Embed Size (px)

Citation preview

Table of Contents OVERVIEW OF OMB SUPERCIRCULAR .................................................................................................................... 1

OBJECTIVES OF THE REFORM ................................................................................................................................. 1

OMB A-21 (COST PRINCIPLES FOR EDUCATIONAL INSTITUTIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS) POLICY CHANGES, UPDATES AND DETAILED CROSSWALK ................................................................................................................... 2

OMB A-87 (COST PRINCIPLES FOR STATE, LOCAL AND INDIAN TRIBAL GOVERNMENTS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS) POLICY CHANGES, UPDATES AND DETAILED CROSSWALK .................................................................................................. 6

OMB A-89 (FEDERAL DOMESTIC ASSISTANCE PROGRAM INFORMATION) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS) POLICY CHANGES, UPDATES AND DETAILED CROSSWALK ................................................................................................................... 7

OMB A-102 (GRANT AND COOPERATIVE AGREEMENTS WITH STATE AND LOCAL GOVERNMENTS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS) POLICY CHANGES, UPDATES AND DETAILED CROSSWALK ...................................................................................... 8

OMB A-110 (UNIFORM ADMIN REQUIREMENTS FOR GRANTS AND AGREEMENTS WITH IHES, HOSPITALS, AND NON-PROFITS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS) POLICY CHANGES, UPDATES AND DETAILED CROSSWALK ............................................. 10

OMB A-122 (COST PRINCIPLES FOR NON-PROFIT ORGANIZATIONS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS) POLICY CHANGES, UPDATES AND DETAILED CROSSWALK ................................................................................................................. 13

OMB A-133 (AUDITS OF STATES, LOCAL GOVERNMENTS, AND NON-PROFITS) TO 2 CFR 200 (UNIFORM ADMIN REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS) POLICY CHANGES, UPDATES AND DETAILED CROSSWALK ................................................................................................................. 14

OVERVIEW OF OMB SUPERCIRCULAR

Office of Management and Budget (“OMB”) issued the “Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, Final Rule (Uniform Guidance) on December 26, 2013”, which is referred to as OMB “Super Circular” or “Omni Circular” and is codified at 2 CFR Part 200. The Super Circular supersedes and streamlines requirements from the following OMB Circulars applicable to the administration, use and audit of federal grant funds by non-profit organizations, state, local and tribal governments, and colleges and universities:

• OMB Circular A-21: Cost Principles for Educational Institutions • OMB Circular A-87: Cost Principles for State, Local and Indian Tribal Governments • OMB Circular A-89: Federal Domestic Assistance Program Information • OMB Circular A-102: Grants and Cooperative Agreements with State and Local Governments • OMB Circular A-110: Uniform Administrative Requirements for Grants and Agreements with

Institutions of Higher Education, Hospitals and Other Non-Profits • OMB Circular A-122: Cost Principles for Non-Profit Organizations • OMB Circular A-133: Audits of States, Local Governments and Non-Profit Organizations

2 CFR Part 200 affects Federal awarding agencies and “non-Federal entities” including non-profits, state and local governments, Indian tribes, and Institutes of Higher Education (IHE) that receive Federal assistance awards as a recipient or sub recipient, as well as their auditors. For profit entities will also be subject to a portion of the rules. These rules apply to Federal assistance awards and to additional funding increments made after December 26, 2014. Existing awards will continue to be governed by the terms and conditions of their Federal award agreement and no retroactive change exists to award terms and conditions.

OBJECTIVES OF THE REFORM

• Eliminate duplicative and conflicting guidance • Reduce administrative burdens on non-Federal entities receiving Federal awards • Increase impact and accessibility of programs by minimizing time spent on compliance • Increase management focus on performance and achieving program outcomes • Strengthen internal controls while providing administrative flexibility • Increase financial management, integrity and accountability over Federal funds by improving

policies that protect against fraud, waste and abuse. • Award grants and cooperative agreements based on merit and financial risk • Streamline and clarify guidance on sub-recipient monitoring • Focus the Single Audit oversight tool to reduce fraud, waste and abuse

1

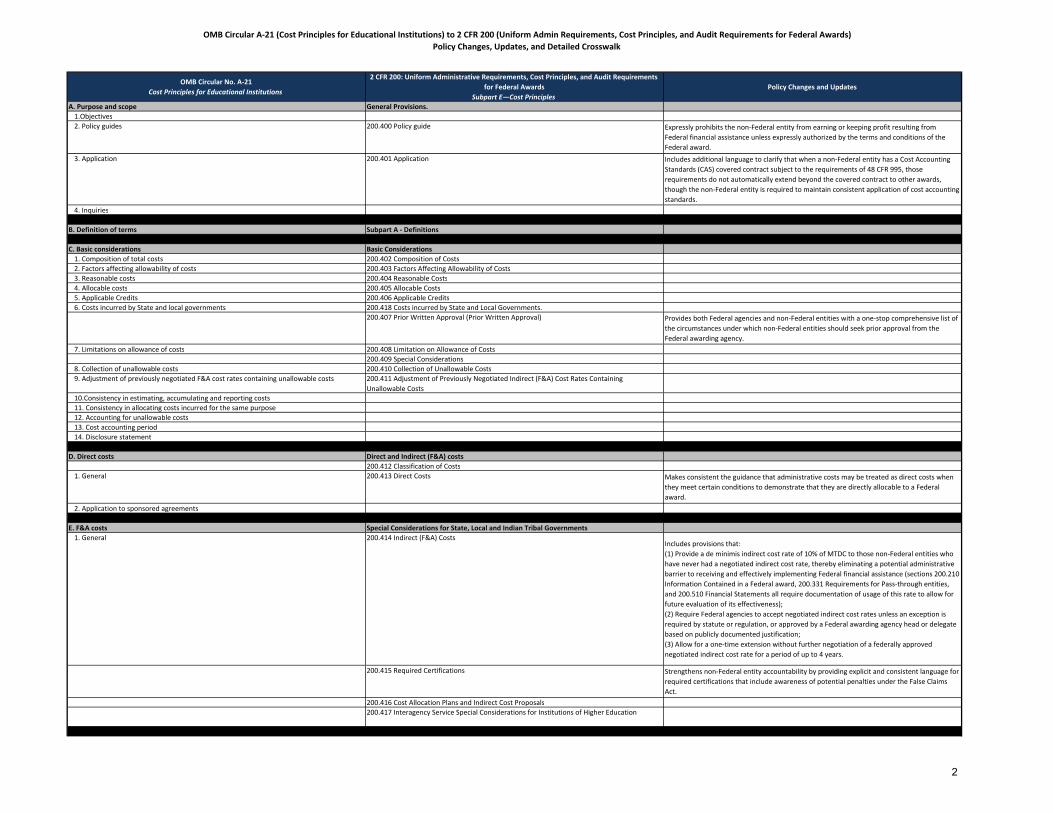

OMB Circular A-21 (Cost Principles for Educational Institutions) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

OMB Circular No. A-21

Cost Principles for Educational Institutions

2 CFR 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

for Federal Awards

Subpart E—Cost Principles

Policy Changes and Updates

A. Purpose and scope General Provisions.

1.Objectives

2. Policy guides 200.400 Policy guide Expressly prohibits the non-Federal entity from earning or keeping profit resulting from

Federal financial assistance unless expressly authorized by the terms and conditions of the

Federal award.

3. Application 200.401 Application Includes additional language to clarify that when a non-Federal entity has a Cost Accounting

Standards (CAS) covered contract subject to the requirements of 48 CFR 995, those

requirements do not automatically extend beyond the covered contract to other awards,

though the non-Federal entity is required to maintain consistent application of cost accounting

standards.

4. Inquiries

B. Definition of terms Subpart A - Definitions

C. Basic considerations Basic Considerations

1. Composition of total costs 200.402 Composition of Costs

2. Factors affecting allowability of costs 200.403 Factors Affecting Allowability of Costs

3. Reasonable costs 200.404 Reasonable Costs

4. Allocable costs 200.405 Allocable Costs

5. Applicable Credits 200.406 Applicable Credits

6. Costs incurred by State and local governments 200.418 Costs incurred by State and Local Governments.

200.407 Prior Written Approval (Prior Written Approval) Provides both Federal agencies and non-Federal entities with a one-stop comprehensive list of

the circumstances under which non-Federal entities should seek prior approval from the

Federal awarding agency.

7. Limitations on allowance of costs 200.408 Limitation on Allowance of Costs

200.409 Special Considerations

8. Collection of unallowable costs 200.410 Collection of Unallowable Costs

9. Adjustment of previously negotiated F&A cost rates containing unallowable costs 200.411 Adjustment of Previously Negotiated Indirect (F&A) Cost Rates Containing

Unallowable Costs

10.Consistency in estimating, accumulating and reporting costs

11. Consistency in allocating costs incurred for the same purpose

12. Accounting for unallowable costs

13. Cost accounting period

14. Disclosure statement

D. Direct costs Direct and Indirect (F&A) costs

200.412 Classification of Costs

1. General 200.413 Direct Costs Makes consistent the guidance that administrative costs may be treated as direct costs when

they meet certain conditions to demonstrate that they are directly allocable to a Federal

award.

2. Application to sponsored agreements

E. F&A costs Special Considerations for State, Local and Indian Tribal Governments

1. General 200.414 Indirect (F&A) CostsIncludes provisions that:

(1) Provide a de minimis indirect cost rate of 10% of MTDC to those non-Federal entities who

have never had a negotiated indirect cost rate, thereby eliminating a potential administrative

barrier to receiving and effectively implementing Federal financial assistance (sections 200.210

Information Contained in a Federal award, 200.331 Requirements for Pass-through entities,

and 200.510 Financial Statements all require documentation of usage of this rate to allow for

future evaluation of its effectiveness);

(2) Require Federal agencies to accept negotiated indirect cost rates unless an exception is

required by statute or regulation, or approved by a Federal awarding agency head or delegate

based on publicly documented justification;

(3) Allow for a one-time extension without further negotiation of a federally approved

negotiated indirect cost rate for a period of up to 4 years.

200.415 Required Certifications Strengthens non-Federal entity accountability by providing explicit and consistent language for

required certifications that include awareness of potential penalties under the False Claims

Act.

200.416 Cost Allocation Plans and Indirect Cost Proposals

200.417 Interagency Service Special Considerations for Institutions of Higher Education

2

OMB Circular A-21 (Cost Principles for Educational Institutions) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

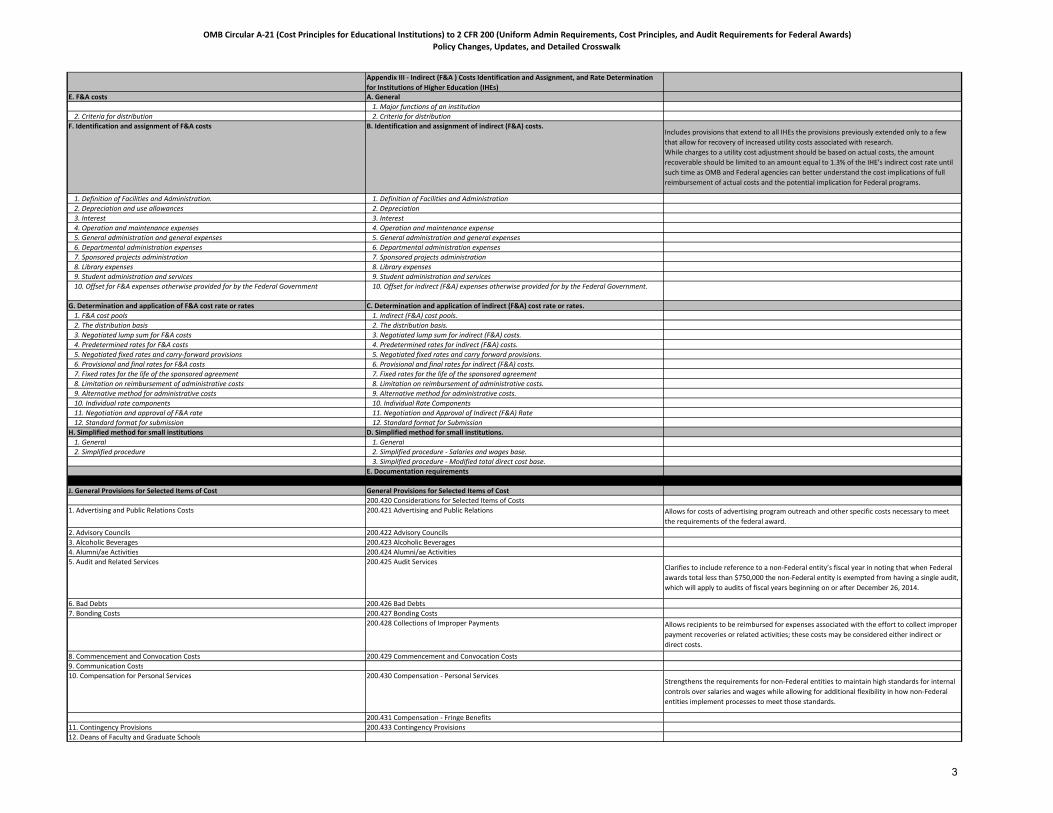

Appendix III - Indirect (F&A ) Costs Identification and Assignment, and Rate Determination

for Institutions of Higher Education (IHEs)

E. F&A costs A. General

1. Major functions of an institution

2. Criteria for distribution 2. Criteria for distribution

F. Identification and assignment of F&A costs B. Identification and assignment of indirect (F&A) costs.Includes provisions that extend to all IHEs the provisions previously extended only to a few

that allow for recovery of increased utility costs associated with research.

While charges to a utility cost adjustment should be based on actual costs, the amount

recoverable should be limited to an amount equal to 1.3% of the IHE’s indirect cost rate until

such time as OMB and Federal agencies can better understand the cost implications of full

reimbursement of actual costs and the potential implication for Federal programs.

1. Definition of Facilities and Administration. 1. Definition of Facilities and Administration

2. Depreciation and use allowances 2. Depreciation

3. Interest 3. Interest

4. Operation and maintenance expenses 4. Operation and maintenance expense

5. General administration and general expenses 5. General administration and general expenses

6. Departmental administration expenses 6. Departmental administration expenses

7. Sponsored projects administration 7. Sponsored projects administration

8. Library expenses 8. Library expenses

9. Student administration and services 9. Student administration and services

10. Offset for F&A expenses otherwise provided for by the Federal Government 10. Offset for indirect (F&A) expenses otherwise provided for by the Federal Government.

G. Determination and application of F&A cost rate or rates C. Determination and application of indirect (F&A) cost rate or rates.

1. F&A cost pools 1. Indirect (F&A) cost pools.

2. The distribution basis 2. The distribution basis.

3. Negotiated lump sum for F&A costs 3. Negotiated lump sum for indirect (F&A) costs.

4. Predetermined rates for F&A costs 4. Predetermined rates for indirect (F&A) costs.

5. Negotiated fixed rates and carry-forward provisions 5. Negotiated fixed rates and carry forward provisions.

6. Provisional and final rates for F&A costs 6. Provisional and final rates for indirect (F&A) costs.

7. Fixed rates for the life of the sponsored agreement 7. Fixed rates for the life of the sponsored agreement

8. Limitation on reimbursement of administrative costs 8. Limitation on reimbursement of administrative costs.

9. Alternative method for administrative costs 9. Alternative method for administrative costs.

10. Individual rate components 10. Individual Rate Components

11. Negotiation and approval of F&A rate 11. Negotiation and Approval of Indirect (F&A) Rate

12. Standard format for submission 12. Standard format for Submission

H. Simplified method for small institutions D. Simplified method for small institutions.

1. General 1. General

2. Simplified procedure 2. Simplified procedure - Salaries and wages base.

3. Simplified procedure - Modified total direct cost base.

E. Documentation requirements

J. General Provisions for Selected Items of Cost General Provisions for Selected Items of Cost

200.420 Considerations for Selected Items of Costs

1. Advertising and Public Relations Costs 200.421 Advertising and Public Relations Allows for costs of advertising program outreach and other specific costs necessary to meet

the requirements of the federal award.

2. Advisory Councils 200.422 Advisory Councils

3. Alcoholic Beverages 200.423 Alcoholic Beverages

4. Alumni/ae Activities 200.424 Alumni/ae Activities

5. Audit and Related Services 200.425 Audit ServicesClarifies to include reference to a non-Federal entity’s fiscal year in noting that when Federal

awards total less than $750,000 the non-Federal entity is exempted from having a single audit,

which will apply to audits of fiscal years beginning on or after December 26, 2014.

6. Bad Debts 200.426 Bad Debts

7. Bonding Costs 200.427 Bonding Costs

200.428 Collections of Improper Payments Allows recipients to be reimbursed for expenses associated with the effort to collect improper

payment recoveries or related activities; these costs may be considered either indirect or

direct costs.

8. Commencement and Convocation Costs 200.429 Commencement and Convocation Costs

9. Communication Costs

10. Compensation for Personal Services 200.430 Compensation - Personal ServicesStrengthens the requirements for non-Federal entities to maintain high standards for internal

controls over salaries and wages while allowing for additional flexibility in how non-Federal

entities implement processes to meet those standards.

200.431 Compensation - Fringe Benefits

11. Contingency Provisions 200.433 Contingency Provisions

12. Deans of Faculty and Graduate Schools

3

OMB Circular A-21 (Cost Principles for Educational Institutions) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

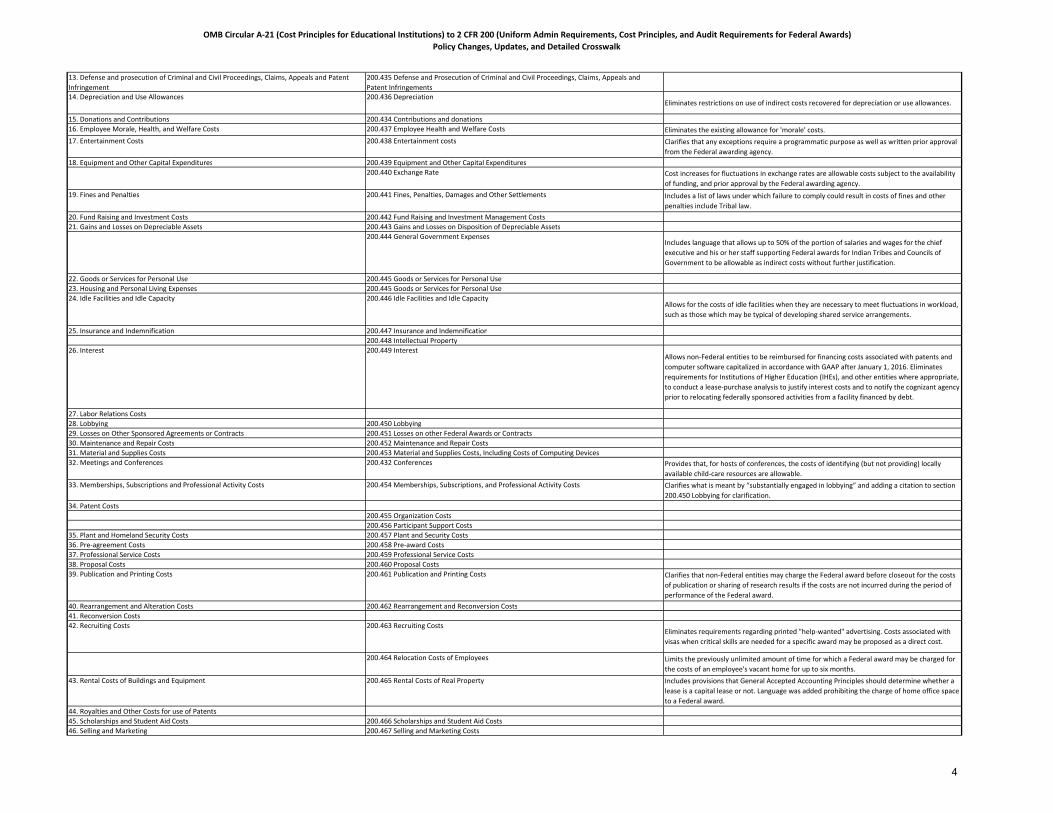

13. Defense and prosecution of Criminal and Civil Proceedings, Claims, Appeals and Patent

Infringement

200.435 Defense and Prosecution of Criminal and Civil Proceedings, Claims, Appeals and

Patent Infringements

14. Depreciation and Use Allowances 200.436 DepreciationEliminates restrictions on use of indirect costs recovered for depreciation or use allowances.

15. Donations and Contributions 200.434 Contributions and donations

16. Employee Morale, Health, and Welfare Costs 200.437 Employee Health and Welfare Costs Eliminates the existing allowance for 'morale' costs.

17. Entertainment Costs 200.438 Entertainment costs Clarifies that any exceptions require a programmatic purpose as well as written prior approval

from the Federal awarding agency.

18. Equipment and Other Capital Expenditures 200.439 Equipment and Other Capital Expenditures

200.440 Exchange Rate Cost increases for fluctuations in exchange rates are allowable costs subject to the availability

of funding, and prior approval by the Federal awarding agency.

19. Fines and Penalties 200.441 Fines, Penalties, Damages and Other Settlements Includes a list of laws under which failure to comply could result in costs of fines and other

penalties include Tribal law.

20. Fund Raising and Investment Costs 200.442 Fund Raising and Investment Management Costs

21. Gains and Losses on Depreciable Assets 200.443 Gains and Losses on Disposition of Depreciable Assets

200.444 General Government ExpensesIncludes language that allows up to 50% of the portion of salaries and wages for the chief

executive and his or her staff supporting Federal awards for Indian Tribes and Councils of

Government to be allowable as indirect costs without further justification.

22. Goods or Services for Personal Use 200.445 Goods or Services for Personal Use

23. Housing and Personal Living Expenses 200.445 Goods or Services for Personal Use

24. Idle Facilities and Idle Capacity 200.446 Idle Facilities and Idle CapacityAllows for the costs of idle facilities when they are necessary to meet fluctuations in workload,

such as those which may be typical of developing shared service arrangements.

25. Insurance and Indemnification 200.447 Insurance and Indemnification

200.448 Intellectual Property

26. Interest 200.449 InterestAllows non-Federal entities to be reimbursed for financing costs associated with patents and

computer software capitalized in accordance with GAAP after January 1, 2016. Eliminates

requirements for Institutions of Higher Education (IHEs), and other entities where appropriate,

to conduct a lease-purchase analysis to justify interest costs and to notify the cognizant agency

prior to relocating federally sponsored activities from a facility financed by debt.

27. Labor Relations Costs

28. Lobbying 200.450 Lobbying

29. Losses on Other Sponsored Agreements or Contracts 200.451 Losses on other Federal Awards or Contracts

30. Maintenance and Repair Costs 200.452 Maintenance and Repair Costs

31. Material and Supplies Costs 200.453 Material and Supplies Costs, Including Costs of Computing Devices

32. Meetings and Conferences 200.432 Conferences Provides that, for hosts of conferences, the costs of identifying (but not providing) locally

available child-care resources are allowable.

33. Memberships, Subscriptions and Professional Activity Costs 200.454 Memberships, Subscriptions, and Professional Activity Costs Clarifies what is meant by “substantially engaged in lobbying” and adding a citation to section

200.450 Lobbying for clarification.

34. Patent Costs

200.455 Organization Costs

200.456 Participant Support Costs

35. Plant and Homeland Security Costs 200.457 Plant and Security Costs

36. Pre-agreement Costs 200.458 Pre-award Costs

37. Professional Service Costs 200.459 Professional Service Costs

38. Proposal Costs 200.460 Proposal Costs

39. Publication and Printing Costs 200.461 Publication and Printing Costs Clarifies that non-Federal entities may charge the Federal award before closeout for the costs

of publication or sharing of research results if the costs are not incurred during the period of

performance of the Federal award.

40. Rearrangement and Alteration Costs 200.462 Rearrangement and Reconversion Costs

41. Reconversion Costs

42. Recruiting Costs 200.463 Recruiting CostsEliminates requirements regarding printed "help-wanted" advertising. Costs associated with

visas when critical skills are needed for a specific award may be proposed as a direct cost.

200.464 Relocation Costs of Employees Limits the previously unlimited amount of time for which a Federal award may be charged for

the costs of an employee's vacant home for up to six months.

43. Rental Costs of Buildings and Equipment 200.465 Rental Costs of Real Property Includes provisions that General Accepted Accounting Principles should determine whether a

lease is a capital lease or not. Language was added prohibiting the charge of home office space

to a Federal award.

44. Royalties and Other Costs for use of Patents

45. Scholarships and Student Aid Costs 200.466 Scholarships and Student Aid Costs

46. Selling and Marketing 200.467 Selling and Marketing Costs

4

OMB Circular A-21 (Cost Principles for Educational Institutions) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

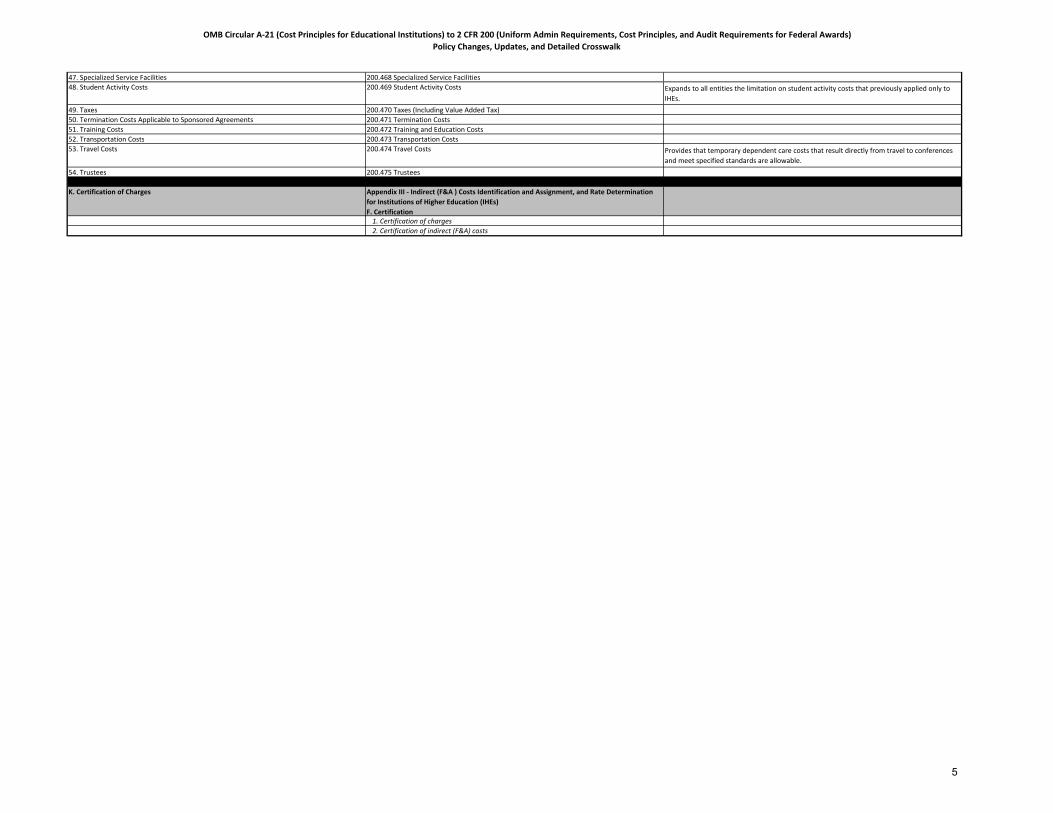

47. Specialized Service Facilities 200.468 Specialized Service Facilities

48. Student Activity Costs 200.469 Student Activity Costs Expands to all entities the limitation on student activity costs that previously applied only to

IHEs.

49. Taxes 200.470 Taxes (Including Value Added Tax)

50. Termination Costs Applicable to Sponsored Agreements 200.471 Termination Costs

51. Training Costs 200.472 Training and Education Costs

52. Transportation Costs 200.473 Transportation Costs

53. Travel Costs 200.474 Travel Costs Provides that temporary dependent care costs that result directly from travel to conferences

and meet specified standards are allowable.

54. Trustees 200.475 Trustees

K. Certification of Charges Appendix III - Indirect (F&A ) Costs Identification and Assignment, and Rate Determination

for Institutions of Higher Education (IHEs)

F. Certification

1. Certification of charges

2. Certification of indirect (F&A) costs

5

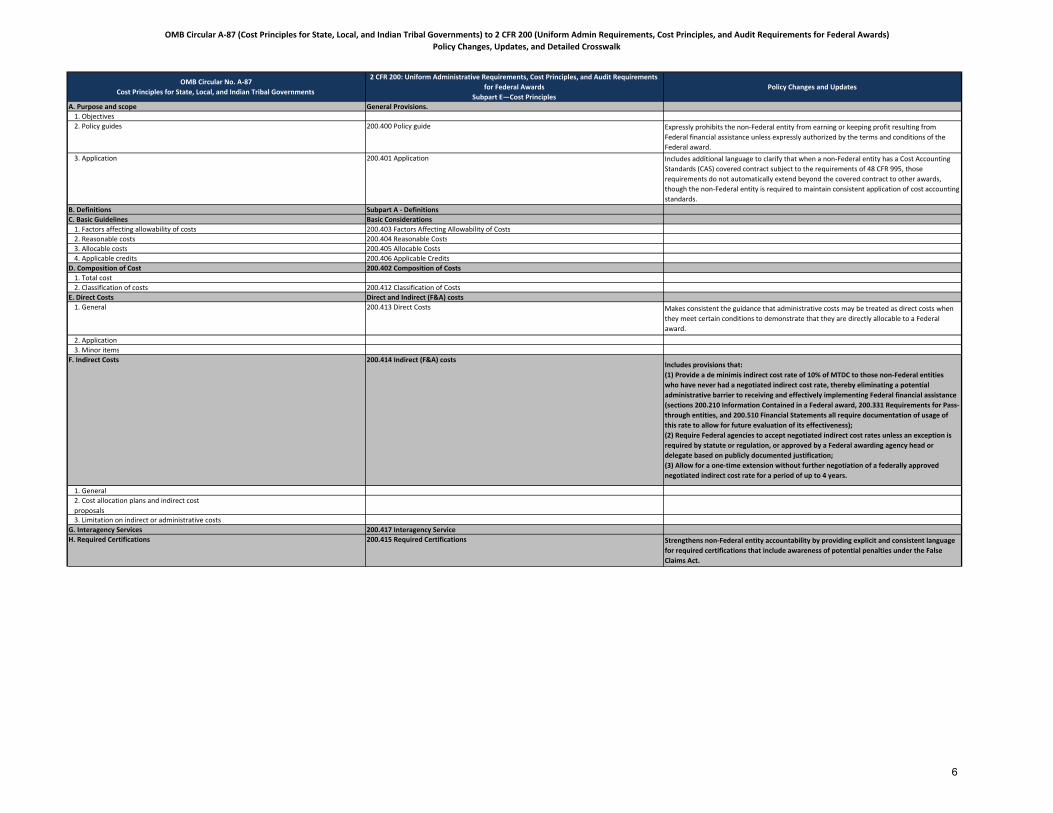

OMB Circular A-87 (Cost Principles for State, Local, and Indian Tribal Governments) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

OMB Circular No. A-87

Cost Principles for State, Local, and Indian Tribal Governments

2 CFR 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

for Federal Awards

Subpart E—Cost Principles

Policy Changes and Updates

A. Purpose and scope General Provisions.

1. Objectives

2. Policy guides 200.400 Policy guide Expressly prohibits the non-Federal entity from earning or keeping profit resulting from

Federal financial assistance unless expressly authorized by the terms and conditions of the

Federal award.

3. Application 200.401 Application Includes additional language to clarify that when a non-Federal entity has a Cost Accounting

Standards (CAS) covered contract subject to the requirements of 48 CFR 995, those

requirements do not automatically extend beyond the covered contract to other awards,

though the non-Federal entity is required to maintain consistent application of cost accounting

standards.

B. Definitions Subpart A - Definitions

C. Basic Guidelines Basic Considerations

1. Factors affecting allowability of costs 200.403 Factors Affecting Allowability of Costs

2. Reasonable costs 200.404 Reasonable Costs

3. Allocable costs 200.405 Allocable Costs

4. Applicable credits 200.406 Applicable Credits

D. Composition of Cost 200.402 Composition of Costs

1. Total cost

2. Classification of costs 200.412 Classification of Costs

E. Direct Costs Direct and Indirect (F&A) costs

1. General 200.413 Direct Costs Makes consistent the guidance that administrative costs may be treated as direct costs when

they meet certain conditions to demonstrate that they are directly allocable to a Federal

award.

2. Application

3. Minor items

F. Indirect Costs 200.414 Indirect (F&A) costsIncludes provisions that:

(1) Provide a de minimis indirect cost rate of 10% of MTDC to those non-Federal entities

who have never had a negotiated indirect cost rate, thereby eliminating a potential

administrative barrier to receiving and effectively implementing Federal financial assistance

(sections 200.210 Information Contained in a Federal award, 200.331 Requirements for Pass-

through entities, and 200.510 Financial Statements all require documentation of usage of

this rate to allow for future evaluation of its effectiveness);

(2) Require Federal agencies to accept negotiated indirect cost rates unless an exception is

required by statute or regulation, or approved by a Federal awarding agency head or

delegate based on publicly documented justification;

(3) Allow for a one-time extension without further negotiation of a federally approved

negotiated indirect cost rate for a period of up to 4 years.

1. General

2. Cost allocation plans and indirect cost

proposals

3. Limitation on indirect or administrative costs

G. Interagency Services 200.417 Interagency Service

H. Required Certifications 200.415 Required Certifications Strengthens non-Federal entity accountability by providing explicit and consistent language

for required certifications that include awareness of potential penalties under the False

Claims Act.

6

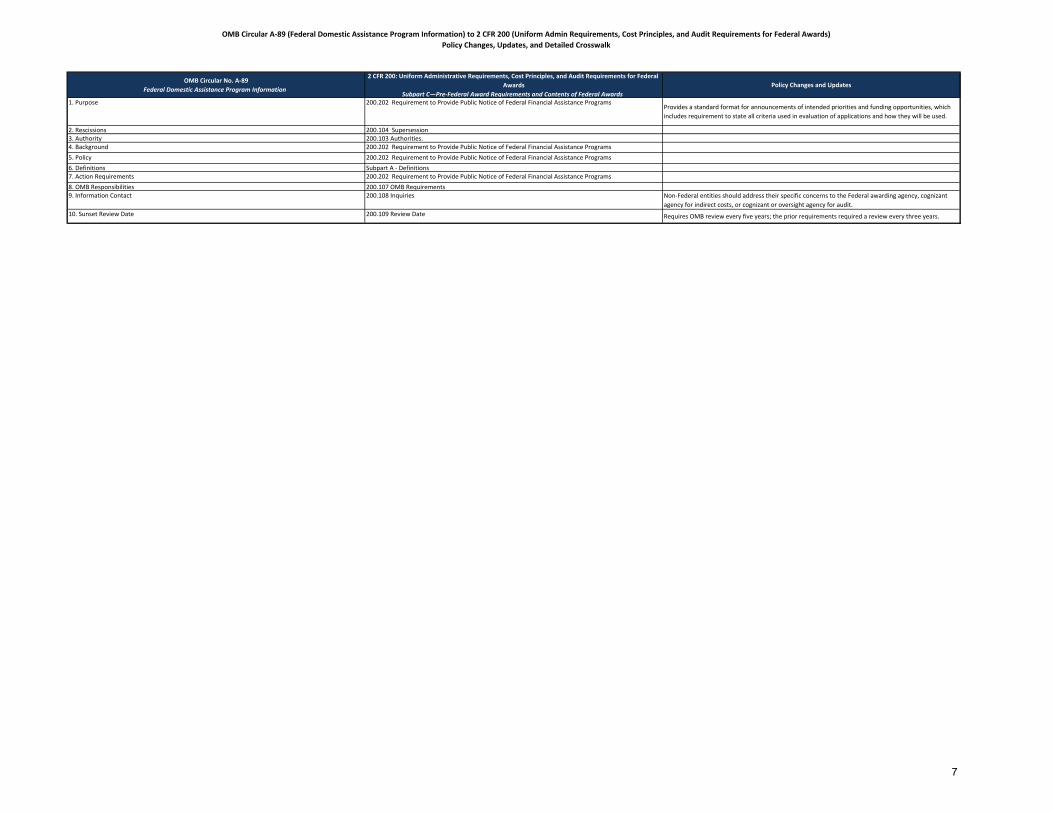

OMB Circular A-89 (Federal Domestic Assistance Program Information) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

OMB Circular No. A-89

Federal Domestic Assistance Program Information

2 CFR 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal

Awards

Subpart C—Pre-Federal Award Requirements and Contents of Federal Awards

Policy Changes and Updates

1. Purpose 200.202 Requirement to Provide Public Notice of Federal Financial Assistance ProgramsProvides a standard format for announcements of intended priorities and funding opportunities, which

includes requirement to state all criteria used in evaluation of applications and how they will be used.

2. Rescissions 200.104 Supersession

3. Authority 200.103 Authorities.

4. Background 200.202 Requirement to Provide Public Notice of Federal Financial Assistance Programs

5. Policy 200.202 Requirement to Provide Public Notice of Federal Financial Assistance Programs

6. Definitions Subpart A - Definitions

7. Action Requirements 200.202 Requirement to Provide Public Notice of Federal Financial Assistance Programs

8. OMB Responsibilities 200.107 OMB Requirements

9. Information Contact 200.108 Inquiries Non-Federal entities should address their specific concerns to the Federal awarding agency, cognizant

agency for indirect costs, or cognizant or oversight agency for audit.

10. Sunset Review Date 200.109 Review Date Requires OMB review every five years; the prior requirements required a review every three years.

7

OMB Circular A-102 (Grants and Cooperative Agreements with State and Local Governments) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

OMB Circular No. A-102*

Grants and Cooperative Agreements with State and Local Governments

2 CFR 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal

Awards

Subpart C—Pre-Federal Award Requirements and Contents of Federal Awards and Subpart D—Post

Federal Award Requirements

Policy Changes and Updates

Subpart A - General Subpart B - General Provisions

.1 Purpose and Scope 200.100 Purpose

.2 Scope of subpart

.3 Definitions Subpart A - Definitions

.4 Applicability 200.101 Applicability

.5 Effect on Other Issuances 200.105 Effect on Other Issuances

.6 Additions and Exceptions 200.102 Exceptions

Subpart B - Pre-Award Requirements Subpart C - Pre-Federal Award Requirements and Contents of Federal Awards

.10 Forms for Applying for Grants 200.206 Standard Application Requirements

Requires Federal awarding agencies to consistently use OMB-approved standard information collections

in their management of Federal awards.

.11 State Plans Appendix I Full Text of Notice of Funding Opportunity

.12 Special Grant or Subgrant Conditions for "High Risk" Grantees 200.205 Federal Awarding Agency Review of Risk Posed by Applicants

Requires Federal awarding agencies to evaluate the merit and risks associated with potential Federal

awards and to impose specific conditions when necessary to mitigate potential risks of waste, fraud, and

abuse before the money is spent.

Subpart C - Post-Award Requirements Subpart D - Post Federal Award Requirements

Financial Administration Standards for Financial and Program Management

.20 Standards for Financial Management Systems 200.302 Financial Management

.21 Payment 200.305 Payment

Clarifies the meaning of project costs and extends to non-Federal entities the flexibility to pay interest

earned on Federal funds annually to the agency, rather than “promptly” to each Federal awarding

agency.

.22 Allowable Costs 200.401 Application

.23 Period of Availability of Funds 200.309 Period of Performance

.24 Matching or Cost Sharing 200.306 Cost Sharing or Matching

Clarifies policies on voluntary committed cost sharing to ensure that such cost sharing is only solicited for

research proposals (when required by regulation) and is transparent in the notice of funding

opportunities.

.25 Program Income 200.307 Program Income

.26 Non-Federal Audit

Changes, Property, and Subawards Property Standards

.30 Changes 200.308 Revision of Budget and Program Plans

.31 Real Property 200.311 Real Property

When title is retained, Non-Federal entities can use net proceeds of disposition as an offset to the cost of

replacement property. When selling property and compensating the Federal awarding agency, if the

award has not been closed out, the net proceeds from sale may be offset against the original cost of the

property.

.32 Equipment 200.313 Equipment

.33 Supplies 200.314 Supplies

.34 Copyrights 200.315 Intangible Property

.35 Subawards to Debarred and Suspended Parties 200.205 Federal Awarding Agency Review of Risk Posed by Applicants

Procurement Standards

.36 Procurement

a) States 200.317 Procurement by States

b) Procurement Standards 200.318 General Procurement

The non-Federal entity may use time and material type contracts only after a determination that no

other type of contract is suitable and if the contract includes a ceiling price.

c) Competition 200.319 Competition

d) Methods of Procurement to be Followed 200.320 Methods of Procurement to be Followed

e) Contracting with Small and Minority Firms, Women's Business Enterprise and Labor Surplus Area Firms

200.321 Contracting with Small and Minority Business, Women's Business Enterprises, and Labor Surplus

Area Firms

f) Contract Cost and Price 200.323 Contract Cost and Price

Non-Federal entities must negotiate profit as a separate element of the price for each contract. Cost plus

and percentage of construction cost methods cannot be used.

g) Awarding Agency Review 200.324 Federal Awarding Agency or Pass-Through Entity Review

Changes the threshold for a procurement review from the Small Purchase Threshold to the Simplified

Acquisition Threshold.

h) Bonding Requirements 200.325 Bonding RequirementsChanges the threshold for bonding requirements from $100,000 to the Simplified Acquisition Threshold.

i) Contract Provisions 200.326 Contract Provisions

.37 Subgrants

200.330 Subrecipient and Contractor Determinations

200.331 Requirements for Pass-Through Entities

200.332 Fixed Amount Subawards

Requires pass-through entities to honor the indirect cost rates negotiated at the Federal level, negotiate

a rate in accordance with Federal guidelines, or provide the minimum flat rate.

A pass-through entity may provide subawards based on fixed amounts up to the Simplified Acquisition

Threshold.

Reports, Record Retention, and Enforcement Performance and Financial Monitoring and Reporting

.40 Monitoring and Reporting Program Performance 200.328 Monitoring and Reporting Performance

.41 Financial Reporting 200.327 Financial Reporting

Record Retention and Access

.42 Retention and Access Requirements for Records 200.333 Record Retention and Access Adds language for record retention policies for program income transactions.

Remedies for Non-Compliance

.43 Enforcement 200.338 Remedies for Non-compliance

.44 Termination 200.339 Termination

Subpart D - After-the-Grant Requirements Subpart D - Post Federal Award Requirements

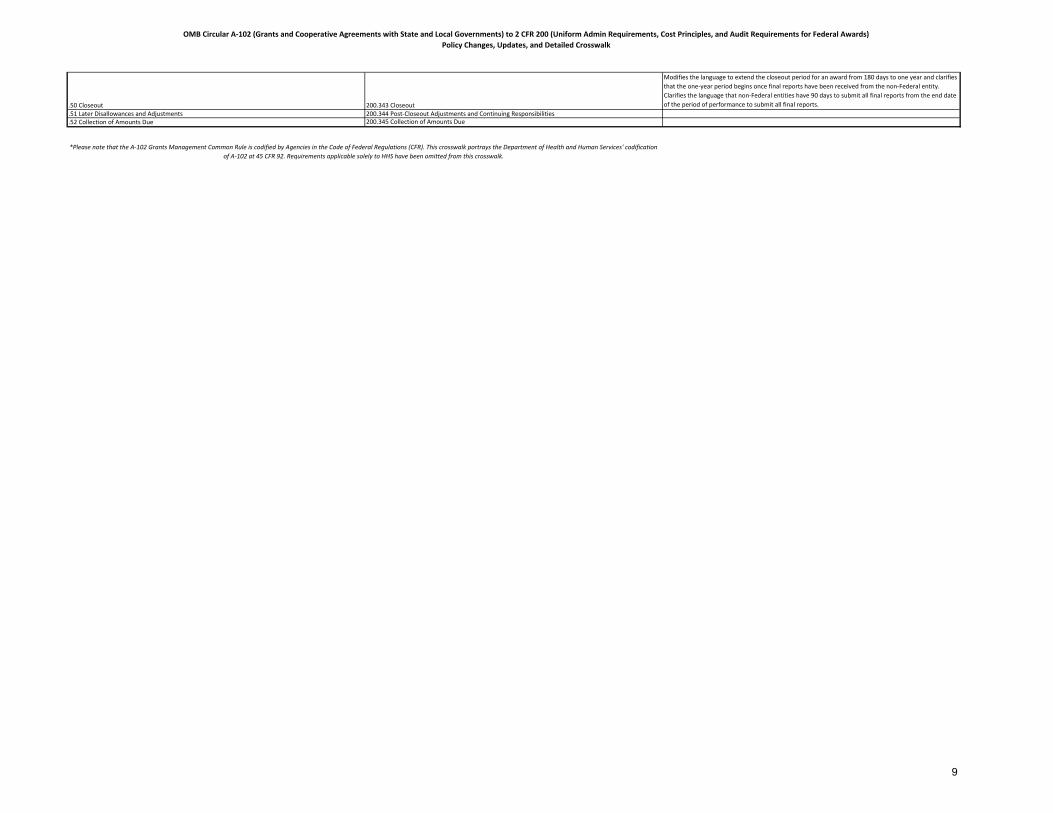

8

OMB Circular A-102 (Grants and Cooperative Agreements with State and Local Governments) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

.50 Closeout 200.343 Closeout

Modifies the language to extend the closeout period for an award from 180 days to one year and clarifies

that the one-year period begins once final reports have been received from the non-Federal entity.

Clarifies the language that non-Federal entities have 90 days to submit all final reports from the end date

of the period of performance to submit all final reports.

.51 Later Disallowances and Adjustments 200.344 Post-Closeout Adjustments and Continuing Responsibilities

.52 Collection of Amounts Due 200.345 Collection of Amounts Due

*Please note that the A-102 Grants Management Common Rule is codified by Agencies in the Code of Federal Regulations (CFR). This crosswalk portrays the Department of Health and Human Services' codification

of A-102 at 45 CFR 92. Requirements applicable solely to HHS have been omitted from this crosswalk.

9

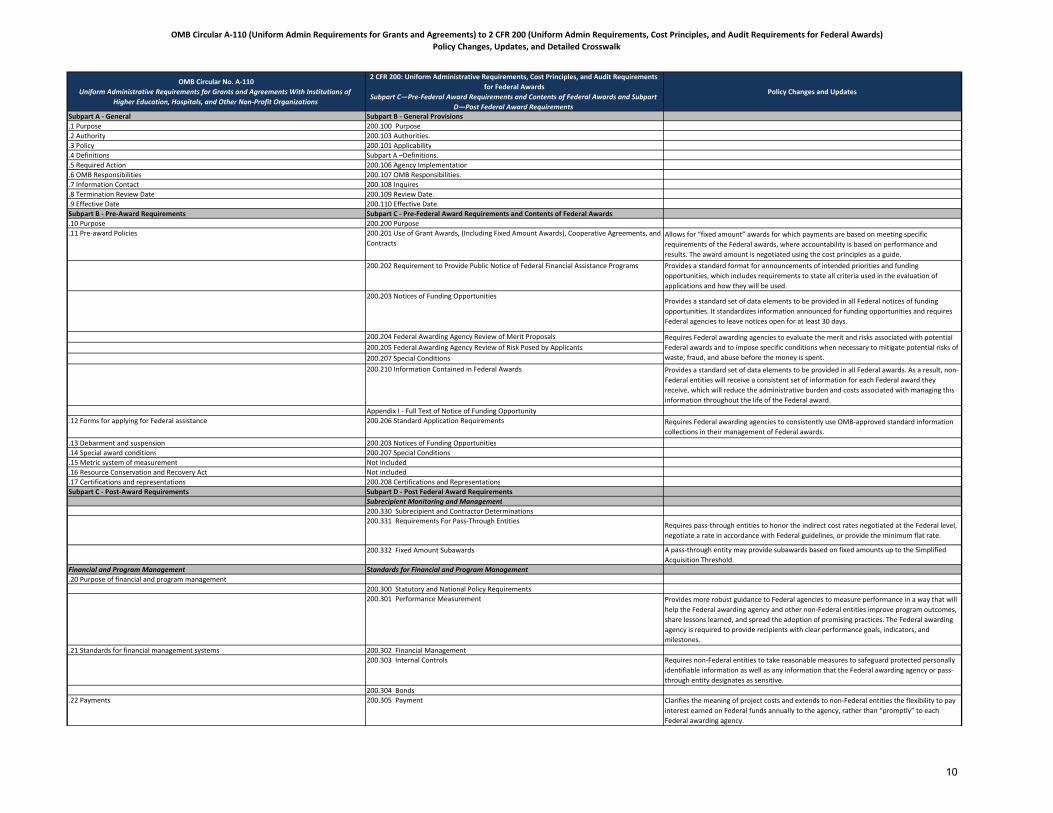

OMB Circular A-110 (Uniform Admin Requirements for Grants and Agreements) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

OMB Circular No. A-110

Uniform Administrative Requirements for Grants and Agreements With Institutions of

Higher Education, Hospitals, and Other Non-Profit Organizations

2 CFR 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

for Federal Awards

Subpart C—Pre-Federal Award Requirements and Contents of Federal Awards and Subpart

D—Post Federal Award Requirements

Policy Changes and Updates

Subpart A - General Subpart B - General Provisions

.1 Purpose 200.100 Purpose

.2 Authority 200.103 Authorities.

.3 Policy 200.101 Applicability

.4 Definitions Subpart A –Definitions.

.5 Required Action 200.106 Agency Implementation

.6 OMB Responsibilities 200.107 OMB Responsibilities.

.7 Information Contact 200.108 Inquires

.8 Termination Review Date 200.109 Review Date.

.9 Effective Date 200.110 Effective Date.

Subpart B - Pre-Award Requirements Subpart C - Pre-Federal Award Requirements and Contents of Federal Awards

.10 Purpose 200.200 Purpose

.11 Pre-award Policies 200.201 Use of Grant Awards, (Including Fixed Amount Awards), Cooperative Agreements, and

Contracts

Allows for “fixed amount” awards for which payments are based on meeting specific

requirements of the Federal awards, where accountability is based on performance and

results. The award amount is negotiated using the cost principles as a guide.

200.202 Requirement to Provide Public Notice of Federal Financial Assistance Programs Provides a standard format for announcements of intended priorities and funding

opportunities, which includes requirements to state all criteria used in the evaluation of

applications and how they will be used.

200.203 Notices of Funding OpportunitiesProvides a standard set of data elements to be provided in all Federal notices of funding

opportunities. It standardizes information announced for funding opportunities and requires

Federal agencies to leave notices open for at least 30 days.

200.204 Federal Awarding Agency Review of Merit Proposals

200.205 Federal Awarding Agency Review of Risk Posed by Applicants

200.207 Special Conditions

200.210 Information Contained in Federal Awards Provides a standard set of data elements to be provided in all Federal awards. As a result, non-

Federal entities will receive a consistent set of information for each Federal award they

receive, which will reduce the administrative burden and costs associated with managing this

information throughout the life of the Federal award.

Appendix I - Full Text of Notice of Funding Opportunity

.12 Forms for applying for Federal assistance 200.206 Standard Application Requirements Requires Federal awarding agencies to consistently use OMB-approved standard information

collections in their management of Federal awards.

.13 Debarment and suspension 200.203 Notices of Funding Opportunities

.14 Special award conditions 200.207 Special Conditions

.15 Metric system of measurement Not included

.16 Resource Conservation and Recovery Act Not included

.17 Certifications and representations 200.208 Certifications and Representations

Subpart C - Post-Award Requirements Subpart D - Post Federal Award Requirements

Subrecipient Monitoring and Management

200.330 Subrecipient and Contractor Determinations

200.331 Requirements For Pass-Through EntitiesRequires pass-through entities to honor the indirect cost rates negotiated at the Federal level,

negotiate a rate in accordance with Federal guidelines, or provide the minimum flat rate.

200.332 Fixed Amount Subawards A pass-through entity may provide subawards based on fixed amounts up to the Simplified

Acquisition Threshold.

Financial and Program Management Standards for Financial and Program Management

.20 Purpose of financial and program management

200.300 Statutory and National Policy Requirements

200.301 Performance Measurement Provides more robust guidance to Federal agencies to measure performance in a way that will

help the Federal awarding agency and other non-Federal entities improve program outcomes,

share lessons learned, and spread the adoption of promising practices. The Federal awarding

agency is required to provide recipients with clear performance goals, indicators, and

milestones.

.21 Standards for financial management systems 200.302 Financial Management

200.303 Internal Controls Requires non-Federal entities to take reasonable measures to safeguard protected personally

identifiable information as well as any information that the Federal awarding agency or pass-

through entity designates as sensitive.

200.304 Bonds

.22 Payments 200.305 Payment Clarifies the meaning of project costs and extends to non-Federal entities the flexibility to pay

interest earned on Federal funds annually to the agency, rather than “promptly” to each

Federal awarding agency.

Requires Federal awarding agencies to evaluate the merit and risks associated with potential

Federal awards and to impose specific conditions when necessary to mitigate potential risks of

waste, fraud, and abuse before the money is spent.

10

OMB Circular A-110 (Uniform Admin Requirements for Grants and Agreements) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

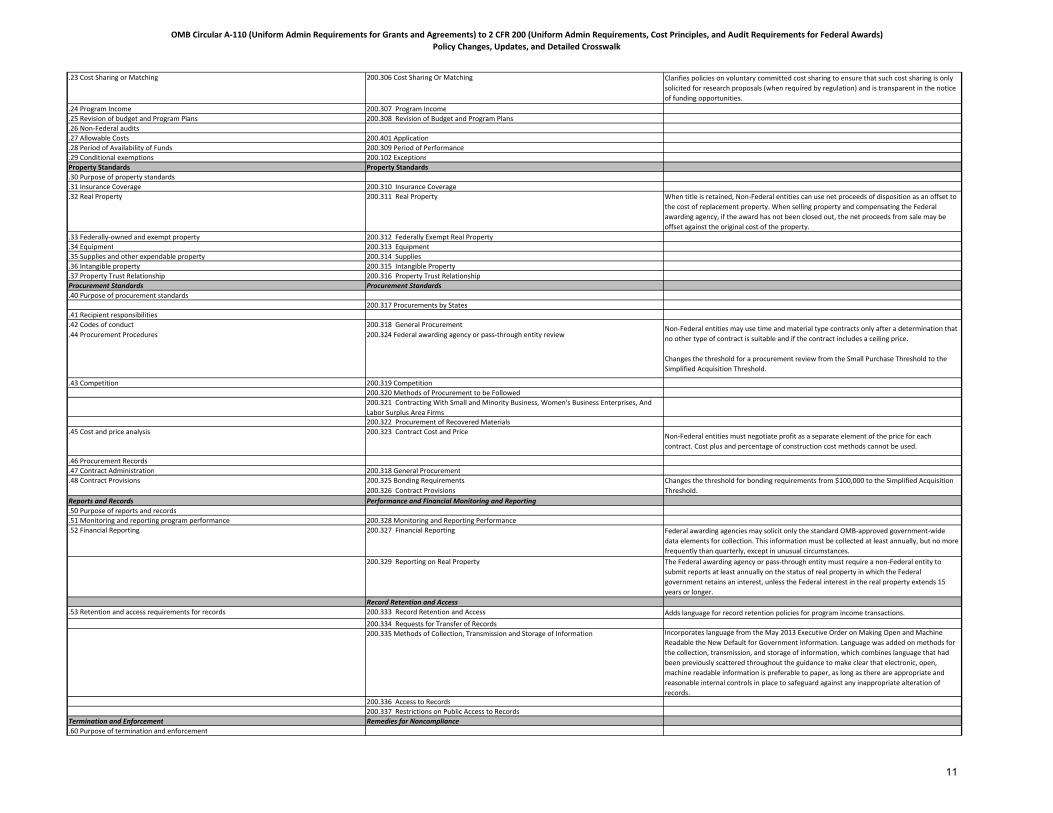

.23 Cost Sharing or Matching 200.306 Cost Sharing Or Matching Clarifies policies on voluntary committed cost sharing to ensure that such cost sharing is only

solicited for research proposals (when required by regulation) and is transparent in the notice

of funding opportunities.

.24 Program Income 200.307 Program Income

.25 Revision of budget and Program Plans 200.308 Revision of Budget and Program Plans

.26 Non-Federal audits

.27 Allowable Costs 200.401 Application

.28 Period of Availability of Funds 200.309 Period of Performance

.29 Conditional exemptions 200.102 Exceptions

Property Standards Property Standards

.30 Purpose of property standards

.31 Insurance Coverage 200.310 Insurance Coverage

.32 Real Property 200.311 Real Property When title is retained, Non-Federal entities can use net proceeds of disposition as an offset to

the cost of replacement property. When selling property and compensating the Federal

awarding agency, if the award has not been closed out, the net proceeds from sale may be

offset against the original cost of the property.

.33 Federally-owned and exempt property 200.312 Federally Exempt Real Property

.34 Equipment 200.313 Equipment

.35 Supplies and other expendable property 200.314 Supplies

.36 Intangible property 200.315 Intangible Property

.37 Property Trust Relationship 200.316 Property Trust Relationship

Procurement Standards Procurement Standards

.40 Purpose of procurement standards

200.317 Procurements by States

.41 Recipient responsibilities

.42 Codes of conduct

.44 Procurement Procedures

200.318 General Procurement

200.324 Federal awarding agency or pass-through entity reviewNon-Federal entities may use time and material type contracts only after a determination that

no other type of contract is suitable and if the contract includes a ceiling price.

Changes the threshold for a procurement review from the Small Purchase Threshold to the

Simplified Acquisition Threshold.

.43 Competition 200.319 Competition

200.320 Methods of Procurement to be Followed

200.321 Contracting With Small and Minority Business, Women's Business Enterprises, And

Labor Surplus Area Firms

200.322 Procurement of Recovered Materials

.45 Cost and price analysis 200.323 Contract Cost and PriceNon-Federal entities must negotiate profit as a separate element of the price for each

contract. Cost plus and percentage of construction cost methods cannot be used.

.46 Procurement Records

.47 Contract Administration 200.318 General Procurement

.48 Contract Provisions 200.325 Bonding Requirements

200.326 Contract Provisions

Changes the threshold for bonding requirements from $100,000 to the Simplified Acquisition

Threshold.

Reports and Records Performance and Financial Monitoring and Reporting

.50 Purpose of reports and records

.51 Monitoring and reporting program performance 200.328 Monitoring and Reporting Performance

.52 Financial Reporting 200.327 Financial Reporting Federal awarding agencies may solicit only the standard OMB-approved government-wide

data elements for collection. This information must be collected at least annually, but no more

frequently than quarterly, except in unusual circumstances.

200.329 Reporting on Real Property The Federal awarding agency or pass-through entity must require a non-Federal entity to

submit reports at least annually on the status of real property in which the Federal

government retains an interest, unless the Federal interest in the real property extends 15

years or longer.

Record Retention and Access

.53 Retention and access requirements for records 200.333 Record Retention and Access Adds language for record retention policies for program income transactions.

200.334 Requests for Transfer of Records

200.335 Methods of Collection, Transmission and Storage of Information Incorporates language from the May 2013 Executive Order on Making Open and Machine

Readable the New Default for Government Information. Language was added on methods for

the collection, transmission, and storage of information, which combines language that had

been previously scattered throughout the guidance to make clear that electronic, open,

machine readable information is preferable to paper, as long as there are appropriate and

reasonable internal controls in place to safeguard against any inappropriate alteration of

records.

200.336 Access to Records

200.337 Restrictions on Public Access to Records

Termination and Enforcement Remedies for Noncompliance

.60 Purpose of termination and enforcement

11

OMB Circular A-110 (Uniform Admin Requirements for Grants and Agreements) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

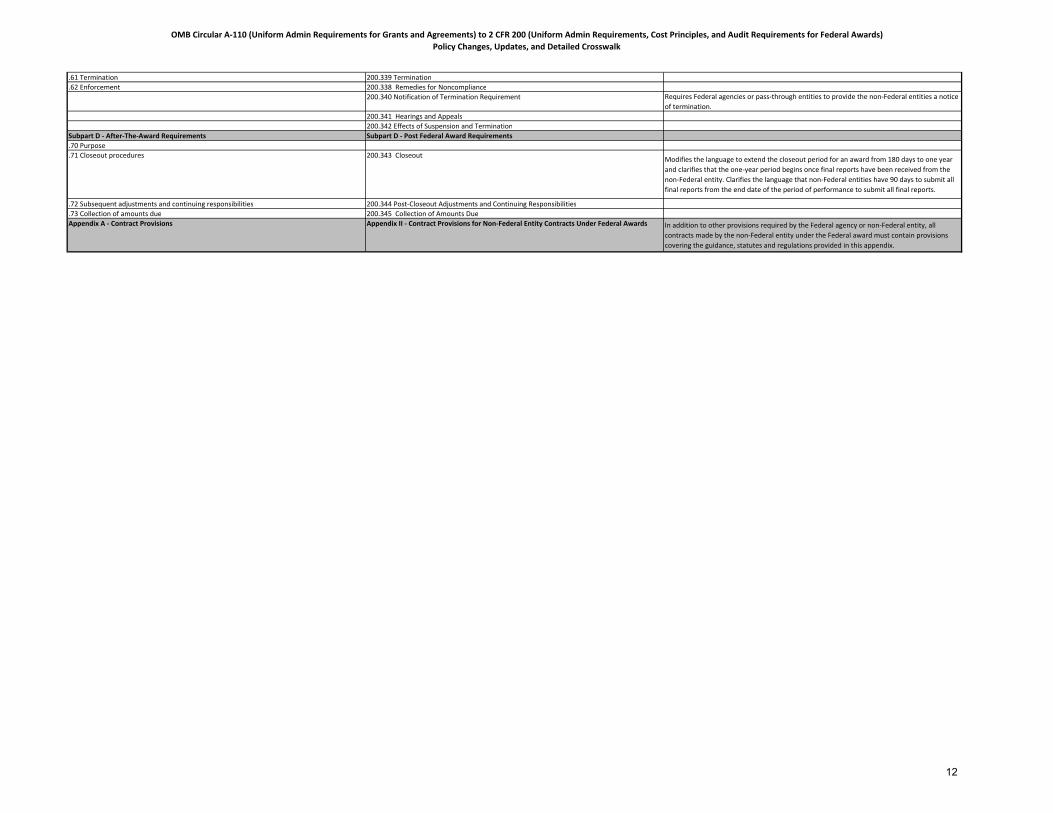

.61 Termination 200.339 Termination

.62 Enforcement 200.338 Remedies for Noncompliance

200.340 Notification of Termination Requirement Requires Federal agencies or pass-through entities to provide the non-Federal entities a notice

of termination.

200.341 Hearings and Appeals

200.342 Effects of Suspension and Termination

Subpart D - After-The-Award Requirements Subpart D - Post Federal Award Requirements

.70 Purpose

.71 Closeout procedures 200.343 CloseoutModifies the language to extend the closeout period for an award from 180 days to one year

and clarifies that the one-year period begins once final reports have been received from the

non-Federal entity. Clarifies the language that non-Federal entities have 90 days to submit all

final reports from the end date of the period of performance to submit all final reports.

.72 Subsequent adjustments and continuing responsibilities 200.344 Post-Closeout Adjustments and Continuing Responsibilities

.73 Collection of amounts due 200.345 Collection of Amounts Due

Appendix A - Contract Provisions Appendix II - Contract Provisions for Non-Federal Entity Contracts Under Federal Awards In addition to other provisions required by the Federal agency or non-Federal entity, all

contracts made by the non-Federal entity under the Federal award must contain provisions

covering the guidance, statutes and regulations provided in this appendix.

12

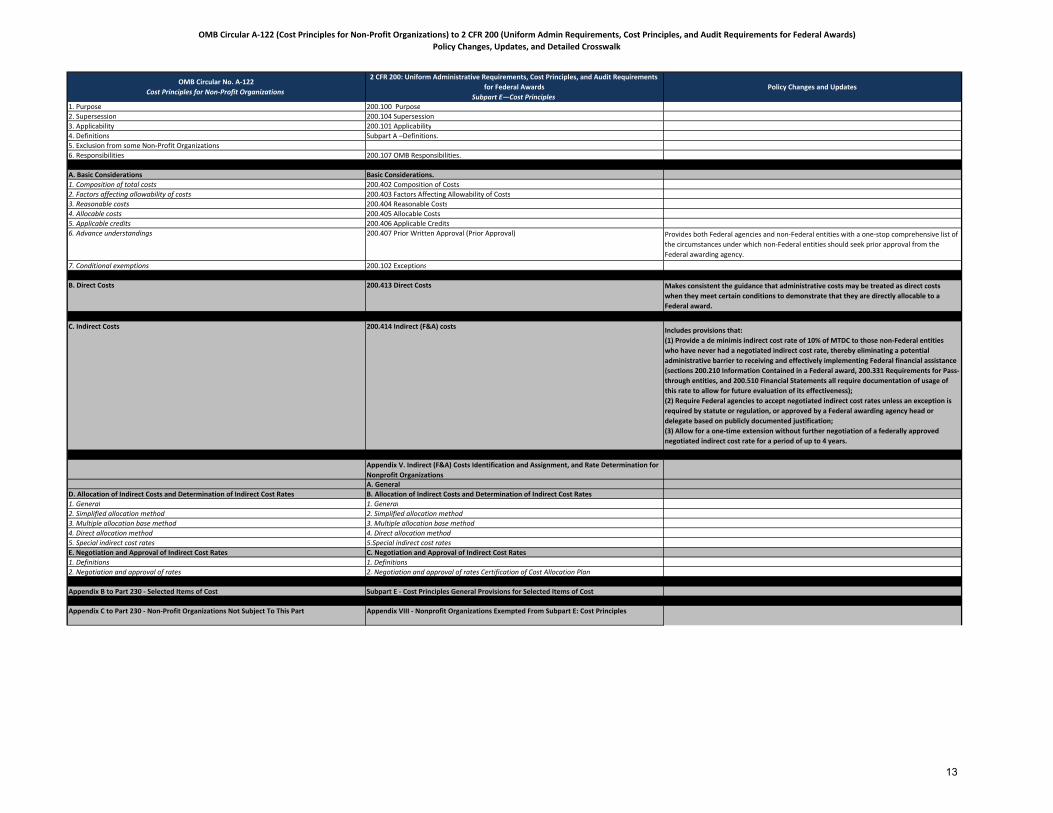

OMB Circular A-122 (Cost Principles for Non-Profit Organizations) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

OMB Circular No. A-122

Cost Principles for Non-Profit Organizations

2 CFR 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

for Federal Awards

Subpart E—Cost Principles

Policy Changes and Updates

1. Purpose 200.100 Purpose

2. Supersession 200.104 Supersession

3. Applicability 200.101 Applicability

4. Definitions Subpart A –Definitions.

5. Exclusion from some Non-Profit Organizations

6. Responsibilities 200.107 OMB Responsibilities.

A. Basic Considerations Basic Considerations.

1. Composition of total costs 200.402 Composition of Costs

2. Factors affecting allowability of costs 200.403 Factors Affecting Allowability of Costs

3. Reasonable costs 200.404 Reasonable Costs

4. Allocable costs 200.405 Allocable Costs

5. Applicable credits 200.406 Applicable Credits

6. Advance understandings 200.407 Prior Written Approval (Prior Approval) Provides both Federal agencies and non-Federal entities with a one-stop comprehensive list of

the circumstances under which non-Federal entities should seek prior approval from the

Federal awarding agency.

7. Conditional exemptions 200.102 Exceptions

B. Direct Costs 200.413 Direct Costs Makes consistent the guidance that administrative costs may be treated as direct costs

when they meet certain conditions to demonstrate that they are directly allocable to a

Federal award.

C. Indirect Costs 200.414 Indirect (F&A) costsIncludes provisions that:

(1) Provide a de minimis indirect cost rate of 10% of MTDC to those non-Federal entities

who have never had a negotiated indirect cost rate, thereby eliminating a potential

administrative barrier to receiving and effectively implementing Federal financial assistance

(sections 200.210 Information Contained in a Federal award, 200.331 Requirements for Pass-

through entities, and 200.510 Financial Statements all require documentation of usage of

this rate to allow for future evaluation of its effectiveness);

(2) Require Federal agencies to accept negotiated indirect cost rates unless an exception is

required by statute or regulation, or approved by a Federal awarding agency head or

delegate based on publicly documented justification;

(3) Allow for a one-time extension without further negotiation of a federally approved

negotiated indirect cost rate for a period of up to 4 years.

Appendix V. Indirect (F&A) Costs Identification and Assignment, and Rate Determination for

Nonprofit Organizations

A. General

D. Allocation of Indirect Costs and Determination of Indirect Cost Rates B. Allocation of Indirect Costs and Determination of Indirect Cost Rates

1. General 1. General

2. Simplified allocation method 2. Simplified allocation method

3. Multiple allocation base method 3. Multiple allocation base method

4. Direct allocation method 4. Direct allocation method

5. Special indirect cost rates 5.Special indirect cost rates

E. Negotiation and Approval of Indirect Cost Rates C. Negotiation and Approval of Indirect Cost Rates

1. Definitions 1. Definitions

2. Negotiation and approval of rates 2. Negotiation and approval of rates Certification of Cost Allocation Plan

Appendix B to Part 230 - Selected Items of Cost Subpart E - Cost Principles General Provisions for Selected Items of Cost

Appendix C to Part 230 - Non-Profit Organizations Not Subject To This Part Appendix VIII - Nonprofit Organizations Exempted From Subpart E: Cost Principles

13

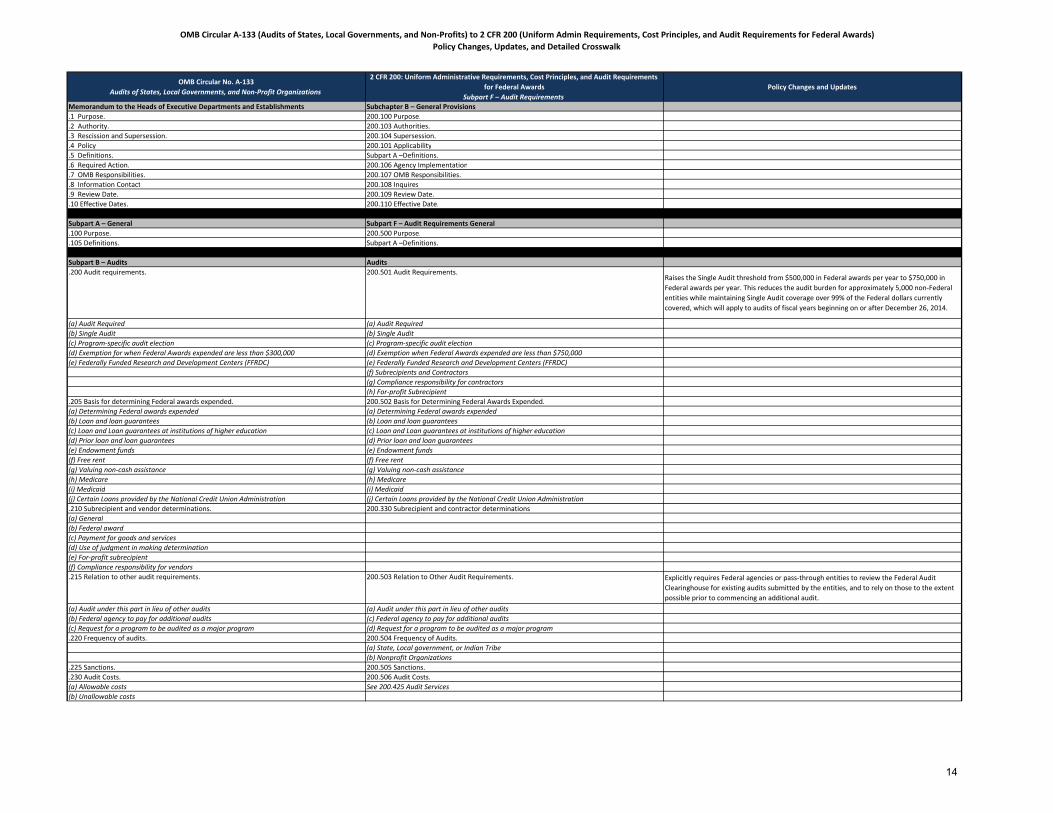

OMB Circular A-133 (Audits of States, Local Governments, and Non-Profits) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

OMB Circular No. A-133

Audits of States, Local Governments, and Non-Profit Organizations

2 CFR 200: Uniform Administrative Requirements, Cost Principles, and Audit Requirements

for Federal Awards

Subpart F – Audit Requirements

Policy Changes and Updates

Memorandum to the Heads of Executive Departments and Establishments Subchapter B – General Provisions

.1 Purpose. 200.100 Purpose.

.2 Authority. 200.103 Authorities.

.3 Rescission and Supersession. 200.104 Supersession.

.4 Policy 200.101 Applicability

.5 Definitions. Subpart A –Definitions.

.6 Required Action. 200.106 Agency Implementation

.7 OMB Responsibilities. 200.107 OMB Responsibilities.

.8 Information Contact 200.108 Inquires

.9 Review Date. 200.109 Review Date.

.10 Effective Dates. 200.110 Effective Date.

Subpart A – General Subpart F – Audit Requirements General

.100 Purpose. 200.500 Purpose.

.105 Definitions. Subpart A –Definitions.

Subpart B – Audits Audits

.200 Audit requirements. 200.501 Audit Requirements.Raises the Single Audit threshold from $500,000 in Federal awards per year to $750,000 in

Federal awards per year. This reduces the audit burden for approximately 5,000 non-Federal

entities while maintaining Single Audit coverage over 99% of the Federal dollars currently

covered, which will apply to audits of fiscal years beginning on or after December 26, 2014.

(a) Audit Required (a) Audit Required

(b) Single Audit (b) Single Audit

(c) Program-specific audit election (c) Program-specific audit election

(d) Exemption for when Federal Awards expended are less than $300,000 (d) Exemption when Federal Awards expended are less than $750,000

(e) Federally Funded Research and Development Centers (FFRDC) (e) Federally Funded Research and Development Centers (FFRDC)

(f) Subrecipients and Contractors

(g) Compliance responsibility for contractors

(h) For-profit Subrecipient

.205 Basis for determining Federal awards expended. 200.502 Basis for Determining Federal Awards Expended.

(a) Determining Federal awards expended (a) Determining Federal awards expended

(b) Loan and loan guarantees (b) Loan and loan guarantees

(c) Loan and Loan guarantees at institutions of higher education (c) Loan and Loan guarantees at institutions of higher education

(d) Prior loan and loan guarantees (d) Prior loan and loan guarantees

(e) Endowment funds (e) Endowment funds

(f) Free rent (f) Free rent

(g) Valuing non-cash assistance (g) Valuing non-cash assistance

(h) Medicare (h) Medicare

(i) Medicaid (i) Medicaid

(j) Certain Loans provided by the National Credit Union Administration (j) Certain Loans provided by the National Credit Union Administration

.210 Subrecipient and vendor determinations. 200.330 Subrecipient and contractor determinations

(a) General

(b) Federal award

(c) Payment for goods and services

(d) Use of judgment in making determination

(e) For-profit subrecipient

(f) Compliance responsibility for vendors

.215 Relation to other audit requirements. 200.503 Relation to Other Audit Requirements. Explicitly requires Federal agencies or pass-through entities to review the Federal Audit

Clearinghouse for existing audits submitted by the entities, and to rely on those to the extent

possible prior to commencing an additional audit.

(a) Audit under this part in lieu of other audits (a) Audit under this part in lieu of other audits

(b) Federal agency to pay for additional audits (c) Federal agency to pay for additional audits

(c) Request for a program to be audited as a major program (d) Request for a program to be audited as a major program

.220 Frequency of audits. 200.504 Frequency of Audits.

(a) State, Local government, or Indian Tribe

(b) Nonprofit Organizations

.225 Sanctions. 200.505 Sanctions.

.230 Audit Costs. 200.506 Audit Costs.

(a) Allowable costs See 200.425 Audit Services

(b) Unallowable costs

14

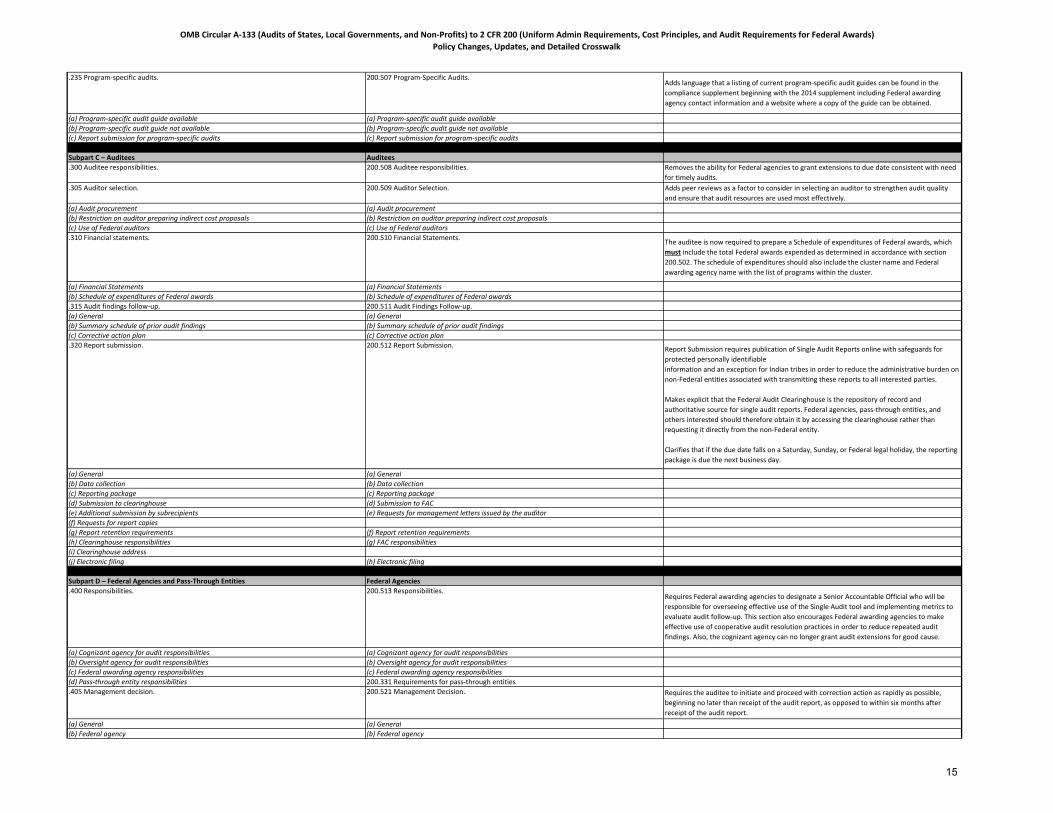

OMB Circular A-133 (Audits of States, Local Governments, and Non-Profits) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

.235 Program-specific audits. 200.507 Program-Specific Audits.Adds language that a listing of current program-specific audit guides can be found in the

compliance supplement beginning with the 2014 supplement including Federal awarding

agency contact information and a website where a copy of the guide can be obtained.

(a) Program-specific audit guide available (a) Program-specific audit guide available

(b) Program-specific audit guide not available (b) Program-specific audit guide not available

(c) Report submission for program-specific audits (c) Report submission for program-specific audits

Subpart C – Auditees Auditees

.300 Auditee responsibilities. 200.508 Auditee responsibilities. Removes the ability for Federal agencies to grant extensions to due date consistent with need

for timely audits.

.305 Auditor selection. 200.509 Auditor Selection. Adds peer reviews as a factor to consider in selecting an auditor to strengthen audit quality

and ensure that audit resources are used most effectively.

(a) Audit procurement (a) Audit procurement

(b) Restriction on auditor preparing indirect cost proposals (b) Restriction on auditor preparing indirect cost proposals

(c) Use of Federal auditors (c) Use of Federal auditors

.310 Financial statements. 200.510 Financial Statements.The auditee is now required to prepare a Schedule of expenditures of Federal awards, which

must include the total Federal awards expended as determined in accordance with section

200.502. The schedule of expenditures should also include the cluster name and Federal

awarding agency name with the list of programs within the cluster.

(a) Financial Statements (a) Financial Statements

(b) Schedule of expenditures of Federal awards (b) Schedule of expenditures of Federal awards

.315 Audit findings follow-up. 200.511 Audit Findings Follow-up.

(a) General (a) General

(b) Summary schedule of prior audit findings (b) Summary schedule of prior audit findings

(c) Corrective action plan (c) Corrective action plan

.320 Report submission. 200.512 Report Submission.Report Submission requires publication of Single Audit Reports online with safeguards for

protected personally identifiable

information and an exception for Indian tribes in order to reduce the administrative burden on

non-Federal entities associated with transmitting these reports to all interested parties.

Makes explicit that the Federal Audit Clearinghouse is the repository of record and

authoritative source for single audit reports. Federal agencies, pass-through entities, and

others interested should therefore obtain it by accessing the clearinghouse rather than

requesting it directly from the non-Federal entity.

Clarifies that if the due date falls on a Saturday, Sunday, or Federal legal holiday, the reporting

package is due the next business day.

(a) General (a) General

(b) Data collection (b) Data collection

(c) Reporting package (c) Reporting package

(d) Submission to clearinghouse (d) Submission to FAC

(e) Additional submission by subrecipients (e) Requests for management letters issued by the auditor

(f) Requests for report copies

(g) Report retention requirements (f) Report retention requirements

(h) Clearinghouse responsibilities (g) FAC responsibilities

(i) Clearinghouse address

(j) Electronic filing (h) Electronic filing

Subpart D – Federal Agencies and Pass-Through Entities Federal Agencies

.400 Responsibilities. 200.513 Responsibilities.Requires Federal awarding agencies to designate a Senior Accountable Official who will be

responsible for overseeing effective use of the Single Audit tool and implementing metrics to

evaluate audit follow-up. This section also encourages Federal awarding agencies to make

effective use of cooperative audit resolution practices in order to reduce repeated audit

findings. Also, the cognizant agency can no longer grant audit extensions for good cause.

(a) Cognizant agency for audit responsibilities (a) Cognizant agency for audit responsibilities

(b) Oversight agency for audit responsibilities (b) Oversight agency for audit responsibilities

(c) Federal awarding agency responsibilities (c) Federal awarding agency responsibilities

(d) Pass-through entity responsibilities 200.331 Requirements for pass-through entities

.405 Management decision. 200.521 Management Decision. Requires the auditee to initiate and proceed with correction action as rapidly as possible,

beginning no later than receipt of the audit report, as opposed to within six months after

receipt of the audit report.

(a) General (a) General

(b) Federal agency (b) Federal agency

15

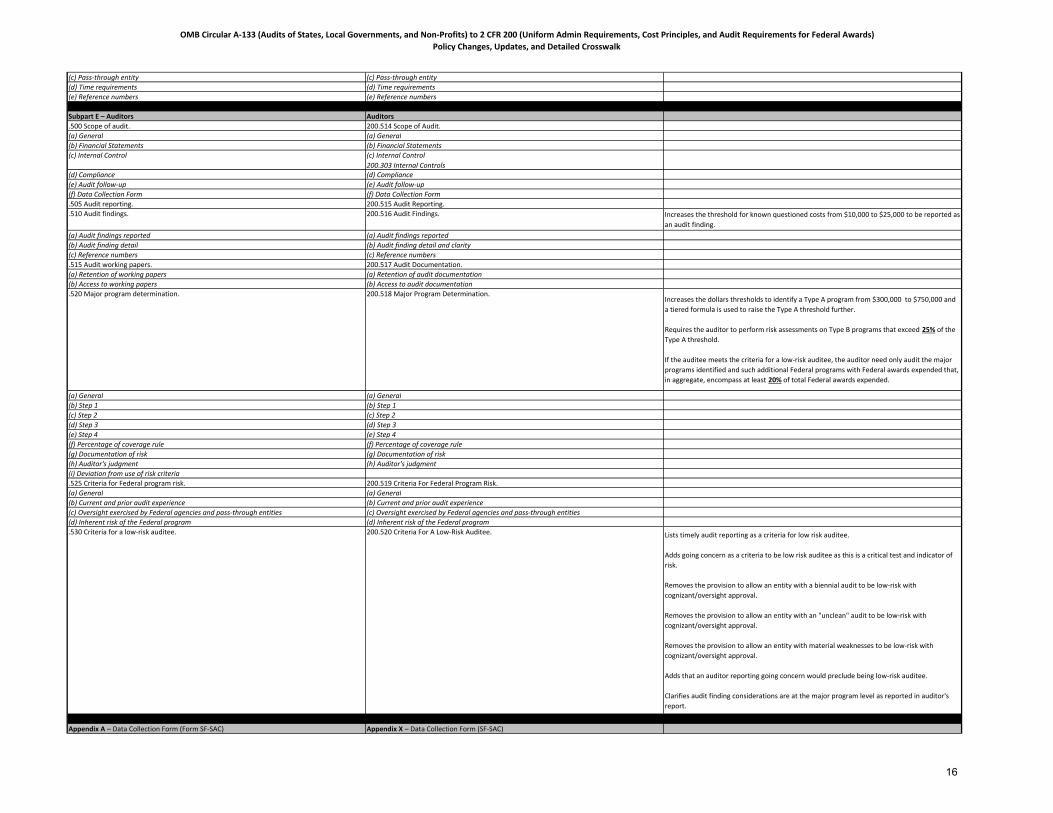

OMB Circular A-133 (Audits of States, Local Governments, and Non-Profits) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

(c) Pass-through entity (c) Pass-through entity

(d) Time requirements (d) Time requirements

(e) Reference numbers (e) Reference numbers

Subpart E – Auditors Auditors

.500 Scope of audit. 200.514 Scope of Audit.

(a) General (a) General

(b) Financial Statements (b) Financial Statements

(c) Internal Control (c) Internal Control

200.303 Internal Controls

(d) Compliance (d) Compliance

(e) Audit follow-up (e) Audit follow-up

(f) Data Collection Form (f) Data Collection Form

.505 Audit reporting. 200.515 Audit Reporting.

.510 Audit findings. 200.516 Audit Findings. Increases the threshold for known questioned costs from $10,000 to $25,000 to be reported as

an audit finding.

(a) Audit findings reported (a) Audit findings reported

(b) Audit finding detail (b) Audit finding detail and clarity

(c) Reference numbers (c) Reference numbers

.515 Audit working papers. 200.517 Audit Documentation.

(a) Retention of working papers (a) Retention of audit documentation

(b) Access to working papers (b) Access to audit documentation

.520 Major program determination. 200.518 Major Program Determination.Increases the dollars thresholds to identify a Type A program from $300,000 to $750,000 and

a tiered formula is used to raise the Type A threshold further.

Requires the auditor to perform risk assessments on Type B programs that exceed 25% of the

Type A threshold.

If the auditee meets the criteria for a low-risk auditee, the auditor need only audit the major

programs identified and such additional Federal programs with Federal awards expended that,

in aggregate, encompass at least 20% of total Federal awards expended.

(a) General (a) General

(b) Step 1 (b) Step 1

(c) Step 2 (c) Step 2

(d) Step 3 (d) Step 3

(e) Step 4 (e) Step 4

(f) Percentage of coverage rule (f) Percentage of coverage rule

(g) Documentation of risk (g) Documentation of risk

(h) Auditor's judgment (h) Auditor's judgment

(i) Deviation from use of risk criteria

.525 Criteria for Federal program risk. 200.519 Criteria For Federal Program Risk.

(a) General (a) General

(b) Current and prior audit experience (b) Current and prior audit experience

(c) Oversight exercised by Federal agencies and pass-through entities (c) Oversight exercised by Federal agencies and pass-through entities

(d) Inherent risk of the Federal program (d) Inherent risk of the Federal program

.530 Criteria for a low-risk auditee. 200.520 Criteria For A Low-Risk Auditee. Lists timely audit reporting as a criteria for low risk auditee.

Adds going concern as a criteria to be low risk auditee as this is a critical test and indicator of

risk.

Removes the provision to allow an entity with a biennial audit to be low-risk with

cognizant/oversight approval.

Removes the provision to allow an entity with an "unclean" audit to be low-risk with

cognizant/oversight approval.

Removes the provision to allow an entity with material weaknesses to be low-risk with

cognizant/oversight approval.

Adds that an auditor reporting going concern would preclude being low-risk auditee.

Clarifies audit finding considerations are at the major program level as reported in auditor's

report.

Appendix A – Data Collection Form (Form SF-SAC) Appendix X – Data Collection Form (SF-SAC)

16

OMB Circular A-133 (Audits of States, Local Governments, and Non-Profits) to 2 CFR 200 (Uniform Admin Requirements, Cost Principles, and Audit Requirements for Federal Awards)

Policy Changes, Updates, and Detailed Crosswalk

Appendix B – Circular A-133 Compliance Supplement Appendix XI – Compliance Supplement

17