Embed Size (px)

Citation preview

Table of Contents

Page

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

0

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

660 Newport Center Drive

Suite 950

Newport Beach, CA 92660

949.415.7321 - Office

949.415.7320 - Fax

WWW.CBCAPITAL.COM

MEMBER FINRA

March 8, 2017

A S S E T M A N A G E M E N T I N V E S T M E N T B A N K I N G R E S E A R C H

Presentation For:

Table of Contents

Page

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

1

Forecasts

Financial Overview

About CB Capital Partners 2

21

38

The Business Plan Process 12

2

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

About CB Capital Partners, Inc.

CB Capital Partners differentiates itself by providing customized financial

advisory, investment, and global research services

Conservative, disciplined and efficient approach

Providing innovative, long-term solutions to demanding client needs

Commitment to high quality services to high-growth companies

Senior-level commitment to provide resources for all areas of client

requirements from initial engagement to successful completion

3

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

About CB Capital Partners, Inc.

Corporate Vision & Mission

To deliver the highest quality financial advisory and investment services to

our clients

To bring innovative and value-added solutions to our clients through a

conservative and disciplined application of our diverse professional banking

talents

To be an ethical service provider for capital and ideas

To give our clients the confidence that they have partnered with a high-

quality advisor with the expertise and insight available to achieve their

performance-based business objectives

4

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

About CB Capital Partners, Inc.

CB Capital Partners’ Platform

Proven corporate finance model

Strong investment track record

Defined institutional industry

focus and expertise

Long term clients and partners

Developed international presence

Increased deal pipeline with

national coverage

Macroeconomic and industry

research

CB Capital Partners

Founded 2001

Broaden Deal Pipeline –

Equity Raises, Debt

Restructuring

M&A Sell-Side Assignment

Deal Pipeline Escalates

Larger Deal Size

2008

Strategic Board

Expanded

Established investment research

practice

20022004

2006

Growth Momentum

Expand New

Opportunities

20032005

2007

2010

Established

Larger Newport

Beach offices

Established

Broker-Dealer Five

9 Securities

2009

2012 2013 20142015

Established China-

based Practice

Expands into

Middle East

Established

India-based

Practice

2016

Established

Dallas, Texas

office

Established

Shanghai, China

office

2011

5

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

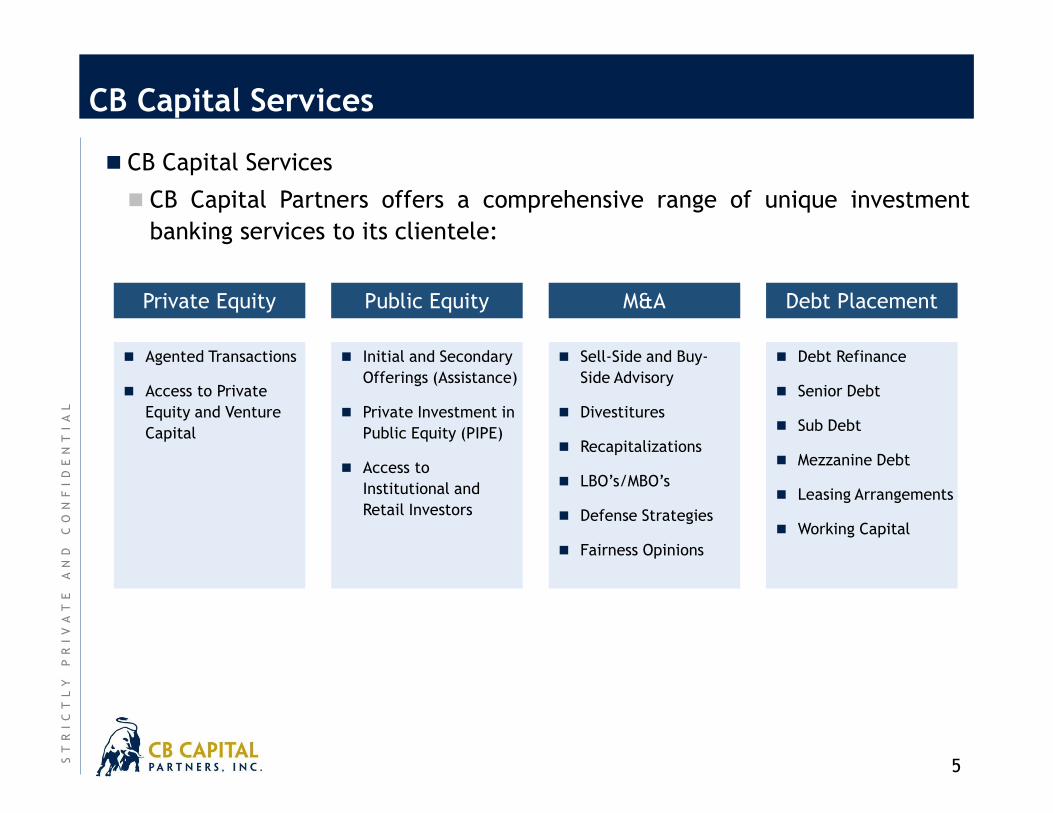

CB Capital Services

CB Capital Services

CB Capital Partners offers a comprehensive range of unique investment

banking services to its clientele:

Public Equity M&APrivate Equity

Agented Transactions

Access to Private

Equity and Venture

Capital

Debt Placement

Initial and Secondary

Offerings (Assistance)

Private Investment in

Public Equity (PIPE)

Access to

Institutional and

Retail Investors

Sell-Side and Buy-

Side Advisory

Divestitures

Recapitalizations

LBO’s/MBO’s

Defense Strategies

Fairness Opinions

Debt Refinance

Senior Debt

Sub Debt

Mezzanine Debt

Leasing Arrangements

Working Capital

6

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

CB Capital on Cover of Orange County Business Journal

Orange County Business Journal (OCBJ) recently published an extended

article about CB Capital Partners, Inc.'s deals in India extensively featuring

our India head, Mrs. Meghana Gaikwad.

7

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

CB Capital Research

CB Capital Research

CB Capital Research is headed by Mr. Henry To, CFA, CAIA, FRM. In that

capacity, Mr. To manages the general research process and publication of

CB Capital Partners’ Institutional Macro Research, which includes global

macroeconomics research, industry analyses, and insights on the

investment impact of certain economic themes and public policies. In

addition, Mr. To publishes for numerous financial journals including Forbes,

MarketWatch and Trader Planet.

8

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Broad Global Macro Experience and Coverage

Henry To, CFA, CAIA, FRMChief Investment Officer

Our research has been featured in:

Meghana GaikwadDirector

Over 10 investment professionals with over 100 investment transactions completed

Christopher BaclawskiManaging Partner & CEO

Henry To, CFA, CAIA, FRMPartner & CIO

Meghana GaikwadDirector, India

Bernardo OrtizAdvisor, Latin America

http://www.marketwatch.com/story/why

-gold-is-still-a-solid-long-term-investment-

2014-11-21

http://www.traderplanet.com/articles/view

/167267-the-euro-will-reach-parity-with-the-

u-s-dollar-in-2-3-years-stay-short/

http://www.forbes.com/sites/greatspeculat

ions/2015/03/23/investing-in-the-potential-

of-new-asian-infrastructure-investment-

bank/

9

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

CB Capital Research

Mr. Henry To is a regular contributor on Forbes, MarketWatch.com, and many

other reputed financial publications that provides business news, analysis

and stock market data

In addition, Mr. To is a regular commentator on various media outlets such as

CNBC, CCTV, and others

Source: CNBC 07-8-15

10

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

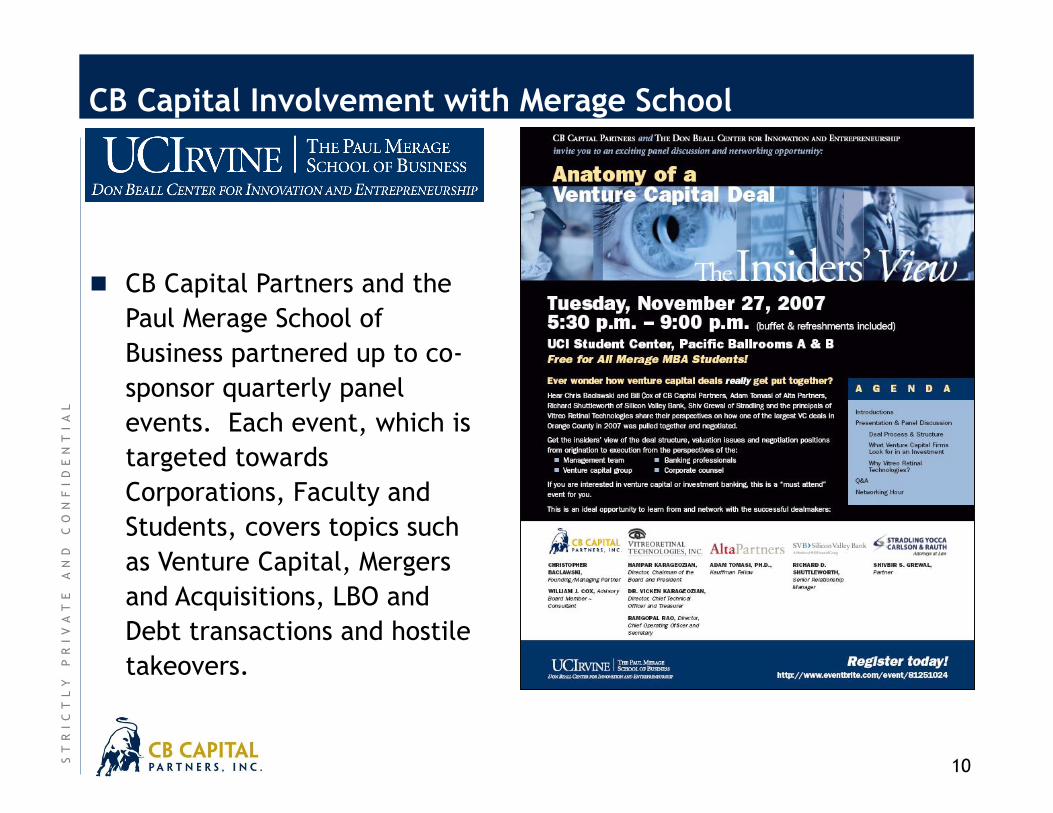

CB Capital Involvement with Merage School

CB Capital Partners and the

Paul Merage School of

Business partnered up to co-

sponsor quarterly panel

events. Each event, which is

targeted towards

Corporations, Faculty and

Students, covers topics such

as Venture Capital, Mergers

and Acquisitions, LBO and

Debt transactions and hostile

takeovers.

Table of Contents

Page

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

11

Forecasts

Financial Overview

About CB Capital Partners 2

21

38

The Business Plan Process 12

12

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Lifecycle of a Company

Venture

Capital

Institutional

Private

Equity

IPO

Secondary

Private Debt

Convertibles

Mergers &

Acquisitions

Product/Concept

Development

Senior

Management

Team

Industry

Market

Opportunity

Competition

Execution

Proven Concept

Sustainable

Competitive

Advantage

Achievable

Distribution

Market Size vs.

Market Niche

Infrastructure

Financing

Continued

Growth

Opportunities

Predictability

Backlog

Valuation

Credit Quality

Cash Flow

Stability

Synergies

Control

Complementary

Management

Consolidating

Industry

Valuation

Company Attributes

Our

Focus

Here

13

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Business Plan

When raising venture capital, thorough planning in the form of a professional

Business Plan will help you obtain sufficient funds to achieve your milestones

at an acceptable valuation, from value-added investors and with minimal

disruption to your company. Today I will offer you some guidelines and

describe the valuation process in detail.

14

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Business Plan

Smart entrepreneurs need to do a lot of homework and planning before

seeking funds from venture capitalists eager to invest in start-up companies.

You can increase your chances of raising capital for the start-up through good

planning and an understanding of how potential investors treat valuation.

15

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Investors

Venture capital firms have money to invest (over $10 billion during the past

four years), and many are interested in technology start-ups because returns

on medical investments have been good.

Targeted Venture Investors focus on specific industries with individual

strategic objectives.

Know your audience.

16

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

1. To set a direction for the Company.

2. To capture the interest of potential venture capital investors.

3. To project confidence to potential investor and project value.

Business Plan Objectives

17

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Business Plan

Good business plans are usually between 20 and 50 pages in length, with

optional supporting data (articles, glossary of terms, endorsement letters)

placed in an appendix or addendum.

18

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Fund Raising essentials

Before beginning a search for venture capital, most start-ups will write a

Business Plan describing what they plan to do and how they plan to do it. The

following is a summary of what should be included in each section of the

plan:

19

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Business Plan Outline

Executive summary/Company strategy;

Technology/products

Technology description, Development plan, Proprietary protection

Markets/marketing:

Markets, Selling and distribution, Competition, Forecasts

Industrial/Regulatory

Manufacturing and operations:

Facilities, Equipment, Process, Cost of goods sold;

Management team

Financials

Profit and loss, Balance sheet, Cash flow (sources and uses);

Risks

Appendices

Table of Contents

Page

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

20

Forecasts

Financial Overview

About CB Capital Partners 2

21

38

The Business Plan Process 12

21

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

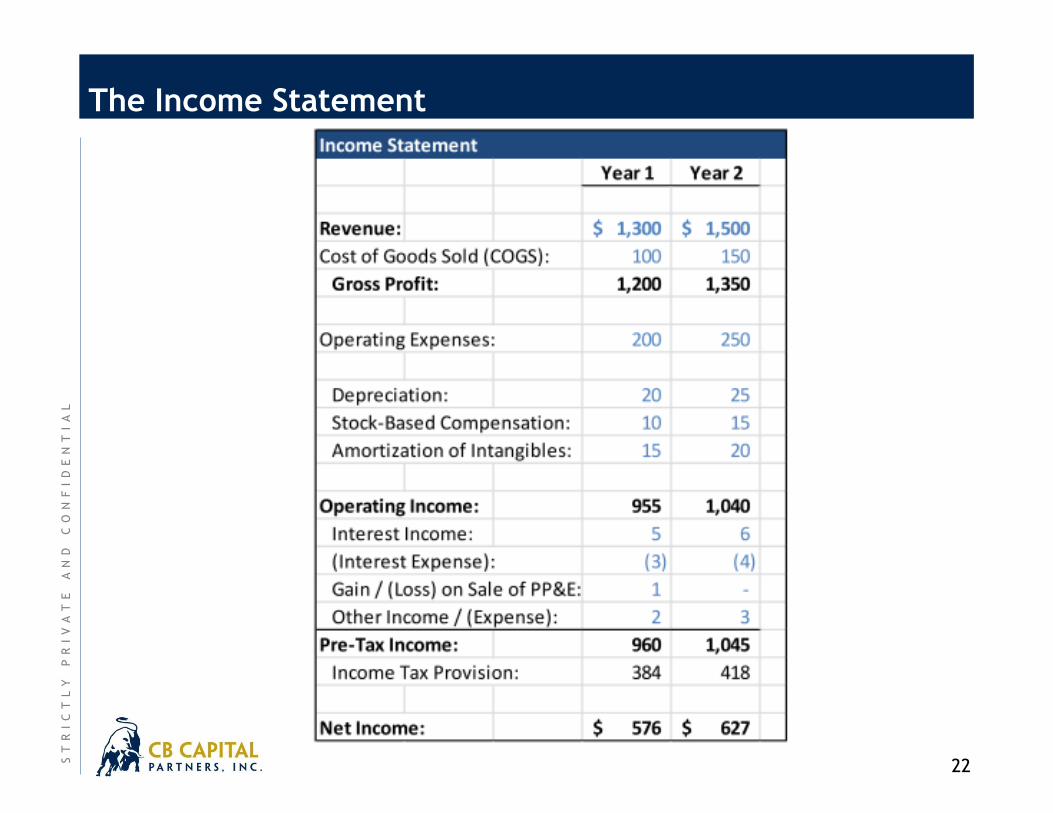

The Income Statement

The Income Statement lists a company’s revenue, expenses, and taxes, with

its after-tax profit at the very bottom, over a period of time (one quarter,

one month, or one year).

To appear on the Income Statement, each item must meet the following

criteria:

It must correspond to the period shown on the Income Statement only – if

you’re paying for an asset that will last for 10-20 years, it would not appear

on a 1-year Income Statement.

It must affect the company’s taxes. For example, interest paid on debt is

tax-deductible so it appears on the Income Statement… but repaying debt

principal is not tax-deductible, so it does not appear on the Income

Statement.

22

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Income Statement

23

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Income Statement

The 4 main sections to be aware of:

Revenue and Cost of Goods Sold (COGS): Revenue is the value of the

products/services that a company sells in the period (Year 1 or Year 2), and

COGS represents the expenses that are linked directly to the sale of those

products/services.

Operating Expenses: Items that are not directly linked to product sales –

employee salaries, rent, marketing, research and development, as well as

non-cash expenses like Depreciation and Amortization.

Other Income and Expenses: This goes between Operating Income and Pre-

Tax Income. Interest shows up here, as well as items such as Gains and

Losses when Assets are sold, Impairment Charges, Write-Downs, and

anything else that is not part of the company’s core business operations.

Taxes and Net Income: Net Income represents the company’s “bottom line”

– how much in after-tax profits it has earned. Net Income = Revenue –

Expenses – Taxes.

24

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Income Statement

A few points on Income Statement revenue, expenses, and taxes:

They do not need to be related to a company’s operational activities –

Gains and Losses on asset sales, Depreciation, and Interest Expense still

appear on the IS but are not related to everyday business.

They do not need to be cash expenses (or cash revenue) – for example,

Depreciation and Amortization are both non-cash expenses. Also, companies

often record revenue and expenses here before they receive or pay them in

cash.

Sometimes, items may be embedded in other items – for example,

sometimes Depreciation is included in COGS or Operating Expenses; other

times it is a separate item.

25

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Income Statement

Here are more rules of thumb about what appears on the Income Statement:

Always Appears: Revenue, COGS, Operating Expenses, Depreciation,

Amortization, Stock-Based Compensation, Interest, Gains / (Losses), Write-

Downs, Other Income / (Expenses)

Never Appears: Capital Expenditures, Purchasing or Selling Investments and

PP&E (Plants, Property & Equipment), Dividends, Issuing or Repaying Debt

Principal, Issuing or Repurchasing Shares, Changes to Balance Sheet Items

such as Cash, Debt, Accounts Receivable, Accounts Payable, and so on

=> The “Always Appears” do affect the company’s taxes (e.g. paying an

employee’s salary reduces the company’s taxable income); and They

correspond to the period shown on the Income Statement (e.g. revenue in

Year 1 refers to all sales to customers in Year 1… not Year 2). The opposite is

true for “Never Appears”

26

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Balance Sheet

The Balance Sheet shows the company’s resources – its Assets – and how it

acquired those resources – its Liabilities & Equity – at a specific point in time.

27

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Balance Sheet

Here are the key Balance Sheet rules:

Assets must always equal Liabilities + Equity – no exceptions.

An Asset is an item that will result in, directly or indirectly, additional cash

in the future.

A Liability is an item that will result in, directly or indirectly, less cash in

the future. Most Liabilities are related to external parties – payments owed

to suppliers, or borrowed money, for example. Liabilities are used to fund a

business.

Equity line items are similar to Liabilities (used to fund a business), but

they refer to the company’s own internal operations rather than external

parties.

28

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Balance Sheet Definitions of key Assets:

Cash: Just like cash in your bank account.

Short-Term Investments: Less liquid than cash – Certificates of Deposit (CDs)

and money-market accounts and such.

Accounts Receivable: The company has recorded this as revenue on its

Income Statement but hasn’t received it in cash yet. It’s like an “IOU” from a

customer. And it will turn into cash when the customer pays.

Prepaid Expense: The company has paid these expenses in cash but hasn’t

recorded them as expenses on the Income Statement yet.

Inventory: What they need to manufacture and sell products – for a company

like Apple, all the parts that go into iPhones and iPads.

29

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Balance Sheet Definitions of key Assets: (Cont’d)

PP&E: Factories, buildings, land, equipment, and anything else that will last

for over a year and contribute to the company’s core business.

Other Intangible Assets: Patents, trademarks, intellectual property… usually

the result of acquisitions. Similar to Goodwill, but this balance amortizes

(decreases) over time as these items “expire.”

Long-Term Investments: Less liquid and longer-lasting investments than Cash

or Short-Term Investments.

Goodwill: The premium that the company has paid over other companies’

Shareholders’ Equity when acquiring them.

30

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Balance Sheet Definitions of key Liabilities:

Revolver: Similar to a “credit card” for a company; it borrows money as

needed and must repay it quickly.

Accounts Payable: The company has recorded these as expenses on the

Income Statement, but hasn’t yet paid them out in cash yet – used for one-

time items with specific invoices, such as payment for legal services.

Accrued Expenses: The company has recorded these as expenses on the

Income Statement, but hasn’t yet paid them out in cash yet – used for

recurring monthly items without invoices, such as employee wages,

utilities, and rent.

Deferred Revenue: The company has collected cash in advance from

customers for products/services yet to be delivered, and it will recognize

this as real revenue over time.

Deferred Tax Liability: The company has paid lower taxes than what it

really owes, and needs to make it up by paying additional taxes to the

government in the future.

Long-Term Debt: Similar to a mortgage or a car loan: debt that is due and

must be repaid in over a year’s time.

31

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Balance Sheet Definitions of Equity line items:

Common Stock & Additional Paid-In Capital (APIC): This represents the

market value of shares at the time those shares were issued by the

company. When a company goes public, the total dollar value of shares

issued shows up here. This does not change even if the share price changes

afterward.

Treasury Stock: This represents the cumulative value of shares the company

has repurchased from investors. This does not change even if the share

price changes afterward.

Retained Earnings: This represents the company’s saved up, after-tax

profits (minus any dividends it has issued). This is like the $200K you saved

up, after-taxes, in our “personal Balance Sheet” example above.

Accumulated Other Comprehensive Income (AOCI): This is a section for

“miscellaneous saved-up income” – you see items like the effect of foreign

currency exchange rate changes here, as well as unrealized gains and losses

on certain types of securities (i.e. if their values go up or down but the

company has not yet sold them).

32

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Cash Flow Statement Similar to the Income Statement, the Cash Flow Statement tracks changes

over a period of time (one month, one quarter, or one year). It exists for 2

reasons:

You may have shown non-cash revenue or expenses on the Income

Statement. These need to be adjusted on the Cash Flow Statement to

determine how your cash balance actually changes.

There may be additional cash inflows and outflows that have not appeared

on the Income Statement. For example, Capital Expenditures and Dividends

are both real cash expenses. You need to factor these in to figure out how

your cash balance really changes by.

33

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Cash Flow Statement

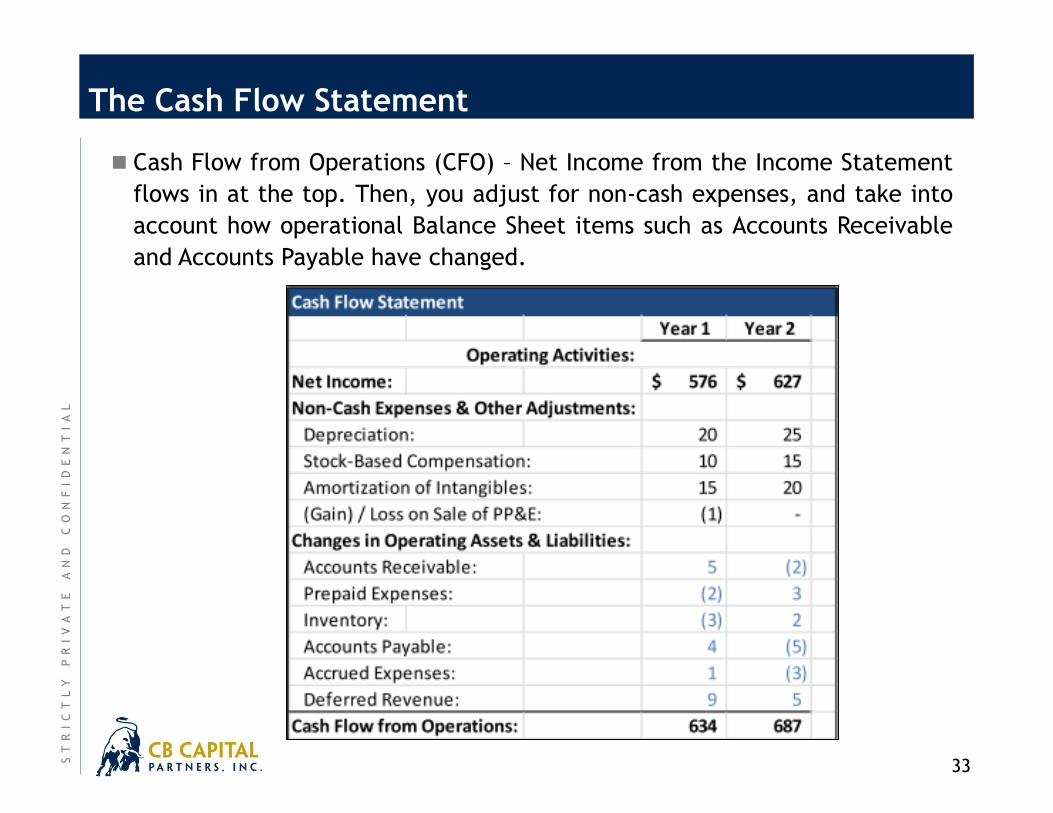

Cash Flow from Operations (CFO) – Net Income from the Income Statement

flows in at the top. Then, you adjust for non-cash expenses, and take into

account how operational Balance Sheet items such as Accounts Receivable

and Accounts Payable have changed.

34

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Cash Flow Statement

Cash Flow from Investing (CFI) – Anything related to the company’s

investments, acquisitions, and PP&E shows up here. Purchases are negative

because they use up cash, and sales are positive because they result in

more cash.

35

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

The Cash Flow Statement

Cash Flow from Financing (CFF) – Items related to debt, dividends, and

issuing or repurchasing shares show up here.

36

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

How To Link The Three Statements First, Net Income from the bottom of the Income Statement becomes the top

line of the Cash Flow Statement.

Second, you add back non-cash expenses from the Income Statement (and flip

the signs of items such as Gains and Losses).

Third, you reflect changes in operational Balance Sheet line items – if an

Asset goes up, cash flow goes down and vice versa; if a Liability goes up, cash

flow goes up and vice versa.

Fourth, you reflect Purchases and Sales of Investments and PP&E in Cash Flow

from Investing.

Fifth, you reflect Dividends, Debt issued or repurchased, and Shares issued or

repurchased in Cash Flow from Financing.

Sixth, you calculate the net change in cash at the bottom of the CFS, and

then link this into cash at the top of the next period’s Balance Sheet.

Seventh, you update the Balance Sheet to reflect changes in Cash, Debt,

Equity, Investments, PP&E, and anything else that came from the Cash Flow

Statement.

Table of Contents

Page

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

37

Forecasts

Financial Overview

About CB Capital Partners 2

21

38

The Business Plan Process 12

38

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Financial Model Example

XYZ Corp Confidential - Not for Distribution

Series A Model

Table of Contents

Section 1 - Summary Page

1. Summary Income Statement 2

2. Summary Balance Sheet 3

3. Summary Cash Flow Statement 4

4. Headcount and Personnel Expenses 5

Section 2 - Assumptions

5. Revenue Assumptions 6

6. Policies 7

7. Operating Expenses 9

3/8/2017

39

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

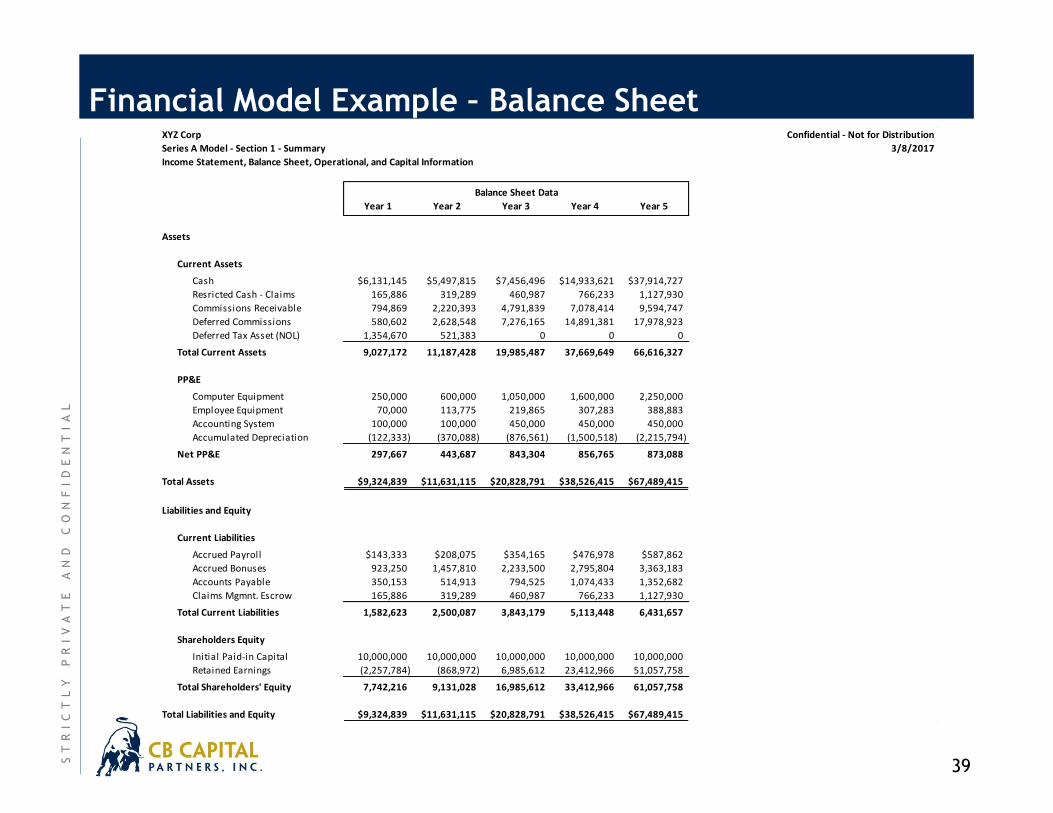

Financial Model Example – Balance Sheet XYZ Corp Confidential - Not for Distribution

Series A Model - Section 1 - Summary

Income Statement, Balance Sheet, Operational, and Capital Information

Balance Sheet Data

Year 1 Year 2 Year 3 Year 4 Year 5

Assets

Current Assets

Cash $6,131,145 $5,497,815 $7,456,496 $14,933,621 $37,914,727

Resricted Cash - Claims 165,886 319,289 460,987 766,233 1,127,930

Commissions Receivable 794,869 2,220,393 4,791,839 7,078,414 9,594,747

Deferred Commissions 580,602 2,628,548 7,276,165 14,891,381 17,978,923

Deferred Tax Asset (NOL) 1,354,670 521,383 0 0 0

Total Current Assets 9,027,172 11,187,428 19,985,487 37,669,649 66,616,327

PP&E

Computer Equipment 250,000 600,000 1,050,000 1,600,000 2,250,000

Employee Equipment 70,000 113,775 219,865 307,283 388,883

Accounting System 100,000 100,000 450,000 450,000 450,000

Accumulated Depreciation (122,333) (370,088) (876,561) (1,500,518) (2,215,794)

Net PP&E 297,667 443,687 843,304 856,765 873,088

Total Assets $9,324,839 $11,631,115 $20,828,791 $38,526,415 $67,489,415

Liabilities and Equity

Current Liabilities

Accrued Payroll $143,333 $208,075 $354,165 $476,978 $587,862

Accrued Bonuses 923,250 1,457,810 2,233,500 2,795,804 3,363,183

Accounts Payable 350,153 514,913 794,525 1,074,433 1,352,682

Claims Mgmnt. Escrow 165,886 319,289 460,987 766,233 1,127,930

Total Current Liabilities 1,582,623 2,500,087 3,843,179 5,113,448 6,431,657

Shareholders Equity

Initial Paid-in Capital 10,000,000 10,000,000 10,000,000 10,000,000 10,000,000

Retained Earnings (2,257,784) (868,972) 6,985,612 23,412,966 51,057,758

Total Shareholders' Equity 7,742,216 9,131,028 16,985,612 33,412,966 61,057,758

Total Liabilities and Equity $9,324,839 $11,631,115 $20,828,791 $38,526,415 $67,489,415

3/8/2017

40

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Financial Model Example - Income Statement XYZ Corp Confidential - Not for Distribution

Series A Model - Section 1 - Summary

Income Statement, Balance Sheet, Operational, and Capital Information

Income Statement Data % of Revenue

Year 1 Year 2 Year 3 Year 4 Year 5 Year 1 Year 2 Year 3 Year 4 Year 5

Revenue

Commissions - C&D $0 $439,701 $1,985,006 $4,573,195 $8,254,280 0.0% 3.1% 6.0% 8.4% 10.3%

Commissions - CRE 1,675,885 5,879,426 13,271,185 20,383,383 27,592,878 42.3% 41.5% 40.1% 37.5% 34.6%

Commissions - C&I 2,284,647 7,650,791 16,447,195 23,998,385 30,776,672 57.7% 54.0% 49.7% 44.1% 38.6%

Risk / Profit Sharing 0 188,430 1,413,082 5,468,043 13,155,842 0.0% 1.3% 4.3% 10.0% 16.5%

Total Revenue 3,960,532 14,158,348 33,116,468 54,423,007 79,779,672 100.0% 100.0% 100.0% 100.0% 100.0%

Operating Costs

Underwriting Expenses 1,342,870 2,512,193 5,495,092 8,834,150 11,988,101 33.9% 17.7% 16.6% 16.2% 15.0%

Claims Expenses 165,886 585,127 1,327,891 2,175,776 2,961,059 4.2% 4.1% 4.0% 4.0% 3.7%

Marketing Expenses 1,299,750 1,949,751 2,623,442 3,285,673 4,184,042 32.8% 13.8% 7.9% 6.0% 5.2%

Distribution Expenses 1,046,867 2,218,679 4,273,598 5,522,159 6,851,431 26.4% 15.7% 12.9% 10.1% 8.6%

Finance & Risk Mgmt Expenses 1,260,125 1,349,519 1,635,281 1,686,175 1,738,741 31.8% 9.5% 4.9% 3.1% 2.2%

MIS Expenses 342,600 398,996 581,001 771,621 971,281 8.7% 2.8% 1.8% 1.4% 1.2%

Legal Expenses 300,000 547,973 812,415 829,426 846,997 7.6% 3.9% 2.5% 1.5% 1.1%

HR Expenses 419,400 220,566 588,632 643,597 657,186 10.6% 1.6% 1.8% 1.2% 0.8%

Director and Executive Expenses 1,143,800 1,251,563 1,259,508 1,267,641 1,275,968 28.9% 8.8% 3.8% 2.3% 1.6%

Overhead Expenses 243,816 724,750 1,518,494 2,632,690 3,743,390 6.2% 5.1% 4.6% 4.8% 4.7%

Total Operating Costs 7,565,114 11,759,116 20,115,354 27,648,909 35,218,197 191.0% 83.1% 60.7% 50.8% 44.1%

EBITDA (3,604,581) 2,399,232 13,001,114 26,774,097 44,561,475 NA 16.9% 39.3% 49.2% 55.9%

Depreciation Expense 122,333 247,755 506,473 623,957 715,277 3.1% 1.7% 1.5% 1.1% 0.9%

Operating Income (3,726,915) 2,151,477 12,494,641 26,150,141 43,846,199 NA 15.2% 37.7% 48.0% 55.0%

Other Income (Expenses)

Interest Income (Expenses) 114,461 70,622 72,693 133,626 385,468 2.9% 0.5% 0.2% 0.2% 0.5%

Pre-Tax Income (3,612,454) 2,222,099 12,567,335 26,283,767 44,231,667 NA 15.7% 37.9% 48.3% 55.4%

Income Taxes (1,354,670) 833,287 4,712,750 9,856,413 16,586,875 NA 5.9% 14.2% 18.1% 20.8%

Net Income ($2,257,784) $1,388,812 $7,854,584 $16,427,354 $27,644,792 NA 9.8% 23.7% 30.2% 34.7%

3/8/2017

41

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Financial Model Example – Cash Flow

XYZ Corp Confidential - Not for Distribution

Series A Model - Section 1 - Summary

Income Statement, Balance Sheet, Operational, and Capital Information

Cash Flow Data

Year 1 Year 2 Year 3 Year 4 Year 5

Net Income ($2,257,784) $1,388,812 $7,854,584 $16,427,354 $27,644,792

Operating Activities

Depreciation 122,333 247,755 506,473 623,957 715,277

Decrease (Increase) in Res. Cash (165,886) (153,403) (141,698) (305,246) (361,697)

Decrease (Increase) in C/R (794,869) (1,425,524) (2,571,446) (2,286,574) (2,516,333)

Decrease (Increase) in Def. Com. (580,602) (2,047,946) (4,647,617) (7,615,217) (3,087,542)

Decrease (Increase) in NOL (1,354,670) 833,287 521,383 0 0

Increase (Decrease) in C/L 1,582,623 917,464 1,343,092 1,270,270 1,318,209

Cash Flow from Operations (1,191,072) (1,628,366) (4,989,813) (8,312,811) (3,932,087)

Financing Activities

Financing Activities 0 0 0 0 0

Cash Flow from Financing 0 0 0 0 0

Investing Activities

Capital Expenditures (420,000) (393,775) (906,090) (637,418) (731,599)

Cash Flow from Investing (420,000) (393,775) (906,090) (637,418) (731,599)

Change in Cash ($3,868,855) ($633,330) $1,958,681 $7,477,125 $22,981,105

3/8/2017

42

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Financial Model Example – Supplemental Information

XYZ Corp Confidential - Not for Distribution

Series A Model - Section 1 - Summary

Income Statement, Balance Sheet, Operational, and Capital Information

Income Statement Data

Year 1 Year 2 Year 3 Year 4 Year 5

Operating Information ($ in millions)

Year End Policies (New) 600 1,625 3,067 4,249 5,119

Year End Policies (Renewal) 0 480 1,684 3,494 5,362

Total 600 2,105 4,751 7,743 10,482

Personal Guarantee Liability $1,200 $4,210 $9,502 $15,486 $20,963

Premium Revenue $16.6 $58.5 $132.8 $217.6 $296.1

Average Premium Rate 1.38% 1.39% 1.40% 1.41% 1.41%

Revenue - Bank Channel $329,742 $1,491,888 $3,666,514 $6,470,292 $9,999,813

Revenue - Direct Marketing $3,630,791 $12,478,030 $28,036,872 $42,484,671 $56,624,018

Revenue - General Marketing $0 $0 $0 $0 $0

Personnel Information (Excludes Sales Personnel Hired Immediately Prior to Year End)

Total Employees 28 45 85 117 146

Additional Profit Share Information (Final Payments Four Years After Year of Operations)

Estimated Future Payments $2,216,495 $9,889,493 $26,433,200 $50,554,120 $77,839,435

Cash Requirement $10,000,000

3/8/2017