Embed Size (px)

Citation preview

ICICI Securities Ltd. | Retail Equity Research

October 18, 2017

Monthly Update

Respite on GST but US stress to persist in Q2

l-direct coverage companies are expected to witness a revival on the

domestic front post-GST implementation in Q2. However, no respite is likely

on the US front as the core issue of pricing pressure continues to weigh.

Accordingly, we expect the I-direct universe to register mere ~3% YoY

growth to | 39389 crore. US business (select pack) is expected to decline

11% YoY to | 10452 crore. On the domestic front, we expect ~10% YoY

growth to | 9334 crore (select pack) as most companies are expecting

normalcy to be back in the distribution channels. However, due to GST

related changes in accounting and reporting, domestic growth numbers

may witness a marginal negative impact. On the companies front, Cadila

(due to launch of limited competition gLialda in the US) is expected to

register strong growth. On the other hand, 11 out of 19 companies of I-

direct healthcare universe are expected to register negative or low single

digit growth.

EBITDA of the I-direct healthcare universe is expected to decline 13% YoY

to | 8315 crore. EBITDA margins are likely to decline 388 bps YoY to 21%.

An adverse product mix, increase in R&D expenditure and higher plant

related fixed costs are likely to cause a sharp margin erosion for the

universe during the quarter. Net profit is expected to decline ~17% YoY to

| 4997 crore, mainly due to a subdued operational performance.

On the regulatory front, Sun Pharma’s Dadra & Nagar Haveli formulation

plant has received an establishment inspection report (EIR) from the

USFDA, thus effectively closing the Form 483 observation letter that was

issued by the USFDA on April 13, 2017.

On the acquisition front, Lupin has acquired US based Symbiomix

Therapeutics, which has one branded oral bacterial vaginosis (BV) medicine

Solosec (approved by USFDA on September 15, 2017). The acquisition has

been made for a cash consideration of US$ 150 million including US$50

million upfront, other time based contingent and sales based royalty

payment (low mid teen). The acquisition will be funded from internal funds.

The company expects five to six years of payback of this acquisition. Lupin

is already selling branded Methergine in the gynaecology segment in US.

Finally, the Indian pharmaceutical market (IPM) grew 2.8% YoY to | 10420

crore for September. The volume growth has shown a revival this month.

However, the price component continues to be a dampener.

GST disturbance to be temporary but respite unlikely on US front

EIRs from the USFDA for clearance of plants are coming faster than

expected. This may further expedite product approvals, thus intensifying

competition. This will further intensify pricing pressure that has been the

core issue compared to compliance. From our I-direct universe, almost all

players with US franchisee are facing intense competition in the US owing

to client consolidation and increase in product approvals, leading to price

erosion in existing products to high single digit to low double digit.

Similarly, other issues/uncertainties in the US like pricing probe by the

Department of Justice (DoJ) and adapting to the bidding process are other

near term overhangs. Back home, domestic growth, post GST

implementation, has shown signs of a recovery. Despite a steep correction

in some stocks, the undercurrent remains cautious for the sector. However,

we expect the earnings momentum to normalise post H2FY19 on the back

of incremental product launches largely on speciality, biosimilar and

injectables front in the US besides normalising of Indian formulations

growth and recovery in emerging markets.

Health Check

Health Check

Stocks Performance

Mcap

Company 1M 3M YTD 1Y 17-Oct

Sun Pharma.Inds. 5 -4 -13 -25 131743

Cadila Health. 3 -7 40 28 51028

Cipla 10 11 9 6 49882

Lupin 6 -7 -28 -26 48157

Aurobindo Pharma 1 2 14 -5 44852

Dr Reddy's Labs 8 -12 -22 -21 39551

Divi's Lab. 1 20 12 -28 23287

Biocon 11 -6 22 22 23088

Torrent Pharma. 9 2 0 -19 22337

Glaxosmit Pharma 1 -4 -10 -18 20701

Glenmark Pharma. 2 -10 -31 -33 17297

Natco Pharma 22 0 70 65 17219

Apollo Hospitals 1 -14 -9 -21 14907

Ajanta Pharma -1 -19 -33 -37 10587

Jubilant Life -10 -9 2 -1 10257

Syngene Int. 2 -1 -12 -3 9889

Alembic Pharma 3 -8 -16 -27 9442

Strides Arcolab -10 -15 -17 -9 7917

Pfizer -3 -4 -5 -8 7891

Wockhardt 0 2 -4 -26 7011

Ipca Labs. -5 2 -7 -19 6277

Unichem Labs. 6 -7 -1 -11 2312

Indoco Remedies 24 24 -4 -21 2300

Return (%)

Market cap in | crore

Global Indices Performance

Company 1M 3M YTD 1Y 3Y 5Y

S&P 500 Pharm Index (US) 0 4 14 13 10 13

NASDAQ Biotechnology (US) 2 7 28 27 9 19

S&P Pharmaceuticals (US) 0 -2 10 3 -2 11

DJ Pharma and Biotech (US) 1 7 22 22 10 16

DJ STOXX Healthcare (EU) 2 0 9 11 8 12

TOPIX Pharma Index (Japan) 4 6 10 13 15 19

MSCI World Pharm & Biotech 1 5 20 18 7 13

NSE Pharma 4 -2 -5 -13 -1 12

Return (%)

Research Analyst

Siddhant Khandekar

Mitesh Shah

Harshal Mehta

ICICI Securities Ltd. | Retail Equity Research

Page 2

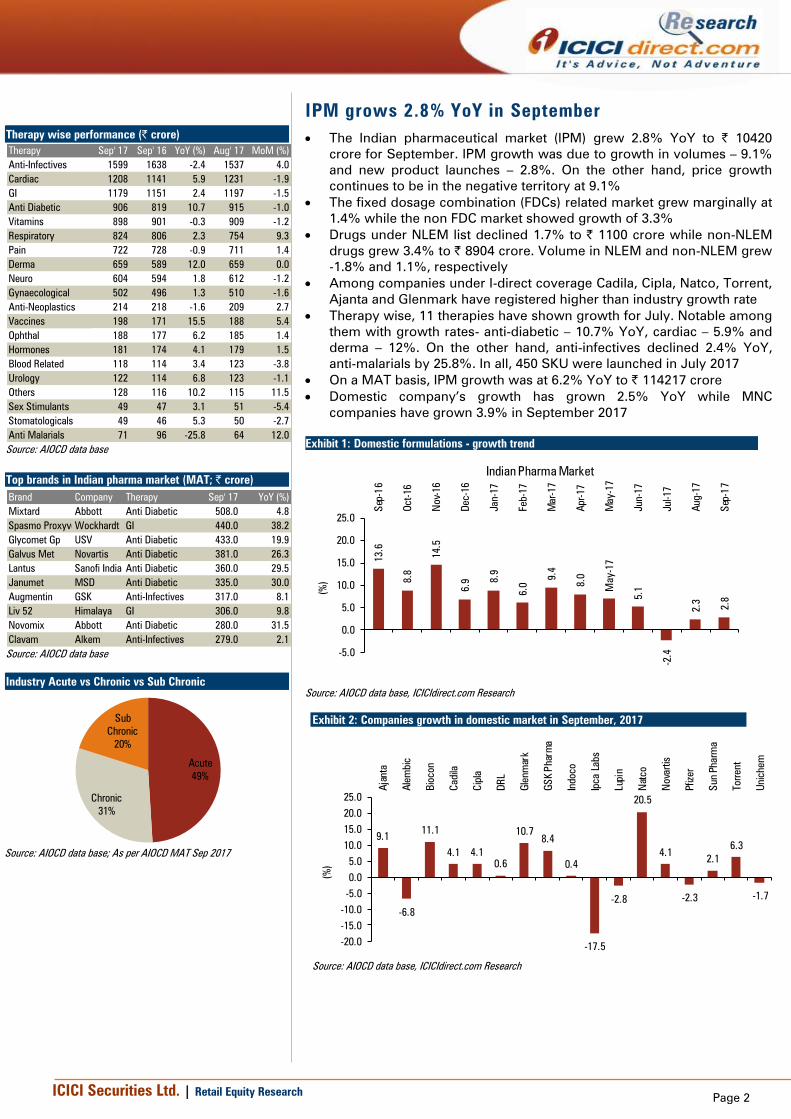

IPM grows 2.8% YoY in September

The Indian pharmaceutical market (IPM) grew 2.8% YoY to | 10420

crore for September. IPM growth was due to growth in volumes – 9.1%

and new product launches – 2.8%. On the other hand, price growth

continues to be in the negative territory at 9.1%

The fixed dosage combination (FDCs) related market grew marginally at

1.4% while the non FDC market showed growth of 3.3%

Drugs under NLEM list declined 1.7% to | 1100 crore while non-NLEM

drugs grew 3.4% to | 8904 crore. Volume in NLEM and non-NLEM grew

-1.8% and 1.1%, respectively

Among companies under I-direct coverage Cadila, Cipla, Natco, Torrent,

Ajanta and Glenmark have registered higher than industry growth rate

Therapy wise, 11 therapies have shown growth for July. Notable among

them with growth rates- anti-diabetic – 10.7% YoY, cardiac – 5.9% and

derma – 12%. On the other hand, anti-infectives declined 2.4% YoY,

anti-malarials by 25.8%. In all, 450 SKU were launched in July 2017

On a MAT basis, IPM growth was at 6.2% YoY to | 114217 crore

Domestic company’s growth has grown 2.5% YoY while MNC

companies have grown 3.9% in September 2017

Exhibit 1: Domestic formulations - growth trend

[

13.6

8.8

14.5

6.9 8

.9

6.0

9.4

8.0

May-17

5.1

-2.4

2.3

2.8

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Sep-1

6

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-1

7

(%

)

Indian Pharma Market

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 2: Companies growth in domestic market in September, 2017

9.1

-6.8

11.1

4.1 4.1

0.6

10.7

8.4

0.4

-17.5

-2.8

20.5

4.1

-2.3

2.1

6.3

-1.7

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Ajanta

Ale

mbic

Bio

con

Cadila

Cip

la

DR

L

Gle

nm

ark

GS

K P

harm

a

Indoco

Ipca Labs

Lupin

Natco

Novartis

Pfiz

er

Sun P

harm

a

Torrent

Unic

hem

(%

)

Source: AIOCD data base, ICICIdirect.com Research

Therapy wise performance (| crore)

Therapy Sep' 17 Sep' 16 YoY (%) Aug' 17 MoM (%)

Anti-Infectives 1599 1638 -2.4 1537 4.0

Cardiac 1208 1141 5.9 1231 -1.9

GI 1179 1151 2.4 1197 -1.5

Anti Diabetic 906 819 10.7 915 -1.0

Vitamins 898 901 -0.3 909 -1.2

Respiratory 824 806 2.3 754 9.3

Pain 722 728 -0.9 711 1.4

Derma 659 589 12.0 659 0.0

Neuro 604 594 1.8 612 -1.2

Gynaecological 502 496 1.3 510 -1.6

Anti-Neoplastics 214 218 -1.6 209 2.7

Vaccines 198 171 15.5 188 5.4

Ophthal 188 177 6.2 185 1.4

Hormones 181 174 4.1 179 1.5

Blood Related 118 114 3.4 123 -3.8

Urology 122 114 6.8 123 -1.1

Others 128 116 10.2 115 11.5

Sex Stimulants 49 47 3.1 51 -5.4

Stomatologicals 49 46 5.3 50 -2.7

Anti Malarials 71 96 -25.8 64 12.0

Source: AIOCD data base

Top brands in Indian pharma market (MAT; | crore)

Brand Company Therapy Sep' 17 YoY (%)

Mixtard Abbott Anti Diabetic 508.0 4.8

Spasmo Proxyvon PlusWockhardt GI 440.0 38.2

Glycomet Gp USV Anti Diabetic 433.0 19.9

Galvus Met Novartis Anti Diabetic 381.0 26.3

Lantus Sanofi India Anti Diabetic 360.0 29.5

Janumet MSD Anti Diabetic 335.0 30.0

Augmentin GSK Anti-Infectives 317.0 8.1

Liv 52 Himalaya GI 306.0 9.8

Novomix Abbott Anti Diabetic 280.0 31.5

Clavam Alkem Anti-Infectives 279.0 2.1

Source: AIOCD data base

Industry Acute vs Chronic vs Sub Chronic

Acute

49%

Chronic

31%

Sub

Chronic

20%

Source: AIOCD data base; As per AIOCD MAT Sep 2017

ICICI Securities Ltd. | Retail Equity Research

Page 3

IPM grows 1% in Q2FY18

The Indian pharmaceutical market (IPM) grew 1% YoY to | 30037 crore

in Q2FY18. Growth was mainly driven by new product launches – 2.8%

followed by flat volume growth and price decline of 1.8%

The fixed dosage combination (FDCs) related market de-grew 8.7% to

| 541 crore

Drugs under NLEM list declined 5.9% to | 3136 crore while non-NLEM

drugs posted growth of 1.8% to | 25687 crore. Volume de-growth in

NLEM was 3.7% while for non-NLEM the de-growth was 1.1%

Among companies under I-direct coverage Ajanta, Biocon, Glenmark,

Lupin, Sun Pharma, Torrent and Cadila have outperformed IPM growth

Therapy wise, 14 therapies have outpaced IPM growth. Notable among

them with growth rates- anti diabetic –11.3%, cardiac – 6.3% & derma –

10.6%

Domestic companies have grown 0.3% while MNC companies have

grown 3.6% in Q2FY18

Exhibit 3: Domestic formulations - quarterly growth trend

3.8

6.7

2.2

-0.4

7.9

4.83.9

2.6

0.0

4.6

5.0

5.2

4.5

2.5

1.8

1.32.1

-1.8

3.6

3.3

3.7

3.7

3.7

3.7

3.33.0

2.8

12.0

15.0

11.0

7.8

14.1

10.3

8.67.6

1.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

19.0

2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17 1QFY18 2QFY18

(%

)

Volumes Price Increases New Products

[

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 4: Company wise growth trends in Q2FY18

6.4

(10.7)

9.7

(1.0)

0.8

4.9 5.5

(8.0)

(16.8)

2.6

(5.8)

7.9

(5.7)

5.8

1.1

4.6

(5.1)

3.8 4.8

(22.0)

(17.0)

(12.0)

(7.0)

(2.0)

3.0

8.0

13.0

18.0

23.0

28.0

Ajanta

Ale

mbic

Bio

con

Cip

la

Dr Reddy's

GS

K P

harm

a

Gle

nm

ark

Indoco

Ipca

Lupin

Natco

Novartis

Pfiz

er

Sanofi In

dia

Sun P

harm

a

Torrent

Unic

hem

Wockhardt

Cadila

(%

)

Source: AIOCD data base, ICICIdirect.com Research

Therapy wise performance (| crore)

Therapy Q2FY18 Q2FY17 YoY (%) Q1FY18 QoQ (%)

Anti-Infectives 4400 4825 -8.8 3698 19.0

Cardiac 3596 3382 6.3 3578 0.5

GI 3521 3486 1.0 3482 1.1

Anti Diabetic 2698 2424 11.3 2696 0.1

Vitamins 2656 2658 -0.1 2580 2.9

Respiratory 2181 2315 -5.8 1723 26.6

Pain 2068 2116 -2.3 1914 8.1

Derma 1905 1723 10.6 1773 7.5

Neuro 1777 1721 3.3 1732 2.6

Gynaecological 1496 1479 1.1 1529 -2.2

Anti-Neoplastics 602 593 1.5 580 3.9

Vaccines 565 512 10.3 569 -0.7

Ophthal 546 517 5.5 572 -4.6

Hormones 517 493 5.0 487 6.2

Blood Related 363 340 7.0 375 -3.0

Urology 360 337 6.7 337 6.7

Others 346 319 8.6 325 6.5

Sex Stimulants 145 141 2.9 159 -9.0

Stomatologicals 144 137 5.5 141 2.3

Anti Malarials 180 257 -30.0 98 84.0

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 4

Domestic Formulations – I-Direct Coverage universe data summary

Exhibit 5: Domestic formulations – Market share (MAT Value Sep-17)

[

8.4%

4.7%4.2%

3.1%

2.2% 2.2% 2.1%

1.5%1.3%

0.9% 0.7% 0.6% 0.6% 0.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

Sun

Cip

la

Cadila

Lupin

Torrent

Dr. R

eddys

Gle

nm

ark

IPCA

Ale

mbic

Unic

hem

Indoco Rem

edie

s

Natco

Ajanta

Bio

con

Market Share

Market Share

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 6: Acute vs Chronic vs Sub Chronic (MAT Value Sep-17)

38

58

21

47 5040

83

67

33

93

41

2336

49

5122

70

4129

36

627

49

0

46

52

58 32

1219

9 1221 23

12 619

714

25

618

0

20

40

60

80

100

120

Ajanta

Ale

mbic

Bio

con

Cip

la

Dr. R

eddys

Gle

nm

ark

Indoco

IPCA

Lupin

Natco

Sun

Torrent

Unic

hem

Cadila

%

Acute Chronic Sub Chronic

Source: AIOCD data base, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 5

Exhibit 7: Top five brands in value terms (MAT value Sep-17)

[5

Sun Brand Therapy Sales (|cr)

1 Volini Pain 235

2 Istamet Anti Diabetic 224

3 Rosuvas Cardiac 221

4 Gemer Anti Diabetic 200

5 Levipil Neuro 186

Cipla Brand Therapy Sales (|cr)

1 Foracort Respiratory 240

2 Duolin Respiratory 190

3 Seroflo Respiratory 154

4 Budecort Respiratory 143

5 Asthalin Respiratory 141

Cadila Brand Therapy Sales (|cr)

1 Skinlite Derma 194

2 Deriphyllin Respiratory 117

3 Pantodac GI 113

4 Mifegest Kit Gynaecological 110

5 Atorva Cardiac 108

Lupin Brand Therapy Sales (|cr)

1 Gluconorm-G Anti Diabetic 191

2 Budamate Respiratory 104

3 Tonact Cardiac 91

4 Rablet-D GI 65

5 Rablet GI 54

Torrent Brand Therapy Sales (|cr)

1 Shelcal Vitamins 186

2 Chymoral FortePain 112

3 Nikoran Cardiac 96

4 Azulix-Mf Anti Diabetic 87

5 Nebicard Cardiac 81

Dr. Reddys Brand Therapy Sales (|cr)

1 Omez GI 113

2 Omez D GI 103

3 Econorm GI 72

4 Atarax Respiratory 71

5 Razo D GI 64

Glenmark Brand Therapy Sales (|cr)

1 Telma Cardiac 178

2 Telma H Cardiac 171

3 Ascoril Plus Respiratory 116

4 Candid Derma 113

5 Candid-B Derma 96

IPCA Brand Therapy Sales (|cr)

1 Zerodol Sp Pain 121

2 Zerodol P Pain 94

3 Hcqs Anti Malarials 84

4 Larinate Anti Malarials 55

5 Glycinorm M Anti Diabetic 47

Alembic Brand Therapy Sales (|cr)

1 Azithral Anti-Infectives 145

2 Althrocin Anti-Infectives 75

3 Wikoryl Respiratory 57

4 Gestofit Gynaecological 55

5 Roxid Anti-Infectives 49

Unichem Brand Therapy Sales (|cr)

1 Losar H Cardiac 102

2 Losar Cardiac 74

3 Ampoxin Anti-Infectives 68

4 Unienzyme GI 61

5 Vizylac GI 32

Natco Brand Therapy Sales (|cr)

1 Hepcinat Anti-Infectives 201

2 Geftinat Anti-Neoplastics 146

3 Veenat Anti-Neoplastics 101

4 Erlonat Anti-Neoplastics 100

5 Natdac Anti-Infectives 88

Indoco Brand Therapy Sales (|cr)

1 Febrex Plus Respiratory 78

2 Cyclopam GI 48

3 Oxipod Anti-Infectives 44

4 Sensodent-K Stomatologicals 38

5 Cital Urology 35

Ajanta Brand Therapy Sales (|cr)

1 Met Xl Cardiac 83

2 Atorfit Cv Cardiac 51

3 Melacare Derma 49

4 Feburic Pain 24

5 Rosufit Cv Cardiac 22

Biocon Brand Therapy Sales (|cr)

1 Insugen Anti Diabetic 107

2 Basalog Anti Diabetic 75

3 Canmab Anti-Neoplastics 34

4 Erypro Blood Related 27

5 Insugen R Anti Diabetic 23

Source: Bloomberg, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 6

Exhibit 8: Top five therapies in value term (MAT value Sep-17)

[5

Sun Therapy Sales (|cr)

1 Anti-Infectives 977

2 Cardiac 1850

3 GI 1140

4 Anti Diabetic 931

5 Vitamins 380

Cipla Therapy Sales (|cr)

1 Anti-Infectives 1247

2 Cardiac 659

3 GI 400

4 Anti Diabetic 51

5 Vitamins 75

Cadila Therapy Sales (|cr)

1 Anti-Infectives 730

2 Cardiac 626

3 GI 556

4 Anti Diabetic 143

5 Vitamins 206

Lupin Therapy Sales (|cr)

1 Anti-Infectives 665

2 Cardiac 927

3 GI 310

4 Anti Diabetic 564

5 Vitamins 183

Torrent Therapy Sales (|cr)

1 Anti-Infectives 79

2 Cardiac 772

3 GI 415

4 Anti Diabetic 200

5 Vitamins 373

Dr. Reddys Therapy Sales (|cr)

1 Anti-Infectives 198

2 Cardiac 355

3 GI 540

4 Anti Diabetic 176

5 Vitamins 76

Glenmark Therapy Sales (|cr)

1 Anti-Infectives 377

2 Cardiac 626

3 GI 97

4 Anti Diabetic 176

5 Vitamins 55

IPCA Therapy Sales (|cr)

1 Anti-Infectives 95

2 Cardiac 266

3 GI 120

4 Anti Diabetic 83

5 Vitamins 37

Alembic Therapy Sales (|cr)

1 Anti-Infectives 320

2 Cardiac 219

3 GI 184

4 Anti Diabetic 110

5 Vitamins 113

Unichem Therapy Sales (|cr)

1 Anti-Infectives 150

2 Cardiac 425

3 GI 111

4 Anti Diabetic 59

5 Vitamins 22

Natco Therapy Sales (|cr)

1 Anti-Infectives 401

2 Cardiac 1

3 GI 0

4 Anti Diabetic 0

5 Respiratory 0

Indoco Therapy Sales (|cr)

1 Anti-Infectives 134

2 Cardiac 10

3 GI 109

4 Anti Diabetic 30

5 Vitamins 58

Ajanta Therapy Sales (|cr)

1 Anti-Infectives 15

2 Cardiac 277

3 GI 14

4 Anti Diabetic 15

5 Vitamins 30

Biocon Therapy Sales (|cr)

1 Anti-Infectives 11

2 Cardiac 15

3 GI 3

4 Anti Diabetic 243

5 Vitamins 1

Source: Bloomberg, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 7

Exhibit 9: Summary of USFDA approvals for Sep, 2017

[5

Company Drug Name Therapeutic Area Innovator company Generic Version of Market Size

Sun Pharma Fenofibrate Tablets Anti-Cholesterol Abbott Tricor US$ 307 million

Glenmark Pharma Propafenone Hydrochloride Arrhythmia Glaxosmithkline Pharma Rythmol Sr US$ 44 million

Lupin Metronidazole Tablets Anti-Infective Gd Searle Flagyl US$ 69 million

Cadila Healthcare Modafinil Insomnia Cephalon Provigil US$ 149 million

Glenmark Pharma Desonide Dermatology Galderma Labs Desowen US$ 23 million

Cadila Healthcare Donepezil Hydrochloride Cns Eisai Inc. Aricept US$ 52 million

Cadila Healthcare Itraconazole Anti- Fungal Janssen Pharma Sporanox US$ 42 million

Cadila Healthcare Desoximetasone Crèam Dermatology Taro Topicort Lp Emollient US$ 33 million

Glenmark Pharma Nitroglycerin Cvs Pfizer Nitrostat US$ 113 million

Unichem Labs Irbesartan; Hydrochlorothiazide Cvs Sanofi Aventis Avalide NA

Cadila Healthcare Labetalol Hydrochloride Cvs Cnty Line Pharma Trandate NA

Cadila Healthcare Amlodipine And Omlesartan Medoxomil Bloodpressure Daiichi Sankyo Azor US$ 174 million

Lupin Clobetasol Propionate Spray Dermatology Galderma Labs Clobex US$ 14 million

Cadila Healthcare Indomethacin Anti-Inflammatory Iroko Pharma Tivorbex US$ 6 million

Lupin Doxycycline Hyclate Anti-Infective Pfizer Vibra US$ 150 million

Cadila Healthcare Doxycycline Hyclate Anti-Infective Pfizer Vibra US$ 150 million

Ajanta Pharma Rivastigmine Tartrate Cns Novartis Exelon US$ 26.7 million

Dr Reddy'S Sevelamer Carbonate Nephrology Genzyme Renvela US$ 1.9 billion

Company Drug Name Therapeutic Area Innovator company Generic Version of Market Size

Cadila Healthcare Solifenacin Succinate Urology Astellas Pharma Vesicare US$ 1 billion

Cipla Efavirenz;Lamivudine;Tenofovir Disoproxil Fumarate Antivirtal Mylan Telura NA

Cadila Healthcare Pregabalin Tablets Cns Forest Lyrica NA

Aurobindo Lorcaserin Hydrochloride Weight Loss Arena Pharma Belviq NA

Tentative Approvals

ICICI Securities Ltd. | Retail Equity Research

Page 8

Exhibit 10: US patent litigations [5

Month Innovator ANDA Filer Brand Name API Used for

May-17 Takeda Pharma Torrent Pharma Nesina Alogliptin Diabetes

May-17 Takeda Pharma Glenmark Qudexy XR Topiramate Epilepsy

Jun-17 Allergan Taro Pharma Aczone Dapsone Leprosy

Jun-17 Genentech Sun Pharma Tarceva Erlotinib Cancer

Jun-17 Bayer AG Alembic Pharma Xarelto Rivaroxaban Blood Thinner

Jun-17 Teva Dr Reddy's Lab Copaxone Glatiramer Multiple Sclerosis

Jun-17 Valeant Pharma Sun Pharma Uceris Budesonide Ulcerative Colitis

Jun-17 Omeros Corp Lupin Omidria Phenylephrine And Ketorolac Pupil Dilation

Jun-17 Amgen Lupin Sensipar Cinacalcet Calcium Reducer

Jun-17 Biogen Aurobindo Pharma Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jun-17 Biogen Sun Pharma Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jun-17 Biogen Cipla Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jun-17 Biogen Glenmark Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jun-17 Biogen Lupin Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jun-17 Biogen Torrent Pharma Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jun-17 Forest Laboratories Sun Pharma Linzess Linaclotide Irritable Bowel Syndrome

Jun-17 Biogen Torrent Pharma Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jun-17 Biogen Cadila healthcare Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jul-17 Janssen Pharma Aurobindo Pharma Invokana Canagliflozin Diabetes

Jul-17 Actelion Pharma Sun Pharma Veletri Epoprostenol Pulmonary Arterial Hypertension

Jul-17 Biogen Cadila healthcare Tecfidera Dimethyl Fumarate Multiple Sclerosis

Jul-17 Delcor Asset Corp Sun Pharma Evoclin Clindamycin Acne vulgaris

Jul-17 Celgene Corp Dr Reddy's Lab Revlimid Lenalidomide Oncology

Jul-17 PreCision Dermatology Lupin Locoid Hydrocortisone butyrate Dermatitis

Jul-17 BMS Cadila healthcare Reyataz Atazanavir HIV

Jul-17 Endo Pharma Lupin Nascobal Cyanocobalamin Vitamin B12 deficiency

Jul-17 Bayer Sun Pharma Aczone Clindamycin Acne vulgaris

Aug-17 Bayer AG Lupin Xarelto Rivaroxaban Blood Thinner

Aug-17 Horizon Therapeutics Lupin Ravicti Glycerol Phenylbutyrate Inborn Urea Cycle Disorder

Aug-17 Celgene Cipla Revlimid Lenalidomide Oncology

Aug-17 Kissei Pharmaceuticals Aurobindo Rapaflo Silodosin Enlarged Prostate

Aug-17 Bayer AG Torrent Pharma Xarelto Rivaroxaban Blood Thinner

Aug-17 Forest Laboratories Aurobindo Linzess Linaclotide Irritable Bowel Syndrome

Aug-17 Alcon Research Cipla Pazeo Olopatadine Ocular Itching

Aug-17 Sanofi-Aventis Aurobindo Multaq Dronedarone Atrial Fibrillation

Sep-17 Janssen Products LP Aurobindo Prezista Darunavir Hiv

Sep-17 Allergan Aurobindo Lastacaft Alcaftadine Allergic Conjunctivitis

Sep-17 Eli Lilly and Co Glenmark Cialis Tadalafil Erectile Dysfunction

Sep-17 Indivior Dr Reddy's Lab Suboxone Buprenorphine Opioid Dependence

Sep-17 Teijin Ltd Aurobindo Uloric Febuxostat Gout

Sep-17 Takeda Pharma Indoco Remedies Nesina Alogliptin Diabetes

Sep-17 Allergan, Inc Alembic Pharma Latisse Bimatoprost Hypotrichosis

Sep-17 Wyeth Pharma Sun Pharma Bosulif Bosutinib Leukemia

Source: Bloomberg, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 9

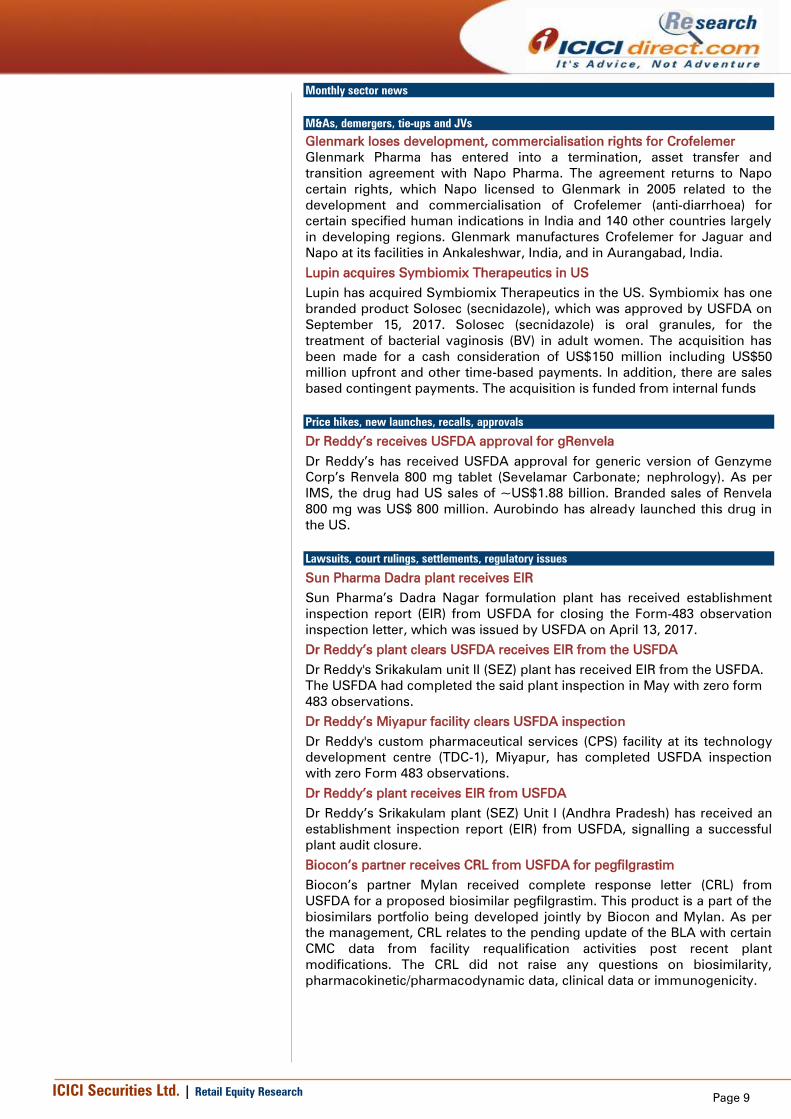

Monthly sector news

M&As, demergers, tie-ups and JVs

Glenmark loses development, commercialisation rights for Crofelemer

Glenmark Pharma has entered into a termination, asset transfer and

transition agreement with Napo Pharma. The agreement returns to Napo

certain rights, which Napo licensed to Glenmark in 2005 related to the

development and commercialisation of Crofelemer (anti-diarrhoea) for

certain specified human indications in India and 140 other countries largely

in developing regions. Glenmark manufactures Crofelemer for Jaguar and

Napo at its facilities in Ankaleshwar, India, and in Aurangabad, India.

Lupin acquires Symbiomix Therapeutics in US

Lupin has acquired Symbiomix Therapeutics in the US. Symbiomix has one

branded product Solosec (secnidazole), which was approved by USFDA on

September 15, 2017. Solosec (secnidazole) is oral granules, for the

treatment of bacterial vaginosis (BV) in adult women. The acquisition has

been made for a cash consideration of US$150 million including US$50

million upfront and other time-based payments. In addition, there are sales

based contingent payments. The acquisition is funded from internal funds

Price hikes, new launches, recalls, approvals

Dr Reddy’s receives USFDA approval for gRenvela

Dr Reddy’s has received USFDA approval for generic version of Genzyme

Corp’s Renvela 800 mg tablet (Sevelamar Carbonate; nephrology). As per

IMS, the drug had US sales of ~US$1.88 billion. Branded sales of Renvela

800 mg was US$ 800 million. Aurobindo has already launched this drug in

the US.

Lawsuits, court rulings, settlements, regulatory issues

Sun Pharma Dadra plant receives EIR

Sun Pharma’s Dadra Nagar formulation plant has received establishment

inspection report (EIR) from USFDA for closing the Form-483 observation

inspection letter, which was issued by USFDA on April 13, 2017.

Dr Reddy’s plant clears USFDA receives EIR from the USFDA

Dr Reddy's Srikakulam unit II (SEZ) plant has received EIR from the USFDA.

The USFDA had completed the said plant inspection in May with zero form

483 observations.

Dr Reddy’s Miyapur facility clears USFDA inspection

Dr Reddy's custom pharmaceutical services (CPS) facility at its technology

development centre (TDC-1), Miyapur, has completed USFDA inspection

with zero Form 483 observations.

Dr Reddy’s plant receives EIR from USFDA

Dr Reddy’s Srikakulam plant (SEZ) Unit I (Andhra Pradesh) has received an

establishment inspection report (EIR) from USFDA, signalling a successful

plant audit closure.

Biocon’s partner receives CRL from USFDA for pegfilgrastim

Biocon’s partner Mylan received complete response letter (CRL) from

USFDA for a proposed biosimilar pegfilgrastim. This product is a part of the

biosimilars portfolio being developed jointly by Biocon and Mylan. As per

the management, CRL relates to the pending update of the BLA with certain

CMC data from facility requalification activities post recent plant

modifications. The CRL did not raise any questions on biosimilarity,

pharmacokinetic/pharmacodynamic data, clinical data or immunogenicity.

ICICI Securities Ltd. | Retail Equity Research

Page 10

NPPA, DoP proposes changes in price setting method

National Pharmaceutical Pricing Authority (NPPA) and the Department of

Pharmaceuticals (DoP) have proposed and amendment to the four-year-old

Drug Price Control Order (DPCO), which aims to bring non-scheduled drugs

under price control by changing the price setting method. Also, if a

company is launching a new drug that may be a combination of a

scheduled and a non-scheduled drug, the regulator will fix the ceiling price

of the drug.

Others

Aurobindo Pharma enters multilateral deal for ARV treatment

Aurobindo Pharma has entered into a multilateral agreement with

Government of South Africa and Kenya as well as UNAIDS, Bill & Melinda

Gates foundation, etc, to provide a new class of anti-retroviral (ARV)

treatment to low-and middle-income countries. Aurobindo and Mylan Lab

are the two firms that will supply the once-a-day generic fixed-dose

combination of tenofovir disoproxil fumarate, lamivudine and Dolutegravir

(TLD) under this initiative

Amgen delays its launch of its biosimilar version of AbbVie’s Humira

Amgen has reached settlement with Abbvie that will delay the launch of

Amgen’s biosimilar version of AbbVie’s Humira (osteoarthritis) till January

31, 2023. Biocon’s biosimilar version of Humira is currently in global Phase

III clinical trials.

Exhibit 11: One year forward PE

0.0

10.0

20.0

30.0

40.0

50.0

9/21/201

1

3/21/201

2

9/21/201

2

3/21/201

3

9/21/201

3

3/21/201

4

9/21/201

4

3/21/201

5

9/21/201

5

3/21/201

6

9/21/201

6

3/21/201

7

9/21/201

7

x

NSE Pharma Nifty

27% Premium

Source: ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 11

ICICIdirect.com coverage universe (Healthcare)

Company I-Direct CMP TP Rating M Cap

Code (|) (|) (| Cr) FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E

Ajanta Pharma AJAPHA 1202 1,420 Buy 10590.8 110.0 56.6 51.8 67.1 10.9 21.2 23.2 17.9 46.2 41.8 30.5 31.5 37.3 33.2 24.5 25.3

Alembic Pharma ALEMPHA 500 570 Hold 9431.5 38.2 21.2 19.7 28.8 13.1 23.6 25.4 17.4 52.2 25.3 19.2 23.9 45.1 21.0 16.9 20.8

Apollo Hospitals APOHOS 1071 1,180 Hold 14900.3 13.2 15.9 6.9 19.5 81.1 67.4 155.9 55.0 6.6 6.0 5.8 8.9 5.3 6.0 2.5 6.7

Aurobindo Pharma AURPHA 767 745 Hold 44937.2 33.9 38.8 46.1 40.6 22.6 19.8 16.6 18.9 23.1 24.4 25.2 19.3 27.2 24.2 22.7 16.8

Biocon BIOCON 385 380 Hold 23124.0 7.7 11.0 7.6 13.6 50.0 35.1 50.5 28.3 9.3 11.9 10.0 16.0 11.5 13.6 8.8 14.0

Cadila Healthcare CADHEA 498 440 Hold 50987.5 15.0 14.5 19.4 22.8 33.3 34.2 25.7 21.9 24.9 13.1 17.3 19.8 34.4 21.4 23.5 22.9

Cipla CIPLA 613 525 Hold 49391.6 18.5 12.5 21.6 26.1 33.2 48.9 28.3 23.5 11.8 7.7 12.6 14.2 12.9 8.0 12.5 13.4

Divi's Lab DIVLAB 875 665 Hold 23232.5 41.5 39.3 34.9 41.5 21.1 22.3 25.1 21.1 31.0 25.0 20.4 21.4 25.7 19.5 15.5 16.3

Dr Reddy's Labs DRREDD 2388 2,400 Hold 39587.8 141.4 70.6 70.2 125.0 16.9 33.8 34.0 19.1 15.3 6.1 6.6 11.9 19.2 9.5 8.8 13.8

Glenmark Pharma GLEPHA 612 730 Hold 17294.1 32.2 46.0 40.7 40.3 19.0 13.3 15.1 15.2 16.2 18.9 16.5 15.4 21.2 25.5 18.6 15.7

Indoco Remedies INDREM 250 180 Hold 2303.8 9.4 8.4 5.4 12.2 26.7 29.9 46.4 20.5 12.9 8.4 6.0 12.1 14.8 12.0 7.3 14.6

Ipca Laboratories IPCLAB 499 410 Hold 6283.4 7.4 15.4 12.4 25.5 67.6 32.4 40.2 19.5 4.5 8.7 6.9 12.5 4.1 7.9 6.1 11.3

Jubilant Life JUBLIF 643 845 Buy 10236.2 26.0 36.1 46.9 58.4 24.7 17.8 13.7 11.0 12.0 13.3 15.4 17.4 14.2 16.8 18.1 18.6

Lupin LUPIN 1066 1,070 Hold 48193.2 50.4 56.6 40.4 52.6 21.2 18.8 26.4 20.3 17.8 16.6 12.2 15.3 20.3 18.9 12.2 14.0

Natco Pharma NATPHA 989 1,065 Buy 17239.0 9.0 27.0 26.4 15.8 109.4 36.6 37.5 62.4 16.0 33.0 28.1 16.0 12.2 28.8 23.2 12.6

Sun Pharma SUNPHA 548 445 Hold 131898.6 23.4 29.0 14.5 20.0 23.4 18.9 37.8 27.4 18.6 19.8 9.7 12.3 18.0 19.0 9.0 11.2

Syngene Int. SYNINT 494 490 Hold 9871.0 11.1 14.3 14.3 17.4 43.9 33.9 33.9 27.9 14.1 16.8 16.2 17.8 21.6 20.3 17.2 17.4

Torrent Pharma TORPHA 1315 1,260 Hold 22264.7 110.9 55.2 48.9 66.2 11.9 23.8 26.9 19.9 46.5 18.9 17.8 20.8 53.7 21.5 16.7 19.3

Unichem Lab UNILAB 254 235 Hold 2312.1 12.3 12.0 12.5 19.4 20.6 21.2 20.3 13.1 13.8 11.8 11.0 15.6 11.7 10.2 9.8 13.4

RoE (%)EPS (|) PE(x) RoCE (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 12

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Add, Reduce and Sell. The performance horizon is two years unless specified and the

notional target price is defined as the analysts' valuation for a stock.

Sector view:

Over weight compared to index

Equal weight compared to index

Under weight compared to index

Index here refers to BSE 500

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No. 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd. | Retail Equity Research

Page 13

ANALYST CERTIFICATION

We /I, Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance), Harshal Mehta (MTech) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed

in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific

recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance), Harshal Mehta (MTech) Research Analysts of this report have not received any compensation from the companies mentioned

in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance), Harshal Mehta (MTech) Research Analysts do not serve as an officer, director or employee of the companies mentioned in

the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation

or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any

material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER Mitesh Shah MS (Finance), Harshal Mehta (MTech) Research Analysts of this report have not received any compensation from the companies mentioned

in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the

publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.