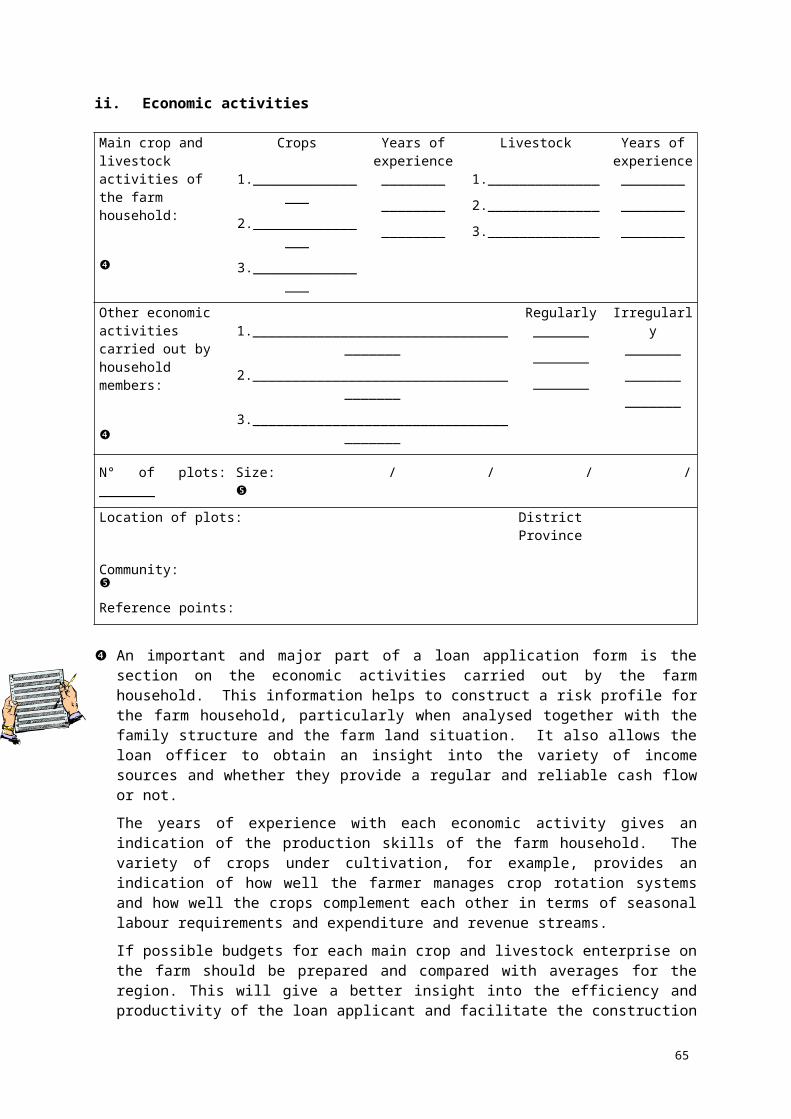

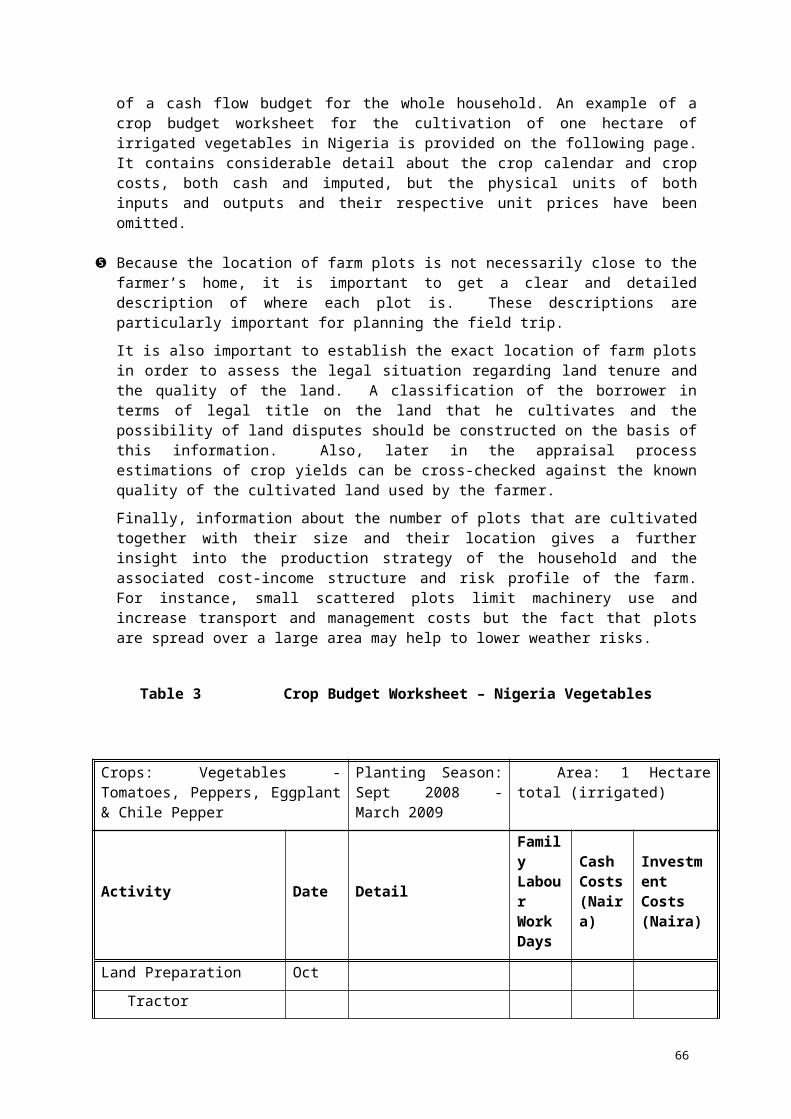

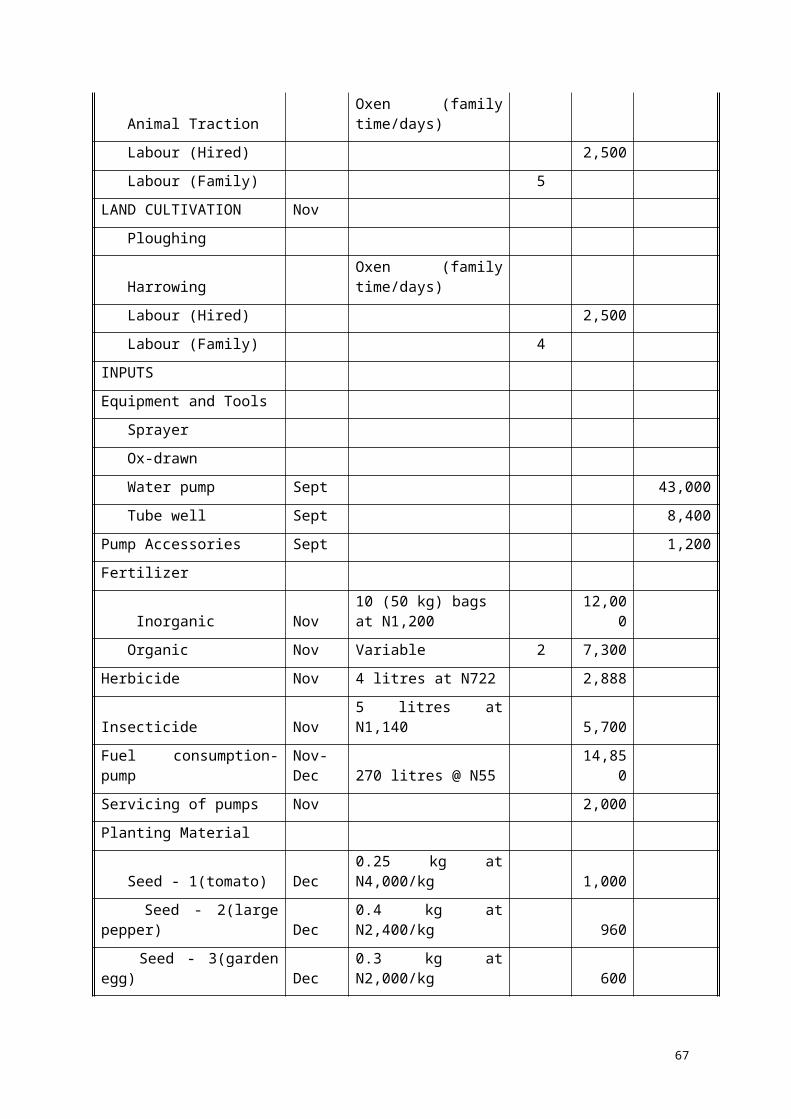

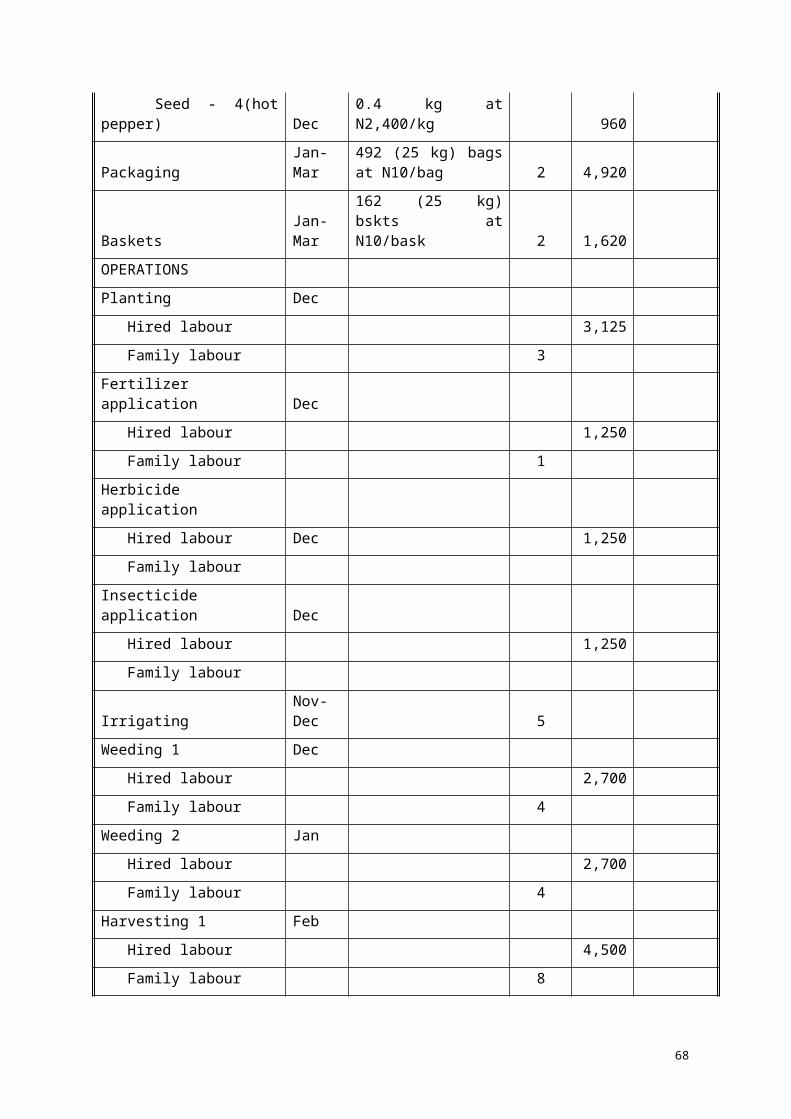

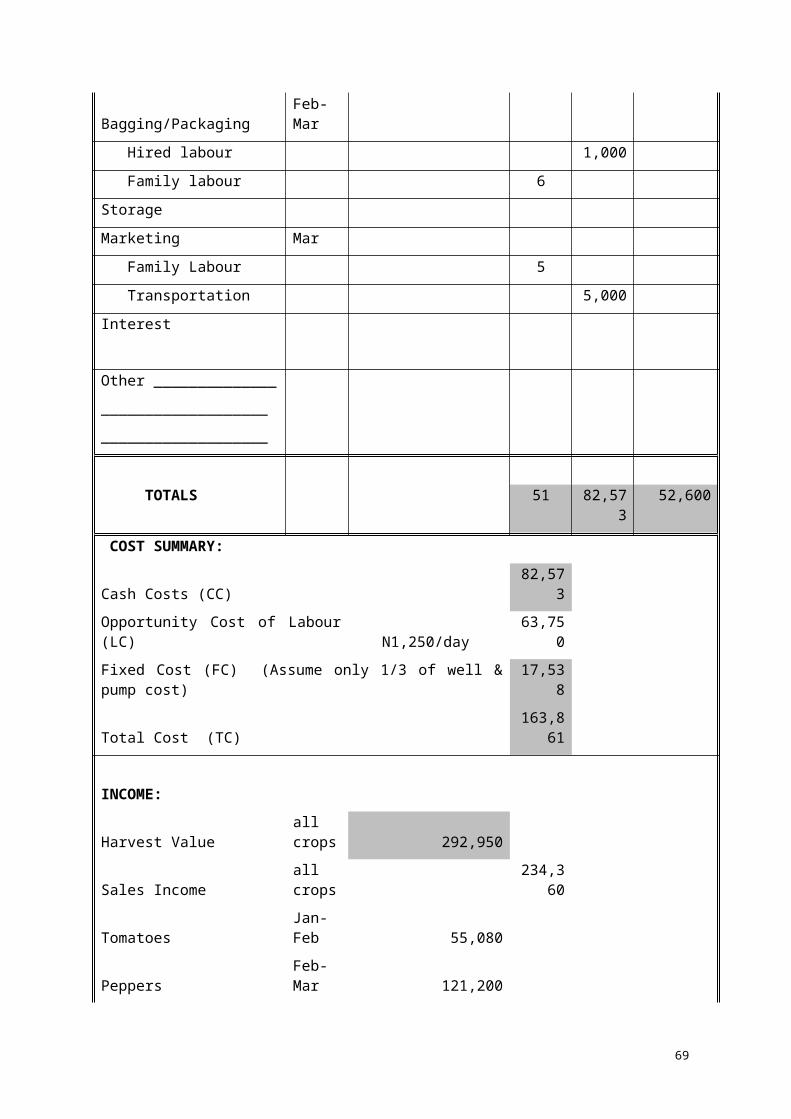

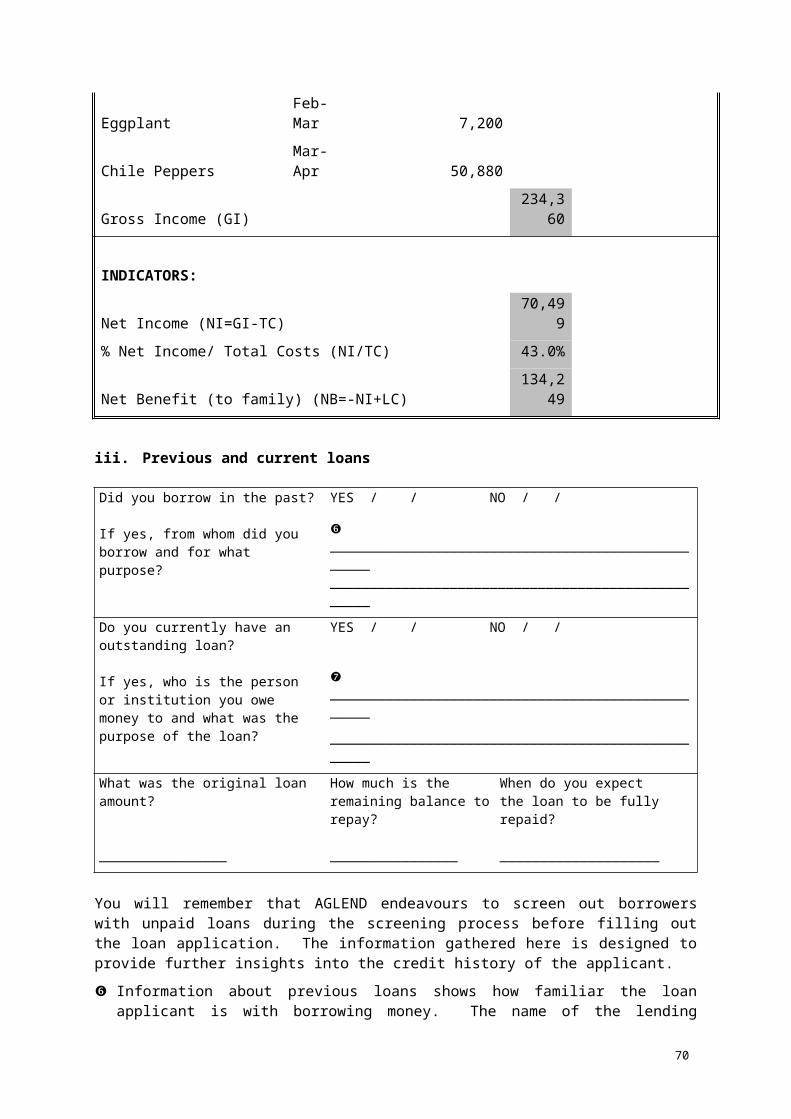

Table 3 Crop Budget Worksheet – Nigeria Vegetables.................................................42

DIAGRAMS:

Diagram 1 The Financial Sector...........................................................................................9

Diagram 2 A typical loan cycle...........................................................................................33

Diagram 3 Analysing loan default......................................................................................91

Diagram 4 Factors influencing regional risks...................................................................97

Diagram 5 Factors influencing Sector Risks.....................................................................99

Diagram 6 Example of the possible links in agricultural value chains:........................113

3

Introduction

Agricultural lending to small farmers in developing countries is particularly challenging and has been a concern of governments for a long time. As a result of the change in approach in the 1990s from “directed agricultural credit” towards a broader view of “rural financial market development” the access farm households have to formal agricultural credit has almost completely disappeared and this situation continues until today.

Banks generally avoid dealing with small farmers, as they perceive lending to them to be both costly and risky. Microfinance institutions, although anxious to extend their operations into rural areas, also worry about how best to provide effective financial services and, in particular, how to lend safely to farm households. Agricultural finance today is at a crossroads: at the same time as more working and investment capital is needed to meet the increasing demand for food, agricultural lending, particularly to small farmers, remains restricted, leading to a demand gap in the provision of rural financial services.

This agricultural lending training toolkit is designed as a self-study manual and training resource for agricultural lending institutions around the world. It highlights the common principles of sound agricultural lending and can be used by loan officers who are dealing with agricultural lending on a daily basis or by desk officers of donor agencies which provide support to local rural financial institutions. It may also be useful as basic reference material for local trainers.

The document is structured as follows:

The first chapter highlights the change in approach from supply-led and subsidized, directed agricultural credit to rural financial market development. The supply and demand components of rural lending are explained and, in recognition of the efforts of microfinance institutions to extend their operations into rural areas, the main characteristics of microcredit and the unique features of agricultural lending to small farmers are summarized.

The second chapter explores the unique challenges of agricultural lending to small farm households, in particular the high costs and risks involved, and emphasizes the need to use strategies which aim to reduce costs and mitigate risks.

Chapter three sets out some of the basic knowledge needed for effective agricultural lending such as, the different types of loan products that might be offered, cost effective ways of identifying good farmer clients, methods of building up a good agricultural database to provide a basis for sound loan decisions and the background and experience needed by agricultural loan officers in rural financial institutions.

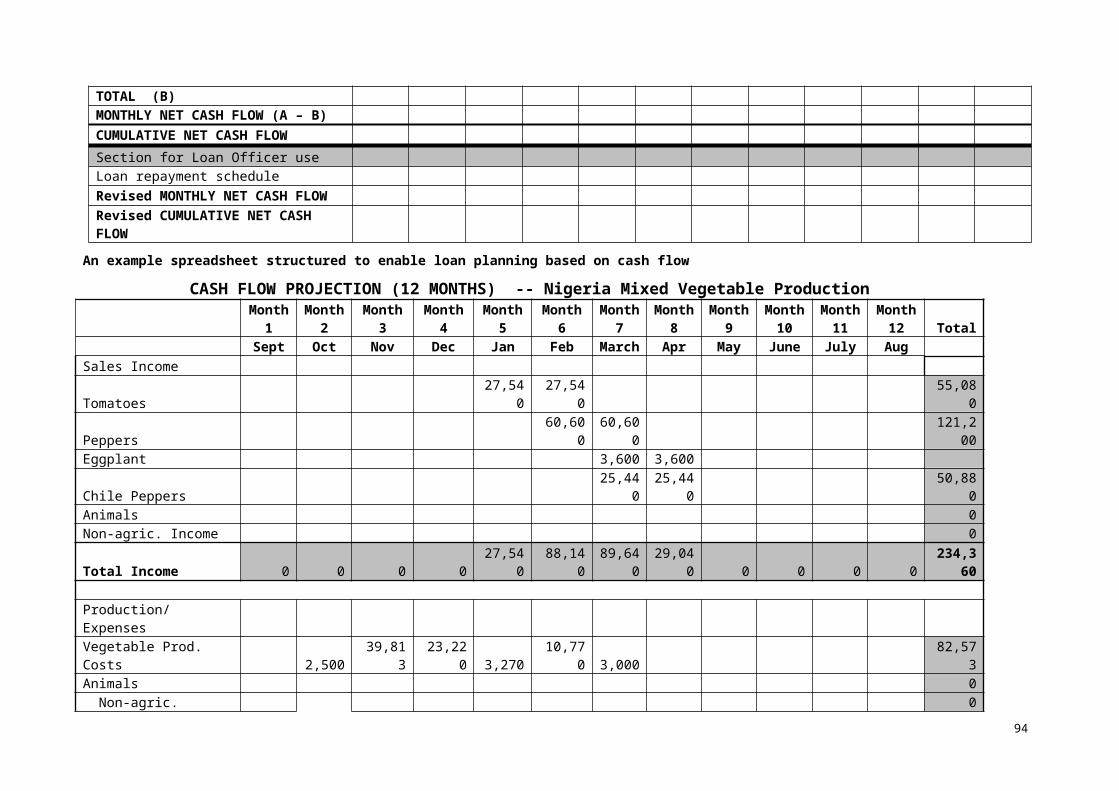

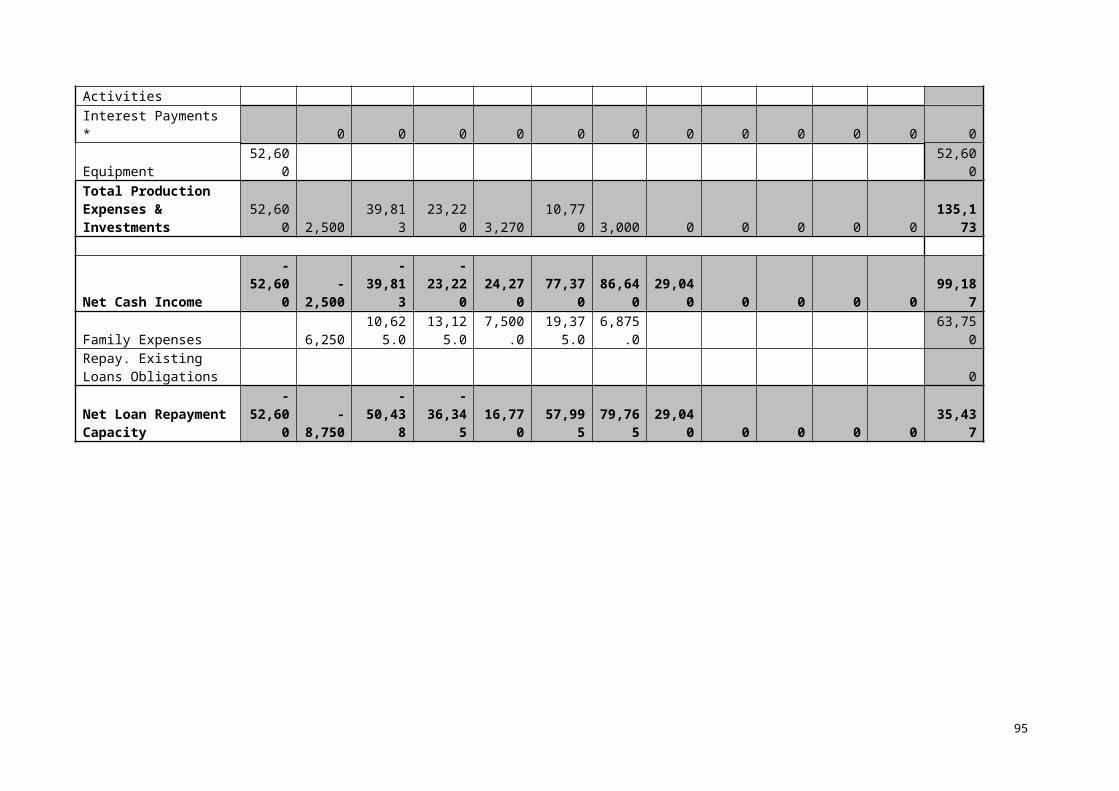

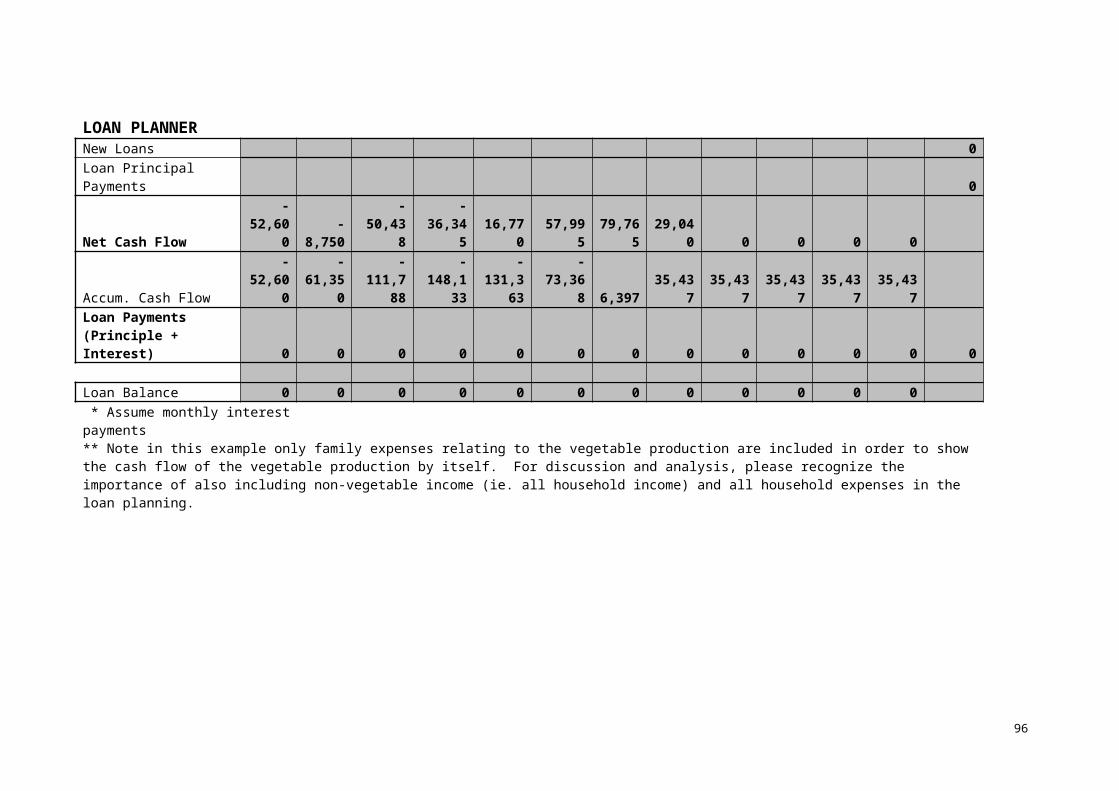

Chapter four constitutes the crucial part of the toolkit and it takes the loan officer through the different steps of the loan cycle. Excel electronic spreadsheets with examples of the data that should be collected by the loan officer and the analysis required for effective loan appraisal will be provided together with the toolkit. There will be a need to adapt these sheets to local conditions in order to make them suitable for practical use by loan officers. However, the electronic management information systems of lending institutions on loan accounts should provide loan officers with “real time” records on loan disbursement and repayment, which are indispensable for loan monitoring and follow-up.

The fifth chapter deals with overall loan portfolio risk management, which is of particular relevance to the managers of agricultural lending institutions. Risks present a major challenge in agricultural lending and risk mitigation measures at individual borrower level need to be complemented with overall loan portfolio risk management strategies. Diversification of the loan portfolio to cover different geographic areas, economic activities, types of borrowers and loan products is a common strategy for reducing the high “covariant or inter-related risks” associated with agricultural lending.

4

The final chapter examines the fast development of agricultural value chains all over the world and highlights the importance of traditional interlinked credit arrangements, as well as new ways of developing value chain finance. The chapter closes with a section outlining the opportunities and challenges that value chains pose for financial institutions involved in lending to small farm households.

This toolkit was written by Norah Becerra, Michael Fiebig and Sylvia Wisniwski with support and advice by FAO.

5

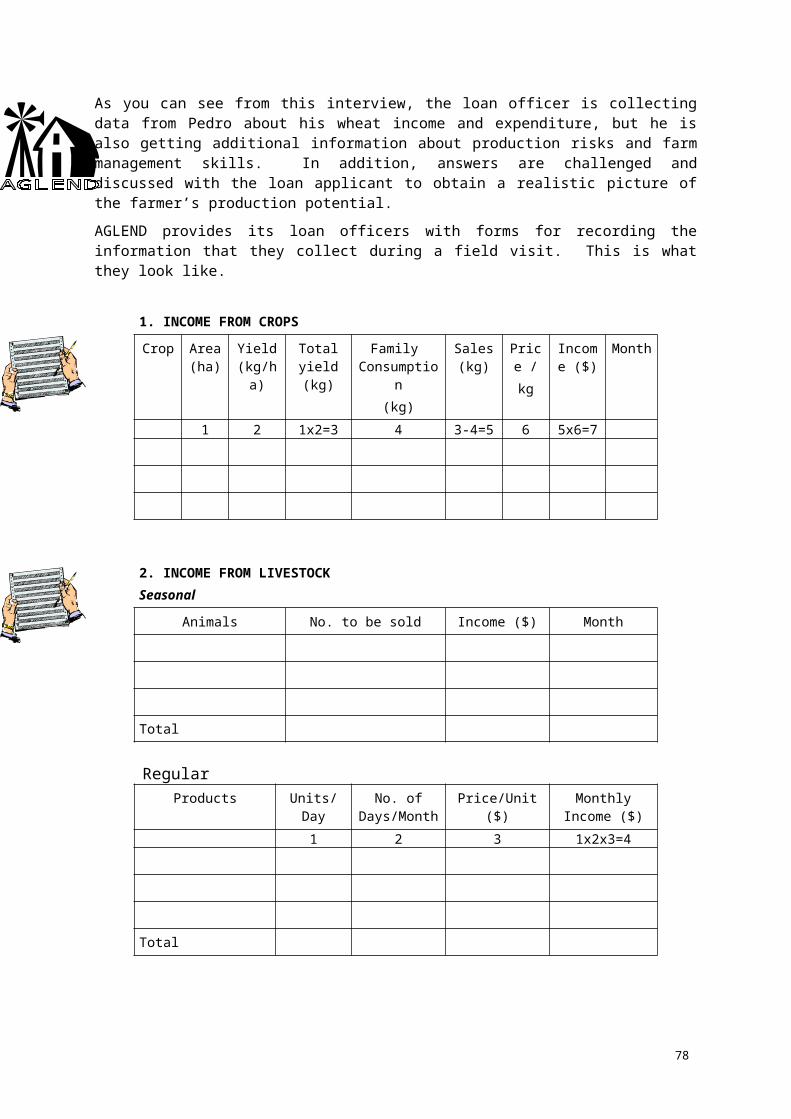

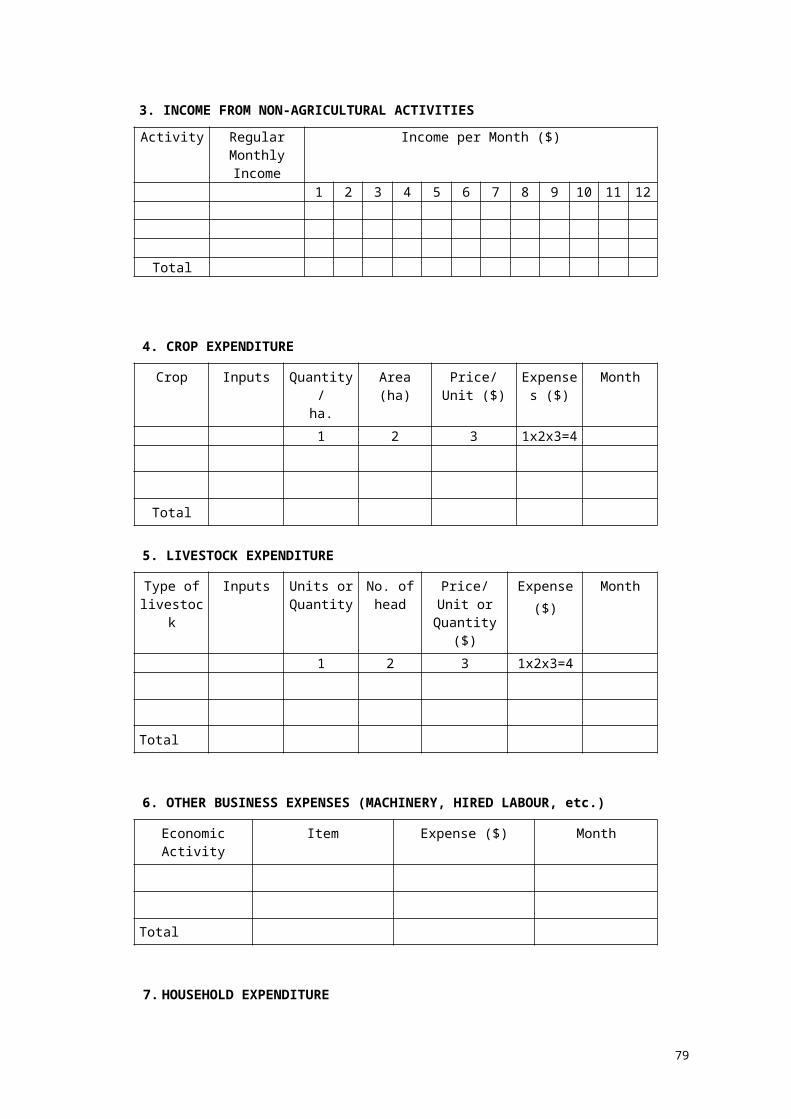

The toolkit uses an imaginary lending institution and farming family to illustrate many of the procedures that are being introduced and these are identified by the following icons:

AGLEND:

The AGLEND icon indicates that an example based on the imaginary agricultural lending institution, AGLEND, is being used.

Family Crespo:

This icon indicates when the imaginary family Crespo, clients of AGLEND, are being used as an example.

Other important features of the toolkit are highlighted by these icons:

Case Study:

This globe icon indicates that a real-life case study or institutional experience from a specific country is being used.

Questions:

The clip-board icon indicates that questions to help readers review the key messages of each chapter have been provided.

Exercises:

The paper and calculator icon indicates an exercise section. Here, more complex questions are posed and readers may be asked to give a solution to a specific problem.

Answers to calculations are provided at the end of the toolkit.

6

Chapter 1: Agricultural Lending to Small Farmers

Objective: To provide an overview of agricultural lending and its role in rural development

1.1 From Directed Agricultural Credit to Rural Financial Market DevelopmentThe majority of the rural population in developing countries depends on farming for a livelihood and small farm development is considered important for economic growth and improved food security, as well as the reduction of rural poverty. The provision of agricultural credit to small farmers, however, has turned out to be difficult. Early development planners were primarily concerned with the need to increase food crop production and they used the provision of cheap credit to small farmers as a means to stimulate the adoption of modern, yield-increasing farm inputs. These programs, however, were based on a number of wrong assumptions regarding the nature of the farm households that they targeted and they were also designed in an unfavourable market environment, characterized by heavy government interventions and negative terms of trade for the agricultural sector.

Until the late 1980s large amounts of government and donor money were directed to smallholder farmers for specific production purposes often in the form of a package of subsidized credit, public agricultural extension services and state-controlled agricultural input supply and output marketing. This targeted approach failed, however, to produce increased farm income, as the new technologies and farm inputs were not sufficiently profitable at the prevailing crop prices. Moreover, the agricultural development banks, through which most of the credit was channelled, were unable to operate as sustainable financial institutions and as a result, they have either been liquidated or reformed.

Since then major market liberalization and financial sector reforms have been initiated and significant changes have also taken place in agricultural and rural development strategies. In particular, the earlier directed agricultural credit policy has been replaced by a market-based financial system development approach. Rural financial market development now aims at providing sustainable financial services for the rural population which are responsive to the effective demand for deposit facilities and credit for profitable income-generating activities, including farm, farm-related and non-farm enterprises. The key words for market-based financial institutions are performance, outreach and sustainability.

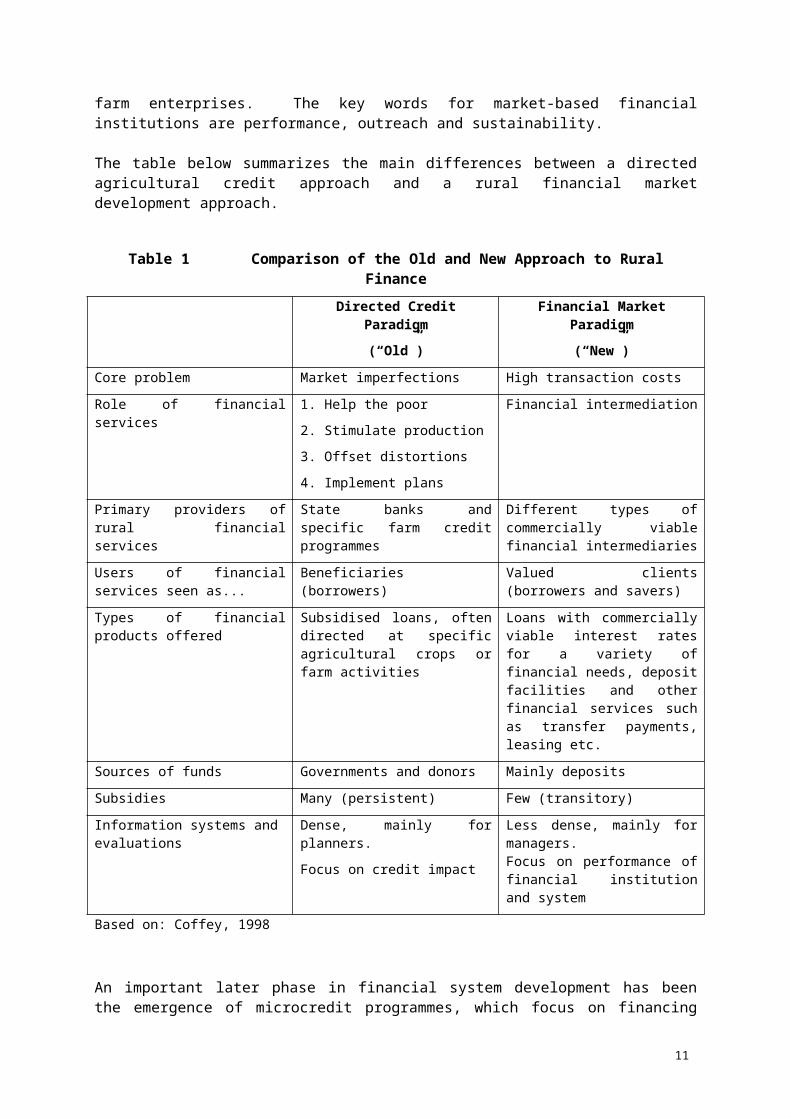

The table below summarizes the main differences between a directed agricultural credit approach and a rural financial market development approach.

Table 1 Comparison of the Old and New Approach to Rural Finance

Directed Credit Paradigm

(“Old”)

Financial Market Paradigm

(“New”)

Core problem Market imperfections High transaction costs

Role of financial services 1. Help the poor

2. Stimulate production

3. Offset distortions

4. Implement plans

Financial intermediation

Primary providers of rural financial services

State banks and specific farm credit programmes

Different types of commercially viable financial intermediaries

Users of financial services seen as...

Beneficiaries (borrowers) Valued clients (borrowers and savers)

Types of financial products offered Subsidised loans, often directed at Loans with commercially viable

7

specific agricultural crops or farm activities

interest rates for a variety of financial needs, deposit facilities and other financial services such as transfer payments, leasing etc.

Sources of funds Governments and donors Mainly deposits

Subsidies Many (persistent) Few (transitory)

Information systems and evaluations

Dense, mainly for planners.

Focus on credit impact

Less dense, mainly for managers.Focus on performance of financial institution and system

Based on: Coffey, 1998

An important later phase in financial system development has been the emergence of microcredit programmes, which focus on financing short-term and regular income-generating activities of poor people in urban and rural areas. These programmes have demonstrated that low-income clients are ready to pay high interest rates, if the credit offered meets their specific financial needs. At first microcredit was offered primarily by NGOs, but today microfinance has turned into a new line of business for many different types of financial service providers including specialized microfinance institutions, development banks and even private commercial banks. A number of international microfinance investment funds with a pro-poor interest support local microfinance institutions. Important progress has been made in the design of appropriate lending technologies and in institutional sustainability and operational outreach of these institutions.

Microfinance, however, is largely concentrated in urban areas and the majority of small farmers and other rural entrepreneurs in developing counties and transition economies have no access to financial services, mainly due to the highly risky nature of agricultural enterprises. The challenge of how best to develop a viable rural financial system and, in particular, finance small farmers in a cost-effective and risk-reducing way remains open. This is crucial: at the same time as small farmers need more working and investment capital in order to meet an increasing demand for food, agricultural lending remains restricted. As a result there is an important demand gap in the supply of rural financial services.

It is encouraging, however, that a number of microfinance institutions have started to expand their operations into rural areas. Take, for example, the initiative of the Incofin Investment Management Group in Belgium, which launched a Rural Impulse Fund in 2007. This international public-private partnership fund has a capital base of US$ 38 million and provides both loans and equity capital to selected local microfinance partners in an attempt to assist the expansion of their outreach into rural areas.

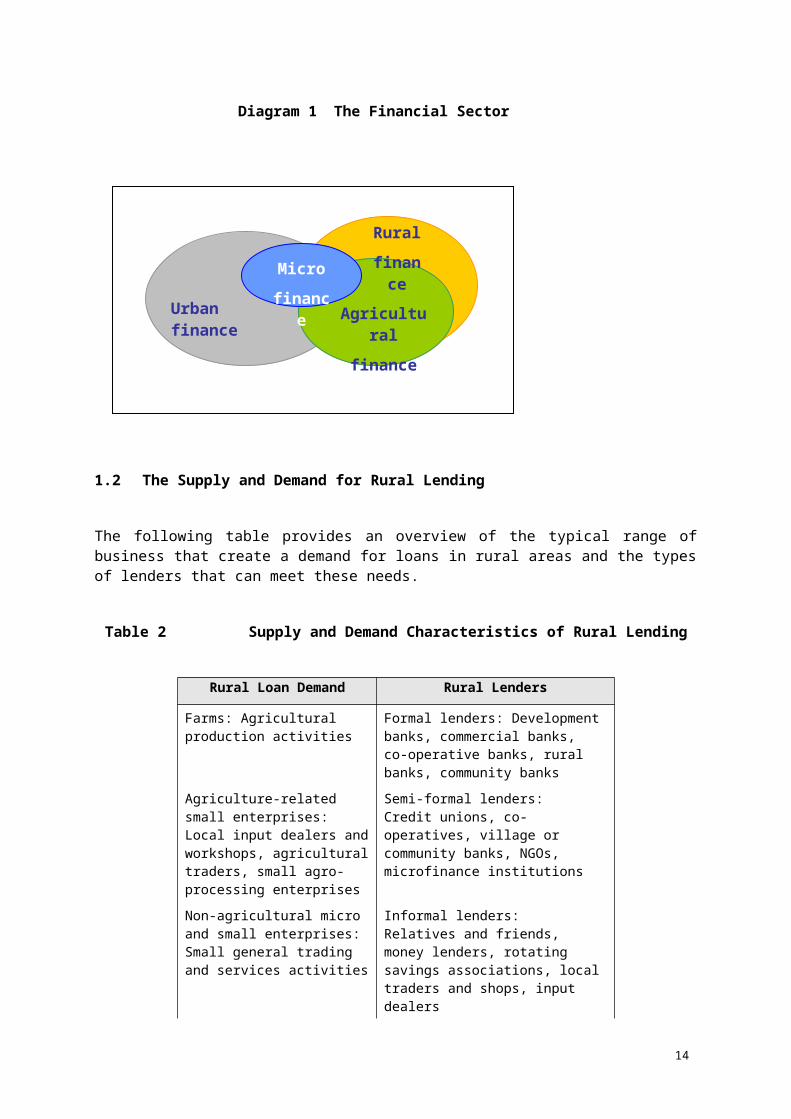

The following diagram illustrates the overlapping relationship that exists between different components of the financial sector. Attempts to increase the outreach of agricultural financial services to small farmers should benefit from the experience that has been obtained in microfinance. However, the unique features of agricultural lending mean that the best practices of more urban-based microcredit do not transfer easily to rural areas.

8

Diagram 1 The Financial Sector

1.2 The Supply and Demand for Rural Lending

The following table provides an overview of the typical range of business that create a demand for loans in rural areas and the types of lenders that can meet these needs.

Table 2 Supply and Demand Characteristics of Rural Lending

Rural Loan Demand Rural Lenders

Farms: Agricultural production activities

Formal lenders: Development banks, commercial banks, co-operative banks, rural banks, community banks

Agriculture-related small enterprises: Local input dealers and workshops, agricultural traders, small agro-processing enterprises

Semi-formal lenders: Credit unions, co-operatives, village or community banks, NGOs, microfinance institutions

Non-agricultural micro and small enterprises: Small general trading and services activities

Informal lenders: Relatives and friends, money lenders, rotating savings associations, local traders and shops, input dealers

Large agriculture- related enterprises, often based in urban areas: Agro-processors, wholesalers, retailers, exporters

Interlinked agricultural credit arrangements: Agricultural input and equipment suppliers, crop buyers, agro-processing companies, wholesalers, retailers, exporters

9

Urban finance

Ruralfinan

ce

Agricultural

finance

Microfinanc

e

Rural lenders: Commercial banks, which have few or no rural branches, rarely engage in rural lending and, in particular, they do not lend to small farm households. Instead, they focus their attention on servicing large agribusiness clients, who are often located in urban areas. Semi-formal lenders, who usually operate under different regulations, raise most of their funds from short-term savings and this seriously limits their ability to lend to agricultural enterprises which are seasonal and have relatively long production cycles. Informal rural lenders and local businessmen such as traders, shopkeepers and input dealers fill some part of the rural finance demand gap with trade and supplier credit. Their advantages are a local presence and good knowledge of their clients, which enables them to provide convenient and timely access to credit. In general this compensates for the relatively high lending rates and unfavourable terms of trade that they offer. Modern forms of interlinked agricultural credit arrangements such as contract farming are playing an increasingly important role in the financing of small farmer production and are of particular relevance for agricultural commodities that require specialized agro-processing. The increasing importance of agricultural value chains as a means of financing farm production will be dealt with in the final chapter of this toolkit.

Demand for Agricultural and Rural Lending: A number of the assumptions that were made about small farmers in the directed agricultural credit approach have proved to be wrong. Small farm households, even if they are poor, do save and, in fact, precautionary savings form an integral part of farm household livelihood strategies. Savings both in kind and in cash, are used to bridge the period between successive harvests and can be used for a variety of production, consumption and contingency expenditure, as well as for investment purposes. Another misconception was that small farmers would be unable to pay market interest rates for the credit that they need. The widespread use of informal credit, however, has shown that convenient, timely and regular access to small contingency loans compensates for its high costs. Small farmers tend to be risk averse and diversify their revenue generation across a range of farm and non-farm income-generating activities. A close look at the cash flows of low income farm households shows the complex relationships between farm and family household expenditures and revenues. This complexity was not taken into consideration in the directed agricultural credit approach.

1.3 Lessons from Microfinance

The lessons or “best practices” that microcredit programmes have provided relate to the strategies that have been developed to reduce the high costs and risks associated with granting small, short duration loans to low-income clients for income-generating activities, usually trading or providing services.

Cost reduction strategies: The main strategies used to reduce costs are standardization of loan products and the use of streamlined lending procedures. Microfinance institutions generally offer a limited number of highly standardized loan products, usually in the form of short-term working capital loans for microenterprise activities. Loans to first-time clients are small and are granted for terms ranging from a few weeks to a few months. As the information-gathering costs of established clients are considerably reduced, borrowers with good repayment records are rewarded with repeat loans, the size and duration of which are gradually increased. However, as the costs associated with providing very small loans are relatively high, microfinance institutions usually charge higher interest rates than those used by traditional formal lenders. A lean organizational structure helps to reduce the overhead costs of the financial institution, while staff performance incentives schemes are widely used to increase the number of clients that are managed by each loan officer and to improve the loan portfolio quality. Cost and loan quality considerations usually determine whether an institution chooses group lending or individual lending, although over time there may be a trend to more individualized lending methods. Information on the credit history and creditworthiness of potential borrowers is usually sought from relevant local organizations and communities, while a key element of loan appraisal is using household cash flow to determine loan repayment capacity.

10

Risk management strategies: In the selection of borrowers most microfinance providers pay particular attention to identifying a target clientele who have a minimum level of experience and track record in the microenterprise business activity for which loans are given. Loans usually need to be repaid in weekly or monthly instalments, which means the income-generating activities must have a high turnover and generate regular income flows. Door-step banking procedures and delegation of a limited lending authority to loan officers ensure that loan decisions are made by those who are closest to their customers and know them best. As the microcredit target clientele rarely possesses the conventional types of loan collateral demanded by banks, various types of collateral substitutes are accepted for the small and short-term loans, such as household goods, co-signers and third-party guarantors. Graduation of clients to larger follow-up loans creates an important incentive for good loan discipline and loan repayment behaviour.

1.4 Unique Features of Agricultural Lending

The application of microcredit best practices to agricultural lending is limited by a number of unique features of the small farm sector.

Political sensitivity of agriculture: Essential pre-conditions for viable agricultural lending are the existence of sound policies for the agricultural sector and a favourable, market-oriented rural business environment. Food production and food security, however, are highly politically sensitive issues and often dominate agricultural development policies. Thus terms of trade are often distorted to keep the price of basic food products low for urban consumers and this has a negative effect on the profitability of farmers, which discourages financial institutions from serving them. Moreover, as experience from the directed agricultural credit approach has shown, state intervention in rural financial markets, such as enforcing low interest rates for small farmer borrowers or promoting loan default waivers, does not compensate for the low profitability of farming.

Nature of farm lending activities: Agricultural loans are larger and require much longer repayment periods than most microcredit loans. The length of agricultural production cycles means that loan repayments are restricted to large, lumpy instalments, so loan supervision costs tend to be high because of the need for strict loan monitoring. In addition agricultural lending is seasonal, so the work load of loan officers is not even throughout the year. This results in high personnel costs, especially when financial institutions do not diversify their overall loan portfolio sufficiently. The importance of assessing all the different income-generating activities of farm households and the complex inter-relationship between production and consumption expenditure and revenue also contribute to the high information and staff costs for agricultural lending institutions.

High transaction costs of lending in rural areas: Rural areas, unlike towns, are characterized by low population density and an inadequate infrastructure. The fact that potential clients of rural financial institutions are widely dispersed makes the provision of financial services to them very costly. Establishing and maintaining a rural branch network leads to high overhead costs and, while the use of mobile loan officers and door-step banking procedures may reduce the transaction costs of both lender and borrower, it does not resolve the overall problem of high costs. Consequently financial institutions which decide to work in rural areas may initially concentrate their operations in more favourable regions or focus on clusters of profitable business activities. If successful, they may gradually extend their operations to other areas.

High risks associated with agricultural lending: Risks and uncertainties in agriculture are more serious than in most non-agricultural economic activities. The type and severity of these risks vary according to the type of farming systems practised, the prevailing farm enterprises, the quality of individual farm management skills, the local physical and economic conditions, and the effect of government policies. The risk of individual loan default can be serious in environments which have a

11

history of failed agricultural credit programs. One way of reducing the high cost of gathering client information and moral hazard risks in agricultural lending is to collaborate closely with local organizations that can provide reliable information about new clients.

Covariant or inter-dependent risks which may affect many or all farmers in the same location, and at the same time, represent by far the most important challenge to agricultural lending. They arise from both production and market risks. Production or physical yield risks are due to natural hazards such as unfavourable weather conditions, pests and diseases, and they have a negative and unpredictable impact on physical farm production. On the other hand, market risks of agricultural commodities are due to product-specific market fluctuations and changes in domestic and international agricultural and trading policies which have a direct impact on product prices. Rural financial institutions can protect themselves against the potentially devastating effects of high covariant risks in agricultural lending by diversifying their loan portfolio. Other instruments that can be used are insurance products, warehouse inventory credit, contract farming and other forms of vertical integration in the agricultural value chain. In the event of natural disasters, careful loan rescheduling and close coordination with emergency aid organisations may help in reducing the adverse impact of covariant risks on agricultural lending institutions.

Agricultural loan collateral limitations: Small farm households possess few valuable assets that they can pledge as collateral for agricultural loans and this lack of collateral poses specific problems for lenders. For instance, the usefulness of farm land as collateral is limited by problems with ownership titles, uncertain legal procedures associated with foreclosure and weak land markets. Movable assets such as equipment and livestock are regarded as even more risky forms of security, particularly if they are not covered by insurance. As a result, lenders value rural assets very conservatively and they may require a collateral value that is much higher than the loan value. This reduces the effective demand for agricultural loans by small farmers.

Questions:

1. What are the core differences between the old and new approaches to agricultural lending? What consequences does the change have for agricultural lenders and small farmers?

2. Has there been a change in approach in your country? How has this affected the rural financial markets there?

3. What are the major types of organisation lending to agriculture in your country? Which are the main providers in your region?

4. What kind of microfinance institutions operate in your country? Which practices do they follow? Compare the different roles played by NGOs, savings and credit co-operatives, development banks and commercial banks.

5. Which clients do the microfinance institutions serve in your country? Do rural smallholders have access to small loans?

12

Chapter 2: The Challenges of Agricultural Lending

Objective: To increase awareness of the particular risks and costs associated with agricultural lending and identify the important characteristics that an agricultural loan officer needs.

2.1 The Risks

i) Moral hazard

In any lender-borrower relationship, there is a general problem of moral hazard that is the result of specific personal characteristics and decisions of each individual borrower. In this regard, farmers do not differ from any other borrower group in terms of information, incentives, monitoring and enforcement problems associated with the lending process.

Firstly, it is obvious that the lender does not have the same information as the borrower. The latter knows exactly what his/her own management capacity is and how the loan will be used. The lender does not know the potential borrower to such an extent. In rural financial markets, information about low income loan applicants is particularly difficult to obtain. Secondly, even if the loan applicant frankly shares all relevant information for the loan decision, his/her future actions cannot be fully predicted. Therefore, it is crucial for financial institutions to use incentives to encourage borrowers to behave in such a way that repayment is assured.

Thirdly, the farmer may decide to change his/her economic behaviour, invest the money elsewhere or simply move to another part of the country. Many subsidised agricultural credit programmes tried to manage this risk by undertaking regular monitoring of the borrower but this is costly. Finding cost-effective methods for monitoring borrowers is a particular challenge in agricultural lending.

However, there are other risks beyond the general behavioural risks of a borrower. This second category of loan loss risks is associated with the agricultural sector and agricultural production. It refers to factors external to the farmer’s repayment attitude.

ii) The nature of farming

Farming is a risky business. The weather affects productivity and may cause crops to fail. If productivity is lower than expected, farmers may not be able to repay loans. Market prices also fluctuate and are difficult to predict when crops are planted. These risks and many others need to be identified, measured and actively managed in order to prevent lending institutions turning away from a farming clientele. Let's look at the various external risk categories that need to be taken into account in agricultural lending.

Agricultural production and crop yield risks

Crop yields are generally uncertain, as natural hazards such as weather, pests and diseases and other production calamities impact on farm produce. Even slight changes in weather conditions, e.g. less rain than usual, can seriously impact on farm production. Pests and diseases can spread quickly, causing the loss of all or part of a crop’s production. The quality of soil in farming plots and their location are other factors that significantly influence productivity and crop yield risks.

13

Experienced farmers know the specific risk profiles of agricultural products and try to manage these risks. One strategy applied by many small farmers is diversification, as having a variety of activities counters the risk of losing everything if one enterprise fails. Many small farmers are so risk-averse, they do not readily venture into new crops or production methods in which they are, as yet, inexperienced.

Weather impact is managed in various ways. For example, irrigation systems may limit the risk of drought. Greenhouse production - among other benefits – can limit the risk of frost damage and increase overall productivity significantly. On the other hand, however, modern farm technologies can also increase the risk exposure of a farmer if they are little known or poorly managed.

Ways to reduce the damage caused by pests and diseases include the use of insecticides and other chemical products. Animal illness and mortality can likewise be managed through vaccination and maintenance of strict hygiene precautions. Contacting agricultural extension agents or veterinary surgeons for advice may help to complement the farmer’s own knowledge and experience in managing production and yield risks.

In all these risk management techniques, the experience and skill of the small farmer are core requirements for good results. In fact the risk of inappropriate management is another element of production risk. So, prudent lending decisions need to include an assessment of the management capacity of the farmer.

Seasonality of agricultural production constitutes another important risk. People invest in work today for a future return in the form of a crop harvest several months after planting. If the harvest is poor and not enough to see people through to the next one, they will be weakened by malnutrition and in extreme situations can die from starvation. A particular feature of seasonality risk is the fact that, if in a given season part or all of a crop is lost, new planting often has to wait until the start of the following season. Besides which, funds for investing in additional agricultural inputs for a new production cycle may not be available. Complying with the repayment schedule for a current seasonal loan may also become impossible, if other sources of income cannot be mobilised.

Price and market risks

Price uncertainty due to market fluctuations is particularly significant where market information is lacking or scarce or where markets are imperfect – features which are prevalent in many developing countries. The relatively long period of time between planting a crop or starting livestock activities and obtaining the final product makes it likely that market prices will have changed considerably from that originally foreseen. This problem is particularly relevant to long term agricultural production activities, such as perennial tree crops like cocoa or coffee, where several years pass between planting and the first harvest.

Price fluctuations may be particularly severe in export markets, but under- or over-production of crops will also influence domestic market prices to a significant degree. In many countries, price uncertainty has increased with the liberalisation of agricultural markets. In the past state controlled marketing boards often set fixed prices, but today agricultural prices are left to fluctuate freely in many countries. Private crop buyers rarely fix a blanket-buying price prior to harvest, even though inter-linked purchase and credit arrangements for specific crops have become more common. These arrangements almost always involve setting a fixed price or a range of prices prior to planting.

Another source of market risk is the potential losses that arise when marketing agricultural products. Transportation, for instance, is a major challenge in many rural areas and substantial losses or damage may be incurred as a result of inappropriate storage facilities. The lower quality of a poorly stored product also reduces its price.

14

Lack of diversification

Price and market risks, as well as production and yield risks, are often higher for farmers who specialise in a single crop or livestock activity. Accordingly, many farmers diversify their production and apply risk mitigation techniques to reduce their risks. Complementing farm production for market with food production for subsistence is a livelihood strategy used by most small farmers and this assist their survival if production and price risks wipe out expected profits.

Small farmers’ annual incomes often depend on one main crop enterprise. This is particularly challenging when it takes many months to reach harvest time. The situation is even more difficult if the farmer's plots are very small. Thus, an alternative approach to diversification is to generate additional household income between agricultural seasons by engaging in off-farm activities. This can be essential for farmers who are operating in a high-risk agricultural production environment, e.g. when they face a continuous threat of drought or floods.

While diversification of agricultural production is very common, its effect on reducing income insecurity is often insufficient. In fact, small farmers have a long history of experiencing bad years during which their cash income is close to zero, interspersed with some better years, in which a small surplus may be produced. As income risks directly affect the outcome and repayment of an agricultural loan, a lack of sufficient production diversification and risk mitigation remains a major challenge for agricultural lending.

iii) Politicians

Political interference in agricultural markets is a common feature which is found in many developing countries. Price intervention is popular for example, as low food prices are in the interest of the urban population which has a loud voice. Abolishing price ceilings for basic food products in former socialist states led to severe social unrest. Accordingly, stabilising food prices has been a common feature of political interventions in many countries. On the other hand, fixed farm gate prices for agricultural products are also frequently used by governments to ensure a minimum level of income for small farmers.

Changes in policy and state interventions can have a severely damaging impact on rural financial markets. Agricultural lending has, in fact, a long-standing history of political intervention and market distortion, which has significantly contributed to the lack of interest from commercial banks in lending to farmers. Promising debt cancellation is a common feature of populist political campaigns and is extremely damaging to the operations of viable financial services providers. Even well-intentioned credit programmes earmarked for specific target groups and regions can substantially distort prudent agricultural lending.

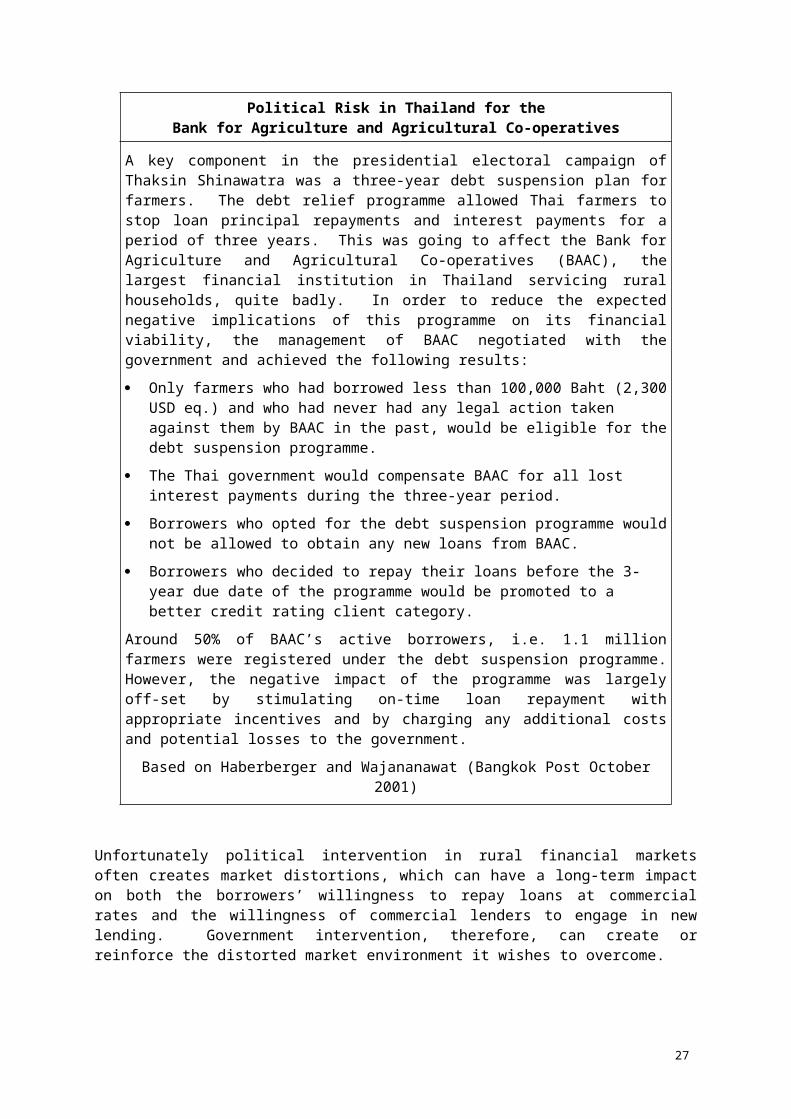

Have a look at the following example:

15

Political Risk in Thailand for theBank for Agriculture and Agricultural Co-operatives

A key component in the presidential electoral campaign of Thaksin Shinawatra was a three-year debt suspension plan for farmers. The debt relief programme allowed Thai farmers to stop loan principal repayments and interest payments for a period of three years. This was going to affect the Bank for Agriculture and Agricultural Co-operatives (BAAC), the largest financial institution in Thailand servicing rural households, quite badly. In order to reduce the expected negative implications of this programme on its financial viability, the management of BAAC negotiated with the government and achieved the following results:

Only farmers who had borrowed less than 100,000 Baht (2,300 USD eq.) and who had never had any legal action taken against them by BAAC in the past, would be eligible for the debt suspension programme.

The Thai government would compensate BAAC for all lost interest payments during the three-year period.

Borrowers who opted for the debt suspension programme would not be allowed to obtain any new loans from BAAC.

Borrowers who decided to repay their loans before the 3-year due date of the programme would be promoted to a better credit rating client category.

Around 50% of BAAC’s active borrowers, i.e. 1.1 million farmers were registered under the debt suspension programme. However, the negative impact of the programme was largely off-set by stimulating on-time loan repayment with appropriate incentives and by charging any additional costs and potential losses to the government.

Based on Haberberger and Wajananawat (Bangkok Post October 2001)

Unfortunately political intervention in rural financial markets often creates market distortions, which can have a long-term impact on both the borrowers’ willingness to repay loans at commercial rates and the willingness of commercial lenders to engage in new lending. Government intervention, therefore, can create or reinforce the distorted market environment it wishes to overcome.

iv) Collateral problems

If a borrower does not repay on time, a lender must enforce repayment. In traditional bank lending, collateral is used to compensate for potential loan loss. Small farmers, however, rarely have conventional types of collateral and legal procedures to use collateral are often cumbersome and costly. Developing and applying effective and cost efficient enforcement mechanisms is, therefore, another challenge facing those wishing to control loan loss risks in agricultural lending.

Small farmers rarely possess land titles which can be used as loan collateral by banks and if they do have a title, it may have a very limited commercial value, due to the absence of a rural land market. Land registration is often imperfect in developing countries and land titles may be unavailable or costly to obtain.

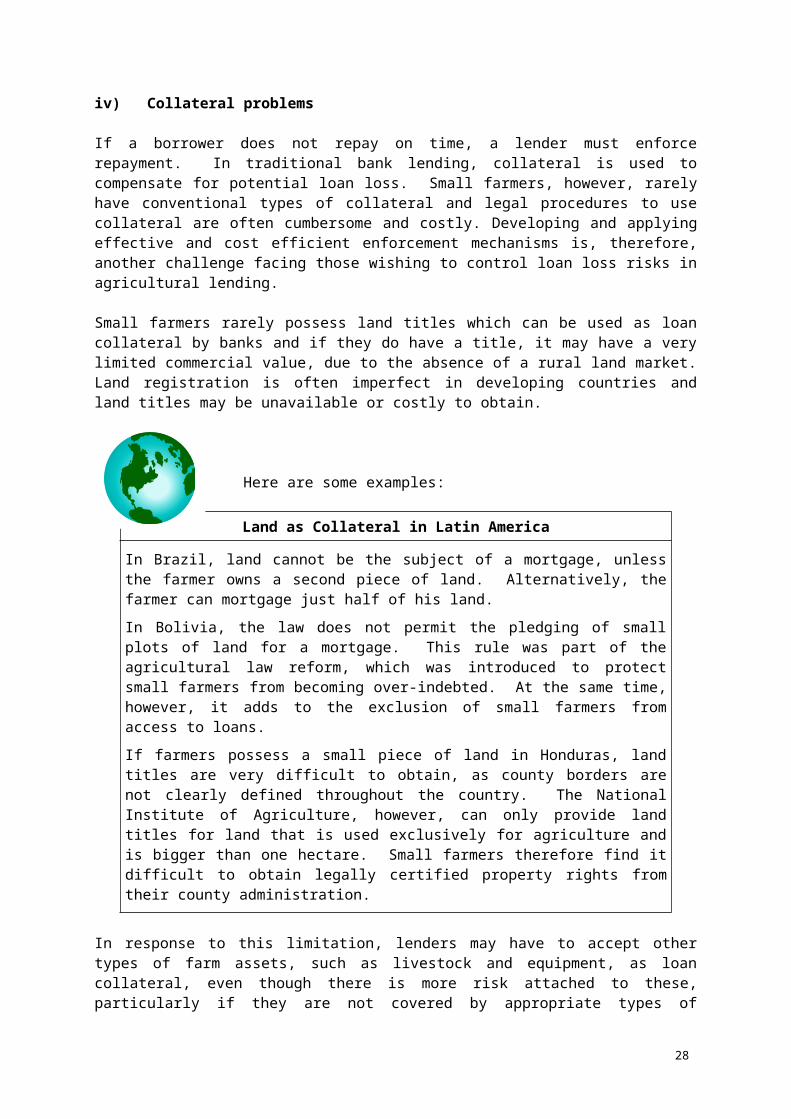

Here are some examples:

16

Land as Collateral in Latin America

In Brazil, land cannot be the subject of a mortgage, unless the farmer owns a second piece of land. Alternatively, the farmer can mortgage just half of his land.

In Bolivia, the law does not permit the pledging of small plots of land for a mortgage. This rule was part of the agricultural law reform, which was introduced to protect small farmers from becoming over-indebted. At the same time, however, it adds to the exclusion of small farmers from access to loans.

If farmers possess a small piece of land in Honduras, land titles are very difficult to obtain, as county borders are not clearly defined throughout the country. The National Institute of Agriculture, however, can only provide land titles for land that is used exclusively for agriculture and is bigger than one hectare. Small farmers therefore find it difficult to obtain legally certified property rights from their county administration.

In response to this limitation, lenders may have to accept other types of farm assets, such as livestock and equipment, as loan collateral, even though there is more risk attached to these, particularly if they are not covered by appropriate types of insurance. Microfinance institutions use a combination of different types of collateral that vary with the loan size, and personal and third party guarantees and co-signing by a spouse are often accepted as alternative or collateral substitutes to “real” assets. Group guarantees are also used in agricultural lending and this approach is based on functional social control, mutual trust and joint liability by group members.

A better approach may be to focus on the use of preventive measures to secure loan repayment. These measures put less emphasis on the provision of collateral and more on the importance of adequate appraisal of the loan applicant and his business, and close follow up and monitoring. Moreover, loans should be designed in such a way that they stimulate good repayment discipline, for example by providing access to larger loans in future or by offering the possibility of obtaining parallel loans.

Questions:

1. What kinds of risk affect agricultural lending? Is there a relationship between the risks farmers face in agricultural production and the risks of lending to them? What other risks do lenders have?

2. Which of the following affect production risks:

concentration on one crop; soil quality; livestock diseases; weather changes; lack of water; the farmer’s experience?

3. Identify the most important factors that influence the price and market risks of the five major agricultural products in your country.

4. How do politicians influence the moral hazard risk? Have they affected rural financial markets in your country?

5. What are the limitations of using farm land as loan collateral in your country?

17

2.2 The Costs

Lending to small farmers is generally a costly business. Clients are normally widely dispersed and long distances have to be travelled by loan officers and/or customers. The costs of loan appraisal, follow up and monitoring are more or less fixed and do not vary with the size of a loan, which makes it relatively more costly to administer small loans in comparison with large ones.

The key factors that determine lending costs are the need to collect detailed information about a potential borrower and his business and the need to monitor loan use closely. Information is vital in assessing and managing risks. Good client information serves as a partial substitute for a lack of collateral assets and as a means of countering moral hazard. However, in rural settings it is often difficult to obtain good information on potential clients.

Let’s have a closer look at some of the factors that influence transaction costs for agricultural loans:

i) Lack of credit history information There is a general absence of credit history information, as few financial institutions offer the possibility for rural people to build up track-records on their loan behaviour with them. Also there is an absence of credit reference bureaus in rural areas that collect and store information on borrowers.

To initiate a relationship between an agricultural lender and a client, therefore, is particularly costly and involves substantial “start-up” information costs. The financial institution itself must capture key information from the borrower, which requires time and experienced staff. Once loan track records have been established with an agricultural lender, client information costs diminish considerably. In order to achieve these economies of long-term relationship, the financial service provider must have an appropriate client information system and a comprehensive database which tracks customer performance and cost and risk profiles of their economic activities.

ii) Lack of farm records Small farmers usually have a low level of formal education and are not used to keeping documents and written records. Consequently, loan appraisal must often be based on information that is obtained by interviewing potential borrowers.

iii) Individuality of farm household clients

The heterogeneity of agricultural production conditions and the unique combination of farm and non-farm economic activities of each farm household, calls for a thorough, highly individual approach to loan appraisal. This need for carrying out a tailor-made agricultural loan analysis, which caters for the complexity of and the inter-relations between different farm income sources and expenditure requirements, is rather cost-intensive. It involves employing location and farming system specific loan appraisal techniques, loan product design and loan disbursement and repayment schedules.

iv) Farmers’ sensitivity to client transaction costs

Small farmers are particularly sensitive to high client transaction costs such as travelling to bank offices. Particularly during peak periods in the agricultural season, for example during planting and at harvest time, farmers face a heavy workload, which makes it difficult for them to spend time and money on visiting the offices of financial institutions. Successful agricultural lenders, therefore, often offer door-step banking services and visit clients at their homes or in their fields. Consequently, agricultural loan officers need to travel extensively. This leads to high costs for transport, personnel and other costs such as accident insurance.

18

Other rural financial institutions try to get closer to their customers by maintaining an extensive branch network. Establishing offices in rural areas lowers the transaction costs for the borrowers, but increases the overhead costs of the financial institution. Balancing both cost sides is a major challenge.

v) Seasonality of agricultural production

Typical agricultural production cycles mean that agricultural lending is a highly seasonal business. Given the fact that seasonal agricultural production activities are very time-sensitive, loan appraisal must be carried out within a short period of time and timely loan disbursements must be ensured. Consequently, agricultural lenders must adjust their institutional capability to these changes in workload during the year. There might be a need for employing additional, temporary staff in financial institutions during peak periods while in other months a reduced workload in agricultural lending must be off-set by involvement in other non-farm lending activities. Cost-effective staff and work load planning is therefore a challenging endeavour for agricultural lending institutions.

vi) Cost reducing strategies

Given the complex combination of risk structures and high transaction costs in agricultural lending, cost efficiency becomes essential. Thus, the implementation of highly streamlined policies, procedures and tools in agricultural lending is a must. However, standardisation of lending procedures has to be balanced by the need to meet the specific requirements of a diverse farmer clientele and the financing requirements of the different economic activities within each farm household. The following list summarises various approaches that may help to reduce the transaction costs of agricultural lending while maintaining a healthy overall loan portfolio:

Decentralisation of limited lending approval authority to branch managers and loan officers.

Delegation of parts of the loan appraisal, disbursement and supervision procedures to intermediary organisations that are in close contact with the borrowers, e.g. community groups and farmers organizations, local authorities and leaders, other agricultural support service providers, agricultural extension staff and business development centres, etc.

Definition of borrower eligibility criteria which will assist in the initial screening of loan applicants and eliminate at an early stage those who may be unable or unwilling to repay.

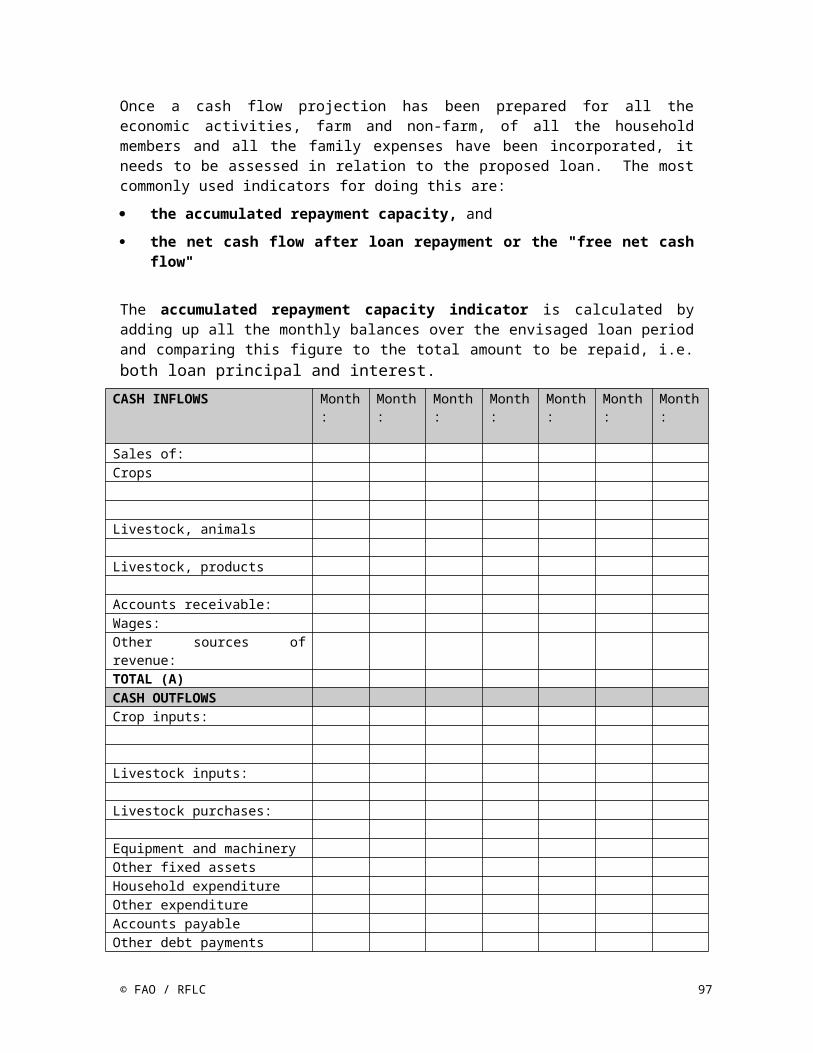

The use of standard loan appraisal formats and assessment indicators, the principles of which will be set out in the next chapter. Example computer spreadsheets for loan analysis and loan planning by loan officers will accompany this agricultural lending toolkit.

Reducing the transport costs of loan officers by using motorcycles.

Adoption of appropriate work and route-planning for loan officers in order to avoid excessive travelling costs.

Using staff performance evaluation and incentive schemes for loan officers and branch staff to encourage operational quality and efficiency.

19

Questions:

1. Summarise the key cost drivers in agricultural lending.2. Review measures to reduce the transaction costs in agricultural lending.

What implications do these measures have on loan default risk?

2.3 The Loan Officer

The knowledge, skills, experience and personality of the loan officer are the key to success in agricultural lending. Good loan officers are the “engines” that drive financial institutions. Loan officers should be in charge of the full loan cycle, i.e. they should be responsible for a loan all the way from the initial client visit until the loan is completely recovered. This has several advantages:

The loan officer is accountable for his/her own loan portfolio. If a loan becomes overdue, the loan officer who recommended or approved it carries the responsibility. He/she cannot blame others for being responsible for a bad loan and cannot delegate problem loans to other staff members.

Loan officers are the “human face” of the financial institution. They should establish a personal relationship with each borrower, which is particularly important for rural people. Confidence and mutual trust can only be established on a personal basis. The loan officer’s personal knowledge of clients is also important as loan decisions are taken not only on the basis of “hard facts”, but also on the officer's judgement of loan repayment willingness and the client’s management capacity.

As we have already noted, rural lenders rarely have access to credit reference systems – or if they exist, these systems give little or incomplete information about farmers' credit histories. Therefore, the loan officer who builds up an “institutional memory” of clients is particularly important in a rural context.

In addition, a data bank cataloguing the physical and economic characteristics of farming activities with their typical risk profiles in the geographic area of a bank branch office can only be built up with the support of the loan officers.

So, to be effective, agricultural loan officers need some quite specific skills, knowledge and personal qualities. For obvious reasons, the details of loan officer job profiles will vary from institution to institution and from regional context to regional context. However, we can look at an example of how a rural financial institution specified what it expected of its agricultural loan officers:

1. Loan officers must be ready and willing to spend the majority of their time outside the office, working in the field. They should be able to cope with uncomfortable working conditions in a rural environment.

2. Loan officers must have good communication skills. Since little or no written records are available in farm households, key information must be obtained by talking to people. Therefore, the ability to speak the local language or dialect is crucial. Loan officers must also be good listeners and able to detect information inconsistencies.

3. Loan officers must be able to make sound judgements and have the confidence to take appropriate decisions and actions.

4. Loan officers need a basic knowledge of agricultural production and economics. Practical experience is more important than academic knowledge. Thus a university degree in agricultural economics is not sufficient, unless combined with experience of working on farms.

5. Loan officers must be willing to work flexible hours. Farmers are used to starting their work very early in the morning and rural markets often take place at weekends, so loan officers will have to ensure that their work plans fit the time frames of rural life.

6. Loan officers must have basic accounting skills and be able to carry out calculations quickly when they start. However, experience with loan appraisal, including the construction of cash flow projections and balance sheets, and using computer spreadsheets, will be built up on the job.

7. Loan officers should have a motorcycle driving licence, as most clients cannot be reached by public transport or walking.

It is clearly quite a challenge to be an agricultural loan officer!

20

Questions:

3. Do you agree that “loan officers are the engine of a financial institution”? Why do people think so?

4. Can you define five key skills and personal characteristics that you think a loan officer in your institution should have?

5. How important is higher education when hiring loan officers for agricultural lending?

6. What are the advantages or disadvantages of training former agricultural extension staff as loan officers?

In the next chapter, we will start to use the imaginary financial institution, AGLEND, and the imaginary family Crespo, in order to illustrate many of the points we are making. Although AGLEND is based on a real life rural financial institution, it is important to remember that it is not a model or blue print for all situations. It simply provides you, the reader, with a concrete example to study and from which you may be able to develop solutions that are appropriate to your own context.

Here is some background information about AGLEND and the family Crespo:

AGLEND is a financial institution that was founded in the early nineties as an NGO-based microcredit organization. In the beginning, its target clientele were micro and small entrepreneurs in the urban area. However, since the majority of the population in the country live in rural areas, AGLEND decided to diversify its loan portfolio and provide loans to rural households as well. To do this effectively they redesigned their lending technology to suit the new market.

AGLEND followed a gradual approach by offering loans to rural entrepreneurs outside the agricultural sector first and then moving on to farm households and agricultural production. They started the agricultural lending operations in the valleys where good irrigation systems and physical infrastructure exists. From there, they moved on to other regions and now they have rural branches in the tropical lowlands, along the coast and in the highlands.

The farm households that get loans from AGLEND mainly produce cereals (maize, wheat, rice etc.), coffee and vegetables. There are also a considerable number of cattle farms (dairy and meat production). Most of them also obtain additional income from non-farm or off-farm economic activities.

AGLEND started with one basic loan product, an “equal monthly repayment” loan. However, they are now introducing more flexible loan terms, allowing repayments with varying amounts and less frequent instalments.

At present, AGLEND’s average loan size is USD500 for crop production and USD1,000 for cattle breeding.

21

The Crespo family farm at Eagle’s Peak, which is a small village in an Andean valley, about 15 km away from the district capital. Pedro and his wife, Maria, have three children, aged between 15 -20 years who live with them on the farm. The only daughter will marry soon and leave the farm. The two sons work occasionally as construction workers in the district capital, as does their father Pedro.

The family owns 4 hectares of fertile land. Two hectares are used for wheat production, one for sunflower and one for maize. In addition, Maria has a small garden close to the house, where she cultivates vegetables and flowers that she sells at the market in the district capital.

The family owns two oxen that are used primarily for ploughing. There is also one milk cow and a heifer. In addition, Maria keeps five hens. The milk and eggs are used just for family consumption and are not sold.

22

Chapter 3: Basic Features of Agricultural Lending

Objective: To introduce the main types and features of agricultural loan products and suggest ways that staff can build up knowledge about the agricultural sector and its markets, and identify good customers.

3.1 Types of Agricultural Loan Products

Loans to farmers can be provided for different purposes and with different lending terms. The most common loan types are:

Seasonal Loans for Working Capital. These loans are used to buy agricultural production inputs such as seeds, fertiliser and tools, as well as financing operating costs such as wages for hired farm labour. It is important that these loans fit in with the seasonal nature of agricultural production. They are usually short term, lasting only a few months.

Harvesting Loans. These are short-term loans used to hire labour or machinery at harvest time. They may also be used to finance other marketing costs.

Medium term Improvement Loans. This type of loan is used to invest in durable improvements to increase farm productivity, such as the installation of water pumps for irrigation. They are generally repaid over a period of 1-2 years.

Long term Investment Loans. These are loans which are used to purchase farm land or farm machinery for long-term use, such as tractors. Other uses for long term loans include buying breeding livestock and financing the establishment of perennial crops such as coffee, fruit trees or rubber trees that will require several years before they generate returns. Repayment periods usually extend over many years.

Loan duration

As you can see, loan terms range from a few months to a few years. The definition of whether a loan term is short, medium or long differs from country to country and from institution to institution. A possible classification refers to short term loans as loans with a repayment period of up to 12 months, medium term loans up to 36 months and long term loans beyond 36 months.

Medium and long term loans are more difficult for farmers to obtain, as they involve substantially higher risks for the agricultural lender. Establishing a long term client relationship, however, can reduce default risk and provide lending institutions with the information needed to assess other longer term investments in the future.

Disbursement schedules

Whether an entire loan amount is disbursed in one or several instalments will vary according to the loan purpose, i.e. the activities that they are meant to finance. In the case of wheat production, for example, there are different financial needs during the crop production cycle. At the beginning of the cycle, seeds are purchased. During the growing period, fertilisers and pesticides are applied at different times. At the end of the production cycle, there may be a need to finance extra labour or the hire costs of harvesting and threshing machinery.

Generally, loan disbursement and repayment schedules should reflect the actual situation of a farm household, with both disbursement and repayment based on the cash-flow situation. Therefore, the design of agricultural loans requires good information about clients’ financial needs and patterns of loan demand, the mix of agricultural activities involved and their associated cash-flows and risks.

23

Farmers do not only need finance for agriculture, but also for many other non-farm economic activities and household consumption. Thus they may need loans for:

Working or investment capital for non-farm enterprises;

Consumption purposes between planting and harvest;

Special events such as medical costs, school fees, weddings, funerals, etc.

Diversifying their loan portfolio over these different financing needs allows rural financial institutions to balance the seasonal nature of agricultural lending. While farm production loans will always be characterised by seasonal peak demand periods during the year, a lending institution with a diversified loan portfolio, including non-agricultural loans, will be able to manage their liquidity and profitability planning more easily.

Credit Lines or Overdrafts

A credit line or overdraft facility that allows farmers the flexibility to draw funds when they need it up to their allowed credit “ceiling”, which is equivalent to an approved loan amount, might offer a better solution for farm finance. However, credit lines can be more complex for financial institutions to manage and smaller institutions tend to stick with fixed term loan products for specific purposes with defined disbursement and repayment schedules.

Questions:

1. Which types of loans do small farmers usually ask for in your country?

2. Under what circumstances might a financial institution consider giving more than one loan at the same time to a client?

3. Do you think that your financial institution could manage credit lines for farmers?

3.2 Finding Good Customers

Financial institutions have to market their products like any other business. To build up an agricultural loan portfolio, therefore, it is important to undertake the promotion of agricultural loans in ways that ensure the prospect of capturing clients who have a sound income and risk profile, even though the first concern may be to reach out to small farm households.

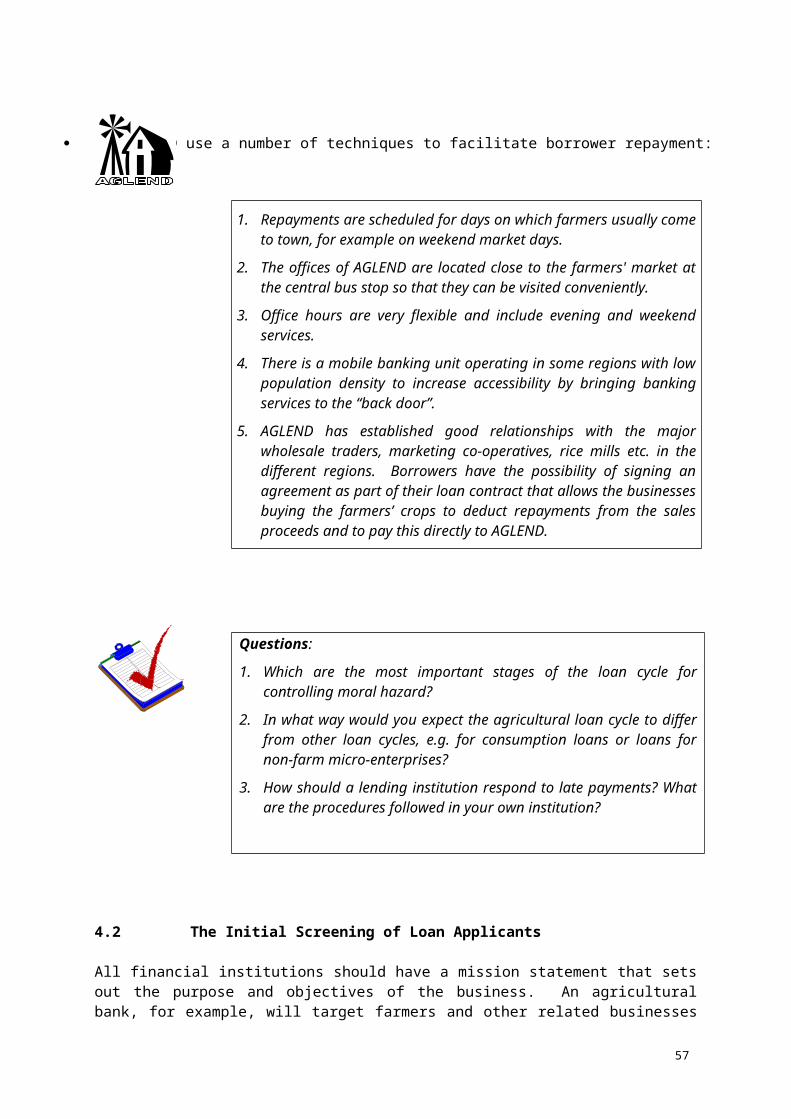

Let's look at how AGLEND targets its marketing efforts at high potential clients, thus securing good customers in a cost effective and efficient way.

1. They hold regular meetings with well-established irrigation co-operatives.

In the valleys, many farmers have formed irrigation co-operatives that distribute water rights to their members, for which they pay a fee. There are some well-managed irrigation co-operatives, while others operate poorly. The former have good irrigation systems, while those of the latter are in poor condition and do little to enhance farm production. Farmers who are members of the

24

well-organised irrigation co-operatives are more likely to be good borrowers than the farmers in the poorly-performing irrigation co-operatives. So AGLEND regional credit managers regularly attend the meetings of the well-managed irrigation co-operatives and provide information about the loan products of the institution. Farmers who are interested in obtaining loans can immediately submit loan applications.

2. They maintain close links with marketing co-operatives

There are several marketing co-operatives that support small coffee and rice producers. Farmers that are registered with these co-operatives have several advantages that enhance their income and risk profile. They have access to good storage facilities that help to preserve the quality of their crops. The co-operatives test the crop quality and certify it. Thus co-operative members find it easier to sell their crops and get better prices than farmers who sell their products on their own. AGLEND uses these co-operatives as a conduit for the marketing of their financial services. AGLEND loan officers participate in co-operative meetings, but also visit individual co-operative members to provide information on their financial services.

3. They liaise with dealers and shops that sell high-quality agricultural inputs and farm machinery centres that hire machines out to farmers.

AGLEND keeps contacts with well-known agricultural input supply and farm machinery business enterprises in the same way as they do with marketing co-operatives. From the farmer customers of these enterprises, AGLEND can identify reliable potential borrowers with suitable income and risk features. For example, farmers who buy internationally certified seeds and plastic sheets for covering crops should be able to generate higher incomes than producers who do not use these types of yield increasing agricultural inputs.

4. They try not to lose customers.

It is important from an institutional and economic perspective that the lender/borrower relationship does not end with loan repayment. Rather, loans should be seen as part of an on-going client relationship, ideally involving a range of financial products which cater for differing client needs. Once a loan is repaid, AGLEND loan officers seek an opportunity to speak with the client about future loans or the need for other financial products.

Questions:

4. With what local organisations and business enterprises should your financial institution liaise in order to identify good customers for agricultural loans?

3.3 Understanding Agriculture

A thorough understanding of the agricultural sector is a fundamental prerequisite for lending successfully to farm households. Sound knowledge of crop and livestock markets, production methods and external factors that can have an impact on agricultural production, is essential for loan officers, if they are to understand the income and risk profiles of potential clients. Such knowledge will help them to select good customers and make better loan appraisals, thus enhancing their loan portfolio quality. It will also enable the financial institution to design loan products that meet farmers' needs better and set appropriate loan conditions in terms of disbursement, repayment schedules and interest rates.

25

In order to build up their knowledge of the agricultural sector, lending officers of rural financial institutions are advised to establish a comprehensive database of key information on the agricultural production systems in their area, the economics of new technologies, agricultural commodity markets, and the risk profiles associated with specific agricultural production methods and products. During the loan appraisal process, it is of particular importance to be able to compare the information collected from loan applicants with that of an “average” farm household engaged in a similar activity in the same climatic region in order to decide whether the planned expenditures and expected income revenues are realistic or not. This type of data must be collated region by region, because the characteristics of agricultural activities vary from one location to the other. So an information database needs to include:

a. Production activity calendars for agricultural enterprises;

b. Efficiency or productivity indicators, e.g. yields per hectare for different crops;

c. Purchase prices for agricultural inputs and sales prices for agricultural products;

d. Weather information, e.g. rainfall data.

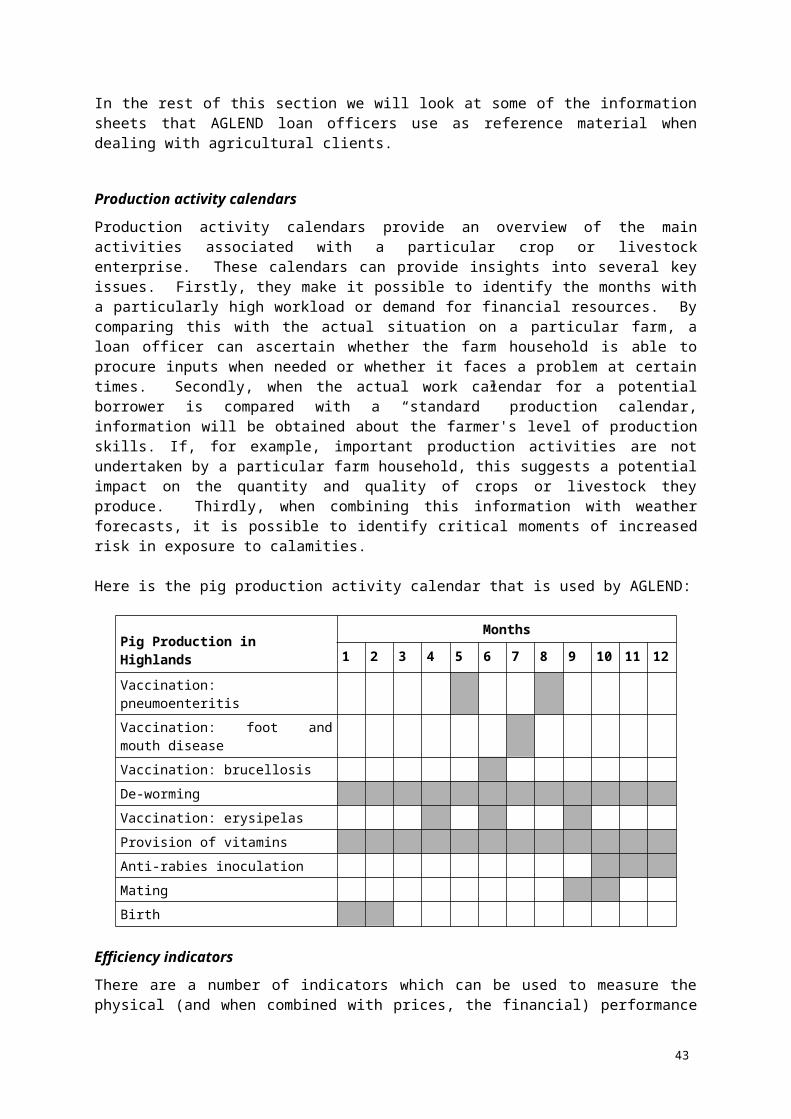

In the rest of this section we will look at some of the information sheets that AGLEND loan officers use as reference material when dealing with agricultural clients.

Production activity calendars

Production activity calendars provide an overview of the main activities associated with a particular crop or livestock enterprise. These calendars can provide insights into several key issues. Firstly, they make it possible to identify the months with a particularly high workload or demand for financial resources. By comparing this with the actual situation on a particular farm, a loan officer can ascertain whether the farm household is able to procure inputs when needed or whether it faces a problem at certain times. Secondly, when the actual work calendar for a potential borrower is compared with a “standard” production calendar, information will be obtained about the farmer's level of production skills. If, for example, important production activities are not undertaken by a particular farm household, this suggests a potential impact on the quantity and quality of crops or livestock they produce. Thirdly, when combining this information with weather forecasts, it is possible to identify critical moments of increased risk in exposure to calamities.

Here is the pig production activity calendar that is used by AGLEND:

Pig Production in HighlandsMonths

1 2 3 4 5 6 7 8 9 10 11 12

Vaccination: pneumoenteritisVaccination: foot and mouth disease

Vaccination: brucellosisDe-worming

Vaccination: erysipelasProvision of vitamins

Anti-rabies inoculationMating

Birth

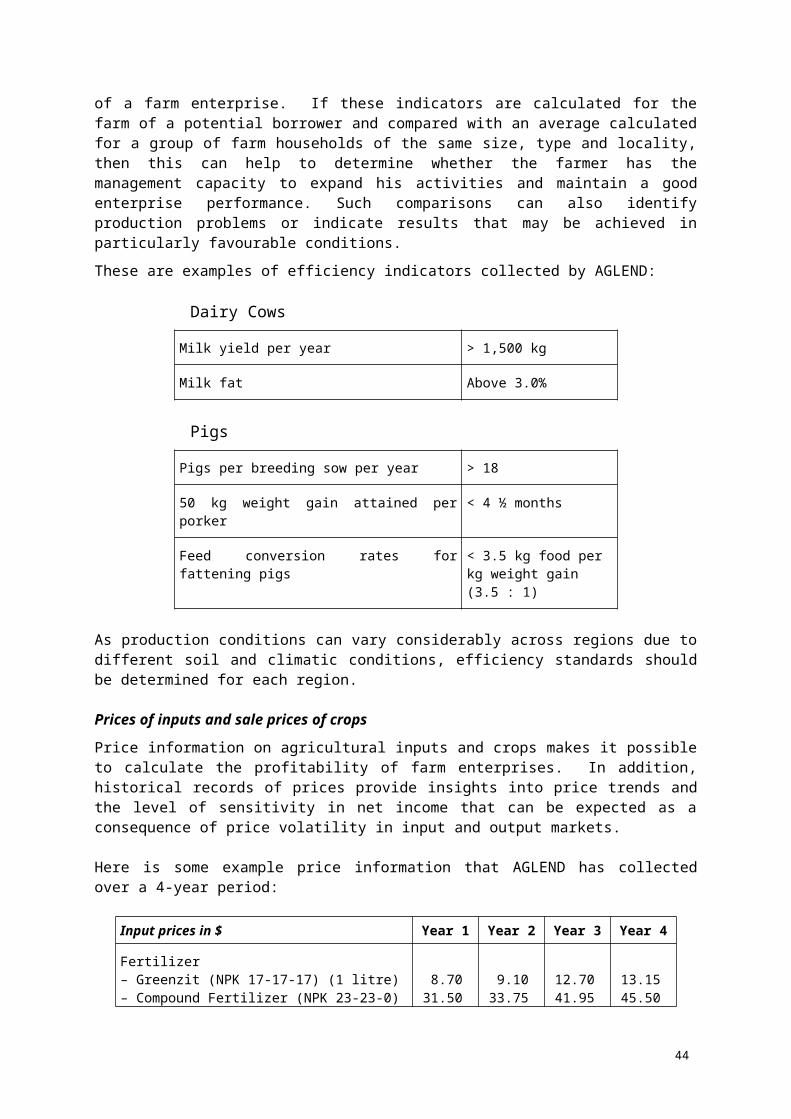

Efficiency indicators

26

There are a number of indicators which can be used to measure the physical (and when combined with prices, the financial) performance of a farm enterprise. If these indicators are calculated for the farm of a potential borrower and compared with an average calculated for a group of farm households of the same size, type and locality, then this can help to determine whether the farmer has the management capacity to expand his activities and maintain a good enterprise performance. Such comparisons can also identify production problems or indicate results that may be achieved in particularly favourable conditions.

These are examples of efficiency indicators collected by AGLEND:

Dairy Cows

Milk yield per year > 1,500 kg

Milk fat Above 3.0%

Pigs

Pigs per breeding sow per year > 18

50 kg weight gain attained per porker < 4 ½ months

Feed conversion rates for fattening pigs < 3.5 kg food per kg weight gain (3.5 : 1)

As production conditions can vary considerably across regions due to different soil and climatic conditions, efficiency standards should be determined for each region.

Prices of inputs and sale prices of crops

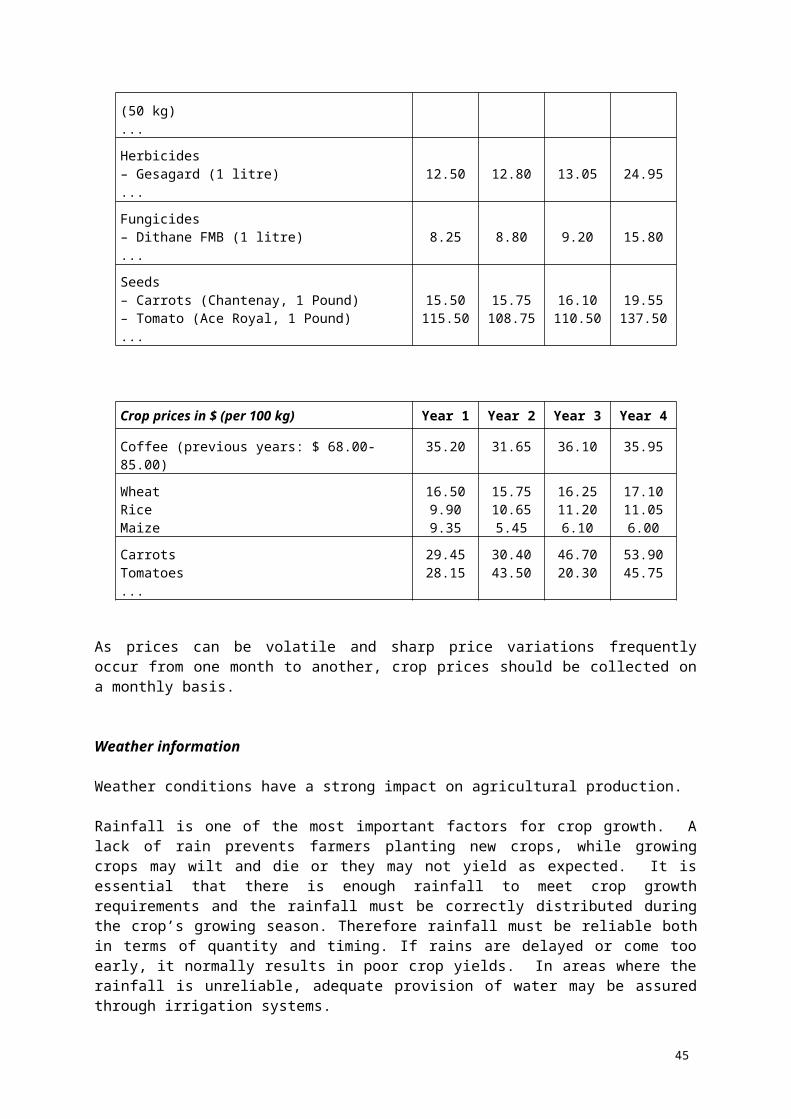

Price information on agricultural inputs and crops makes it possible to calculate the profitability of farm enterprises. In addition, historical records of prices provide insights into price trends and the level of sensitivity in net income that can be expected as a consequence of price volatility in input and output markets. Here is some example price information that AGLEND has collected over a 4-year period:

Input prices in $ Year 1 Year 2 Year 3 Year 4

Fertilizer– Greenzit (NPK 17-17-17) (1 litre)– Compound Fertilizer (NPK 23-23-0) (50 kg)...

8.7031.50

9.1033.75

12.7041.95

13.1545.50

Herbicides– Gesagard (1 litre)...

12.50 12.80 13.05 24.95

Fungicides– Dithane FMB (1 litre)...

8.25 8.80 9.20 15.80

Seeds– Carrots (Chantenay, 1 Pound)– Tomato (Ace Royal, 1 Pound)...

15.50115.50

15.75108.75

16.10110.50

19.55137.50

27

Crop prices in $ (per 100 kg) Year 1 Year 2 Year 3 Year 4

Coffee (previous years: $ 68.00-85.00) 35.20 31.65 36.10 35.95

WheatRice Maize

16.509.909.35

15.7510.655.45

16.2511.206.10

17.1011.056.00

CarrotsTomatoes...

29.4528.15

30.4043.50

46.7020.30

53.9045.75

As prices can be volatile and sharp price variations frequently occur from one month to another, crop prices should be collected on a monthly basis.

Weather information Weather conditions have a strong impact on agricultural production.

Rainfall is one of the most important factors for crop growth. A lack of rain prevents farmers planting new crops, while growing crops may wilt and die or they may not yield as expected. It is essential that there is enough rainfall to meet crop growth requirements and the rainfall must be correctly distributed during the crop’s growing season. Therefore rainfall must be reliable both in terms of quantity and timing. If rains are delayed or come too early, it normally results in poor crop yields. In areas where the rainfall is unreliable, adequate provision of water may be assured through irrigation systems.

Temperature affects agriculture in a number of ways. Each crop has an optimum range of temperature for its growth. If the temperature falls below the minimum, crop production is seriously affected. Temperature affects the incidence of diseases in crops. It also influences the biochemical growth processes, which have an impact on the rate of growth, crop maturity and crop quality.

Natural calamities like floods, hurricanes or drought do hit some locations with a certain frequency. In Bangladesh, for example, the lowlands are flooded every year and there have been major floods affecting the majority of the country every 5-10 years. Natural calamities have a devastating effect on the agricultural production and large parts or even the total harvest can be destroyed.

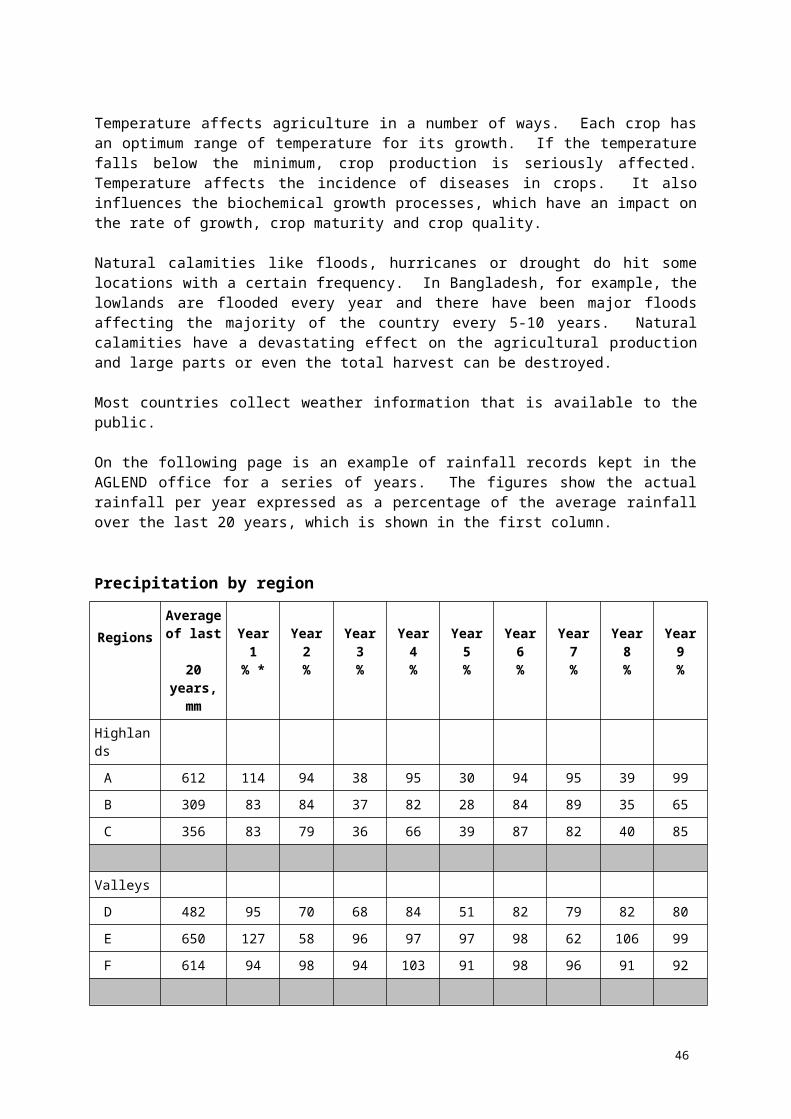

Most countries collect weather information that is available to the public.