Embed Size (px)

DESCRIPTION

T4 - part B – case study report – May 2010

Citation preview

1 © The Chartered Institute of Management Accountants 2010

T4- Part B – Case Study

CeeCee - Retail fashion case – May 2010

REPORT To: Carla Celli, CeeCee CEO From: Management Accountant Date: 27 May 2010

Review of issues facing CeeCee Contents 1.0 Introduction 2.0 Terms of reference 3.0 Prioritisation of the issues facing CeeCee 4.0 Discussion of the issues facing CeeCee 5.0 Ethical issues and recommendations on ethical issues 6.0 Recommendations 7.0 Conclusions Appendices Appendix 1 SWOT analysis Appendix 2 PEST analysis Appendix 3 Financial and ratio analysis Appendix 4 Evaluation of franchising proposal Appendix 5 Evaluation of proposal to open a second distribution centre Appendix 6 Summary for presentation to the CeeCee Board on the proposal to franchise CeeCee shops in Asia 1.0 Introduction CeeCee operates a chain of retail fashion shops in Europe selling ladies’ clothes, men’s clothes, children’s clothes and home furnishings. At the end of December 2009, it had 630 shops in operation and sales of almost €2.8 billion. 2.0 Terms of reference I am the Management Accountant appointed to write a report to the CEO which prioritises, analyses and evaluates the issues facing CeeCee and makes appropriate recommendations.

2 © The Chartered Institute of Management Accountants 2010

I have been asked to prepare a summary of points for presentation to the CeeCee Board on the proposal to franchise CeeCee shops in Asia and this is included in Appendix 6 to this report. 3.0 Prioritisation of the issues facing CeeCee 3.1 Top priority – Proposal to franchise CeeCee shops in Asia The proposal to open franchised shops as part of CeeCee’s expansion into Asia is the top priority as it is a fundamental change to CeeCee’s current business plan, where all shops are managed by CeeCee. This proposal could enable CeeCee to expand into Asia faster and generate higher operating profits than the agreed 5 year plan and therefore will have an impact on shareholders. 3.2 Second priority – Proposal to open a second distribution centre This issue is the second priority as it changes the way in which CeeCee operates in Europe and could enable operational savings to be achieved. If this proposal were to be rejected, then operating costs would increase and this would have an adverse effect on operating profits. However, there are other factors to be considered here, notably that the opening of the proposed second distribution centre could increase inventory by 3 days and could slow up new designs reaching CeeCee’s shops. The CeeCee business model is founded on the fast fashion principle where the speed from drawing board to shop is very important. Therefore there is a dilemma here between cost savings and speed of products to shops. 3.3 Third priority – Proposal to appoint a famous brand name designer This has been placed as the third priority issue as this could generate additional revenues and operating profit over the next 3 years and could attract good publicity and new customers into CeeCee’s shops. 3.4 Fourth priority – Problems with Supplier Y This has been placed a fourth priority as CeeCee is not treating this supplier with respect and goes against its good CSR principles of handling its suppliers. It is unfair to threaten to terminate the contract with Suppler Y simply because it is suffering from IT problems. It should help and support its suppliers. There are also ethical aspects to this issue. Additionally if the contract with Supplier Y is terminated then an additional supplier will need to be appointed, or CeeCee will need to establish whether any of its existing suppliers can increase the volume and range of products to meet the production that Supplier Y is currently manufacturing. 3.5 Other issues The need to reduce carbon emissions is discussed in ethical issues below. A SWOT analysis summarising the strengths, weaknesses, opportunities and threats is shown in Appendix 1. A PEST analysis is shown in Appendix 2.

3 © The Chartered Institute of Management Accountants 2010

Note: It was necessary to rank the franchising proposal in the top 1 or 2 issues in order to gain pass marks in Prioritisation.

4.0 Discussion of the issues facing CeeCee 4.1 Overview CeeCee is forecast to achieve its planned level of profits for 2010, but there is always an ongoing need to identify areas for change that could bring operational efficiencies or that could generate higher profits, therefore increasing shareholder value. There are 3 proposals, which are to franchise, to open a second distribution centre and to appoint a famous designer. These could all increase profitability for CeeCee over the next few years, although they each carry business risks. These proposals are discussed in more detail below. CeeCee’s marketing strategy is to differentiate itself based on Porter’s Generic Strategies, by delivering large ranges of new products. The product life cycle of each product line is short, as CeeCee does not hold inventory for very long. Unlike Marks and Spencer, which holds the same products throughout each season (such as Winter season, where the same products are available from October through to March in European shops), inventory in CeeCee shops is constantly being replaced by new, but similar, product lines. 4.2 – Proposal to franchise CeeCee shops in Asia Juliette Lespere, CeeCee’s Sales and Marketing Director, has proposed that CeeCee should consider franchising to speed up CeeCee’s planned growth in new shops openings in Asia. CeeCee has no experience of managing shops in Asia and this is the company’s first expansion of its business outside of Europe. There is always a need for local knowledge and experience to minimise the risks to the business. CeeCee could expand by employing an agent to assist with local or cultural problems. Alternatively, it could form a Joint Venture with an experienced Asian retailer. All of these methods have risks. The use of franchising is widely used in the retail fashion industry. The real life retailer Zara, which is owned by parent company Inditex, has expanded into Asia by opening franchised shops. Inditex tends to use franchisees in countries that it considers to be risky or that have significant cultural differences or administrative barriers. In some Asian countries, CeeCee would find it hard (or legally impossible) to open its own shops, notably China which insists on some local ownership of all shops. Tesco has expanded into China but has had to form a Joint Venture with a large Chinese company to obtain the required permits to open its stores. CeeCee would face the same obstacles in this high growth market. Franchising would overcome this hurdle and would also bring local expertise to CeeCee’s expansion into the Asian market. This would reduce CeeCee’s political risk.

4 © The Chartered Institute of Management Accountants 2010

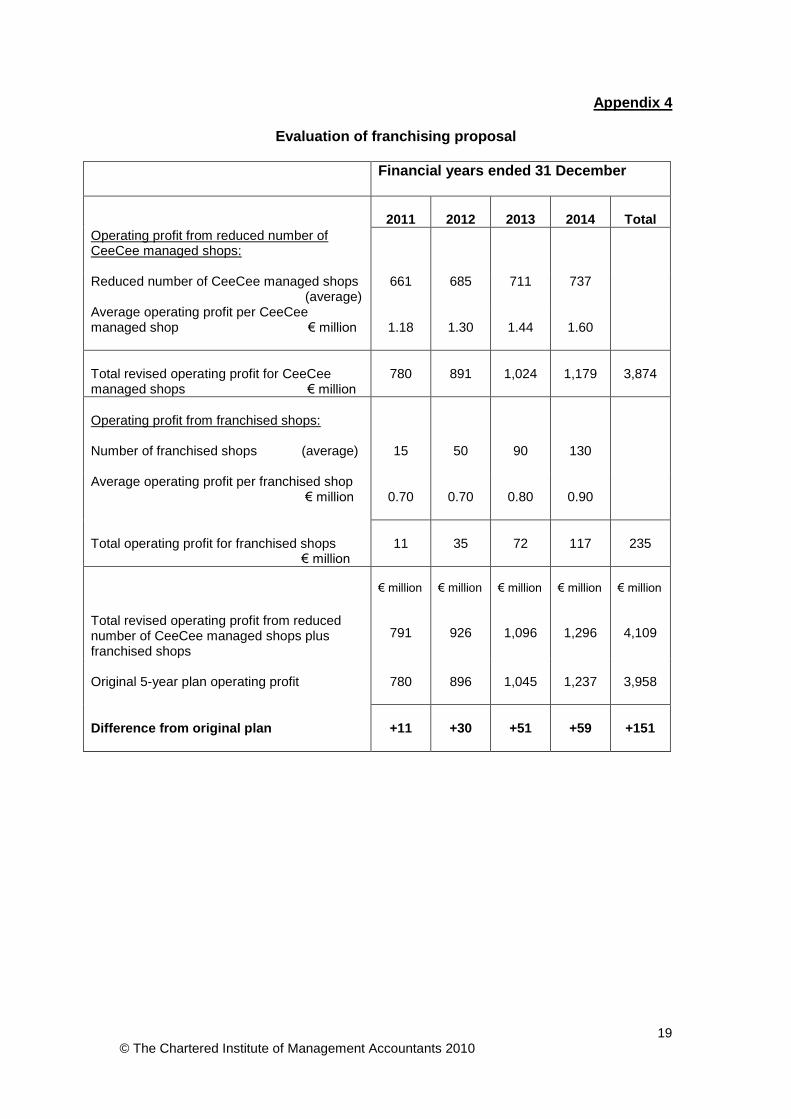

Therefore the proposal to open 100 CeeCee managed shops and 150 franchised shops over the 4 year period ended 31 December 2014 seems commercially sensible and realistic due to local restrictions in some Asian countries. Juliette Lespere’s comment that franchising would allow CeeCee to expand faster in Asia is correct. CeeCee could have 250 new shops (CeeCee managed and franchised) rather than 150 CeeCee managed shops under the current proposal. It would also reduce CeeCee capital expenditure commitment. The agreed 5-year plan shows an increase of 150 new shops in the 4 year period from 2011 to 2014, at an average capital expenditure cost of €4.4 million per shop. Therefore the capital expenditure programme on these new shop openings (ignoring all other shop refurbishments) was €660 million. Under the franchising proposal, CeeCee would open only 100 of its own shops in this 4 year period. This would cost only €440 million, a capital expenditure saving of €220 million. However, the franchisees would need to finance the capital expenditure for the franchised shops. The 150 franchised shops would cost all of the franchisees a total of €660 million. There is reduced risk of failure for CeeCee as it is not using its own finance to fund the capital expenditure for franchised shops. There is an incentive for franchisees to work hard to make each shop profitable so that the up-front shop opening costs are recouped as soon as possible. The average operating profit that CeeCee generates from its own managed shops is considerably higher than the profit that it can make from franchised shops. Therefore, it is allowing franchisees to share in the profitable CeeCee brand name. However, while CeeCee would share future profits, it shares some of the business risk and even eliminates some of its risks entirely. The capital cost of franchised shops is borne entirely by franchisees. The franchising proposal would generate an additional €151 million in operating profit (not discounted) over the next 4 years compared to same 4 year period included in the current agreed 5 year plan. This is due to lower profitability generated for CeeCee from franchised shops offset by a greater number of shop openings over the 4 year period. The franchising proposal is for a total of 250 new shop openings (100 CeeCee managed shops and 150 franchised shops) compared to 150 new shops in the agreed 5-year plan. The franchised shops are forecast to generate operating profits of €235 million (not discounted) over the next 4 years from the proposed 150 franchised shops. This represents the fees payable by the franchisees, usually a percentage of the revenues generated, less the cost to CeeCee to provide marketing and IT support. Franchised shops are also more likely to be successful as the franchisee has invested in the shops and will be motivated to generate sales. However, can CeeCee recruit enough franchisees to meet the target of 150 franchised shops over the next 4 years? CeeCee would need to manage and control all aspects of the franchised shops to ensure that all franchisees adhere to all aspects of the franchising agreement. However, it does free up CeeCee’s management time as CeeCee would not have to manage the day-to-day operations of the franchised shops or recruit the staff working at franchised shops, as this is the responsibility of the franchisees.

5 © The Chartered Institute of Management Accountants 2010

CeeCee will have to manage the franchised shops and ensure that all franchisee conform to CeeCee’s house style and do not break contractual terms, such as selling non-CeeCee products. However, franchising is a totally new venture for CeeCee and it has no experience of it. The Board would need to recruit and appoint an experienced Franchising Manager and a small team to manage the entire franchising proposal, from selection of franchisees to assisting with marketing and IT support. There is also the additional risk of losing some of CeeCee’s experienced shop managers. Juliette Lespere has discussed this proposal with some of CeeCee’s European shop managers. She should not have discussed this proposal before the CeeCee Board has approved it and this aspect will be discussed in Ethics in paragraph 5.0 below. CeeCee had 630 shops operational at the end of December 2009 and these shops are managed by employees who do not currently share in the profits that the shops generate. With their experience, they could become a franchisee and manage a successful franchised shop. This could generate a problem for CeeCee as it could lose experienced shop managers which the company has trained. The loss of their management skills could have a detrimental effect on the revenues and profitability of the European shops which they currently manage. Currently, Juliette Lespere has an interest from over 50 shop managers in becoming franchisees. However, realistically how many of these 50 managers would actually resign and move to Asia to set up as a franchisee. Additionally, how many of these employees would be able to raise the €4.4 million capital costs of opening franchised shops and the working capital necessary for inventory? It is considered that a much smaller number, probably fewer than 10 of these managers would actually become franchisees. They would probably be much more interested in becoming franchisees in Europe. However, the current franchising proposal is to franchise shops in Asia only. Another risk of franchising, which is especially risky in some Asian countries, is loss of control of what the franchisees sell in the branded CeeCee shops and possible loss of intellectual property rights (IPR’s). CeeCee would be supplying franchised shops with all of the current new designs of clothes and other products and it would need to ensure that its franchisees do not “copy” these clothes to sell in other shops that they may own, or sell the designs to other retailers. CeeCee would need to employ a small team to closely monitor and audit what its franchisees are doing to ensure that they do not breach any aspects of the franchising agreement with CeeCee. The legal franchising agreement would need to ensure that the service quality terms, and the length of the franchising agreement, were specified. CeeCee would also need to ensure that the franchising contract protected it from a franchisee cancelling the agreement at short notice.

6 © The Chartered Institute of Management Accountants 2010

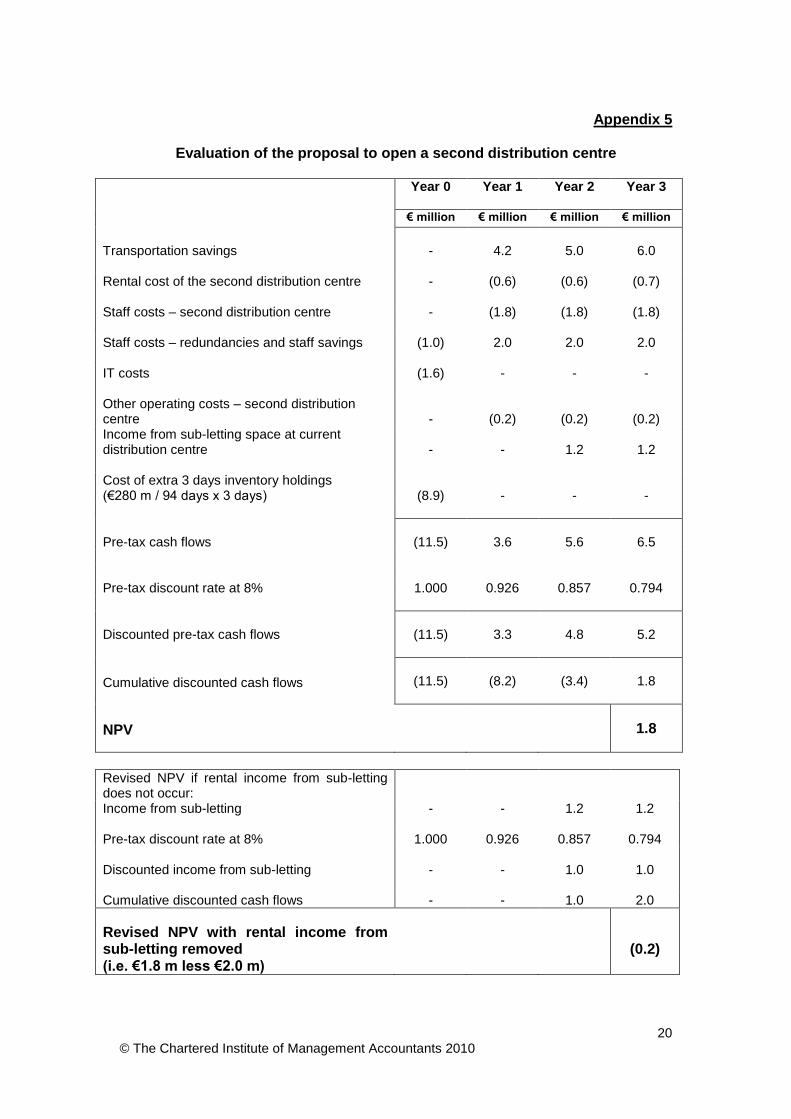

4.3 - Proposal to open a second distribution centre There are 3 aspects to this issue. These are:

Cost savings and financial impact of this change

Impact on the logistics for CeeCee business

Reduction in carbon emissions and the timing of these reductions Taking each of these 3 aspects in turn, the NPV shown in Appendix 5 shows a positive NPV of €1.8 million. Therefore using the assumptions prepared by Jim Bold, the Head of Logistics, the proposal is worthwhile and will generate costs savings to the CeeCee business. However, the CeeCee sales revenue planned for 2010 (as per the 5-year plan shown in Appendix 4 to the pre-seen material) was €2,985 million with operating profit planned to be €690 million. Therefore, CeeCee operating costs in total are planned to be €2,295 million. The NPV in Appendix 5 of page 20 shows a positive NPV over a 3 year period of only €1.8 million. Whilst these are cash flow figures, the annual impact of this small level of savings overall is not a significant amount compared to the total operating costs of CeeCee’s business. However, any increases in efficiencies, or cost savings, should be welcomed. The NPV is positive but the key factor to be considered here is the risk to the “fast fashion” business model and the resultant increase in inventory costs which slows down new products reaching the shops. The over-riding issue here is that CeeCee’s fast fashion business model should not be changed. Jim Bold estimates that “having two distribution centre will increase inventory by 3 days overall”. This is a significant change and must be investigated further. There is a need to speed up the time taken from design drawing board to the finished clothing or product appearing on display in CeeCee’s shops. The estimate by Jim Bold that there will 3 additional days on average for most products to go into and then out of, both of the distribution centres is the most worrying point here. Speed to market is one of the underlying reasons for CeeCee’s success. Decisions should not be taken based on the NPV of the proposal without consideration of this important business factor. The extra 3 days inventory would be valued at around €8.9 million (€280 million for 94 days inventory at end December 2009 x 3 days extra inventory = €8.9 million). It is important to get these new products to CeeCee’s shops as quickly as possible. The reason for opening the distribution centre is to accept products straight from CeeCee’s suppliers in Eastern Europe and ways need to be found to speed up the process of getting products into shops. It would be hoped that the proposed second distribution centre should speed the process up and not slow it down. The shops in Eastern Europe would be served directly from the second distribution centre and this should cut several days of products travelling to and then from CeeCee’s current distribution centre in Northern Europe. Therefore an investigation needs to take place to find out why Jim Bold is estimating an average of 3 additional days inventory on average. The aim should be the same, or a lower, number of inventory days. Unless the estimate of increased inventory days can be reduced, this proposal could damage CeeCee’s fast fashion business model. The proposal only generates a minor cost saving and introduces a risk of losing sales to competitors.

7 © The Chartered Institute of Management Accountants 2010

The third aspect of this issue concerns the forecast reduction in carbon emissions. As a listed company, CeeCee should aim to manage its business responsibly. Aside from any ethical aspects of this issue on the timing of when CeeCee should open the second distribution centre, if the proposal is approved, CeeCee should always aim to improve operating efficiencies and to reduce carbon emissions at the earliest opportunity. If CeeCee chose not to open the second distribution centre, then it will face higher road transportation costs over the next few years, with a rise of 20% each year. This will have an impact on CeeCee’s operating profit margin. Steps should be taken to try to minimise this transportation cost. It is a fine line between selection of suppliers which are close to CeeCee’s shops or distribution centre and the reduced cost of products from suppliers in Eastern Europe and Asia. The cost of the product (as well as its quality) has a greater impact on CeeCee’s profitability than the transportation costs. So location of the supplier should not be a key factor in the selection of new suppliers. There is also another problem with the proposal to open the second distribution centre. This is that 70 employees will have to be made redundant if they cannot be transferred to other roles in CeeCee. The CeeCee business has grown fast in the past and these employees were probably not expecting to lose their jobs. As a responsible employer, CeeCee should help them to find new positions within the company or assist them with finding new jobs. It should also ensure that these staff are kept informed and are treated respectfully and given redundancy pay in accordance with the statutory requirements of the country in which they are employed. The financial proposal incorporates an income from sub-letting space in CeeCee’s current, owned distribution centre. There is a risk that CeeCee may be unable to sub-let this space in the current distribution centre. This would reduce the cash flows by €2.4 million, (a reduction of €2.0 million after discounting at CeeCee’s 8% cost of capital) which would reduce the NPV to a loss at €(0.2) million. This makes the proposal very risky and not financially attractive. 4.4 – Proposal to appoint a famous brand name designer The proposal is for the designer, Ben Eastwood, to prepare 4 collections a year for a 3 year contract period. The contract would need to include specifications that the designs are not too extreme and that they would appeal to High Street shoppers. The contract would also need clauses to ensure that Ben Eastwood did not prepare designs for any of CeeCee’s competitors during this 3 year period. It would also need to cover other possible problems, such as not delivering designs in Years 2 or 3. The forecast annual sales revenues would be around €60 million (€30 per item x 4 collections a year x 0.5 million items in total to be manufactured in each of the collections). If CeeCee were to be successful in selling all of the Ben Eastwood products, then this could increase the company’s sales revenue by almost 2% in 2011 (€60 million / €3,319 million planned total sales revenue for 2011). It is important that the supply of Ben Eastwood designs are limited to a small number such as 0.5 million items to maintain the level of exclusivity. With this small number of items spread across CeeCee’s 672 shops (end 2011) it would result in only 744 items being available for each of the shops. This would generate demand and it is likely that all of the exclusive Ben Eastwood designs would sell out.

8 © The Chartered Institute of Management Accountants 2010

The retailer H & M has used the designer Stella McCartney to design exclusive clothes which were very popular and sold out very quickly. This also attracted customers to its shops who purchased the normal clothes as well, thereby boosting sales. Additionally, the retailer Top Shop has used the model and designer Kate Moss to produce a small collection of exclusive clothes, which have proved very popular and generated much publicity for the chain of Top Shop stores. The Ben Eastwood designs would generate revenues of €60 million and using CeeCee’s average operating profit percentage for 2009 of 22.8%, the profit could be around €14 million. On a marginal cost basis, using gross margins only at around 60%, the profits (before payment to Ben Eastwood) would be around €36 million. This could have a substantial effect on net operating margins. Post-tax, this revenue is €25 million per year, as given in the case material. However, CeeCee would also bear the risk of the designs not selling as expected, although this is unlikely. As stated above, there have been many real life examples of famous designers preparing small ranges of clothes for High Street shops. The Kate Moss design ranges for Topshop usually sold out on the first day they were available, generating much good publicity and attracting customers into the shops. Additionally if CeeCee chose not to appoint Ben Eastwood as a designer for its brand, then one of its competitors may appoint him and CeeCee would lose this opportunity to boost sales and generate publicity. In respect of the range of fees that could be payable to Ben Eastwood, the absolute maximum would be to give 100% of the profits to designer, which would be a fee of €36 million (pre tax) per year. However, as CeeCee would be responsible for delivery to shops and marketing costs and the risk of unsold inventory, it is very unlikely that this highest figure should be offered. Ultimately, the fees will be dependent on market forces and what other designers have secured from other High Street shops and also what Ben Eastwood requires as a minimum. The fee would need to be negotiated. The gross margin for these clothes (assuming gross margins are similar to CeeCee’s other products) at around 60% results in a total annual gross margin of €36 million. It is suggested that the minimum is 10% of this figure, which is €3.6 million, so, say €4 million. The suggested maximum is to share the gross margin 50/50 with Ben Eastwood, which is €18 million per year. 4.5 – Problems with Supplier Y CeeCee relies on all of its suppliers to manufacture its products in a tight production schedule and to get the products into its shops quickly. It cannot manage its business if some of its suppliers cannot meet what is expected of them. In return for exclusivity of supply, CeeCee offers all of its suppliers the opportunity to expand their businesses, as greater volumes of products are required in CeeCee’s expanding number of shops. It is not in anyone’s interests to lose a loyal supplier but clearly the situation with Supplier Y is difficult for CeeCee to manage. It is also worrying that Supplier Y is suffering such extreme IT problems after an upgrade to its IT systems. It does not give the impression of a professional company which is in control of its IT systems.

9 © The Chartered Institute of Management Accountants 2010

There is the concern that Supplier Y has been irresponsible in having its IT systems upgraded without thorough testing and parallel running. This indicates poor management control by Supplier Y and CeeCee should question whether this one-off incident affects Supplier Y’s longer term ability to continue to be a reliable supplier. Supplier Y is just another of CeeCee’s small suppliers and could fairly easily be replaced. It supplies CeeCee with only €20 million worth of inventory each year. CeeCee’s total cost of goods sold is around €1,221 million (based on 2010 sales figure of €2,985 million x 59.1% gross margin percentage (2009 figure) = €1,764 million gross margin = €1,221 million cost of good sold). Therefore, Supplier Y only manufactures around 1.6% of CeeCee’s total value of products. If CeeCee were to terminate its contract with Supplier Y, then its employees could lose their jobs and Supplier Y could go into liquidation. This is an extreme effect of Supplier Y being totally dependent on CeeCee. Supplier Y could argue that as it works under an exclusive contract with CeeCee, a reasonable notice period should be given. A 14 day notice period could be deemed to be too short. Supplier Y’s IT problems could be overcome in the short term by communicating orders to Supplier Y in other ways, such as email, fax or phone. The queries arising from billing problems should be investigated by both Supplier Y and CeeCee. Furthermore, CeeCee should offer to help and support Supplier Y to overcome these temporary IT problems. However, Supplier Y should bear the cost of any IT support provided by CeeCee or CeeCee’s outsourced IT consultants. 5.0 Ethical issues and recommendations on ethical issues 5.1 Range of ethical issues facing CeeCee There is a range of ethical issues that will be discussed and recommendations made, including the following:

1. Carbon emission targets 2. Potential termination of contract with Supplier Y

3. Staff redundancies at current distribution centre

4. Juliette Lespere discussing the confidential proposal for franchising with

CeeCee shop managers before the CeeCee Board has approved or rejected the franchising proposal.

5.2 Carbon emission targets 5.2.1 Why this is an ethical issue There are 2 different ethical aspects to this issue:

The first is whether CeeCee should consider delaying the implementation of the second distribution centre from January 2011 to a later date as CeeCee has been unofficially advised that 2011 is to be made the base year against which emission reductions will be measured. This could make further

10 © The Chartered Institute of Management Accountants 2010

emission reductions harder for CeeCee to achieve in the future, especially if CeeCee were to proceed with the proposed opening of a second distribution centre which would reduce carbon emissions by 18% from January 2011.

The second aspect is what actions the CeeCee Board members should take with the information on penalties for future carbon emissions that Paulo Badeo has passed onto them, which he had been advised of unofficially and in confidence. The Board members now have this “inside” information with regard to the penalties for carbon emissions, and they must act ethically.

5.2.2 Recommendations for this ethical issue It is recommended that CeeCee should make the decision to open a second distribution centre based on the speed of products to shops, so that they are not delayed and therefore the recommendation on this issue is to reject this proposal. However, if the decision were to be made to accept the proposal and to open the second distribution centre, then this should occur as planned, for January 2011. It would be unethical if CeeCee were to delay the opening in order to “manipulate” its level of carbons emission in what may (or may not) become the base year for future measurements and financial penalties. The CeeCee Board should not delay making the reductions in carbon emissions and it should act responsibly. Furthermore, the CeeCee Board should not alter or amend any of the actions or decisions it takes on the opening of the proposed second distribution centre as a result of it now being aware of the “inside” information that Paulo Badeo has shared with Board members. The CeeCee Board has been informed of this information from sources that it should not have had access to. It should ignore the information it has been given. Business decisions should be taken based on data that the company has obtained in an official capacity and possession of this “inside” information should not lead the company to make a different decision or to delay the implementation of the second distribution centre, as this would result in the CeeCee Board acting un-ethically. Additionally, the Chairman should advise Paulo Badeo to keep any information that has been given to him confidentially to himself in future and he should not jeopardise the integrity of other Board members. 5.3 Potential termination of the contract with Supplier Y 5.3.1 Why this is an ethical issue CeeCee should treat all of its suppliers with respect and CeeCee should assist and offer IT support to Supplier Y through its current IT problems. Instead, CeeCee is threatening that its contract will be terminated. This would result in Supplier Y, which works 100% exclusively for CeeCee, losing all of its business. This could lead to the liquidation of Supplier Y unless it could find other business. In the short term, at best, Supplier Y would have to make some of its employees redundant. These “heavy handed” techniques are not how a listed company such as CeeCee should behave. It has stated CSR policies to work with suppliers and ensure that they operate ethically. CeeCee should also act ethically and not threaten Supplier Y which has been a loyal supplier for 9 years, simply due to IT problems over a very short period of time.

11 © The Chartered Institute of Management Accountants 2010

5.3.2 Recommendations for this ethical issue CeeCee should work with Supplier Y to overcome the IT problems. The threat of termination of the contract with Supplier Y should be withdrawn and an apology made. CeeCee should offer to supply (at cost) some of its own IT people to assist with the problems or arrange for an outsourcing IT company to assist Supplier Y. 5.4 Staff redundancies 5.4.1 Why this is an ethical issue If the decision to open the second distribution centre is approved, then 70 employees would be made redundant. They should be offered alternative jobs elsewhere in CeeCee, at shops or perhaps at the second distribution centre. The ethical issue here is that CeeCee should treat its staff fairly. 5.4.2 Recommendations for this ethical issue CeeCee should ensure that all of its employees are treated fairly and that the company keeps its employees informed of the decision. If CeeCee were to go ahead and open the second distribution centre, then it should try to offer alternative jobs within the CeeCee group if possible or re-locate some employees to the new distribution centre. 5.5 Discussion of the franchising proposal with CeeCee shop managers 5.5.1 Why this is an ethical issue The franchising proposal being prepared by Juliette Lespere, the Sales and Marketing Director, is confidential and is a proposal that has not yet been put before the Board of CeeCee. Therefore it is very unethical for Juliette Lespere to have discussed this proposal with many of CeeCee’s shop managers (as over 50 have expresses an interest). Until the proposal has been approved by the Board the proposal should have been kept confidential. It is unreasonable to have discussed the franchising proposal with so many of CeeCee’s employees before the Board has had a chance to consider it. Some of the shop managers may discuss the proposal and the press or competitors could find out about the plans before the CeeCee Board. This could affect the potential success of this proposal. 5.5.2 Recommendations for this ethical issue Juliette Lespere should be reminded of her duties as a director of the company. Confidentiality of Board proposals is important for several reasons, including the need to keep this confidential information within the company. She should be informed that any further breaches of confidentiality could result in her being removed from the Board or her contract of employment terminated.

12 © The Chartered Institute of Management Accountants 2010

6.0 Recommendations 6.1 – Proposal to franchise CeeCee shops in Asia 6.1.1 Recommendation The recommendation of this report is to proceed with franchising shops in Asia as it will help to achieve growth and market penetration faster than having all CeeCee managed shops. 6.1.2 Justification The justification for accepting the franchising proposal would be faster growth of CeeCee branded shops across Asia. Under this franchising proposal CeeCee would have 900 shops operational by the end of 2014 versus the current agreed 5-year plan level of 800 shops. The franchising proposal will generate higher operating profits for shareholders. The operating profit would be €151 million higher (not discounted) over the next 4 years. CeeCee is planning to expand into a different region of the world, of which it has no experience of. There is also the legal need to have local partners involved in shop management in some Asian countries, especially China. Therefore, the franchising proposal, with shops owned and managed by franchisees, under a franchising agreement, would overcome this constraint. It is widely recognised that local knowledge through the use of franchisees, could help to make CeeCee’s expansion into Asia more successful and generate higher revenues. This would enable the CeeCee brand name to become more widely recognised. 6.1.3 Actions to be taken To enable CeeCee to expand in Asia, through both its own managed shops and franchised shops, it needs to establish a supply chain and distribution centre in one or more Asian countries. CeeCee will need to increase the volume of orders from its clothing and other product suppliers, in both Europe and Asia, in order to have the required inventory available across all product ranges to supply the new shops in Asia. With greater volume of production there is an opportunity for CeeCee to negotiate better manufacturing prices for the products due to higher volumes. Some manufacturers should be able to achieve, and share, their economies of scale. CeeCee would need to appoint a Franchising Manager to be responsible for all franchised shops. This new manager would need to have a team of support staff who will be based in Asia to assist, support and closely monitor all franchisees.

13 © The Chartered Institute of Management Accountants 2010

As this is a change from CeeCee’s current business model, there may be many risks it faces. Franchising may involve changes to its IT systems and logistics. The franchisees need to be helped to get the franchised shops operational. The new Franchising Manager will also have to recruit and select suitable franchisees. This may include some of CeeCee’s existing shop managers, but the disadvantage here is that they have no experience operating in Asia and may have little or no local knowledge. This may affect their success. CeeCee will need specialised legal advice to prepare a franchising contract, that covers all aspects of their operation and circumstances where CeeCee may wish to terminate the franchised shop. For example, if a franchisee was found to be selling non-CeeCee branded goods in a franchised shop. 6.2 - Proposal to open a second distribution centre 6.2.1 Recommendation It is the recommendation of this report that CeeCee should not open a second distribution centre in Eastern Europe based on the data in the proposal. The forecast delay of 3 days for inventory is too important in the fast fashion business model. 6.2.2 Justification The most important factor to be considered here is the speed of new products to the market. This proposal as it currently stands is to slow down new inventory by 3 days. This is an important delay and is not acceptable. Unless the logistics of the second distribution centre can be investigated to eliminate or reduce the inventory days, then this proposal should not be approved, despite the cost savings. The NPV for opening a second distribution centre is only €1.8 million over 3 years. However, these cost savings are still small in the scale of CeeCee’s business. With growing transportation costs, this is a sensible proposal which will generate cost savings and should achieve operational efficiencies, but the over-riding issue here is speed of new designs to the market. This proposal slows this down. A second distribution centre in Eastern Europe is a good idea in principle but the slow down of products reaching shops is not acceptable. Therefore until the delay of 3 days inventory is resolved, the proposal in its current form should be rejected. 6.2.3 Actions to be taken Based on the decision to reject this proposal, the actions are to review the logistics to understand why the proposed second distribution centre will increase inventory days by 3 days. If the speed of products to shops and number of days inventory could be reduced, then the proposal becomes viable. Until the proposal is amended to reduce the speed of new products to shops, then there is no further action to be taken. If the number of inventory days and speed to market can be reduced then this proposal could become viable. Only then, the following actions would be required:

14 © The Chartered Institute of Management Accountants 2010

1. Communication of the decision to employees to stop rumours and keep

employees informed 2. Selection of the location for new distribution centre 3. Start to recruit employees for new distribution centre 4. Start required IT updates 5. Project manage the opening of the new distribution centre 6. Start to find a suitable company to sub-let space in the current distribution

centre. 6.3 – Proposal to appoint a famous brand name designer 6.3.1 Recommendation It is the recommendation of this report that CeeCee should appoint Ben Eastwood to design 4 collections each year under a 3 year contract. It is recommended that CeeCee should try to negotiate to pay between €4 million rising to a maximum of €18 million per year. This higher figure represents 50% of the pre-tax operating profit generated from these sales. The absolute maximum that would be payable would be €36 million (which is equal to €25 million post-tax) but this would give all of the profits to the designer and leave CeeCee with all of the risk of any unsold inventory, although this risk is minimal. 6.3.2 Justification An association with a famous designer will increases sales. The extra sales revenue from the small designer collection will generate €60 million per year and it is likely that additional sales of CeeCee’s own clothing and products will be made to customers visiting CeeCee shops to look at or buy the Ben Eastwood designs. An association with a famous designer will help to increase CeeCee’s brand awareness. It will also attract more customers, some of which may be new customers, into CeeCee’s shops. The use of a famous designer has attracted much publicity generally for other shops (such as Topshop and H & M), which have even had queues of people waiting for the shops to open on the day of the launch of each new designer collection. Overall, an association with the famous designer Ben Eastwood would have a positive effect on profits, assuming that not all profits are paid to Ben Eastwood in fees. 6.3.3 Actions to be taken There is a need to negotiate the fee level to be paid to Ben Eastwood. There is a wide margin to negotiate ranging from €4 million up to €18 million. No announcements should be made until contracts are signed with Ben Eastwood. Preparation, with legal advice, of a contract with Ben Eastwood, that ensures that CeeCee minimises all of the risks that could occur, such as non delivery of one of the 12 collections (4 collections per year for 3 years) or late delivery of designs.

15 © The Chartered Institute of Management Accountants 2010

CeeCee’s marketing department needs to plan the launch of the new Ben Eastwood clothes range and all of the media coverage. Juliette Lespere should arrange a press release and use this opportunity to generate publicity about signing Ben Eastwood with CeeCee. 6.4 – Problems with Supplier Y 6.4.1 Recommendation It is the recommendation of this report that CeeCee should support Supplier Y and that CeeCee should assist Supplier Y in resolving its IT problems. If CeeCee provides its own in-house IT experts, or arranges for its external IT consultants to assist Supplier Y, it should be agreed that Supplier Y should pay for the cost of this IT support. It is in everyone’s interests that Supplier Y is operational again as quickly as possible so that it can continue to supply CeeCee with its products.

6.4.2 Justification CeeCee should not terminate its contract with a loyal supplier of 9 years following short-term IT problems. It should work with Supplier Y to try to assist it to overcome this short-term problem. The extra management time that could be taken to identify and recruit a new supplier and to put contracts in place could be far longer than helping Supplier Y to resolve its problems. 6.4.3 Actions to be taken CeeCee’s IT Director, Roberta Downs, should arrange to provide experienced IT expertise to Supplier Y as soon as possible. CeeCee’s admin staff should liaise with Supplier Y to try to establish what orders it has, or has not, received using other communication methods, so that Supplier Y’s factory can carry on manufacturing the items required. CeeCee’s finance department must work closely with Supplier Y’s finance department to cancel any incorrectly raised invoices and to establish which deliveries have been made and agree trade payable balances. 7.0 Conclusions CeeCee is operating in a competitive market in difficult trading conditions. It has a successful brand and the company is operating over 630 shops throughout Europe. With the above recommendations for change, particularly the recommendation to franchise in Asia, CeeCee could achieve faster growth and generate higher profits than originally planned. The future for CeeCee looks very promising.

16 © The Chartered Institute of Management Accountants 2010

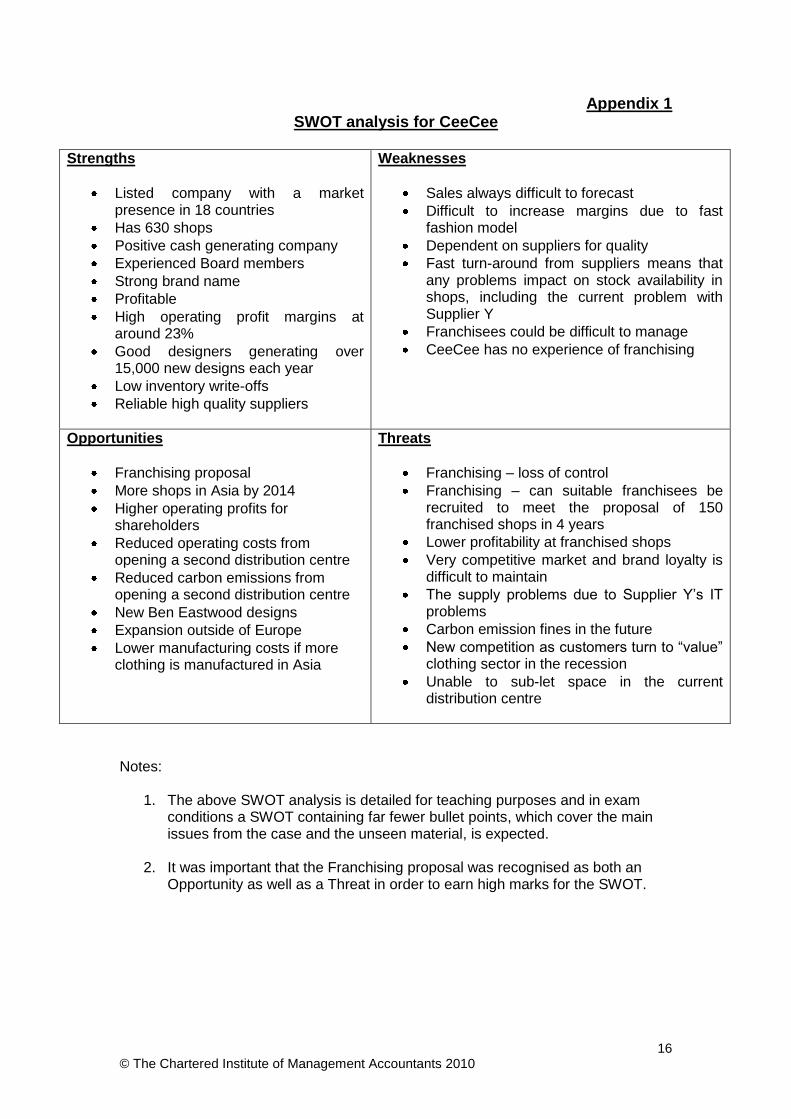

Appendix 1 SWOT analysis for CeeCee

Strengths

Listed company with a market presence in 18 countries

Has 630 shops

Positive cash generating company

Experienced Board members

Strong brand name

Profitable

High operating profit margins at around 23%

Good designers generating over 15,000 new designs each year

Low inventory write-offs

Reliable high quality suppliers

Weaknesses

Sales always difficult to forecast

Difficult to increase margins due to fast fashion model

Dependent on suppliers for quality

Fast turn-around from suppliers means that any problems impact on stock availability in shops, including the current problem with Supplier Y

Franchisees could be difficult to manage

CeeCee has no experience of franchising

Opportunities

Franchising proposal

More shops in Asia by 2014

Higher operating profits for shareholders

Reduced operating costs from opening a second distribution centre

Reduced carbon emissions from opening a second distribution centre

New Ben Eastwood designs

Expansion outside of Europe

Lower manufacturing costs if more clothing is manufactured in Asia

Threats

Franchising – loss of control

Franchising – can suitable franchisees be recruited to meet the proposal of 150 franchised shops in 4 years

Lower profitability at franchised shops

Very competitive market and brand loyalty is difficult to maintain

The supply problems due to Supplier Y’s IT problems

Carbon emission fines in the future

New competition as customers turn to “value” clothing sector in the recession

Unable to sub-let space in the current distribution centre

Notes:

1. The above SWOT analysis is detailed for teaching purposes and in exam conditions a SWOT containing far fewer bullet points, which cover the main issues from the case and the unseen material, is expected.

2. It was important that the Franchising proposal was recognised as both an

Opportunity as well as a Threat in order to earn high marks for the SWOT.

17 © The Chartered Institute of Management Accountants 2010

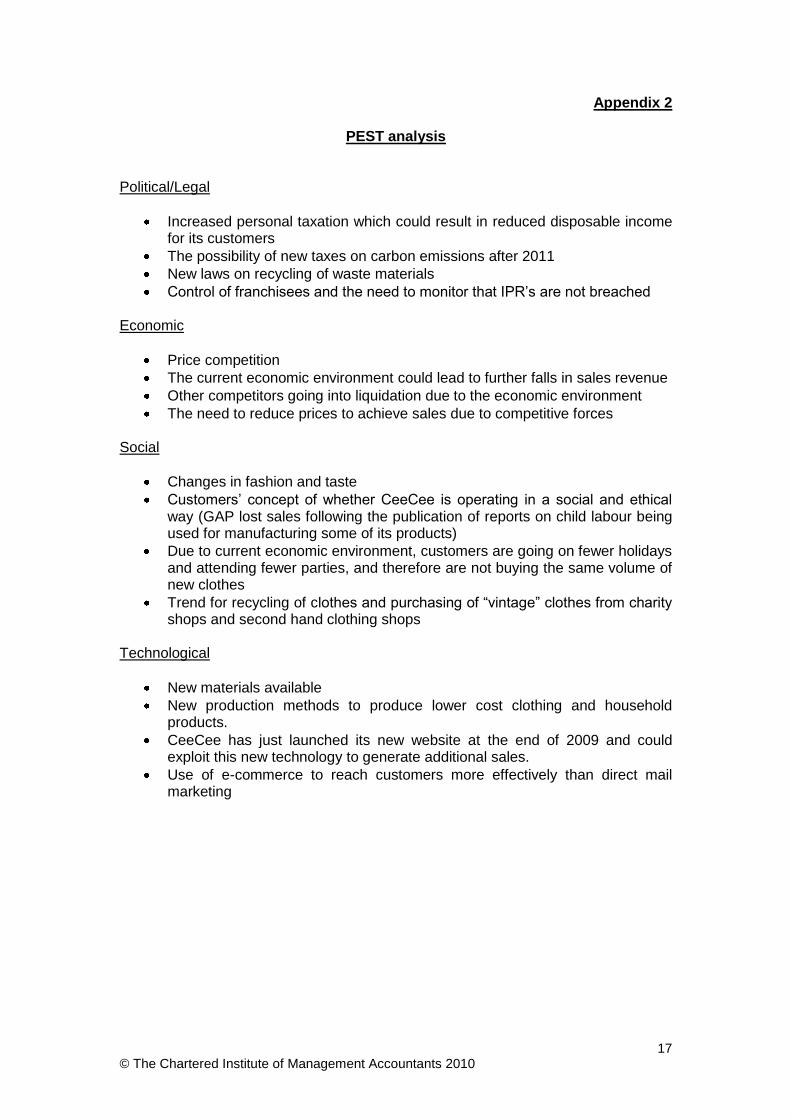

Appendix 2

PEST analysis

Political/Legal

Increased personal taxation which could result in reduced disposable income for its customers

The possibility of new taxes on carbon emissions after 2011

New laws on recycling of waste materials

Control of franchisees and the need to monitor that IPR’s are not breached Economic

Price competition

The current economic environment could lead to further falls in sales revenue

Other competitors going into liquidation due to the economic environment

The need to reduce prices to achieve sales due to competitive forces Social

Changes in fashion and taste

Customers’ concept of whether CeeCee is operating in a social and ethical way (GAP lost sales following the publication of reports on child labour being used for manufacturing some of its products)

Due to current economic environment, customers are going on fewer holidays and attending fewer parties, and therefore are not buying the same volume of new clothes

Trend for recycling of clothes and purchasing of “vintage” clothes from charity shops and second hand clothing shops

Technological

New materials available

New production methods to produce lower cost clothing and household products.

CeeCee has just launched its new website at the end of 2009 and could exploit this new technology to generate additional sales.

Use of e-commerce to reach customers more effectively than direct mail marketing

18 © The Chartered Institute of Management Accountants 2010

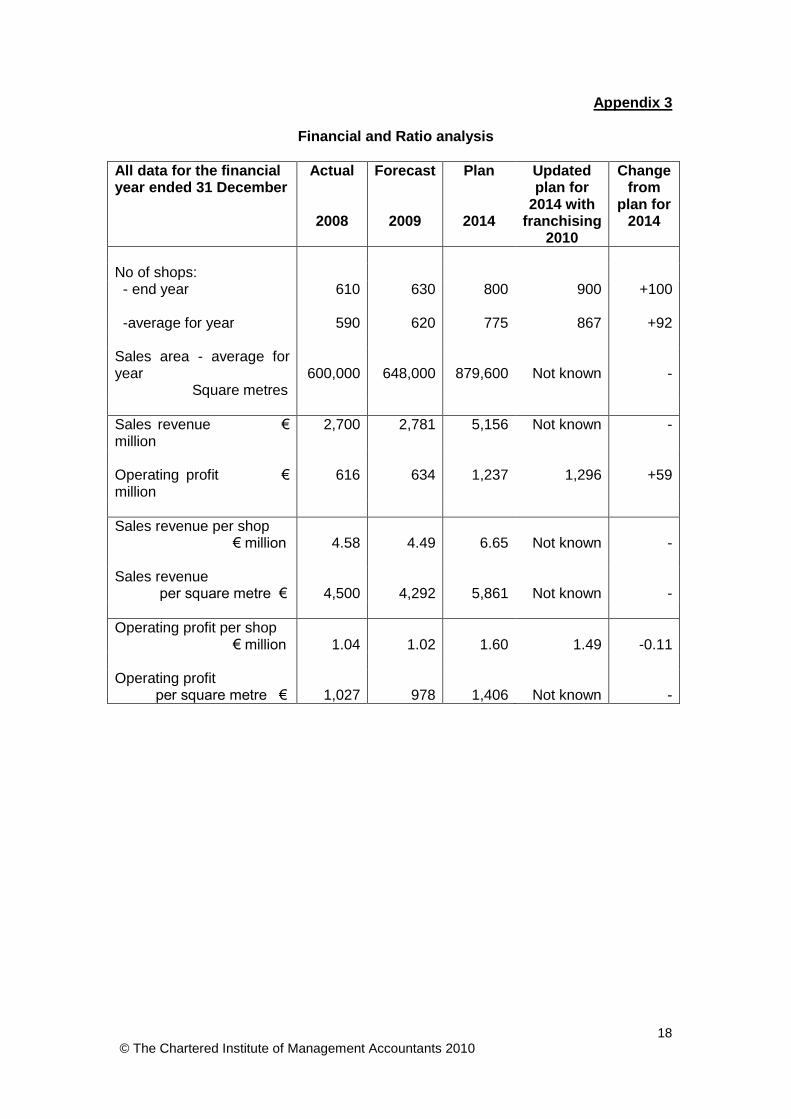

Appendix 3

Financial and Ratio analysis

All data for the financial year ended 31 December

Actual

2008

Forecast

2009

Plan

2014

Updated plan for

2014 with franchising

2010

Change from

plan for 2014

No of shops: - end year 610 630

800 900 +100

-average for year 590 620 775 867 +92 Sales area - average for year Square metres

600,000

648,000

879,600

Not known

-

Sales revenue € million

2,700 2,781 5,156 Not known -

Operating profit € million

616 634 1,237 1,296 +59

Sales revenue per shop € million

4.58

4.49

6.65

Not known

-

Sales revenue per square metre €

4,500

4,292

5,861

Not known

-

Operating profit per shop € million

1.04

1.02

1.60

1.49

-0.11

Operating profit per square metre €

1,027

978

1,406

Not known

-

19 © The Chartered Institute of Management Accountants 2010

Appendix 4

Evaluation of franchising proposal

Financial years ended 31 December

2011

2012

2013

2014

Total

Operating profit from reduced number of CeeCee managed shops:

Reduced number of CeeCee managed shops (average)

661 685 711 737

Average operating profit per CeeCee managed shop € million

1.18

1.30

1.44

1.60

Total revised operating profit for CeeCee managed shops € million

780

891

1,024

1,179

3,874

Operating profit from franchised shops:

Number of franchised shops (average) 15 50 90 130

Average operating profit per franchised shop € million

0.70

0.70

0.80

0.90

Total operating profit for franchised shops € million

11

35

72

117

235

Total revised operating profit from reduced number of CeeCee managed shops plus franchised shops

€ million

791

€ million

926

€ million

1,096

€ million

1,296

€ million

4,109

Original 5-year plan operating profit

780

896

1,045

1,237

3,958

Difference from original plan

+11

+30

+51

+59

+151

20 © The Chartered Institute of Management Accountants 2010

Appendix 5

Evaluation of the proposal to open a second distribution centre

Year 0

Year 1 Year 2 Year 3

€ million € million € million € million

Transportation savings

-

4.2

5.0

6.0

Rental cost of the second distribution centre - (0.6) (0.6) (0.7)

Staff costs – second distribution centre - (1.8) (1.8) (1.8)

Staff costs – redundancies and staff savings (1.0) 2.0 2.0 2.0

IT costs (1.6) - - -

Other operating costs – second distribution centre

-

(0.2)

(0.2)

(0.2)

Income from sub-letting space at current distribution centre

-

-

1.2

1.2

Cost of extra 3 days inventory holdings (€280 m / 94 days x 3 days)

(8.9)

-

-

-

Pre-tax cash flows

(11.5)

3.6

5.6

6.5

Pre-tax discount rate at 8% 1.000 0.926 0.857 0.794

Discounted pre-tax cash flows

(11.5)

3.3

4.8

5.2

Cumulative discounted cash flows

(11.5)

(8.2)

(3.4)

1.8

NPV

1.8

Revised NPV if rental income from sub-letting does not occur:

Income from sub-letting - - 1.2 1.2

Pre-tax discount rate at 8% 1.000 0.926 0.857 0.794 Discounted income from sub-letting

-

-

1.0

1.0

Cumulative discounted cash flows - - 1.0 2.0

Revised NPV with rental income from sub-letting removed (i.e. €1.8 m less €2.0 m)

(0.2)

21 © The Chartered Institute of Management Accountants 2010

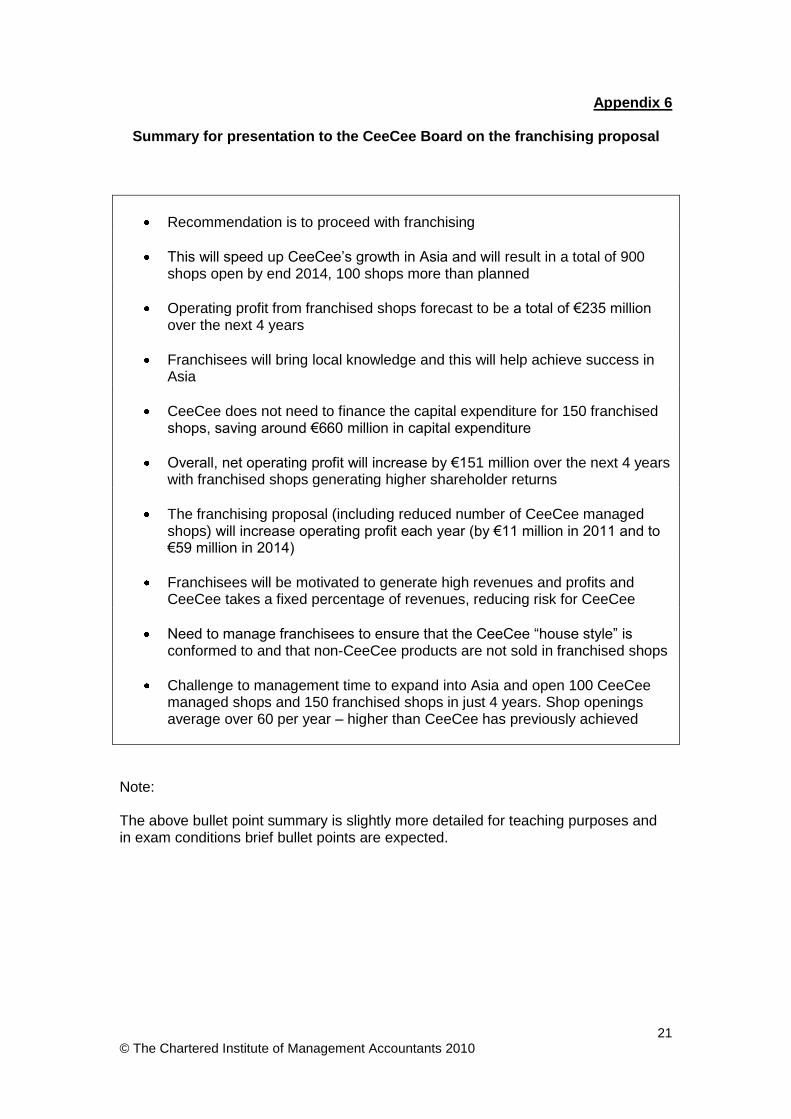

Appendix 6

Summary for presentation to the CeeCee Board on the franchising proposal

Recommendation is to proceed with franchising

This will speed up CeeCee’s growth in Asia and will result in a total of 900 shops open by end 2014, 100 shops more than planned

Operating profit from franchised shops forecast to be a total of €235 million over the next 4 years

Franchisees will bring local knowledge and this will help achieve success in Asia

CeeCee does not need to finance the capital expenditure for 150 franchised shops, saving around €660 million in capital expenditure

Overall, net operating profit will increase by €151 million over the next 4 years with franchised shops generating higher shareholder returns

The franchising proposal (including reduced number of CeeCee managed shops) will increase operating profit each year (by €11 million in 2011 and to €59 million in 2014)

Franchisees will be motivated to generate high revenues and profits and CeeCee takes a fixed percentage of revenues, reducing risk for CeeCee

Need to manage franchisees to ensure that the CeeCee “house style” is conformed to and that non-CeeCee products are not sold in franchised shops

Challenge to management time to expand into Asia and open 100 CeeCee managed shops and 150 franchised shops in just 4 years. Shop openings average over 60 per year – higher than CeeCee has previously achieved

Note: The above bullet point summary is slightly more detailed for teaching purposes and in exam conditions brief bullet points are expected.