Embed Size (px)

Citation preview

GOOD TO GREATBY JIM COLLINS

CHAPTER 1

TEAM 2CAITLIN CLARK

STEPHEN MASSIMI

WILL MAYRATH

MATT VATANKHAH

KATIE TREVINO

GOOD IS THE ENEMY OF THE GREAT.

Overview While presenting his first book, Bill Meehan,

the managing director of the San Francisco office of McKinsey & Company, told Jim Collins,“You know, Jim, we love Built to Last around

here. You and your coauthor did a very fine job on the research and writing. Unfortunately, it’s useless.”

This was the spark of curiosity that began five years of research and resulted in Good to Great.

Overview, continued

The five-year research effort yielded many insights, but one conclusion stands out above the others Most any organization can substantially

improve its stature and performance, perhaps even become great, if it conscientiously applies the framework of ideas we’ve uncovered

Phase 1: The Search First task was to find companies that

showed the good-to-great pattern (Table 1) Launched a six-month “death march of

financial analysis,” looking for companies that showed the following basic pattern:Fifteen-year cumulative stock returns at or below

the general stock market, punctuated by a transition point, then cumulative returns at least three times the market over the next fifteen years

Phase 1: The Search, continuedCompany Results from Transition

Point to 15 Years beyond Transition

Point*

T Year to T Year + 15

Abbot 3.98 times the market 1974 – 1989

Circuit City 18.50 times the market 1982 – 1997

Fannie Mae 7.56 times the market 1984 - 1999

Gillette 7.39 times the market 1980 - 1995

Kimberly-Clark 3.42 times the market 1972 – 1987

Kroger 4.17 times the market 1973 – 1988

Nucor 5.16 times the market 1975 – 1990

Philip Morris 7.06 times the market 1964 – 1979

Pitney Bowes 7.16 times the market 1973 – 1988

Walgreens 7.34 times the market 1975 – 1990

Wells Fargo 3.99 times the market 1983 – 1998

*Ratio of cumulative stock returns relative to the general stock market

Phase 1: The Search, continued

Criteria for Selection as a Good-to-Great CompanyCompany shows a pattern of “good” performance

punctuated by a transition point, after which it shifts to “great” performance

Good-to-great shift must be a company shift, not an industry event

At the transition point, the company must have been an established, ongoing company, not a start-up

Phase 1: The Search, continued

Criteria for Selection as a Good-to-Great Company, continued The transition point had to occur before 1985

so that there would be enough data to assess the sustainability of the transition

Whatever the year of transition, the company still had to be a significant, ongoing, stand-alone company at the time of selection

At the time of selection, the company should still show an upward trend

Phase 1: The Search, continued

The Good-to-Great Screening and Selection ProcessCut 1: From the Universe of Companies to 1,435

Companies ○ Selected from the Fortune 500, 1965 – 1995

Cut 2: From 1,435 Companies to 126 Companies○ Selected into full CRSP data pattern analysis

Cut 3: From 126 Companies to 19 Companies ○ Selected into Industry Analysis

Cut 4: From 19 Companies to 11 Good-to-Great Companies ○ Selected into Good-to-Great Set

Phase 2: Compared to What?

Two types of comparison companiesDirect comparisons

○ Companies that were in the same industry as the good-to-great opportunities and similar resources at the time of transition, but showed no leap from good to great

Unsustained comparisons○ Companies that made a short-term shift from good

to great but failed to maintain the trajectory○ Intended to address the question of sustainability○ Comparisons are displayed in Appendix 1.C, page

234

Phase 2: Compared to What, continued Direct Comparisons

Purpose of direct comparison analysis is to create as close to a “historical controlled experiment” as possible

Helped in identifying distinguishing variables that account for the transition from good to great

Performed a systematic and methodical collection and scoring of all obvious comparison candidates for each good-to-great company

Phase 2: Compared to What?, continued Direct Comparison Criteria

Business Fit○ At the time of transition, the comparison candidate

had similar products and services as the good-to-great company

Size Fit ○ At the time of transition, the comparison candidate

was the same basic size as the good-to-great company

Age Fit○ The comparison candidate was founded in the

same era as the good-to-great company

Phase 2: Compared to What?, continued Direct Comparison Criteria, continued

Stock Chart Fit○ The cumulative stock returns to market chart of the

comparison candidate roughly tracks the pattern of the good-to-great company until the point of transition

Conservative Test○ At the time of transition, the comparison candidate was

more successful than the good-to-great company Face Validity

○ Takes into account two factorsComparison candidate is in a similar line of business at the time of

selectionComparison candidate is less successful than the good-to-great

company at the time of selection

Phase 2: Compared to What?, continued Direct Comparison Scoring

Scored each comparison candidate on each of the six criteria on a scale of 1 to 4: ○ 4 = comparison candidate fits the criteria

extremely well—there are no issues or qualifiers○ 3 = comparison candidate fits the criteria

reasonably well—there are minor issues or qualifiers

○ 2 = comparison candidate fits the criteria poorly—there are major issues and concerns

○ 1 = comparison candidate fails the criteria

Phase 2: Compared to What?, continued

The Entire Study Set

Good-to-Great Companies

Comparison Companies

Abbot Upjohn

Circuit City Silo

Fannie Mae Great Western

Gillette Warner-Lambert

Kimberly-Clark Scott Paper

Kroger A&P

Nucor Bethlehem Steel

Philip Morris R.J. Reynolds

Pitney Bowes Addressograph

Walgreens Eckerd

Wells Fargo Bank of America

Unsustained Companies

Burroughs

Chrysler

Harris

Hasbro

Rubbermaid

Teledyne

Phase 3: Inside the Black Box Research Phase

Systematically coded all materials into categories, conducted interviews, and initiated a wide range of analyses

Project began with the goal of building a

theory from the ground up

Phase 3: Inside the Black Box, continued In the study, what they didn’t find turned

out to be some of the best clues to the inner workings of good to great

Good Results

What’s Inside the

BLACK BOX?

Great Results

Phase 3: Inside the Black Box, continued Company Coding Documents Collected

All major articles published on the company over its entire history

Materials obtained directly from companies Books written about the industry, company, and/or

its leaders Business school case studies and industry

analyses Business and industry reference materials Annual reports, proxy statements, analyst reports,

and any other materials available on the company, especially during the transition era

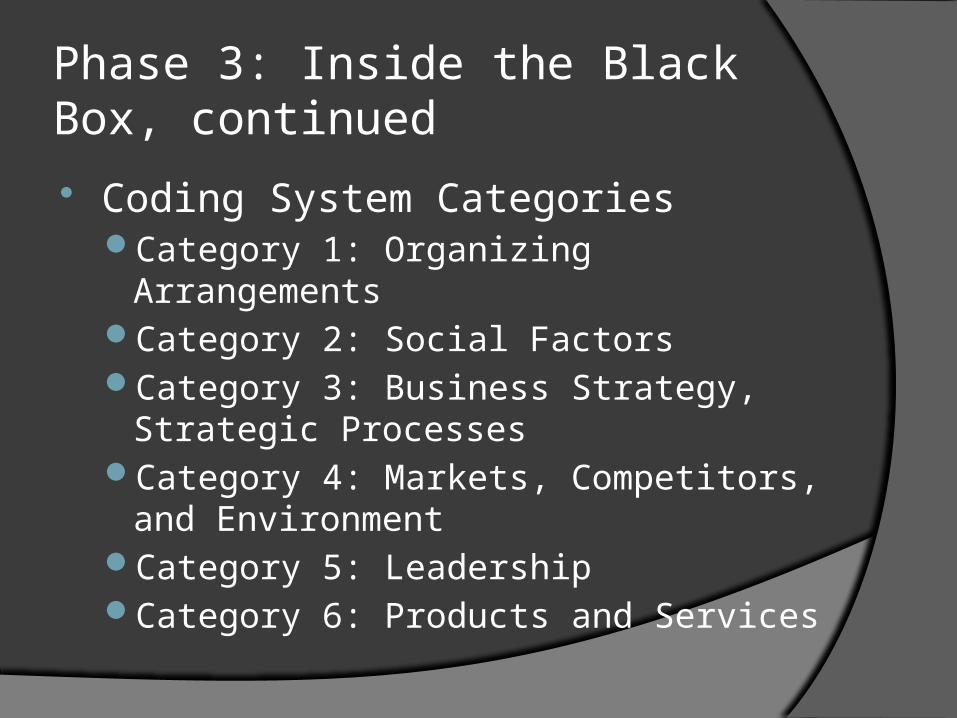

Phase 3: Inside the Black Box, continued Coding System Categories

Category 1: Organizing ArrangementsCategory 2: Social FactorsCategory 3: Business Strategy, Strategic

ProcessesCategory 4: Markets, Competitors, and

EnvironmentCategory 5: Leadership Category 6: Products and Services

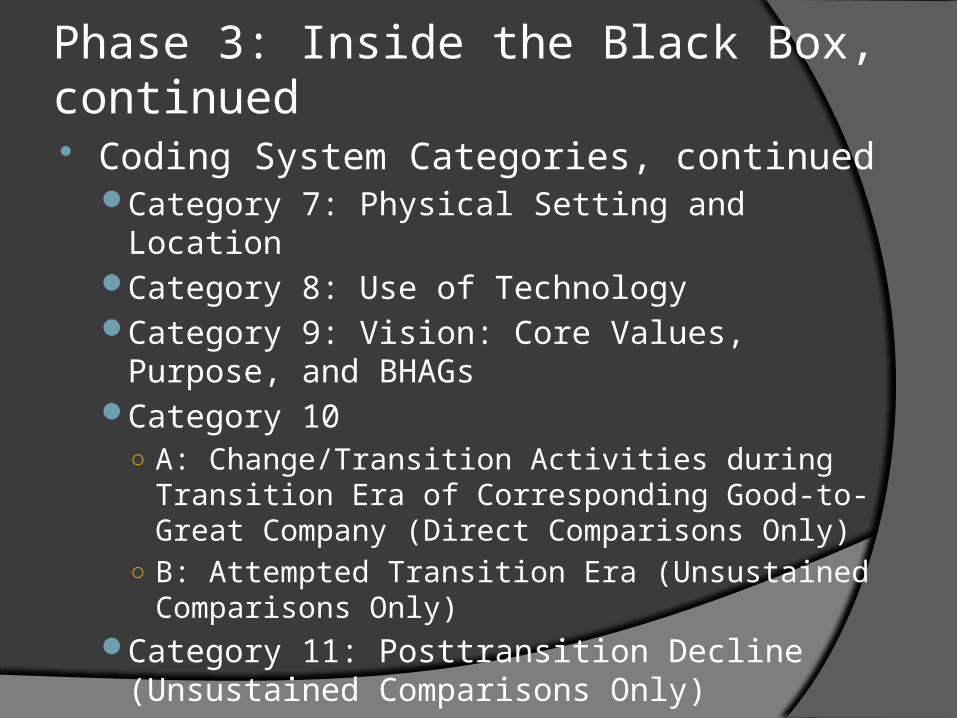

Phase 3: Inside the Black Box, continued Coding System Categories, continued

Category 7: Physical Setting and Location Category 8: Use of TechnologyCategory 9: Vision: Core Values, Purpose, and

BHAGsCategory 10

○ A: Change/Transition Activities during Transition Era of Corresponding Good-to-Great Company (Direct Comparisons Only)

○ B: Attempted Transition Era (Unsustained Comparisons Only)

Category 11: Posttransition Decline (Unsustained Comparisons Only)

Phase 3: Inside the Black Box, continued Other Research Elements

Financial Spreadsheet Analysis ○ Examined all financial variables for 980 combined

years of data (35 years on average per company)○ Comprised gathering raw income and balance

sheet data and examining variables in both the pre- and posttransition decades

Executive Interviews○ Conducted interviews of senior management and

board members, focusing on those in office during the transition era

Phase 3: Inside the Black Box, continued Special Analysis Units

Acquisitions and Divestitures ○ Sought to understand the role of acquisitions and

divestments in the transition from good to greatIndustry Performance Analysis

○ Looked at the performance of the companies versus the performance of the industries

Executive Churn Analysis ○ Looked at the extent to which the executive teams

changed during the crucial points in companies’ historiesCEO Analysis

○ Performed a qualitative examination of each set of CEOs during the transition eras in all three sets of companies

Phase 3: Inside the Black Box, continued Special Analysis Units, continued

Executive Compensation ○ Examined across the twenty-eight companies studied, from ten

years before the transition point to 1998Role of Layoffs

○ Sought to examine all companies for evidence of layoffs as a conscious tactic to improve company performance

Corporate Ownership Analysis○ Aimed to determine if there were any significant differences

between companiesMedia Hype Analysis

○ Looked at the degree of “media hype” surrounding the companiesTechnology Analysis

○ Examined the role of technology, drawing largely upon executive interviews and written source materials

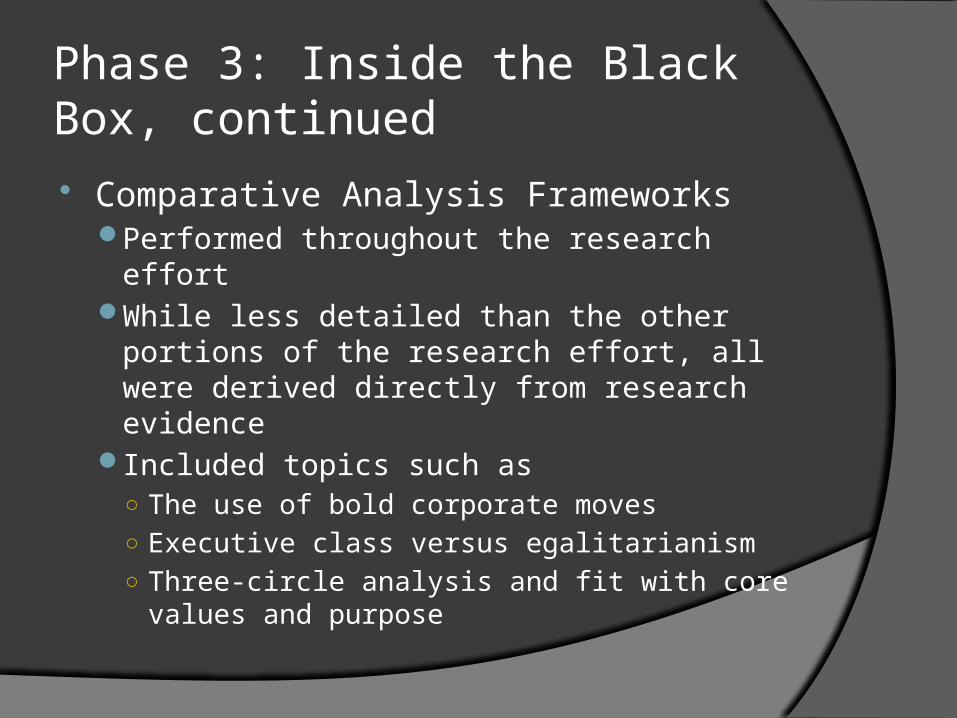

Phase 3: Inside the Black Box, continued Comparative Analysis Frameworks

Performed throughout the research effortWhile less detailed than the other portions of

the research effort, all were derived directly from research evidence

Included topics such as ○ The use of bold corporate moves○ Executive class versus egalitarianism ○ Three-circle analysis and fit with core values

and purpose

Phase 4: Chaos to Concept Every primary concept in the final

framework showed up as a change variable in 100 percent of the good-to-great companies and in less than 30 percent of the comparison companies during the pivotal years

The Flywheel captures the gestalt of the entire process of going from good to great

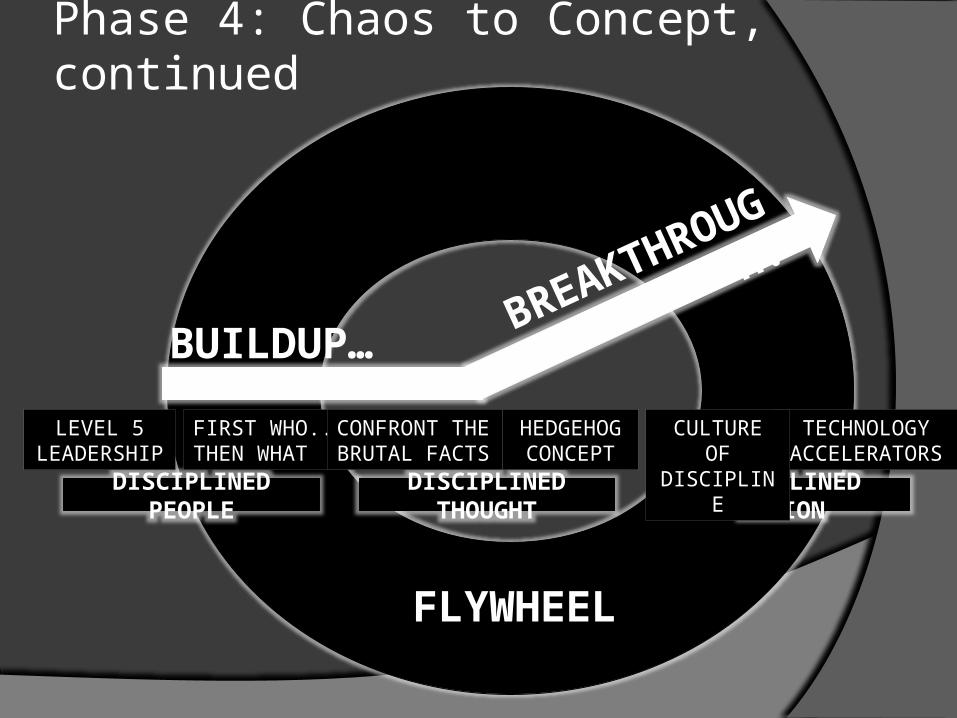

Phase 4: Chaos to Concept, continued

DISCIPLINED PEOPLE

DISCIPLINED THOUGHT

DISCIPLINED ACTION

FIRST WHO.. THEN WHAT

LEVEL 5 LEADERSHI

P

TECHNOLOGY ACCELERATOR

S

HEDGEHOG

CONCEPT

BUILDUP…

BREAKTHRO

UGH!

FLYWHEEL

CULTURE OF

DISCIPLINE

CONFRONT THE BRUTAL FACTS

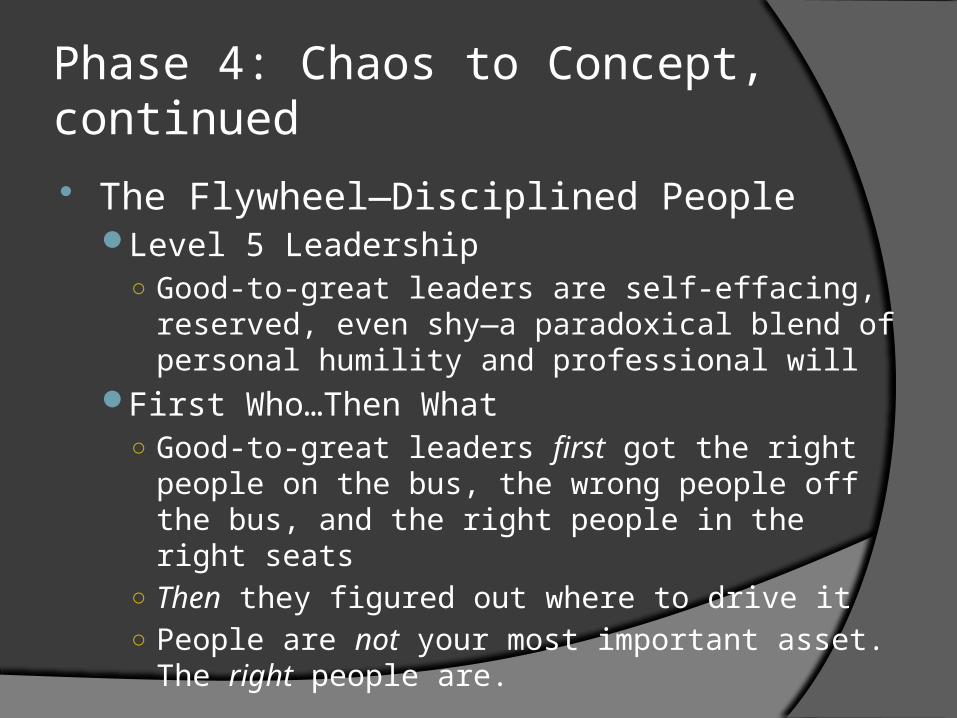

Phase 4: Chaos to Concept, continued The Flywheel—Disciplined People

Level 5 Leadership○ Good-to-great leaders are self-effacing, reserved,

even shy—a paradoxical blend of personal humility and professional will

First Who…Then What○ Good-to-great leaders first got the right people on

the bus, the wrong people off the bus, and the right people in the right seats

○ Then they figured out where to drive it ○ People are not your most important asset. The right

people are.

Phase 4: Chaos to Concept, continued The Flywheel—Disciplined Thought

Confront the Brutal Facts (Yet Never Lose Faith)○ Every good-to-great company embraced what came to

be called the Stockdale ParadoxMust maintain unwavering faith that you can and will prevail in

the end, regardless of the difficulties, AND at the same time have the discipline to confront the most brutal facts of your current reality, whatever they might be

The Hedgehog Concept (Simplicity within the Three Circles)○ To go from good to great requires transcending the

curse of competence○ If you cannot be the best in the world at your core

business, then your core business absolutely cannot form the basis of a great company It must be replaced with a simple concept that reflects deep

understanding of three intersecting circles

Phase 4: Chaos to Concept, continued The Flywheel—Disciplined Action

A Culture of Discipline○ When you have disciplined people, you don’t

need hierarchy○ When you have disciplined thought, you don’t

need bureaucracy○ When you have disciplined action, you don’t

need excessive controls○ When you combine a culture of discipline with

an ethic of entrepreneurship, you get the alchemy of great performance

Phase 4: Chaos to Concept, continued The Flywheel—Disciplined Action,

ContinuedTechnology Accelerators

○ Good-to-great companies think differently about the role of technologyThey never use technology as the primary means of

igniting a transformation

○ Paradoxically, they are pioneers in the application of carefully selected technologies

○ Technology by itself is never a primary, root cause of either greatness or decline

Phase 4: Chaos to Concept, continued The Flywheel and the Doom Loop

Those who launch revolutions, dramatic change programs, and wrenching restructurings will almost certainly fail to make the leap from good to great○ Good-to-great transformations never

happened in one fell swoopRather, the process resembled relentlessly

pushing a giant heavy flywheel in one direction, building momentum until a point of breakthrough

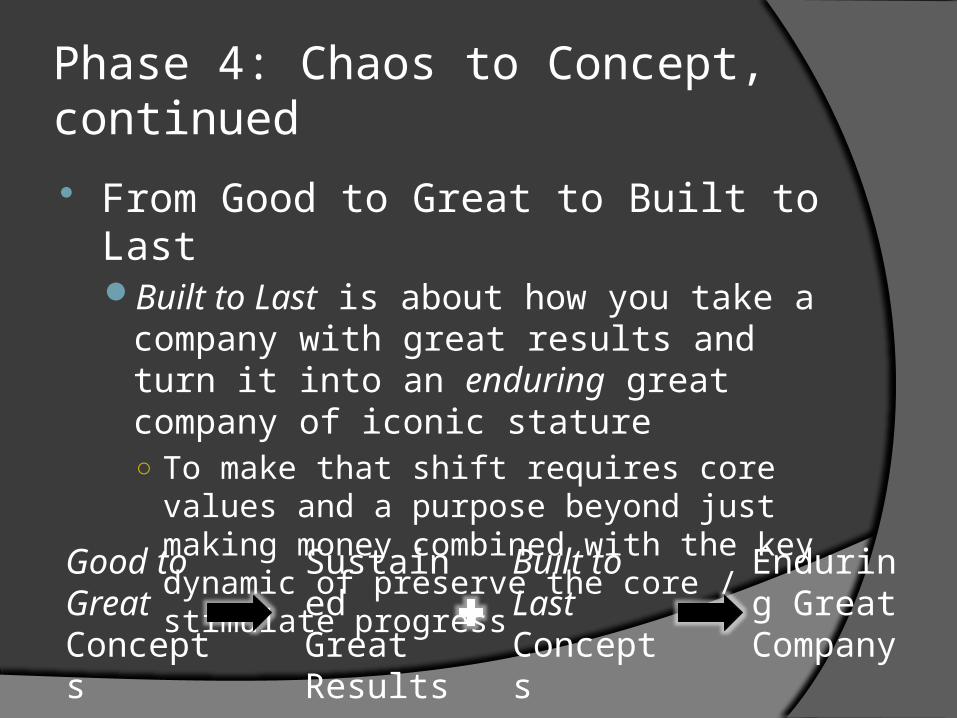

Phase 4: Chaos to Concept, continued From Good to Great to Built to Last

Built to Last is about how you take a company with great results and turn it into an enduring great company of iconic stature ○ To make that shift requires core values and a

purpose beyond just making money combined with the key dynamic of preserve the core / stimulate progress

Good to Great Concepts

Sustained Great Results

Built to Last Concepts

Enduring Great Company

The Timeless “Physics” of Good to Great This book is ultimately about one thing:

The timeless principles of good to great○ It’s about how you take a good organization of any

type and turn it into one that produces sustained great results, using whatever definition of results best applies to your organization

That good is the enemy of great is not just a business problem—it is a human problem If we have cracked the code on the question of

good to great, we should have something of value to any type of organization