Embed Size (px)

Citation preview

Swedish Real Estate Market 2015FEDESSA Swedish Self Storage Association Conference September 3, 2015

FEDESSA | Cushman & Wakefield

More money than ever targeting European and Nordic CRE

Investors are still more risk-averse than previous cyclical peak

Need for new products and markets to satisfy investment targets

Investment themes Transaction market characteristics

FEDESSA | Cushman & Wakefield

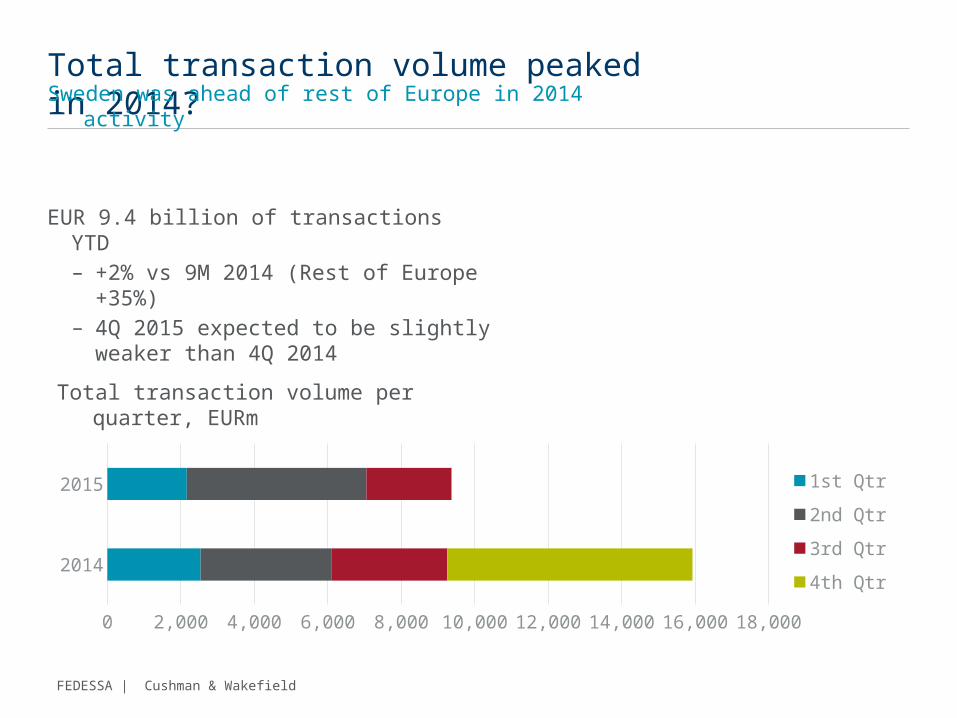

EUR 9.4 billion of transactions YTD– +2% vs 9M 2014 (Rest of Europe +35%)– 4Q 2015 expected to be slightly weaker

than 4Q 2014

2014

2015

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

1st Qtr

2nd Qtr

3rd Qtr

4th Qtr

Total transaction volume per quarter, EURm

Total transaction volume peaked in 2014?Sweden was ahead of rest of Europe in 2014 activity

FEDESSA | Cushman & Wakefield

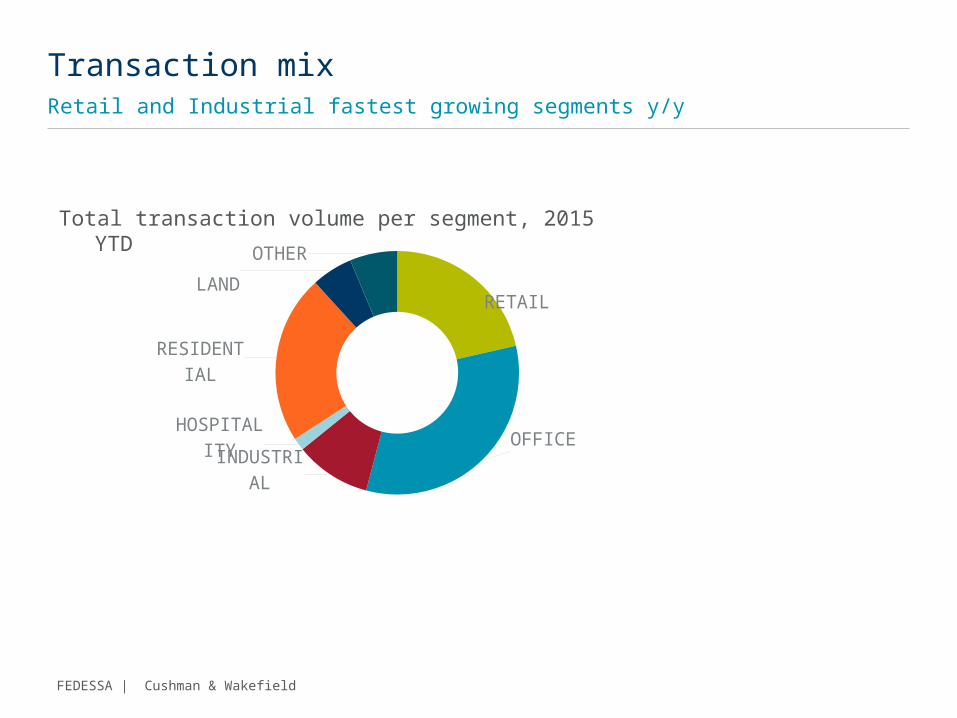

RETAIL

OFFICEIN-

DUS-TRIAL

HOS-PITAL-

ITY

RESI-DENTIAL

LAND

OTHER

Total transaction volume per segment, 2015 YTD

Transaction mix Retail and Industrial fastest growing segments y/y

FEDESSA | Cushman & Wakefield

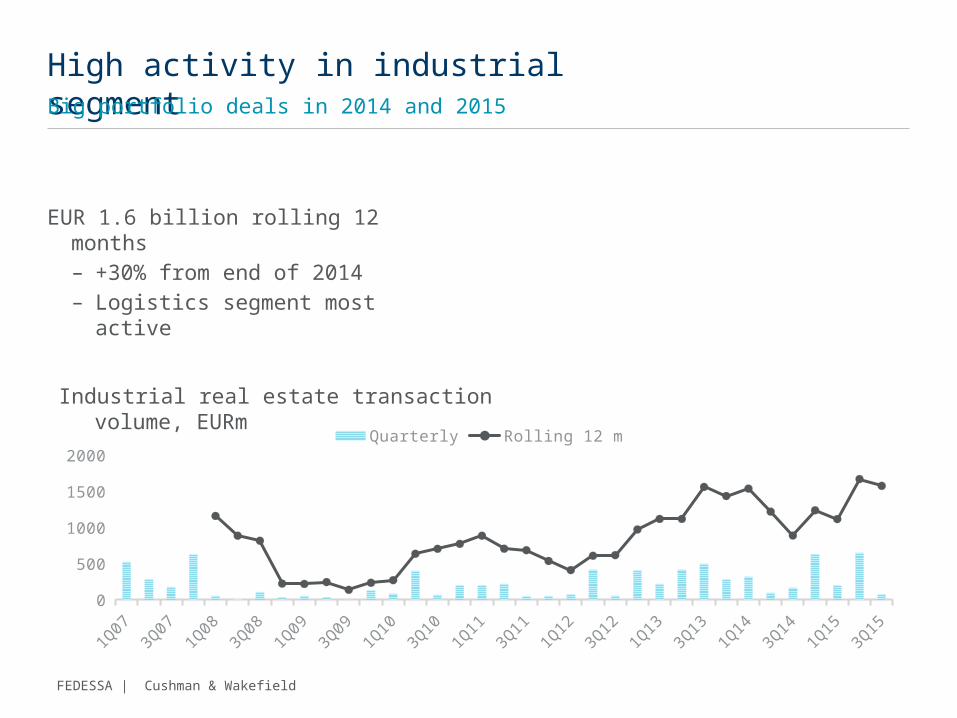

EUR 1.6 billion rolling 12 months– +30% from end of 2014– Logistics segment most active

High activity in industrial segment Big portfolio deals in 2014 and 2015

Industrial real estate transaction volume, EURm

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

0200400600800

10001200140016001800

Quarterly Rolling 12 m

FEDESSA | Cushman & Wakefield

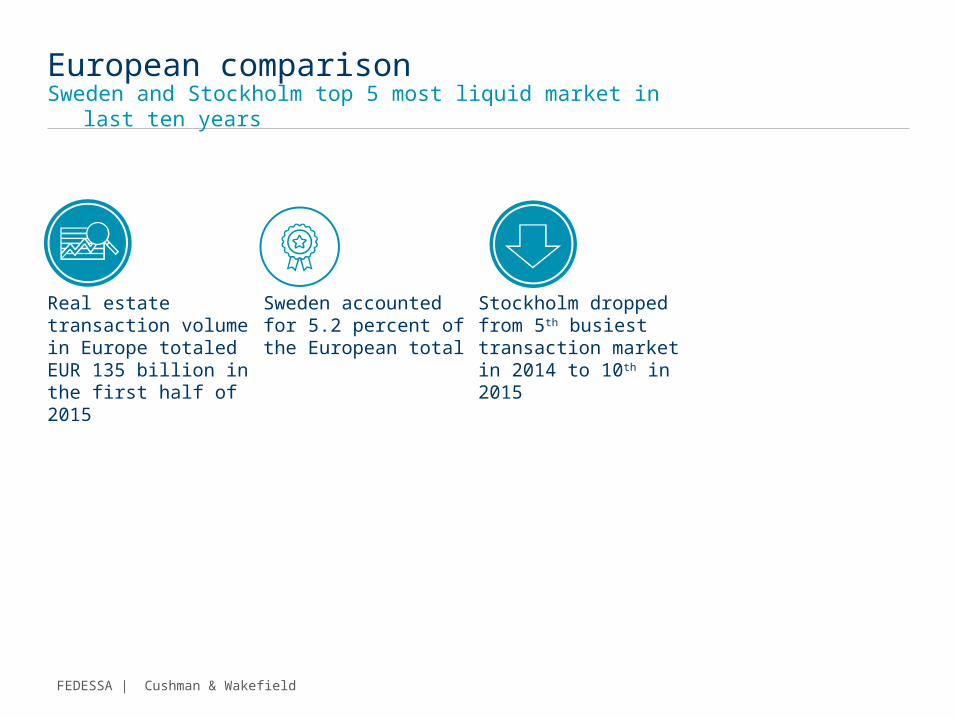

Real estate transaction volume in Europe totaled EUR 135 billion in the first half of 2015

European comparisonSweden and Stockholm top 5 most liquid market in last ten years

Sweden accounted for 5.2 percent of the European total

Stockholm dropped from 5th busiest transaction market in 2014 to 10th in 2015

FEDESSA | Cushman & Wakefield

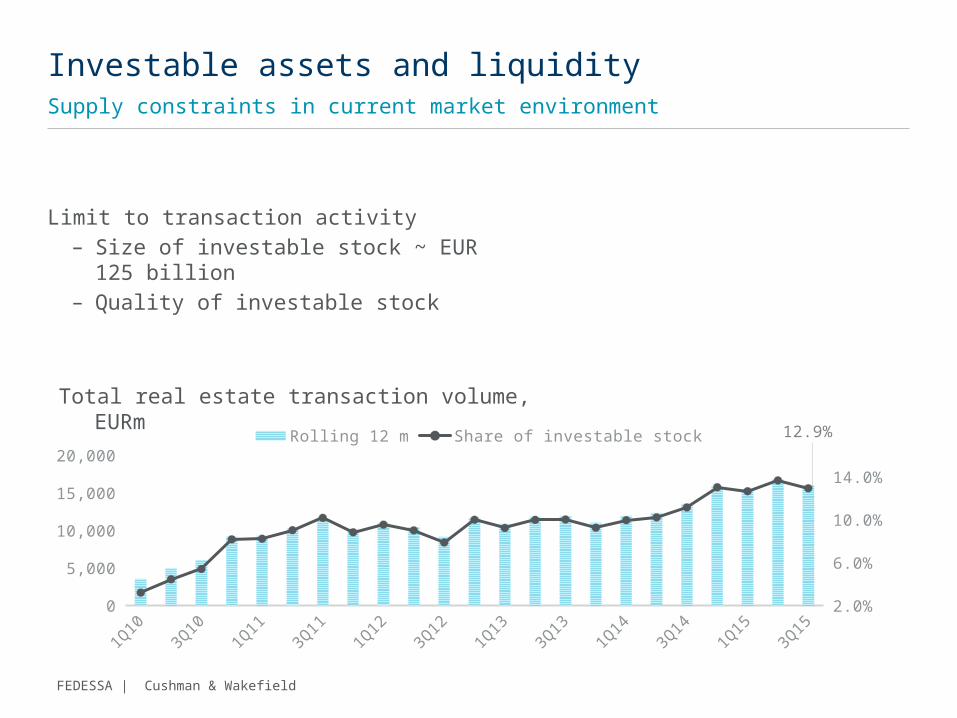

Limit to transaction activity– Size of investable stock ~ EUR 125 billion– Quality of investable stock

Investable assets and liquiditySupply constraints in current market environment

Total real estate transaction volume, EURm

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%12.9%Rolling 12 m Share of investable stock

FEDESSA | Cushman & Wakefield

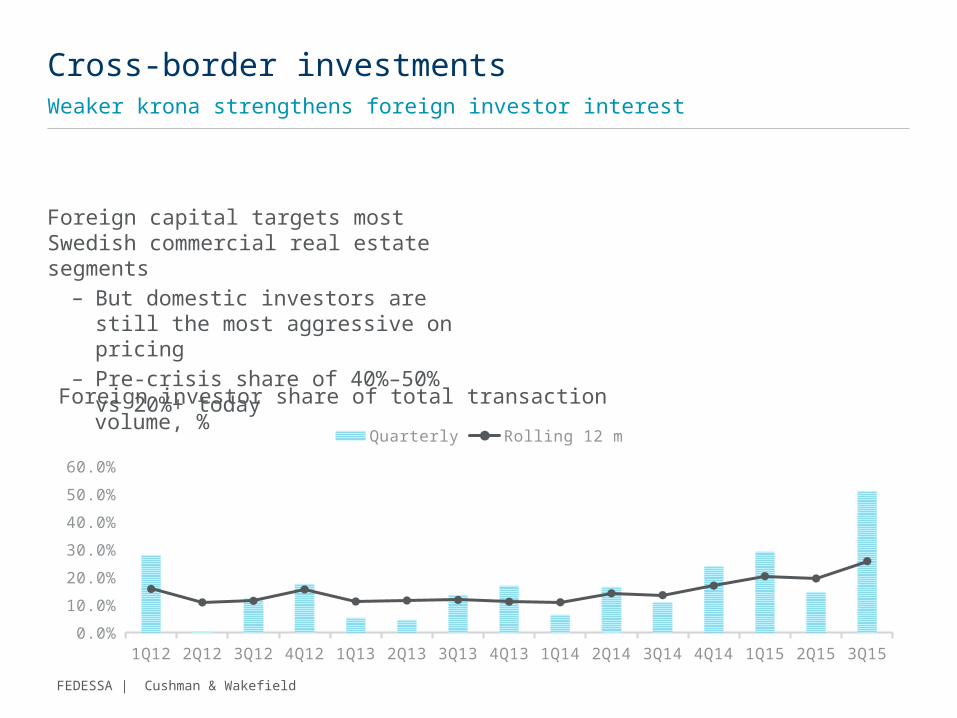

Foreign capital targets most Swedish commercial real estate segments

– But domestic investors are still the most aggressive on pricing

– Pre-crisis share of 40%–50% vs 20%+ today

Cross-border investmentsWeaker krona strengthens foreign investor interest

Foreign investor share of total transaction volume, %

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q150.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Quarterly Rolling 12 m

FEDESSA | Cushman & Wakefield

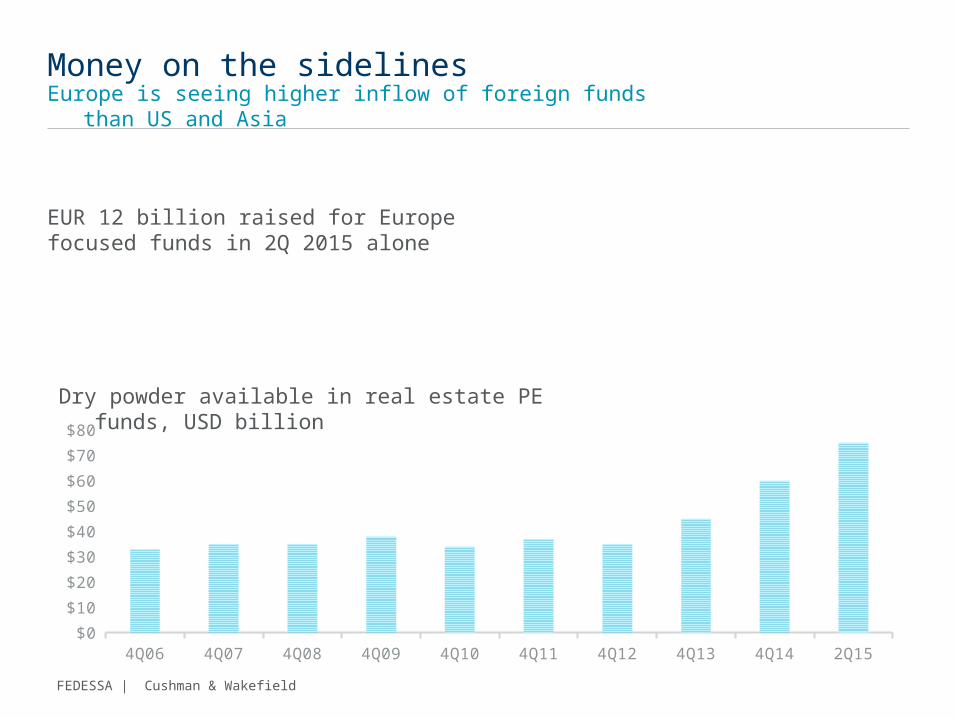

EUR 12 billion raised for Europe focused funds in 2Q 2015 alone

Money on the sidelinesEurope is seeing higher inflow of foreign funds than US and Asia

Dry powder available in real estate PE funds, USD billion

4Q06 4Q07 4Q08 4Q09 4Q10 4Q11 4Q12 4Q13 4Q14 2Q15$0

$10

$20

$30

$40

$50

$60

$70

$80

FEDESSA | Cushman & Wakefield

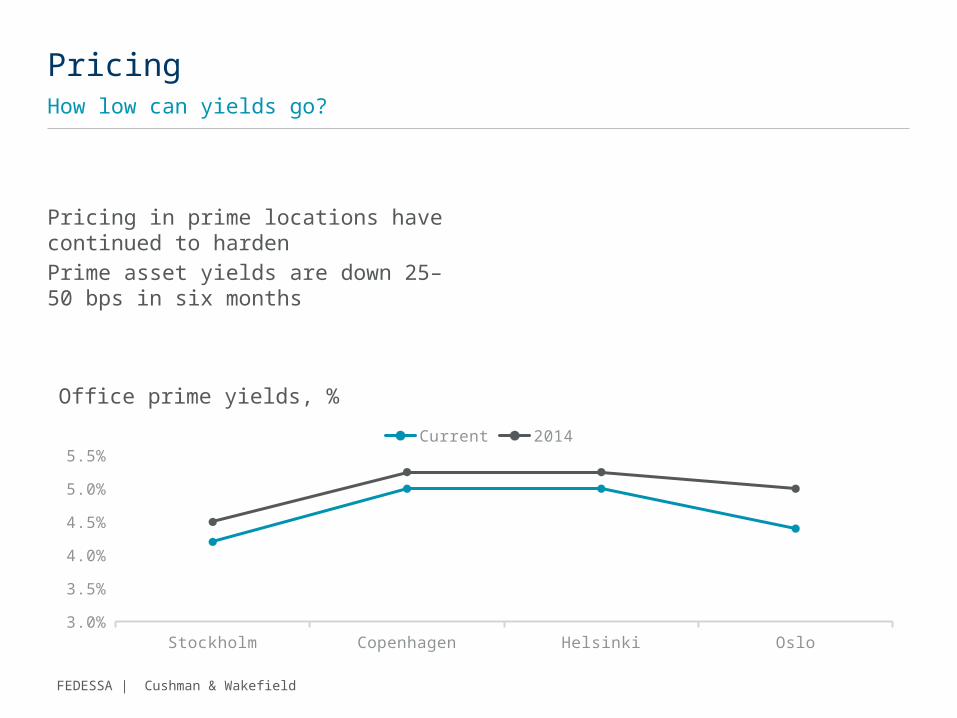

Pricing in prime locations have continued to harden

Prime asset yields are down 25–50 bps in six months

PricingHow low can yields go?

Office prime yields, %

Stockholm Copenhagen Helsinki Oslo3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

Current 2014

FEDESSA | Cushman & Wakefield

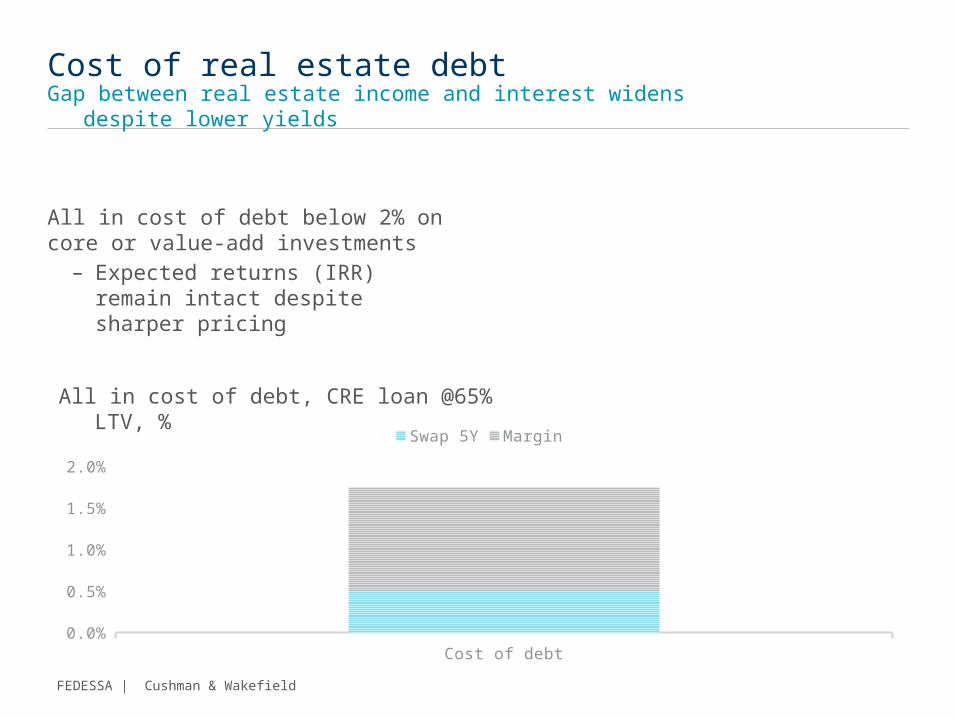

Cost of real estate debtGap between real estate income and interest widens despite lower yields

All in cost of debt, CRE loan @65% LTV, %

Cost of debt0.0%0.2%0.4%0.6%0.8%1.0%1.2%1.4%1.6%1.8%2.0%

Swap 5Y Margin

All in cost of debt below 2% on core or value-add investments

– Expected returns (IRR) remain intact despite sharper pricing

FEDESSA | Cushman & Wakefield

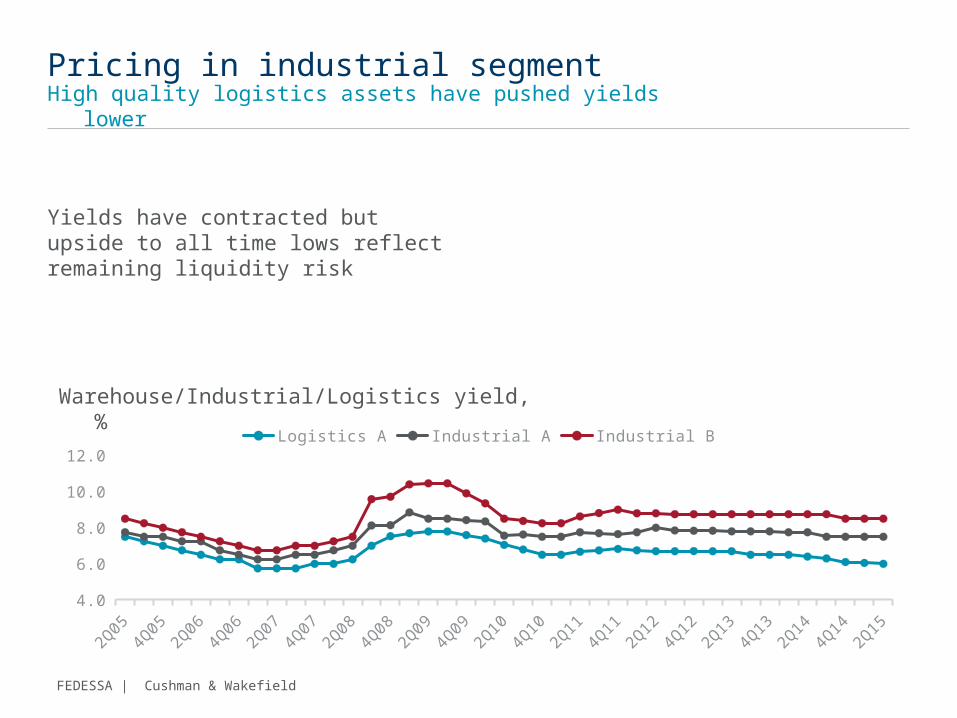

Yields have contracted but upside to all time lows reflect remaining liquidity risk

Pricing in industrial segmentHigh quality logistics assets have pushed yields lower

Warehouse/Industrial/Logistics yield, %

2Q05

4Q05

2Q06

4Q06

2Q07

4Q07

2Q08

4Q08

2Q09

4Q09

2Q10

4Q10

2Q11

4Q11

2Q12

4Q12

2Q13

4Q13

2Q14

4Q14

2Q15

4.05.06.07.08.09.0

10.011.012.0

Logistics A Industrial A Industrial B

FEDESSA | Cushman & Wakefield

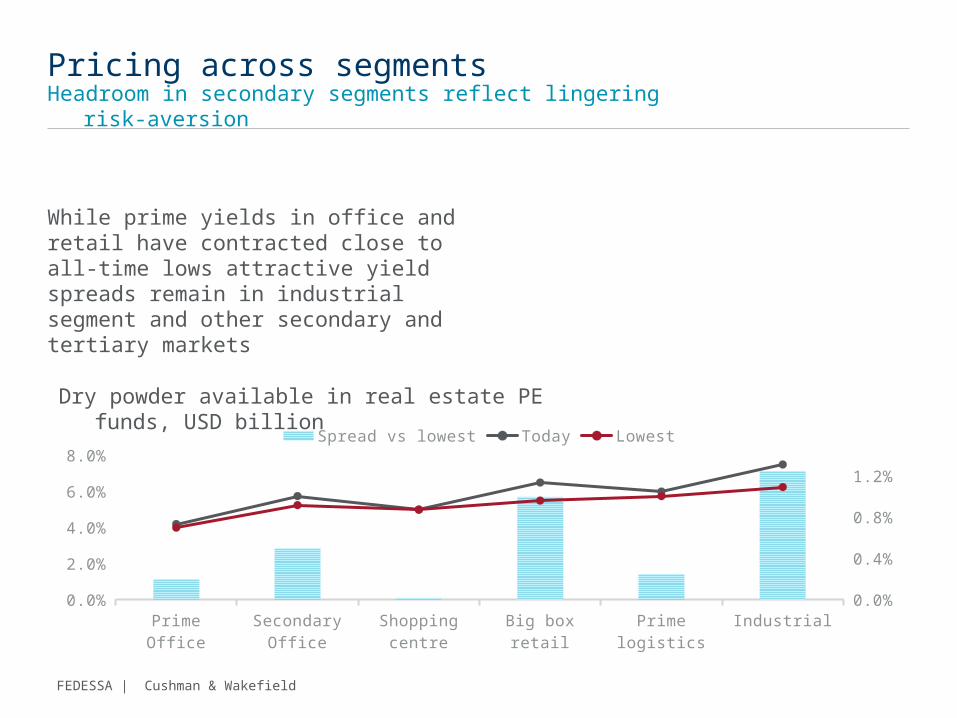

While prime yields in office and retail have contracted close to all-time lows attractive yield spreads remain in industrial segment and other secondary and tertiary markets

Pricing across segmentsHeadroom in secondary segments reflect lingering risk-aversion

Dry powder available in real estate PE funds, USD billion

Prime Office Secondary Office Shopping centre Big box retail Prime logistics Industrial0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

Spread vs lowest Today Lowest

FEDESSA | Cushman & Wakefield

Need for new products and markets to satisfy

investment targets

The search for investable assetsPension money leading hunt for returns in real estate

Pension funds and PE funds looking for new segments of real estate investments

New segments explored since 2010• Public tenant real estate (municipal tenants

or publicly funded operators)• Residential apartments• Food retail• Prime logistics• Student housing• Infrastructure

In the pipeline• Commercial development• Land plays in biggest cities• Joint ventures local and global

FEDESSA | Cushman & Wakefield

Land playsCost of residential building rights

Location SEK per sqm

Secondary suburbs 3,000–5,000

Best suburbs 6,000–10,000

Outside tolls 10,000–20,000

Inner city 20,000–40,000

Central Stockholm 40,000–60,000

FEDESSA | Cushman & Wakefield

The market liquidity will last another 12 months

Investors will remain more cautious than in the last cycle

Yield will be the primary driver of shifts to new real estate segments

Investment themes Summing up

SELF STORAGE SECTORREAL ESTATE OVERVIEW

OLIVER CLOSESEPTEMBER 2015

19

Agenda

MARKET STATUS – MAJOR SELF STORAGE REITS

TRANSACTIONS

PROPERTY VALUATIONS

DRIVERS OF VALUE

SUMMARY & CONCLUSIONS

20

Market Status

US REITS

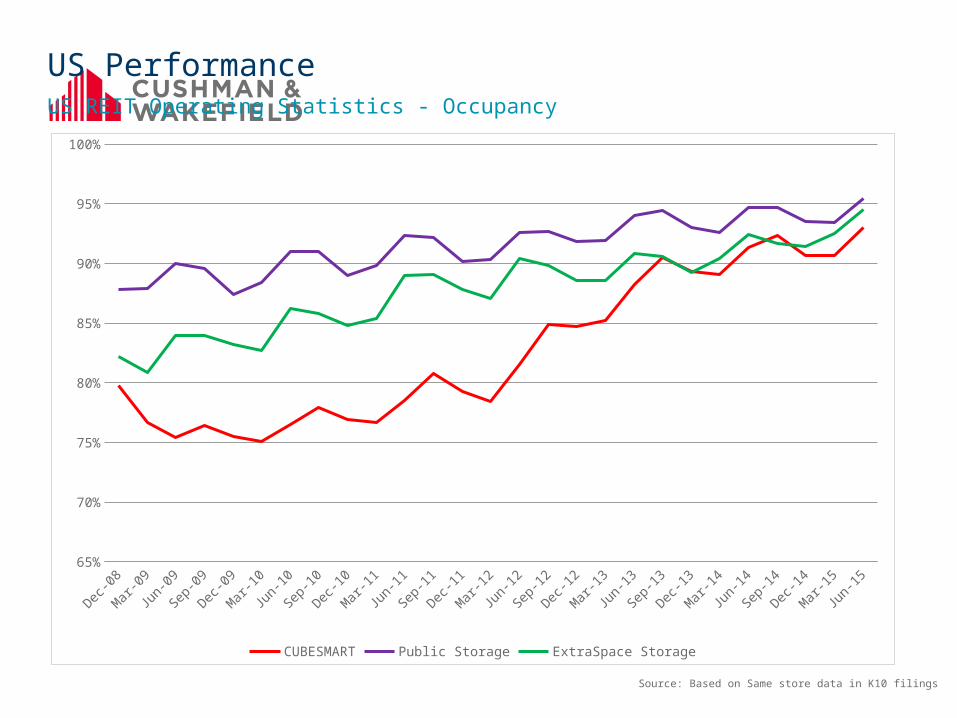

US PerformanceUS REIT Operating Statistics - Occupancy

Dec-0

8

Mar

-09

Jun-

09

Sep-0

9

Dec-0

9

Mar

-10

Jun-

10

Sep-1

0

Dec-1

0

Mar

-11

Jun-

11

Sep-1

1

Dec-1

1

Mar

-12

Jun-

12

Sep-1

2

Dec-1

2

Mar

-13

Jun-

13

Sep-1

3

Dec-1

3

Mar

-14

Jun-

14

Sep-1

4

Dec-1

4

Mar

-15

Jun-

1565%

70%

75%

80%

85%

90%

95%

100%

CUBESMART Public Storage ExtraSpace Storage

Source: Based on Same store data in K10 filings

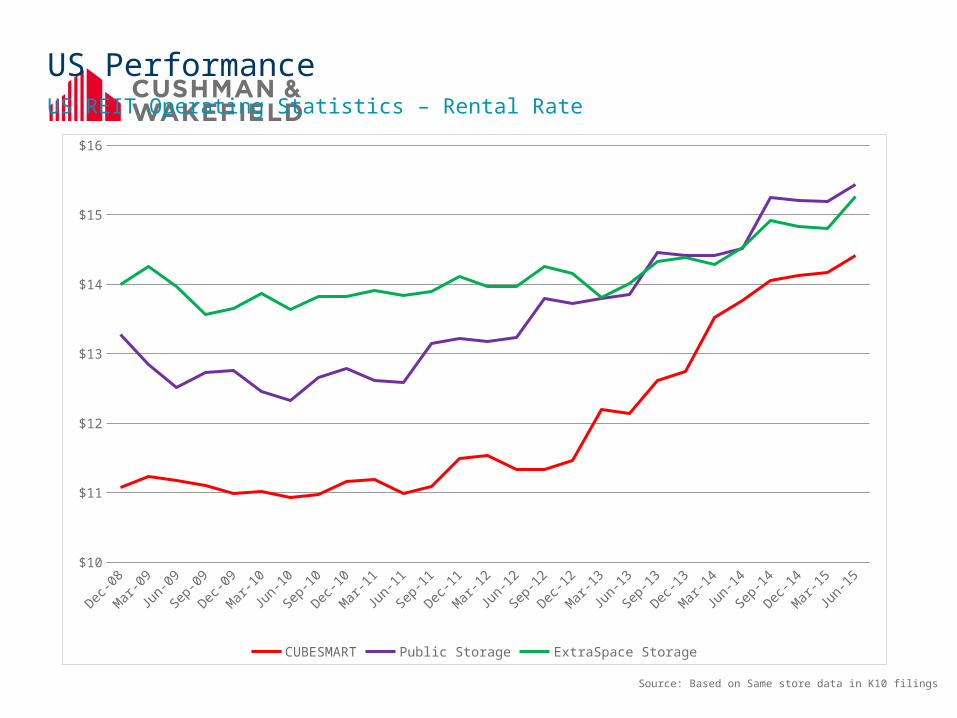

US PerformanceUS REIT Operating Statistics – Rental Rate

Dec-0

8

Mar

-09

Jun-

09

Sep-0

9

Dec-0

9

Mar

-10

Jun-

10

Sep-1

0

Dec-1

0

Mar

-11

Jun-

11

Sep-1

1

Dec-1

1

Mar

-12

Jun-

12

Sep-1

2

Dec-1

2

Mar

-13

Jun-

13

Sep-1

3

Dec-1

3

Mar

-14

Jun-

14

Sep-1

4

Dec-1

4

Mar

-15

Jun-

15$10

$11

$12

$13

$14

$15

$16

CUBESMART Public Storage ExtraSpace Storage

Source: Based on Same store data in K10 filings

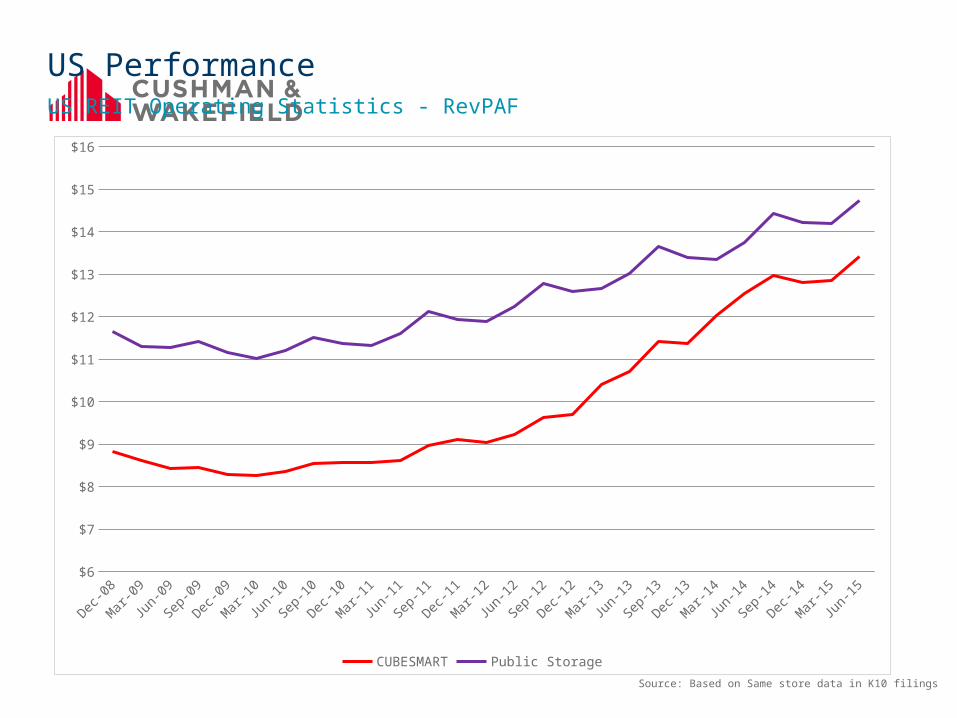

US PerformanceUS REIT Operating Statistics - RevPAF

Source: Based on Same store data in K10 filings

Dec-0

8

Mar

-09

Jun-

09

Sep-0

9

Dec-0

9

Mar

-10

Jun-

10

Sep-1

0

Dec-1

0

Mar

-11

Jun-

11

Sep-1

1

Dec-1

1

Mar

-12

Jun-

12

Sep-1

2

Dec-1

2

Mar

-13

Jun-

13

Sep-1

3

Dec-1

3

Mar

-14

Jun-

14

Sep-1

4

Dec-1

4

Mar

-15

Jun-

15$6

$7

$8

$9

$10

$11

$12

$13

$14

$15

$16

CUBESMART Public Storage

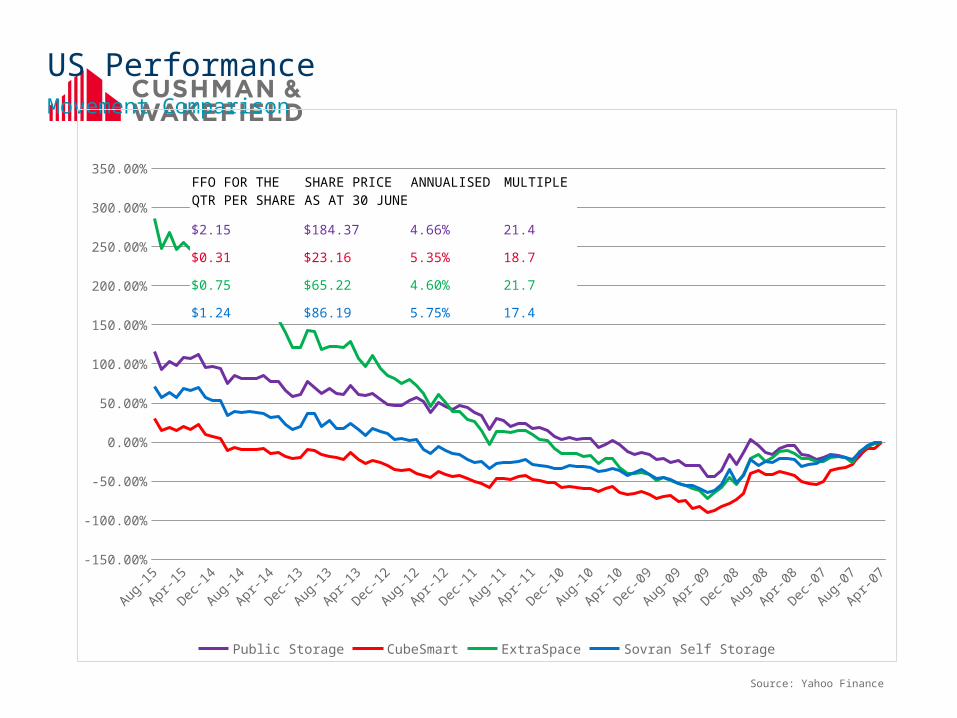

US PerformanceMovement Comparison

Source: Yahoo Finance

Apr-0

7

Jul-0

7

Oct-0

7

Jan-

08

Apr-0

8

Jul-0

8

Oct-0

8

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Jan-

12

Apr-1

2

Jul-1

2

Oct-1

2

Jan-

13

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4

Jan-

15

Apr-1

5

Jul-1

5-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

350.00%

Public Storage CubeSmart ExtraSpace Sovran Self Storage

FFO FOR THE QTR PER SHARE

SHARE PRICE AS AT 30 JUNE

ANNUALISED MULTIPLE

$2.15 $184.37 4.66% 21.4

$0.31 $23.16 5.35% 18.7

$0.75 $65.22 4.60% 21.7

$1.24 $86.19 5.75% 17.4

25

Market Status

EUROPE

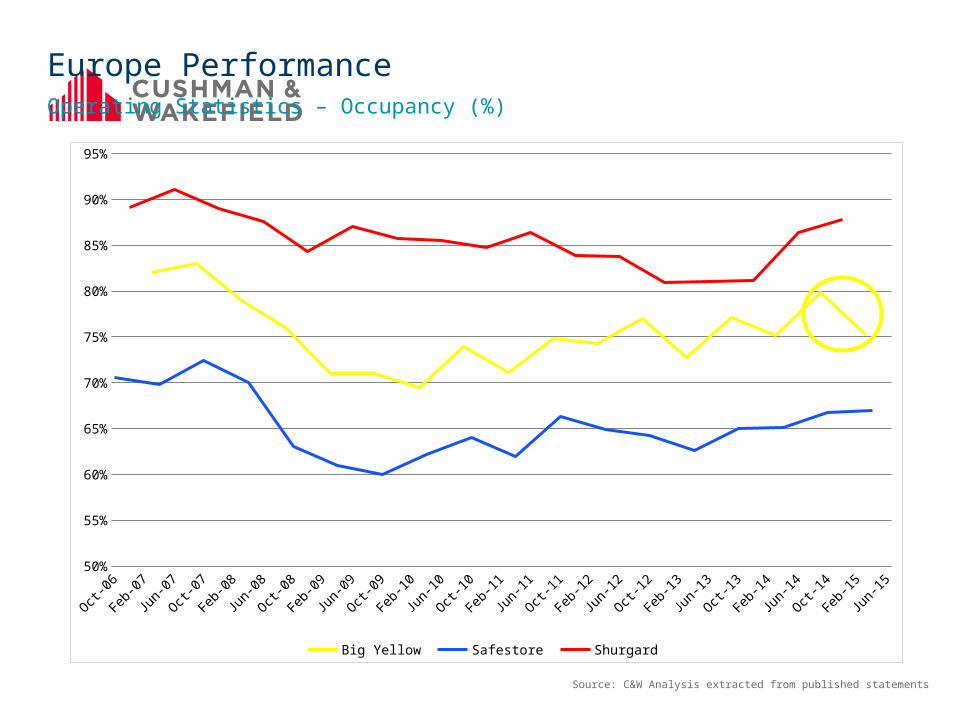

Europe PerformanceOperating Statistics – Occupancy (%)

Source: C&W Analysis extracted from published statements

Oct-0

6

Dec-0

6

Apr-0

7

Jul-0

7

Sep-

07

Dec-0

7

Mar-0

8

Jun-

08

Sep-

08

Dec-0

8

Mar-0

9

Jun-

09

Sep-

09

Dec-0

9

Mar-1

0

Jun-

10

Sep-

10

Dec-1

0

Mar-1

1

Jun-

11

Sep-

11

Dec-1

1

Mar-1

2

Jun-

12

Sep-

12

Dec-1

2

Mar-1

3

Jun-

13

Sep-

13

Dec-1

3

Mar-1

4

Jun-

14

Sep-

14

Dec-1

4

Mar-1

550%

55%

60%

65%

70%

75%

80%

85%

90%

95%

Big Yellow Safestore Shurgard

Europe PerformanceOperating Statistics – Rental Rate (Mixed Currency)

Source: C&W Analysis extracted from published statements

Oct-0

6

Dec-0

6

Mar-0

7

Jun-

07

Sep-

07

Nov-0

7

Feb-

08

May-0

8

Aug-0

8

Oct-0

8

Jan-

09

Apr-0

9

Jul-0

9

Sep-

09

Dec-0

9

Mar-1

0

Jun-

10

Aug-1

0

Nov-1

0

Feb-

11

May-1

1

Jul-1

1

Oct-1

1

Jan-

12

Apr-1

2

Jul-1

2

Sep-

12

Dec-1

2

Mar-1

3

Jun-

13

Aug-1

3

Nov-1

3

Feb-

14

May-1

4

Jul-1

4

Oct-1

4

Jan-

15

Apr-1

514

16

18

20

22

24

26

28

30

Big Yellow (£/ Sq ft) Safestore (£/ Sq ft) Shurgard (€/ Sq ft)

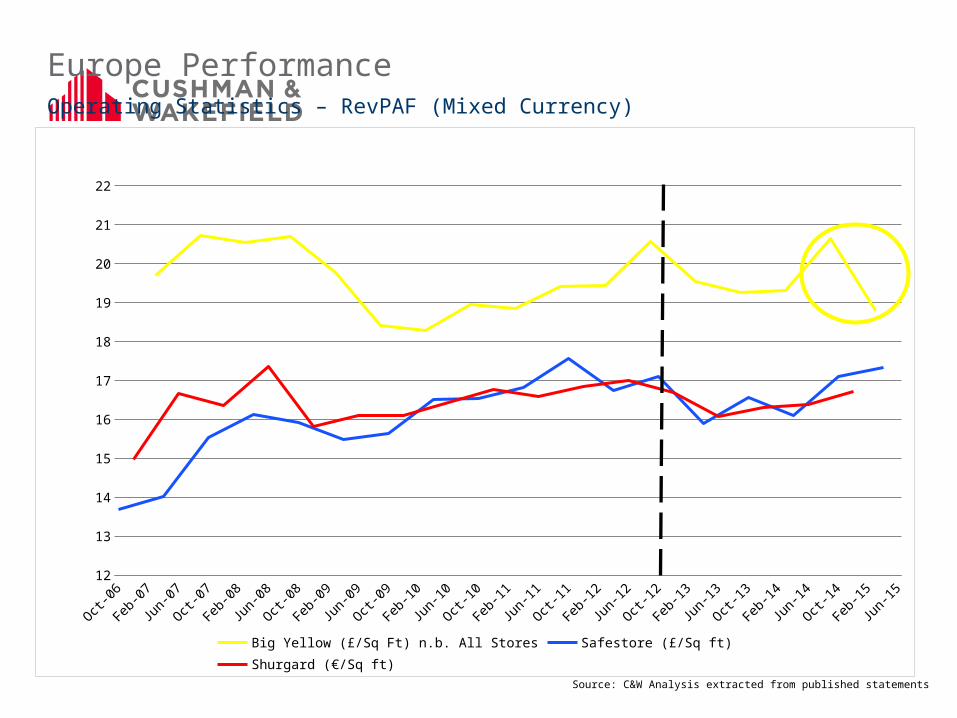

Europe PerformanceOperating Statistics – RevPAF (Mixed Currency)

Source: C&W Analysis extracted from published statements

Oct-0

6

Dec-0

6

Apr-0

7

Jul-0

7

Sep-

07

Dec-0

7

Mar-0

8

Jun-

08

Sep-

08

Dec-0

8

Mar-0

9

Jun-

09

Sep-

09

Dec-0

9

Mar-1

0

Jun-

10

Sep-

10

Dec-1

0

Mar-1

1

Jun-

11

Sep-

11

Dec-1

1

Mar-1

2

Jun-

12

Sep-

12

Dec-1

2

Mar-1

3

Jun-

13

Sep-

13

Dec-1

3

Mar-1

4

Jun-

14

Sep-

14

Dec-1

4

Mar-1

512

13

14

15

16

17

18

19

20

21

22

Big Yellow (£/Sq Ft) n.b. All Stores Safestore (£/Sq ft) Shurgard (€/Sq ft)

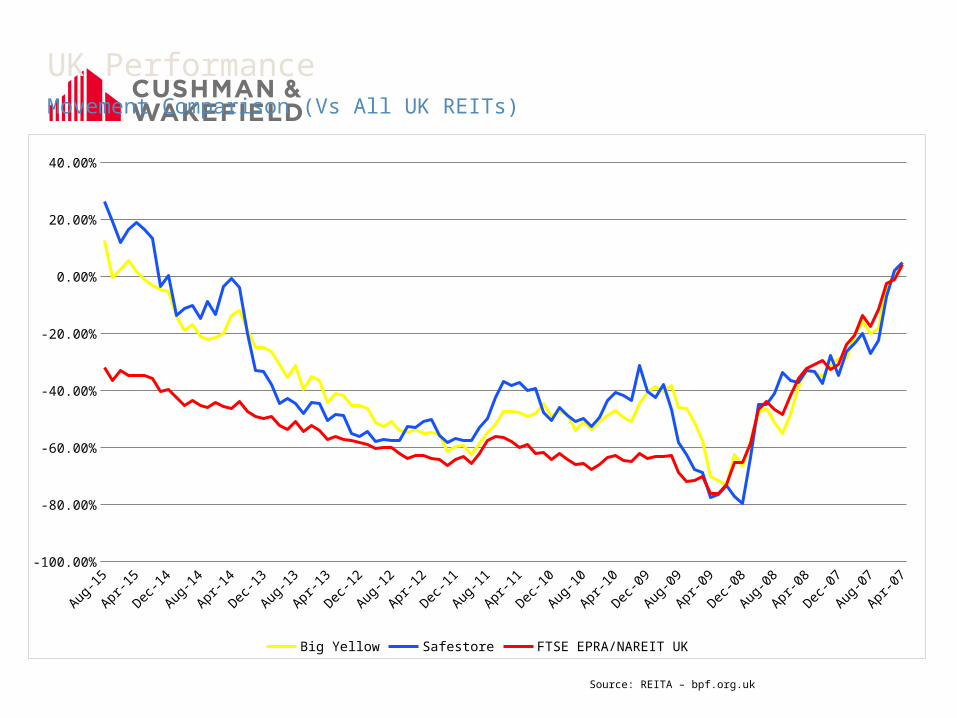

UK PerformanceMovement Comparison (Vs All UK REITs)

Source: REITA – bpf.org.uk

Apr-0

7

Jul-0

7

Oct-0

7

Jan-

08

Apr-0

8

Jul-0

8

Oct-0

8

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Jan-

12

Apr-1

2

Jul-1

2

Oct-1

2

Jan-

13

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4

Jan-

15

Apr-1

5

Jul-1

5-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

Big Yellow Safestore FTSE EPRA/NAREIT UK

30

Supply

Supply ComparisonBubble graph 2: EU - selected countries

0 50 100 150 200 250 300 3500

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

0

0

0

0

0

0

0

0

0

Source: FEDESSA

UKNUMBER OF FACILITIES - 975TOTAL SQ M - 3,200,000SQ M PER PERSON – 0.05

32

Transactions

DEAL OR NO DEAL?

Major Transactions

December 2014

April 2014December 2014

October 2014

June 2015

Transactions – a problem?

35

Valuation Approach• DCF Valuations• Analysis of the trading data• Model set up and process• Freehold -v- Leasehold• Capitalisation rate• Portfolio analysis

Principal Drivers of ValueCashflow

• REVENUE – THE BIG 5 DRIVERS

• MLA

• Stable occupancy assumption

• Fill rate

• Rental rate

• Additional income

• OPERATING COSTS

• RENT, MANAGEMENT FEES & CAPITAL RESERVES

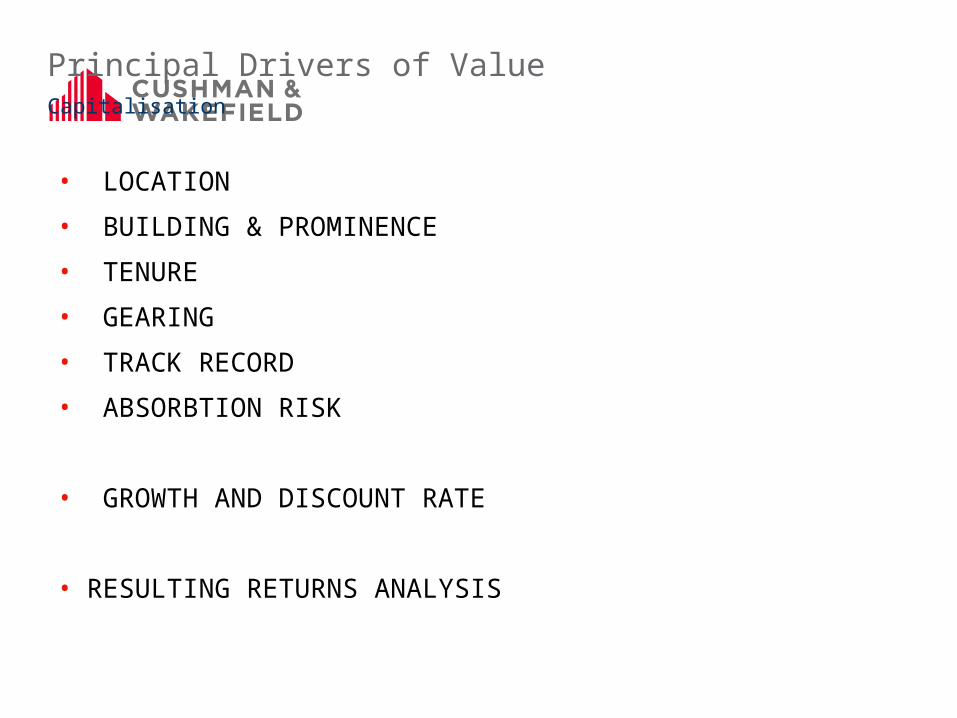

Principal Drivers of ValueCapitalisation

• LOCATION

• BUILDING & PROMINENCE

• TENURE

• GEARING

• TRACK RECORD

• ABSORBTION RISK

• GROWTH AND DISCOUNT RATE

• RESULTING RETURNS ANALYSIS

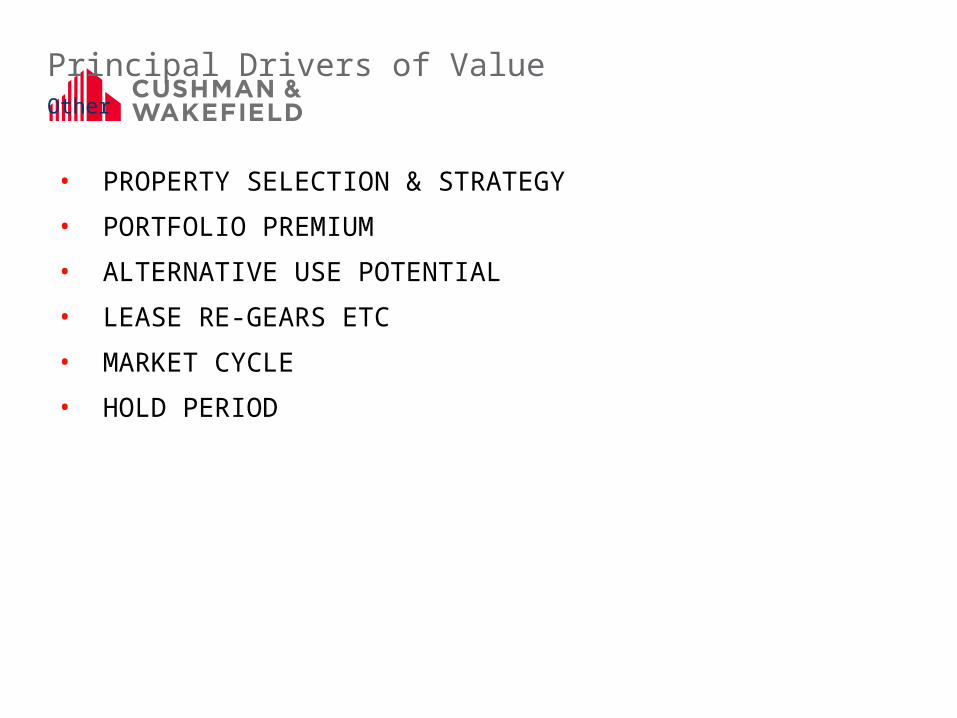

Principal Drivers of ValueOther

• PROPERTY SELECTION & STRATEGY

• PORTFOLIO PREMIUM

• ALTERNATIVE USE POTENTIAL

• LEASE RE-GEARS ETC

• MARKET CYCLE

• HOLD PERIOD

39

Q & A

OLIVER CLOSE

PARTNER, VALUATION & ADVISORY

43/45 Portman Square

London

W1A 3BG

+44 (0)20 7152 5156