Embed Size (px)

Citation preview

Sustainable use ofEarth’s natural resources

IR presentation

Q1-Q4 2016

© Outotec – All rights reserved

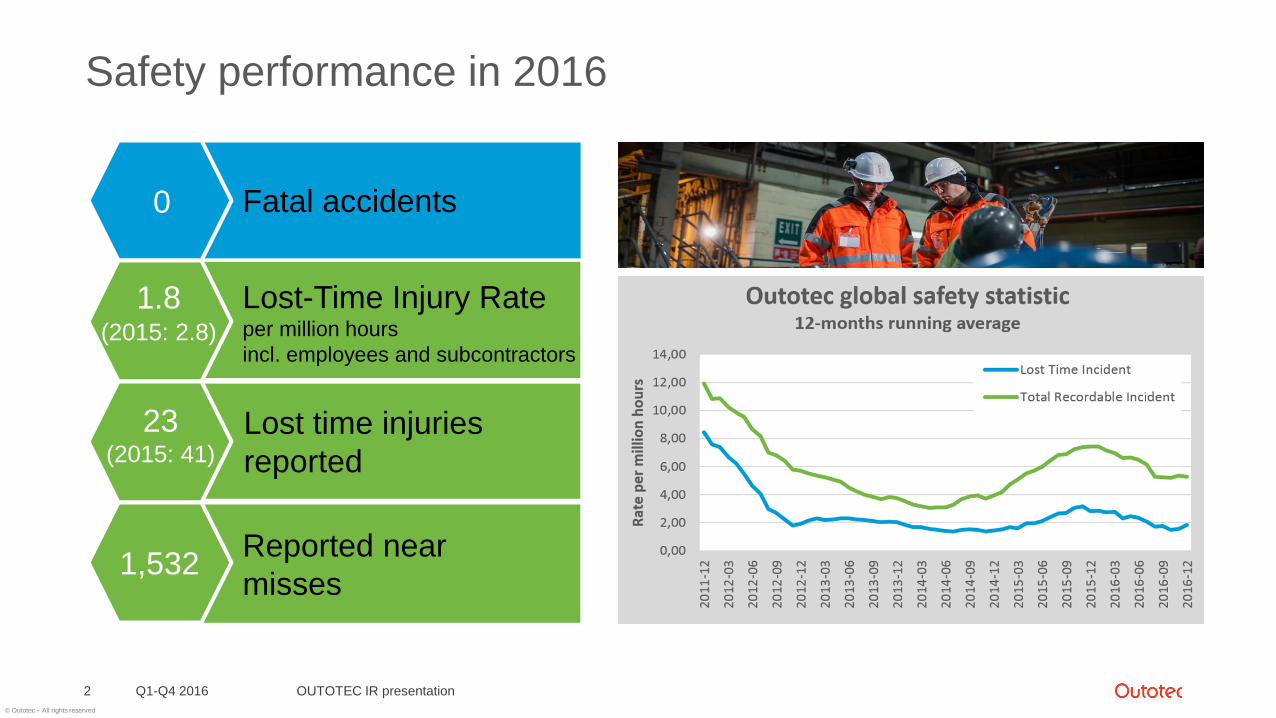

Safety performance in 2016

OUTOTEC IR presentation2 Q1-Q4 2016

0

1.8(2015: 2.8)

Fatal accidents

Lost-Time Injury Rateper million hours

incl. employees and subcontractors

Reported near

misses

23(2015: 41)

Lost time injuries

reported

1,532

© Outotec – All rights reserved

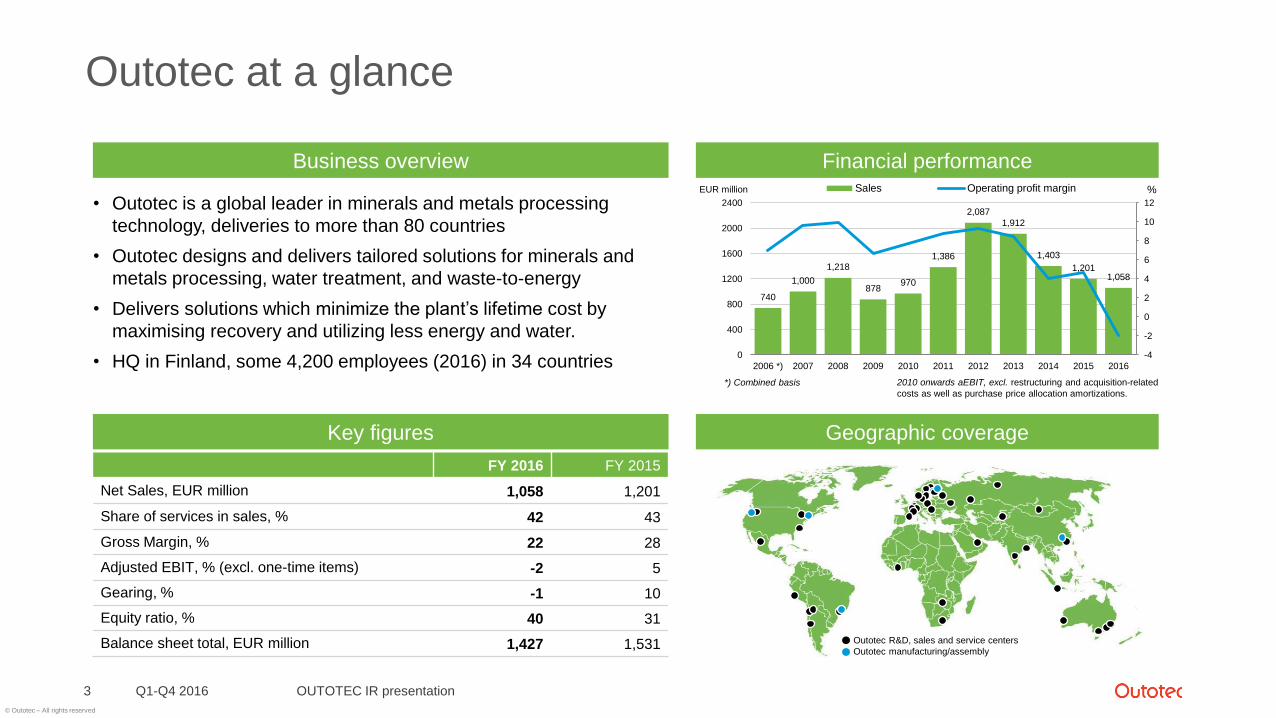

Outotec at a glance

Q1-Q4 2016 OUTOTEC IR presentation3

Key figures

Financial performance

Geographic coverage

Business overview

740

1,000

1,218

878970

1,386

2,087

1,912

1,403

1,2011,058

-4

-2

0

2

4

6

8

10

12

0

400

800

1200

1600

2000

2400

2006 *) 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sales Operating profit margin

*) Combined basis 2010 onwards aEBIT, excl. restructuring and acquisition-related

costs as well as purchase price allocation amortizations.

EUR million %

FY 2016 FY 2015

Net Sales, EUR million 1,058 1,201

Share of services in sales, % 42 43

Gross Margin, % 22 28

Adjusted EBIT, % (excl. one-time items) -2 5

Gearing, % -1 10

Equity ratio, % 40 31

Balance sheet total, EUR million 1,427 1,531

• Outotec is a global leader in minerals and metals processing

technology, deliveries to more than 80 countries

• Outotec designs and delivers tailored solutions for minerals and

metals processing, water treatment, and waste-to-energy

• Delivers solutions which minimize the plant’s lifetime cost by

maximising recovery and utilizing less energy and water.

• HQ in Finland, some 4,200 employees (2016) in 34 countries

Outotec R&D, sales and service centers

Outotec manufacturing/assembly

© Outotec – All rights reserved

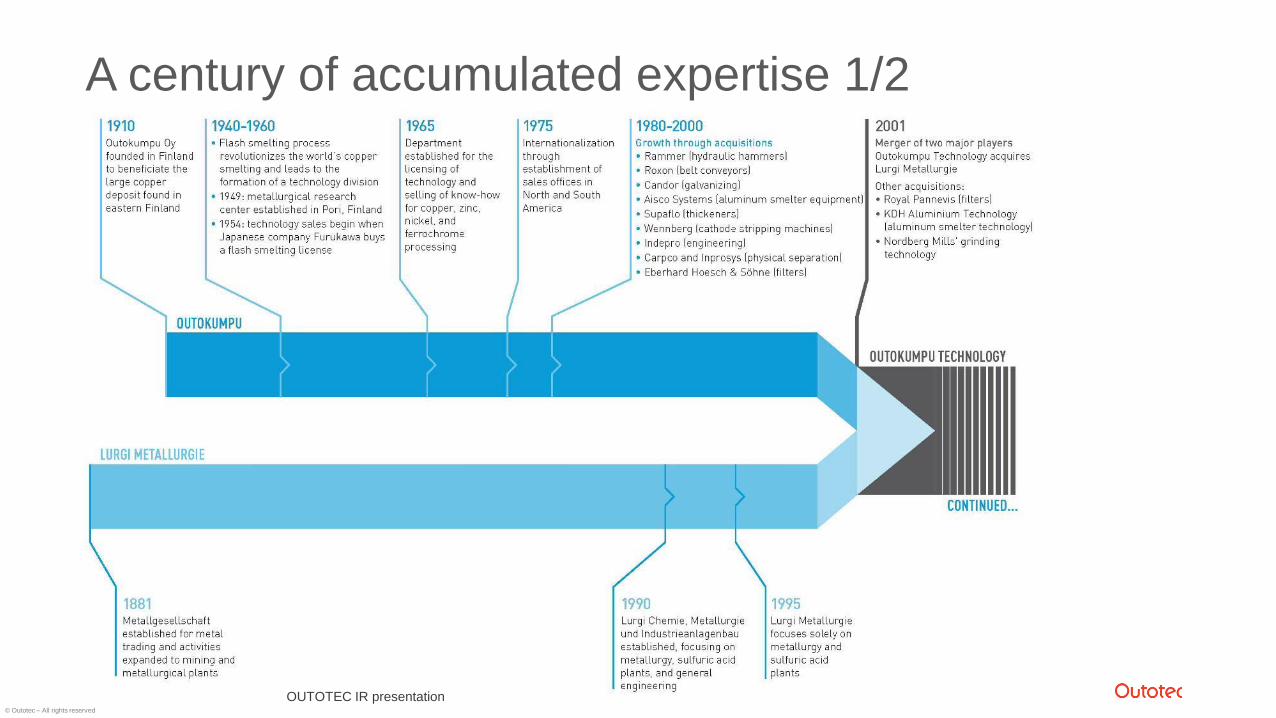

A century of accumulated expertise 1/2

Q1-Q4 2016 OUTOTEC IR presentation4 OUTOTEC IR presentation

© Outotec – All rights reserved

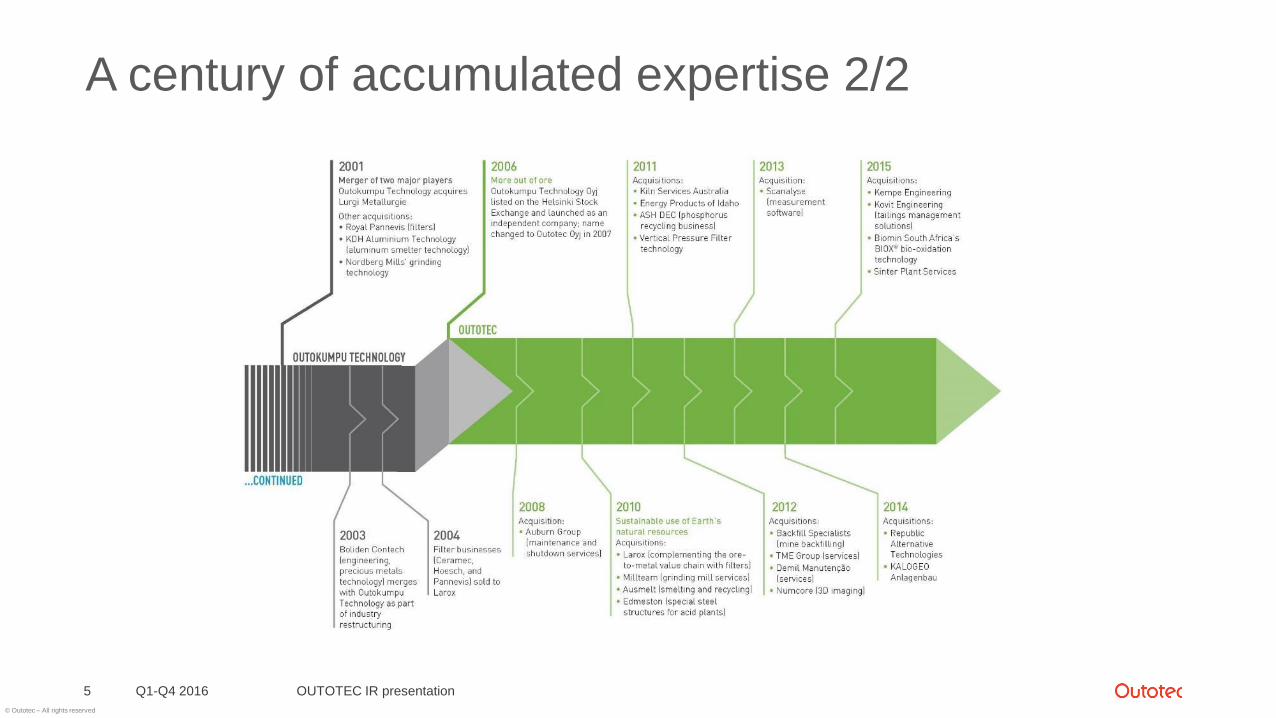

A century of accumulated expertise 2/2

Q1-Q4 2016 OUTOTEC IR presentation5

© Outotec – All rights reserved

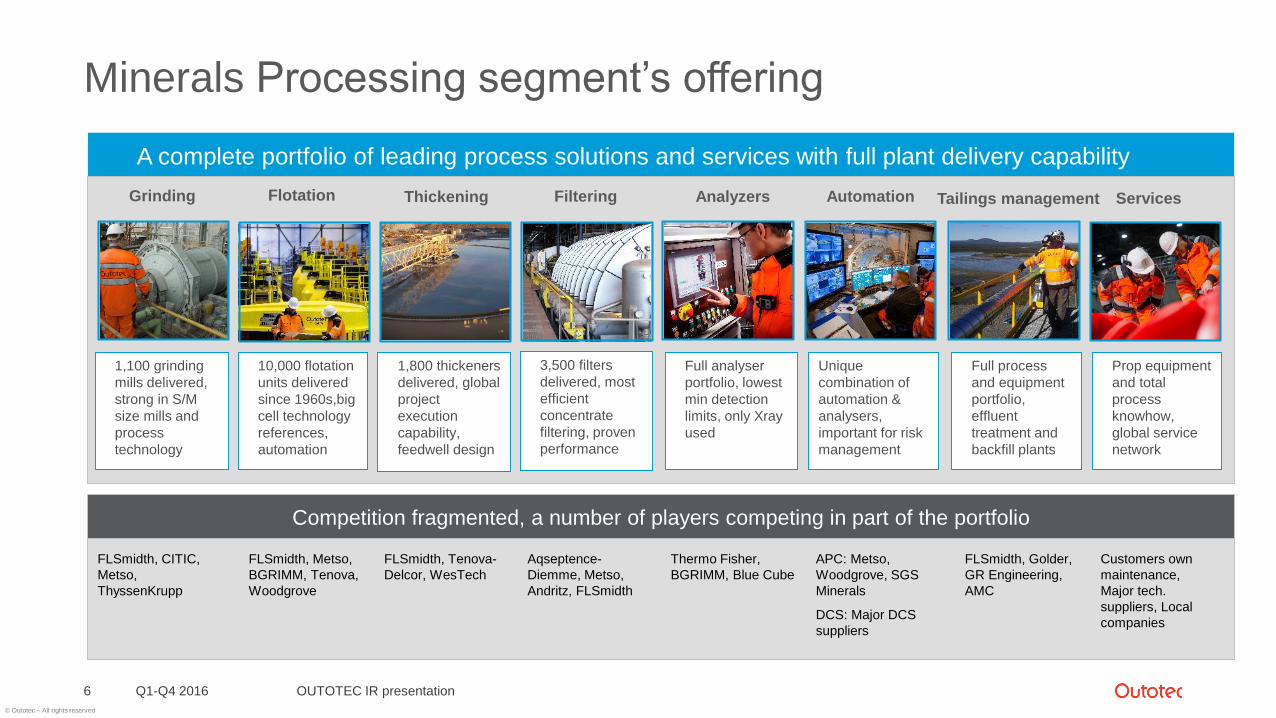

6

Minerals Processing segment’s offering

A complete portfolio of leading process solutions and services with full plant delivery capability

Water

Technology

FLSmidth, CITIC,

Metso,

ThyssenKrupp

FLSmidth, Metso,

BGRIMM, Tenova,

Woodgrove

FLSmidth, Tenova-

Delcor, WesTech

Aqseptence-

Diemme, Metso,

Andritz, FLSmidth

Thermo Fisher,

BGRIMM, Blue Cube

APC: Metso,

Woodgrove, SGS

Minerals

DCS: Major DCS

suppliers

FLSmidth, Golder,

GR Engineering,

AMC

Customers own

maintenance,

Major tech.

suppliers, Local

companies

Thickening AnalyzersGrinding Flotation AutomationFiltering ServicesTailings management

1,100 grinding

mills delivered,

strong in S/M

size mills and

process

technology

10,000 flotation

units delivered

since 1960s,big

cell technology

references,

automation

1,800 thickeners

delivered, global

project

execution

capability,

feedwell design

Full analyser

portfolio, lowest

min detection

limits, only Xray

used

Unique

combination of

automation &

analysers,

important for risk

management

Full process

and equipment

portfolio,

effluent

treatment and

backfill plants

Prop equipment

and total

process

knowhow,

global service

network

3,500 filters

delivered, most

efficient

concentrate

filtering, proven

performance

Competition fragmented, a number of players competing in part of the portfolio

Q1-Q4 2016 OUTOTEC IR presentation

© Outotec – All rights reserved

Q1-Q4 2016 OUTOTEC IR presentation7

Industry-leading technologies, process solutions and services

Metals, Energy & Water segment’s offering

Ferrous metals Sulfuric acid/Off-

gas/Roasting

Fives, FLSmidth,

Metso,

Aqseptence-

Diemme

Kobelco, Metso,

Primetals, Jemeco

SMS Siemag,

Tenova, Jemeco

GEA Bischoff,

MECS

Alumina,

AluminumBase metals (Cu, Ni,

Zn, Au, Ag, PGM)Ferroalloys

Glencore

Technology, Tenova

Strong in CFB

Aluminium

Calcination and

HOT Tube

Digestion

Over 60% of the

world’s pellets are

made with

Outotec’s

travelling grate

technology

650 acid plants

and 270 non-

ferrous roasting

plants

Strong in Cu

smelting, anode

casting, SX and Zn

leaching, strong in

Ni smelting and

EW

Energy Water

Alumina calciner,

Green anode plants,

Rod Hop

Sintering, Pelletizing,

Direct Smelting

Sulfuric acid plant,

Roasting

Smelting, Converting,

Leaching, SX/EW,

electrorefining

Smelting,

Preheating, Steel

Belt Sintering

Waste-to-energy,

Sludge incineration,

Oil shale processing

Industrial water

treatment, municipal

water systems

Competition fragmented, a number of players competing in part of the portfolio

Services

Advisory, maintenance,

operations & remote

services, upgrades

Valmet, Andritz,

Babcock&WilcoxVeolia, GE Water,

Suez

FLSmidth, Metso,

major tech suppliers,

locals and customers

Strong in Ferro

Chrome, 20

pelletizing and

sinter plants and

9 smelters for

ferroalloys

Versatile waste-

to-energy

solution, over

250 materials

used

Effluent

treatment plants,

backfill plants,

water recycling

Shutdown

services, best

suited to provide

services for own

technologies

© Outotec – All rights reserved

Long-term customer relationships with the industry’s top companies

Q1-Q4 2016 OUTOTEC IR presentation8

In history, top ten customers have accounted for some 35% of sales.

Major global mining companiesLocal mining and metallurgical

companies in emerging regionsIntermediate sized companies

Selected reference customers of Outotec

© Outotec – All rights reserved

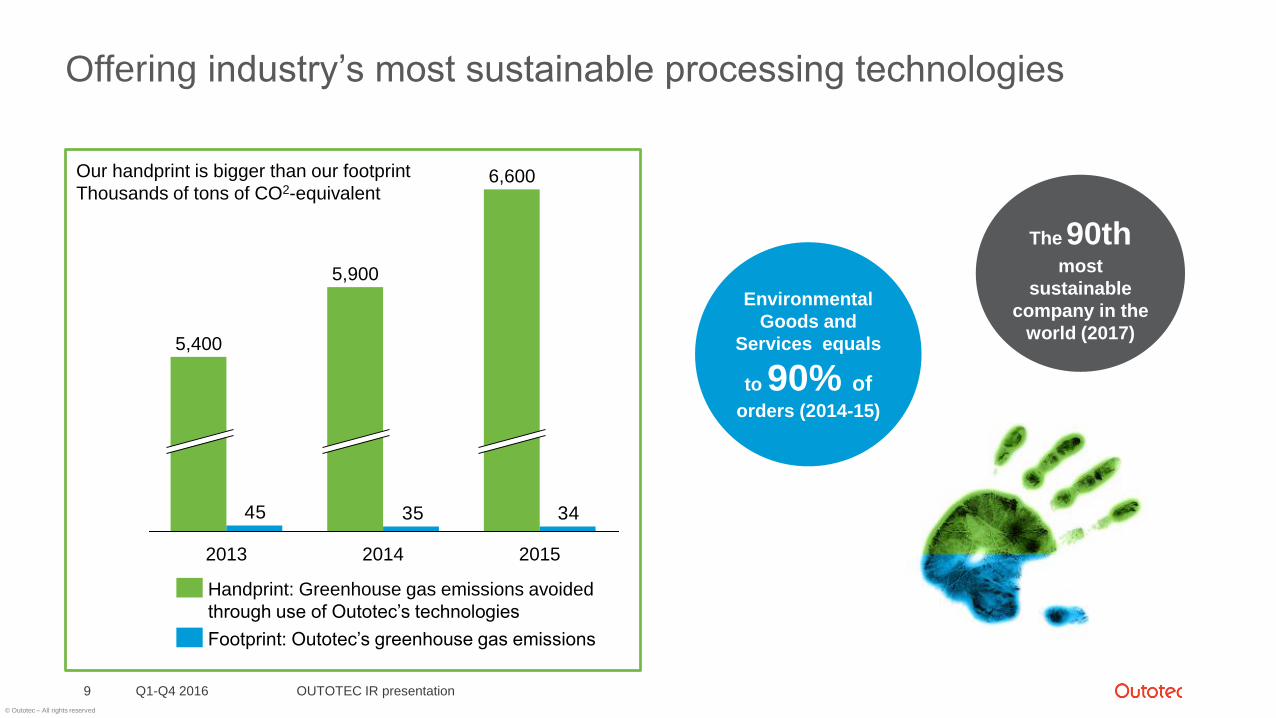

Offering industry’s most sustainable processing technologies

Q1-Q4 2016 OUTOTEC IR presentation9

343545

2015

6,600

2014

5,900

2013

5,400

Our handprint is bigger than our footprint

Thousands of tons of CO2-equivalent

Footprint: Outotec’s greenhouse gas emissions

Handprint: Greenhouse gas emissions avoided

through use of Outotec’s technologies

The 90thmost

sustainable

company in the

world (2017)

Environmental

Goods and

Services equals

to 90% of

orders (2014-15)

© Outotec – All rights reserved

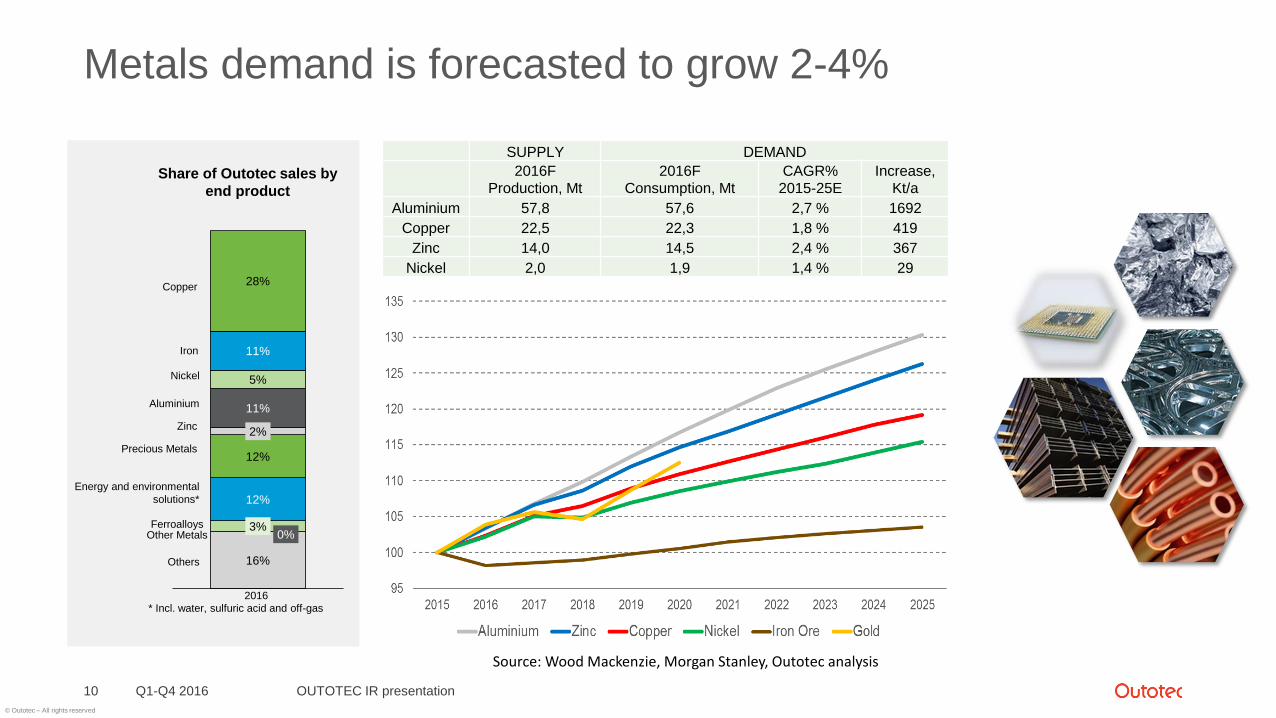

Metals demand is forecasted to grow 2-4%

Q1-Q4 2016 OUTOTEC IR presentation10

SUPPLY DEMAND

2016F

Production, Mt

2016F

Consumption, Mt

CAGR%

2015-25E

Increase,

Kt/a

Aluminium 57,8 57,6 2,7 % 1692

Copper 22,5 22,3 1,8 % 419

Zinc 14,0 14,5 2,4 % 367

Nickel 2,0 1,9 1,4 % 29

Source: Wood Mackenzie, Morgan Stanley, Outotec analysis

Share of Outotec sales by

end product

* Incl. water, sulfuric acid and off-gas

16%

0%3%

12%

12%

2%

11%

5%

11%

28%

Others

Copper

Precious Metals

Zinc

Aluminium

Ferroalloys

Iron

Nickel

Other Metals

2016

Energy and environmental

solutions*

© Outotec – All rights reserved

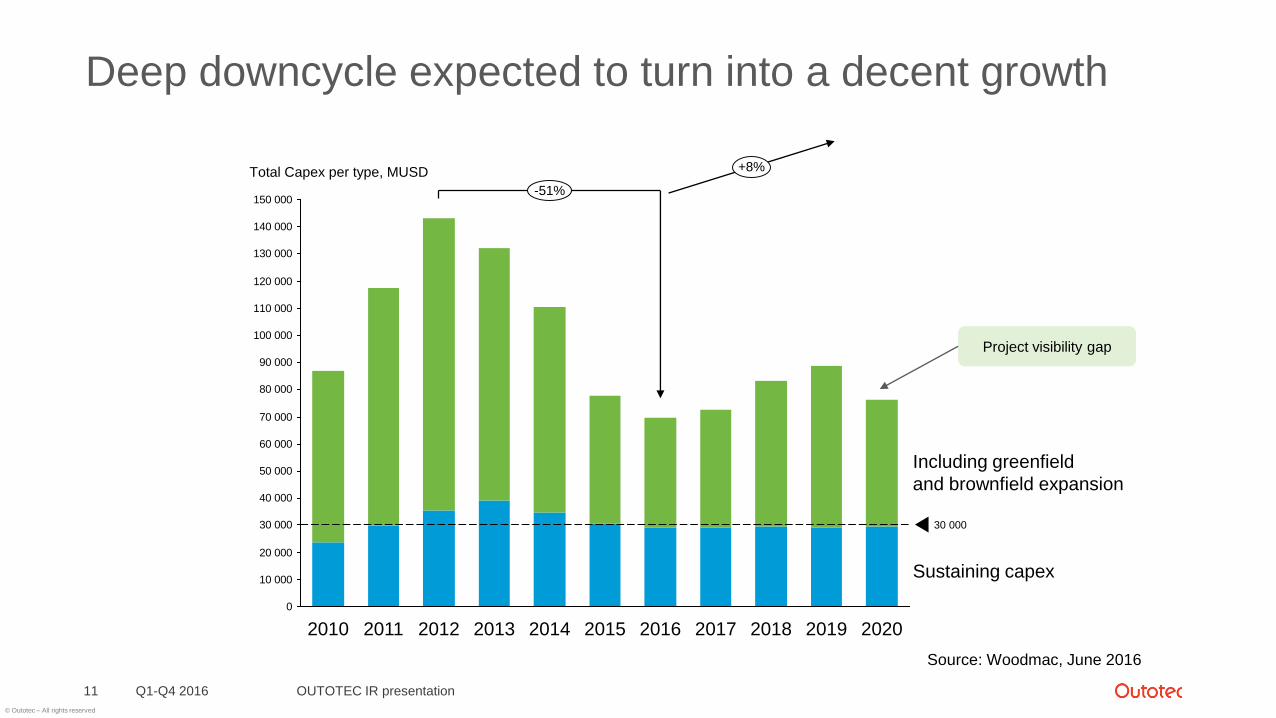

Deep downcycle expected to turn into a decent growth

Q1-Q4 2016 OUTOTEC IR presentation11

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

110 000

120 000

130 000

140 000

150 000

2019 2020201820172016201520142013201220112010

30 000

+8%

-51%

Sustaining capex

Including greenfield

and brownfield expansion

Total Capex per type, MUSD

Project visibility gap

Source: Woodmac, June 2016

© Outotec – All rights reserved

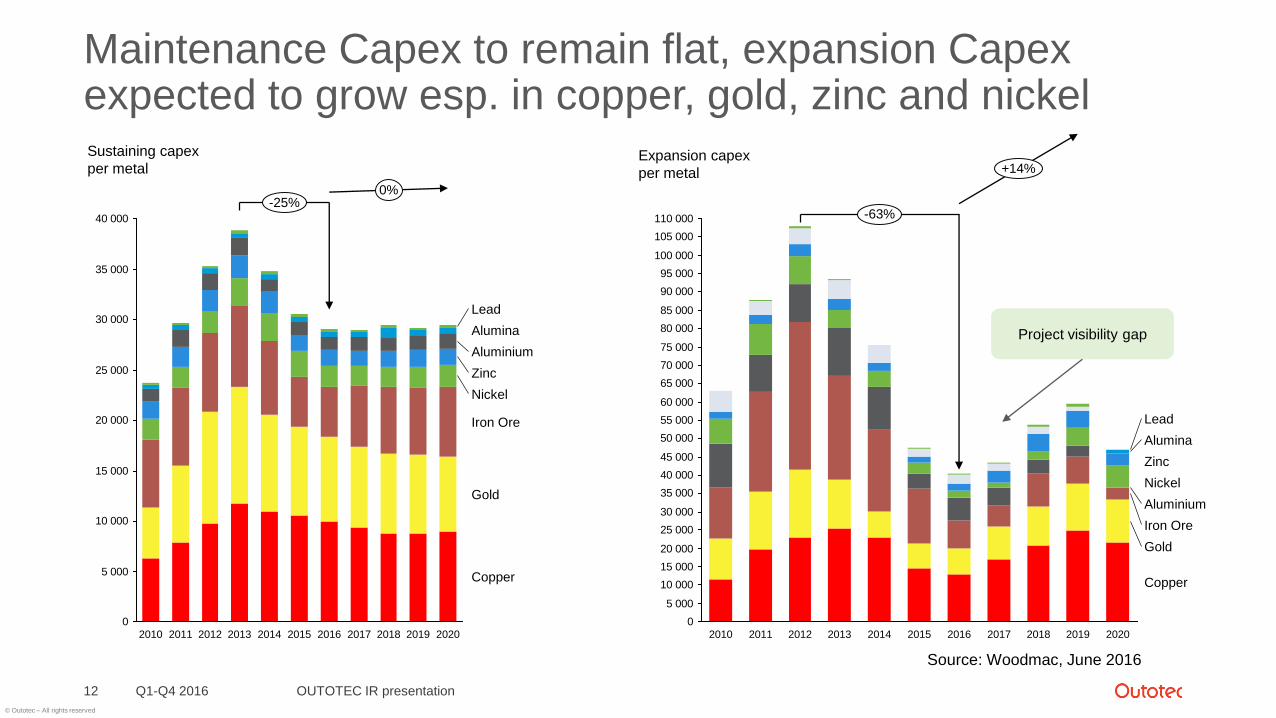

Maintenance Capex to remain flat, expansion Capexexpected to grow esp. in copper, gold, zinc and nickel

Q1-Q4 2016 OUTOTEC IR presentation12

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

0%-25%

Copper

Gold

Iron Ore

Nickel

Zinc

Aluminium

Alumina

Lead

20202019201820172016201520142013201220112010

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

55 000

60 000

65 000

70 000

75 000

80 000

85 000

90 000

95 000

100 000

105 000

110 000

20152014201320122011 201820172010 2016

+14%

-63%

Copper

Gold

Iron Ore

Aluminium

Nickel

Zinc

Alumina

Lead

20202019

Sustaining capex

per metalExpansion capex

per metal

Project visibility gap

Source: Woodmac, June 2016

© Outotec – All rights reserved

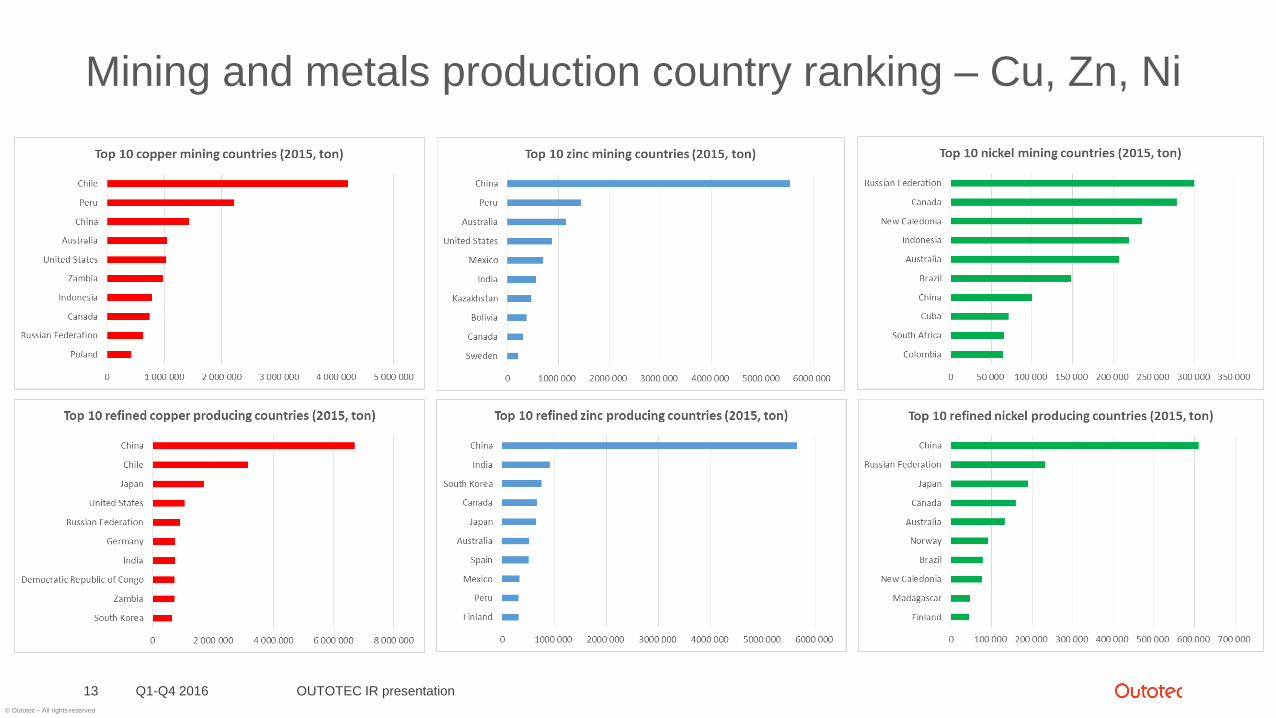

Mining and metals production country ranking – Cu, Zn, Ni

Q1-Q4 2016 OUTOTEC IR presentation13

© Outotec – All rights reserved

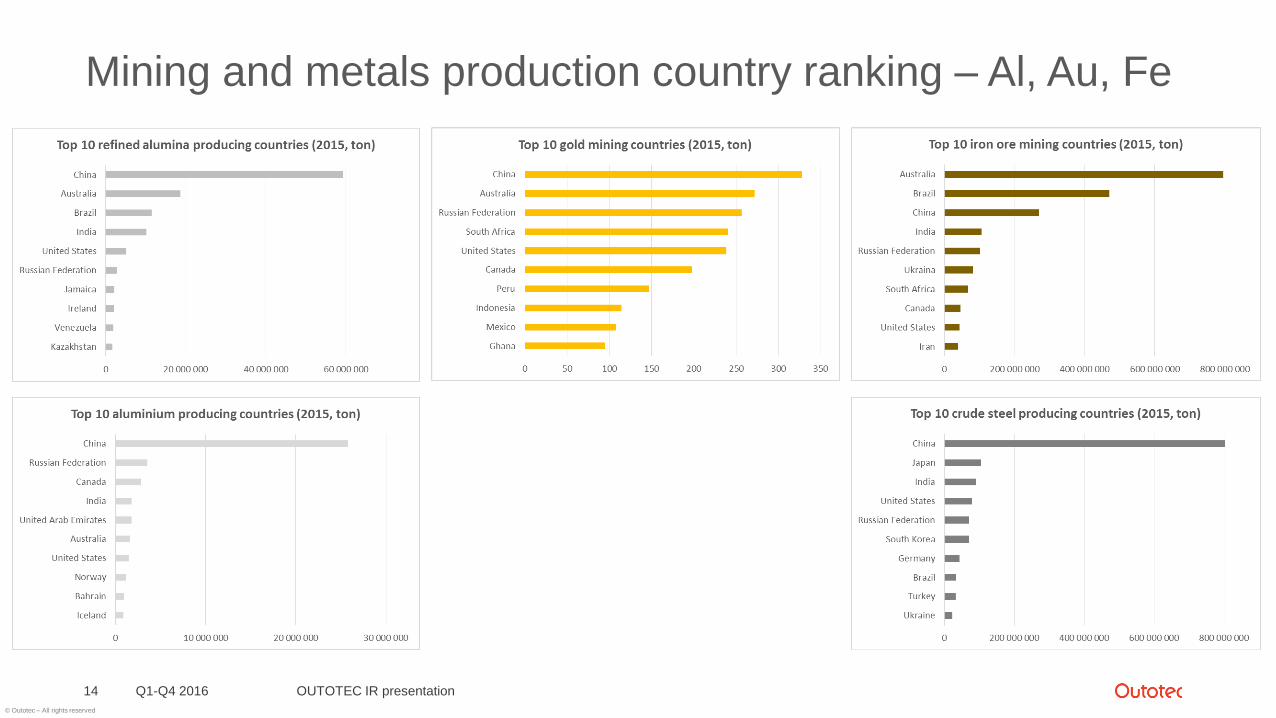

Mining and metals production country ranking – Al, Au, Fe

Q1-Q4 2016 OUTOTEC IR presentation14

© Outotec – All rights reserved

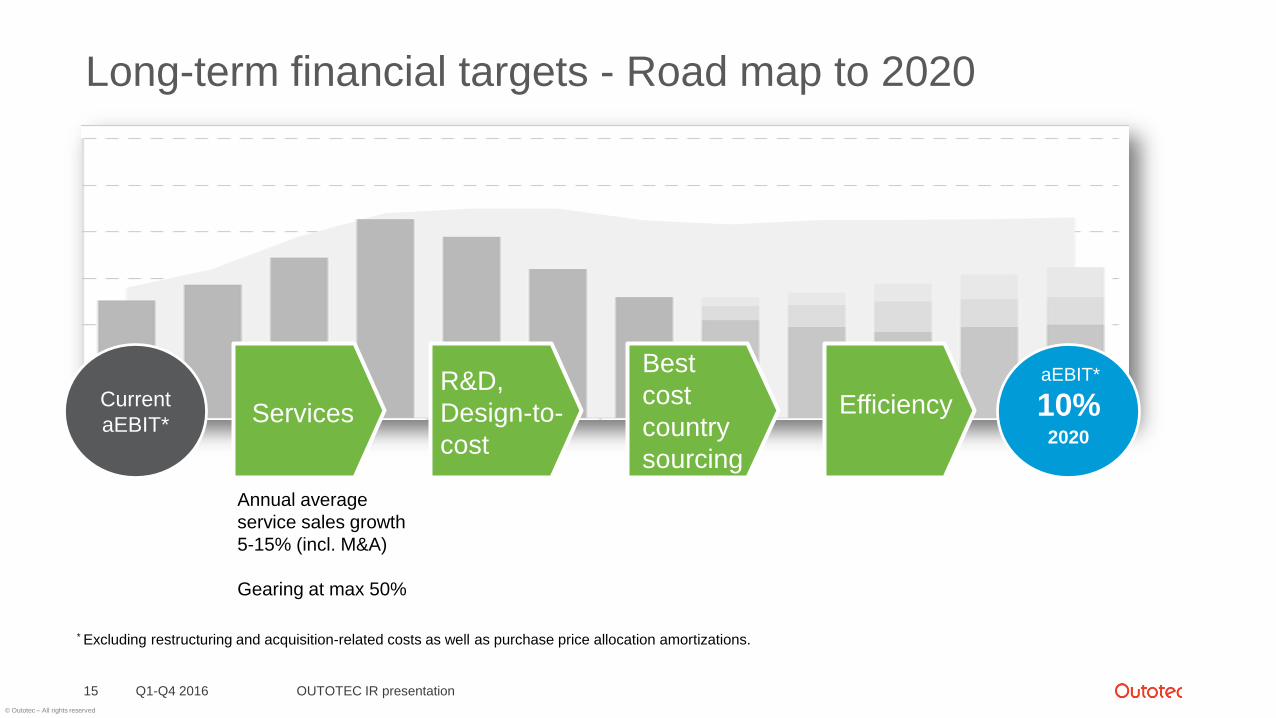

Long-term financial targets - Road map to 2020

Q1-Q4 2016 OUTOTEC IR presentation15

10%2020

Current

aEBIT*

aEBIT*

Services

R&D,

Design-to-

cost

Best

cost

country

sourcing

Efficiency

Annual average

service sales growth

5-15% (incl. M&A)

Gearing at max 50%

* Excluding restructuring and acquisition-related costs as well as purchase price allocation amortizations.

© Outotec – All rights reserved

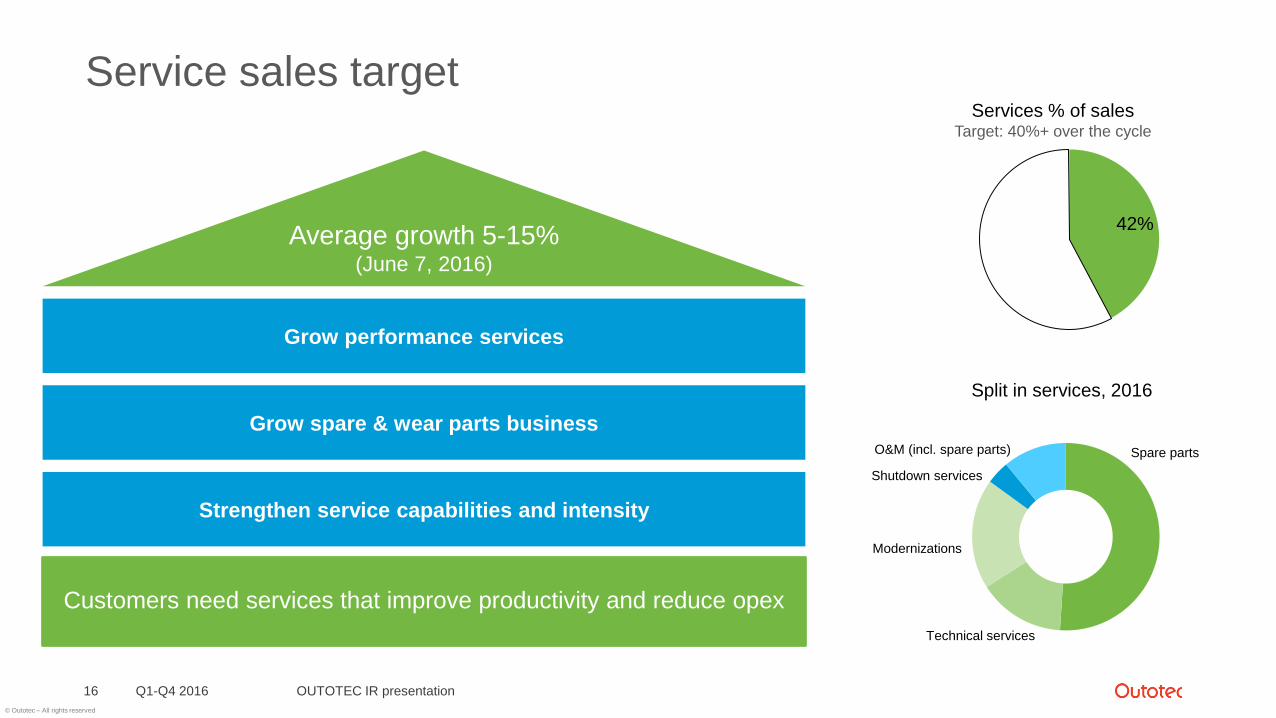

Service sales target

Q1-Q4 2016 OUTOTEC IR presentation16

Grow performance services

Grow spare & wear parts business

Strengthen service capabilities and intensity

Customers need services that improve productivity and reduce opex

Average growth 5-15%(June 7, 2016)

42%

Services % of salesTarget: 40%+ over the cycle

Spare parts

Technical services

Modernizations

Shutdown services

O&M (incl. spare parts)

Split in services, 2016

© Outotec – All rights reserved

Q1-Q4 2016 financial information

Q1-Q4 2016 OUTOTEC IR presentation17

© Outotec – All rights reserved

One MEW project

weakenedprofitability

Goodprofitability in

MineralsProcessing

Twosegments in

differentphases

EUR 70 million cost

savings

New Services business unit as of April 1,

2017

2016 in a nutshell

Q1-Q4 2016 OUTOTEC IR presentation18

© Outotec – All rights reserved

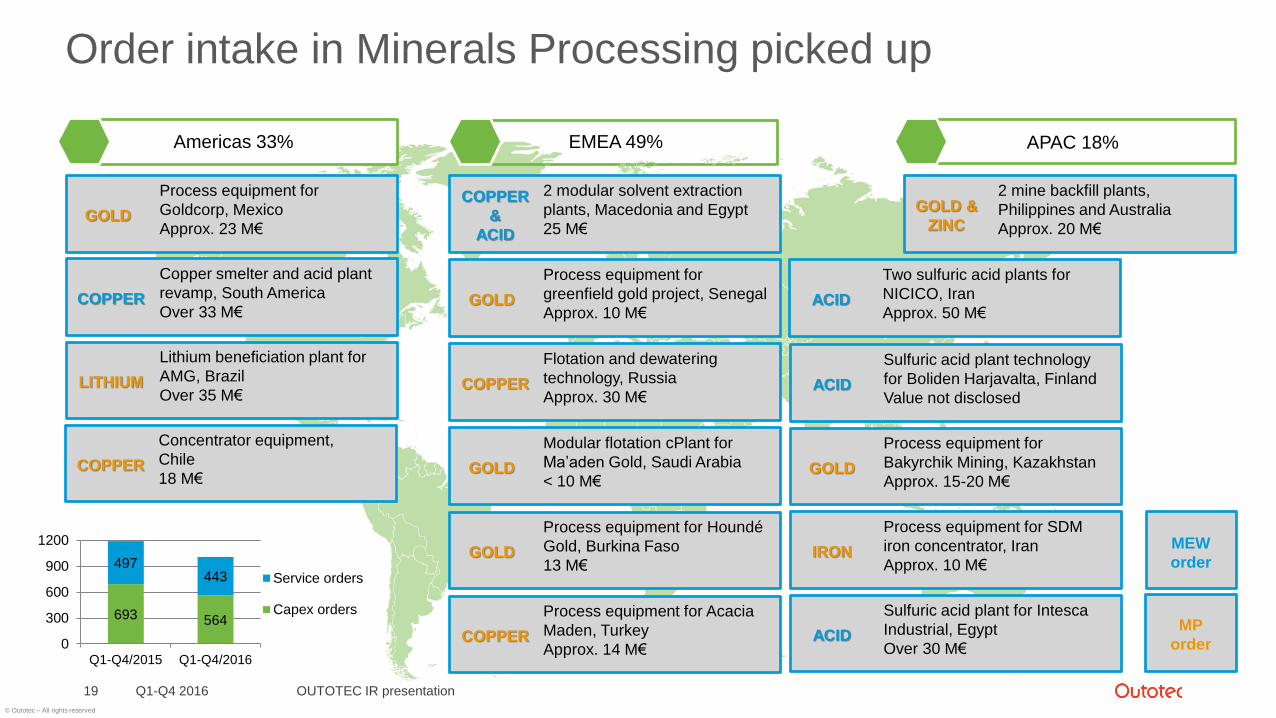

Order intake in Minerals Processing picked up

Q1-Q4 2016 OUTOTEC IR presentation19

Americas 33% EMEA 49% APAC 18%

GOLD

Process equipment for

Goldcorp, Mexico

Approx. 23 M€

COPPER

&

ACID

2 modular solvent extraction

plants, Macedonia and Egypt

25 M€

GOLD &

ZINC

2 mine backfill plants,

Philippines and Australia

Approx. 20 M€

GOLD

Process equipment for

greenfield gold project, Senegal

Approx. 10 M€

COPPER

Flotation and dewatering

technology, Russia

Approx. 30 M€

GOLD

Modular flotation cPlant for

Ma’aden Gold, Saudi Arabia

< 10 M€

COPPER

Copper smelter and acid plant

revamp, South America

Over 33 M€

GOLD

Process equipment for Houndé

Gold, Burkina Faso

13 M€

COPPER

Process equipment for Acacia

Maden, Turkey

Approx. 14 M€

GOLD

Process equipment for

Bakyrchik Mining, Kazakhstan

Approx. 15-20 M€

IRON

Process equipment for SDM

iron concentrator, Iran

Approx. 10 M€

ACID

Sulfuric acid plant for Intesca

Industrial, Egypt

Over 30 M€

ACID

Sulfuric acid plant technology

for Boliden Harjavalta, Finland

Value not disclosed

693 564

497443

0

300

600

900

1200

Q1-Q4/2015 Q1-Q4/2016

Service orders

Capex orders

LITHIUM

Lithium beneficiation plant for

AMG, Brazil

Over 35 M€

COPPER

Concentrator equipment,

Chile

18 M€

MEW

order

MP

order

ACID

Two sulfuric acid plants for

NICICO, Iran

Approx. 50 M€

© Outotec – All rights reserved

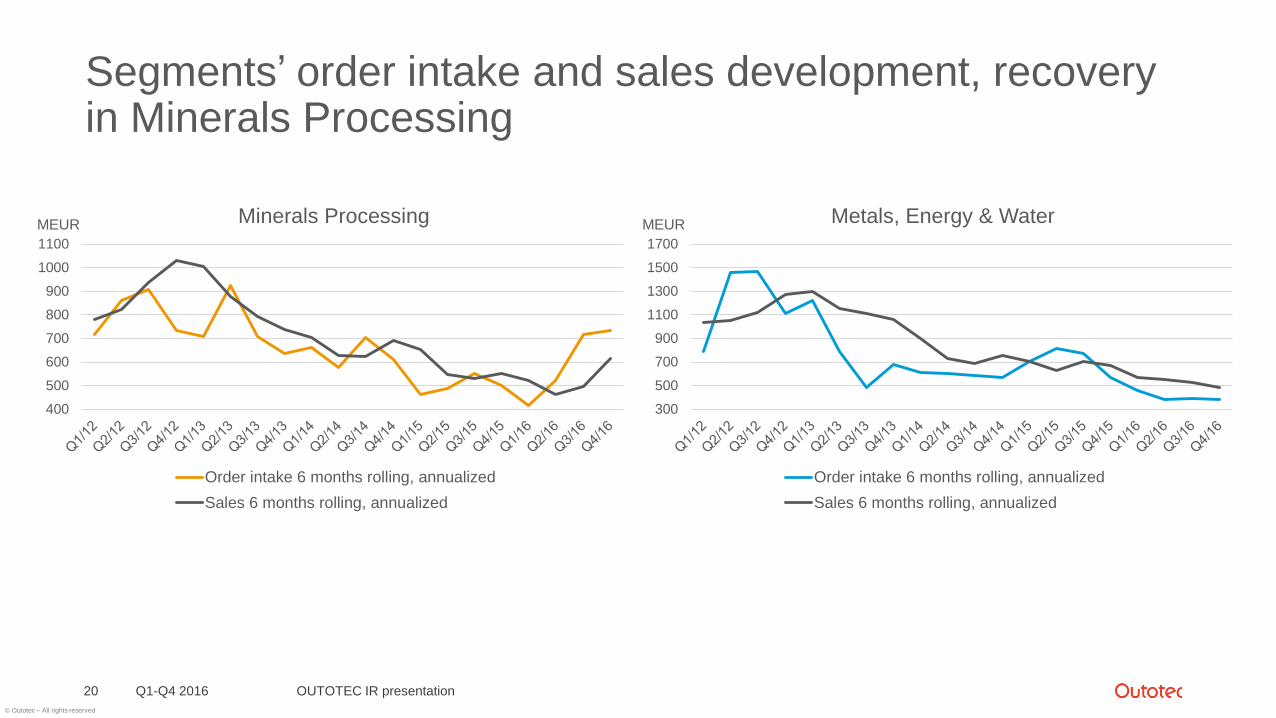

Segments’ order intake and sales development, recoveryin Minerals Processing

Q1-Q4 2016 OUTOTEC IR presentation20

300

500

700

900

1100

1300

1500

1700

Metals, Energy & Water

Order intake 6 months rolling, annualized

Sales 6 months rolling, annualized

MEURMEUR

400

500

600

700

800

900

1000

1100

Minerals Processing

Order intake 6 months rolling, annualized

Sales 6 months rolling, annualized

© Outotec – All rights reserved

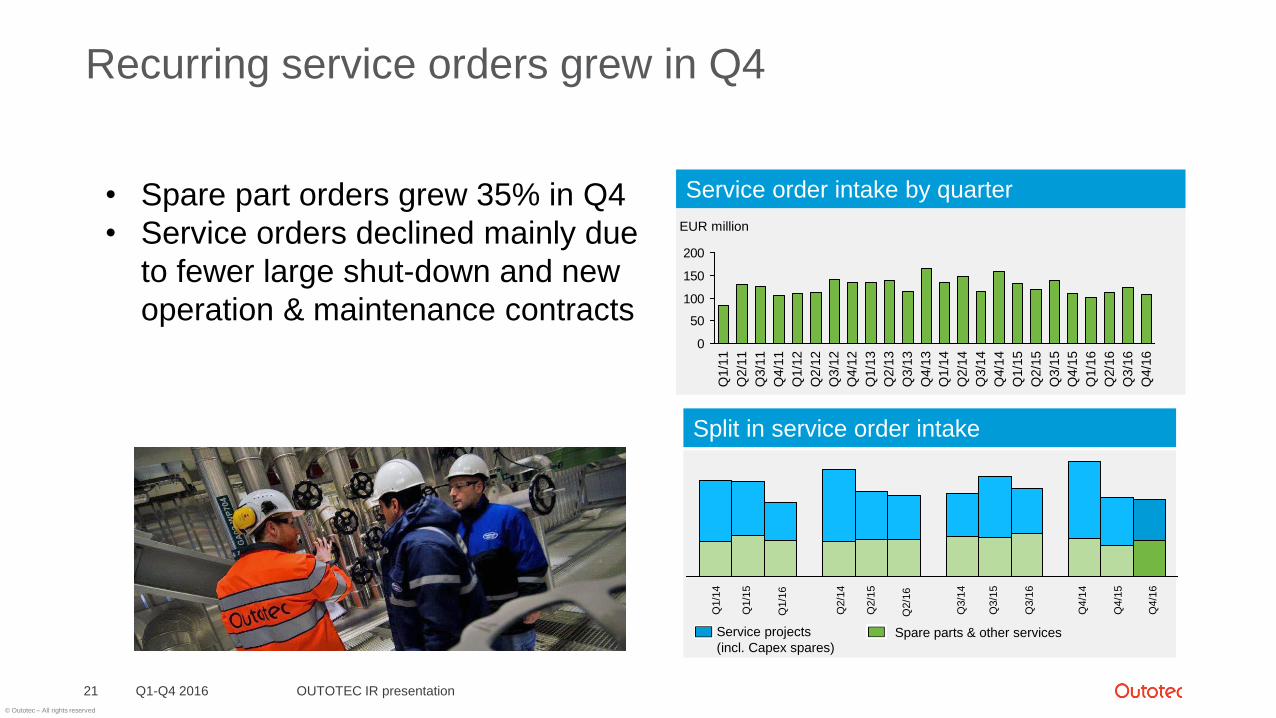

Service order intake by quarter

0

50

100

150

200

Q4/1

6

EUR million

Q3/1

6

Q2/1

6

Q1/1

6

Q4/1

5

Q3/1

5

Q2/1

5

Q1/1

5

Q4/1

4

Q3/1

4

Q2/1

4

Q1/1

4

Q4/1

3

Q3/1

3

Q2/1

3

Q1/1

3

Q4/1

2

Q3/1

2

Q2/1

2

Q1/1

2

Q4/1

1

Q3/1

1

Q2/1

1

Q1/1

1

Recurring service orders grew in Q4

Q1-Q4 2016 OUTOTEC IR presentation21

Split in service order intake

Spare parts & other servicesService projects

(incl. Capex spares)

Q1/1

4

Q1/1

5

Q2/1

4

Q2/1

5

Q3/1

4

Q3/1

5

Q4/1

4

Q4/1

5

Q1/1

6

Q2/1

6

Q3/1

6

Q4/1

6

• Spare part orders grew 35% in Q4

• Service orders declined mainly due

to fewer large shut-down and new

operation & maintenance contracts

© Outotec – All rights reserved

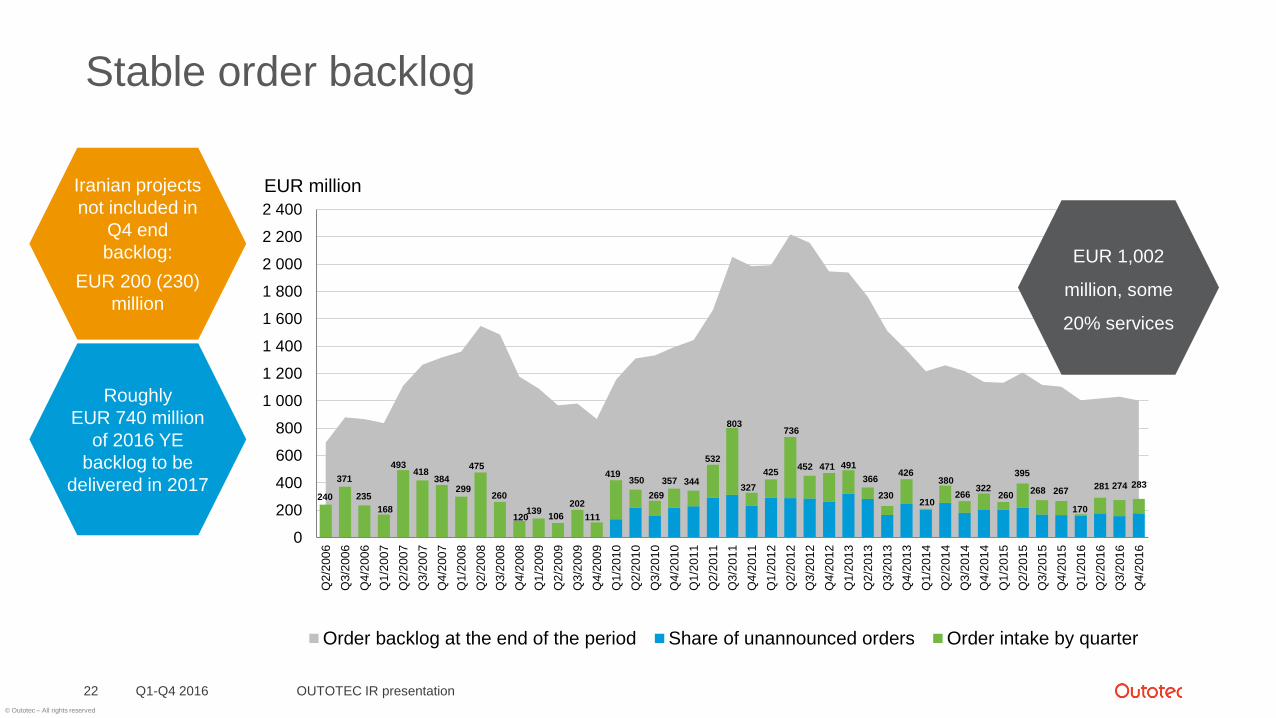

Stable order backlog

Q1-Q4 2016 OUTOTEC IR presentation22

EUR millionIranian projects

not included in

Q4 end

backlog:

EUR 200 (230)

million

240

371

235

168

493418

384299

475

260

120139

106

202

111

419350

269

357 344

532

803

327

425

736

452 471 491

366

230

426

210

380

266322

260

395

268 267

170

281 274 283

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

Q2

/200

6

Q3

/200

6

Q4

/200

6

Q1

/200

7

Q2

/200

7

Q3

/200

7

Q4

/200

7

Q1

/200

8

Q2

/200

8

Q3

/200

8

Q4

/200

8

Q1

/200

9

Q2

/200

9

Q3

/200

9

Q4

/200

9

Q1

/201

0

Q2

/201

0

Q3

/201

0

Q4

/201

0

Q1

/201

1

Q2

/201

1

Q3

/201

1

Q4

/201

1

Q1

/201

2

Q2

/201

2

Q3

/201

2

Q4

/201

2

Q1

/201

3

Q2

/201

3

Q3

/201

3

Q4

/201

3

Q1

/201

4

Q2

/201

4

Q3

/201

4

Q4

/201

4

Q1

/201

5

Q2

/201

5

Q3

/201

5

Q4

/201

5

Q1

/201

6

Q2

/201

6

Q3

/201

6

Q4

/201

6

Order backlog at the end of the period Share of unannounced orders Order intake by quarter

Roughly

EUR 740 million

of 2016 YE

backlog to be

delivered in 2017

EUR 1,002

million, some

20% services

© Outotec – All rights reserved

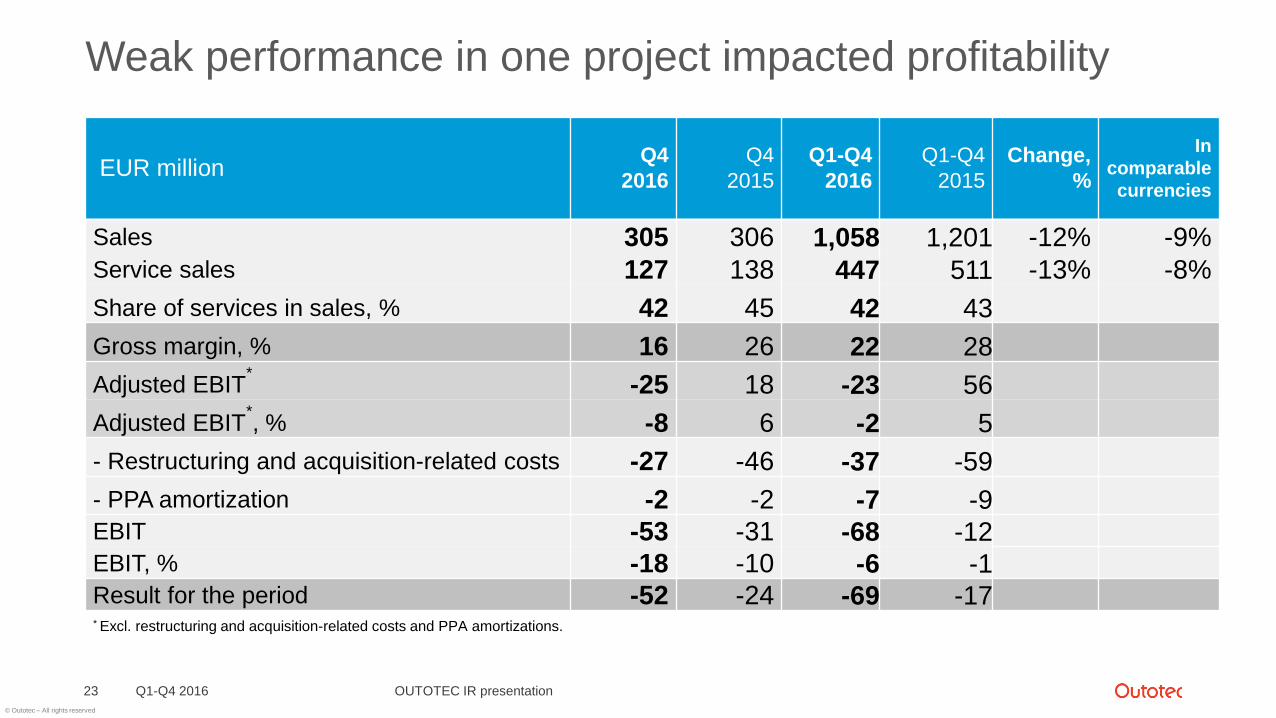

Weak performance in one project impacted profitability

Q1-Q4 2016 OUTOTEC IR presentation23

EUR millionQ4

2016

Q4

2015

Q1-Q4

2016

Q1-Q4

2015

Change,

%

In

comparable

currencies

Sales 305 306 1,058 1,201 -12% -9%

Service sales 127 138 447 511 -13% -8%

Share of services in sales, % 42 45 42 43

Gross margin, % 16 26 22 28

Adjusted EBIT*

-25 18 -23 56

Adjusted EBIT*, % -8 6 -2 5

- Restructuring and acquisition-related costs -27 -46 -37 -59

- PPA amortization -2 -2 -7 -9EBIT -53 -31 -68 -12EBIT, % -18 -10 -6 -1Result for the period -52 -24 -69 -17* Excl. restructuring and acquisition-related costs and PPA amortizations.

© Outotec – All rights reserved

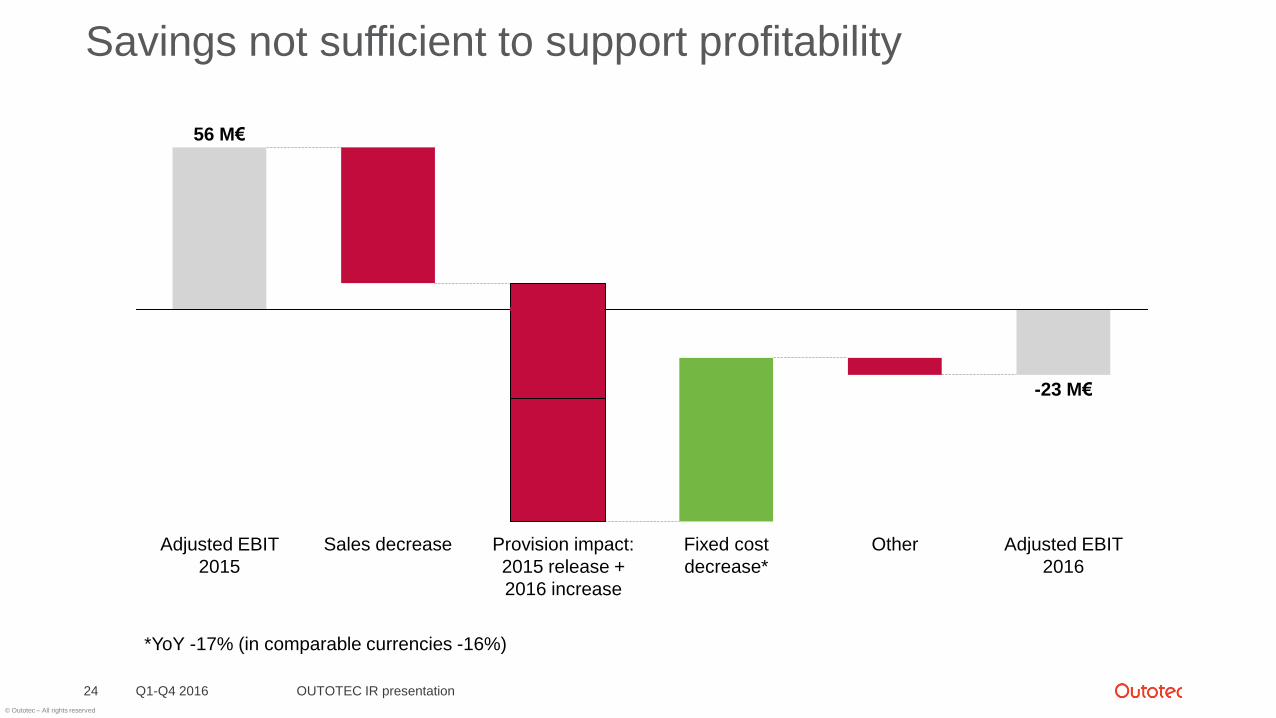

Savings not sufficient to support profitability

Q1-Q4 2016 OUTOTEC IR presentation24

Provision impact:

2015 release +

2016 increase

-23 M€

Fixed cost

decrease*

Other Adjusted EBIT

2016

Sales decreaseAdjusted EBIT

2015

56 M€

*YoY -17% (in comparable currencies -16%)

© Outotec – All rights reserved

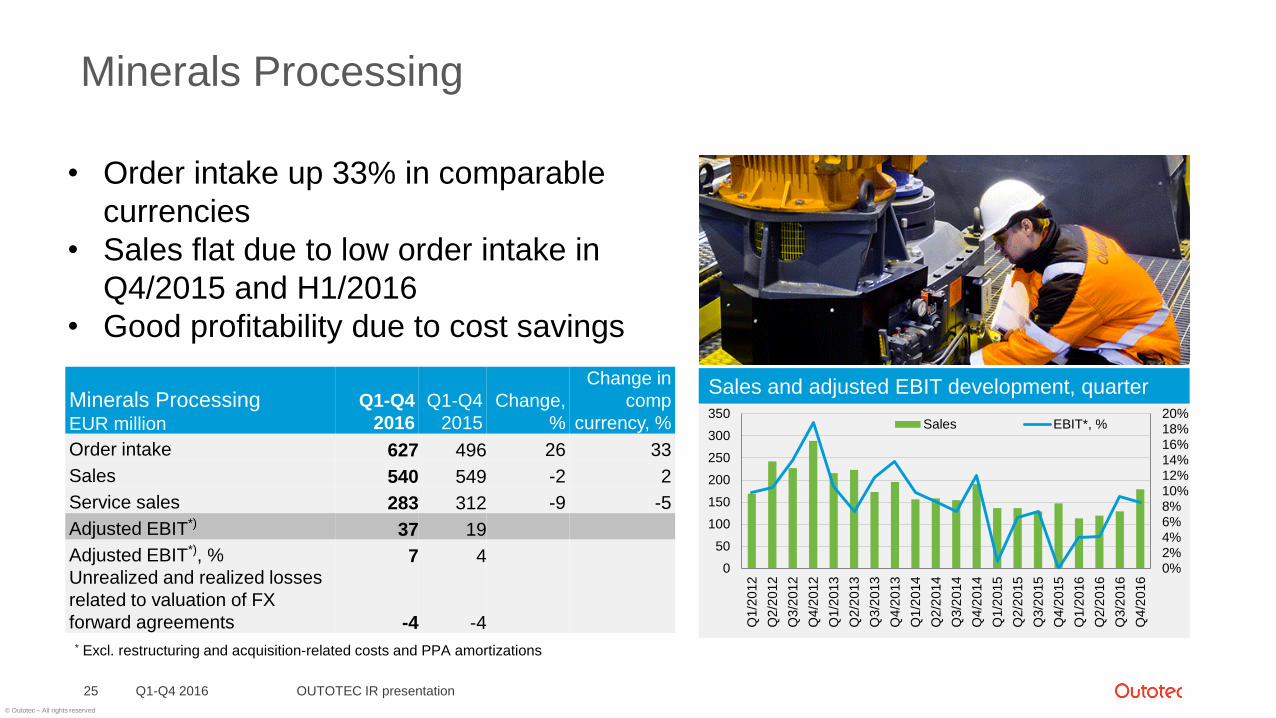

Minerals Processing

Q1-Q4 2016 OUTOTEC IR presentation25

0%2%4%6%8%10%12%14%16%18%20%

0

50

100

150

200

250

300

350

Q1/2

012

Q2/2

012

Q3/2

012

Q4/2

012

Q1/2

013

Q2/2

013

Q3/2

013

Q4/2

013

Q1/2

014

Q2/2

014

Q3/2

014

Q4/2

014

Q1/2

015

Q2/2

015

Q3/2

015

Q4/2

015

Q1/2

016

Q2/2

016

Q3/2

016

Q4/2

016

Sales EBIT*, %

Sales and adjusted EBIT development, quarter

• Order intake up 33% in comparable

currencies

• Sales flat due to low order intake in

Q4/2015 and H1/2016

• Good profitability due to cost savings

Minerals ProcessingEUR million

Q1-Q4

2016

Q1-Q4

2015

Change,

%

Change in

comp

currency, %

Order intake 627 496 26 33

Sales 540 549 -2 2

Service sales 283 312 -9 -5

Adjusted EBIT*) 37 19

Adjusted EBIT*), % 7 4Unrealized and realized losses

related to valuation of FX

forward agreements -4 -4

* Excl. restructuring and acquisition-related costs and PPA amortizations

© Outotec – All rights reserved

-40%

-30%

-20%

-10%

0%

10%

20%

0

50

100

150

200

250

300

350

400

Q1/2

012

Q2/2

012

Q3/2

012

Q4/2

012

Q1/2

013

Q2/2

013

Q3/2

013

Q4/2

013

Q1/2

014

Q2/2

014

Q3/2

014

Q4/2

014

Q1/2

015

Q2/2

015

Q3/2

015

Q4/2

015

Q1/2

016

Q2/2

016

Q3/2

016

Q4/2

016

Sales EBIT*, %

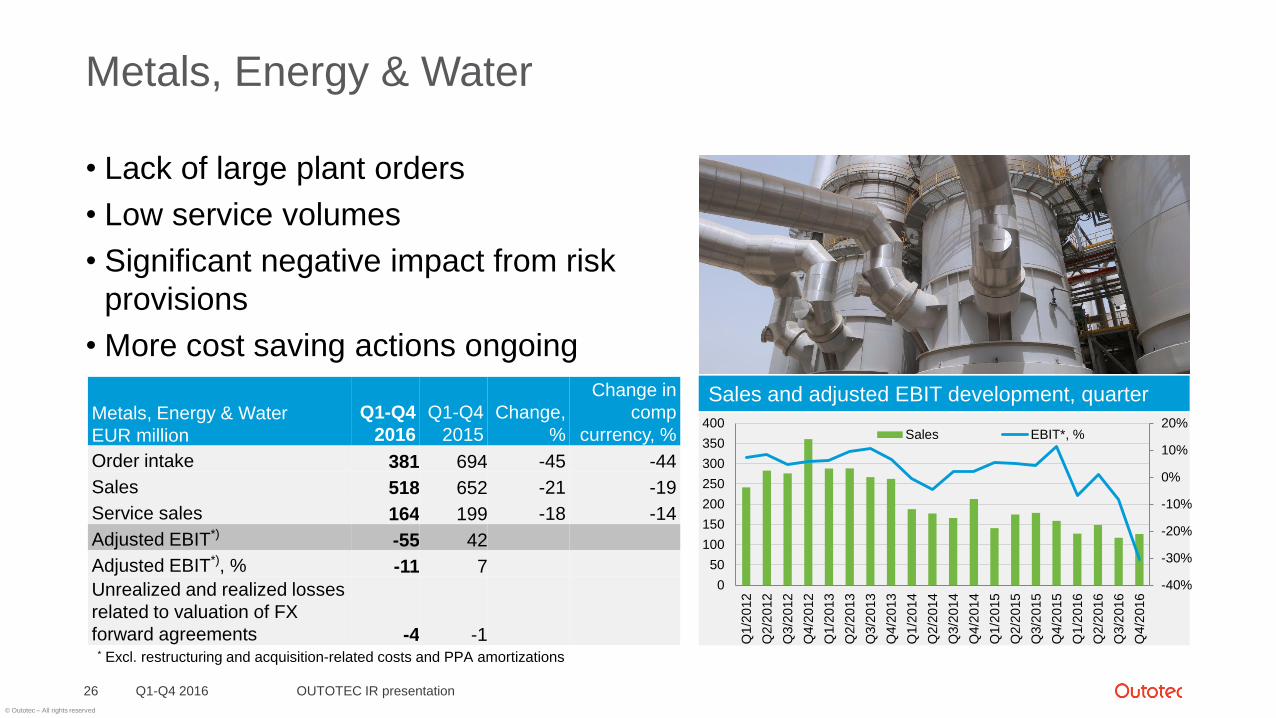

Metals, Energy & Water

• Lack of large plant orders

• Low service volumes

• Significant negative impact from risk

provisions

• More cost saving actions ongoing

Q1-Q4 2016 OUTOTEC IR presentation26

Metals, Energy & Water

EUR million

Q1-Q4

2016

Q1-Q4

2015

Change,

%

Change in

comp

currency, %

Order intake 381 694 -45 -44

Sales 518 652 -21 -19

Service sales 164 199 -18 -14

Adjusted EBIT*) -55 42

Adjusted EBIT*), % -11 7

Unrealized and realized losses

related to valuation of FX

forward agreements -4 -1* Excl. restructuring and acquisition-related costs and PPA amortizations

Sales and adjusted EBIT development, quarter

© Outotec – All rights reserved

Mature backlog, lack of large advance payments and restructuring costs impacted cash flow

Q1-Q4 2016 OUTOTEC IR presentation27

EUR millionQ1-Q4

2016

Q1-Q4

2015

Result for the period -69 -17

Adjustments

- Depreciation & amortization 43 40

- Other adjustments 21 -0

Change in working capital -67 54

Interest -5 -4

Taxes -6 -3

NET CASH FROM OPERATING ACTIVITIES -85 70

NET CASH USED IN INVESTING ACTIVITIES (incl. Capex and acquisitions) -23 -87

Repayments & borrowings of non-current debt -112 49

Hybrid bond 150 -

Dividend - -18

Other financing activities -7 15

NET CASH FROM FINANCING ACTIVITIES 32 45

NET CHANGE IN CASH AND CASH EQUIVALENTS -76 28

Foreign exchange rate effect on cash and cash equivalents 8 -9

Cash and cash equivalents at Dec 31 233 301

© Outotec – All rights reserved

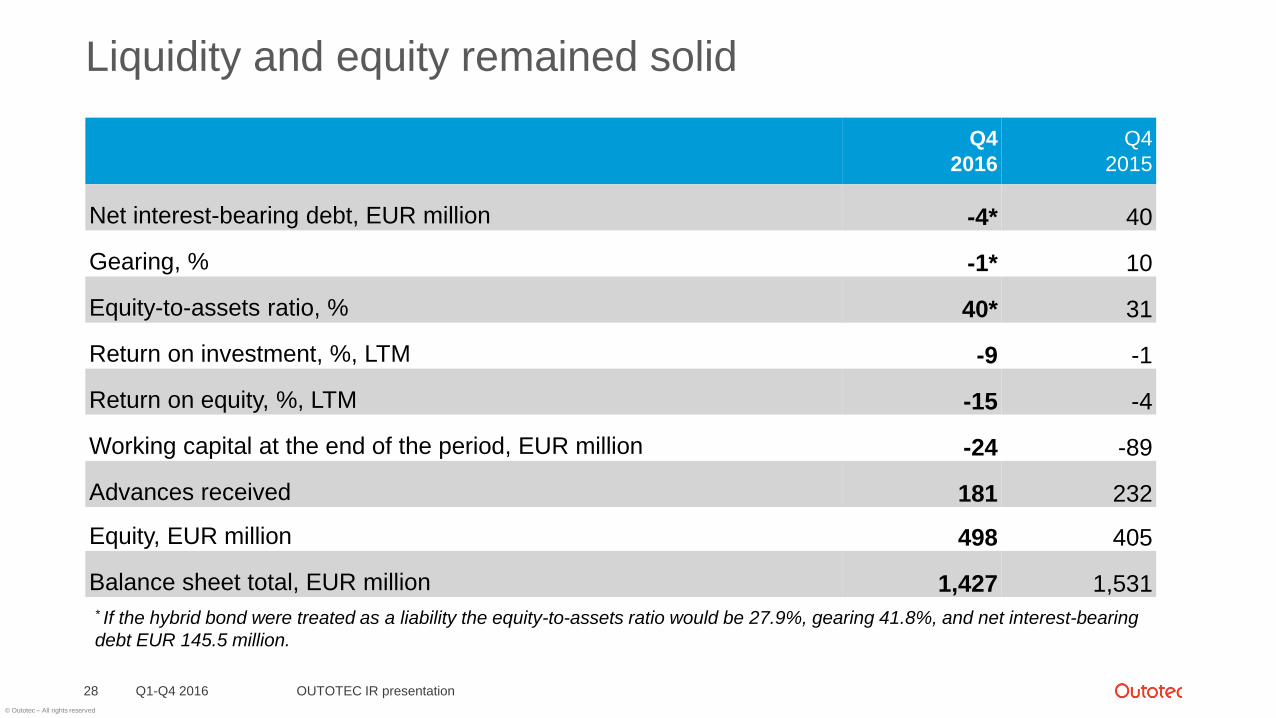

Liquidity and equity remained solid

Q1-Q4 2016 OUTOTEC IR presentation28

Q4

2016

Q4

2015

Net interest-bearing debt, EUR million -4* 40

Gearing, % -1* 10

Equity-to-assets ratio, % 40* 31

Return on investment, %, LTM -9 -1

Return on equity, %, LTM -15 -4

Working capital at the end of the period, EUR million -24 -89

Advances received 181 232

Equity, EUR million 498 405

Balance sheet total, EUR million 1,427 1,531* If the hybrid bond were treated as a liability the equity-to-assets ratio would be 27.9%, gearing 41.8%, and net interest-bearing

debt EUR 145.5 million.

© Outotec – All rights reserved

Market outlook

Q1-Q4 2016 OUTOTEC IR presentation29

Activity increasing in theMetals, Energy &

Water markets

Global economicand politicaluncertaintycontinues

The MineralsProcessing

market expectedto bring newopportunities

Timing of largeorders remains

uncertain

© Outotec – All rights reserved

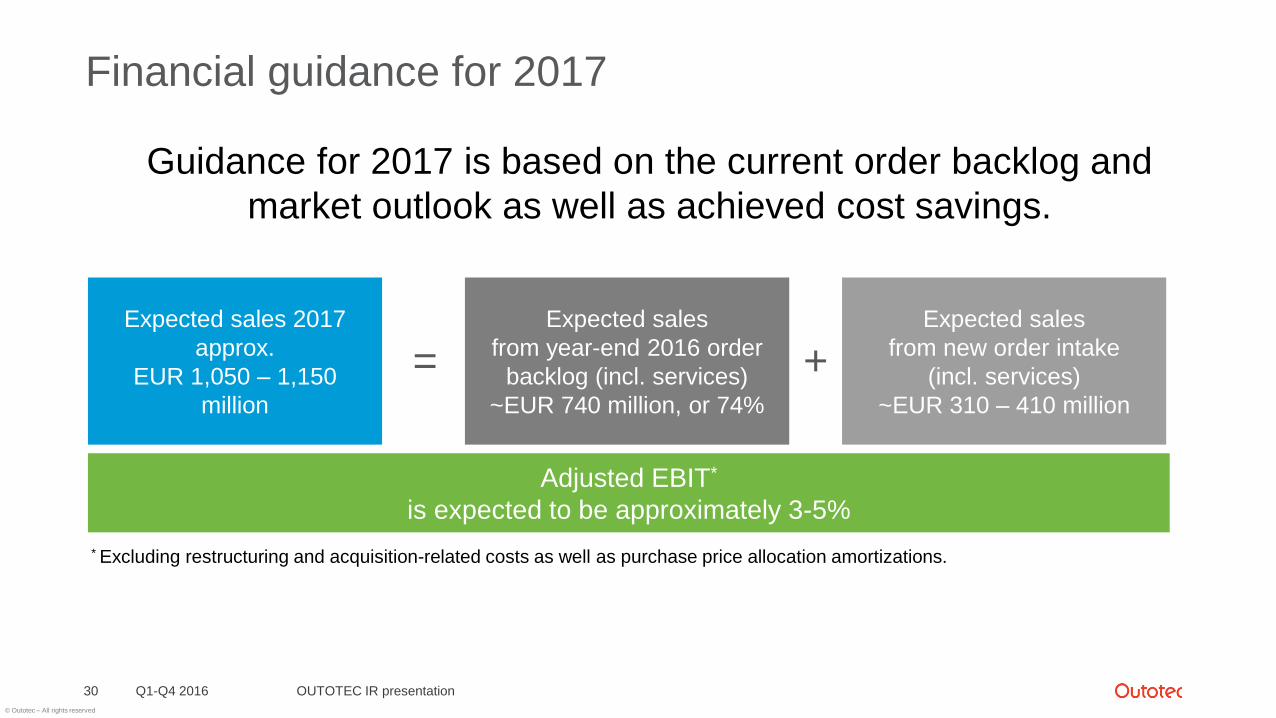

Guidance for 2017 is based on the current order backlog and

market outlook as well as achieved cost savings.

Financial guidance for 2017

Q1-Q4 2016 OUTOTEC IR presentation30

Expected sales

from year-end 2016 order

backlog (incl. services)

~EUR 740 million, or 74%

Expected sales

from new order intake

(incl. services)

~EUR 310 – 410 million

+=Expected sales 2017

approx.

EUR 1,050 – 1,150

million

Adjusted EBIT*

is expected to be approximately 3-5%

* Excluding restructuring and acquisition-related costs as well as purchase price allocation amortizations.

© Outotec – All rights reserved

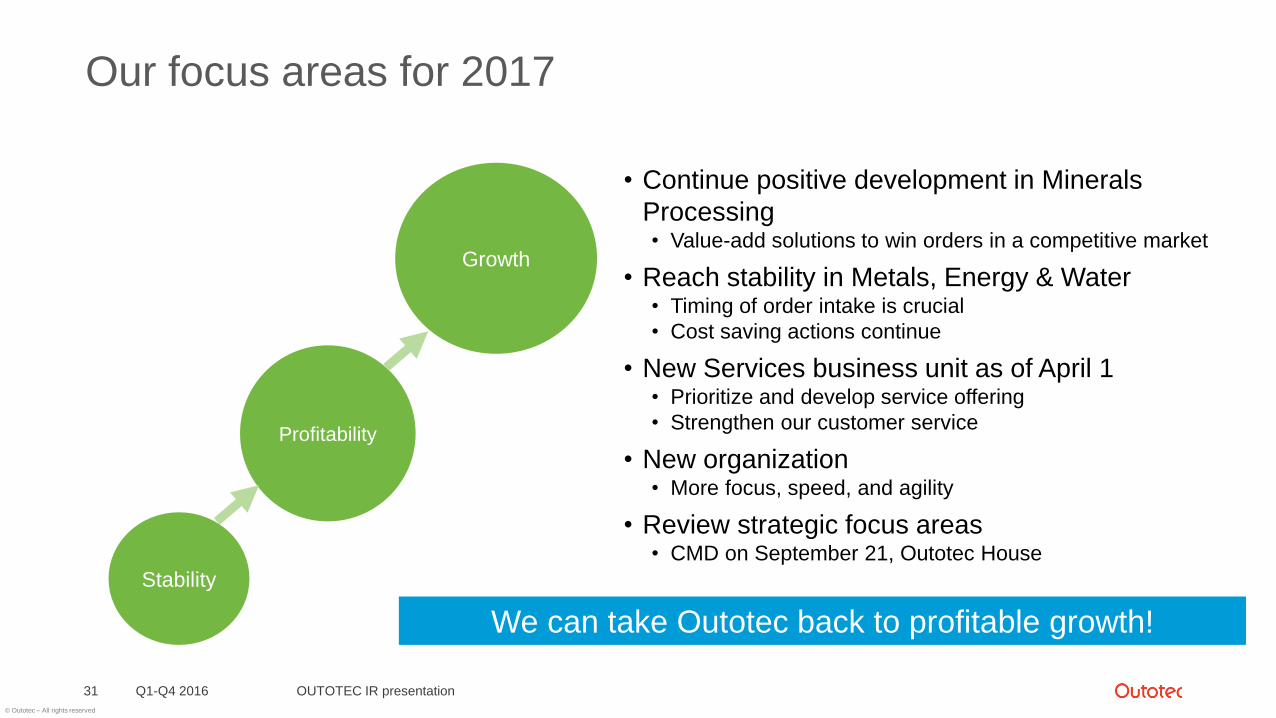

Our focus areas for 2017

Q1-Q4 2016 OUTOTEC IR presentation31

We can take Outotec back to profitable growth!

Stability

Profitability

Growth

• Continue positive development in Minerals

Processing• Value-add solutions to win orders in a competitive market

• Reach stability in Metals, Energy & Water• Timing of order intake is crucial

• Cost saving actions continue

• New Services business unit as of April 1• Prioritize and develop service offering

• Strengthen our customer service

• New organization• More focus, speed, and agility

• Review strategic focus areas• CMD on September 21, Outotec House

© Outotec – All rights reserved

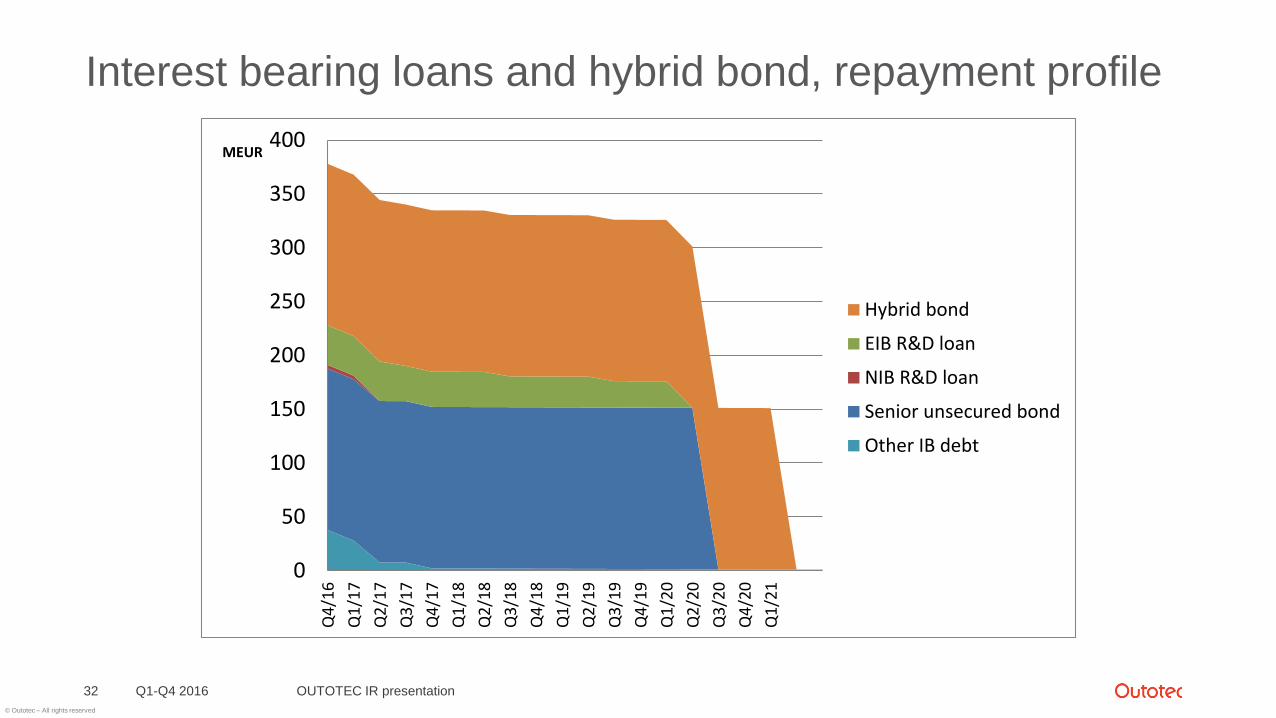

Interest bearing loans and hybrid bond, repayment profile

Q1-Q4 2016 OUTOTEC IR presentation32

0

50

100

150

200

250

300

350

400

Q4

/16

Q1

/17

Q2

/17

Q3

/17

Q4

/17

Q1

/18

Q2

/18

Q3

/18

Q4

/18

Q1

/19

Q2

/19

Q3

/19

Q4

/19

Q1

/20

Q2

/20

Q3

/20

Q4

/20

Q1

/21

MEUR

Hybrid bond

EIB R&D loan

NIB R&D loan

Senior unsecured bond

Other IB debt

© Outotec – All rights reserved

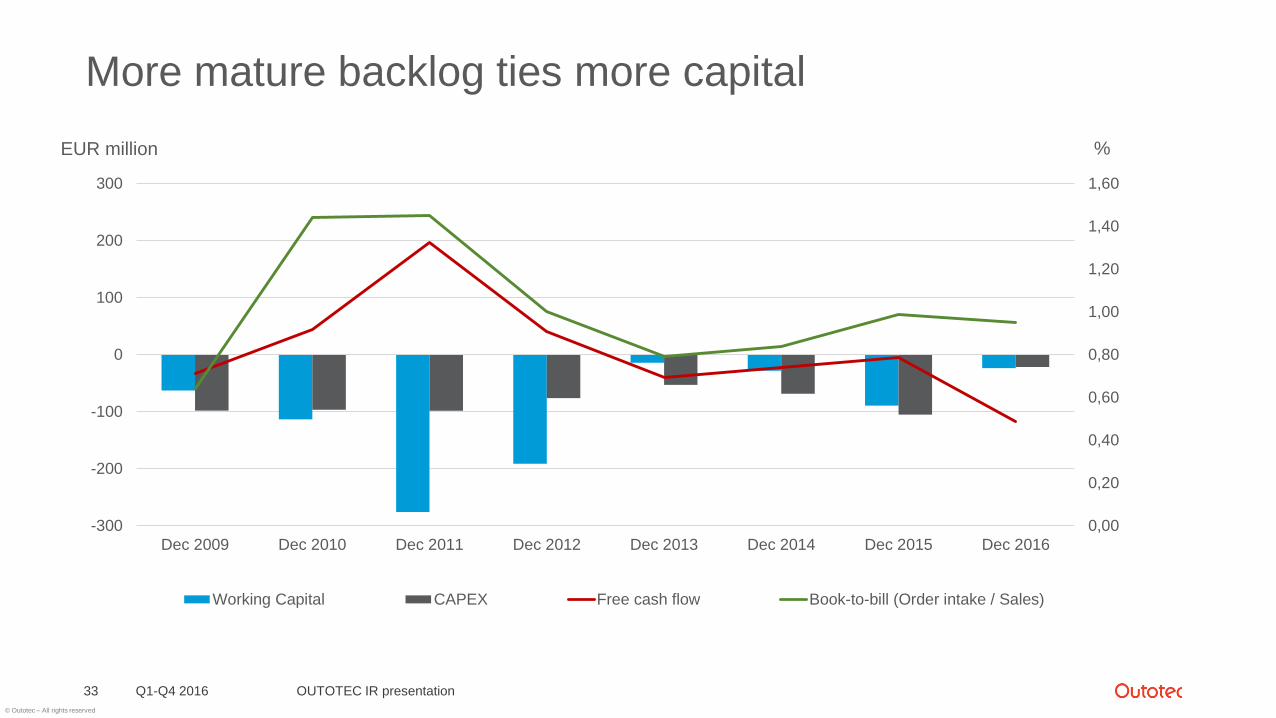

More mature backlog ties more capital

Q1-Q4 2016 OUTOTEC IR presentation33

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

-300

-200

-100

0

100

200

300

Dec 2009 Dec 2010 Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015 Dec 2016

Working Capital CAPEX Free cash flow Book-to-bill (Order intake / Sales)

EUR million %

© Outotec – All rights reserved

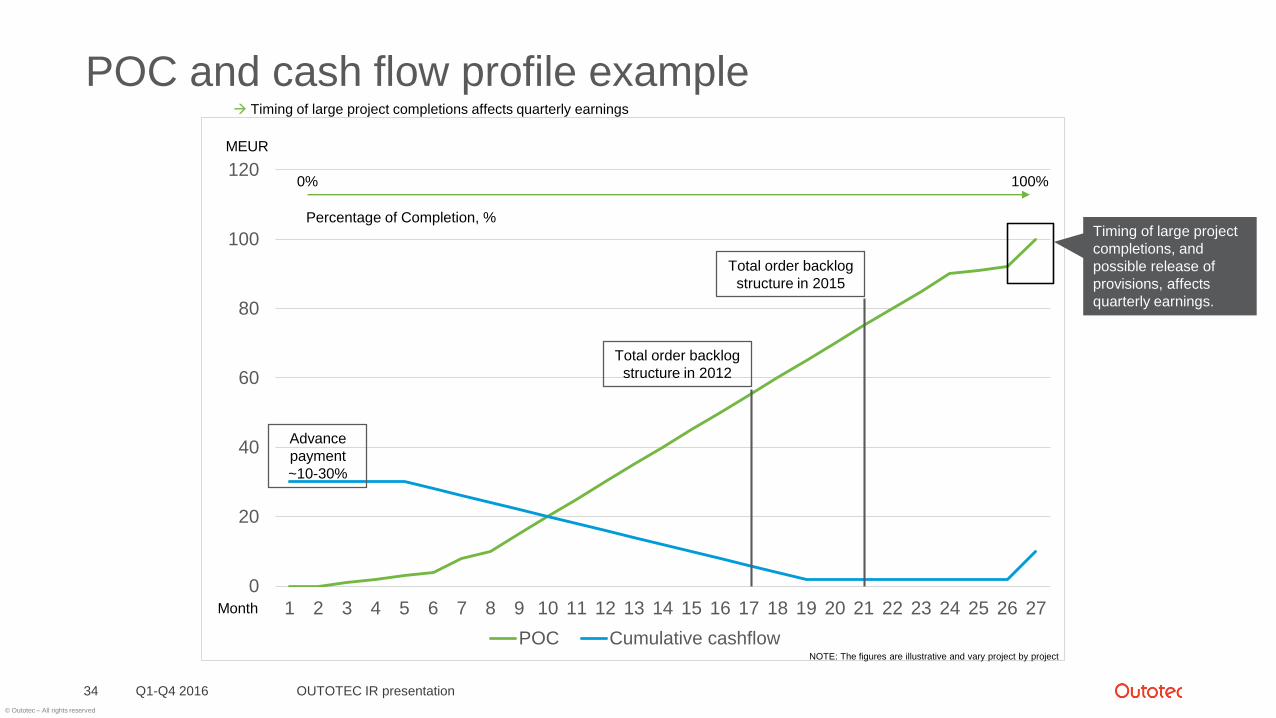

POC and cash flow profile example

Q1-Q4 2016 OUTOTEC IR presentation34

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

POC Cumulative cashflow

MEUR

Month

Total order backlog

structure in 2012

Total order backlog

structure in 2015

0% 100%

Percentage of Completion, %Timing of large project

completions, and

possible release of

provisions, affects

quarterly earnings.

Advance

payment

~10-30%

NOTE: The figures are illustrative and vary project by project

Timing of large project completions affects quarterly earnings

© Outotec – All rights reserved

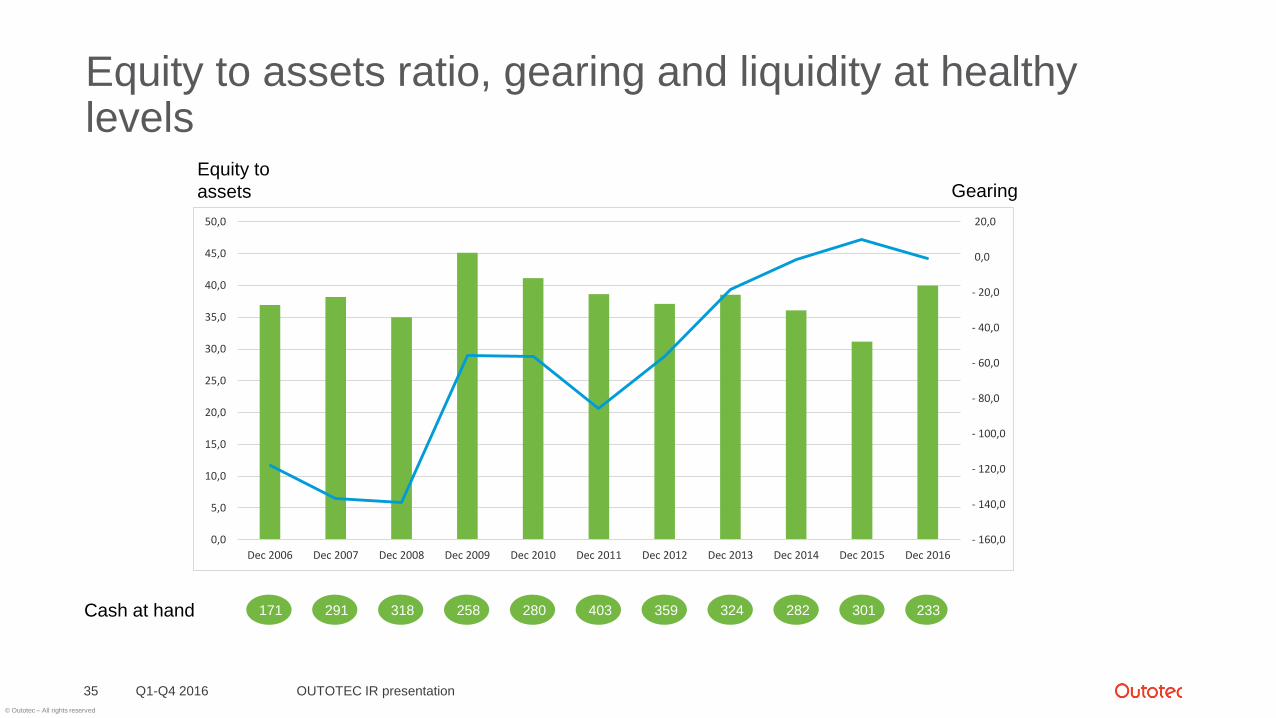

Equity to assets ratio, gearing and liquidity at healthylevels

Q1-Q4 2016 OUTOTEC IR presentation35

171 291 318 258 280 403 359 324 282 301 Cash at hand

Equity to

assets Gearing

233

- 160,0

- 140,0

- 120,0

- 100,0

- 80,0

- 60,0

- 40,0

- 20,0

0,0

20,0

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

50,0

Dec 2006 Dec 2007 Dec 2008 Dec 2009 Dec 2010 Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015 Dec 2016

© Outotec – All rights reserved

Customer solutions

Q1-Q4 2016 OUTOTEC IR presentation36

© Outotec – All rights reserved

Laiva Gold mine in FinlandCustomer case, ore sorting

Q1-Q4 2016 OUTOTEC IR presentation37

Outotec solution

• Outotec sensor-based ore

sorting solution removing

waste rock and improving the

head grade.

• When waste rock is removed

there is less ore feed to the

crushing and grinding circuit,

reducing energy and water

consumption

Customer challenge

• Mine is closed because of low head

grade ore

• Study completed around Outotec ore

sorting solution considering reopening

the mine

Study indicates that the Outotec ore sorting solution

enables reopening the mine:

“The economic assessment for the Laiva Gold Mine

indicated the potential for restarting the site, which

can be operated on a long-term basis at a broad

range of commodity prices. Base-case net present

value of €77 million, producing 529,000 troy ounces

of gold over a seven-year mine life.”

© Outotec – All rights reserved

Reducing mill downtime at a gold mineCustomer case, comminution

Q1-Q4 2016 OUTOTEC IR presentation38

Customer challenge

• Excessive grinding mill downtime during the year

leading to decreased yearly production

• Unplanned mill downtime due to liner failure

• Inadequate tooling

• Limited reline shutdown planning

• Coordination between different maintenance

vendors

• In total of over 340 hours downtime

due to mill maintenance

Outotec solution

• Pre shutdown planning

• Liner redesign – to reduce the number of pieces

• Tooling improvements – liner handler, skid steers & hand tooling

• Changes to liner fixtures & fittings

• Continuous Improvement Program

• Optimizing liner life time through Outotec patented MillMapper™ software

Customer benefits

• 50% less downtime due to mill

maintenance

• In total a reduction of 170 hours

of reline incurred downtime

• Safer, less labor intensive relines

• Circa 12-14 million USD in

additional production revenue

© Outotec – All rights reserved

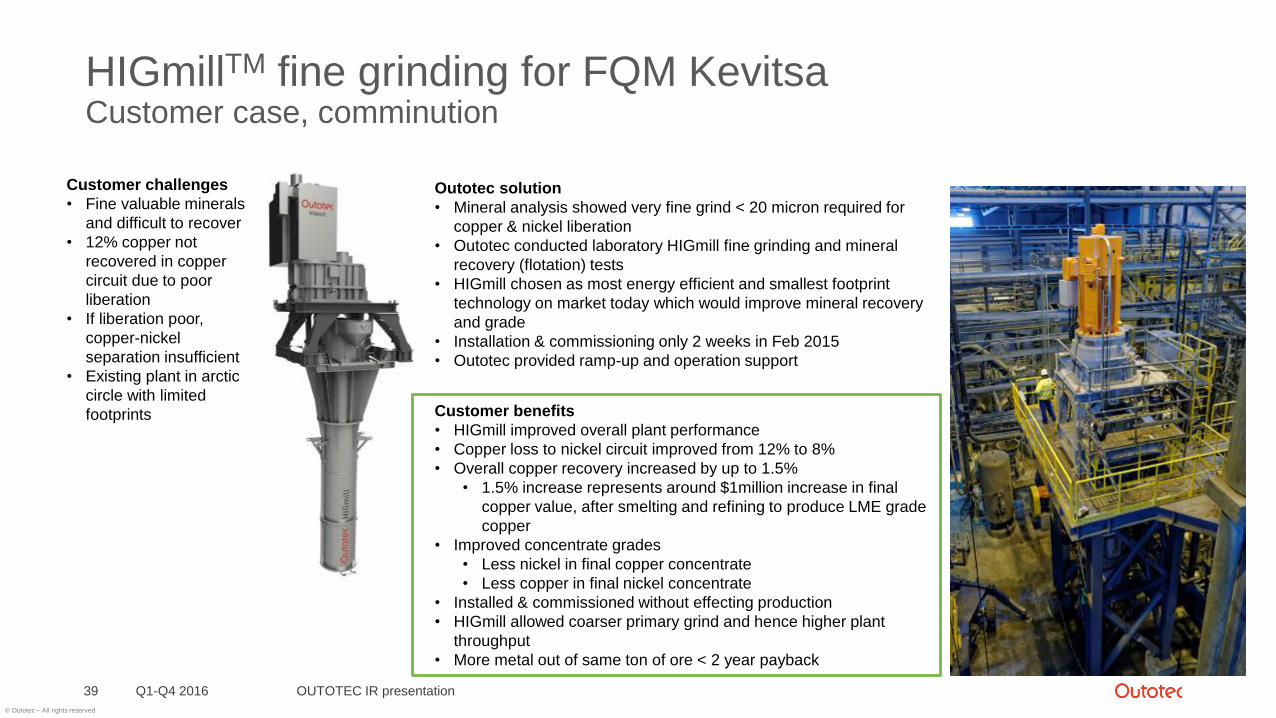

HIGmillTM fine grinding for FQM KevitsaCustomer case, comminution

Customer challenges

• Fine valuable minerals

and difficult to recover

• 12% copper not

recovered in copper

circuit due to poor

liberation

• If liberation poor,

copper-nickel

separation insufficient

• Existing plant in arctic

circle with limited

footprints

Q1-Q4 2016 OUTOTEC IR presentation39

Outotec solution

• Mineral analysis showed very fine grind < 20 micron required for

copper & nickel liberation

• Outotec conducted laboratory HIGmill fine grinding and mineral

recovery (flotation) tests

• HIGmill chosen as most energy efficient and smallest footprint

technology on market today which would improve mineral recovery

and grade

• Installation & commissioning only 2 weeks in Feb 2015

• Outotec provided ramp-up and operation support

Customer benefits

• HIGmill improved overall plant performance

• Copper loss to nickel circuit improved from 12% to 8%

• Overall copper recovery increased by up to 1.5%

• 1.5% increase represents around $1million increase in final

copper value, after smelting and refining to produce LME grade

copper

• Improved concentrate grades

• Less nickel in final copper concentrate

• Less copper in final nickel concentrate

• Installed & commissioned without effecting production

• HIGmill allowed coarser primary grind and hence higher plant

throughput

• More metal out of same ton of ore < 2 year payback

© Outotec – All rights reserved

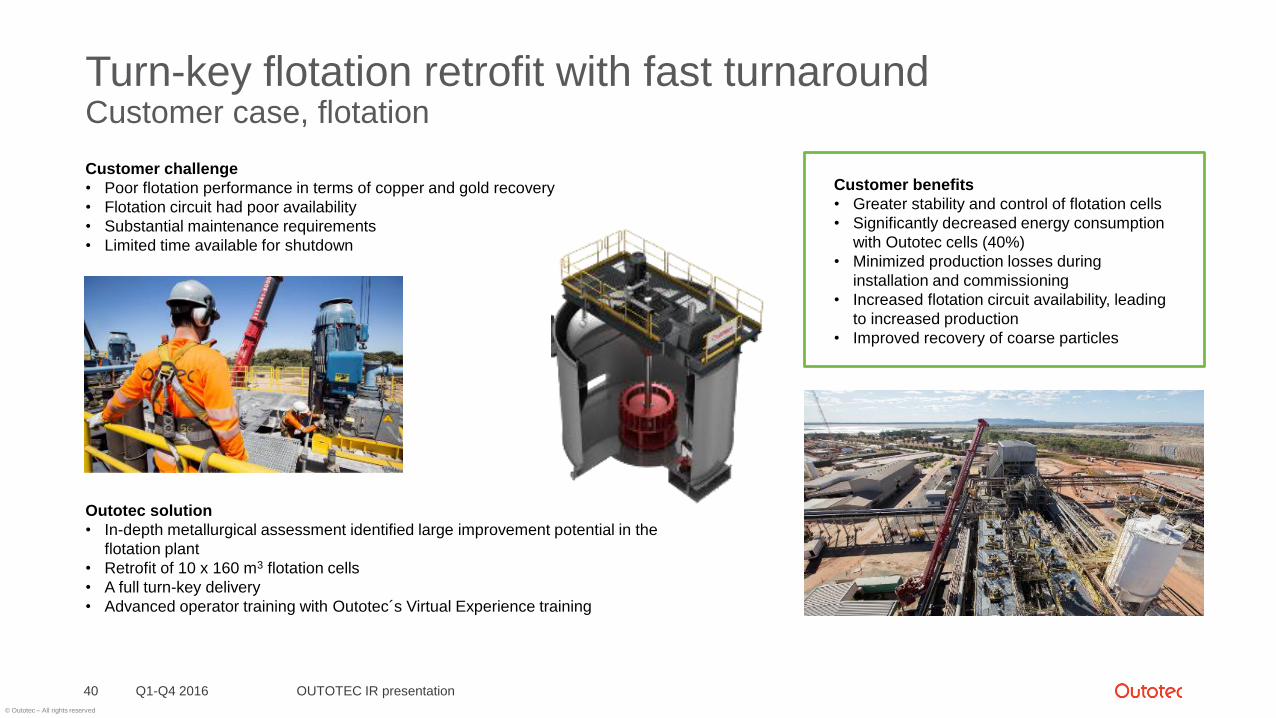

Turn-key flotation retrofit with fast turnaroundCustomer case, flotation

Customer challenge

• Poor flotation performance in terms of copper and gold recovery

• Flotation circuit had poor availability

• Substantial maintenance requirements

• Limited time available for shutdown

Q1-Q4 2016 OUTOTEC IR presentation40

Customer benefits

• Greater stability and control of flotation cells

• Significantly decreased energy consumption

with Outotec cells (40%)

• Minimized production losses during

installation and commissioning

• Increased flotation circuit availability, leading

to increased production

• Improved recovery of coarse particles

Outotec solution

• In-depth metallurgical assessment identified large improvement potential in the

flotation plant

• Retrofit of 10 x 160 m3 flotation cells

• A full turn-key delivery

• Advanced operator training with Outotec´s Virtual Experience training

© Outotec – All rights reserved

Digitalization creating new growth and opportunities -managing water balance and quality at mine sites

Q1-Q4 2016 OUTOTEC IR presentation41

Solution: Intelligent digital solution for monitoring and managing data

on the mine site’s water balance and quality.

Value: Sustainable balance of water supply and consumption,

while stabilizing production and reducing business risks.

Online

monitoring

Digital

platform

Modeling &

simulation

Predictability

& reliability

Access

to water

Alternative

water

sources

Stable

process

Mitigation

of risks

License

to

operate

© Outotec – All rights reserved

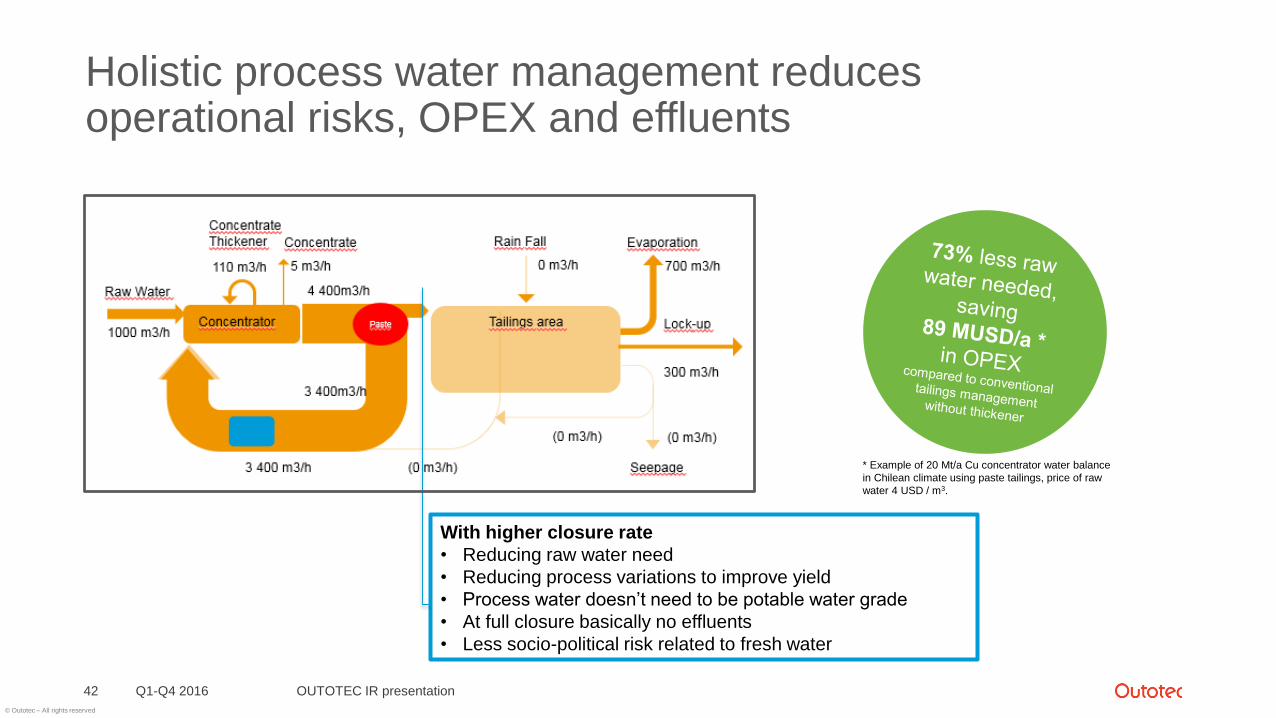

Holistic process water management reduces operational risks, OPEX and effluents

Q1-Q4 201642

With higher closure rate

• Reducing raw water need

• Reducing process variations to improve yield

• Process water doesn’t need to be potable water grade

• At full closure basically no effluents

• Less socio-political risk related to fresh water

OUTOTEC IR presentation

* Example of 20 Mt/a Cu concentrator water balance

in Chilean climate using paste tailings, price of raw

water 4 USD / m3.

© Outotec – All rights reserved

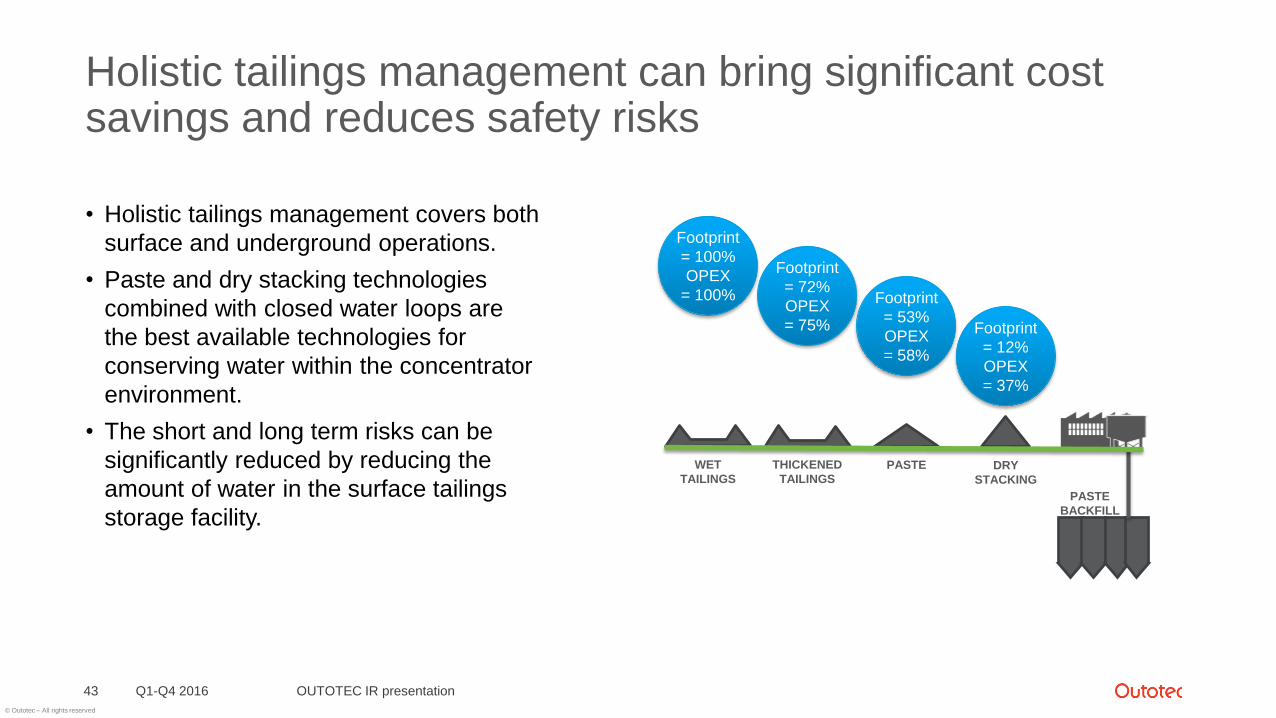

Holistic tailings management can bring significant cost savings and reduces safety risks

• Holistic tailings management covers both

surface and underground operations.

• Paste and dry stacking technologies

combined with closed water loops are

the best available technologies for

conserving water within the concentrator

environment.

• The short and long term risks can be

significantly reduced by reducing the

amount of water in the surface tailings

storage facility.

Q1-Q4 2016 OUTOTEC IR presentation43

PASTE

BACKFILL

DRY

STACKING

Footprint

= 12%

OPEX

= 37%

PASTE

Footprint

= 53%

OPEX

= 58%

THICKENED

TAILINGS

Footprint

= 72%

OPEX

= 75%

WET

TAILINGS

Footprint

= 100%

OPEX

= 100%

© Outotec – All rights reserved

Codelco Ministro Hales 1/2Customer case, full solution

Q1-Q4 201644

Customer challenges

• Ore with very high content of impurities, primarily

arsenic causing challenge in processing

• Commercial terms for the concentrate not

favourable for selling

OUTOTEC IR presentation

Outotec solution

• Several studies and test campaigns over the years to identify

best metallurgical solution

• Complete, integrated process which is based on patented

Outotec solutions and technologies and proven Outotec

proprietary equipment

• Arsenic levels of the concentrate lowered without loosing sulphur

• Sustainable water and effluent treatment in challenging

environment

1991

•Codelco and Outotec start working together on solving the challenges

2010

• Investment decisionmade

2014

•Commissioningcompleted

2016

•Official inauguration

© Outotec – All rights reserved

Codelco Ministro Hales 2/2Customer case, full solution

Q1-Q4 2016 OUTOTEC IR presentation45

Partial roasting

• Patented Outotec solution which

removes over 90% of the arsenic in

the ore concentrate

• Exceeding 605,000 tpa concentrate

(110%)

Gas Cleaning

• Outotec’s proprietary gas cleaning

and sulfuric acid production

technology eliminates over 99.9% of

the gaseous emission of the facility.

Effluent Treatment

• Outotec’s proprietary effluent treatment technology cleans the process

effluents and recirculates clean water back to the process.

Outotec delivers a complete, integrated solution from a broad portfolio of patented and

proprietary solutions, and a long history of process technology

© Outotec – All rights reserved

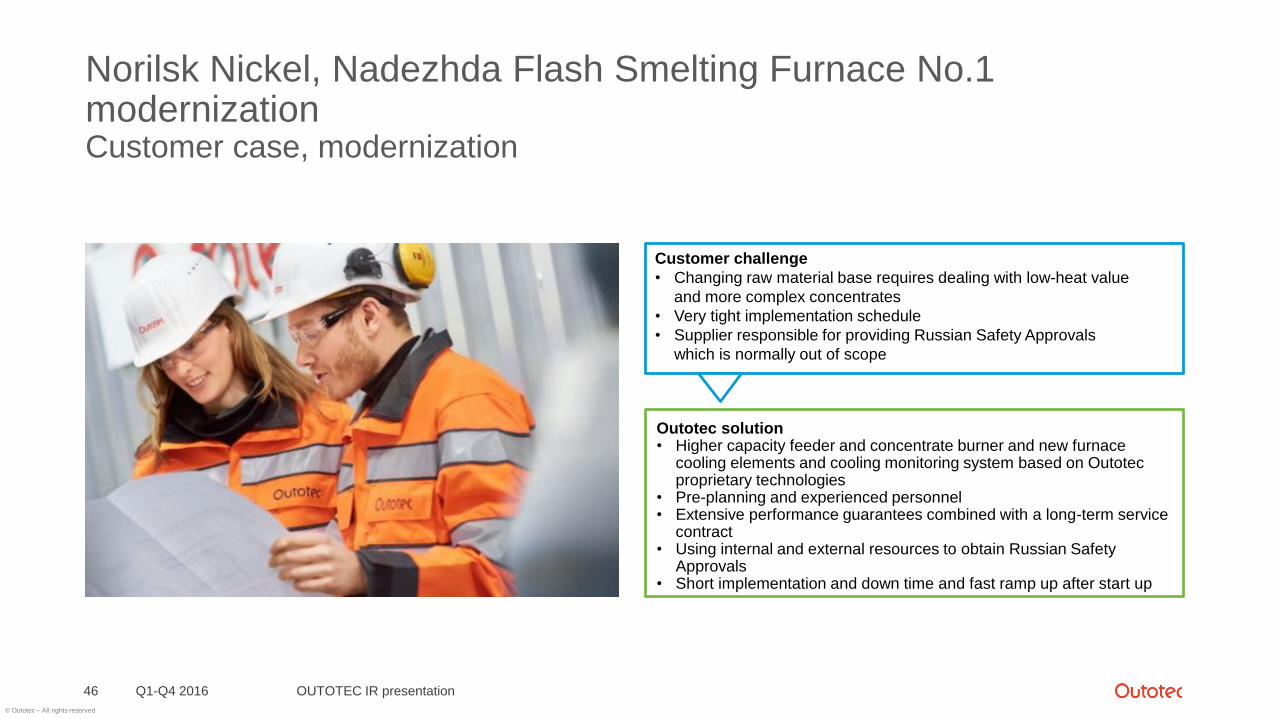

Norilsk Nickel, Nadezhda Flash Smelting Furnace No.1 modernizationCustomer case, modernization

Q1-Q4 201646 OUTOTEC IR presentation

Customer challenge

• Changing raw material base requires dealing with low-heat value

and more complex concentrates

• Very tight implementation schedule

• Supplier responsible for providing Russian Safety Approvals

which is normally out of scope

Outotec solution• Higher capacity feeder and concentrate burner and new furnace

cooling elements and cooling monitoring system based on Outotec proprietary technologies

• Pre-planning and experienced personnel• Extensive performance guarantees combined with a long-term service

contract• Using internal and external resources to obtain Russian Safety

Approvals• Short implementation and down time and fast ramp up after start up

© Outotec – All rights reserved

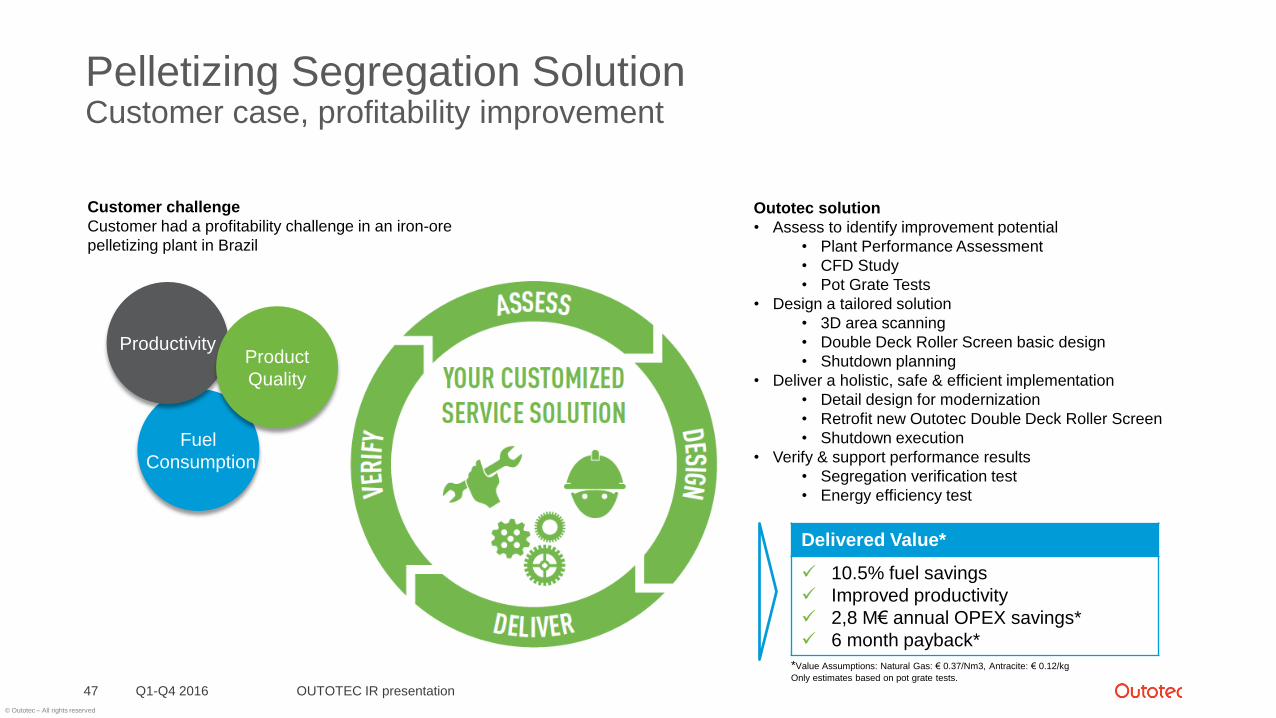

Pelletizing Segregation SolutionCustomer case, profitability improvement

OUTOTEC IR presentationQ1-Q4 201647

Customer challenge

Customer had a profitability challenge in an iron-ore

pelletizing plant in Brazil

Fuel

Consumption

ProductivityProduct

Quality

Outotec solution

• Assess to identify improvement potential

• Plant Performance Assessment

• CFD Study

• Pot Grate Tests

• Design a tailored solution

• 3D area scanning

• Double Deck Roller Screen basic design

• Shutdown planning

• Deliver a holistic, safe & efficient implementation

• Detail design for modernization

• Retrofit new Outotec Double Deck Roller Screen

• Shutdown execution

• Verify & support performance results

• Segregation verification test

• Energy efficiency test

Delivered Value*

10.5% fuel savings

Improved productivity

2,8 M€ annual OPEX savings*

6 month payback*

*Value Assumptions: Natural Gas: € 0.37/Nm3, Antracite: € 0.12/kg

Only estimates based on pot grate tests.

© Outotec – All rights reserved

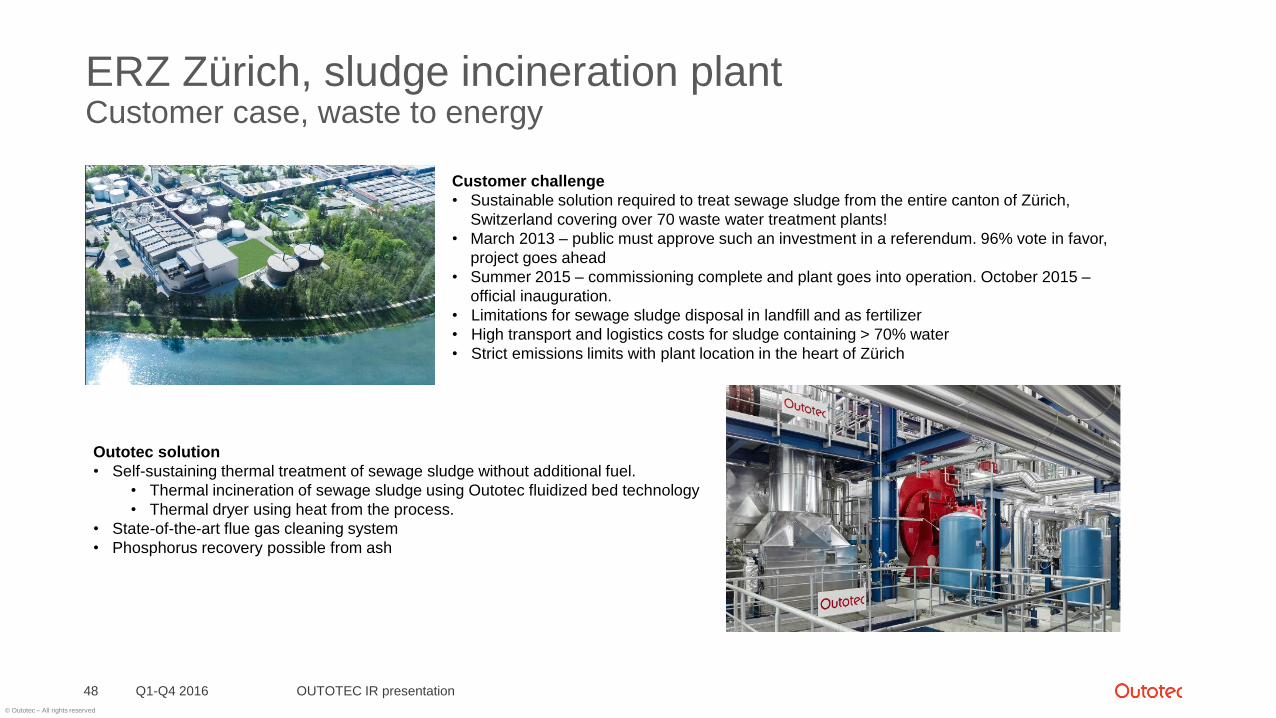

ERZ Zürich, sludge incineration plantCustomer case, waste to energy

Q1-Q4 201648

Customer challenge

• Sustainable solution required to treat sewage sludge from the entire canton of Zürich,

Switzerland covering over 70 waste water treatment plants!

• March 2013 – public must approve such an investment in a referendum. 96% vote in favor,

project goes ahead

• Summer 2015 – commissioning complete and plant goes into operation. October 2015 –

official inauguration.

• Limitations for sewage sludge disposal in landfill and as fertilizer

• High transport and logistics costs for sludge containing > 70% water

• Strict emissions limits with plant location in the heart of Zürich

OUTOTEC IR presentation

Outotec solution

• Self-sustaining thermal treatment of sewage sludge without additional fuel.

• Thermal incineration of sewage sludge using Outotec fluidized bed technology

• Thermal dryer using heat from the process.

• State-of-the-art flue gas cleaning system

• Phosphorus recovery possible from ash

© Outotec – All rights reserved

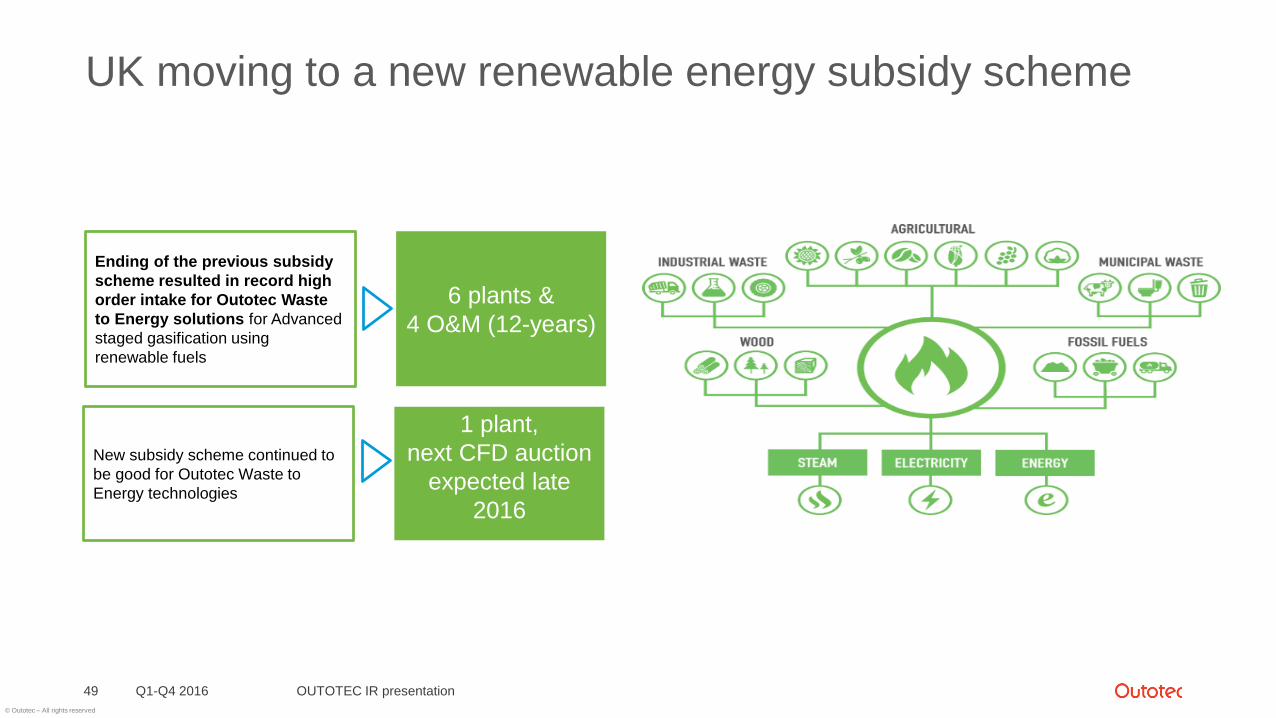

UK moving to a new renewable energy subsidy scheme

Q1-Q4 2016 OUTOTEC IR presentation49

Ending of the previous subsidy

scheme resulted in record high

order intake for Outotec Waste

to Energy solutions for Advanced

staged gasification using

renewable fuels

6 plants &

4 O&M (12-years)

New subsidy scheme continued to

be good for Outotec Waste to

Energy technologies

1 plant,

next CFD auction

expected late

2016

© Outotec – All rights reserved

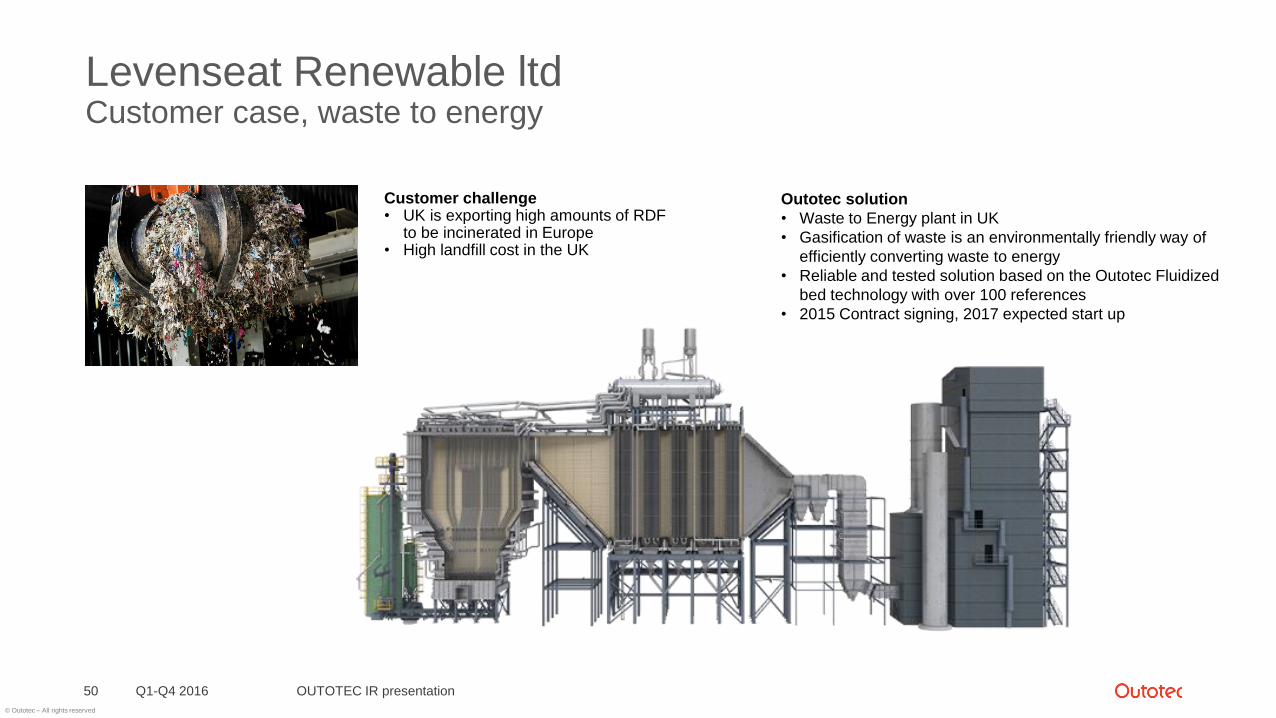

Levenseat Renewable ltdCustomer case, waste to energy

Q1-Q4 201650

Customer challenge• UK is exporting high amounts of RDF

to be incinerated in Europe • High landfill cost in the UK

OUTOTEC IR presentation

Outotec solution

• Waste to Energy plant in UK

• Gasification of waste is an environmentally friendly way of

efficiently converting waste to energy

• Reliable and tested solution based on the Outotec Fluidized

bed technology with over 100 references

• 2015 Contract signing, 2017 expected start up

© Outotec – All rights reserved

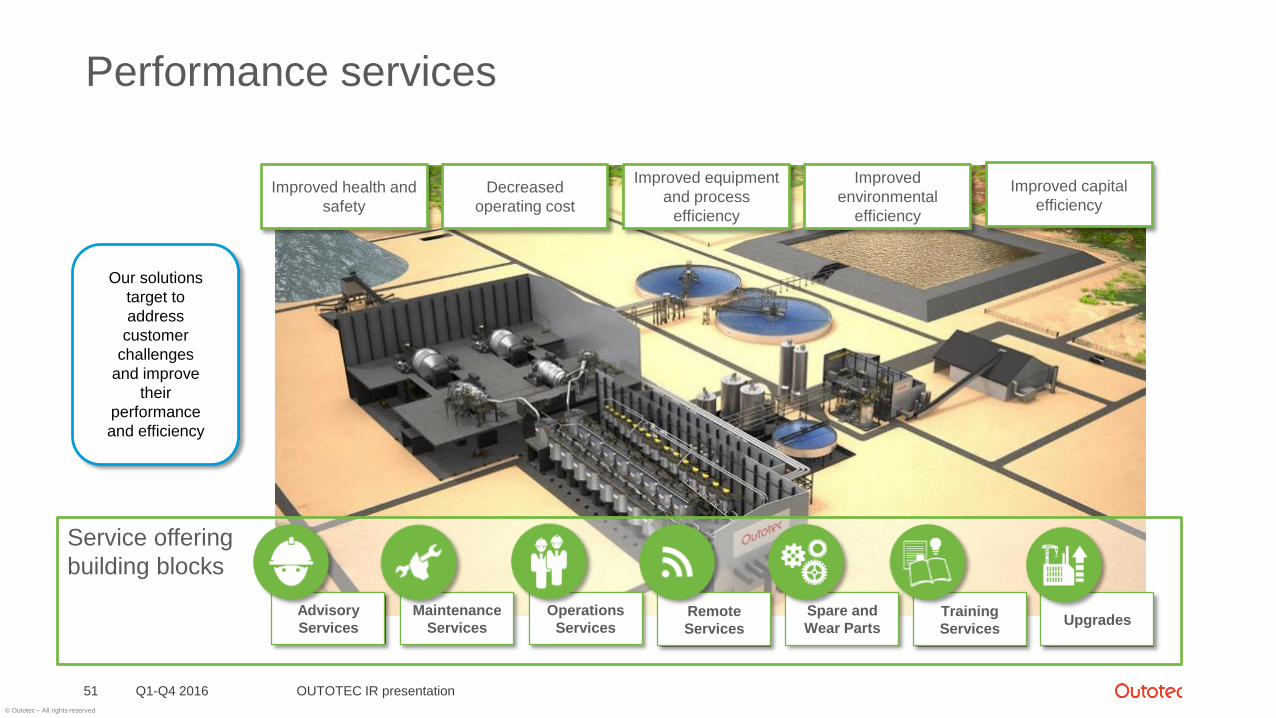

Service offering

building blocks

Performance services

Q1-Q4 2016 OUTOTEC IR presentation51

Operations

Services

Advisory

Services

Maintenance

ServicesRemote

Services

Training

Services

Spare and

Wear PartsUpgrades

Decreased

operating cost

Improved health and

safety

Improved

environmental

efficiency

Improved capital

efficiency

Improved equipment

and process

efficiency

Our solutions

target to

address

customer

challenges

and improve

their

performance

and efficiency

© Outotec – All rights reserved

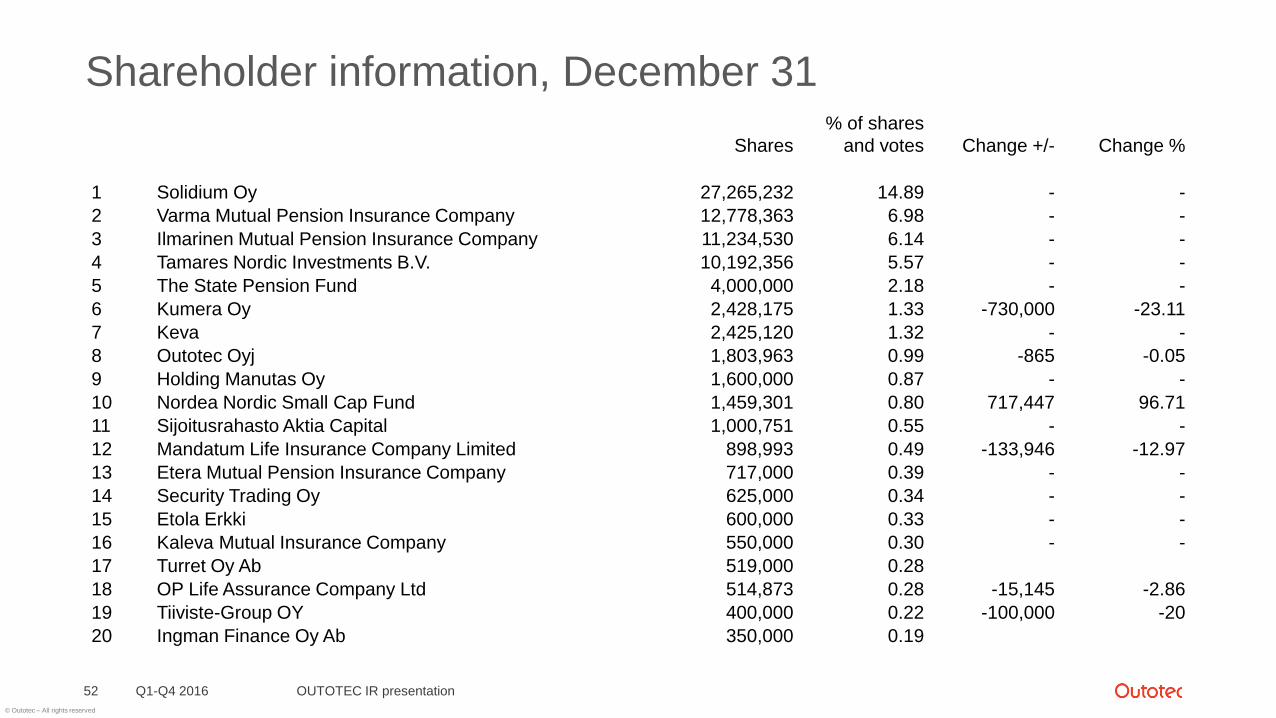

Shareholder information, December 31

Q1-Q4 2016 OUTOTEC IR presentation52

Shares

% of shares

and votes Change +/- Change %

1 Solidium Oy 27,265,232 14.89 - -

2 Varma Mutual Pension Insurance Company 12,778,363 6.98 - -

3 Ilmarinen Mutual Pension Insurance Company 11,234,530 6.14 - -

4 Tamares Nordic Investments B.V. 10,192,356 5.57 - -

5 The State Pension Fund 4,000,000 2.18 - -

6 Kumera Oy 2,428,175 1.33 -730,000 -23.11

7 Keva 2,425,120 1.32 - -

8 Outotec Oyj 1,803,963 0.99 -865 -0.05

9 Holding Manutas Oy 1,600,000 0.87 - -

10 Nordea Nordic Small Cap Fund 1,459,301 0.80 717,447 96.71

11 Sijoitusrahasto Aktia Capital 1,000,751 0.55 - -

12 Mandatum Life Insurance Company Limited 898,993 0.49 -133,946 -12.97

13 Etera Mutual Pension Insurance Company 717,000 0.39 - -

14 Security Trading Oy 625,000 0.34 - -

15 Etola Erkki 600,000 0.33 - -

16 Kaleva Mutual Insurance Company 550,000 0.30 - -

17 Turret Oy Ab 519,000 0.28

18 OP Life Assurance Company Ltd 514,873 0.28 -15,145 -2.86

19 Tiiviste-Group OY 400,000 0.22 -100,000 -20

20 Ingman Finance Oy Ab 350,000 0.19

© Outotec – All rights reserved

0

5

10

15

20

25

30

35

40

45

50

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Balance sheet reflects a stable financial position

Q1-Q4 2016 OUTOTEC IR presentation54

-160

-140

-120

-100

-80

-60

-40

-20

0

20

40

-400

-350

-300

-250

-200

-150

-100

-50

0

50

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gearing, %Net debt MEUR

Net debt, actual Gearing

Net debt & Gearing Equity ratio

%