Embed Size (px)

Citation preview

Page 2

TABLE OF CONTENTS

The statements contained in this supplemental may include forward-looking statements within the meaning of the federal securities law. These forward-looking statements include statements relating to, amongothers things, achievement of strategic targets, expectations for our operating results, business and financial condition, business and our growth prospects, as well as statements that are generally accompanied bywords such as believes, anticipates, expects, estimates, should, seeks, intends, proposed, planned, outlook, remain confident, and goal or similar expressions. Although Liberty believes that the expectations reflectedin such forward-looking statements are based on reasonable assumptions, it can give no assurance that its expectations will be achieved. As forward-looking statements, these statements involve risks, uncertaintiesand other factors that could cause actual results to differ materially from the expected results. These risks, uncertainties and other factors include, without limitation, uncertainties affecting real estate businessgenerally (such as entry into new leases, renewals of leases and dependence on tenants’ business operations), risks relating to the integration of the operations of entities that we have acquired or may acquire, risksrelating to our plans for disposing of certain properties, risks relating to financing arrangements and sales of securities, possible environmental liabilities, risks relating to leverage and debt service (including availabilityof financing terms acceptable to the company and sensitivity of the company’s operations and financing arrangements to fluctuations in interest rates), dependence on the primary markets in which the company’sproperties are located, the existence of complex regulations relating to status as a REIT and the adverse consequences of the failure to qualify as a REIT, risks relating to litigation, including without limitation litigationinvolving entities that we have a acquired or may acquire, and the potential adverse impact of market interest rates on the market price for the company’s securities, and other risks and uncertainties detailed in thecompany’s filings with the Securities and Exchange Commission. The company assumes no obligation to update or supplement forward-looking statements that become untrue because of subsequent events.

NEWS RELEASE 3

HIGHLIGHTS 6

FINANCIAL INFORMATION Consolidated Balance Sheets 7 Consolidated Statements of Comprehensive Income 8 Funds from Operations and Adjusted Funds from Operations 9 Adjusted EBITDA 10

OPERATIONS Portfolio Profile 11 Lease Analysis 16 Lease Expirations 19 Top Ten Largest Tenants 21 Same Store Properties 22 Fully Stabilized Properties 23

REAL ESTATE INVESTMENTS Completed Development Properties 24 Development Starts 25 Development Properties 26 Acquisitions 28 Dispositions 29 Unconsolidated Joint Ventures 30

CAPITALIZATION Debt & Preferred Unit Analysis 31 Debt Statistics & Ratios 32 Debt Covenants & Credit Ratings 33

GUIDANCE 34

NET ASSET VALUE COMPONENTS 35

NON-GAAP FINANCIAL MEASURES AND OTHER DEFINED TERMS 36

SECOND QUARTER 2017 SUPPLEMENTAL

NEWS RELEASE

SECOND QUARTER 2017 SUPPLEMENTAL

Inquiries: Jeanne Leonard, Liberty Property Trust, 610.648.1704

Liberty Property Trust Announces Second Quarter 2017 Results

Malvern, PA, July 25, 2017 - Liberty Property Trust announced financial and operating results for the quarter ended June 30, 2017.

Management Comments”Liberty’s results at mid-year reflect the continued strength of the industrial real estate market,” said Bill Hankowsky, chairman and chiefexecutive officer. “We anticipate consistently strong leasing volumes, rent growth and occupancy gains for the remainder of the year.” Highlights for Second Quarter 2017

▪ Net income available to common shareholders $0.35 per diluted share▪ NAREIT Funds from Operations $0.65 per diluted share▪ Same store operating income increased by 1.4%, over prior year quarter▪ Same store operating income for the industrial portfolio increased by 2.7%▪ Portfolio occupancy on a commenced basis at quarter-end 95.6%, and on a signed basis 97.2%▪ 6.5 million square feet of lease transactions completed▪ Rents on industrial leases up 11.9%▪ Rents on office leases up 5.7%▪ $73.6 million in development starts

Earnings Guidance▪ Liberty increased Funds from Operations guidance range for 2017 to be $2.49 - $2.55 per diluted share

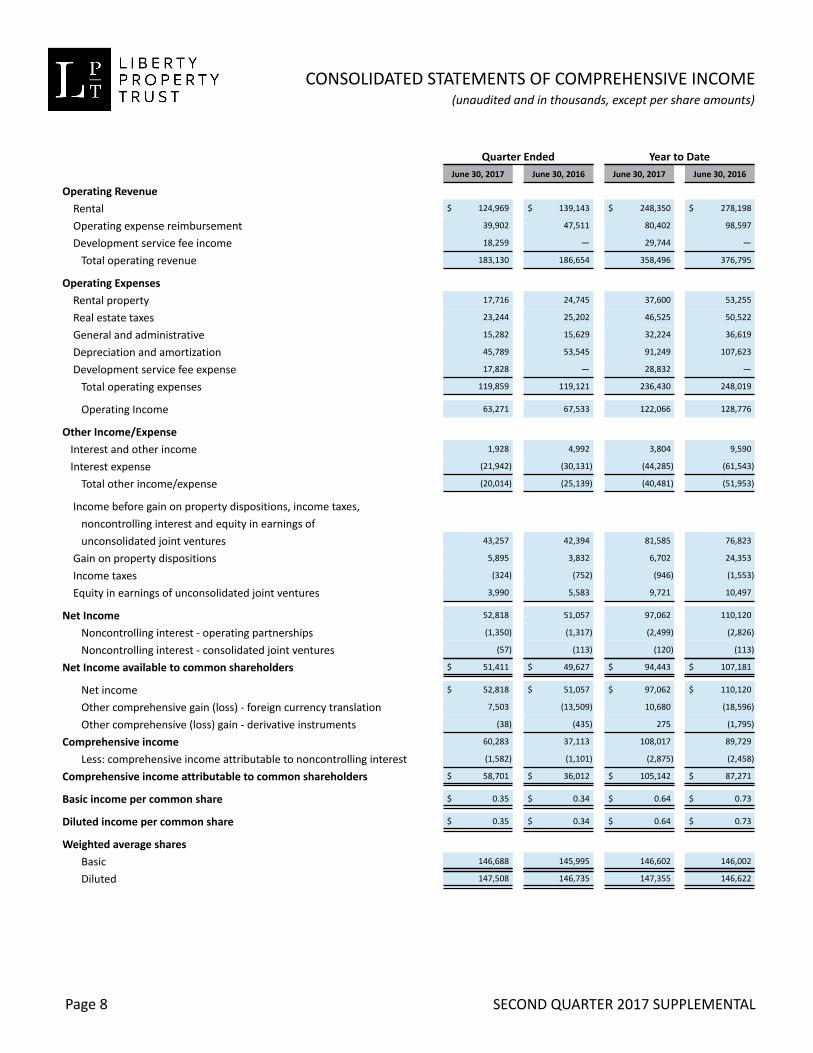

Financial ResultsNet income: Net income available to common shareholders for the second quarter of 2017 was $51.4 million, or $0.35 per diluted share,compared to $49.6 million, or $0.34 per diluted share, for the second quarter of 2016.

For the six months ended June 30, 2017, net income available to common shareholders was $94.4 million, or $0.64 per diluted share,compared to $107.2 million, or $0.73 per diluted share, for the first six months of 2016.

Funds from Operations: The company uses the National Association of Real Estate Investment Trusts (“NAREIT”) definition of Funds fromOperations (“FFO”) as an operating measure of the company’s financial performance. A reconciliation of U.S. GAAP net income to NAREITFFO is included in the financial data tables accompanying this press release.

NAREIT FFO available to common shareholders for the second quarter of 2017 was $98.2 million, or $0.65 per diluted share, compared to$102.2 million, or $0.68 per diluted share, for the second quarter of 2016.

Net income and NAREIT FFO for the second quarter of 2017 were impacted by gain on the sale of non-depreciable assets of $3.8 million($0.025 per diluted share).

FFO available to common shareholders for the six months ended June 30, 2017 was $188.8 million, or $1.25 per diluted share, compared to$195.3 million, or $1.30 per diluted share, for the first six months of 2016.

Operating PerformanceSame Store Performance: Property level operating income for same store properties increased by 0.7% on a cash basis and by 1.4% on astraight line basis for the second quarter of 2017, compared to the same quarter in 2016. For the six months ended June 30, 2017, propertylevel operating income for same store properties increased by 1.1% on a cash basis and on a straight line basis, compared to the same periodin 2016.

▪ Same store operating income for the industrial portfolio increased by 2.1% on a cash basis and 2.7% on a straight line basis. For thesix months ended June 30, 2017, industrial same store operating income increased by 2.3% on a cash basis and 2.4% on a straightline basis, compared to the same period in 2016.

NEWS RELEASE

SECOND QUARTER 2017 SUPPLEMENTAL

▪ Same store operating income for the office portfolio decreased by 6.6% on a cash basis and by 5.5% on a straight line basis. For thesix months ended June 30, 2017, office same store operating income decreased by 5.2% on a cash basis and on a straight line basis,compared to the same period in 2016.

Occupancy: At June 30, 2017, Liberty’s operating portfolio of 98.9 million square feet was 95.6% occupied, compared to 96.1% at the end ofthe first quarter 2017. During the quarter, Liberty completed lease transactions totaling 6.5 million square feet of space, and occupancy on asigned but not yet commenced basis is 97.2%.

Industrial Portfolio: The primary driver of Liberty’s results is the performance of its industrial portfolio. The 92.3 million square footindustrial portfolio was 95.9% leased at quarter-end, compared to 96.6% for the previous quarter. Industrial distribution rents increased11.9% on renewal and replacement leases signed during the quarter. 96% of these leases have built-in rent escalators.

Office Portfolio: Occupancy of Liberty’s 6.6 million square foot office portfolio was 91.5%, up from 88.4% from the previous quarter. Duringthe quarter, a previously announced lease for 170,000 square feet of office space commenced. This lease resulted in a significant increase inoffice occupancy, as well as a higher than usual tenant improvement costs. Office rents increased 5.7% on renewal and replacement leasessigned in the office portfolio, and 97% of these leases contain built-in rent escalators.

Real Estate InvestmentsDevelopment Deliveries: In the second quarter, Liberty brought into service four wholly-owned development properties for a totalinvestment of $65.2 million. The properties contain 724,000 square feet of leasable space and were 100% occupied as of the end of thequarter. The yield on these properties at June 30, 2017 was 7.9%.

Development Starts: In the second quarter, Liberty began development of two wholly-owned properties totaling 1,026,000 square feet ofleasable space at a projected investment of $73.6 million. The properties consist of:

▪ 7157 Ridge Road, Hanover, MD, 220,000 square feet, 100% leased▪ 100 Carolina Way, Carlisle, PA 805,600 square feet for inventory

Real Estate AcquisitionsDuring the second quarter, Liberty purchased one 101,000 square foot industrial building currently under development in Gardena, CA for$20.1 million.

Real Estate DispositionsDuring the second quarter, Liberty sold two suburban office buildings totaling 94,000 square feet for $8.1 million.

2017 OutlookA reconciliation of projected NAREIT FFO per share to projected U.S. GAAP net income available to common shareholders per share for 2017is below (all amounts projected). Additional information on assumptions underlying this guidance is included in Liberty’s second quartersupplemental financial report on the company’s website.

About the CompanyLiberty Property Trust (NYSE:LPT) is a leader in commercial real estate, serving customers in the United States and United Kingdom, throughthe development, acquisition, ownership and management of superior office and industrial properties. Liberty's 99 million square footoperating portfolio includes 560 properties which provide office, distribution and light manufacturing facilities to 1,200 tenants.

Revised 2017 Outlook Previous 2017 Outlook

Net income available to common shareholders per diluted share $1.99 - $2.19 $1.42 - $1.75

Depreciation and amortization of unconsolidated joint ventures 0.05 - 0.07 0.06 - 0.08

Depreciation and amortization 1.18 - 1.20 1.24 - 1.28

Gain on property dispositions (1) (0.74) - (0.92) (0.30) - (0.60)

Noncontrolling interest share of addbacks 0.01 - 0.01 0.00 - 0.01

NAREIT FFO, per diluted share $2.49 - $2.55 $2.42 - $2.52

(1) Includes equity share of gain on disposition of unconsolidated joint ventures.

NEWS RELEASE

SECOND QUARTER 2017 SUPPLEMENTAL

Additional information about the company, including Liberty’s Quarterly Supplemental Package with detailed financial information, isavailable in the Investors section of the Company’s web site at www.libertyproperty.com. If you are unable to access the web site, a copy ofthe supplemental package may be obtained by contacting Liberty by phone at 610-648-1704, or by e-mail to [email protected].

Liberty will host a conference call during which management will discuss second quarter results on Tuesday, July 25, 2017, at 1 p.m. EasternTime. To access the conference call, please dial 855-277-7530. The passcode needed for access is 46839831. A replay of the call will beavailable until August 25, 2017, by dialing 1-855-859-2056 using the same passcode as above. The call can also be accessed via the Interneton the Investors page of Liberty’s web site at www.libertyproperty.com.

The statements contained in this press release may include forward-looking statements within the meaning of the federal securities law.These forward-looking statements include statements relating to, among others things, achievement of strategic targets, expectations for ouroperating results, business and financial condition, business and our growth prospects, as well as statements that are generally accompanied by words such as “believes,” “anticipates,” “expects,” “estimates,” “should,” “seeks,” “intends,” “proposed,” “planned,”“outlook,” “remain confident,” and “goal” or similar expressions. Although Liberty believes that the expectations reflected in such forward-looking statements are based on reasonable assumptions, it can give no assurance that its expectations will be achieved. As forward-lookingstatements, these statements involve risks, uncertainties and other factors that could cause actual results to differ materially from theexpected results. These risks, uncertainties and other factors include, without limitation, uncertainties affecting real estate businessgenerally (such as entry into new leases, renewals of leases and dependence on tenants’ business operations), risks relating to our ability tomaintain and increase property occupancy and rental rates, risks relating to the continued repositioning of the Company's portfolio, risksrelating to construction and development activities, risks relating to acquisition and disposition activities, risks relating to the integration ofthe operations of entities that we have acquired or may acquire, risks relating to joint venture relationships and any possible need toperform under certain guarantees that we have issued or may issue in connection with such relationships, risks related to propertiesdeveloped by the Company on a fee basis, risks associated with tax abatement, tax credit programs, or other government incentives,possible environmental liabilities, risks relating to leverage and debt service (including availability of financing terms acceptable to theCompany and sensitivity of the Company's operations and financing arrangements to fluctuations in interest rates), dependence on theprimary markets in which the Company's properties are located, the existence of complex regulations relating to status as a REIT and theadverse consequences of the failure to qualify as a REIT, risks relating to litigation and the potential adverse impact of market interest rateson the market price for the Company's securities, and other risks and uncertainties detailed in the company’s filings with the Securities andExchange Commission. The company assumes no obligation to update or supplement forward-looking statements that become untruebecause of subsequent events.

# # #

HIGHLIGHTS

SECOND QUARTER 2017 SUPPLEMENTAL

EARNINGS

Quarter Ended Year to Date

6/30/2017 6/30/2016 6/30/2017 6/30/2016

Net income per share - diluted $ 0.35 $ 0.34 $ 0.64 $ 0.73

NAREIT FFO per share - diluted $ 0.65 $ 0.68 $ 1.25 $ 1.30

Dividend per share $ 0.40 $ 0.475 $ 0.80 $ 0.95

OPERATIONS

Straight Line Cash

Quarter ended6/30/2017 Year to Date 2017

Quarter ended6/30/2017 Year to Date 2017

Same store NOI growth 1.4 % 1.1 % 0.7 % 1.1 %

Same store NOI growth - Industrial 2.7 % 2.4 % 2.1 % 2.3 %

Same store NOI growth- Office (5.5)% (5.2)% (6.6)% (5.2)%

Rent growth 9.6 % 13.1 % 0.9 % 4.0 %

Rent growth - Industrial 11.9 % 14.9 % 3.5 % 5.8 %

Rent growth - Office 5.7 % 6.1 % (4.0)% (3.1)%

OCCUPANCY (includes joint ventures at 100%)

6/30/2017 3/31/2017 12/31/2016

Total Company 95.6% 96.1% 96.4 %

Industrial 95.9% 96.6% 96.7 %

Office 91.5% 88.4% 92.0 %

REAL ESTATE INVESTMENTS (includes joint ventures at 100%)

Quarter ended 6/30/2017

# of bldgs Square Feet OccupancyInvestment

(in 000s)Development starts (1) 2 1,025,600 21.5% $ 73,579

Development completions 4 723,505 100.0% 65,198

Acquisitions 1 100,580 — (2) 20,069

Dispositions 2 93,502 29.4% 8,068

6/30/2017

# of bldgs Square Feet Percent LeasedInvestment

(in 000s)Development under construction 30 8,358,017 52.7% $ 1,600,700

(1) Occupancy for development starts represents percent pre-leased.

(2) This property was under development when acquired. It is 100% pre-leased.

Page 6

CONSOLIDATED BALANCE SHEETS

SECOND QUARTER 2017 SUPPLEMENTAL

(unaudited and in thousands)

June 30, 2017 December 31, 2016

Assets Real estate:

Land and land improvements $ 1,094,121 $ 1,094,470

Building and improvements 4,562,908 4,501,921

Less: accumulated depreciation (995,032) (940,115)

Operating real estate 4,661,997 4,656,276

Development in progress 410,027 267,450

Land held for development 351,933 336,569

Net real estate 5,423,957 5,260,295

Cash and cash equivalents 14,748 43,642

Restricted cash 18,115 12,383

Accounts receivable 14,509 13,994

Deferred rent receivable 120,124 109,245

Deferred financing and leasing costs, net 159,112 153,393

Investments in and advances to unconsolidated joint ventures 268,346 245,078

Assets held for sale 2,731 4,548

Prepaid expenses and other assets 137,993 150,235

Total assets $ 6,159,635 $ 5,992,813

Liabilities

Mortgage loans, net $ 271,851 $ 276,650

Unsecured notes, net 2,281,650 2,280,286

Credit facility 177,000 —

Accounts payable 56,188 65,914

Accrued interest 21,718 21,878

Dividend and distributions payable 60,334 71,501

Other liabilities 222,697 206,124

Total liabilities 3,091,438 2,922,353

Noncontrolling interest 7,537 7,537

Equity Shareholders' equity

Common shares of beneficial interest 147 147

Additional paid-in capital 3,666,703 3,655,910

Accumulated other comprehensive loss (45,332) (56,031)

Distributions in excess of net income (619,929) (596,635)

Total shareholders' equity 3,001,589 3,003,391

Noncontrolling interest - operating partnership 54,170 54,631

Noncontrolling interest - consolidated joint ventures 4,901 4,901

Total equity 3,060,660 3,062,923

Total liabilities, noncontrolling interest - operating partnership and equity $ 6,159,635 $ 5,992,813

Page 7

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

SECOND QUARTER 2017 SUPPLEMENTAL

(unaudited and in thousands, except per share amounts)

Quarter Ended Year to DateJune 30, 2017 June 30, 2016 June 30, 2017 June 30, 2016

Operating Revenue

Rental $ 124,969 $ 139,143 $ 248,350 $ 278,198

Operating expense reimbursement 39,902 47,511 80,402 98,597

Development service fee income 18,259 — 29,744 —

Total operating revenue 183,130 186,654 358,496 376,795

Operating Expenses

Rental property 17,716 24,745 37,600 53,255

Real estate taxes 23,244 25,202 46,525 50,522

General and administrative 15,282 15,629 32,224 36,619

Depreciation and amortization 45,789 53,545 91,249 107,623

Development service fee expense 17,828 — 28,832 —

Total operating expenses 119,859 119,121 236,430 248,019

Operating Income 63,271 67,533 122,066 128,776

Other Income/Expense

Interest and other income 1,928 4,992 3,804 9,590

Interest expense (21,942) (30,131) (44,285) (61,543)

Total other income/expense (20,014) (25,139) (40,481) (51,953)

Income before gain on property dispositions, income taxes,

noncontrolling interest and equity in earnings of

unconsolidated joint ventures 43,257 42,394 81,585 76,823

Gain on property dispositions 5,895 3,832 6,702 24,353

Income taxes (324) (752) (946) (1,553)

Equity in earnings of unconsolidated joint ventures 3,990 5,583 9,721 10,497

Net Income 52,818 51,057 97,062 110,120

Noncontrolling interest - operating partnerships (1,350) (1,317) (2,499) (2,826)

Noncontrolling interest - consolidated joint ventures (57) (113) (120) (113)

Net Income available to common shareholders $ 51,411 $ 49,627 $ 94,443 $ 107,181

Net income $ 52,818 $ 51,057 $ 97,062 $ 110,120

Other comprehensive gain (loss) - foreign currency translation 7,503 (13,509) 10,680 (18,596)

Other comprehensive (loss) gain - derivative instruments (38) (435) 275 (1,795)

Comprehensive income 60,283 37,113 108,017 89,729

Less: comprehensive income attributable to noncontrolling interest (1,582) (1,101) (2,875) (2,458)

Comprehensive income attributable to common shareholders $ 58,701 $ 36,012 $ 105,142 $ 87,271

Basic income per common share $ 0.35 $ 0.34 $ 0.64 $ 0.73

Diluted income per common share $ 0.35 $ 0.34 $ 0.64 $ 0.73

Weighted average shares

Basic 146,688 145,995 146,602 146,002

Diluted 147,508 146,735 147,355 146,622

Page 8

SECOND QUARTER 2017 SUPPLEMENTAL

Quarter Ended Year to Date

June 30, 2017 June 30, 2016 June 30, 2017 June 30, 2016

NAREIT FFO

Reconciliation of net income available to common shareholders to NAREITFFO available to common shareholders:

Net income available to common shareholders $ 51,411 $ 49,627 $ 94,443 $ 107,181

Adjustments:

Depreciation and amortization of unconsolidated joint ventures 2,295 2,262 4,620 4,938

Depreciation and amortization 45,343 53,142 90,421 106,894

Gain on property dispositions / impairment - real estate assets ofunconsolidated joint ventures — (153) — (1,993)

Gain on property dispositions / impairment - real estate assets (2,108) (3,832) (2,915) (24,353)

Noncontrolling interest share in addback for depreciation and amortizationand gain on property dispositions / impairment - real estate assets (1,065) (1,213) (2,155) (2,017)

NAREIT FFO available to common shareholders - basic 95,876 99,833 184,414 190,650

Noncontrolling interest share in addback for depreciation and amortizationand gain on property dispositions / impairment - real estate assets 1,065 1,213 2,155 2,017

Noncontrolling interest excluding preferred unit distributions 1,232 1,199 2,263 2,590

NAREIT FFO available to common shareholders - diluted $ 98,173 $ 102,245 $ 188,832 $ 195,257

NAREIT FFO available to common shareholders - basic per share $ 0.65 $ 0.68 $ 1.26 $ 1.31

NAREIT FFO available to common shareholders - diluted per share $ 0.65 $ 0.68 $ 1.25 $ 1.30

AFFO

NAREIT FFO available to common shareholders - diluted $ 98,173 $ 102,245 $ 188,832 $ 195,257

Straight line rent adjustment, net of related bad debt expense (4,979) (3,179) (9,946) (7,603)

Share - based compensation expense 2,324 1,615 8,864 8,802

Tenant Improvements and Lease Transaction Costs (18,213) (18,515) (28,012) (29,928)

Non-reimbursed Capital Expenditures (4,527) (2,871) (4,933) (4,459)

Gain on sale of non-depreciable assets (3,801) — (3,817) —

Gain on debt extinguishment — (3,331) — (4,243)

AFFO available to common shareholders - diluted $ 68,977 $ 75,964 $ 150,988 $ 157,826

Reconciliation of weighted average shares:

Weighted average common shares - all basic calculations 146,688 145,995 146,602 146,002

Dilutive shares for long term compensation plans 820 740 753 620

Diluted shares for net income calculations 147,508 146,735 147,355 146,622

Weighted average common units 3,528 3,539 3,528 3,539

Diluted shares for NAREIT FFO calculations 151,036 150,274 150,883 150,161

(in thousands, except per share amounts)

Page 9

FUNDS FROM OPERATIONSADJUSTED FUNDS FROM OPERATIONS

ADJUSTED EBITDA

SECOND QUARTER 2017 SUPPLEMENTAL

(in thousands)

Quarter Ended Year to Date

June 30, 2017 June 30, 2016 June 30, 2017 June 30, 2016

Net Income $ 52,818 $ 51,057 $ 97,062 $ 110,120

Depreciation and amortization expense 45,789 53,545 91,249 107,623

Interest expense 21,942 30,131 44,285 61,543

Gain on property dispositions (5,895) (3,832) (6,702) (24,353)

Income taxes 324 752 946 1,553

Share-based compensation expense 2,324 1,615 8,864 8,802

Adjusted EBITDA $ 117,302 $ 133,268 $ 235,704 $ 265,288

Page 10

PORTFOLIO PROFILE - TOTAL COMPANY

SECOND QUARTER 2017 SUPPLEMENTAL

MarketsNumber ofProperties Square Feet

Percent ofSF Occupancy Net Rent

Net Rent perOccupied SF

Percent ofNet Rent

WHOLLY OWNED

Operating:

Arizona 2,390,625 2.6% 93.1% $ 15,619,577 $ 7.02 3.3%

Atlanta 2,090,709 2.2% 93.2% 7,468,941 3.83 1.6%

Carolinas 8,163,114 8.7% 98.1% 36,387,430 4.54 7.8%

Chicago/Milwaukee 7,222,412 7.7% 93.7% 29,164,814 4.31 6.3%

Cincinnati/Columbus/Indianapolis 3,948,376 4.2% 99.6% 13,146,497 3.34 2.8%

Dallas 2,202,641 2.4% 100.0% 9,971,290 4.53 2.1%

Houston 7,439,119 8.0% 89.0% 39,551,386 5.97 8.5%

Lehigh Valley/Central PA 25,920,067 27.8% 98.0% 127,356,986 5.01 27.3%

Maryland 3,708,262 4.0% 95.2% 18,288,792 5.18 3.9%

Minnesota 2,984,807 3.2% 85.9% 12,117,060 4.73 2.6%

New Jersey 825,985 0.9% 100.0% 3,356,800 4.06 0.7%

Orlando 2,350,932 2.5% 94.5% 15,265,122 6.87 3.3%

Philadelphia 1,417,853 1.5% 98.2% 30,983,925 22.25 6.6%

Richmond/Hampton Roads 4,519,206 4.9% 95.6% 19,551,867 4.52 4.2%

South Florida 2,437,157 2.6% 98.3% 17,029,707 7.11 3.6%

Southeastern PA 2,618,893 2.8% 93.0% 37,616,921 15.44 8.1%

Southern California 2,089,212 2.2% 92.3% 9,463,290 4.91 2.0%

Tampa 1,805,494 1.9% 99.5% 9,103,833 5.07 2.0%

United Kingdom 1,518,861 1.6% 98.6% 12,479,910 8.33 2.7%

Washington D.C. 146,472 0.2% 66.6% 2,682,925 27.50 0.6%

Total Operating Properties 497 85,800,197 91.9% 95.7% $ 466,607,073 $ 5.68 100.0%

Development:

Arizona 894,847 1.0%

Atlanta 235,234 0.3%

Carolinas 574,220 0.6%

Chicago/Milwaukee 95,962 0.1%

Dallas 562,468 0.6%

Houston 415,272 0.4%

Lehigh Valley/Central PA 1,905,600 2.0%

Maryland 436,000 0.4%

New Jersey 182,000 0.2%

Philadelphia 266,971 0.3%

South Florida 536,520 0.6%

Southern California 256,843 0.3%

United Kingdom 206,865 0.2%

Total Development Properties 27 6,568,802 7.0%

Redevelopment:

Atlanta 247,000 0.3%

Maryland 125,469 0.1%

Southeastern PA 380,974 0.4%

Washington D.C. 290,762 0.3%

Total Redevelopment Properties 10 1,044,205 1.1%

Total Wholly Owned Properties 534 93,413,204 100.0%

Page 11

PORTFOLIO PROFILE - TOTAL COMPANY

SECOND QUARTER 2017 SUPPLEMENTAL

Markets

Numberof

PropertiesPercentOwned Square Feet

Percentof SF Occupancy Net Rent

Net Rentper

OccupiedSF

Percent ofNet Rent

JOINT VENTURES AT 100%

Operating:

Chicago/Milwaukee 25% 4,857,179 32.6% 93.9% $ 16,271,539 $ 3.57 14.3%

New Jersey 25% 4,502,278 30.3% 99.2% 22,396,902 5.01 19.7%

Orlando 50% 1,505,353 10.1% 88.5% 7,452,921 5.59 6.5%

Philadelphia 20% 1,253,876 8.5% 99.6% 42,490,898 34.01 37.3%

United Kingdom 20% 488,786 3.3% 78.2% 8,894,621 23.28 7.8%

Washington D.C. 25% 451,284 3.1% 93.7% 16,465,244 38.93 14.4%

Total Operating Properties 63 13,058,756 87.9% 95.1% $ 113,972,125 $ 9.18 100.0%

Development:

New Jersey 25% 302,400 2.0%

Orlando 50% 154,400 1.1%

Philadelphia 20% 1,332,415 9.0%

Total Development Properties 3 1,789,215 12.1%

Total Joint Venture Properties 66 14,847,971 100.0%

SUMMARY

Operating properties 560 98,858,953 91.3% 95.6% $ 580,579,198 $ 6.14

Development properties 30 8,358,017 7.7%

Redevelopment 10 1,044,205 1.0%

Total Company 600 108,261,175 100.0%

Joint ventures at 100%

Page 12

PORTFOLIO PROFILE - INDUSTRIAL PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

MarketsNumber ofProperties Square Feet

Percent ofSF Occupancy Net Rent

Net Rent perOccupied SF

Percent ofNet Rent

WHOLLY OWNED

Operating:

Arizona 1,821,010 2.1% 90.9% $ 6,550,264 $ 3.96 1.7%

Atlanta 2,090,709 2.4% 93.2% 7,468,941 3.83 1.9%

Carolinas 8,163,114 9.3% 98.1% 36,387,430 4.54 9.2%

Chicago/Milwaukee 7,222,412 8.2% 93.7% 29,164,814 4.31 7.4%

Cincinnati/Columbus/Indianapolis 3,948,376 4.5% 99.6% 13,146,497 3.34 3.3%

Dallas 2,202,641 2.5% 100.0% 9,971,290 4.53 2.5%

Houston 7,232,311 8.2% 90.9% 38,622,931 5.87 9.8%

Lehigh Valley/Central PA 25,920,067 29.5% 98.0% 127,356,986 5.01 32.3%

Maryland 3,708,262 4.2% 95.2% 18,288,792 5.18 4.6%

Minnesota 2,639,807 3.0% 84.1% 10,654,560 4.80 2.7%

New Jersey 825,985 0.9% 100.0% 3,356,800 4.06 0.9%

Orlando 2,200,181 2.5% 94.5% 13,580,945 6.54 3.4%

Philadelphia 625,571 0.7% 100.0% 8,666,259 13.85 2.2%

Richmond/Hampton Roads 4,519,206 5.2% 95.6% 19,551,867 4.52 5.0%

South Florida 2,437,157 2.8% 98.3% 17,029,707 7.11 4.3%

Southeastern PA 552,797 0.6% 94.9% 6,476,024 12.34 1.6%

Southern California 2,089,212 2.4% 92.3% 9,463,290 4.91 2.4%

Tampa 1,805,494 2.1% 99.5% 9,103,833 5.07 2.3%

United Kingdom 1,380,878 1.6% 100.0% 9,719,349 7.04 2.5%

Total Industrial Operating Properties 447 81,385,190 92.7% 96.0% $ 394,560,579 $ 5.05 100.0%

Development:

Arizona 658,716 0.8%

Atlanta 235,234 0.3%

Carolinas 574,220 0.6%

Chicago/Milwaukee 95,962 0.1%

Dallas 562,468 0.6%

Houston 415,272 0.5%

Lehigh Valley/Central PA 1,905,600 2.2%

Maryland 436,000 0.5%

New Jersey 182,000 0.2%

South Florida 536,520 0.6%

Southern California 256,843 0.3%

United Kingdom 206,865 0.2%

Total Industrial DevelopmentProperties 24 6,065,700 6.9%

Redevelopment:

Atlanta 247,000 0.3%

Maryland 125,469 0.1%

Total Industrial RedevelopmentProperties 2 372,469 0.4%

Total Wholly Owned IndustrialProperties 473 87,823,359 100%

Page 13

PORTFOLIO PROFILE - INDUSTRIAL PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

MarketsNumber ofProperties

PercentOwned

SquareFeet

Percent ofSF Occupancy Net Rent

Net Rentper

OccupiedSF

Percent ofNet Rent

JOINT VENTURES AT 100%

Operating:

Chicago/Milwaukee 25% 4,857,179 42.9% 93.9% $ 16,271,539 $ 3.57 35.3%

New Jersey 25% 4,502,278 39.8% 99.2% 22,396,902 5.01 48.6%

Orlando 50% 1,505,353 13.3% 88.5% 7,452,921 5.59 16.1%

Total Industrial OperatingProperties 46 10,864,810 96.0% 95.4% $ 46,121,362 $ 4.45 100.0%

Development:

New Jersey 25% 302,400 2.7%

Orlando 50% 154,400 1.3%

Total Industrial DevelopmentProperties 2 456,800 4.0%

Total Joint Venture IndustrialProperties 48 11,321,610 100.0%

SUMMARY

Operating properties 493 92,250,000 93.0% 95.9% $440,681,941 $ 4.98

Development properties 26 6,522,500 6.6%

Redevelopment properties 2 372,469 0.4%

Total Industrial Properties 521 99,144,969 100.0%

Joint ventures at 100%

Page 14

PORTFOLIO PROFILE - OFFICE PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

MarketsNumber ofProperties

PercentOwned Square Feet

Percent ofSF Occupancy Net Rent

Net Rentper

Occupied SFPercent ofNet Rent

WHOLLY OWNED

Operating:

Arizona 569,615 10.2% 100.0% $ 9,069,313 $ 15.92 12.6%

Houston 206,808 3.7% 21.6% 928,455 20.82 1.3%

Minnesota 345,000 6.2% 100.0% 1,462,500 4.24 2.0%

Orlando 150,751 2.7% 94.6% 1,684,177 11.81 2.4%

Philadelphia 792,282 14.2% 96.8% 22,317,666 29.10 31.0%

Southeastern PA 2,066,096 36.9% 92.5% 31,140,897 16.29 43.2%

United Kingdom 137,983 2.5% 85.1% 2,760,561 23.50 3.8%

Washington D.C. 146,472 2.6% 66.6% 2,682,925 27.50 3.7%

Total Office Operating Properties 50 4,415,007 79.0% 90.5% $ 72,046,494 $ 18.03 100.0%

Development:

Arizona 236,131 4.2%

Philadelphia 266,971 4.8%

Total Office Developmentproperties 3 503,102 9.0%

Redevelopment:

Southeastern PA 380,974 6.8%

Washington D.C. 290,762 5.2%

Total Office RedevelopmentProperties 8 671,736 12.0%

Total Office Wholly OwnedProperties 61 5,589,845 100.0%

JOINT VENTURES AT 100%

Operating:

Philadelphia 20% 1,253,876 35.5% 99.6% $ 42,490,898 $ 34.01 62.6%

United Kingdom 20% 488,786 13.9% 78.2% 8,894,621 23.28 13.1%

Washington D.C. 25% 451,284 12.8% 93.7% 16,465,244 38.93 24.3%

Total Office Operating Properties 17 2,193,946 62.2% 93.6% $ 67,850,763 $ 33.03 100.0%

Philadelphia 20% 1,332,415 37.8%

Total Office DevelopmentProperties 1 1,332,415 37.8%

Total Joint Venture OfficeProperties 18 3,526,361 100.0%

SUMMARY

Operating properties 67 6,608,953 72.5% 91.5% $ 139,897,257 $ 23.12

Development properties 4 1,835,517 20.1%

Redevelopment properties 8 671,736 7.4%

Total Office Properties 79 9,116,206 100.0%

Joint Ventures at 100%

Page 15

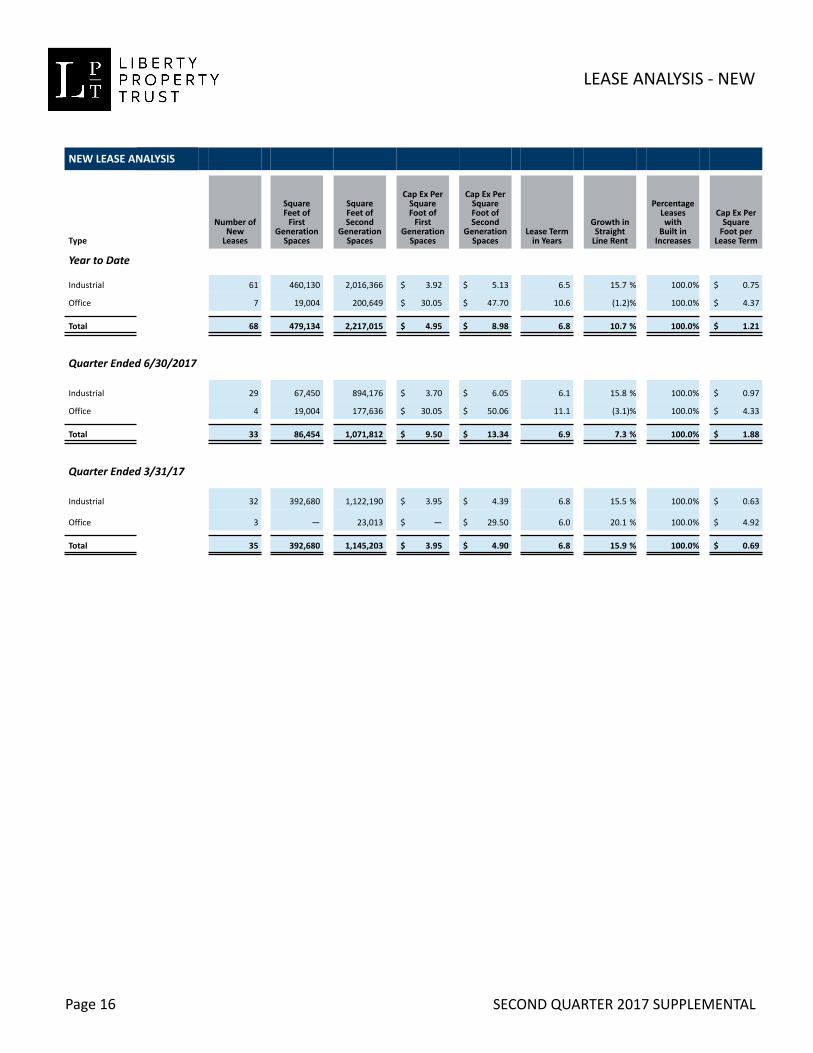

LEASE ANALYSIS - NEW

SECOND QUARTER 2017 SUPPLEMENTAL

NEW LEASE ANALYSIS

Type

Number ofNew

Leases

SquareFeet of

FirstGeneration

Spaces

SquareFeet ofSecond

GenerationSpaces

Cap Ex PerSquareFoot of

FirstGeneration

Spaces

Cap Ex PerSquareFoot ofSecond

GenerationSpaces

Lease Termin Years

Growth inStraight

Line Rent

PercentageLeaseswith

Built inIncreases

Cap Ex PerSquare

Foot perLease Term

Year to Date

Industrial 61 460,130 2,016,366 $ 3.92 $ 5.13 6.5 15.7 % 100.0% $ 0.75

Office 7 19,004 200,649 $ 30.05 $ 47.70 10.6 (1.2)% 100.0% $ 4.37

Total 68 479,134 2,217,015 $ 4.95 $ 8.98 6.8 10.7 % 100.0% $ 1.21

Quarter Ended 6/30/2017

Industrial 29 67,450 894,176 $ 3.70 $ 6.05 6.1 15.8 % 100.0% $ 0.97

Office 4 19,004 177,636 $ 30.05 $ 50.06 11.1 (3.1)% 100.0% $ 4.33

Total 33 86,454 1,071,812 $ 9.50 $ 13.34 6.9 7.3 % 100.0% $ 1.88

Quarter Ended 3/31/17

Industrial 32 392,680 1,122,190 $ 3.95 $ 4.39 6.8 15.5 % 100.0% $ 0.63

Office 3 — 23,013 $ — $ 29.50 6.0 20.1 % 100.0% $ 4.92

Total 35 392,680 1,145,203 $ 3.95 $ 4.90 6.8 15.9 % 100.0% $ 0.69

Page 16

LEASE ANALYSIS - RENEWAL

SECOND QUARTER 2017 SUPPLEMENTAL

RENEWAL ANALYSIS

Expiring Leases Leases RenewedPercentage

SquareFeet

Renewed

Cap Ex perSquare

FootLease Term

in Years

Growth inStraight

Line Rent

PercentageLeases

with Builtin

Increases

Cap Ex PerSquare

Foot perLease TermType Number

SquareFeet Number

SquareFeet

Year to Date

Industrial 160 9,283,511 94 5,515,607 59.4% $ 1.53 4.6 14.5% 96.9% $ 0.33

Office 27 598,956 15 249,773 41.7% $ 11.84 10.2 11.2% 95.2% $ 1.16

Total 187 9,882,467 109 5,765,380 58.3% $ 1.98 4.9 14.1% 96.6% $ 0.41

Quarter Ended 6/30/2017

Industrial 69 4,765,087 37 2,668,338 56.0% $ 1.52 4.9 10.5% 94.3% $ 0.31

Office 19 310,516 13 229,951 74.1% $ 12.38 10.7 11.8% 94.9% $ 1.16

Total 88 5,075,603 50 2,898,289 57.1% $ 2.38 5.4 10.8% 94.5% $ 0.44

Quarter Ended 3/31/2017

Industrial 91 4,518,424 57 2,847,269 63.0% $ 1.54 4.3 18.5% 99.3% $ 0.36

Office 8 288,440 2 19,822 6.9% $ 5.57 3.9 4.7% 100.0% $ 1.45

Total 99 4,806,864 59 2,867,091 59.6% $ 1.57 4.3 18.0% 99.3% $ 0.36

Page 17

LEASE ANALYSIS - COMBINED

SECOND QUARTER 2017 SUPPLEMENTAL

SECOND GENERATION AND RENEWAL ANALYSIS

TypeTotal Square

FeetCap Ex per

Square Foot

Growth inStraight Line

Rent

PercentageLeases with

Built inIncreases

Year to Date

Industrial 7,531,973 $ 2.49 14.9% 97.8%

Office 450,422 $ 27.81 6.1% 97.1%

Total 7,982,395 $ 3.92 13.1% 97.6%

Quarter ended 6/30/2017

Industrial 3,562,514 $ 2.65 11.9% 95.9%

Office 407,587 $ 28.8 5.7% 96.8%

Total 3,970,101 $ 5.34 9.6% 96.2%

Quarter ended 3/31/2017

Industrial 3,969,459 $ 2.35 17.8% 99.5%

Office 42,835 $ 18.43 11.6% 100.0%

Total 4,012,294 $ 2.52 17.5% 99.5%

Page 18

LEASE EXPIRATIONS

SECOND QUARTER 2017 SUPPLEMENTAL

(by type)

Square Feet Net Rent per Square Foot (at end of lease term)

Year of Expiration Total Industrial Office Total Industrial Office

WHOLLY OWNED - TOTAL

2017 (remaining) 3,170,403 3,096,621 73,782 $ 4.90 $ 4.80 $ 9.31

2018 10,217,887 9,942,857 275,030 5.23 4.82 20.04

2019 12,986,358 12,757,063 229,295 5.54 5.24 22.44

2020 13,389,014 13,060,485 328,529 5.94 5.50 23.06

2021 7,883,345 7,709,454 173,891 6.00 5.69 19.59

Thereafter 34,474,532 31,559,677 2,914,855 7.86 6.37 23.92

Total LeasedSquare Feet 82,121,539 78,126,157 3,995,382 $ 6.56 $ 5.72 $ 23.04

Total Square Feet 85,800,197 81,385,190 4,415,007

JOINT VENTURES - TOTAL

2017 (remaining) 626,466 529,289 97,177 $ 8.33 $ 5.07 $ 26.08

2018 2,134,273 1,792,002 342,271 9.30 4.33 35.32

2019 856,642 783,062 73,580 7.38 5.35 28.94

2020 2,226,448 2,176,621 49,827 4.66 4.15 26.84

2021 600,009 500,146 99,863 10.58 5.45 36.28

Thereafter 5,971,230 4,579,715 1,391,515 13.27 5.44 39.01

Total LeasedSquare Feet 12,415,068 10,360,835 2,054,233 $ 10.26 $ 4.95 $ 36.99

Total Square Feet 13,058,756 10,864,810 2,193,946

PORTFOLIO - TOTAL

2017 (remaining) 3,796,869 3,625,910 170,959 $ 5.47 $ 4.84 $ 18.84

2018 12,352,160 11,734,859 617,301 5.93 4.74 28.51

2019 13,843,000 13,540,125 302,875 5.66 5.25 24.02

2020 15,615,462 15,237,106 378,356 5.75 5.31 23.56

2021 8,483,354 8,209,600 273,754 6.32 5.68 25.68

Thereafter 40,445,762 36,139,392 4,306,370 8.66 6.26 28.80

Total LeasedSquare Feet 94,536,607 88,486,992 6,049,615 $ 7.04 $ 5.63 $ 27.78

Total Square Feet 98,858,953 92,250,000 6,608,953

Page 19

LEASE EXPIRATIONS

SECOND QUARTER 2017 SUPPLEMENTAL

(by city)

SQUARE FEET

Markets2017

(remaining) 2018 2019 2020 2021 Thereafter

WHOLLY OWNED

Arizona 55,574 83,029 189,608 73,781 180,420 1,642,325

Atlanta 19,999 352,752 262,501 347,727 295,570 669,751

Carolinas 444,885 1,287,169 1,073,305 1,262,203 1,156,703 2,784,469

Chicago/Milwaukee 175,725 914,010 386,733 2,149,848 88,613 3,052,085

Cincinnati/Columbus/Indianapolis 85,800 1,844,982 1,003,600 135,456 387,929 473,433

Dallas 268,071 184,251 329,992 227,825 483,416 709,086

Houston 401,110 735,195 1,649,330 639,875 583,167 2,610,922

Lehigh Valley/Central PA 691,966 531,678 4,865,083 5,385,271 2,332,095 11,603,474

Maryland 250,581 492,328 308,545 197,843 59,842 2,222,308

Minnesota 44,780 127,412 340,892 532,635 180,472 1,337,898

New Jersey — 204,369 — 209,106 — 412,510

Orlando 177,812 272,961 421,123 96,046 306,662 946,094

Philadelphia — 5,082 28,276 22,170 3,769 1,333,198

Richmond/Hampton Roads 158,223 1,281,854 948,266 637,329 400,397 895,394

South Florida 265,526 206,922 346,850 359,303 403,131 812,989

Southeastern PA 62,742 201,590 316,274 440,440 207,995 1,207,441

Southern California — 44,507 373,771 172,500 230,981 1,107,447

Tampa 58,965 575,619 96,597 460,973 168,131 436,978

United Kingdom 6,897 855,397 12,024 6,537 409,716 207,757

Washington D.C. 1,747 16,780 33,588 32,146 4,336 8,973

Total Leased Square Feet 3,170,403 10,217,887 12,986,358 13,389,014 7,883,345 34,474,532

JOINT VENTURES

Chicago/Milwaukee 223,005 973,760 54,375 2,083,897 251,151 975,752

New Jersey 219,502 706,819 228,687 92,724 215,623 3,003,063

Orlando 86,782 111,423 500,000 — 33,372 600,900

Philadelphia 14,449 29,702 16,414 — 1,123 1,187,504

United Kingdom 79,157 58,429 51,850 49,827 42,329 100,473

Washington D.C. 3,571 254,140 5,316 — 56,411 103,538

Total Leased Square Feet 626,466 2,134,273 856,642 2,226,448 600,009 5,971,230

Page 20

TOP TEN LARGEST TENANTS

SECOND QUARTER 2017 SUPPLEMENTAL

(by type)

Square Feet(1) Percent of Net Rent(2)

INDUSTRIAL TENANTS

Uline, Inc. 1,683,876 2.5%

Amazon.com 2,710,370 2.2%

Home Depot U.S.A., Inc. 1,318,590 1.7%

The Procter & Gamble Distributing LLC 1,692,159 1.5%

Kellogg Sales Company 1,561,460 1.3%

XPO Last Mile, Inc. 1,825,525 1.3%

Wakefern Food Corp. 1,029,600 1.2%

Geodis Logistics LLC 1,317,906 1.2%

Ryder Integrated Logistics, Inc. 1,200,000 1.1%

The Clorox Company 1,081,720 0.9%

15,421,206 14.9%

OFFICE TENANTS

The Vanguard Group, Inc. 1,094,970 4.2%

Comcast Corporation 1,203,610 1.7%

GlaxoSmithKline LLC 207,779 1.6%

United States of America 757,172 1.2%

The Pennsylvania Hospital 153,242 0.9%

Yellow Book USA, Inc. 154,820 0.7%

Deutsche Post DHL Group 312,813 0.6%

Franklin Square Holdings, LP 80,050 0.5%

Centene Management Company, LLC 116,857 0.4%

Iroko Intermediate Holdings, Inc. 67,816 0.3%

4,149,129 12.1%

TOTAL 19,570,335 27.0%

(1) Joint Ventures included at 100%

(2) Joint Ventures included at equity share.

Page 21

SAME STORE PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

TOTAL COMPANYQuarter Ended Year to Date

6/30/2017 6/30/2016 % Change 6/30/2017 6/30/2016 % Change

Number of Properties 472 472 472 472

Square Feet 79,075,380 79,075,380 79,075,380 79,075,380

Average Occupancy 95.6% 95.9% 96.0% 95.8%

Rental Revenue $ 109,768 $ 109,091 0.6 % $ 218,907 $ 217,557 0.6 %

Operating Expenses: Rental Property Expense 16,642 16,511 34,838 35,795

Real Estate Taxes 19,221 18,296 38,100 36,528

Operating Expense Recovery (35,914) (34,072) (72,235) (70,503)

Unrecovered Operating Expenses (51) 735 703 1,820

NOI - Straight Line Basis 109,819 108,356 1.4 % 218,204 215,737 1.1 %

Less Straight Line Rent 3,472 2,761 6,679 6,424

NOI - Cash Basis $ 106,347 $ 105,595 0.7 % $ 211,525 $ 209,313 1.1 %

INDUSTRIALQuarter Ended Year to Date

6/30/2017 6/30/2016 % Change 6/30/2017 6/30/2016 % Change

Number of Properties 428 428 428 428

Square Feet 75,286,857 75,286,857 75,286,857 75,286,857

Average Occupancy 95.9% 96.1% 96.3% 96.1%

Rental Revenue $ 92,668 $ 90,898 1.9 % $ 184,896 $ 181,518 1.9 %

Operating Expenses: Rental Property Expense 11,579 11,682 24,444 25,300

Real Estate Taxes 16,976 16,163 33,638 32,247

Operating Expense Recovery (28,825) (27,433) (57,817) (56,356)

Unrecovered Operating Expenses (270) 412 265 1,191

NOI - Straight Line Basis 92,938 90,486 2.7 % 184,631 180,327 2.4 %

Less Straight Line Rent 2,605 2,033 5,193 4,850

NOI - Cash Basis $ 90,333 $ 88,453 2.1 % $ 179,438 $ 175,477 2.3 %

OFFICEQuarter Ended Year to Date

6/30/2017 6/30/2016 % Change 6/30/2017 6/30/2016 % Change

Number of Properties 44 44 44 44

Square Feet 3,788,523 3,788,523 3,788,523 3,788,523

Average Occupancy 89.7% 92.1% 89.3% 89.2%

Rental Revenue $ 17,100 $ 18,193 (6.0)% $ 34,011 $ 36,039 (5.6)%

Operating Expenses: Rental Property Expense 5,063 4,829 10,394 10,495

Real Estate Taxes 2,245 2,133 4,462 4,281

Operating Expense Recovery (7,089) (6,639) (14,418) (14,147)

Unrecovered Operating Expenses 219 323 438 629

NOI - Straight Line Basis 16,881 17,870 (5.5)% 33,573 35,410 (5.2)%

Less Straight Line Rent 867 728 1,486 1,574

NOI - Cash Basis $ 16,014 $ 17,142 (6.6)% $ 32,087 $ 33,836 (5.2)%

Page 22

FULLY STABILIZED PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

TOTAL COMPANYQuarter Ended Year to Date

6/30/2017 6/30/2016 % Change 6/30/2017 6/30/2016 % Change

Number of Properties 484 484 480 480

Square Feet 81,045,419 81,045,419 80,523,129 80,523,129

Average Occupancy 95.3% 95.0% 95.8% 94.8%

Rental Revenue $ 113,210 $ 111,255 1.8 % $ 223,615 $ 220,642 1.3 %

Operating Expenses: Rental Property Expense 16,969 16,633 35,399 35,857

Real Estate Taxes 20,010 19,014 39,462 37,716

Operating Expense Recovery (36,986) (34,475) (73,837) (71,104)

Unrecovered Operating Expenses (7) 1,172 1,024 2,469

NOI - Straight Line Basis 113,217 110,083 2.8 % 222,591 218,173 1.1 %

Less Straight Line Rent 3,804 3,423 7,102 7,465

NOI - Cash Basis $ 109,413 $ 106,660 2.6 % $ 215,489 $ 210,708 2.3 %

INDUSTRIALQuarter Ended Year to Date

6/30/2017 6/30/2016 % Change 6/30/2017 6/30/2016 % Change

Number of Properties 437 437 434 434

Square Feet 76,815,229 76,815,229 76,363,717 76,363,717

Average Occupancy 95.7% 95.2% 96.3% 95.3%

Rental Revenue $ 94,797 $ 91,843 3.2 % $ 187,721 $ 182,860 2.7 %

Operating Expenses: Rental Property Expense 11,577 11,539 24,551 25,040

Real Estate Taxes 17,457 16,607 34,390 32,929

Operating Expense Recovery (29,529) (27,629) (58,871) (56,651)

Unrecovered Operating Expenses (495) 517 70 1,318

NOI - Straight Line Basis 95,292 91,326 4.3 % 187,651 181,542 2.4 %

Less Straight Line Rent 2,789 2,328 5,507 5,243

NOI - Cash Basis $ 92,503 $ 88,998 3.9 % $ 182,144 $ 176,299 3.3 %

OFFICEQuarter Ended Year to Date

6/30/2017 6/30/2016 % Change 6/30/2017 6/30/2016 % Change

Number of Properties 47 47 46 46

Square Feet 4,230,190 4,230,190 4,159,412 4,159,412

Average Occupancy 87.7% 91.2% 86.0% 85.7%

Rental Revenue $ 18,413 $ 19,412 (5.1)% $ 35,894 $ 37,782 (5.0)%

Operating Expenses: Rental Property Expense 5,392 5,094 10,848 10,817

Real Estate Taxes 2,553 2,407 5,072 4,787

Operating Expense Recovery (7,457) (6,846) (14,966) (14,453)

Unrecovered Operating Expenses 488 655 954 1,151

NOI - Straight Line Basis 17,925 18,757 (4.4)% 34,940 36,631 (5.2)%

Less Straight Line Rent 1,015 1,095 1,595 2,222

NOI - Cash Basis $ 16,910 $ 17,662 (4.3)% $ 33,345 $ 34,409 (3.1)%

Page 23

COMPLETED DEVELOPMENT PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

WHOLLY OWNED DEVELOPMENT COMPLETIONS

Investment Square Feet Occupancy 6/30/2017 Stabilized Yield

First Quarter 2017 $ 16,307 215,000 81.7% 10.3%

Second Quarter 2017 65,198 723,505 100.0% 7.9%

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 $ 81,505 938,505 95.8% 8.4%

JOINT VENTURE DEVELOPMENT COMPLETIONS

Investment Square Feet Occupancy 6/30/2017 Stabilized Yield

First Quarter 2017 $ — — —% —%

Second Quarter 2017 — — —% —%

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 $ — — —% —%

COMPLETED DEVELOPMENT IN SECOND QUARTER 2017

Address

Inv.or

BTSBldgType Invest.

SquareFeet Occupancy

%Own

ShellCompDate

Operatingas of:

CurrentYield

StabilizedYield

Wholly Owned:

951 Valleyview Lane Irving, TX Inv. I $ 18,685 341,442 100.0% 100% Aug-16 May-17

1930 W Rio SaladoParkway

Tempe, AZ Inv. O 29,831 135,663 100.0% 100% Oct-16 May-17

3525 Gravel SpringsRoad

Buford, GA Inv. I 7,492 120,400 100.0% 100% Sep-16 Jun-17

1953 TW AlexanderDrive

Durham, NC Inv. I 9,190 126,000 100.0% 100% Jan-17 Jun-17

Total Wholly Owned $ 65,198 723,505 100.0% 7.9% 7.9%

Page 24

DEVELOPMENT STARTS

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

WHOLLY OWNED DEVELOPMENT STARTS

Projected Investment Square Feet

First Quarter 2017 $ 84,239 777,313

Second Quarter 2017 73,579 1,025,600

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 157,818 1,802,913

JOINT VENTURE DEVELOPMENT STARTS

Projected Investment Square Feet

First Quarter 2017 $ 11,918 154,400

Second Quarter 2017 — —

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 $ 11,918 154,400

DEVELOPMENT STARTS IN SECOND QUARTER 2017

Address Location

Invor

BTSBldgType

ProjectedInvestment

PercentComplete

SquareFeet

PercentPre-Leased

%Own

AnticipatedIn Service

Date

WHOLLY OWNED:

7157 Ridge Road Hanover, MD BTS I $ 23,721 24.9% 220,000 100.0% 100% 2Q2018

100 Carolina Way Carlisle, PA Inv I 49,858 27.3% 805,600 - 100% 2Q2019

Total Wholly Owned $ 73,579 26.5% 1,025,600 21.5%

JOINT VENTURE:

Total Joint Venture $ — —

Total Development Starts $ 73,579 26.5% 1,025,600 21.5%

Page 25

DEVELOPMENT PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

Address LocationInv orBTS

BldgType

ProjectedInvestment

PercentComplete

SquareFeet

PercentPre-

Leased

AnticipatedIn Service

DateProjectedSL Yield

WHOLLY OWNED: (1)

11440 NW 122 Street Medley, FL Inv I $ 17,309 95.7% 159,180 100.0% 3Q2017

4485 Premier Drive High Point, NC Inv I 8,656 93.8% 140,000 57.1% 3Q2017

5430 FAA Boulevard Irving, TX Inv I 14,404 82.1% 196,560 - 3Q2017

1200 Intrepid Avenue Philadelphia, PA Inv O 35,114 83.9% 91,971 60.5% 3Q2017

2988 Green Road Greer, SC Inv I 9,817 87.8% 171,600 100.0% 3Q2017

3535 Gravel Springs Road Buford, GA Inv I 13,970 85.1% 235,234 43.7% 3Q2017

1801 South 16th Street LaPorte, TX Inv I 31,540 77.6% 415,272 100.0% 4Q2017

1951 TW Alexander Drive Durham, NC Inv I 4,924 91.9% 58,500 100.0% 4Q2017

6017 Southern Boulevard West Palm Beach, FL Inv I 14,677 87.8% 140,400 69.2% 4Q2017

6035 Southern Boulevard West Palm Beach, FL Inv I 8,767 86.8% 77,760 33.3% 4Q2017

7205 W Buckeye Road Phoenix, AZ Inv I 14,342 88.0% 222,910 39.2% 4Q2017

1720 West 135th Street Gardena, CA Inv I 20,531 96.9% 100,580 100.0% 4Q2017

1870 W Rio SaladoParkway

Tempe, AZ BTS O 51,278 52.9% 236,131 100.0% 1Q2018

7157 Ridge Road Hanover, MD BTS I 23,721 24.9% 220,000 100.0% 2Q2018

1050 Constitution Avenue Philadelphia, PA BTS O 45,527 76.2% 175,000 100.0% 2Q2018

1075 King George PostRoad

Edison, NJ Inv I 17,130 79.7% 182,000 100.0% 2Q2018

1200 Claybrick Road Landover, MD Inv I 22,447 90.5% 216,000 60.0% 2Q2018

2250 East Bardin Road Arlington, TX BTS I 38,279 30.6% 365,908 100.0% 2Q2018

1500 S 71st Avenue Phoenix, AZ Inv I 27,091 81.8% 435,806 60.1% 3Q2018

Worcester 1 - Plot 4 Worcester, UK Inv I 4,889 81.8% 44,835 - 3Q2018

Worcester 2 - Plot 3 Worcester, UK Inv I 14,770 75.8% 162,030 - 3Q2018

3929 Shutterfly Road Charlotte, NC Inv I 13,579 72.2% 204,120 - 3Q2018

8801 Congdon Hill Drive Mertztown, PA Inv I 85,379 70.8% 1,100,000 - 4Q2018

11430 NW 122 Street Medley, FL Inv I 18,418 52.9% 159,180 - 4Q2018

9724 Alabama Street San Bernardino, CA Inv I 15,525 44.2% 156,263 - 4Q2018

350 North York Road Bensenville, IL Inv I 12,017 32.7% 95,962 - 1Q2019

100 Carolina Way Carlisle, PA Inv I 49,858 27.3% 805,600 - 2Q2019

Total Wholly Owned (1) $ 633,959 66.8% 6,568,802 44.5% 7.8%

Page 26

DEVELOPMENT PROPERTIES

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

Address Location

Invor

BTSBldgType

ProjectedInvestment

PercentComplete

SquareFeet

PercentPre-

Leased%

Own

AnticipatedIn Service

DateProjectedSL Yield

JOINT VENTURE:

1800 Arch Street (1) Philadelphia, PA BTS O $ 934,307 89.3% 1,332,415 99.5% 20% 3Q2017

2904 Tradeport Drive Orlando, FL BTS I 11,918 40.4% 154,400 100.0% 50% 4Q2017

200 Arlington Boulevard Swedesboro, NJ Inv I 20,516 76.5% 302,400 - 25% 4Q2018

Total Joint Venture $ 966,741 88.4% 1,789,215 82.7% 8.1%

Total Development Properties (2) $ 1,600,700 79.9% 8,358,017 52.7% 8.0%

(2) Includes a 217-room Four Seasons Hotel.

Page 27

(1) Amounts above exclude $43.4M investment, 88,415 SF for the active redevelopment of a portion of2100 M Street NW, Washington DC Property

ACQUISITIONS

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

WHOLLY OWNED ACQUISITIONS

Investment Square Feet Occupancy 6/30/2017Projected Stabilized

Yield

First Quarter 2017 $ — — —% —%

Second Quarter 2017 20,069 100,580 —% 5.2%

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 $ 20,069 100,580 —% 5.2%

JOINT VENTURE ACQUISITIONS

Investment Square Feet Occupancy 6/30/2017Projected Stabilized

Yield

First Quarter 2017 $ — — —% —%

Second Quarter 2017 — — —% —%

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 $ — — —% —%

SECOND QUARTER 2017

Address City/State Bldg TypePercentOwned Square Feet Occupancy Investment

Wholly Owned:

1720 W 135th Street Gardena, CA I 100% 100,580 —% $ 20,069 (1)

Total Wholly Owned: 100,580 —% $ 20,069

(1) This property was under development when acquired. See Development Properties schedule on page 26.

Page 28

DISPOSITIONS

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

WHOLLY OWNED DISPOSITIONS

Sale Proceeds Square FeetOccupancy

(at sale date)

First Quarter 2017 $ 2,075 33,027 4.1%

Second Quarter 2017 8,068 93,502 29.4%

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 $ 10,143 126,529 22.8%

JOINT VENTURE DISPOSITIONS

Sale Proceeds Square FeetOccupancy

(at sale date)

First Quarter 2017 — — —

Second Quarter 2017 — — —

Third Quarter 2017

Fourth Quarter 2017

Year to Date 2017 — — —

SECOND QUARTER 2017

Address Date Sold City/State Bldg TypePercentOwned

SquareFeet Occupancy

SalesProceeds

Wholly Owned:

7777 Golden Triangle Drive 5/31/2017 Eden Prairie, MN O 100% 31,116 — $ 3,100

10, 20 Liberty Boulevard 6/15/2017 Malvern, PA O 100% 62,386 44.4% 4,968

Total Wholly Owned: 93,502 29.4% $ 8,068

Page 29

UNCONSOLIDATED JOINT VENTURES

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

LibertyVenture I,

LPKings HillUnit Trust

LibertyIllinois, LP

LibertyAIPO LP

LibertyWashington,

LP

Liberty/Comcast1701 JFKBlvd, LP

LibertyProperty18th andArch (D) Other Total

BALANCE SHEET (A) as of June 30, 2017

Real estate assets $ 227,581 $ 145,069 $ 251,306 $ 71,710 $ 289,454 $ 495,866 $ — $ — $ 1,480,986

Accumulated depreciation (45,908) (28,834) (54,459) (10,557) (46,608) (131,977) — — (318,343)

Real estate assets, net 181,673 116,235 196,847 61,153 242,846 363,889 — — 1,162,643

Development in progress 15,630 — — 4,205 — — 785,918 — 805,753

Land held for development — — 32,376 10,708 — — — 30,165 73,249

Other assets 20,865 10,864 18,346 9,276 17,606 46,318 44,374 16,430 184,079

Total assets $ 218,168 $ 127,099 $ 247,569 $ 85,342 $ 260,452 $ 410,207 $ 830,292 $ 46,595 $ 2,225,724

Debt $ 160,018 $ 88,645 $ 137,203 $ 58,194 $ 103,151 $ 307,358 $ — $ — $ 854,569

Other liabilities 7,290 25,684 7,407 3,686 3,817 8,514 91,692 6,915 155,005

Equity 50,860 12,770 102,959 23,462 153,484 94,335 738,600 39,680 1,216,150

Total liabilities and equity $ 218,168 $ 127,099 $ 247,569 $ 85,342 $ 260,452 $ 410,207 $ 830,292 $ 46,595 $ 2,225,724

LPT's ownership percentage 25% 20% 25% 50% 25% 20% 20% 20-50%

LPT's share of equity $ 10,661 $ 5,546 $ 15,032 $ 12,108 $ 38,253 $ 17,686 $ 158,158 $ 10,902 $ 268,346

RESULTS OF OPERATIONS (A) Year to Date June 30, 2017

Total revenue $ 15,228 $ 5,936 $ 11,862 $ 4,560 $ 12,658 $ 32,356 $ — $ 490 $ 83,090

Operating expenses 3,732 2,276 3,781 1,173 4,524 12,982 222 137 28,827

NET OPERATING INCOME 11,496 3,660 8,081 3,387 8,134 19,374 (222) 353 54,263

Interest 2,906 1,145 3,056 1,399 1,993 9,662 — — 20,161

Depreciation and amortization 3,770 1,550 3,466 1,037 2,986 7,243 — — 20,052

Other (income)/expense 82 (85) 44 4 30 166 (148) (12,027) (11,934)

NET INCOME $ 4,738 $ 1,050 $ 1,515 $ 947 $ 3,125 $ 2,303 $ (74) $ 12,380 $ 25,984

LPT's share of net income $ 1,407 $ 274 $ 583 $ 458 $ 1,024 $ 819 $ (15) $ 5,171 $ 9,721

LPT's share of depr and amort 929 278 724 519 747 1,423 — — 4,620

LPT's share of NAREIT FFO $ 2,336 $ 552 $ 1,307 $ 977 $ 1,771 $ 2,242 $ (15) $ 5,171 $ 14,341

LPT's share of NOI $ 2,874 $ 732 $ 2,020 $ 1,694 $ 2,034 $ 3,875 $ (44) $ 74 $ 13,259

DEBT as of June 30, 2017

Interest rate 3.20% -3.95%

2.00% 2.66% -6.05%

4.02% -4.95%

3.40% -3.89%

6.00% — —

LPT's share of debt (B) $ 40,005 $ 17,729 $ 34,301 $ 29,097 $ 25,788 $ 61,472 $ — $ — $ 208,392

Debt maturity date (C) 7/18 - 11/25 11/20 10/17 -12/17 6/19 - 1/27 4/19 - 7/24 4/18 — —

JV DEBT MATURITIES(INCLUDING AMORITIZATION)(A) Reported at 100% of joint venture.

(B) All joint venture debt is non-recourse. (In 000's)(C) The maturity dates and corresponding future maturities are shown at the debt's first call date. Total LPT Share(D) Represents the combined results of two joint ventures related to the property at 2017 $ 140,810 $ 35,244 18th and Arch, Philadelphia. 2018 317,531 64,441(E) Includes deferred financing costs and market adjustments. 2019 51,379 13,195

2020 92,377 18,9722021 2,941 1,108

Thereafter 253,673 76,573$ 858,711 $ 209,533

Reconciling Items (E) (4,142) (1,141)

$ 854,569 $ 208,392

Page 30

DEBT & PREFERRED UNIT ANALYSIS

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

DEBT MATURITIES

Mortgages (1)

Amortization Maturities TotalsUnsecured

Notes (2)Credit

Facility (3) Total

WeightedAverage

Interest Rate

2017 $ 3,919 $ — $ 3,919 $ — $ — $ 3,919 4.94%

2018 6,565 26,995 33,560 — 177,000 210,560 2.50%

2019 6,504 50,043 56,547 — — 56,547 4.02%

2020 3,539 67,361 70,900 350,000 — 420,900 4.93%

2021 2,504 65,009 67,513 — — 67,513 4.06%

2022 2,172 — 2,172 400,000 — 402,172 4.13%

2023 2,281 — 2,281 300,000 — 302,281 3.39%

2024 2,395 — 2,395 450,000 — 452,395 4.40%

2025 2,503 — 2,503 400,000 — 402,503 3.76%

2026 and thereafter 22,294 1,946 24,240 400,000 — 424,240 3.34%

$ 54,676 $ 211,354 $ 266,030 $ 2,300,000 $ 177,000 $ 2,743,030

Reconciling Items (4) — — 5,821 (18,350) — (12,529)

$ 54,676 $ 211,354 $ 271,851 $ 2,281,650 $ 177,000 $ 2,730,501 3.91%

(1) Mortgages are fixed rate bearing interest at a weighted average interest rate of 4.74%.

(2) The unsecured notes include $350,000 principal bearing interest at 4.75%,

$400,000 principal bearing interest at 4.125%, $300,000 principal bearing interest at 3.375%,

$450,000 principal bearing interest at 4.40%, $400,000 principal bearing interest at 3.75% and

$400,000 principal bearing interest at 3.25%, for a blended weighted average interest rate of 3.96%

(3) The $800 million credit facility bears interest at LIBOR + 105 basis points and expires on March 26, 2018.

(4) Includes deferred financing costs, premium/discount and market adjustments.

PREFERRED UNITS

SecurityDividend

RateLiquidationPreference Optional Redemption Date

Series I -2 6.25% $7,537 November 2016 - July 2027

Page 31

DEBT STATISTICS & RATIOS

SECOND QUARTER 2017 SUPPLEMENTAL

Quarter Ended Year to Date

6/30/2017 6/30/2016 6/30/2017 6/30/2016

Average Net Debt to Adjusted EBITDA 5.7x 6.0x 5.6x 5.9x

Interest Expense Coverage 5.3x 4.4x 5.3x 4.3x

Cash Interest Expense Coverage 4.2x 3.7x 4.3x 3.6x

Fixed Charge Coverage 3.9x 3.5x 4.0x 3.4x

As of

6/30/2017 6/30/2016

Debt to Gross Assets 38.2% 41.9%

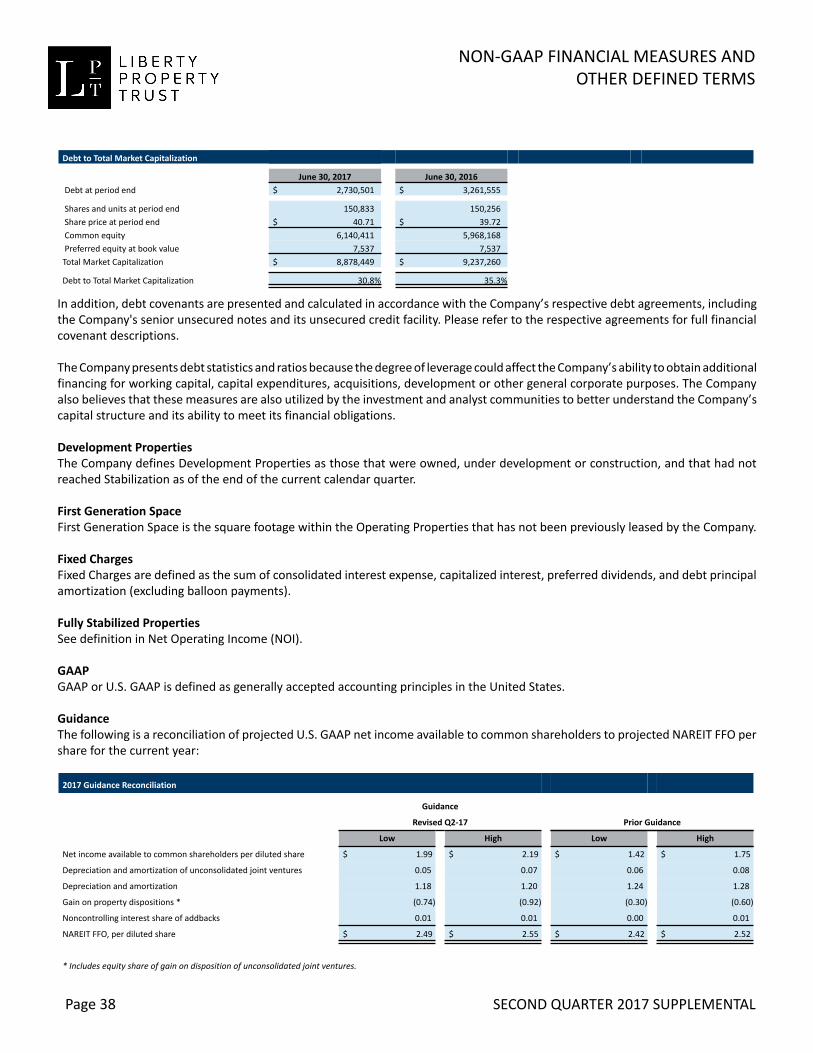

Debt to Total Market Capitalization 30.8% 35.3%

Page 32

DEBT COVENANTS & CREDIT RATINGS

SECOND QUARTER 2017 SUPPLEMENTAL

SENIOR UNSECURED NOTES

Required 6/30/2017 6/30/2017

Covenant (1) (2)

Debt/Total Assets ≤ 60% 39% 39%

Annual Service Charge Coverage ≥ 1.5 4.5 4.5

Secured Debt ≤ 40% 4% 4%

Unencumbered Total Asset Value/Unsecured Debt ≥ 1.5 2.4 2.4

UNSECURED LINE OF CREDIT

Covenant (1) (2)

Unsecured Debt : Unencumbered Properties ≤ 60% 46% 46%

Unencumbered NOI : Unsecured Interest Expense ≥ 1.75 4.0 4.0

Total Debt : Total Assets (Gross) ≤ 60% 40% 40%

Secured Debt : Total Assets (Gross) ≤ 35% 6% 6%

EBITDA : Fixed Charges ≥ 1.5 3.3 3.3

Dividend : FFO ≤ 90% 80% 80%

(1) Defined terms used in the above covenant calculations may differ between the Senior UnsecuredNotes and the Unsecured Line of Credit.

(2) Ratios use calculations that are defined in the Trust Indenture or Credit Facility Credit Agreementas appropriate.

CREDIT RATINGS

Agency Rating Outlook Last Update

Moody's Investor Services, Inc. Baa1 Stable January 2017

Standard and Poor's Ratings Services BBB Stable March 2017

Fitch, Inc. BBB Stable June 2016

Page 33

GUIDANCE

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in millions)

2017 Range

GuidanceRevised Q2-17 Prior Guidance

Low High Low HighProjected net income available tocommon shareholders per share

$1.99 $2.19 $1.42 $1.75

Projected NAREIT FFO per diluted share $2.49 $2.55 $2.42 $2.52

Capital Activity

Total Investment Average Yield

Acquisitions $50 - $200 4.5% - 6.5%

Land Acquisitions $20 - $50

Dispositions $200 - $350 5.5% - 8.5%

Development Deliveries $250 - $350 7.5% - 8.5%

Development Deliveries (JV) $750 8.2%

Development Starts $400 - $500

Development Starts (JV) $0 - $50

Development Spend $400 - $475

Development Spend (JV) $50

Same Store Property Level Operating Income (2017 - 2016) Percent Change

GuidanceRevised Q2-17 Prior Guidance

Total 1% - 2% 0% - 2%

Industrial 2% - 3% 1% - 3%

Office (3%) - (4%) (3%) - (5%)

Portfolio Performance Assumptions

GuidanceRevised Q2-17 Prior Guidance

Average Occupancy

Industrial 95% - 97% 95% - 97%

Office 90% - 92% 88% - 90%

Rental Rate Change - Straight Line 10% - 12% 9% - 11%

Industrial 11% - 13% 9% - 11%

Office 7% - 10% 10% - 12%

Rental Rate Change - Cash 3% - 5% 1% - 3%

Industrial 3% - 6% 1% - 3%

Office (1%) - 1% 0% - 2%

Page 34

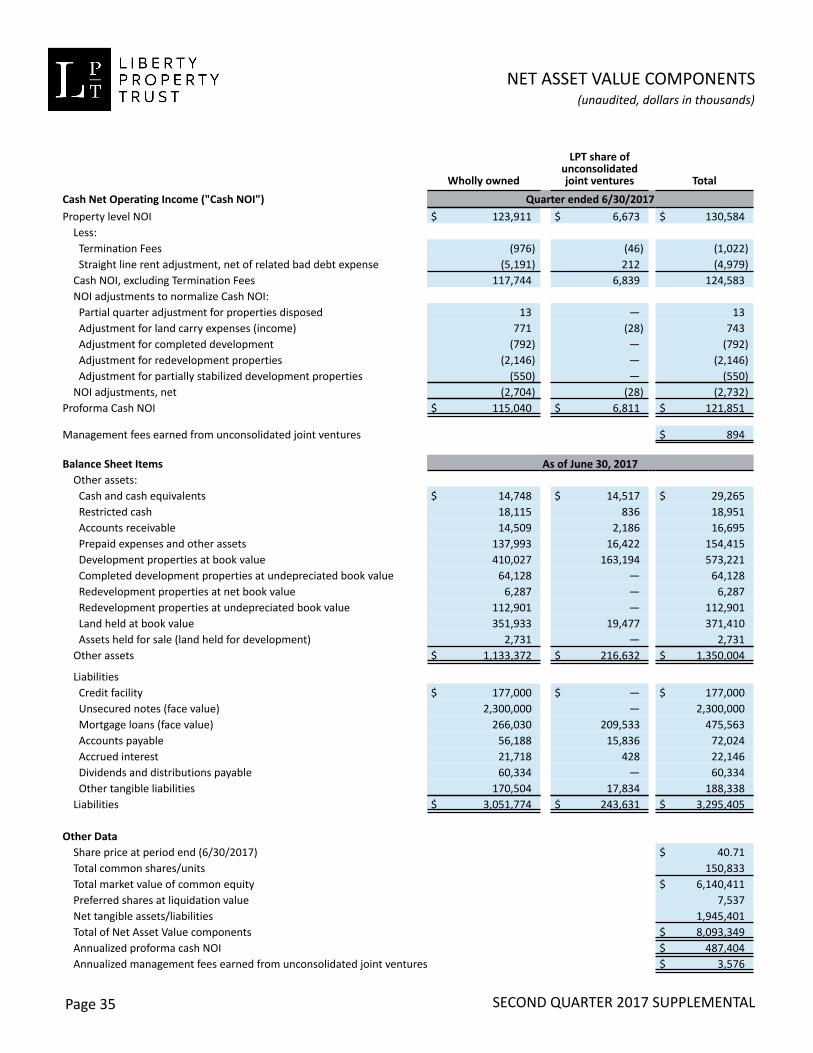

NET ASSET VALUE COMPONENTS

SECOND QUARTER 2017 SUPPLEMENTAL

(unaudited, dollars in thousands)

Wholly owned

LPT share ofunconsolidatedjoint ventures Total

Cash Net Operating Income ("Cash NOI") Quarter ended 6/30/2017

Property level NOI $ 123,911 $ 6,673 $ 130,584 Less: Termination Fees (976) (46) (1,022) Straight line rent adjustment, net of related bad debt expense (5,191) 212 (4,979) Cash NOI, excluding Termination Fees 117,744 6,839 124,583 NOI adjustments to normalize Cash NOI: Partial quarter adjustment for properties disposed 13 — 13 Adjustment for land carry expenses (income) 771 (28) 743 Adjustment for completed development (792) — (792) Adjustment for redevelopment properties (2,146) — (2,146) Adjustment for partially stabilized development properties (550) — (550) NOI adjustments, net (2,704) (28) (2,732)Proforma Cash NOI $ 115,040 $ 6,811 $ 121,851

Management fees earned from unconsolidated joint ventures $ 894

Balance Sheet Items As of June 30, 2017 Other assets: Cash and cash equivalents $ 14,748 $ 14,517 $ 29,265 Restricted cash 18,115 836 18,951 Accounts receivable 14,509 2,186 16,695 Prepaid expenses and other assets 137,993 16,422 154,415 Development properties at book value 410,027 163,194 573,221 Completed development properties at undepreciated book value 64,128 — 64,128 Redevelopment properties at net book value 6,287 — 6,287 Redevelopment properties at undepreciated book value 112,901 — 112,901 Land held at book value 351,933 19,477 371,410 Assets held for sale (land held for development) 2,731 — 2,731 Other assets $ 1,133,372 $ 216,632 $ 1,350,004

Liabilities Credit facility $ 177,000 $ — $ 177,000 Unsecured notes (face value) 2,300,000 — 2,300,000 Mortgage loans (face value) 266,030 209,533 475,563 Accounts payable 56,188 15,836 72,024 Accrued interest 21,718 428 22,146 Dividends and distributions payable 60,334 — 60,334 Other tangible liabilities 170,504 17,834 188,338 Liabilities $ 3,051,774 $ 243,631 $ 3,295,405

Other Data Share price at period end (6/30/2017) $ 40.71 Total common shares/units 150,833 Total market value of common equity $ 6,140,411 Preferred shares at liquidation value 7,537 Net tangible assets/liabilities 1,945,401 Total of Net Asset Value components $ 8,093,349 Annualized proforma cash NOI $ 487,404 Annualized management fees earned from unconsolidated joint ventures $ 3,576

Page 35

NON-GAAP FINANCIAL MEASURES AND OTHER DEFINED TERMS

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

Non-GAAP Financial Measures and Other Defined Terms The Company uses certain non-GAAP financial measures and other defined terms in this Supplemental. The non-GAAP financialmeasures include Funds from Operations (FFO), Adjusted Funds from Operations (AFFO), Adjusted EBITDA, Net Operating Income(NOI), and other defined terms. The definitions of non-GAAP financial measures are listed below. The Company uses these measuresto monitor the operating and financial performance of the Company and believes that these measures are helpful to investors inmeasuring financial performance and/or liquidity and comparing such performance and/or liquidity to other REITs. These non-GAAPfinancial measures are supplemental measures of operating performance that do not represent and should not be considered asan alternative to net income or cash flow from operating, investing or financing activities as determined under U.S. GAAP, and theCompany’s calculation thereof may not be comparable to similar measures reported by other companies.

Adjusted EBITDAAdjusted EDITDA is defined as net income, after adjusting for depreciation and amortization expense, interest expense, impairmentcharges and the effect of other non-cash items, debt extinguishment gains (losses), gains (losses) on property dispositions, incometax expense (benefit), and share-based compensation expenses, as applicable.

The Company uses Adjusted EBITDA as a supplemental measure of its operating performance. The Company believes it providesinvestors and analysts with relevant and useful information to view its operating performance on an unleveraged basis before theeffects of interest, income taxes, depreciation and amortization, gains (losses) on the sales of property, debt extinguishment gains(losses) and other non-cash items noted above. By excluding interest expense, Adjusted EBITDA allows investors and analysts tomeasure the Company’s operating performance independent of its capital structure and indebtedness that allows a moremeaningful comparison to similar measures reported by other companies. The Company also believes that Adjusted EBITDAassists investors and analysts in analyzing its ability to meet debt service obligations and make quarterly dividend payments.While Adjusted EBITDA is a relevant and widely used measure of operating performance, it does not represent net income asdefined by U.S. GAAP, and it should not be considered as an alternative to those measures in evaluating the Company’s operatingperformance or liquidity. Further, the Company’s computation of Adjusted EBITDA may not be comparable to EBITDA or AdjustedEBITDA reported by other companies. The Company believes that the line on its consolidated statements of comprehensiveincome entitled “net income” is the most directly comparable U.S. GAAP measure to Adjusted EBITDA - see reconciliation on page10.

Adjusted Funds from Operations (AFFO)AFFO is defined as FFO less Tenant improvement and Lease Transaction Costs and Non-reimbursed Capital Expenditures, and afteradjusting for the impact of straight-line rents adjustments, share-based compensation expense, impairment charges and the effectof other non-cash items, gains (losses) on sales of non-depreciable assets, and debt extinguishment gains (losses), as applicable.AFFO is used as an additional measure in evaluating Company performance, as an indication of the REIT’s ability to fund its operatingcapital expenditures through earnings and in reviewing its common dividend policy over time. In addition, since other equity REITsprovide AFFO, or similar supplemental measures, to the investment community, the Company believes that AFFO is a usefulsupplemental measure for comparing the Company to other equity REITs. The Company believes that the line on its consolidatedstatements of comprehensive income entitled “net income available to common shareholders” is the most directly comparable U.S.GAAP measure to AFFO - see reconciliation on page 9.

Capital Expenditures (Cap Ex)Capital expenditures include costs incurred for roof or HVAC replacements, parking lot replacements, drainage solutions, pavingreplacements, exterior building coatings and landscaping renovations or other costs that extend the life of the property. Capitalexpenditures do not include costs for redevelopments, or that otherwise would be considered revenue-generating, or are includedin the underwriting for acquisition properties.

Current YieldCurrent Yield is the straight line net operating income generated at period end divided by the total cost of the investment.

Page 36

NON-GAAP FINANCIAL MEASURES AND OTHER DEFINED TERMS

SECOND QUARTER 2017 SUPPLEMENTAL

(dollars in thousands)

Debt Statistics and RatiosThe Company uses a number of debt statistics and ratios as supplemental measures of its capital structure and indebtedness, aswell as to assist investors and analysts in evaluating its ability to meet its debt service obligations and make quarterly dividendpayments. The numerator and/or the denominator of certain of these statistics and/or ratios include non-GAAP financial measuresthat have been reconciled to the most directly comparable U.S. GAAP financial measure. The calculation of these debt statistics andratios is provided below:

Cash Interest Expense CoverageQuarter Ended

June 30, 2017 June 30, 2016 June 30, 2017 June 30, 2016 Adjusted EBITDA $ 117,302 $ 133,268 $ 235,704 $ 265,288

Interest expense 21,942 30,131 44,285 61,543Capitalized interest 5,907 6,195 10,888 11,260Cash interest expense $ 27,849 $ 36,326 $ 55,173 $ 72,803

Cash Interest Expense Coverage 4.2x 3.7x 4.3x 3.6x

Fixed Charge CoverageQuarter Ended Year to Date

June 30, 2017 June 30, 2016 June 30, 2017 June 30, 2016Adjusted EBITDA $ 117,302 $ 133,268 $ 235,704 $ 265,288

Interest expense 21,942 30,131 44,285 61,543 Capitalized interest 5,907 6,195 10,888 11,260 Preferred dividends 118 118 236 236 Principal amortization 1,946 2,080 3,875 4,337Total fixed charges $ 29,913 $ 38,524 $ 59,284 $ 77,376

Fixed Charge Coverage 3.9x 3.5x 4.0x 3.4x

Average Net Debt to Adjusted EBITDAQuarter Ended Year to Date

June 30, 2017 June 30, 2016 June 30, 2017 June 30, 2016 Average Debt $ 2,725,926 $ 3,222,319 $ 2,673,433 $ 3,194,759 less: average unrestricted cash (29,996) (36,460) (33,809) (38,804) Average net debt 2,695,930 3,185,859 2,639,624 3,155,955

Adjusted EBITDA $ 117,302 $ 133,268 $ 235,704 $ 265,288

Average Net Debt to Adjusted EBITDA 5.7x 6.0x 5.6x 5.9x

Debt to Gross Assets

June 30, 2017 June 30, 2016Debt at period end $ 2,730,501 $ 3,261,555

Total assets 6,159,635 6,584,868Accumulated depreciation 995,032 1,199,941Gross assets $ 7,154,667 $ 7,784,809

Debt to Gross Assets 38.2% 41.9%

Page 37

Interest Expense CoverageQuarter Ended Year to Date

June 30, 2017 June 30, 2016 June 30, 2017 June 30, 2016 Adjusted EBITDA $ 117,302 $ 133,268 $ 235,704 $ 265,288

Interest expense $ 21,942 $ 30,131 $ 44,285 $ 61,543

Interest Expense Coverage 5.3x 4.4x 5.3x 4.3x

NON-GAAP FINANCIAL MEASURES AND OTHER DEFINED TERMS

SECOND QUARTER 2017 SUPPLEMENTAL

In addition, debt covenants are presented and calculated in accordance with the Company’s respective debt agreements, includingthe Company's senior unsecured notes and its unsecured credit facility. Please refer to the respective agreements for full financialcovenant descriptions.

The Company presents debt statistics and ratios because the degree of leverage could affect the Company’s ability to obtain additionalfinancing for working capital, capital expenditures, acquisitions, development or other general corporate purposes. The Companyalso believes that these measures are also utilized by the investment and analyst communities to better understand the Company’scapital structure and its ability to meet its financial obligations.

Development PropertiesThe Company defines Development Properties as those that were owned, under development or construction, and that had notreached Stabilization as of the end of the current calendar quarter.

First Generation Space First Generation Space is the square footage within the Operating Properties that has not been previously leased by the Company.

Fixed ChargesFixed Charges are defined as the sum of consolidated interest expense, capitalized interest, preferred dividends, and debt principalamortization (excluding balloon payments).

Fully Stabilized PropertiesSee definition in Net Operating Income (NOI).

GAAPGAAP or U.S. GAAP is defined as generally accepted accounting principles in the United States.

GuidanceThe following is a reconciliation of projected U.S. GAAP net income available to common shareholders to projected NAREIT FFO pershare for the current year:

Debt to Total Market Capitalization

June 30, 2017 June 30, 2016 Debt at period end $ 2,730,501 $ 3,261,555

Shares and units at period end 150,833 150,256 Share price at period end $ 40.71 $ 39.72 Common equity 6,140,411 5,968,168 Preferred equity at book value 7,537 7,537Total Market Capitalization $ 8,878,449 $ 9,237,260

Debt to Total Market Capitalization 30.8% 35.3%

2017 Guidance Reconciliation

Guidance

Revised Q2-17 Prior Guidance

Low High Low High

Net income available to common shareholders per diluted share $ 1.99 $ 2.19 $ 1.42 $ 1.75

Depreciation and amortization of unconsolidated joint ventures 0.05 0.07 0.06 0.08

Depreciation and amortization 1.18 1.20 1.24 1.28

Gain on property dispositions * (0.74) (0.92) (0.30) (0.60)

Noncontrolling interest share of addbacks 0.01 0.01 0.00 0.01

NAREIT FFO, per diluted share $ 2.49 $ 2.55 $ 2.42 $ 2.52

* Includes equity share of gain on disposition of unconsolidated joint ventures.

Page 38

NON-GAAP FINANCIAL MEASURES AND OTHER DEFINED TERMS

NAREIT Funds from Operations (FFO)NAREIT Funds from Operations available to common shareholders is defined by NAREIT as net income (computed in accordancewith U.S. GAAP), excluding gains (or losses) from sales of depreciable property and impairments of depreciable real estate assets,plus depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. The SEC has agreedto the disclosure of this non-GAAP financial measure on a per share basis in its Release No. 34-47226, Conditions for Use of Non-GAAP Financial Measures. The Company believes that the calculation of NAREIT FFO is helpful to investors and management as it isa measure of the Company’s operating performance that excludes depreciation and amortization and gains and losses from operatingproperty dispositions. As a result, year over year comparison of NAREIT FFO reflects the impact on operations from trends inoccupancy rates, rental rates, operating costs, development activities, general and administrative expenses, and interest costs,providing perspective not immediately apparent from net income. In addition, management believes that NAREIT FFO providesuseful information to the investment community about the Company’s financial performance when compared to other REITs sinceNAREIT FFO is generally recognized as the standard for reporting the operating performance of a REIT. NAREIT FFO available tocommon shareholders does not represent net income or cash flows from operations as defined by U.S. GAAP and does not necessarilyindicate that cash flows will be sufficient to fund cash needs. It should not be considered as an alternative to net income as anindicator of the Company’s operating performance or to cash flows as a measure of liquidity. NAREIT FFO available to commonshareholders also does not represent cash flows generated from operating, investing or financing activities as defined by U.S. GAAP.The Company believes that the line on its consolidated statements of comprehensive income entitled “net income available tocommon shareholders” is the most directly comparable U.S. GAAP measure to FFO - see reconciliation on page 9.

Net Asset Value (NAV)The Company considers NAV to be a useful supplemental measure of its operating performance because it enables investors toestimate the fair value of its business and its underlying net real estate assets. This Supplemental provides the components andadjustments to certain U.S. GAAP financial measures and NOI that the Company uses internally to calculate NAV. The assessmentof NAV is subjective and can be calculated using different methods. Therefore, the Company has presented components andadjustments to property operating results and other net assets that it believes are important in calculating NAV, but have notpresented any specific methodology, nor provided any guidance on the assumptions or estimates that should be used in calculatingNAV.

Within its NAV disclosure the Company presents NOI for properties that have reached Stabilization as of the 1st day of the applicablequarter ended (including its share of unconsolidated joint ventures), so that a capitalization rate may be applied and an approximatevalue for the assets determined. Properties not stabilized as of the 1st day of the applicable quarter are presented at undepreciatedcost, or in certain instances, at net book value. Other tangible assets and liabilities are presented at book value. Preferred sharesare presented at liquidation value.