Embed Size (px)

Citation preview

IFRS FINANCIAL STATEMENTS 2016

Table of contentsTABLE OF CONTENTS...........................................................................................................................................................2FINANCIAL HIGHLIGHTS.......................................................................................................................................................3GENERAL INFORMATION.....................................................................................................................................................4DIRECTORS’ REPORT............................................................................................................................................................5REPORT OF SHARIA SUPERVISORY BOARD..........................................................................................................................7REPORT OF THE INDEPENDENT AUDITORS..........................................................................................................................8STATEMENT OF COMPREHENSIVE INCOME.........................................................................................................................9STATEMENT OF FINANCIAL POSITION................................................................................................................................10STATEMENT OF CHANGES IN EQUITY.................................................................................................................................11STATEMENT OF CASH FLOWS............................................................................................................................................121. REPORTING ENTITY..............................................................................................................................................132. BASIS OF PREPARATION.......................................................................................................................................143. SIGNIFICANT ACCOUNTING POLICIES...................................................................................................................144. FINANCIAL RISK MANAGEMENT...........................................................................................................................225. INCOME FROM ISLAMIC FINANCE.......................................................................................................................376. RETURN TO CUSTOMERS......................................................................................................................................377. FEE AND COMMISSION INCOME..........................................................................................................................378. FEES AND COMMISSION EXPENSES.....................................................................................................................389. NET TRADING INCOME.........................................................................................................................................3810. OTHER OPERATING INCOME................................................................................................................................3811. PERSONNEL EXPENSES........................................................................................................................................3812. OPERATING LEASE EXPENSE................................................................................................................................3913. ADMINISTRATION AND GENERAL EXPENSES.......................................................................................................3914. INCOME TAX EXPENSE.........................................................................................................................................3915. INCOME TAX LIABILITY.........................................................................................................................................4016. DEFERRED TAX EXPENSE......................................................................................................................................4017. EARNINGS PER SHARE..........................................................................................................................................4118. CASH AND CASH EQUIVALENTS............................................................................................................................4219. ISLAMIC FINANCING AND RELATED ASSETS.........................................................................................................4220. HELD-TO-MATURITY INVESTMENT SECURITIES....................................................................................................4321. INVESTMENTS IN PROPERTIES.............................................................................................................................4322. PROPERTY, PLANT AND EQUIPMENT....................................................................................................................4323. INTANGIBLE ASSETS............................................................................................................................................4424. OTHER ASSETS.....................................................................................................................................................4525. DEPOSITS FROM BANKS......................................................................................................................................4526. DEPOSITS FROM CUSTOMERS.............................................................................................................................4627. OTHER LIABILITIES...............................................................................................................................................4628. STATEMENT OF CHANGES IN EQUITY...................................................................................................................4629. OFF BALANCE SHEET CONTINGENCIES AND COMMITMENTS ........................................................................4730. RELATED PARTIES ................................................................................................................................................4831. SUBSEQUENT EVENTS.........................................................................................................................................4932. NEW STANDARDS, INTERPRETATIONS AND AMENDMENTS TO EXISTING STANDARDS THAT ARE NOT YET EFFECTIVE.............................................................................................................................................49VALUE ADDED STATEMENT................................................................................................................................................51LIST OF TOP 20 SHAREHOLDERS........................................................................................................................................52

1

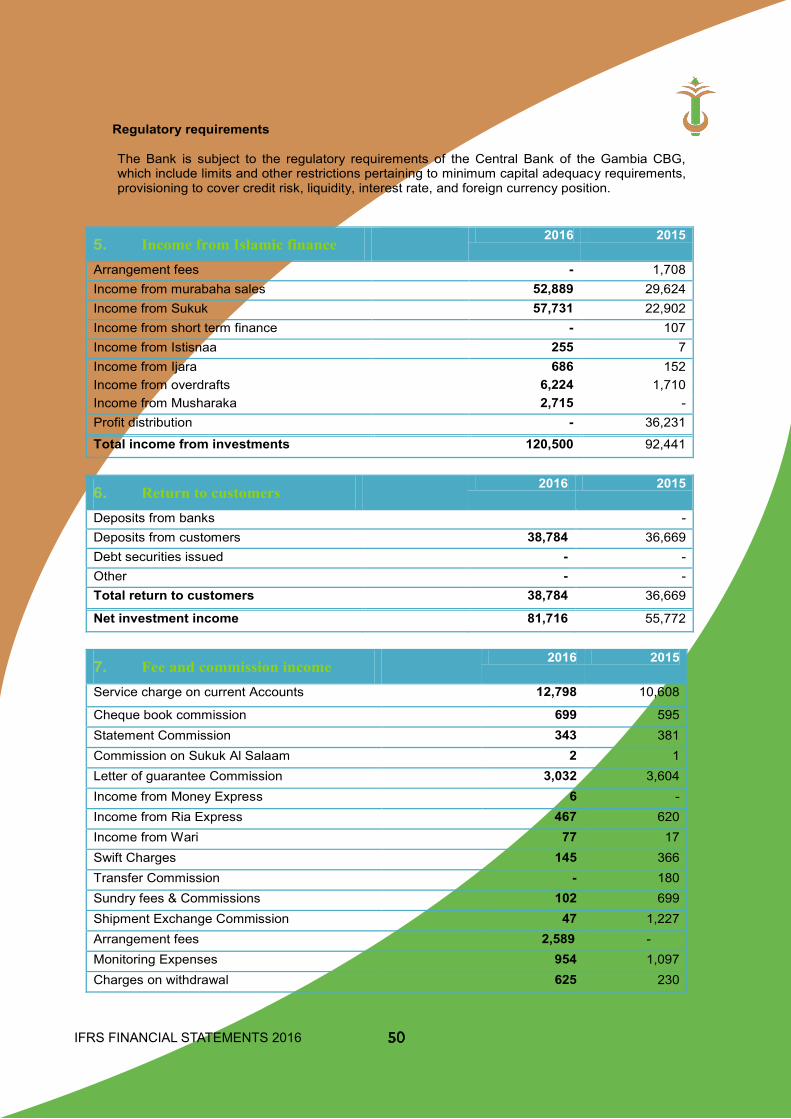

IFRS FINANCIAL STATEMENTS 2016

VISION STATEMENT“To be distinctive in all aspects of our business”

MISSION STATEMENT“To provide quality and accessible banking services based on Islamic

financial principles with equitable reward to stakeholders, driven by highly motivated well-trained people

and state-of-the art technology”

PAY OFF…..Working today for your tomorrow

VALUESThe core values of the bank are shared belief that drives behavior in

the company backed by Islamic faith. Some of these values, which are aimed at realizing the bank’s vision,

mission and goals are:

• Honesty• Tolerance• Brotherhood (treat each other as a sister/brother)• Team work

2

IFRS FINANCIAL STATEMENTS 2016

THE BANK PROFILE

AGIB Ltd was incorporated as a private limited liability company in November, 1994 and was granted a banking license by The Central Bank of The Gambia in September 1996. The bank became fully operational in January, 1997. It is worth mentioning here that the Finan-cial Institution Act 1992 was amended to provide for the establishment of an Islamic Bank in The Gambia.

AGIB is the first and the only Islamic Bank in The Gambia and it is legally allowed to own equity in other companies and also operate in commodities and Real Estate markets on its own account.

In September, 2008 AGIB consummated a strategic alliance with First Inland Bank (FINBANK) of Nigeria. In May 2014 FINBANK shares were all bought by Gambian businessman making him the majority shareholder. The Islamic Development Bank in Jeddah also holds significant shares. The bank currently has 103 employees and has 6 branches strategically located in Banjul, New Jeshwang, Tranquil, Bakoteh, Brikama and Basse and 6 ATMs in Banjul, Churchill’s Town, Brikama and Basse branchesand at 2 offsite locations at QCell head office on Kairaba Avenue and at Brusubi roundabout.

AGIB operates on the Islamic Economic Principle of Risk/Reward also known as Profit and Loss Sharing.

Unique characteristics:

• Only Islamic bank in a 90% Muslim dominated country• Offers only Sharia compliant products• Only bank allowed to own and develop real state• Assist disadvantaged people in the community• Legally allowed to own equity in other companies

3

IFRS FINANCIAL STATEMENTS 2016

Murabaha (Cost plus mark-up agreement)Murabaha is a contract in which the customer requests for the Islamic financial institution to purchase a commodity and sell it to him/her at a cost plus mark-up will be on adeferred payment basis. The cost of the commodity is paid to the supplier of the goods delivered directly to the institution or to the customer.

Mudaraba (profit sharing)Mudaraba is a profit sharing contract in which one party offer the funds (investor) and the other (the financial institutions) invest and manage the fund. It’s a mutual agreement between the investor and the specialist with the expertise. The investor (Rabal Mal) is the dormant partner and the bank is the manager of the funds (Mudarib). Profits are shared at a fixed ratio while any loss is borne by the owner of the funds provided that the mudarib is not negligent in the investment of the funds.

Musharaka (Partnership financing)

Musaraka is referred to as joint venture agreement where both the bank and the customer contribute towards the funds required for the venture in the agreed proportion in short it is base on equity participation between the Islamic Financial Institution and a Client.

Istisna’a (contract of manufacture)

This is where the bank agrees to finance the manufacture or production of a product and the payment is made upon completion and delivery of the item in question. Income generated from providing this product is small (less than one percent of total investment income). Is sna’a is currently advanced to staff.

Ijara

This is similar to conventional leasing operating leases where the income generated is in the form of rental income accruing to the bank.

PRODUCTS AND SERVICES

HAJJ SAVINGS SCHEMEIn addition to this saving scheme, products and services to be rendered to pilgrims are straight forward and simple. Already, the Bank has been involved in the provision of Saudi Riyals for exchange though volumes dwindled significantly during the period under review.

BUSINESS ADVISORY SERVICE

In addition to traditional commercial banking, AGIB has been mandated to carry out investment financing by granting medium to long-term finances to customers. The preparation of project documents is also within the purview of the Investment Department. Some customers may have sound investment ideas but may not be able to transform them into reality. Thus, the department offers advice to customers of the Bank on various aspects of their business, ranging from feasibility studies to keeping proper books of account.

ACCOUNTS

AGIB SAVING ACCOUNTThis is designed specifically to meet require-ments of customers who would like the bank to invest their money, they can deposit and withdraw as and when they want and they are paid profits as permitted by the Shariah

AGIB CURRENT ACCOUNT

It is a profit-free account which is designed to meet the requirements of Customers. Account holders can deposit and withdraw money by cheque at any of the bank’s 6 branches. It is available to all categories of customers

4

IFRS FINANCIAL STATEMENTS 2016

PRODUCTS AND SERVICES AGIB INVESTMENT ACCOUNTThis is a high return account that would enable customers to deposit fixed sums of money in the bank through our the year and for a fixed periods ranging from (three months six months and twelve months). The bank invests the money and profit is distributed in accordance with Islamic Sharia law as per the agreement signed between the two parties.

Our Technology

Information technology remains the bedrock of service delivery. The bank continues to exploit and master new technologies to package and deliver innovative products and services. AGIB is a technology and service driven Bank, through enhanced service delivery channels leveraging on cutting edge solutions.

Our People

Our customers are unique and require individual approach. AGIB has competence and expertise in the delivery of customized and unique solutions tailored to address our customers distinctive needs. Our staff are polite, well-trained and experienced in customer service.

IFRS FINANCIAL STATEMENTS 2016 Page | 3

Financial Highlights

2016 D’000

2015 D’000

Income Statement

Profit before tax

53,901 15,087

Post-tax profits

47,388 15,127

Income from Islamic finances 81,716 55,772

Operating expenses 85,780 76,824

Impairment 10,199 3,248

Balance sheet

Total Assets

1,369,887 1,077,257

Islamic financing and related assets

476,390 259,001

Customer Deposits

862,506 699,273

Equity 358,408 311,021

Ratios

Earnings Per Share (Butut)

1.87 0.60

Return on Asset (ROA)

3.46% 1.41%

Return on Equity (ROE)

15.04% 6.24%

Capital Adequacy 21.0% 26.9%

Cost to Income Ratio 66.25% 86.65% Liquidity Ratio 196.1% 210.10%

Non Performing Loan Ratio 1.07% 6.97%

Financial Highlights

5

IFRS FINANCIAL STATEMENTS 2016

IFRS FINANCIAL STATEMENTS 2016 Page | 4

General information

Directors Mr Muhamed Jah Chairman Mr. Nuha Marenah Managing Director

Mr. Mamour Malick Jagne Director

Mr. Fye Ceesay Director

IDB Representative Director

Company secretary/ Legal Adviser Mrs. Hawa Sisay Sabally

Sharia Advisory Committee Alhagie Muhamed Sarr Member Alhagie Ousman Jah Member Essa Darboe from April 2016 Member Tijan Kah from April 2016 Member Secretary Alhagie Matarr Drammeh Auditors DT Associates - The Gambia Audit, Tax, Advisory 1 Paradise Beach Place Bertil Harding Highway P O Box 268 Banjul, The Gambia Bankers Bank Islamique du Senegal – Dakar Ghana International Bank Central Bank of The Gambia Solicitor Hawa Sisay-Sabally 60B Antouman Faal Street Banjul, The Gambia Registered office Bekka Plaza Ecowas Avenue Banjul, The Gambia

6

IFRS FINANCIAL STATEMENTS 2016

Chairman’s Statement

Assalamualaikum.On behalf of the Board of Directors, I am delighted to welcome you to the Annual General Meeting of your bank Agib Bank Ltd. I have the honour of presenting the highlights

of the bank's operating performance for the year ended December31, 2016, as well as an overview of the major developments that impacted the international and domestic environments in which your bank operated.

International EnvironmentThe year under review was characterized by contrasting fortunes for developed countries and emerging and developing countries. There was strong growth registered by developed economies whereas there was a slowdown in major developing economies mainly in Latin America. Overall, the United States recovered strongly in the second half of the year when unemployment was re-duced to its lowest level over a number of years after a lackluster first half. Europe did not enjoy same level of success though domestic demand in Spain and in the United Kingdom exceeded forecasts despite the Brexit vote in the UK.

The economies of emerging markets and developing countries (EMDEs) was a lot more diverse. The growth rate in China was stronger than expected while performance was sluggish in some key Latin American countries such as Argentina and Brazil which went into recession. Turkey was bewildered by political turmoil while Russia did slightly better than expected as a result of improved oil prices after Opec’s decision to reduce output to push prices up.

The IMF reported that headline inflation rates recovered in advanced economies with the bottoming out of commodity prices. Core inflation rates have remained broadly unchanged and generally below inflation targets during 2016. In developing countries, inflation trends have been heterogeneous, reflecting differing exchange rate movements in particular and producer prices.

Distinguished Shareholders, Ladies and Gentlemen,

In Financial market developments. long-term nominal and real interest rates have risen substantially since August, particularly in the United Kingdom and in the United States (since the November election). Trump government was expected to pursue an expansionary fiscal policy which fuel inflation.

The U.S. dollar appreciated against most major currencies during the year particularly against the Great Britain Pound and the Japanese Yen. However, the currencies of some commodity ex-porting countries like Russia strengthened as a result of overall increases in commodity prices.

The Domestic Economy

The Gambian economy is heavily dependent on the agricultural sector both in terms of its contribution to GDP and in terms of the huge number of people engaged in the sector for their livelihood. The sector contributes 25% of GDP and employs about 75% of the work force.

The Gambia has sparse natural resource deposits. Households rely heavily on remittances from workers overseas and tourist receipts. Remittance inflows to The Gambia amount to approximately 20% of the country’s GDP

Small-scale manufacturing activity features the processing of peanuts, fish, and hides. Re-ex-port trade accounts for almost 80% of goods ex-ports with China as the largest trading partner for both exports and imports.

7

IFRS FINANCIAL STATEMENTS 2016

The Gambia's natural beauty and proximity to Europe has made it a preferred tourist destination in West Africa, boosted by government and private sector investments in eco-tourism and upscale facilities. Tourism contributes about 20% of GDP. The sector is yet to recover from hit in 2014 which was occasioned by fears of Ebola virus in neighboring West African countries. The run up to the elections of 2016 ushered in uncertainty and fears of violence resulting in cancellations of tourists’ bookings and an unprecedented drop in tourist arrivals with its attendant effects on the economy (drop in employment, low contribution to GDP, reduced government earnings etc). Overall, Q4 of 2016 was arguably the most unproductive quarter for the tourism industry in the history of independent Gambia mainly due to political uncertainly which culminated in the impasse of December 2016 and January 2017. Unemployment peaked and incomes plummeted.

DOMESTIC BANKING SECTOR

The banking sector remains strong and safe as indicated by the financial soundness indicators. The capital adequacy ratio for the industry averaged 38.5% up from 37.9% at the corresponding period last year.

Total assets of the sector increased by 0.7% to D29.6 billion (69.8% of GDP) Gross loans and advances declined by 15.7% com-pared to the same period last year. Gross loans and advances constitute 14.4% of the industry’s total assets.

Non-performing loans ratio dropped from 11.6% same period last year to 7.6%. This signifies a marked improvement in the quality of banks’ assets

Deposit liabilities, which constitute 54% of the industry’s total liabilities, declined by 2.9% to D16.1 million. Liquidity ratio averaged 88.7% well above the required

The last few months of 2016 were however punctuated by a high-impact political impasse which literally crippled the economy. Businesses closed down temporarily while their proprietors sought refuge out of the country or in the countryside. This went into the new year. Agib Bank Ltd, like other commercial banks and the Central Bank of The Gambia, closed its head office in Banjul for a few days and operated from our the Disaster Recovery (DR) site in Bakote. I am glad to say that our operations from DR site was seamless with no adverse impact on services. Infact Agib Bank’s customers did not notice that we were operating from the DR site.

Chairman’s Statement

8

IFRS FINANCIAL STATEMENTS 2016

FINANCIAL PERFORMANCE OF AGIB BANK LTD

In the last AGM in June 2016, the Board of Directors’ recommendation to change the bank’s name from Arab Gambian Islamic Bank (AGIB) Ltd to Agib Bank Ltd was approved. Following the approval, authorization was sought from the Central Bank of The Gambia to effect the name changand it was granted. All necessary procedures and requirements have been complied with and the name change has been finalized and published in the papers for public notification.

Chairman’s Statement

9

Profit after tax increased from D15.1 million in 2015 to D47.4 million in 2016 i.e. a growth of 213.27%

Return on Assets (ROA) grew from 1.41% to 3.46%; an increase of 145.39%

Return on Equity (ROE) grew from 6.24% to 15.04% in 2016; a growth of 141.03%

Earnings per share improved from 0.6% in 2015 to 1.87% in 2016; an increase of 211.67%

Deposits grew from D699.27 million in 2015 to D952.51 in 2016; a growth of 36.21%

Non-performing loan ratio improved from 6.97% to 1.07%; an improvement of 84.65%

SIGNIFICANT EVENTS DURING THE YEAR 2016

I am pleased to inform you that your bank made a strategic decision to buy a piece of land on Kairaba Avenue in heart of the business district for the purpose of constructing its head office. As you are all aware, the bank is currently housed in a rented shopping complex in Banjul which is obviously not ideal. Architectural and structural drawings/designs have been completed and the construction will be tendered shortly.

It is refreshing to report that the IDB is now committed to attend all our Board meetings and are in the process of identifying a permanent representative. A representative attended the last meeting with a Power of Attorney from IDB.

IFRS FINANCIAL STATEMENTS 2016

OUTLOOK FOR 2017

Results of 1st December 2016 elections were challenged by the defeated sitting government resulting in the infamous political impasse and economic devastation as discussed earlier. 2017 started under very stressful, volatile and unprecedented conditions. This was swiftly addressed by the intervention of sub-regional forces which saw the former President seek exile in Equitorial Guinea. His departure was a necessary but not a sufficient condition for immediate positive changes in the political, social and economic conditions of the majority of Gambians.

Given the lack of any meaningful quantity of natural resources and the depleted government coffers, progress depends on sustained bilateral and multilateral aid, onresponsible government economic management, and on continued technical assistance from multilateral and bilateral donors. The good news is that International donors and lenders are enthused by the return of democracy to the country and a number of them have pledged funds for budgetary support and for financing much-needed infrastructural and capacity building projects. Your bank is well poised to take advantage of the opportunities that present themselves.

CONCLUSION

On behalf of the Board of Directors and Management, I want to thank our customers for their trust and patronage, our shareholders for their support and confidence in us and our staff for their commitment towards sustaining and actualizing the ideals and the corporate objectives of your noble institution. I would also like to thank the CentraI Bank for their effective oversight and guidance. I pray that Almighty Allah SAW would continue to guide and direct your bank and every one of us.

Finally, may I take this opportunity to seek you approval for the payment of dividend at 98 bututs per share.

Chairman’s Statement

10

IFRS FINANCIAL STATEMENTS 2016

Managing Director’s Statement

It is indeed a great privilege to brief you on the activities of your bank for the period January to December 2016

THE GLOBAL ECONOMYThe year 2016 was a mixed bag of fortunes for the world economy. The first half of the year saw relative stability while there was far less certainty in global markets in the second half of the year due primarily to the BREXIT vote in the United Kingdom and the election of Donald P Trump as the President of the United States. The unprecedented upsurge in terrorist activity in both Germany and France, the two economic and political powerhouses in the European Union caused nervousness in stock markets in the Euro Zone. The IMF and other major multilateral financial institutions had no alternative but to reduce their global growth forecasts for 2016 to 1.8% in 2016 lower than the 1.9% in 2015 mainly influenced by weak consumer appending, lower oil and gas prices in the first half of the year. The strengthening of the US Dollar against all other major currencies like GBP and the Japanese Yen did not help consumer spending either. Against the backdrop of low oil prices and dampening consumer demand in most major economies, inflation pressures remain generallylow.

Growth in emerging markets and developing countries remained strong at 4.1% for 2016 driven by a 6.7% growth forecast for China. For Sub-Saharan Africa, growth forecast in the region has been revised down to 1.6% which is much lower than the 3.3% growth in 2015. This is mainly due to difficulties in South Africa and Nigeria where the local currency, the Naira had to be devalued. Prices of both oil and non-oil commodities remain well below historical averages.

Assalamu Alaykum Warahmatullah tala wabarakatuhu

Distinguished Ladies and Gentlemen

In The Gambia, domestic debt is estimated at 67.9 percent of GDP in 2016 up from 53.9 percent in 2015 reflecting high domestic debt accumulation. The ratio of external debt to GDP ratios in 2016 stood at 50.9 percent compared with the established threshold of 30 percent. Overall, national debt exceeded GDP

The FX market remained unpredictable throughout 2016 with significant volatilities especially after the lifting of the executive order that pegged the USD to D40/$. USD sky-rocketed from D40/$ to 54.50/$ immediately after the lifting of the Executive Order due to the growing importance of the parallel market. On 1st November 2016, the CBG issued a directive after intensive consultation with players in the market that restricted commercial banks’ spread to D1.00 per Dollar. It also required commercial banks to sell at least 15% of their total FX purchases to the Central purchases to build up depleted national FX reserves. Obviously these interventions affected revenues negatively. Revenues from FX Trading normally constitute a significant portion of the bank’s revenue but that was not the case in 2017 due to the negative impact of the bad executive order and the burgeoning parallel market.

Banking Sector highlightsThe banking sector remains strong and safe as indicated by the financial soundness indicators. The capital adequacy ratio for the industry averaged 38.5% up from 37.9% corresponding period last year.

Total assets of the sector increased by 0.7% to D29.6 billion (69.8% of GDP)

Gross loans and advances declined by 15.7% compared to the same period last year. They constitute 14.4% of the industry’s total assets

Non-performing loans ratio dropped from 11.6% same period last year to 7.6%. This signifies a marked improvement in the quality of banks’ assets

Deposit liabilities declined by 2.9% to D16.1 million. Deposit liabilities constitute 54% of the industry’s total liabilities. Liquidity ratio averaged 88.7% well above the required minimum of 30%.

11

IFRS FINANCIAL STATEMENTS 2016

Yields on the 91 day and 182-day treasury bills declined to 17.15% and 17.83 percent in June 2016 from 17.28% and 18.44% in June 2015. In contrast, yields on the 364 day bills, on the other hand, rose to 21.85% from 21.45% a year ago. Yields on the 91 day and 182 day SAS declined to 17.5% and 17.9% in June 2016 compared to 17.6% and 18.4% respectively in June 2015. Yields on 364 day SAS, on the other hand, rose to 21.90 percent from 20.54 percent in June 2015.

Preliminary balance of payments estimates for the first half of 2016 indicate a deficit of US$24.7 million from a surplus of US$21.8 million in the same period last year. The current account defi-cit narrated to US$58.1 million in June 2016 compared to US$69.7 million a year ago, mainly on account of improved trade balance.

These indicators were contained in the Central Bank of The Gambia’s Monetary Policy Committee’s Press release of September 2016 and are the latest available official numbers as at the time of writing this report.

The last few months of 2016 were however punctuated by a high-impact political impasse which literally crippled the economy. Businesses closed down temporarily while their proprietors sought refuge out of the country or in the coun-tryside. This went into the new year.

OVERVIEW OF THE BANKIt was in the forgoing environment that your bank operated in 2016. Additionally, I would like to highlight some key performance indicators as at 31st December 2016

Financial Performance Indicators

• Customer deposits increased from D699m in 2015 to D953m in 2016 I.e. an increase of 36%

• Bank registered a pre-tax profit of D54m (fifty four million Dalasi only) as at 31st December 2016 from D15m in 2015 i.e. 260% increase

• Operating expenses increased from D73.6m in 2015 to D75.6m in 2016 i.e. 3% increase

• Income from Treasury Operations increased from D7.9m 2015 to D8.4m in 2016 i.e 6% increase

Managing Director’s Statement

• Income from banking service increased from D16.6M to in 2015 to D19.5 in 2016 i.e 18% increase

• Income from Islamic finance increased from D55.8m in 2015 to D81.7m in 2016 i.e.47% increase

• Non-performing loans ratio declined from 6.9% in 2015 to 1.07% in 2016 i.e. a decline of 84%

• Cost/income ratio reduced from 86.65% in 2015 to 66.25% in 2016 i.e. a decline of 24%

Human Resources

Training continues to be the priority. During the year, in-house training sessions were conducted for all staff in Operational Risk Management, AML and Terrorist Financing. In addition to the in-house training, our staff attended all relevant training programs organised by the Gambia Bankers’ association. At the Annual Dinner of the Association, the Gambia Bankers’ Association recognised your banks performance in the training space by awarding us a certificate for being one of the most active banks in capacity building. We believe human resources to be the most important component of any business so we consider training to be a worthwhile investment.

Every staff took their full annual leave entitlement during the year

In June 2016, a minimum increase of 10% of staff salary was implemented across board as approved by you in the AGM of 3rd June 2016. Staff morale is currently at an all-time high as a result of which we have been able to attract some good resources from competitor banks

An in-house provident fund was set up to promote a savings culture amongst staff with a view to enhance their incomes at retirement. Contributions to the fund are voluntary and are deducted from their salaries at source.

12

IFRS FINANCIAL STATEMENTS 2016

Managing Director’s StatementTECHNOLOGYThe IT team had intensive training in ORACLE, the platform on which the bank’s core banking software, iMAL sits to reduce dependence in order to enhance the team's knowledge in report generation and better understanding of the software itself. The training was facilitated by a certified oracle IT specialist.

Your bank implemented internet banking in May 2016 to provide our customers with modern banking our customers can now do their banking in the confort of their homes.

We achieved a remarkable level of uptime of over 95% on all our major technology platforms (like iMAL core banking, ATMs and iBanking).

During the impasse, we had to close our head office and our data centre in Banjul for a few days and resorted to operating from our Disaster Recovery site in Bakote. We were able to operate seamlessly with no impact on service. This confirmed the robustness the bank’s technology platforms and the efficiency of your technology team.

I am pleased to inform you that all our processes are now fully automated.

Outlook for 2017The main challenges for 2017 will be the diminishing revenue from fixed income investments. Sukuk Al Salam floats are reducing at an alarming rate and the trend is most likely not going to be reversed given the budgetary support that international donor community is providing for the New Gambia. It is not only the quantum of the float that is going down but the rates as well. The budget rate for 364-day bills was 22% but as of today, the actual rate is 12% which is a significant reduction in the revenues.

Trade Services is an integral part of our operations and as such we are embarking on developing in-house capability to handle the transactions/volumes we anticipate in the commodities market.

In 2016 we requested for a murabaha financing credit line in the sum of $5million (five million United States Dollars only) from IDB. A due diligence team from IDB visited the bank and their findings were very positive.The request has since been approved and the legal documentation is near finalization prior to disbursement.

Our outlook for the 2017 is bright and very promising. The on boarding of NFSC into the bank’s books will undoubtedly be an immense opportunity to increase the bank’s performance both in terms of business volumes and income. Coupled with this is the increasing support coming from IDB. It must be noted that Sukuk yields are not expected to go up for the foreseeable future. However, this will be mitigated by working on increasing the bank’s portfolio size using the excesses of the funds strategically.

Head Office buildingThe architect has submitted the final plans and are being reviewed. We have issue notice of termination of the tenancy contract to our cur-rent landlord for 30th November 2017 but that is being reviewed for extension as construction work is not likely to be completed before 30th November when the current tenancy will expire.

Agency BankingFollowing Central Bank of The Gambia’s ap-proval for commercial banks to roll out agency banking in areas where we do not have a foot print, we are piloting in two towns, Numuyel and Garawole, in the URR. Staff have been trained as Tellers and CSOs for the two sites in Basse Branch in December 2016. The Agencies are expected to commence operations soon.

CONCLUSION AND ACKNOWLEDGEMENTSIn conclusion, I would like to assure you the shareholders that your bank is on the right trajectory and Management and staff of the bank are enthused by the confidence and trust that you, the shareholders and the Board of Directors have placed in us. We will continue to exploit the prospects and opportunities that present themselves with a view to move your bank to the next level. We thank you for your invaluable trust and support throughout the year.I would also like to express our sincere gratitude to the Central Bank of The Gambia for their invaluable support and guidance.

It is evident that without our esteemed customers, we would not have achieved all what we are celebrating today. We thank them for their custom and for their partnership.

Finally, on behalf of the Chairman, Board of Directors and Management of the bank, I would like to thank the staff of your bank for their honesty, commitment, dedication and genuine desire to achieve the goals of the bank while maintaining full compliance with Shariah, the rockbed of Islamic banking and with regulatory guidelines. May Allah SWT The Almighty continue to bless, protect and guide us all. Amen.

THANK YOU13

IFRS FINANCIAL STATEMENTS 2016

IFRS FINANCIAL STATEMENTS 2016 Page | 5

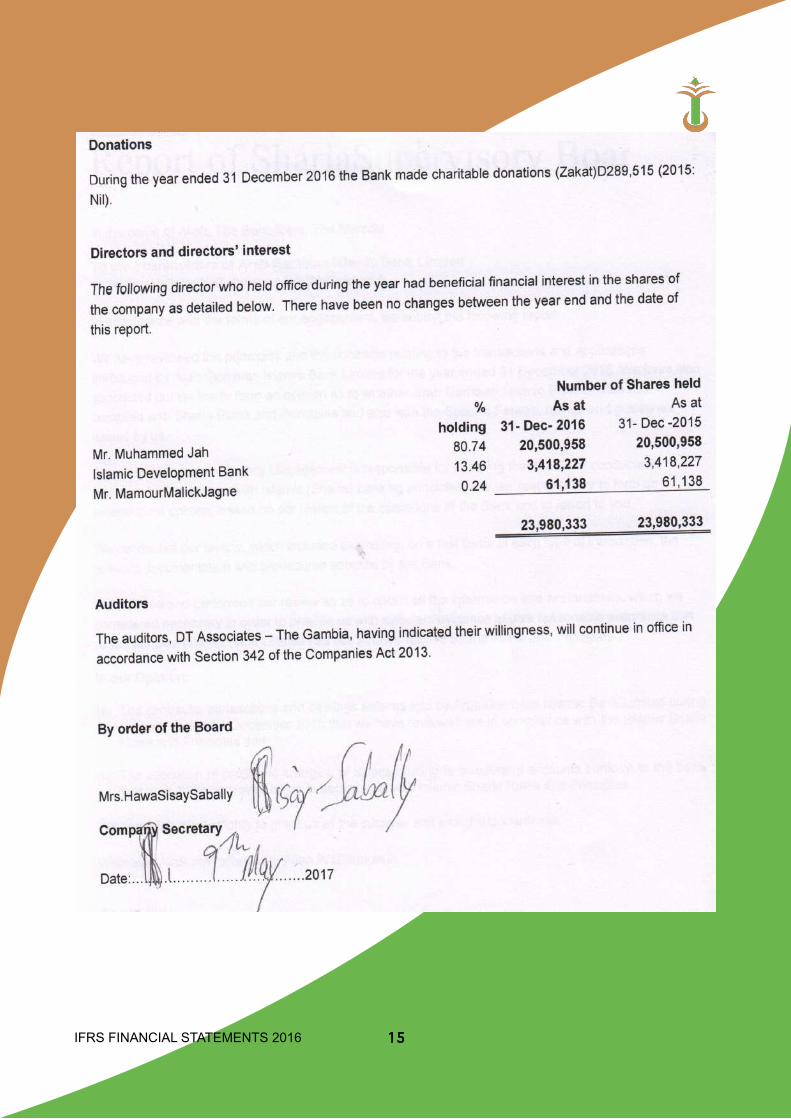

Directors’ report

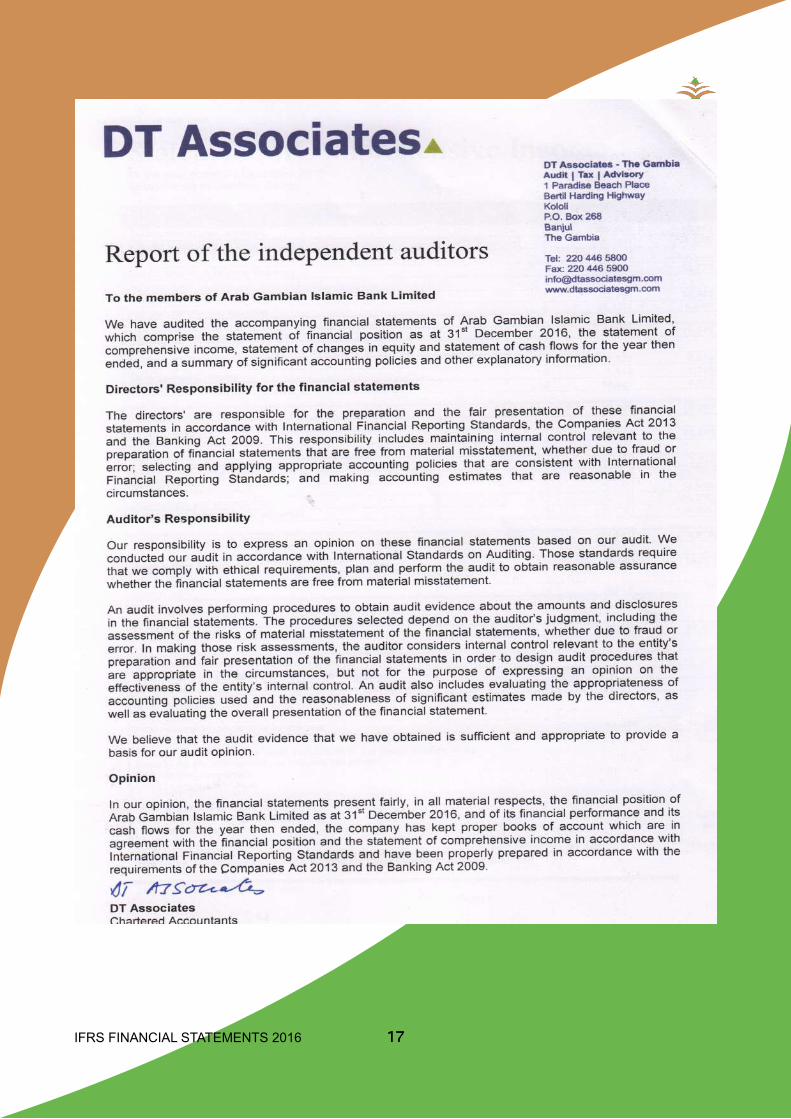

The Directors present their report and audited financial statements of Arab Gambian Islamic Bank Limited for the year ended 31 December 2016.

Statement of directors’ responsibilities The Companies Act 2013 requires the directors to prepare the financial statements for each financial year which give a true and fair view of the state of affairs of the company and of its profit or loss for that period. In preparing the financial statements, the directors are required to:

select suitable accounting policies and then apply them consistently;

make judgments and estimates that are reasonable and prudent;

state whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the financial statements;

prepare the financial statements on the going concern basis unless it is inappropriate to presume that the company will continue in business.

The directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the company and to enable them ensure that the financial statements comply with the Banking Act 2009 and the Companies Act 2013. They are responsible for safeguarding the assets of the company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities. Principal business activity The company provides banking services in all its departments and branches in accordance with Islamic (Sharia) banking principles, regulations of the Central Bank of The Gambia and the Banking Act 2009, with a view to making profit for its shareholders and depositors and to contribute to the socioeconomic development of The Gambia. Apart from accepting deposits from customers and providing services traditionally rendered by conventional banks, the bank also grants financing facilities for short, medium and long term economically and financial viable undertakings. Results and dividends The results of the company are as detailed in the accompanying financial statements. The directors are proposing to pay dividend of D0.40 bututs per share.

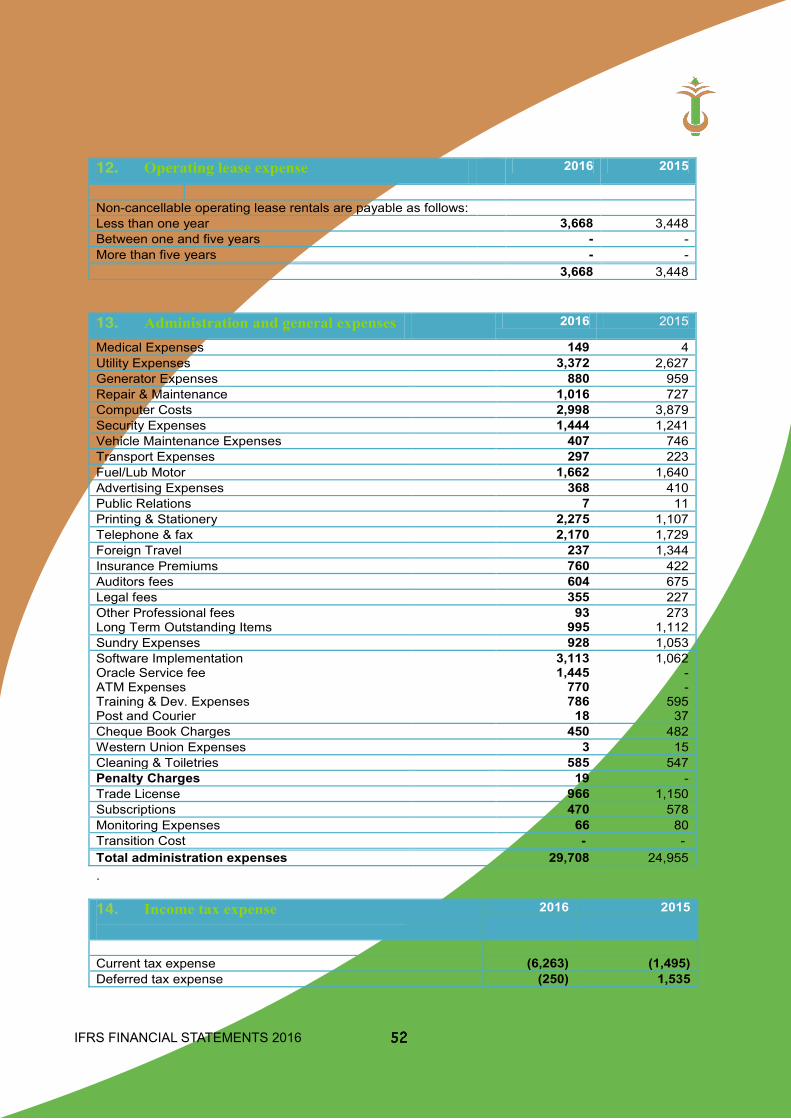

Property, plant and equipment The property, plant and equipment of the company are as detailed in note 22 of the financial statements. There has not been any permanent diminution in the value of the property, plant and equipment and as a result a provision has not been deemed necessary.

14

IFRS FINANCIAL STATEMENTS 2016 15

IFRS FINANCIAL STATEMENTS 2016 16

IFRS FINANCIAL STATEMENTS 2016 17

IFRS FINANCIAL STATEMENTS 2016

IFRS FINANCIAL STATEMENTS 2016 Page | 9

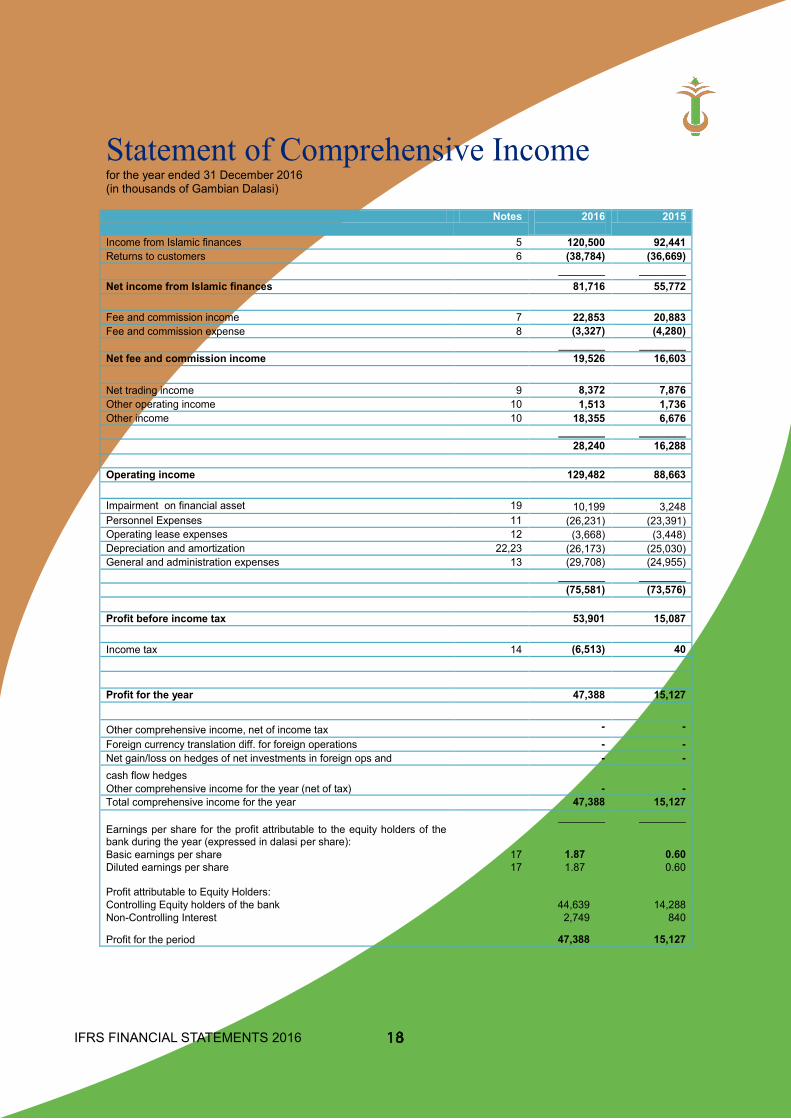

Statement of Comprehensive Income for the year ended 31 December 2016 (in thousands of Gambian Dalasi) Notes 2016

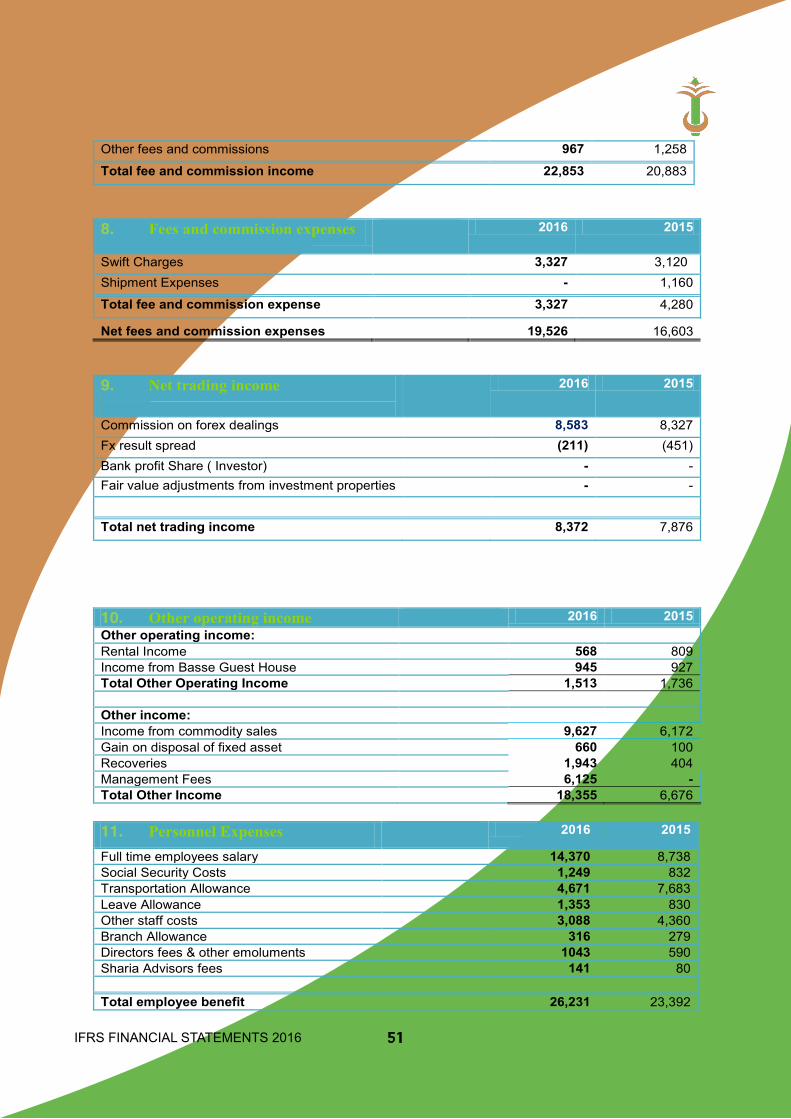

2015

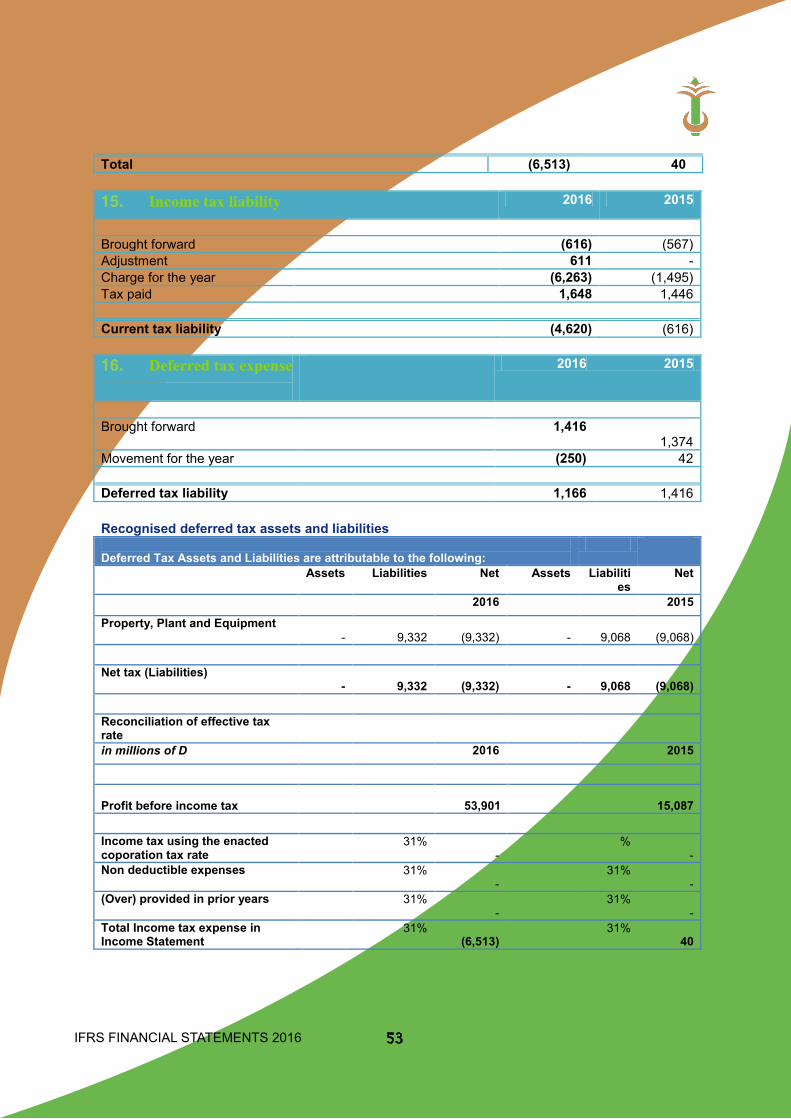

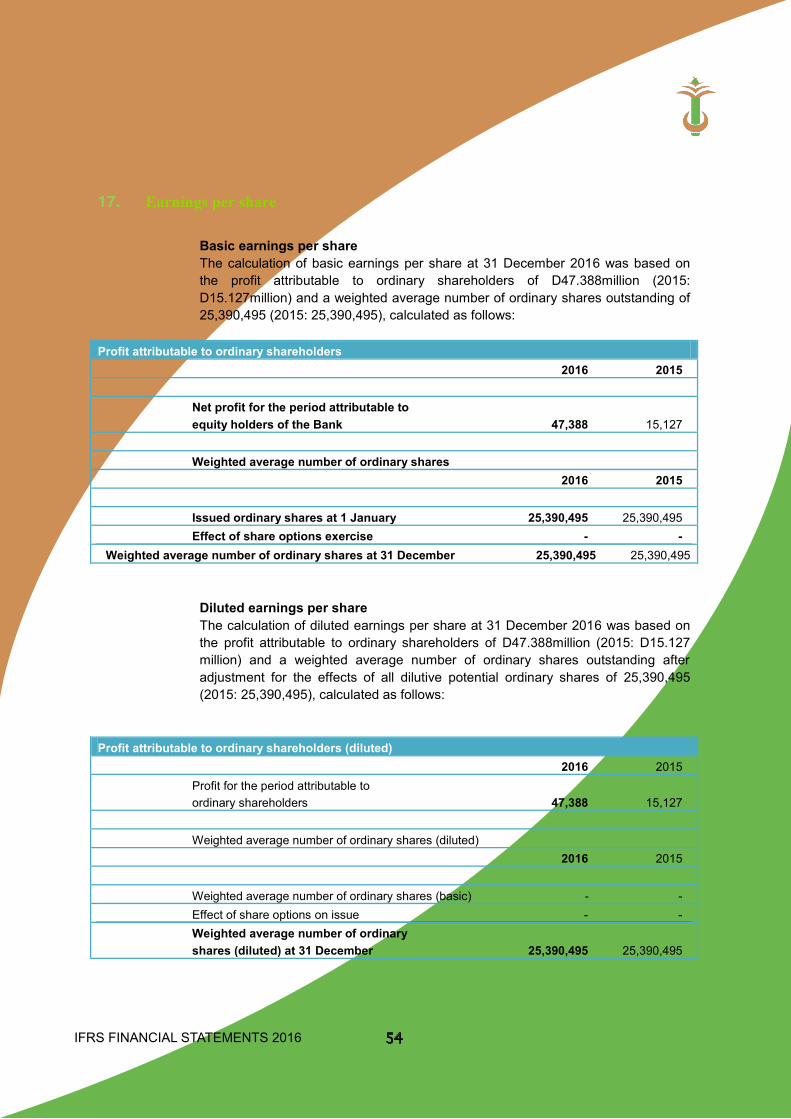

Income from Islamic finances 5 120,500 92,441 Returns to customers 6 (38,784) (36,669) ________ ________ Net income from Islamic finances 81,716 55,772 Fee and commission income 7 22,853 20,883 Fee and commission expense 8 (3,327) (4,280) ________ ________ Net fee and commission income 19,526 16,603 Net trading income 9 8,372 7,876 Other operating income 10 1,513 1,736 Other income 10 18,355 6,676 ________ ________ 28,240 16,288 Operating income 129,482 88,663 Impairment on financial asset 19 10,199 3,248 Personnel Expenses 11 (26,231) (23,391) Operating lease expenses 12 (3,668) (3,448) Depreciation and amortization 22,23 (26,173) (25,030) General and administration expenses 13 (29,708) (24,955) ________ ________ (75,581) (73,576) Profit before income tax 53,901 15,087 Income tax 14 (6,513) 40 Profit for the year 47,388 15,127 Other comprehensive income, net of income tax - - Foreign currency translation diff. for foreign operations - - Net gain/loss on hedges of net investments in foreign ops and - - cash flow hedges Other comprehensive income for the year (net of tax) - - Total comprehensive income for the year 47,388 15,127 Earnings per share for the profit attributable to the equity holders of the bank during the year (expressed in dalasi per share):

________ ________

Basic earnings per share 17 1.87 0.60 Diluted earnings per share Profit attributable to Equity Holders:

17 1.87 0.60

Controlling Equity holders of the bank 44,639 14,288 Non-Controlling Interest 2,749 840

Profit for the period 47,388 15,127 The notes on pages 13 to 49 are an integral part of these financial statement

18

IFRS FINANCIAL STATEMENTS 2016 19

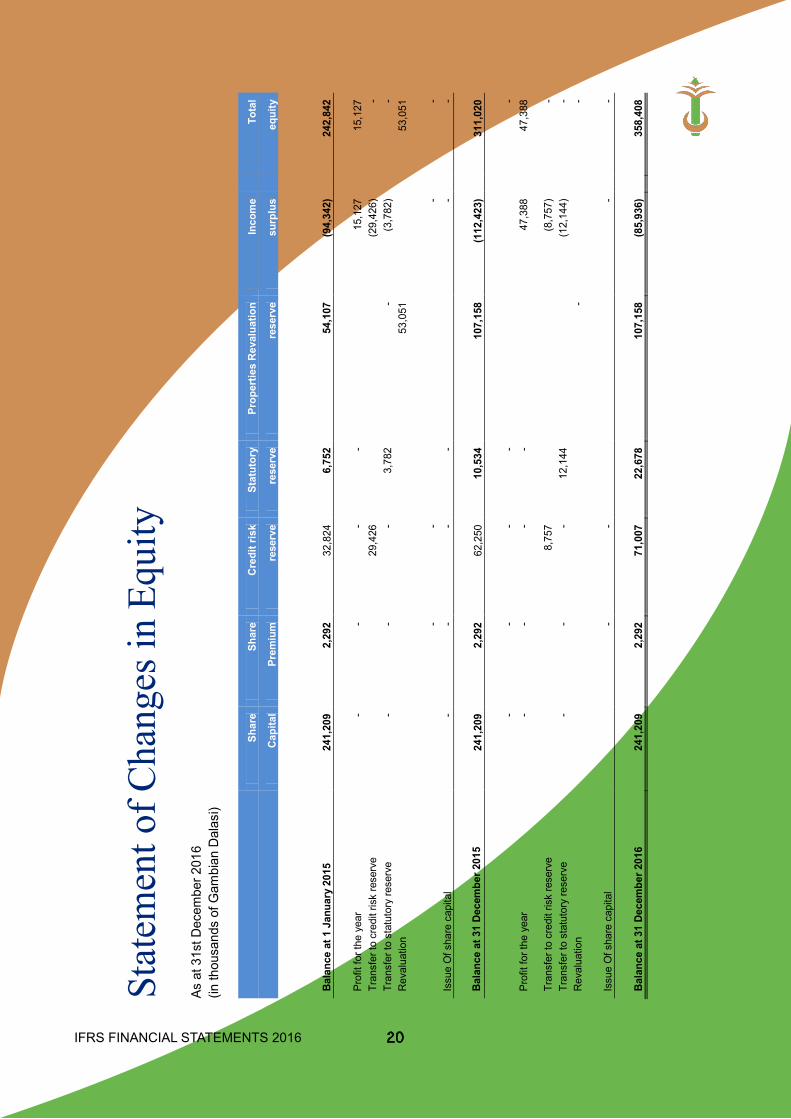

IFRS FINANCIAL STATEMENTS 2016

IFRS

FIN

ANCI

AL S

TATE

MEN

TS 2

016

Page

| 11

Stat

emen

t of C

hang

es in

Equ

ity

As a

t 31s

t Dec

embe

r 201

6

(in

thou

sand

s of

Gam

bian

Dal

asi)

Sh

are

Shar

e

Cred

it ris

k

Stat

utor

y

Prop

ertie

s Re

valu

atio

n

Inco

me

To

tal

C

apita

l Pr

emiu

m

rese

rve

rese

rve

rese

rve

surp

lus

eq

uity

Ba

lanc

e at

1 J

anua

ry 2

015

241,

209

2,29

2 32

,824

6,

752

54,1

07

(94,

342)

242,

842

Pr

ofit

for t

he y

ear

-

-

-

-

15,1

27

15

,127

Tr

ansf

er to

cre

dit r

isk

rese

rve

29,4

26

(29,

426)

-

Tr

ansf

er to

sta

tuto

ry re

serv

e

-

-

-

3,

782

-

(3

,782

)

-

R

eval

uatio

n

53

,051

53

,051

-

-

-

-

Issu

e O

f sha

re c

apita

l -

-

-

-

-

-

Ba

lanc

e at

31

Dece

mbe

r 201

5 24

1,20

9 2,

292

62,2

50

10,5

34

107,

158

(112

,423

)

311,

020

-

-

-

-

-

Pr

ofit

for t

he y

ear

-

-

-

-

47,3

88

47

,388

Tran

sfer

to c

redi

t ris

k re

serv

e

8,

757

(8,7

57)

-

Tran

sfer

to s

tatu

tory

rese

rve

-

-

-

12,1

44

(1

2,14

4)

-

Rev

alua

tion

-

-

Is

sue

Of s

hare

cap

ital

-

-

-

-

Bala

nce

at 3

1 De

cem

ber 2

016

241,

209

2,29

2 71

,007

22

,678

10

7,15

8 (8

5,93

6)

35

8,40

8

The

note

s on

pag

es13

to 4

9 ar

e an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

20

IFRS FINANCIAL STATEMENTS 2016 21

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016 Page | 12

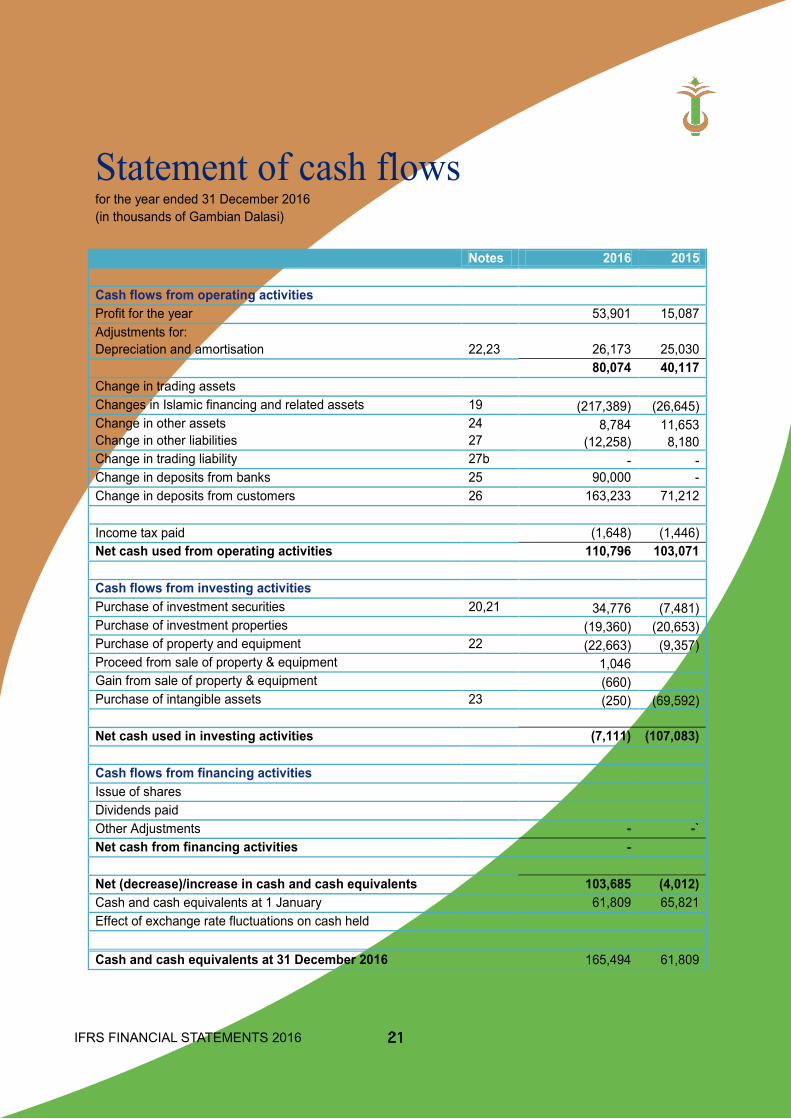

Statement of cash flows for the year ended 31 December 2016 (in thousands of Gambian Dalasi) Notes 2016 2015 Cash flows from operating activities Profit for the year 53,901 15,087 Adjustments for: Depreciation and amortisation 22,23 26,173 25,030 80,074 40,117 Change in trading assets Changes in Islamic financing and related assets 19 (217,389) (26,645) Change in other assets 24 8,784 11,653 Change in other liabilities 27 (12,258) 8,180 Change in trading liability 27b - - Change in deposits from banks 25 90,000 - Change in deposits from customers 26 163,233 71,212 Income tax paid (1,648) (1,446) Net cash used from operating activities 110,796 103,071 Cash flows from investing activities Purchase of investment securities 20,21 34,776 (7,481) Purchase of investment properties (19,360) (20,653) Purchase of property and equipment 22 (22,663) (9,357) Proceed from sale of property & equipment 1,046 Gain from sale of property & equipment (660) Purchase of intangible assets 23 (250) (69,592) Net cash used in investing activities (7,111) (107,083) Cash flows from financing activities Issue of shares Dividends paid Other Adjustments - -` Net cash from financing activities -

Net (decrease)/increase in cash and cash equivalents 103,685 (4,012) Cash and cash equivalents at 1 January 61,809 65,821 Effect of exchange rate fluctuations on cash held Cash and cash equivalents at 31 December 2016 165,494 61,809 The notes on pages 13 to 49 are an integral part of these financial statements.

IFRS FINANCIAL STATEMENTS 2016

The accompanying notes are an integral part of the financial statements. 13

Notes to the financial statements (forming an integral part of the financial statements)

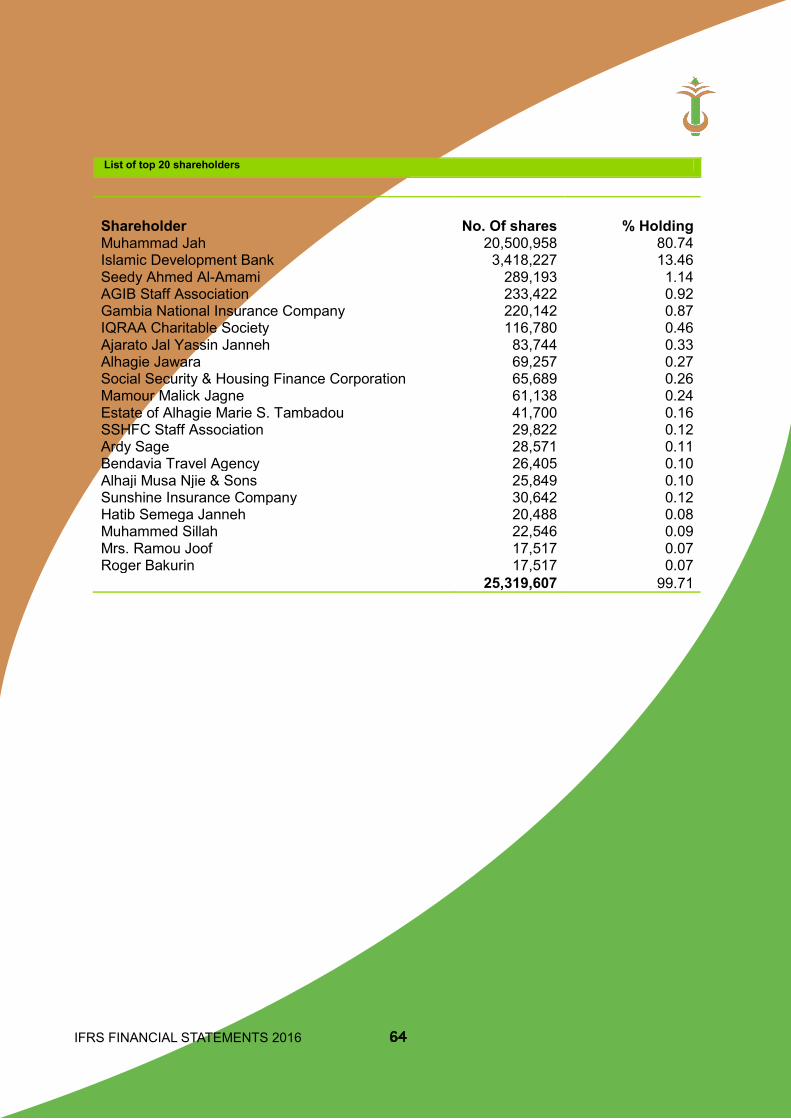

1. Reporting entity Arab Gambian Islamic Bank Limited (“the Bank”) was established on November 11, 1994 and obtained its banking license on September 12, 1996. The address of the registered office of the Bank is: Bekka Plaza, Ecowas Avenue, Banjul, The Gambia. The major shareholder of the bank is Mr. Muhammed Jah, the Managing Director of Qcell, a telecommunication company incorporated in the Gambia. He acquired 76.45% of First City Monument Bank shareholding in May 2014 .The Bank is primarily involved in corporate and retail banking.

The Bank’s shareholders as a percentage of subscribed registered capital:

2016

2015

2014

Mr. Muhammed Jah 80.74% 80.74% 76.45%

Islamic Development Bank 13.46% 13.46% 12.75%

Other minority shareholders 5.80% 5.80% 5.48%

The Bank performs its activities in the Gambia through its 6 branches. Revenue was mainly generated from the provision of Islamic banking services in the Gambia. The Bank considers that its products and services arise from one segment of business - the provision of banking and related services. During the year ended 31 December 2016, the Bank’s executive and non-executive directors were as follows:

Names Period Executive Directors:

Mr. Nuha Marenah – Director From January 2015

Non-Executive Directors:

Mr. Muhammed Jah –Chairman From May 2014

Mr. Mamour Malick Jagne- Director Long serving member

Mr. Fye Ceesay-Director Long serving member

IDB Representative Long serving member

22

IFRS FINANCIAL STATEMENTS 2016 23

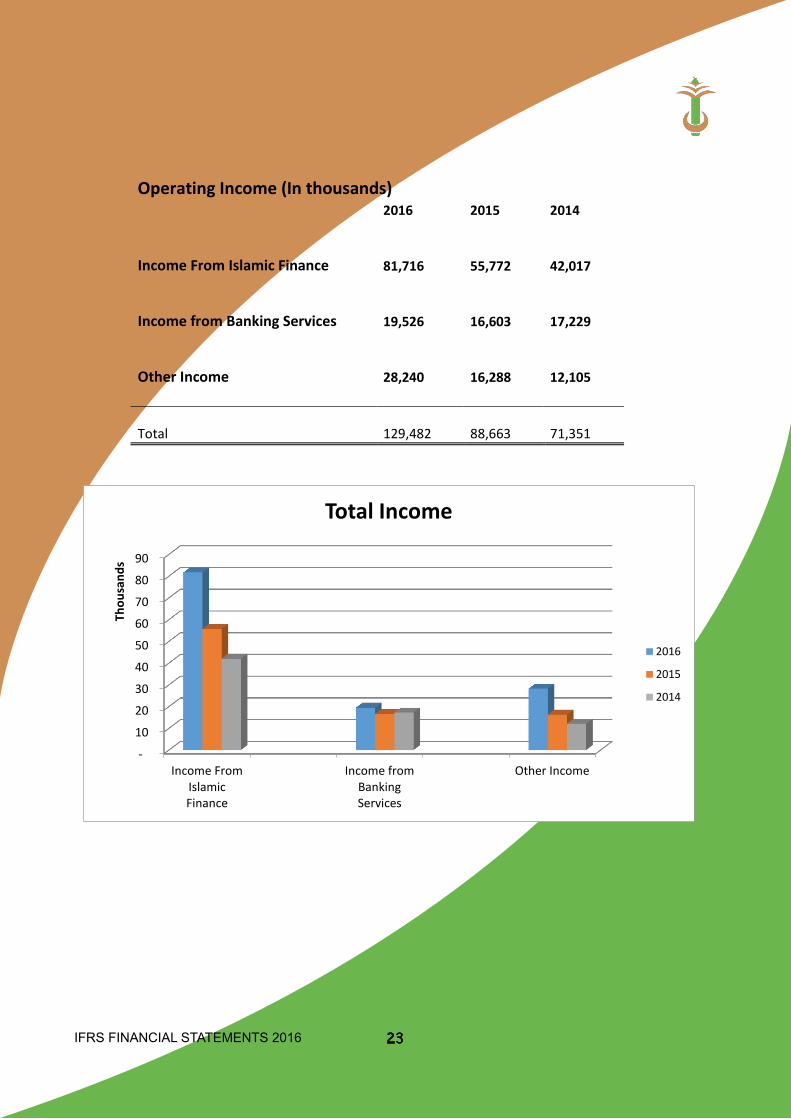

Operating Income (In thousands)

2016 2015 2014

Income From Islamic Finance

81,716

55,772

42,017

Income from Banking Services

19,526

16,603

17,229

Other Income

28,240

16,288

12,105

Total

129,482

88,663

71,351

-

10

20

30

40

50

60

70

80

90

Income FromIslamicFinance

Income fromBankingServices

Other Income

Thou

sand

s

Total Income

2016

2015

2014

IFRS FINANCIAL STATEMENTS 2016

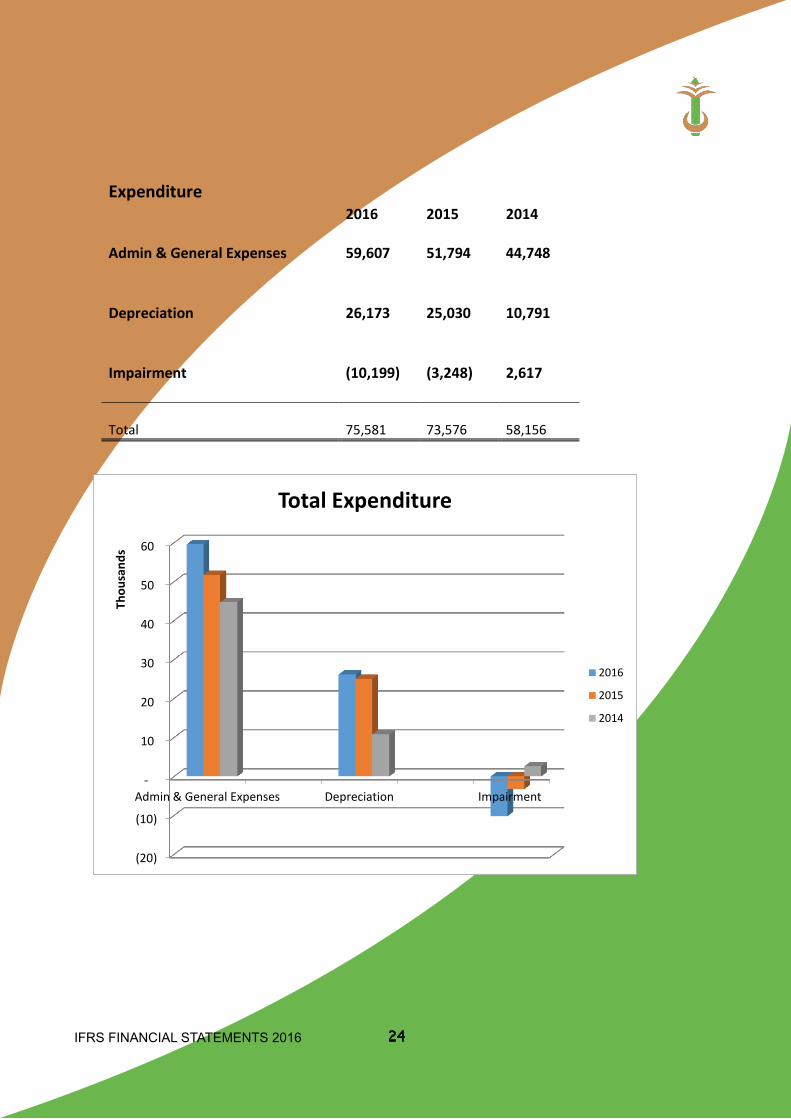

Expenditure

2016 2015 2014

Admin & General Expenses 59,607

51,794

44,748

Depreciation 26,173

25,030

10,791

Impairment (10,199)

(3,248)

2,617

Total

75,581

73,576

58,156

(20)

(10)

-

10

20

30

40

50

60

Admin & General Expenses Depreciation Impairment

Thou

sand

s

Total Expenditure

2016

2015

2014

24

IFRS FINANCIAL STATEMENTS 2016 25

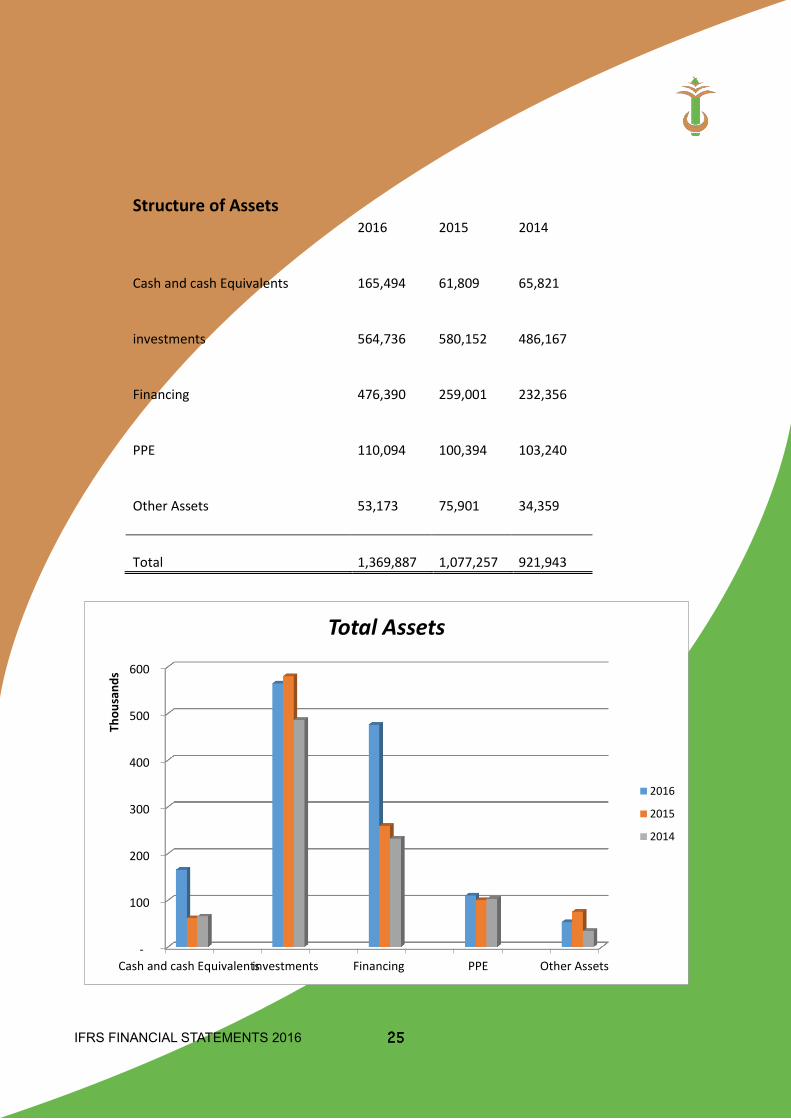

Structure of Assets

2016 2015 2014

Cash and cash Equivalents

165,494

61,809

65,821

investments

564,736

580,152

486,167

Financing

476,390

259,001

232,356

PPE 110,094

100,394

103,240

Other Assets

53,173

75,901

34,359

Total

1,369,887

1,077,257

921,943

-

100

200

300

400

500

600

Cash and cash Equivalentsinvestments Financing PPE Other Assets

Thou

sand

s

Total Assets

2016

2015

2014

IFRS FINANCIAL STATEMENTS 2016

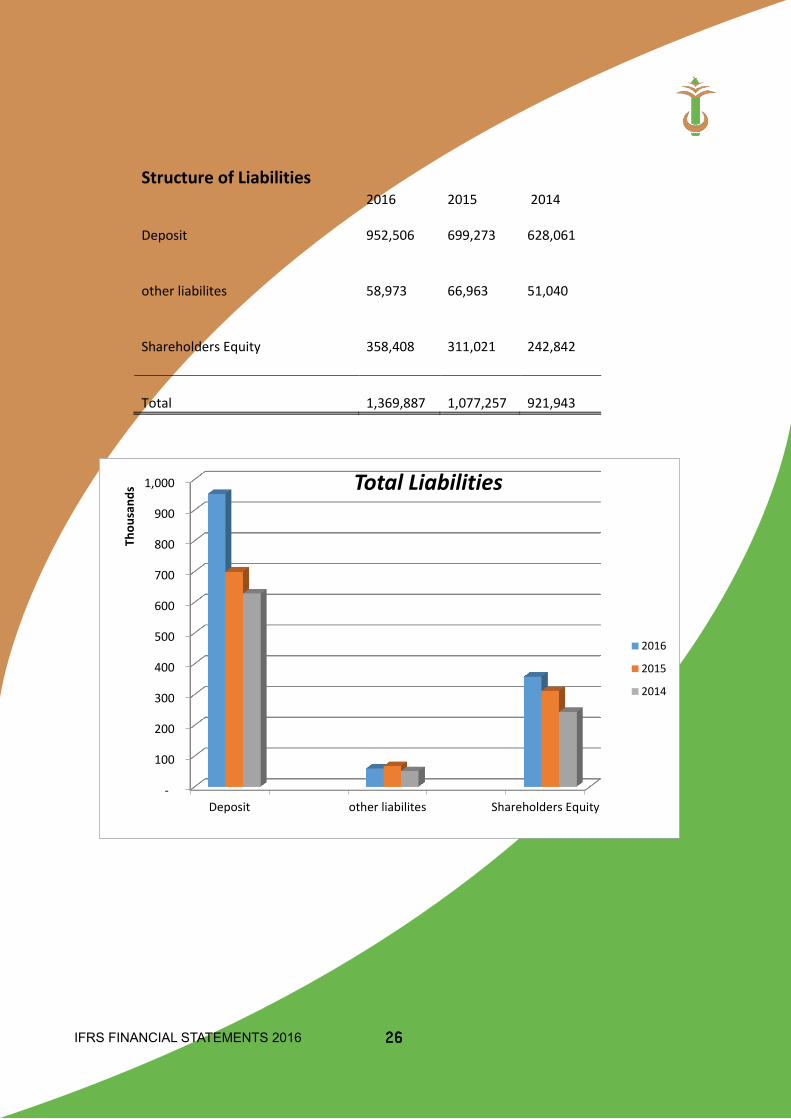

Structure of Liabilities

2016 2015 2014

Deposit 952,506

699,273

628,061

other liabilites

58,973

66,963

51,040

Shareholders Equity

358,408

311,021

242,842

Total

1,369,887

1,077,257

921,943

-

100

200

300

400

500

600

700

800

900

1,000

Deposit other liabilites Shareholders Equity

Thou

sand

s Total Liabilities

2016

2015

2014

26

IFRS FINANCIAL STATEMENTS 2016 27

2. Basis of preparation

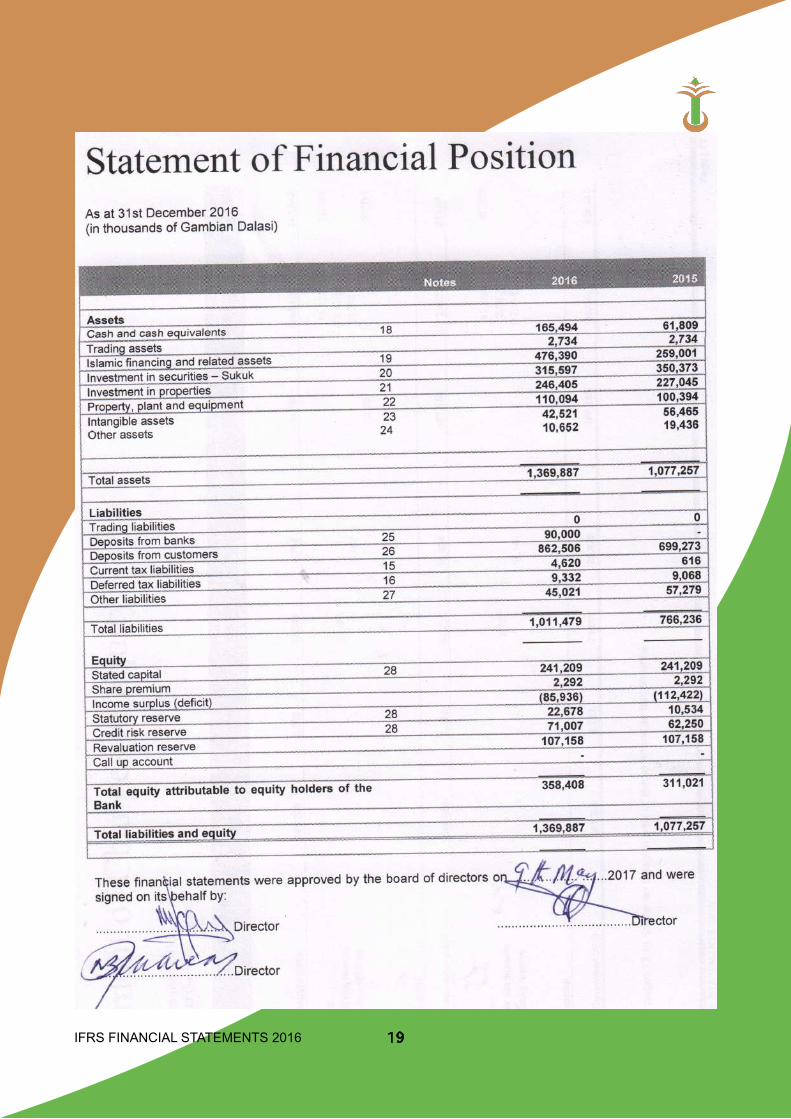

2.1 Statement of compliance These financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and current interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”) and with the relevant provisions of the Banking Act 2009 and The Companies Act 2013.. The financial statements were approved by the Board of Directors on …………………..9th May .........2017.

2.2 Basis of measurement These financial statements are prepared under the historical cost basis.

2.3 Functional and presentation currency The financial statements are presented in The Gambian dalasis (D), which represents the functional and presentation currency of the Bank, being the currency of the economic environment in which the Bank operates. The financial statements have been prepared under the assumption that the Bank will continue as a going concern.

2.4 Use of estimates and judgments The presentation of financial statements in conformity with IFRS requires the preparation of estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and their reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates and future changes in the economic conditions, business strategies, regulatory requirements, accounting rules or/and other factors could subse-quently result in a change in estimates that could have a material impact on the reported financial position and results of operations. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

The following are the critical judgements that the directors have made in the process of applying the Bank’s accounting policies and that have the most significant effect on the amounts recognised in financial statements.

Provisioning for incurred credit losses and identified contingencies involve many uncertainties about the outcome of those risks and require the management of the Bank to make many subjective judgements in estimating the loss amounts.

The income taxes rules and regulations have recently experienced significant changes; there is no major historical precedent and/or interpretation judgement with respect to the extensive and complex issue affecting the banking sector.

3. Significant Accounting Policies The accounting policies set out below have been applied consistently to all periods presented in these financial statements

IFRS FINANCIAL STATEMENTS 2016

3.1 Foreign currency activities

Transactions in currencies other than Dalasi are recorded at the rates of exchange prevailing on the dates of the transactions. At each balance sheet date, monetary assets and liabilities that are denominated in foreign currencies are retranslated at the rates prevailing on the balance sheet date. Non-monetary assets and liabilities carried at fair value that are denominated in foreign currencies are translated at the rates prevailing at the date when the fair value was determined. Gains and losses arising on retranslation are included in net profit or loss for the period, except for exchange differences arising on non-monetary assets and liabilities where the changes in fair value are recognized directly in equity.

3.2 Revenue from investmentsRevenue is generally recognised when future economic benefits of the underlying assets will flow to the Bank and it can be reliably measured. It is income derived from use of an entity’s assets and hence the revenue is mostly dependent on the underlying agreement. Investment income and expense is accrued on a time basis, by reference to the principal outstanding and the effective interest rate applicable. The effective interest rate is the rate that exactly discounts the estimated future cash payments and receipts through the expected life of the financial asset or liability (or, where appropriate, a shorter period) to the carrying amount of the financial asset or liability.

The calculation of the effective interest rate includes all fees paid or received transaction costs, and discounts or premiums that are an integral part of the effective interest rate. Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial asset or liability. Investment income and expense presented in the income statement include:

Profit (markup) on financial assets and liabilities at amortised cost on an effective interest rate basis.

Profit (markup) on Held to maturity investments (Sukuk al Salam) on an effective interest basis.

Investment income and expense on all trading assets and liabilities are considered to be incidental to the bank’s trading operations and are presented together with all other changes in the fair value of trading assets and liabilities in net trading income.

3.3 Fees and commissionFees and commission income and expenses that are integral to the effective interest rate on a financial asset or liability are included in the measurement of the effective interest rate.

Fees and commissions that do not form part of the effective interest rate are recognised as expense and income in the income statement on an accrual basis.

Other fees and commission expense relates mainly to transaction and service fees, which are expensed as the services are received.

3.4 Net trading incomeNet trading income comprises gains less losses related to trading assets and liabilities, and includes all realised and unrealised fair value changes, interest, dividends and foreign exchange differences.

3.5 Lease payments madePayments made under operating leases (Ijaara financing) are recognised in profit or loss on a straight-line basis over the term of the lease.

28

IFRS FINANCIAL STATEMENTS 2016 29

3.6 Income tax expenseIncome tax expense comprises current and deferred tax. Income tax expense is recognised in the income statement except to the extent that it relates to items recognised directly in equity, in which case it is recognised in equity.

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantively enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

Deferred tax is provided using the balance sheet method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is measured at the tax rates that are expected to be applied to the temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the reporting date.

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be available against which the asset can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

3.7 Financial assets and liabilitiesMurabaha is an Islamic financing transaction, which represents an agreement whereby the bank buys a commodity and sells it to a counterparty based on a promise received from that counterparty to buy the commodity according to specific terms and conditions. The selling price comprises of the cost of the commodity and a pre-agreed profit margin.

(i) RecognitionThe Bank initially recognises account receivables issued on the date that they are originated. All other financial assets and liabilities (including assets and liabilities designated at fair value through profit or loss) are initially recognised on the trade date at which the Bank becomes a party to the contractual provisions of the instrument.

Murabaha receivables are recognised upon the sale of the commodity to the counterparty. Income on Murabaha receivables is recognised on an effective yield basis. The effective yield rate is the rate that exactly discounts the estimated future cash payments and receipts through the agreed payment term of the contract to the carrying amount of the receivable. The effective yield is established on initial recognition of the asset and is not revised subsequently. The calculation of the effective yield rate includes all fees paid or received, transaction costs, and discounts or premiums that are an integral part of the effective yield rate.

Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial asset or liability. Commodity Murabaha receivables are initially recorded at fair value and are subsequently measured at amortised cost using the effective yield method, less impairment losses. The accrued income receivable is classified under other assets. Other advances to banks are stated at cost and are non-return bearing.

3.8 Deposits from customersProfit sharing accounts are based on the principle of Mudaraba whereby the Company and the customer share an agreed percentage of any profit earned on the customer’s deposit. The customer’s share of profit is paid in accordance with the terms and conditions of the account. The profit calculation is undertaken at the end of each calendar month.

IFRS FINANCIAL STATEMENTS 2016

Customer Murabaha deposits consist of an Islamic financing transaction involving the Company arranging the purchase of an asset on behalf of the customer and the purchase thereof from the same customer by the Company at cost plus an agreed profit (mark-up) with settlement on a deferred payment basis. Customer Murabaha deposit balances are included in the statement of financial position under deposits from customers and the accrued returns payable to the customer are classified under other liabilities. Returns payable on customer Murabaha deposits are recognised on an effective yield basis over the period of the contract.

3.9 Profit stabilisation reserveThe profit stabilisation reserve is used to maintain returns payable to customers on Mudaraba based savings accounts. Returns payable on these profit sharing accounts are credited to customers in accordance with the terms and conditions of the account. Any surplus returns arising from the investment of funds are then credited to this reserve. In the case of inadequate returns generated by these funds, the Company will maintain the return to depositors by utilising this reserve.

(ii) De-recognitionThe Bank derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards of ownership of the financial asset are transferred.

The Bank derecognises a financial liability when its contractual obligations are discharged or cancelled or expire.

The Bank enters into transactions whereby it transfers assets recognised on its balance sheet, but retains either all risks and rewards of the transferred assets or a portion of them. If all or substantially all risks and rewards are retained, then the transferred assets are not derecognised from the balance sheet.

(iii) OffsettingFinancial assets and liabilities are set off and the net amount presented in the balance sheet when, and only when, the Bank has a legal right to set off the amounts and intends either to settle on a net basis or to realise the asset and settle the liability simultaneously.

Income and expenses are presented on a net basis only when permitted by the accounting standards, or for gains and losses arising from a group of similar transactions such as in trading activity.

(iv) Amortised cost measurementThe amortised cost of a financial asset or liability is the amount at which the financial asset or liability is measured at initial recognition, minus principal repayments, plus or minus the cumulative amortisation using the effective interest method of any difference between the initial amount recognised and the maturity amount, minus any reduction for impairment.

(v) Fair value measurementThe determination of fair values of financial assets and financial liabilities is based on quoted market prices or dealer price quotations for financial instruments traded in active markets. For all other financial instruments fair value is determined by using valuation techniques. Valuation techniques include net present value techniques, the discounted cash flow method, comparison to similar instruments for which market observable prices exist, and valuation models.

30

IFRS FINANCIAL STATEMENTS 2016 31

(i) dentification and measurement of impairmentAt each reporting date the Bank assesses whether there is objective evidence that financial assets not carried at fair value through profit or loss are impaired. Financial assets are impaired when objective evidence demonstrates that a loss event has occurred after the initial

recognition of the asset, and that the loss event has an impact on the future cash flows on the asset that can be estimated reliably.

The bank considers evidence of impairment at both an individual and collective level. All individually significant financial assets are assessed for specific impairment. All significant assets found not to be specifically impaired are then collectively assessed for any impairment that has been incurred but not yet identified. Assets that are not individually significant are then collectively assessed for impairment by grouping together financial assets (carried at amortised cost) with similar risk characteristics.

Objective evidence that financial assets (including equity securities) are impaired can include default or delinquency by a borrower, restructuring of a loan or advance by the Bank on terms that the Bank would not otherwise consider, indications that a borrower or issuer will enter bankruptcy, the disappearance of an active market for a security, or other observable data relating to a group of assets such as adverse changes in the payment status of borrowers or issuers or economic conditions that correlate with defaults. In assessing collective impairment the Bank uses statistical modelling of historical trends of the probability of default, timing of recoveries and the amount of loss incurred, adjusted for management’s judgement as to whether current economic and credit conditions are such that the actual losses are likely to be greater or less than suggested by historical modelling. Default rates, loss rates and the expected timing of future recoveries are regularly benchmarked against actual outcomes to ensure that they remain appropriate.

Impairment losses on assets carried at amortised cost are measured as the difference between the carrying amount of the financial assets and the present value of estimated cash flows discounted at the assets’ original effective interest rate. Losses are recognised in profit or loss and reflected in an allowance account against loans and advances. When a subsequent event causes the amount of impairment loss to decrease, the impairment loss is reversed through profit or loss.

Impairment losses on available-for-sale investment securities are recognised by transferring the difference between the amortised acquisition cost and current fair value out of equity to profit or loss. When a subsequent event that can be related to the event causes the amount of impairment loss on an available-for-sale debt security to decrease, the impairment loss is reversed through profit or loss.

However, any subsequent recovery in the fair value of an impaired available-for-sale equity security is recognised directly in equity. Changes in impairment provisions attributable to time value are reflected as a component of interest income.

IFRS FINANCIAL STATEMENTS 2016

3.10 Cash and cash equivalentsCash and cash equivalents include notes and coins on hand, unrestricted balances held with central banks and highly liquid financial assets with original maturities of less than three months, which are subject to insignificant risk of changes in their fair value, and are used by the Bank in the management of its short-term commitments.

3.11 Account receivablesAccount receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market and that the Bank does not intend to sell immediately or in the near term.

Account receivables are initially measured at amortised cost plus incremental direct transaction costs, and subsequently measured at their amortised cost using the effective interest method less any impairment losses.

3.12 Sukuk Al SalamSukuk al Salam are initially measured at fair value plus incremental direct transaction costs and subsequent-ly accounted for depending on their classification as either held-to-maturity.

(i) Held-to-maturityHeld-to-maturity investments are non-derivative assets with fixed or determinable payments and fixed maturity that the Bank has the positive intent and ability to hold to maturity, and which are not designated at fair value through profit or loss or available-for-sale. Held-to-maturity investments are carried at amortised cost using the effective interest method. Any sale or reclassification of a significant amount of held-to-maturity investments not close to their maturity would result in the reclassification of all held-to-maturity investments as available-for-sale, and prevent the Bank from classifying investment securities as held-to-maturity for the current and the following two financial years. It must be noted that IFRS 9 only considers fair value and amortised cost based on the business models for managing the financial asset and the contractual cash flow characteristics of the financial asset. Thus all HTM assets are classified as amortised cost. (ii) Fair value through profit or loss

The Bank carries no investment securities at fair value, with fair value changes recognised immedi ately in profit or loss.

(iii) Available-for-sale

Available-for-sale investments are non-derivative investments that are not designated as another category of financial assets. Unquoted equity securities whose fair value cannot be reliably measured are carried at cost. All other available-for-sale investments are carried at fair value.Interest income is recognised in profit or loss using the effective interest method. Dividend income is recognised in profit or loss when the Bank becomes entitled to the dividend. Foreign exchange gains or losses on available-for-sale debt security investments are recognised in profit or loss. Other fair value changes are recognised directly in equity until the investment is sold or impaired and the balance in equity is transferred to profit or loss.

3.13 Property, plant and equipment(i) Recognition and measurementItems of property and equipment are measured at cost less accumulated depreciation and impairment loss-es.

32

IFRS FINANCIAL STATEMENTS 2016 33

(ii) DepreciationDepreciation is recognised in profit or loss on a straight-line basis over the estimated useful lives of each item of property, plant and equipment. Leased assets are depreciated over the shorter of the lease term and their useful lives. Land is not depreciated.

The estimated useful lives for the current and comparative periods are as follows:

• Buildings 10%• Furniture and equipment 20%• Motor Vehicle 25%

Depreciation methods, useful lives and residual values are reassessed at each reporting date. 3.14 Intangible assets

An Intangible asset is generally considered as an identifiable non-monetary asset without physical substance. It is distinguished from goodwill based on the identifiability concept. It is recognised when future economic benefits will flow to the Bank and it can be reliably measured. The useful life may be finite or indefinite depending on the nature and legal framework underpinning the transaction. Impairment assessment is made of all indefinite intangibles at each reporting date and the appropriate adjustments made.

(i) SoftwareSoftware acquired by the Bank is stated at cost less accumulated amortisation and accumulated impairment losses.

Subsequent expenditure on software assets is capitalised only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is expensed as incurred.

Amortisation is recognised in profit or loss on a straight-line basis over the estimated useful life of the software, from the date that it is available for use. The estimated useful life of software is three to five years. 3.15 Leased assets – lessee (Ijaara financing)

Other leases are operating leases and, except for investment property, the leased assets are not recognised on the bank’s statement of financial position. Investment property held under an operating lease is recognised on the Bank’s financial position at its fair value.

3.16 Impairment of non-financial assetsThe carrying amounts of the Bank’s non-financial assets, other than investment property and deferred tax assets are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists then the asset’s recoverable amount is estimated. The recoverable amount of goodwill is estimated at each reporting date.

An impairment loss is recognised if the carrying amount of an asset or its cash-generating unit exceeds its recoverable amount. A cash-generating unit is the smallest identifiable asset group that generates cash flows that largely are independent from other assets and groups. Impairment losses are recognised in profit or loss. Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amount of any goodwill allocated to the units and then to reduce the carrying amount of the other assets in the unit (group of units) on a pro rata basis.

IFRS FINANCIAL STATEMENTS 2016

The recoverable amount of an asset or cash-generating unit is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset.

3.17 ProvisionsA provision is recognised if, as a result of a past event, the Bank has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability.

A provision for restructuring is recognised when the Bank has approved a detailed and formal restructuring plan, and the restructuring either has commenced or has been announced publicly. Future operating costs are not provided for.

3.18 Personnel Expenses

(i) Defined contribution plansThe Bank operates a defined contribution plan for all employees. Under the plan, fixed contributions are paid into a separate entity and the Bank will have no legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution pension plans are recognised as an employee benefit ex-pense in profit or loss in the periods during which services are rendered by employees. Prepaid contributions are recognised as an asset to the extent that a cash refund or a reduction in future payments is available.

(ii) Short-term benefitsShort-term employee benefit obligations are measured on an undiscounted basis and are expensed as the related service is provided.

A provision is recognised for the amount expected to be paid under short-term cash bonus or profit-sharing plans if the Bank has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee and the obligation can be estimated reliably. 3.19 Share capital and reserves The Bank classifies capital instruments as financial liabilities or equity instruments in accordance with the substance of the contractual terms of the instrument.

Share issue costsIncremental costs directly attributable to the issue of an equity instrument are deducted from the initial mea-surement of the equity instruments.

34

IFRS FINANCIAL STATEMENTS 2016 35

3.20 Earnings per share

The bank presents basic and diluted earnings per share (EPS) data for its ordinary shares. Basic EPS is calculated by dividing the profit or loss attributable to ordinary shareholders of the bank by the weighted average number of ordinary shares outstanding during the period. Diluted EPS is determined by adjusting the profit or loss attributable to ordinary shareholders and the weighted average number of ordinary shares outstanding for the effects of all dilutive potential ordinary shares.

3.21 DividendsDividends are recognised as a liability in the period in which they are declared.

3.22 Sukuk Al SalamSecurities purchased from the Central Bank of The Gambia under agreement to resell (reverse Repos), are disclosed as Sukuk al Salam as they are held to maturity after which they are repurchased and are not nego-tiable or discounted during the tenure.

3.23 Acceptances and letters of credit

Acceptances and Letters of credits are considered contingent liabilities and are disclosed unless the possibil-ity of an outflow of resources involving economic benefits is remote.

3.24 Borrowings (liabilities to banks and customers)

Borrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are subse-quently stated at amortised cost using the effective interest method, any differences between proceeds (net of transaction costs) and the redemption value is recognised in the income statement over the period of the borrowings. Borrowings and other forms of financial liabilities shall be de-recognised from the books only when they are extinguished, ie when the obligation specified in the contract is discharged or cancelled or expires.

4. Financial risk management

Introduction and overviewThe Bank has exposure to the following risks arising from the use of financial instruments. Typical of such risks are as follows:

• credit risk• liquidity risk• market risk• operational risk.

These are principal risks of the Bank. This note presents information about the Bank exposure to these risks, including the objectives, policies and processes for measuring and managing the risks as well as their impact on earnings and capital.

IFRS FINANCIAL STATEMENTS 2016

Risk management frameworkThis depends mainly on the Risk Management framework set out by the Central Bank. Bank specific frame-work based on the overall structure of the Bank ensures that the Board of Directors has overall responsibility for the establishment and oversight of the Bank’s risk management framework. The Board has established the Asset and Liability (ALCO), Credit and Operational Risk committees, which are responsible for develop-ing and monitoring risk management policies in their specified areas. All Board committees have both execu-tive and non-executive members and report regularly to the Board of Directors on their activities.

The Bank’s risk management policies are established to identify and analyse the risks faced by the Bank, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk man-agement policies and systems are reviewed regularly to reflect changes in market conditions, products and services offered. The bank, through its training and management standards and procedures, aims to develop a disciplined and constructive control environment, in which all employees understand their roles and obliga-tions.

The Bank’s Audit Committee is responsible for monitoring compliance with the Bank’s risk manage-ment policies and procedures, and for reviewing the adequacy of the risk management framework in relation to the risks faced by the Bank. The Bank’s Audit Committee is assisted in these functions by Internal Audit. Internal Audit undertakes both regular and ad-hoc reviews of risk management controls and procedures, the results of which are reported to the Audit Committee.